malaysia in focus - pwc · living survey 2011 104th (out of 214 cities) eca international cost of...

TRANSCRIPT

Malaysia in focus

Malaysia’s success as an investment location continues to grow. We look forward to helping you maximise the benefits of a Malaysian investment.

www.pwc.com/my

This material was prepared by PricewaterhouseCoopers (PwC) and is not to be used, distributed or relied upon by any third party without

PwC’s prior written consent. The analysis and opinions contained in this document are based on publicly available sources. PwC has not

independently verified this information and makes no representation or warranty, express or implied, that such information is accurate and/or

complete.

Recipients of this material must make their own independent assessment of the material and neither PwC nor any of its affiliates, partners,

officers, employees, agents or advisers shall be liable for any direct, indirect or consequential loss and/or damage suffered by any person as a

result of relying on any statement in, or alleged omission from, this material.

PwC

Malaysia is a country on the move. From a nation dependent on agriculture and primary commodities, Malaysia has today become an export-driven economy spurred on by high technology, knowledge-based and capital-intensive industries. We’re proud of how far we’ve come as a multi-sector economy.

Since the 1970s, Malaysia has been the choice destination for many multinational companies due to its geographical location, political stability, reliable infrastructure and attractive incentives. By the 1990s, Malaysia achieved Newly-Industrialised Country (NIC) status, with 30% of exports consisting of manufactured goods.

As Malaysia embarks on its vision to becoming a high income nation by the year 2020, it has positioned the Economic Transformation Programme (ETP) as a key pillar to driving change. The Government is proactively encouraging private investment-led growth with the ETP creating many investment opportunities.

Capitalise on Malaysia’s transformation as this opens up unique investment opportunities, with enhanced financial incentives and business-friendly policies.

The time to invest in Malaysia is now.

Mohammad Faiz Azmi Executive Chairman

Welcome. Selamat Datang.

3

PwC

Contents

I. About Malaysia 6

II. The economy 9

III. Business and investment landscape 13

IV. Abbreviations and key contacts 27

5

PwC 6

I. About Malaysia

6

PwC

Malaysia 29 million

7

Facts and figures

Source: Economist Intelligence Unit (EIU) and Bloomberg

2012 Malaysia

Land area 330,252 sq km

GDP (US$ bln) 237.8

GDP per capita (US$) 8,420

GDP growth (%) 4.8 (est)

Inflation (%) 2.6

Market capitalisation (US$ bln) 411

Equity market return (%) 11.63

Equity market price earning ratio 16.4

Credit rating

- Standard & Poor’s

- Moody’s

A

A3

EIU country risk rating

- Sovereign risk

- Currency risk

- Banking sector risk

BBB

A

BBB

Unemployment rate (%) 3.3%

Note:

Exchange rate (as at 31 May 2012): US$ 1 = MYR 3.1750

A multi-ethnic and multi-cultural country, Malaysia is located at the heart of Southeast Asia.

Malaysia is a nation capitalising on its transformation with over US$400 bln worth of investment opportunities.

PwC

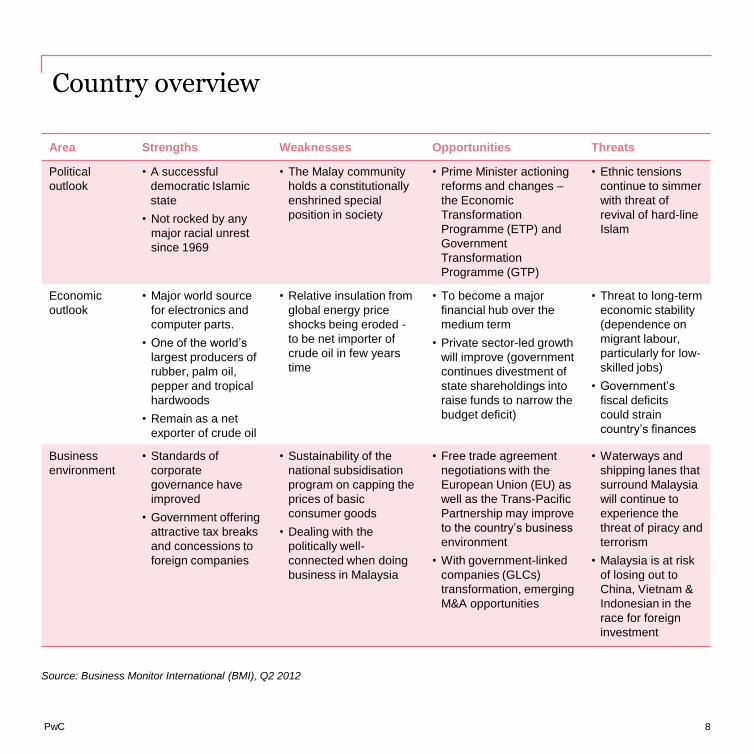

Area Strengths Weaknesses Opportunities Threats

Political

outlook

• A successful

democratic Islamic

state

• Not rocked by any

major racial unrest

since 1969

• The Malay community

holds a constitutionally

enshrined special

position in society

• Prime Minister actioning

reforms and changes –

the Economic

Transformation

Programme (ETP) and

Government

Transformation

Programme (GTP)

• Ethnic tensions

continue to simmer

with threat of

revival of hard-line

Islam

Economic

outlook

• Major world source

for electronics and

computer parts.

