mapping the secondary resources in the eu (urban...

TRANSCRIPT

MSP-REFRAMCoordination and Support Actions (Coordinating) (CSA-CA)

Co-funded by the European Commission under theEuratom Research and Training Programme on Nuclear

Energy within the Seventh Framework ProgrammeGrant Agreement Number : 688993

Start date : 2015-12-01 Duration : 19 Months

Mapping the secondary resources in the EU (urban mines)

Authors : Mr. Witold KURYLAK (IMN) Ulla-Maija Mroueh (VTT), Susanna Casanovas (Amphos21); Rocio Barras Garcia andSantiago Cuesta (ICCRAM); Witold Kurylak, Katarzyna Leszczynska-Sejda (IMN)

MSP-REFRAM - D4.1 - Issued on 2016-05-11 16:08:25 by IMN

MSP-REFRAM - D4.1 - Issued on 2016-05-11 16:08:25 by IMN

MSP-REFRAM - Contract Number: 688993Multi-Stakeholder Platform for a Secure Supply of Refractory Metals in EuropeEC Scientific Officer: Stéphane Bourg (CEA)

Document title Mapping the secondary resources in the EU (urban mines)

Author(s)Mr. Witold KURYLAK; Ulla-Maija Mroueh (VTT), Susanna Casanovas (Amphos21); RocioBarras Garcia and Santiago Cuesta (ICCRAM); Witold Kurylak, Katarzyna Leszczynska-Sejda(IMN)

Number of pages 78

Document type Deliverable

Work Package WP4

Document number D4.1

Issued by IMN

Date of completion 2016-05-11 16:08:25

Dissemination level Public

Summary

Mapping the secondary resources in the EU (urban mines)

Approval

Date By

2016-05-11 16:09:29 Mr. Witold KURYLAK (IMN)

2016-05-11 17:26:06 Mr. BOURG STéPHANE (CEA)

MSP-REFRAM - D4.1 - Issued on 2016-05-11 16:08:25 by IMN

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 1

1. CONTENT

1. Content ........................................................................................................................1

1. Introduction .................................................................................................................5

1.1. Scope and objectives ................................................................................................5

1.2. Global Recycling rates of refractory metals...............................................................5

2. Mapping and Collection of Niobium containing end-OF-Life waste and scrap ..............8

2.1. Applications containing niobium ..............................................................................8

2.1.1. Steel products ...................................................................................................8

2.1.2. Superalloys ......................................................................................................10

2.1.3. Niobium-based Alloys ......................................................................................10

2.1.4. Fine Ceramics ..................................................................................................11

2.2. Nb in applications and end-of-life wastes ...............................................................12

2.3. End-of-life volymes of products and Nb in products ...............................................18

2.3.1. Waste electrical and electronic equipment, WEEE ...........................................18

2.3.2. End of life vehicles (EOL) .................................................................................21

2.4. Current fate of End-Of_life produts ........................................................................23

2.5. Methods of collection of the products ....................................................................25

2.6. Incentives for collection of the products.................................................................25

2.7. References .............................................................................................................26

3. Mapping and Collection of tantalum containing end-OF-Life waste and scrap ...........28

3.1. Introduction ...........................................................................................................28

3.2. Applications containing tantalum ...........................................................................28

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 2

3.2.1. Capacitors .......................................................................................................28

3.2.2. Estimated content and Form of Ta in capacitors ..............................................29

3.2.3. Other electronic components ..........................................................................30

3.2.4. Cemented carbides .........................................................................................30

3.2.5. Ta superalloys .................................................................................................30

3.2.6. Process equipment ..........................................................................................31

3.2.7. Medical applications........................................................................................31

3.2.8. Other applications ...........................................................................................31

3.3. Ta and Ta containing components in products And end-of-life waste .....................32

3.3.1. End-of-life volumes of Products and refractory metals in products .................37

3.4. Current fate of end-of-life products And manufacturing scrap ...............................39

3.4.1. WEEE ...............................................................................................................39

3.4.2. End-of-Life Vehicles .........................................................................................40

3.4.3. Other end-of-life applications ..........................................................................40

3.4.4. Recycling of manufacturing scrap ....................................................................41

3.5. Methods for Collection of the products ..................................................................41

3.5.1. ELV and WEEE .................................................................................................42

3.5.2. Other Ta containing End-of-Life products ........................................................42

3.6. Legislative and Economic Incentives .......................................................................43

3.6.1. ELV and WEEE collection .................................................................................43

3.7. References .............................................................................................................43

4. Mapping and collection of molybdenum containing End-of-Life waste and scrap ......46

4.1. Molybdenum containing products ..........................................................................46

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 3

4.1.1. Stainless steel ..................................................................................................47

