management platforms magic quadrant for energy trading and...

TRANSCRIPT

Industry ResearchG00227079

Magic Quadrant for Energy Trading and RiskManagement PlatformsPublished: 13 March 2012

Analyst(s): Keith Harrison, David Furlonger

Energy trading and risk management platforms provide energy marketparticipants with a means of optimizing the physical and financial positionsof multiple commodities. This Magic Quadrant analyzes the leadingproviders of these platforms.

Market Definition/DescriptionFor a full definition of the energy trading and risk management (ETRM) platform market, see "MarketDefinition: Energy Trading and Risk Management Platforms." The core functional requirements of anETRM platform include the following for at least two energy-related commodities:

■ Transaction/deal capture: Many of the larger multicommodity ETRM platform solutions beganas trade/deal capture solutions and developed from there. The trade or deal can be viewed asthe initial transaction in a process that will conclude with the settlement of an invoice. Real-timetrade capture is a key component for power generators, using links with generation operationsto ensure that the company remains in balance with supply meeting demand. The potentialrange of transactions is extensive, covering financial instruments from simple deals to complexsingle- and cross-commodity or asset-class transactions, as well as physical-commoditytransactions.

■ Logistics and delivery: The delivery of energy or commodities is a significant part of an ETRMplatform. All commodities associated with energy trading (with the exception of emissions) havea physical delivery aspect, although, where energy is traded on a purely speculative basis, thisis less of a concern. There are many unique constraints and considerations with the delivery ofthese commodities. Power is scheduled and delivered via a transmission network; natural gasvia pipelines and storage facilities; coal via shipping, rail and road; and so on. In each case, theability to optimize the delivery of a commodity is an ETRM platform requirement.

■ Trader tools/analytics: Traders are key users of ETRM platforms and should be provided witha range of tools used in establishing the potential value of a transaction in isolation, and whenset against a book or portfolio.

■ Position management and reporting: Possibly the most critical capability of an ETRMplatform is the ability to reflect the status of the company's energy portfolio from physical and

financial perspectives. Additionally, the end user should be able to view the position through anumber of operational lenses — for example, by book, strategy, commodity, trader,counterparty and so on. Wherever possible, this should be in real time or near real time.

■ Risk management and reporting: Many risks can be quantified and reported via an ETRMplatform — from credit-related or counterparty-related risks to market-related or price-relatedrisks, risks related to the physical aspect of delivery, and risks related to compliance withregulatory requirements — such as accounting standards. Many specialized energy riskmanagement solution providers do not offer ETRM platforms; however, portfolio riskmanagement capabilities have been a feature of ETRM platforms for several years.

■ Straight-through processing (STP): This ETRM platform capability — the ability to automatethe management and control of all touchpoints among trade entry, invoicing and settlement —significantly reduces the potential for errors associated with the use of multiple systems. Thiscapability can also help reduce the burden associated with IT and business unit compliance.

■ Integration: An ETRM platform's integration capabilities with internal solutions (such asfinancial and operational systems), external systems and data sources (such as market pricesand intelligence providers) are critical to the wholesale or marketing operations. In some cases,these interfaces are with real-time systems, such as scheduling, and supervisory control anddata acquisition solutions. Such interfaces need to be reliable and secure.

Page 2 of 29 Gartner, Inc. | G00227079

Magic QuadrantFigure 1. Magic Quadrant for Energy Trading and Risk Management Platforms

Source: Gartner (March 2012)

Vendor Strengths and Cautions

Allegro

Product: Allegro v.8

In 2011, Allegro delivered new functionality in the areas of option modeling and analytics, Europeanpower market connectivity, and trader productivity. Allegro continues to reap the benefits of themove to the v.8 architecture, with a steady flow of new functionality delivered in association with theuser community, including the recent addition of Trade Connect 8.1 for the integration of instant-message-based trades, and Decision Metrics 8.1, which provides a configurable view of typical keyperformance indicators (KPIs) for trading and risk functions, deliverable to a wide range of devices,including tablets.

Gartner, Inc. | G00227079 Page 3 of 29

Strengths

■ Allegro is an established ETRM vendor in the energy sector, with a sizable presence in thesectors of exploration and production, refining and marketing, and utilities.

■ Allegro offers a functionally rich, fully integrated product suite, with coverage for all energy-related commodities.

■ The company supports a wide range of physical and financial transactions, and has excellentmarket and exchange connectivity to 22 commonly used derivative exchanges.

■ Its energy risk management coverage extends into hedge accounting, with support forInternational Accounting Standard (IAS) 39, and for Financial Accounting Standards Board(FASB) 133, FASB 161 and FASB 157 compliance requirements.

■ Its product has been based on the .NET framework with XML Web services and service-oriented architecture (SOA) since 2002. Architecturally, Allegro v.8 remains one of the mostflexible, secure and scalable solutions within the Leaders quadrant.

■ It has established partnerships and relationships with many third parties, including professionalservices organizations, such as Deloitte, Opportune, The Structure Group, Baringa Partners,Sapient and Indra.

■ Allegro's agile deployment method and collaborative development program leverage the v.8architecture to provide for reduced implementation times and development times for newfunctionality.

■ Allegro's revised software development process actively engages customers in all aspects ofdesign, and makes use of the architectural improvements in v.8 to improve turnaround times.

Cautions

■ For customers on v.6 and earlier, realizing the architectural and functional benefits of a v.8installation can involve a complex migration.

■ Allegro has consistently chosen a path of organic growth. While relatively low risk, this may limitgrowth prospects as others grow by acquisition.

■ Asia/Pacific has accounted for a declining share of revenue since 2009, although actual revenuein the region has increased.

Amphora

Products: Symphony Cornerstone (CS) v.2.1 (trade capture and processing), Fleetime (waterbornetransportation and logistics for crude/products), Market Connector (exchange connectivity) andLivePrices (imports settled prices to Symphony or third-party risk systems)

In 2011, Amphora added functionality for trade aggregation and automated feeds to a number ofexchanges, renewable identification number functionality in support of alternative fuels processing,and loop inventory management functionality.

Page 4 of 29 Gartner, Inc. | G00227079

Strengths

■ Amphora is primarily focused on oil markets, although with a commodity-neutral approach. ItsSymphony product has a good reputation within oil and gas markets globally.

■ Since its inception in 1997, Amphora has not lost a customer to its competitors.

■ Its functional coverage within oil markets is extensive, and it is particularly strong in logistics,physical movements, position management and reporting, with a growing footprint inemissions.

■ Its architecture lends itself well to large deployments in terms of number of concurrent users,integration and performance. Amphora offers competitive pricing/ownership costs when setagainst larger ETRM vendor solutions.

■ It has a good partner network covering system integrators (SIs), professional services and othercomplementary solution providers in the ETRM space, such as specialist risk managementsolution providers.

■ Its solutions are available on a lease basis and through perpetual license agreements, whichprovide flexibility for procurement functions. A hosted deployment option is available.

Cautions

■ Although the Cornerstone ETRM platform is commodity-neutral in terms of trade capture andprocessing through settlement and invoicing, its current use beyond crude or hydrocarbonmarkets remains limited.

■ Sales and marketing resources remain limited in comparison with the competition, whichhampers growth.

■ Amphora does not offer a software as a service (SaaS) solution

Aspect Enterprise Solutions

Products: AspectCTRM — LE (lite edition), SE (standard edition) and EE (enterprise edition)

In 2011, Aspect continued to enhance its SaaS-based offerings with the release of Aspect PhysicalOperations, providing support for crude storage operations among other usability and functionalimprovements, and improvements in the underlying platform's performance and scalability.

Strengths

■ Aspect's customer growth from a small base is targeted at midmarket or high-end usersseeking a SaaS solution. This is particularly applicable in global oil markets, where companieshave a wide range of locations.

