management 3 quantitative methods the time value of money part 2b present value of annuities revised...

TRANSCRIPT

Management 3Quantitative Methods

The Time Value of MoneyPart 2b

Present Value of AnnuitiesRevised 2/18/15

w/ Solutions to Quiz #6

New Scenario

We can trade a single sum of money today, a

(PV)

in return for a series of periodic future

payments (FV’s).

This is what a Loan is …

• Borrow (Lend) today a large single amount) and

make (payments) or receive payments in the

future to repay the Loan or recover the Loan.

Annuities, again• An annuity is a “fixed” periodic payment

or deposit:• These payments that are made at the end

of the financing period are called “Ordinary” Annuities.

• This is the only type of payment that we will consider in this section of the course.

• If you borrow (take a mortgage), you agree to pay an Ordinary Annuity because your 1st payment is not due the day you borrow, but one month later.

The PV of an AnnuityIn the Slides TVM 2a, we calculated the FV of $10,000/year for 5 years at 5 percent and found that that future value was $55,256, i.e. we calculated:

$A x FVFA(r, t) = $FV$10,000 x [[1-(1+r) t -1] /r ] = $FV

$10,000 x 5.5256 = $ 55,256

Let’s reverse this process by asking - what is the PV of $10,000/year for 5 years at 5 percent?

It will be < $50,000 because each of the five $10,000 installments are paid in the future, so they need to be discounted.

Calculate the PV of each $10,000 payment by using Table 2 and taking the PVF’s from the 5% column down to 5 years.

Interest = r 5.00%

Periods = t

PVFs Installments Present Value

1 0.9524 $ 10,000 $ 9,524

2 0.9070 $ 10,000 $ 9,070

3 0.8638 $ 10,000 $ 8,638

4 0.8227 $ 10,000 $ 8,227

5 0.7835 $ 10,000 $ 7,835

4.329 $ 43,295

Table 2 applied to the $10,000 installments.

The PV of an AnnuityRather than run the sum of five products, we can factor-out the $10,000 and sum the PVFs, then find the product.

= $10,000 x ( (1.05)-t ) for t=1 to 5

= $10,000 x PFVA (r=5%, t=5)

= $10,000 x 4.329 from Table 4

= $43,295

Present Value Annuity Factors

Table 4is constructed using this formula

Each Factor, called a PVFA, is defined by its rate “r” and its time in years “t”:

PVFA(r, t) = [ 1- PVF(r, t)] /rPVFA(r, t) = [[1-(1+r) -t] /r ]

These are called Present Value Factors of Annuities and are found on the PVFA Table 4

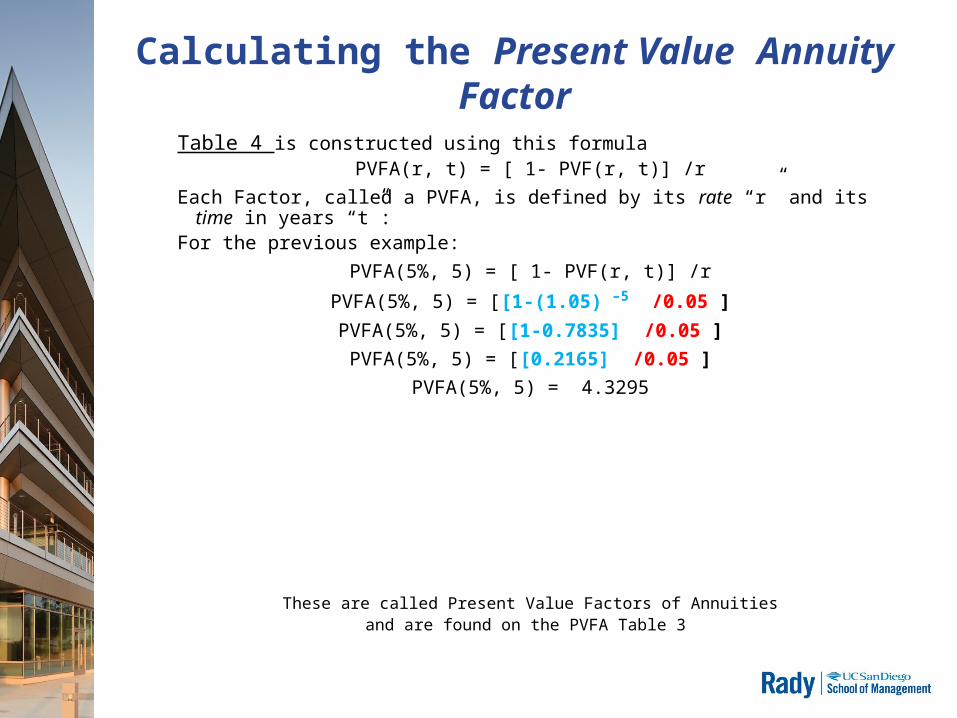

Calculating the Present Value Annuity Factor

Table 4 is constructed using this formulaPVFA(r, t) = [ 1- PVF(r, t)] /r

Each Factor, called a PVFA, is defined by its rate “r” and its time in years “t”:

