m&a and investment banking

TRANSCRIPT

M&A and Investment Banking

Lecture 5.1 – Valuation Techniques

1

Valuation Techniques

Relative Valuation

Comps

Compaq

Intrinsic Valuation

DDM

FCFE

FCFF

2

Relative Valuation In relative valuation, the value of an asset is compared to the values assessed by the market for

similar or comparable assets.

Relative valuation process:

1. Identify comparable assets and obtain market values for these assets.

2. Convert these market values into standardized values, since the absolute prices cannot be compared.

This process of standardizing creates price multiples.

3. Compare the standardized value or multiple for the asset being analyzed to the standardized values for

comparable asset, controlling for any differences between the firms that might affect the multiple, to

judge whether the asset is under or over valued

3

Advantages and Disadvantages of Valuation Multiples

Advantages Disadvantages

▲ Useful – multiples can be robust tools that provide useful

information about relative value

▲ Simple – ease of calculation and wide availability of data make

multiples an appealing method for assessing value

▲ Relevant – Multiples are based on key statistics that investors use

▼ Simplistic – combine many value drivers into a point estimate.

Difficult to disaggregate the effect of different value drivers

▼ Static – Multiples measure value at a single point in time and do not

fully capture the dynamic nature of business and competition

▼ Difficult to compare – Multiples differ for many reasons, not all

relating to true differences in value. This can result in misleading

‘apples-to-oranges’ comparisons among multiples

Multiples are Standardized Estimates of Price

4 Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Market Value of Equity

Market Value for the Firm

Firm Value = Market

Value of Equity + Market

Value of Debt

Market Value of Operating

Assets of Firm

Enterprise Value (EV) =

Market Value of Equity +

Market Value of Debt -

Cash

Revenues

Accounting revenues

Drivers

No. of Customers

No. of Subscribers

No. of Units

Earnings

To Equity investors

Net income

Earnings per share

To Firm

Operating income

(EBIT)

Cash Flow

To Equity

Net Income +

Depreciation

Free CF to Equity

To Firm

EBIT + DA

(EBITDA)

Free CF to Firm

Book Value

Equity

= BV of Equity

Firm

= BV of Debt + BV

of Equity

Invested Capital

= BV of Equity +

BV of Debt – Cash

Multiple =

Numerator = What You are Paying for the Asset

Denominator = What You are Getting in Return

Comparable Companies Analysis (Comps) Steps

5

Select the Universe of Comparable Companies

Locate the Necessary Financial Information

Spread Key Statistics, Ratios, and Trading Multiples

Benchmark the Comparable Companies

Determine Valuation

1

2

3

4

5

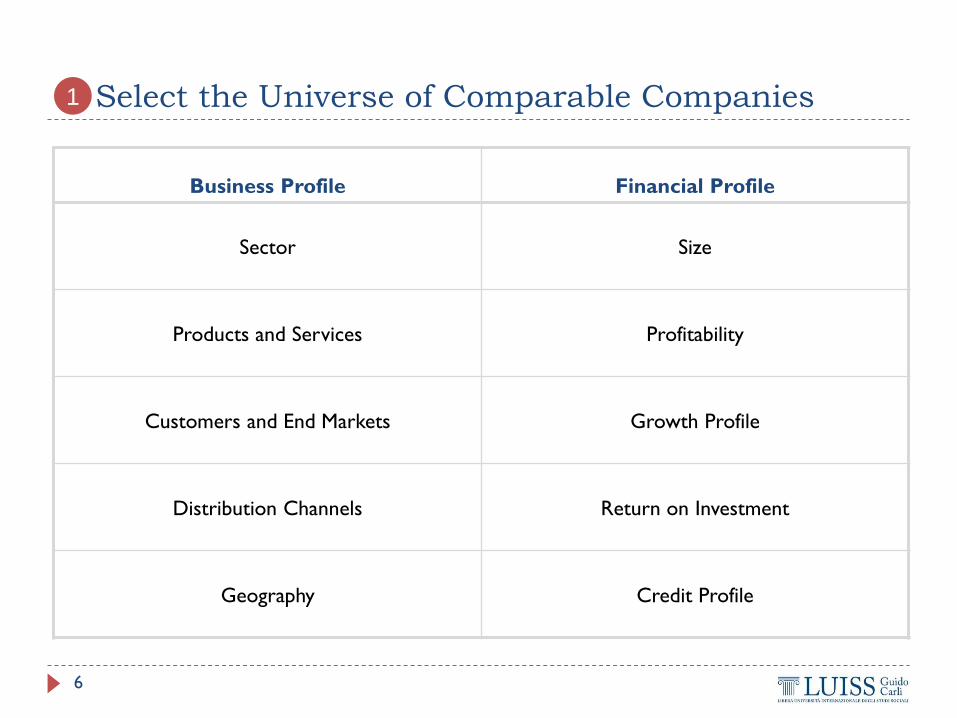

Select the Universe of Comparable Companies

6

Business Profile Financial Profile

Sector Size

Products and Services Profitability

Customers and End Markets Growth Profile

Distribution Channels Return on Investment

Geography Credit Profile

1

Locate the Necessary Financial Information

7

2

Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Notes: (1) As a non-GAAP (generally accepted accounting principles) financial measure, EBITDA is not reported on a public filer’s income statement. It

may, however, be disclosed as supplemental information in the company’s public filings.

Information Item Source

Income Statement Data

Sales

Gross Profit

EBITDA(1)

EBIT

Net Income/EPS

Most recent 10-K, 10-Q, 8-K, Press Release

Research Estimates First Call or IBES, individual equity research reports

Balance Sheet Data

Cash Balance

Debt Balances

Shareholders’ Equity

Most recent 10-K, 10-Q, 8-K, Press Release

Cash Flow Statement Data

Depreciation and Amortisation

Capital Expenditures

Most recent 10-K, 10-Q, 8-K, Press Release

Share Data

Basic Shares Outstanding 10-K, 10-Q, or Proxy Statement, whichever is most recent

Options and Warrants Data 10-K or 10-Q, whichever is more recent

Market Data

Share Price Data Financial information service

Credit Ratings Rating agencies’ websites, Bloomberg

Spread Key Statistics, Ratios, and Trading Multiples

8

3

Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Key Trading Multiples

Multiple= a measure of market valuation in the numerator (e.g., enterprise value, equity

value) / a universal measure of financial performance in the denominator (e.g., EBITDA, net

income)

Enterprise Value Multiples: The denominator employs a financial statistic that flows to

both debt and equity holders (e.g.: sales, EBITDA, and EBIT)

Equity Value (or Share Price) Multiples: The denominator must be a financial statistic

that flows only to equity holders, such as net income (or diluted EPS)

Enterprise Value vs. Equity Multiples

9

Enterprise Value Multiples Equity Multiples

Allow the user to focus on statistics where accounting policy

differences can be minimised (EBITDA, OpFCF)

Avoid the influence of capital structure on equity value

multiples

More comprehensive (apply to the entire enterprise)

Wider range of multiples possible

Easier to apply to cash flow

Enables the user to exclude non-core assets

More relevant to equity valuation

More reliable (estimating enterprise value involves more

subjectivity, especially in the valuation of non-core assets)

More familiar to investors

Equity Value Multiples

10

Multiple Definition Advantages Disadvantages

P/E ratio

Share price / Earnings per share (EPS) EPS

is net income/weighted average no of

shares in issue

EPS may be adjusted to eliminate

exceptional items (core EPS) and/or

outstanding dilutive elements (fully diluted

EPS)

Most commonly used equity multiple

Data availability is high

EPS can be subject to differences in

accounting policies and manipulation

Unless adjusted, can be subject to one-off

exceptional items

Cannot be used if earnings are negative

Price / cash

earnings

Share price / earnings per share plus

depreciation amortization and changes in

non-cash provisions.

Cash earnings are a rough measure of

cash flow

Unaffected by differences in accounting

for depreciation

Incomplete treatment of cash flow

Usually used as a supplement to other

measures if accounting differences are

material

Price / book

ratio Share price / book value per share.

Can be useful where assets are a core

driver of earnings such as capital-

intensive industries

Most widely used in valuing financial

companies, such as banks, which rely on

a large asset base to generate profits

Book values for tangible assets are stated

at historical cost, which is not a reliable

indicator of economic value

Book value for tangible assets can be

significantly impacted by differences in

accounting policies

PEG ratio Prospective PE ratio / prospective average

earnings growth.

Most suitable when valuing high growth

companies

Requires credible forecasts of growth

Can understate the higher risk associated

with many high-growth stocks

Dividend

yield Dividend per share / share price.

Useful for comparing cash returns with

types of investments

Can be used to establish a floor price for

a stock

Dependent on distribution policy of the

company

Yield to investor is subject to differences

in taxation between jurisdictions

Assumes the dividend is sustainable

Price / Sales Share price / sales per share.

