managing your personal taxes 2016-17 - appendix a to contents appendix a - personal income tax rates...

TRANSCRIPT

Managing Your Personal Taxes 2017-18 | 120Back to contents

Appendix A - Personal income tax rates in Canada

Alberta

Combined federal and provincial personal income tax rates - 20171

Combined personal income tax rates

Taxable income AlbertaMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 18,690 – 15.00% 0.00% 5.24% 7.50%18,691 to 45,916 1,058 25.00% 0.00% 14.38% 12.50%45,917 to 91,831 7,865 30.50% 7.56% 20.82% 15.25%91,832 to 126,625 21,869 36.00% 15.15% 27.25% 18.00%

126,626 to 142,353 34,395 38.00% 17.91% 29.59% 19.00%142,354 to 151,950 40,371 41.00% 22.05% 33.10% 20.50%151,951 to 202,600 44,306 42.00% 23.43% 34.27% 21.00%202,601 to 202,800 65,579 43.00% 24.81% 35.44% 21.50%202,801 to 303,900 65,665 47.00% 30.33% 40.12% 23.50%303,901 and up 113,182 48.00% 31.71% 41.29% 24.00%

1.The tax rates reflect budget proposals and news releases to 30 June 2017.Where the tax is determined under the alternative minimum tax provisions(AMT), the table is not applicable. AMT may be applicable where the taxotherwise payable is less than the tax determined by applying the relevant AMTrate to the individual’s taxable income adjusted for certain preference items.

2.The tax determined by the table should be reduced by the applicable federaland provincial tax credits, other than the basic personal tax credits, which havebeen reflected in the calculations.

3.The rates apply to the actual amount of taxable dividends received fromtaxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by the payorcorporation as an eligible dividend). Where the dividend tax credit exceedsthe federal and provincial tax otherwise payable on the dividends, the rates donot reflect the value of the excess credit that may be used to offset taxespayable from other sources of income. This assumption is consistent with prioryear rates.

4.The rates apply to the actual amount of the capital gain. The capital gainsexemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specific properties.

Managing Your Personal Taxes 2017-18 | 121Back to contents

Appendix A - Personal income tax rates in Canada

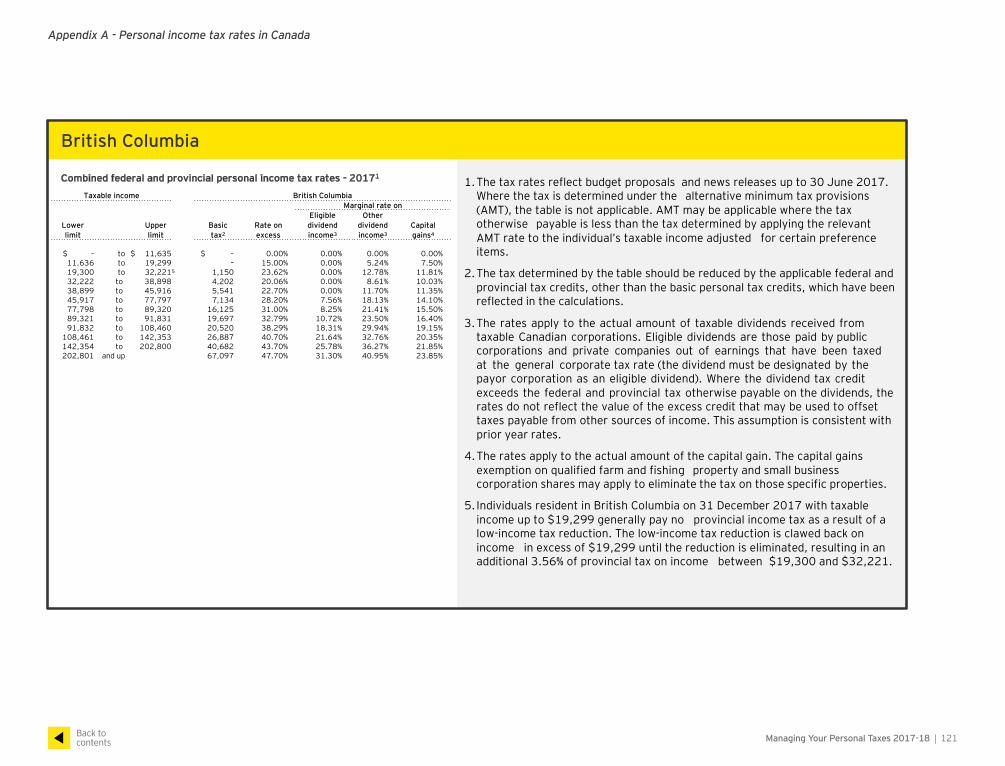

British Columbia

Combined federal and provincial personal income tax rates - 20171

Combined personal income tax rates

Taxable income British ColumbiaMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 19,299 – 15.00% 0.00% 5.24% 7.50%19,300 to 32,221 5 1,150 23.62% 0.00% 12.78% 11.81%32,222 to 38,898 4,202 20.06% 0.00% 8.61% 10.03%38,899 to 45,916 5,541 22.70% 0.00% 11.70% 11.35%45,917 to 77,797 7,134 28.20% 7.56% 18.13% 14.10%77,798 to 89,320 16,125 31.00% 8.25% 21.41% 15.50%89,321 to 91,831 19,697 32.79% 10.72% 23.50% 16.40%91,832 to 108,460 20,520 38.29% 18.31% 29.94% 19.15%

108,461 to 142,353 26,887 40.70% 21.64% 32.76% 20.35%142,354 to 202,800 40,682 43.70% 25.78% 36.27% 21.85%202,801 and up 67,097 47.70% 31.30% 40.95% 23.85%

1.The tax rates reflect budget proposals and news releases up to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the tax otherwise payable is less than the tax determined by applying the relevantAMT rate to the individual’s taxable income adjusted for certain preference items.

2.The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, which have beenreflected in the calculations.

3.The rates apply to the actual amount of taxable dividends received fromtaxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by thepayor corporation as an eligible dividend). Where the dividend tax creditexceeds the federal and provincial tax otherwise payable on the dividends, therates do not reflect the value of the excess credit that may be used to offsettaxes payable from other sources of income. This assumption is consistent withprior year rates.

