magnesita 3 q12_presentation_en

DESCRIPTION

TRANSCRIPT

1

Earnings Call – 3Q12 November 9th, 2012

2

Index

3Q12 Highlights New strategic view

3

Consolidated Revenues (R$ million)

Quarter YTD

561.5637.6 608.1

3Q11 2Q12 3Q12

1,719.81,852.6

9M11 9M12

-4.6%

+8.3% +7.7%

50.2%

18.1%

22.6%

9.0%

2Q12

50.9%

16.9%

22.4%

9.4%0.4%

3Q11

49.1%

21.6%

20.0%

9.3%

3Q12

South America

North America

Europe

Asia

RoW

4

87.0% 84.0% 86.3%

13,0%16,0% 13,7%

3Q11 3Q11 3Q12

Steel Industrial

496.7 566.9 535.2-5.6%

+7.7%

86.0% 84.0%

14,0%16,0%

9M11 9M12

Steel Industrial

1,517.81,652.4

+8,9%

Revenues – Refractories Solutions (R$ million)

Steel Industrial

Quarter Acumulated

432.0476.3 462.0

3Q11 3Q11 3Q12

6.9%

-3.0%1,305,4

1,388.9

9M11 9M12

6.4%

64.7

90.673.1

3Q11 3Q11 3Q12

13.1%

-19.2%212.4

263.6

9M11 9M12

24.1%

5

Gross profit and gross margin by segment

Segment (R$ million) Quarter Var. % YTD Var. %

Refractory Solution 3Q12 (a) 2Q12 (b) 3Q11 (c) (a/b) (a/c) 9M12 (d) 9M11 (e) (d/e)

Gross Profit (R$ million) 165.9 183.6 160.1 -9.6% 3.7% 519.1 494.4 5.0%

Gross Margin (%) 31.0% 32.4% 32.2% -139 bp -122 bp 31.4% 32.6% -116 bp

Minerals

Gross Profit (R$ million) 13.6 14.8 14.2 -8.1% -4.2% 38.9 38.7 0.6%

Gross Margin (%) 45.0% 43.7% 50.6% 128 bp -559 bp 43.5% 46.2% -275 bp

Services

Gross Profit (R$ million) 5.9 3.2 3.8 87.7% 56.3% 10.8 14.0 -22.5%

Gross Margin (%) 13.9% 8.6% 10.4% 533 bp 354 bp 9.8% 11.8% -202 bp

TOTAL

Gross Profit (R$ million) 185.5 201.6 178.1 -8.0% 4.2% 568.9 547.1 4.0%

Gross Margin (%) 30.5% 31.6% 31.7% -112 bp -122 bp 30.7% 31.8% -111 bp

6

EBITDA and Net profit

EBITDA and EBITDA margin R$ million and %

Net profit and net margin R$ million and %

118.7105.2

84.3

21.1%

16.5%13.9%

3Q11 (c) 2Q12 (b) 3Q12 (a)

EBITDA EBITDA Margin (%)

315.7277.0

18.4%

15.0%

9M11 9M12

EBITDA Margem EBITDA (%)

34.4 36.7

10.7

6.1% 5.8%

1.8%

3Q11 (c) 2Q12 (b) 3Q12 (a)

Net Profit Net Margin (%)

87.075.8

5.1%

4.1%

9M11 9M12

Net Profit Net Margin (%)