Easy to calculate

Can be applied to loss making firms

Less susceptible to accounting differences

than other measures

Mismatch between nominator and

denominator in formula (EV/Sales is a

more appropriate measure)

Not used except in very broad, quick

approximations

Enterprise Value Multiples

11

Multiple Definition Advantages Disadvantages

EV/Sales Enterprise value / net sales

Least susceptible to accounting differences

Remains applicable even when earnings are negative

or highly cyclical

A crude measure as sales are rarely a direct value

driver

EV/EBITDAR Enterprise value / Earnings before Interest, Tax,

Depreciation & Amortization and Rental Costs

Proxy for operating free cash flows

Attempts to normalize capital intensity between

companies that choose to rent rather than own their

core assets

Most often used in the transport, hotel and retail

industries

Rental costs may not be reported and need to be

estimated

Ignores variations in capital expenditure and

depreciation

Ignores value creation through tax management

EV/EBITDA

Enterprise value / Earnings before Interest, Tax,

Depreciation & Amortization. Also excludes

movements in non-cash provisions and exceptional

items

EBITDA is a proxy for free cash flows

Probably the most popular of the EV based multiples

Unaffected by depreciation policy

Ignores variations in capital expenditure and

depreciation

Ignores potential value creation through tax

management

EV/EBIT and

EV/EBITA

Enterprise value / Earnings before interest and

taxes (and Amortisation)

Better allows for differences in capital intensiveness

compared to EBITDA by incorporating maintenance

capital expenditure

Susceptible to differences in depreciation policy

Ignores potential value creation through tax

management

EV/NOPLAT Enterprise value / Net Operating Profit After Adjusted

Tax

NOPLAT incorporates a number of adjustments to

better reflect operating profitability

NOPLAT adjustments can be complicated and are not

applied consistently by different analysts

EV/opFCF

Enterprise value / Operating Free Cash FlowOpFCF is

core EBITDA less estimated normative capital

expenditure requirement and estimated normative

variation in working capital requirement

Better allows for differences in capital intensiveness

compared to EBITDA

Less susceptible to accounting differences than EBIT

Use of estimates allows for smoothing of irregular real

capital expenditures

Introduces additional subjectivity in estimates of

capital expenditure

EV/ Enterprise

FCF

Enterprise value / Free cash flowEnterprise FCF is core

EBITDA less actual capital expenditure requirement and

actual increase in working capital requirement

Less subjective than opFCF

Better allows for differences in capital intensiveness

compared to EBITDA

Less susceptible to accounting differences than EBIT

Can be volatile and difficult to interpret as capital

expenditure is often irregular and “lumpy”

EV/Invested

Capital Enterprise value / Invested capital

Can be useful where assets are a core driver of

earnings, such as for capital-intensive industries

Book values for tangible assets are stated at historical

cost, which is not a reliable indicator of economic

value

Book value for tangible assets can be significantly

impacted by differences in accounting policies

EV/Capacity

Measure

Depends on industry (e.g. EV/subscribers,

EV/production capacity, EV/audience)

Not susceptible to accounting differences

Remains applicable even when earnings are negative

or highly cyclical

A crude measure as capacity measures are rarely a

direct value driver

Choosing the Pricing Date

12

Alternative Pricing Bases for Multiples

Multiple Comparisons and Lifecycles

Source: UBS Global Equity Research, 2001. Valuation Multiples: A Primer

Pricing Basis Calculation Profit or Cash Flow Used Use in Valuation

Historical Average price or enterprise value for

a period

Historical profit for the same period Established a historical

trading range

Current Current price or enterprise value Any historical or forecast profit Investigation of current value – best to

use current year forecast profit

Forward Forward price or enterprise value Forecast profit for a period related to

the forward price date

Investigation of current value – superior

to current-priced multiple for forecasts

beyond one year

Partial-

forward

Current market cap plus forecast net debt

(applies to enterprise value only)

Forecast profit for a period related to

the forward price date

Investigation of current value but the

partial-forward price is inconsistent and

difficult to interpret

Growth rate

Now Time Forward

Multiples likely to be most

comparable where

companies are at similar

points in their lifecycles

Conventional Usage of the Main Trading Multiples

13

Sector Multiple Used Rationale

Cyclical Manufacturing PE, Relative PE Often with normalized earnings

Growth Firms PEG ratio Big differences in growth rates

Young Growth Firms with

Losses

Revenue Multiples What choice do you have?

Infrastructure EV/EBITDA Early losses, big DA

REIT P/CFE (where CFE = Net

income + Depreciation)

Big depreciation charges

on real estate

Financial Services Price/ Book equity Marked to market?

Retailing Revenue Multiples Margins equalize sooner

or later

Sector-Specific Valuation Multiples

14

Valuation Multiple Sector

Enterprise Value

Access Lines/Fiber Miles/Route Miles Telecommunications

Broadcast Cash Flow (“BCF”) Media

Telecommunications

Earnings Before Interest Taxes, Depreciation, Amortisation, and

Rent Expense (“EBITDAR”)

Casinos

Restaurants

Retail

Earnings Before Interest Taxes, Depreciation, Depletion, Amortisation, and Exploration Expense

(“EBITDAX”)

Natural Resources

Oil and Gas

Population (“POP”) Telecommunications

Production/Capacity (in Units) Metals and Mining

Natural Resources

Oil and Gas

Paper and Forest Products

Reserves Metals and Mining

Natural Resources

Oil and Gas

Subscriber Media

Telecommunications

Square Footage Real Estate

Retail

Valuation Multiple Sector

Equity Value (Price)

Book Value (per Share) Financial Institutions

Homebuilders

Cash Available for Distribution (per Share) Real Estate

Discretionary Cash Flow (per Share) Natural Resources

Funds from Operations (“FFO”) (per Share) Real Estate

Net Asset Value (NAV) (per Share) Financial Institutions

Real Estate

Benchmark the Comparable Companies

15

Benchmarking centers on analyzing and comparing each of the comparable

companies with one another and the target. The ultimate objective is to determine

the target’s relative ranking so as to frame valuation accordingly.

It is a two-stage process:

1. Benchmark the Financial Statistics and Ratios (measures of size, profitability, growth,

returns and credit strength)

Goal: identifying the closest or “best” comparables and noting potential outliers

2. Benchmark the Trading Multiples

Emphasis on the best comparables

4

Example of Financial Statistics and Ratios

16 Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Example of Financial Statistics and Ratios (Cont’d)

17 Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Example of Trading Multiples Output Page

18 Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

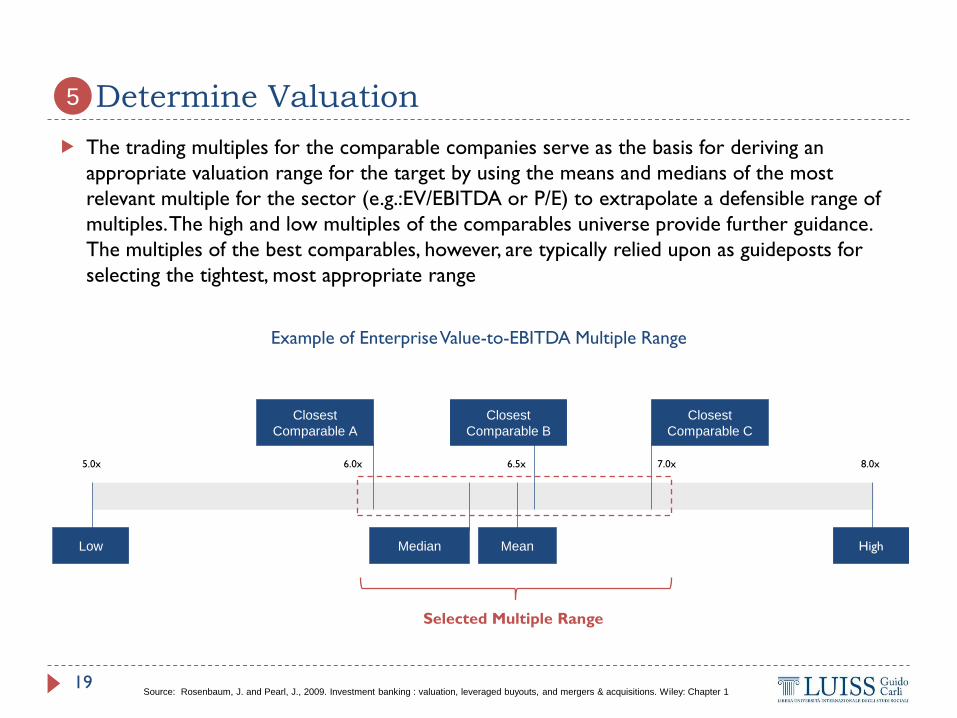

Determine Valuation

19

The trading multiples for the comparable companies serve as the basis for deriving an

appropriate valuation range for the target by using the means and medians of the most

relevant multiple for the sector (e.g.:EV/EBITDA or P/E) to extrapolate a defensible range of

multiples. The high and low multiples of the comparables universe provide further guidance.

The multiples of the best comparables, however, are typically relied upon as guideposts for

selecting the tightest, most appropriate range

Example of Enterprise Value-to-EBITDA Multiple Range

5

Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

High Median Mean

Closest

Comparable A

Closest

Comparable B

Closest

Comparable C

Low

6.0x 5.0x 6.5x 7.0x 8.0x

Selected Multiple Range

Net Income

Fully Diluted

Shares

LTM $70 12.00x – 15.00x $840 – $1,050 100 $8.40 – $10.50

2008E $75 11.00x – 14.00x $825 – $1,050 100 $8.25 – $10.50

2009E $80 10.00x – 13.00x $800 – $1,040 100 $8.00 – $10.40

Multiple Range Implied Equity Value Implied Share Price

Net Income Plus: Net Debt

LTM $70 12.00x – 15.00x $840 – $1,050 500 $1,340 – $1,550

2008E $75 11.00x – 14.00x $825 – $1,050 500 $1,325 – $1,550

2009E $80 10.00x – 13.00x $800 – $1,040 500 $1,300 – $1,540

Multiple Range Implied Equity Value Implied Enterprise Value

EBITDA

Less: Net

Debt

Fully

Diluted

Shares

LTM $200 6.50x – 7.50x $1,300 – $1,500 (500) $800 – $1,000 100 $8.00 – $10.00

2008E $215 6.00x – 7.00x $1,290 – $1,505 (500) $790 – $1,005 100 $7.90 – $10.05

2009E $230 5.50x – 6.50x $1,265 – $1,495 (500) $765 – $995 100 $7.65 – $9.95

Implied Share PriceMultiple Range Implied Enterprise Value Implied Equity Value

Implied Valuation

20

The selected multiple range is applied to the target’s appropriate financial statistics to derive an implied

valuation range

Example of Valuation Implied by P/E – Share Price

Example of Valuation Implied by P/E – Enterprise Value

Example of Valuation Implied by EV/EBITDA

Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Comparable Precedent Transactions Analysis

(Compaq)

21

Precedent transactions analysis, like comparable companies analysis, employs a multiples-based

approach to derive an implied valuation range for a given company, division, business, or

collection of assets (“target”)

Compaq is premised on multiples paid for comparable companies in prior M&A transactions

Steps:

1. Select the Universe of Comparable Acquisitions

2. Locate the Necessary Deal-Related and Financial Information

3. Spread Key Statistics, Ratios, and Transaction Multiples

4. Benchmark the Comparable Acquisitions

5. Determine Valuation

Compaq: Pros & Cons

22

Pros Cons

Market-based – analysis is based on actual

acquisition multiples and premiums paid for

similar companies

Market-based – multiples may be skewed

depending on capital markets and/or

economic environment at the time of the transaction

Current – recent transactions tend to reflect

prevailing M&A, capital markets and general

economic conditions

Time Lag – precedent transactions, by definition,

have occurred in the past and, therefore, may not

be truly reflective of prevailing market conditions

(e.g., the LBO boom in the mid-2000s vs. the

ensuing credit crunch)