4.The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small businesscorporation shares may apply to eliminate the tax on those specific properties.

5. Individuals resident in British Columbia on 31 December 2017 with taxable income up to $19,299 generally pay no provincial income tax as a result of a low-income tax reduction. The low-income tax reduction is clawed back on income in excess of $19,299 until the reduction is eliminated, resulting in an additional 3.56% of provincial tax on income between $19,300 and $32,221.

Managing Your Personal Taxes 2017-18 | 122Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

Manitoba

Combined federal and provincial personal income tax rates - 20171

Taxable income ManitobaMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $9,271 $ – 0.0% 0.00% 0.00% 0.00%9,272 to 11,635 – 10.80% 3.86% 11.72% 5.40%

11,636 to 31,465 255 25.80% 3.86% 16.96% 12.90%31,466 to 45,916 5,371 27.75% 6.56% 19.24% 13.88%45,917 to 68,005 9,382 33.25% 14.12% 25.68% 16.63%68,006 to 91,831 16,726 37.90% 20.53% 31.12% 18.95%91,832 to 142,353 25,756 43.40% 28.12% 37.55% 21.70%

142,354 to 202,800 47,683 46.40% 32.26% 41.06% 23.20%202,801 and up 75,730 50.40% 37.78% 45.74% 25.20%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the tax otherwise payable is less than the tax determined by applying the relevant AMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, whichhave been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received from taxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by the payor corporation as an eligible dividend). Where the dividend tax credit exceeds the federal and provincial tax otherwise payable on the dividends, the rates do not reflect the value of the excess credit that may be used tooffset taxes payable from other sources of income. This assumption is consistent with prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small businesscorporation shares may apply to eliminate the tax on those specificproperties.

Managing Your Personal Taxes 2017-18 | 123Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

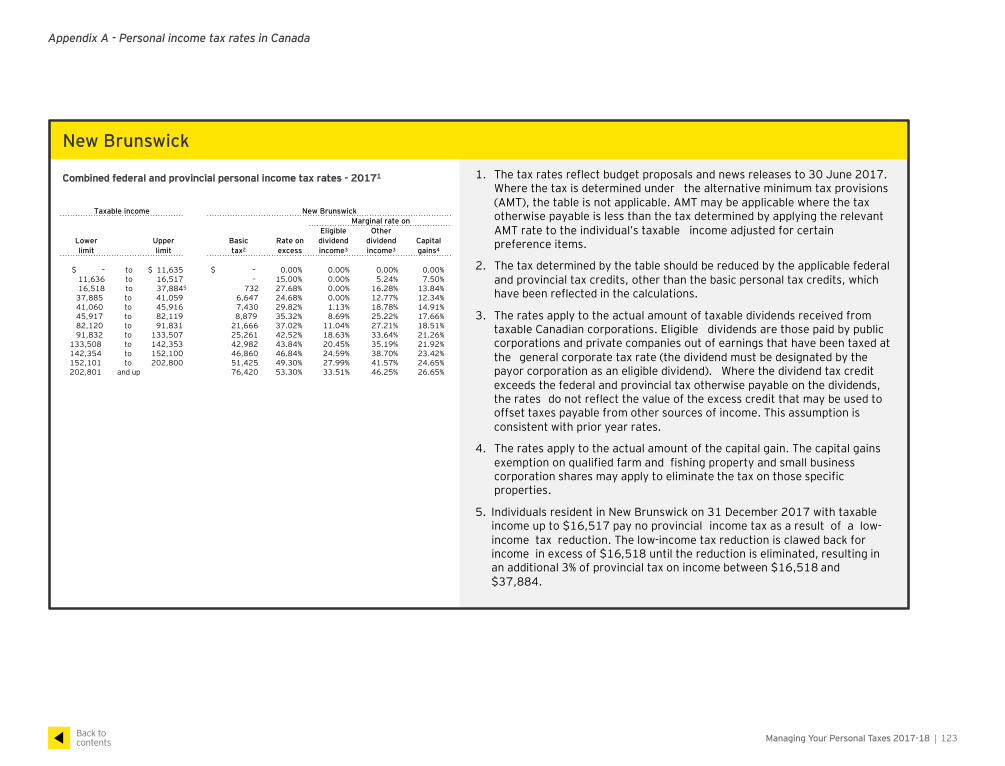

New Brunswick

Combined federal and provincial personal income tax rates - 20171

Taxable income New BrunswickMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 16,517 – 15.00% 0.00% 5.24% 7.50%16,518 to 37,8845 732 27.68% 0.00% 16.28% 13.84%

37,885 to 41,059 6,647 24.68% 0.00% 12.77% 12.34%41,060 to 45,916 7,430 29.82% 1.13% 18.78% 14.91%45,917 to 82,119 8,879 35.32% 8.69% 25.22% 17.66%82,120 to 91,831 21,666 37.02% 11.04% 27.21% 18.51%91,832 to 133,507 25,261 42.52% 18.63% 33.64% 21.26%

133,508 to 142,353 42,982 43.84% 20.45% 35.19% 21.92%142,354 to 152,100 46,860 46.84% 24.59% 38.70% 23.42%152,101 to 202,800 51,425 49.30% 27.99% 41.57% 24.65%202,801 and up 76,420 53.30% 33.51% 46.25% 26.65%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the tax otherwise payable is less than the tax determined by applying the relevant AMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, whichhave been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received from taxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by the payor corporation as an eligible dividend). Where the dividend tax credit exceeds the federal and provincial tax otherwise payable on the dividends, the rates do not reflect the value of the excess credit that may be used tooffset taxes payable from other sources of income. This assumption isconsistent with prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small businesscorporation shares may apply to eliminate the tax on those specificproperties.

5. Individuals resident in New Brunswick on 31 December 2017 with taxable income up to $16,517 pay no provincial income tax as a result of a low-income tax reduction. The low-income tax reduction is clawed back for income in excess of $16,518 until the reduction is eliminated, resulting inan additional 3% of provincial tax on income between $16,518 and$37,884.

