management accounting - marriott school of …marriottschool.net/emp/mrs/files/hyundai/hyundai...

TRANSCRIPT

Hyundai Heavy Industries Executive Program

MANAGEMENT ACCOUNTING

Slides by Monte Swain, PhD, CPA

Brigham Young University

Reprinted with the permission of the author No further copying allowed

August 2012

Page M1

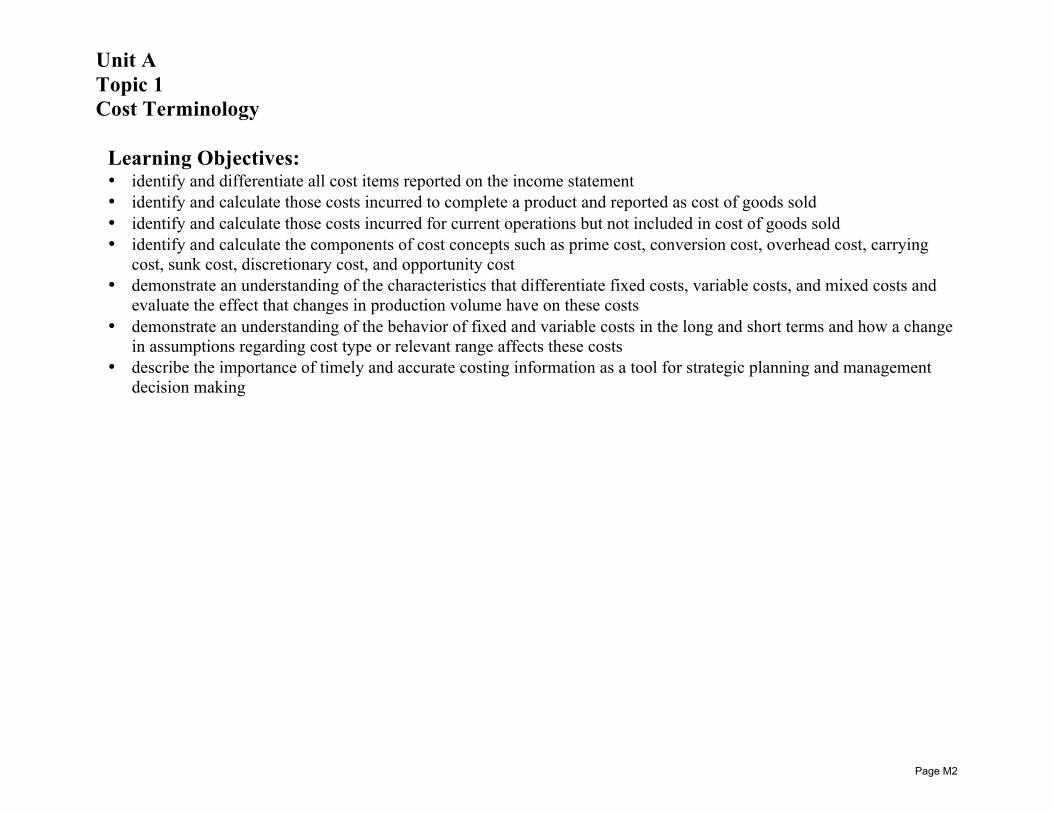

Unit A Topic 1 Cost Terminology

Learning Objectives: • identify and differentiate all cost items reported on the income statement • identify and calculate those costs incurred to complete a product and reported as cost of goods sold • identify and calculate those costs incurred for current operations but not included in cost of goods sold • identify and calculate the components of cost concepts such as prime cost, conversion cost, overhead cost, carrying

cost, sunk cost, discretionary cost, and opportunity cost • demonstrate an understanding of the characteristics that differentiate fixed costs, variable costs, and mixed costs and

evaluate the effect that changes in production volume have on these costs • demonstrate an understanding of the behavior of fixed and variable costs in the long and short terms and how a change

in assumptions regarding cost type or relevant range affects these costs • describe the importance of timely and accurate costing information as a tool for strategic planning and management

decision making

Page M2

Costs on the Income Statement

Sales Revenue $750,000 Cost of Goods Sold (COGS) 425,000 Gross Profit $325,000 Selling, General, Admin (SGA) Exp. 278,000 Operating Income $ 47,000

n Product Costs

o Labor, materials, and production overhead costs o Initially assigned to inventory (balance sheet) o Eventually expensed when “sold” (income statement) o “Above the Line” costs

n Period Costs o Selling, administrative, and other operating costs o Immediately expensed to the income statement o “Below the Line” costs

Remember: Only product costs are assigned to inventory and can be reported on the balance sheet (according to GAAP).

Product Costs

Period Costs

The “Line”

Page M3

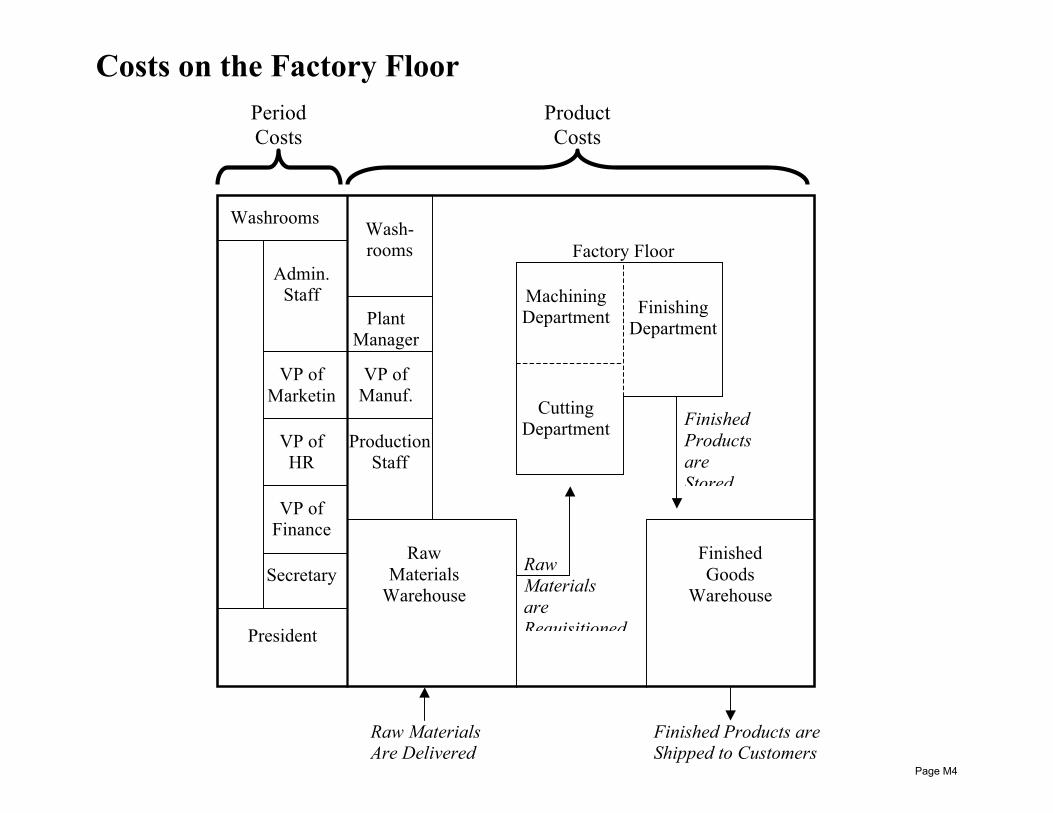

Costs on the Factory Floor

President

Secretary

VP of Finance

VP of HR

VP of Marketin

g

Admin. Staff

Washrooms

Production Staff

VP of Manuf.

Plant Manager

Wash- rooms

Raw Materials

Warehouse

Finished Goods

Warehouse

Cutting Department

Finishing Department

Machining Department

Raw Materials are Requisitioned

Finished Products are Stored

Raw Materials Are Delivered

Finished Products are Shipped to Customers

Factory Floor

Period Costs

Product Costs

Page M4

Cost Classifications

n Direct Costs o Costs that are specifically traceable to the unit or business, or segment,

or product being analyzed § In other words, the costs that will be avoided if we remove the

segment or product

n Indirect Costs o Costs that benefit multiple segments or products that are often allocated

(but not traceable) to individual segments/products § Sometimes called common costs or joint costs

n Direct Materials Costs o Materials that become part of the product and are traceable to it

n Direct Labor Costs o Wages paid to those who physically work on the direct materials and

convert them into finished product § These costs are traceable to the product

n Prime Costs o The costs that can be “primarily seen” in the product

§ Direct labor and direct materials

Page M5

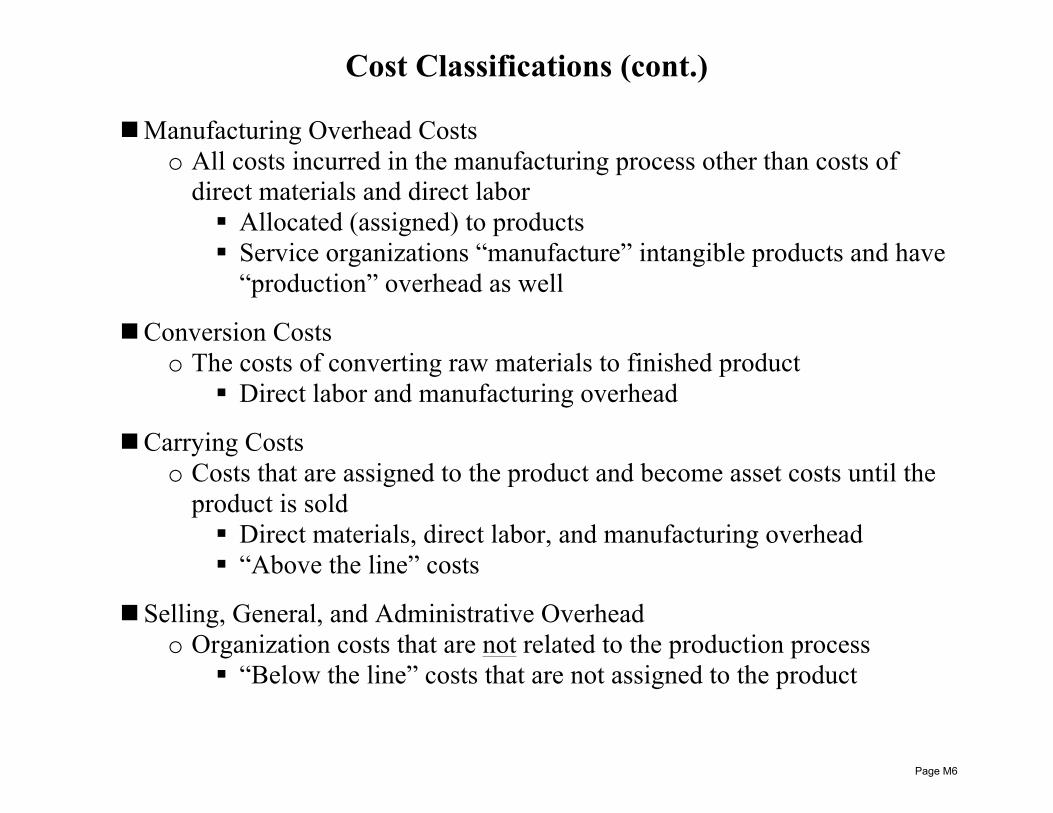

Cost Classifications (cont.) n Manufacturing Overhead Costs

o All costs incurred in the manufacturing process other than costs of direct materials and direct labor § Allocated (assigned) to products § Service organizations “manufacture” intangible products and have

“production” overhead as well

n Conversion Costs o The costs of converting raw materials to finished product

§ Direct labor and manufacturing overhead

n Carrying Costs o Costs that are assigned to the product and become asset costs until the

product is sold § Direct materials, direct labor, and manufacturing overhead § “Above the line” costs

n Selling, General, and Administrative Overhead o Organization costs that are not related to the production process

§ “Below the line” costs that are not assigned to the product

Page M6

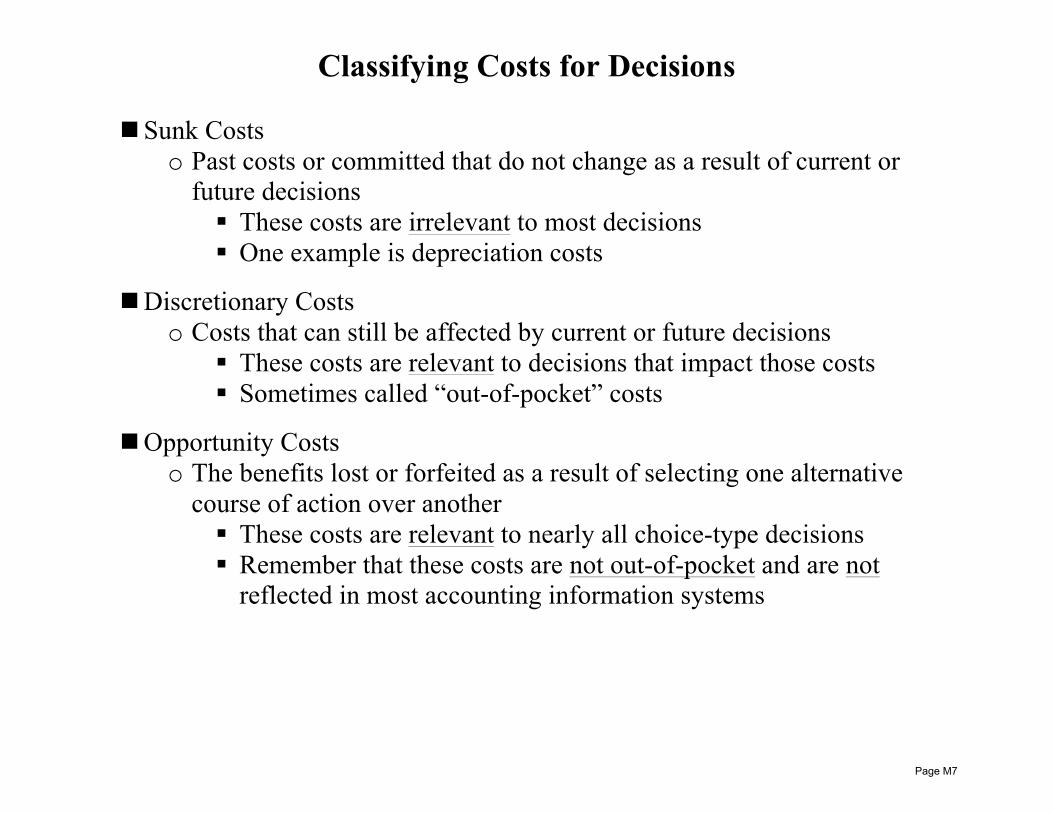

Classifying Costs for Decisions

n Sunk Costs o Past costs or committed that do not change as a result of current or

future decisions § These costs are irrelevant to most decisions § One example is depreciation costs

n Discretionary Costs o Costs that can still be affected by current or future decisions

§ These costs are relevant to decisions that impact those costs § Sometimes called “out-of-pocket” costs

n Opportunity Costs o The benefits lost or forfeited as a result of selecting one alternative

course of action over another § These costs are relevant to nearly all choice-type decisions § Remember that these costs are not out-of-pocket and are not

reflected in most accounting information systems

Page M7

Costs Behavior

n Cost Behavior is Described in relation to Key Activities within the Company o Activity levels are often measured in terms of output, input, or a

combination of both § Traditional examples are units sold, units produced, labor hours,

and machine hours

n Fixed Costs o Costs that remain constant in total regardless of changes in the activity

level

n Variable Costs o Costs that change in total in direct proportion to changes in the activity

level

n Mixed Costs o Costs that include both fixed cost and variable cost components

§ These costs must be segregated before data can be used for most types of decisions

§ Methods that can be used to segregate mixed costs include the graphing and visual fit analysis, high-low analysis, and statistical regression analysis

Page M8

Costs Behavior (cont.) n Relevant Range of Activity

o The normal or expected range of production/sales § Production/sales that occur outside of the relevant range typically

result in significant changes to the cost structure § Fixed costs do not stay constant, nor do variable costs remain

proportional, outside of relevant range (critical assumption!)

n Relevant Range and Time Horizons o The longer the time horizon, the larger the relevant range

§ In the long run, most costs are variable § In the very short run, most costs are fixed

o The critical point is that the distinction between fixed and variable costs is a function of assumptions regarding the relevant range/time horizon

Page M9

Cost-Based Decisions

n Cost data are Necessary for making decisions o As the accuracy and timeliness of cost data improves, decision making

become faster and more confident

n But cost data are usually Not Sufficient for making decisions o Marketing, HR, competitor analysis, technology, etc. all combine to

form the organization’s strategy § Nevertheless, until costs are understood, it is difficult to proceed to

a discussion of issues such as marketing and HR.

Page M10

Unit A Topic 2 Cost Measurement Concepts

Learning Objectives: • recognize cost objects and cost pools and assign costs to appropriate activities • demonstrate an understanding of the nature and types of cost drivers and the causal relationship that exists between

cost drivers and costs incurred • demonstrate a thorough understanding of the various methods for measuring costs and accumulating work-in-process

and finished goods inventories and a basic understanding of how inventories are relieved • identify and calculate the components of cost measurement techniques such as actual costing, normal costing, and

standard costing; recognize the appropriate use of each technique; and describe the benefits and limitations of each technique

Page M11

Cost Assignment Systems

n Cost Assignment is Critical (and Difficult) for both Manufacturing and Service Organizations o Both of these organizations are production based o The critical issue is how to assign costs of materials, labor, and

overhead to work-in-process accounts

n Cost assignment work is not nearly as challenging in a merchandising organization

Direct Materials

Costs

Direct Labor Costs

Production Overhead

Costs

Work-in-Process

Inventory

Finished Goods

Inventory

Cost of Goods Sold

The Balance Sheet

The Income

Statement

Page M12

Cost Assignment Systems (cont.)

n Three types of Cost Accounting Systems o Actual costing o Normal costing o Standard costing

n Actual Costing (rarely used) o Assign costs of materials, labor, and overhead to work-in-process

(WIP) as these costs are actually consumed o Advantages

§ The accounting is easy and inexpensive § Reduced chance for costs to be assigned to the wrong products

o Disadvantages § Many costs (mainly overhead costs) can not be assigned at all to

products because there is no direct relationship between the cost and the production of the product

§ There is no system to budget and control production costs because costs are simply assigned as they incur

Page M13

Cost Assignment Systems (cont.)

n Normal Costing (often used) o Assign actual costs of materials and labor to WIP as these resources are

consumed o Allocate costs of overhead to WIP using a predetermined (budgeted)

overhead rate o Advantages

§ All overhead costs are accounted for and assigned to products § There is some budget and control in the accounting process, but

only for overhead costs o Disadvantages

§ Accounting is more complicated compared to actual costing systems

§ The accuracy and usefulness of the cost system is only as good as the estimates used to create the predetermined overhead rate (this is a major problem!)

§ There is still no system to budget and control materials and labor costs

Page M14

Cost Assignment Systems (cont.)

n Standard Costing (often used, especially in large organizations) o Assign standard costs of materials and labor to WIP as these resources

are consumed o Allocate costs of overhead to WIP using a predetermined (budgeted)

overhead rate o Advantages

§ Budget and control exists within the accounting process for all product costs

o Disadvantages § Accounting is more complicated than actual and normal costing

systems § The accuracy and usefulness of the cost system is only as good as

the cost standards used for materials, labor, and overhead (this is a major problem!)

o The process of reconciling the budgeted (standard) costs with actual costs in the accounting system results in variances (to be discussed in a later topic)

Page M15

Unit A Topic 3 Cost Accumulation Systems

Learning Objectives: • understand the strategic value of cost information regarding products and services, pricing, overhead allocations, and

other issues • define the nature of the system, understand the cost flows of the system, and recognize its appropriate use • calculate inventory values and cost of goods sold • understand the benefits and limitations of each cost accumulation system • understand the concept of life-cycle costing and the strategic value of including upstream costs, manufacturing costs,

and downstream costs

Page M16

Strategic Cost Management

n Classic Strategic Views o Quality products/services at low prices o Unique products/services (sometimes at premium prices) o In either case, accurate cost information is necessary to plan, control,

and evaluate the effectiveness of these strategies

n Strategic Cost Information is Useful in Answering Strategic Questions o Who are our critical customers?

§ How sensitive are these customers to price, quality, and service? o Who are our important suppliers?

§ How do the products/services of our suppliers impact our costs and service?

o What substitute products/services exist? § How are these substitutes different in terms of price and quality?

