management’s discussion and analysis - mega … · management’s discussion and analysis ......

TRANSCRIPT

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 2

Report to Shareholders Fourth quarter and year ended December 31, 2013 MEGA Brands reported its financial results for the fourth quarter and full year ended December 31, 2013 on March 4, 2014. Full year 2013

• Consolidated net sales decreased 4% to $404.7 million in 2013 compared to $420.3 million in 2012.

• Net earnings increased 25% to $20.8 million or $0.93 per diluted share, compared to $16.6 million or $0.84 per diluted share in 2012.

Net sales decreased 5% in the Toys segment while net sales for Stationery & Activities increased 1%. On a geographic segment basis, net sales decreased 3% in North America and 5% in International. Adjusted earnings before interest, taxes, depreciation and amortization (‘‘EBITDA’’) was $47.0 million compared to $49.2 million in 2012. Fourth quarter

• Consolidated net sales decreased 21% to $101.2 million compared to $127.5 million in the fourth quarter of 2012.

• Net earnings were $1.4 million or $0.04 per diluted share, compared to $4.0 million or $0.01 per diluted share in the same 2012 period.

Net sales were down 24% in the Toys segment and 3% in Stationery & Activities. On a geographic segment basis, North American net sales decreased 20% and International net sales decreased 23%. Adjusted EBITDA was $8.9 million compared to $13.9 million in the fourth quarter of 2012. Several factors contributed to the decline in our fourth quarter shipments, including a very challenging retail environment which affected the performance of the entire toy industry, particularly in products for boys. We were also up against a difficult comparison with the fourth quarter of 2012, which saw an 18% net sales increase compared to the previous year. 2013 highlights The MEGA BLOKS First Builders product line had a year of record growth and the retail performance of our Call of Duty line equaled or bettered the sell through of any previous MEGA BLOKS product launch. According to NPD Group, our Call of Duty product line was the top-selling new brand in the construction toy category during the fourth quarter despite limited availability. We ended 2013 in a strong financial position, with long-term debt reduced 48% to $59.3 million compared to $113.0 million at the end of 2012, cash on hand of $16.4 million, more than double the $8.0 million the previous year, and no borrowings against our working capital facility. We also completed a three-year program during which we invested over $30 million to increase efficiency and production capacity in our Montreal facility. Our cash production costs in Montreal are now lower than in Asia and our competitive advantage has been further reinforced with the recent decline in the Canadian dollar.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 3

Report to Shareholders Fourth quarter and year ended December 31, 2013 (cont’d) Subsequent event On February 28, 2014, the Corporation announced a definitive agreement with Mattel, Inc. for the acquisition by a wholly-owned subsidiary of Mattel of all of the Corporation’s issued and outstanding common shares and warrants, and the assumption of the Corporation’s debt. Highlights of the agreement include the following:

• MEGA Brands shareholders will receive CA$17.75 per share in cash. • Warrant holders will receive a net consideration of CA$7.81 per 20 warrants. They may acquire

one common share of MEGA Brands in exchange for every 20 warrants at an exercise price of CA$9.94 per common share.

• Debenture holders will receive 105% of the principal amount of the debentures, plus accrued and unpaid interest.

• The transaction represents a total enterprise value of approximately $460.0 million, including the Corporation’s net debt to be assumed or repaid by Mattel, and is about 9.8 times the Corporation’s 2013 adjusted EDITDA of $47.0 million.

The transaction, structured as a plan of arrangement, is expected to close in the second quarter of 2014, subject to certain closing conditions including, among others, court approval of the plan of arrangement, relevant regulatory approvals and the approval of at least two-thirds of the votes cast at a special meeting of the Corporation’s shareholders. The arrangement agreement provides that the Corporation is subject to non-solicitation provisions and provides that the Board of Directors of the Corporation may, under certain circumstances, terminate the agreement in favor of an unsolicited superior proposal, subject to payment of a termination fee of $12 million to Mattel, as well as reimbursement of expenses not to exceed $0.8 million, and subject to a right of Mattel to match the superior proposal in question. The Corporation’s Board of Directors has unanimously approved the transaction and recommends that common shareholders approve it. The financial advisor to the Board has provided an opinion that the consideration proposed to be paid to the Corporation’s common shareholders is fair from a financial point of view. Shareholders who together hold approximately 39% of the Corporation’s outstanding common shares have entered into voting support agreements and agreed to vote their common shares in favor of the arrangement.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 4

Management's Discussion and Analysis Fourth quarter and year ended December 31, 2013 The following Management's Discussion and Analysis of Financial Position and Results of Operations (‘‘MD&A’’) for MEGA Brands Inc. and its subsidiaries (referred to hereunder as ‘‘MEGA Brands’’ or the ‘‘Corporation’’) should be read in conjunction with the audited Consolidated Financial Statements and Notes thereto for the years ended December 31, 2013 and 2012. The Corporation prepares its financial statements in accordance with Canadian generally accepted accounting principles (‘‘GAAP’’) as set forth

in the Chartered Professional Accountants of Canada (CPA Canada) Handbook, which incorporates International Financial Accounting Standards (‘‘IFRS’’) issued by the International Accounting Standards Board. This MD&A is current as at March 4, 2014.

All figures in this MD&A are expressed in U.S. dollars, unless otherwise indicated.

Forward-Looking Statements

The Corporation may make statements in this MD&A that reflect its current expectations regarding future results of operations, performance and achievements. These are “forward-looking” statements and reflect management’s current beliefs. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may”, “could”, “should”, “would”, “will”, “expect”, “intend”, “estimate”, “anticipate”, “plan”, “foresee”, “believe” or “continue” or the negatives of these terms or variations of them or other similar terminology. This MD&A includes, but is not limited to, forward-looking statements regarding: the shipment of Assassin’s Creed and SpongeBob SquarePants construction sets to retailers; the launch of the MEGA BLOKS American Builders and World Builders brands; the continuation of strong growth momentum for the MEGA BLOKS First Builders product lines; the positioning of the Rose Art brand; and expectations for the resumption of net sales growth in 2014.

Readers are cautioned, however, not to place undue reliance on forward-looking statements as there can be no assurance that the plans, intentions or expectations upon which they are based will occur. By their nature, forward-looking statements involve numerous assumptions, known and unknown risks and uncertainties, both general and specific, that contribute to the possibility that the predictions, forecasts, projections and other forward-looking statements will not occur. This may cause the Corporation’s actual performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward-looking statements. The Corporation disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required pursuant to applicable laws. The following important factors could cause the Corporation’s actual performance or financial results to differ materially from historical results and/or those results presently estimated or projected: general economic conditions; success in developing new products; difficulty in predicting consumer preferences and the acceptance of new products; the Corporation’s ability to maintain licensed products; the seasonality of the Toy and Stationery industries; liquidity and interest rate risk; risks inherent in the Corporation’s international operations; foreign currency fluctuations; the Corporation’s dependence on a few large customers; risks associated with customer and credit risk; fluctuations in the price of plastic resins and other raw materials used by the Corporation; risks associated with the Corporation’s tax structure; risks associated with litigation; risks associated with product liability claims, product recalls and government regulation; and the Corporation’s ability to obtain adequate insurance coverage. For more information on the risks, uncertainties and assumptions that could cause the Corporation’s actual performance or financial results to differ materially from historical results and/or current expectations, please refer to the ‘‘Risks and Uncertainties’’ section of this MD&A.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 5

Business Overview

MEGA Brands designs, manufactures and markets high quality toys and stationery products. Headquartered in Montreal, the Corporation has approximately 1,700 employees with offices, manufacturing facilities or distribution centers in 17 countries. The Corporation's products are sold in over 100 countries. The Corporation has a global sales organization with direct sales in 16 countries and distributor agreements worldwide. Distribution centers are located in the United States (Seattle), Canada (Montreal), Mexico, Belgium, Australia and the People’s Republic of China. The Corporation manufactures construction toys in Canada and woodcase pencils in the United States. The balance of the Corporation’s products is manufactured by qualified suppliers located in Asia, primarily in China. The Corporation manages its operations under two product segments, Toys and Stationery & Activities. � The Toys segment is comprised of MEGA BLOKS® construction toys and MEGA PUZZLES®.

� The Stationery & Activities segment is comprised of ROSE ART® art materials and craft and activity sets, BOARD DUDES® presentation boards and accessories, and WRITE DUDES®

writing

instruments.

Strategy, Objectives and 2013 Developments

Competitive Environment Competition in the Corporation’s product lines is based primarily on play experience, quality and price, and extends to the marketing and distribution of products and the acquisition of shelf space at retail. Certain of the Corporation’s competitors have greater financial resources, larger sales, marketing and product development departments, more diversified product offerings and benefit from greater economies of scale. Furthermore, the construction toy category, which represents the majority of the Corporation’s annual sales, is attractive to new competitors due to sustained consumer demand which have made this category one of the best performers in the toy industry during recent years.

The Corporation’s success rests on the execution of its strategic priorities: develop innovative products based on proprietary content and licensing agreements with popular brands and entertainment properties, manufacture and source high quality products on a competitive basis, and market its products to leading retailers and consumers worldwide.

Innovation and Content Product innovation is the main growth driver in the toy industry. The Corporation invests 3-4% of net sales annually to develop proprietary content and products and to integrate popular licensed content – from traditional, Web-based and videogame properties – into its product lines. Recognized for its successful track record in product innovation, the Corporation is an attractive partner for licensors seeking to expand the reach of their content into the growing construction toy category worldwide. The Corporation annually replaces approximately 40-50% of prior year toy sales with new product lines, and extensions and enhancements of existing lines. In 2013, the Corporation expanded its category-leading MEGA BLOKS® First Builders

TM line of

construction toys for preschoolers with new characters, vehicles and themes. Several products, including MEGA BLOKS Billy Beats Dancing Piano, won accolades for play and educational value. According to NPD Group, a market research firm, the MEGA BLOKS brand was number one in retail sales in the Preschool construction toy category in the United States in 2013. Sales of the Corporation’s construction toys for girls increased in 2013, led by an extensive MEGA BLOKS Barbie offering, a new line of MEGA BLOKS Smurfs playsets, and girl favorites MEGA BLOKS Hello Kitty and MEGA BLOKS Dora.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 6