For the previous example:

PVFA(5%, 5) = [ 1- PVF(r, t)] /r

PVFA(5%, 5) = [[1-(1.05) –5 /0.05 ]

PVFA(5%, 5) = [[1-0.7835] /0.05 ]

PVFA(5%, 5) = [[0.2165] /0.05 ]

PVFA(5%, 5) = 4.3295

These are called Present Value Factors of Annuities

and are found on the PVFA Table 3

The PV of an AnnuityThe present value of an annuity is the Annuity x the PVFA(r, t).

In our first example it is:

= $10,000 x PVFA(5%,5)

= $10,000 x 4.329 where we find 4.329

by calculating it or looking on Table 4

= $43,295

The PV of an Annuity in Reverse

In the prior example, we found that the PV of a 5 year $10,000 ordinary annuity at 5% is $43,295. Reversing that, let’s ask:What is the FV of a 5 year $10,000 ordinary annuity at 5%?Formulate it:FV(Annuity) = Annuity x FVFA(5%, 5)FV(Annuity) = $ 10,000 x 5.5256 FV (A =$10,000) = $ 55,526

The PV of an Annuity in Reverse

What do we have now?•We have a Present Value of $ 43,295.•We have a Future Value of $ 55,256. •These are linked by 5 years?•What is the CAGR that bring the two values and the term of 5 years in line?Formulate this:

The CAGR = [(FV/PV)^(1/5)] -1CAGR = [(55,256/43,295)^0.20] -1

CAGR = [(1.276)^0.20]-1CAGR = 1.05 -1 = 5 percent

A Car Loan

You want to purchase a new car. You find the car and negotiate a price,

$35,000 all-in. You make a $5,000 down payment and

borrow the remaining $30,000 from your credit union at 6% over 4 years.

What is a good approximation for your monthly payment?

Car LoanLet’s find your annual payment – just

as we did earlier - and divide by twelve (months).

• You are borrowing a PV = $30,000.• You will pay-back this $30,000 PV with a

4 year 6% ordinary annuity. • The PV of your four annual payments

must be equal to $30,000. That is …. And this is IMPORTANT.

• You must return the same PV that you borrowed.

Car Loan• You must return the same PV that

you borrowed.• This means that the annual payments

will be somewhat greater than $ 7,500, which is $30,000 / 4.

• In other words, because you will be paying-off the loan with future dollars, the lender will need more than $30,000 of them.

• If you understand this, corporate finance is in your hands.

Formulation

PVFA’s transform a series of future payments or deposits into a Present Value.

Annuity x PVFA (r, t) = Present ValueAnnuity = PV / PVFA(r, t)Annuity = PV / [[1-(1+r) -

t] /r ]

Annual Payment = $30,000 / PVFA(6%, 4)

Car Loan Example, con’t

Here is the formula we need to solve:Payment = $30,000 / PVFA(6%, 4)

Go to Table 4 and find the Factor at 4 and 6%.Present Value of $1 Annuity Table of Factors

1.00% 2.00% 3.00% 4.00% 5.00% 6.00%

Periods

1 0.9901 0.9804 0.9709 0.9615 0.9524 0.9434

2 1.9704 1.9416 1.9135 1.8861 1.8594 1.8334

3 2.9410 2.8839 2.8286 2.7751 2.7232 2.6730

4 3.9020 3.8077 3.7171 3.6299 3.5460 3.4651

Car Loan Example, con’tInsert the PVFA(6%, 4) = 3.4651 into the

formula: Annual Payment x 3.4652 = $30,000Annual Payment = $30,000 / 3.4652

$ 8,657.74 = $30,000 / 3.4652

This means that an approximation of your monthly payment is:

$ 8,657.74 / 12 = $ 721.48

Car Loan Example proves that

1) The Loan Payments on the 4 year 6% $30,000 loan are $ 8,657.74 per year, and

2) $ 8,657.74 per year are the annual future payments that return a present value of $30,000 @ 6%.