Relativity – multiples approach provides traight

forward reference points across sectors and time

periods

Existence of Comparable Acquisitions – in some

cases it may be difficult to find a robust universe

of precedent transactions

Simplicity – key multiples for a few selected

transactions can anchor valuation

Availability of Information – information may be

insufficient to determine transaction multiples for

many comparable acquisitions

Objectivity – precedent-based and, therefore, avoids

making assumptions about a company’s future

performance

Acquirer’s Basis for Valuation – multiple paid by the

buyer may be based on expectations governing

the target’s future financial performance (which is

typically not publicly disclosed) rather than on

reported LTM financial information

Example of Precedent Transactions Input Page

Template

23 Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

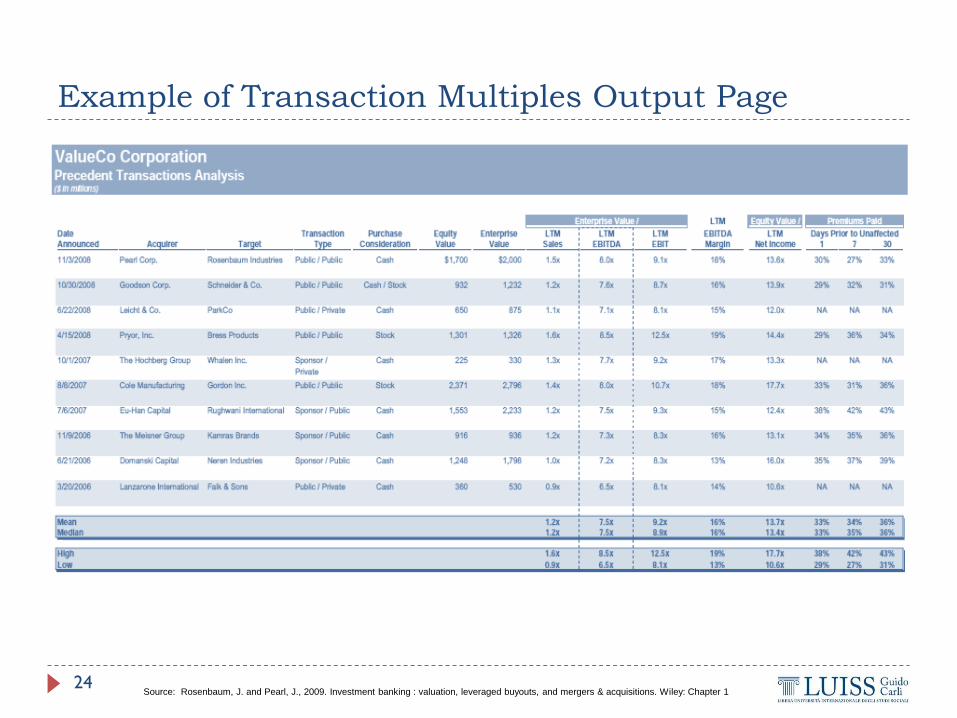

Example of Transaction Multiples Output Page

24 Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

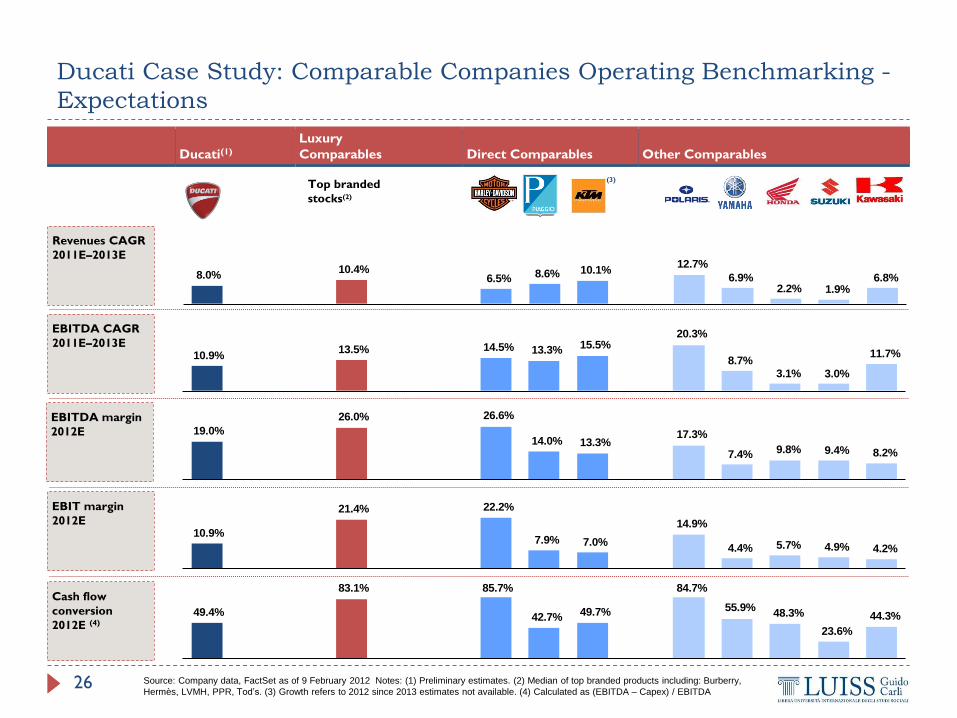

Ducati Case Study: Comparable Companies Operating Benchmarking –

Historical Performance

18.1%

26.0% 20.2%

13.0% 16.4% 14.4%

8.0% 13.0%

10.0% 6.9%

(3.3%)

20.1%

(12.6%)

9.0%

24.7% 1.0% 6.5%

(1.4%)

8.5% 4.0%

8.9% 14.7% 14.9%

7.5% 4.9%

11.1%

4.7% 9.5%

(5.2%) (4.6%)

(8.6%)

10.0%

(9.7%)(2.7%)

(10.7%) (6.2%)(6.2%) (7.1%)

(27.2%)(20.7%)

Revenues CAGR

2008A–2010A

EBITDA margin

2010A

EBITDA CAGR

2008A–2010A

EBIT margin

2010A

Luxury

Comparables Direct Comparables Ducati(1)

Top branded

stocks(2)

Cash flow

conversion

2010A 41.8%

81.6% 79.1% 87.3%

54.9% 74.8%

63.7% 64.6%

45.9% 31.6%

(3)

25

Other Comparables

Source: Company data, FactSet as of 9 February 2011. Notes: (1) Data as of December 2010 annual report. (2) Median of top branded products

including: Burberry, Hermès, LVMH, PPR, Tod’s. (3) Calculated as (EBITDA – Capex) / EBITDA

26

EBITDA margin

2012E

EBITDA CAGR

2011E–2013E

EBIT margin

2012E

19.0%

26.0% 26.6%

14.0% 13.3% 17.3%

7.4% 9.8% 9.4% 8.2%

10.9% 13.5% 14.5% 13.3% 15.5%

20.3%

8.7% 3.1% 3.0%

11.7%

10.9%

21.4% 22.2%

7.9% 7.0%

14.9%

4.4% 5.7% 4.9% 4.2%

Top branded

stocks(2)

(3)

49.4%

83.1% 85.7%

42.7% 49.7%

84.7%

55.9% 48.3%

23.6%

44.3%

Cash flow

conversion

2012E (4)

Revenues CAGR

2011E–2013E

8.0% 10.4%

6.5% 8.6% 10.1% 12.7%

6.9% 2.2% 1.9%

6.8%

Luxury

Comparables Direct Comparables Ducati(1) Other Comparables

Ducati Case Study: Comparable Companies Operating Benchmarking -

Expectations

Source: Company data, FactSet as of 9 February 2012 Notes: (1) Preliminary estimates. (2) Median of top branded products including: Burberry,

Hermès, LVMH, PPR, Tod’s. (3) Growth refers to 2012 since 2013 estimates not available. (4) Calculated as (EBITDA – Capex) / EBITDA

10.0x 11.4x 11.3x

7.6x 6.8x 7.5x

16.3x

11.9x14.6x

12.5x 12.9x 12.7x

9.4x

15.1x

9.3x 10.8x15.6x

11.9x

21.6x

Top branded

stocks(1)

EV / EBITDA

2013E

EV / (EBITDA –

Capex) 2012E

EV / (EBITDA –

Capex) 2013E

7.9x 7.9x9.8x

4.5x

6.1x 4.5x8.1x

3.2x

6.4x

ex fin. services

Avg. 2013: 7.2x Avg. 2013: 5.7x

Avg. 2012: 12.4x Avg. 2012: 13.8x

Avg. 2013: 9.5x Avg. 2013: 11.4x

EV / EBITDA

2012E 9.5x

8.7x10.8x

5.2x

7.5x 7.9x5.5x

8.4x

3.3x

7.1x

Avg. 2012: 7.8x Avg. 2012: 6.4x

n.a.

27

Luxury

Comparables Direct Comparables Other Comparables

n.a.