Managing Your Personal Taxes 2017-18 | 124Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

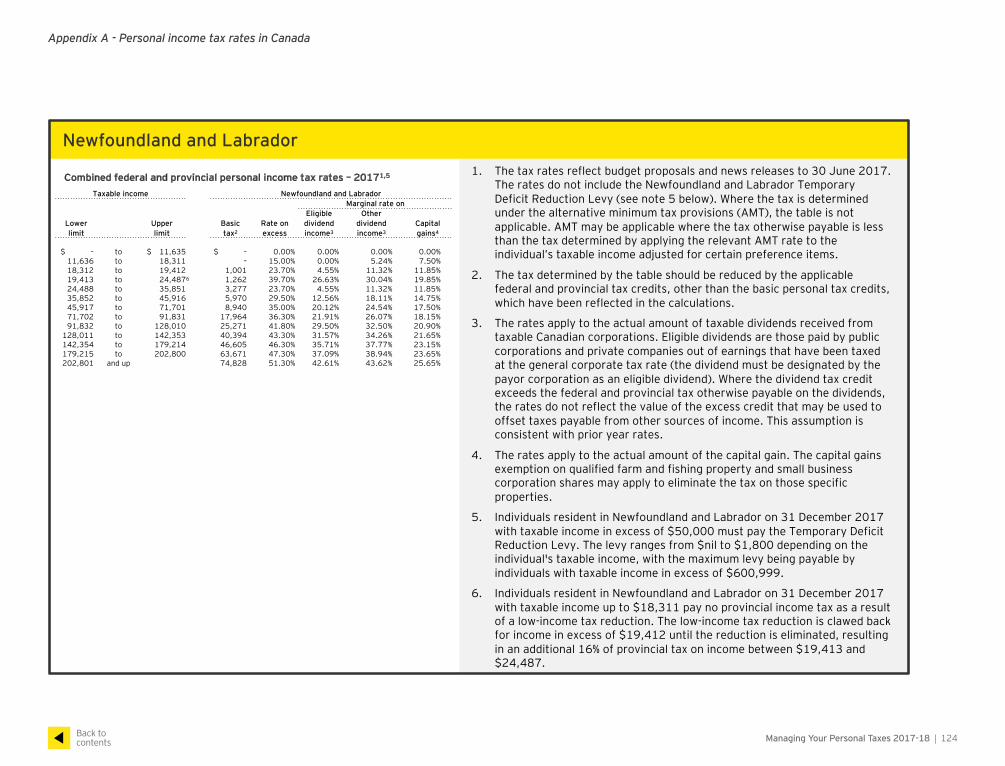

Newfoundland and Labrador

Combined federal and provincial personal income tax rates – 20171,5

Taxable income Newfoundland and LabradorMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 18,311 – 15.00% 0.00% 5.24% 7.50%18,312 to 19,412 1,001 23.70% 4.55% 11.32% 11.85%19,413 to 24,487 6 1,262 39.70% 26.63% 30.04% 19.85%24,488 to 35,851 3,277 23.70% 4.55% 11.32% 11.85%35,852 to 45,916 5,970 29.50% 12.56% 18.11% 14.75%45,917 to 71,701 8,940 35.00% 20.12% 24.54% 17.50%71,702 to 91,831 17,964 36.30% 21.91% 26.07% 18.15%91,832 to 128,010 25,271 41.80% 29.50% 32.50% 20.90%

128,011 to 142,353 40,394 43.30% 31.57% 34.26% 21.65%142,354 to 179,214 46,605 46.30% 35.71% 37.77% 23.15%179,215 to 202,800 63,671 47.30% 37.09% 38.94% 23.65%202,801 and up 74,828 51.30% 42.61% 43.62% 25.65%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. The rates do not include the Newfoundland and Labrador Temporary Deficit Reduction Levy (see note 5 below). Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the tax otherwise payable is less than the tax determined by applying the relevant AMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, which have been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received from taxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by the payor corporation as an eligible dividend). Where the dividend tax credit exceeds the federal and provincial tax otherwise payable on the dividends, the rates do not reflect the value of the excess credit that may be used to offset taxes payable from other sources of income. This assumption is consistent with prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specific properties.

5. Individuals resident in Newfoundland and Labrador on 31 December 2017 with taxable income in excess of $50,000 must pay the Temporary Deficit Reduction Levy. The levy ranges from $nil to $1,800 depending on the individual's taxable income, with the maximum levy being payable by individuals with taxable income in excess of $600,999.

6. Individuals resident in Newfoundland and Labrador on 31 December 2017 with taxable income up to $18,311 pay no provincial income tax as a result of a low-income tax reduction. The low-income tax reduction is clawed back for income in excess of $19,412 until the reduction is eliminated, resulting in an additional 16% of provincial tax on income between $19,413 and $24,487.

Managing Your Personal Taxes 2017-18 | 125Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

