managing risks in multiple online auctions: an options approach ram gopal steven thompson y. alex...

TRANSCRIPT

Managing Risks in Multiple Online Auctions:

An Options Approach

Ram GopalSteven Thompson

Y. Alex TungDepartment of Operations and Information Management

University of Connecticut

Andrew B. WhinstonDepartment of Management Science and Information Systems

University of Texas at Austin

Presentation Outline

• Introduction• Risks (buyer and seller)• Overview of Options

– In Financial Markets– In Auction Markets

• A framework for Auction Options• Heuristic and Illustration• Concluding Remarks

Introduction• Online Auctions are becoming

increasingly popular as a sales channel for new items.– eBay Stores opened to rave

review with 18,000 stores signing up.

– ebay.com/stores• Repeat Seller’s sponsor a

significant proportion of auctions (data from 8 week period Nov. 02 – Jan. 03)

• We are concerned with sellers that move a number of new, identical items through single unit auctions over a sustained period of time.

Item Total # of auctions Repeat Seller Percentage

Bose Radio 375 66.1%

Grand Theft Auto 2178 81.4%

Palm 515 304 82.2%

Palm Tungsten 383 76.5%

Philips MP3 player 250 93.2%

Play Station 2 1963 79.5%

Windows XP 691 76.8%

Seller Risks: We Sold It For What!?

• Primarily an issue of revenue uncertainty.

• Allocative Efficiency– Individual auctions are

efficient, but sets of auctions do not reliably allocate items to the top bidders

Item Number of auctions by most active seller

Number of top M bidders that did not win an item

Bose Radio 29 8

Grand Theft Auto 51 13

Palm 515 40 7

Palm Tungsten 26 3

Philips MP3 player 111 0

Play Station 2 136 65

Windows XP 161 67

Buyer Risks: Time, Money, and Loser’s Lament

• Wasted Time: “Time is money”

• Uncertainty of Acquisition: A firm time constraint exists

• Price Uncertainty: Will the time spent at auction result in a price that is “worth it”?

• Loser’s Lament: A “loser” places a bid that would have made her a winner at a different auction.

Item Number of items (M)

Total number of bidders # of bidders who left empty-handed who bid higher than:

0th percentile 50th percentile

75th percentile

Bose Radio 29 174 53 7 1

Grand Theft Auto 51 121 26 2 2

Palm 515 40 60 9 6 6

Palm Tungsten 26 29 3 3 3

Philips MP3 player 111 109 4 3 3

Play Station 2 136 1214 339 86 25

Windows XP 161 1053 272 62 32

Options: What Are They?• An option is a contract: The seller agrees to buy or

sell the underlying at an agreed upon price by or on a pre-determined date.

– Many types of options: Calls, Puts, American, European, Real

– Example: A covered call option on shares of GE common stock

• Options are risk management tools: The seller of an option assumes the risk.

– Risk is defined in terms of price fluctuations of the underlying asset.

– The magnitude of the risk largely determines the price of the option.

Options in Auction Markets: Some Issues

• How Options work in online auctions: Example-A call option on a Bose Radio

• Would anyone want to buy one?– Data on “Buy-it-now” usage suggests an interest in risk

management

• Can Sellers profit from issuing options?• How would they be priced?

– There are a number of option-pricing models (real and financial), most famous is the Black-Scholes model

– All share some common fundamentals.• No arbitrage

• Redundant Security

• Law of one price

“Traditional” Option PricingScenario: A sells a call option to B.

Current asset price = $30, Strike price = $35, A single time period

The price of the asset will either go up (to $50) or down (to $20).

