m&a deal report - sparke helmore lawyers · reopening of china’s capital markets ... (slide...

TRANSCRIPT

1

M&A Deal Report May 2015

Contact: Nick Humphrey

Partner and Head of Corporate

Sparke Helmore Lawyers

tel + 61 2 9260 2747

Global activity in 2014

Australian activity in 2014

Sparke Helmore Deal

Trends Report

3

Global M&A highlights

Dramatic rebound in global M&A for

calendar year 2014 (only 11.8% by value

below 2007 peak levels)

Global 2014 saw a 44.7% increase by value

(US$3,230bn) on 2013’s total

(US$2,232.5bn)

US record levels with a 55.6% increase by

value (US$1,409bn) on 2013’s total

(US$900.1bn) and a 21.5% increase in deal

count (4,782)

Best year for Asia Pacific M&A on record

(62% increase on 2013 levels)

European M&A up 55%

Close to pre-GFC levels Global quarterly trend

Sources: Mergermarket 2014 M&A Deal Trend Report, Thomson Reuters Mergers and Acquisitions Review – Financial Advisors Full Year 2014

4

Australian M&A activity

Australian-announced M&A up 20% (US$119.8bn), the highest full year total since 2011

Large deals v mid-market

Source: Baker Tilly Pitcher Partners Dealmakers: Middle Market M&A in Australia 2015

16%

43%

18%

7%

7%

5% 4%

US$0m - US$9m

US$10m - US$50m

US$51m - US$150m

US$151m - US$250m

US$251m - US$500

US$501 - US$1,000m

>US$1,001m

Increase in large-value transactions

continued into Q1 2015 (e.g

Federation Centres/Novion Property

Group (US$8.2bn) and Japan Post /

Toll Holdings (US$6.3bn))

However, mid-market transactions

(US$10m to US$ 250m) still accounted

for 68% of all Australian M&A in 2014

5

Global private equity

Global record in private equity exits by both value

(to 21.4% above 2007's peak) and number of deals at

2,054

Strategic buyers bought 715 PE portfolio

companies (13% more than in 2013) for

US$303bn (a 91% jump) – led by the sale

of Alliance Boots by KKR to Walgreen

Global buy-out backed IPO’s numbered 210 (20%

more than in 2013) with a value of US$86bn (up

48%) – Asia Pacific IPO numbers buoyed by the

reopening of China’s capital markets (eg US$21.8bn

listing of Alibaba)

60% of assets sold had been held for more than five

years with fewer than 10% held for less than three

years. Fund-raising and investments remained steady

Record exits Global trend

Source: Bain & Company Global Private Equity Report 2015

6

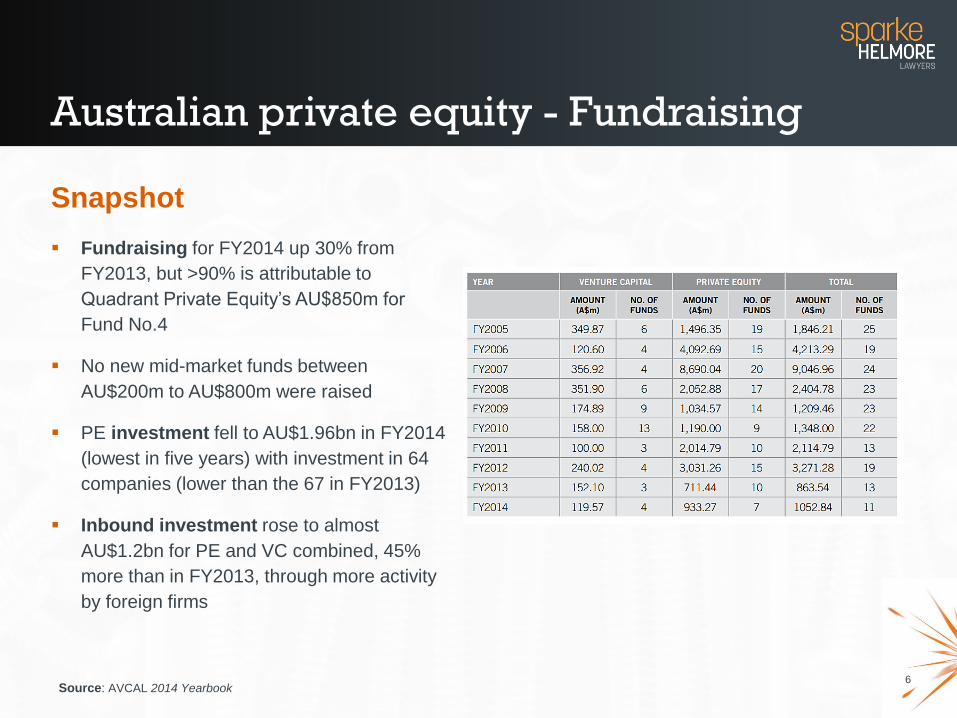

Australian private equity - Fundraising

Fundraising for FY2014 up 30% from

FY2013, but >90% is attributable to

Quadrant Private Equity’s AU$850m for

Fund No.4

No new mid-market funds between

AU$200m to AU$800m were raised

PE investment fell to AU$1.96bn in FY2014

(lowest in five years) with investment in 64

companies (lower than the 67 in FY2013)