Gartner, Inc. | G00227079 Page 5 of 29

■ The company has flexible offerings and keen pricing. Its main product is available in threeoptions, offering end users the choice of a light solution (AspectCTRM LE), the standard offering(AspectCTRM SE) or a more comprehensive tool (AspectCTRM EE for large enterprises).

■ The company offers a forward curve solution, which was developed in collaboration with amajor oil client.

■ Aspect provides market data, news and analytics through its portal-based Aspect DecisionSupport Center (AspectDSC), which sits on the same platform as its AspectCTRM solution,linking the two solutions together to add further value to the installation. This also providesAspect with another channel to market.

■ AspectCTRM solutions are well-suited for merchants in the oil and refined products space thatare looking for a keenly priced trading solution with a rapid deployment time.

■ SaaS-based ETRM solutions, and other alternatives to traditional on-site deployments, areexpected to gain momentum in the coming years, as end users seek to reduce costs andoperational (IT) exposures. Aspect is well-positioned to capitalize on this.

Cautions

■ Aspect's support for credit risk management functions remains limited, compared with largercompetitors.

■ Its support for logistics and transportation remains limited, compared with competitors,although the 2011 introduction of physical operations functionality partially addressed this, andplans for further physical operations functionality for 2012 are in place.

■ Aspect remains a small, but growing, company that will continue to be challenged to competewith bigger vendors without substantial organic investments. It will also compete viaacquisitions.

■ There is no direct access to major electronic marketplaces/exchanges from AspectCTRM,although this is in the development road map for 2012.

■ Aspect has no formal partnering arrangements because of a market philosophy that centers onsimplifying the product development/deployment process.

■ Its changed business model from a license-oriented, professional-services-supported offeringto SaaS targeted at the small or midsize business market may create operational challenges forexisting clients.

Brady

Product: Elviz ETRM v.11.2

Brady successfully assimilated Viz Risk Management into the fold in 2011 following the acquisitionlate in 2010. Elviz ETRM became the core energy platform product for Brady, with its Trinity andFinTrade products used for other commodities. Enhancement to Elviz ETRM included

Page 6 of 29 Gartner, Inc. | G00227079

improvements to the curve server (new definitions), product interfaces and batch processingimprovements.

Note: In February 2012, Brady announced the intended acquisition of two companies active in theenergy trading space: Navita (a Norwegian ETRM platform vendor) and syseca (a Swiss provider ofscheduling and logistics solutions for energy). The acquisition of Navita will substantially increaseBrady's footprint in European energy companies and utilities, and the syseca acquisitioncomplements the current Elviz ETRM offering.

Strengths

■ Through Viz Risk Management, Brady has secured a strong European presence focused onenergy trading.

■ It continues to demonstrate the ability to tackle new energy-market-related challenges forenergy companies — for example, the functionality added last year for retail contract pricing,which is a key issue for utilities.

■ A sizeable proportion of Brady's energy customers are using Elviz ETRM to manage the EUEmissions Trading System's (EU ETS's) positions.

■ It has a commodity-neutral approach, with extensive support for market risk management,including cash flow at risk (CFaR), value at risk (VaR) and sensitivity analysis perspectives, aswell as configurable parameters, such as prices, volatilities, correlations and volumes.

■ Viz Risk Management was the only Software Engineering Institute Capability Maturity ModelIntegration (SEI-CMMI)-rated software company in this Magic Quadrant. Brady is continuing thisengagement for the Elviz ETRM product line.

■ Elviz ETRM is quick to deploy and is keenly priced, with a range of plug-in areas, such asstorage and generation optimization, data warehouse and business intelligence (BI) support,and enhanced scenario analyses.

■ Its leasing approach to payments reduces end-user capital exposure and provides an exit routeshould the service/solution not meet requirements. This is fairly unique. In times of capitalconstraints in the European market, this could have increasing value to potential clients.

Cautions

■ Elviz is not yet available outside of Europe; however, with the Navita acquisition, Brady has asmall footprint in North America.

■ Brady's logistical, scheduling and transportation support is less complete than much of thecompetition, although partnering arrangements exist in this area, and the recently announcedacquisitions of Navita and syseca should address the gap.

■ The acquisition of Navita could prove distracting to staff on both sides, and premerger productroad maps could change.

Gartner, Inc. | G00227079 Page 7 of 29

Murex

Product: Murex MX.3

Murex delivered a range of additional functional and user interface enhancements in 2011 to MX.3,including further model enhancements and a new swing model that reduces modeling times;enhancements for handling bulk deliveries; and clearing and regulatory reporting workflows. Inaddition, most end-user operations are available as Web services, which provide additionalflexibility for end users.

Strengths

■ Murex is a large, long-standing, privately held vendor with a global reach. MX.3 is a cross-commodity and cross-asset-class trading and risk management platform.

■ The Murex product architecture has a range of connectivity options for internal integration andexternal connections with various trading and data platforms/exchanges, including Reuters,Bloomberg, Trayport, IntercontinentalExchange (ICE) and Eurex.

■ The company has a solid global sales presence and a professional services support capability.

■ Its system has a strong front-office to back-office capability, especially in terms of transactionmanagement and derivatives modeling.

■ Murex offers solid reporting capabilities. It is also strong in over-the-counter derivatives forprincipal trading and structured products.

■ The vendor has extensive risk management capabilities, including scenario generation, backtesting, aggregation analysis, limits, collateral management and reporting tools. In addition tosupporting a range of VaR calculations, MX.3 calculates earnings at risk (EaR), which is of valuein power markets when factoring in volumetric or delivery risks for assets held to maturity.

■ MX.3 can manage multiple commodities, including oil, natural gas, power, emissions/carbon,metals, agriculture and freight. Its predominant capabilities center on the trading, risk andprocessing aspects of these commodities.

■ MX.3 is configurable and a functionally rich product. To streamline the implementation process,Murex offers an accelerated deployment methodology (MXpress), based on the use ofpreconfigured solutions with "out of the box" functionality and an associated implementationmethodology.

Cautions

■ Murex is used as a cross-asset-class trading platform in many financial institutions; however, itspresence among energy merchants remains smaller than many of its key competitors in thisMagic Quadrant.

■ The company is increasing its focus on physical trading functions. In particular, its coverage ofpower and natural gas in the EU, as well as oil (hydrocarbons), has improved. Support for vesseloperations and logistics remains an area of catch-up with key competitors.

Page 8 of 29 Gartner, Inc. | G00227079

■ MX.3 is a substantial platform technically and functionally. Its management and developmentrequire skilled resources that are familiar with the product's configuration and integration tools.Murex provides training and support for technical and functional staff.

■ Although Murex can offer a hosted delivery model in some cases, the majority of its clients optfor a traditional deployment.

Navita

Products: Pomax ECTRM v.11.0 (core platform), Pomax TRM, Structuring Manager, variouscommodity/regionally specific logistics modules, Curve Manager, and Broker Price Manager

In 2011, Navita introduced new functionality in the form of a new online analytical processing(OLAP) database/BI solution for improved reporting from Pomax; a Trade Loader module forimporting trades from exchanges, such as ICE, the New York Mercantile Exchange (NYMEX) andNord Pool; and a new contract standard calculation engine for the calculation of delivered value,traded value, portfolio trade value and portfolio market-to-market traded value on contracts storedwithin Pomax ETRM.

Note: Navita was acquired by Brady in March 2012. Brady has now acquired two European ETRMplatform vendors, Navita and Viz Risk Management. There is a degree of duplication between theElviz and Pomax ETRM platforms. Existing Navita customers should review plans for Navitaapplications with the new owner.