4.1.2. Molybdenum grade Alloy Steels & Irons ..........................................................47

4.1.3. Molybdenum grade superalloys ......................................................................47

4.1.4. Molybdenum metal & alloys ............................................................................48

4.1.5. Chemical Uses Of Molybdenum .......................................................................48

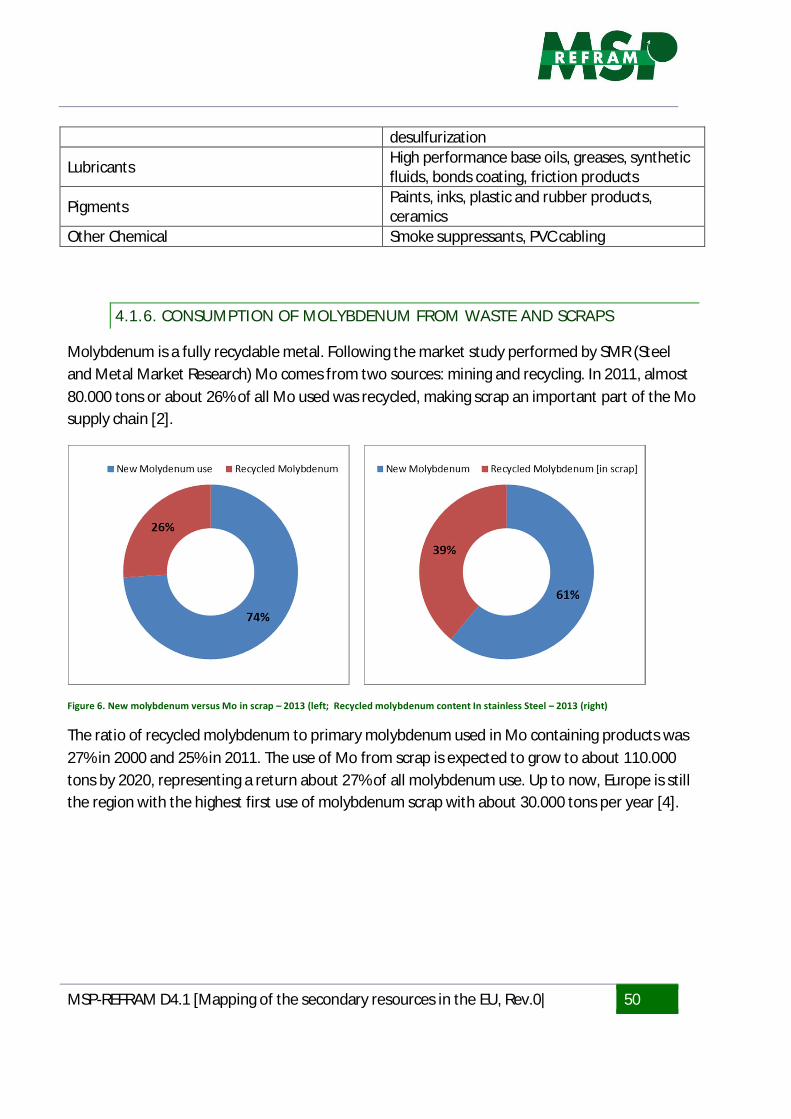

4.1.6. Consumption of Molybdenum from Waste and scraps ....................................50

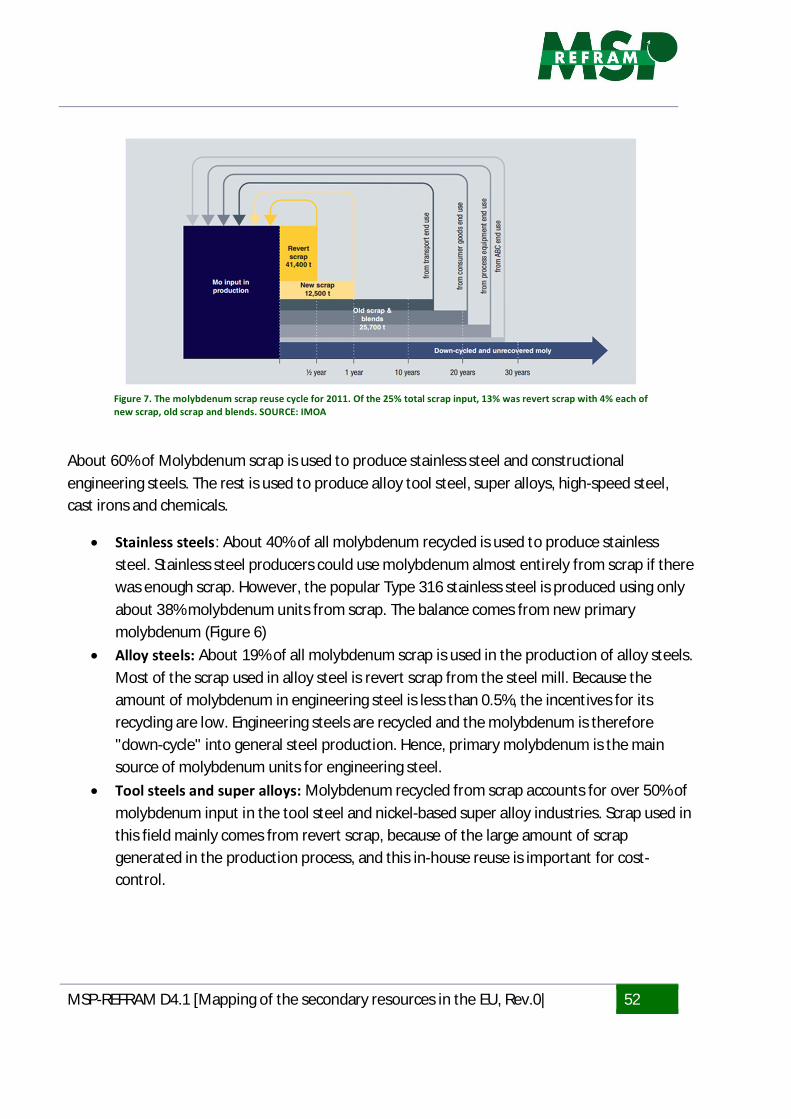

4.2. Recycling of Molybdenum from End oF-LIFE products and scraps ...........................51

4.2.1. Steel and alloy scraps ......................................................................................51

4.2.2. Spent Ni-Mo catalyst .......................................................................................57

4.2.3. Other wastes ...................................................................................................57

4.3. Quantities of Mo containing waste and scrap .........................................................57

4.3.1. End-Of-life vehicles .........................................................................................59

4.4. REFERENCES ...........................................................................................................59

5. Mapping and collection of RHENIum containing End-of-Life waste and scrap ............61

5.1. Introduction ...........................................................................................................61

5.2. Applications containing rhenium ............................................................................61

5.2.1. development of the use of rhenium ................................................................61

5.2.2. Current status of Re consumption ...................................................................62

5.3. Recycling of Re .......................................................................................................66

