maintaining letter of credit & some basic theory

TRANSCRIPT

Presented by

Md. Samsujjaman (Sobuj)

Senior Officer

Finance & Accounts Dept.

New Hope Farms Bangladesh Ltd

Mamarishpur, Mollikbari, Bhaluka, Mymensingh.

Cell: +8801710357458

Email: [email protected]

The name "letter of credit" derives from the French word "accréditation", a power to do something, which derives from the Latin "accreditivus", meaning trust.

Letter of Credit: Is a written instruments issued by a bank at the request of customer, the importer (buyer), whereby the bank promises to pay the Exporter (Beneficiary) for goods or services, provided that the Exporter represents all documents call for, exactly as stipulated in the letter of credit, and meet all others terms and condition set out in the letter of credit.

But in Europe prefer to use “documentary credit” or “D/C” instead of L/C.

a) Central Bank

b) Foreign Exchange management act /Custom Act

c) Uniform Custom and Practice for Documentary Credit (UCPDC)

d) International Chamber and Commerce (ICC)

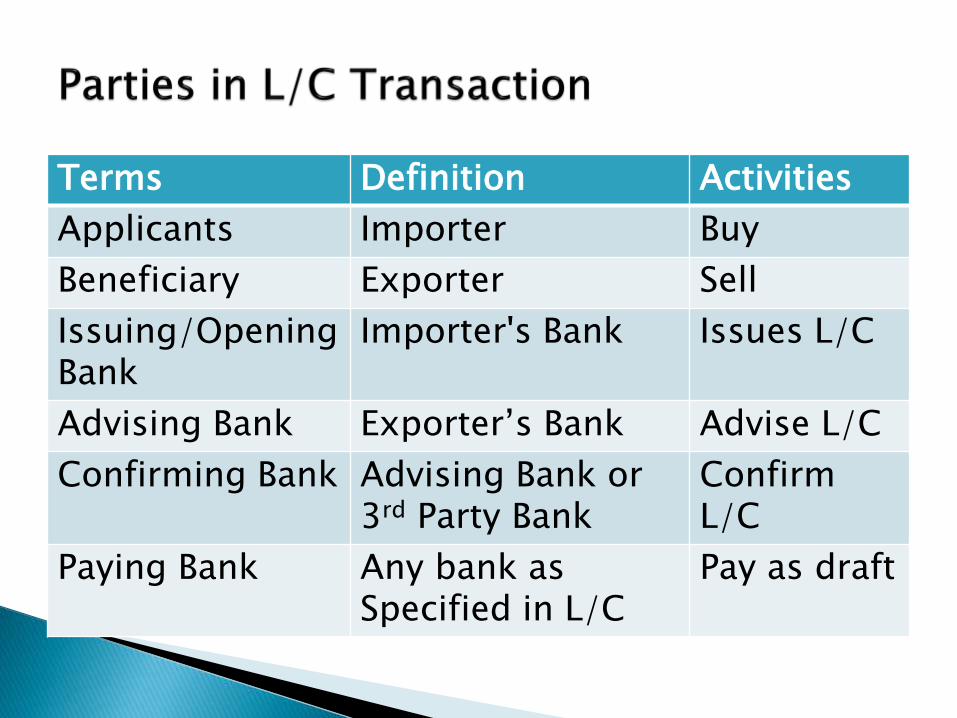

A transaction in a Letters of Credit may involved several parties from the issue of the L/C till making payment of the bill to the seller-

a) Applicant/Importer/Consignee: The buyer who finalizes the terms & conditions of purchase transaction and submits the request to his bank for issuing L/C in favor of seller.

b) Beneficiary/Exporter/Consigner: The seller of the Letter of Credit is generally the person in whose favor the credit has been issued.

Issuing Bank/Opening Bank: An issuing bank is the one which on receipt of the request from it’s customer, the applicant (buyer’s) bank examines the proposal and open L/C in favor of beneficiary with the stipulated terms and conditions.

Advising Bank/Corresponding Bank: In case of seller (beneficiary) reside in a foreign country or different place, the issuing bank may contact some others bank in the beneficiary country may agree to advice the credit to the beneficiary & thus play the role of an advising bank.