In Boys & Collectors construction toys, the Corporation signed a multi-year global license with Activision Publishing, Inc. to develop construction toys based on the Call of Duty® franchise. Shipments of the new product line, Call of Duty Collector Construction Sets, began in September 2013, and was the top-selling new construction toy brand at U.S. retail in the fourth quarter of 2013, according to NPD Group. The Collector Series will be expanded in 2014 with the planned launch of Assassin’s Creed Collector Construction Sets following a licensing agreement with Ubisoft, owner of the Assassin’s Creed® franchise. The Corporation also signed an agreement with Nickelodeon for SpongeBob SquarePants, a global children’s favorite with one of the top-rated TV shows. Construction sets based on this property are expected to be at retail beginning in North America in Fall 2014, followed by international markets. The Corporation expects to launch two new construction toy brands in 2014, MEGA BLOKS American Builders in the United States and MEGA BLOKS World Builders in international markets. These brands will feature construction sets based on iconic names that are part of children’s everyday lives, including Caterpillar, John Deere and Jeep. In Stationery & Activities, the Corporation launched new activities playsets, a new line of learning products and extended its selection of writing instruments, boards and accessories. Operational Efficiency The Corporation seeks to optimize its supply chain by balancing its own manufacturing with products sourced from third-party suppliers located mainly in China. Each product line is sourced from the most competitive location based on production and transportation costs as well as other factors. Reflecting the significant increase in manufacturing input costs in China, the Corporation has progressively increased its Canadian production in recent years to over 50% of dollar sales in 2013. In 2013, the Corporation completed a three-year program to increase efficiency and production capacity at its Montreal facility. The investment in state-of-the-art tooling and equipment over this period totaled over $30 million and included the purchase and commissioning of energy-efficient high and medium capacity injection molding presses, in-mold labeling technology, high precision and high volume counting and bagging lines, as well as automated assembly and packaging equipment. Global Distribution The Corporation’s primary market is North America (U.S. and Canada). The MEGA BLOKS brand enjoys strong consumer recognition in North America and the Corporation has a significant market share in the construction toy category. In Stationery & Activities, the Corporation is a major player in the Activities category through its ROSE ART brand and in Stationery through BOARD DUDES and WRITE DUDES. The Corporation’s objective is to gain additional shelf space with existing retail customers and to penetrate new retail channels. Net sales in North America decreased 3% to $282.5 million in 2013 and accounted for 70% of consolidated net sales compared to 69% in 2012. Penetration of international markets has historically been an important growth driver for the MEGA BLOKS brand. The Corporation’s toys are sold in over 100 countries, supported by its own sales and marketing organization, partnerships and distributorships, providing global market coverage. International net sales decreased 5% to $122.2 million in 2013 and accounted for 30% of consolidated net sales compared to 31% in 2012. Please refer to the Results of Operations section of this MD&A for a discussion of factors affecting 2013 net sales by geographic segment.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 7

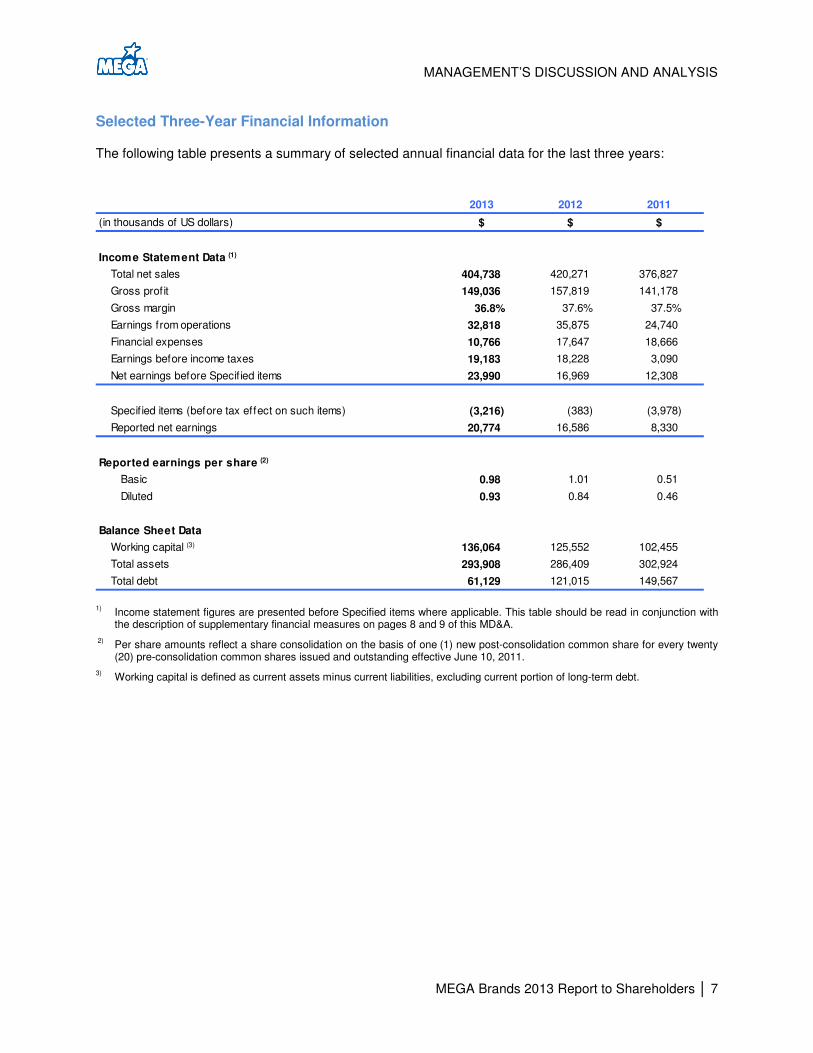

Selected Three-Year Financial Information

The following table presents a summary of selected annual financial data for the last three years:

(in thousands of US dollars)

Income Statement Data (1)

404,738 420,271 376,827

149,036 157,819 141,178

Gross margin 36.8% 37.6% 37.5%

32,818 35,875 24,740

Financial expenses 10,766 17,647 18,666

19,183 18,228 3,090

Net earnings before Specif ied items 23,990 16,969 12,308

(3,216) (383) (3,978)

Reported net earnings 20,774 16,586 8,330

Basic 0.98 1.01 0.51

Diluted 0.93 0.84 0.46

Working capital (3) 136,064 125,552 102,455

Total assets 293,908 286,409 302,924

Total debt 61,129 121,015 149,567

2013 2012 2011

$ $ $

Reported earnings per share (2)

Balance Sheet Data

Total net sales

Gross profit

Earnings from operations

Earnings before income taxes

Specif ied items (before tax effect on such items)

1) Income statement figures are presented before Specified items where applicable. This table should be read in conjunction with

the description of supplementary financial measures on pages 8 and 9 of this MD&A.

2) Per share amounts reflect a share consolidation on the basis of one (1) new post-consolidation common share for every twenty (20) pre-consolidation common shares issued and outstanding effective June 10, 2011.

3) Working capital is defined as current assets minus current liabilities, excluding current portion of long-term debt.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 8

Results of Operations

Supplementary Financial Measures The analysis of the Corporation’s operating performance and financial condition is based primarily on IFRS financial measures. The Corporation also analyses its results using additional IFRS measures (defined as measures which are not required under IFRS), as well as non-IFRS measures. The Corporation uses these additional IFRS and non-IFRS measures internally and includes them in this MD&A because it believes they are commonly used by investors as a means of assessing its financial performance and that of other companies in the toy industry. The non-IFRS measures and their definition are as follows:

• EBITDA is calculated as net earnings before interest, taxes, depreciation and amortization.

• Adjusted EBITDA is calculated as EBITDA excluding Specified items, which are described below. Specified items are excluded because they do not necessarily reflect the Corporation’s underlying financial performance. Adjusted EBITDA is used internally as the key benchmark for incentive compensation and by investors and lenders as a measure of the Corporation’s profitability and its ability to fund working capital requirements, investment in property, plant and equipment, and debt repayments. Such measures also allow for the assessment of the Corporation’s operating performance and financial condition on a basis that is both consistent and comparable between reporting periods.

• Net earnings before Specified items is calculated as net earnings excluding Specified items, which are described below.

Readers are cautioned that non-IFRS financial measures do not have standardized meaning and are unlikely to be comparable to similar measures used by other issuers. The additional IFRS measures and their definition are as follows:

• Gross profit is calculated as net sales less cost of sales.

• Gross margin is calculated as gross profit divided by net sales.

• Earnings from operations is calculated as net earnings before financial expenses and income taxes.

Specified items The Corporation has identified certain charges as ‘‘Specified items’’. These are described below under various headings, along with their classification in the financial statements according to IFRS. The Corporation does not imply that Specified items are non-recurring. Fourth quarter and year ended December 31, 2013 Specified items had a negative impact on earnings before income taxes of $3.3 million in year ended December 31, 2013 ($0.1 million in the fourth quarter), as follows: Early redemption of debentures The Corporation recorded a charge of $2.9 million (nil in the fourth quarter) related to the early redemption of debentures. This charge is presented as a separate item on the income statement. Contingent consideration on business acquisition The Corporation recorded a contingent consideration on business acquisition of $0.4 million ($0.1 million in the fourth quarter) related to the Stationery & Activities segment. This charge is presented as a separate item in the income statement.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 9

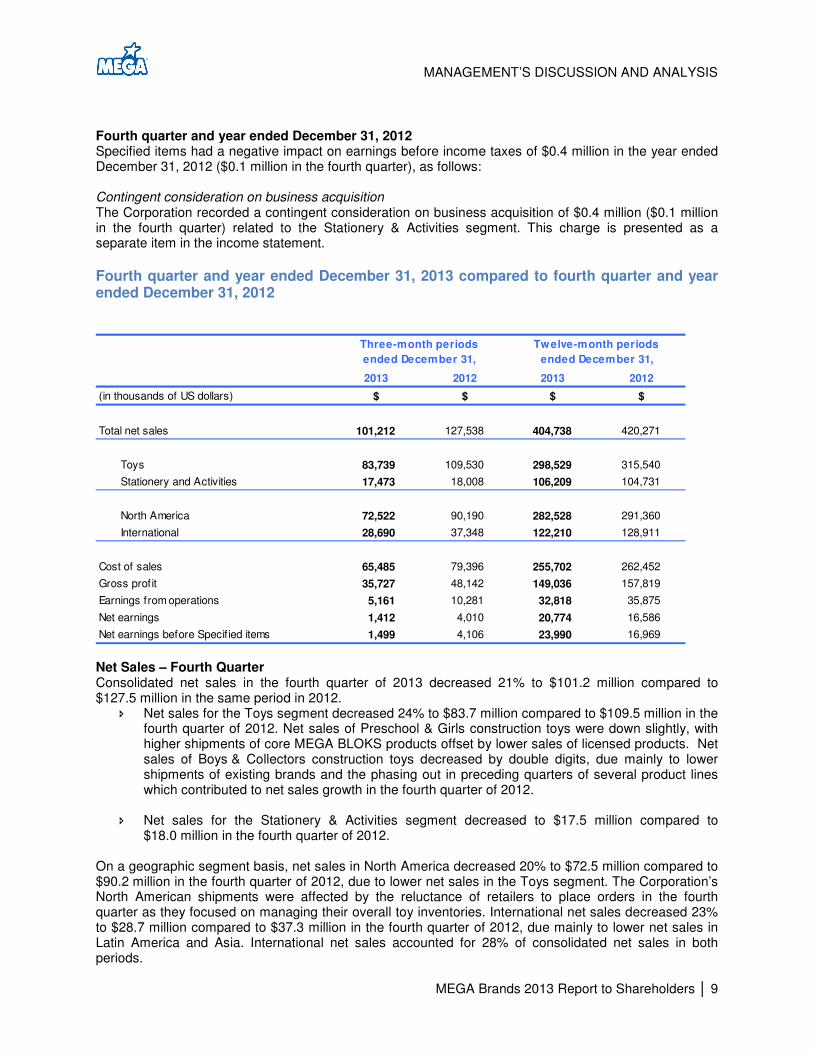

Fourth quarter and year ended December 31, 2012 Specified items had a negative impact on earnings before income taxes of $0.4 million in the year ended December 31, 2012 ($0.1 million in the fourth quarter), as follows: Contingent consideration on business acquisition The Corporation recorded a contingent consideration on business acquisition of $0.4 million ($0.1 million in the fourth quarter) related to the Stationery & Activities segment. This charge is presented as a separate item in the income statement.