Strengths

■ Through its Pomax product, Navita provides a comprehensive ETRM solution at a lower pricepoint than many of the more established and well-known ETRM vendors.

■ It is well-suited for asset-heavy end users, such as utilities and energy merchants, with manydeployments (mostly in the EU) integrating directly with system operators. It has acomprehensive range of external interfaces with exchanges and market data providers.

■ Another key feature of the Pomax product is its ability to undertake the majority of typicalconfiguration, modeling and setup activities directly through the product management andutility screens, thereby minimizing the need to use scripting or coding facilities to model assetsor complex contracts.

■ Pomax's user-friendly configuration screens contribute to lower installation times than much ofthe competition.

■ Navita offers comprehensive support for market and credit risk management functions,including Monte Carlo and parametric VaR, profit at risk (PaR), CFaR, and EaR analysis andreporting.

■ Support for carbon dioxide (CO2)/emissions trading under the EU ETS is strong.

Gartner, Inc. | G00227079 Page 9 of 29

■ Pomax can be purchased under a traditional perpetual license, or it can be a lease-basedmodel, which reduces initial capital outlay.

■ Navita offers attractive pricing in comparison to its larger competitors.

Cautions

■ Navita is predominantly a supplier to European-based companies. Efforts to expand in the U.S.are ongoing.

■ Competition among the larger players is reducing prices, which could adversely impact part ofNavita's value proposition.

■ The Brady acquisition could prove distracting for staff on both sides, and premerger productstrategies could change.

OATI

Products: webTrader (webTrader Power, webTrader Gas, webTrader Enterprise, webTrader Market,webSettlement, webIntelligence) and webRisk

Functional enhancements during the past year include the ability to model a utility's Monte-Carlo-based revenue-at-risk, CFaR and EaR support for the Southwest Power Pool Integrated market,and the expansion of deal types supported to include heat rate products and FX transactions.

Strengths

■ OATI is an established vendor in North America — primarily in power, but also in natural gas,coal and emission trading under the Clean Air Interstate Rule (CAIR).

■ The company is the largest and most established provider of SaaS-based ETRM platformsolutions in this Magic Quadrant.

■ It has deep knowledge of North American independent system operator (ISO) and regionaltransmission organization (RTO) power market operations. More than 700 companies useOATI's e-tagging solutions.

■ OATI solutions are provided predominantly under the SaaS model, which reduces on-site ITdeployment times and risks, hardware capital costs, and customer IT staff time. Given thisapproach, webTrader Power and webTrader Gas can be of particular interest to smaller regionalenergy merchants, utilities or supply companies, and to financial services organizations seekingentry into North American physical markets for power and natural gas.

■ OATI's functional coverage in physical power logistics is strong, with additional functionalities inasset optimization, management and reporting, which are provided through its webPlantapplication.

■ The vendor has a symbiotic and productive relationship with its extensive user base through anactive, formal user group. Through an annual user conference and quarterly conference calls,users can propose and vote on the prioritization of enhancements and modifications.

Page 10 of 29 Gartner, Inc. | G00227079

Cautions

■ OATI's multicommodity coverage remains limited and does not include crude or refinedproducts. However, a three-year development road map (unchanged from 2011) includes plansto expand into other asset classes, such as coal and precious metals, as well as increasefinancial trading capabilities.

■ Market coverage is limited to North America. Although inroads into the financial sector havebeen made, because this market differs considerably from OATI's traditional utility market, amore strategic approach will be required if growth is to be more than organic in nature.

■ Although the number of SaaS-based ETRM deployments has grown slightly, this remainspredominantly among small and midsize entities. Larger entities will consider SaaS-basedsolutions for specific ETRM components, but traditional deployment remains the dominantdelivery method for ETRM platforms.

OpenLink Financial

Products: Endur; pMotion/ESS, gMotion and cMotion modules; iOPT modules for forecasting andoptimization; vDesktop; RiskPak; Risk Dashboard; Tax Module; Hedge Analyzer; AccountingManager; Trade Process Manager; Collateral Management; Energy Scenario Management;Reconciliation Module; Producer Services Module; Active Data Services; standard gateways (forexample, ICE, NYMEX, European Energy Exchange [EEX], Trayport, Reuters and Bloomberg); dbcSMARTsoft (supporting the biofuels market); and SolArc RightAngle v.11

2011 saw a change of ownership for OpenLink, followed quickly by the acquisition of SolArc. Whilethere is a degree of crossover between Endur/cMotion and RightAngle solutions in the bulk/liquidsmarkets, OpenLink's post-acquisition strategy focuses Endur-based solutions at multicommodityopportunities with RightAngle, providing customers an alternative solution focused specifically onbulk/liquid markets.

Strengths

■ OpenLink is an established ETRM vendor with operations in all major geographic marketlocations. Across all commodity markets — from smaller regional operators to multinationalenergy companies — OpenLink continues to demonstrate a broad and deep understanding ofall energy markets, including recent developments (such as the Dodd-Frank Act).

■ SolArc's RightAngle solution has a loyal following. The merger provides prospective customersin bulk and liquid markets with an alternative to Endur/cMotion, and support from a marketleader in terms of expertise and professional services capability.

■ The merger has allowed OpenLink to optimize resources and R&D efforts for the Endur andRightAngle solutions.

■ Endur is a highly configurable cross-commodity product, with extensive support for physicaland financial transactions, portfolio asset modeling, and valuation and analysis.

Gartner, Inc. | G00227079 Page 11 of 29

■ Endur and RightAngle are capable of scaling to very large international deployments, andprovide extensive integration capabilities.

■ Through the modules it gained from its IRM acquisition and its "smart ETRM" strategy,OpenLink provides energy data management, load/price forecasting, planning and transport/storage/asset optimization capabilities as an extension of the Endur ETRM platform. For asset-heavy companies, linking asset optimization and ETRM makes sense for an asset-centricenterprise portfolio valuation. In addition, OpenLink is integrating IRM with SolArc's RightAngleproduct and its new Compass visualization tool to provide additional decision supportcapabilities in the crude and products area — for example, demand forecast or bulk andliquefied natural gas (LNG) transport optimization.

■ OpenLink has a range of deployment options for Endur and RightAngle solutions, includingapplication service provider (ASP) offerings, which provide end users with flexibility when itcomes to IT deployments and capital/revenue payment options.

■ Extensions of and enhancements to OpenLink's product lines are continual.

■ OpenLink continues to have one of the largest dedicated internal professional services staff ofall the companies surveyed. The acquisition of SolArc has added to the already substantialknowledgebase of the company.

Cautions

■ Endur is a substantial application. Extensive product training and education will be required fornew users — particularly staff members involved in functions such as asset, risk and scenariomodeling. OpenLink University provides training in all areas.

■ Implementation time scales for an Endur deployment can be underestimated based on end-usercapabilities and the relatively complex nature of Endur's architecture. The introduction of"Packages" — a more preconfigured approach to installations for specific commodities inspecific regions and with specific generic functionality prebuilt (such as reporting and metrics)— should help reduce installation time scales for customers seeking a more rapid deployment.

■ OpenLink limits the distribution of product road map information beyond prospects and existingclients. However, prospects are invited to user conferences, where more information is shared.

■ In an effort to ensure consistency across all customers and minimize transitional risk,OpenLink's approach to upgrading the product architecture is cautious. Although OpenLinkuses an SOA for all external-facing integration points, IT staff at some customers would like tosee a wider adoption of SOA principles and a data-centric design in Endur. RightAngle wasmigrated to a .NET architecture three to four years ago.

Pioneer Solutions

Products: TRMTracker, FASTracker, SettlementTracker and EmissionsTracker

Page 12 of 29 Gartner, Inc. | G00227079

In 2011, Pioneer Solutions delivered an OLAP cube reporting capability, enhanced template-baseddeal entry and offered a swap data repository submission solution, building on a strong backgroundin financial regulatory and compliance solutions.