• One of the world’s

largest producers of

rubber, palm oil,

pepper and tropical

hardwoods

• Remain as a net

exporter of crude oil

• Relative insulation from

global energy price

shocks being eroded -

to be net importer of

crude oil in few years

time

• To become a major

financial hub over the

medium term

• Private sector-led growth

will improve (government

continues divestment of

state shareholdings into

raise funds to narrow the

budget deficit)

• Threat to long-term

economic stability

(dependence on

migrant labour,

particularly for low-

skilled jobs)

• Government’s

fiscal deficits

could strain

country’s finances

Business

environment

• Standards of

corporate

governance have

improved

• Government offering

attractive tax breaks

and concessions to

foreign companies

• Sustainability of the

national subsidisation

program on capping the

prices of basic

consumer goods

• Dealing with the

politically well-

connected when doing

business in Malaysia

• Free trade agreement

negotiations with the

European Union (EU) as

well as the Trans-Pacific

Partnership may improve

to the country’s business

environment

• With government-linked

companies (GLCs)

transformation, emerging

M&A opportunities

• Waterways and

shipping lanes that

surround Malaysia

will continue to

experience the

threat of piracy and

terrorism

• Malaysia is at risk

of losing out to

China, Vietnam &

Indonesian in the

race for foreign

investment

8

Country overview

Source: Business Monitor International (BMI), Q2 2012

PwC

II. The economy

9

PwC 10

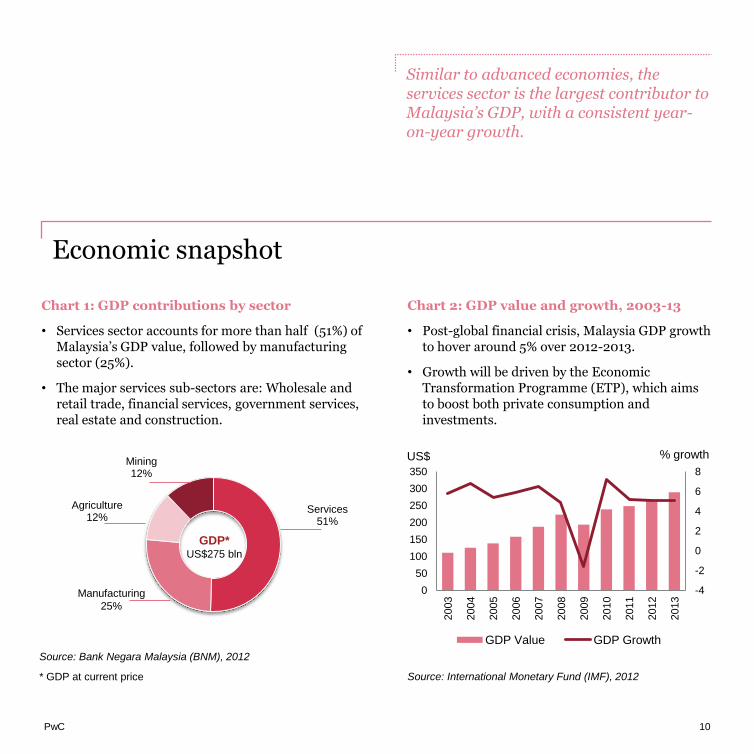

Economic snapshot

Chart 1: GDP contributions by sector

• Services sector accounts for more than half (51%) of Malaysia’s GDP value, followed by manufacturing sector (25%).

• The major services sub-sectors are: Wholesale and retail trade, financial services, government services, real estate and construction.

Chart 2: GDP value and growth, 2003-13

• Post-global financial crisis, Malaysia GDP growth to hover around 5% over 2012-2013.

• Growth will be driven by the Economic Transformation Programme (ETP), which aims to boost both private consumption and investments.

Source: International Monetary Fund (IMF), 2012

Services 51%

Agriculture 12%

Mining 12%

GDP* US$275 bln

-4

-2

0

2

4

6

8

0

50

100

150

200

250

300

350

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

GDP Value GDP Growth

US$ % growth

* GDP at current price

Similar to advanced economies, the services sector is the largest contributor to Malaysia’s GDP, with a consistent year-on-year growth.

Source: Bank Negara Malaysia (BNM), 2012

Manufacturing

25%

PwC 11

Trade overview

• Malaysia continues to show strong trade performance in 2011 despite the slow US economic recovery, Eurozone debt crisis uncertainties and supply chain disruptions from Japan’s tsunami and Thailand’s floods.

Source: BNM, 2012

50

100

150

200

250

300

350

400

450

2006 2007 2008 2009 2010 2011

Exports Imports Total trade

US$ bln

Chart 3: Malaysian trade, 2007 – 2011

"Malaysia is the third most open economy in Asia, after Hong Kong and Singapore”

International Chamber of Commerce (ICC) Open Market Index 2011

PwC

S'pore 13%

China 13%

Japan 11%

Other SEA 15%

Other NEA 11%

EU 10%

North America 10%

Oceania 3%

India 2%

Others 12%

Total

imports US$189 bln

12

• Malaysia is a leading exporter of electrical appliances, electronic parts and components, palm oil and natural gas.

• The major category of imports includes electronics and electrical goods, chemicals and chemical products, machinery, appliances and parts.