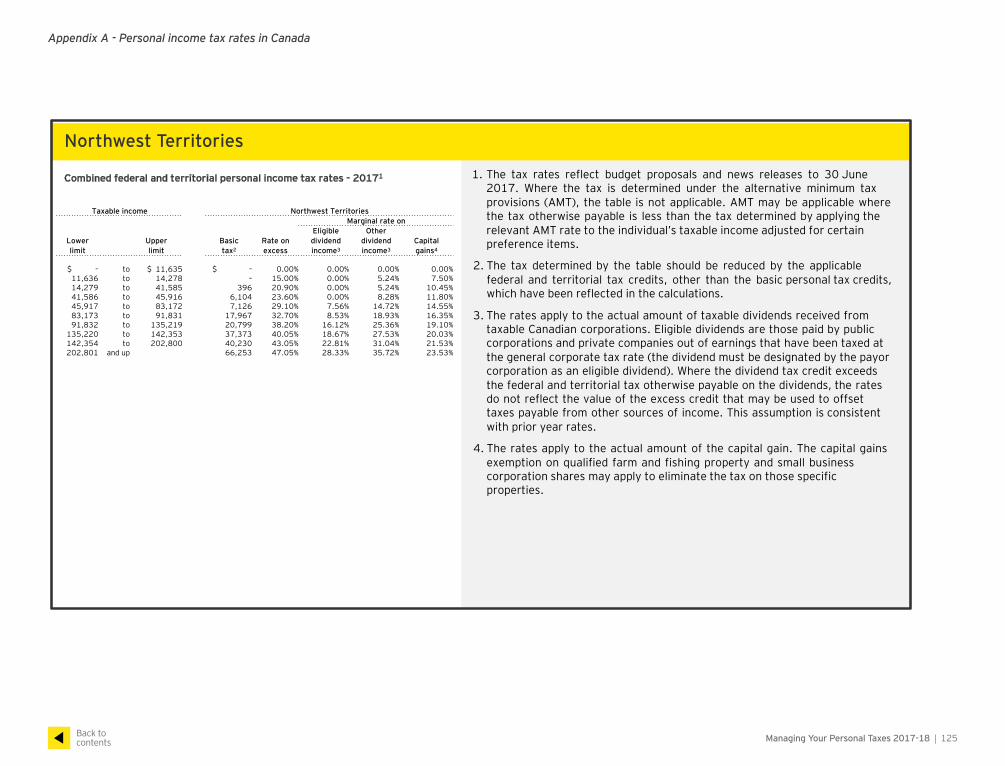

Northwest Territories

Combined federal and territorial personal income tax rates - 20171

Taxable income Northwest TerritoriesMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 14,278 – 15.00% 0.00% 5.24% 7.50%14,279 to 41,585 396 20.90% 0.00% 5.24% 10.45%41,586 to 45,916 6,104 23.60% 0.00% 8.28% 11.80%45,917 to 83,172 7,126 29.10% 7.56% 14.72% 14.55%83,173 to 91,831 17,967 32.70% 8.53% 18.93% 16.35%91,832 to 135,219 20,799 38.20% 16.12% 25.36% 19.10%

135,220 to 142,353 37,373 40.05% 18.67% 27.53% 20.03%142,354 to 202,800 40,230 43.05% 22.81% 31.04% 21.53%202,801 and up 66,253 47.05% 28.33% 35.72% 23.53%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable wherethe tax otherwise payable is less than the tax determined by applying therelevant AMT rate to the individual’s taxable income adjusted for certainpreference items.

2. The tax determined by the table should be reduced by the applicable federal and territorial tax credits, other than the basic personal tax credits,which have been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received fromtaxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed atthe general corporate tax rate (the dividend must be designated by the payorcorporation as an eligible dividend). Where the dividend tax credit exceedsthe federal and territorial tax otherwise payable on the dividends, the ratesdo not reflect the value of the excess credit that may be used to offsettaxes payable from other sources of income. This assumption is consistentwith prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gainsexemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specificproperties.

Managing Your Personal Taxes 2017-18 | 126Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

Nova ScotiaCombined federal and provincial personal income tax rates - 20171

Taxable income Nova ScotiaMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 11,894 – 15.00% 0.00% 5.24% 7.50%11,895 to 15,000 39 23.79% 0.00% 11.62% 11.90%15,001 to 21,000 5 778 28.79% 6.82% 17.47% 14.40%21,001 to 29,590 2,505 23.79% 0.00% 11.62% 11.90%29,591 to 45,916 4,549 29.95% 8.42% 18.83% 14.98%45,917 to 59,180 9,438 35.45% 15.98% 25.27% 17.73%59,181 to 91,831 14,140 37.17% 18.35% 27.28% 18.59%91,832 to 93,000 26,277 42.67% 25.94% 33.71% 21.34%93,001 to 142,353 26,776 43.50% 27.09% 34.68% 21.75%

142,354 to 150,000 48,244 46.50% 31.23% 38.19% 23.25%150,001 to 202,800 51,800 50.00% 36.06% 42.29% 25.00%202,801 and up 78,200 54.00% 41.58% 46.97% 27.00%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions(AMT), the table is not applicable. AMT may be applicable where the taxotherwise payable is less than the tax determined by applying the relevantAMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, whichhave been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received fromtaxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed atthe general corporate tax rate (the dividend must be designated by the payor corporation as an eligible dividend). Where the dividend tax creditexceeds the federal and provincial tax otherwise payable on the dividends, the rates do not reflect the value of the excess credit that may be used tooffset taxes payable from other sources of income. This assumption is consistent with prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specificproperties.

5. Individuals resident in Nova Scotia on 31 December 2017 with taxableincome up to $11,894, pay no provincial income tax as a result of a low income tax reduction. The low-income tax reduction is clawed back forincome in excess of $15,000 until the reduction is eliminated, resulting inan additional 5% of provincial tax on income between $15,001 and $21,000.

Managing Your Personal Taxes 2017-18 | 127Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

