managing sales tax data: streamlining internal...

TRANSCRIPT

Managing Sales Tax Data:

Streamlining Internal Controls

to Maximize Compliance Efficiency

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers.

Please refer to the instructions emailed to registrants for additional information. If you have any questions,

please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, FEBRUARY 20, 2014

Presenting a live 110-minute teleconference with interactive Q&A

Mike Dillon, President, Dillon Tax Consulting, Annapolis, Md.

Kenneth Stites, Principal, Stites Tax Consulting, Austin, Texas

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

Attendees must listen throughout the program, including the Q & A session, in

order to qualify for full continuing education credits. Strafford is required to

monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Managing Sales Tax Data: Streamlining Internal Controls to Maximize Compliance Efficiency

Michael T. Dillon, Dillon Tax Consulting

Feb. 20, 2014

Ken Stites, Stites Tax Consulting

Today’s Program

Sales Tax Data Requirements and Return Preparation

[Kenneth Stites]

Internal Controls and Audit Defense

[Michael T. Dillon]

Slide 8 – Slide 19

Slide 20 – Slide 37

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Sales Tax Data Requirements and Return Preparation

Kenneth Stites Principal at STITES TAX CONSULTING

(866) 705-6739

STITES TAX CONSULTING

www.stitestaxconsulting.com

Data Requirements for Sales and Use Tax Compliance

Sales Transactions and Exemption Documentation

Purchases of Fixed Assets

Purchases of Expense Items

STITES TAX CONSULTING

www.stitestaxconsulting.com 9

Sales Transactions

Required Data and Available Data

Summary data for sales with breakdowns by jurisdiction, taxable sales, exempt sales, tax invoiced

Transactions with unique tax calculations

Adjustments to sales amounts such as credit and debit memos

Journal entry detail for JE’s that affect recorded sales or recorded sales tax accrual

STITES TAX CONSULTING

www.stitestaxconsulting.com 10

Sales Transactions

Evaluating Systems that are in Place

Determine the systems that are collecting sales data, whether it be a module in the accounting software package or a separate billing software package or some combination of systems

Analyze system reports that are available and the potential for report customization

Consider data exports to spreadsheets to manage data in an efficient manner

Utilization of data stored by Sales Tax software package

STITES TAX CONSULTING

www.stitestaxconsulting.com 11

Sales Transactions

Access to and Maintenance of transaction detail

Copies of invoices retrievable by invoice number, customer name and date

Copies of credit memos that adjust sales amounts with reference to the original sales documents

Copies of contracts that provide definition of products or services

Journal entry back up for write offs that are processed

Exemption certificates

STITES TAX CONSULTING

www.stitestaxconsulting.com 12

Fixed Asset Purchases

Analyze or establish process to accrue and remit taxes on assets when necessary

Determine the dollar cutoffs with respect to items to be reviewed on an actual basis

Establish the process to be implemented to review fixed asset transactions for proper tax calculation

Develop a methodology to capture the tax due, accrue the tax on the books and report it on the sales and use tax return

