mandatory combined reporting for state income...

TRANSCRIPT

Mandatory Combined Reporting

for State Income Taxes Improving Tax Compliance to Manage Conflicting State Rules

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

WEDNESDAY, MAY 22, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Robert Rosato, Manager of State Income-Franchise Tax, Ryan, Pittsburgh

Jeffrey Reed, Attorney, Mayer Brown, New York

Mike Shaikh, Reed Smith, Los Angeles

Robert Porcelli, Partner, State and Local Tax Group, PricewaterhouseCoopers, Tyson’s Corner, Va.

For this program, attendees must listen to the audio over the telephone.

Tips for Optimal Quality

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Continuing Education Credits

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Mandatory Combined Reporting for State Income Taxes Seminar

Mike Shaikh, Reed Smith

Robert Porcelli, PricewaterhouseCoopers

May 22, 2013

Robert Rosato, Ryan

Jeffrey Reed, Mayer Brown

Today’s Program

Overview Of Background Concepts And Trends

[Robert Rosato]

Mandatory Unitary Combined Reporting States

[Mike Shaikh, Jeffrey Reed and Robert Porcelli]

Discretionary Combined Reporting States

[Jeffrey Reed and Mike Shaikh]

Next States Likely To Act

[Robert Porcelli]

Slide 8 – Slide 25

Slide 53 – Slide 65

Slide 26 – Slide 45

Slide 46 – Slide 52

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

7

OVERVIEW OF BACKGROUND CONCEPTS AND TRENDS

Robert Rosato, Ryan

State Filing Methodologies Separate company reporting

– Individual entity basis, with income of affiliates excluded

Consolidated reporting

– Common ownership, usually 80% or more

– Some states require that a federal consolidated return be filed as a

prerequisite to filing a state consolidated return.

– Single return filed for the affiliated group

Combined reporting

– Common ownership, usually 50% or more

– Usually same trade or business

Evidenced by functional integration, centralized management

and economies of scale

9

Separate Company Reporting Filing separately

– The parent company and its affiliates are treated separately when

determining taxable income.

– Nexus is analyzed with regard to each company's contacts with the

state.

LLCs are treated as taxable entities by some states.

– Separate company reporting is not common among the states.

Some remaining separate reporting states have proposals to

shift away from this methodology.

10

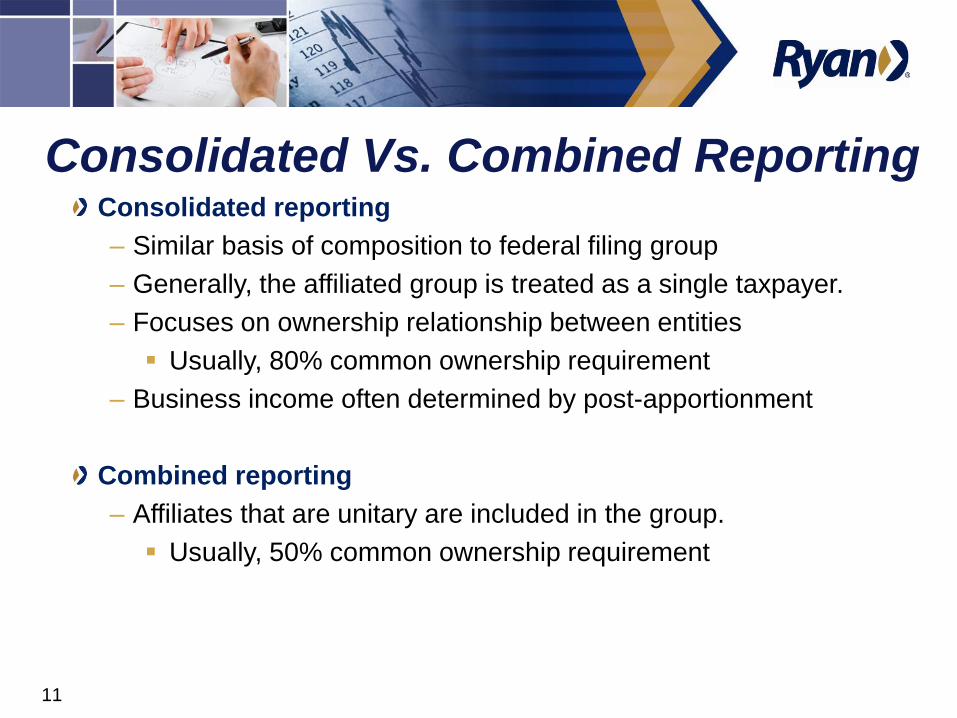

Consolidated Vs. Combined Reporting Consolidated reporting

– Similar basis of composition to federal filing group

– Generally, the affiliated group is treated as a single taxpayer.

– Focuses on ownership relationship between entities

Usually, 80% common ownership requirement

– Business income often determined by post-apportionment

Combined reporting

– Affiliates that are unitary are included in the group.

Usually, 50% common ownership requirement

11

Combined Reporting Types of combined filing

– Mandatory combined reporting

Roughly 20 jurisdictions require a unitary business to file a

combined report.

Unitary members are forced by statute to file a combined report.

– Elective/discretionary combined reporting

Generally, these states also allow separate company returns.

State requires or permits taxpayer to elect to file a combined

report, if certain conditions are met.

Combined report is used to accurately reflect group’s income

earned in the state.

– Nexus combination reporting

All members with nexus in the state are included in return.