S'pore 13%

China 13%

Japan 11%

Other SEA 12%

Other NEA 12%

EU 10%

North America 9%

Oceania 4%

India 4%

Others 12%

Total

exports US$ 229 bln

Source: BNM, 2012

Trade overview

Chart 4: Malaysian exports & imports, 2011

Malaysia has a well established trade relationship within Asia - providing inroads to Southeast Asia economies and its market of over 600 million people.

Notes:

Other SEA: Other Southeast Asia countries

Other NEA: Other Northeast Asia countries

PwC 13

III. Business and investment landscape

13 13

14 PwC

Chart 5: Malaysia business rankings

• Malaysia has a conducive business environment. What makes it:

- Stable. A resilient macroeconomic environment and a sound financial sector.

- Market-oriented. An efficient goods market and large export earner.

- Well connected. World class infrastructure comprising excellent transport connectivity and advanced communications infrastructure.

- Cost effective. Affordable costs of living and doing business.

- Business friendly. Attractive governmental support through government policies and tax incentives.

Malaysia rankings

World Bank Country Income

Group 2012

Upper middle

income economy*

World Bank's Ease of Doing

Business Survey 2012 18th

World Economic Forum (WEF)

World Competitiveness

Ranking 2011-2012

21st

Institute for Management

Development (IMD) World

Competitiveness Ranking 2012

16th

WEF Global Enabling Trade

Ranking 2012 24th

A.T. Kearney FDI Confidence

Index 2012 10th

A.T. Kearney Global Services

Location Index 2011 3rd

MERCER Worldwide Cost of

Living Survey 2011

104th

(out of 214 cities)

ECA International Cost of

Living Survey 2011

33rd (out of

53 cities in Asia)

PwC World Bank Ease of

Paying Taxes 2012 28th

* Countries with GNI per capita of US$3,976 - US$12,275,

Malaysia’s GNI per capita in 2010 was US$7,760

Source: Various sources

Business and investment landscape

PwC 15

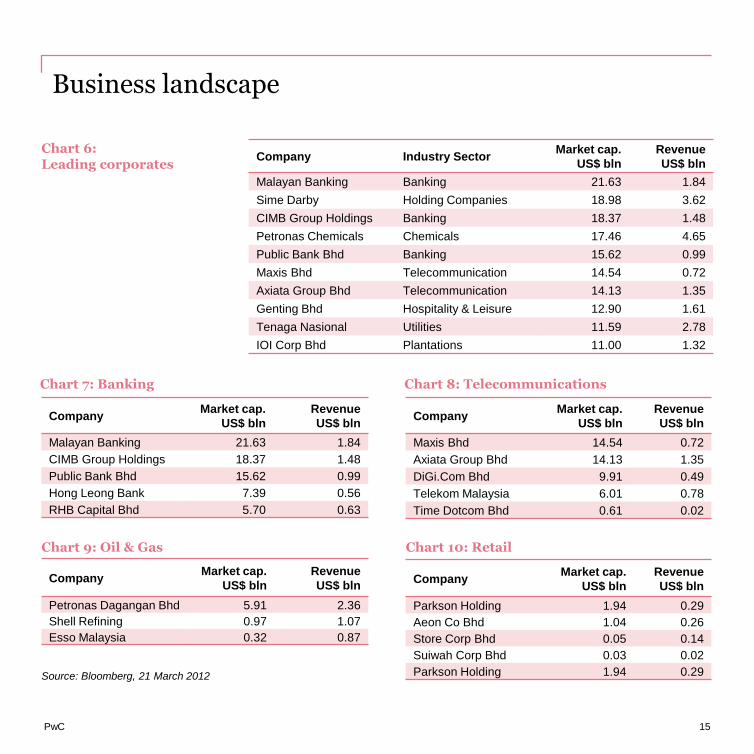

Business landscape

Source: Bloomberg, 21 March 2012

Company Industry Sector Market cap.

US$ bln

Revenue

US$ bln

Malayan Banking Banking 21.63 1.84

Sime Darby Holding Companies 18.98 3.62

CIMB Group Holdings Banking 18.37 1.48

Petronas Chemicals Chemicals 17.46 4.65

Public Bank Bhd Banking 15.62 0.99

Maxis Bhd Telecommunication 14.54 0.72

Axiata Group Bhd Telecommunication 14.13 1.35

Genting Bhd Hospitality & Leisure 12.90 1.61

Tenaga Nasional Utilities 11.59 2.78

IOI Corp Bhd Plantations 11.00 1.32

Company Market cap.

US$ bln

Revenue

US$ bln

Malayan Banking 21.63 1.84

CIMB Group Holdings 18.37 1.48

Public Bank Bhd 15.62 0.99

Hong Leong Bank 7.39 0.56

RHB Capital Bhd 5.70 0.63

Company Market cap.

US$ bln

Revenue

US$ bln

Maxis Bhd 14.54 0.72

Axiata Group Bhd 14.13 1.35

DiGi.Com Bhd 9.91 0.49

Telekom Malaysia 6.01 0.78

Time Dotcom Bhd 0.61 0.02

Company Market cap.

US$ bln

Revenue

US$ bln

Petronas Dagangan Bhd 5.91 2.36

Shell Refining 0.97 1.07

Esso Malaysia 0.32 0.87

Company Market cap.

