ma chapter 1

DESCRIPTION

• A target cost per unit is the estimated long-run cost per unit of a product (or service) that, when sold at the target price, enables the company to achieve the target operating income per unit. A target cost per unit is the estimated unit long-run cost of a product that will enable a company to enter or to remain in the market and compete profitably against its competitors.In this case, to compete the competitors and maintain company’s market share and profits, Product Manager estimates the C1 to have manufacturing cost of approximately £680 and C2 to have a manufacturing cost of approximately £390. To achieve the target cost, they conduct to revise the cost of C1 and C2 by reducing cost production per unit:TRANSCRIPT

242015

1

Prepared by

Ms Dao Nam Giang

Associate Dean of Accounting and Auditing Faculty (namgiangrivergmailcom)

OVERVIEW

Class rules

Team learning approachgroup - based instructional format

Assessment

Course materials

Course objects

Learning outcomes

Studying progress

Class rules Please be on time (an acceptable margin of 5 minutes)

Kindly turn off all cell phones during the lecture

Attendance is important and will be taken in different ways

Class interaction be prepared for your lessons and actively

participate in the lecture

Questions and comment box

Basis of respect

bull Stay and interact with others silently Once the lecture starts You

are not allowed to leave the lecture room and do other tasks

bull Share freely with others your thoughts and feelings in a friendly

or cordial manner You may raise your hands to signify your

intention to give an opinion in case somebody is still talking

bull Letrsquos give due courtesy to those who are speaking

242015

2

Team leaning approach Study group 3 to 5 students leader exchange

information and keep contacted

Study group will be maintained during the semester and will assigned different tasks every one or two weeks

Pre ndash lecture quizzes

Assessment 2 assignments

First assignment be submitted week 9 - Individual assignment + oral exams and progress tests

Second assignment be submitted week 16 - Individual assignment + oral exams and progress tests

Short progress tests during the course

Focus on 1 or 2 learning outcomes

The result will be used as a substitute for the oral examinations (done correctly 70 or more of each test -gt not be questioned on the related outcomes in the oral exam)

Course materials Text book

Handouts and exercises (will be send to your classrsquo email)

Incomplete notes so you are required to print out and bring the handout with you to the class

Other reading introduced in each chapter

242015

3

Course objectives

Accounting provide information about economic activities of one organization to interested users

Financial Accounting vs Management accounting

A A field of accounting that provides economic and financial field of accounting that provides economic and financial information for managers and other internal usersinformation for managers and other internal users

Also Also calledcalled Managerial Accounting

Definition of Management AccountingManagement Accounting

Course objectives Provide learners with the understanding and ability to

use cost information for budgeting and forecasting purposes in the management of business

How cost data is collected compiled and analysed and processed into useful information

Deal with budgetary planning and control how to prepare forecasts and budgets and to compare these to actual business results

Consider different costing and budgetary systems and the causes of resulting variances possible implications and corrective action

Learning outcomes1 Be able to analyze cost information within a business

11 Classify different types of cost

12 Using different costing methods

13 Calculate costs using appropriate techniques

14 Analyse cost data using appropriate techniques

2 Be able to propose methods to reduce costs and

enhance value within a business

21 Prepare and analyze routine cost report

22 Use performance indicators to identify potential improvements

23 Suggest improvements to reduce cost enhance value and

quality

242015

4

Learning outcomes3 Be able to prepare forecasts and budgets for a business

31 Explain the purpose and nature of the budgeting process

32 Select appropriate budgeting methods for the organization

and its needs

33 Prepare budgets according to the chosen budgeting method

34 Prepare a cash budget

4 Be able to Monitor performance against budgets within

a business41 Calculate variances identify possible causes and recommend

corrective actions

42 Prepare an operating statement reconciling budgeted and

actual results

43 Report findings to management in accordance with identified

responsibility centers

Week Content

1 Chapter 1 Cost accounting classification and behavior

2 Chapter 2 Material and labor cost

3 Chapter 3 Overhead apportionment and absorption

4 Chapter 4 Marginal and absorption costing

5 Chapter 6 Costing system

6 Chapter 7 Process costing (I)

7 Chapter 5 Price value and quality and checking draft

8 Chapter Review and checking draft

9 Submit assignment 1 and oral examination

10 Chapter 7 Process costing (II)

11 Chapter 8 Budgeting

12 Chapter 8 Budgeting

13 Chapter 9 Standard costing and variance analysis

14 Chapter 10 Responsibility accounting

15 Review and checking draft

STY

DY

ING

PR

OG

RES

S

Warm up activity How does the course related to other subjects that you

have studied

Discuss to form your study group

242015

5

Managing financial resources and decisions

Management accounting

Financial reporting

Review on MFRS Chapter 1- 3 different assets and liabilities

(sources of finances) of a business

Chapter 5 Basis procedures in accounting

Chapter 7 Cost terms and cost classification

Chapter 4 Stocks and cash

Chapter 9 Pricing decisions

Chapter 6 Evaluating financial performance

Chapter 8 Budgets

Activity 1 Review of basis terms in accounting

242015

6

Content Cost concepts

Direct cost vs indirect cost

Cost behavior

Cost estimation

Manufacturing activity and manufacturing costs

Prepare income statement for manufacturer

Costs classification for decision makingdifferential cost analysis

242015

7

Cost concepts Cost ndash sacrificed resource to achieve a specific

objective

Cost accounting measure and reports financial and non financial information relating to the cost of acquiring or utilizing resources in an organization Cost accounting provide information to assist

Establishing stock valuation profit and balance sheet items

Planning

Control

Decision making

Cost concepts Cost unit a unit of product or service to which costs can be

related The cost unit is the basic control unit for costing purposes Can you give some examples

Cost centre cost pool a location or a function or an activity or an item of equipment Each cost centre act as a collecting place for certain cost before they are analyzed further In production department the department itself a machine or

group of machines in the department a foremanrsquos group a workbench

Production ldquoservicerdquo or ldquoback-uprdquo departments (maintenance storehellip)

Administration sales or distribution departments (personnel accounting purchasinghellip

Cost centre of shared costs for directly allocated (rent rates heating lighting)

Cost concepts - example Chocolate cakes production

Cost unit Box of chocolate cake

Cost centers

Mixing department

Baking department

Stores department

242015

8

Cost concepts

Cost centers 1

Cost centers 2

Cost centers 3

Cost unit 1

Cost unit 2

cost

Hanoi 11-16 December 2005 24

Direct costs vs Indirect costs Direct Costs

Costs that can be easily and conveniently traced in full to the product service or department that is being costed

Example Parts Assembly line wages

Indirect Costs

Costs that is incurred in the course of making a product providing a service or running a department but cannot be traced directly and in full to the product service or department Ex Electricity Rent

Instead of being traced these costs are allocated to a cost object in a rational and systematic manner

Direct and indirect cost - examples

SHOP RESTAURANT

242015

9

Cost Behaviorbull Cost behavior the variability of input costs with

bull

bull Cost behavior the variability of input costs with activity undertaken

bull Level of activity amount of work done or the number of events occurred

bull The volume of production in a period

bull The number of item sold

bull The value of items sold

bull The number of invoices issued

bull hellip

Cost Behavior

Behavior of Cost (within the relevant range)

Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remains

as activity level changes the same over wide ranges

of activity

Fixed Total fixed cost remains Average fixed cost per unit goes

the same even when the down as activity level goes up

activity level changes

242015

10

Step Costs

A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but only within certain levels of activityonly within certain levels of activity

