management accounting and supply chain performance of

TRANSCRIPT

UNIVERSITY OF GHANA

(College of Humanities)

Management Accounting and Supply Chain Performance of Healthcare

Institutions in Ghana

Nartey Edward

(10072443)

This thesis is submitted to the University of Ghana, Legon in partial fulfilment of the

requirement for the award of PhD Accounting degree

JUNE, 2018

University of Ghana http://ugspace.ug.edu.gh

i

DECLARATION

I, the undersigned, do hereby declare that this work is the result of my own research and has

not been presented by anyone for any academic award in this university or any other university.

All references used in the work have been fully acknowledged. I bear responsibility for any

shortcomings.

………………………………………… ……….………………….

NARTEY EDWARD DATE

University of Ghana http://ugspace.ug.edu.gh

ii

CERTIFICATION

I, the undersigned, do hereby certify that this thesis was supervised in accordance with the

procedures laid down by the university.

……………………………………………… …….………………

DR. FRANCIS ABOAGYE-OTCHERE DATE

……………………………………………… …….………………

DR. SAMUEL NANA YAW SIMPSON DATE

University of Ghana http://ugspace.ug.edu.gh

iii

DEDICATION

I dedicate this work to my two lovely boys: Nana and June

University of Ghana http://ugspace.ug.edu.gh

iv

ACKNOWLEDGEMENTS

Completing a major research effort would be virtually impossible without getting the energy

and strength given from above. First of all, I thank the almighty God for giving me the strength

to successfully complete this project. This project also couldn’t have seen the light without the

support and assistance from a number of special people. I especially appreciate the assistance

and insight from my supervisors Dr. Francis Aboagye-Otchere and Dr. Samuel Nana Yaw

Simpson who in diverse ways were invaluable in helping me progress through the various

iterations. I was always impressed about how responsive and focused they seem to be when I

need their input. Finally, I would like to express my profound gratitude to Professor Joshua

Abor, Dean of the Business School for his encouragement and support towards the successful

completion of this project.

University of Ghana http://ugspace.ug.edu.gh

v

TABLE OF CONTENTS

DECLARATION.................................................................................................................................... i

CERTIFICATION ................................................................................................................................ ii

DEDICATION...................................................................................................................................... iii

ACKNOWLEDGEMENTS ................................................................................................................ iv

TABLE OF CONTENTS ..................................................................................................................... v

LIST OF TABLES ............................................................................................................................... xi

LIST OF FIGURES ............................................................................................................................ xii

LIST OF ABBREVIATIONS ........................................................................................................... xiii

ABSTRACT ........................................................................................................................................ xiv

CHAPTER ONE ................................................................................................................................... 1

INTRODUCTION ................................................................................................................................. 1

1.1 Brief Overview of the Study ............................................................................................ 1

1.2 Research Background ....................................................................................................... 2

1.3. The Research Problem .................................................................................................... 5

1.4 Study Objectives ............................................................................................................ 10

1.5 General Research Questions........................................................................................... 10

1.6 Significance of the Study ............................................................................................... 11

1.7 Outline of Remainder of Thesis ..................................................................................... 13

1.8 Chapter Summary ........................................................................................................... 13

CHAPTER TWO ................................................................................................................................ 15

CONTEXTUAL BACKGROUND, MANAGEMENT ACCOUNTING SYSTEM DESIGN AND

THE HEALTH SUPPLY CHAIN ..................................................................................................... 15

2.1. Introduction ................................................................................................................... 15

2.2. Recent Studies on MAS Design and Hospital SC Performance ................................... 16

2.3 Ghana’s Health SCM System ......................................................................................... 18

2.4 Managerial and Costing Systems in Ghana’s Healthcare Management ........................ 20

2.5. Reforms in the Health Logistics and Commodity Management System ...................... 21

2.6 The Health Supply Chain ............................................................................................... 27

2.6.1 Elements of the Health Supply Chain ................................................................................... 29

2.6.2 SCM in Healthcare Context .................................................................................................. 30

2.6.3 Minimizing Health Supply Chain Cost ........................................................................ 32

2.7 Nature of MAS Design ................................................................................................... 32

2.8 Functions of the MAS Information in Healthcare Management .................................... 34

2.8.1 Costing Systems Design in Hospitals .................................................................................... 35

University of Ghana http://ugspace.ug.edu.gh

vi

2.8.2 Formal MAS Design in Health SCM Decisions ...................................................................... 36

2.8.3 Inter-Health Organizational Cost Management in Supply Chains ....................................... 37

2.9 Chapter Summary ........................................................................................................... 39

CHAPTER THREE ............................................................................................................................ 41

CONTINGENCY-BASED MANAGEMENT ACCOUNTING STUDIES .................................... 41

3.1 Introduction .................................................................................................................... 41

3.2 Theoretical Background of Contingency Fit .................................................................. 41

3.3 Contingency Fit Models ................................................................................................. 43

3.3.1 Cartesian vs. Configuration .................................................................................................. 43

3.3.2 Congruence vs. Contingency ................................................................................................ 45

3.4 Typology of Contingency Fit Models ............................................................................ 47

3.4.1 Selection Fit Models ............................................................................................................. 48

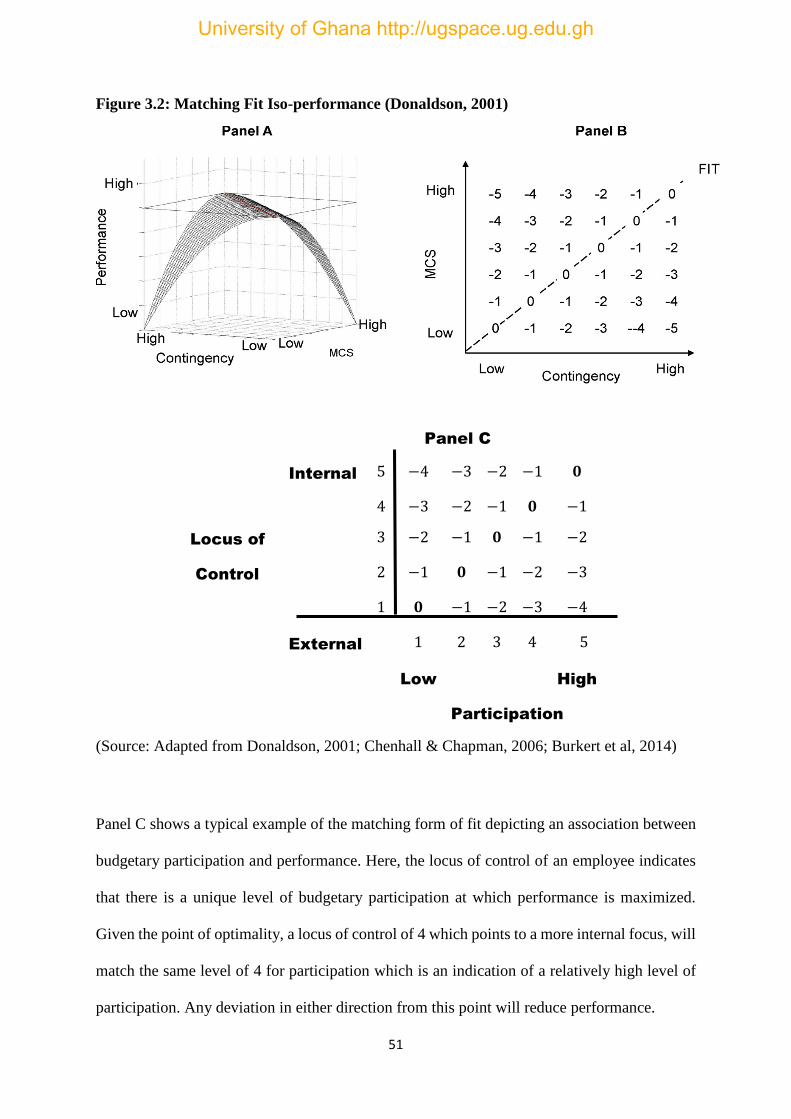

3.4.2 Matching Fit Models ............................................................................................................ 49

3.4.3 Interaction (Moderation) Fit Models .................................................................................... 52

3.4.4 Mediation Form of Fit .......................................................................................................... 55

3.5 Approaches to Testing Contingency Fit Models ............................................................ 56

3.5.1 Deviation Score and Residual Analysis Techniques .............................................................. 56

3.5.2 Approach to Testing Moderation Fit Models ....................................................................... 60

3.5.3 Approach to Testing Mediation Form of Fit Models ............................................................ 61

3.6 Conceptualization of Contingency Fit and its Attainment ............................................. 62

3.7 Levels of Contingency Fit Analysis ............................................................................... 64

3.8 Early Contingency-Based Management Accounting Studies ........................................ 65

3.9 Selection, Definition and Measurement of MAS Variables ........................................... 66

3.9.1 Arbitrary Selection of Variables ........................................................................................... 66

3.9.2 Empirical Estimation of Contingency Fit Models .................................................................. 70

3.10 Empirical Estimation of Moderation Forms of Fit ....................................................... 71

3.10.1 Hypotheses Formulation and Statistical Analysis .............................................................. 71

3.10.2 Strength of the Relationship .............................................................................................. 78

3.10.3 Lower-Order Effects ........................................................................................................... 79

3.10.4 Interaction and Effect Size ................................................................................................. 82

3.10.5 Multiple and Higher-Order Interaction .............................................................................. 84

3.11 The Use of Higher-Order of Abstraction Models in SEM ........................................... 86

3.12 Chapter Summary ......................................................................................................... 87

CHAPTER FOUR ............................................................................................................................... 89

THEORETICAL MODEL AND HYPOTHESES DEVELOPMENT ........................................... 89

4.1 Introduction .................................................................................................................... 89

University of Ghana http://ugspace.ug.edu.gh

vii

4.2 Theoretical Framework .................................................................................................. 89

4.2.1 Contingency Fit ..................................................................................................................... 90

4.3 Theoretical Foundation of Constructs ............................................................................ 96

4.3.1 Management Accounting Systems (MAS) ............................................................................ 96

4.3.2 Supply Chain Integration (SCI) ............................................................................................ 102

4.3.3 Hospital SC Performance .................................................................................................... 107

4.4 Formulation of Hypotheses .......................................................................................... 109

4.4.1 MAS Information and Hospital Supplier Partnerships ....................................................... 109

4.4.2 MAS Information and Hospital Supply Chain Integration (Internal Integration) ............... 112

4.4.3 MAS Information and Level of Information Exchange ....................................................... 114

4.4.4 MAS Information and Hospital Supply Chain Risk and Uncertainty ................................... 116

4.5. Mediating Role of MAS Information in Supply Chain Performance ......................... 118

4.5.1: MAS and Supplier Relations (External Integration) on Performance ................................ 118

4.5.2. MAS and Supply Chain Integration (Internal Integration) on Performance ...................... 121

4.5.3: MAS and Level of Knowledge Exchange on Performance ................................................. 122

4.5.4. MAS and Supply Chain Risk and Uncertainty on Performance ......................................... 123

4.6 Contingency Effect of the SCM Contextual Dimensions ............................................ 124

4.6.1. Supplier Relations (External Integration) to Performance ................................................ 124

4.6.2. Relationship of Internal Integration to Performance ........................................................ 125

4.6.3. Relationship of Level of Knowledge Exchange to Performance ........................................ 126

4.6.4. Relationship of Supply Chain Risk and Uncertainty to Performance................................. 127

4.7 Chapter Summary ...................................................................................................................... 128