Strengths

■ Pioneer Solutions has a solid set of core market and credit risk metrics and analyses that meetthe needs of most energy companies or utilities.

■ Its rapid deployment and integration times (less than six months) are of interest to many endusers.

■ Its solution is keenly priced against the competition.

■ Although Pioneer Solutions' installed base remains relatively small, it is growing, and feedbackfrom end users is positive.

■ Its highly configurable solution provides end users with a high degree of control with OLAPcapabilities.

■ Its solution is available and supported in the North American and European markets.

Cautions

■ Pioneer Solutions' support for physical/logistical operations remains less comprehensive thanmuch of the competition.

■ As a relatively new solution, there is a danger of fragmented version control and maintenanceoverheads, as unique end-user-driven developments stem from the core code base.

■ This is a relatively small company, with limited year-over-year growth. Maintaining customersatisfaction levels and growing the business will require careful planning.

SAS

Products: SAS BookRunner Commodity Capture v.12, SAS BookRunner Analytics Workbench v.12and SAS BookRunner Advanced Analytics v.12

In 2011, SAS delivered further enhancements to the BookRunner graphical user interface and the BIcapabilities of BookRunner, with respectable growth in terms of new customers (particularly amongutilities).

Strengths

■ SAS offers two options for analytical capabilities. A core level of position/risk analytics withcommodity-neutral deal capture for multiple physical and financial transaction types is providedthrough BookRunner. BookRunner Advanced Analytics provides a more comprehensive set of

Gartner, Inc. | G00227079 Page 13 of 29

analytical tools, including a range of VaR reporting options, current and potential exposures,scenario analysis, and sensitivity analysis.

■ For organizations that want to undertake a BI approach to risk and portfolio analysis, SAS is amarket leader in BI solutions. The SAS BookRunner approach and solutions could be ofparticular value in situations requiring the consolidation of data from multiple trading platformsfor an aggregated view of risk and associated analytics.

■ Many organizations have SAS-trained programmers who could leverage BookRunner's openapplication programming interface to customize the product and avoid paying substantialprofessional services fees.

■ The provision of a physical asset optimization solution demonstrates an ability to leverage thewider organizational capabilities of SAS, and provides value-adding functionality for asset-heavy energy companies with diverse portfolios. A range of interface options is provided forintegration with internal/external applications and data sources.

■ The expansion of SAS ETRM solutions into the EU demonstrates the company's capability toextend the geographical footprint of a solution.

■ SAS has demonstrated a solid understanding of the issues, risks and impacts associated withregulatory and legislative developments, such as the Dodd-Frank Act.

Cautions

■ The extent of BookRunner support for physical operations remains less complete than manyother vendors in this Magic Quadrant. Third-party products will be required for scheduling,nomination, shipping and transportation functionalities, and SAS is positioned to enable third-party product interoperability, rather than native development.

■ The SAS-for-ETRM solution is SaaS-ready. However, SAS currently sees no client demand forthis deployment option.

■ Although SAS continues to demonstrate an ability to tackle complex analytical and reportingfunctional requirements, much of this has been delivered on an as-needed basis, rather than asout-of-the-box configurable application functionality. Ongoing productization remains part ofthe SAS product road map.

SoftSmiths

Product: SoftSmiths TMS

Functionality added in 2011 included a redesigned user interface for SoftSmiths' ISO/RTO pricingmonitoring service featuring an overlay of weather conditions and a heat map and a dashboardmodule with graphical representation of KPIs. Additional enhancements were made to the positionmanagement application and the ISO/RTO scheduling and settlement suite.

Page 14 of 29 Gartner, Inc. | G00227079

Strengths

■ SoftSmiths maintains a good knowledge of North American markets. It is more suitable forsmall and midsize North American utilities and load-serving utilities without resources.

■ Its lease-based solution is well-suited to small or midsize end users, or to companies seeking alimited IT footprint solution for power.

■ The company offers robust logistical coverage for North American power and gas companies.

■ SoftSmiths has extensive integration capabilities through its e-Link modules.

■ Its SaaS solution has grown in favor among customers and is now the prominent deliverymethod.

Cautions

■ SoftSmiths remains a small and privately held/funded company focused solely on NorthAmerican power and gas solutions.

■ Its solutions are only available in North American markets, and it doesn't have plans at themoment to expand geographically.

■ Its market and credit risk facilities remain restricted to limit management, market-to-market,credit exposure and position reporting.

SunGard

Products: Aligne 3.0 and Kiodex

SunGard's energy and commodities 2011 enhancements included the complete integration of itsglobal back office for all transaction types across Aligne and the release of Aligne PipelineOperations covering contracts, nominations, confirmations, scheduling, allocations and settlements/accounting. 2011 also saw improvements to forward price curve production and management.

Strengths

■ SunGard remains particularly strong in physical/logistical areas of ETRM, and in power andnatural gas markets. The range and geographical coverage of the available solutions in thesemarkets are among the widest in this vendor group.

■ Consolidation of the various commodity-specific and risk management tools continues to bedeveloped under the Aligne architecture and a common reference data model, which havegreatly improved the fit of the various components, improved the overall flexibility of thesolution, and facilitated improved deployment times. SunGard offers hosted and managedservice options for Aligne installations.

■ SunGard has an extensive customer base in the energy sector and has further simplified itsproduct offering brands — Aligne and the SaaS offering Kiodex. The use of standard

Gartner, Inc. | G00227079 Page 15 of 29

technology and SunGard IP for integration and user experience allows for greater configurabilityand deployment options.

■ The company is supported by a substantial consulting/professional services function.

■ SunGard has a robust user community, and it actively identifies, promotes, prioritizes and, insome cases, funds product development activities.

■ It has a substantial, long-standing track record in the energy and financial services industries,with significant deployments of multi-asset-class trading and risk management platforms.

■ SunGard's support for emissions trading remains among the strongest of the vendors in thisMagic Quadrant.

Cautions

■ Although pre-Aligne legacy code streams will remain supported, and established migrationpaths exist for Entegrate and GMS/GTMS users, legacy solution users may choose to examinethe value of migrating to the Aligne architecture, compared with a replacement solution.

■ SunGard solutions supporting crude and refined product operations remain behind much of thecompetition.

■ The company continues to maintain separately branded products, regardless of the Alignebrand. This continues to cause some market confusion and the potential for product/functionaloverlap.

■ Although intending to streamline operations, staffing and management changes may createcommunication issues for existing clients.

Triple Point Technology

Products: Commodity XL (power, gas, oil, coal, freight, biofuels, emissions, natural gas liquids[NGLs], LNG, credit risk and fair value disclosure, and hedge accounting); Xchange (managementdashboard, strategic planning and procurement); MarketData Hub; Commodity SL (preintegratedwith SAP); Commodity XL — Oracle (preintegrated with Oracle eBusiness Suite); and Visual Cockpit(logistics solutions for bulk/liquids/packaged commodities, chartering and vessel operations, powerscheduling, and natural gas)

Triple Point Technology continued to grow in 2011 through sales and its acquisition of Qmastor,which is commonly associated with mining applications. The Qmastor acquisition provides TriplePoint Technology with additional optimization and coal supply chain solutions. Additionalfunctionality in the areas of mobility (including a mobile management dashboard) and credit riskmanagement (including a new credit risk BI solution) is available, which reduces analysis times.

Strengths

■ Triple Point Technology has an extensive range of functional coverage in all aspects of energy/commodity trading and risk management, with particularly solid support for risk management. It

Page 16 of 29 Gartner, Inc. | G00227079

continues to offer the most comprehensive credit risk management hedge accounting/IAS andFASB compliance solutions in this Magic Quadrant, and demonstrates a deep understanding ofcurrent regulatory and compliance issues, such as the implications of the Dodd-Frank Act.