-- Rent depreciation maintenancehellipRent depreciation maintenancehellip

Volume

Co

st

Fixed Monthly

Charge

Variable

Cost per minutes talked

Activity (minutes talked)

To

tal

tele

ph

on

e b

ill

X

Y

A mixed cost has both fixed and variable

costs

A mixed cost has both fixed and variable

components Consider your telephone costs

Mixed Costs semi-variable costs

Fixed Monthly

Charge

Variable

Cost per minutes talked

Activity (minutes talked)

To

tal

tele

ph

on

e b

ill

X

Y

Mixed Costs semi-variable costsThe total mixed cost line can be expressed

as an equation Y = a + bX

Where Y = the total mixed cost

a = the total fixed cost (the

vertical intercept of the line)

b = the variable cost per unit of

activity (the slope of the line)

X = the level of activity

242015

11

Activity 3 Are the following likely to be fixed variable or mixed

cost

Telephone bill

Annual salary of the chief accountant

The management accountantrsquos annual membership fee to his professional body (paid by the company)

Cost of materials used to pack 20 units of product X into a box

Plot the data points on a graph (total Plot the data points on a graph (total Plot the data points on a graph (total Plot the data points on a graph (total cost vs activity)cost vs activity)

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

The Scattergraph Method

242015

12

The Scattergraph Method

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

Draw a line Draw a line through the through the data points data points

points above points above

Draw a line Draw a line through the through the data points data points with about with about an equal an equal

number of number of points above points above and below and below the line the line

The Scattergraph MethodUse one Use one

data point data point to estimate to estimate

total cost total cost

Use one Use one data point data point to estimate to estimate

the totalthe totallevel of level of activity activity and the and the

total cost total cost Intercept = Fixed cost $10000

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

Patient days = 800Patient days = 800

Total maintenance cost = $11000Total maintenance cost = $11000

The Scattergraph Method

Make a quick estimate of variable cost perMake a quick estimate of variable cost perMake a quick estimate of variable cost perMake a quick estimate of variable cost perunit and determine the cost equation unit and determine the cost equation

Variable cost per unit = $1000

800= $125patient$125patient--dayday

Y = $10000 + $125XY = $10000 + $125XY = $10000 + $125XY = $10000 + $125X

Total maintenance at 800 patients 11000$

Less Fixed cost 10000

Estimated total variable cost for 800 patients 1000$

Total maintenance costTotal maintenance costTotal maintenance costTotal maintenance cost Number of patient daysNumber of patient daysNumber of patient daysNumber of patient days

242015

13

The High-Low MethodAssume the following hours of maintenance work

and the total maintenance costs for six months

]

The High-Low MethodThe The variable cost per variable cost per hourhour of maintenance of maintenance The The variable cost per variable cost per hourhour of maintenance of maintenance

is equal to the is equal to the change in cost change in cost divided by the divided by the

change in hourschange in hours

Hours Total Cost

High 800 9800$

Low 500 7400

Change 300 2400$

The High-Low Method

Total Fixed Cost = Total Cost Total Fixed Cost = Total Cost ndashndash Total Variable CostTotal Variable Cost

Total Fixed Cost Total Fixed Cost ==

Total Fixed Cost Total Fixed Cost ==

Total Fixed Cost Total Fixed Cost ==

242015

14

The High-Low Method

Y = $3400 + $800Y = $3400 + $800XX

The Cost Equation for Maintenance

Quick Check

Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units

Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units are sold Using the high-low method what is thevariable portion of sales salaries and commission

a $008 per unit

b $010 per unit

c $012 per unit

d $0125 per unit

Quick Check

Sales salaries and commissions are $10000 when Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units are sold Using the high-low method what is the fixed portion of sales salaries and commissions

a $ 2000

b $ 4000

c $10000

d $12000

242015

15

Manufacturing activity

Manufacturing cost

Comparing Merchandising and Manufacturing Activities

Merchandisers

Buy finished goods

Sell finished goods

Manufacturers

Buy raw materials

Produce and sell finished goods

MegaLoMart

inventory on hand Raw materials - inventory on hand and available for use

Work in process -Work in process -partially

completed goods

Finished goods-

goods awaiting

Finished goods-completed

goods awaiting sale

Inventories of a Manufacturing Business

242015

16

Manufacturing consists of activities and processes to convert raw materials into finished goods

Manufacturing costs are the cost to produce a unit of product and typically classified as

Manufacturing activityManufacturing activityManufacturing activityManufacturing activity

The ProductThe Product

DirectMaterials

DirectMaterials

DirectLaborDirectLabor

ManufacturingOverhead

ManufacturingOverhead

Direct Materials Raw materials that become an integral part of the product

(unless used in negligible amounts andor having negligible cost)

Component parts or other materials specially purchased for a particular job order or process

Part-finished work transferred from previous process

Primary packing material (cartons and boxes)

Example What are direct materials in Example What are direct materials in producinged a car

Direct wages Wages paid for labour (either as basic hours

or as overtime) expended on work on the product itself

Example Wages paid to automobile assembly workersExample Wages paid to automobile assembly workers

242015

17

Direct wages ndash activity 1 Classify the following labour costs as either direct or

indirect

The basic pay of direct workers (cash paid tax or other deductions)

The basic pay of indirect workers

Overtime premium (the premium over basic pay for working overtime)

Bonus payments under a group bonus payments scheme

Employerrsquos National Insurance contributions

Idle time of direct workers

Work on installation of equipment

Direct expenses Expenses are incurred on a specific product other than

direct material cost and direct wages

Example

The cost of special designs drawings or layouts

The hire of tools or equipments or a particular job

Maintenance cost of tools fixtures hellip

ProductionManufacturing OverheadManufacturing costs cannot be traced directly to

specific units produced

bullIndirect materials

bull

Maintenance workers janitors and security guardsbull

bullIndirect materials bullMaterials used to support the production process bullExamples Lubricants and cleaning supplies used in the automobile assembly plant

bullIndirect labor bullWages paid to employees who are not directly involved in production work bullExamples Maintenance workers janitors and security guards

bullIndirect expenses bullRent rate Insurance of a factorybullDepreciation fuel power repairs and maintenance of plant machinery and factory buildings hellip

242015

18

Direct Materials

Purchased

Direct Materials

Purchased

Direct Materials

Direct Materials

Used

Direct Direct Labor

Manufacturing Manufacturing Overhead

Finished Finished Goods

Goods SoldGoods Sold

MegaLoMart

Flow of Physical Goods in Production

Nonmanufacturing Costs

Selling Costsoverhead

Costs necessary to get the order and deliver

the product

Administrative Costsoverhead

All executive organizational and

clerical costs associated with the general

management of an organization

Product Costs Versus Period Costs

Inventory

Cost of Goods Sold

BalanceSheet

IncomeStatement

Sale

Product costs include direct materials direct

labor and manufacturing

overhead

Period costs are not included in product

costs They are expensed on the

income statement

Expense

IncomeStatement

242015

19

Quick Check Which of the following costs would be considered a period rather than a product cost in a manufacturing company

A Manufacturing equipment depreciation

B Property taxes on corporate headquarters

C Direct materials costs

D Electrical costs to light the production

facility

E Sales commissions

Prime Cost and Conversion Cost

DirectMaterialDirect

MaterialDirectDirectLabor

ManufacturingManufacturingOverhead

PrimeCost

ConversionCost

Manufacturing costs are oftenclassified as follows

Exercise The Sloane Company specializes in producing a set of

wood patio furniture consisting of a table and four chairs Cost data for the year 2012 as follow