Time 0 Time T

Current Price = $30

Strike Price = $35

Stock Price = $20

Stock Price = $50

Time 0 Time T

Current Price = $30

Strike Price = $35

Stock Price = $20

Stock Price = $50A’s net benefit is: -50+35+Poption = Poption-15

A’s net benefit is: Poption

Case 1: A sells an “uncovered” option to B

So long as Poption > $15, A can achieve risk-free profits

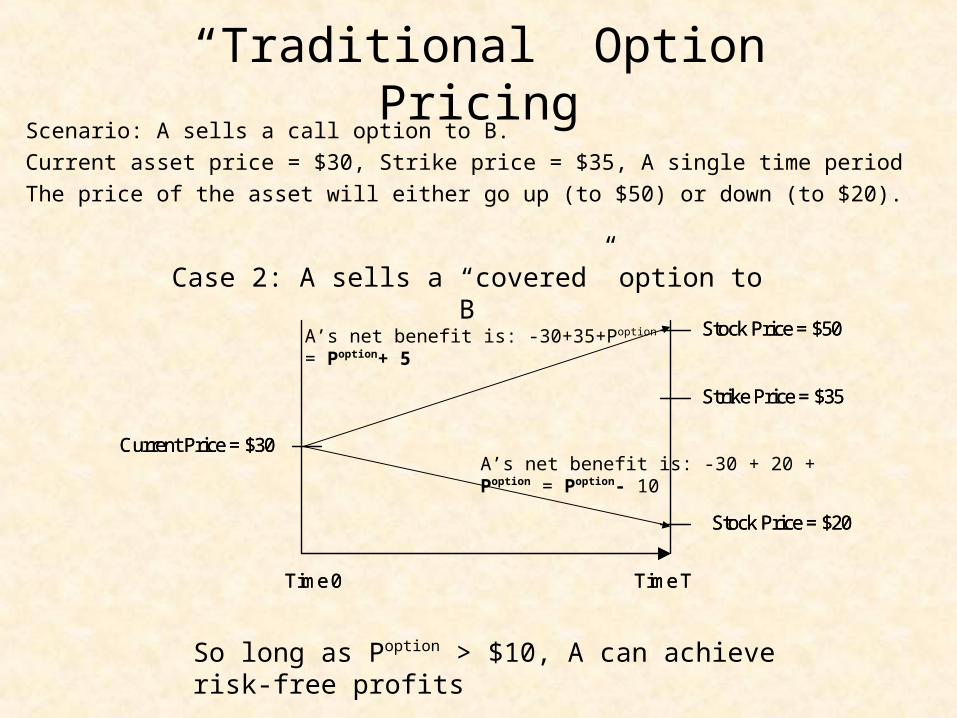

“Traditional” Option PricingScenario: A sells a call option to B.

Current asset price = $30, Strike price = $35, A single time period

The price of the asset will either go up (to $50) or down (to $20).

Time 0 Time T

Current Price = $30

Strike Price = $35

Stock Price = $20

Stock Price = $50

Time 0 Time T

Current Price = $30

Strike Price = $35

Stock Price = $20

Stock Price = $50A’s net benefit is: -30+35+Poption = Poption+ 5

A’s net benefit is: -30 + 20 + Poption = Poption- 10

Case 2: A sells a “covered” option to B

So long as Poption > $10, A can achieve risk-free profits

“Traditional” Option Pricing• In general, A could purchase x units of the underlying asset to cover the risk

associated with selling a single option.

x

Option Price

15

0.75 1

10

x

Option Price

15

0.75 1

10

Stock price is high: B will exercise the option.

A will have to buy the stock at $50 and then give this stock to B.

B will then give A $35 (the strike price) for it. A can sell his x units of stock at $50.

A’s net benefit is: -30x-50+35+Poption+50x = Poption+20x -15

Poption+20x -15

Make Money

Lose Money

“Traditional” Option Pricing• In general, A would purchase x units of the underlying asset to cover the risk

associated with selling a single option.

x

Option Price

15

0.75 1

10

x

Option Price

15

0.75 1

10

Stock price is low: In this case B will not exercise the option.

A will have to sell his stock at $20 and get his money back.

A’s net benefit is: -30x + 20x+ Poption = Poption-10x

Poption+20x -15Poption-10x

Feasible Region For Arbitrage

At this point there is no arbitrage but also no risk of losing money, regardless of what the price does! That is the price the market will give to the option.

For 1 time period this is a simple LP. Black-Scholes generalizes this to a generic asset price and across multiple time periods.

“Traditional” Option Pricing

• Solving the LP gives us the option price and the “hedge ratio”

• The decision variables are Poption and x.

0

0

010

01520

..

x

P

xP

xP

ts

PMin

option

option

option

option

In this case Poption and x are $5 and .5 respectively.

Pricing Options: Traditional vs. Auction Markets

• Fundamental assumptions of extant option-pricing models do not apply in auction markets.– Arbitrage is possible (Gopal, et al)

• Due largely to limited information processing• A seller could win some other auction for less than the current top

bid at his auction, make a quick risk-free buck

– Options impact price movements of underlying asset• Auction markets are comparatively illiquid• Behavioral differences between bidders and option holders impact

auction ending price.

– At any given moment multiple prices exist• Posted price, other auctions, etc.

– This creates a problem from the standpoint of pricing auction options.

An Alternative Framework

• Based simply on supply and demand

• Three fundamental components– Demand for Options

– Option holder behavior

– Impact of option holder behavior on auction outcomes

Standard notation:optionPstrikePissuedOsoldtOexercisedtO

),...,1( Mi

iN

= Option contract price

= Option strike price

= Number of options issued

= Number sold at time t

= Number exercised at time t

Index the M auctions

= Number of option holders participating in auction i

Demand for options

1 . D e m a n d is n o n -d e c re a s in g in n u m b e r o f b id d e rs .