Page M17

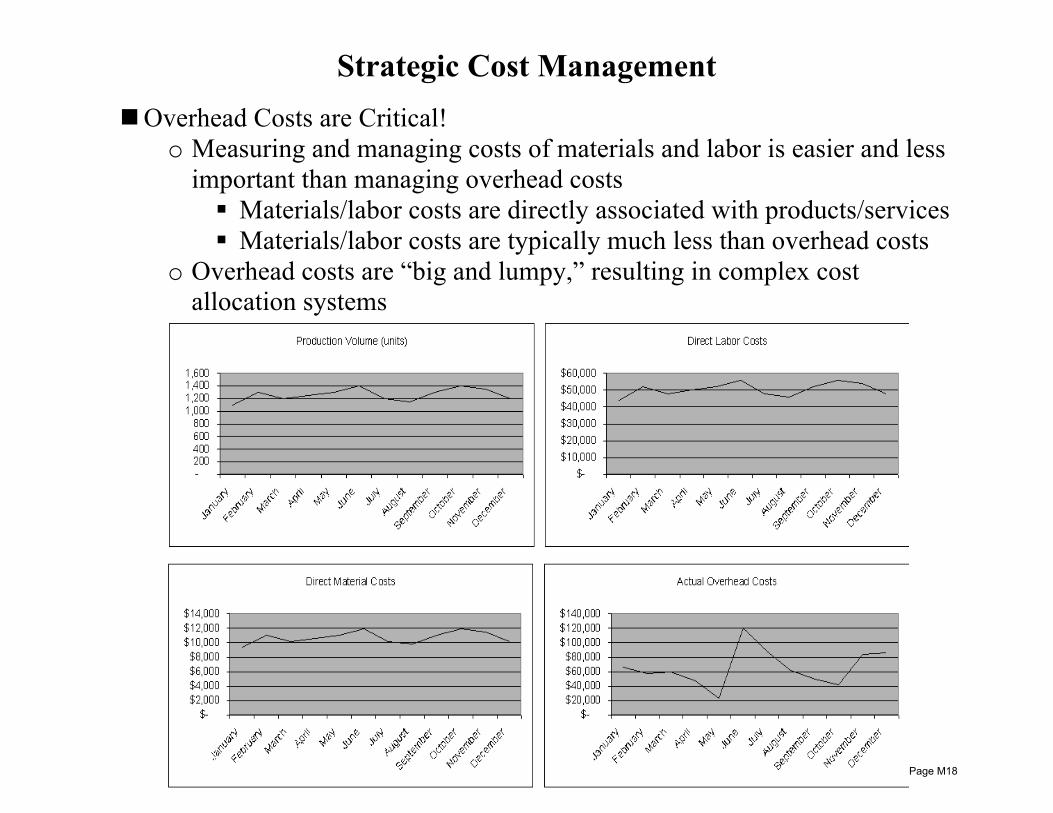

Strategic Cost Management

n Overhead Costs are Critical! o Measuring and managing costs of materials and labor is easier and less

important than managing overhead costs § Materials/labor costs are directly associated with products/services § Materials/labor costs are typically much less than overhead costs

o Overhead costs are “big and lumpy,” resulting in complex cost allocation systems

Page M18

Manufacturing Cost Flows

Work-in-Process

Inventory

xx

Cost of Goods Sold

xx

Wages Payable

xx

xx

x

Finished Goods Inventory

xx xx

Manufacturing Overhead

x x

x x x

x

x x x

xxx

xxx

Raw Materials Inventory

x

xx

x

Page M19

Service Cost Flows

Unbilled Services

xx

Cost of Services

xx

Salaries Payable

xx

xx

x

Service Overhead

x x

x x x

x x x

xxx

xxx

Supplies Inventory

x

Page M20

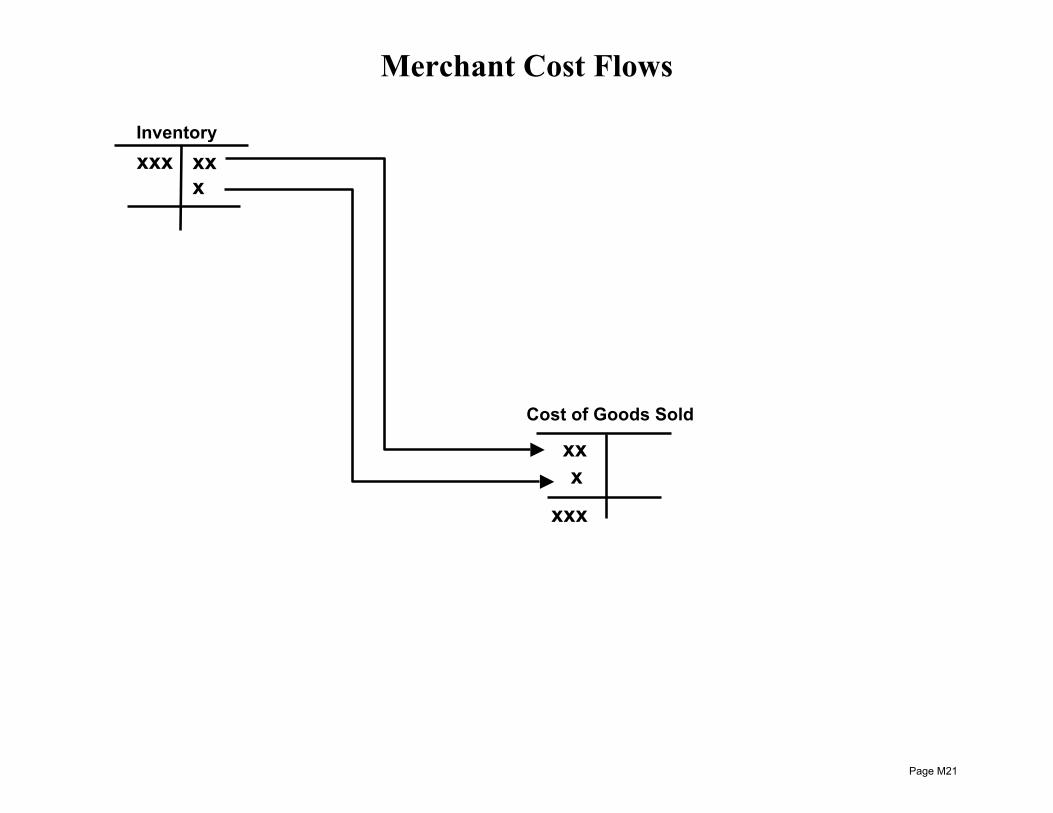

Merchant Cost Flows

Cost of Goods Sold

xx

xx x

x

xxx

xxx Inventory

Page M21

Cost of Goods Manufactured Statement Direct materials costs: Direct materials purchases $ 90,000 Direct materials beginning inventory 14,000 Direct materials ending inventory (16,000) $ 88,000 Direct labor costs 65,000 Manufacturing overhead applied 179,000 Total production costs $332,000 Work-in-process beginning inventory 45,000 Work-in-process ending inventory (13,000) Cost of goods manufactured $364,000 Cost of goods manufactured $364,000 Finished goods beginning inventory 23,000 Finished goods ending inventory (21,000) Cost of goods sold (unadjusted) $366,000 Overapplied manufacturing overhead (9,000) Cost of goods sold (adjusted) $357,000

Page M22

179,000

Work-in-Process Inventory

Cost of Goods Sold

Wages Payable

Finished Goods Inventory

Manufacturing Overhead

14,000 90,000

16,000

Direct Materials Inventory

88,000

45,000 88,000 65,000

179,000

13,000

65,000

8,000 67,000

113,000

9,000

364,000

366,000

23,000 364,000

21,000

366,000

357,000

9,000

Page M23

Accounting for Production Costs

n Job-Order Costing o The production that flows through the system is identifiable (usually

customized per customer) o Direct materials and direct labor costs are assigned directly to jobs as

these costs are used (easy) o Overhead costs are allocated to jobs based on some type of allocation

basis (harder) n Process Costing

o The production that flows through the system is homogenous and is not identifiable

o Direct materials and direct labor costs are assigned to jobs based on the amount of work done during the time period (harder)

o Overhead costs are allocated to jobs based on some type of allocation basis (harder)

Page M24

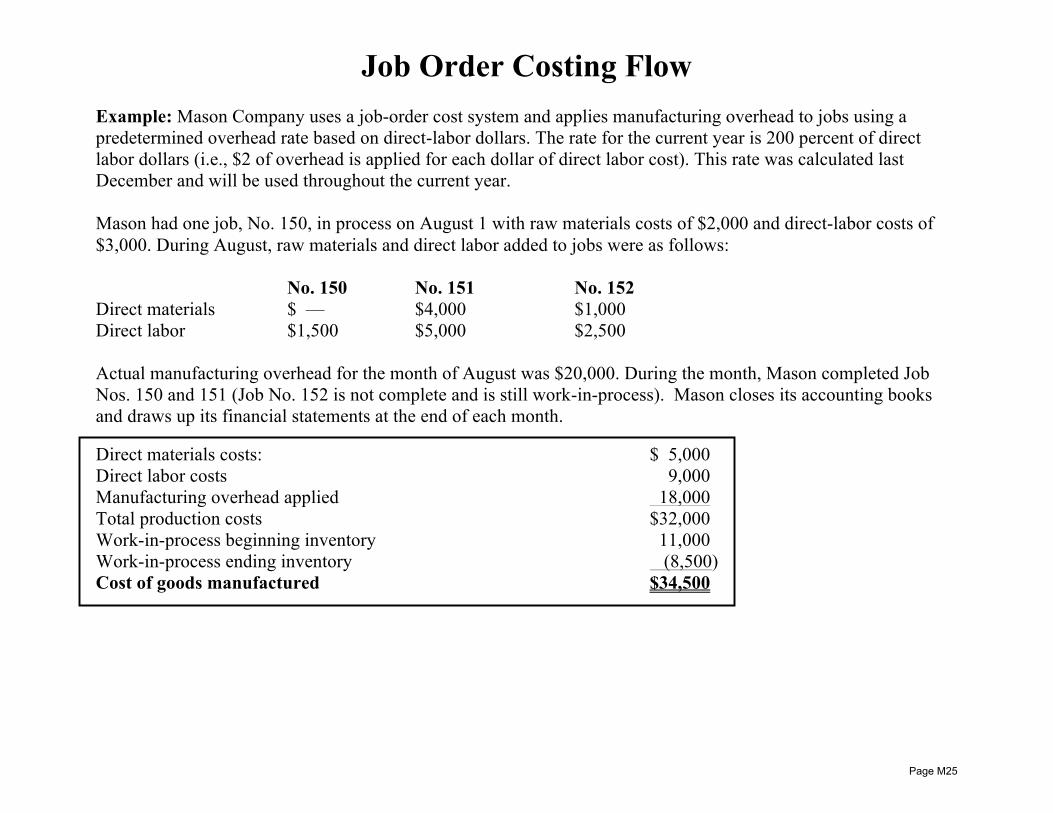

Job Order Costing Flow Example: Mason Company uses a job-order cost system and applies manufacturing overhead to jobs using a predetermined overhead rate based on direct-labor dollars. The rate for the current year is 200 percent of direct labor dollars (i.e., $2 of overhead is applied for each dollar of direct labor cost). This rate was calculated last December and will be used throughout the current year. Mason had one job, No. 150, in process on August 1 with raw materials costs of $2,000 and direct-labor costs of $3,000. During August, raw materials and direct labor added to jobs were as follows: No. 150 No. 151 No. 152 Direct materials $ — $4,000 $1,000 Direct labor $1,500 $5,000 $2,500 Actual manufacturing overhead for the month of August was $20,000. During the month, Mason completed Job Nos. 150 and 151 (Job No. 152 is not complete and is still work-in-process). Mason closes its accounting books and draws up its financial statements at the end of each month. Direct materials costs: $ 5,000 Direct labor costs 9,000 Manufacturing overhead applied 18,000 Total production costs $32,000 Work-in-process beginning inventory 11,000 Work-in-process ending inventory (8,500) Cost of goods manufactured $34,500

Page M25

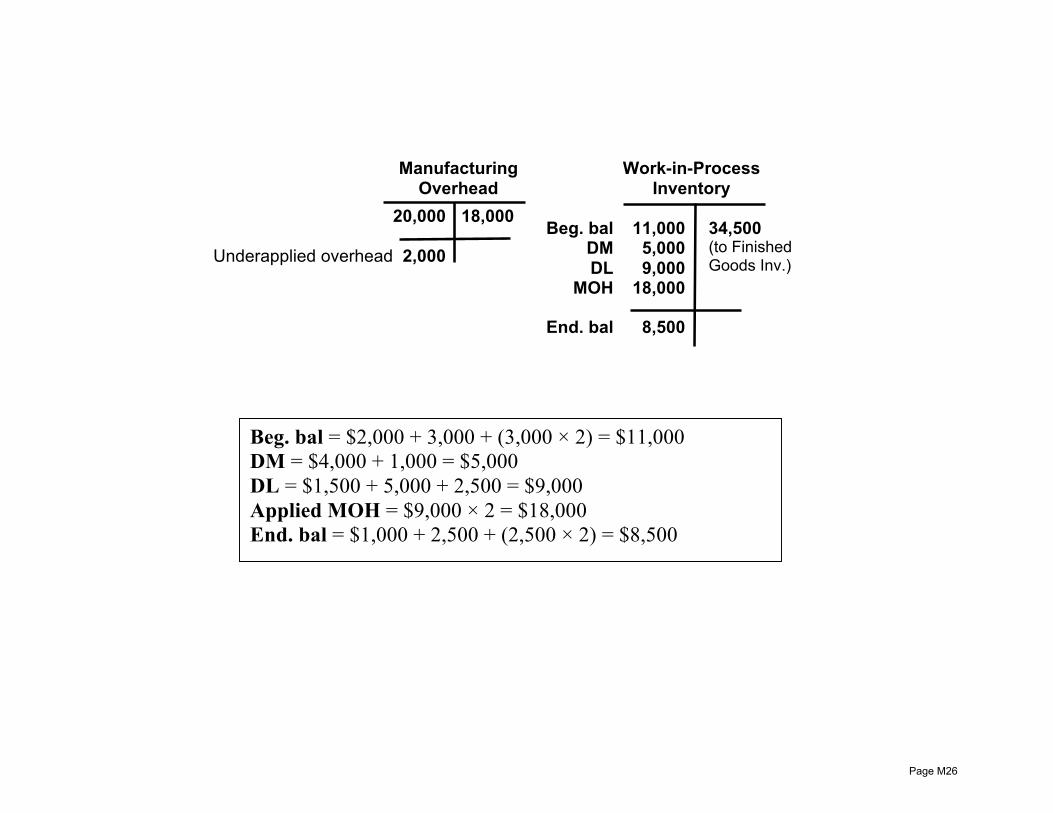

18,000

Manufacturing Overhead

20,000

Underapplied overhead 2,000

Work-in-Process Inventory

11,000 5,000 9,000

18,000

8,500

34,500 (to Finished Goods Inv.)

Beg. bal DM DL

MOH

End. bal

Beg. bal = $2,000 + 3,000 + (3,000 × 2) = $11,000 DM = $4,000 + 1,000 = $5,000 DL = $1,500 + 5,000 + 2,500 = $9,000 Applied MOH = $9,000 × 2 = $18,000 End. bal = $1,000 + 2,500 + (2,500 × 2) = $8,500

Page M26

Life-Cycle Costing (cont.)

n Another Version à The Customer Viewpoint o What does the product cost the customer over the life of the product?

§ Initial purchase price § Upgrade costs § Repair and maintenance costs

o Sometimes called the “Customer Life-Cycle Cost” or “Whole-Life Cost”

n Accounting o These data can not be directly measured and accounted for within the

organization’s system § There are no expenditures

o Requires good market analyses and good estimates o This is very useful competitive analysis information

§ Use to price and market products § Use to assess current and potential markets

n Value Engineering o Most of the life-cycle and customer life-cycle costs are committed in

the R&D process o The theory is that this stage is where real cost control takes place

(versus the production stage) Page M27

Unit A Topic 4 Accumulating and Assigning Overhead Costs

Learning Objectives: • demonstrate an understanding of the fixed and variable nature of overhead expenses • determine the appropriate time frame for both variable and fixed overhead expenses demonstrate an understanding that

overhead rates can be determined in a variety of ways, e.g., plant-wide rates, departmental rates, and individual cost driver rates and describe the benefits and limitations of each of these methods

• demonstrate an understanding of the need to allocate the cost of support departments such as Human Resources or Information Technology to production departments

• understand and use the direct method, the reciprocal method, and the step-down method to allocate support department costs

• identify the components of variable overhead expense • determine the appropriate allocation base for variable overhead expenses • calculate the per unit variable overhead expense • identify the components of fixed overhead expense • identify the appropriate allocation base for fixed overhead expense and demonstrate an understanding that because the

allocation base is generally variable (e.g., direct labor hours), fixed factory overhead is often over or under applied • calculate the fixed overhead application rate • demonstrate an understanding of overhead control accounts, overhead allocation accounts, and the expensing of over

or under applied overhead expenses • compare and contrast traditional overhead allocation with activity-based overhead allocation • calculate overhead expense in an activity-based setting and describe the benefits derived from activity-based overhead

allocation • define the elements of activity-based costing such as cost pool, cost driver, resource driver, activity driver, and value-

added activity • calculate product cost using an activity-based system and compare and analyze the results with costs calculated using a

traditional system

Page M28

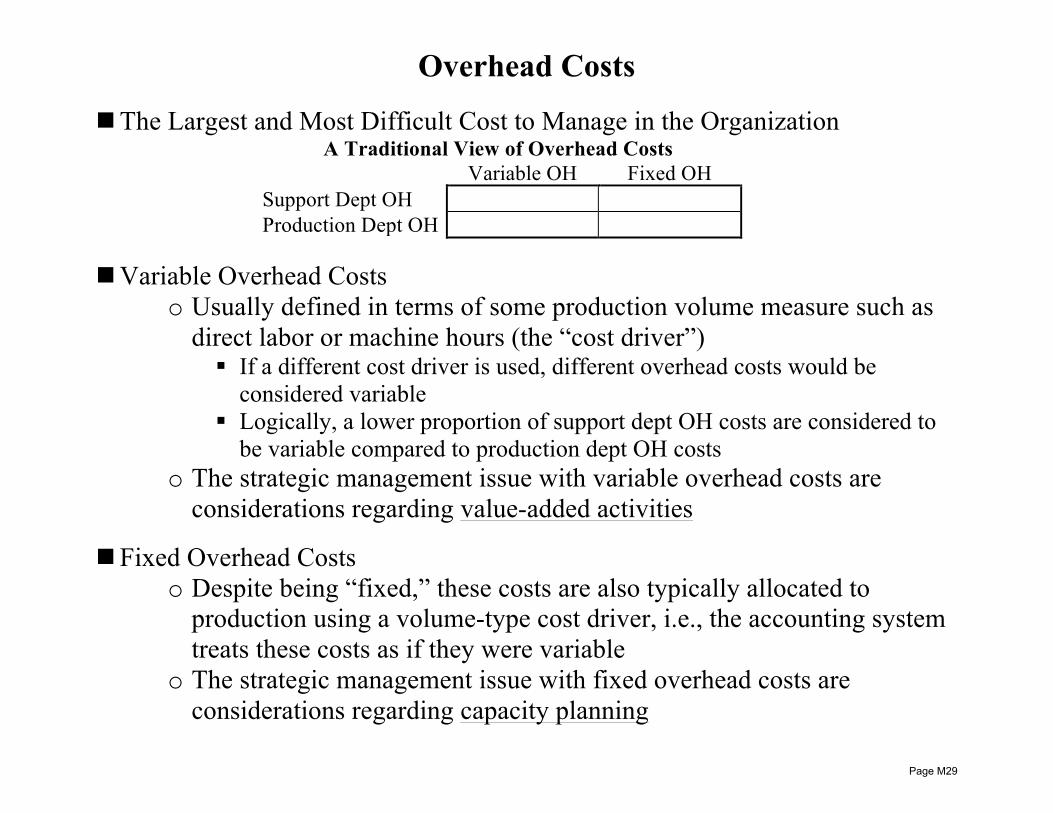

Overhead Costs

n The Largest and Most Difficult Cost to Manage in the Organization A Traditional View of Overhead Costs

Variable OH Fixed OH Support Dept OH Production Dept OH

n Variable Overhead Costs

o Usually defined in terms of some production volume measure such as direct labor or machine hours (the “cost driver”) § If a different cost driver is used, different overhead costs would be

considered variable § Logically, a lower proportion of support dept OH costs are considered to

be variable compared to production dept OH costs o The strategic management issue with variable overhead costs are

considerations regarding value-added activities

n Fixed Overhead Costs o Despite being “fixed,” these costs are also typically allocated to

production using a volume-type cost driver, i.e., the accounting system treats these costs as if they were variable

o The strategic management issue with fixed overhead costs are considerations regarding capacity planning

Page M29

Overhead Costs Allocation

n The Cost Allocation Model o Typically, materials and labor costs can be assigned directly to products

because these costs are direct § Exceptions are process products and joint products

o Only overhead costs are allocated because these costs are indirect o The basic model:

**The activity used in the cost driver rate is based (hopefully) on a relationship that actually exists between the cost pool and the cost object, i.e., the activity “drives” the cost

n The Traditional Single-Stage Plantwide Allocation Process

o Simple, but high potential for inaccuracies

Total Plant Overhead Products

Single Plantwide

Rate

Plantwide Rate = Total Plant Overhead Dollars ÷ Total Activity Basis

Cost Pool

Cost Object

Cost Driver

Cost Driver Rate = Total Cost Pool Dollars ÷ Total Activity Basis

Cost Pool Cost Object

Page M30

Overhead Costs Allocation (cont.)

n The Traditional Two-Stage Departmental Allocation Process

o More complex with multiple cost pools and cost drivers, but still has significant

potential for inaccuracies

n Allocating Support Department Costs (Stage 1) o By definition, all costs are overhead costs o A necessary cost of the product o Support depts. often provide resources to production depts. and other support

depts. § e.g., HR or Information Technology depts. § This complicates the allocation!