3) Thus, the loan payments are the present value of a $30,000 loan meaning the Lender gets $30,000 of present value from four future payments of $ 8,658 each.

4) Therefore, if our calculations are correct, the Lender should be indifferent between:

a) lending to you at 6% for 4 years;b) putting the $30,000 in the bank at 6%.Let’s check this ….

We will compare: 1) the Lender’s Future Value of a single $30,000 deposited for 4 years @6% and 2) the Future Value of $ 8,658 per year for 4 years @6%.

Bear in mind that someone with $30,000, and a 4 year investment horizon, has two choices: (a) put it all in the bank earning 6% per year, or (b) or lend it to you for 4 years expecting 4 annual payments.

Comparing the Lender’s two choices are no different in Future Value:

FV Factors

$30,000 in the Bank

Compound-ing

Pay-ments

Payments Compounded

0 1.0000 30,000 0 0

1 1.0600 31,800 8,658 8,658

2 1.1238 33,708 8,658 9,177

3 1.1910 35,730 8,658 9,727

4 1.2625 37,874 8,658 10,311

Total 37,874

4th payment

3rd payment

2nd payment

1st payment

Future Value of all four Payments

Choice (a) Choice (b)

Quiz #61. Calculate, showing all work, the CAGR

for a $30,000 investment that returns $37,874 in 4 years.

2. Calculate, showing all work, the CAGR on a $30,000 investment that pays $ 8,658 per year (ordinary annuity) for 4 years in a 6 percent world.

3. Calculate, showing all work, the future value of a 4 year, $ 8,658 ordinary annuity at 6 percent.

Quiz #61. Calculate, showing all work, the CAGR

for a $30,000 investment that returns $37,874 in 4 years.

FormulaCAGR = [(FV / PV)(1/t)]-1Data CAGR = [(37,874 / 30,000)

(1/4)]-1Calculate CAGR = [(1.2625)(0.25)]-1 =

1.059-1 CAGR = 6%

Quiz #62. Calculate, showing all work, the CAGR on a $30,000 investment that pays $ 8,658 per year (ordinary annuity) for 4 years in a 6 percent world.

Formula CAGR = [($A x FVFA) / PV)(1/t)]-1Data CAGR = [(37,874 / 30,000)(1/4)]-1Calculate CAGR = [(1.2625)(0.25)]-1 = 1.059-1

CAGR = 6%

Quiz #63. Calculate, showing all work, the future value of a 4 year, $ 8,658 ordinary annuity at 6 percent.

Formula FV($A=10,000) = $A x FVFA(6%, 4)Data FV($A) = $ 8,658 x 4.3746Calculate FV(A= 8,658) = $37,874

Analysis of Car Loan Example

Your approximate monthly payment on the 48 month, 6%, $ 30,000 car loan is

$ 721.48.

Annuities w/ Monthly Compounding

To get a more precise calculation for the car loan payment, we need to make some adjustments to the basic formula.

= $ 30,000 / PVFA (r /12, t x12)= $ 30,000 / PVFA (0.005, 48)= $ 30,000 / [1- (1.005) -48] / 0.005 = $ 30,000 / [1- 0.7870] / 0.005 = $ 30,000 / 0.2130 / 0.005= $ 30,000 / 42.58= $ 704.55 per month

Some Observations• The monthly payment calculated w/ adjusted, i.e. more precise, parameters:

4 years x 12 months = 48 months, and 6%/12 = 0.5% interest

is smaller than the approximate payment.• How many total dollars will be paid in consideration of this loan?

You will pay 48 x $ 704.55 = $ 33,818 •What are the financing costs, i.e. the interest your will pay on the loan?

Interest = Total paid less Principal$ 3,818 = $ 33,818 - $ 30,000

Formulation Review

PVFA’s transform a series of future payments or deposits into a Present Value.

Annuity x PVFA (r, t) = Present Value

Deposit x [ 1- PVF(r, t)] /r] = Present Value

Payment x [[1-(1+r) -t] /r ] = Present Value

Formulation & Transformation

• We know how much we want to borrow – the $PV and • We know how many years or months “t” we’d like to have to pay it back

and •The market gives us the “r”So•What are our loan payments?

Use this: Payment x PVFA(r, t) = LoanThus:

Payment = Loan / PVFA(r, t)