5.4. References .............................................................................................................67

6. Mapping and collection of Tungsten containing End-of-Life waste and scrap .............68

6.1. applications of tungsten .........................................................................................68

6.1.1. Tungsten life-cycle...........................................................................................69

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 4

6.1. tungsten end-of-life products and manufacturing waste ........................................70

6.1.1. Spent Ni-W catalyst. ........................................................................................70

6.1.2. Other W bearing wastes ..................................................................................70

6.2. Collection and recycling of tungsten scrap ..............................................................73

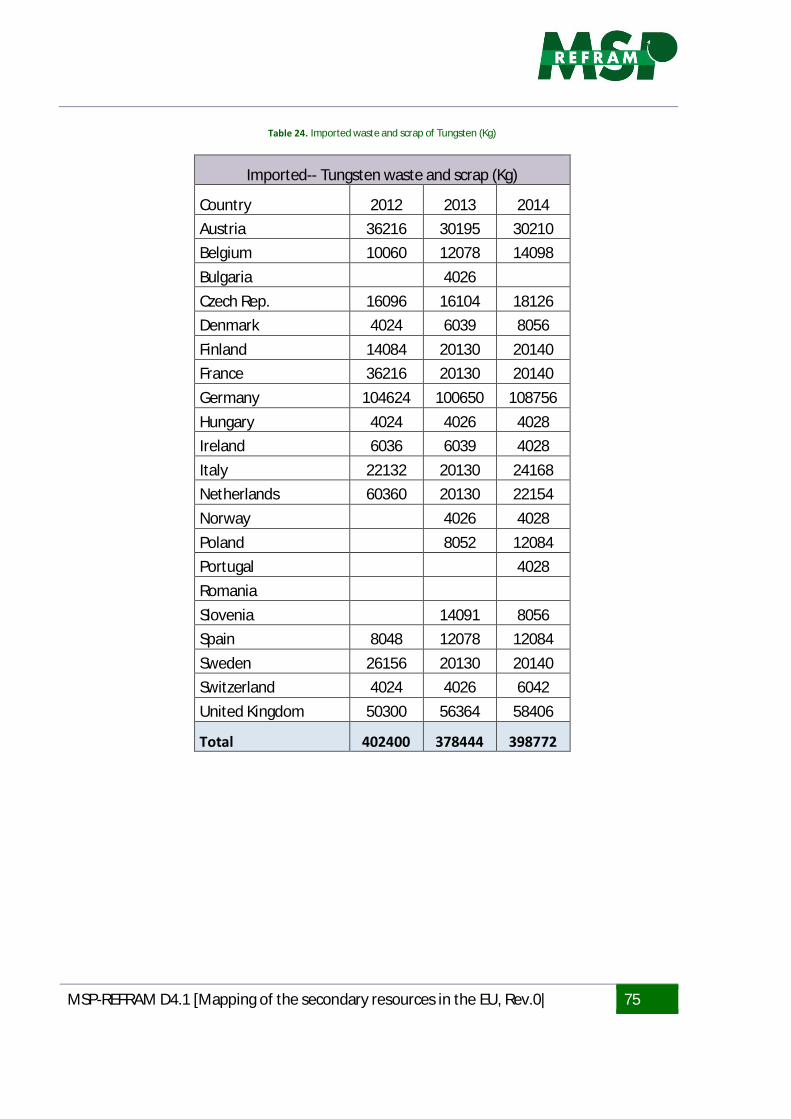

6.3. Rererences .............................................................................................................76

7. SUmmary - Knowledge gaps .......................................................................................77

The deliverable has been prepared by Susanna Casanovas, Amphos21; Rocio Barras Garciaand Santiago Cuesta, ICCRAM; Witold Kurylak, IMN and Ulla-Maija Mroueh, VTT

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 5

MSP-REFRAMD411 MAPPING THE SECONDARYRESOURCES IN THE EUUlla-Maija Mroueh, VTT, Susanna Casanovas, Amphos21; Rocio Barras Garcia and SantiagoCuesta, ICCRAM; Witold Kurylak, IMN

1. INTRODUCTION

1.1.SCOPE AND OBJECTIVES

This report is a part of the European project Multi-Stakeholder Platform for a Secure Supplyof Refractory Metals, MSP-REFRAM. The project aims for providing key information at policy,technical and market level to stakeholders along the refractory metals (molybdenum,niobium, tantalum, tungsten and rhenium) value chain in order to strengthen Europeanmarket as well as establishing a multi-stakeholder platform supporting the refractory metalssector in Europe.