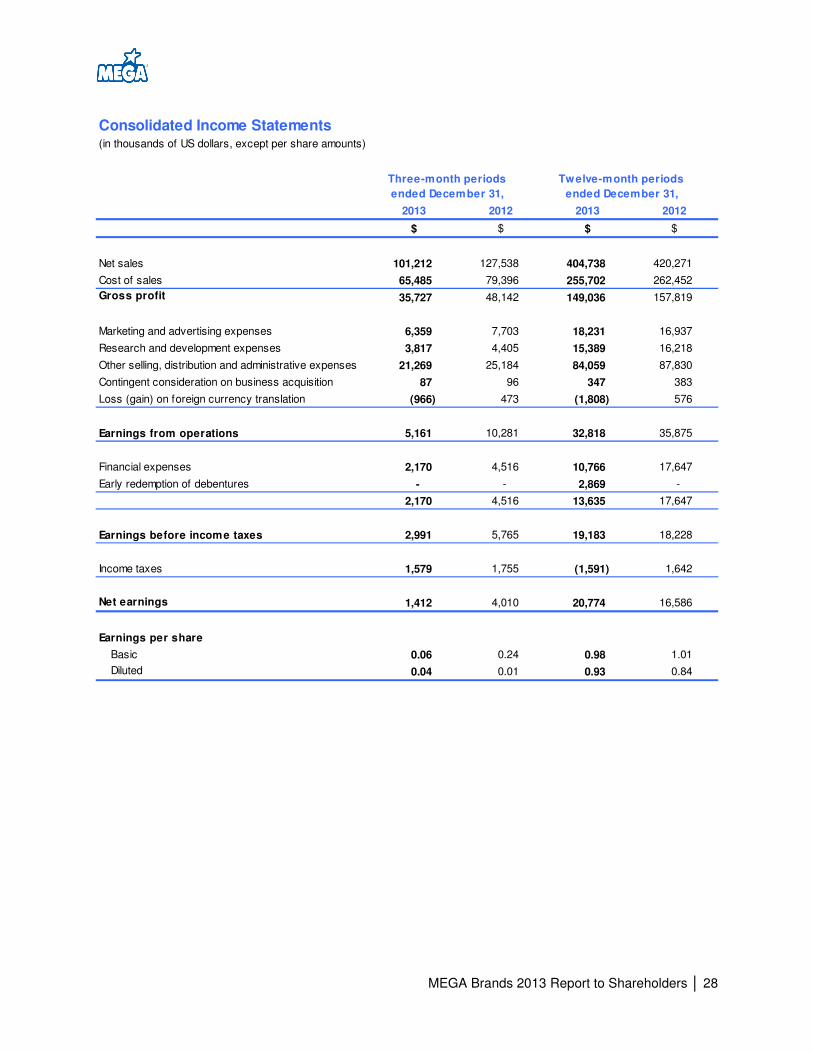

Fourth quarter and year ended December 31, 2013 compared to fourth quarter and year ended December 31, 2012

(in thousands of US dollars)

101,212 127,538 404,738 420,271

Toys 83,739 109,530 298,529 315,540

Stationery and Activities 17,473 18,008 106,209 104,731

North America 72,522 90,190 282,528 291,360

International 28,690 37,348 122,210 128,911

65,485 79,396 255,702 262,452

35,727 48,142 149,036 157,819

5,161 10,281 32,818 35,875

Net earnings 1,412 4,010 20,774 16,586

Net earnings before Specif ied items 1,499 4,106 23,990 16,969

Cost of sales

Gross profit

Earnings from operations

Total net sales

2013

$

2012

$

Three-month periods

ended December 31,

Twelve-month periods

ended December 31,

2013 2012

$ $

Net Sales – Fourth Quarter Consolidated net sales in the fourth quarter of 2013 decreased 21% to $101.2 million compared to $127.5 million in the same period in 2012.

� Net sales for the Toys segment decreased 24% to $83.7 million compared to $109.5 million in the fourth quarter of 2012. Net sales of Preschool & Girls construction toys were down slightly, with higher shipments of core MEGA BLOKS products offset by lower sales of licensed products. Net sales of Boys & Collectors construction toys decreased by double digits, due mainly to lower shipments of existing brands and the phasing out in preceding quarters of several product lines which contributed to net sales growth in the fourth quarter of 2012.

� Net sales for the Stationery & Activities segment decreased to $17.5 million compared to $18.0 million in the fourth quarter of 2012.

On a geographic segment basis, net sales in North America decreased 20% to $72.5 million compared to $90.2 million in the fourth quarter of 2012, due to lower net sales in the Toys segment. The Corporation’s North American shipments were affected by the reluctance of retailers to place orders in the fourth quarter as they focused on managing their overall toy inventories. International net sales decreased 23% to $28.7 million compared to $37.3 million in the fourth quarter of 2012, due mainly to lower net sales in Latin America and Asia. International net sales accounted for 28% of consolidated net sales in both periods.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 10

Net Sales – Full Year Reflecting the impact of weak fourth quarter net sales, consolidated net sales in 2013 decreased 4% to $404.7 million compared to $420.3 million in 2012.

� Net sales for the Toys segment decreased 5% to $298.5 million compared to $315.5 million in 2012, as lower shipments in the fourth quarter more than offset higher year-over-year shipments through the first nine months of 2013. Shipments of Preschool & Girls construction toys increased compared to 2012, with net sales growth in both core MEGA BLOKS and licensed products. This strong performance was offset mainly by softness in Boys & Collectors construction toys resulting from lower shipments of existing brands and the phasing out of several product lines during the year.

� Net sales for the Stationery & Activities segment increased 1% to $106.2 million compared to $104.7 million in 2012.

On a geographic segment basis, net sales in North America decreased 3% to $282.5 million compared to $291.4 million in 2012, reflecting lower net sales in the Toys segment. International net sales decreased 5% to $122.2 million compared to $128.9 million in 2012. This decrease is explained mainly by lower sales in Latin America. International net sales accounted for 30% of consolidated net sales compared to 31% in 2012. According to NPD Group, 2013 retail sales of MEGA BLOKS construction toys increased 4.4% in the United Sates. Cost of Sales and Gross Profit Cost of sales decreased to $65.5 million compared to $79.4 million in the fourth quarter of 2012. Gross profit was $35.7 million compared to $48.1 million in the fourth quarter of 2012, while gross margin was 35.3% compared to 37.7%. The lower gross profit and gross margin reflect the decrease in net sales and unfavorable product mix compared to the fourth quarter of 2012. For the year ended December 31, 2013, cost of sales decreased to $255.7 million compared to $262.5 million in 2012. Gross profit was $149.0 million, or 36.8% of net sales, compared to $157.8 million, or 37.6% of net sales, in 2012. These negative variances reflect mainly lower net sales and unfavorable product mix compared to 2012, which more than offset higher efficiency in the Corporation’s Montreal facility. It should be noted that gross margins for the Corporation’s Boys & Collectors product lines are typically higher than for its Preschool & Girls product lines. Operating Expenses and Other Marketing and advertising expenses were $6.4 million compared to $7.7 million in the fourth quarter of 2012. For the year ended December 31, 2013, such expenses were $18.2 million compared to $16.9 million in 2012. Research and development expenses were $3.8 million compared to $4.4 million in the fourth quarter of 2012. For the year ended December 31, 2013, such expenses were $15.4 million compared to $16.2 million in 2012, in line with the Corporation’s objective to devote 3-4% of net sales annually to product and content innovation. Other selling, distribution and administrative expenses decreased to $21.3 million compared to $25.2 million in the fourth quarter of 2012. This decrease reflects mainly lower selling and distribution costs in line with net sales in the 2013 period and lower compensation expenses related to the Corporation’s 2013 financial performance. For the year ended December 31, 2013, such expenses were $84.1 million compared to $87.8 million in 2012, reflecting mainly lower selling and distribution expenses.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 11

Earnings from operations As a result of the above, earnings from operations were $5.2 million compared to $10.3 million in the fourth quarter of 2012. � On a product segment basis, earnings from operations for Toys were $3.6 million compared to

$8.3 million in the fourth quarter of 2012. Earnings from operations for Stationery & Activities were $1.6 million compared to $2.0 million in the fourth quarter of 2012.

� On a geographic segment basis, earnings from operations for North America were $2.6 million compared to $5.7 million in the fourth quarter of 2012. Earnings from operations for International were $2.6 million compared to $4.5 million in the fourth quarter of 2012.

For the year ended December 31, 2013, earnings from operations were $32.8 million compared to $35.9 million in 2012. � On a product segment basis, earnings from operations for Toys were $30.7 million compared to

$33.8 million in 2012. For Stationery & Activities, earnings from operations were $2.1 million compared to $2.1 million in 2012.

� On a geographic segment basis, earnings from operations for North America were $25.1 million

compared to $26.6 million in 2012. Earnings from operations for International were $7.7 million compared to $9.3 million in 2012.

Financial Expenses Financial expenses were $2.2 million compared to $4.5 million in the fourth quarter of 2012. For the year ended December 31, 2013, financial expenses declined to $10.8 million compared to $17.6 million in 2012. The decline in both periods is due mainly to the reduction in long-term debt following the scheduled principal repayment of $7.1 million on the Corporation’s debentures on March 30, 2013, the early redemption of $52.9 million in principal amount of debentures on April 15, 2013, as well as lower utilization of the Corporation’s working capital facility. Early Redemption of Debentures The Corporation recorded a charge of $2.9 million in the first quarter of 2013 related to the early redemption of debentures. No such charge was recorded in 2012. Income Tax Expense (Recovery) Income tax expense was $1.6 million compared to $1.8 million in the fourth quarter of 2012. This decrease reflects lower net earnings before income taxes in the 2013 period. For the year ended December 31, 2013, income tax recovery was $1.6 million compared to an expense of $1.6 million in 2012. The recovery in 2013 results mainly from the reimbursement of taxes paid in prior years following an appeal by the Corporation and a favorable decision by Canadian tax authorities. The tax rate used to establish the income tax expense is the applicable estimated effective rate of each entity of the Corporation. Net Earnings Net earnings were $1.4 million or $0.04 per diluted share ($0.06 per basic share) compared to $4.0 million or $0.01 per diluted share ($0.24 per basic share) in the fourth quarter of 2012. Basic earnings per share were calculated on the basis of 22,939,531 weighted average common shares outstanding in 2013 and 16,456,870 shares in 2012. Diluted earnings per share were calculated on the basis of 27,744,222 weighted average common shares outstanding in 2013 and 28,719,603 common shares in 2012.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 12