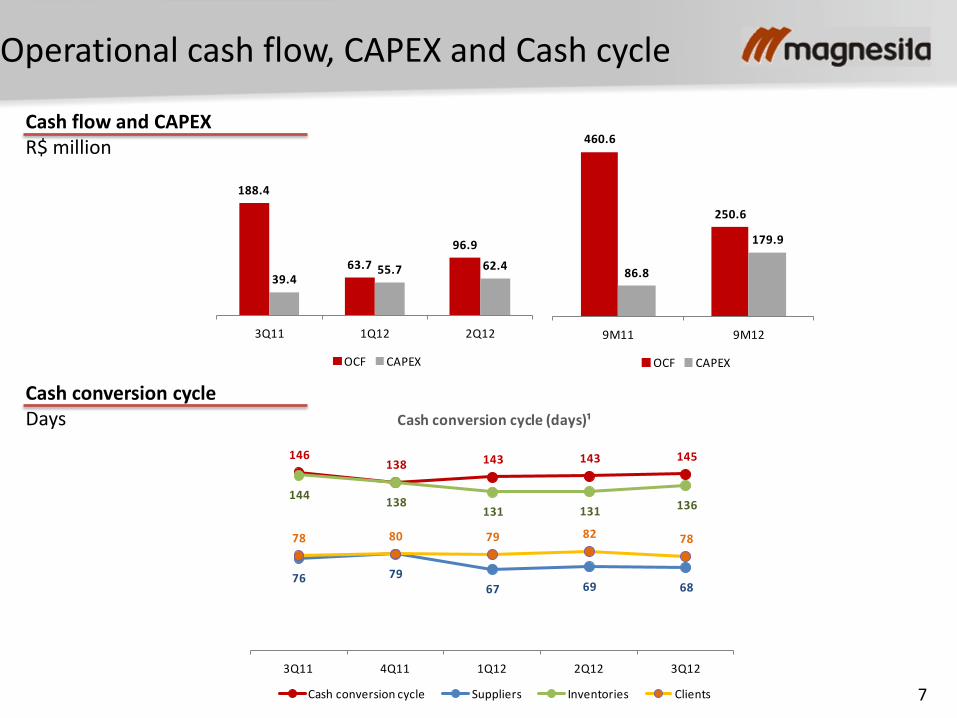

7

188.4

63.7

96.9

39.455.7 62.4

3Q11 1Q12 2Q12

OCF CAPEX

460.6

250.6

86.8

179.9

9M11 9M12

OCF CAPEX

Operational cash flow, CAPEX and Cash cycle

Cash flow and CAPEX R$ million

Cash conversion cycle Days

146 138 143 143 145

76 79 67 69 68

144 138

131 131 136

78 80 79 82 78

3Q11 4Q11 1Q12 2Q12 3Q12

Cash conversion cycle (days)¹

Cash conversion cycle Suppliers Inventories Clients

8

Debt and leverage

Net debt and leverage R$ million

Debt profile

900.2 957.3 968.0

1,060.0 1,074.4

787.7 761.2 791.8 819.1 834.7

2.11x2.24x 2.30x

2.51x

2.76x

3Q11 4Q11 1Q12 2Q12 3Q12

Net Debt Working capital Net Debt/EBITDA

6.8%

93.2%

Short term Long term

16.9%

83.1%

Local currency (BRL) Foreign currencies

9

3Q12 Highlights

• Net revenue of R$ 608.1 million, up 8.3% over 3Q11, but down 4.6% over 2Q12

• EBITDA of R$84.3 million, margin 13.9%, compared to R$118.7 million (margin 21.1%) in 3Q11 and

R$105.2 million (margin 16.5%) in 2Q12.

• Services: Revenue of R$42.7 million with gross margin at 13.9%, compared to R$36.6 million (margin at

10.4%) in 3Q11 and R$36.8 million (margin 8.6%) in 2Q12

• Brumado Expansion: Went into operation the new furnace in Brumado (Brazil), increasing the

production capacity of high-grade magnesite sinter to 240,000 tons per year

• Graphite Project: Obtainment of the Preliminary Environmental License

10

Index

3Q12 Highlights New strategic view

11

The new vision and the 4 strategy pillars

Vision: Be the best provider of refractories solutions and industrial minerals,

leveraging and developing our minerals base

Continue to develop high quality, low cost raw material sources to support our current busi-nesses as well as new businesses where we can have a sustainable com-petitive advantage