Establish procedures for retaining detail for audit support

STITES TAX CONSULTING

www.stitestaxconsulting.com 13

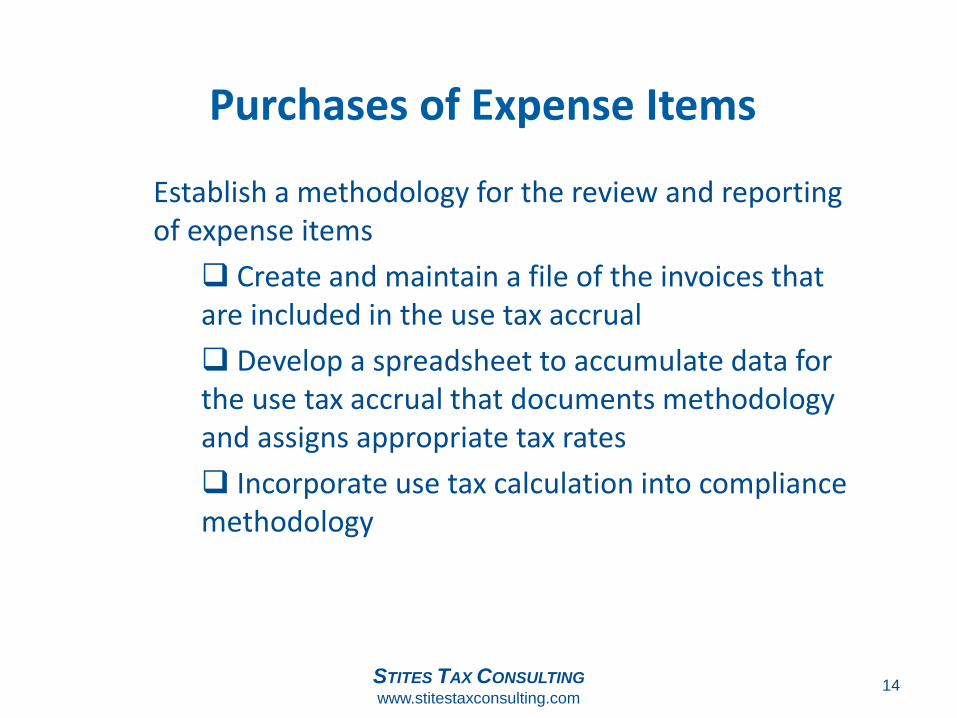

Purchases of Expense Items

Establish a methodology for the review and reporting of expense items

Create and maintain a file of the invoices that are included in the use tax accrual

Develop a spreadsheet to accumulate data for the use tax accrual that documents methodology and assigns appropriate tax rates

Incorporate use tax calculation into compliance methodology

STITES TAX CONSULTING

www.stitestaxconsulting.com 14

Tax Return Preparation

Utilize summary data via system reports and prepared spreadsheets to prepare returns for filing.

Back end sales tax software can be used to generate returns, possibly facilitating direct uploads to the tax authorities.

Retain spreadsheets used to capture data from outside of the billing system, which is included on the tax returns.

STITES TAX CONSULTING

www.stitestaxconsulting.com 15

Tax Return Preparation

Create file for filed tax returns including copies of reports, spreadsheets, use tax back up, payment processing and mailing certification whether it is through the USPS or electronic.

Reconcile sales tax accrual account or accounts to the returns filed, adjustments and amounts that need to remain in the accrual.

STITES TAX CONSULTING

www.stitestaxconsulting.com 16

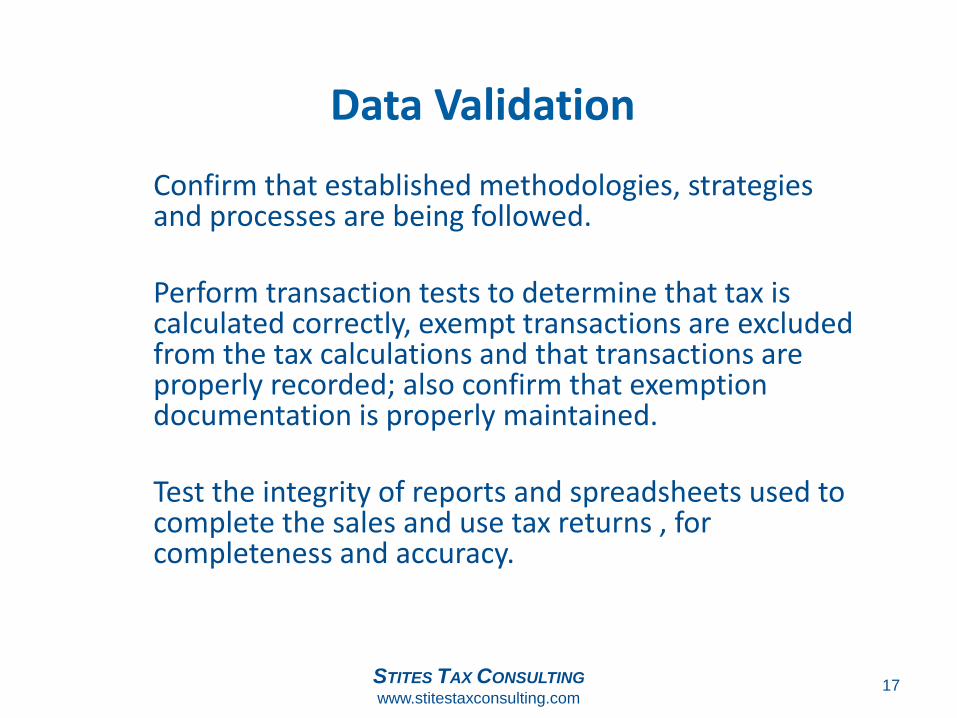

Data Validation

Confirm that established methodologies, strategies and processes are being followed. Perform transaction tests to determine that tax is calculated correctly, exempt transactions are excluded from the tax calculations and that transactions are properly recorded; also confirm that exemption documentation is properly maintained. Test the integrity of reports and spreadsheets used to complete the sales and use tax returns , for completeness and accuracy.