■ It has many partnership arrangements — from technology providers to SIs and professionalservices firms — and has participated in innovative projects, such as the use of Commodity XLand Enerbility solutions to underpin a demand-side response initiative.

■ A range of deployment options, including ASP and a quick-start "lite" solution, provide flexibilityto suit larger international and smaller regional installations. ASP customer numbers continue togrow, and there is a solid client base for this delivery option.

■ Through the Management Dashboard module, which is a decision support solution, users areable to dig into the data structure of Commodity XL, and generate a range of custom reportsand analyses, without the need to learn a complicated scripting or interrogative tool. Decisionsupport capabilities were enhanced in 2011 with the arrival of the Credit Risk BI solution.

■ Market coverage and support are global, with an active user group providing input to productdevelopment. The acquisition of Qmastor will provide further market opportunities to cross-selland upsell.

■ Triple Point Technology continues to demonstrate an ability to acquire and integrate specialistsolution providers quickly, having successfully completed the acquisition of Qmastor in 2011.

■ It has successfully leveraged relationships with many SIs and professional services firms toextend its deployment and implementation capabilities.

■ Its architecture supports extensive integration, configuration and performance capabilities(including Oracle Exa-Stack Ready, which is certified to Oracle high-performance databaseapplications), with all applications or modules sharing the same code base.

Cautions

■ Triple Point Technology's product suite is substantial in terms of functional scope, and it can beoverwhelming to first-time users.

■ Its support for physical energy asset optimization is less comprehensive than some of thecompetition; however, the Qmastor acquisition provides optimization capabilities that could beapplied to generation and delivery assets.

Ventyx

Products: TRM v.5.0 and ETRM v.4.0

In 2011, Ventyx made the ETRM v.4.0 solution and the TRM v.5.0 solution available to the market.The TRM v.5.0 solution is based on a former Siemens New Energy solution, and the ETRM v.4.0solution is based on a former KWI/Global Energy Decisions solution. TRM is primarily focused onU.S. markets, and ETRM is focused on the EU. Additional functionality has been delivered in areas

Gartner, Inc. | G00227079 Page 17 of 29

such as enhancement to PaR calculations, path-based power scheduling in the U.S. and an OLAPcube reporting capability.

Strengths

■ Ventyx covers all aspects of the energy value chain for power — from generation to distributionand supply, and retail operations. It provides a range of solutions that are complementary to theTRM solution (formerly known as Monaco, but rebranded to fit with other product lines), such asgeneration optimization, asset management and load forecasting tools.

■ Its commodity coverage extends to power, natural gas, crude, coal and emissions. Most of itsinstallations are primarily power-oriented and natural-gas-oriented.

■ Ventyx's ETRM capabilities were largely gained through the acquisition of a number ofcompanies with strong histories in the ETRM/wholesale solution market, such as NewEnergyAssociates (formerly part of Siemens) and Global Energy Decisions (which acquired KWI andHenwood Energy Services).

■ TRM and ETRM provide good coverage for risk management, and volumetric and delivery riskanalysis, as well as a range of market and credit risk measures and analytics. It caters to a widerange of physical and financial transaction types.

■ Ventyx's Energy Portfolio Management trading and risk software is installed with an almostequal split between EMEA and North American deployments.

■ Ventyx has an extensive range of partnership arrangements, including SIs and professionalservices firms that provide installation and integration services around the TRM product.

Cautions

■ Despite a strong legacy of ETRM platform solutions, TRM and ETRM remain behind much ofthe competition in terms of the depth and breadth of support for ETRM functions.

■ Ventyx doesn't have a SaaS offering; however, it has the capability to accommodate clients ifrequested.

■ There have been no new clients of either solution in the past two years.

Vendors Added or Dropped

We review and adjust our inclusion criteria for Magic Quadrants and MarketScopes as marketschange. As a result of these adjustments, the mix of vendors in any Magic Quadrant orMarketScope may change over time. A vendor appearing in a Magic Quadrant or MarketScope oneyear and not the next does not necessarily indicate that we have changed our opinion of thatvendor. This may be a reflection of a change in the market and, therefore, changed evaluationcriteria, or a change of focus by a vendor.

Page 18 of 29 Gartner, Inc. | G00227079

Added■ Brady (acquired Viz Risk Management)

Dropped■ SolArc (acquired)

■ Viz Risk Management (acquired)

Inclusion and Exclusion Criteria

Inclusion Criteria

All analyses for this Magic Quadrant relate to vendor submissions that had to be provided as ofDecember 2011. ETRM platform vendors were considered for inclusion based on these criteria:

■ The offering must be software products developed and owned by the vendor, and intendedsolely for energy and/or commodity trading and risk management.

■ The offering must be delivered via a traditional software license or ASP/SaaS business model.

■ A vendor must have at least 12 paying, unique institutions (energy companies or utilities) ascustomers using its products for ETRM purposes, and must be able to demonstrate at least twoyears of live implementations.

Products must be able to demonstrate:

■ Support for multiple commodities

■ Transaction/deal capture facilities

■ Logistics (for example, scheduling, nominations, balancing and transportation) facilities

■ Trader tools and analytics

■ Physical and financial position management and reporting

■ Risk management and reporting

■ STP (transaction to invoice)

■ The ability to integrate with enterprise applications

Exclusion Criteria

■ Vendors and products that did not sufficiently meet the specifics of the inclusion criteria, andthose that did not have a sufficient number of clients/implementations in the energy tradingarea, were not considered for this Magic Quadrant.

Gartner, Inc. | G00227079 Page 19 of 29

■ Vendor service-based products or consulting-led offerings were not included, although werecognize that IT and business services are an important element of ETRM solutions.

Magic Quadrant Vendors

From an initial pool of 16 vendors, 15 were originally selected for this Magic Quadrant based oninclusion/exclusion criteria, client feedback, general industry visibility and relevant fit to the market.However, as a result of sector consolidation, the initial list of 15 was reduced to 14. This reflects theacquisition of SolArc by OpenLink and Brady's acquisition of Navita. Our survey requestedinformation about company size, distribution channels, financials, unit sales, product features/functionalities, alliances and technical architectures. Additional input to the overall analysis camefrom the Gartner client inquiry process. Vendors were advised that they would be ranked by havingtheir products compared against our criteria, and by our analyses of other vendors. Here are thevendors and products included in this Magic Quadrant:

■ Allegro Development: Allegro v.8

■ Amphora: Symphony CS v.2.1 (trade capture and processing), Fleetime (waterbornetransportation and logistics for crude/products), Market Connector (exchange connectivity) andLivePrices (imports settled prices to Symphony or third-party risk systems)

■ Aspect Enterprise Solutions: AspectCTRM — LE (lite edition), SE (standard edition) and EE(enterprise edition)

■ Brady: Elviz ETRM v.11.2

■ Murex: MX.3

■ Navita: Pomax ECTRM v.11.0 (core platform), Pomax TRM, Structuring Manager, variouscommodity/regionally specific logistics modules, Curve Manager, and Broker Price Manager

■ OATI: webTrader (webTrader Power, webTrader Gas, webTrader Enterprise, webTrader Market,webSettlement, webIntelligence) and webRisk

■ OpenLink Financial: Endur; pMotion/ESS, gMotion and cMotion modules; iOPT modules forforecasting and optimization; vDesktop; RiskPak; Risk Dashboard; Tax Module; HedgeAnalyzer; Accounting Manager; Trade Process Manager; Collateral Management; EnergyScenario Management; Reconciliation Module; Producer Services Module; Active DataServices; standard gateways (for example, ICE, NYMEX, European Energy Exchange [EEX],Trayport, Reuters and Bloomberg); dbc SMARTsoft (supporting the biofuels market); and SolArcRightAngle v.11