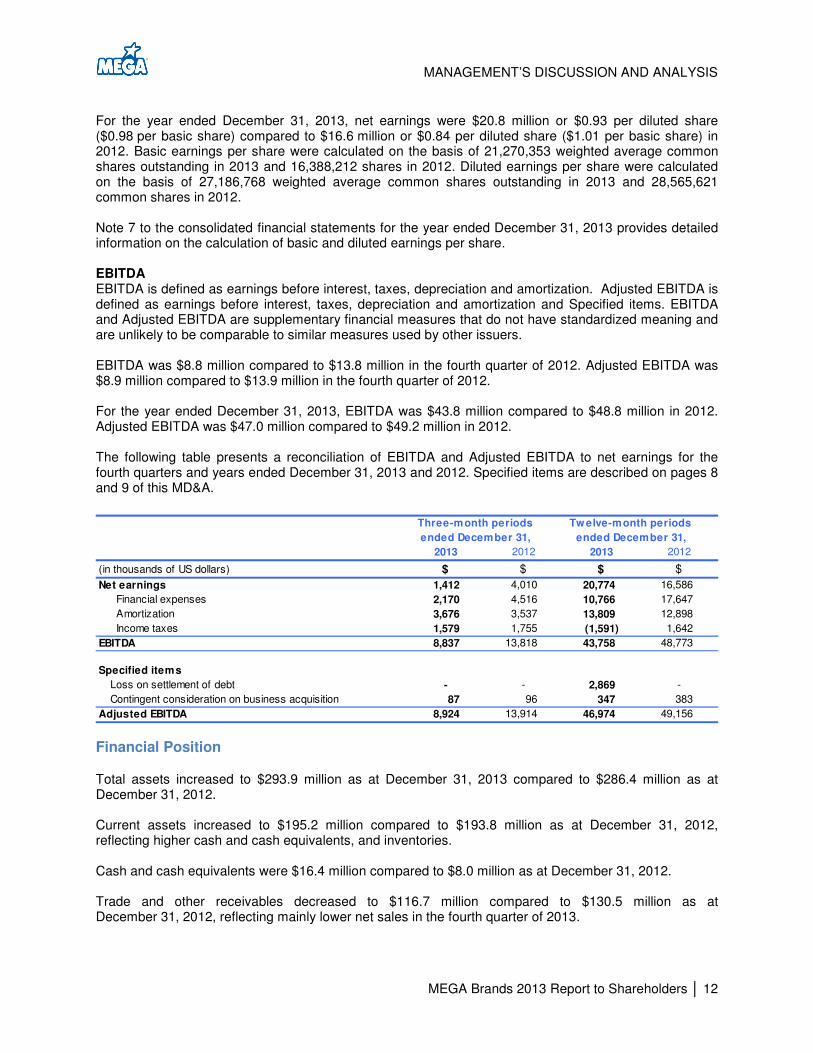

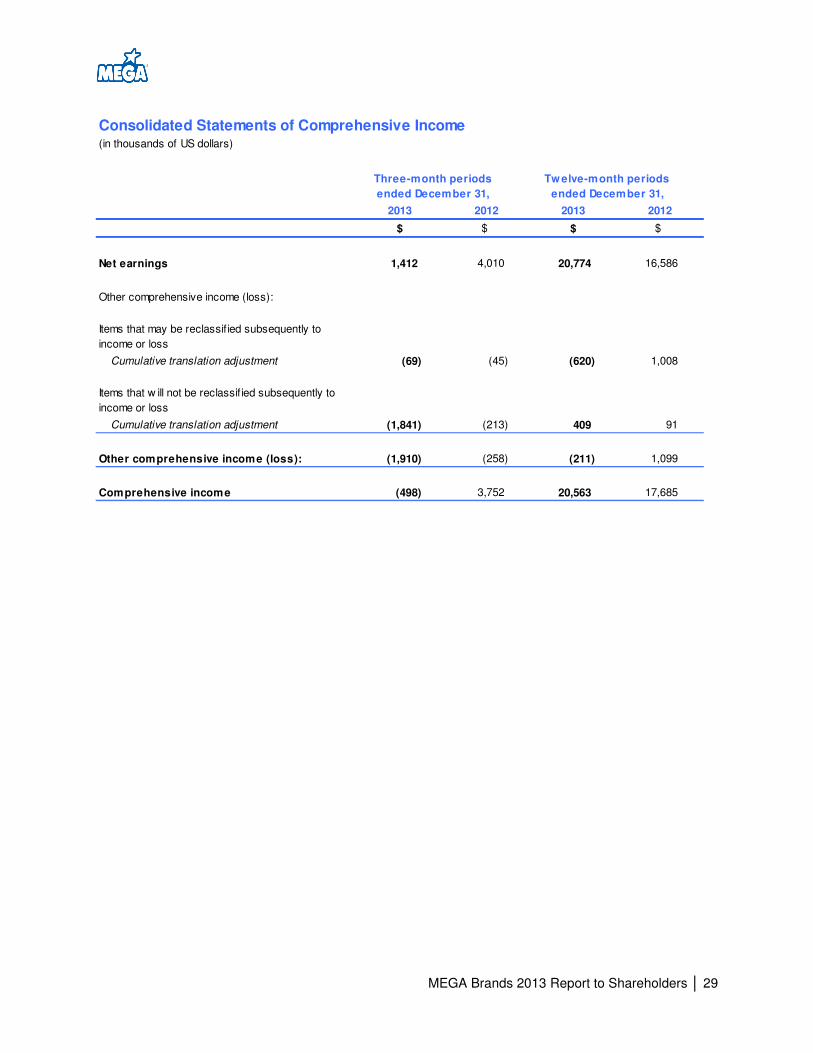

For the year ended December 31, 2013, net earnings were $20.8 million or $0.93 per diluted share ($0.98 per basic share) compared to $16.6 million or $0.84 per diluted share ($1.01 per basic share) in 2012. Basic earnings per share were calculated on the basis of 21,270,353 weighted average common shares outstanding in 2013 and 16,388,212 shares in 2012. Diluted earnings per share were calculated on the basis of 27,186,768 weighted average common shares outstanding in 2013 and 28,565,621 common shares in 2012. Note 7 to the consolidated financial statements for the year ended December 31, 2013 provides detailed information on the calculation of basic and diluted earnings per share. EBITDA EBITDA is defined as earnings before interest, taxes, depreciation and amortization. Adjusted EBITDA is defined as earnings before interest, taxes, depreciation and amortization and Specified items. EBITDA and Adjusted EBITDA are supplementary financial measures that do not have standardized meaning and are unlikely to be comparable to similar measures used by other issuers. EBITDA was $8.8 million compared to $13.8 million in the fourth quarter of 2012. Adjusted EBITDA was $8.9 million compared to $13.9 million in the fourth quarter of 2012. For the year ended December 31, 2013, EBITDA was $43.8 million compared to $48.8 million in 2012. Adjusted EBITDA was $47.0 million compared to $49.2 million in 2012. The following table presents a reconciliation of EBITDA and Adjusted EBITDA to net earnings for the fourth quarters and years ended December 31, 2013 and 2012. Specified items are described on pages 8 and 9 of this MD&A.

(in thousands of US dollars)

Net earnings 1,412 4,010 20,774 16,586

Financial expenses 2,170 4,516 10,766 17,647

Amortization 3,676 3,537 13,809 12,898

Income taxes 1,579 1,755 (1,591) 1,642

EBITDA 8,837 13,818 43,758 48,773

Specified items

Loss on settlement of debt - - 2,869 -

Contingent consideration on business acquisition 87 96 347 383

Adjusted EBITDA 8,924 13,914 46,974 49,156

$ $ $ $

Three-month periods Twelve-month periods

ended December 31, ended December 31,

2013 2012 2013 2012

Financial Position

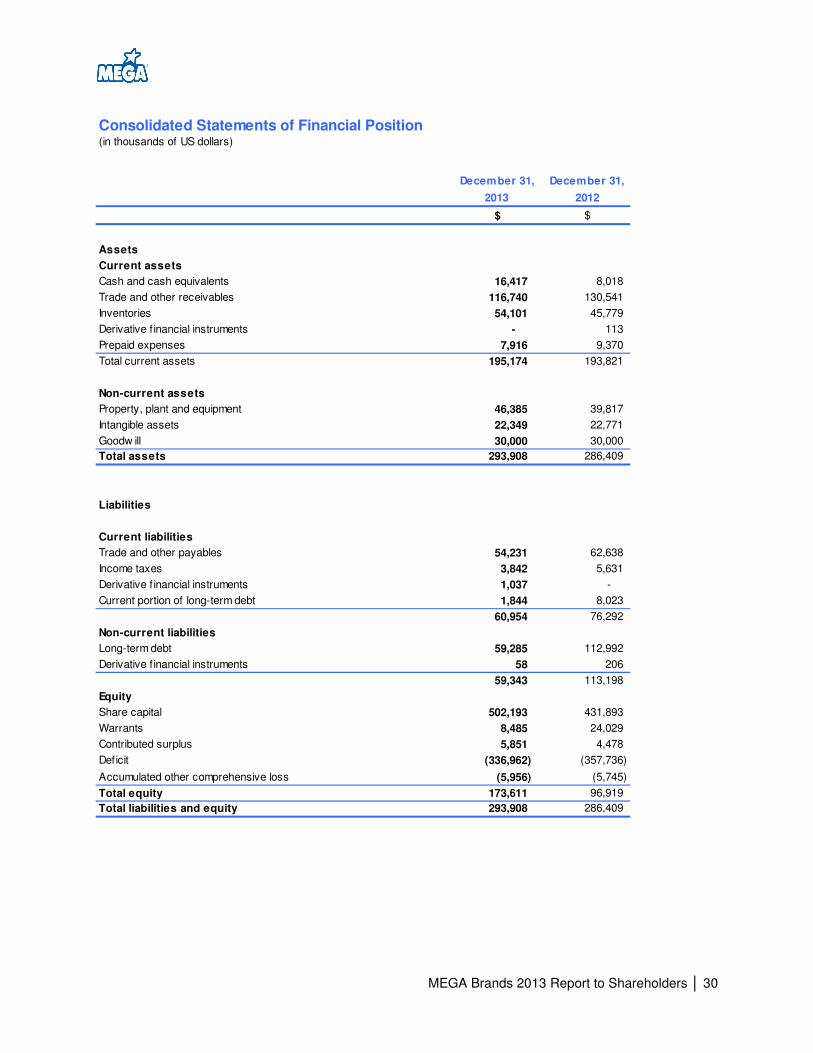

Total assets increased to $293.9 million as at December 31, 2013 compared to $286.4 million as at December 31, 2012. Current assets increased to $195.2 million compared to $193.8 million as at December 31, 2012, reflecting higher cash and cash equivalents, and inventories. Cash and cash equivalents were $16.4 million compared to $8.0 million as at December 31, 2012. Trade and other receivables decreased to $116.7 million compared to $130.5 million as at December 31, 2012, reflecting mainly lower net sales in the fourth quarter of 2013.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 13

Inventories increased to $54.1 million compared to $45.8 million as at December 31, 2012, also reflecting lower net sales in the fourth quarter of 2013. Non-current assets increased to $98.7 million compared to $92.6 million as at December 31, 2012. This is due mainly to higher property, plant and equipment, which rose to $46.4 million compared to $39.8 million as at December 31, 2012, as a result of investments in new tooling and equipment at the Corporation’s Montreal facility, net of depreciation and amortization. Current liabilities were $61.0 million compared to $76.3 million as at December 31, 2012. This reflects mainly a decrease in current portion of long-term debt and lower accounts payable and accrued liabilities. Unlike in 2013, no principal repayments are scheduled on the Corporation’s debentures in 2014. Trade and other payables decreased to $54.2 million compared to $62.6 million as at December 31, 2012, reflecting mainly tight cost management in the fourth quarter of 2013 in light of lower net sales. Long-term debt was $59.3 million compared to $113.0 million as at December 31, 2012. This decline is explained mainly by a scheduled principal repayment of $7.1 million on the Corporation’s debentures on March 30, 2013 and the early redemption of $52.9 million in principal amount of debentures on April 15, 2013. As at December 31, 2013, the Corporation recorded an unrealized loss on derivative financial instruments of $1.1 million related to unrealized foreign exchange contracts, due mainly to the weakening of the Canadian dollar against the US dollar at the balance sheet date. As at December 31, 2012, the Corporation recorded an unrealized loss of $0.1 million on derivative financial instruments. The following table presents selected data relating to the Corporation’s financial position for the indicated periods:

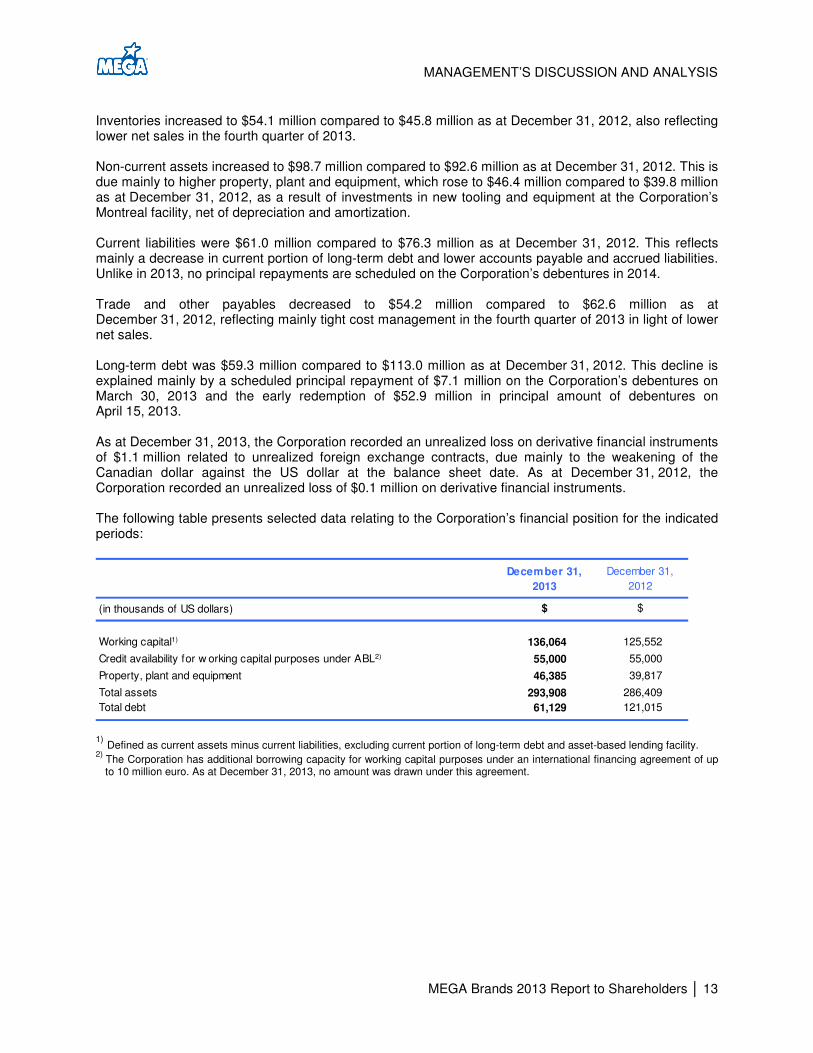

(in thousands of US dollars)

Working capital1) 136,064 125,552

Credit availability for w orking capital purposes under ABL2) 55,000 55,000

Property, plant and equipment 46,385 39,817

Total assets 293,908 286,409

Total debt 61,129 121,015

December 31, December 31,

2013 2012

$$

1)

Defined as current assets minus current liabilities, excluding current portion of long-term debt and asset-based lending facility. 2)

The Corporation has additional borrowing capacity for working capital purposes under an international financing agreement of up to 10 million euro. As at December 31, 2013, no amount was drawn under this agreement.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 14

Cash Flows

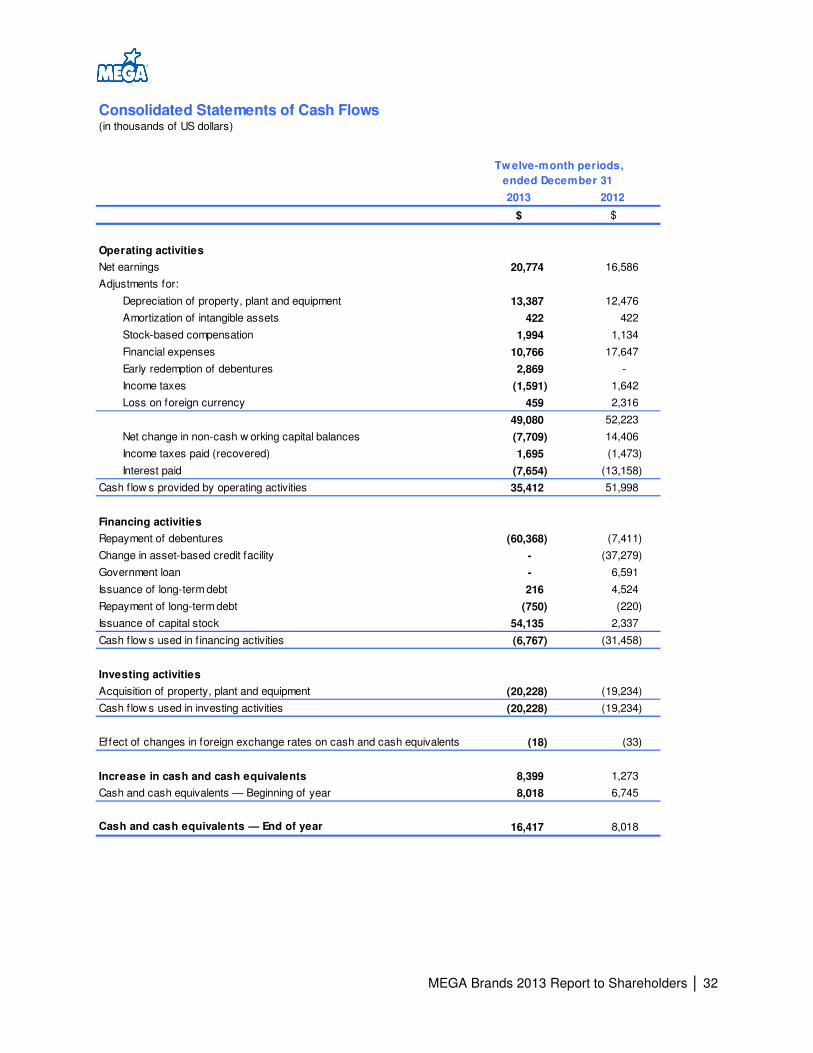

Operating Activities Operating activities provided cash flows of $35.4 million in 2013 compared to $52.0 million in 2012. The year-over-year decline in cash flows reflects mainly unfavorable changes in non-cash working capital balances, due mainly to higher inventories and lower trade and other payables. Changes in non-cash working capital balances are presented in Note 17 to the consolidated financial statements. Financing Activities Financing activities used cash flows of $6.8 million in 2013, compared to cash flows used of $31.5 million in 2012. In 2013, the Corporation issued common shares as a result of the exercise of warrants for cash proceeds of $54.1 million and redeemed $52.9 million in principal amount of its debentures. The Corporation also made a scheduled principal repayment of $7.1 million on its debentures. In 2012, the Corporation raised $6.6 million from a government loan, $4.5 million from a capital lease financing and $2.3 million from the issuance of common shares as a result of the exercise of warrants and options. The Corporation fully repaid its asset-based credit facility in the amount of $37.3 million and made a scheduled principal repayment of $7.4 million on its debentures. Investing Activities Investing activities used cash flows of $20.2 million in 2013, compared to $19.2 million in 2012. The amounts in both years represent investments in new tooling and equipment to increase the efficiency and production capacity of the Corporation’s Montreal facility, as well as recurring investments in production molds for new product lines. Foreign exchange Fluctuations in foreign exchange rates did not have a material impact on cash and cash equivalents in 2013 and 2012. The Corporation holds the majority of its cash and cash equivalents in US dollars, its reporting currency.

Liquidity and Capital Resources

The Corporation’s primary sources of liquidity are cash flows from operations and short-term borrowings under a $55-million asset-based credit facility and an international financing agreement. Cash flows from operations could be negatively impacted by decreased demand for the Corporation’s products, which could result from factors such as adverse economic conditions and changes in public and consumer preferences, the continued confidence of the Corporation’s principal customers in the Corporation and its product lines, or by increased costs associated with manufacturing and distribution of products. The Corporation’s primary capital needs are related to inventory financing, accounts receivable funding, debt servicing and capital expenditures for new product initiatives. As a result of the seasonal nature of the toy and stationery industries, working capital requirements are variable throughout the year. Working capital needs typically grow through the first three quarters as inventories are built-up for the peak sales periods for retailers, being the July-September quarter for the Stationery & Activities product lines and the October-December quarter for the Toys product lines. The Corporation’s cash flows from operating activities are typically at their highest levels of the year in the fourth quarter. The Corporation reduced the outstanding principal amount of its debentures to CA$53.7 million as at December 31, 2013, compared to CA$114.6 million as at December 31, 2012. This reduction in long-term debt includes a scheduled principal repayment of $7.1 million on March 30, 2013 and the early redemption of $52.9 million in principal amount of debentures on April 15, 2013 using proceeds from the exercise of common share purchase warrants by the Corporation’s three largest shareholders and other warrant holders. No principal repayments are scheduled on the debentures in 2014 and the amount outstanding is repayable in full on March 30, 2015.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 15

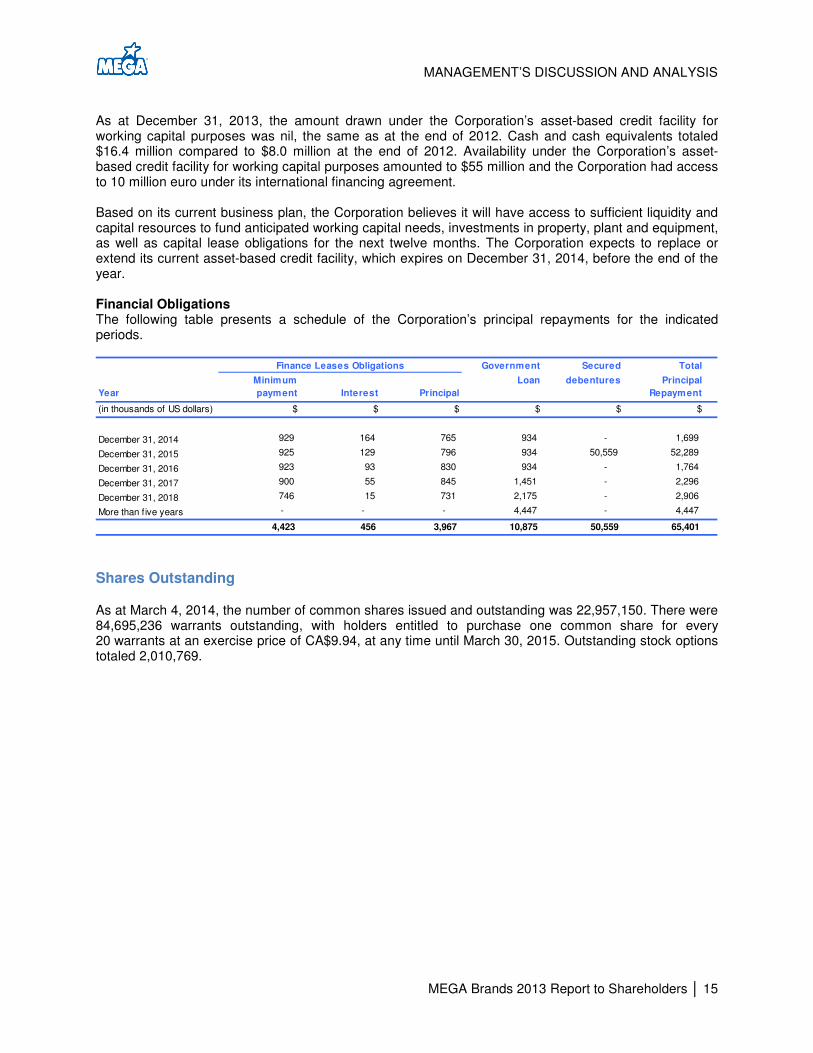

As at December 31, 2013, the amount drawn under the Corporation’s asset-based credit facility for working capital purposes was nil, the same as at the end of 2012. Cash and cash equivalents totaled $16.4 million compared to $8.0 million at the end of 2012. Availability under the Corporation’s asset-based credit facility for working capital purposes amounted to $55 million and the Corporation had access to 10 million euro under its international financing agreement. Based on its current business plan, the Corporation believes it will have access to sufficient liquidity and capital resources to fund anticipated working capital needs, investments in property, plant and equipment, as well as capital lease obligations for the next twelve months. The Corporation expects to replace or extend its current asset-based credit facility, which expires on December 31, 2014, before the end of the year. Financial Obligations The following table presents a schedule of the Corporation’s principal repayments for the indicated periods.