CHAPTER FIVE .............................................................................................................................. 130

METHODOLOGY ........................................................................................................................... 130

5.1 Introduction .................................................................................................................. 130

5.2 The Study’s Philosophical Underpinning .................................................................... 131

5.3. Dimensions of Philosophical Assumptions ................................................................. 132

5.3.1. Ontology ............................................................................................................................ 132

5.3.2. Epistemology ..................................................................................................................... 133

5.3.3. Methodology ..................................................................................................................... 134

5.3.4. Axiology ............................................................................................................................. 134

5.4. Paradigms in Management Research .......................................................................... 135

5.4.1. Positivism .......................................................................................................................... 135

5.4.2. Social Constructivism ........................................................................................................ 136

5.4.3. Pragmatism ....................................................................................................................... 137

5.5. Paradigms in Accounting Research............................................................................. 138

University of Ghana http://ugspace.ug.edu.gh

viii

5.6. The Study’s Philosophical Stance ............................................................................... 139

5.7. Purpose and Design Strategies of the Survey.............................................................. 140

5.8 Survey Strategy ............................................................................................................ 143

5.9. Population, Sample and Sampling Procedure ............................................................. 143

5.9.1. Study Sample ..................................................................................................................... 145

5.9.2. Sampling Procedure .......................................................................................................... 145

5.9.3. Sample Size........................................................................................................................ 146

5.10. Approach to Data Collection ..................................................................................... 147

5.11. Scale Development and Measurements..................................................................... 148

5.12. Constructs and their Sources ..................................................................................... 149

5.13. The Modelling Process .............................................................................................. 151

5.14. Summary of Analysis Procedure ............................................................................... 152

6.15. Chapter Summary ...................................................................................................... 154

CHAPTER SIX ................................................................................................................................. 155

SURVEY ANALYSIS AND RESULTS .......................................................................................... 155

6.1 Introduction .................................................................................................................. 155

6.2 Preliminary Analysis of the Sample Data .................................................................... 156

6.3 Sample Characteristics ................................................................................................. 157

6.4 Assessment of Data for Normality ............................................................................... 159

6.4.1 Assessing Data for Multivariate Outliers ........................................................................... 162

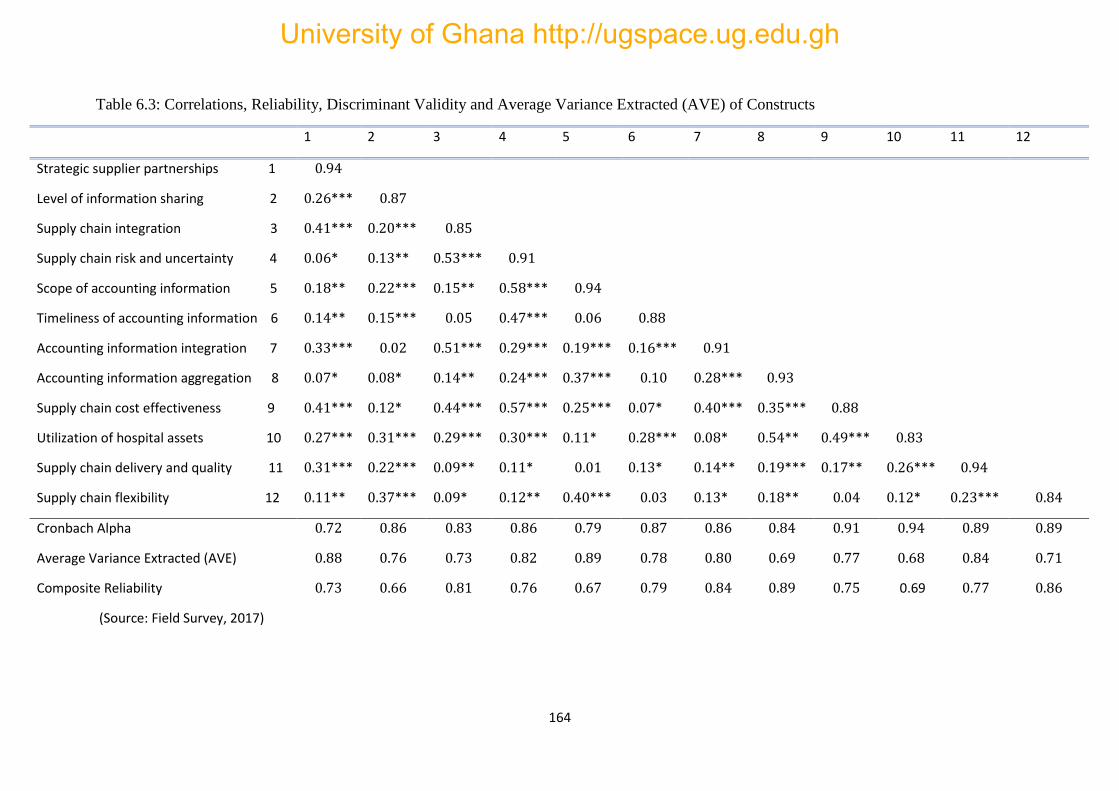

6.4.2 Correlation Analysis ........................................................................................................... 163

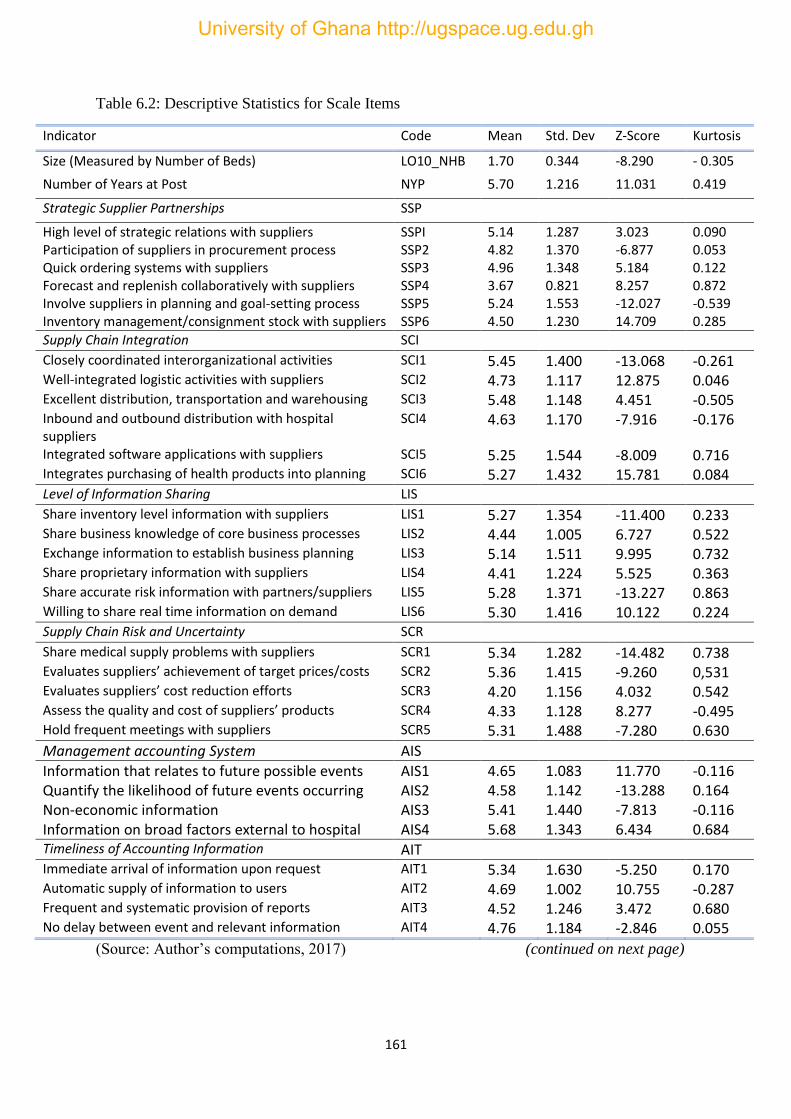

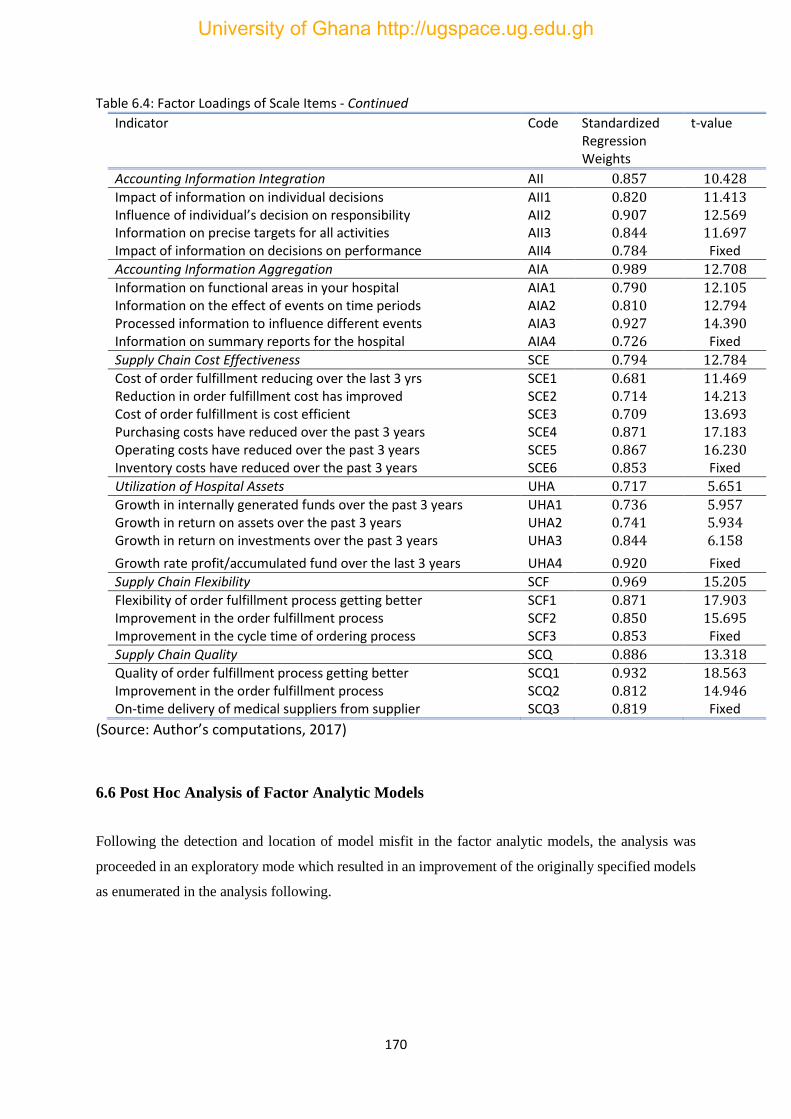

6.5 Measures of Reliability and Validity of Scale Items.................................................... 165

6.6 Post Hoc Analysis of Factor Analytic Models ............................................................. 170

6.6.1 Model 2 of the Factor Analytic Models .............................................................................. 172

6.6.2 Model 3 of the Factor Analytic Models .............................................................................. 172