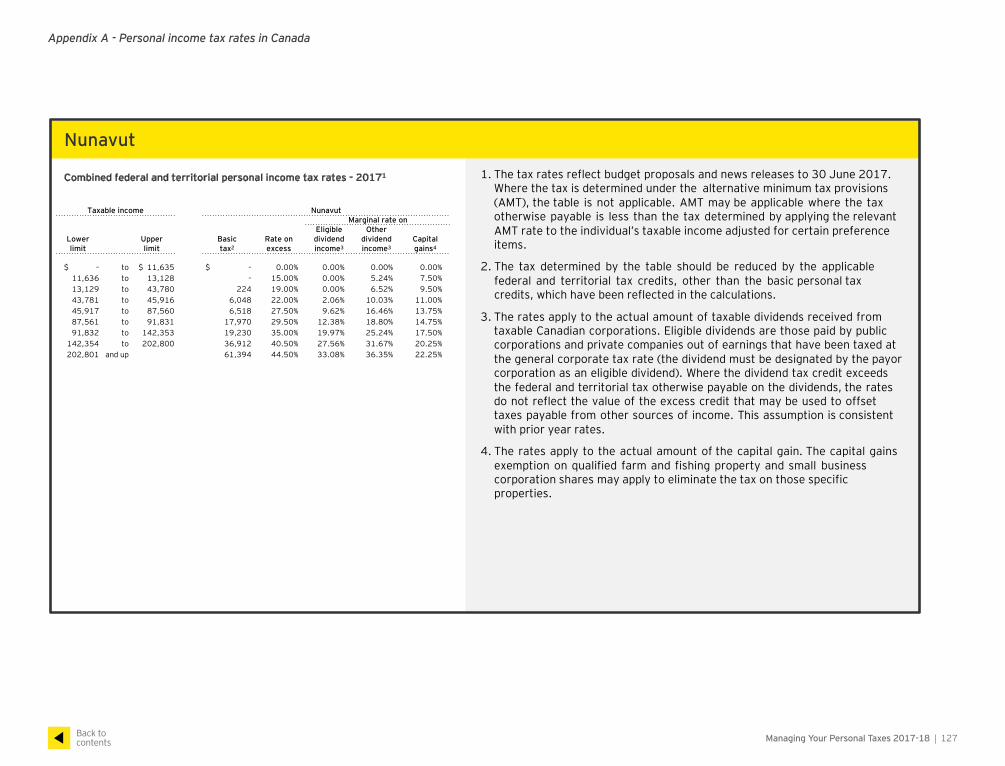

Nunavut

Combined federal and territorial personal income tax rates - 20171

Taxable income NunavutMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 13,128 – 15.00% 0.00% 5.24% 7.50%13,129 to 43,780 224 19.00% 0.00% 6.52% 9.50%43,781 to 45,916 6,048 22.00% 2.06% 10.03% 11.00%45,917 to 87,560 6,518 27.50% 9.62% 16.46% 13.75%87,561 to 91,831 17,970 29.50% 12.38% 18.80% 14.75%91,832 to 142,353 19,230 35.00% 19.97% 25.24% 17.50%

142,354 to 202,800 36,912 40.50% 27.56% 31.67% 20.25%202,801 and up 61,394 44.50% 33.08% 36.35% 22.25%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions(AMT), the table is not applicable. AMT may be applicable where the taxotherwise payable is less than the tax determined by applying the relevantAMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and territorial tax credits, other than the basic personal taxcredits, which have been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received fromtaxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed atthe general corporate tax rate (the dividend must be designated by the payorcorporation as an eligible dividend). Where the dividend tax credit exceedsthe federal and territorial tax otherwise payable on the dividends, the ratesdo not reflect the value of the excess credit that may be used to offsettaxes payable from other sources of income. This assumption is consistentwith prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gainsexemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specificproperties.

Managing Your Personal Taxes 2017-18 | 128Back to contents

Appendix A - Personal income tax rates in Canada

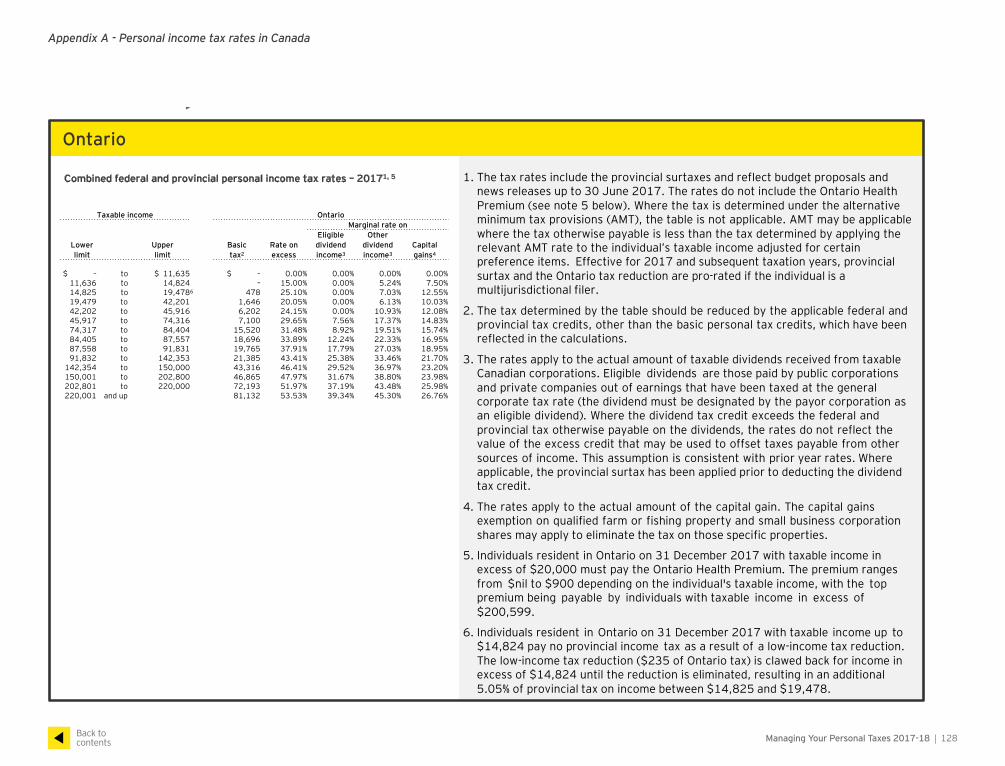

Combined personal income tax ratesOntario

Combined federal and provincial personal income tax rates – 20171, 5

Taxable income OntarioMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 14,824 – 15.00% 0.00% 5.24% 7.50%14,825 to 19,478 6 478 25.10% 0.00% 7.03% 12.55%19,479 to 42,201 1,646 20.05% 0.00% 6.13% 10.03%42,202 to 45,916 6,202 24.15% 0.00% 10.93% 12.08%45,917 to 74,316 7,100 29.65% 7.56% 17.37% 14.83%74,317 to 84,404 15,520 31.48% 8.92% 19.51% 15.74%84,405 to 87,557 18,696 33.89% 12.24% 22.33% 16.95%87,558 to 91,831 19,765 37.91% 17.79% 27.03% 18.95%91,832 to 142,353 21,385 43.41% 25.38% 33.46% 21.70%

142,354 to 150,000 43,316 46.41% 29.52% 36.97% 23.20%150,001 to 202,800 46,865 47.97% 31.67% 38.80% 23.98%202,801 to 220,000 72,193 51.97% 37.19% 43.48% 25.98%220,001 and up 81,132 53.53% 39.34% 45.30% 26.76%

1. The tax rates include the provincial surtaxes and reflect budget proposals andnews releases up to 30 June 2017. The rates do not include the Ontario Health Premium (see note 5 below). Where the tax is determined under the alternativeminimum tax provisions (AMT), the table is not applicable. AMT may be applicablewhere the tax otherwise payable is less than the tax determined by applying the relevant AMT rate to the individual’s taxable income adjusted for certain preference items. Effective for 2017 and subsequent taxation years, provincial surtax and the Ontario tax reduction are pro-rated if the individual is amultijurisdictional filer.