US$ bln

Revenue

US$ bln

Parkson Holding 1.94 0.29

Aeon Co Bhd 1.04 0.26

Store Corp Bhd 0.05 0.14

Suiwah Corp Bhd 0.03 0.02

Parkson Holding 1.94 0.29

Chart 6: Leading corporates

Chart 9: Oil & Gas

Chart 10: Retail

Chart 7: Banking

Chart 8: Telecommunications

16 PwC

Investment overview

• UNCTAD’s World Investment Report 2011 projected that global FDI flows will continue to recover from pre-crisis level to US$1.4-US$1.6 trillion. FDI flows are expected to rise around 12% p.a. to US$1.9 trillion in 2013.

Source: UNCTAD, 2012

983

1,462

1,971

1,744

1,185 1,290

1,509

1,700

1,900

200

700

1,200

1,700

2,200

2005 2006 2007 2008 2009 2010 2011* 2012* 2013*

US$ bln

Chart 11: Global foreign direct investment (FDI) inflows, 2005 – 2013

Malaysia is fast gaining foreign investors interest and is expected to be a beneficiary of global FDI inflow.

17 PwC

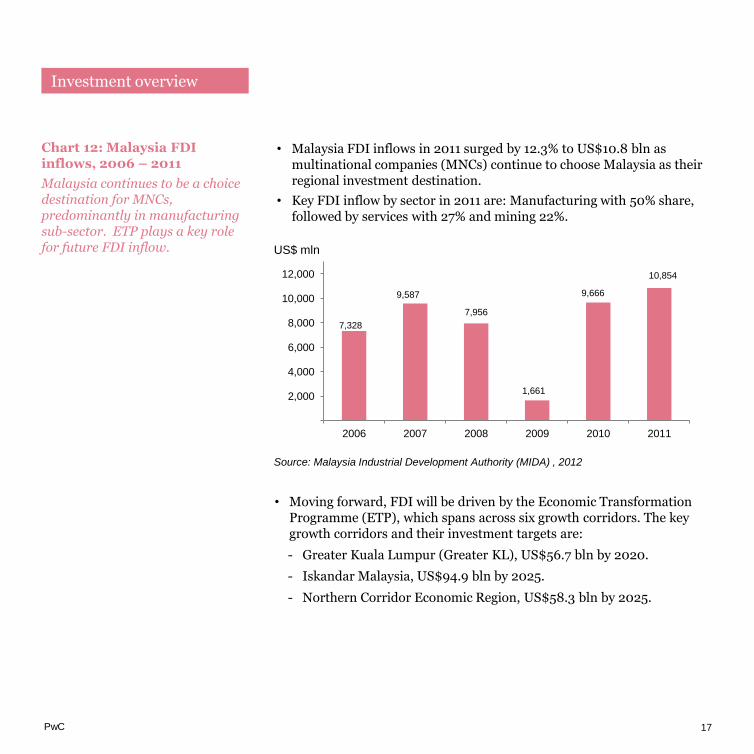

• Malaysia FDI inflows in 2011 surged by 12.3% to US$10.8 bln as multinational companies (MNCs) continue to choose Malaysia as their regional investment destination.

• Key FDI inflow by sector in 2011 are: Manufacturing with 50% share, followed by services with 27% and mining 22%.

• Moving forward, FDI will be driven by the Economic Transformation Programme (ETP), which spans across six growth corridors. The key growth corridors and their investment targets are:

- Greater Kuala Lumpur (Greater KL), US$56.7 bln by 2020.

- Iskandar Malaysia, US$94.9 bln by 2025.

- Northern Corridor Economic Region, US$58.3 bln by 2025.

Source: Malaysia Industrial Development Authority (MIDA) , 2012

7,328

9,587

7,956

1,661

9,666

10,854

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010 2011

US$ mln

Investment overview

Chart 12: Malaysia FDI inflows, 2006 – 2011

Malaysia continues to be a choice destination for MNCs, predominantly in manufacturing sub-sector. ETP plays a key role for future FDI inflow.

18 PwC

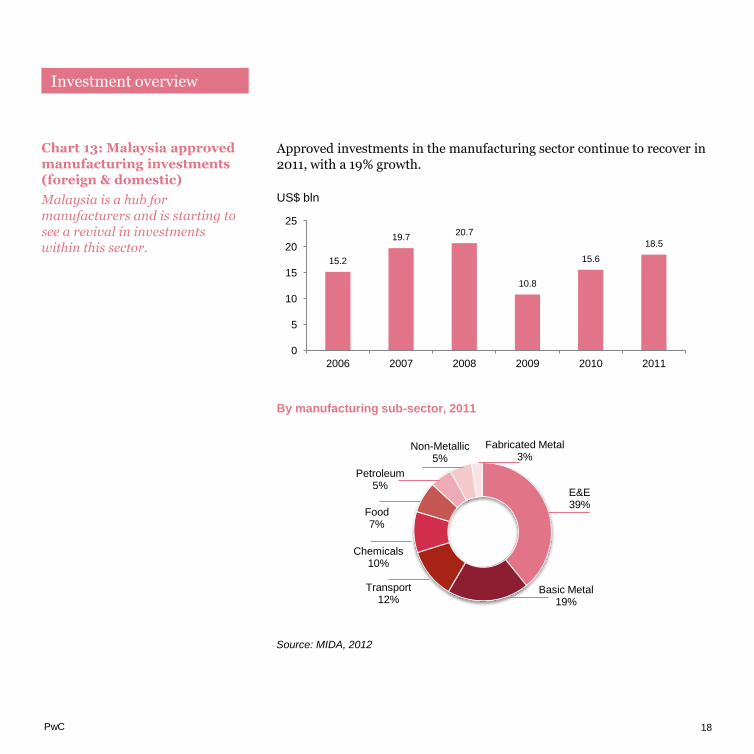

Approved investments in the manufacturing sector continue to recover in 2011, with a 19% growth.