Ducati Case Study: Trading Multiples of Key Peers

Source: Company data, FactSet as of 9 February 2012. Notes: (1) Median of top branded products including: Burberry, Hermès, LVMH, PPR, Tod’s

–

5.0x

10.0x

15.0x

20.0x

25.0x

30.0x

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Ducati EV / EBITDA HD EV / EBITDA 1999-2008 Ducati average EV / EBITDA 1999-2008 HD average EV / EBITDA

12.9x

7.8x

28

Ducati Case Study: Historical Multiples Evolution NTM EV / EBITDA

Reference Motorcyle Sector Transactions

29

Luxury Flash Spot Automotive Transactions

Ducati Case Study: Comparable Acquisitions Analysis

Target Enterprise EV Multiples Inputs (local currency)

Date Bidder Value LTM revenue LTM EBITDA Comments

1 19-Feb-08 Ducati Motor Holding SpA € 401m 1.4x 10.5x

Performance Motorcycles SpA

2 22-Dec-06 KTM Power Sports AG € 454m 0.9x 7.9x

Cross Industries AG

3 21-Oct-99 Piaggio € 693m 0.7x 10.0x

Morgan Grenfell Private Equity

Average 1.0x 9.5x

Median 0.9x 10.0x

4 09-Aug-09 Volkswagen € 12 , 400m 1.9x 8.5x Volkswagen acquiring 49.9% stake of Porsche

Porsche

5 26-Jul-07 Mubadala Development Co. € 2 , 280m 1.9x 8.6x Mubadala Development acquiring a 5% stake in Ferrari

Ferrari

6 12-May-07 Investor Group € 783m 1.0x 7.0x Investor Group acquiring 91 % of Aston Martin for € 783 m

Aston Martin

7 12-Jun-00 Volkswagen € 106m 2.2x NA Volkswagen acquiring 100% of Lamborghini

Lamborghini

Average 1.8x 8.0x

Median 1.9x 8.5x

Overall average 1.4x 8.7x

Overall median 1.4x 8.6x

Public offer for ordinary shares at a price of € 1 . 70 each

Cross Industries acquired 1.38m shares (20% stake) of KTM

Power Sports AG from Polaris for € 58 . 5 m

Morgan Grenfell acquired Piaggio. Morgan is to hold 80%,

TPG 10% and Umberto Agnelli 10%

Note: Exchange rates used for deal value is the rate as on the date of transaction

Valuation driver €860m: value paid by

Audi(1) for the

acquisition of Ducati

in April 2012

10.2x 22.0x 9.0x 18.3x

30

2012E 8.8x – 9.8x 19.2x – 21.4x 7.8x – 8.7x 15.6x – 17.4x

2013E 8.8x – 9.7x 19.1x – 21.1x 7.8x – 8.6x 15.5x – 17.1x

2012E 7.2x – 8.5x 15.7x – 18.6x 6.4x – 7.5x 12.7x – 15.1x

2013E 6.3x – 9.7x 13.7x – 21.0x 5.6x – 8.5x 11.1x – 17.1x

8.7x – 10.5x 18.9x – 22.8x 7.7x – 9.3x 15.4x – 18.6x

LBO 7.5x – 8.5x 16.3x – 18.5x 6.6x – 7.5x 13.3x – 15.0x

- Low: overall average of

comparable transactions (8.7x LTM

EBITDA)

- High: VTO on Ducati by

Investindustrial (10.5x LTM

EBITDA)

EV / EBITDA

multiple

Implied EV/ 2012

(EBITDA - Capex)

Implied EV/

2012 EBITDA Comments

-Low: average value of direct

comparables trading multiple (7.8x

2012E EBITDA and 7.2x 2013E

EBITDA)

-High: trading multiple of Harley

Davidson ex. Financial Services

(8.7x 2012E EBITDA and 7.9x

2013E EBITDA)

Tra

din

g V

alu

ati

on

Implied EV/

2011 EBITDA

Implied EV/ 2011

(EBITDA - Capex)

Targeting c. 2.0x CoC returns over

5 years

EV / (EBITDA -

Capex)

Multiple

-Low: median trading multiple of

direct comparables (12.7x 2012E

EBITDA - Capex and 9.5x 2013E

EBITDA - Capex)

-High: trading multiple of KTM

(15.1x EBITDA - Capex) for 2012E;

trading multiple of Kawasaki (14.6x

EBITDA - Capex) for 2013E

Comparable Precedent

Transactions

Enterprise Value Methodology

Co

ntr

ol

Valu

ati

on

630

731

528

606

738

742 826

814

717

811

882

715

Ducati historical

NTM EV/EBITDA

average multiple of

7.8x

(~€740m)

Ducati Case Study: Indicative Valuation Overview

Note: (1) According to press release

Purchase Consideration

31

Purchase Consideration refers to the mix of cash, stock, and/or other securities that the acquirer offers to

the target’s shareholders.

All-Cash Transaction: the acquirer makes an offer to purchase all or a portion of the target’s shares

outstanding for cash.

Equity value: cash offer price per share multiplied by the number of fully diluted shares outstanding.

Receipt of such consideration triggers a taxable event as opposed to the exchange or receipt of shares

of stock, which, if structured properly, is not taxable until the shares are eventually sold.

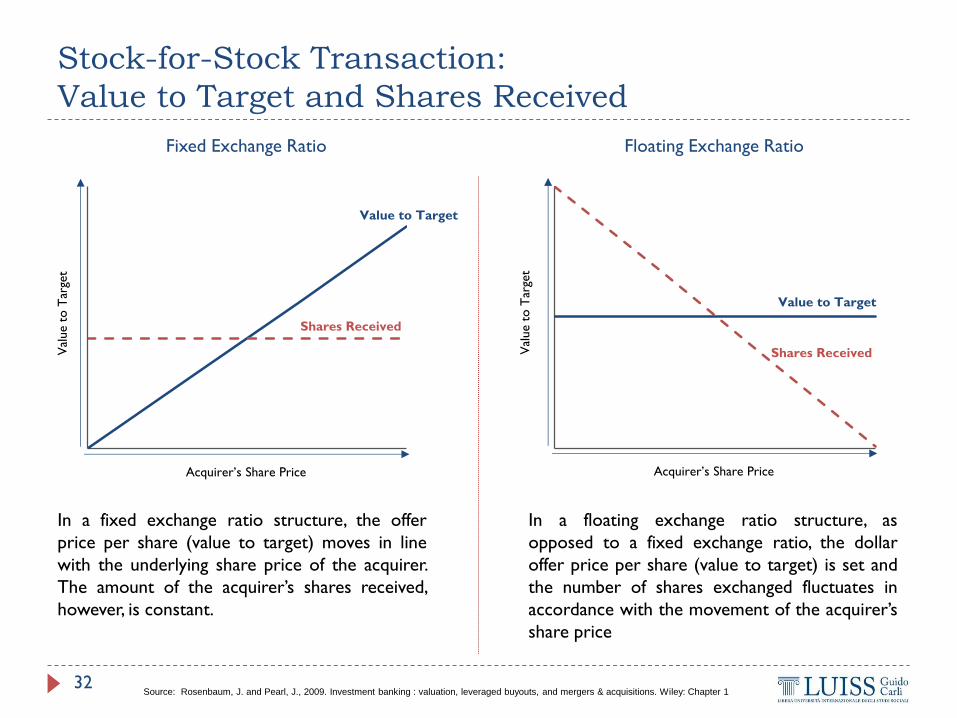

Stock-for-Stock Transaction:

Equity value: calculation based on a fixed exchange ratio or a floating exchange ratio (“fixed price”). The

exchange ratio is calculated as offer price per share divided by the acquirer’s share price.

Cash and Stock Transaction: the acquirer offers a combination of cash and stock as purchase consideration.

The cash portion of the offer represents a fixed value per share for target shareholders. The stock

portion of the offer can be set according to either a fixed or floating exchange ratio.

Offer Price per Share and Equity Value is calculates as follows:

Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Offer Price

per Share

Equity Value

Cash Offer

per Share

Cash Offer

per Share

Exchange Ratio

Exchange Ratio

Acquirer’s

Share Price

Acquirer’s

Share Price

Target’s Fully Diluted

Shares Outstanding

= + x

= + x x

Stock-for-Stock Transaction:

Value to Target and Shares Received

32

In a fixed exchange ratio structure, the offer

price per share (value to target) moves in line

with the underlying share price of the acquirer.

The amount of the acquirer’s shares received,

however, is constant.

Floating Exchange Ratio Fixed Exchange Ratio

In a floating exchange ratio structure, as

opposed to a fixed exchange ratio, the dollar

offer price per share (value to target) is set and

the number of shares exchanged fluctuates in

accordance with the movement of the acquirer’s

share price

Source: Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged buyouts, and mergers & acquisitions. Wiley: Chapter 1

Val

ue t

o T

arge

t

Acquirer’s Share Price

Value to Target

Shares Received

Val

ue t

o T

arge

t

Acquirer’s Share Price

Value to Target

Shares Received

Discounted Cash Flow Analysis (DCF)

33

In intrinsic valuation, an asset is valued based upon its intrinsic characteristics

For cash flow generating assets, the intrinsic value will be a function of the magnitude of

the expected cash flows on the asset over its lifetime and the uncertainty about receiving

those cash flows

The value of a risky asset can be estimated by discounting the expected cash flows

on the asset over its life at a risk-adjusted discount rate:

Where the asset has a n-year life, E(CFt) is the expected cash flow in period t and r is a

discount rate that reflects the risk of the cash flows

𝑉𝑎𝑙𝑢𝑒 𝑜𝑓 𝑎𝑛 𝐴𝑠𝑠𝑒𝑡 = 𝐸 𝐶𝐹1

(1 + 𝑟)+

𝐸 𝐶𝐹2

1 + 𝑟 2+ ⋯ +

𝐸 𝐶𝐹𝑛

1 + 𝑟 𝑛

DCF Choices: Equity Valuation vs. Firm Valuation

34 Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Assets Liabilities

Existing Investments

Generate cashflows today

Includes long lived (fixed) and short-

lived (working capital) assets

Assets in Place

Growth Assets

Debt

Equity Expected Value that will be created by

future investments

Fixed Claim on cash flows

Little or No role in management

Fixed Maturity

Tax Deductible

Residual Claim on cash flows

Significant Role in management

Perpetual Lives

Firm Valuation: Value the entire business

Equity Valuation: Value just the equity

claim in the business

DCF Choices: Equity Valuation vs. Firm Valuation (Cont’d)

35

Firm Valuation

Equity Valuation

Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Assets Liabilities

Cash flows considered are

cashflows from assets, after debt

payments and after making

reinvestments needed for

future growth

Assets in Place

Growth Assets

Debt

Equity Discount rate reflects only the

cost of raising equity financing

Present value is value of just the equity claims on the firm

Assets Liabilities

Cash flows considered are

cashflows from assets, prior to

any debt payments but after firm

has reinvested to create growth

assets

Assets in Place

Growth Assets

Debt

Equity

Discount rate reflects the cost

of raising both debt and equity

financing, in proportion to

their use

Present value is value of the entire firm, and reflects the value

of all claims on the firm

Discounted Cash Flow Valuation: The Steps

36

Estimate the discount rate or rates to use in the valuation

Discount rate can be either a cost of equity (if doing equity valuation) or a cost of capital (if

valuing the firm)

Discount rate can be in nominal terms or real terms, depending upon whether the cash flows are

nominal or real

Discount rate can vary across time

Estimate the current earnings and cash flows on the asset, to either equity investors

(CF to Equity) or to all claimholders (CF to Firm)

Estimate the future earnings and cash flows on the firm being valued, generally by

estimating an expected growth rate in earnings

Estimate when the firm will reach “stable growth” and what characteristics (risk &

cash flow) it will have when it does

Choose the right DCF model for this asset and value it

Generic DCF Valuation Model

37 Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Value

Firm: Value of Firm

Equity: Value of Equity

Length of Period of High Growth

Terminal Value

CF1 CF2 CF3 CF4 CF5 CFn

Forever

……..