States vary regarding pre- and post-apportionment of income. 12

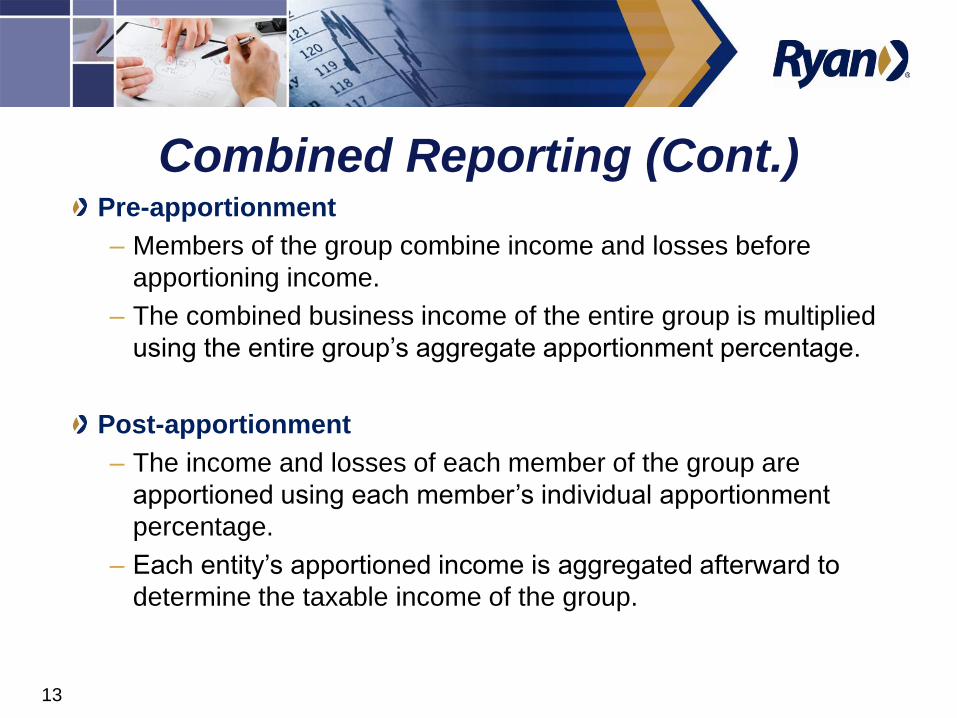

Combined Reporting (Cont.) Pre-apportionment

– Members of the group combine income and losses before

apportioning income.

– The combined business income of the entire group is multiplied

using the entire group’s aggregate apportionment percentage.

Post-apportionment

– The income and losses of each member of the group are

apportioned using each member’s individual apportionment

percentage.

– Each entity’s apportioned income is aggregated afterward to

determine the taxable income of the group.

13

Combined Reporting (Cont.) Unitary business

– States are limited by the U.S. Constitution when determining which

entities are unitary.

– Fact-dependent analysis, often evidenced by factors including

centralized management, functional integration and economies of

Scale

– Determining which entities are unitary

MTC regulations

Three unities test

Contribution and dependency test

Flow of value test

Factors of profitability test

14

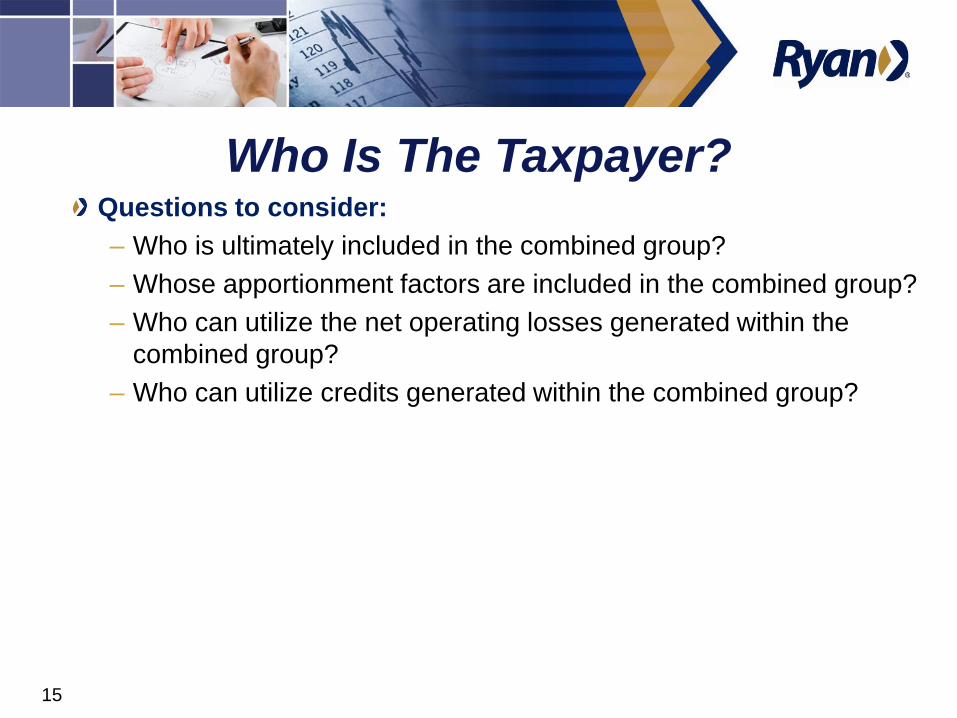

Who Is The Taxpayer? Questions to consider:

– Who is ultimately included in the combined group?

– Whose apportionment factors are included in the combined group?