For each item determine it is period cost or product cost direct cost or indirect cost FIXED OR VARIABLE COST

242015

20

Factory labor direct $150000

Advertising $32500

Factory supervision $28000

Property taxes factory building $2000

Sales commissions $97000

Insurance factory $6500

Depreciation office equipment $5000

Lease cost factory equipment $19000

Indirect materials factory $10000

Depreciation factory building $20500

General office supplies (billing) $3500

General office salaries $73000

Direct materials used (wood bolts etc) $120000

Utilities factory $16000

Income statement Report revenues and expenses =gt net profitnet loss

Revenue

- Cost of sales (cost of goods sold)

Gross profit

- Selling expenses

- Administrative expenses

Net income

bull Issue how to calculate cost of goods sold

242015

21

Inventory Flows

Beginningbalance to inventory

Additionsto inventory++ ==

Endingbalance

WithdrawalsWithdrawalsfrom

inventory++

Manufacturing Company

Cost of goods sold

Beg Finished goods inv 14200$

+ Cost of goods manufactured 234150

Goods available for sale 248350$

- Ending finished goods inventory (12100)

= Cost of goods sold 236250$

Schedule of Cost of Goods Manufactured

Calculates the cost of raw material direct labor and

manufacturing overhead used in production

Calculates the manufacturing costs associated with goods

that were finished during the period

Manufacturing Work

Raw Materials Costs In Process

Beginning raw

materials inventory

+ Raw materials

purchased

= Raw materials

available for use

in production

ndash Ending raw materials

inventory

= Raw materials used

in production

As items are removed from raw materials inventory and placed As items are removed from raw materials inventory and placed

into the production process they are called direct

materials

Schedule of Cost of Goods Manufactured

242015

22

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials

materials inventory + Direct labor

+ Raw materials + Mfg overhead

purchased = Total manufacturing

= Raw materials costs

available for use

in production

ndash Ending raw materials

inventory

= Raw materials used

in production

Conversion

direct material finished

Conversion costs are costs

incurred to convert the

direct material into a finished

product

As items are removed from raw materials inventory and placed into

As items are removed from raw materials inventory and placed into

the production process they arecalled direct materials

Schedule of Cost of Goods Manufactured

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials Beginning work in

materials inventory + Direct labor process inventory

+ Raw materials + Mfg overhead + Total manufacturing

purchased = Total manufacturing costs

= Raw materials costs = Total work in

available for use process for the

in production period

ndash Ending raw materials ndash Ending work in

inventory process inventory

= Raw materials used = Cost of goods

in production manufactured

All manufacturing costs incurred

beginning balance of work in process

All manufacturing costs incurred during the period are added to the

beginning balance of work in process

Schedule of Cost of Goods Manufactured

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials Beginning work in

materials inventory + Direct labor process inventory

+ Raw materials + Mfg overhead + Total manufacturing

purchased = Total manufacturing costs

= Raw materials costs = Total work in

available for use process for the

in production period

ndash Ending raw materials ndash Ending work in

inventory process inventory

= Raw materials used = Cost of goods

in production manufactured

Costs associated with the goods that Costs associated with the goods that are completed during the period are

transferred to finished goods inventory

Schedule of Cost of Goods Manufactured

242015

23

Work

In Process Finished Goods

Beginning work in Beginning finished

process inventory goods inventory

+ Manufacturing costs + Cost of goods

for the period manufactured

= Total work in process = Cost of goods

for the period available for sale

ndash Ending work in - Ending finished

process inventory goods inventory

= Cost of goods Cost of goods

manufactured sold

Cost of Goods Sold

Manufacturing Cost Flows

Selling andAdministrative

Period Costs

FinishedGoods

Cost of GoodsSold

Selling andAdministrative

ManufacturingOverhead

Work inProcess

Direct Labor

Balance SheetCosts Inventories

Income StatementExpensesMaterial Purchases Raw Materials

Quick Check

Beginning raw materials inventory was $32000 During the month $276000 of raw material was purchased A count at the end of the month revealed that $28000 of raw material was still present What is the cost of direct material used

A $276000

B $272000

C $280000

D $ 2000

242015

24

Quick Check

Direct materials used in production totaled $280000 Direct labor was $375000 and factory overhead was $180000 What were total manufacturing costs incurred for the month

A $555000

B $835000

C $655000

D Cannot be determined

Quick Check

Beginning work in process was $125000 Manufacturing costs incurred for the month were $835000 There were $200000 of partially finished goods remaining in work in process inventory at the end of the month What was the cost of goods manufactured during the month

A $1160000B $ 910000C $ 760000D Cannot be determined

Quick Check Beginning finished goods inventory was $130000 The cost of goods manufactured for the month was $760000 The ending finished goods inventory was $150000 What was the cost of goods sold for the month

A $ 20000

B $740000

C $780000

D $760000

242015

25

Production costProduct cost

FINISHEDFINISHED GOODSGOODS

Period Cost Cost of good sold

Cost and decision making Fixed and variable cost

Relevant and non - relevant cost

Cost-benefit analysisDifferential analysis

242015

26

Relevant cost Relevant cost is a future cashflow arising as a direct

consequence of a decision

Future cost cost incurred (paid or not yet paid) is irrelevant

Cashflows

Arises as a direct consequence of a decision costs differ under some or all the alternativesavailable opportunities ndash incremental costdifferential costs

Some times expressed as opportunity cost ndash the benefit foregone by choosing one opportunity instead of the next best alternative

Non relevant cost Sunk costs cannot be changed by any decision

They are not differential costs and should be ignored when making decisions (Paid)

Committed costs future cash outflow that will be incurred anyway whatever decision is taken now about alternative opportunities

Notional costsImputed cost no actual cash expense incurred Notional rent charged to the branch for the use of the

buildings owned by the company

Notional interest charges on capital used by the branch

JamCo currently sells 100000 units of its product The company has revenue and costs

as shown below

Per Unit Total

Sales 1000$ 1000000$

Direct materials 350 350000

Direct labor 220 220000

Factory overhead 110 110000

Selling expenses 140 140000

Administrative expenses 080 80000

Total expenses 900$ 900000$

Operating income 100$ 100000$

Example 1

242015

27

JamCo is approached by an overseascompany that offers to purchase

10000 units at $850 per unit

If JamCo accepts the offer total factoryoverhead will increase by $5000 total selling

expenses will increase by $2000 and total administrative expenses will increase

by $1000

Should JamCoaccept the offer

Special Order Decisions

OserCo has 10000 defective units thatcost $100 each to make The units can be

scrapped now for $40 each or rebuilt at an additional cost of $80 per unit

If rebuilt the units can be sold for the normal selling price of $150 each Rebuilding the 10000

defective units will prevent the production of 10000 new units that would also sell for $150

Should OserCo scrap or rebuild

Example 2

Summary of the Types of Cost Classifications

Financial Reporting

Predicting Cost

Behavior

Assigning Costs to Cost

Objects

Decision Making

242015

2

Team leaning approach Study group 3 to 5 students leader exchange

information and keep contacted

Study group will be maintained during the semester and will assigned different tasks every one or two weeks

Pre ndash lecture quizzes

Assessment 2 assignments

First assignment be submitted week 9 - Individual assignment + oral exams and progress tests

Second assignment be submitted week 16 - Individual assignment + oral exams and progress tests

Short progress tests during the course

Focus on 1 or 2 learning outcomes

The result will be used as a substitute for the oral examinations (done correctly 70 or more of each test -gt not be questioned on the related outcomes in the oral exam)