Cash Flows

Firm: Pre-debt cash flow

Equity: After debt

cash flows

Expected Growth

Firm: Growth in

Operating Earnings

Equity: Growth in Net

Income/EPS Firm is in stable growth:

Grows at constant rate forever

Discount Rate

Firm: Cost of Capital

Equity: Cost of Equity

The Different Valuation Models

38

Input

Dividend

Discount Model

FCFE (Potential

dividend)

discount model

FCFF (firm)

valuation model

Cash Flow Dividend

Potential dividends

= FCFE = Cash

flows after taxes,

reinvestment needs

and debt cash

flows

FCFF = Cash

flows before debt

payments but after

reinvestment needs

and taxes.

Expected

Growth

In equity income

and dividends

In equity income

and FCFE

In operating

income and FCFF

Discount Rate Cost of equity Cost of equity Cost of capital

Steady State

When dividends

grow at constant

rate forever

When FCFE grow

at constant rate

forever

When FCFF grow

at constant rate

forever

Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Dividend Discount Model (DDM)

39 Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Value of Equity

Riskfree Rate

No default risk

No reinvestment risk

In same currency and in same

terms (real or nominal) as

cash flows

Beta

Measures market risk

Risk Premium

Premium for average

risk investment

Type of

Business

Operating

Leverage

Financial

Leverage Base Equity

Premium

Country Risk

Premium

+

x

Discount at Cost of Equity

Terminal Value = Dividend n+1/(ke-gn)

Dividend1 Dividend2 Dividend3 Dividend4 Dividend5 Dividendn Forever

……..

Dividends

Net Income

* Payout Ratio

= Dividends

Expected Growth

Retention Ratio *

Return on Equity

Firm is in stable growth:

Grows at constant rate forever

Cost of Equity

Free Cash Flow to Equity (FCFE)

40 Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Value of Equity

Riskfree Rate

No default risk

No reinvestment risk

In same currency and in same

terms (real or nominal) as

cash flows

Beta

Measures market risk

Risk Premium

Premium for average

risk investment

Type of

Business

Operating

Leverage

Financial

Leverage Base Equity

Premium

Country Risk

Premium

+

x

Discount at Cost of Equity

Terminal Value = FCFE n+1/(ke-gn)

FCFE1 FCFE2 FCFE3 FCFE4 FCFE5 FCFEn Forever

……..

Cashflow to Equity

Net Income

- (Cap Ex – Depr) (1-DR)

- Change in WC (1-DR)

= FCFE

Expected Growth

Retention Ratio *

Return on Equity Firm is in stable growth:

Grows at constant rate forever

Cost of Equity

Financing

Weights

Debt ratio = DR

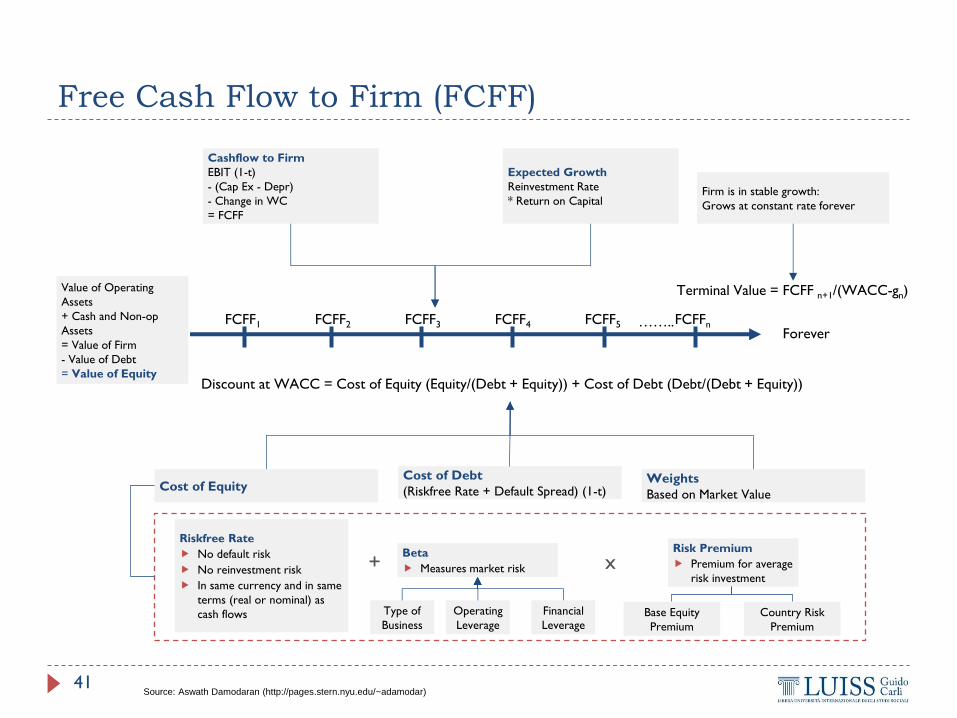

Free Cash Flow to Firm (FCFF)

41 Source: Aswath Damodaran (http://pages.stern.nyu.edu/~adamodar)

Value of Operating

Assets

+ Cash and Non-op

Assets

= Value of Firm

- Value of Debt

= Value of Equity

Riskfree Rate

No default risk

No reinvestment risk

In same currency and in same

terms (real or nominal) as

cash flows

Beta

Measures market risk

Risk Premium

Premium for average

risk investment

Type of

Business

Operating

Leverage

Financial

Leverage Base Equity

Premium

Country Risk

Premium

+

x

Discount at WACC = Cost of Equity (Equity/(Debt + Equity)) + Cost of Debt (Debt/(Debt + Equity))

Terminal Value = FCFF n+1/(WACC-gn)

FCFF1 FCFF2 FCFF3 FCFF4 FCFF5 FCFFn Forever

……..

Cashflow to Firm

EBIT (1-t)

- (Cap Ex - Depr)

- Change in WC

= FCFF

Expected Growth

Reinvestment Rate

* Return on Capital Firm is in stable growth:

Grows at constant rate forever

Cost of Equity Cost of Debt

(Riskfree Rate + Default Spread) (1-t) Weights

Based on Market Value

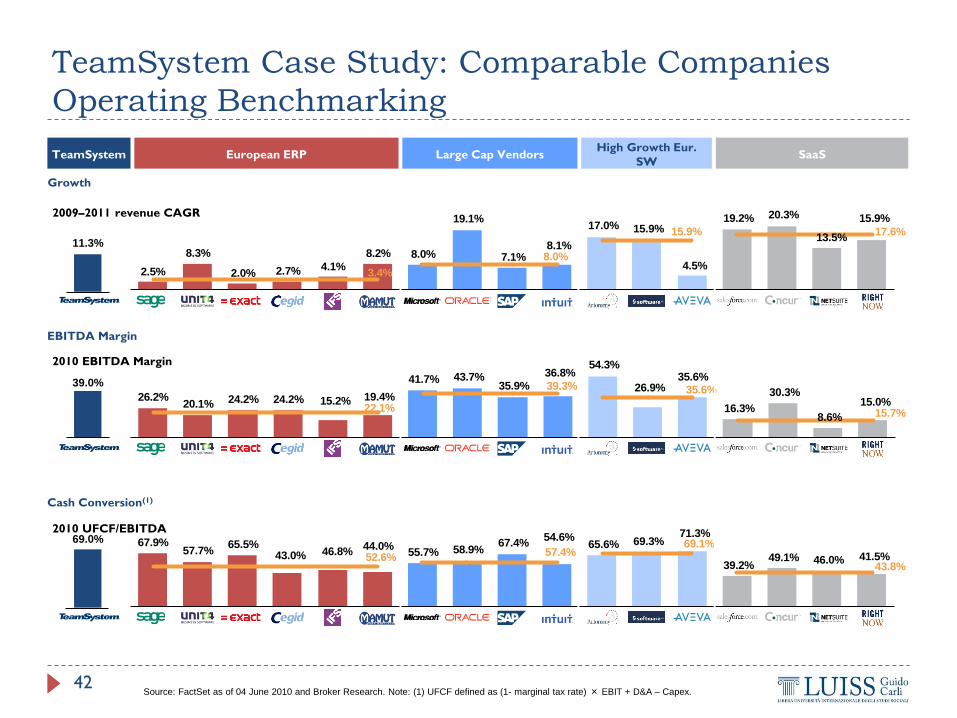

TeamSystem Case Study: Comparable Companies

Operating Benchmarking

Growth

2.5%

8.3%

2.0% 2.7% 4.1%

8.2% 8.0%

19.1%

7.1%8.1%

17.0% 15.9%

4.5%

19.2% 20.3%

13.5%

15.9%

3.4%

8.0%

15.9% 17.6%

European ERP SaaS Large Cap Vendors High Growth Eur.

SW

Cash Conversion(1)

67.9%57.7%

65.5%43.0% 46.8%

44.0%55.7% 58.9%

67.4%54.6%

65.6% 69.3%71.3%

39.2%49.1% 46.0% 41.5%52.6% 57.4%

69.1%

43.8%

EBITDA Margin

26.2%20.1% 24.2% 24.2% 15.2% 19.4%

41.7% 43.7%35.9%

36.8%54.3%

26.9%35.6%

16.3%

30.3%

8.6%

15.0%22.1%

39.3% 35.6%

15.7%

TeamSystem

11.3%

2009–2011 revenue CAGR

2010 EBITDA Margin

2010 UFCF/EBITDA

39.0%

69.0%

42 Source: FactSet as of 04 June 2010 and Broker Research. Note: (1) UFCF defined as (1- marginal tax rate) × EBIT + D&A – Capex.