Confirming Bank: The confirming bank adds it’s guarantee to the credit opened by another bank, thereby undertaking the responsibility of payments/negotiation acceptance under the credit, in additional to that of the issuing bank. Confirming bank playing an important role where the exporter is not satisfied with the undertaking of only the issuing bank.

Reimbursing Bank: Reimbursing bank is the bank authorized to honor the reimbursement claim in the settlement of negotiation/acceptance/payments lodged with it by the negotiation bank. It is normally the bank with which issuing bank has an account from which payment has to be made.

Nominated/Negotiating Bank: The negotiating bank is the bank who negotiates the documents submitted to them by the beneficiary under the credit either advised though them or restricted to them for negotiation. On negotiation of the documents they will claim the reimbursement under their credit and makes the payment to the beneficiary provided the documents submitted are in accordance with the terms & conditions of the L/C.

Terms Definition Activities

Applicants Importer Buy

Beneficiary Exporter Sell

Issuing/OpeningBank

Importer's Bank Issues L/C

Advising Bank Exporter’s Bank Advise L/C

Confirming Bank Advising Bank or 3rd Party Bank

Confirm L/C

Paying Bank Any bank as Specified in L/C

Pay as draft

H.S (Harmonized System) Code: The HS was created and is administered by the Brussels-based World Customs Organization (WCO). There has 8 digit & The first 6 digits of an HS code indicate the same product description for all 190 countries, but that does not mean that the rates of customs duties are the same & other 2 digit country Identification of goods or Services.

Tenor: The length of time until a loan is due. For L/C purpose usually it would credit 30/45/60/90/180 days for reimbursement.

SWIFT: SWIFT stand for Society for World wide Interbank Financial Telecommunication. Belgium based global banking network that enrich 6495 banks & financial institute in 178 countries 24 hours a day. SWIFT is highly secure network to send & receive fund transfer, L/C related, remittance message etc.

Payment At Sight: A payment due on demand. An at sight payment will require the party receiving the good or service to pay a certain sum immediately upon being presented with the bill of exchange.

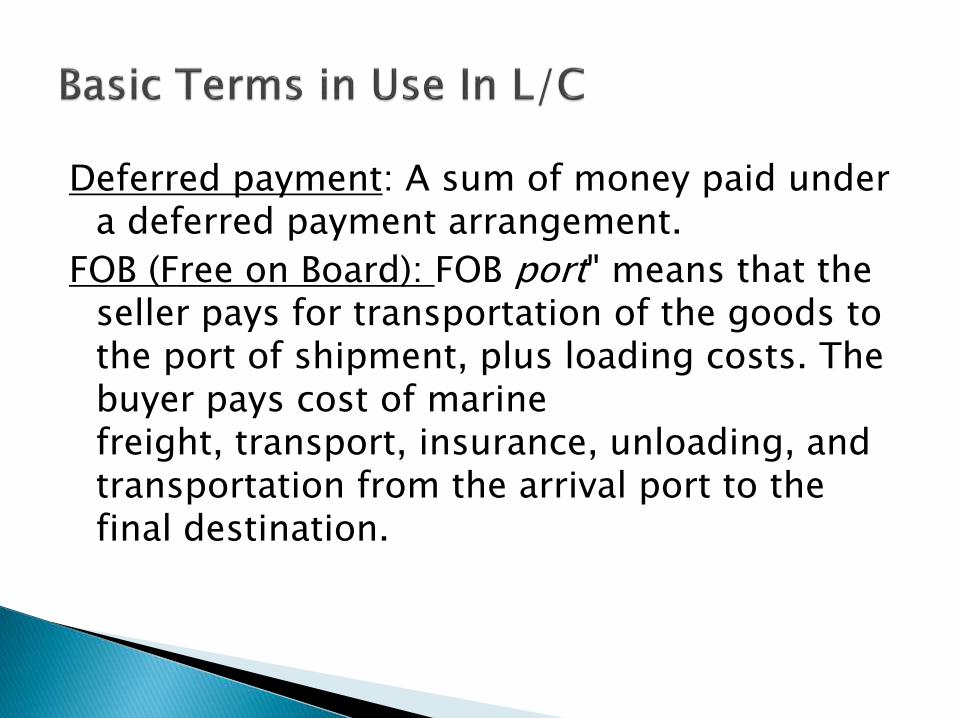

Deferred payment: A sum of money paid under a deferred payment arrangement.