Inbound investment rose to almost

AU$1.2bn for PE and VC combined, 45%

more than in FY2013, through more activity

by foreign firms

Snapshot

Source: AVCAL 2014 Yearbook

7

Australian private equity - Exits

FY14 exit proceeds were highest in five years, led by

upturn in Australian equity capital markets: 29% of portfolio

company exits and 63% of total divestment at cost

Source: AVCAL 2014 Yearbook

8

Other key statistics

IPO market was strong with 74 floats raising $26bn (56 in 2013

raising $11.9bn)

Australia saw considerable interest from overseas investors

including PE funds and Sovereign Wealth in financial services,

education, agriculture

Healthy tech sector with active angel groups and venture investors

Strong IPO market means private M&A having to compete on price

and terms (so high multiples, less warranty protection and less

earn-outs)

9

Sparke Helmore

Deal Trends

Report

10

We reviewed 79 share purchase agreements (SPA) over last 3 years

We focused on mid-market and excluded deals over $250m

Broad spectrum of deal sizes with average around $30m

We had mixture of roles (buyer, seller, management, insurer)

There were dozens of different law firms (so reasonable test of

market custom)

25% = total deals involving a PE fund, VC fund or sovereign wealth

fund

23.6% include a cross-border element

Sparke Helmore Deal Trends Report

11

Deal Trends Report - general

Broad range of structures used

When referring to what is “customary”, note:

Some mechanisms interrelated (if you have protection of W&I

insurance, parent guarantee or escrow may be less likely to

push other protections)

Depends on pricing, balance of power, regional differences

In competitive deals (auction situation) more likely to be seller

friendly

Depends on “house rules” (big difference between trade deal,

receiver sale and PE deal)

12

Warranties

13

Warranties – escrow

Escrow or retention amount for potential warranty

breaches

Of those deals that used an escrow amount, what

number also used W & I insurance?

Australia

12%

22%

US deals included an escrow or holdback

Size of escrow

Escrow period

US

97%

Avg 11.8%

Avg 18 months

Source: SRS Acquiom M&A Deal Terms Study

14

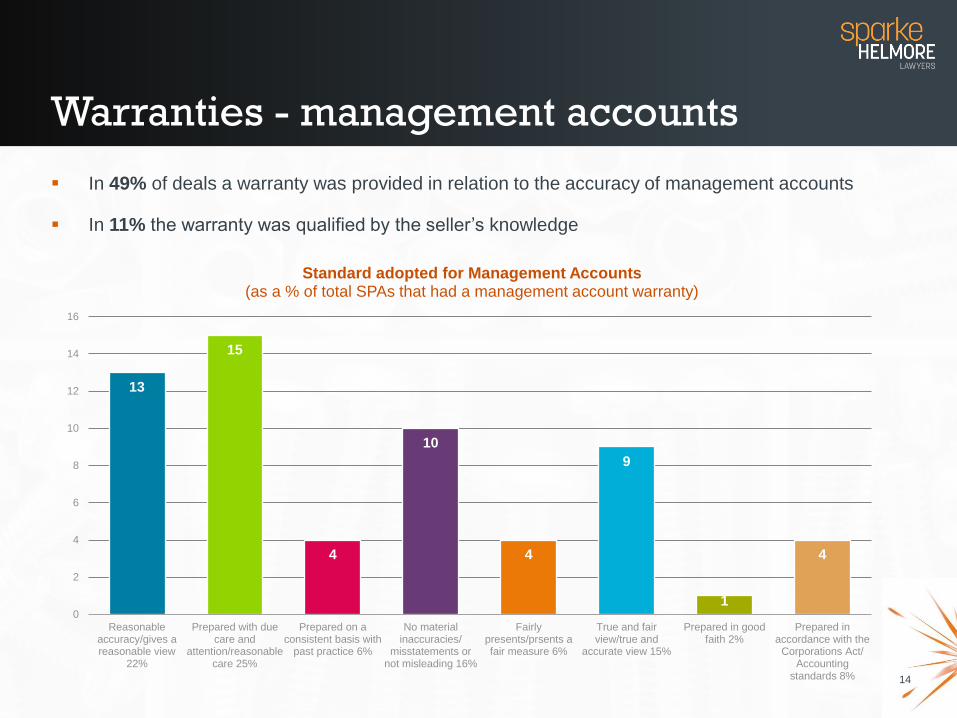

Warranties - management accounts

In 49% of deals a warranty was provided in relation to the accuracy of management accounts