6.7 Structural Model Specification..................................................................................... 175

6.7.1 Specification of the Hypothesized Model ........................................................................... 176

6.7.2 Identification of the Hypothesized Model .......................................................................... 178

6.8 Fitting the Hypothesized Model ................................................................................... 180

6.8.1 Statistical Significance ........................................................................................................ 180

6.8.2 Model Estimation Process .................................................................................................. 180

6.8.3 Structural Model Fitting Process ........................................................................................ 181

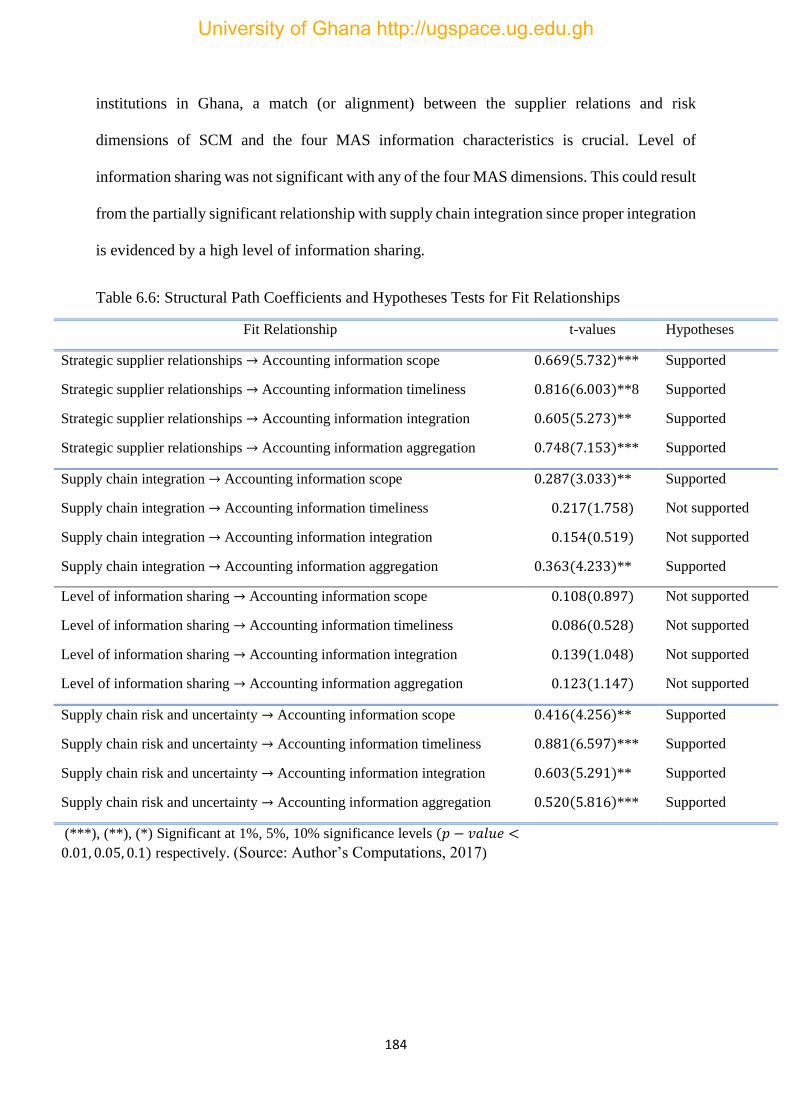

6.9 Hypotheses Tests of the Structural Model ................................................................... 181

6.10 Selection Fit Model – Test of H1 (a – d), H2 (a – d), H3 (a – d), and H4 (a – d) ...... 182

6.11 Mediating Effect of MAS Construct – Test of H5 (a) to H5 (d) ................................ 187

University of Ghana http://ugspace.ug.edu.gh

ix

6.11.1. Confounding Variables Effect .......................................................................................... 187

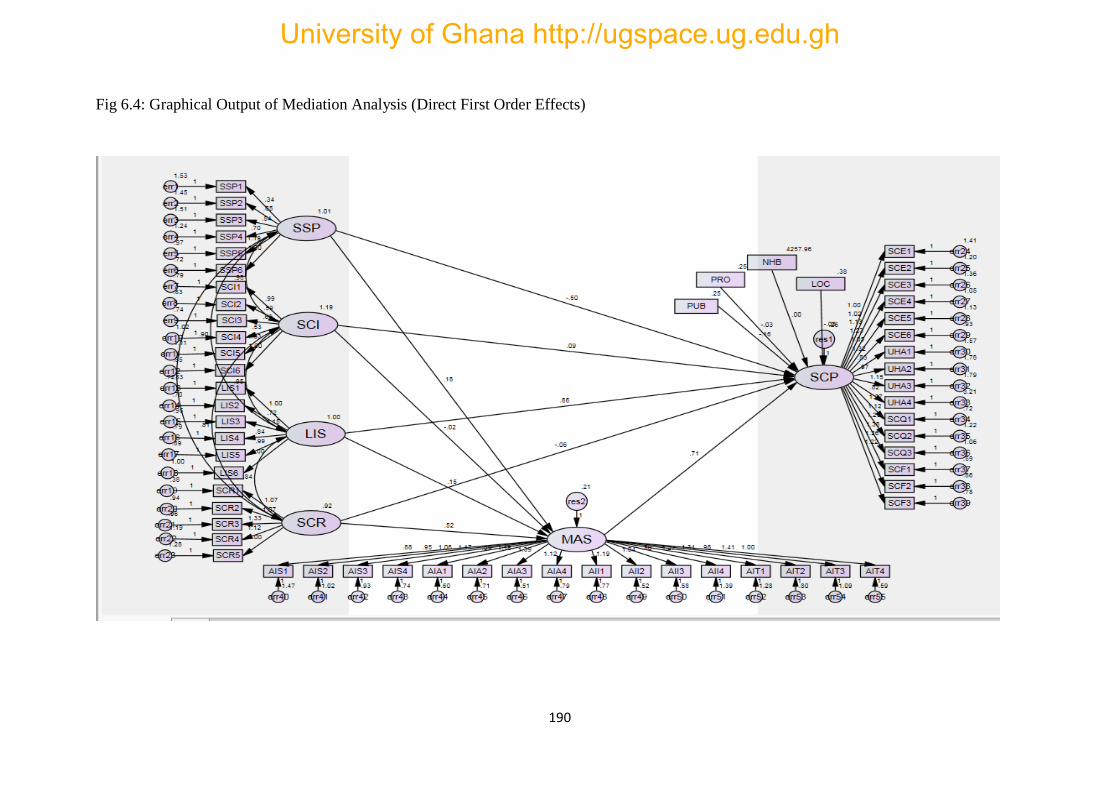

6.11.2 Mediation Effect of the MAS Construct............................................................................ 187

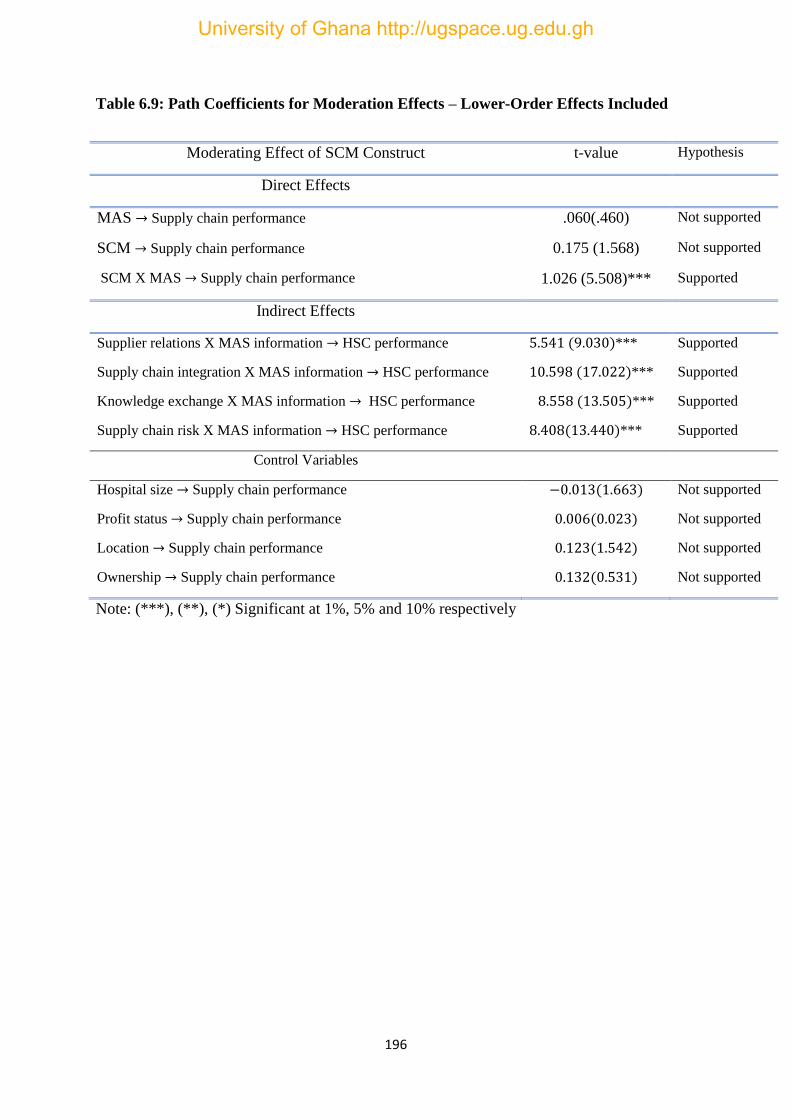

6.13 Moderating Effects of the SCM Constructs – Hypotheses H 6(a) – H 6(d) .............. 193

6.13.2 Inclusion of Lower-Order Effects ...................................................................................... 193

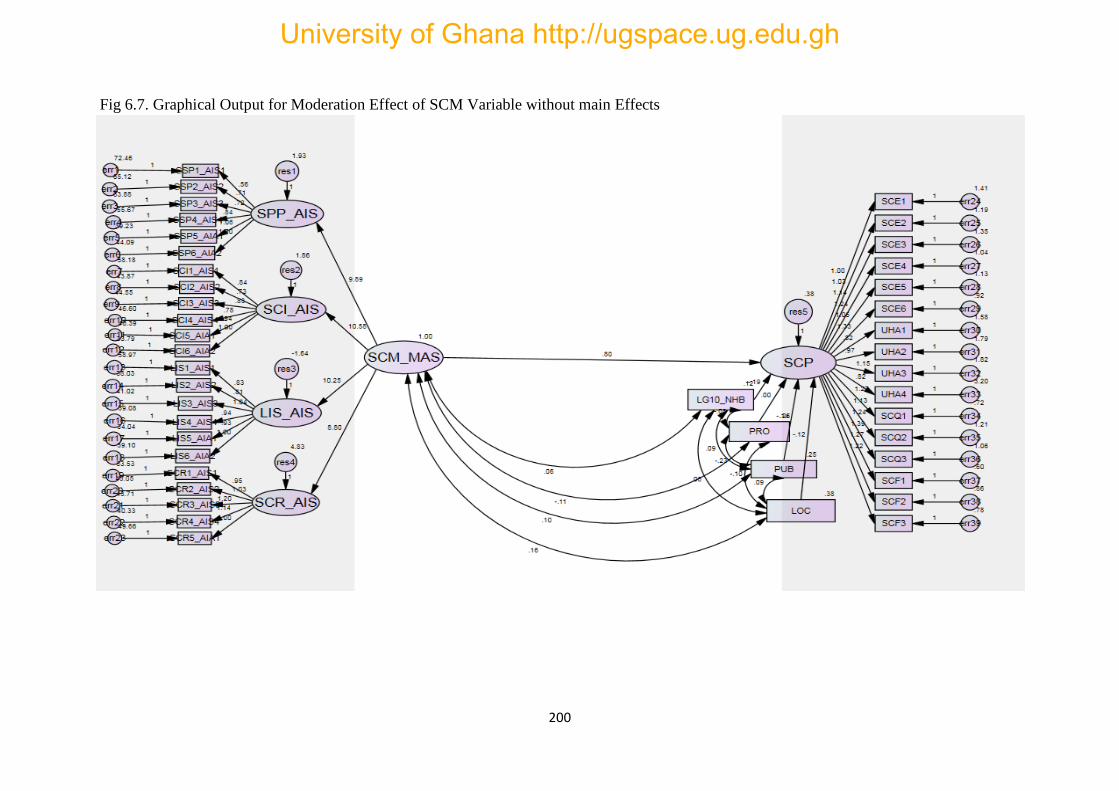

6.13.1 Exclusion of Lower-Order Effects...................................................................................... 198