Course materials Text book

Handouts and exercises (will be send to your classrsquo email)

Incomplete notes so you are required to print out and bring the handout with you to the class

Other reading introduced in each chapter

242015

3

Course objectives

Accounting provide information about economic activities of one organization to interested users

Financial Accounting vs Management accounting

A A field of accounting that provides economic and financial field of accounting that provides economic and financial information for managers and other internal usersinformation for managers and other internal users

Also Also calledcalled Managerial Accounting

Definition of Management AccountingManagement Accounting

Course objectives Provide learners with the understanding and ability to

use cost information for budgeting and forecasting purposes in the management of business

How cost data is collected compiled and analysed and processed into useful information

Deal with budgetary planning and control how to prepare forecasts and budgets and to compare these to actual business results

Consider different costing and budgetary systems and the causes of resulting variances possible implications and corrective action

Learning outcomes1 Be able to analyze cost information within a business

11 Classify different types of cost

12 Using different costing methods

13 Calculate costs using appropriate techniques

14 Analyse cost data using appropriate techniques

2 Be able to propose methods to reduce costs and

enhance value within a business

21 Prepare and analyze routine cost report

22 Use performance indicators to identify potential improvements

23 Suggest improvements to reduce cost enhance value and

quality

242015

4

Learning outcomes3 Be able to prepare forecasts and budgets for a business

31 Explain the purpose and nature of the budgeting process

32 Select appropriate budgeting methods for the organization

and its needs

33 Prepare budgets according to the chosen budgeting method

34 Prepare a cash budget

4 Be able to Monitor performance against budgets within

a business41 Calculate variances identify possible causes and recommend

corrective actions

42 Prepare an operating statement reconciling budgeted and

actual results

43 Report findings to management in accordance with identified

responsibility centers

Week Content

1 Chapter 1 Cost accounting classification and behavior

2 Chapter 2 Material and labor cost

3 Chapter 3 Overhead apportionment and absorption

4 Chapter 4 Marginal and absorption costing

5 Chapter 6 Costing system

6 Chapter 7 Process costing (I)

7 Chapter 5 Price value and quality and checking draft

8 Chapter Review and checking draft

9 Submit assignment 1 and oral examination

10 Chapter 7 Process costing (II)

11 Chapter 8 Budgeting

12 Chapter 8 Budgeting

13 Chapter 9 Standard costing and variance analysis

14 Chapter 10 Responsibility accounting

15 Review and checking draft

STY

DY

ING

PR

OG

RES

S

Warm up activity How does the course related to other subjects that you

have studied

Discuss to form your study group

242015

5

Managing financial resources and decisions

Management accounting

Financial reporting

Review on MFRS Chapter 1- 3 different assets and liabilities

(sources of finances) of a business

Chapter 5 Basis procedures in accounting

Chapter 7 Cost terms and cost classification

Chapter 4 Stocks and cash

Chapter 9 Pricing decisions

Chapter 6 Evaluating financial performance

Chapter 8 Budgets

Activity 1 Review of basis terms in accounting

242015

6

Content Cost concepts

Direct cost vs indirect cost

Cost behavior

Cost estimation

Manufacturing activity and manufacturing costs

Prepare income statement for manufacturer

Costs classification for decision makingdifferential cost analysis

242015

7

Cost concepts Cost ndash sacrificed resource to achieve a specific

objective

Cost accounting measure and reports financial and non financial information relating to the cost of acquiring or utilizing resources in an organization Cost accounting provide information to assist

Establishing stock valuation profit and balance sheet items

Planning

Control

Decision making

Cost concepts Cost unit a unit of product or service to which costs can be

related The cost unit is the basic control unit for costing purposes Can you give some examples

Cost centre cost pool a location or a function or an activity or an item of equipment Each cost centre act as a collecting place for certain cost before they are analyzed further In production department the department itself a machine or

group of machines in the department a foremanrsquos group a workbench

Production ldquoservicerdquo or ldquoback-uprdquo departments (maintenance storehellip)

Administration sales or distribution departments (personnel accounting purchasinghellip

Cost centre of shared costs for directly allocated (rent rates heating lighting)

Cost concepts - example Chocolate cakes production

Cost unit Box of chocolate cake

Cost centers

Mixing department

Baking department

Stores department

242015

8

Cost concepts

Cost centers 1

Cost centers 2

Cost centers 3

Cost unit 1

Cost unit 2

cost

Hanoi 11-16 December 2005 24

Direct costs vs Indirect costs Direct Costs

Costs that can be easily and conveniently traced in full to the product service or department that is being costed

Example Parts Assembly line wages

Indirect Costs

Costs that is incurred in the course of making a product providing a service or running a department but cannot be traced directly and in full to the product service or department Ex Electricity Rent

Instead of being traced these costs are allocated to a cost object in a rational and systematic manner

Direct and indirect cost - examples

SHOP RESTAURANT

242015

9

Cost Behaviorbull Cost behavior the variability of input costs with

bull

bull Cost behavior the variability of input costs with activity undertaken

bull Level of activity amount of work done or the number of events occurred

bull The volume of production in a period

bull The number of item sold

bull The value of items sold

bull The number of invoices issued

bull hellip

Cost Behavior

Behavior of Cost (within the relevant range)

Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remains

as activity level changes the same over wide ranges

of activity

Fixed Total fixed cost remains Average fixed cost per unit goes

the same even when the down as activity level goes up

activity level changes

242015

10

Step Costs

A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but only within certain levels of activityonly within certain levels of activity

-- Rent depreciation maintenancehellipRent depreciation maintenancehellip

Volume

Co

st

Fixed Monthly

Charge

Variable

Cost per minutes talked

Activity (minutes talked)

To

tal

tele

ph

on

e b

ill

X

Y

A mixed cost has both fixed and variable

costs

A mixed cost has both fixed and variable

components Consider your telephone costs

Mixed Costs semi-variable costs

Fixed Monthly

Charge

Variable

Cost per minutes talked

Activity (minutes talked)

To

tal

tele

ph

on

e b

ill

X

Y

Mixed Costs semi-variable costsThe total mixed cost line can be expressed

as an equation Y = a + bX

Where Y = the total mixed cost

a = the total fixed cost (the

vertical intercept of the line)

b = the variable cost per unit of

activity (the slope of the line)

X = the level of activity

242015

11

Activity 3 Are the following likely to be fixed variable or mixed

cost

Telephone bill

Annual salary of the chief accountant

The management accountantrsquos annual membership fee to his professional body (paid by the company)

Cost of materials used to pack 20 units of product X into a box

Plot the data points on a graph (total Plot the data points on a graph (total Plot the data points on a graph (total Plot the data points on a graph (total cost vs activity)cost vs activity)

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

The Scattergraph Method

242015

12

The Scattergraph Method

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

Draw a line Draw a line through the through the data points data points

points above points above

Draw a line Draw a line through the through the data points data points with about with about an equal an equal

number of number of points above points above and below and below the line the line

The Scattergraph MethodUse one Use one

data point data point to estimate to estimate

total cost total cost

Use one Use one data point data point to estimate to estimate

the totalthe totallevel of level of activity activity and the and the

total cost total cost Intercept = Fixed cost $10000

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

Patient days = 800Patient days = 800

Total maintenance cost = $11000Total maintenance cost = $11000

The Scattergraph Method

Make a quick estimate of variable cost perMake a quick estimate of variable cost perMake a quick estimate of variable cost perMake a quick estimate of variable cost perunit and determine the cost equation unit and determine the cost equation