These highly strategic resources are mainly imported to Europe as metals or in products andproduct components because the primary production is very limited. Therefore it would beimportant to map and valorise better the secondary resources which exist in Europe. Theaim of this report is to identify the end-of-life waste products (urban mine) and theircomponents containing refractory metals, estimate their quantities and form in the productsin the limits of the available data, to identify the existing collection infrastructures and theincentives for delivery of waste products to legal operators.

1.2.GLOBAL RECYCLING RATES OF REFRACTORY METALS

Graedel et al. [1] propose various recycling metrics to estimate global end-of life recyclingrates. Figure 1 illustrates a simplified metal and production life cycle.

The different types of recycling are related to the type of scrap and its treatment:

· Home scrap: generated during material production or during fabrication ormanufacturing that can be directly reinserted in the process

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 6

· New scrap: generated during fabrication and manufacturing but it is not recycledwith the same facility but rather is transfer to the scrap market.

· Old scrap: metal in products that has reached their end of life.· Functional recycling: portion of end of life recycling in which the metal in a discarded

product is separated and sorted to obtain recycles that are returned to raw materialproduction process that generate metal or metal alloy.

· Nonfunctional recycling: portion of end of life recycling in which the metal iscollected as old metal scrap and incorporated in an associated large-magnitudematerial stream as a tramp or impurity elements.

· Losses occur when metal is not completely captured through any of the recyclingstream mentioned.

Figure 1. The life cycle of a metal

At end of life, the recycling efficiency of a metal can be measured at three levels [1]:

1. Old scrap collection rate (CR)2. Functional recycling (EOL-RR: End-of life – Recycling Rate)3. Old scrap in the recycling flow (OSR)

A summary of the recycling rates of the refractory metals Mo, W, Ta, Nb and Re is presentedin the Table 1.

Table 1. Recycling rates of refractory metals [1]

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 7

Refractory Metal FunctionalRecycling

Old Scrapcollection rate

Old scrap in therecycling flow

Mo >25-50% >25-50 >25-50Nb >50 >50 >25-50Re >50 >10-25 >25-50W >10-25 >25-50 >50Ta <1 >10-25 >1-10

The study of Graedel et al. provides additionally different ranges of recycling rates usingdifferent methods found in the literature. These results are presented in the table below:

Table 2. Recycling rates of refractory metals using different methodologies

Refractory Metal FunctionalRecycling

Old Scrapcollection rate

Old scrap in therecycling flow

Mo 301 331 332, 671

Nb 503, 562 223 442, 563

Re >50 10-50 50W 10-25,664 464 804

Ta <1, 355 10-25, 215 1-10, 435

1. J. W. Blosson, Molybdenum recycling in the United States in 1998, USGS Circular 119-L.

2. Working group consensus3. L.D. Cunningham, 2004a. Columbium (niobium) recycling in the United States in

1998, USGS Circular 1196-I4. K.B. Shedd. Tungsten recycling in the United States in 2000, USGS Open File Report

IFR-2005-1028 (2005)5. L.D. Cunningham, 2004b. Tantalum recycling in the United States in 1998, USGS

Circular 1196-Z

[1] T. E. Graedel, J. Allwood, J. Birat, M. Buchert, C. Hagelüken, B. K. Reck, S.F... Sibley, G.Sonnenmann. 2011. Journal of Industrial Ecology 15 (3), 355-366.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 8

2. MAPPING AND COLLECTION OF NIOBIUM CONTAINING END-OF-LIFE WASTEAND SCRAP

2.1.APPLICATIONS CONTAINING NIOBIUM

The unique properties of niobium make it a vital component in a diverse range ofapplications and products, e.g.: superconductivity, corrosion-resistance, very high meltingtemperatures, shape memory properties, high coefficient of capacitance and bio-compatibility (BGS, 2011).

The most important application for niobium (89% of total production) is as an alloyingelement to strengthen high-strength-low-alloy steels used to build automobiles and high-pressure gas transmission pipelines. The major niobium engineering alloys produced areFerro niobium, nickel-niobium and niobium metal and oxide. Ferro niobium is usedworldwide as an alloying component in steels for vehicles. High-purity Ferro niobium andnickel niobium are used in nickel-, cobalt-, and iron based superalloys for applications suchas jet engine components, rocket subassemblies, and heat-resistant equipment.

The remaining 11% of total production is utilized in superconducting niobium-titanium alloysused for building and Magnetic Resonance Imagery (MRI) and other minor applications.These include, in oxide form, electronic ceramics and camera lenses because niobiumincreases the refraction index. Electronic components include frequency filters made of theone crystal quality of Nb2O5 and anti-reflex layers in form of sputtering targets (CBMM, HCStarck).