FOB (Free on Board): FOB port" means that the seller pays for transportation of the goods to the port of shipment, plus loading costs. The buyer pays cost of marine freight, transport, insurance, unloading, and transportation from the arrival port to the final destination.

CFR (Cost and Freight): "Cost and Freight" means that the seller must pay the costs and freight necessary to bring the goods to the named port of destination but the risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time the goods have been delivered on board the vessel is transferred from the seller to the buyer when the goods pass the ship's rail in the port of shipment.

CPT-Carriage Paid to: Carriage paid to..." means that the seller pays the freight for the carriage of the goods to the named destination. The risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time the goods have been delivered to the carrier is transferred from the seller to the buyer when the goods have been delivered into the custody of the carrier.

Transshipment: Transshipment is the shipment of goods or containers to an intermediate destination, then to yet another destination. One possible reason for transshipment is to change the means of transport during the journey (e.g., from ship transport to road transport), known as translating.

1. Revocable (বাতিল য াগ্য) 2. Irrevocable

3. At Sight 4. Deferred/ Usance5. Unconfirmed

6. Confirmed7. Transferable 8. Assignment of Proceeds

9. Revolving10. Standby11. Back to Back

Revocable: The buyer and the bank that established the LC are able to manipulate the LC or make corrections without informing or getting permissions from the seller. According to UCP 600, all LCs are irrevocable, hence this type of LC is obsolete.

Irrevocable: Any changes (amendment) or cancellation of the LC (except it is expired) is done by the applicant through the issuing bank. It must be authenticated and approved by the beneficiary.

At Sight: A credit that the announcer bank immediately pays after inspecting the carriage documents from the seller.

Deferred/Usance: A credit that is not paid/assigned immediately after presentation, but after an indicated period that is accepted by both buyer and seller. Typically, seller allows buyer to pay the required money after taking the related goods and selling them.

Unconfirmed: This type does not acquire the other bank's confirmation.

Confirmed: An LC is said to be confirmed when a second bank adds its confirmation (or guarantee) to honor a complying presentation at the request or authorization of the issuing bank.

Transferable: A letter of credit can be transferred to the second beneficiary at the request of the first beneficiary only if it expressly states that the letter of credit is "transferable". A bank is not obligated to transfer a credit.

Assignment of Proceeds: Transferring all or part of the proceeds from a L/C to 3rd Beneficiary. To receive an assignment of proceeds, the beneficiary of L/C is require to submit in writing, a request to the bank to assign the funds to a different person or company.

Revolving: Single L/C that cover multiple-shipments over a Long period. Instead of arranging a new L/C for each separate shipment.

Stand by: Operates like a Commercial Letter of Credit, except that typically it is retained as a "standby" instead of being the intended payment mechanism.

Back to Back: A pair of LCs in which one is to the benefit of a seller who is not able to provide the corresponding goods for unspecified reasons. In that event, a second credit is opened for another seller to provide the desired goods. Back-to-back is issued to facilitate intermediary trade.

1. Financial documents: Bill of Exchange- an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the person to whom it is addressed to pay on demand, or at a fixed or determinable future time, a sum certain in money to or to the order of a specified person, or to bearer.

2. Commercial documents: Proforma Invoice (PI), Packing List

a) Proforma Invoice: a Proforma invoice is a document that states a commitment from the seller to provide specified goods to the buyer at specific prices.

2. Commercial documents: Proforma Invoice (PI), Packing List

a) Proforma Invoice: a Proforma invoice is a document that states a commitment from the seller to provide specified goods to the buyer at specific prices.

Content of PI:

The word invoice (or Tax Invoice)

A unique reference number (in case of correspondence about the invoice).