– Who can utilize the net operating losses generated within the

combined group?

– Who can utilize credits generated within the combined group?

15

Who Is The Taxpayer? (Cont.) Worldwide reporting

– Combined return includes income from all foreign and domestic

entities in the unitary group.

– Upheld by the U.S. Supreme Court in Container Corporation of

America v. Franchise Tax Board, 103 S. Ct. 2933 (1983)

Water’s edge election

– Taxpayer may exclude foreign members of the combined group

that are not organized in the U.S.

16

Who Is The Taxpayer? (Cont.) Joyce v. Finnigan

– Appeal of Joyce, Inc., No. 66 SBE 069 (Cal. SBE Nov. 11, 1966)

A shoe company was unitary with a subsidiary in California but had no

nexus in California.

A unitary member without nexus to the taxing jurisdiction must remove

its sales from the sales numerator, for apportionment purposes.

A unitary member with nexus must throw back sales to jurisdictions

where the member has no nexus.

– Appeal of Finnigan Corp., Cal. St. Bd. of Equal., August 25, 1988

Two taxpayers with nexus to California had sales outside California to

a taxing jurisdiction where only one entity had nexus,

All members of the unitary group include in-state sales in the

apportionment numerator of a Finnigan state,

Nexus based on the entire group: Sales by a member without

individual nexus are not thrown back, because nexus was established

by the entire group. 17

Who Is The Taxpayer? (Cont.) Throwback of sales

– Requires taxpayers that are not taxable in the destination state to

source sales back to the state of origin

Sales are “thrown back” into the numerator of the jurisdiction

from which the goods were shipped.

Reasoning behind throwback is to ensure that all sales are

assigned to the numerator of a jurisdiction.

– Double-throwback

Illinois “throws back” sales to its sales numerator when the

taxpayer’s activities in Illinois go beyond P.L. 86-272, and the

taxpayer’s receipts are taxable in neither the destination state

nor the origin state.

18

Who Is The Taxpayer? (Cont.) Credits

– Multiple approaches exist regarding application of credits to a

unitary group.

Some states only allow application of the credit to the entity that

earned the credit, despite the unitary nature of the group.

Other states allow application of the credit to any entity in the

unitary group, though another entity in the group actually

earned the credit.

19

Who Is The Taxpayer? (Cont.) Net operating losses

– NOLs can be treated as pre-apportioned losses carried forward for

use by the entire group.

– Some states treat NOLs as a post-apportioned loss in the

aggregate, for use by the entire group.

– Some states treat NOLs as a post-apportioned losses for each

separate entity.

Application of NOLs is limited in application to the entity that

incurred the loss, not to other unitary entities.

– How are net operating losses allocated when members join or

leave the group?

– What happens if a member converts to an LLC?

20

California Combined Reporting Update Recent changes in California

– California converts to Finnigan.

All sales of the combined reporting group are included in the

California sales numerator for apportionment purposes,

regardless of a unitary member’s nexus with the state.

– Single-sales factor apportionment

For 2011 and 2012, taxpayers can elect to use single-sales

factor apportionment or a double-weighted sales factor.

» Election for 2011 and 2012 must be on a timely filed return

and made by all entities in the combined group.

In 2013, most taxpayers are required to use single-sales factor

apportionment, including corporations in a combined group.

21

California Combined Reporting Update (Cont.)

California law changes

– Economic nexus

Cal. Rev. & Tax. Code §3101

» A taxpayer is doing business in California if California sales

exceed the lesser of $500,000 or 25% of its total sales.

– California Chief Counsel Ruling 2012-03 (Aug. 28, 2012)

A taxpayer should not throw back sales to a jurisdiction where

the taxpayer has greater than $500,000 of sales.

» Having $500,000 of receipts in California creates economic

nexus with California.

» Despite another jurisdiction's statutes, $500,000 of sales into

that jurisdiction creates economic nexus, for California

throwback purposes.

22

State Throwback Updates Recent rulings and proposed laws

– Indiana – sales to foreign countries subject to throwback

A taxpayer’s sales are thrown back when its business activities

do not rise to the level of “doing business” in other states or

foreign jurisdictions.

– Kentucky – House Bill 142

Proposed bill would adopt a throwback rule, in addition to

mandatory combined reporting, beginning on or after Jan. 1,

2014.

– Minnesota – H.F. 37

Proposed bill would adopt throwback rule to sales of tangible

personal property and services, beginning in 2014.

23

Slide Intentionally Left Blank

Net Operating Loss Update Wisconsin NOL application

– Wis. Stat. 71.255(6)(a) allows a post-apportioned NOL not used by

a member of the combined group to be applied to other members

of the combined group that can use the NOL.

– For taxable years after 2012, members of the combined group

cannot share NOLs generated in tax years before Jan. 1, 2009.

– Beginning in tax year 2011 and for 19 years thereafter, an entity

with a pre-2009 NOL may use that NOL against its own income,

then use up to 5% of the pre-2009 NOL to offset income of other

entities.