Variable cost per unit = $1000

800= $125patient$125patient--dayday

Y = $10000 + $125XY = $10000 + $125XY = $10000 + $125XY = $10000 + $125X

Total maintenance at 800 patients 11000$

Less Fixed cost 10000

Estimated total variable cost for 800 patients 1000$

Total maintenance costTotal maintenance costTotal maintenance costTotal maintenance cost Number of patient daysNumber of patient daysNumber of patient daysNumber of patient days

242015

13

The High-Low MethodAssume the following hours of maintenance work

and the total maintenance costs for six months

]

The High-Low MethodThe The variable cost per variable cost per hourhour of maintenance of maintenance The The variable cost per variable cost per hourhour of maintenance of maintenance

is equal to the is equal to the change in cost change in cost divided by the divided by the

change in hourschange in hours

Hours Total Cost

High 800 9800$

Low 500 7400

Change 300 2400$

The High-Low Method

Total Fixed Cost = Total Cost Total Fixed Cost = Total Cost ndashndash Total Variable CostTotal Variable Cost

Total Fixed Cost Total Fixed Cost ==

Total Fixed Cost Total Fixed Cost ==

Total Fixed Cost Total Fixed Cost ==

242015

14

The High-Low Method

Y = $3400 + $800Y = $3400 + $800XX

The Cost Equation for Maintenance

Quick Check

Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units

Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units are sold Using the high-low method what is thevariable portion of sales salaries and commission

a $008 per unit

b $010 per unit

c $012 per unit

d $0125 per unit

Quick Check

Sales salaries and commissions are $10000 when Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units are sold Using the high-low method what is the fixed portion of sales salaries and commissions

a $ 2000

b $ 4000

c $10000

d $12000

242015

15

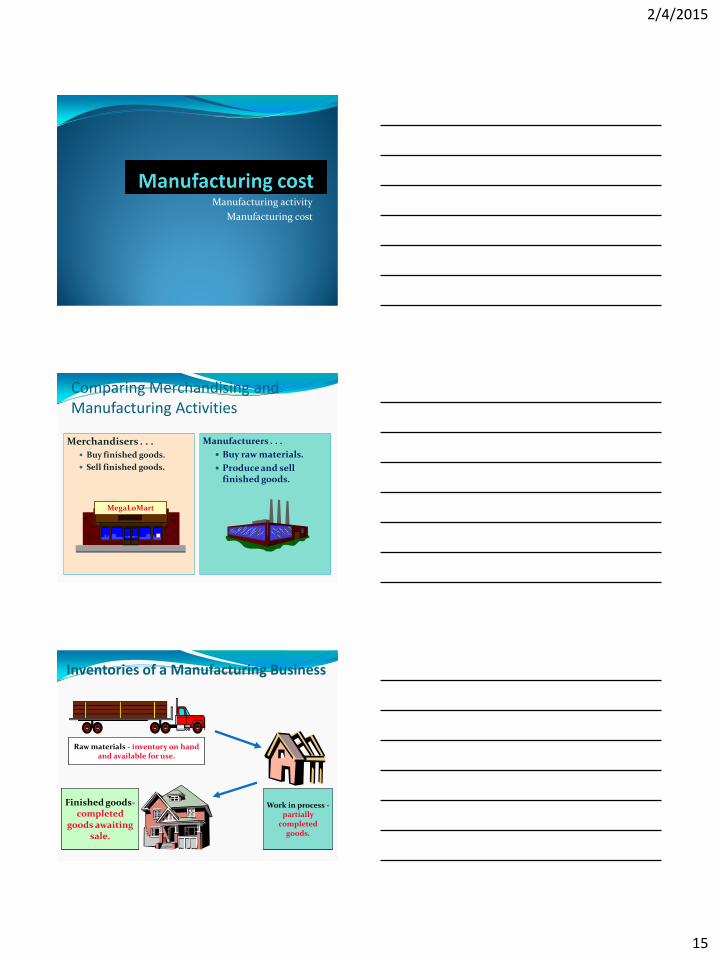

Manufacturing activity

Manufacturing cost

Comparing Merchandising and Manufacturing Activities

Merchandisers

Buy finished goods

Sell finished goods

Manufacturers

Buy raw materials

Produce and sell finished goods

MegaLoMart

inventory on hand Raw materials - inventory on hand and available for use

Work in process -Work in process -partially

completed goods

Finished goods-

goods awaiting

Finished goods-completed

goods awaiting sale

Inventories of a Manufacturing Business

242015

16

Manufacturing consists of activities and processes to convert raw materials into finished goods

Manufacturing costs are the cost to produce a unit of product and typically classified as

Manufacturing activityManufacturing activityManufacturing activityManufacturing activity

The ProductThe Product

DirectMaterials

DirectMaterials

DirectLaborDirectLabor

ManufacturingOverhead

ManufacturingOverhead

Direct Materials Raw materials that become an integral part of the product

(unless used in negligible amounts andor having negligible cost)

Component parts or other materials specially purchased for a particular job order or process

Part-finished work transferred from previous process

Primary packing material (cartons and boxes)

Example What are direct materials in Example What are direct materials in producinged a car

Direct wages Wages paid for labour (either as basic hours

or as overtime) expended on work on the product itself

Example Wages paid to automobile assembly workersExample Wages paid to automobile assembly workers

242015

17

Direct wages ndash activity 1 Classify the following labour costs as either direct or

indirect

The basic pay of direct workers (cash paid tax or other deductions)

The basic pay of indirect workers

Overtime premium (the premium over basic pay for working overtime)

Bonus payments under a group bonus payments scheme

Employerrsquos National Insurance contributions

Idle time of direct workers

Work on installation of equipment

Direct expenses Expenses are incurred on a specific product other than

direct material cost and direct wages

Example

The cost of special designs drawings or layouts

The hire of tools or equipments or a particular job

Maintenance cost of tools fixtures hellip

ProductionManufacturing OverheadManufacturing costs cannot be traced directly to

specific units produced

bullIndirect materials

bull

Maintenance workers janitors and security guardsbull

bullIndirect materials bullMaterials used to support the production process bullExamples Lubricants and cleaning supplies used in the automobile assembly plant

bullIndirect labor bullWages paid to employees who are not directly involved in production work bullExamples Maintenance workers janitors and security guards

bullIndirect expenses bullRent rate Insurance of a factorybullDepreciation fuel power repairs and maintenance of plant machinery and factory buildings hellip

242015

18

Direct Materials

Purchased

Direct Materials

Purchased

Direct Materials

Direct Materials

Used

Direct Direct Labor

Manufacturing Manufacturing Overhead

Finished Finished Goods

Goods SoldGoods Sold

MegaLoMart

Flow of Physical Goods in Production

Nonmanufacturing Costs

Selling Costsoverhead

Costs necessary to get the order and deliver

the product

Administrative Costsoverhead

All executive organizational and

clerical costs associated with the general

management of an organization

Product Costs Versus Period Costs

Inventory

Cost of Goods Sold

BalanceSheet

IncomeStatement

Sale

Product costs include direct materials direct

labor and manufacturing

overhead

Period costs are not included in product

costs They are expensed on the

income statement

Expense

IncomeStatement

242015

19

Quick Check Which of the following costs would be considered a period rather than a product cost in a manufacturing company