2. The tax determined by the table should be reduced by the applicable federal andprovincial tax credits, other than the basic personal tax credits, which have beenreflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received from taxable Canadian corporations. Eligible dividends are those paid by public corporationsand private companies out of earnings that have been taxed at the generalcorporate tax rate (the dividend must be designated by the payor corporation asan eligible dividend). Where the dividend tax credit exceeds the federal andprovincial tax otherwise payable on the dividends, the rates do not reflect thevalue of the excess credit that may be used to offset taxes payable from othersources of income. This assumption is consistent with prior year rates. Whereapplicable, the provincial surtax has been applied prior to deducting the dividendtax credit.

4. The rates apply to the actual amount of the capital gain. The capital gainsexemption on qualified farm or fishing property and small business corporation shares may apply to eliminate the tax on those specific properties.

5. Individuals resident in Ontario on 31 December 2017 with taxable income inexcess of $20,000 must pay the Ontario Health Premium. The premium ranges from $nil to $900 depending on the individual's taxable income, with the top premium being payable by individuals with taxable income in excess of$200,599.

6. Individuals resident in Ontario on 31 December 2017 with taxable income up to $14,824 pay no provincial income tax as a result of a low-income tax reduction. The low-income tax reduction ($235 of Ontario tax) is clawed back for income inexcess of $14,824 until the reduction is eliminated, resulting in an additional5.05% of provincial tax on income between $14,825 and $19,478.

Managing Your Personal Taxes 2017-18 | 129Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

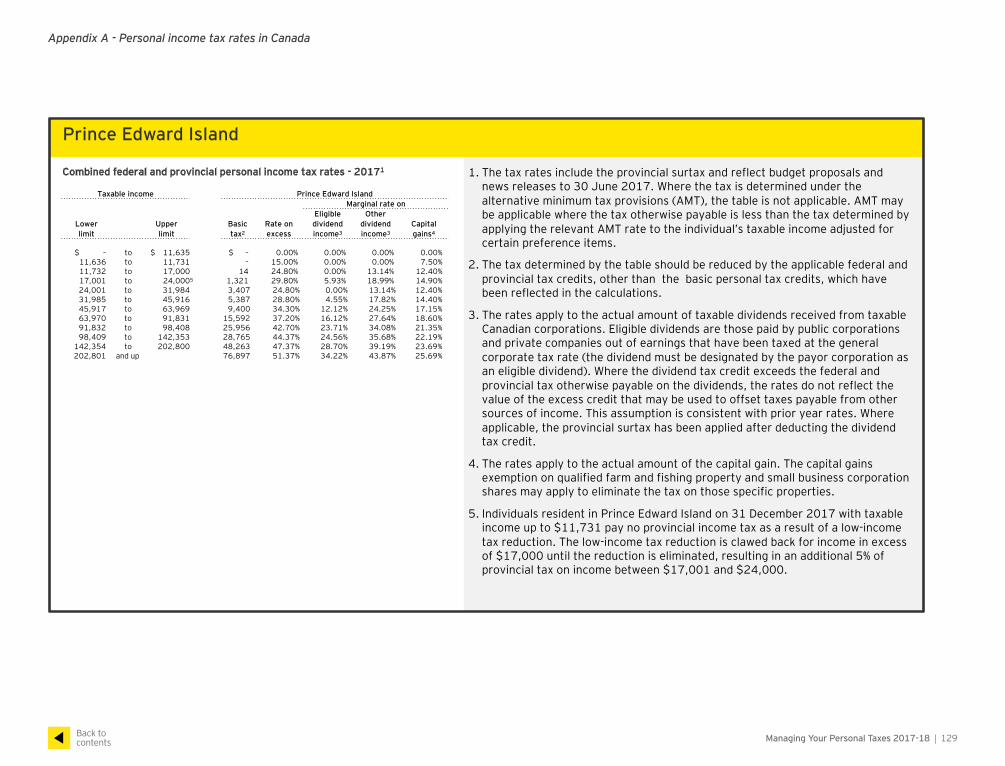

Prince Edward Island

Combined federal and provincial personal income tax rates - 20171

Taxable income Prince Edward IslandMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 11,731 – 15.00% 0.00% 0.00% 7.50%11,732 to 17,000 14 24.80% 0.00% 13.14% 12.40%17,001 to 24,000 5 1,321 29.80% 5.93% 18.99% 14.90%24,001 to 31,984 3,407 24.80% 0.00% 13.14% 12.40%31,985 to 45,916 5,387 28.80% 4.55% 17.82% 14.40%45,917 to 63,969 9,400 34.30% 12.12% 24.25% 17.15%63,970 to 91,831 15,592 37.20% 16.12% 27.64% 18.60%91,832 to 98,408 25,956 42.70% 23.71% 34.08% 21.35%98,409 to 142,353 28,765 44.37% 24.56% 35.68% 22.19%

142,354 to 202,800 48,263 47.37% 28.70% 39.19% 23.69%202,801 and up 76,897 51.37% 34.22% 43.87% 25.69%

1. The tax rates include the provincial surtax and reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the tax otherwise payable is less than the tax determined by applying the relevant AMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, which have been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received from taxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by the payor corporation as an eligible dividend). Where the dividend tax credit exceeds the federal and provincial tax otherwise payable on the dividends, the rates do not reflect the value of the excess credit that may be used to offset taxes payable from other sources of income. This assumption is consistent with prior year rates. Where applicable, the provincial surtax has been applied after deducting the dividend tax credit.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specific properties.

5. Individuals resident in Prince Edward Island on 31 December 2017 with taxable income up to $11,731 pay no provincial income tax as a result of a low-income tax reduction. The low-income tax reduction is clawed back for income in excess of $17,000 until the reduction is eliminated, resulting in an additional 5% of provincial tax on income between $17,001 and $24,000.