Production Departments Products

Support Departments

Allocation Cost Driver

Cost Pools Cost Pools Cost Objects Cost Objects

Production Dept #1

HR Dept

IT Dept

Production Dept #2

Production Dept #3

Janitorial Dept

Page M31

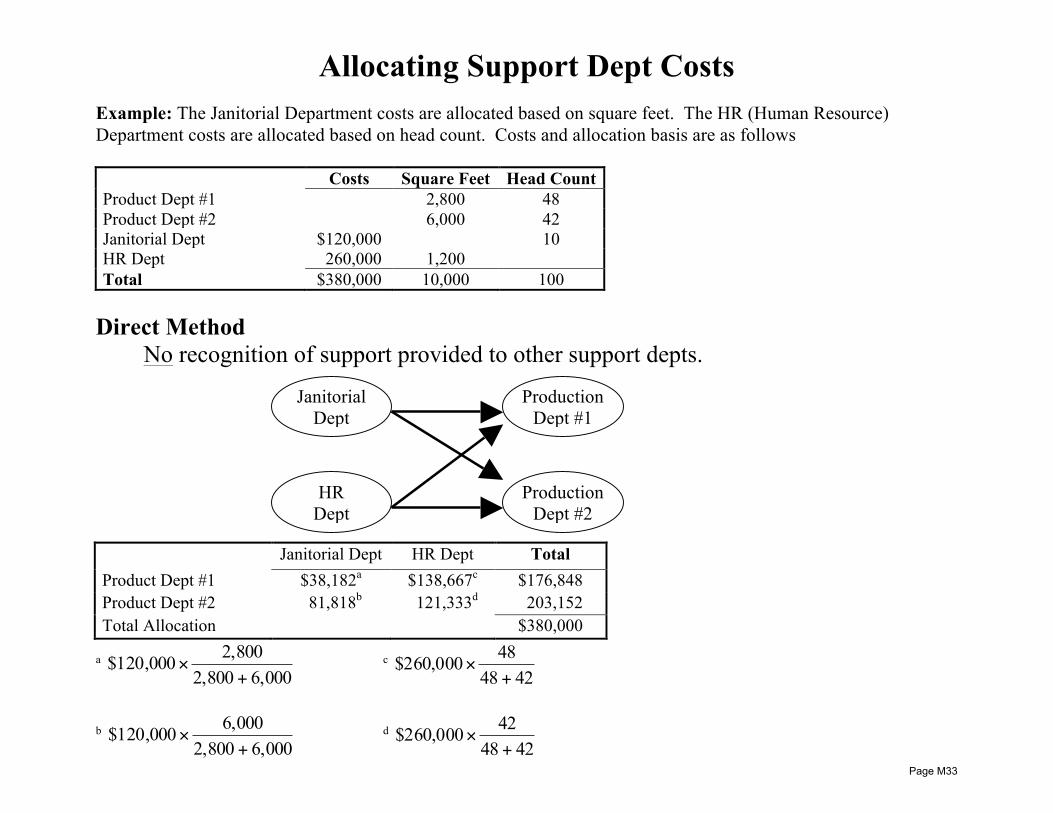

Allocating Support Dept Costs n Direct Method

o No recognition of support provided to other support depts. n Step-Down Method

o Partial recognition of support provided to other support depts. n Reciprocal Method

o Total recognition of support provided to other support depts.

Production Dept #1

HR Dept

Production Dept #2

Janitorial Dept

Production Dept #1

HR Dept

Production Dept #2

Janitorial Dept

Production Dept #1

HR Dept

Production Dept #2

Janitorial Dept

Page M32

Allocating Support Dept Costs Example: The Janitorial Department costs are allocated based on square feet. The HR (Human Resource) Department costs are allocated based on head count. Costs and allocation basis are as follows Costs Square Feet Head Count Product Dept #1 2,800 48 Product Dept #2 6,000 42 Janitorial Dept $120,000 10 HR Dept 260,000 1,200 Total $380,000 10,000 100

Direct Method

No recognition of support provided to other support depts. Janitorial Dept HR Dept Total Product Dept #1 $38,182a $138,667c $176,848 Product Dept #2 81,818b 121,333d 203,152 Total Allocation $380,000

a 6,000 2,800

2,800 $120,000+

× c 42 48

48 $260,000+

×

b

6,000 2,8006,000 $120,000+

× d 42 48

42 $260,000+

×

Production Dept #1

HR Dept

Production Dept #2

Janitorial Dept

Page M33

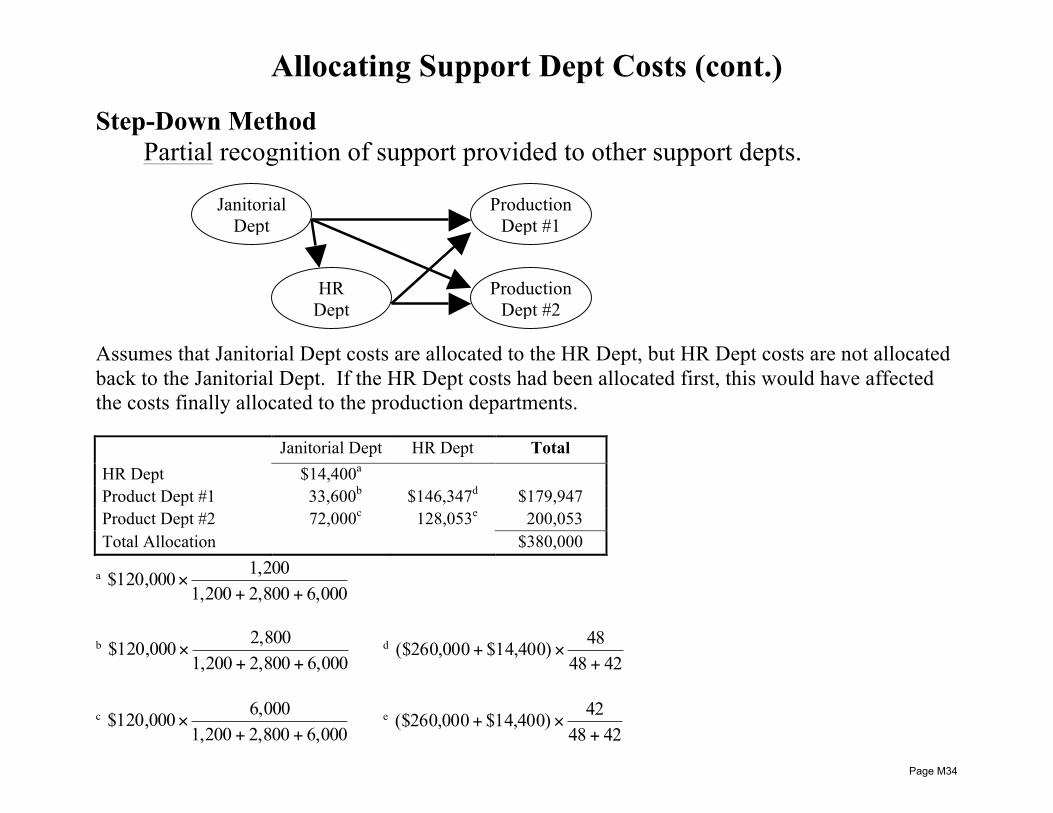

Allocating Support Dept Costs (cont.) Step-Down Method

Partial recognition of support provided to other support depts. Assumes that Janitorial Dept costs are allocated to the HR Dept, but HR Dept costs are not allocated back to the Janitorial Dept. If the HR Dept costs had been allocated first, this would have affected the costs finally allocated to the production departments. Janitorial Dept HR Dept Total HR Dept $14,400a Product Dept #1 33,600b $146,347d $179,947 Product Dept #2 72,000c 128,053e 200,053 Total Allocation $380,000

a 6,000 2,800 1,200

1,200 $120,000++

×

b 6,000 2,800 1,200

2,800 $120,000++

× d 42 48

48 $14,400) ($260,000+

×+

c

6,000 2,800 1,2006,000 $120,000

++× e

42 4842 $14,400) ($260,000+

×+

Production Dept #1

HR Dept

Production Dept #2

Janitorial Dept

Page M34

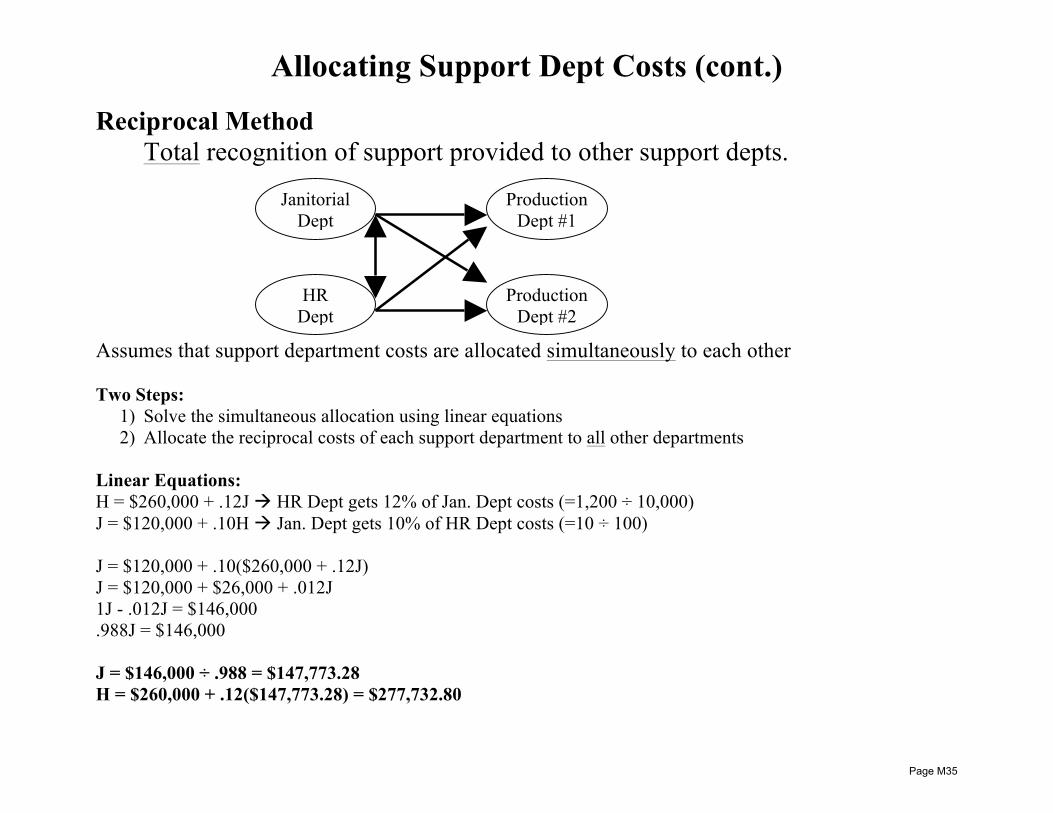

Allocating Support Dept Costs (cont.) Reciprocal Method

Total recognition of support provided to other support depts. Assumes that support department costs are allocated simultaneously to each other Two Steps:

1) Solve the simultaneous allocation using linear equations 2) Allocate the reciprocal costs of each support department to all other departments

Linear Equations: H = $260,000 + .12J à HR Dept gets 12% of Jan. Dept costs (=1,200 ÷ 10,000) J = $120,000 + .10H à Jan. Dept gets 10% of HR Dept costs (=10 ÷ 100) J = $120,000 + .10($260,000 + .12J) J = $120,000 + $26,000 + .012J 1J - .012J = $146,000 .988J = $146,000 J = $146,000 ÷ .988 = $147,773.28 H = $260,000 + .12($147,773.28) = $277,732.80

Production Dept #1

HR Dept

Production Dept #2

Janitorial Dept

Page M35

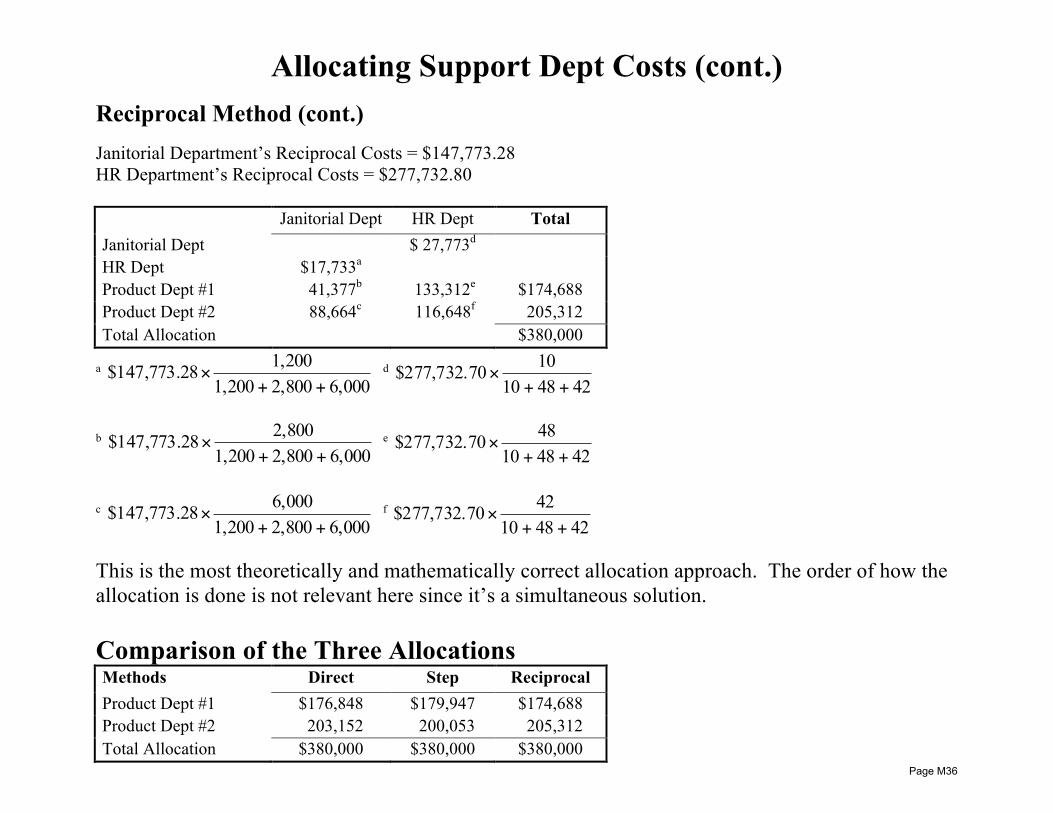

Allocating Support Dept Costs (cont.)

Reciprocal Method (cont.) Janitorial Department’s Reciprocal Costs = $147,773.28 HR Department’s Reciprocal Costs = $277,732.80 Janitorial Dept HR Dept Total Janitorial Dept $ 27,773d HR Dept $17,733a Product Dept #1 41,377b 133,312e $174,688 Product Dept #2 88,664c 116,648f 205,312 Total Allocation $380,000

a 6,000 2,800 1,200

1,200 8$147,773.2++

× d 42 48 10

10 0$277,732.7++

×

b 6,000 2,800 1,200

2,800 8$147,773.2++

× e 42 48 10

48 0$277,732.7++

×

c

6,000 2,800 1,2006,000 8$147,773.2

++× f

42 48 1042 0$277,732.7++

×

This is the most theoretically and mathematically correct allocation approach. The order of how the allocation is done is not relevant here since it’s a simultaneous solution. Comparison of the Three Allocations Methods Direct Step Reciprocal Product Dept #1 $176,848 $179,947 $174,688 Product Dept #2 203,152 200,053 205,312 Total Allocation $380,000 $380,000 $380,000

Page M36

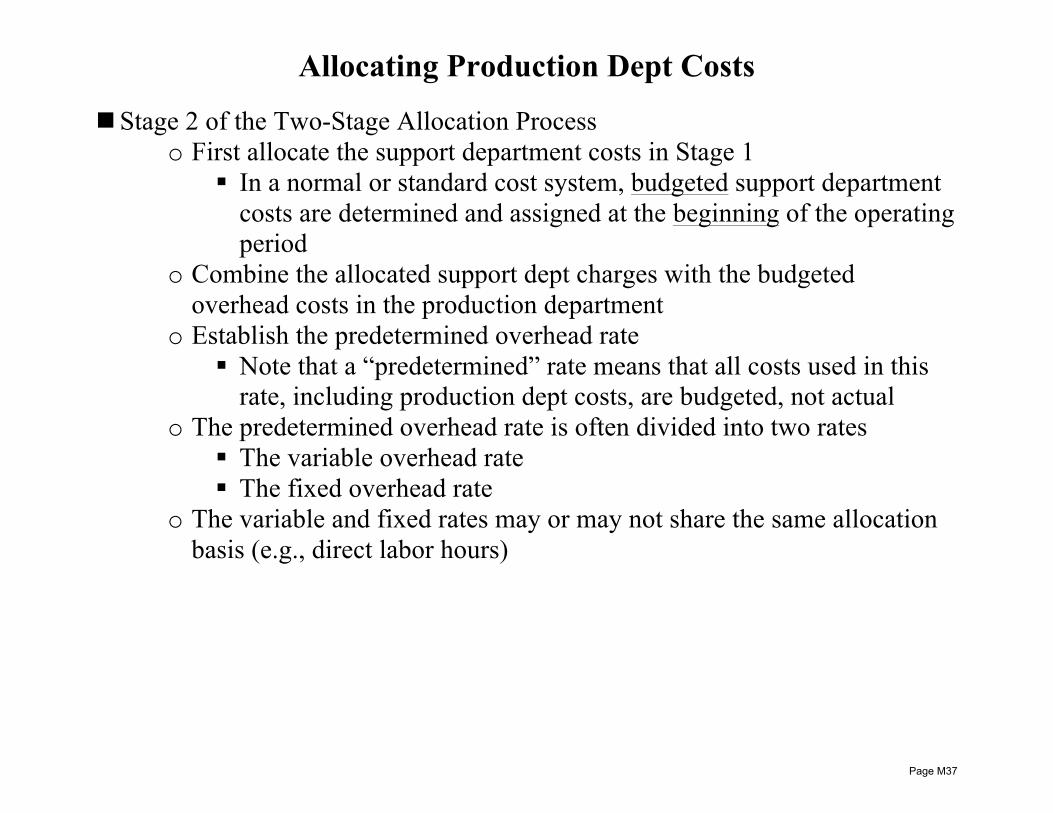

Allocating Production Dept Costs

n Stage 2 of the Two-Stage Allocation Process o First allocate the support department costs in Stage 1

§ In a normal or standard cost system, budgeted support department costs are determined and assigned at the beginning of the operating period

o Combine the allocated support dept charges with the budgeted overhead costs in the production department

o Establish the predetermined overhead rate § Note that a “predetermined” rate means that all costs used in this

rate, including production dept costs, are budgeted, not actual o The predetermined overhead rate is often divided into two rates

§ The variable overhead rate § The fixed overhead rate

o The variable and fixed rates may or may not share the same allocation basis (e.g., direct labor hours)

Page M37

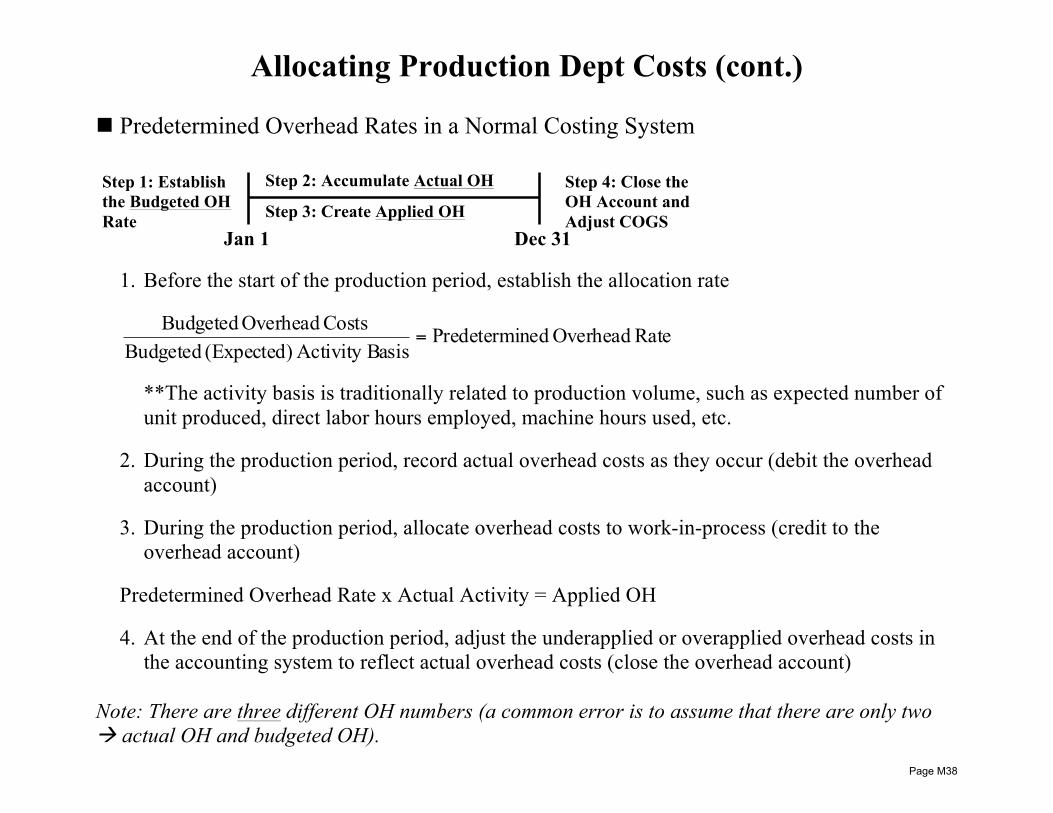

Allocating Production Dept Costs (cont.) n Predetermined Overhead Rates in a Normal Costing System

1. Before the start of the production period, establish the allocation rate

RateOverhead nedPredetermiasisActivity B (Expected) Budgeted

Costs Overhead Budgeted=

**The activity basis is traditionally related to production volume, such as expected number of unit produced, direct labor hours employed, machine hours used, etc.