A Manufacturing equipment depreciation

B Property taxes on corporate headquarters

C Direct materials costs

D Electrical costs to light the production

facility

E Sales commissions

Prime Cost and Conversion Cost

DirectMaterialDirect

MaterialDirectDirectLabor

ManufacturingManufacturingOverhead

PrimeCost

ConversionCost

Manufacturing costs are oftenclassified as follows

Exercise The Sloane Company specializes in producing a set of

wood patio furniture consisting of a table and four chairs Cost data for the year 2012 as follow

For each item determine it is period cost or product cost direct cost or indirect cost FIXED OR VARIABLE COST

242015

20

Factory labor direct $150000

Advertising $32500

Factory supervision $28000

Property taxes factory building $2000

Sales commissions $97000

Insurance factory $6500

Depreciation office equipment $5000

Lease cost factory equipment $19000

Indirect materials factory $10000

Depreciation factory building $20500

General office supplies (billing) $3500

General office salaries $73000

Direct materials used (wood bolts etc) $120000

Utilities factory $16000

Income statement Report revenues and expenses =gt net profitnet loss

Revenue

- Cost of sales (cost of goods sold)

Gross profit

- Selling expenses

- Administrative expenses

Net income

bull Issue how to calculate cost of goods sold

242015

21

Inventory Flows

Beginningbalance to inventory

Additionsto inventory++ ==

Endingbalance

WithdrawalsWithdrawalsfrom

inventory++

Manufacturing Company

Cost of goods sold

Beg Finished goods inv 14200$

+ Cost of goods manufactured 234150

Goods available for sale 248350$

- Ending finished goods inventory (12100)

= Cost of goods sold 236250$

Schedule of Cost of Goods Manufactured

Calculates the cost of raw material direct labor and

manufacturing overhead used in production

Calculates the manufacturing costs associated with goods

that were finished during the period

Manufacturing Work

Raw Materials Costs In Process

Beginning raw

materials inventory

+ Raw materials

purchased

= Raw materials

available for use

in production

ndash Ending raw materials

inventory

= Raw materials used

in production

As items are removed from raw materials inventory and placed As items are removed from raw materials inventory and placed

into the production process they are called direct

materials

Schedule of Cost of Goods Manufactured

242015

22

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials

materials inventory + Direct labor

+ Raw materials + Mfg overhead

purchased = Total manufacturing

= Raw materials costs

available for use

in production

ndash Ending raw materials

inventory

= Raw materials used

in production

Conversion

direct material finished

Conversion costs are costs

incurred to convert the

direct material into a finished

product

As items are removed from raw materials inventory and placed into

As items are removed from raw materials inventory and placed into

the production process they arecalled direct materials

Schedule of Cost of Goods Manufactured

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials Beginning work in

materials inventory + Direct labor process inventory

+ Raw materials + Mfg overhead + Total manufacturing

purchased = Total manufacturing costs

= Raw materials costs = Total work in

available for use process for the

in production period

ndash Ending raw materials ndash Ending work in

inventory process inventory

= Raw materials used = Cost of goods

in production manufactured

All manufacturing costs incurred

beginning balance of work in process

All manufacturing costs incurred during the period are added to the

beginning balance of work in process

Schedule of Cost of Goods Manufactured

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials Beginning work in

materials inventory + Direct labor process inventory

+ Raw materials + Mfg overhead + Total manufacturing

purchased = Total manufacturing costs

= Raw materials costs = Total work in

available for use process for the

in production period

ndash Ending raw materials ndash Ending work in

inventory process inventory

= Raw materials used = Cost of goods

in production manufactured

Costs associated with the goods that Costs associated with the goods that are completed during the period are

transferred to finished goods inventory

Schedule of Cost of Goods Manufactured

242015

23

Work

In Process Finished Goods

Beginning work in Beginning finished

process inventory goods inventory

+ Manufacturing costs + Cost of goods

for the period manufactured

= Total work in process = Cost of goods

for the period available for sale

ndash Ending work in - Ending finished

process inventory goods inventory

= Cost of goods Cost of goods

manufactured sold

Cost of Goods Sold

Manufacturing Cost Flows

Selling andAdministrative

Period Costs

FinishedGoods

Cost of GoodsSold

Selling andAdministrative

ManufacturingOverhead

Work inProcess

Direct Labor

Balance SheetCosts Inventories

Income StatementExpensesMaterial Purchases Raw Materials

Quick Check

Beginning raw materials inventory was $32000 During the month $276000 of raw material was purchased A count at the end of the month revealed that $28000 of raw material was still present What is the cost of direct material used

A $276000

B $272000

C $280000

D $ 2000

242015

24

Quick Check

Direct materials used in production totaled $280000 Direct labor was $375000 and factory overhead was $180000 What were total manufacturing costs incurred for the month

A $555000

B $835000

C $655000

D Cannot be determined

Quick Check

Beginning work in process was $125000 Manufacturing costs incurred for the month were $835000 There were $200000 of partially finished goods remaining in work in process inventory at the end of the month What was the cost of goods manufactured during the month

A $1160000B $ 910000C $ 760000D Cannot be determined

Quick Check Beginning finished goods inventory was $130000 The cost of goods manufactured for the month was $760000 The ending finished goods inventory was $150000 What was the cost of goods sold for the month

A $ 20000

B $740000

C $780000

D $760000

242015

25

Production costProduct cost

FINISHEDFINISHED GOODSGOODS

Period Cost Cost of good sold

Cost and decision making Fixed and variable cost

Relevant and non - relevant cost

Cost-benefit analysisDifferential analysis

242015

26

Relevant cost Relevant cost is a future cashflow arising as a direct

consequence of a decision

Future cost cost incurred (paid or not yet paid) is irrelevant

Cashflows

Arises as a direct consequence of a decision costs differ under some or all the alternativesavailable opportunities ndash incremental costdifferential costs

Some times expressed as opportunity cost ndash the benefit foregone by choosing one opportunity instead of the next best alternative

Non relevant cost Sunk costs cannot be changed by any decision

They are not differential costs and should be ignored when making decisions (Paid)

Committed costs future cash outflow that will be incurred anyway whatever decision is taken now about alternative opportunities

Notional costsImputed cost no actual cash expense incurred Notional rent charged to the branch for the use of the

buildings owned by the company

Notional interest charges on capital used by the branch

JamCo currently sells 100000 units of its product The company has revenue and costs

as shown below

Per Unit Total

Sales 1000$ 1000000$

Direct materials 350 350000

Direct labor 220 220000

Factory overhead 110 110000

Selling expenses 140 140000

Administrative expenses 080 80000

Total expenses 900$ 900000$

Operating income 100$ 100000$

Example 1

242015

27

JamCo is approached by an overseascompany that offers to purchase

10000 units at $850 per unit

If JamCo accepts the offer total factoryoverhead will increase by $5000 total selling

expenses will increase by $2000 and total administrative expenses will increase

by $1000

Should JamCoaccept the offer

Special Order Decisions

OserCo has 10000 defective units thatcost $100 each to make The units can be

scrapped now for $40 each or rebuilt at an additional cost of $80 per unit

If rebuilt the units can be sold for the normal selling price of $150 each Rebuilding the 10000

defective units will prevent the production of 10000 new units that would also sell for $150

Should OserCo scrap or rebuild

Example 2

Summary of the Types of Cost Classifications

Financial Reporting

Predicting Cost

Behavior

Assigning Costs to Cost

Objects

Decision Making

242015

3

Course objectives

Accounting provide information about economic activities of one organization to interested users

Financial Accounting vs Management accounting

A A field of accounting that provides economic and financial field of accounting that provides economic and financial information for managers and other internal usersinformation for managers and other internal users