EV/EBITDA 2010

9.2x 7.6x 6.9x4.1x 4.6x

5.4x6.9x 8.1x 9.4x

9.0x 12.9x 11.0x

13.7x

43.2x21.0x

49.5x

13.8x

6.3x8.6x

12.9x 32.1x

EV/UFCF 2010(1)

13.6x 13.1x 10.5x 9.4x 9.8x12.3x

12.3x 13.7x 14.0x16.5x 19.6x

15.9x

19.2x

110.0x

42.7x

107.7x

33.1x

11.6x14.1x 19.2x

75.6x

EV/EBITDA minus capex 2010

10.0x 10.5x7.9x 6.9x 7.3x

9.2x7.4x 8.3x 10.1x

10.1x 14.3x11.6x

14.1x

56.0x

26.0x

n.m.

20.6x

8.8x 9.3x14.1x

26.0x

European ERP SaaS Large cap vendors High growth Eur. SW

43

TeamSystem Case Study: Trading Multiples of Key

Peers

Source: FactSet as of 04 June 2010 and Broker Research. Note: (1) UFCF defined as (1- marginal tax rate) × EBIT + D&A – Capex.

TeamSystem Case Study: Precedent Transaction

Analysis

Acquiror Target Revenue EBITDA EBIT Target description

13/05/2010 Honeywell Matrikon €105 1.4x 16.0x 19.5x Provides software to manage production and operations for industrial plants

12/05/2010 SAP Sybase €4,502 4.8x 12.6x 15.5x Provides enterprise and mobile software to manage, analyze and mobilize information

05/05/2010 ABB Ventyx €777 4.0x NA NA Provider of software solutions for managing energy networks

04/05/2010 PE Consortium IDC €2,336 4.0x 11.3x 12.8x Leading provider of financial markets data, analytics, & related solutions

03/05/2010 Apax Sophos €630 3.2x 16.0x NA Provider of security and data protection solutions

16/04/2010 Oracle Phase Forward €414 2.6x 11.9x 16.6x Life sciences data management solutions for clinical trials

31/03/2010 Investor Group SkillSoft PLC €832 3.6x 9.2x 9.6x SaaS provider of on-demand, e-learning and performance support solutions

02/03/2010 Elliott Associates Novell €783 1.2x 6.6x 7.7x Provider of enterprise infrastructure, software and services

11/02/2010 Advanced Comp. Software COA Soltn's €115 1.7x 8.1x NA Supplier of accounting and budgeting software to the healthcare industry

08/12/2009 Francisco Partners QuadraMed €81 0.8x 8.1x 11.1x Provider of healthcare information technologies and services

01/12/2009 Vista Equity Partners Intuit- Real Estate Solutions €85 1.7x NA 21.3x Provider of software and services to companies in the real estate management and investment industry

05/11/2009 JDA Software Group i2 Technologies €271 1.7x 6.6x 7.1x Dallas-based developer of supply chain management software

07/10/2009 Compuware Gomez €201 5.6x 48.2x 70.3x Provider of on-demand platform for web and mobile applications

06/10/2009 Sykes ICT Group €146 0.5x 7.8x 69.6x Provider of customer management and BPO solutions

29/09/2009 Investor Group MSC Software €171 1.1x 9.3x 12.7x Provider of simulation and software services

15/09/2009 Adobe Omniture €1,179 5.1x 25.0x 42.8x Online business optimization software provider

02/09/2009 Axel Springer AG StepStone ASA €119 1.1x 6.9x 10.2x Provider of e-recruiting solutions and human capital management software

28/07/2009 IBM Corporation SPSS Inc. €590 2.8x 9.7x 12.7x Provider of predictive analytics software and solutions

13/07/2009 Software AG IDS Scheer €401 1.0x 16.5x 20.1x Provider of business process management software solutions

02/06/2009 Intuit Paycycle €119 5.2x NA NA Provider of online payroll services

27/05/2009 Vista Equity Partners SumTotal Systems €80 1.0x 15.0x 39.2x Provider of learning, performance, and talent management solutions

22/01/2009 Autonomy Interwoven €494 2.5x 13.1x 14.8x Provider of enterprise content management software

18/09/2008 Wulters Kluwer Addison Software €192 NA NA NA Provides software applications for tax advisors

14/01/2008 Unit4 Coda €214 3.7x 12.1x 13.1x Provider of finance-based management information solutions

17/12/2007 Epicor NSB €227 3.1x 12.9x 19.3x Provider of application management software and services to the retail industry

01/06/2007 Hellman & Friedman Iris €768 NA NA NA Provider of accounting software

23/03/2007 Hellman & Friedman Kronos €1,322 2.9x 13.0x 14.1x Provider of workforce and talent management software and services

Average 2.7x 13.5x 21.9x

Median 2.6x 12.0x 14.8x

Enterprise value / LTM

Announcement

date

Enterprise

value

(1)

(data in €m)

Significant software

transactions announced

since March 2010 have

commanded median

LTM EBITDA and LTM

EBIT multiples of 12.3x

and 14.1x, respectively

(1)

44 Note: (1) Defined as fully diluted equity value less cash plus total debt.

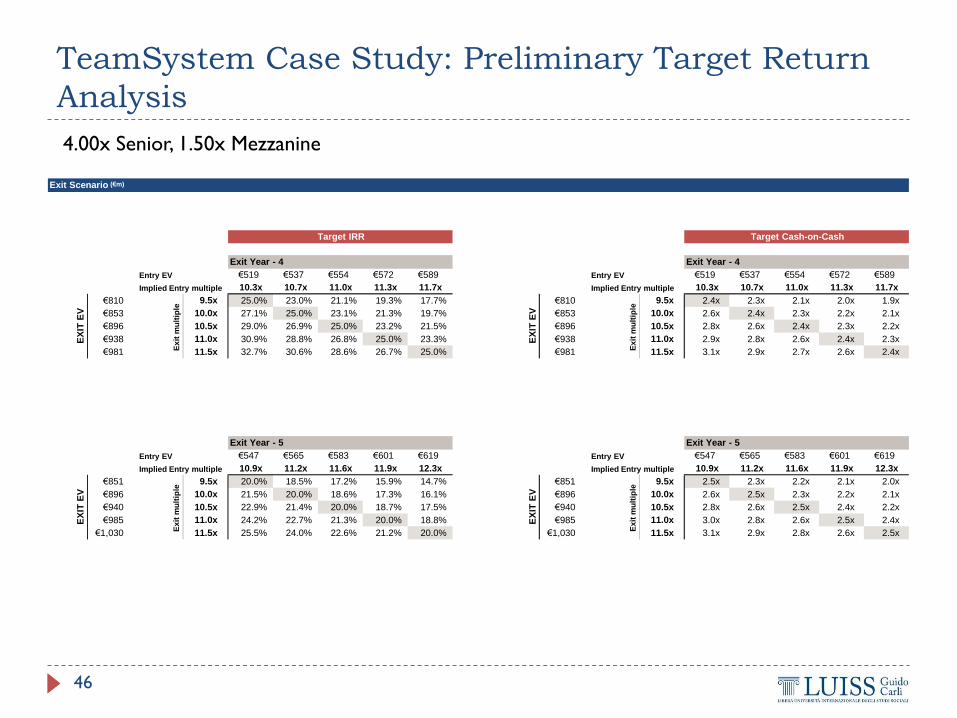

TeamSystem Case Study: Preliminary IRR Analysis

45

4.00x Senior, 1.50x Mezzanine

Exit Scenario (€m)

IRR Cash-on-Cash

Exit Year - 4 Exit Year - 4

Entry EV € 529 € 554 € 580 € 605 € 630 Entry EV € 529 € 554 € 580 € 605 € 630

Entry multiple 10.5x 11.0x 11.5x 12.0x 12.5x Entry multiple 10.5x 11.0x 11.5x 12.0x 12.5x

€ 896 10.5x 27.8% 25.0% 22.4% 20.1% 18.0% € 940 10.5x 2.67x 2.44x 2.25x 2.08x 1.94x

€ 938 11.0x 29.7% 26.8% 24.2% 21.9% 19.7% € 985 11.0x 2.83x 2.59x 2.38x 2.21x 2.06x

€ 981 11.5x 31.5% 28.6% 25.9% 23.5% 21.4% € 1 , 030 11.5x 2.99x 2.73x 2.52x 2.33x 2.17x

€ 1 , 024 12.0x 33.2% 30.2% 27.6% 25.2% 23.0% € 1 , 075 12.0x 3.15x 2.88x 2.65x 2.46x 2.29x

€ 1 , 066 12.5x 34.9% 31.9% 29.2% 26.7% 24.5% € 1 , 120 12.5x 3.31x 3.02x 2.78x 2.58x 2.40x

12.5

Exit Year - 5 Exit Year - 5

Entry EV € 529 € 554 € 580 € 605 € 630 Entry EV € 529 € 554 € 580 € 605 € 630

Entry multiple 10.5x 11.0x 11.5x 12.0x 12.5x Entry multiple 10.5x 11.0x 11.5x 12.0x 12.5x

€ 940 10.5x 24.5% 22.3% 20.2% 18.4% 16.8% € 940 10.5x 2.99x 2.73x 2.52x 2.33x 2.17x

€ 985 11.0x 25.8% 23.6% 21.6% 19.7% 18.0% € 985 11.0x 3.16x 2.89x 2.66x 2.46x 2.29x

€ 1 , 030 11.5x 27.1% 24.9% 22.8% 21.0% 19.3% € 1 , 030 11.5x 3.33x 3.04x 2.80x 2.59x 2.41x

€ 1 , 075 12.0x 28.4% 26.1% 24.0% 22.2% 20.4% € 1 , 075 12.0x 3.49x 3.19x 2.94x 2.72x 2.54x

€ 1 , 120 12.5x 29.6% 27.3% 25.2% 23.3% 21.6% € 1 , 120 12.5x 3.66x 3.35x 3.08x 2.85x 2.66x

12.0

Ex

it m

ult

iple

E

xit

mu

ltip

le

EX

IT E

V

EX

IT E

V

EX

IT E

V

EX

IT E

V

Ex

it m

ult

iple

E

xit

mu

ltip

le

46

TeamSystem Case Study: Preliminary Target Return

Analysis

4.00x Senior, 1.50x Mezzanine

Exit Scenario (€m)