2. During the production period, record actual overhead costs as they occur (debit the overhead

account) 3. During the production period, allocate overhead costs to work-in-process (credit to the

overhead account)

Predetermined Overhead Rate x Actual Activity = Applied OH 4. At the end of the production period, adjust the underapplied or overapplied overhead costs in

the accounting system to reflect actual overhead costs (close the overhead account) Note: There are three different OH numbers (a common error is to assume that there are only two à actual OH and budgeted OH).

Jan 1 Dec 31

Step 2: Accumulate Actual OH

Step 3: Create Applied OH

Step 1: Establish the Budgeted OH Rate

Step 4: Close the OH Account and Adjust COGS

Page M38

Allocating Production Dept Costs (cont.)

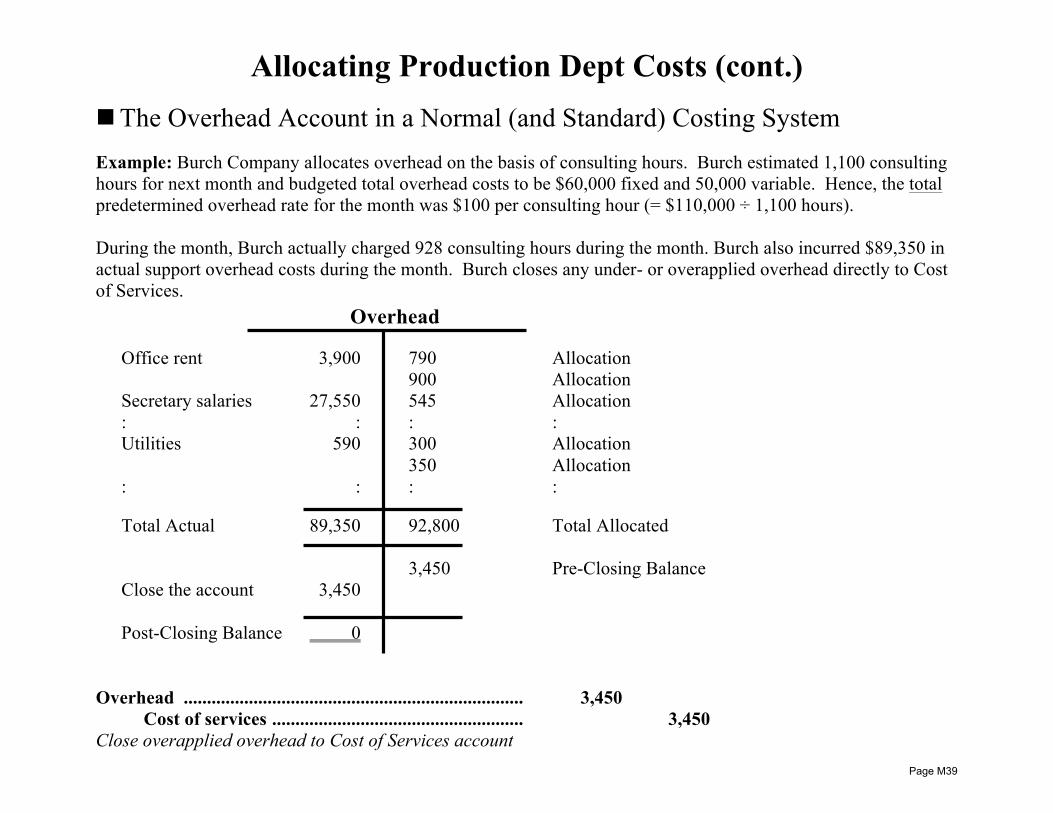

n The Overhead Account in a Normal (and Standard) Costing System Example: Burch Company allocates overhead on the basis of consulting hours. Burch estimated 1,100 consulting hours for next month and budgeted total overhead costs to be $60,000 fixed and 50,000 variable. Hence, the total predetermined overhead rate for the month was $100 per consulting hour (= $110,000 ÷ 1,100 hours). During the month, Burch actually charged 928 consulting hours during the month. Burch also incurred $89,350 in actual support overhead costs during the month. Burch closes any under- or overapplied overhead directly to Cost of Services. Overhead ......................................................................... 3,450 Cost of services ...................................................... 3,450 Close overapplied overhead to Cost of Services account

Total Actual 89,350 92,800 Total Allocated 3,450 Pre-Closing Balance Close the account 3,450 Post-Closing Balance 0

Overhead

Office rent 3,900 790 Allocation 900 Allocation Secretary salaries 27,550 545 Allocation : : : : Utilities 590 300 Allocation

350 Allocation : : : :

Page M39

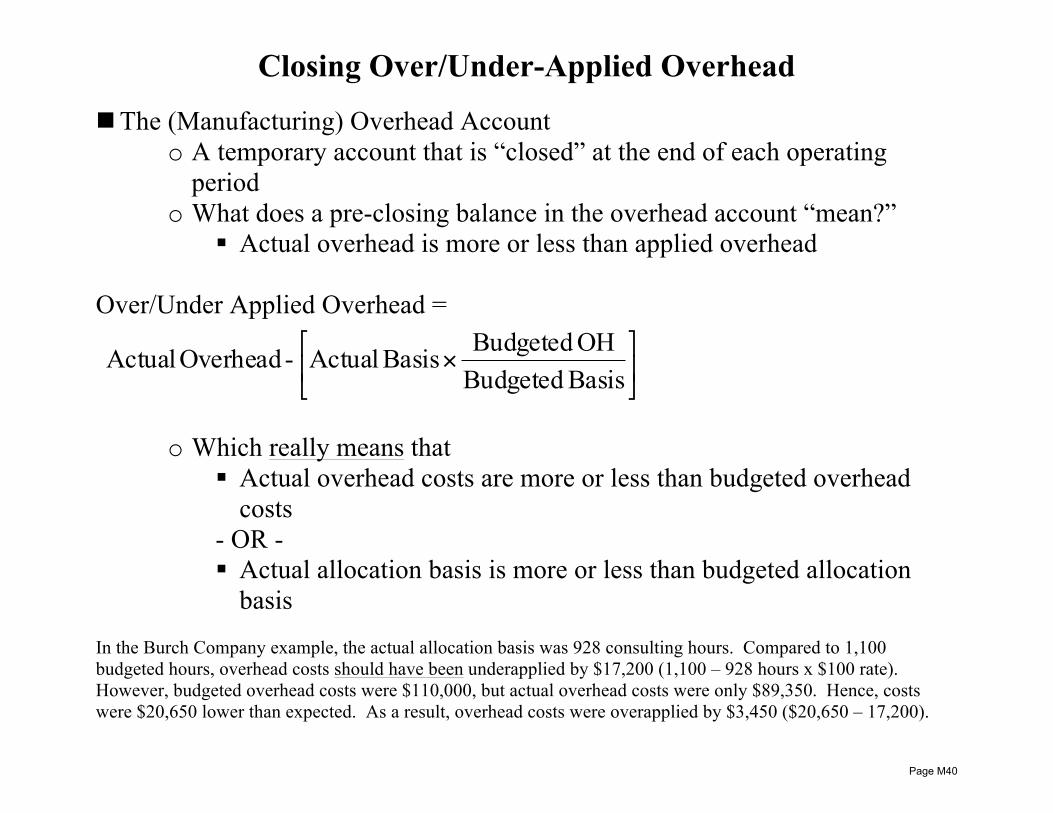

Closing Over/Under-Applied Overhead

n The (Manufacturing) Overhead Account o A temporary account that is “closed” at the end of each operating

period o What does a pre-closing balance in the overhead account “mean?”

§ Actual overhead is more or less than applied overhead

Over/Under Applied Overhead =

⎥⎦

⎤⎢⎣

⎡×

Basis BudgetedOH Budgeted Basis Actual - Overhead Actual

o Which really means that

§ Actual overhead costs are more or less than budgeted overhead costs

- OR - § Actual allocation basis is more or less than budgeted allocation

basis In the Burch Company example, the actual allocation basis was 928 consulting hours. Compared to 1,100 budgeted hours, overhead costs should have been underapplied by $17,200 (1,100 – 928 hours x $100 rate). However, budgeted overhead costs were $110,000, but actual overhead costs were only $89,350. Hence, costs were $20,650 lower than expected. As a result, overhead costs were overapplied by $3,450 ($20,650 – 17,200).

Page M40

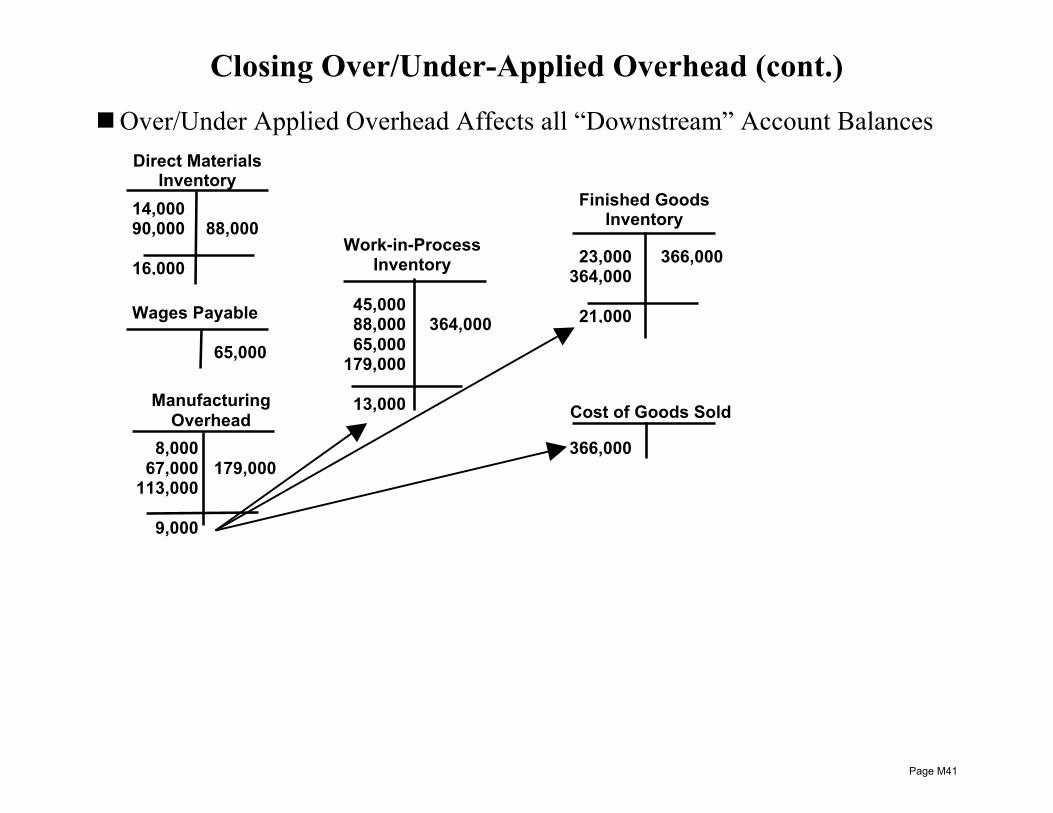

Closing Over/Under-Applied Overhead (cont.)

n Over/Under Applied Overhead Affects all “Downstream” Account Balances

179,000

Work-in-Process Inventory

Cost of Goods Sold

Wages Payable

Finished Goods Inventory

Manufacturing Overhead

14,000 90,000

16,000

Direct Materials Inventory

88,000

45,000 88,000 65,000

179,000

13,000

65,000

8,000 67,000

113,000

9,000

364,000

366,000

23,000 364,000

21,000

366,000

Page M41

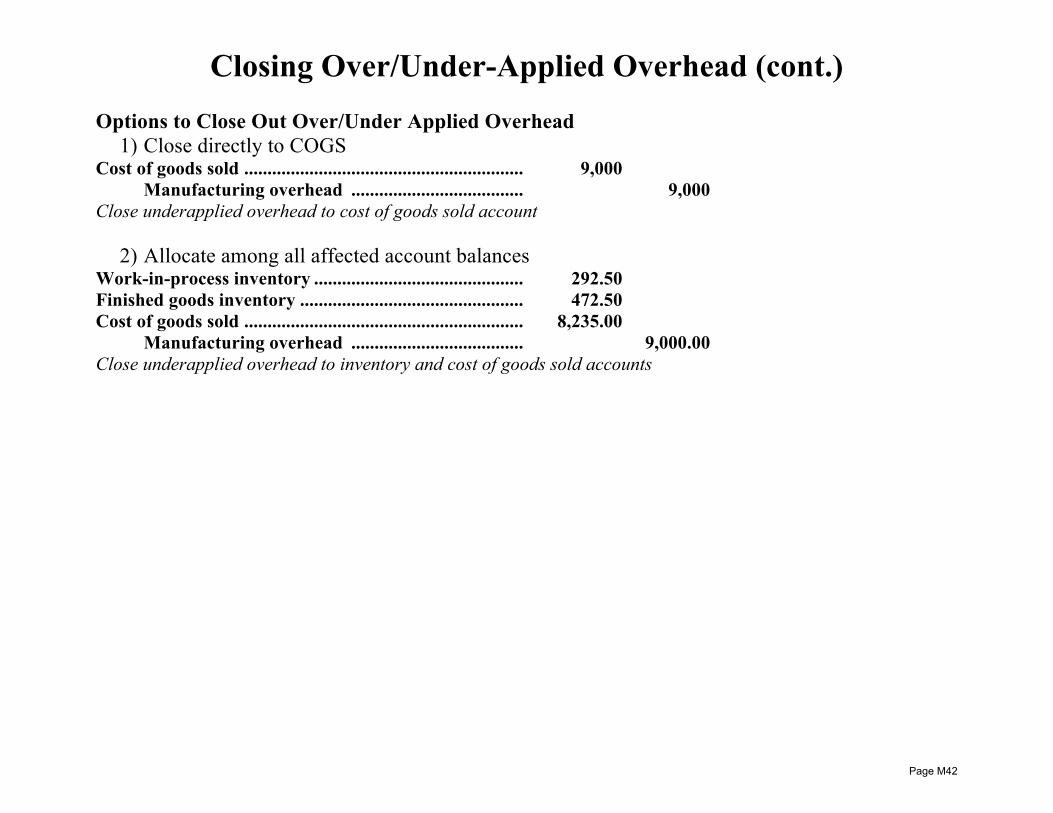

Closing Over/Under-Applied Overhead (cont.) Options to Close Out Over/Under Applied Overhead

1) Close directly to COGS Cost of goods sold ............................................................ 9,000 Manufacturing overhead ..................................... 9,000 Close underapplied overhead to cost of goods sold account

2) Allocate among all affected account balances

Work-in-process inventory ............................................. 292.50 Finished goods inventory ................................................ 472.50 Cost of goods sold ............................................................ 8,235.00 Manufacturing overhead ..................................... 9,000.00 Close underapplied overhead to inventory and cost of goods sold accounts

Page M42

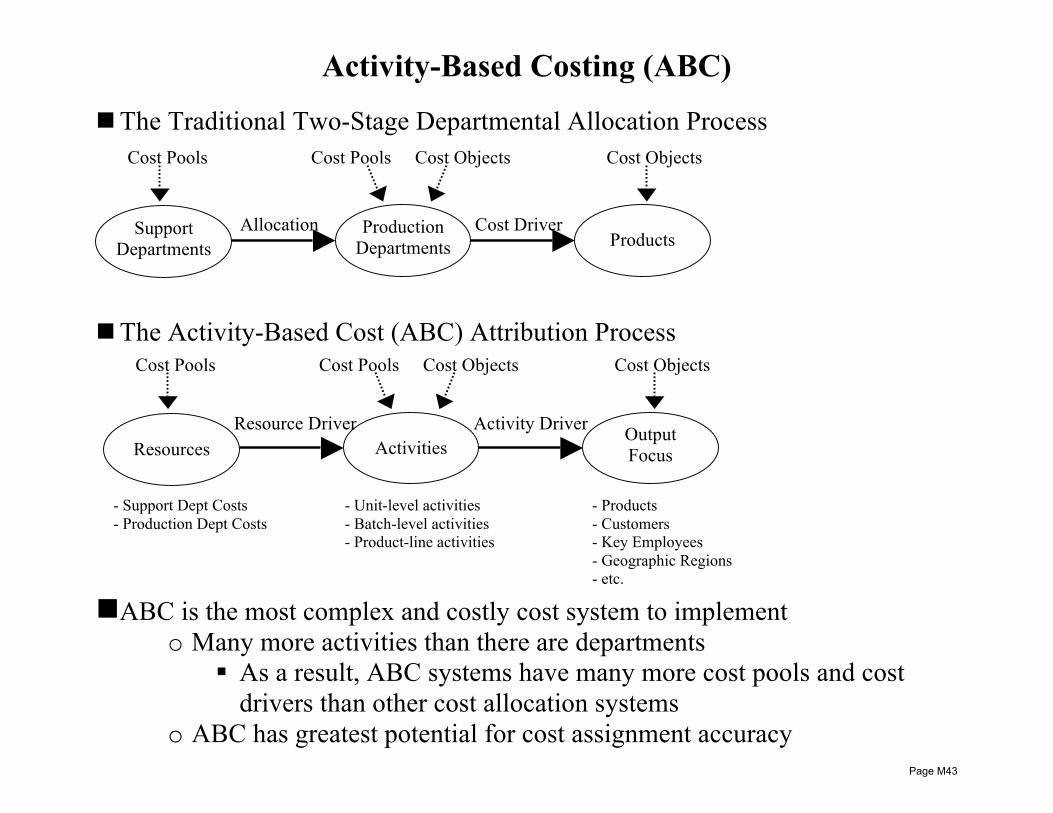

Activity-Based Costing (ABC) n The Traditional Two-Stage Departmental Allocation Process

n The Activity-Based Cost (ABC) Attribution Process

n ABC is the most complex and costly cost system to implement

o Many more activities than there are departments § As a result, ABC systems have many more cost pools and cost

drivers than other cost allocation systems o ABC has greatest potential for cost assignment accuracy

Activities Output Focus Resources

Resource Driver Activity Driver

Cost Pools Cost Pools Cost Objects Cost Objects

- Support Dept Costs - Production Dept Costs

- Unit-level activities - Batch-level activities - Product-line activities

- Products - Customers - Key Employees - Geographic Regions - etc.

Production Departments Products Support

Departments Allocation Cost Driver

Cost Pools Cost Pools Cost Objects Cost Objects

Page M43

Motivation for ABC n Simple is Not Always Best!

o Simple cost allocation systems (i.e., plantwide or departmental) can do great damage in complex organizations with many diversified product lines

n Activity Focus

o Emphasizing an activity view of the organization (versus a departmental view) has the advantage of identifying value-added and non-valued-added activities

n Product Cost Cross-Subsidization

o Costs that are created as a result of the demands of one product are assigned to another product

o In other words, the costs of some products are being subsidized by other products

n Product Cost “Death Spiral”

o Cost having no relationship to products are still allocated “like peanut butter” across all products

o Because of an erroneous income loss reports, products are dropped

n Severe operational and strategic results take place when accounting systems report some products as more or less costly than actuality

Page M44

ABC Hierarchy n The Object of ABC is to Identify One-dimensional Relationships between

Costs and Activities

o Many activities do not have one-to-one relationships with production output volumes

o Many activities do have one-to-one relationships with the volume of batches (e.g., quality inspection) or the number of product lines (e.g., engineering design)

Activities Output Focus Resources

Resource Driver Activity Driver

Total Production Costs

Cost Traceable to Specific Products • Unit Level Activities: direct labor, direct

materials, utility costs, etc. • Batch Level Activities: purchase ordering,

setups, materials handling, etc. • Product-Line Level Activities: engineering,

inventory management, training, etc.