Government Secured Total

Minimum Loan debentures Principal

Year payment Interest Principal Repayment

(in thousands of US dollars) $ $ $ $ $ $

December 31, 2014 929 164 765 934 - 1,699

December 31, 2015 925 129 796 934 50,559 52,289

December 31, 2016 923 93 830 934 - 1,764

December 31, 2017 900 55 845 1,451 - 2,296

December 31, 2018 746 15 731 2,175 - 2,906

More than five years - - - 4,447 - 4,447

4,423 456 3,967 10,875 50,559 65,401

Finance Leases Obligations

Shares Outstanding

As at March 4, 2014, the number of common shares issued and outstanding was 22,957,150. There were 84,695,236 warrants outstanding, with holders entitled to purchase one common share for every 20 warrants at an exercise price of CA$9.94, at any time until March 30, 2015. Outstanding stock options totaled 2,010,769.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 16

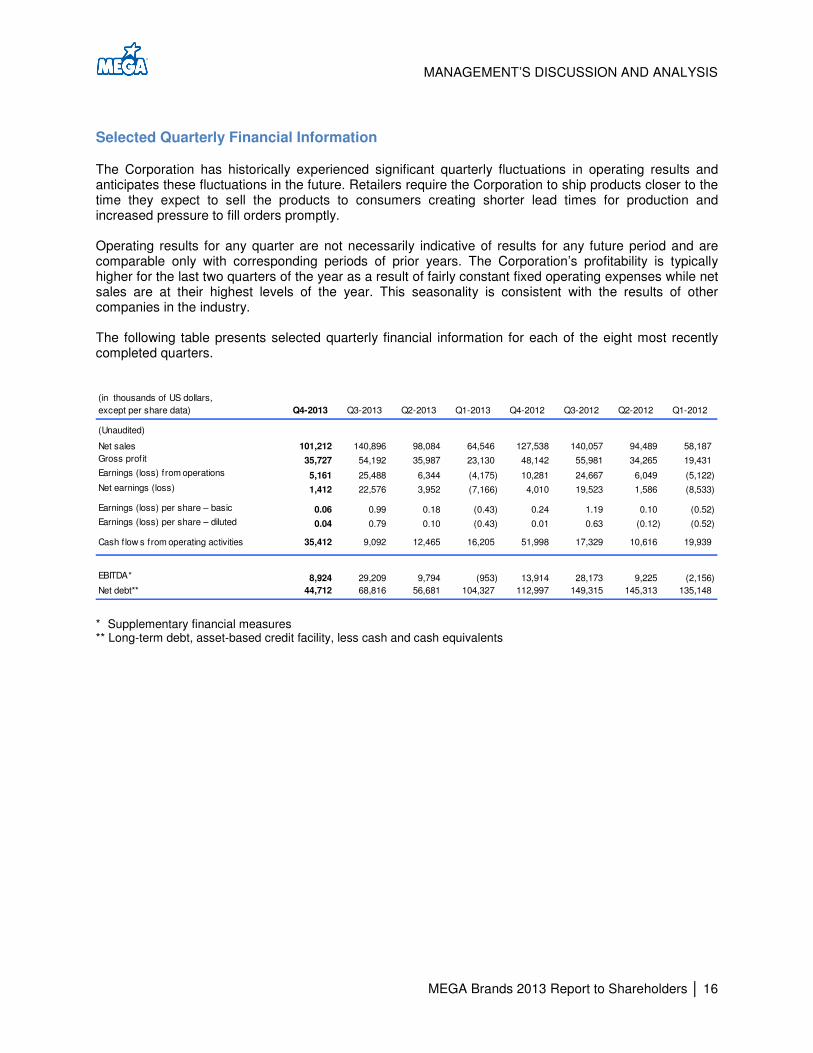

Selected Quarterly Financial Information

The Corporation has historically experienced significant quarterly fluctuations in operating results and anticipates these fluctuations in the future. Retailers require the Corporation to ship products closer to the time they expect to sell the products to consumers creating shorter lead times for production and increased pressure to fill orders promptly. Operating results for any quarter are not necessarily indicative of results for any future period and are comparable only with corresponding periods of prior years. The Corporation’s profitability is typically higher for the last two quarters of the year as a result of fairly constant fixed operating expenses while net sales are at their highest levels of the year. This seasonality is consistent with the results of other companies in the industry. The following table presents selected quarterly financial information for each of the eight most recently completed quarters.

(in thousands of US dollars,

except per share data) Q4-2013 Q3-2013 Q2-2013 Q1-2013 Q4-2012 Q3-2012 Q2-2012 Q1-2012

(Unaudited)

Net sales 101,212 140,896 98,084 64,546 127,538 140,057 94,489 58,187

Gross profit 35,727 54,192 35,987 23,130 48,142 55,981 34,265 19,431

Earnings (loss) from operations 5,161 25,488 6,344 (4,175) 10,281 24,667 6,049 (5,122)

Net earnings (loss) 1,412 22,576 3,952 (7,166) 4,010 19,523 1,586 (8,533)

Earnings (loss) per share – basic 0.06 0.99 0.18 (0.43) 0.24 1.19 0.10 (0.52)

Earnings (loss) per share – diluted 0.04 0.79 0.10 (0.43) 0.01 0.63 (0.12) (0.52)

- - - - - - Cash f low s from operating activities 35,412 9,092 12,465 16,205 51,998 17,329 10,616 19,939

EBITDA* 8,924 29,209 9,794 (953) 13,914 28,173 9,225 (2,156)

Net debt** 44,712 68,816 56,681 104,327 112,997 149,315 145,313 135,148

* Supplementary financial measures ** Long-term debt, asset-based credit facility, less cash and cash equivalents

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 17

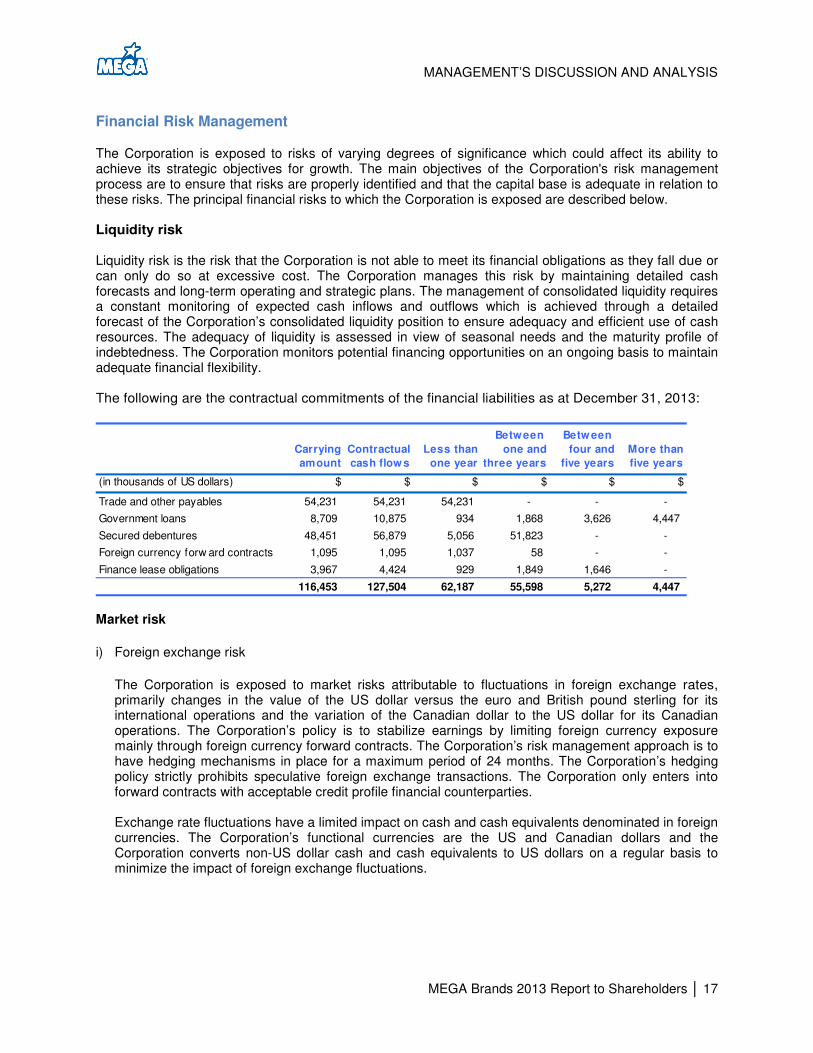

Financial Risk Management

The Corporation is exposed to risks of varying degrees of significance which could affect its ability to achieve its strategic objectives for growth. The main objectives of the Corporation's risk management process are to ensure that risks are properly identified and that the capital base is adequate in relation to these risks. The principal financial risks to which the Corporation is exposed are described below. Liquidity risk Liquidity risk is the risk that the Corporation is not able to meet its financial obligations as they fall due or can only do so at excessive cost. The Corporation manages this risk by maintaining detailed cash forecasts and long-term operating and strategic plans. The management of consolidated liquidity requires a constant monitoring of expected cash inflows and outflows which is achieved through a detailed forecast of the Corporation’s consolidated liquidity position to ensure adequacy and efficient use of cash resources. The adequacy of liquidity is assessed in view of seasonal needs and the maturity profile of indebtedness. The Corporation monitors potential financing opportunities on an ongoing basis to maintain adequate financial flexibility. The following are the contractual commitments of the financial liabilities as at December 31, 2013:

Between Betw een

Carrying Contractual Less than one and four and More than

amount cash flow s one year three years five years five years

(in thousands of US dollars) $ $ $ $ $ $

Trade and other payables 54,231 54,231 54,231 - - -

Government loans 8,709 10,875 934 1,868 3,626 4,447

Secured debentures 48,451 56,879 5,056 51,823 - -

Foreign currency forw ard contracts 1,095 1,095 1,037 58 - -

Finance lease obligations 3,967 4,424 929 1,849 1,646 -

116,453 127,504 62,187 55,598 5,272 4,447 Market risk

i) Foreign exchange risk

The Corporation is exposed to market risks attributable to fluctuations in foreign exchange rates, primarily changes in the value of the US dollar versus the euro and British pound sterling for its international operations and the variation of the Canadian dollar to the US dollar for its Canadian operations. The Corporation’s policy is to stabilize earnings by limiting foreign currency exposure mainly through foreign currency forward contracts. The Corporation’s risk management approach is to have hedging mechanisms in place for a maximum period of 24 months. The Corporation’s hedging policy strictly prohibits speculative foreign exchange transactions. The Corporation only enters into forward contracts with acceptable credit profile financial counterparties.