Target IRR Target Cash-on-Cash

Exit Year - 4 Exit Year - 4

Entry EV € 519 € 537 € 554 € 572 € 589 Entry EV € 519 € 537 € 554 € 572 € 589

Implied Entry multiple 10.3x 10.7x 11.0x 11.3x 11.7x Implied Entry multiple 10.3x 10.7x 11.0x 11.3x 11.7x

€ 810 9.5x 25.0% 23.0% 21.1% 19.3% 17.7% € 810 9.5x 2.4x 2.3x 2.1x 2.0x 1.9x

€ 853 10.0x 27.1% 25.0% 23.1% 21.3% 19.7% € 853 10.0x 2.6x 2.4x 2.3x 2.2x 2.1x

€ 896 10.5x 29.0% 26.9% 25.0% 23.2% 21.5% € 896 10.5x 2.8x 2.6x 2.4x 2.3x 2.2x

€ 938 11.0x 30.9% 28.8% 26.8% 25.0% 23.3% € 938 11.0x 2.9x 2.8x 2.6x 2.4x 2.3x

€ 981 11.5x 32.7% 30.6% 28.6% 26.7% 25.0% € 981 11.5x 3.1x 2.9x 2.7x 2.6x 2.4x

12.5

Exit Year - 5 Exit Year - 5

Entry EV € 547 € 565 € 583 € 601 € 619 Entry EV € 547 € 565 € 583 € 601 € 619

Implied Entry multiple 10.9x 11.2x 11.6x 11.9x 12.3x Implied Entry multiple 10.9x 11.2x 11.6x 11.9x 12.3x

€ 851 9.5x 20.0% 18.5% 17.2% 15.9% 14.7% € 851 9.5x 2.5x 2.3x 2.2x 2.1x 2.0x

€ 896 10.0x 21.5% 20.0% 18.6% 17.3% 16.1% € 896 10.0x 2.6x 2.5x 2.3x 2.2x 2.1x

€ 940 10.5x 22.9% 21.4% 20.0% 18.7% 17.5% € 940 10.5x 2.8x 2.6x 2.5x 2.4x 2.2x

€ 985 11.0x 24.2% 22.7% 21.3% 20.0% 18.8% € 985 11.0x 3.0x 2.8x 2.6x 2.5x 2.4x

€ 1 , 030 11.5x 25.5% 24.0% 22.6% 21.2% 20.0% € 1 , 030 11.5x 3.1x 2.9x 2.8x 2.6x 2.5x

EX

IT E

V

Ex

it m

ult

iple

EX

IT E

V

Ex

it m

ult

iple

EX

IT E

V

Ex

it m

ult

iple

EX

IT E

V

Ex

it m

ult

iple

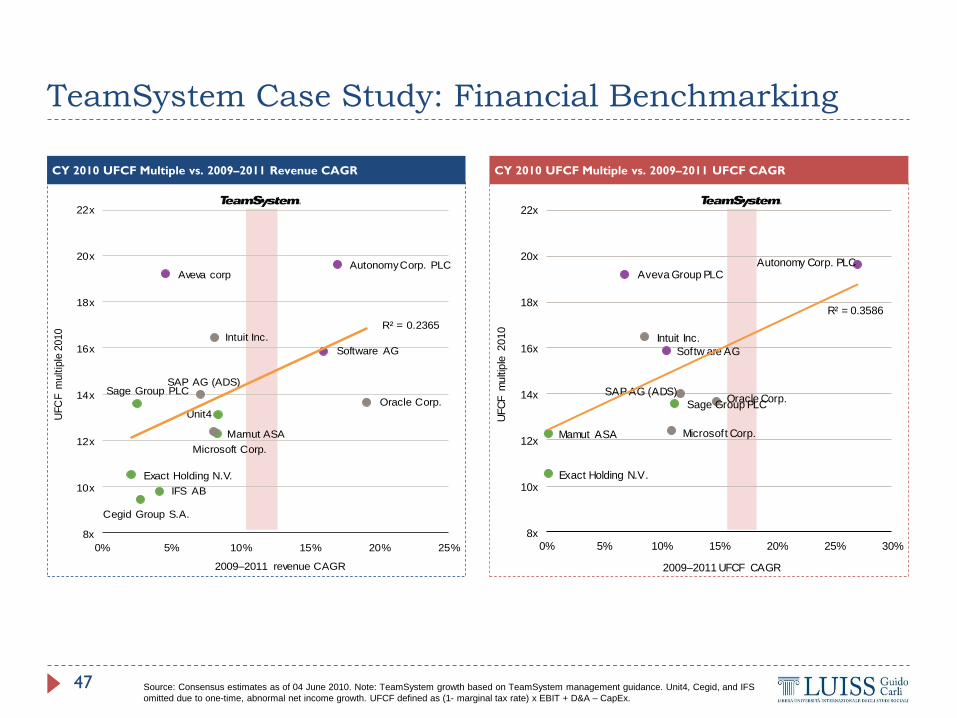

TeamSystem Case Study: Financial Benchmarking

CY 2010 UFCF Multiple vs. 2009–2011 Revenue CAGR CY 2010 UFCF Multiple vs. 2009–2011 UFCF CAGR

Sage Group PLC

Exact Holding N.V.

Mamut ASA

Autonomy Corp. PLCAveva Group PLC

Softw are AG

Microsoft Corp.

Oracle Corp.SAP AG (ADS)

Intuit Inc.

R² = 0.3586

8x

10x

12x

14x

16x

18x

20x

22x

0% 5% 10% 15% 20% 25% 30%

UFC

F m

ulti

ple

2010

2009–2011 UFCF CAGR

Sage Group PLC

Unit4

Exact Holding N.V.

Cegid Group S.A.

IFS AB

Mamut ASA

Autonomy Corp. PLCAveva corp

Software AG

Microsoft Corp.

Oracle Corp.

SAP AG (ADS)

Intuit Inc.R² = 0.2365

8x

10x

12x

14x

16x

18x

20x

22x

0% 5% 10% 15% 20% 25%

UFC

F m

ultip

le 2

010

2009–2011 revenue CAGR

47 Source: Consensus estimates as of 04 June 2010. Note: TeamSystem growth based on TeamSystem management guidance. Unit4, Cegid, and IFS

omitted due to one-time, abnormal net income growth. UFCF defined as (1- marginal tax rate) x EBIT + D&A – CapEx.

TeamSystem Case Study: Preliminary TeamSystem

Summary Valuation

Low: median of European ERP comps

High: 20% premium to Sage, as suggested by superior growth / margin profile relative to European ERP peer group

Company Business Plan elaborated on Company Management Plan up to

2014E. Extrapolations from 2015E to 2020E

Long-term EBITDA margin of c.42%

Theoretical tax rate at 31.4% over the projected period (IRES + IRAP)

Valuation assumptions

WACC in the 9.0%–10.0% range

Perpetuity growth rate in the 1.0%–2.0% range

Low: Skillsoft transaction

Most recent similar transaction

Low / negative growth for Skillsoft suggests TS should be priced

above this

High: Median EV/EBITDA of announced software transactions since March

Low: implied EV to get a 25% target IRR at year 4 (assuming exit at 10.0x

EV/EBITDA 2014E of €85m)

High: implied EV to get a 20% target IRR at year 5 (assuming exit at 11.0x

EV/EBITDA 2015E of €90m)

Comments

M&

A V

alu

ati

on

T

rad

ing M

ult

iple

s D

CF

Valu

ati

on

Implied

EV/EBITDA

’10E

Enterprise Value Methodology

(€m)

6.3x–11.0x

8.1x–11.4x

10.7x–11.9x

FY1 EV/EBITDA –

(CY 10E pro forma

EBITDA: €50m)

DCF Valuation

Precedent Transactions

LBO Valuation

8.4x–11.4x

FY1 EV/(EBITDA minus

capex) – (CY 10E pro forma

EBITDA minus capex:

€47m)

FY1 EV/UFCF– (CY 10E

pro forma UFCF €35m)

12.4x–13.7x

9.3x–12.4x

Same methodology as above

Same methodology as above

Implied

EV/(EBITDA-

capex) ’10E

6.7x–11.7x

8.6x–12.1x

11.3x–12.4x

8.8x–12.0x

13.2x–14.6x

9.9x–13.2x

Implied

EV/UFCF

’10E

9.0x–15.8x

537

464

625

406

418

315

601

620

692

571

570

552

250 450 650 850

€250 €500 €750

11.6x–16.3x

15.4x–16.9x

11.9x–16.3x

18.0x–19.9x

13.3x–17.7x

€565m, value paid by HgCapital for the acquisition

of TeamSystem in August 2010

48 Note: Assumes valuation date as of 31-Dec-2010

49

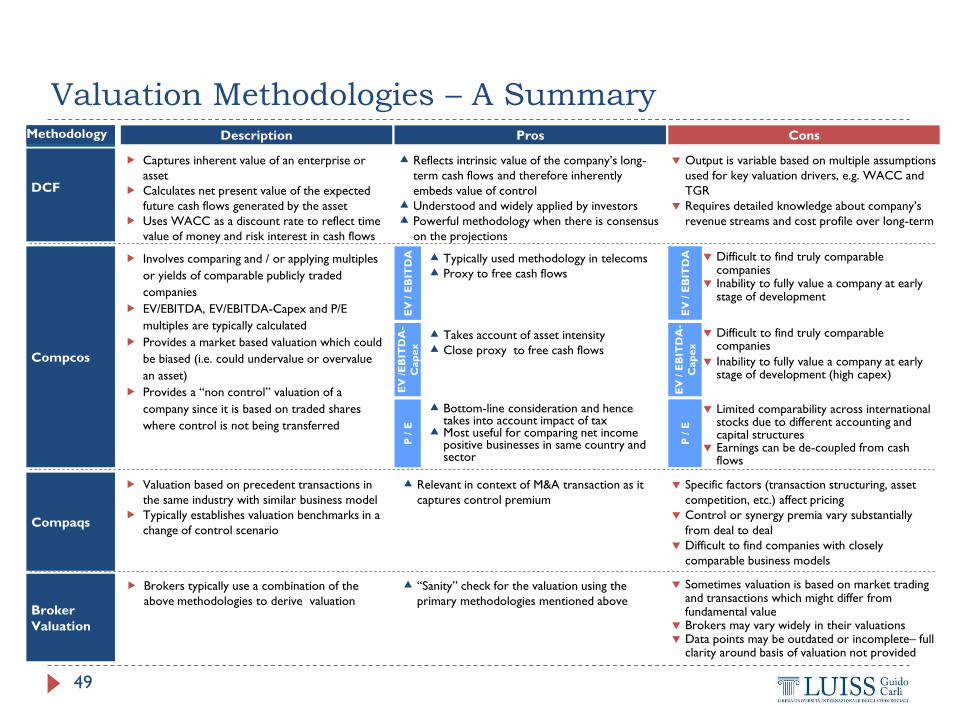

Valuation Methodologies – A Summary Methodology

Broker

Valuation

“Sanity” check for the valuation using the

primary methodologies mentioned above

Sometimes valuation is based on market trading and transactions which might differ from fundamental value