Strive to keep offering high quality and innovative products, unrivaled services and cost performance

Optimize production globally to improve efficiency and support growth

Develop global supply chain management

Pursue long term growth opportunities in selected markets where we can deliver superior value to our customers and shareholders

Expand industrial minerals base

Ensure leadership in our core markets

Maintain a global low cost production base

Grow selectively and aggressively

▪ Meritocracy

▪ Ethics

▪ Profit

▪ Management and Method

▪ Customer

▪ People

▪ Agility and Transparency

▪ Respect for Safety, Environment and Communities

Our values

On

e g

lob

al o

rgan

iza

tio

n

12

Magnesita 2017

Industrial Minerals

New

refractories markets

Core refractories markets

Integrated product offer:

•Raw materials •Refractory Solutions

•Services

• Largest magnesite mine ex-China • Low-cost/high quality source for relevant refractories raw materials • Portfolio of industrials minerals in Brazil

•Leadership in South America and dolomite products

• Sustainable position in selected markets with focus in growth and industrial applications

13

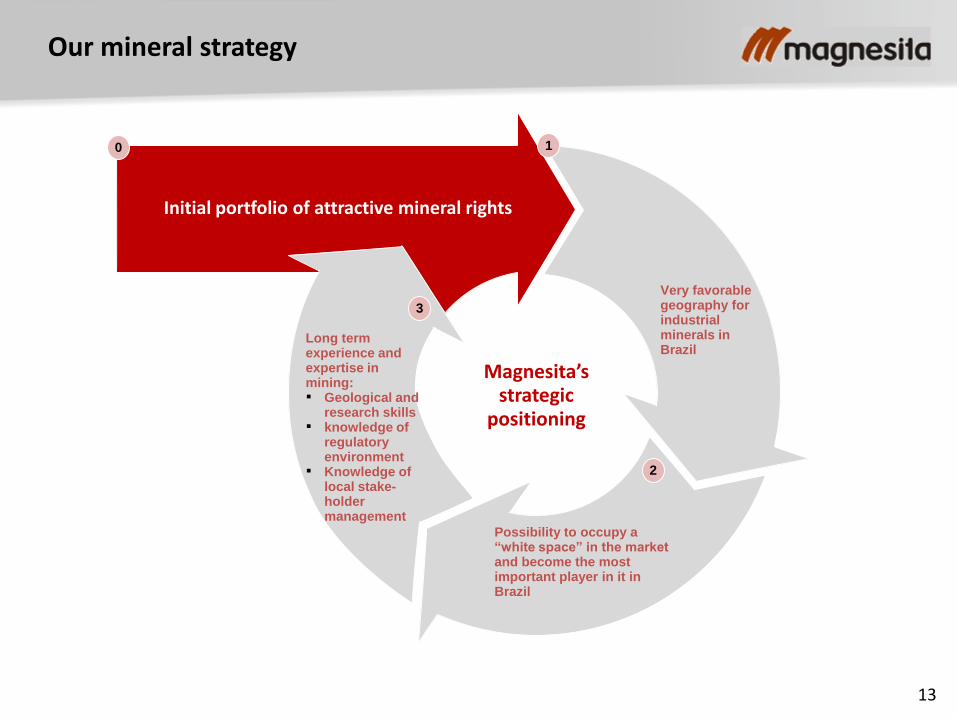

Our mineral strategy

Initial portfolio of attractive mineral rights

Very favorable geography for industrial minerals in Brazil

Possibility to occupy a “white space” in the market and become the most important player in it in Brazil

0 1

2

3

Magnesita’s strategic

positioning

Long term experience and expertise in mining: ▪ Geological and

research skills ▪ knowledge of

regulatory environment

▪ Knowledge of local stake-holder management

14

Investor Relations contacts:

Octavio Pereira Lopes

CEO and IRO

Daniel Domiciano Silva

Investor Relations

Phone: 55 11 3152-3202/3241

www.magnesita.com