Source: MIDA, 2012

US$ bln

15.2

19.7 20.7

10.8

15.6

18.5

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011

E&E 39%

Basic Metal 19%

Transport 12%

Chemicals 10%

Food 7%

Petroleum 5%

Non-Metallic 5%

Fabricated Metal 3%

Investment overview

By manufacturing sub-sector, 2011

Chart 13: Malaysia approved manufacturing investments (foreign & domestic)

Malaysia is a hub for manufacturers and is starting to see a revival in investments within this sector.

19 PwC

Turnaround in approved investments in the services sector, recovering to pre-crisis levels.

US$ bln

By services sub-sector, 2011

Source: MIDA, 2012

18.3

21.9

16.5

12.8 12.1

21.2

0

5

10

15

20

25

2006 2007 2008 2009 2010 2011

Real Estate 26%

Transport 18%

Global Operations Hub

15%

Energy 10%

Education 2%

Others 15%

Investment overview

Chart 14: Malaysia approved services investments (foreign & domestic)

Real estate makes up the largest services sub-sector for approved foreign and domestic investments.

Telecommunications

9%

Financial services

5%

20 PwC

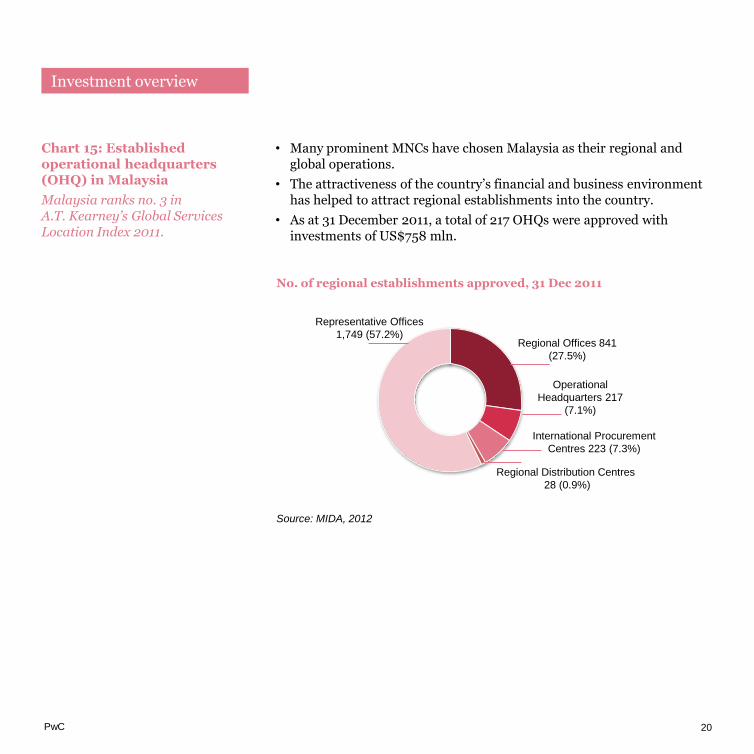

• Many prominent MNCs have chosen Malaysia as their regional and global operations.

• The attractiveness of the country’s financial and business environment has helped to attract regional establishments into the country.

• As at 31 December 2011, a total of 217 OHQs were approved with investments of US$758 mln.

Source: MIDA, 2012

No. of regional establishments approved, 31 Dec 2011

Regional Offices 841

(27.5%)

Representative Offices

1,749 (57.2%)

Regional Distribution Centres

28 (0.9%)

International Procurement

Centres 223 (7.3%)

Operational

Headquarters 217

(7.1%)

Investment overview

Chart 15: Established operational headquarters (OHQ) in Malaysia

Malaysia ranks no. 3 in A.T. Kearney’s Global Services Location Index 2011.