Date of the invoice

Credit terms Tax payments if relevant Name and contact details of the seller Tax or company registration details of seller

e.g. Business Identification Number (BIN) for Bangladesh businesses.]

Name and contact details of the buyer Date that the goods or service was sent or

delivered Purchase order number (or similar tracking

numbers requested by the buyer to be mentioned on the invoice)

Description of the product(s)

Unit price(s) of the product(s) (if relevant) Total amount charged (optionally with

breakdown of taxes, if relevant) Payment terms (including method of payment,

date of payment, and details about charges for late payment)

B) Packing List: It commonly includes an itemized detail of the package contents and does not include customer pricing. It serves to inform all parties, including transport agencies, government authorities, and customers, about the contents of the package. It helps them deal with the package accordingly.

3. Shipping documents: Transport document, insurance certificate, commercial, official or legal documents.

4. Official documents: License, embassy legalization, origin certificate, inspection certificate, sanitary certificate.

5. Transport document: Bill of Loading, airway bill, lorry/truck receipt, railway receipt, CMC other than mate receipt, forwarder cargo receipt.

6. Insurance documents: Insurance policy or certificate, but not a cover note.

One-time Requirement:

Membership certificate of any Chamber of Commerce & Industries or concerned association

No-Objection-Certificate (NOC) from existing bank mentioning no outstanding of overdue bill of entry and no objection to extend trade facilities against IRC No……

Annual/Periodic Requirement: TIN Certificate (Certificate of last assessment year) VAT Certificate (Most recent) Trade License (Renewed copy) Renewed IRC or BOI permissionFor Every Subsequent LC/LCA: LC Application Form (For LC only) (2 Page = 1 Set) LCA Form (For both LC & Contract) (6 copy= 1 set) IMP Form(Foreign Exchange Regulation Act/

Money Exchange Form)- 2 copies (1set) Proforma Invoice Insurance cover note Any other approval (if required by govt./import

policy/FX regulation)

① Negation with beneficiary (Seller) & Issuing Sales Contract & Proforma Invoice.

② Collect L/C Application from (1pcs), LCA from (6pcs set) & IMP from (2pcs) & Fill up according to sales contract & PI & Write Application for opening L/C to Bank.

③ According to PI, Issuing Insurance “cover note” from Insurance company.

④ Along with L/C Application, LCA, IMP & Insurance cover note submit to bank.

⑤ After submitting to bank Asking for Draft copy of L/C.

⑥ After getting draft copy checking carefully & send to checking to beneficiary.

⑦ After finishing checking, if okay then inform to bank for completing. If need amendment, then inform to bank amendment & completing.

⑧ Next beneficiary will send (Load) goods or service, after loading beneficiary will send B.L, C.I, Packing List & Other’s necessary documents directly to your bank or you.

⑨ If they send you directly, after checking, you represent to bank for endorsing along with Accepting of Payments.

⑩ After getting's or endorsing those documents from bank collect Insurance Policy from Insurance company.

⑪ All the documents give to your CNF Agents for clearing your goods & Services.

Sales

Contract(Applicant

& Beneficiary)

Exporter will Loading

goods, then He will send

CI, Packing List , PI, BL &

Others Documents to you

or to Bank

Collected form L/C

related from Bank(L/C

Application, LCA, IMP) &

Fill up these

Issuing Insurance

Cover note from

Insurance company

according to PI

Submit to Bank (fill up

from along with

Insurance Cover note)

Collect L/C draft copy

& Both Parties

Checking, If need

amend, Communicate

with Bank for Amend

Endorse it from Bank

by Accepting of

Payments & Issuing

Insurance Policy

Summit all the

documents to your

CNF Agents to

Release the goods

Through good relationship some one can Import with L/C- that procedure name Latter of Credit Authorization (LCA).

Here, no need to fill up L/C Application from. But need apply in Bangladesh Bank prescribe “KA” form. Therefore, you should have to knowledge about import policy whether which goods or Services can import through LCA.

Under LCA we can import Capital Machinery & Raw Materials but did not spares Parts.