Exchange rate fluctuations have a limited impact on cash and cash equivalents denominated in foreign currencies. The Corporation’s functional currencies are the US and Canadian dollars and the Corporation converts non-US dollar cash and cash equivalents to US dollars on a regular basis to minimize the impact of foreign exchange fluctuations.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 18

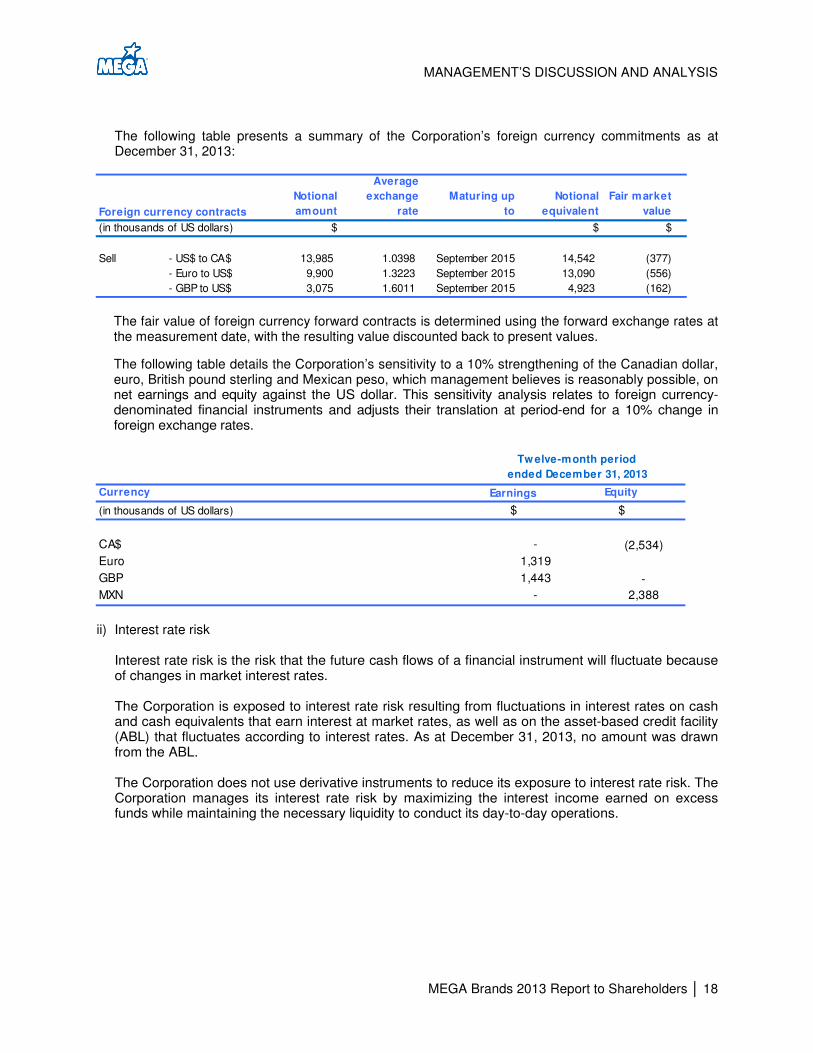

The following table presents a summary of the Corporation’s foreign currency commitments as at December 31, 2013:

Notional

amount

Average

exchange

rate

Maturing up

to

Notional

equivalent

Fair market

value

(in thousands of US dollars) $ $ $

Sell - US$ to CA$ 13,985 1.0398 September 2015 14,542 (377)

- Euro to US$ 9,900 1.3223 September 2015 13,090 (556)

- GBP to US$ 3,075 1.6011 September 2015 4,923 (162)

Foreign currency contracts

The fair value of foreign currency forward contracts is determined using the forward exchange rates at the measurement date, with the resulting value discounted back to present values.

The following table details the Corporation’s sensitivity to a 10% strengthening of the Canadian dollar, euro, British pound sterling and Mexican peso, which management believes is reasonably possible, on net earnings and equity against the US dollar. This sensitivity analysis relates to foreign currency-denominated financial instruments and adjusts their translation at period-end for a 10% change in foreign exchange rates.

Currency Earnings Equity

(in thousands of US dollars) $ $

CA$ - (2,534)

Euro 1,319

GBP 1,443 -

MXN - 2,388

Tw elve-month period

ended December 31, 2013

ii) Interest rate risk

Interest rate risk is the risk that the future cash flows of a financial instrument will fluctuate because of changes in market interest rates. The Corporation is exposed to interest rate risk resulting from fluctuations in interest rates on cash and cash equivalents that earn interest at market rates, as well as on the asset-based credit facility (ABL) that fluctuates according to interest rates. As at December 31, 2013, no amount was drawn from the ABL. The Corporation does not use derivative instruments to reduce its exposure to interest rate risk. The Corporation manages its interest rate risk by maximizing the interest income earned on excess funds while maintaining the necessary liquidity to conduct its day-to-day operations.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 19

Credit risk Credit risk is the risk of an unexpected loss if a customer or third party to a financial instrument fails to meet its contractual obligations. The Corporation reduces its credit risks arising from cash and cash equivalents, derivative financial instruments and deposits with banks and financial institutions by dealing with large financial institutions. The Corporation’s receivables consist of invoices to customers net of provisions for chargebacks for customer-related programs. This risk is reduced through the analysis of the financial position of its customers and the regular review of their credit limits, and by taking steps to mitigate the risk of loss by obtaining credit insurance. Due to the geographic diversity of its customers and its procedures for the management of commercial risks, the Corporation believes there is no particular concentration of credit risk.

Significant Accounting Policies and Use of Estimates

The Corporation prepares its financial statements in accordance with International Financial Reporting Standards (‘‘IFRS’’), using the US dollar as the reporting currency. The consolidated financial statements include the accounts of the Corporation and its wholly-owned subsidiaries since their date of acquisition. All intercompany balances and transactions have been eliminated on consolidation. The Corporation’s significant accounting policies are described in note 2 to the 2013 audited annual consolidated financial statements. The preparation of financial statements in conformity with IFRS requires management to make estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected. The following are critical judgments that management has made in the process of applying accounting policies and that have the most significant effect on the amounts recognized in the consolidated financial statements:

• Income taxes • Indefinite life intangibles

Key sources of estimation uncertainty that have a significant risk of resulting in a material adjustment to the carrying amount of assets and liabilities within the next financial year are as follows:

• Sales allowances

• Allowance for doubtful accounts

• Reserve for inventory obsolescence

• Impairment of non-financial assets

For a more detailed discussion on these areas requiring the use of management judgements and estimates, readers should refer to note 3 to the Corporation’s 2013 audited annual consolidated financial statements.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 20

Accounting Policies and New Accounting Policies Not Yet Applied

Recently Adopted Accounting Standards The Corporation has adopted the following new and revised standards, along with any consequential amendments, effective January 1, 2013. These changes were made in accordance with the applicable transitional provisions. (i) The Corporation has adopted the amendments to IAS 1, Presentation of Financial Statements. These

amendments required the Corporation to group other comprehensive income items according to those that will be reclassified subsequently to profit or loss and those that will not be reclassified.

(ii) IFRS 10, Consolidated Financial Statements, replaces the guidance on control and consolidation in

IAS 27, Consolidated and Separate Financial Statements, and SIC-12, Consolidation – Special Purpose Entities. IFRS 10 requires consolidation of an investee only if the investor possesses power over the investee, has exposure to variable returns from its involvement with the investee and has the ability to use its power over the investee to affect its returns. The accounting requirements for consolidation have remained largely consistent with IAS 27 and the Corporation determined that the adoption of IFRS 10 did not result in any change in the consolidation status of any of its subsidiaries and investees.

(iii) IFRS 12, Disclosure of Interests in Other Entities, establishes disclosure requirements for interests in

other entities, such as subsidiaries, joint arrangements, associates, and unconsolidated structured entities. The standard carries forward existing disclosures and also introduces significant additional disclosure that address the nature of, and risks associated with, an entity’s interests in other entities. The Corporation has incorporated the new disclosure requirements within these financial statements.

(iv) IFRS 13, Fair value measurement, provides a single framework for measuring fair value. The

measurement of the fair value of an asset or liability is based on assumptions that market participants would use when pricing the asset or liability under current market conditions, including assumptions about risk. The Corporation adopted IFRS 13 on January 1, 2013 on a prospective basis. The adoption of IFRS 13 did not require any adjustments to the valuation techniques used by the Corporation to measure fair value and did not result in any measurement adjustments as at January 1, 2013.

(v) In May 2013, the IASB amended IAS 36, Impairment of assets regarding disclosures for non-financial assets. This amendment removed certain disclosures related to the recoverable amount of CGUs which had been included in IAS 36 by the issue of IFRS 13. The amendment is not mandatory until January 1, 2014; however, the Corporation has decided to early adopt the amendment as of January 1, 2013.

(vi) IFRS 7, Financial instruments – disclosure ("IFRS 7") – The amendments to IFRS 7 contain new

disclosure requirements for financial assets and liabilities that are either offset in the consolidated balance sheet or subject to master netting arrangements or other similar arrangements. The amendments are to be applied retrospectively. As a result of the amendments to IFRS 7, the Corporation has provided additional disclosures about offsetting of financial assets and financial liabilities.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 21

Accounting standards issued but not yet applied IFRS 9, Financial Instruments, as issued, reflects the current status of the IASB’s work plan on the replacement of IAS 39 and applies to classification and measurement of financial assets and financial liabilities, as defined in IAS 39. The IASB is also addressing hedge accounting and impairment of financial assets. In December 2013 the IASB removed the mandatory effective date of IFRS 9 until all phases of the project have been completed. The mandatory effective date has yet to be determined; however, it has been deferred beyond annual periods beginning on or after January 1, 2015. The Corporation has not yet quantified the effect of the published phases of the standard nor does it intend at this time to early adopt the standard until the mandatory effective date. IFRIC 21, Levies – IFRIC 21 provides guidance on accounting for levies in accordance with the requirements of IAS 37, Provisions, Contingent Liabilities and Contingent Assets. The interpretation defines a levy as an outflow from an entity imposed by a government in accordance with legislation and confirms that a liability for a levy is recognized only when the triggering event specified in the legislation occurs. The interpretation is effective for annual periods beginning on or after January 1, 2014; however, the Corporation has not yet assessed the impact of this interpretation.