21 PwC

A cross section of established OHQs in Malaysia by leading MNCs

Source: MIDA, 2012

Country Name of Company

USA • General Electric

• Du Pont

• Dow Chemicals

• PepsiCo

• Grey Communications

• Hess Oil & Gas

• Air Products

• Henry Schein

• Schlumberger

• Baker Hughes

• Intel

• Transocean

• Agilent

• IBM

• Mars Foods

• Hewlett-Packard

• E-Storm

• Harman

• Kellogg’s

UK • RMC Industries

• British-American Tobacco

• Diagonal Consulting Group

• Avocet Mining

• OHM Surveys

• Fitness First

• G4S Management

• Velosi

Germany • BASF

• Meuhlbauer

• Eppendorf

• Arvato

• Siemens

• Nordenia

• Bayer

• Binder

• A.Hartodt

Switzerland • Novartis Corporation

• SBM Group

• Omya Group

• Tetra Pak

France • Lafarge

• Thales International

• Monier

Netherlands • Flexsys

• Prometric

• Friesland Foods

• Dow Corning

• Barry Callebaut

• Organon

• Mammoet

• Subsea

• Core

• Acision

Sweden • Volvo

• Ascom

• UCB Group

Norway • Aker Kvaerner

• Wilhelmsen

• AGR

Investment overview

PwC 22

Transforming Malaysia

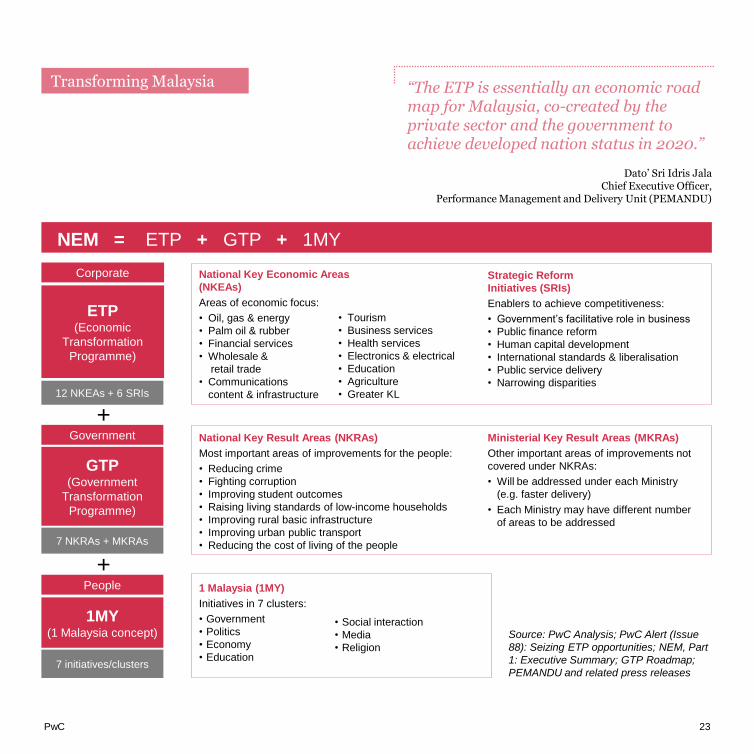

The New Economic Model is a framework which aims to turn Malaysia into a high income nation that is competitive, sustainable and inclusive.

Overview of Malaysia’s New Economic Model (NEM)

PwC

ETP (Economic

Transformation

Programme)

GTP (Government

Transformation

Programme)

1MY (1 Malaysia concept)

Corporate

Government

People

12 NKEAs + 6 SRIs

7 NKRAs + MKRAs

7 initiatives/clusters

National Key Economic Areas

(NKEAs)

Areas of economic focus:

• Oil, gas & energy

• Palm oil & rubber

• Financial services

• Wholesale &

retail trade

• Communications

content & infrastructure

• Tourism

• Business services

• Health services

• Electronics & electrical

• Education

• Agriculture

• Greater KL

Strategic Reform

Initiatives (SRIs)

Enablers to achieve competitiveness:

• Government’s facilitative role in business

• Public finance reform

• Human capital development

• International standards & liberalisation

• Public service delivery

• Narrowing disparities

National Key Result Areas (NKRAs)

Most important areas of improvements for the people:

• Reducing crime

• Fighting corruption

• Improving student outcomes

• Raising living standards of low-income households

• Improving rural basic infrastructure

• Improving urban public transport

• Reducing the cost of living of the people

Ministerial Key Result Areas (MKRAs)

Other important areas of improvements not

covered under NKRAs:

• Will be addressed under each Ministry

(e.g. faster delivery)

• Each Ministry may have different number

of areas to be addressed

+

+ 1 Malaysia (1MY)

Initiatives in 7 clusters:

• Government

• Politics

• Economy

• Education

NEM = ETP + GTP + 1MY

23

• Social interaction

• Media

• Religion

Source: PwC Analysis; PwC Alert (Issue

88): Seizing ETP opportunities; NEM, Part

1: Executive Summary; GTP Roadmap;

PEMANDU and related press releases

Transforming Malaysia “The ETP is essentially an economic road map for Malaysia, co-created by the private sector and the government to achieve developed nation status in 2020.”

Dato’ Sri Idris Jala Chief Executive Officer,

Performance Management and Delivery Unit (PEMANDU)

PwC

Participating in Malaysia’s transformation

Being part of the growth equation

The ETP (Economic Transformation Programme) will play a pivotal role in transforming Malaysia into a high-income nation by 2020. One of the ETP’s top priorities is to facilitate global companies’ efforts to make Malaysia their base. Here are 4 steps for global investors to harness project synergies and generate value from strategic projects.

