managing volatility risk in mining investment decisions

TRANSCRIPT

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 1/9Contents page |

Managing Volatility

Managing VolatilityRisk in mininginvestment decisions

Next pagePrevious page |

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 2/91 Contents page |

Contents

Managing volatility risk in mining investment decisions• Introduction 2• Can your business case effectively respond to

the speed of change 2- Exhibit 1 3

• Building a dynamic business case - three steps 4- Exhibit 2 4- Exhibit 3 5

- Exhibit 4 6• Risks have to and can be managed 7• Contacts 7

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 3/92 Contents page |

Managing volatility risk inmining investment decisions

After reaching record highs in the rst half of 2008,commodity and metal prices, collapsed spectacularlyin the wake of the global nancial crisis, losing nearly50% by mid-2009. However, the effects of the hugestimulus packages co-ordinated by the developedworld governments, and the growth needs of thedeveloping nations led by China and India, broughtthe demand for commodities and pro tability back to

the mining sector. The industry has since recoveredmany of its earlier losses and, in certain cases,achieved impressive gains. But how long will thisbuoyancy last and does it have to end in yet anotherbust cycle?

In this context, it is not surprising that a currentanalysis of the main trends and business risks facingthe mining and metals industry (“Tracking the trends2010”, A look at the 10 of the top issues miningcompanies will face, Deloitte Energy & Resources,2009) indicates that capital allocation emerges as thenumber one strategic risk for the industry in 2010

and, conceivably, well beyond. The decision on howto allocate capital in mining has always been complex,but the unpredictability of the markets and theunprecedented level of volatility they have displayedrecently makes mining investment decision-makingeven more dif cult and increasingly multifaceted.Analysts and industry insiders agree that the next10 years’ business cycle won’t be normal and theenvironment will be volatile within the uplifteddemand circumstance.

How can this volatility risk be managed in mininginvestment decisions? Since volatility appears to behere to stay, companies need to factor it into theirbusiness practices and create new ways to work withit. Deloitte’s dynamic approach to capital ef ciency canprovide some answers.

Can your business case effectively respond tothe speed of change?Capital project planning usually extends over aconsiderable span of time and it is largely aboutbuilding value over the long term. Thus large capitalprojects have to navigate market cycles well beyondthe annual budgeting cycle. But the robustness ofmany capital business cases is weak in terms of their

ability to respond to changing business risks.Many business cases are dated, which re ects alengthy approval process, due to a project being takenthrough various authorisation gates. Average businesscases are also quite static, encapsulated in a few NPVnumbers corresponding to a set of typical scenarios:high, low and base case. A straight line sensitivityanalysis offers no insight (or very limited insight) intothe likelihood of each scenario. Risk assessment oftenamounts to a robot-like categorisation: the impact ofkey risk factors is not quanti ed and there’s a limitedinsight for how to manage for maximum value or howto mitigate risks.

Bringing a business case up to date can be achievedthrough a review of the underlying assumptions, itsconstruction logic and methodology, and the currentrevision of the nancial and economic parameters,through a rigorous deterministic process. However,making it dynamic requires a fresh, probabilistic,approach to accounting for risks (exhibit 1) .

Since volatility appears to be hereto stay, companies need to factorit into their business practices andcreate new ways to work with it.

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 4/93 Contents page |

Exhibit 1The Deloitte approach to capital ef ciency – to turn a dated and static capital project business case into a dynamic one. The probabilisticleg helps manage volatility risk actively and quantitatively.

NPV does not tell the whole story, and robust riskanalysis provides more valuable insight about howto quantify and manage the downside of majorprojects. Executives and project managers do notneed to become nancial risk mathematicians butthey do need to shift their thinking from discrete and

nite numbers into thinking in terms of uncertainties,likelihoods and expected returns. Uncertainties are

associated with every aspect of the economy, businessand nance. The political environment for doingbusiness, commodity prices and exchange rates are afew examples of global factors that are characterisedby uncertainties, particularly in the present volatilecircumstances.

There are equally important project-level factorsassociated with large uncertainties, like technicalsuccess of a novel mining method or understandinggeology of new resource. But how can the project’sdownside risks and upside opportunities be quanti ed,exploited or mitigated?

44

Originalbus ine ss

case

Riskframing

Riskmodelling

Riskprofiling

Riskmitigation

Revision

Re-builtdynam icbus ine ss

case

Sourcesof newvalue

Key

Deterministic leg

Probabilistic leg

Feedback loop

What are the key risks, their interactions and interdependencies?