25

MANDATORY UNITARY COMBINED REPORTING STATES

Mike Shaikh, Reed Smith

Jeffrey Reed, Mayer Brown

Robert Porcelli, PricewaterhouseCoopers

Massachusetts Regulations

• Unity presumptions/indicia

• Who’s in the group

– Water’s edge/worldwide election

– Domestic corporations plus certain foreign corporations

– REITs/RICs/captive insurance companies

• Computation of income

– Inter-company transactions (1.1502-13)

– Deferral regime

• Apportionment

– “California method”

– Finnigan

– Special rules

• Tax attributes

27

West Virginia

• MTC method

• Unity presumptions

• Who’s in the group

– Water’s edge/worldwide election

– Newly formed entities

– Insurance companies (out)

• Computation of income

– Inter-company transactions (conformity to Treasury Reg. 1.1502-13)

– Deferred inter-company stock accounts

• Apportionment

– On a group basis

– Joyce

– Throw-out

• Tax attributes

28

District Of Columbia: Combined Reporting

• Mandatory unitary combined reporting was enacted effective Jan. 1, 2011.

• The final combined reporting regulations were finalized on Sept. 14, 2012.

• A corporation subject to tax must file a combined return if it is engaged in a unitary business with entities related by common ownership.

• Entities are commonly owned or controlled when more than 50% of the voting control of each member is directly or indirectly owned by a common owner or owners.

29

District Of Columbia: Combined Reporting (Cont.)

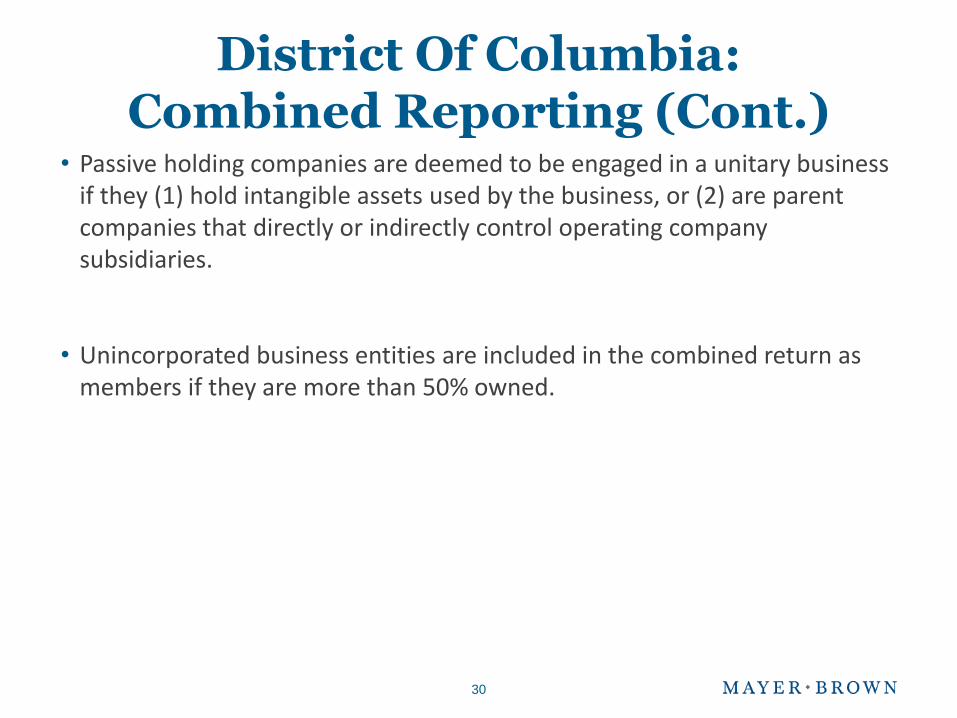

• Passive holding companies are deemed to be engaged in a unitary business if they (1) hold intangible assets used by the business, or (2) are parent companies that directly or indirectly control operating company subsidiaries.

• Unincorporated business entities are included in the combined return as members if they are more than 50% owned.

30

Slide Intentionally Left Blank

Harley Davidson: Securitization Vehicles And Combined Returns

• Harley-Davidson, Inc. & Subs. v. California Franchise Tax Board

– Harley-Davidson offered a financing program to its dealers and to retail customers.

– The loans were packaged and were deposited into special purpose entity trusts (SPEs). The SPEs were established to be bankruptcy remote vehicles.

– The San Diego Superior Court ruled that the SPEs had nexus with California on the basis that they “depended on” Harley-Davidson entities “for their existence,” since their only business was to purchase loans for securitization. Accordingly, their factors were required to be included in the California combined return.

– Additionally, the court ruled that the SPEs were “financial corporations,” because they competed with national banks in selling pools of loans.