Strategic

& detailed

investment case

Robust

investment

analysis

Your high level pitch should include clear:

• analysis of how the project addresses issues & opportunities

identified by the ETP labs

• estimate/range of potential GNI & employment impacts

• articulation of support you may need from the Government

Four steps to becoming an ETP project If there are positive signals on the strategic investment case for your

pitch, the Government will ask for a detailed analysis and business

case be prepared

• Provide a detailed analysis which gives a robust estimate on the project’s impact on GNI,

employment & investment

• Appropriate PEMANDU (Performance Management & Delivery Unit) NKEA (National Key Economic

Area) sector director and team can be engaged to help facilitate the project

• These include meetings with various Government ministers and ministry officials

• These project meetings are important to secure the necessary support and to facilitate fast and

successful implementation of the project

• Any issues that cannot be easily solved can be escalated through problem solving meetings

chaired by PEMANDU

Government includes relevant line ministries, PEMANDU, Economic Planning Unit,

MIDA (Malaysian Industrial Development Authority) and Ministry of Finance

Execute &

follow-up

2

3

4

Engage

Government

early 1

Economic growth opportunities

24

Source: PEMANDU, PwC Analysis; PwC Alert

(Issue 88: Seizing ETP Opportunities)

PwC 25

Examples of growth opportunities across 12 National Key Economic Areas

Participating in Malaysia’s transformation

Oil, Gas and Energy

• Oil fields: Intensify exploration,

enhance oil recovery, rejuvenate

mature oil fields and explore marginal

oil fields

• Oil-field service and equipment

operations

• Energy: Nuclear and renewable

(hydroelectricity and solar)

Financial Services

• Develop regional banking champions

• Global hub for Islamic finance

• Revitalise the capital market

• Create integrated payment eco-system

• Develop asset management industry

Palm Oil

• Oleochemical derivative products

• Food and health-based downstream

segments

• Improve fresh fruit bunch yield

• Accelerate replanting of palm oil

• Develop 2nd generation bio-fuel

Wholesale and Retail

• Develop Malaysian concept shopping

centres overseas

• Large format stores*

• Community markets

• Make Malaysia duty-free

• Modernise small retailers

Healthcare

• Export of generic drugs

• Health metropolis

• Health travel

• Develop medical hub

Education

• Early childcare and education

centres

• International schools

• Private teacher training

• Private skills-training

• Build discipline cluster in health

science, engineering, science,

innovation, business, finance and

hospitality

Agriculture

• Agriculture biotechnology

• Production of swiftlet nests

• Scale up paddy production

• Aquaculture

• Premium fruits and vegetable

Greater KL/Klang Valley

• Integrated urban Mass Rapid Transit

• High-speed KL-Singapore rail

• Attract 100 of the world’s dynamic

firms in priority sectors

• Revitalise the Klang River into a

heritage and commercial district

* Stores of 3,000 to 5,000 sq m or larger e.g. hyperstore and superstore

Tourism

• Improve rates, mix and quality of

hotels

• Increase medium-haul flights/tourists

• Promote biodiversity and develop

ecotourism and eco-nature resort

• Create a Straits Riviera cruise

destination

Business Services

• Aviation maintenance, repair and

overhaul services

• Global business outsourcers and

shared service centre

• Data centre hub

• Green technology industry

• Engineering services

Electronics and Electrical

• Light emitting diode, develop Solid

State Light hub

• Semiconductor: fabrication,

assembly, testing, packaging and

circuit design

• Solar wafer, cell and silicon

production and design

Communications Content and

Infrastructure

• Expand broadband coverage

• Extend regional telecommunication

network

• Content development: creative

content, e-commerce, e-healthcare,

e-learning and e-government

Source: PwC Analysis; PwC Alert (Issue 88):

Seizing ETP opportunities

PwC

Chart 16: Malaysia’s six growth corridors - targeted investment sectors Malaysia’s growth corridors contribute an estimated 62% of total investment approved at US$11.4 bln in 2011

26

Source: PwC analysis, 2012

Sabah Development

Corridor (SDC)

• Tourism

• Logistics

• Agriculture

• Manufacturing

Greater KL

• Wholesale & retail hub

• Transportation hub

• Financial services

• Education

• Healthcare (incl telehealth)

• Shared services and

outsourcing

• Tourism

Northern Corridor

Economic Region

(NCER)

• Agriculture

• Manufacturing -

E&E, oil & gas,

biotechnology

• Tourism

• Logistics

East Coast Economic

Region (ECER)

• Hospitality & leisure

• Oil, gas and

petrochemical

• Manufacturing

• Agriculture

• Education

Iskandar Malaysia (IM)

• E&E

• Petrochemicals &

oleochemicals

• Food & agro processing

• Logistics & related services

• Tourism

• Healthcare

• Education

• Financial services

• Creative industries

Sarawak Corridor of Renewable

Energy (SCORE)

• Manufacturing

- oil-based, glass, timber

• Mining

- aluminium, steel

• Agriculture

- palm oil, livestock,

aquaculture

• Services

- tourism, marine engineering

Investment target:

US$58.3 bln by 2025

Investment target:

US$94.9 bln by 2025

Investment target:

US$ 36.9 bln by 2020 Investment target:

US$25.5 bln by 2020

Investment target:

US$65.9 bln by 2020

Investment target:

US$56.7 bln by 2020

( GNI contribution

US$ 214.3 bln)

ECER

NCER

IM

Greater

KL

SCORE

SDC

Participating in Malaysia’s transformation

PwC 27

IV. Abbreviations and key contacts

27 27

PwC 28

Abbreviations

Abbreviation Full term

1MY 1 Malaysia

BMI Business Monitor International

BNM Bank Negara Malaysia

(Central Bank of Malaysia)