Also Also calledcalled Managerial Accounting

Definition of Management AccountingManagement Accounting

Course objectives Provide learners with the understanding and ability to

use cost information for budgeting and forecasting purposes in the management of business

How cost data is collected compiled and analysed and processed into useful information

Deal with budgetary planning and control how to prepare forecasts and budgets and to compare these to actual business results

Consider different costing and budgetary systems and the causes of resulting variances possible implications and corrective action

Learning outcomes1 Be able to analyze cost information within a business

11 Classify different types of cost

12 Using different costing methods

13 Calculate costs using appropriate techniques

14 Analyse cost data using appropriate techniques

2 Be able to propose methods to reduce costs and

enhance value within a business

21 Prepare and analyze routine cost report

22 Use performance indicators to identify potential improvements

23 Suggest improvements to reduce cost enhance value and

quality

242015

4

Learning outcomes3 Be able to prepare forecasts and budgets for a business

31 Explain the purpose and nature of the budgeting process

32 Select appropriate budgeting methods for the organization

and its needs

33 Prepare budgets according to the chosen budgeting method

34 Prepare a cash budget

4 Be able to Monitor performance against budgets within

a business41 Calculate variances identify possible causes and recommend

corrective actions

42 Prepare an operating statement reconciling budgeted and

actual results

43 Report findings to management in accordance with identified

responsibility centers

Week Content

1 Chapter 1 Cost accounting classification and behavior

2 Chapter 2 Material and labor cost

3 Chapter 3 Overhead apportionment and absorption

4 Chapter 4 Marginal and absorption costing

5 Chapter 6 Costing system

6 Chapter 7 Process costing (I)

7 Chapter 5 Price value and quality and checking draft

8 Chapter Review and checking draft

9 Submit assignment 1 and oral examination

10 Chapter 7 Process costing (II)

11 Chapter 8 Budgeting

12 Chapter 8 Budgeting

13 Chapter 9 Standard costing and variance analysis

14 Chapter 10 Responsibility accounting

15 Review and checking draft

STY

DY

ING

PR

OG

RES

S

Warm up activity How does the course related to other subjects that you

have studied

Discuss to form your study group

242015

5

Managing financial resources and decisions

Management accounting

Financial reporting

Review on MFRS Chapter 1- 3 different assets and liabilities

(sources of finances) of a business

Chapter 5 Basis procedures in accounting

Chapter 7 Cost terms and cost classification

Chapter 4 Stocks and cash

Chapter 9 Pricing decisions

Chapter 6 Evaluating financial performance

Chapter 8 Budgets

Activity 1 Review of basis terms in accounting

242015

6

Content Cost concepts

Direct cost vs indirect cost

Cost behavior

Cost estimation

Manufacturing activity and manufacturing costs

Prepare income statement for manufacturer

Costs classification for decision makingdifferential cost analysis

242015

7

Cost concepts Cost ndash sacrificed resource to achieve a specific

objective

Cost accounting measure and reports financial and non financial information relating to the cost of acquiring or utilizing resources in an organization Cost accounting provide information to assist

Establishing stock valuation profit and balance sheet items

Planning

Control

Decision making

Cost concepts Cost unit a unit of product or service to which costs can be

related The cost unit is the basic control unit for costing purposes Can you give some examples

Cost centre cost pool a location or a function or an activity or an item of equipment Each cost centre act as a collecting place for certain cost before they are analyzed further In production department the department itself a machine or

group of machines in the department a foremanrsquos group a workbench

Production ldquoservicerdquo or ldquoback-uprdquo departments (maintenance storehellip)

Administration sales or distribution departments (personnel accounting purchasinghellip

Cost centre of shared costs for directly allocated (rent rates heating lighting)

Cost concepts - example Chocolate cakes production

Cost unit Box of chocolate cake

Cost centers

Mixing department

Baking department

Stores department

242015

8

Cost concepts

Cost centers 1

Cost centers 2

Cost centers 3

Cost unit 1

Cost unit 2

cost

Hanoi 11-16 December 2005 24

Direct costs vs Indirect costs Direct Costs

Costs that can be easily and conveniently traced in full to the product service or department that is being costed

Example Parts Assembly line wages

Indirect Costs

Costs that is incurred in the course of making a product providing a service or running a department but cannot be traced directly and in full to the product service or department Ex Electricity Rent

Instead of being traced these costs are allocated to a cost object in a rational and systematic manner

Direct and indirect cost - examples

SHOP RESTAURANT

242015

9

Cost Behaviorbull Cost behavior the variability of input costs with

bull

bull Cost behavior the variability of input costs with activity undertaken

bull Level of activity amount of work done or the number of events occurred

bull The volume of production in a period

bull The number of item sold

bull The value of items sold

bull The number of invoices issued

bull hellip

Cost Behavior

Behavior of Cost (within the relevant range)

Cost In Total Per Unit

Variable Total variable cost changes Variable cost per unit remains

as activity level changes the same over wide ranges

of activity

Fixed Total fixed cost remains Average fixed cost per unit goes

the same even when the down as activity level goes up

activity level changes

242015

10

Step Costs

A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but A step cost is a cost which is fixed in nature but only within certain levels of activityonly within certain levels of activity

-- Rent depreciation maintenancehellipRent depreciation maintenancehellip

Volume

Co

st

Fixed Monthly

Charge

Variable

Cost per minutes talked

Activity (minutes talked)

To

tal

tele

ph

on

e b

ill

X

Y

A mixed cost has both fixed and variable

costs

A mixed cost has both fixed and variable

components Consider your telephone costs

Mixed Costs semi-variable costs

Fixed Monthly

Charge

Variable

Cost per minutes talked

Activity (minutes talked)

To

tal

tele

ph

on

e b

ill

X

Y

Mixed Costs semi-variable costsThe total mixed cost line can be expressed

as an equation Y = a + bX

Where Y = the total mixed cost

a = the total fixed cost (the

vertical intercept of the line)

b = the variable cost per unit of

activity (the slope of the line)

X = the level of activity

242015

11

Activity 3 Are the following likely to be fixed variable or mixed

cost

Telephone bill

Annual salary of the chief accountant

The management accountantrsquos annual membership fee to his professional body (paid by the company)

Cost of materials used to pack 20 units of product X into a box

Plot the data points on a graph (total Plot the data points on a graph (total Plot the data points on a graph (total Plot the data points on a graph (total cost vs activity)cost vs activity)

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

The Scattergraph Method

242015

12

The Scattergraph Method

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

Draw a line Draw a line through the through the data points data points

points above points above

Draw a line Draw a line through the through the data points data points with about with about an equal an equal

number of number of points above points above and below and below the line the line

The Scattergraph MethodUse one Use one

data point data point to estimate to estimate

total cost total cost

Use one Use one data point data point to estimate to estimate

the totalthe totallevel of level of activity activity and the and the

total cost total cost Intercept = Fixed cost $10000

0 1 2 3 4

Ma

inte

na

nce

Co

st1

00

0rsquos

of

Do

lla

rs

10

20

0

Patient-days in 1000rsquos

X

Y

Patient days = 800Patient days = 800

Total maintenance cost = $11000Total maintenance cost = $11000

The Scattergraph Method

Make a quick estimate of variable cost perMake a quick estimate of variable cost perMake a quick estimate of variable cost perMake a quick estimate of variable cost perunit and determine the cost equation unit and determine the cost equation