■ Pioneer Solutions: TRMTracker, FASTracker, SettlementTracker and EmissionsTracker

■ SAS: SAS BookRunner Commodity Capture v.12, SAS BookRunner Analytics Workbench v.12and SAS BookRunner Advanced Analytics v.12

■ SoftSmiths: SoftSmiths TMS

■ SunGard: Aligne 3.0 and Kiodex

Page 20 of 29 Gartner, Inc. | G00227079

■ Triple Point Technology: Commodity XL (power, gas, oil, coal, freight, biofuels, emissions,NGLs, LNG, credit risk and fair value disclosure, and hedge accounting); Xchange (managementdashboard, strategic planning and procurement); MarketData Hub; Commodity SL(preintegrated with SAP); Commodity XL — Oracle (preintegrated with Oracle eBusiness Suite);and Visual Cockpit (logistics solutions for bulk/liquids/packaged commodities, chartering andvessel operations, power scheduling, and natural gas)

■ Ventyx: TRM v.5.0 and ETRM v.4.0

Vendors that had been considered for the 2012 ETRM Magic Quadrant update that were excluded:

■ Entero had insufficient data.

■ SolArc was acquired by OpenLink in November 2011. It is now included in the OpenLinkanalysis.

Evaluation Criteria

Ability to Execute

This axis evaluates ETRM software application vendors on the quality and efficiency of theprocesses, systems, methods or procedures that enable their performance to be competitive,efficient and effective, and to positively affect revenue, retention and reputation. These softwareapplication providers are judged on their ability and success in capitalizing on their vision. Ourevaluation of a vendor's Ability to Execute is based on these criteria (see Table 1):

■ Product/Service: The breadth and availability of the vendor's products that compete in andserve the ETRM market.

■ Overall Viability: Product quality and consistency, as well as the vendor's financial strength,including the likelihood of the continued investment in ETRM software for the financial servicesindustry, and advancing the state of the art within the provider's portfolio of products.

■ Sales Execution/Pricing: Capabilities of presales structures and management activities,including pricing and negotiation, as well as the overall effectiveness of sales channels.

■ Market Responsiveness and Track Record: Ability and responsiveness to meet changingmarket dynamics.

■ Marketing Execution: Market share in the global enterprise market.

■ Customer Experience: Ability to provide technical and relationship support and services thatdrive customer satisfaction.

■ Operations: Effectiveness in meeting organizational goals and commitments.

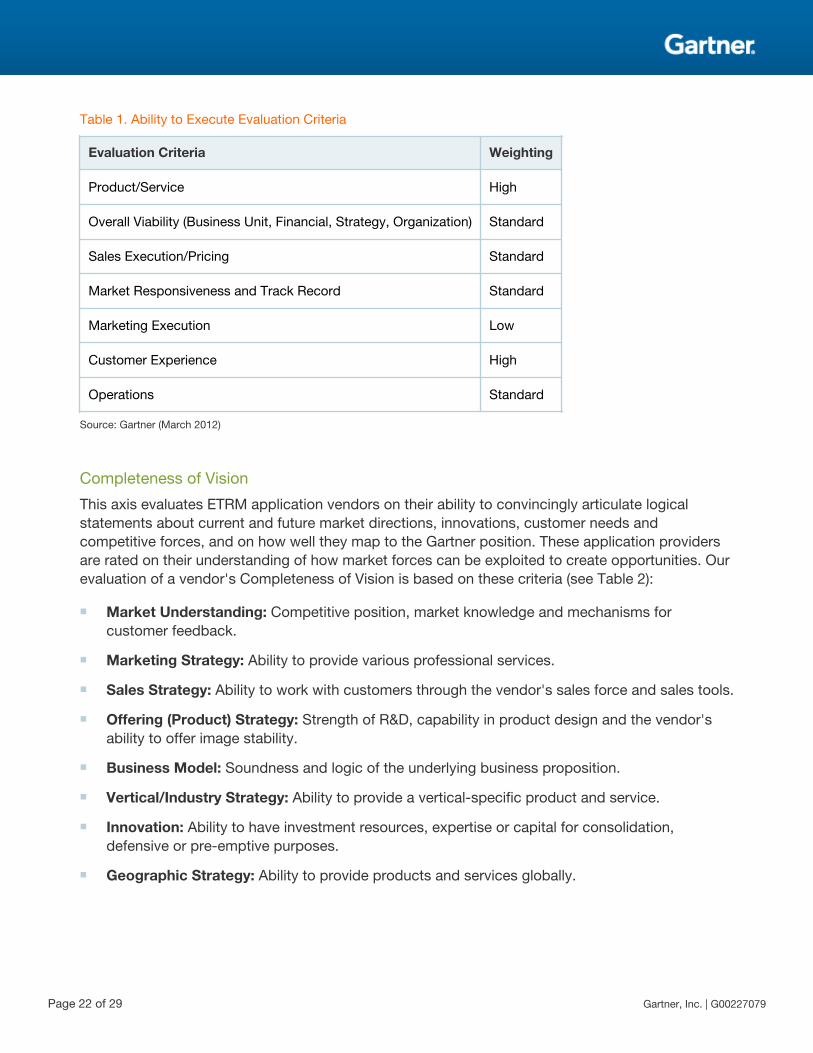

Gartner, Inc. | G00227079 Page 21 of 29

Table 1. Ability to Execute Evaluation Criteria

Evaluation Criteria Weighting

Product/Service High

Overall Viability (Business Unit, Financial, Strategy, Organization) Standard

Sales Execution/Pricing Standard

Market Responsiveness and Track Record Standard

Marketing Execution Low

Customer Experience High

Operations Standard

Source: Gartner (March 2012)

Completeness of Vision

This axis evaluates ETRM application vendors on their ability to convincingly articulate logicalstatements about current and future market directions, innovations, customer needs andcompetitive forces, and on how well they map to the Gartner position. These application providersare rated on their understanding of how market forces can be exploited to create opportunities. Ourevaluation of a vendor's Completeness of Vision is based on these criteria (see Table 2):

■ Market Understanding: Competitive position, market knowledge and mechanisms forcustomer feedback.

■ Marketing Strategy: Ability to provide various professional services.

■ Sales Strategy: Ability to work with customers through the vendor's sales force and sales tools.

■ Offering (Product) Strategy: Strength of R&D, capability in product design and the vendor'sability to offer image stability.

■ Business Model: Soundness and logic of the underlying business proposition.

■ Vertical/Industry Strategy: Ability to provide a vertical-specific product and service.

■ Innovation: Ability to have investment resources, expertise or capital for consolidation,defensive or pre-emptive purposes.

■ Geographic Strategy: Ability to provide products and services globally.