6.14 Chapter Summary ....................................................................................................... 201

CHAPTER SEVEN ........................................................................................................................... 202

DISCUSSION AND INTERPRETATION OF FINDINGS .......................................................... 202

7.1 Introduction .................................................................................................................. 202

7.2 Recap of Research Objectives, Questions and Hypotheses ......................................... 202

7.2.1. Research Questions ........................................................................................................... 203

7.3 Fit between SCM and MAS Information Characteristics ............................................ 203

7.3.1 Strategic Supplier Partnerships (External Integration) and MAS Information ................... 204

7.3.2 Supply Chain Integration (Internal Integration) and MAS Information ............................. 206

7.3.3 Level of Information Sharing and MAS Information .......................................................... 207

7.3.4 Supply Chain Risk and Uncertainty and MAS Information ................................................. 208

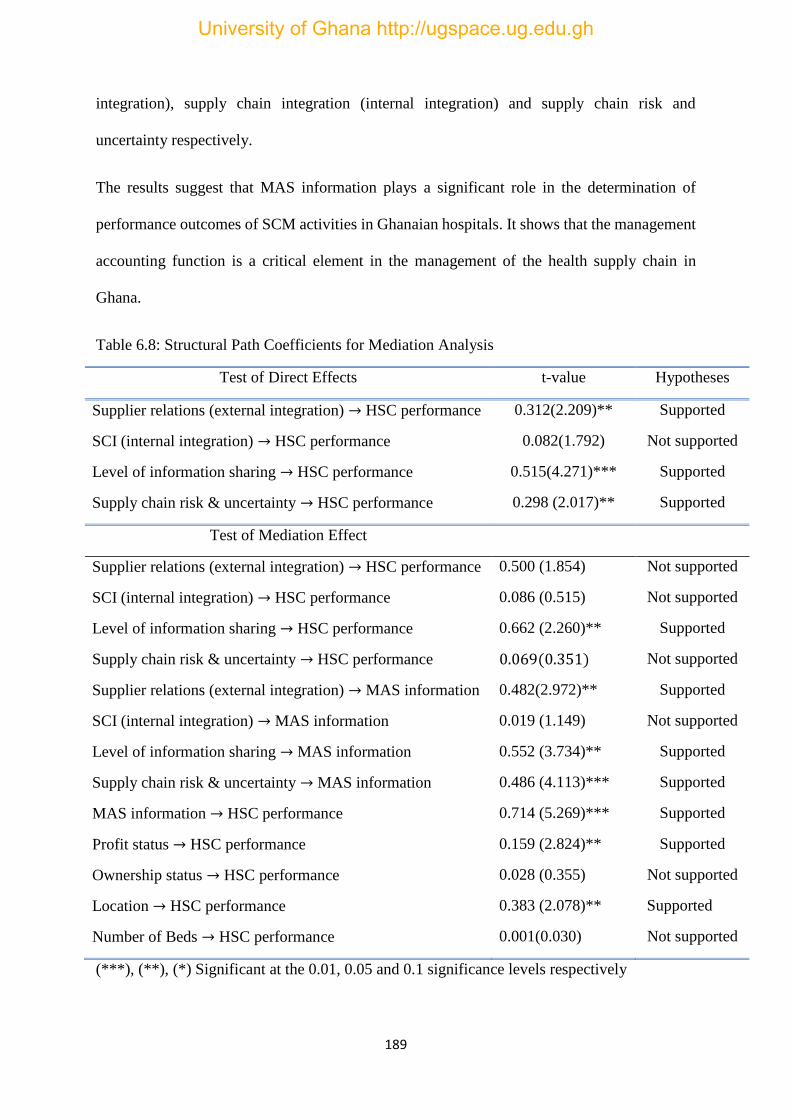

7.4 Interpretation of the MAS Mediation Effect ................................................................ 209

7.4.1 Confounding Variables and Hospital Supply Chain Performance ...................................... 209

7.4.2 Mediating Effect of MAS on Performance ......................................................................... 210

7.4.3 Joint Effect of MAS and SCM on Hospital SC Performance ................................................ 211

7.4.4 Mediating Role of the MAS Information Dimensions......................................................... 212

7.5. Contingency Effect of SCM on Performance ............................................................. 214

7.6 Implications of Findings............................................................................................... 215

7.6.1 Theoretical Implication ...................................................................................................... 216

7.6.2 Practical Implications ......................................................................................................... 216

7.6.3 Policy Implications .............................................................................................................. 218

7.7 Chapter Summary ......................................................................................................... 218

CHAPTER EIGHT ........................................................................................................................... 220

SUMMARY, CONCLUSIONS AND CONTRIBUTIONS ........................................................... 220

8.1 Introduction .................................................................................................................. 220

8.2 Summary of the Study .................................................................................................. 220

8.2.1 The Study’s Main Thrust ..................................................................................................... 220

8.2.2 The Study’s Main Findings.................................................................................................. 227

8.3 Conclusions .................................................................................................................. 230

8.4 Contributions of the Thesis .......................................................................................... 233

8.5. Recommendations ....................................................................................................... 235

University of Ghana http://ugspace.ug.edu.gh

x

8.6 Limitations of the Study ............................................................................................... 236

8.7 Future Research Directions .......................................................................................... 238

8.8 Chapter Summary ......................................................................................................... 239

REFERENCES ................................................................................................................... 240

Appendix A ........................................................................................................................ 262

Questionnaire for Hospital Accountants ............................................................................ 262

University of Ghana http://ugspace.ug.edu.gh

xi

LIST OF TABLES

Table 5.1 Ontology, Epistemology, Methodology, Axiology and Methods Distinguished 135

Table 5.2 Implications of Positivist Philosophical Assumptions 136

Table 5.3 Positivist and Social Constructionist Contrasted 137

Table 5.4 Relationship between Philosophical Assumptions and Paradigms 138

Table 5.5 Distribution of Samples by the Six Regions 147

Table 5.6 Constructs and their Sources of Measured 150

Table 5.7 Summary of Analysis Procedure 153

Table 6.1 Distribution of Hospitals in Terms of Ownerships, Profit Status and Location 158

Table 6.2 Descriptive Statistics for Scale Items 161

Table 6.3 Correlation Analysis, Reliability and Average Variance Extracted of Constructs 164

Table 6.4 Factor Loadings of Scale Items 169

Table 6.5 Post Hoc Analysis for Factor Analytic Models 171

Table 6.6 Structural Path Coefficients and Hypotheses Tests for Fit Relationships 184

Table 6.7 Summary of Goodness-of-Fit Tests for Structural Model 185

Table 6.8 Structural Path Coefficients for Mediation Analysis 189

Table 6.9 Path Coefficients for Moderation Effects – Lower-Order Effects Excluded 196

Table 6.10 Path Coefficients for Moderation Effects – Lower-Order Effects Included 199