Common Costs • Facility Level Activities: plant security,

property taxes, general administration, etc. Page M45

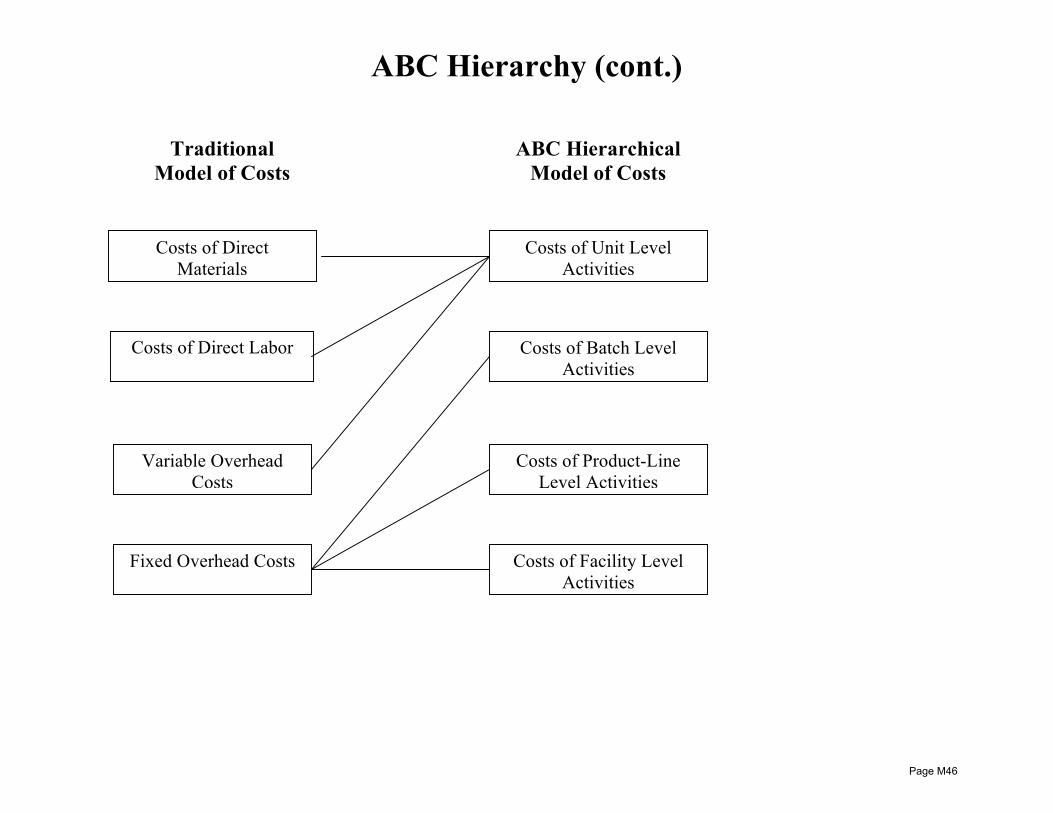

ABC Hierarchy (cont.)

Costs of Direct Materials

Costs of Direct Labor

Variable Overhead Costs

Fixed Overhead Costs Costs of Facility Level Activities

Costs of Product-Line Level Activities

Costs of Batch Level Activities

Costs of Unit Level Activities

Traditional Model of Costs

ABC Hierarchical Model of Costs

Page M46

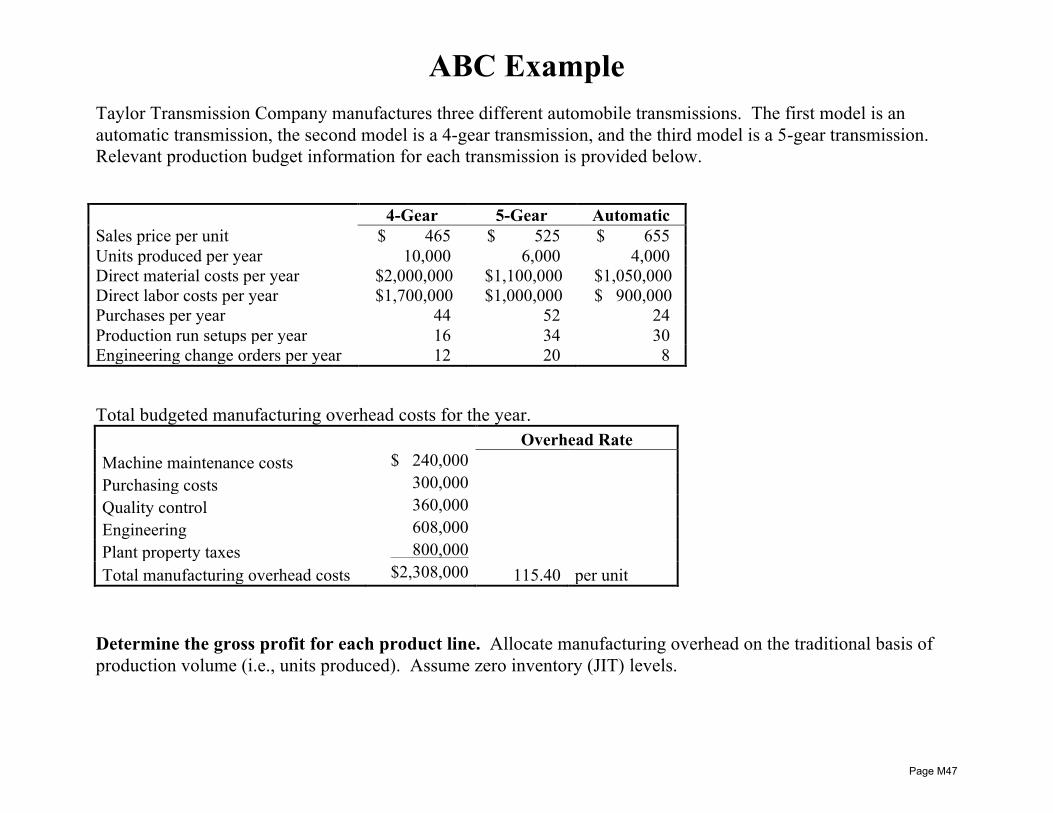

ABC Example Taylor Transmission Company manufactures three different automobile transmissions. The first model is an automatic transmission, the second model is a 4-gear transmission, and the third model is a 5-gear transmission. Relevant production budget information for each transmission is provided below. 4-Gear 5-Gear Automatic Sales price per unit $ 465 $ 525 $ 655 Units produced per year 10,000 6,000 4,000 Direct material costs per year $2,000,000 $1,100,000 $1,050,000 Direct labor costs per year $1,700,000 $1,000,000 $ 900,000 Purchases per year 44 52 24 Production run setups per year 16 34 30 Engineering change orders per year 12 20 8 Total budgeted manufacturing overhead costs for the year. Overhead Rate Machine maintenance costs $ 240,000 Purchasing costs 300,000 Quality control 360,000 Engineering 608,000 Plant property taxes 800,000 Total manufacturing overhead costs $2,308,000 115.40 per unit

Determine the gross profit for each product line. Allocate manufacturing overhead on the traditional basis of production volume (i.e., units produced). Assume zero inventory (JIT) levels.

Page M47

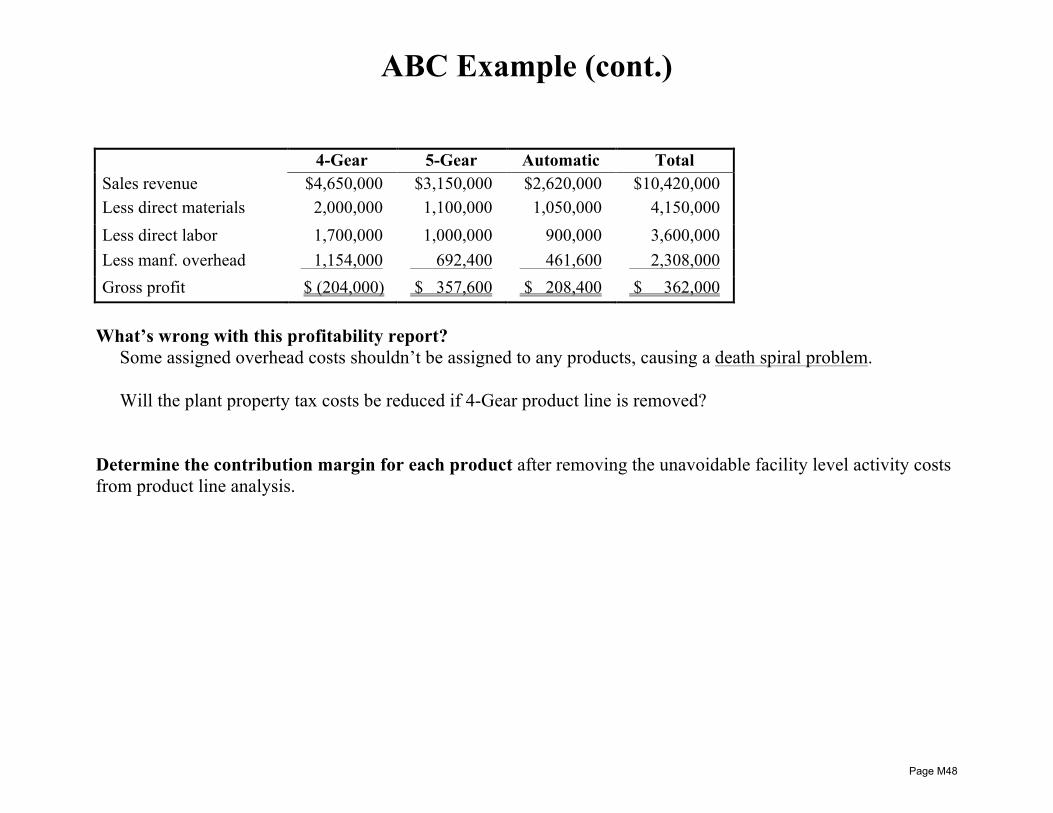

ABC Example (cont.) 4-Gear 5-Gear Automatic Total Sales revenue $4,650,000 $3,150,000 $2,620,000 $10,420,000 Less direct materials 2,000,000 1,100,000 1,050,000 4,150,000 Less direct labor 1,700,000 1,000,000 900,000 3,600,000 Less manf. overhead 1,154,000 692,400 461,600 2,308,000 Gross profit $ (204,000) $ 357,600 $ 208,400 $ 362,000

What’s wrong with this profitability report?

Some assigned overhead costs shouldn’t be assigned to any products, causing a death spiral problem. Will the plant property tax costs be reduced if 4-Gear product line is removed?

Determine the contribution margin for each product after removing the unavoidable facility level activity costs from product line analysis.

Page M48

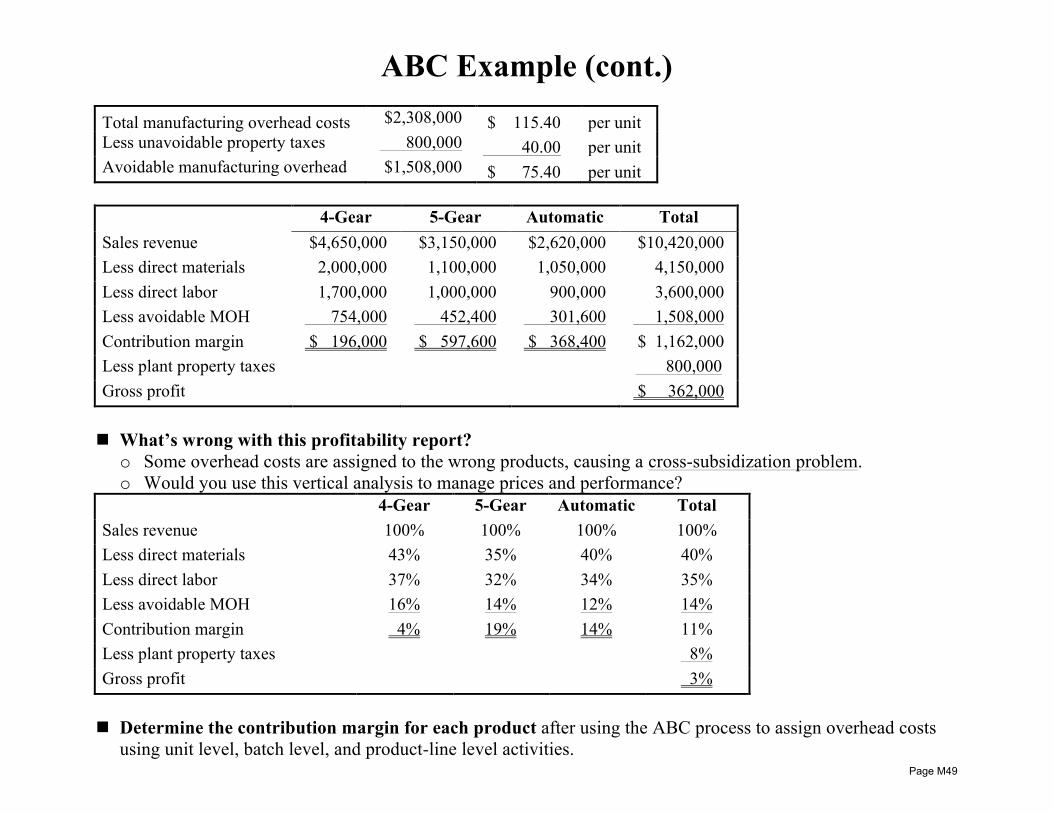

ABC Example (cont.) Total manufacturing overhead costs $2,308,000 $ 115.40 per unit Less unavoidable property taxes 800,000 40.00 per unit Avoidable manufacturing overhead $1,508,000 $ 75.40 per unit

4-Gear 5-Gear Automatic Total Sales revenue $4,650,000 $3,150,000 $2,620,000 $10,420,000 Less direct materials 2,000,000 1,100,000 1,050,000 4,150,000 Less direct labor 1,700,000 1,000,000 900,000 3,600,000 Less avoidable MOH 754,000 452,400 301,600 1,508,000 Contribution margin $ 196,000 $ 597,600 $ 368,400 $ 1,162,000 Less plant property taxes 800,000 Gross profit $ 362,000

n What’s wrong with this profitability report?

o Some overhead costs are assigned to the wrong products, causing a cross-subsidization problem. o Would you use this vertical analysis to manage prices and performance?

4-Gear 5-Gear Automatic Total Sales revenue 100% 100% 100% 100% Less direct materials 43% 35% 40% 40% Less direct labor 37% 32% 34% 35% Less avoidable MOH 16% 14% 12% 14% Contribution margin 4% 19% 14% 11% Less plant property taxes 8% Gross profit 3%

n Determine the contribution margin for each product after using the ABC process to assign overhead costs

using unit level, batch level, and product-line level activities. Page M49

ABC Example (cont.) Overhead Rates

Machine maintenance costs $ 240,000 12.00 per unit (unit level)

Purchasing costs 300,000 2,500.00 per purchase (batch level)

Quality control 360,000 4,500.00 per setup (batch level)

Engineering 608,000 15,200.00 per change (product-line level) Total avoidable MOH costs $1,508,000

4-Gear 5-Gear Automatic Total Sales revenue $4,650,000 $3,150,000 $2,620,000 $10,420,000 Less direct materials 2,000,000 1,100,000 1,050,000 4,150,000 Less direct labor 1,700,000 1,000,000 900,000 3,600,000 Less maintenance overhead 120,000 72,000 48,000 240,000 Less purchasing overhead 110,000 130,000 60,000 300,000 Less quality control overhead 72,000 153,000 135,000 360,000 Less engineering overhead 182,400 304,000 121,600 608,000 Contribution margin $ 465,600 $ 391,000 $ 305,400 $ 1,162,000 Less plant property taxes 800,000 Gross profit $ 362,000

Page M50

ABC Example (cont.) 4-Gear 5-Gear Automatic Total Sales revenue 100% 100% 100% 100% Less direct materials 43% 35% 40% 40% Less direct labor 37% 32% 34% 35% Less maintenance overhead 3% 2% 2% 2% Less purchasing overhead 2% 4% 2% 3% Less quality control overhead 2% 5% 5% 3% Less engineering overhead 4% 10% 5% 6% Contribution margin 10% 12% 12% 11% Less plant property taxes 8% Gross profit 3%

Is this information useful for management?

Page M51

Unit B Topic 5 Behavioral Issues in Developing Budgets and Standards

Learning Objectives: • differentiate between authoritative (top-down) and participative (bottom-up) processes for developing budgets and

standards • identify the advantages and disadvantages of authoritative budget/standards development • describe the likely behavior of employees responsible for implementing and achieving authoritative budgets and

standards • describe the role that top management should play in an effective participative budget process • identify the advantages and disadvantages of participative budget and standards development • describe the likely behavior of employers responsible for implementing and achieving participative budgets and

standards • demonstrate an understanding of the role that communication plays in effective budgeting and standard setting • define the term budgetary slack • describe how budgetary slack can have both positive and negative effects on the budgeting process • describe the behavioral issues that should be considered when adopting ideal (theoretical) standards • describe the likely behavior of employees being measured by practical (currently attainable) standards • recognize that feedback provides the link between planning, control, and evaluation • recognize that the timing and frequency of feedback is dependent on how critical the measures are to the success of the

business • demonstrate an understanding of the purposes of feedback and alternative means of feedback such as reports,

interviews, and team meetings

Page M52

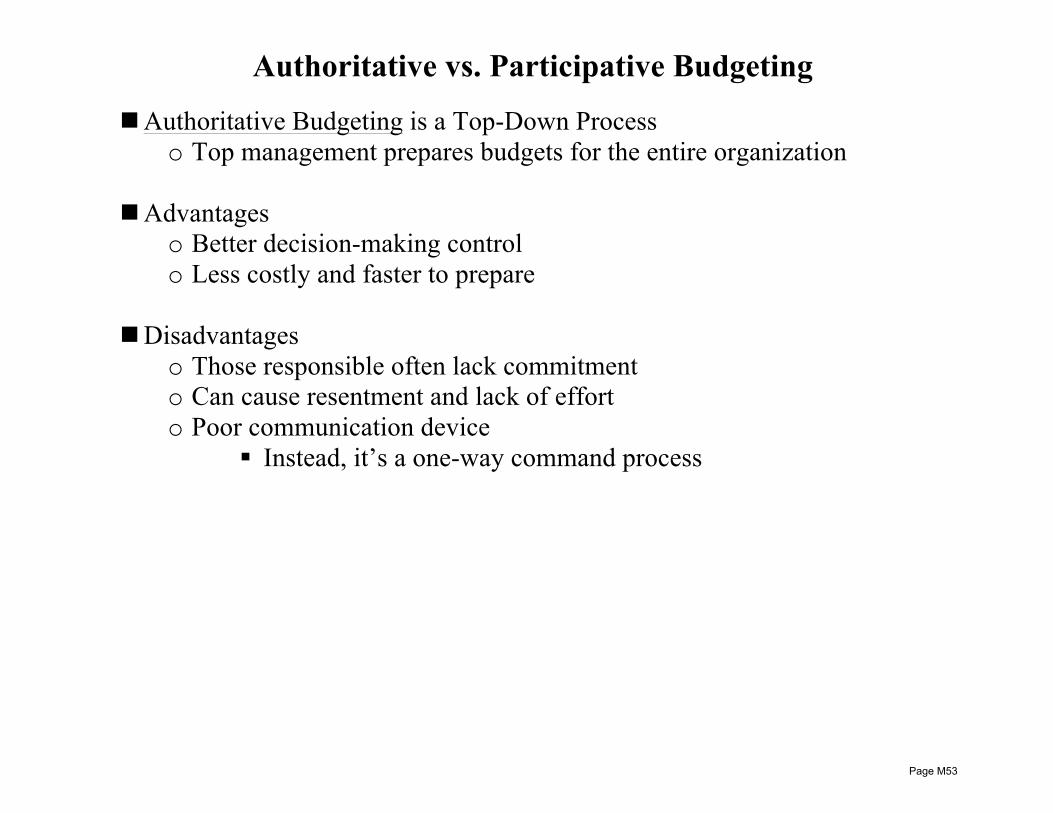

Authoritative vs. Participative Budgeting

n Authoritative Budgeting is a Top-Down Process o Top management prepares budgets for the entire organization

n Advantages o Better decision-making control o Less costly and faster to prepare

n Disadvantages o Those responsible often lack commitment o Can cause resentment and lack of effort o Poor communication device

§ Instead, it’s a one-way command process

Page M53

Authoritative vs. Participative Budgeting (cont.)

n Participative Budgeting is a Bottom-Up Process o Involves everyone (lower- and mid-level managers)

n Advantages o Encourages goal congruence o Better commitment to the budget o Better information on which to prepare the budget o Provides communication of issues to top management

n Disadvantages o Costly and time-intensive o Political maneuvering o Employees may perceive top management as uninvolved and uncommitted to

the budget o Creation of budgetary slack

n Effective Budgeting tries to combines both Authoritative and Participative Processes

o Typical process 1. Divisions prepare initial budgets 2. Top management reviews and comments 3. Divisions make revisions

Page M54

Budgeting Behavior

n Budgetary Slack o Excess of resource inputs requested over the actual resources necessary o Shortage of production outputs committed below the actual outputs

possible

n Managing Budgetary Slack o Significant involvement by top management in understanding the

business processes, including resource inputs and production outputs, can help minimize slack

o A pattern by top management of consistently adjusting submitted budgets can encourage slack