Page 22 of 29 Gartner, Inc. | G00227079

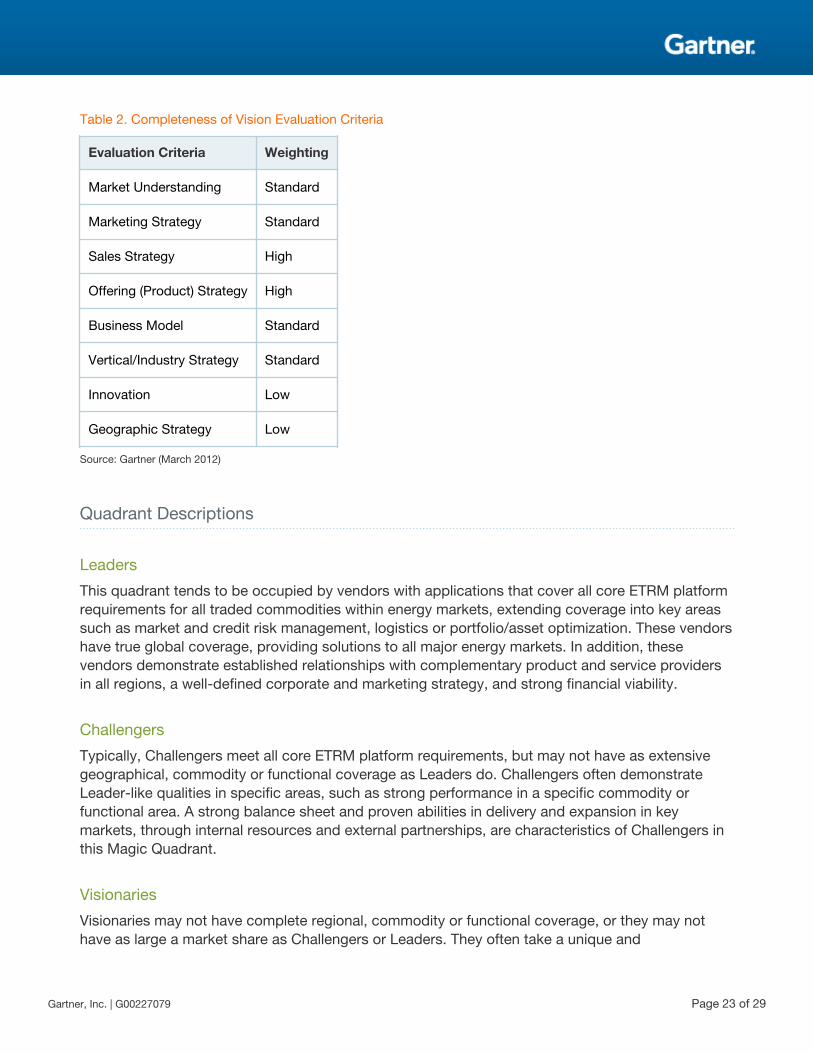

Table 2. Completeness of Vision Evaluation Criteria

Evaluation Criteria Weighting

Market Understanding Standard

Marketing Strategy Standard

Sales Strategy High

Offering (Product) Strategy High

Business Model Standard

Vertical/Industry Strategy Standard

Innovation Low

Geographic Strategy Low

Source: Gartner (March 2012)

Quadrant Descriptions

Leaders

This quadrant tends to be occupied by vendors with applications that cover all core ETRM platformrequirements for all traded commodities within energy markets, extending coverage into key areassuch as market and credit risk management, logistics or portfolio/asset optimization. These vendorshave true global coverage, providing solutions to all major energy markets. In addition, thesevendors demonstrate established relationships with complementary product and service providersin all regions, a well-defined corporate and marketing strategy, and strong financial viability.

Challengers

Typically, Challengers meet all core ETRM platform requirements, but may not have as extensivegeographical, commodity or functional coverage as Leaders do. Challengers often demonstrateLeader-like qualities in specific areas, such as strong performance in a specific commodity orfunctional area. A strong balance sheet and proven abilities in delivery and expansion in keymarkets, through internal resources and external partnerships, are characteristics of Challengers inthis Magic Quadrant.

Visionaries

Visionaries may not have complete regional, commodity or functional coverage, or they may nothave as large a market share as Challengers or Leaders. They often take a unique and

Gartner, Inc. | G00227079 Page 23 of 29

commendable approach to areas such as strategy, marketing and pricing, delivery methods, orfunctional specialization. Innovation of some sort is typically a quality demonstrated by vendors inthis quadrant. Visionaries can become Leaders by improving their ability to deliver and grow thebusiness.

Niche Players

This quadrant contains a number of regional or commodity-specific vendors. This quadrant typicallyaccommodates the vendors in these categories that have a proven track record in their specificgeographies or commodities covered. Typically, in this quadrant, we see vendors covering powerand natural gas, but not oil and refined products, or vice versa, and they have a relatively smallcustomer base compared with Challengers or Leaders.

ContextThe buying and selling of power, natural gas, coal, crude oil, and refined products and emission-related products are core functions for energy producers, consumers and market speculators. Therange of traded products associated with the buying and selling of these commodities is extensive— from simple buy-or-sell transactions in or near real time to ensure that delivery is met, tocomplicated, structured contracts involving multiple commodities. Since the opening of thewholesale U.S. natural gas market in the early 1990s, ETRM platforms have evolved toaccommodate an increasing range of commodities, as well as a diverse array of physical andfinancial instruments, as markets deregulated.

The global energy and utilities market continues to be driven by a confluence of forces — security ofsupply and environmental concerns, ever-changing regulatory and legislative requirements, and thequest for improved performance and profitable business models. Governments are addressingsecurity of supply and energy sustainability concerns through policies that promote investment inclean technologies, and encourage consumers to deploy energy-efficient solutions, includingconsumer-owned distributed energy resources. Consequently, energy and utilities companies areregularly forced to modify their IT and operational technology application portfolios andarchitectures to meet these challenges. ETRM platforms form a significant part of every energy andutilities company's application portfolio, providing a solution to manage and optimize wholesaleenergy market positions and risks. Changes in regulatory and legislative requirements, marketstructures and end-user energy asset portfolios provide opportunities to improve and consolidatethese systems — thus, the significance of this Magic Quadrant in helping end users make the rightselections for new or consolidated platforms.

Market OverviewAn ETRM platform is a single or modular solution that is capable of capturing and managingwholesale energy market transactions from execution to settlement, invoicing, managing, andreporting market and credit exposures. For the purposes of this Magic Quadrant, we have taken a

Page 24 of 29 Gartner, Inc. | G00227079

global perspective, but have also included regional players fitting the inclusion criteria. Among theETRM platform vendors, four additional factors need to be considered:

■ Functional coverage or focus: Some vendors cover all areas in-depth, some are more focusedon the physical logistics of one or two commodities, and some focus on the risk managementaspect through proprietary models or a BI capability.

■ Commodity coverage: Some vendors cover all energy-related commodities and many othercommodities, and some cover only two or three energy-related commodities (see "MarketDefinition: Energy Trading and Risk Management Platforms").

■ Geographical coverage: Some vendors cover all major markets in all geographies, and somecover markets only in North America, EMEA or Asia/Pacific.

■ Deployment options: Increasingly, hosted or SaaS-based solutions are gaining favor amongend users as a means of reducing capital costs, deployment times and support overheads.Traditionally, these solutions were preferred options for smaller end users or end users withlimited functional requirements; however, as the functional capabilities of SaaS- or ASP-baseddeployments grow, the appeal to larger organizations will widen.

The market for ETRM platforms remains fragmented. Mergers and acquisitions among the vendors(mostly privately owned) are an ongoing theme. Approximately 20 ETRM platform vendors offermulticommodity solutions that are in line with the Gartner ETRM platform market definition (see"Market Definition: Energy Trading and Risk Management Platforms"). The wider ETRM solutionecosystem contains approximately 40 other vendors providing point solutions for specific issues(such as market integration, market and/or credit risk management and analytics solutions, andhedge accounting), generation and forecasting, or professional services (such as installation,integration and training). The inclusion criteria for this Magic Quadrant are listed in the Inclusion andExclusion Criteria section.