ECER East Coast Economic Region

EIU Economist Intelligence Unit

ETP Economic Transformation Programme

EU European Union

E&E Electronics and electrical

FDI Foreign direct investment

GDP Gross domestic product

GLC Government-linked companies

GNI Gross national income

GTP Government Transformation

Programme

ICC International Chamber of Commerce

IM Iskandar Malaysia

IMD Institute for Management Development

IMF International Monetary Fund

KL Kuala Lumpur

Abbreviation Full term

MIDA Malaysian Investment Development

Authority

MKRA Ministerial Key Result Area

MNC Multinational companies

NCER Northern Corridor

Economic Region

NEA Northeast Asia

NEM New Economic Model

NKEA National Key Economic Area

NKRA National Key Result Area

OHQ Operational headquarters

PE Price earning ratio

PEMANDU Performance Management &

Delivery Unit

SCORE Sarawak Corridor of Renewable

Energy

SDC Sabah Development

Corridor

SEA Southeast Asia

SRI Strategic Reform

Initiatives

UNCTAD United Nations Conference on

Trade and Development

WEF World Economic Forum

PwC

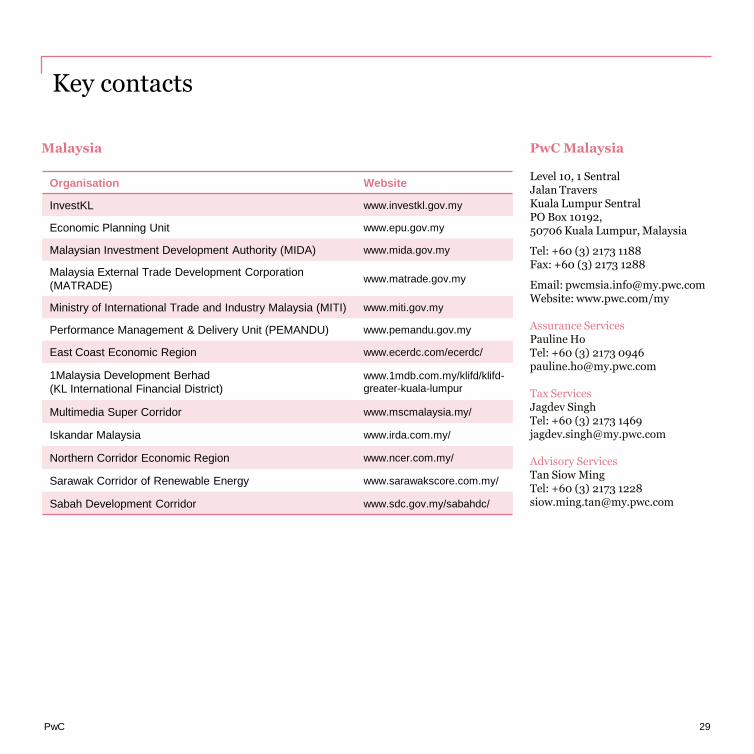

Key contacts

PwC Malaysia Level 10, 1 Sentral Jalan Travers Kuala Lumpur Sentral PO Box 10192, 50706 Kuala Lumpur, Malaysia

Tel: +60 (3) 2173 1188 Fax: +60 (3) 2173 1288

Email: [email protected] Website: www.pwc.com/my Assurance Services Pauline Ho Tel: +60 (3) 2173 0946 [email protected] Tax Services Jagdev Singh Tel: +60 (3) 2173 1469 [email protected] Advisory Services Tan Siow Ming Tel: +60 (3) 2173 1228 [email protected]

29

Organisation Website

InvestKL www.investkl.gov.my

Economic Planning Unit www.epu.gov.my

Malaysian Investment Development Authority (MIDA) www.mida.gov.my

Malaysia External Trade Development Corporation

(MATRADE) www.matrade.gov.my

Ministry of International Trade and Industry Malaysia (MITI) www.miti.gov.my

Performance Management & Delivery Unit (PEMANDU) www.pemandu.gov.my

East Coast Economic Region www.ecerdc.com/ecerdc/

1Malaysia Development Berhad

(KL International Financial District)

www.1mdb.com.my/klifd/klifd-

greater-kuala-lumpur

Multimedia Super Corridor www.mscmalaysia.my/

Iskandar Malaysia www.irda.com.my/

Northern Corridor Economic Region www.ncer.com.my/

Sarawak Corridor of Renewable Energy www.sarawakscore.com.my/

Sabah Development Corridor www.sdc.gov.my/sabahdc/

Malaysia

PwC

Notes

PwC

Notes

pwc.com/my

PwC firms provide industry focused assurance, tax and advisory services to enhance value for their clients. More than 169,000 people

in 158 countries in firms across the PwC network share their thinking, experience and solutions to develop fresh perspective and

practical advice. See pwc.com/my for more information.

© 2012 PricewaterhouseCoopers. All rights reserved. "PricewaterhouseCoopers" and/or "PwC" refers to the individual members of the

PricewaterhouseCoopers organisation in Malaysia each of which is a separate and independent legal entity. Please see

www.pwc.com/structure for further details. CS04971

PwC Malaysia on AppStore

twitter.com/PwC_Malaysia

facebook.com/pwcmsia

youtube.com/pwcmalaysia www.pwc.com/my