Page M55

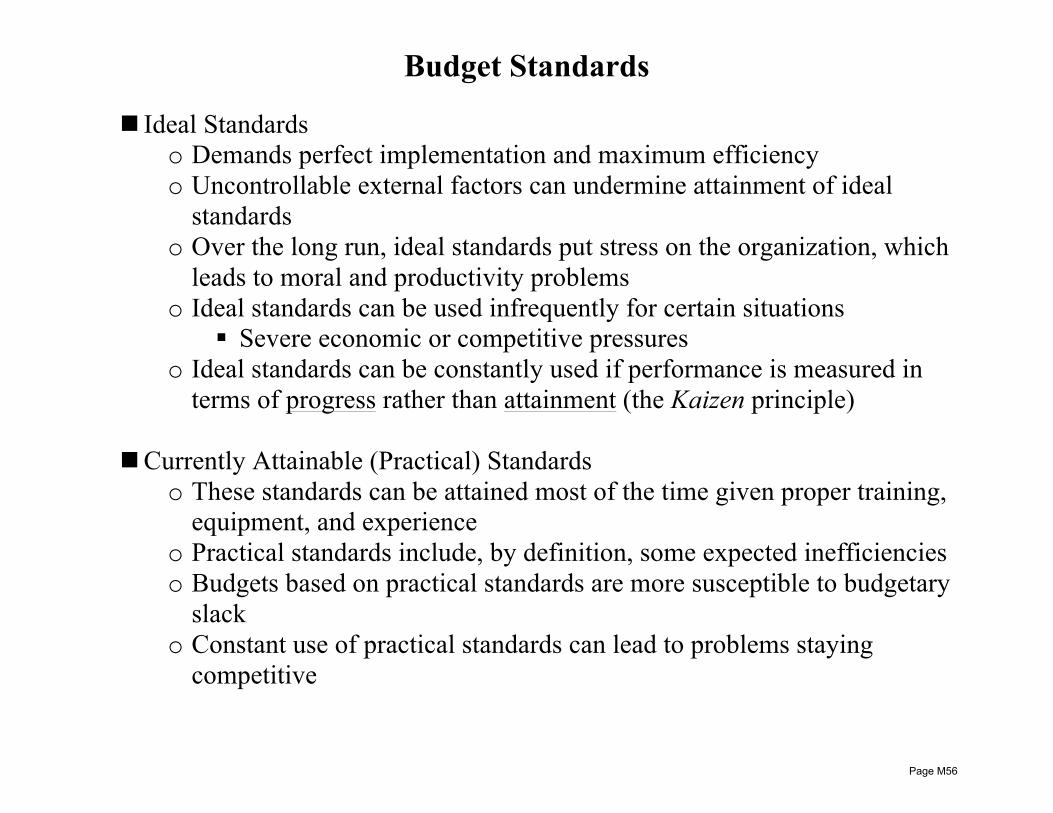

Budget Standards

n Ideal Standards o Demands perfect implementation and maximum efficiency o Uncontrollable external factors can undermine attainment of ideal

standards o Over the long run, ideal standards put stress on the organization, which

leads to moral and productivity problems o Ideal standards can be used infrequently for certain situations

§ Severe economic or competitive pressures o Ideal standards can be constantly used if performance is measured in

terms of progress rather than attainment (the Kaizen principle)

n Currently Attainable (Practical) Standards o These standards can be attained most of the time given proper training,

equipment, and experience o Practical standards include, by definition, some expected inefficiencies o Budgets based on practical standards are more susceptible to budgetary

slack o Constant use of practical standards can lead to problems staying

competitive

Page M56

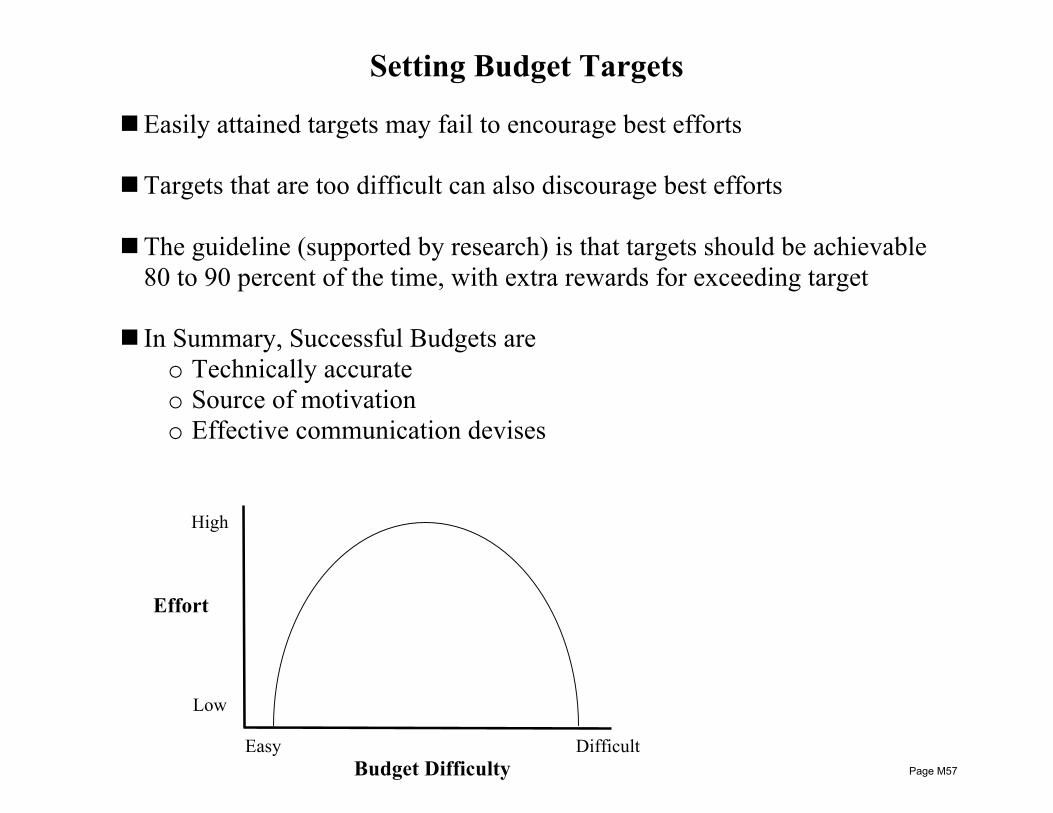

Setting Budget Targets

n Easily attained targets may fail to encourage best efforts n Targets that are too difficult can also discourage best efforts

n The guideline (supported by research) is that targets should be achievable

80 to 90 percent of the time, with extra rewards for exceeding target n In Summary, Successful Budgets are

o Technically accurate o Source of motivation o Effective communication devises

Effort

High

Low

Easy Difficult Budget Difficulty Page M57

Unit B Topic 1 Planning Processes

Learning Objectives: • demonstrate an understanding that strategic planning determines the path an organization chooses for attaining its

long-term goals and missions • identify the time frame appropriate for a strategic plan • identify the external factors that should be analyzed during the strategic planning process and understand how this

analysis leads to recognition of organizational opportunities, limitations, and threats • identify the internal factors that should be analyzed during the strategic planning process and understand how this

analysis leads to recognition of organizational strengths, weaknesses, and competitive advantages • demonstrate an understanding that the analysis of external and internal factors leads to the development of the overall

organizational mission and that this mission leads to the formulation of long-term business objectives such as business diversification, the addition or deletion of product lines, or the penetration of new markets

• recognize the role of capital budgeting and capacity planning in the strategic planning process • recognize that short-term objectives, tactics for achieving these objectives, and operational planning (master budget)

must be congruent with the strategic plan and contribute to the achievement of long-term strategic goals • define value chain analysis • identify the steps in value chain analysis • show how value chain analysis is used to better understand a firm’s competitive advantage • define contingency planning • demonstrate an understanding of the importance of contingency planning, particularly where changes in external

factors might adversely impact strategic plans

Page M58

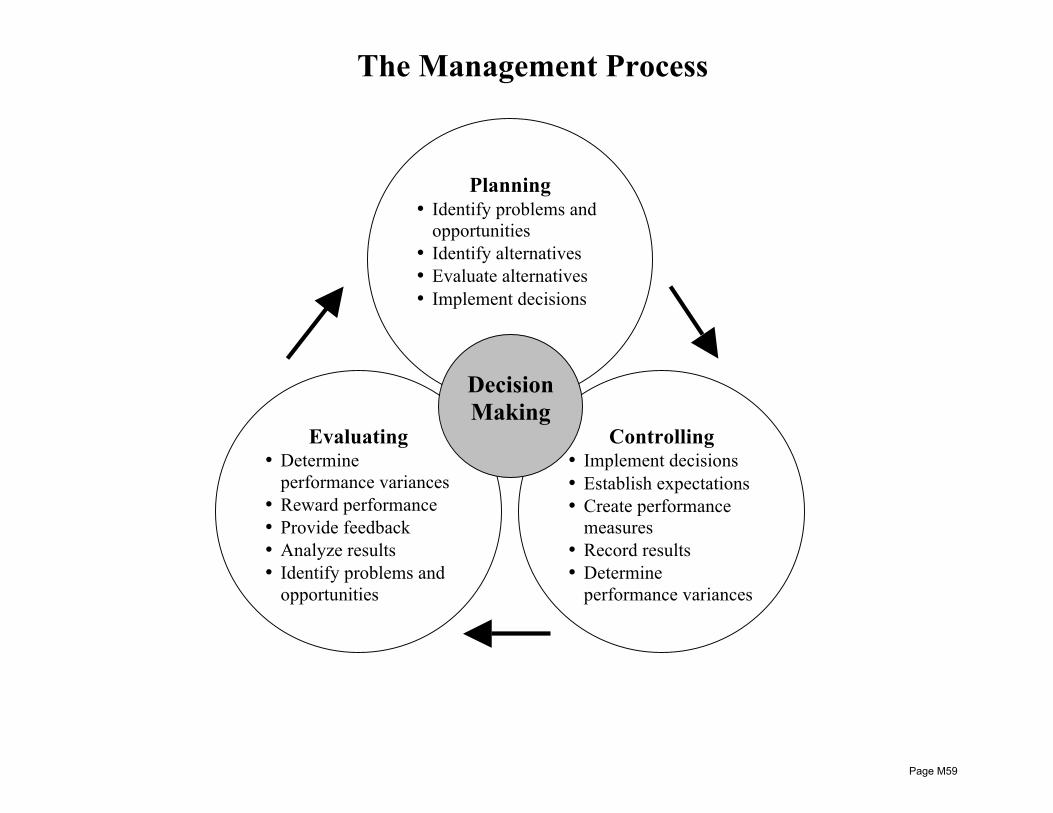

The Management Process

Planning • Identify problems and

opportunities • Identify alternatives • Evaluate alternatives • Implement decisions

Evaluating • Determine

performance variances • Reward performance • Provide feedback • Analyze results • Identify problems and

opportunities • Learn!

Controlling • Implement decisions • Establish expectations • Create performance

measures • Record results • Determine

performance variances

Decision Making

Page M59

Planning

n Long-Run Planning (3- to 5-year horizon, or more) o Strategic Planning

§ Executive-level decision making § Assess the competitive market (external) and organization mission

(internal) § Formulate the action steps

o Capital Budgeting § With strategic plans in place, decisions regarding long-term capital

assets § Sometimes called structure planning and purchase

n Short-Run Planning (current period horizon) o Production and process prioritization

§ With capital structure commitments in place, decisions regarding how to maximize the return on capital investments

§ Results in prioritized goods and services for the current market o Operational budgeting (profit planning)

§ With current period priorities in place, development of operational budgets and schedules

§ Used to establish and communicate daily/weekly/monthly goals (i.e., standards)

Page M60

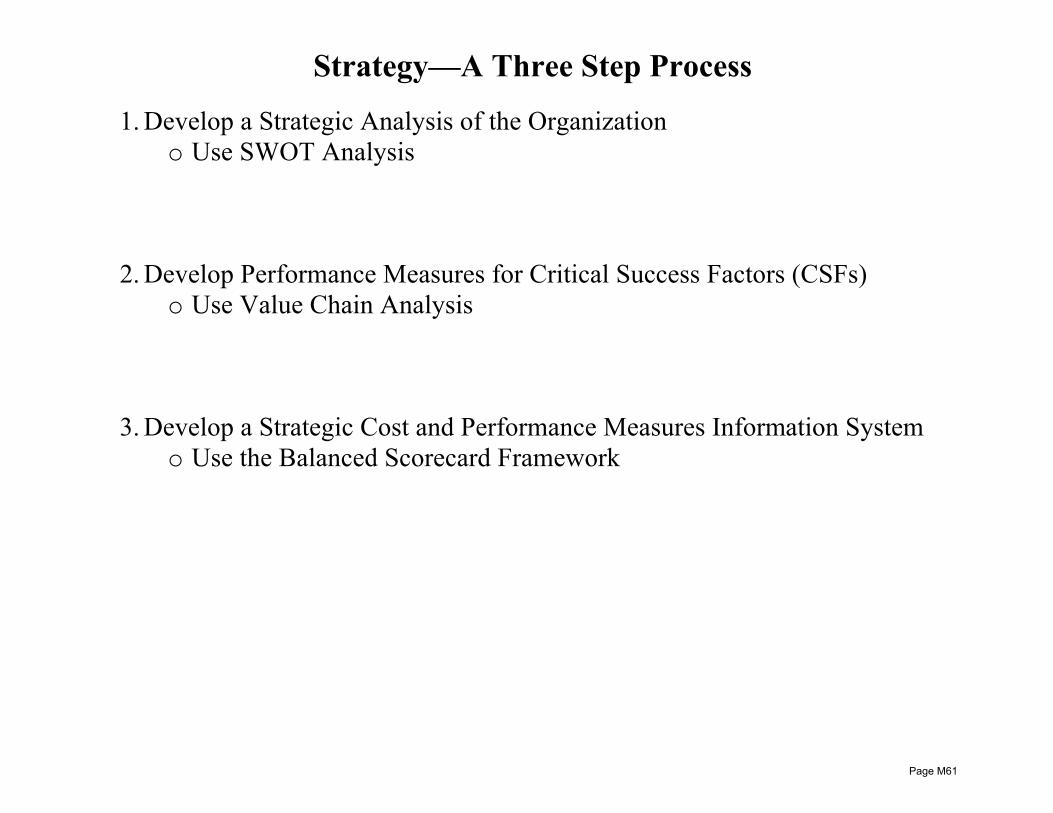

Strategy—A Three Step Process

1. Develop a Strategic Analysis of the Organization o Use SWOT Analysis

2. Develop Performance Measures for Critical Success Factors (CSFs) o Use Value Chain Analysis

3. Develop a Strategic Cost and Performance Measures Information System o Use the Balanced Scorecard Framework

Page M61

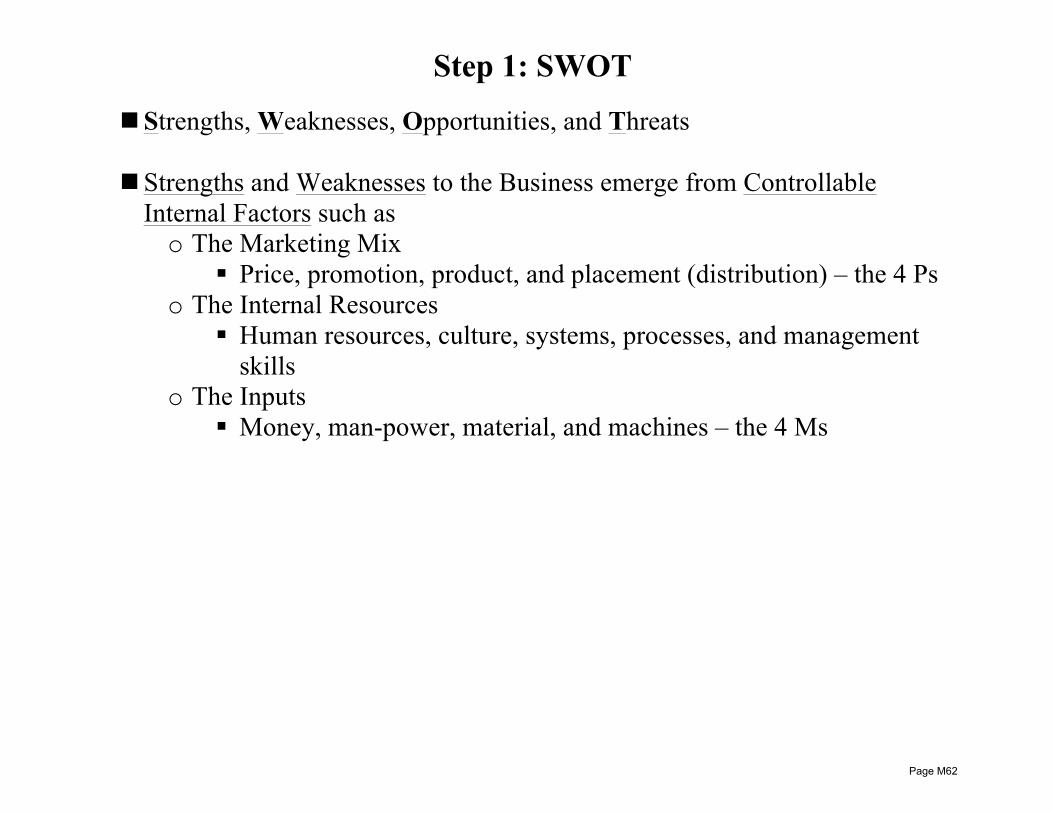

Step 1: SWOT

n Strengths, Weaknesses, Opportunities, and Threats n Strengths and Weaknesses to the Business emerge from Controllable

Internal Factors such as o The Marketing Mix

§ Price, promotion, product, and placement (distribution) – the 4 Ps o The Internal Resources

§ Human resources, culture, systems, processes, and management skills

o The Inputs § Money, man-power, material, and machines – the 4 Ms

Page M62

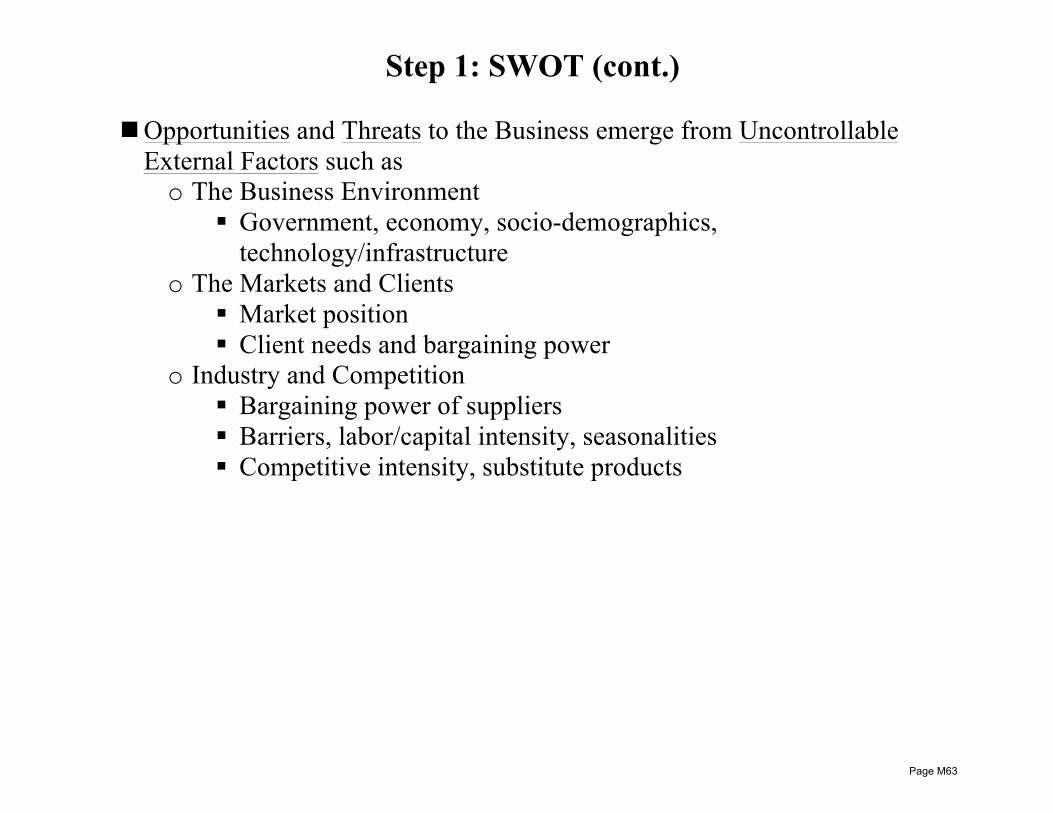

Step 1: SWOT (cont.) n Opportunities and Threats to the Business emerge from Uncontrollable

External Factors such as o The Business Environment

§ Government, economy, socio-demographics, technology/infrastructure

o The Markets and Clients § Market position § Client needs and bargaining power

o Industry and Competition § Bargaining power of suppliers § Barriers, labor/capital intensity, seasonalities § Competitive intensity, substitute products

Page M63

Step 2: Value Chain Analysis

n Tool for Competitive Strength Assessment o Reveals strengths/weaknesses of comparative position compared to rivals o Indicates firm’s competitive advantages/disadvantage against each rival o Provides insight on how firm can focus its strategy on its competitive strengths o Provides insight on how firm can adjust its strategy to alleviate critical

competitive weaknesses

n Links in the Value Chain o Research & Development

§ Generating/experimenting with new ideas o Design of products or services

§ Detailed planning and engineering of proved products or services o Production

§ Acquiring/coordinating/assembling resources to produce the product or service

o Marketing § Promoting and selling goods or services

o Distribution § Delivering products or services

o Customer service § Providing after-sale support

Page M64

Step 2: Value Chain Analysis (cont.)

n The Key to using Value Chain Analysis for Strategic Positioning o Concentrate resources on those activities in the value chain where the

company can gain dominating expertise to serve target customers

n Factors to Examine o Strength of the company’s current competitive position o How does the company rank relative to key rivals on each link in the

value chain o Trend à is the company’s competitive position strengthening or

deteriorating?