2 . D e m a n d is n o n - in c re a s in g in optionP a n d strikeP

3 . D e m a n d is in v e rs e ly re la te d to th e le v e l o f r is k to le ra n c e o f b id d e rs ( r is k in te rm s o f u n c e r ta in ty o f a c q u is i t io n a n d o f p r ic e p a id )

4 . F o r a g iv e n v a lu e o f strikeoption PP , d e m a n d

is n o n - in c re a s in g in optionP .

Option Holder Behavior

• Could be anything– Active deal seeking

• Option holders participate in all auctions conducted during life of option

– Passive deal taking• Option holders buy the option and exercise it

immediately

– Semi-active deal seeking• Any extreme between active deal seeking and

passive deal taking

Impact of Option Holders on Auction Outcome

Unsold Options Proposition

0),( )(

dpONpg availableii

PP

ioptionstrike

when

available

iO )( > 0

Pstrike + Poption

Time

Auc

tion

e nd i

n g p

ric e

Impact of Option Holders on Auction OutcomeVariance Reduction Proposition

dp)O,Np(g(p) dp f available)i(i

P

i

P

i

strikestrike

11

00

Ni 2, 1

0

dp)O,Np(g(p) dp f available)i(i

Pi

Pi

strikestrike

22

Ni 2, 2

0

Impact of Option Holders on Auction OutcomeVariance Reduction Proposition

dp)O,Np(g(p) dp f available)i(i

P

i

P

i

strikestrike

11

00

Ni 2, 1

0

dp)O,Np(g(p) dp f available)i(i

Pi

Pi

strikestrike

22

Ni 2, 2

0

Impact of Option Holders on Auction OutcomeOption Holder Competition Proposition

dp)O,Np(g) dp O,N(pg available)i(i

P

i

Pavailable

)i(ii

strikestrike

1 11

00

dp)O,Np(g) dp O,N(pg available)i(i

Pi

P

available)i(ii

strikestrike

1

22

3iN

Impact of Option Holders on Auction OutcomeOption Holder Competition Proposition

dp)O,Np(g) dp O,N(pg available)i(i

P

i

Pavailable

)i(ii

strikestrike

1 11

00

dp)O,Np(g) dp O,N(pg available)i(i

Pi

P

available)i(ii

strikestrike

1

22

5iN

A Heuristic For The Initial Foray

• A learning algorithm• Uses bid-by-bid data from previous M auctions

– Determines option holders• Probability of purchase

• First-come, first served

– User selects an option holder behavior patters• Active deal seeking

• Passive deal taking

• A version of semi-active deal seeking

– Determines auction ending price

auctioniP̂ {1max

ib, 2max

ib+ , optionstrikePP, strikeP, 1max

ib, strikeP}

Assumed Option Holder Behavior Number of Auctions: 7 Passive Deal Taking Semi-Active Deal Seeking Active Deal Seeking

Passive Deal Taking

17.9% 13.5% 17.4% Semi-Active Deal Seeking

18.90% 19.37% 26.19%

Act

ual O

ptio

n H

olde

r B

ehav

ior

Active Deal Seeking

12.46% 13.50% 19.72%

Assumed Option Holder Behavior Number of Auctions: 5 Passive Deal Taking Semi-Active Deal Seeking Active Deal Seeking

Passive Deal Taking

40.26% 42.08% 48.1% Semi-Active Deal Seeking

41.36% 44.27% 41.36%

Act

ual O

ptio

n H

olde

r B

ehav

ior

Active Deal Seeking

21.2% 24% 35.56% Assumed Option Holder Behavior Number of Auctions: 6

Passive Deal Taking Semi-Active Deal Seeking Active Deal Seeking

Passive Deal Taking

35.1% 33.48% 41.8% Semi-Active Deal Seeking

35.4% 34.23% 42.17%

Act

ual O

ptio

n H

olde

r B

ehav

ior

Active Deal Seeking

15.44% 13.06% 25.72%

Example: The Impact of Options

Closing Remarks and Future Research

• A first step into an unexplored facet of e-business risk management

• Additional research– Option holder behavior– Impact of options on auction outcome– Formal option-pricing models

Questions

Item # of auctions

Auctions ending with ‘Buy it now’

Proportion ending with ‘Buy it now’

Bose Radio 375 125 .333 Grand Theft Auto

2178 461 .212

Palm 515 304 110 .362 Palm Tungsten 383 140 .365 Philips MP3 player

250 120 .48

Play Station 2 1963 437 .223 Windows XP 691 132 .191

Prevalence of ‘Buy-it-now’