STITES TAX CONSULTING

www.stitestaxconsulting.com 17

Slide Intentionally Left Blank

INTERNAL CONTROLS AND AUDIT DEFENSE

Michael T. Dillon, Dillon Tax Consulting

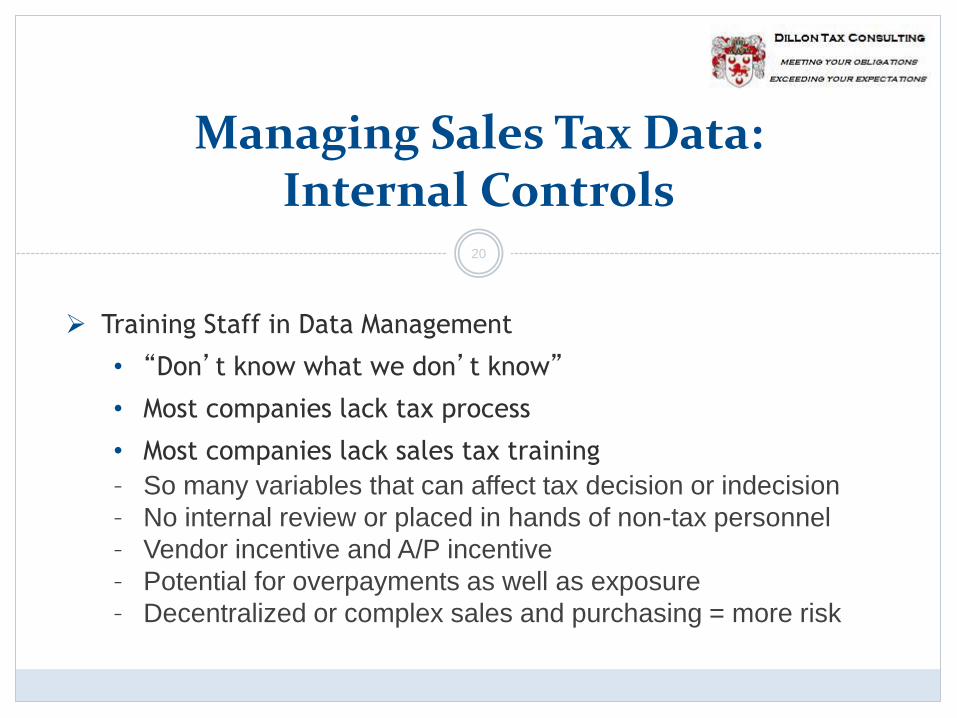

Managing Sales Tax Data: Internal Controls

Training Staff in Data Management

• “Don’t know what we don’t know”