n Management Accounting Role in Value Chain Analysis o Gather and report CSF data on cost, quality, and timing for each value

chain link o In particular, develop performance cost measurement and analysis for

each link § Critical in that management accounting traditionally focuses only

on costs of production, marketing, distribution, and customer service

§ However, most costs are committed in the first two links of R&D and Design

Page M65

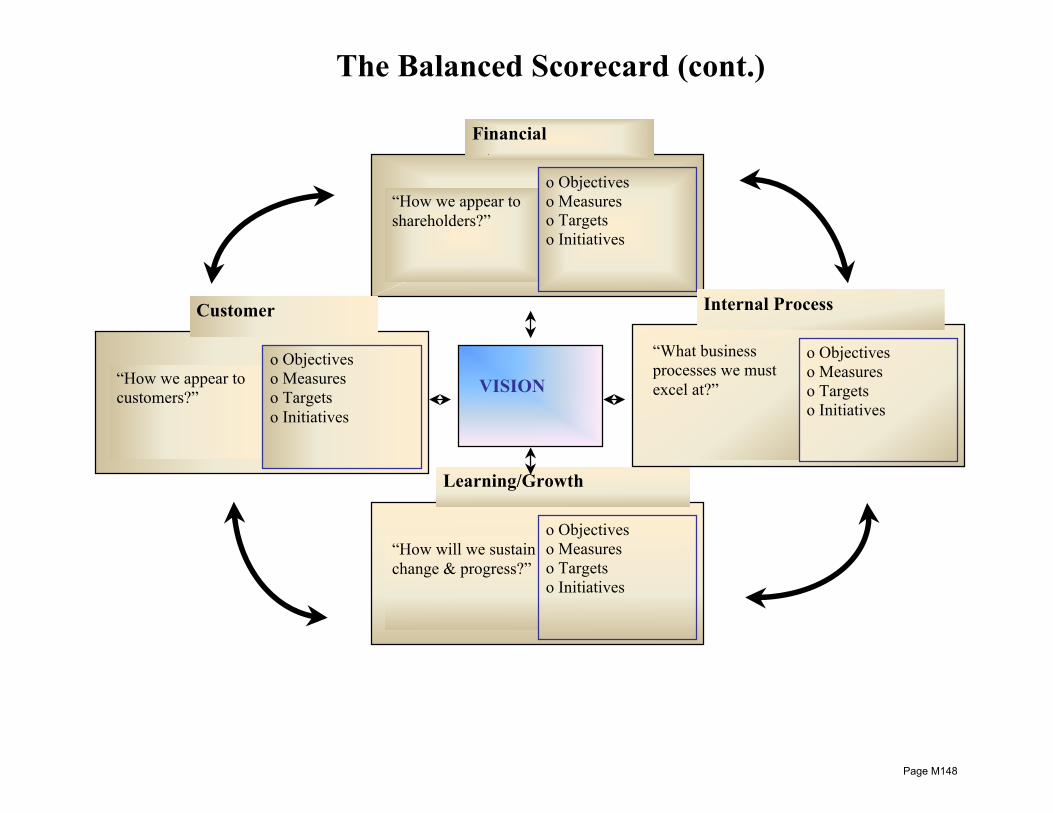

Step 3: The Balanced Scorecard

n Critical Success Factors (CSF) can be Organized and Linked as Performance Measures across Four Areas o Financial factors

§ Examples: profitability, liquidity, sales, market value o Customer factors

§ Examples: customer satisfaction, dealer/distributor strength, marketing/selling o Internal Business factors

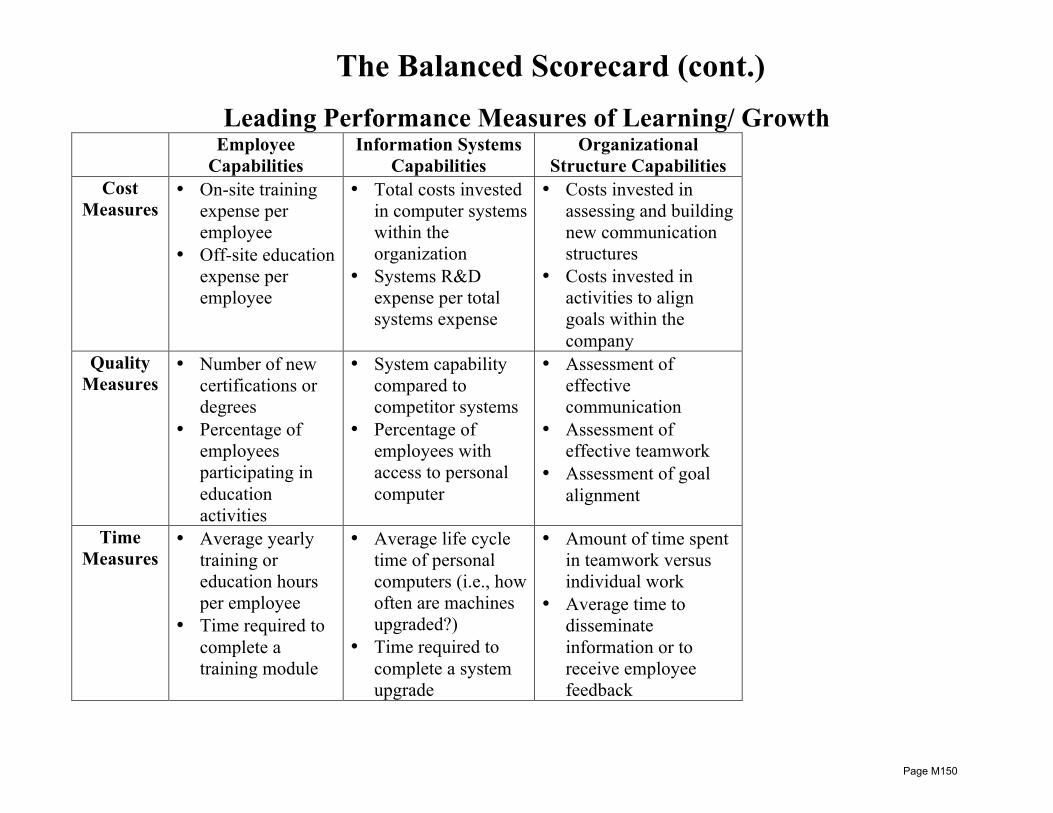

§ Examples: quality, timeliness, productivity, flexibility, process efficiency, safety o Learning and Growth factors

§ Examples: product innovation, skill development, morale, communication

Page M66

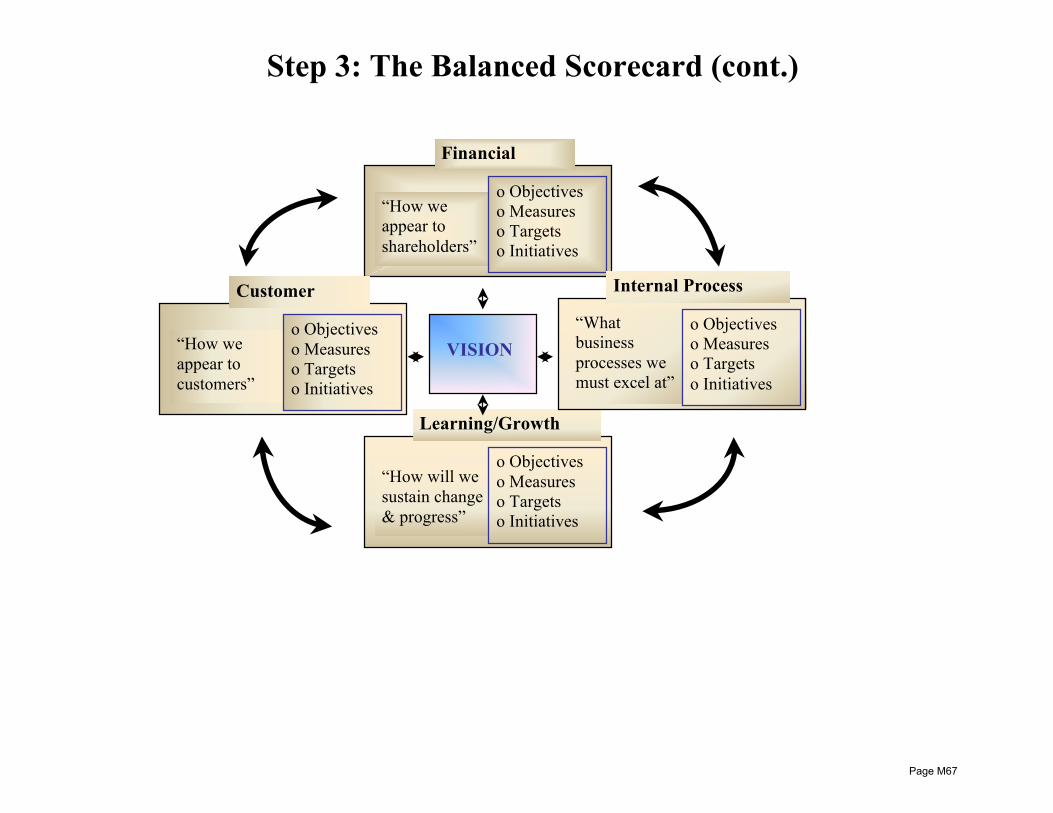

Step 3: The Balanced Scorecard (cont.)

“How we appear to shareholders”

o Objectives o Measures o Targets o Initiatives

Financial

“How we appear to customers”

o Objectives o Measures o Targets o Initiatives

Customer

“How will we sustain change & progress”

o Objectives o Measures o Targets o Initiatives

Learning/Growth

“What business processes we must excel at”

o Objectives o Measures o Targets o Initiatives

Internal Process

VISION

Page M67

Contingency Planning

n Risk Management o A broad range of activities to identify, control, and mitigate risks to the

business n Risks to the Business

o Natural disasters o Human error or sabotage o Technological breakdowns o Change in regulation o Disruptive technologies o Competitor shifts o Economic downturns

n Contingency Plans o Conduct business impact analysis (BIA) o Identify preventative controls (if possible) o Develop recovery operation plans or adaptation strategic plans o Train management and personnel o Maintain the plan (regular updates)

Page M68

Unit B Topic 2 Planning and Budgeting Concepts

Learning Objectives: • demonstrate an understanding of the role that budgeting plays in formulating short-term objectives and planning and

controlling operations to meet those objectives • identify the characteristics that define successful budgeting • demonstrate an understanding of the role that budgets play in measuring performance against established goals • show how the budgeting process facilitates communication among organizational units • demonstrate how the budgeting process enhances coordination of organizational activities • define a responsibility center (strategic business unit) and identify various types of responsibility centers (strategic

business units) • explain the concept of a controllable cost as it relates to both budgeting and performance evaluation • prepare an operational budget for a responsibility center (strategic business unit) • demonstrate an understanding of the concept of management-by-objective and how it relates to performance evaluation • identify the benefits and limitations of management-by-objective • demonstrate an understanding of how the planning process coordinates the efficient allocation of organizational

resources • recognize the appropriate time frame for various types of budgets • identify who should participate in the budgeting process for optimum success • describe the role of top management in successful budgeting • identify the role of top management or the budget committee in providing appropriate guidelines for the budget and

identify items that should be included in these guidelines • demonstrate an understanding of the use of cost standards in budgeting • differentiate between ideal standards and currently attainable standards • differentiate between authoritative standards and participative standards • identify the steps to be taken in developing standards for both direct material and direct labor • define the role of benchmarking in standard setting • identify the benefits of benchmarking in creating a competitive advantage • show an understanding of the need to have a policy that allows budget revisions that accommodate the impact of

significant changes in budget assumptions

Page M69

The Role of Budgeting

n Successful Budgeting Factors o Compels strategic planning and implementation of plans

§ Also provides feedback on the strategy o Provides a framework for judging performance

§ Past performance is a poor measuring stick § Past results incorporate miscues and substandard performance § Future conditions may be different from the past

o Motivates managers and employees § Challenging goals can improve performance § Unreasonable goals create anxiety without motivation

o Establishes communication among subunits within the organization § Communication is getting goals to be understood in meaningful

terms and establishing expectations among and between people and business units

§ Coordination is meshing and balancing all factors of production or service

o Promotes coordination of shared resources § All resources are limited and must be assigned (allocated) to

business units that provide the most strategic value

Page M70

Responsibility Accounting

n Responsibility Centers o Subunits of an organization whose managers are accountable for

specific set of activities o The organizational chart defines the responsibility centers for a

particular company o Responsibility centers are also called strategic business units (SBUs)

n Responsibility Accounting o A system that reports plans (budgets) and actions (results) for each

responsibility center o Key point: Costs and activities assigned to the responsibility of the

SBU are controllable by the SBU

n Types of Responsibility Centers (defined by accountability, i.e., controllability) o Cost Center: Manager is accountable for costs only o Revenue Center: Manager is accountable for revenues only o Profit Center: Manager is accountable for both costs and revenues o Investment Center: Manager is accountable for costs, revenues, and

investments (i.e., assets)

Page M71

Management-by-Objective

n Performance Evaluation and Control o Operational Control is the evaluation of operating level employees by

mid-level managers § Focus on short-term performance

o Management Control is the evaluation of mid-level managers by upper-level managers § Focus on long-term strategic issues

n Operational Control follows a Management-by-Exception Approach o Identification of units or individuals whose performance is not in

compliance with expectations (variance analysis) o Correct the problem efficiently and effectively

n Management Control follows a Management-by-Objective Approach o Establish long-term strategic objectives (i.e., growth, customer

satisfaction, employee development) and periodically measure against these goals

Page M72

Management-by-Objective (cont.)

n Objectives of Management Control o Motivate mid-level managers to focus on organizational goals

(strategies) o Provide incentives to mid-level managers to make decisions consistent

with organizational goals o Fairly determine the rewards that managers receive for effort and

effective decision-making

n Challenges of Management-by-Objective Systems o Uncertainty

§ Unavoidable internal factors (e.g., machine breakdowns) and unexpected external factors (e.g., market demand) create uncertainty about the effectiveness of the manager’s actions

o Lack of observability § Mid-level managers often possess private information not known

by top-level management § Efforts and most decisions of mid-level managers are unobservable

n Bottom Line: Evaluating SBUs based solely on outcomes creates efficiency and equity problems in the performance evaluation system

Page M73

Management-by-Objective (cont.) n Three Principles of Effective Employment Contracting

1. Separate the outcome of the manager’s action from the effort and decision-making skill of the manager § The performance of the manager ≠ the performance of the SBU

2. Exclude known uncontrollable factors from the performance evaluation § Obviously, fairness is still not guaranteed

3. Make adjustments for the expected risk aversion of the manager § Because of uncertainty, managers are biased to avoid decisions

with uncertain outcomes § In contrast, top-level managers have a greater tolerance for risk in

decisions that don’t affect them personally n Budgetary Slack

o Overestimating expensing and underestimating sales o Effective employment contracting helps minimize budgetary slack

Page M74

Time Coverage of Budgets n Long-Term Planning

o Strategy analysis and capital budgeting o 3- to 5-year horizon (or more)

n Master Budgets o Includes operating budgets and financial budgets o Time frame depends on the purpose of the project/process/SBU being

budgeted § A large construction project or total profitability of a new product

line may have a budget extending over several years § The budget for a small construction project or special research

project may only last for several months o Traditional time horizons are one year

§ Subdivided by months for the first quarter § Subdivided by quarters for remaining year § Many organizations have 3- to 5-year annual budgets as well (these

are quite general)

n Rolling Budget (i.e., Continuous Budget) o Disciplines the organization to perpetually maintain the budget o Perpetually adds a month or quarter to the future budget as the month

or quarter just ended is dropped Page M75

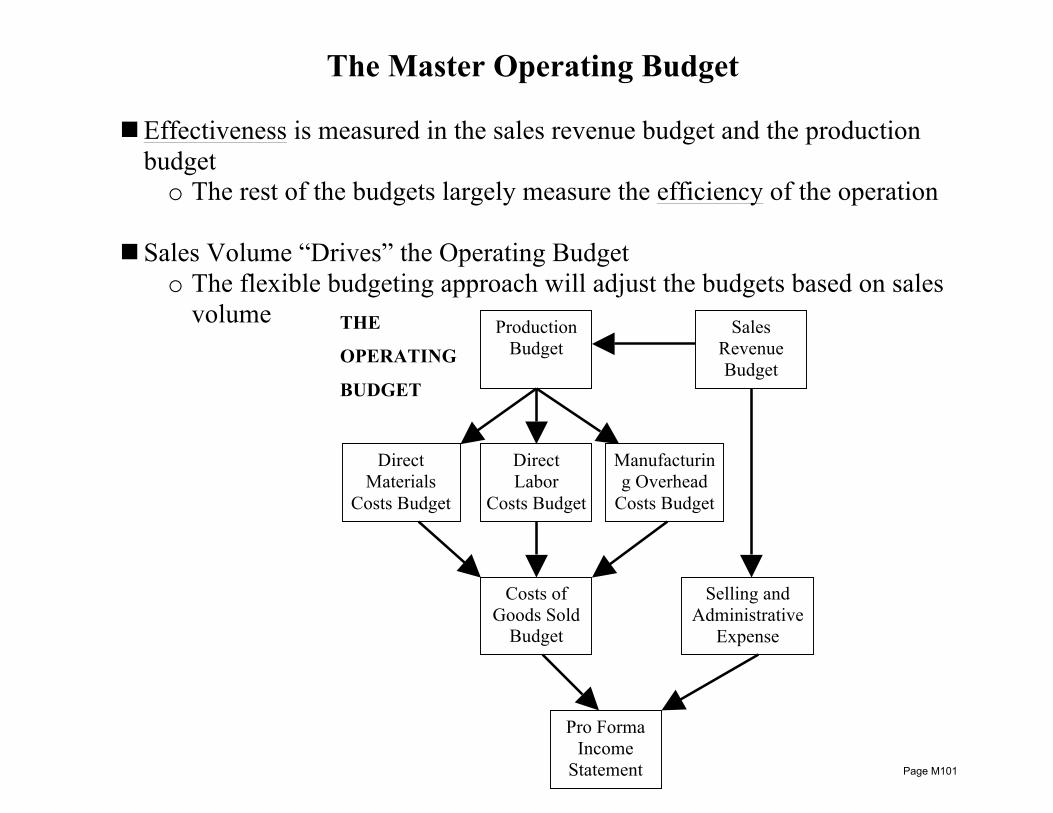

Overview of the Master Budget

Sales Revenue Budget*

Selling and Administrative

Expense Budget*

Capital Expenditures

Budget

Cash Budget

Budgeted#

Balance Sheet

Budgeted# Statement of Cash Flows

Strategic Goals and

Plans

Short-Term Objectives

Manufacturing Overhead

Costs Budget*

Production Budget

Direct Labor Costs Budget*

Direct Materials Costs

Budget*

Costs of Goods Sold

Budget

Budgeted# Income

Statement * * * * *

*These budgets all flow into the Cash Budget

#Also known as pro forma financial statements

OPERATING

BUDGET

FINANCIAL

BUDGET

Capital Project Plans

Page M76

The Management Role in the Budgeting Process

n An Informal Simple Process in a Small Firm

n A Lengthy Procedure in a Large Organization n The Budget Committee

o Typically composed of CEO or designated VP, CFO, and heads of critical SBUs

n Budget Guidelines

o Set by budget committee o Determines the “tone” for the budgeting process o Based on multiple factors

§ Organization strategy § Outlook of the market and economy § Specific current period goals § Operating results of the year to date § Etc.

n Initial Budget Proposals o Each SBU provides its initial budget proposal

Page M77

The Management Role in the Budgeting Process (cont.)

n Budget Negotiation o Occur across all levels of the organization o The core of the budgeting process o Can take the bulk of the budget preparation time

n Review and Approval o Proposals are examined by budget committee for consistency with

guidelines o Budget is approved and submitted to the board of directors (if relevant)

n Revision o Uncertainty regarding internal and external factors creates need for

subsequent budget revisions o How (and if) budget revisions are accommodated is specific to the

organization § Periodic revision is an advantage in dynamic operations § Regular revisions may cause a loss of rigor in subsequent

budgeting processes

Page M78

Standard Costs

n The “Golfer’s Par” in the Operating Budget o A standard of performance o The foundation for planning and control within the budgeting process

n In Theory, standard costs exists for all production, selling, and administrative activities

n In Traditional Practice, standard costs exists for the direct materials, direct

labor, and production overhead budget o Direct costs are traced to production output by:

Standard prices x standard inputs allowed o Indirect costs are allocated to production output by:

Standard allocation rates x standard bases allowed o “Allowed” means what should have been used or allocated based on

actual production output

Page M79

Standard Costs (cont.)

n Ideal Standards o Perfect implementation and maximum efficiency o Use of ideal standards can be controversial o Best use is when ideal standards are used to measure improvement, not

attainment § The concept of continuous improvement (Kaizen)

n Currently Attainable (Normal) Standards

o Employees with proper training and experience can generally attain without extraordinary effort

o Assumes some inefficiencies and deviations o Can create problems in a highly competitive market

n Setting Standard Costs o Authoritative standards are “top down”

§ Used to ensure consideration of all operating factors and management expectations

§ Expedites the standard setting process o Participative standards involves everybody (“bottom up”)

§ Ensures that all available info is used § Helps establish “buy in” by all § Slows down the standard setting process

Page M80

Standard Costs (cont.) n Setting Standards for Direct Materials Costs

o Specify the Quality § Impacts quantity needed (scrap) § Processing time § Amount of supervision required

o Determine the Quantity § Purchase discounts and shipping/handling costs are included and are

impacted o Establish the price

§ Supplier negotiations/bidding, dependability of suppliers, commitments, etc.