In 11% the warranty was qualified by the seller’s knowledge

13

15

4

10

4

9

1

4

0

2

4

6

8

10

12

14

16

Reasonableaccuracy/gives areasonable view

22%

Prepared with duecare and

attention/reasonablecare 25%

Prepared on aconsistent basis with

past practice 6%

No materialinaccuracies/

misstatements ornot misleading 16%

Fairlypresents/prsents afair measure 6%

True and fairview/true and

accurate view 15%

Prepared in goodfaith 2%

Prepared inaccordance with the

Corporations Act/Accounting

standards 8%

Standard adopted for Management Accounts (as a % of total SPAs that had a management account warranty)

15

Warranties - general statistics

Australia US

Specific seller indemnities 44%

Disclosure letter/schedule 60% High

Seller was permitted to disclose data room generally against warranties 63% Low

Warranty provided for quality of data in data room 65%

‘No undisclosed liability’ warranty 32% 94%

Of those deals, the warranty was qualified by the seller’s knowledge 21% 5%

Right for the buyer to terminate prior to closing for breach of warranties 29%

Of those, the termination right could only be triggered if the breach had a

material adverse affect 50%

Source: Private Target Mergers & Acquisitions Deal Points Study (2013) (slide 47)

16

Warranties – time limits (other than tax and title)

US deals

Source: 2014 SRS Acquiom M&A Deal Terms Study

6%

27%

4%

36%

8%

16%

3%

24 months +

24 months

>18 months <24months

18 months

>12 months <18months

12 months

Less than 12 months

Australian deals

0%

13%

0%

52%

9%

26%

0%

24 months +

24 months

>18 months <24months

18 months

>12 months <18months

12 months

Less than 12 months

17

Warranties – Tax/Title Warranties

In 76% of our deals there was a cap on claims for breaches of title/tax warranties

3% 5%

5% 3%

16%

68%

Australian deals (% of purchase price)

0% - 25% 26% - 49% 50%

51% - 75% 76% - 99% 100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100% more than7 years

7 years

5 years

Less than5 years

Australian deals (Time Limit in Tax Warranty claims)

18

Warranties - aggregate claim thresholds

Aggregate threshold for warranty claims: 68% of our deals 97% US deals

56%

25%

8%

11%

Australian deals

0.0% - 1.0% (56%) 1.1% - 2.0% (25%)

2.1% - 3% (8%) 3.1% + (11%)

89%

8%

2% 1%

US deals

0.0% - 1.0% (89%) 1.1% - 2.0% (8%)

2.1% - 3.0% (2%) 3.1% + (1%)

Source: SRS Acquiom M & A Deal Terms Study 2014 (slide 59)

19

Warranties - de minimus thresholds

Minimum claim threshold: 71% of our deals 20% US deals

45%

28%

10%

11%

6%

Minimum claim thresholds- Australian Deals (as % of purchase price)

0.0 - less than 0.1 (44%)

0.1 - less than 0.5 (27%)

0.5 - less than 1.0 (11%)

1.0 - less than 1.5 (11%)

1.5+ (7%)

Source: US data from SRS Acquiom M & A Deal Terms Study 2014 (slide 63)

20

Warranties - caps on claims (other than title and tax)

In 78% of our deals there was a cap on claims for breaches of seller warranties.

12%

12%

34%

17%

8%

17%

Australian deals (as % of purchase price)

0% - 25% 26% - 49% 50%

51% - 75% 76% - 99% >=100%

Source: SRS Acquiom M & A Deal Terms Study 2014 (slide 66)

Mean = 12.9%

Median = 10.00%

Minimum = 2.00%

Maximum = 53.2%

US deals (as % of purchase price)

21

Purchase price

adjustments

(other than earn-

outs)

22

Purchase price adjustments

Australian deals US deals

No AdjustmentProvision (48%)

IncludesAdjustmentProvision (52%)

Source: Private Target Mergers & Acquisitions Deal Points Study (2013) (slide 13)

No AdjustmentProvision (15%)

IncludesAdjustmentProvision (85%)

23

Purchase price adjustments – adjustment methodology

Australian deals US deals

Net Debt (10%)

CapitalExpenditure (7%)

Net Assets (27%)

Net WorkingCapital (68%)

Other (14%)

Net Debt (10%)

CapitalExpenditure…

Net Assets (3%)

Net WorkingCapital (91%)

Other (35%)

Purchase price adjustment paid only if exceeds threshold: 4% of our deals 9% US deals

Source: Private Target Mergers & Acquisitions Deal Points Study (2013) (slides 13; 19)