The following sections describe main applications of niobium in its different forms, itsproperties or technical attributes and the final components/products where niobium iscontained. The identification of products containing niobium will enable the identification ofthe corresponding end of life (EOL) products and waste streams where niobium may bepresent (BGS 2011, CBMM, H.C. Starck):

2.1.1. STEEL PRODUCTS

In the steel industry, niobium is added in the form of ferro niobium and finds its principalapplication in microalloyed steel products (steels containing small additions of Nb, Ti or V,usually less than 0.10 wt.-%), and stainless steels.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 9

The easiest way to increase the strength of steel is to increase its carbon content. Thistraditional expedient, however, also deteriorates other desirable properties such asweldability, toughness and formability. Microalloying with niobium, vanadium or titanium inamounts below 0.10 wt. % is an alternative method for enhancing the strength of steel whilestill preserving acceptable secondary properties.

Flat products

Niobium microalloyed high strength steel plates are used in a variety of applications. Largediameter line pipe for the transmission of gas (and oil) is the most important item producedfrom plate. Gas transmission line pipe requires a high level of strength to contain the high-pressure gas as well as acceptable toughness to prevent propagation of a long fracture in theevent that external forces (such as an earthquake) initiate a fracture. This is especiallyimportant where "rich" gas is involved. Good weldability is also needed to allow for easyfabrication of a transmission system.

Long products

Long products are steel products such as bars, sections or wire rod. All these products can beproduced in higher strength grades using niobium. Structural sections (e.g. angles, beams)are widely used in civil construction, railway wagons, transmission towers, etc.

Stainless steels

Ferritic stainless steels with niobium can withstand the higher temperatures that areessential for optimal catalytic efficiency in modern exhaust systems. Temperatures up to 950ºC in the manifold are fundamental for the catalytic system to convert carbon monoxide intocarbon dioxide and to reduce the level of nitrogen oxide and sulphur oxide in the emissions.Niobium helps reduce emissions of vehicle greenhouse gases by making catalytic conversionmore efficient.

Ferritic stainless steels with niobium are also used in a variety of new applications, such asbuilding roofs and facades, solar water heaters and potable water pipes.

Other iron and steel products

Other miscellaneous products using niobium include seamless pipe, tool steel, cast iron andsteel castings. High strength niobium microalloyed grades are used in oil and gas well drillingoperations (drill pipe and well casing).

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 10

A variety of alternative cutting tool materials, such as niobium carbides, have been recentlydeveloped as well. Tool steels are still the most important machining devices, which rely on avariety of alloying elements to develop cutting capability. The addition of niobium to formhard niobium carbides upgrades the performance of tool steels. Some tool steelcompositions are being used to manufacture other items such as rolling mill rolls and hard-facing electrodes.

The use of niobium in cast iron is a relatively new technology. The most significantapplications are in automotive cylinder heads, piston rings and truck brakes. The formationof very hard carbides (good for wear resistance) and the modification of graphite cell size aretwo of niobium's attributes in this application.

Steel castings use niobium as a microalloy, for good combination of strength and toughness.Several new applications have been developed, such as ingot moulds, slag pots, rolling millback-up rolls, nodes for offshore platforms and machinery components.

2.1.2. SUPERALLOYS

The so-called superalloys are materials designed to function for extended periods in highlyoxidizing and corrosive atmospheres at temperature above 650°C. Superalloys represent thesecond largest use of niobium outside the steel industry.

There are scores of different superalloys used in a variety of high temperature or corrosiveenvironments. However, the single most important member of the class is Inconel 718, anickel-based alloy containing 5.3-5.5 wt.-% niobium. This alloy forms the backbone ofcommercial and military jet engine manufacture. The most common jet engine in servicetoday, the CFM56 made by the GE/Snecma joint venture, contains about 300 kilos ofniobium. Other industrially important nickel-based alloys containing niobium are Inconel 706(3 wt.-% Nb) and Inconel 625 (3.5 wt.-% Nb).

Alloy 718 was initially developed as a disk material for aircraft gas turbines even though itsuses have expanded over recent years to include other engine parts such as bolts, fastenersand rotor shafts. Further uses for this remarkable alloy have also been found in otherindustries such as nuclear, cryogenics and petrochemicals. Land based turbines for electricitygeneration are becoming increasingly important as the efficiencies of these machines arebeing increased to acceptable levels (56-58%) by increasing operating temperatures.

2.1.3. NIOBIUM-BASED ALLOYS

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 11

Alloying niobium with other elements such as titanium, zirconium, hafnium, tantalum,tungsten and other metals produces materials with highly desirable engineering properties.

Niobium itself has long being known to exhibit superconductivity (the loss of all electricalresistivity, below a critical temperature near absolute zero). Although pure niobium findsapplication in microwave cavities used in particle accelerators, the most importantsuperconductor materials are niobium-titanium and niobium-tin.

Magnetic Resonance Imaging (MRI) used in medical diagnostics, and Nuclear MagneticResonance used in spectrographic (analytical) applications, are the two commercialapplications for niobium as a superconductor material.