n Setting Standards for Direct Labor Costs

o Assess the type of work and complexity of product or service o Determine the type and condition of equipment used o Determine the skill level of workers o Factor in strategy issues regarding company culture, labor unions, etc. o Includes fringe benefits and payroll taxes

n Setting Standards for Manufacturing Overhead Costs

o This is the predetermined overhead rate process o Perhaps the most complex standard cost issue

Page M81

Benchmarking n The Search for Best Practices both Within and Across Industries

o A theory of competition developed in the last 25 years o Used as a important mechanism for continuous improvement and

effective competition

n Benchmarking is a very effective means of establishing cost (and other performance) standards! o Can help avoid the tension between ideal and normal standards o Can help avoid the tension between authoritative and participative

standards

n The Benchmarking Process o Identify critical success factors (CSFs) o Study the best practices of competitors or organizations in other

industries (or other SBUs within the organization) o Implement improvements to beat the performance of competitors or to

match the performance of organizations in other industries § The idea of using benchmark standards from other industries is a

more recent and important innovation on the benchmarking process

Page M82

Unit B Topic 3 Types of Budget Systems

Learning Objectives: • For each of the budget systems identified (Annual/Master budgets, Project budgeting, Activity-based budgeting, Zero-

based budgeting, Continuous budgeting, Kaizen budgeting, and Flexible budgeting), the candidate should be able to: • define its purpose, appropriate use, and time frame • identify the budget components and explain the interrelationships among the components • demonstrate an understanding of how the budget is developed • compare and contrast the benefits and limitations of the budget system • calculate budget components on the basis of information presented • evaluate a business situation and recommend the appropriate budget solution

Page M83

Budgeting Systems

n Different Types of Organizations and Different Strategic Needs of Organizations Determine the Type of Budgeting System Used o The distinction in budget systems is largely in terms of the annual

master budget o Specific project budgets are less distinct in terms of different

management theories being used in practice o Regardless of the type of system being used, these budgets can follow a

continuous budgeting process and/or a flexible budgeting process § Continuous budgeting constantly rolls the budget forward over

time § Flexible budgeting identifies costs that are expected to vary based

on output or activity volumes, then builds the budget after the fact based on what should have happened given actual activity

Annual Master Budgets

• Traditional • Zero-Based • Activity-Based • Kaizen

Page M84

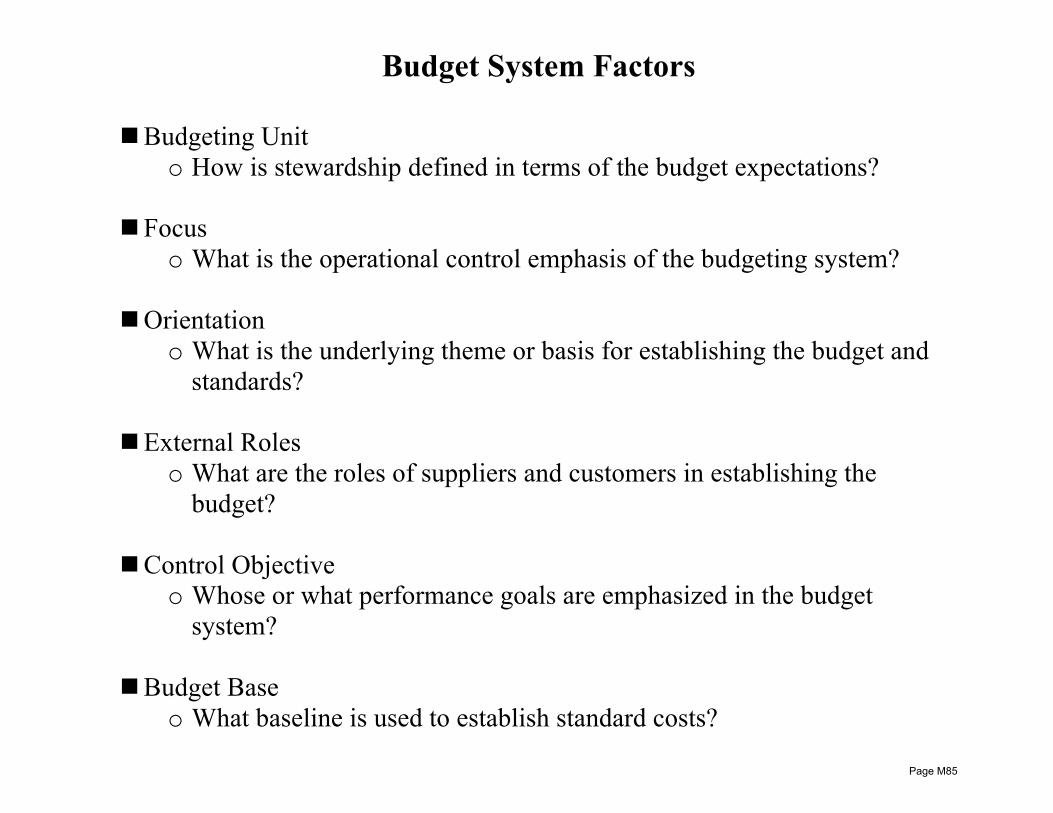

Budget System Factors

n Budgeting Unit o How is stewardship defined in terms of the budget expectations?

n Focus o What is the operational control emphasis of the budgeting system?

n Orientation o What is the underlying theme or basis for establishing the budget and

standards?

n External Roles o What are the roles of suppliers and customers in establishing the

budget?

n Control Objective o Whose or what performance goals are emphasized in the budget

system?

n Budget Base o What baseline is used to establish standard costs?

Page M85

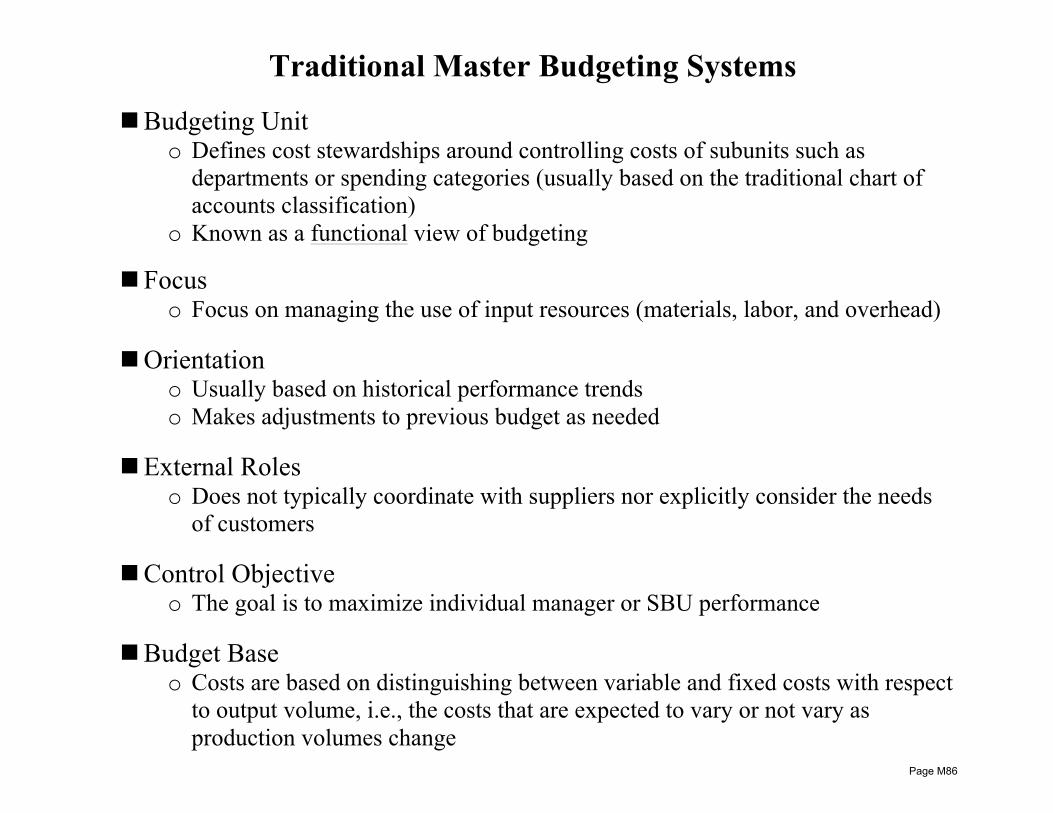

Traditional Master Budgeting Systems

n Budgeting Unit o Defines cost stewardships around controlling costs of subunits such as

departments or spending categories (usually based on the traditional chart of accounts classification)

o Known as a functional view of budgeting

n Focus o Focus on managing the use of input resources (materials, labor, and overhead)

n Orientation o Usually based on historical performance trends o Makes adjustments to previous budget as needed

n External Roles o Does not typically coordinate with suppliers nor explicitly consider the needs

of customers

n Control Objective o The goal is to maximize individual manager or SBU performance

n Budget Base o Costs are based on distinguishing between variable and fixed costs with respect

to output volume, i.e., the costs that are expected to vary or not vary as production volumes change

Page M86

Zero-Based Budgeting Systems

n Very Similar to Traditional Budgeting n Only Difference is Orientation

o Unlike traditional budgeting systems, requires that analysis and justification for every cost and subunit take place annually

o Creates awareness of activities or functions that have outlived their usefulness

n Very Popular in the 1970s o Although popularity has faded, still used in many government and not-for-

profit organizations today

n The Principle of Zero-Based Budgeting is Alive and Well! o Many organizations find it impossible to perform and complete a review every

year on every activity and function o Many organizations schedule zero-based budgeting reviews periodically or

rotate these reviews through the organizations on a multi-year basis

Page M87

Activity-Based Budgeting Systems

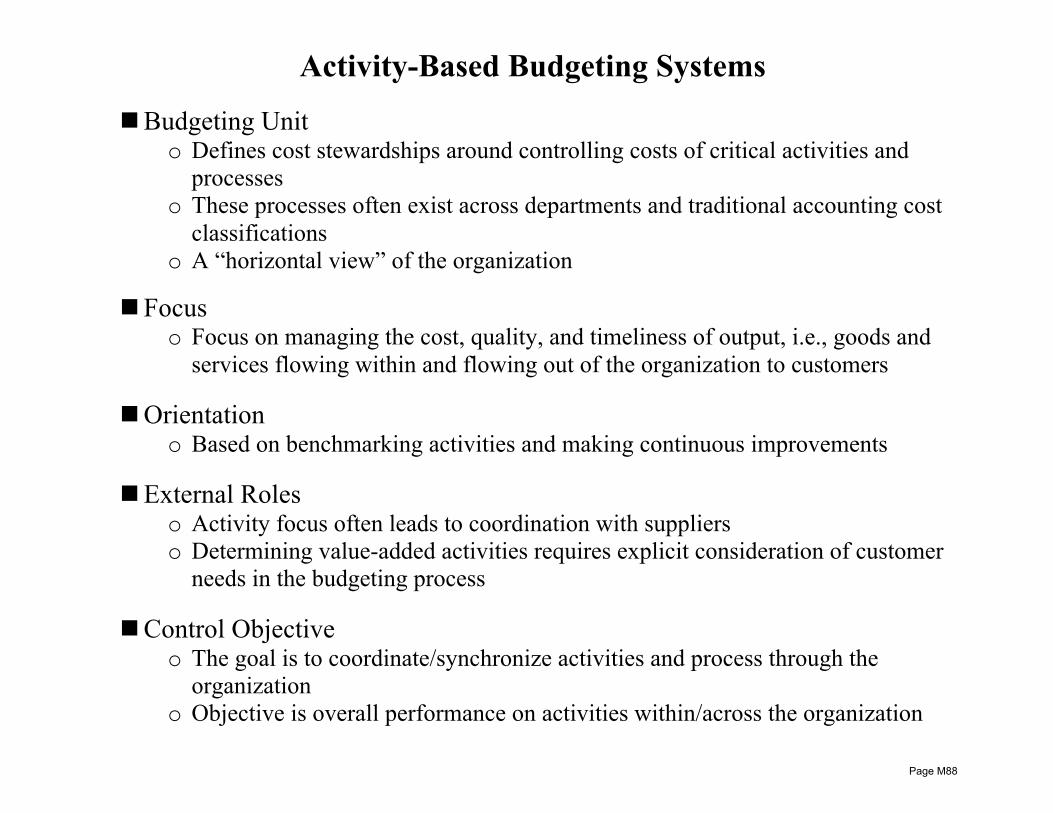

n Budgeting Unit o Defines cost stewardships around controlling costs of critical activities and

processes o These processes often exist across departments and traditional accounting cost

classifications o A “horizontal view” of the organization

n Focus o Focus on managing the cost, quality, and timeliness of output, i.e., goods and

services flowing within and flowing out of the organization to customers

n Orientation o Based on benchmarking activities and making continuous improvements

n External Roles o Activity focus often leads to coordination with suppliers o Determining value-added activities requires explicit consideration of customer

needs in the budgeting process

n Control Objective o The goal is to coordinate/synchronize activities and process through the

organization o Objective is overall performance on activities within/across the organization

Page M88

Activity-Based Budgeting Systems (cont.)

n Budget Base o Defines activity cost pools that respond linearly to changes in activity volumes

§ Hence, unit level, batch level, and product-line level costs are all considered variable

§ Hence, the “fixed versus variable” issue is not critical o Costs are often based on distinguishing between utilized and unutilized

activity/process capacity

n Activity-Based Budgeting Changes the Stewardship Structure o Complete implementation defeats the purpose of functional/departmental lines o Requires establishment of activity/process managers rather than department

managers

Page M89

Kaizen Budgeting Systems

n Budgeting Unit o A process (horizontal) view of the organization

n Focus o Focus on desired future operating process results o Cost, quality, and timeliness

n Orientation o Orientation is on finding improvements o Hence, budget variances are not based on improvement from past results, but

variance from future desired results

n External Roles o Kaizen is not limited to internal improvements o Suppliers and partners are often required to constantly improve by cutting

costs, improving quality, and improving timeliness

n Control Objective o Objective is overall performance within/across the organization

n Budget Base o The baseline is progress towards ideal standards of performance

Page M90

Unit B Topic 4 Alignment of Managerial and Organizational Goals

Learning Objectives: • differentiate between responsibility and authority • demonstrate an understanding of the issues surrounding responsibility without authority • identify ways in which authority is established • identify the purposes for goal setting as they relate to employee behavior (motivation) • explain how goal congruence relates to the success or failure of budgetary plans • describe the relationship between employee goals and needs and the goals of the firm • define the concept of goal congruence and recognize the concept of agency theory and how it relates to goal

congruence

Page M91

Authority

n The Management by Objectives Process o Motivate managers to exert high effort in the business process o Provide incentives to managers to make decisions consistent with

organizational goals o Fairly determine the rewards managers receive for high effort and

effective decision-making

n The Key to Management by Objectives is delegating both responsibility and authority for decisions made and effort expended o Responsibility is often granted for cost, revenues, and/or assets in

SBUs o Authority to make decisions the impact costs, revenues, and assets is

sometimes not granted

n Responsibility and authority disconnects happen when performance measures are misaligned o An SBU is treated like a profit center (e.g., segment margin measures),

but doesn’t have the authority to make revenue decisions (price, customer focus, etc.)

An SBU is treated like an investment center (e.g., ROI measures), but doesn’t have authority to make asset decisions (e.g., acquisition and replacement decisions)

Page M92

Goal Congruence

n Consistency between the Goals of the Firm and the Goals of its Employees o A simple concept in theory o Difficult to achieve in practice o Management systems, particularly budgeting systems, that don’t strive for goal

congruence throughout the organization will fail § However, there will always be some conflicts of interest between

employers and employees throughout the organization

n Employee Desires o High compensation o Low effort o Minimal risks

n Employer (Owner) Desires o Low costs o High productivity o Balance between risks and rewards

n The Approach to Conflict of Interest is Governed by the Organization’s View of Employees o Theory X holds that employees are uncommitted, lack self-control, and

incapable of good decisions and creativity o Theory Y holds the opposite view of employees

Page M93

Agency Theory

n Two Key Factors in the Relationship between the Employer (the Principal) and Employee (the Agent)

1. Uncertainty in the environment § No matter what the agent does, the agent cannot completely

control the outcome of the business process § External factors such as machine breakdowns and market price

swings are typically uncontrollable 2. Lack of Observability

§ The principal cannot observe the agent’s true effort, nor many of the agent’s decisions

§ The principal can only observe the outcome of the business process § Outcome is a function of the agent’s decisions and effort and other

uncontrollable factors

n Incentive Compensation Systems o Fixed wages create an incentive to shirk o Compensation should be linked to outcomes of the business process

(e.g., residual income) o Nevertheless, system should be designed to reduce the negative effect

on agent’s compensation due to uncertainty in the environment and its effect on the agent’s risk aversion

Page M94

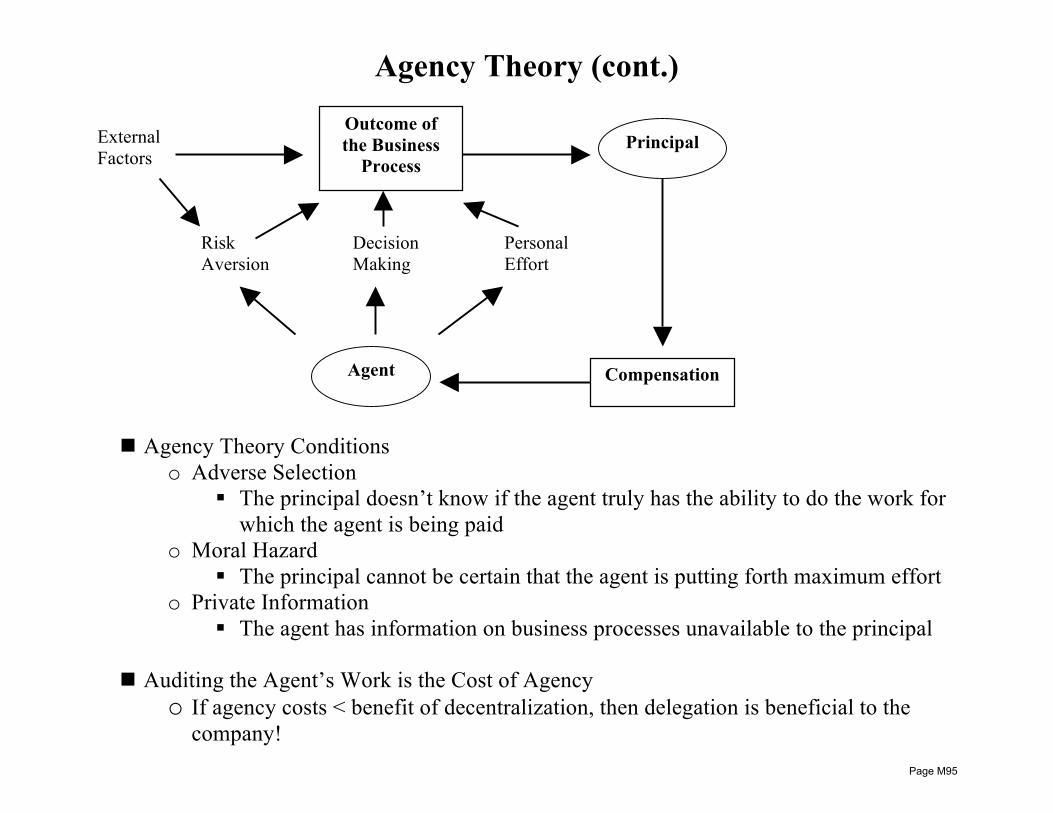

Agency Theory (cont.)

n Agency Theory Conditions o Adverse Selection

§ The principal doesn’t know if the agent truly has the ability to do the work for which the agent is being paid

o Moral Hazard § The principal cannot be certain that the agent is putting forth maximum effort

o Private Information § The agent has information on business processes unavailable to the principal

n Auditing the Agent’s Work is the Cost of Agency o If agency costs < benefit of decentralization, then delegation is beneficial to the

company!

External Factors

Outcome of the Business

Process

Risk Aversion

Decision Making

Personal Effort

Agent

Principal

Compensation

Page M95

Unit C Topic 1 Factors for and Techniques to Control and Evaluate Operations

Learning Objectives: • demonstrate an understanding that performance against operational goals can be measured by a variety of methods

including measures based on revenue, manufacturing costs, non-manufacturing costs, and profit depending on the type of center or unit being measured

• recognize that performance evaluation measures should be directly related to the factors that drive the element being measured, e.g., cost drivers and revenue drivers

• demonstrate an understanding that responsibility centers or business units are often measured on the effectiveness of asset usage and describe the benefits of treating all centers as investment units

• recognize that performance is frequently evaluated on the basis of non-financial performance measures such as customer satisfaction, quality, and innovation

• Understand that traditional evaluation is based on comparing actual results to the master budget and calculating favorable and unfavorable variances from budget

• define a standard cost system and identify the reasons for adopting a standard cost system • Understand the concept of Management by Exception

Page M96

Performance Evaluation

n Effectiveness o Most organizations have multiple strategic goals

§ Profits, growth, quality, community, etc. o An operation (business unit) within the organization is effective if it

meets the goals set for the operation § Alignment of business unit goals with the organization is critical!

n Efficiency