32

PwC

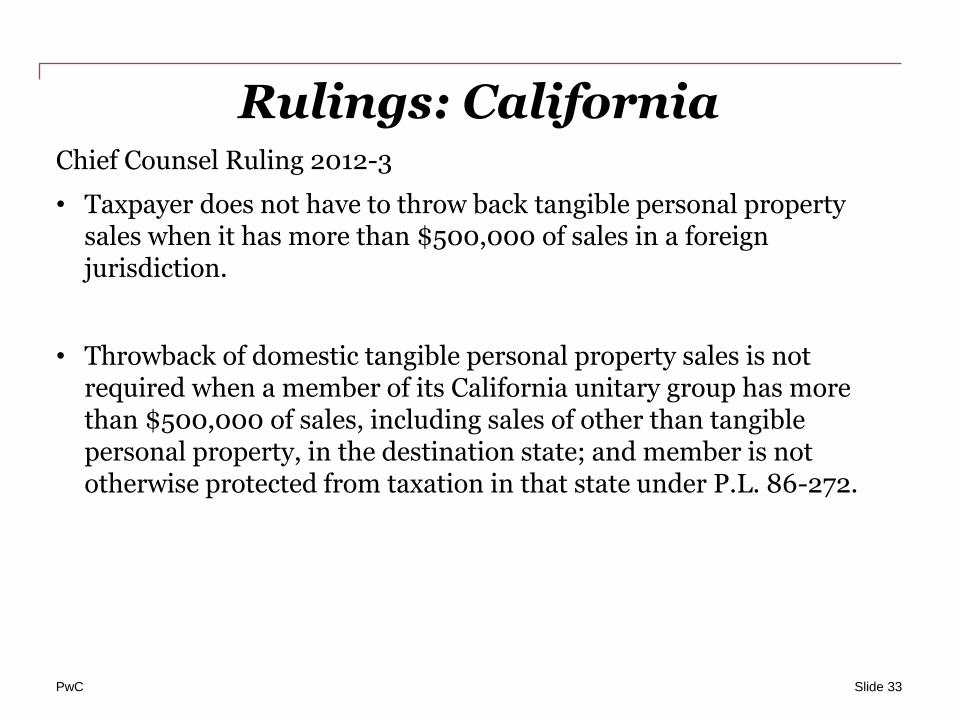

Rulings: California Chief Counsel Ruling 2012-3

• Taxpayer does not have to throw back tangible personal property sales when it has more than $500,000 of sales in a foreign jurisdiction.

• Throwback of domestic tangible personal property sales is not required when a member of its California unitary group has more than $500,000 of sales, including sales of other than tangible personal property, in the destination state; and member is not otherwise protected from taxation in that state under P.L. 86-272.

Slide 33

PwC

Rulings: California (Cont.)

Chief Counsel Ruling 2012-06

• Certain corporations included in federal consolidated return converted to limited liability companies, as a result of filing under Chap. 11.

• Members of consolidated group were disallowed a worthless stock deduction on conversion of insolvent corporations under Treas. Reg. Sec. 1.337(d)-2(a)(1).

• FTB held that because California does not permit a consolidated return, Treas. Reg. Sect. 1.337(d)-2(a)(1) will not operate to disallow any worthless stock deduction pertaining to insolvent converted entities, otherwise applicable under federal consolidated rules.

Slide 34

PwC

Cases: California

Apple, Inc. v. Franchise tax Board, Cal. Circuit Ct., Dkt. Nos. A128091, A129090, 9/12/2011; Cal. S. Ct., Dkt. No. S197381, petition for review denied 01/04/2012

• Dividends from the accumulated earnings of a partially included CFC of a water’s edge filer are governed by the last-in/first-out ordering provisions and must be treated as coming from current-year earnings until exhausted, and then from the most recent years’ earnings without regard to whether the earnings represent included or excluded income.

• Interest expense attributable to funds proven to have some economic connection to the generation of taxable income qualify for deduction.

Slide 35

PwC

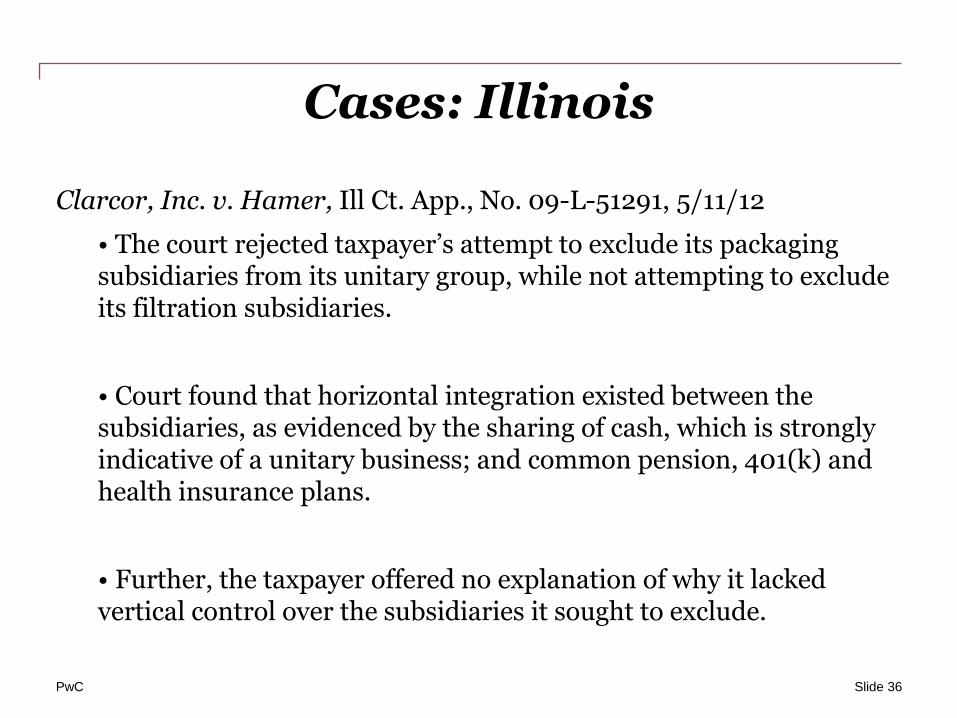

Cases: Illinois

Clarcor, Inc. v. Hamer, Ill Ct. App., No. 09-L-51291, 5/11/12

• The court rejected taxpayer’s attempt to exclude its packaging subsidiaries from its unitary group, while not attempting to exclude its filtration subsidiaries.

• Court found that horizontal integration existed between the subsidiaries, as evidenced by the sharing of cash, which is strongly indicative of a unitary business; and common pension, 401(k) and health insurance plans.

• Further, the taxpayer offered no explanation of why it lacked vertical control over the subsidiaries it sought to exclude.