Which risks impact value the most?

What is the project’s risk profile andhow to mitigate it for maximum value?

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 5/94 Contents page |

Building a dynamicbusiness case - three steps

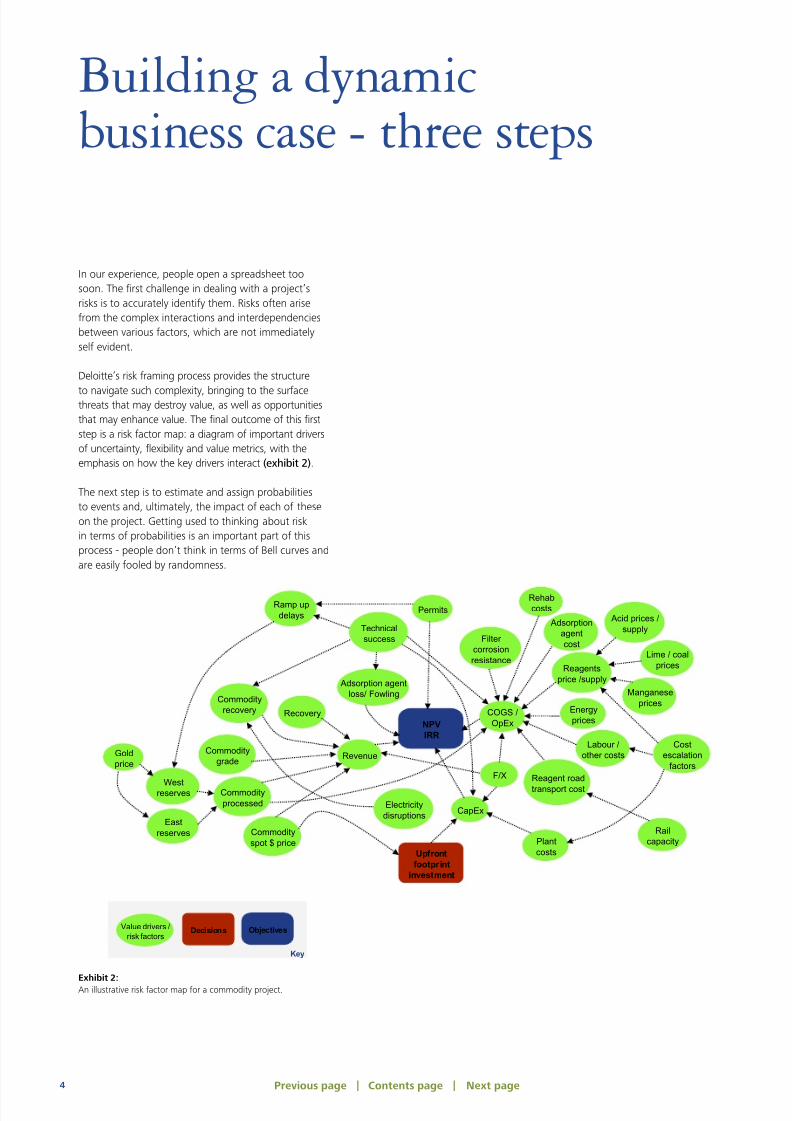

In our experience, people open a spreadsheet toosoon. The rst challenge in dealing with a project’srisks is to accurately identify them. Risks often arisefrom the complex interactions and interdependenciesbetween various factors, which are not immediatelyself evident.

Deloitte’s risk framing process provides the structure

to navigate such complexity, bringing to the surfacethreats that may destroy value, as well as opportunitiesthat may enhance value. The nal outcome of this rststep is a risk factor map: a diagram of important driversof uncertainty, exibility and value metrics, with theemphasis on how the key drivers interact (exhibit 2) .

The next step is to estimate and assign probabilitiesto events and, ultimately, the impact of each of theseon the project. Getting used to thinking about riskin terms of probabilities is an important part of thisprocess - people don’t think in terms of Bell curves andare easily fooled by randomness.

Exhibit 2:An illustrative risk factor map for a commodity project.