University of Ghana http://ugspace.ug.edu.gh

xii

LIST OF FIGURES

Figure 1.1 Research Scope 1

Figure 1.2 Gaps Linking MAS, SCI and SCP 8

Figure 2.1 Ghana’s Health Supply Chain Management System 23

Figure 3.1 (a)-(b) Cartesian and Configuration Models 45

Figure 3.2 (a)-(c) Matching Fit Iso-performance 51

Figure 3.3 Moderation Fit Relationship 53

Figure 3.4 (a-(d) Non-Monotonic (Symmetrical) and Cross Over Interaction 54

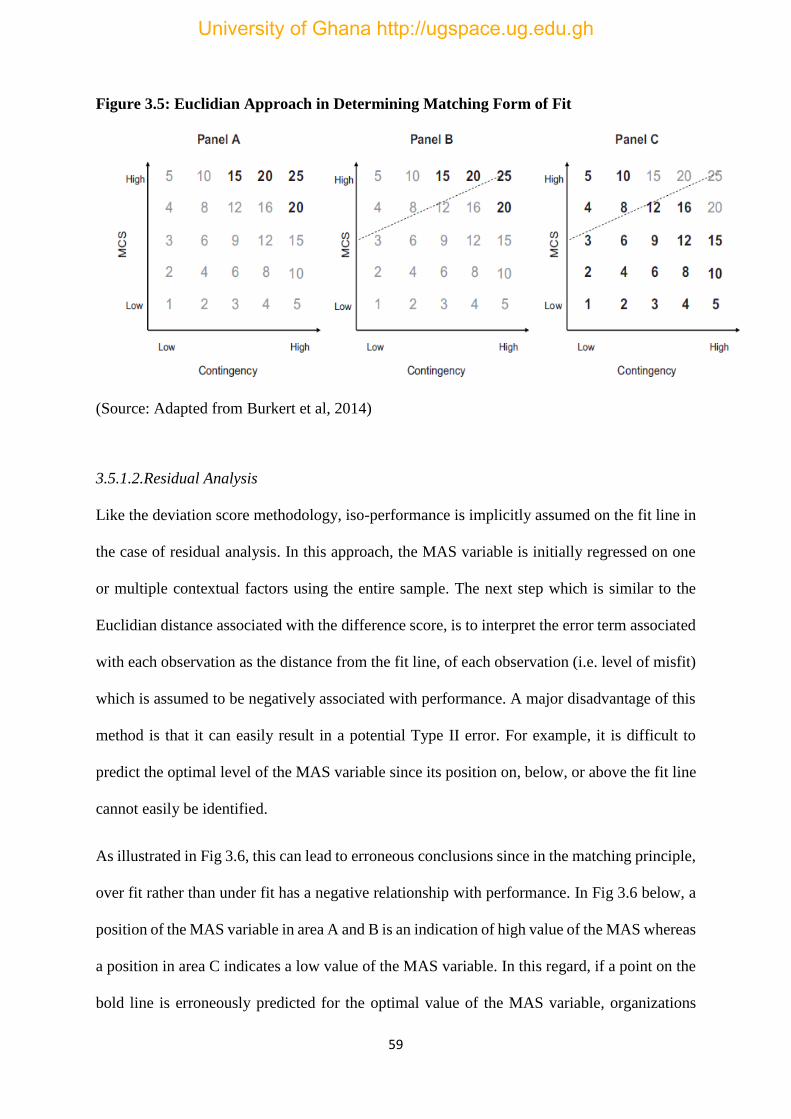

Figure 3.5 Euclidian Approach in Determining Matching Form of Fit 59

Figure 3.6 Potential Type II Error Associated with Residual Analysis 60

Figure 3.7 (a) Mediation Form of Fit Models 62

Figure 3.7 (b) Four Step Procedure for Testing Mediation Form of Fit 63

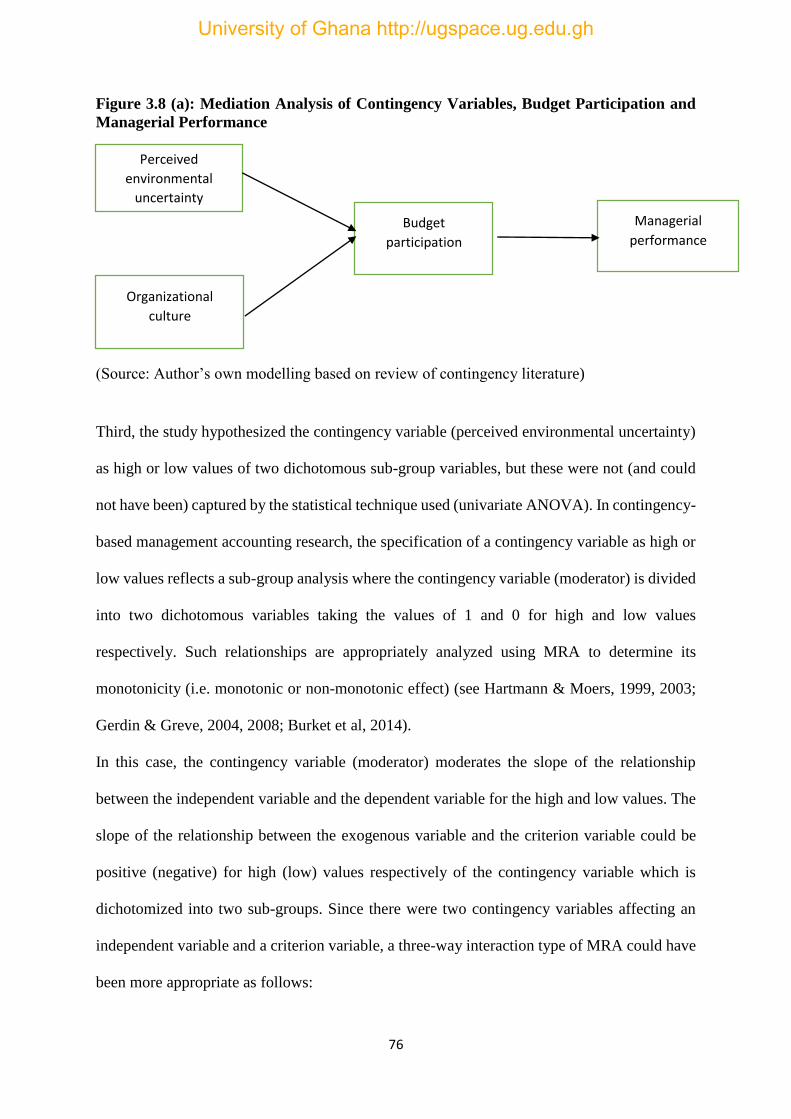

Figure 3.8 (a) Mediation Analysis of Contingency Variables, Budget Participation

and Managerial Performance

76

Figure 3.8 (b) Moderation Analysis of Contingency Variables, Budget Participation

and Managerial Performance

77

Figure 3.9 (a)-(d) Strength Versus Form Interaction 79

Figure 4.1 Theoretical Framework 91

Figure 4.2 Classification of the MAS Dimensions 99

Figure 6.1 (a)-(b) Graphical Output of Factor Analytic Model for SCM Context Factors 166

Figure 6.1 (c) –(d) Graphical Output of Factor Analytical Model for MAS Information

Dimensions

167

Figure 6.1 (c) Graphical Output of Factor Analytic Model for SCP Dimensions 167

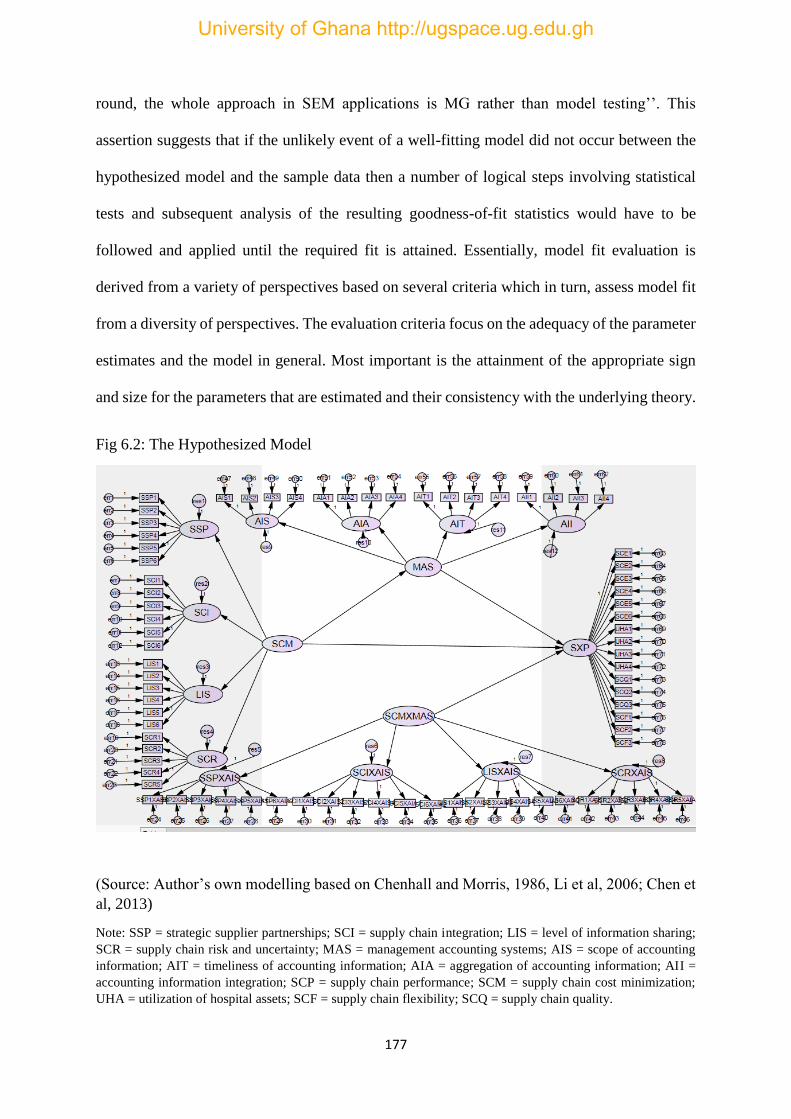

Figure 6.2 The Hypothesized Model 177

Figure 6.3 Structural Output for Fit Relationships 186

Figure 6.4 Structural Output of Mediation Analysis 190

Figure 6.5 Structural Output for Mediation Analysis (Second-order) 192

Figure 6.6 Structural Output for Moderation Effects (Lower-order effects

included)

197

Figure 6.7 Structural Output for Moderation Effects (Lower order effects

excluded)

200

University of Ghana http://ugspace.ug.edu.gh

xiii

LIST OF ABBREVIATIONS

CEO Chief Executive Officer

CMS Central Medical Stores

GHS Ghana Health Service

HCSCMP Health Commodity Supply Chain Management Plan

HSC Hospital Supply Chain

MA Management Accounting

MAS-CS Management Accounting System Supply Chain

MAS-SCM Management Accounting System Supply Chain Management

MOH Ministry of Health

NPM New Public Management

RMS Regional Medical Stores

SC Supply Chain

SCI Supply Chain Integration

SCM Supply Chain Management

SCN Supply Chain Network

SDP Service Distribution Points

TCE Transaction Cost Economics

WHO World Health Organization

University of Ghana http://ugspace.ug.edu.gh

xiv

ABSTRACT

This work analyzes the contingency effects of supply chain integration (SCI), information

sharing (or knowledge exchange), supply chain (SC) risk and uncertainty and management

accounting system (MAS) design on hospital SC performance in Ghana. Increasingly seen as

crucial in the management accounting (MA) literature over the past three decades has been the

design and implementation of effective MASs that extend beyond organizational boundaries

for the management and performance of relationships in the inter-firm exchanges domain. Such

studies have become one of the most important and critical areas for the CEOs and executive

leaderships of hospitals in their efforts to improve operational efficiency at minimal costs.

However, while the relationship between several SCM contextual factors and MAS

information, and the impact of SCI on SC performance have been extensively examined,

virtually no study had empirically examined in a single comprehensive study, the SCM-

performance impacts of MAS design. The underdevelopment of such studies is even more

pronounced in service oriented organizations. In addition, the literature on MAS-SCM

relationships had emphasized the design of MAS in the transaction context which in most cases

results in misaligned control. Transactions costs economics (TCE) although provides insights

on the MAS organizations should install to achieve fit, the actual observed patterns of MAS

use and the contextual factors that underpin MAS design in the inter-firm exchanges domain

are not fully explained by the theory. Hence, TCE tends to ignore the dimensions of internal fit

(i.e. internal integration) of the SC. Given this void, a survey of management accountants

drawn from 237 public and private hospitals in Ghana was used to test the contingency effects

of these relationships on hospital supply chain aggregate performance using hierarchical

factorial structures. Whereas the results partially support the presence of the selection and

mediation fit, the moderating form of fit was fully supported by the sample data. Also, internal

University of Ghana http://ugspace.ug.edu.gh

xv

integration was only supported by the moderation fit model. However, level of information (or

knowledge) exchange was not supported by the selection fit model although it was fully

supported by the moderation fit model and partially supported by the mediation model. This

finding suggests that choices of the MAS information characteristics to facilitate SCM

decisions among hospitals in Ghana is either excessive or insufficient. However, the findings

suggest that optimal choices of MAS design in the inter-firm exchanges domain to enhance SC

operational performance can be explained by contingency theory. Consistent with several prior

studies, it can be theorized that SCI as well as level of knowledge exchange and SC risk and

uncertainty have contingency effects in the design of MAS in the inter-organizational domains

in healthcare context. Hence, they could be considered as added external variables in the MAS-

contingency paradigm. The study’s key contribution is the development and testing of a novel

theoretical model of the relationship between the selection, mediation and moderation fit

models that link SCI, level of information sharing, and SC risk and uncertainty and MAS design

on hospital SC performance. It also offers Ghanaian hospital managers the usefulness of the

MAS-contingency framework in enhancing hospital SCM decisions.