Managing Your Personal Taxes 2017-18 | 130Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

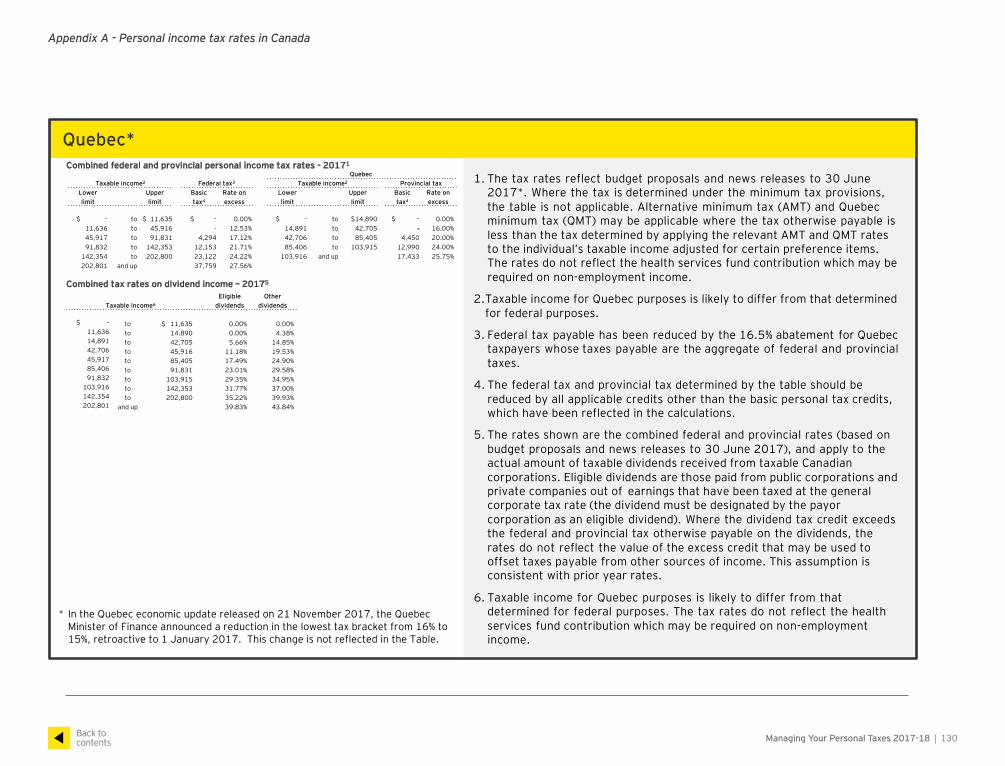

Quebec*Combined federal and provincial personal income tax rates - 20171

QuebecTaxable income2 Federal tax3 Taxable income2 Provincial tax

Lower Upper Basic Rate on Lower Upper Basic Rate onlimit limit tax4 excess limit limit tax4 excess

$ – to $ 11,635 $ – 0.00% $ – to $14,890 $ – 0.00%11,636 to 45,916 – 12.53% 14,891 to 42,705 16.00%45,917 to 91,831 4,294 17.12% 42,706 to 85,405 4,450 20.00%91,832 to 142,353 12,153 21.71% 85,406 to 103,915 12,990 24.00%

142,354 to 202,800 23,122 24.22% 103,916 and up 17,433 25.75%202,801 and up 37,759 27.56%

Eligible OtherTaxable income6 dividends dividends

$ – to $ 11,635 0.00% 0.00%11,636 to 14,890 0.00% 4.38%14,891 to 42,705 5.66% 14.85%42,706 to 45,916 11.18% 19.53%45,917 to 85,405 17.49% 24.90%85,406 to 91,831 23.01% 29.58%91,832 to 103,915 29.35% 34.95%

103,916 to 142,353 31.77% 37.00%142,354 to 202,800 35.22% 39.93%202,801 and up 39.83% 43.84%

Combined tax rates on dividend income – 20175

1. The tax rates reflect budget proposals and news releases to 30 June 2017*. Where the tax is determined under the minimum tax provisions,the table is not applicable. Alternative minimum tax (AMT) and Quebecminimum tax (QMT) may be applicable where the tax otherwise payable isless than the tax determined by applying the relevant AMT and QMT rates to the individual’s taxable income adjusted for certain preference items.The rates do not reflect the health services fund contribution which may berequired on non-employment income.

2.Taxable income for Quebec purposes is likely to differ from that determined for federal purposes.

3. Federal tax payable has been reduced by the 16.5% abatement for Quebectaxpayers whose taxes payable are the aggregate of federal and provincial taxes.

4. The federal tax and provincial tax determined by the table should bereduced by all applicable credits other than the basic personal tax credits,which have been reflected in the calculations.

5. The rates shown are the combined federal and provincial rates (based onbudget proposals and news releases to 30 June 2017), and apply to theactual amount of taxable dividends received from taxable Canadiancorporations. Eligible dividends are those paid from public corporations andprivate companies out of earnings that have been taxed at the generalcorporate tax rate (the dividend must be designated by the payorcorporation as an eligible dividend). Where the dividend tax credit exceedsthe federal and provincial tax otherwise payable on the dividends, therates do not reflect the value of the excess credit that may be used tooffset taxes payable from other sources of income. This assumption is consistent with prior year rates.

6. Taxable income for Quebec purposes is likely to differ from thatdetermined for federal purposes. The tax rates do not reflect the healthservices fund contribution which may be required on non-employment income.

-

* In the Quebec economic update released on 21 November 2017, the Quebec Minister of Finance announced a reduction in the lowest tax bracket from 16% to 15%, retroactive to 1 January 2017. This change is not reflected in the Table.

Managing Your Personal Taxes 2017-18 | 131Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

Saskatchewan

Combined federal and provincial personal income tax rates - 20171

Taxable income SaskatchewanMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 16,065 – 15.00% 0.00% 5.24% 7.50%16,066 to 45,225 665 25.75% 0.00% 13.88% 12.88%45,226 to 45,916 8,173 27.75% 2.76% 16.22% 13.88%45,917 to 91,831 8,365 33.25% 10.32% 22.65% 16.63%91,832 to 129,214 23,632 38.75% 17.91% 29.09% 19.38%

129,215 to 142,353 38,118 40.75% 20.67% 31.43% 20.38%142,354 to 202,800 43,472 43.75% 24.81% 34.94% 21.88%202,801 and up 69,917 47.75% 30.33% 39.62% 23.88%

1. The tax rates reflect budget proposals and news releases to 30 June 2017. Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the tax otherwise payable is less than the tax determined by applying the relevant AMT rate to the individual’s taxable income adjusted for certain preference items.