Slide 36

PwC

Cases: Minnesota Express Scripts, Inc. v. Commissioner of Revenue, Minnesota Tax Court, Ramsey County, Docket No. 8272R, 8/20/12

• A taxpayer’s corporate acquisition triggered an IRC Sect. 382 limitation of the acquired company’s net operating loss carryovers equal to approximately $30 million. The Minnesota Department of Revenue apportioned that limitation using the apportionment ratio of the income years, which reduced the amount of available loss to approximately $120,000.

• Despite department guidance to the contrary, there was no statutory authority for the department’s position to apportion the Sect. 382 limitation.

• Additionally, the Tax Court found that the taxpayer was not unitary with one of its LLC subsidiaries, because the facts did not support a flow of value and there was not sufficient control over the subsidiary.

Slide 37

PwC

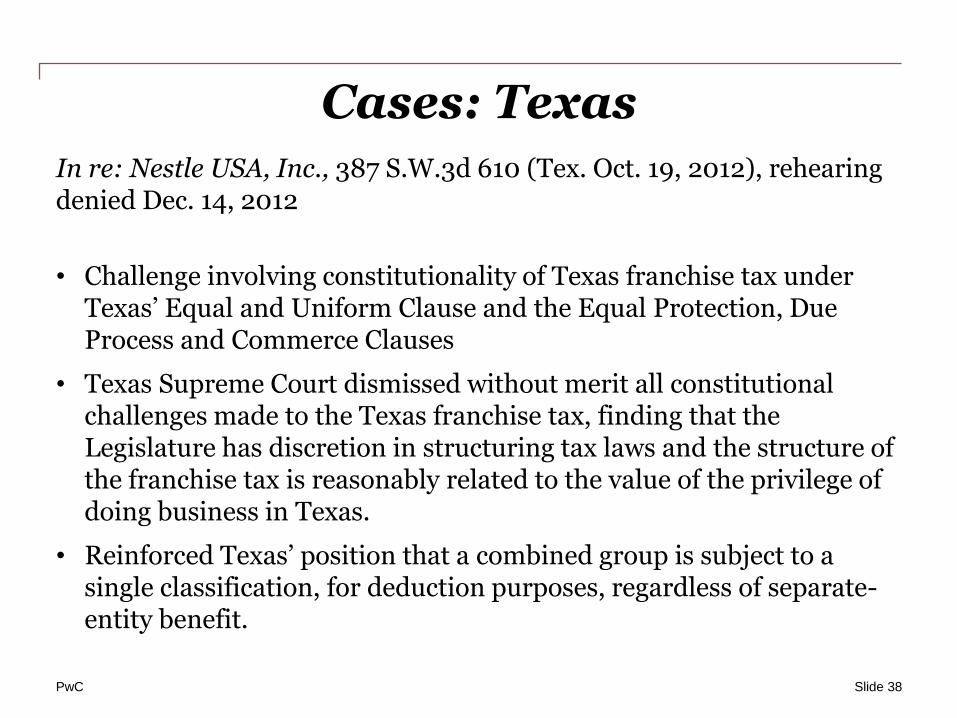

Cases: Texas

In re: Nestle USA, Inc., 387 S.W.3d 610 (Tex. Oct. 19, 2012), rehearing denied Dec. 14, 2012

• Challenge involving constitutionality of Texas franchise tax under Texas’ Equal and Uniform Clause and the Equal Protection, Due Process and Commerce Clauses

• Texas Supreme Court dismissed without merit all constitutional challenges made to the Texas franchise tax, finding that the Legislature has discretion in structuring tax laws and the structure of the franchise tax is reasonably related to the value of the privilege of doing business in Texas.

• Reinforced Texas’ position that a combined group is subject to a single classification, for deduction purposes, regardless of separate-entity benefit.

Slide 38

Costco Wholesale Corp. v. Oregon Department of Revenue

• Bermuda insurance company not independently subject to tax or required to file in Oregon.

• Held insurance company income required to be in included in group income

• Compare with Stancorp

Oregon Tax Court, TC 4956

39

Coca-Cola Enterprises, Inc. v. Alabama Department of Revenue

• Consolidated group filing

• Issue of whether the group can carry forward NOLs incurred before an election to file consolidated return

• Application of SRLY rules

• Held: Group may carry forward NOLs before election but may not deduct losses incurred before consolidated filing was an option.

Docket No. Corp. 09-641

40

Inclusion Of Foreign Entities In Combined Returns

• Most states provide for “water’s edge” combined reporting or worldwide combined reporting as a default, and water’s edge combined reporting may be elected.

• In some states, all foreign corporations (i.e., corporations incorporated in foreign countries) are excluded from the combined return.

• In other states, at least some foreign corporations are included in the combined return.