Variable cost per unit = $1000

800= $125patient$125patient--dayday

Y = $10000 + $125XY = $10000 + $125XY = $10000 + $125XY = $10000 + $125X

Total maintenance at 800 patients 11000$

Less Fixed cost 10000

Estimated total variable cost for 800 patients 1000$

Total maintenance costTotal maintenance costTotal maintenance costTotal maintenance cost Number of patient daysNumber of patient daysNumber of patient daysNumber of patient days

242015

13

The High-Low MethodAssume the following hours of maintenance work

and the total maintenance costs for six months

]

The High-Low MethodThe The variable cost per variable cost per hourhour of maintenance of maintenance The The variable cost per variable cost per hourhour of maintenance of maintenance

is equal to the is equal to the change in cost change in cost divided by the divided by the

change in hourschange in hours

Hours Total Cost

High 800 9800$

Low 500 7400

Change 300 2400$

The High-Low Method

Total Fixed Cost = Total Cost Total Fixed Cost = Total Cost ndashndash Total Variable CostTotal Variable Cost

Total Fixed Cost Total Fixed Cost ==

Total Fixed Cost Total Fixed Cost ==

Total Fixed Cost Total Fixed Cost ==

242015

14

The High-Low Method

Y = $3400 + $800Y = $3400 + $800XX

The Cost Equation for Maintenance

Quick Check

Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units

Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units are sold Using the high-low method what is thevariable portion of sales salaries and commission

a $008 per unit

b $010 per unit

c $012 per unit

d $0125 per unit

Quick Check

Sales salaries and commissions are $10000 when Sales salaries and commissions are $10000 when 80000 units are sold and $14000 when 120000 units are sold Using the high-low method what is the fixed portion of sales salaries and commissions

a $ 2000

b $ 4000

c $10000

d $12000

242015

15

Manufacturing activity

Manufacturing cost

Comparing Merchandising and Manufacturing Activities

Merchandisers

Buy finished goods

Sell finished goods

Manufacturers

Buy raw materials

Produce and sell finished goods

MegaLoMart

inventory on hand Raw materials - inventory on hand and available for use

Work in process -Work in process -partially

completed goods

Finished goods-

goods awaiting

Finished goods-completed

goods awaiting sale

Inventories of a Manufacturing Business

242015

16

Manufacturing consists of activities and processes to convert raw materials into finished goods

Manufacturing costs are the cost to produce a unit of product and typically classified as

Manufacturing activityManufacturing activityManufacturing activityManufacturing activity

The ProductThe Product

DirectMaterials

DirectMaterials

DirectLaborDirectLabor

ManufacturingOverhead

ManufacturingOverhead

Direct Materials Raw materials that become an integral part of the product

(unless used in negligible amounts andor having negligible cost)

Component parts or other materials specially purchased for a particular job order or process

Part-finished work transferred from previous process

Primary packing material (cartons and boxes)

Example What are direct materials in Example What are direct materials in producinged a car

Direct wages Wages paid for labour (either as basic hours

or as overtime) expended on work on the product itself

Example Wages paid to automobile assembly workersExample Wages paid to automobile assembly workers

242015

17

Direct wages ndash activity 1 Classify the following labour costs as either direct or

indirect

The basic pay of direct workers (cash paid tax or other deductions)

The basic pay of indirect workers

Overtime premium (the premium over basic pay for working overtime)

Bonus payments under a group bonus payments scheme

Employerrsquos National Insurance contributions

Idle time of direct workers

Work on installation of equipment

Direct expenses Expenses are incurred on a specific product other than

direct material cost and direct wages

Example

The cost of special designs drawings or layouts

The hire of tools or equipments or a particular job

Maintenance cost of tools fixtures hellip

ProductionManufacturing OverheadManufacturing costs cannot be traced directly to

specific units produced

bullIndirect materials

bull

Maintenance workers janitors and security guardsbull

bullIndirect materials bullMaterials used to support the production process bullExamples Lubricants and cleaning supplies used in the automobile assembly plant

bullIndirect labor bullWages paid to employees who are not directly involved in production work bullExamples Maintenance workers janitors and security guards

bullIndirect expenses bullRent rate Insurance of a factorybullDepreciation fuel power repairs and maintenance of plant machinery and factory buildings hellip

242015

18

Direct Materials

Purchased

Direct Materials

Purchased

Direct Materials

Direct Materials

Used

Direct Direct Labor

Manufacturing Manufacturing Overhead

Finished Finished Goods

Goods SoldGoods Sold

MegaLoMart

Flow of Physical Goods in Production

Nonmanufacturing Costs

Selling Costsoverhead

Costs necessary to get the order and deliver

the product

Administrative Costsoverhead

All executive organizational and

clerical costs associated with the general

management of an organization

Product Costs Versus Period Costs

Inventory

Cost of Goods Sold

BalanceSheet

IncomeStatement

Sale

Product costs include direct materials direct

labor and manufacturing

overhead

Period costs are not included in product

costs They are expensed on the

income statement

Expense

IncomeStatement

242015

19

Quick Check Which of the following costs would be considered a period rather than a product cost in a manufacturing company

A Manufacturing equipment depreciation

B Property taxes on corporate headquarters

C Direct materials costs

D Electrical costs to light the production

facility

E Sales commissions

Prime Cost and Conversion Cost

DirectMaterialDirect

MaterialDirectDirectLabor

ManufacturingManufacturingOverhead

PrimeCost

ConversionCost

Manufacturing costs are oftenclassified as follows

Exercise The Sloane Company specializes in producing a set of

wood patio furniture consisting of a table and four chairs Cost data for the year 2012 as follow

For each item determine it is period cost or product cost direct cost or indirect cost FIXED OR VARIABLE COST

242015

20

Factory labor direct $150000

Advertising $32500

Factory supervision $28000

Property taxes factory building $2000

Sales commissions $97000

Insurance factory $6500

Depreciation office equipment $5000

Lease cost factory equipment $19000

Indirect materials factory $10000

Depreciation factory building $20500

General office supplies (billing) $3500

General office salaries $73000

Direct materials used (wood bolts etc) $120000

Utilities factory $16000

Income statement Report revenues and expenses =gt net profitnet loss

Revenue

- Cost of sales (cost of goods sold)

Gross profit

- Selling expenses

- Administrative expenses

Net income

bull Issue how to calculate cost of goods sold

242015

21

Inventory Flows

Beginningbalance to inventory

Additionsto inventory++ ==

Endingbalance

WithdrawalsWithdrawalsfrom

inventory++

Manufacturing Company

Cost of goods sold

Beg Finished goods inv 14200$

+ Cost of goods manufactured 234150

Goods available for sale 248350$

- Ending finished goods inventory (12100)

= Cost of goods sold 236250$

Schedule of Cost of Goods Manufactured

Calculates the cost of raw material direct labor and

manufacturing overhead used in production

Calculates the manufacturing costs associated with goods

that were finished during the period

Manufacturing Work

Raw Materials Costs In Process

Beginning raw

materials inventory

+ Raw materials

purchased

= Raw materials

available for use

in production

ndash Ending raw materials

inventory

= Raw materials used

in production

As items are removed from raw materials inventory and placed As items are removed from raw materials inventory and placed

into the production process they are called direct

materials

Schedule of Cost of Goods Manufactured

242015

22

Manufacturing Work

Raw Materials Costs In Process

Beginning raw Direct materials

materials inventory + Direct labor

+ Raw materials + Mfg overhead

purchased = Total manufacturing

= Raw materials costs

available for use

in production

ndash Ending raw materials

inventory

= Raw materials used

in production

Conversion

direct material finished

Conversion costs are costs

incurred to convert the

direct material into a finished

product