University of Ghana http://ugspace.ug.edu.gh

1

CHAPTER ONE

INTRODUCTION

1.1 Brief Overview of the Study

This thesis is concerned with empirical examination of the contingency fit relationships among

four dimensions (broad scope, timeliness, integration and aggregation) of management

accounting system (MAS) information and supply chain integration (SCI), level of knowledge

exchange, and supply chain risk and uncertainty that can leverage hospital supply chain

aggregate performance in Ghana. This represents the intersection of three key areas:

management accounting systems (MAS), supply chain integration (SCI), and hospital supply

chain (SC) performance as shown in Fig 1.1. In this chapter, the background linking the

research problem and layout of the whole thesis’s logical sequence is presented. The chapter

ends with a summary.

Figure 1.1: Study Scope

(Source: Author’s own drawing based on review of literature)

Management Accounting

System (MAS) Design

Hospital Supply Chain Performance

Supply Chain Integration

(SCI)

Fit Relationships in

Healthcare

Institutions

University of Ghana http://ugspace.ug.edu.gh

2

1.2 Research Background

The supply chain (SC) concept which emerged in the 1990s as a strategic management tool,

has become a key driver that enhances overall organizational performance (Maestrini, Luzzini,

Maccarrone & Caniato, 2017; Ataseven & Nail, 2017). This strategic aspect of the SC has been

investigated by several research studies through empirical examination of the associations

between different SCM contextual factors and MAS design on one hand, and both operational

and financial performance on the other (van der Meer-Kooistra & Vosselman, 2000; Dekker,

2004; Flynn, Huo & Zhao, 2010; Wong, Boon-itt & Wong, 2011; Dekker, Groot & Schoute,

2013; Qi, Huo, Wang & Yeung, 2017). However, research that examines the impact of the

MAS information characteristics on either SC operational or financial performance is relatively

underdeveloped and largely remains a void (Burritt & Scaltegger, 2014). While this gap

remains, SCI, and sharing of information (or knowledge exchange) about the risks associated

with inter-firm exchanges have been identified as the most influencing factors that facilitate

the effective design and implementation of MAS information in enhancing hospital SC

performance (Kwon, Kim and Martin, 2016).

In addition, existing works on SCI and performance have predominantly been dominated by

the industrial dynamics and logistics literature as the literature has extensively focused on

product type organizations mostly discrete parts manufacturing and consumer goods (e.g.

Flynn et al, 2010; Wang et al, 2011; Qi et al, 2017). There have been relatively little research

that look at the impact of the MAS information characteristics on SCM decisions in service

oriented organizations, and more specifically, healthcare institutions (Anderson & Dekker,

2015). Consequently, increasingly seen as crucial in the literature over the past two decades

has been the design and implementation of effective MASs that align with contextual factors

within healthcare organizations (Wardhani, Utarini, van Dijk, Post & Groothoff, 2009;

Aidemark & Funck, 2009). This is because the effective formulation, management and efficient

University of Ghana http://ugspace.ug.edu.gh

3

functioning of the SC is highly associated with the fit between MAS information characteristics

and SCM contextual factors (Seal Cullen, Dunlop, Berry & Ahmed, 1999; Reusen &

Stouthuysen, 2017). For example, in healthcare services, information relating to SC costs such

as inventory management, procurement, transportation, warehousing, cost of operating

facilities, link between cost and cost drivers, commodity throughput as well as revealing

information on ineffective and inefficient hospital operations through the consumption of

resources etc., are provided by effective MAS design.

Furthermore, the SC constitutes the most critical element in overall organizational cost control

and has become one of the most important and critical areas for the chief executive officers

(CEOs) and executive leaderships of hospitals (Barlow, 2010c). This is because improvement

upon overall efficiency and cost reduction strategies have been a challenging issue in hospital

management (Pizzini, 2006; Abernethy, Chua, Grafton & Mahama, 2007). Also, the power

structure of healthcare has changed with the evolution of the new public management (NPM),

making MASs more dominant than medical skills in the monitoring and evaluation of clinical

performance (WHO, 2000; Malmmose, 2015). However, for effective monitoring and hence

optimal performance, the MAS design should traditionally be based on the ‘matching’ principle

where the installation of MASs by organizations align with contextual variables (Reusen &

Stouthuysen, 2017). Although these theoretical interrelationships fundamentally underpin the

installation and implementation of MAS for performance, the large volume of MAS-SC studies

had emphasized fit in the transaction context other than fit in the organizational context (van

der Meer-Kooistra & Vosselman, 2000; Dekker, 2004; Dekker et al, 2013). This is because the

theoretical lens of transaction costs economics (TCE) explains how MASs are installed as a

function of the specific transaction context that arises from contracting risks between suppliers

and buyers other than internal dimensions such as internal integration of the SC.

University of Ghana http://ugspace.ug.edu.gh

4

In this regard, TCE tends to ignore the dimensions of internal fit (e.g. internal integration) of

the SC. The internal fit of the supply chain represents the cross-functioning of systems and

collective responsibility across functions from a strategic perspective. Collaborations across

procurement, warehousing and distribution functions take place within internal integration to

meet customer (patient) requirements at a low total cost (Qi et al, 2017). Also, internal

integration efforts facilitate the sharing of real-time information and knowledge across key

functions through the break-down of functional barriers (Wong et al, 2011). These functional

barriers impact significantly on inventory management and warehousing, quality of hospital

processes and clinical costs, operating cost of hospital facilities, commodity throughput, costs

and cost drivers, etc. that have significant effect on SC operational performance (Chen, Preston

& Xia, 2013; Ataseven & Nair, 2017). In addition, the TCE does not seem to fully explain the

actual observed patterns of MAS use and the contextual factors that underpin its design in the

inter-firm exchanges domain, although it provides insights on the MAS organizations should

adopt to achieve fit (Anderson & Dekker, 2015). Furthermore, adoption of the TCE is mainly

based on mitigating the risk associated with the transactions in the inter-firm exchanges domain

(Langfield-Smith, 2008; Dekker et al, 2013). Risks such as heightened vulnerability and the

possibility that partners engaged in the transactions will opportunistically exploit the dependent

relationship are typical examples.

In this regard, the general contention has been that the excessive use of the MAS information

is required for transactions that suggest higher levels of risk attributes in order to foster mutual

collaboration and coordination (Reusen & Stouthuysen, 2017). Whilst there is wide acceptance

of this notion of alignment, the relationship between an organization’s MAS structure and

transactions context will often be in a state of misalignment to adversely affect performance.

Choices that entail either excessive or insufficient use of the MAS relative to the contextual

variable will result in misalignment, and negatively affect performance (Otley, 1980, 2016;

University of Ghana http://ugspace.ug.edu.gh

5

Burkert, Davila, Mehta & Oyon, 2014). Based on these voids, this study tests the contingency

effects of the MAS-SC performance using empirical data from healthcare institutions in Ghana.

In business strategy, the contingency perspective examines a particular set of organizational

and environmental factors at the optimal level (Burkert et al, 2014). However, the benefits of

contingency theory’s application in the inter-firm exchanges domain with respect to MAS

design has received little (or possibly no attention) in the literature (Jamal & Tayles, 2010).

Furthermore, existing works on the contingency paradigm were conducted based on samples

drawn from the developed world such as the US, UK, Canada and Australia (Jamal & Tayles,

2010). Hence arguments regarding the convergence of the contingency theory’s usefulness

remains contested. Similar works in developing economies such as Ghana will allow for the

assessment of the validity of the contingency arguments.

1.3. The Research Problem

The design of MAS information for SCM decisions in the inter-firm exchanges domain has

been considered as mere extensions of the conventional intra-firm cost accounting tools of the

traditional MAS. To this end, no attempt has been made by management accounting researchers

to test the contextual factors that underpin MAS design in the inter-firm exchanges domain as

compared to the intra-organizational domains which have been extensively studied.

Consequently, organizations have relied on the practice of imitating individuals’ MAS

structure when designing and installing MASs in inter-firm exchanges (Reusen & Stouthuysen,

2017). Reusen & Stouthuysen (2017) found this practice to be one of the root causes of

misalignment in the MAS-context relationship in the inter-firm exchanges domain.

It has been argued that ‘‘the planning and controlling processing abilities that are fundamental

to managing costs internally is the same for managing inter-firm relationships hence, can be

University of Ghana http://ugspace.ug.edu.gh

6

applied to SCM activities’’ (Fayard et al, 2012, p.170). In this regard, organizations that have

installed internal cost management systems considered to be at the highest level would be able

to use their expertise and knowledge to model similar costing systems for SCM decisions.

Although it is possible to use the expertise and knowledge of the traditional intra-firm cost

accounting tools to proxy SCM decisions in the inter-firm exchanges domain, the key concept

of fit is missing which ultimately results in misalignment to negatively affect performance.

Studying the impact of the MAS dimensions on SCM characteristics determines the functions

of the MAS in SCM decisions. In other words, the MAS has already been installed and is being

used to make decisions in the SCM context. This aspect of the MA-SC relationship has been

extensively studied from the theoretical lens of transaction cost economics (TCE) which

according to Anderson & Dekker (2015), does not fully explain the actual observed patterns of

the MAS use and the contextual factors that underpin its design in the inter-firm exchanges

domain. On the other hand, studying the effect of the SCM characteristics on MAS design

determines the MAS-context relationship that impact on performance in the inter-firm

exchanges domain. That is, it determines the design and type of MAS that appropriately fits

the SCM characteristics to maximize performance.

This study focuses on hospitals in Ghana because the SCM challenges that confront the health

sector could be as a result of improper design and use of the MAS for SCM decisions resulting

in misalignment between SCM practices and MAS design. (Asamoah, Abor and Opare, 2011;

Manso Annan & Anane, 2013; Denkyira, 2015). This will by extension, translate the body of

literature on MAS-contingency knowledge from the intra-organizational domains (which has

been the predominant MAS design studies in extant literature) to the inter-firm exchanges

domain in supply chains. Management of Ghana’s health commodity and SCM system has in

recent years, been characterized by ineffectiveness and weaknesses as ‘gaps’ (WHO, 2009;

Manso, Annan & Anane, 2013; Denkyira, 2015). To this end, various models (e.g. the five-

University of Ghana http://ugspace.ug.edu.gh

7

year development plan of the Ministry of Health (MOH) spanning the period 2008-2012, and

the MOH’s Health Commodity Supply Chain Master Plan (HCSCMP) of 2012 etc.) have been

tried and tested yet the problem remain unaddressed and have widened rather than curtailed.

For example, a study by Asamoah, Abor and Opare (2011) to examine the healthcare SC for

Artemisinin (ACT) Based Combination Therapies in Ghana revealed weaknesses such as

disruptions and delays in the SCM system due to poor SCI (both internal and external

integration) and weak inventory management systems. They further identified the integration

of the SC and weak information linkages as the main threat to the health SC and this ultimately

results in price increases at the pharmacy level.

The identified weaknesses have significant impact on the design and implementation of MAS

information because MAS serves not only to provide information to oil the wheels of a SC

network but also, integrates functional units and entities which are internal and external to

organizations (Burns, 2002; Thrane & Hald, 2006; Dacosta-Claro, 2002; Scheller & Smeltzer,

2006). It also serves to reduce costs and create value in SCs (Fayard, Lee, Leitch & Kettinger,

2012). However, these relationships have not been examined as part of the numerous models

already tried and tested. Perhaps, the MASs installed and used in hospitals might not be in

alignment (or fit) with hospital SCM activities thereby providing little value for managerial

decisions in the inter-firm exchanges domain. Studies into the contingency models linking

MAS information characteristics and SCM could offer some insights to solving the problem.