Niobium-based alloys are also used as refractory materials for aerospace applications sincethey have excellent high temperature strength above 1,300°C and readily accept coatings toprotect against oxidation. The most important alloy in this case is called C-103 (a niobium-hafnium-titanium alloy) used mainly in rocket thrusters and rocket nozzles.

Niobium-1% zirconium alloy is used as a precision support member in high-efficiency andhigh-intensity sodium vapour street lamps. These tiny components require a material withhigh hot strength and superior formability which must be resistant to corrosion from sodiumvapour.

Niobium is also used in heavy water nuclear reactors of the CANDU (Canada DeuteriumUranium) type in a Zirconium-2.5% niobium alloy. This alloy's high strength permits the useof thin wall sections, allowing better neutron economy. Another application is in nuclearreactors for submarines.

2.1.4. FINE CERAMICS

High purity niobium oxide is being used in the manufacture of fine ceramics. These specialmaterials are generally classified as being either functional or structural (engineering)materials. The former category includes ceramic capacitors for electronics and optical lenses.The latter group consists of heat resistant and abrasion resistant materials, tools, engineparts and other structural articles. Industrial applications of functional materials haveadvanced far ahead of structural materials.

The world demand for niobium oxide in functional ceramics is mainly for optical lenses andceramic condensers and actuators. The balance is very high purity 99.99% Nb2O5 which isused to produce lithium niobate single crystals for application in surface acoustic wave(SAW) devices for TV receivers.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 12

2.2.NB IN APPLICATIONS AND END-OF-LIFE WASTES

Table 3 summarizes main applications of niobium in its different forms, the finalcomponents/products where niobium is contained, the estimated content (where available)and the corresponding End of Life (EoL) products/waste streams where niobium could betraced.

Few references have been identified regarding the content of niobium in EOL products suchas WEEE or ELV. As described in section Error! Reference source not found., niobium-steelalloys, super alloys magnets and capacitors containing niobium are used in electric andelectronic equipment. According to UNEP, 2013, a computer can contain 0.0002% ofniobium in welding alloy and housing.

The recovery of Au, Ag, Cu and Nb from PCBs (printed circuit boards) of discarded computersusing leaching column technique is described by Montero, 2012 as the PCBs (printed circuitboards) are the components in electronic waste where the precious metals concentrationsare higher. The amount of Au, Ag, Nb and Cu found in used PCBs were: Au 613 g/t, Ag 1,515g/t, Nb 36 g/t and Cu 23.4%.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 13