NPVIRR

Revenue

COGS /OpEx

CapEx

Permits

Technicalsuccess Filter

corrosionresistance

Railcapacity

Acid prices /supply

Manganeseprices

Reagent roadtransport cost

F/X

Costescalation

factors

Adsorption agentloss/ FowlingCommodity

recovery

Commoditygrade

Commodityprocessed

Commodityspot $ price

Recovery Energyprices

Plantcosts

Lime / coalprices

Electricitydisruptions

Reagentsprice /supply

Adsorptionagentcost

Ramp updelays

Westreserves

Eastreserves

Goldprice

Labour /other costs

Rehabcosts

Upf rontfootpri nt

invest ment

Value drivers /risk factors

Deci si on s Objec tive s

Key

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 6/95 Contents page |

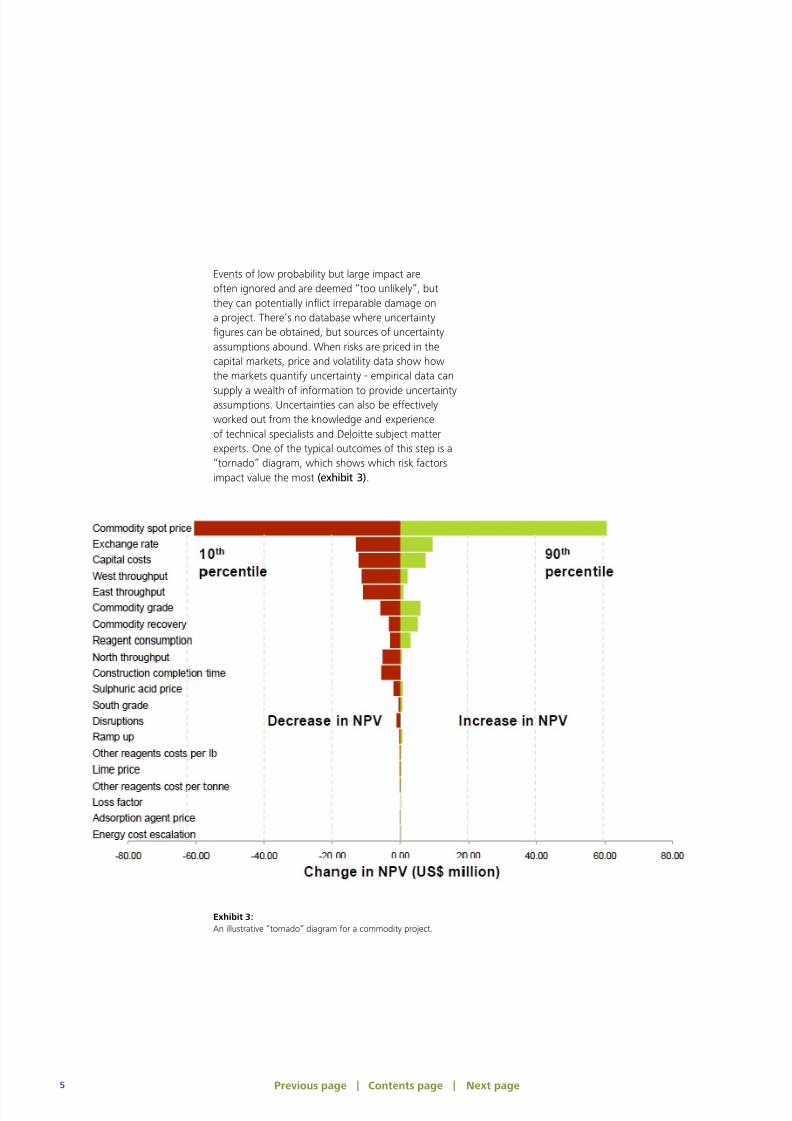

Events of low probability but large impact areoften ignored and are deemed “too unlikely”, butthey can potentially in ict irreparable damage ona project. There’s no database where uncertainty

gures can be obtained, but sources of uncertaintyassumptions abound. When risks are priced in thecapital markets, price and volatility data show howthe markets quantify uncertainty - empirical data can

supply a wealth of information to provide uncertaintyassumptions. Uncertainties can also be effectivelyworked out from the knowledge and experienceof technical specialists and Deloitte subject matterexperts. One of the typical outcomes of this step is a“tornado” diagram, which shows which risk factorsimpact value the most (exhibit 3) .

Exhibit 3:An illustrative “tornado” diagram for a commodity project.

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 7/96 Contents page |

Finally, rather than constructing project high- andlow-road scenarios, expected value curves or riskpro les are generated which represent all possiblescenarios. All identi ed risk factors and theiruncertainty ranges are used to construct the curves(exhibit 4). This is accomplished by using the DecisionProgramming Language (DPL) software, which applieseither decision tree analysis or Monte Carlo simulation,

depending on speci c considerations for eachparticular project or problem.