Brokers may vary widely in their valuations Data points may be outdated or incomplete– full

clarity around basis of valuation not provided

Takes account of asset intensity

Close proxy to free cash flows

Difficult to find truly comparable companies

Inability to fully value a company at early stage of development (high capex)

DCF

Reflects intrinsic value of the company’s long-

term cash flows and therefore inherently

embeds value of control

Understood and widely applied by investors

Powerful methodology when there is consensus

on the projections

Output is variable based on multiple assumptions

used for key valuation drivers, e.g. WACC and

TGR

Requires detailed knowledge about company’s

revenue streams and cost profile over long-term

Compaqs

Relevant in context of M&A transaction as it

captures control premium

Specific factors (transaction structuring, asset

competition, etc.) affect pricing

Control or synergy premia vary substantially

from deal to deal

Difficult to find companies with closely

comparable business models

Typically used methodology in telecoms

Proxy to free cash flows

Difficult to find truly comparable companies

Inability to fully value a company at early stage of development

Compcos

Bottom-line consideration and hence takes into account impact of tax

Most useful for comparing net income positive businesses in same country and sector

Limited comparability across international stocks due to different accounting and capital structures

Earnings can be de-coupled from cash flows

Captures inherent value of an enterprise or

asset

Calculates net present value of the expected

future cash flows generated by the asset

Uses WACC as a discount rate to reflect time

value of money and risk interest in cash flows

Involves comparing and / or applying multiples

or yields of comparable publicly traded

companies

EV/EBITDA, EV/EBITDA-Capex and P/E

multiples are typically calculated

Provides a market based valuation which could

be biased (i.e. could undervalue or overvalue

an asset)

Provides a “non control” valuation of a

company since it is based on traded shares

where control is not being transferred

Brokers typically use a combination of the

above methodologies to derive valuation

Valuation based on precedent transactions in

the same industry with similar business model

Typically establishes valuation benchmarks in a

change of control scenario

EV

/E

BIT

DA

-

Cap

ex

EV

/ E

BIT

DA

P

/ E

EV

/ E

BIT

DA

E

V / E

BIT

DA

-

Cap

ex

P / E

Cons Pros Description

50

Valuation Approach Relevance

Applied valuation methodologies will focus on DCF and IRR, depending on the nature of the potential buyers

Intrinsic valuation; discounts expected future cash flows

Allows fundamental view on input assumptions

Allows to implement sensitivities on pipeline execution

Comments Valuation

methodology

Precedent transactions can be used as reference during transactions

Allows to incorporate control premium in valuation

Can be used as a relative benchmark to understand if price offered is in

line with market valuation of similar assets

Relatively easy application for equity investors

Focus on roll-forward EV / EBITDA and EV / EBIT multiples

Relevant methodology for financial investors

Influenced by credit market conditions and access to credit of each single

bidder

Depending on the nature of the investor will encompass a different time

period and target IRR

Comparable

Acquisitions

Comparable

Companies

IRR Analysis

DCF

2

3

4

1

Relevance

Financial

Buyer

Industrial

Buyer IPO

Pri

mary

meth

od

olo

gy

Valu

ati

on

Su

pp

ort

M&A and Investment Banking

Lesson 5.2 – How can M&A create value?

51

Does M&A Pay? Findings about the Drivers of M&A

Profitability

52

Diversification destroys value. Focus conserves it. Berger and Ofek (1995) found an average loss in value from diversification of between 13-15%. The degree of relatedness between the businesses of the buyer and seller is positively associated with returns. Intuitively, this makes sense if synergies or savings arise from the economics of the two firms. In particular, conglomerate deals (unrelated lines of business) are associated with the poorest returns. Diversifying (unrelated) mergers tend to be associated with worse performance than related mergers. Maquieira et al. (1998) found negative, but insignificant returns to buyers in conglomerate deals; in contrast, they found positive and significant returns to buyers in non-conglomerate deals. In a study of bank mergers, DeLong (2001) found that mergers that focus both activity and geography enhance buyer’s share value by 2 to 3% more than other types of mergers.

Expected synergies are important drivers of the wealth creation through merger. Houston, James and Ryngaert (2001) studied the association of forecasted cost savings and revenue enhancements in bank mergers and found a significant relationship between the present value of these benefits, and the announcement day returns. The market appears to discount the value of these benefits, however, and applies a greater discount to revenue-enhancing synergies, and a smaller discount to cost-reduction synergies.

Value acquiring pays, glamour acquiring does not. Rau and Vermaelen (1998) found that post-acquisition underperformance by buyers was associated with “glamour” acquirers (companies with high book-to-market value ratios). Value-oriented buyers (low book-to-market ratios) outperform glamour buyers. Value acquirers earn significant abnormal returns of 8% in mergers, and 16% in tender offers, while glamour acquirors earn a significant -17% in mergers and insignificant +4% in tender offers.

M&A to build market power does not pay. Studies by Ravenscraft and Scherer (1987), Mueller (1985), and Eckbo (1992) reveal that efforts to enhance market position through M&A yield no better performance, and sometimes worse. Studies by Stillman(1983) and Eckbo (1983) find that share price movements of competitive rivals of the buyer do not conform to increases in market power by buyers. It suggests that the sources of gains from M&A do not derive from anticompetitive combination of firms.

Bruner, 2004. Applied Mergers and Acquisitions. Wiley Finance: chapters 3, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=286054

Does M&A Pay? Findings about the Drivers of M&A

Profitability (Cont’d)

53

Paying with stock is costly; paying with cash is neutral. Asquith, Bruner and Mullins (1987), Huang and Walkling (1987), Travlos (1987) and Yook (2000) found that stock-based deals are associated with significantly negative returns at deal announcements, whereas cash deals are zero or slightly positive. This finding is consistent with theories that managers time the issuance of shares of stock to occur at the high point in the cycle of the company’s fortunes, or in the stock market cycle. Thus, the announcement of the payment with shares (like an announcement of an offering of seasoned stock) could be taken as a signal that managers believe the firm’s shares are overpriced.

M&A regulation is costly to investors. Weir (1983) and Eckbo (1983) find evidence suggesting that US Federal Trade Commission antitrust actions benefit competitive rivals of the buyer and target. Schipper and Thompson (1983) consider four regulatory changes between 1968 and 1970, and found wealth-reducing effects associated with increased regulation.

M&A to use excess cash generally destroys value except when redeployed profitably. Cash-rich firms have a choice of returning the cash to investors through dividends, or reinvesting it through such activities as M&A. Studies report value destruction by the announcement of M&A transactions by firms with excess cash. However, Bruner (1988) reports that the pairing of slack-poor and slack-rich firms creates value. Before merger, buyers have more cash and lower debt ratios than non-acquirers. And the return to the buyers’ shareholders increases with the change in the buyer’s debt ratio due to the merger.

Tender offers create value for bidders. Mergers are typically friendly affairs, negotiated between the top management of buyer and target firms. Tender offers are structured as take-it-or-leave-it proposals, directly to the target firm shareholders. Quite often, tender offers are unfriendly. Research suggests that bypassing the target firm’s management, and appealing directly to target shareholders can pay. Several studies report larger announcement returns to bidders in tender offers, as compared with friendly negotiated transactions. These findings are consistent with the view that unwanted suitors are entrepreneurs who have uncovered special value-creating insights about the target firm. By making an unsolicited bid, the buyer seeks to retain value for itself, rather than give it up in a negotiation.

Bruner, 2004. Applied Mergers and Acquisitions. Wiley Finance: chapters 3, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=286054

Does M&A Pay? Findings about the Drivers of M&A

Profitability (Cont’d)

54

When managers have more at stake, more value is created. Studies suggest that returns to buyer firm

shareholders are associated with larger equity interests by managers and employees. In assessing the

pattern of performance associated with deal characteristics, Healey, Palepu and Ruback (1997) concluded

“while takeovers were usually break-even investments, the profitability of individual transactions varied

widely…the transactions characteristics that were under management control substantially influenced the

ultimate payoffs from takeovers.” A related finding is that LBOs create value for buyers. The sources of

these returns are not only from tax savings due to debt and depreciation shields, but also significantly from

efficiencies and greater operational improvements implemented after the LBO. In LBOs, managers tend to

have a significant portion of their net worth committed to the success of the transaction. Several studies

about LBOs reveal that cash flow increases, and capital spending declines materially in the years following

the transaction.

The initiation of M&A programs is associated with creation of value for buyers. Asquith, Bruner and Mullins

(1983), Gregory (1997), and Schipper and Thompson (1983) report that when firms announce they are

undertaking a series of acquisitions in pursuit of some strategic objectives, their share price rises

significantly. That these kinds of announcements should create value suggests that M&A generally creates

value, and that the announcement is taken as a serious signal of value creation.

Bruner, 2004. Applied Mergers and Acquisitions. Wiley Finance: chapters 3, available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=286054

References

55

Bruner, 2004. Applied Mergers and Acquisitions. Wiley Finance: chapters 3(1),

9, 11,12

Damodaran, 2012. Investment Valuation: Tools and Techniques for

Determining the Value of Any Asset.Wiley Finance

Damodaran web site: http://pages.stern.nyu.edu/~adamodar

Fleuriet, 2008. Investment banking explained. McGraw-Hill: chapters 16

Rosenbaum, J. and Pearl, J., 2009. Investment banking : valuation, leveraged

buyouts, and mergers & acquisitions.Wiley: chapters 1,2,3

UBS Global Equity Research, 2001. Valuation Multiples: A Primer

Note: (1) Available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=286054