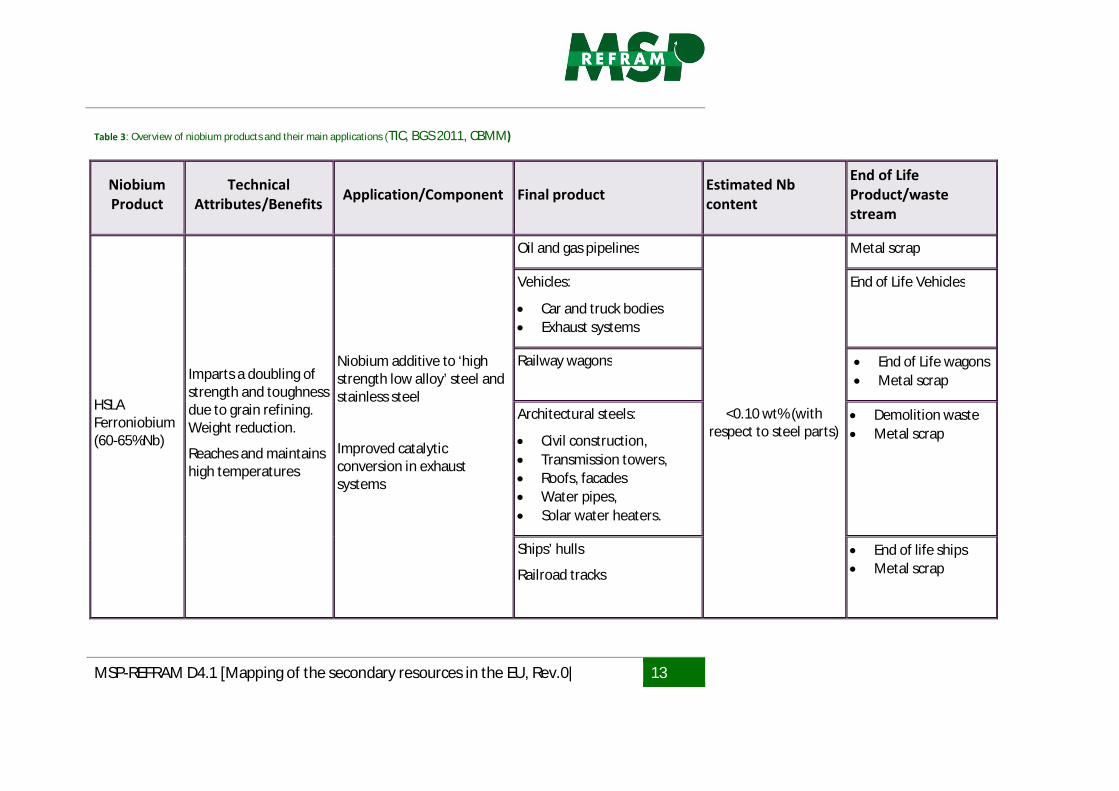

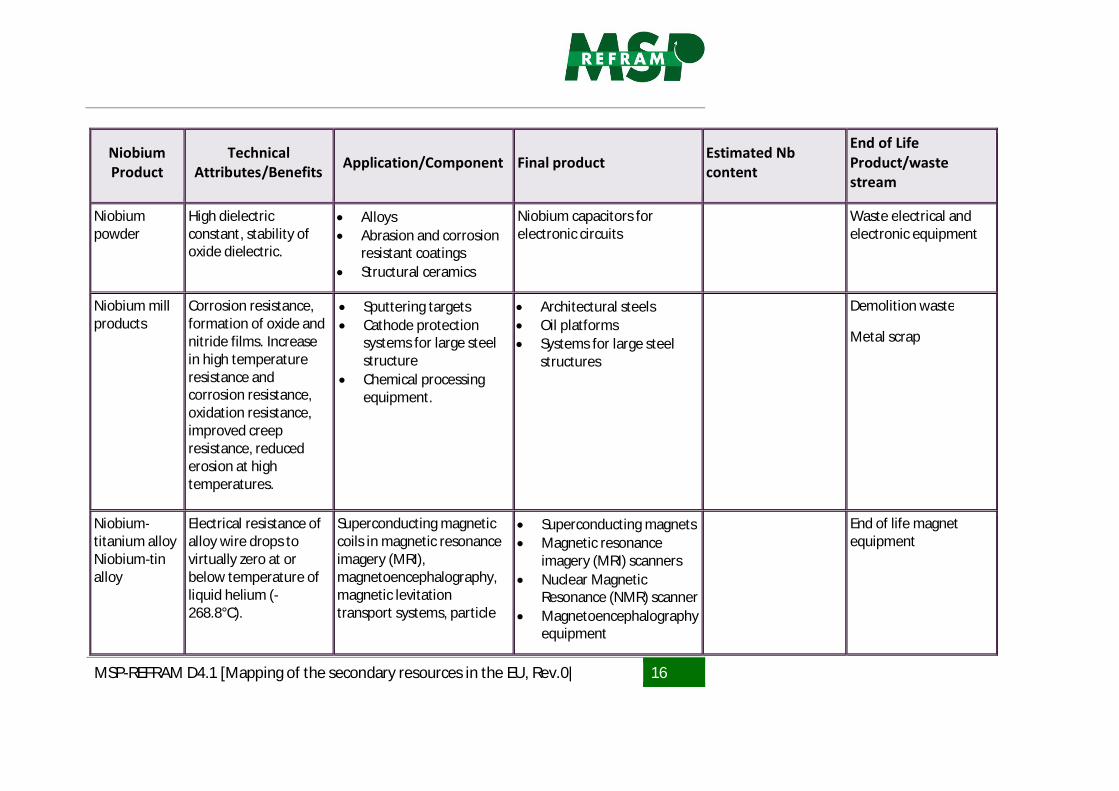

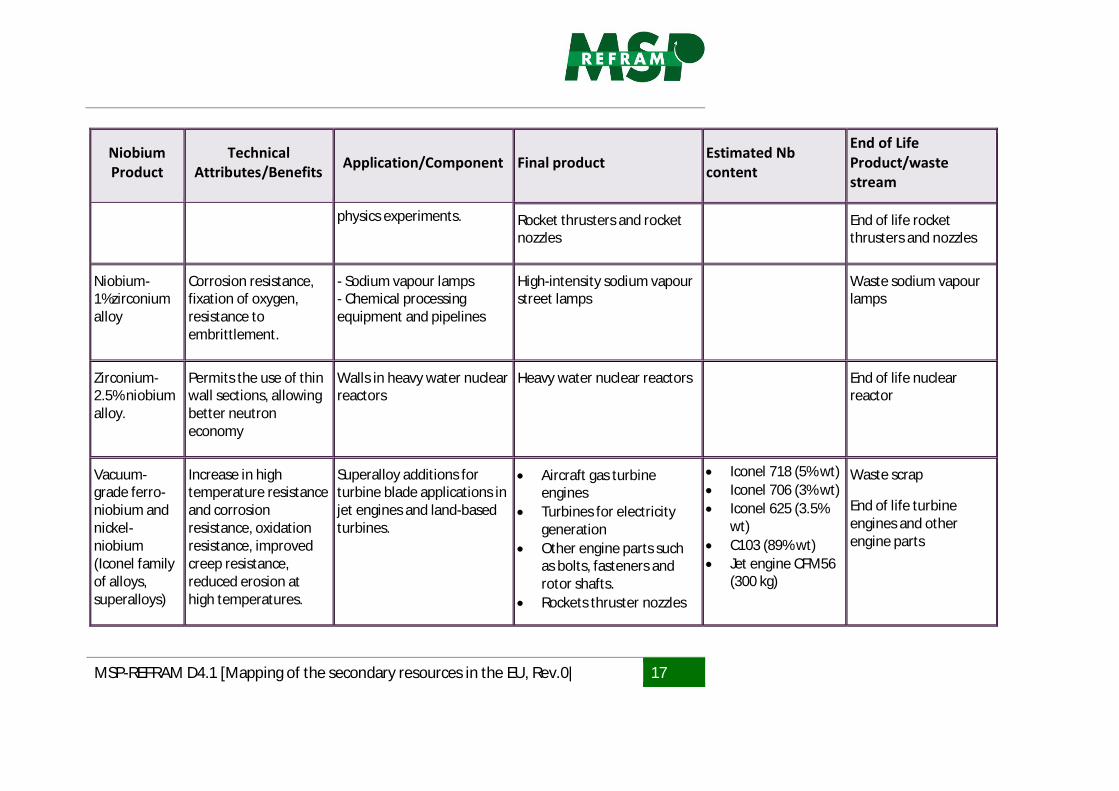

Table 3: Overview of niobium products and their main applications (TIC, BGS 2011, CBMM)

NiobiumProduct

TechnicalAttributes/Benefits Application/Component Final product Estimated Nb

content

End of LifeProduct/wastestream

HSLAFerroniobium(60-65%Nb)

Imparts a doubling ofstrength and toughnessdue to grain refining.Weight reduction.

Reaches and maintainshigh temperatures

Niobium additive to ‘highstrength low alloy’ steel andstainless steel

Improved catalyticconversion in exhaustsystems

Oil and gas pipelines

<0.10 wt% (withrespect to steel parts)

Metal scrap

Vehicles:

· Car and truck bodies· Exhaust systems

End of Life Vehicles

Railway wagons · End of Life wagons· Metal scrap

Architectural steels:

· Civil construction,· Transmission towers,· Roofs, facades· Water pipes,· Solar water heaters.

· Demolition waste· Metal scrap

Ships’ hulls

Railroad tracks

· End of life ships· Metal scrap

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 14

NiobiumProduct

TechnicalAttributes/Benefits Application/Component Final product Estimated Nb

content

End of LifeProduct/wastestream

Niobium incast iron

Good for wearresistance

Formation of very hardcarbides

Automotive cylinder heads,piston rings and truck brakes

Vehicles End of Life Vehicles

Niobium insteel castings

Good combination ofstrength and toughness

· Ingot moulds· slag pots· rolling mill back-up rolls· nodes for offshore

platforms· machinery components

Metal scrap

Niobiumoxide

· High index ofrefraction

· High dielectricconstant.

· Increase lighttransmittance.

Speciality glasses andstructural ceramics:

· Camera and eyeglasslenses

· Coating on glass forscreens

· Ceramic for capacitorsand high performancebearings.

· Cameras,· Computer screens,· TV receivers

0,0002% in computers(weldingalloy/housing)

Waste electrical andelectronic equipment:

· Cameras,· Computers· TVs· Printed circuit

boards

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 15

NiobiumProduct

TechnicalAttributes/Benefits Application/Component Final product Estimated Nb

content