24

Locked Box Mechanisms

Source: ‘The ‘locked box’ mechanism - brings more certainty to M & A transactions’, PriceWaterhouseCoopers

Australian Deals UK Deals US Deals

In 5% of our deals, the

purchase price was

determined via a ‘locked

box’ mechanism

In 25% of deals with a

‘locked box’ mechanism

there was a private

equity, venture capital or

sovereign wealth fund

involved

In approximately 50% of

UK deals, the purchase

price is determined via a

‘locked box’ mechanism -

this figure is increasing

Locked Box Mechanisms

are very rare in US deals

25

Earnouts

26

Earnouts

Australian deals US deals

% of deals with earn-out 23% 13%

Earn-out was referrable to

EBITDA/earnings 80% 20%

Median earn-out duration 20 months 27 months

Source: SRS Acquiom M&A Deal Terms Study (slide 18)

27

Earnouts – period of earnout

48 months(5.5%)

36 months(17%)

>24 to <36 months (5.5%)

24 months(22.5%)

>12 to <24 months (5.5%)

12 months(16%)

<12 months(28%)

Source: Private Target Mergers & Acquisitions Deal Points Study (2013) (slide 21)

US deals Australian deals

not determinable(21%)

48 months(12%)

36 months(9%)

>24 to <36 months (3%)

24 months(18%)

>12 to <24 months (0%)

12 months(32%)

<12 months(6%)

28

Earn-outs – acceleration and covenants

Source: SRS Acquiom M&A Deal Terms Study 2014 (slide 19)

Of those deals with

earn-outs: Australia US

Covenant to run 17%

• 13% of US deals in 2013 had a

covenant to run in accordance with

seller’s past practices

• 20% of US deals in 2013 had a

covenant to run the business to

maximise earn-out payment clause

Acceleration clause 14%

• 13% of US deals had an acceleration

clause that accelerated payment

(fully or partially) on change in

control of earn-out assets

Lapsing clause 14%

29

Other key features

Non-cash consideration (scrip) was utilised in 20% of our deals.

In US deals, 21% of deals utilised scrip consideration.

Material adverse change (MAC) condition precedent more

commonly used than pre-GFC. 30% of our deals used a MAC

condition precedent; 94% of US deals in 2012.

In US in 2014:

only 11% of MAC include “prospects” (trending down from 24%

in 2010) - so more seller friendly;

95% of these conditions include “force majeure carve-outs”

(ie. material change other than due to change in economic

conditions, act of war or terrorism, change in law etc).

Source: SRS Acquiom M&A Deal Terms Study 2014 (slide 10); ABA Private Target Mergers & Acquisitions Deal Points Study 2013 (slide 67)

30

Warranty &

Indemnity (W&I)

Insurance

31

W&I Insurance

• W & I insurance was used in 9% of deals

• In 85% of deals that had W&I insurance it was taken out

by the buyer

• In 27% of deals where W&I insurance was used, the deal

also involved a private equity fund, venture capital fund

or sovereign wealth fund

• In 12% of deals that had W&I insurance, ‘new breach

cover’ was used in the policy

32

W&I Insurance

19% of deals that used W&I insurance had a foreign

buyer

19% of deals that used W&I insurance had multiple

sellers

7% of deals that used W&I insurance were a partial

sell-down of shares

33

About Sparke Helmore

Nick Humphrey Partner & Head of National Corporate Group

Sparke Helmore Lawyers

Tel: (02) 9260 2747

www.sparke.com.au

Sparke Helmore celebrated its 130 anniversary in 2012 and is an integrated, national full service law firm. Our

Corporate Group is dedicated to providing a boutique offering servicing mid-market M&A, banking and private equity,

delivering world class service and expertise. Our team combines senior partners and associates with experience

gained on some of the most iconic and cutting edge deals while working in top tier Australian and global law firms.

Sparke Helmore is a proud partner of the Australian Growth Company Awards, alongside Deloitte, Macquarie Capital,

Intralinks, MYOB, AVCAL, 2020 Exchange, The Australian and Private Equity Media.

Some of our key clients include Macquarie Bank, CHAMP Ventures, Anacacia Capital, Olympus Capital, Westpac

and AMP.

Nick Humphrey is the Head of Corporate and Head of Private Equity at Sparke Helmore. Nick chairs the annual

Australian Growth Company Awards and wrote the Australian Private Equity Handbook (CCH), a plain English guide

with step-by-step advice on implementing PE transactions. Nick has been recognised by a number of influential

awards as one of Australia's leading private equity and M&A lawyers, including PLC, Chambers & Partners Asia, The

Legal 500 Asia Pacific, IFLR, Euromoney’s Guide, AFR’s Best Lawyers and Global Private Equity Counsel. He was a

finalist for Dealmaker of the Year and The Partner Award in the Lawyers Weekly Australian Law Awards