2. The tax determined by the table should be reduced by the applicable federal and provincial tax credits, other than the basic personal tax credits, which have been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received from taxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed at the general corporate tax rate (the dividend must be designated by the payor corporation as an eligible dividend). Where the dividend tax credit exceeds the federal and provincial tax otherwise payable on the dividends, the rates do not reflect the value of the excess credit that may be used to offset taxes payable from other sources of income. This assumption is consistent with prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specific properties. Individuals resident in Saskatchewan on 31 December 2017 who reported a capital gain from the disposition of qualified farm property or small business corporation shares may be eligible for an additional capital gains credit of up to 2%.

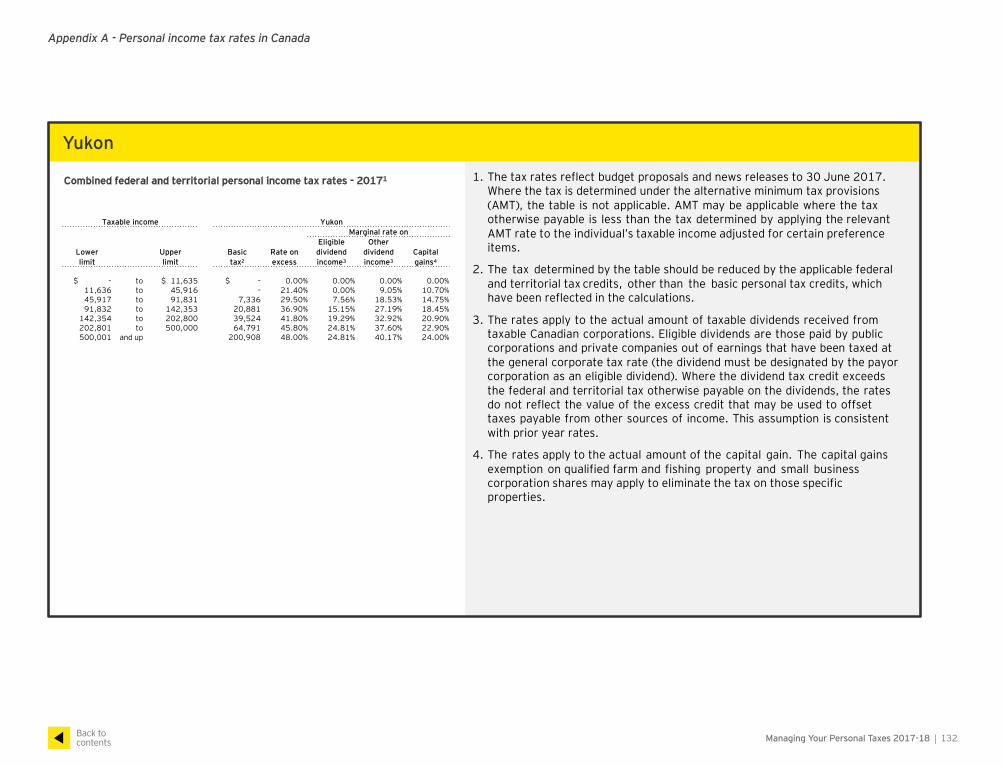

Managing Your Personal Taxes 2017-18 | 132Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

Yukon

Combined federal and territorial personal income tax rates - 20171

Taxable income YukonMarginal rate on

Eligible OtherLower Upper Basic Rate on dividend dividend Capitallimit limit tax2 excess income3 income3 gains4

$ – to $ 11,635 $ – 0.00% 0.00% 0.00% 0.00%11,636 to 45,916 – 21.40% 0.00% 9.05% 10.70%45,917 to 91,831 7,336 29.50% 7.56% 18.53% 14.75%91,832 to 142,353 20,881 36.90% 15.15% 27.19% 18.45%

142,354 to 202,800 39,524 41.80% 19.29% 32.92% 20.90%202,801 to 500,000 64,791 45.80% 24.81% 37.60% 22.90%500,001 and up 200,908 48.00% 24.81% 40.17% 24.00%

1. The tax rates reflect budget proposals and news releases to 30 June 2017.Where the tax is determined under the alternative minimum tax provisions (AMT), the table is not applicable. AMT may be applicable where the taxotherwise payable is less than the tax determined by applying the relevantAMT rate to the individual’s taxable income adjusted for certain preferenceitems.

2. The tax determined by the table should be reduced by the applicable federal and territorial tax credits, other than the basic personal tax credits, whichhave been reflected in the calculations.

3. The rates apply to the actual amount of taxable dividends received fromtaxable Canadian corporations. Eligible dividends are those paid by public corporations and private companies out of earnings that have been taxed atthe general corporate tax rate (the dividend must be designated by the payorcorporation as an eligible dividend). Where the dividend tax credit exceedsthe federal and territorial tax otherwise payable on the dividends, the ratesdo not reflect the value of the excess credit that may be used to offsettaxes payable from other sources of income. This assumption is consistentwith prior year rates.

4. The rates apply to the actual amount of the capital gain. The capital gains exemption on qualified farm and fishing property and small business corporation shares may apply to eliminate the tax on those specificproperties.

Managing Your Personal Taxes 2017-18 | 133Back to contents

Appendix A - Personal income tax rates in Canada

Combined personal income tax rates

Non-residents

Federal personal income tax rates - 20171 1. The tax rates reflect budget proposals and news releases to 30 June 2017.

Taxable income Non-resident rate of 48%

Lower Upper BasicRate on

limit limit tax excess

$ – to $ 45,916 $ – 22.20%45,917 to 91,831 10,193 30.34%91,832 to 142,353 24,124 38.48%

142,354 to 202,800 43,565 42.92%202,801 and up 69,509 48.84%