Despite the fragmented nature of the ETRM platform market, the majority of core functionalrequirements are met by the market leaders. The adoption of SOA has led to improved performanceand integration capabilities. Beyond the core ETRM platform requirements, in an attempt todifferentiate themselves, vendors are focusing their efforts on different areas, such as building:

■ Richer functional coverage in areas such as risk management (for example, real-time marketrisk, cross-product/asset risk assessments and compliance with accounting rules)

■ The link between trading and upstream forecasting, and physical asset optimization

■ The physical or logistical aspects of trading

■ Architectural or graphical user interface improvements

Many vendors have developed solutions for the management of CO2 emission certificateinventories, allowing the ETRM platform to play a key role in the management of emission-relatedpositions. ETRM platforms are particularly suited to this kind of activity — essentially paper trading.As global concerns over greenhouse gas emissions intensify — and as the global markets for CO2

Gartner, Inc. | G00227079 Page 25 of 29

emission certificates, projects and related products grow — they could lead to further evolution ofthe ETRM platform.

2011 brought little change in the requirements driving new or replacement ETRM platform projects.Financial, energy, regulatory and legislative developments (such as the Dodd-Frank Act in the U.S.)continue to impact end-user deployment. However, one noteworthy market development has beenamong the vendors. In the second half of 2011, the market leaders, OpenLink and Triple PointTechnology, both had a change of ownership. Additionally, both acquired businesses around thesame time. Triple Point Technology acquired Qmastor (more associated with mining) and OpenLinkacquired SolArc, extending the gap in terms of ETRM platform revenue from other ETRM vendors.

In March 2012, Brady — the only publicly listed vendor in this Magic Quadrant — acquired Navita,becoming the largest European-based vendor in terms of revenue from ETRM platforms. Theconsolidation we are now experiencing in the vendor market is revealing a bifurcation betweensmaller, more transactionally oriented platforms and full-service providers. Either group hassomething of value to offer the market, but we do not believe the smaller vendors will be able toclose the competitive gap through organic growth.

A noteworthy development in 2011 has been an increasing desire among end users to reduce thecomplexity and costs associated with the ongoing development and support of ETRM platformdeployments. Through inquiries from clients during the past year, sourcing is becoming a moresignificant issue, with more end users now receptive to the idea of outsourcing the ongoing supportand development of their deployments to the original vendors or SIs. The market supporting this isimmature, which we expect will change as a result of the rising demand.

The market for ETRM platform solutions is more fragmented than markets for establishedadministrative solutions, such as customer information systems or general ledger systems. Thereasons for this fragmentation — and the consequently wide range of vendors — include regionaland regulatory market variations, the range of end-user requirements, and the extent and rapidity ofmarket change. Some businesses, such as investment banks and hedge funds, focus more onfinancial trading (see "Magic Quadrant for Financial Services Commodity Trading and RiskManagement Platforms"). Some other businesses, such as load-servicing entities meeting demandor load requirement needs, focus more on physical delivery aspects. Industrial end users (forexample, airlines involved in fuel hedging) focus on optimizing energy procurement. All participantstransact with third parties directly with a counterparty, and/or via exchanges or brokers. Thesetransactions must be managed from execution through physical delivery to invoicing andsettlement. Furthermore, all market participants must manage positions in all their tradedcommodities, which means monitoring market price movements and counterparty status, andtracking the impact of many variables on the current and future value of contracts, assets, tradingbooks, and the entire portfolio. These common functions are the domain of the ETRM platform.

The complexities of the ETRM marketplace increase the need for careful installation andconfiguration to achieve sustainable project success. Based on our research and anecdotalevidence, installation times will range from a minimum of three months for a small-scale or single-commodity SaaS solution to 18 months or more for a multicommodity or multinational deployment.No two ETRM platform installations are the same. There is a wide variety of energy portfolioelements, and how they are modeled and valued varies across market participants. When

Page 26 of 29 Gartner, Inc. | G00227079

purchasing or replacing an ETRM platform, buyers must recognize that the configuration of theplatform to accommodate internal views of asset modeling and valuation will require translation intothe configuration screens or scripting tools of the new platform. Some end users rely on third-partySIs to undertake much of this work (see "Energy Trading and Risk Management Solutions: Gettingthe Most Out of System Integrators"), and some end users train internal resources. Either way, thisis a critical activity.

Another key concern is that, although ETRM platforms will cover much of the wholesale energycommercial process, it is likely that a new installation will require extensive integration with existinginternal systems — from financial systems to spreadsheets and other legacy commoditymanagement tools, and from external data sources for price and market data to exchanges fortransaction execution. The establishment or enhancement of an enterprise information managementstrategy and solution to cope with the number, frequency and time-critical nature of ETRMinterfaces is key to success (see "Tactical and Strategic Options for Improving Market DataManagement").

Many factors continue to influence the ETRM platform market — not the least of which includes thegeneral economic climate, such as the eurozone crisis in 2011. Some of these factors, in noparticular order, are:

■ A continuing interest in widening the use of simulation and scenario-based analytics ("what if"analysis)

■ The desire to reduce the ongoing costs and risks associated with multiple commodity platforms

■ Greater and more-varied connectivity to trading markets

■ Continued globalization of commodity and energy markets

■ Increasing correlation between commodities — for example, burning fuel to produce power alsoproduces emissions

■ Linking trading operations to physical asset optimization — for example, optimizing powergeneration across asset types (coal, gas, wind, solar and nuclear) based on physicalconstraints, the weather and market parameters

■ The need for deeper, more responsive risk management capabilities and a holistic view of riskacross the enterprise

■ Responding to tightening regulatory and legislative reporting requirements

■ Widening the asset types (such as new forms of power generation or energy storage) to bemodeled and valued

Another factor influencing the ETRM platform market is a widening of the type of market participant.As a result of the recent financial crisis, many hedge funds that once traded energy in forwardmarkets are no longer doing so. However, increasingly, banks and investment companies are takinga more active position in physical markets, as well as forward markets. As energy markets becomeincreasingly politicized and volatile, and as energy-related developments attract government

Gartner, Inc. | G00227079 Page 27 of 29

subsidies and the interest of the wider investment community, we can expect the nature of energymarket participants to widen and their number to increase.

Recommended ReadingSome documents may not be available as part of your current Gartner subscription.

"Magic Quadrants and MarketScopes: How Gartner Evaluates Vendors Within a Market"

"Energy Trading and Risk Management Solutions: Getting the Most Out of System Integrators"

"Market Definition: Energy Trading and Risk Management Platforms"

"Tactical and Strategic Options for Improving Market Data Management"

"Cloud-Based Energy Trading and Risk Management Won't Take Off Until Legacy Issues AreAddressed"

Page 28 of 29 Gartner, Inc. | G00227079

GARTNER HEADQUARTERS

Corporate Headquarters56 Top Gallant RoadStamford, CT 06902-7700USA+1 203 964 0096

Regional HeadquartersAUSTRALIABRAZILJAPANUNITED KINGDOM

For a complete list of worldwide locations,visit http://www.gartner.com/technology/about.jsp

© 2012 Gartner, Inc. and/or its affiliates. All rights reserved. Gartner is a registered trademark of Gartner, Inc. or its affiliates. Thispublication may not be reproduced or distributed in any form without Gartner’s prior written permission. The information contained in thispublication has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness oradequacy of such information and shall have no liability for errors, omissions or inadequacies in such information. This publicationconsists of the opinions of Gartner’s research organization and should not be construed as statements of fact. The opinions expressedherein are subject to change without notice. Although Gartner research may include a discussion of related legal issues, Gartner does notprovide legal advice or services and its research should not be construed or used as such. Gartner is a public company, and itsshareholders may include firms and funds that have financial interests in entities covered in Gartner research. Gartner’s Board ofDirectors may include senior managers of these firms or funds. Gartner research is produced independently by its research organizationwithout input or influence from these firms, funds or their managers. For further information on the independence and integrity of Gartnerresearch, see “Guiding Principles on Independence and Objectivity” on its website, http://www.gartner.com/technology/about/ombudsman/omb_guide2.jsp.

Gartner, Inc. | G00227079 Page 29 of 29