Disclosure controls and procedures

Disclosure controls and procedures are designed to provide reasonable assurance that all relevant information is gathered and reported to senior management, including the Corporation’s President and Chief Executive Officer, on a timely basis so that appropriate decisions can be made regarding public disclosure. The Corporation’s system of disclosure controls and procedures includes, but is not limited to, the effective functioning of its Audit Committee and procedures in place to systematically identify matters warranting consideration of disclosure by the Audit Committee. As at the end of the period covered by this MD&A, management of the Corporation, with the participation of the President and Chief Executive Officer and the Vice-President and Chief Financial Officer, evaluated the effectiveness of the Corporation’s disclosure controls and procedures as required by applicable Canadian securities laws. The evaluation included documentation review, enquiries and other procedures considered by management to be appropriate in the circumstances. Based on that evaluation, the President and Chief Executive Officer and the Vice-President and Chief Financial Officer have concluded that, as of the end of the period covered by this MD&A, the disclosure controls and procedures were effective to provide reasonable assurance that information required to be disclosed in the Corporation’s annual filings and interim filings and other reports filed or submitted under applicable Canadian securities laws, is recorded, processed, summarized and reported within time periods specified by those laws and that material information is accumulated and communicated to management of the Corporation, including the President and Chief Executive Officer and the Vice-President and Chief Financial Officer, as appropriate to allow timely decisions regarding required disclosure. While management believes that the Corporation has designed adequate disclosure controls and procedures, there is no certainty that lapses in the disclosure controls and procedures will not occur. Upon discovery of lapses in the effectiveness of designed controls, the Corporation takes steps to implement changes and enforcement as deemed appropriate to reduce the risks of material errors or misstatements in its reporting.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 22

Internal Controls over Financial Reporting

Disclosure controls and procedures and internal controls over financial reporting In accordance with National Instrument 52-109 the Corporation’s President and Chief Executive Officer and the Vice-President and Chief Financial Officer certify that they have designed the Corporation’s internal controls over financial reporting, or caused them to be designed under their supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS as at December 31, 2013. An evaluation was carried out, under the supervision of the Corporation’s President and Chief Executive Officer and the Vice-President and Chief Financial Officer, of the design and effectiveness of its internal controls over financial reporting. Based on this evaluation the Corporation’s President and Chief Executive Officer and the Vice-President and Chief Financial Officer concluded that the internal controls over financial reporting (ICFR) are effective, using the criteria set forth by the Committee of Sponsoring Organizations of the Treadway Commission (COSO) on Internal Control – Integrated Framework. Changes in internal controls over financial reporting There have been no changes to the Corporation's internal controls over financial reporting during the twelve-month period ended December 31, 2013 that have materially affected, or are reasonably likely to materially affect, its internal controls over financial reporting.

Related Party Transactions

Certain of the Corporation’s directors, including certain executive officers who are directors, participated in the private placement of 10% secured debentures as part of the Corporation’s recapitalization transaction completed on March 30, 2010. These transactions with directors and officers were concluded on the same terms as the transactions with other investors. The total amount of debentures held by Board members and officers as at December 31, 2013 was CA$4.2 million.

Risks and Uncertainties

The Corporation is subject to a variety of risks and uncertainties that could materially affect its business, financial condition and results of operations. General economic conditions All components of the Corporation’s budgeting and forecasting, including its estimates of the demand for its products, are dependent upon the Corporation’s estimates of growth or contraction in the markets it serves. It is difficult to estimate the level of growth or contraction of the economy as a whole in the Corporation’s markets or the factors that may increase or reduce consumer confidence. Continuing weak economic conditions in the markets in which the Corporation operates, lower consumer spending, higher inflation or deflation, higher commodity prices (such as the price of oil), political conditions, unemployment, volatility in stock markets, labor strikes or other factors affecting economic conditions generally could negatively impact the Corporation’s sales or profitability in 2014 or beyond. The difficulty of accurately forecasting prevailing economic conditions and consumer demand as a reflection of these conditions renders estimates of the Corporation’s future sales and expenditures very difficult to make. Adverse changes may occur in the areas indicated above or in other variables and may negatively affect the Corporation’s sales. Adverse economic conditions may also increase the Corporation’s exposure to losses from bad debts, increase the cost of financing and decrease its availability, increase the risk of loss on investments, or increase costs associated with manufacturing and distributing products.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 23

Product and brand development To support revenue growth, the Corporation must continuously launch new products, update existing products, strengthen existing brands and develop new ones. The Corporation therefore invests significantly in product design and development. Should the popularity of existing products decline, should the Corporation fail to bring new products to market in a timely manner or should any new products developed by the Corporation fail to be approved by the appropriate regulatory authorities, where applicable, this could have a material adverse effect on the Corporation’s financial condition and results of operations. Consumer preferences and acceptance of new products The success of the Corporation depends, in large part, on the continued appeal of its existing products and on the acceptance by the marketplace of its new products. However, consumer preferences in the toy and stationery industries are continuously changing and are difficult to predict. Products typically have short life cycles, and, in recent years, there have been trends towards children outgrowing toys at younger ages, particularly in favor of interactive and high technology products, and an increased use of high technology in toys. There can be no assurance that: (i) any of the Corporation’s current product lines will continue to be popular for any significant period of time; (ii) any new product introduced by the Corporation will achieve an adequate degree of market acceptance; or (iii) any new product's life cycle will be sufficient to permit the Corporation to recover development, manufacturing, marketing and other costs. A decline in the popularity of the Corporation’s existing products or the failure of new products to achieve and sustain market acceptance and to produce acceptable margins could have a material adverse effect on the Corporation’s financial condition and results of operations. Risks relating to licensed products While the Corporation attempts to balance its licensed and non-licensed product offerings, and to make a judicious selection of brands and entertainment properties which it licenses from third-parties, there is a risk that guaranteed royalty payments and advances thereon which the Corporation is required to pay to licensors may not be recouped from the sale of licensed products. There is also a risk that key licenses may not be renewed or may be revoked. Additionally, the sale of licensed products relating to entertainment properties, particularly theatrical releases, often presents limited durations during which the Corporation’s customers will carry licensed product inventory, which consequently could reduce demand for such licensed products. Any of these issues could have a material adverse effect on the financial condition and results of operations of the Corporation. Seasonality The business of the Corporation is seasonal and therefore its annual operating results depend in large part on its sales during the third and fourth quarters. Retailers require the Corporation to ship products closer to the time they expect to sell the products to consumers creating shorter lead times for production and increased pressure to fill orders promptly. The logistics of supplying more products within shorter time periods increases the risk that the Corporation will fail to achieve compressed shipping schedules, which may reduce its sales and have a material adverse effect on its financial performance.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 24

Liquidity and interest rate risk The Corporation’s primary sources of liquidity are cash flows from operations and short-term borrowings under its asset-based credit facility. Cash flows from operations could be negatively impacted by decreased demand for the Corporation’s products, which could result from factors such as adverse economic conditions and changes in public and consumer preferences, the continued confidence of the Corporation’s principal customers in the Corporation and its product lines, or by increased costs associated with manufacturing and distribution of products. The Corporation’s primary capital needs are related to inventory financing, accounts receivable funding, debt servicing and capital expenditures for new product initiatives. As a result of the seasonal nature of the toy and stationery industries, working capital requirements are variable throughout the year. Working capital needs typically grow through the first three quarters as inventories are built-up for the peak sales periods for retailers, being the July-September quarter for the Stationery & Activities product lines and the October-December quarter for the Toys product lines. The Corporation’s cash flows from operating activities are typically at their highest levels of the year in the fourth quarter. Available borrowings under the Corporation’s asset-based credit facility are based on eligible accounts and inventory, and are thus subject to change over time. Certain accounts and inventory may not be deemed eligible and thus may be excluded from the borrowing base depending on a number of factors, including their age and quality. There can be no assurance that the full amount of the facility will be available. Furthermore, increases in interest rates could negatively affect the cost of financing the Corporation’s working capital requirements. International operations The Corporation’s sales and distribution facilities abroad, as well as foreign third-party distributors, independent sales representatives and contract manufacturers relied on by the Corporation in its operations, are subject to the risks normally associated with international operations, including: (i) costs associated with the repatriation of earnings; (ii) civil unrest and political and economic instability; (iii) significantly concentrated outbreaks of communicable diseases; (iv) greater difficulty protecting intellectual property rights; (v) complications in complying with foreign laws, fiscal regulations and changes in governmental policies; (vi) increased delivery lead time and potential for transportation delays and interruptions; (vii) the imposition of tariffs or trade sanctions; (viii) the loss of "most favored" trading status by China in the United States or the European Union; (ix) increases in the price of commodities, transportation or labor; and (x) changes in government-fixed currency exchange rates, particularly the Chinese yuan. There can be no assurance that these issues will not result in a material adverse effect on the financial condition and results of operations of the Corporation. Foreign currency fluctuations The Corporation is exposed to market risks attributable to fluctuations in foreign currency exchange rates, primarily changes in the value of the U.S. dollar versus other currencies such as the Canadian dollar, the Euro, the British pound, the Mexican peso and the Australian dollar. The Corporation’s policy is to stabilize earnings by limiting foreign currency exposure mainly through forward exchange contracts. The Corporation’s risk management approach is to have hedging mechanisms in place for a maximum period of 24 months. The Corporation’s hedging policy strictly prohibits unauthorized speculative foreign exchange transactions. The Corporation only enters into forward contract agreements with solid financial counterparties.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 25

Customer concentration For the year ended December 31, 2013, the Corporation’s three largest customers accounted for approximately 53% of sales. The Corporation does not have firm purchase commitments from any of its customers. Customers’ perceptions of the Corporation’s financial condition or prospects could affect the extent to which they continue to do business with the Corporation. If some of these customers were to cease doing business with the Corporation or to reduce the amount of their purchases, by virtue of experiencing financial difficulty or otherwise, it could have a material adverse effect on the Corporation’s sales, financial condition and results of operations. In addition, most large retail chains sell private-label toys, arts and crafts and office products designed and branded by the retailers themselves. Such private label items may be sold at prices lower than the Corporation’s comparable products, and may result in lower purchases of the Corporation’s products by such retailers. Additionally, in recent years, several large customers engaged in price cutting of toy products during the holiday season, and arts and crafts and stationery products during the back-to-school season, which, if these trends continue, could have a material adverse effect on the Corporation’s gross profit, profitability and consumer perception of the brand equity of its products. Customer and credit risk The majority of the Corporation’s revenue is derived from sales to major retail chains in North America and Europe. To minimize credit risk, the Corporation conducts ongoing credit reviews and maintains credit insurance on selected accounts. Should certain of these major retailers cease operations or experience liquidity problems, there could be a material adverse effect on the Corporation’s results of operations. In the long term, the Corporation believes that should certain retailers cease to exist, consumers will shop at competitors at which the Corporation’s products will generally also be sold. Prices of raw materials The Corporation’s principal raw material is plastic resin, which is subject to the volatility of crude oil prices. Approximately 50% of the Corporation’s toy sales are generated from products manufactured at its Montreal facility. Resin for these production needs is purchased directly and the Corporation does not hedge against adverse price fluctuations for such purchases. The balance of the Corporation’s sales is derived from products manufactured under contract by qualified third-party suppliers in Asia. Contracts with these suppliers include specific provisions with respect to resin prices which typically trigger a renegotiation by either party if resin prices fluctuate beyond certain parameters. Decreases in supplier production capacity and/or strong demand could exert upward pressure on prices. While in the past the Corporation has succeeded in passing on a portion of the increase in resin prices to its customers, there is no assurance it will be able to continue to do so in the future, particularly if there are substantial price increases or if such increases are sustained over an extended period of time. There is no assurance the Corporation will be successful in limiting price increases or benefiting from price decreases of the resin it purchases indirectly as part of its manufacturing contracts with third-party suppliers. Prices of other raw materials used by the Corporation are also subject to fluctuations. Unfavorable swings in commodity prices could have a material adverse effect on the financial condition and results of operations. Income taxes The Corporation’s current organizational structure has resulted in a comparatively low effective income tax rate. This structure and the resulting tax rate are supported by current domestic tax laws in which the Corporation operates and by the interpretation and application of these tax laws. The rate can also be affected by the application of income tax treaties between those various jurisdictions. Unanticipated changes to these interpretations and applications of current domestic tax laws, or to the tax rates and treaties, could impact the effective income tax rate of the Corporation going forward.

MANAGEMENT’S DISCUSSION AND ANALYSIS

MEGA Brands 2013 Report to Shareholders │ 26