A risk pro le, such as the one illustrated by aStrategy-1 curve in exhibit 6, can be interpreted interms of likelihood as follows: for (100-X)% of allpossible scenarios, the NPV value for the project is noless than Y-dollars. This is a much more powerful andquantitatively precise statement than saying: if a lowroad scenario materialises, then the NPV of the projectwill be Y, where the likelihood of the scenario is notquanti ed. Moreover, expressing project outcomes interms of the risk pro le enables one to modify thatpro le in such a way as to maximise the outcome:enter quantitative risk management.

Exhibit 4:Illustrative risk pro les for different project strategies.

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 8/97 Contents page |

Risk analysis informs one’s strategy and a dynamicroad map can capture the impact of uncertaintiesfaced by the project, what milestones and thresholdsneed to be monitored and what mitigating actionsare available at each point. One would ideally liketo make the risk pro le steeper (less NPV variationin a larger range of probability) and move it towardshigher NPV values, as illustrated by Strategy-2 curve in

exhibit 6. Managing a project with strategic exibilityentails contingency planning for future decisions. Onemay decide to hedge a certain portion of the foreigncurrency exposure in order to ensure nancial certaintyat the critical point of the capital schedule, or to sellforward some of the future output in the event thatthe commodity price is expected to turn against theproject at some point. Either way, one’s modi ed riskpro le will provide a quantitative assessment of theresulting value, at an instant, without the necessity of alaborious re-construction of discrete scenarios togetherwith the project’s responses to each.

Deloitte’s dynamic approach to capital ef ciencyenables active and quantitative risk mitigation andmanaging the project to maximum value by helpingto discover hidden value, improve business practicesand identify innovative strategies. It blunts the edge ofvolatility on investment decisions.

ContactsJacek GuzekExecutive LeadTel: +27 (82) 940 6896Email: [email protected]

Louis Kruger

Associate DirectorTel: +27 (83) 388 7261Email: [email protected]

Risks have to andcan be managed

Previous page | Next page

8/8/2019 Managing Volatility Risk in Mining Investment Decisions

http://slidepdf.com/reader/full/managing-volatility-risk-in-mining-investment-decisions 9/9

1. Determine, on each engagement, who our clientsare and directly ascertain their expectationsfor our performance. Clients may include theboard of directors, the audit committee, and

management, all of whom are representatives ofshareholder interests.

2. Analyse our clients’ needs and professional servicerequirements.

3. Develop client service objectives that will enableus to ful l our professional responsibilities, satisfyour clients’ needs, and aim to exceed theirexpectations. Prepare an appropriate client serviceplan to achieve these client service objectives.

4. Execute the client service plan in a manner thathas earned us our reputation for quality andendeavours to ensure that commitments are met,potential problems are anticipated, and surprisesare avoided.

5. Establish effective communications, both internaland external, to enhance our clients’ recognitionof the value and quality of our service.

6. Provide our clients with insights on the conditionof their businesses and with meaningfulsuggestions for their improvement.

7. Continually broaden and strengthen ourrelationships with our clients to facilitate effectivecommunication and enhance client con dence,while maintaining professional objectivity.

8. Ensure that any professional, technical, or clientservice problem is resolved promptly with timelyconsultation in an environment of mutual respect.

9. Obtain from our clients, either formallyor informally, a regular assessment of ourperformance.

10. Receive fees that re ect the value of servicesprovided and responsibilities assumed, and thatare considered fair and reasonable.

Client Service Standards

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited byguarantee, and its network of member rms, each of which is a legally separate and independent entity.Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte ToucheTohmatsu Limited and its member rms.

“Deloitte” is the brand under which tens of thousands of dedicated professionals in independent rmsthroughout the world collaborate to provide audit, consulting, nancial advisory, risk management, andtax services to selected clients. These rms are members of Deloitte Touche Tohmatsu Limited (DTTL), a UKprivate company limited by guarantee. Each member rm provides services in a particular geographic areaand is subject to the laws and professional regulations of the particular country or countries in which itoperates. DTTL does not itself provide services to clients. DTTL and each DTTL member rm are separate anddistinct legal entities, which cannot obligate each other. DTTL and each DTTL member rm are liable only

for their own acts or omissions and not those of each other. Each DTTL member rm is structured differentlyin accordance with national laws, regulations, customary practice, and other factors, and may secure theprovision of professional services in its territory through subsidiaries, af liates, and/or other entities.

© 2010 Deloitte & Touche. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

Designed and produced by the Studio at Deloitte, Johannesburg. (801403/ryd)