41

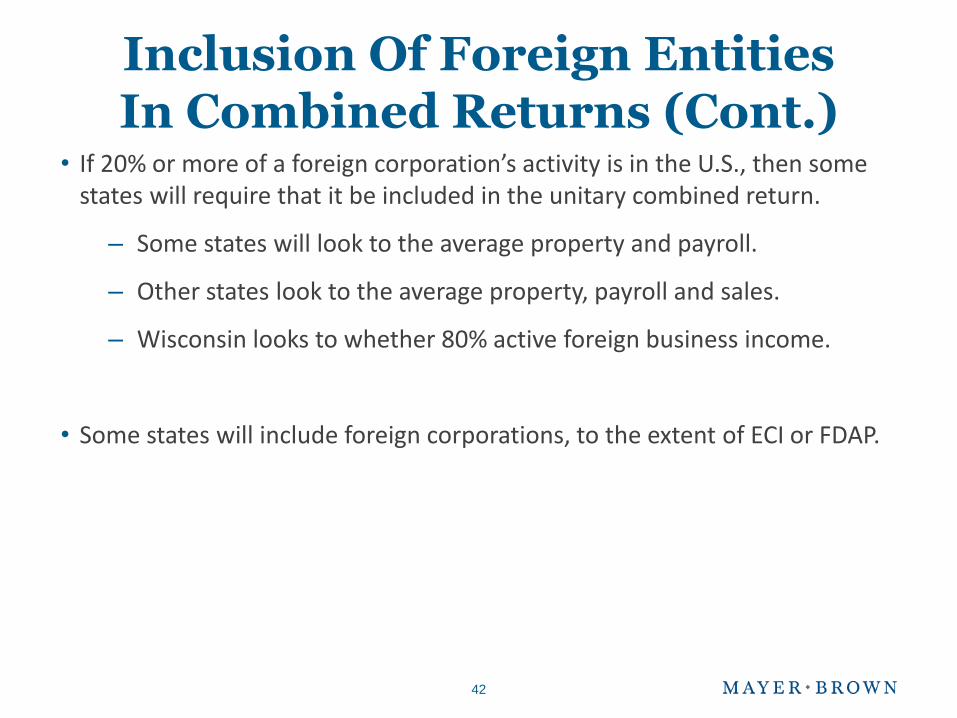

Inclusion Of Foreign Entities In Combined Returns (Cont.)

• If 20% or more of a foreign corporation’s activity is in the U.S., then some states will require that it be included in the unitary combined return.

– Some states will look to the average property and payroll.

– Other states look to the average property, payroll and sales.

– Wisconsin looks to whether 80% active foreign business income.

• Some states will include foreign corporations, to the extent of ECI or FDAP.

42

Inclusion Of Foreign Entities In Combined Returns (Cont.)

• Recently, a few states have started including foreign corporations if more than 20% of the income of the foreign corporation is from intangible property or service-related activities, the costs of which are deductible against the business income of other members of the unitary group (DC, MA and WV).

• A few states include foreign corporations in the combined return if they are doing business in a “tax haven” jurisdiction (AK, DC, MT and WV).

43

Slide Intentionally Left Blank

What’s In the Group?

• Insurance companies

• REITs/RICs/REMICs

45

DISCRETIONARY COMBINED REPORTING STATES

Jeffrey Reed, Mayer Brown

Mike Shaikh, Reed Smith

Discretionary Combined Reporting: New York

• Separate-entity state

• Old law: Combined if distortion

– Presumption of distortion if “substantial intercorporate transactions” between the companies

– If no substantial inter-corporate transactions, may be required or permitted to file combined if separate-entity reporting would not fairly reflect the income of the corporations

47

Discretionary Combined Reporting: New York (Cont.)

• New law:

– Must file combined if there are substantial inter-corporate transactions

– TSB-M-08(2)C details how to determine if there are substantial inter-corporate transactions.

• Receipts test

• Expenditures test

• Asset transfer test

• Loans included but not dividends

– Recent trend toward decombination audits

• IT USA, Inc.

48

North Carolina

• History of forced combination

– Wal-Mart East v. Hinton (2009)

– Delhaize America, Inc. v. Lay (2012)

– North Carolina Directive CD-12-02

• Codification of forced combination

49

Discretionary Combined Reporting: Indiana

• In Indiana, combined reporting is viewed as an alternative to three-factor apportionment. So, combined reporting may be invoked by the Indiana DOR or by taxpayers as a type of alternative apportionment.

• Combined reporting is warranted to “fairly” reflect a taxpayer’s Indiana income. Indiana Code 6-3-2-2

• Penalties

• Burden of proof issues

50

South Carolina

• Combination

– Media General Communications, Inc. v. S.C. Department of Revenue, (S.C. Supreme Court 2010)

• Burden of proof

– CarMax Auto Superstores West Coast, Inc. v. South Carolina Department of Revenue (S.C. Court of Appeals 2012)

51

Slide Intentionally Left Blank

NEXT STATES LIKELY TO ACT

Robert Porcelli, PricewaterhouseCoopers

PwC

Combined Reporting: 2001

Slide 54

AK

HI

ME

RI

VT

NH MA NY

CT

PA

NJ

MD DE

VA WV

NC

SC

GA

FL

IL OH

IN

MI WI

KY

TN

AL MS

AR

LA TX

OK

MO KS

IA

MN ND

SD

NE

NM AZ

CO UT

WY

MT

WA

OR

ID

NV

CA

DC

Combined reporting proposals

Unitary/combined states

Remaining separate entity or elective consolidated reporting/other

PwC

Combined Reporting: 2013

Slide 55

AK

HI

ME

RI

VT

NH MA

NY* CT

PA

NJ

MD DE

VA WV

NC

SC

GA

FL

IL OH

IN

MI WI

KY

TN

AL MS

AR

LA TX

OK

MO KS

IA

MN ND

SD

NE

NM* AZ

CO UT

WY

MT

WA

OR

ID

NV

CA

DC

Combined reporting proposals considered recently and/or currently proposed

Unitary/combined states (now including the Ohio CAT, Texas margin tax and Michigan business tax)

Remaining separate entity or elective consolidated reporting/other

* New Mexico requires certain unitary large retailers to file combined returns (2014).