• Most companies lack tax process

• Most companies lack sales tax training

– So many variables that can affect tax decision or indecision

– No internal review or placed in hands of non-tax personnel

– Vendor incentive and A/P incentive

– Potential for overpayments as well as exposure

– Decentralized or complex sales and purchasing = more risk

20

Managing Sales Tax Data: Internal Controls

TRAINING STAFF IN DATA MANAGEMENT

• Understand the data they manage

• Communicate well with IT and IT systems

• Know how to get the data

• Know how to safeguard and validate the data

21

Managing Sales Tax Data: Internal Controls

Training Staff in Data Management

• Understand the data they manage

- Who, what, when, where, how

- Electronic processes – more detail is ideal

- Coding sales and purchase transactions to correct

jurisdiction, account, product and tax codes

- Tax matrix

- Rating

22

Managing Sales Tax Data: Internal Controls

Training Staff in Data Management

• Understand the data they manage

- Ensuring transaction details match contract and

invoice literals

- Coding sales and use tax to proper accounts

- Prepare back-up documents to support returns – audit

trails

- Reconciling tax accounts to ensure what was collected

and accrued was remitted

23

Managing Sales Tax Data: Internal Controls

TRAINING STAFF IN DATA MANAGEMENT

• Communicate well with IT and IT systems

- IT and data are critical to tax success

- What information exists, in what format

- What information tax needs to prepare returns and

maintain an audit trail

- Establish points of command for communication

between tax and IT

- Future IT needs of tax

24

Slide Intentionally Left Blank

Managing Sales Tax Data: Internal Controls

TRAINING STAFF IN DATA MANAGEMENT

• Know how to get the data

- Who, what, when, where, how fields

- Which systems have tax calculation data

- Which systems provide tax decision data

- Send data to CRM, OE or invoicing

- Query reports required to prepare returns

- Query reports required for audits

- Manual review of complex transactions

26

Managing Sales Tax Data: Internal Controls

TRAINING STAFF IN DATA MANAGEMENT

• Safeguarding and Validating the data

- Correct CRM / OE set-up

- Obtaining exemption and resale certificates

- Maintain tax matrix and audit issue resolution

- Detailed Reporting for audit purposes

- Departmental accountability for audit liabilities

- Manual review / intervention in processes

27

SALES AND USE TAX COMPL IANCE SOFTWARE

• Automated tax dec i s ion, rat ing and return

preparat ion

• Keep account ing personnel focused on h igher -

va lue work

• Data arch ived for aud i t purposes

28

Managing Sales Tax Data: Internal Controls

SALES AND USE TAX COMPL IANCE SOFTWARE: REQS

• Must cons ider and ensure seamless integrat ion

wi th account ing/b i l l ing p lat forms

• Even wi th automat ion, there i s human

i nvo lvement, which a lways leads to the

potent ia l fo r er ror.

– Minimize humans interaction but create reviews by tax for

select accounts, problem vendors, big purchases over

materiality threshhold

29

Managing Sales Tax Data: Internal Controls

SALES AND USE TAX COMPL IANCE SOFTWARE: REQS

• Systems must address who, what, when, where, hows

- More detailed descriptions reduce audit exposure

• Statutory exemptions must be addressed

• Exemption Certificate Management platforms

• Some purchases are exempt based on interstate commerce,

and consideration must be given to multiple jurisdictions and

when title is transferred.

30

Managing Sales Tax Data: Internal Controls

SALES AND USE TAX COMPL IANCE SOFTWARE: WHAT

SYSTEMS ARE AVA ILABLE

• Avalara

• Vertex

• Taxware

• BillSoft EZTax

• TaxAutomation and leading integrators can assist

31

Managing Sales Tax Data: Internal Controls

Obtaining “Buy-In” from the C-level suite

• Audit results are key driver

• Compliance Process Review

- Sales tax expert audits multistate nexus and compliance and

provides a gap and exposure analysis

- Report provides a “road map” for resolving historical exposure

and enhancing prospective compliance processes

• Cost comparison - manual versus automated compliance

• Cost of integration

32

Managing Sales Tax Data: Internal Controls

Slide Intentionally Left Blank

Pre-audit process

• Audit Risk = risk of inaccurate records + risk of misapplication

of the tax laws

• Review the audit information request to ensure:

- who, what, when, where, how – more detailed = better

– The information requested is relevant and available, and

available in the format requested

– If not, be prepared to discuss with auditor before initial

audit meeting and present alternatives

34

Managing Sales Tax Data: Audit Defense

PRE-AUDIT PROCESS

• Review the audit information request to ensure:

– Data fields not requested that will assist the audit process

(e.g., project codes; electronic delivery field)

• Audit Thyself - Review the items to be audited

- System walk-through

- Missing Certificates and Invoices

- Do transaction detail, register and returns reconcile

- Identify issues and prepare responses

35

Managing Sales Tax Data: Audit Defense

Audit process

• How are invoices and certs maintained – electronic v. manual

- Computer-assisted detail v. sampling – success depends on

quality of data and detailed descriptions

• Are there documents not requested that will assist the audit

process

- contracts and exhibits / addenda / SOWs

- accounting behind bundled or mixed transactions

• Consider system walk-through with auditor

36

Managing Sales Tax Data: Audit Defense