Besides, substantial literature document the link between SCI and both SC financial and

operational performance (Flynn et al, 2010; Wong et al, 2011). Another vast stream of literature

examine the relationship between MAS information characteristics and attributes of SCM in

the inter-firm exchanges domain (Copper & Slagmulder, 1999; van der Meer-Kooistra &

Vosselman, 2000; Dekker, 2004, Agndal & Nilsson, 2009; Coad & Cullen, 2006; Fayard et al,

University of Ghana http://ugspace.ug.edu.gh

8

2012; Dekker et al, 2013; Anderson & Dekker, 2015; Reusen & Stouthuysen, 2017). There is

however, virtually no research that simultaneously examines the MAS design, SCI and SC

performance associations in a single comprehensive study. Given the considerable effort

devoted by management accounting researchers in explaining MAS choices in inter-firm

relationships and the fact that SC performance is largely a function of relationship

characteristics, such theoretical interrelationships are important and fill a gap that develops and

tests a novel theoretical model linking both MAS design, SCM, and SC performance in

healthcare context. This is important for the advancement of theory in the inter-firm exchanges

domain. Fig 1.2 illustrates the relationships linking these gaps.

Fig 1.2. Gaps Linking MAS, SCI and SCP

As shown in Fig 1.2, the link between MAS design and SC performance still remains a gap

although they have a strong theoretical background. Besides, the link between SCM and MAS

design is recursive (Ramos, 2004). However, only one-side of this bi-directional relationship

has so far been examined. The impact of SCM on MAS design has virtually received no

University of Ghana http://ugspace.ug.edu.gh

9

empirical investigation. Finally, a study that examines the complete relationship between MAS,

SCM, and SCP hardly exists in the literature. Thus, this study fills a gap by developing a novel

theoretical model that links these three key constructs. Additionally, the link between SCI and

SC performance is associated with levels of effects on various performance dimensions that

differ and vary (Cousins & Menguc, 2006; Devaraj, Krajewski & Wei, 2007; Schoenherr &

Swink, 2012, 2015), rendering the findings of such studies to be inconsistent. More precisely,

the impact of both internal integration and external integration on performance has been

associated with mixed findings. This inconsistencies could be attributed to the measurement of

integration as one construct and also elimination of internal integration in most studies (Flynn

et al, 2010; Ataseven & Nail, 2017).

For example, while Cousins and Menguc (2006) show a positive association between SCI and

suppliers’ communication performance, Devaraj et al (2007) also registered a positive

association between SCI and performance, but found that customer integration and

performance were negatively related. Similarly, Flynn et al (2010) found that supplier

integration and operational performance are not directly related. Schoenherr & Swink (2012)

also found distinct associations between SCI and both financial and operational performance.

Flynn et al (2010) found in both their configuration and contingency approach that SCI was

associated with both operational and business performance and that customer and internal

integration were more strongly associated in enhancing performance than supplier integration.

In general, the literature on the relationship between SCI and performance has very mixed

findings. In order to advance theory development, it is important to ascertain whether

moderating factors underpin certain relationships which is the key concept of contingency

theory and is highly important in situations where the findings about relationships are mixed

(Ataseven & Nail, 2017). Furthermore, much of the literature in this area have been conceptual

in nature coupled with the dominance of inductive methods such as case studies involving two

University of Ghana http://ugspace.ug.edu.gh

10

dyad relationships and occasionally SC triad in the majority of empirical works (e.g. Cooper

& Slagmulder, 2004; Seuring & Muller, 2008; Burritt & Schaltegger, 2014). Although case

studies research can be very helpful for gaining a deeper insights and understanding into factors

that influence the installation of MASs in inter-firm relationships (van der Meer-Kooistra &

Vosselman, 2000), the findings associated with these studies show lack of generalizability and

overall conclusions. This work contributes to filling these gaps.

1.4 Study Objectives

The broad objective of this study is to examine the impact of the relationship between hospital

SCI and four dimensions of MAS design on hospital SC performance. Specifically, the study

seeks to:

1) Examine the association between hospital SCM contextual factors and dimensions of

the MAS information in Ghana.

2) Investigate the mediating effect of the MAS dimensions on SCM contextual factors and

Ghana’s healthcare SC operational performance.

3) Examine the moderating effect of SCM contextual factors on the relationship between

MAS design and Ghana’s healthcare SC operational performance.

1.5 General Research Questions

The following research questions underpin the study:

1) Do the MASs designed and used by healthcare institutions in Ghana align with

internal and external integration, level of information sharing and the risk and

uncertainties of the health supply chain?

University of Ghana http://ugspace.ug.edu.gh

11

2) To what extent do the MASs used in Ghana’s healthcare organizations offer a

mediating role between SCI (internal and external), level of information sharing,

and supply chain risk and uncertainty and hospital SC operational performance?

3) To what extent do SCI (external and internal), level of information sharing, and

supply chain risk and uncertainty have an interaction effect on the association

between MAS information and hospital SC operational performance of healthcare

institutions in Ghana?

1.6 Significance of the Study

The design and use of MAS information in both private and public-sector organizations has

often been encouraged by government policies across the globe (Macinati &Anessi-Pessina,

2014). However, exploitation into its actual usage and benefits in healthcare settings, and

supply chains in particular largely remains a void. Consequently, a study that provides insights

into the performance implications of the causal paths linking SCI and MAS information

characteristics in healthcare context would both extend existing knowledge and provide useful

indications to healthcare managers and policymakers. In addition, modelling and measuring

performance outcomes relating to the MAS-supply chain intersection is needed to permit an

examination of the question of whether an appropriate or inappropriate ‘matching’ between

SCI and MAS information in the hospital SC leads to higher or lower performance. The

findings in this regard, will undoubtedly serve as a reference point (or a guide) for the design

and implementation of MAS information in the SCM context of healthcare institutions. In

particular, it provides empirical evidence that could serve as guiding principles to the health

systems’ pricing decisions, performance assessment, process improvement, and cost reduction

strategies associated with their inter-organizational relations (e.g. suppliers) and the extent of

fit (or alignment) of the managerial and cost information with these decision needs.

University of Ghana http://ugspace.ug.edu.gh

12

This work, apart from the foregoing, also provides information that relates to the current state

of the managerial and cost information systems designed and used by healthcare institutions;

i.e. whether they positively respond to hospital SCM issues and provide management with the

relevant SCM information for effective decisions. In other words, whether the characteristics

of the MASs information and the SCM metrics have any linkage to positively impact on

performance. Given that the accounting systems in these institutions have perhaps reached their

state of obsolescence and hence become dysfunctional due to evolutionary changes in the

processes and procedures of hospital operations that have not been incorporated into their

accounting systems, this work stands in the position to provide information that could lead to

addressing some of these deficiencies and weaknesses. To achieve this, it shows the extent to

which the MAS information designed and used by healthcare institutions fits (or aligns) with

context factors in the inter-organizational domain, and whether per the outcome, these systems

need further improvement or total overhaul.

Indeed, the identified weaknesses and deficiencies in the health SCM system suggests that the

managerial and cost information systems associated with the health logistic and supply chain

have perhaps become obsolete and outdated, and hence, no longer support the strategic

direction of healthcare management although the systems are perfectly adequate for financial

reporting purposes. In this regard, issues on value relevance of the current MAS information

needed for management decision making in terms of the sophistication level of the managerial

and cost information are highly imbedded in this work. For example, issues relating to

advanced accounting techniques such as Activity-Based Costing (ABC) (which is found in

most hospitals’ accounting system) and knowledge of the application of modern costing

concepts become highly relevant.

University of Ghana http://ugspace.ug.edu.gh

13

1.7 Outline of Remainder of Thesis

The remainder of the thesis is organized into seven chapters as follows: Chapters 2 and 3 are

devoted to systematic literature reviews. Chapter two discusses the study’s context, MAS

design and the health supply chain; its distinguishing features from that of the mainstream

discrete parts manufacturing and consumer goods, and the decision-functional role of MAS

information in minimizing hospital supply chain costs. In chapter three, a general discussion

of the study’s theoretical underpinnings is presented together with empirical reviews of the

empirical contingency-based management accounting studies. Chapter four presents the

theoretical framework, and following a refinement of the research questions develops and

formulates the verbal hypotheses. The research methodology is presented in chapter five. It

comprises a detailed discussion of the research design, data collection procedures and

processes, and the approach to statistical tests and analysis. In chapter six, the survey analysis

and results are presented. This is followed by a discussion and interpretation of the findings in

chapter seven. Chapter eight concludes the study with a summary of main findings, key

contributions and future research directions.

1.8 Chapter Summary

In this chapter, the motivation for investigating the contingency fit relationships between MAS

design and SCI, level of information sharing, and SC risk and uncertainty, and their interaction

effect on hospital SC performance in Ghana has been specified. Given that the design and use

of MAS information is known to be commonly associated with organizational contextual

factors that can leverage organizational performance, such studies lack empirical evidence in

the inter-firm exchanges domain in service-oriented organizations. Existing MAS-SC studies

have predominantly not only dominated product type organizations such as discrete parts

manufacturing and consumer goods but also, emphasized the fit in the transaction context to

University of Ghana http://ugspace.ug.edu.gh

14

mainly mitigate the risk between transaction partners. However, an incomplete and potentially

based picture of inter-firm control may be presented when the MAS decisions are explained

using transaction attributes alone as a focus. The actual observed patterns on MAS use, and the

contextual factors that underpin MAS design in the inter-firm exchanges domain are not fully

explained by the TCE. In line with these voids, this study tests the contingency effects of the

MAS-SC performance using empirical data from healthcare institutions in Ghana. Evidence of

the weaknesses and deficiencies that characterize the procurement, warehousing, storage and

distribution arrangements of health commodities which ultimately results in high prices to end

users, have major implications for MAS design in the SCM of Ghana’s healthcare institutions.

Finally, the study outlines the structure and logical sequence of the remainder of the thesis.

University of Ghana http://ugspace.ug.edu.gh

15

CHAPTER TWO

CONTEXTUAL BACKGROUND, MANAGEMENT ACCOUNTING

SYSTEM DESIGN AND THE HEALTH SUPPLY CHAIN

2.1. Introduction

The previous chapter introduced the research problem and the motivation for the study. This

chapter presents a review of the study’s context, the MAS information characteristics and SCM

interactions, and how they combine to impact on the health SC performance. The chapter

begins with a discussion of the importance of hospital SC integration and its effect on

performance. In this case, recent issues on management accounting and SC performance are

discussed. It also gives a description of the study’s context followed by the nature of MAS

design and its possible functions in SCM decisions. The chapter also presents the SCM

challenges that characterize the research sight. It discusses the structure of Ghana’s health SCM

system which basically links three key distributors of health products: the Central Medical

Stores (CMS), the Regional Medical Stores (RMS) and Service Distributed Points (SDP) (or

hospitals). A background of the weaknesses and deficiencies that characterized the current

operations of Ghana’s health logistics and supply management system is also presented.

Furthermore, the current state of the accounting system in the health sector is briefly explained

followed by the numerous reform projects launched by governments since 1998 which were

aimed at transforming the health commodity and supply management system. Finally, a review

of the health SC in terms of levels of complexity and sophistication in comparison to that of

mainstream business organizations is also presented. The chapter ends with a summary.