* New York requires related corporations to file a

combined report upon the existence of

substantial intercorporate transactions

PwC

Combined Reporting

• Vermont – applies to tax years beginning on or after January 1, 2006

• West Virginia – any taxpayer engaged in a unitary business with one or more other corporations must file a combined report, effective Jan. 1, 2009

• Ohio CAT – consolidated or combined reporting required

• Texas margin tax – taxable entities that are part of an affiliated group engaged in a unitary business must file a combined report

• Michigan – taxpayers are required to file based on a unitary combined reporting system, effective Jan. 1, 2008 (MBT) and effective Jan. 1, 2012 (corporate income tax)

• Massachusetts adopted combined reporting, effective Jan. 1, 2009.

• Wisconsin adopted combined reporting, effective for tax years beginning on or after Jan. 1, 2009.

• District of Columbia – applies to tax years beginning after Dec. 31, 2010

Slide 56

PwC

Combined Reporting Legislation: 2012 Activity

Alabama S.B. 333, indefinitely postponed 4/26/12

Florida S.B. 1590, died in committee 3/9/12

Kentucky H.B. 162, introduced 1/3/12 (repeal mandatory nexus consolidation enacted in 2005 – no activity since introduced)

Maryland H.B. 941, 2/10/12 (no action)

New Mexico S.B. 9, vetoed 3/6/12

Pennsylvania H.B. 2383, introduced 5/16/12

Virginia H.B. 1267 (postponed until 2013)

Slide 57

PwC

Combined Reporting Legislation: 2013 Activity (Cont.)

Alabama H.B. 203, pending committee action 2/7/13

Maryland H.B. 1246, failed

Montana S.B. 208, introduced 1/28/13 (repeal water’s-edge election), died in standing committee 4/24/13

New Mexico S.B. 13, introduced 1/15/13

Slide 58

PwC

Proposal: California

• On July 25, 2013, the California Franchise Tax Board will hold a public hearing regarding proposed modifications to California Code of Regulations Sect. 25106.5-1, specifically pertaining to the treatment of deferred inter-company stock accounts (DISAs).

• Proposed changes include:

• Reduction of a DISA through merger with a brother/sister corporation with basis

• Reduction of a DISA through subsequent capital contribution

• Treatment of a distribution through various tiers of stock ownership

• Does not currently address certain issues with respect to triggering a DISA, including a liquidation in a combined group

Slide 59

PwC

Proposal: Illinois

• On March 6, 2013, Illinois Gov. Pat Quinn proposed three corporate income tax changes:

• Suspending the foreign dividend deduction

• Decoupling from the federal domestic production activities deduction

• Suspending the non-combination rule for unitary members with different apportionment formulae

• That same day, Senate Bill 159 was amended to incorporate these three proposed changes, including repeal of the non-combination rule, which would be effective for tax years ending on or after Dec. 31, 2013.

Slide 60

PwC

Proposal: Massachusetts Gov. Patrick proposed budget, 1/23/13

• Switch to market-based sourcing for sales of other than tangible personal property (also in HB 3382)

• Adopt throw-out rule for sale of other than tangible personal property (also in HB 3382)

• Repeal of security and utility classifications (utility classification provision also in HB 3382)

• Repeal of FAS 109 deduction:

o The 2008 tax package established a deduction for any combined group that experienced an increase in the group’s net deferred tax liability as a result of the combined reporting requirements of unitary businesses. The deduction, which will be claimed over a seven-year period, was to take effect for tax years beginning in 2012.

o H.B. 4200 delayed the implementation of the deduction for one year, by allowing deductions to first be claimed in 2014.

Slide 61

PwC

Proposal: Minnesota S.B. 552 and FY 14-15 budget proposal

• Legislation provides that foreign operating corporations (FOCs) would no longer be excluded from filing a Minnesota return or from filing as members of a unitary group.

• Provisions regarding FOCs would be repealed, including the deemed dividend provision and the 80% royalty deduction (presumably because FOCs would file as members of a unitary group).

• Legislation would repeal the royalty deduction from any other foreign corporation (currently at 80%).

• The legislation would provide that income and apportionment factors of a foreign entity would flow to its unitary domestic owner, for purposes of calculating net income and apportionment factors of a unitary business, to the extent the income is included in federal taxable income.

• Adopts Finnigan for purposes of sourcing sales of the unitary group

Slide 62

PwC

Proposal: Montana

Montana S.B. 208

• Died April 24, 2013 in standing committee

• Would have (1) removed the taxpayer election to report as a water’s edge group, and (2) required worldwide combined reporting for a unitary group of taxpayers

• Water’s edge elections made prior to the bill’s effective date would have remained in effect until its three-year term expired.

Slide 63

PwC

Proposal: Pennsylvania

S.B. 882, 2013-2014 regular session

• Imposes mandatory combined reporting requirement

• Water’s edge treated as default classification; worldwide allowed upon election

• No guidance on Joyce/Finnigan contained within legislation

• Combined reporting effective for years beginning after Dec. 31, 2018

Slide 64

PwC

Proposal: Oregon

S.B. 310, referred to Finance and Revenue Committee 1/16/13

• Adopt Finnigan approach for apportionment

• Governor’s executive budget and A.B. 3009, S.B. 2609, introduced 1/22/13

S.B. 311, referred to Finance and Revenue Committee 1/16/13

• Adopt market-based sourcing for sales not involving tangible personal property

Slide 65