University of Ghana http://ugspace.ug.edu.gh

16

2.2. Recent Studies on MAS Design and Hospital SC Performance

In this section, a reportage of recent trending issues on the MAS design, SCI and hospital SC

performance both at the local and international levels is presented. According to Ab Talib,

Abdul Hamid and Thoo (2015) the existing body of knowledge on this topic has a number of

trending issues arising from recent studies. These studies investigate the antecedents,

prerequisites, requirements, or critical success factors that affect SCI and hospital SC

performance. Integration of the SC is currently, considered as one of the widely discussed

topics in the SCM research (Polater and Demirdogen, 2018; Abdallah, Abdallah & Saleh,

2017). Polater and Demirdogen (2018) argue that intensive integration between external

partners and internal processes enhances hospital SC operational performance hence, underlies

the basic motivation for healthcare SCM. While hospitals integrate their internal capabilities to

provide a better service for patients, they benefit from their partners’ resources as well. Several

research studies (e.g. Zhao and Huo, 2013; Skandrani et al. ,2011; Kazemzadeh et al. ,2012;

Lee et al., 2011; Rahimnia and Moghadasian, 2010) have argued that an effective integrated

SC is one of the key competitive advantages of leading organizations and is currently one of

the widely discussed topics in the SCM research.

The concept of SCI has therefore become prevalent in both the public and private health sectors

because of the impact it has on enhancing operational efficiencies, customer satisfaction and

quality of care as well as minimizing wastes and medical errors (Schneller .and Smeltzer, 2011;

Polater and Demirdogen, 2018). The supply of medical products has also become critical to all

hospitals so that performance in terms of costs, quality, responsiveness and patient satisfaction

can be enhanced (Asamoah et al, 2011). Consequently, health providers in both the public and

private sectors have paid more attention to healthcare services and their suppliers in order to

achieve higher service quality, lower costs, and enhance operational performance (Hammad,

Jusoh and Ghozali, 2013). In addition, due to the increasing trend in healthcare spending on

University of Ghana http://ugspace.ug.edu.gh

17

supplies, both governments and private health providers are compelled to focus on the

assessment and improvement of hospital operations efficiency especially in relation to

suppliers of medical products and the overall logistics and SC (Watcharasriroj and Tang, 2004).

According to Chakraborty, Bhattacharya and Dobrzykowski (2014) the general perception of

organizations about SCI and SCM in general has budged toward managing relationships rather

than just the purchasing function. These relationships are however, closely related to MAS

information (Dekker, 2013, 2016) which like the objective of SCM, aims at reducing SC cost

and adding value (Burritt & Scaltegger, 2014). Abdallah et al (2017) provide useful insights in

boosting hospital SC performance when they examined the effect of trust (a key construct of

MAS design) with suppliers on hospital-supplier integration and hospital SC performance.

They established that high levels of SCI not only improve hospital SC performance but also

enhance the transformation of trust benefits into SC performance. The paper further documents

that hospital SCI partially mediates the relationship between trust and hospital SC performance.

In another study, Ataseven and Nail (2017) undertook an extensive examination of the

association between SCI and various performance dimensions using a meta-analytical

methodology. They find that supplier integration, internal integration, and customer integration

have a significant impact on both operational (cost, quality, delivery, and flexibility)

performance and financial performance of a firm. They point to the specific relationships

between SCI and performance that need to examined further within contingency framework to

discern the role of moderating factors. Finally, they offered insights on the dimensions of

integration that have the largest breadth and depth of impact on various performance measures

which is relevant for managerial decision-making.

On the local front, Adu-Poku, Asamoah and Abor (2011) examined the logistics SC system of

the Adansi South District Health Directorate from users’ perspective. They document that

University of Ghana http://ugspace.ug.edu.gh

18

adequate information (i.e. management accounting information) needed to support effective

and efficient SCM activities is lacking hence, a poor collation of patients’ needs during

procurement. They also identified problems such as delay in the procurement system in the

district as a result of poor delivery time by suppliers, delay in evaluating bids. Manso, Annan

and Anane (2013) also assessed the logistics management of the Ghana Health Service and

reported several shortcomings associated with the health SC. They found poor procurement

planning and budgeting, poor quantification and forecasting, delay in the procurement process

and order processing, and delay in receiving insurance claims to characterized the health SC.

Asamoah et al (2011) examined the performance of the SCM activities relating the

pharmaceutical SC for artemisinim-based combination therapies (ACT) in Ghana. They

reported that both the public and private SC networks for the ACT depict evidence of long-tern

relationships with external suppliers and factor interdependence. They also reported of the high

prices that characterized the general price level of the although highly subsidised ACT as a

result of disruptions in the health SC. Frequent disruptions in the link between external

suppliers which was found to be the main threat to the health SC, result in price increases of

health commodities at the pharmacy level. As can be seen from these deficiencies, a study to

examine the interaction effect of the MAS design and SCI is crucial because effective MAS

design provides information for the smooth running of the logistics system (Burritt &

Scaltegger, 2014). The next section explains the health SCM system in Ghana.

2.3 Ghana’s Health SCM System

The mission of the Logistics, Clearing and Warehousing Department of GHS reads: Logistics:

‘‘Our mission is to offer, our clients, a competitive advantage through superior transportation

of logistics services. Through timely communications and quality information, we will meet

and exceed our client’s expectations of service. Also, through our commitment to provide

University of Ghana http://ugspace.ug.edu.gh

19

excellent service, Value added service, continued innovation in management, we will

accomplish our mission: 2) Warehousing: To ensure that regular availability and uninterrupted

supply of health commodities are delivered to health institutions at affordable prices. Using

best practices in storage and distribution of quality, we are capable of responding to the total

commodity requirement and as a centre of excellence, and safe efficacious health commodities”

(Ministry of Health (MOH), 2012, p.2).

The SC system of Ghana’s healthcare which manages health commodities through a three-tier

system, is made up of drug manufacturers, suppliers (wholesalers, distributors, and retailers),

the Central Medical Stores (CMS), Regional Medical Stores (RMS), Service Delivery Points

(SDP), and the transportation networks. Through this SC, supplies and drugs as well as

contraceptives are managed and sent to health facilities across the country. The receipt, storage

and distribution of all medical supplies after procurement by the Ministry of Health (MOH) is

the responsibility of the CMS. The CMS in turn, supplies the lower levels of the tier. Depending

on their geographical location, health facilities (SDPs) receive their supplies from the

appropriate RMS. However, the management of vaccines is slightly different from other

medical supplies. These are managed through refrigerated facilities and a network of

warehouses of cold storage across the regions.

The MOH exercises overall oversight control including policy formulation, evaluation and

monitoring of progress in achieving set targets for the whole system. The service delivery and

Teaching Hospitals are largely undertaken by the Ghana Health Service (GHS). Both of these

institutions constitute the bulk of the MOH institutions under the public health system. A four-

tier system made up of regional, district, sub-district and community constitutes the health

system delivery while the management of health services and health supplies as stated upfront

is operated on a three-tier system comprising the CMS, the RMS, and the SDP. The CMS is

responsible for procuring drugs and vaccines that are primarily financed by external financiers.

University of Ghana http://ugspace.ug.edu.gh

20

Occasionally, and this is an exceptional case, the Teaching Hospitals and the Regional

Hospitals procure directly from suppliers but approval must be sought from the MOH. Thus,

whilst the logistics and supply management system is centralized, the healthcare delivery

system is decentralized. Together with suppliers of drugs and other medical supplies at both

local and international levels, pharmaceutical manufacturers, wholesalers, distributors, and

retailers, transportation networks and other distribution networks constitute the SCN in the

health sector.

2.4 Managerial and Costing Systems in Ghana’s Healthcare Management

As a recap of chapter one, the managerial and cost information systems of most healthcare

institutions in Ghana have reached the state of obsolescence and dysfunctional due to

evolutionary changes in the processes and procedures of hospital operations that have not been

incorporated in their accounting systems. The current MASs have little value for management

decisions in the inter-firm exchanges domain as there is limitation in the use and sophistication

of cost and managerial information. Advanced accounting techniques such as Activity-Based

Costing (ABC) are perhaps not applied and modern costing concepts are largely unknown in

most healthcare institutions. Managerial and cost information are mostly associated with

decisions on pricing rather than process improvement, performance assessment, or cost

reduction strategies. The managerial and cost information systems seemed to have become

outdated and no longer support the strategic direction of healthcare institutions though the

systems are perfectly adequate for financial reporting purposes.

There are also illogical relations among operating cost of facilities, value of commodity

throughput and populations served at various levels. Neither commodity throughput nor service

population appear to drive costs as they should be in an efficiently and rationally operating

system (Manso et al, 2013). Non connection between costs and cost drivers – clear indication

University of Ghana http://ugspace.ug.edu.gh

21

of non-linkage between budgeting process and both commodity throughput and service

populations (WHO, 2009; Denkyira, 2015). Currently, there is the unconventional occurrence

of public sector prices for highly subsidised commodities being higher than private sector

prices (Asamoah et al, 2011; Manso et al, 2013). However, Kelle, Woosley and Schneider

(2012) noted that by paying attention to the three dimensions of SCI (supplier, customer and

internal integration) in the inter-organizational linkages and their alignment with accounting

information characteristics, a hospital can improve its performance through the performance of

other organizations in the SC.

In addition, a hospital can improve upon its procurement and logistics activities by aligning its

inventory management system with a just-in-time MAS technique. Another example is where

hospitals provide a perfect fitting information about their inventory needs by helping their

suppliers more efficiently plan their production schedules to meet their needs. In this case

hospitals’ operating costs are minimized because they perform their procurement and logistics

activities in an efficient manner. In addition, they have less of their capital tied up in stock (or

inventory). Furthermore, sharing of knowledge and expertise in the optimum is easier, and

perhaps improve operations and even provide a competitive advantage in a situation where the

MAS information characteristics are well-fitted with SCM context factors. Hence, the perfect

alignment of SCI with the MAS information characteristics is highly critical to SC performance

in the healthcare setting (Aidemark & Funck, 2009). In this regard, improvements in hospital

SC performance have increasingly gained importance as health care institutions strive to

improve upon their operational efficiency as well as minimize costs (Chen et al, 2013).

2.5. Reforms in the Health Logistics and Commodity Management System

A five-year health sector reform under the Health Sector Support Project (HSSP), and

supported by the World Bank, was undertaken by the Ghana government from 1998 to 2002.

University of Ghana http://ugspace.ug.edu.gh

22

From 2002 to 2006, another health sector reforms project under the five-year medium-term

was undertaken. During this period, several reform packages were implemented under several

health reform initiatives. These initiatives were designed to specifically ensure that the reform

packages are successfully implemented.

In 2008, a review to assess the strengths and weaknesses of Ghana’s health commodity supply

and management system was undertaken by the USAID DELIVER PROJECT and

Management Sciences for Health (MSH)/Strengthening Pharmaceutical System (SPS)

(Adegoke, Bruce, Chimnani, Eghan, Tetteh & Veskov, 2008). In collaboration with the

Procurement and Supply Directorate (PSD) and the Foods and Drugs Authority (FDA), the

existence of weaknesses and inefficiencies as ‘gaps’ in the health SCM system was confirmed

(WHO, 2009; MOH, 2012). Prior to this survey, the Ghana Health Service (GHS) had in 2007,