End of LifeProduct/wastestream

Lithiumniobate

Optical, pyroelectricand piezoelectricproperties

Electronic components:

· Surface acoustic wave(SAW) filters devices.

· Ceramic for capacitors

· Mobile phones· Motion detectors· Laser switching devices· Touch screen

technologies

Waste electrical andelectronic equipment:

· Mobile phones· Touch screens· Laser devices

Niobiumnitride

Superconductivity Components ofsuperconducting magnets

Magnetic resonance imagery(MRI) scanners

End of life MRIscanners

Niobiumcarbide

High temperaturedeformation, controlsgrain growth.

Refractory ceramicsubstances used in highstress, high temperatureapplications.

· Industrial high speedcutting and boring tools.

· Teeth for excavatorbuckets

· Drill bits for the miningindustry

· EoL industrialcutting tools

· EoL teeth ofexcavators

· EoL drill bits

Increases strength andimproves wearresistance, increasingthe life of tool cuttingedged.

Surfaces of tool cuttingedges. Nb is applied usingchemical vapour deposition(CVD) or physical vapourdeposition (PVD).

Industrial cutting tools End of life industrialcutting tools

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 16

NiobiumProduct

TechnicalAttributes/Benefits Application/Component Final product Estimated Nb

content

End of LifeProduct/wastestream

Niobiumpowder

High dielectricconstant, stability ofoxide dielectric.

· Alloys· Abrasion and corrosion

resistant coatings· Structural ceramics

Niobium capacitors forelectronic circuits

Waste electrical andelectronic equipment

Niobium millproducts

Corrosion resistance,formation of oxide andnitride films. Increasein high temperatureresistance andcorrosion resistance,oxidation resistance,improved creepresistance, reducederosion at hightemperatures.

· Sputtering targets· Cathode protection

systems for large steelstructure

· Chemical processingequipment.

· Architectural steels· Oil platforms· Systems for large steel

structures

Demolition waste

Metal scrap

Niobium-titanium alloyNiobium-tinalloy

Electrical resistance ofalloy wire drops tovirtually zero at orbelow temperature ofliquid helium (-268.8°C).

Superconducting magneticcoils in magnetic resonanceimagery (MRI),magnetoencephalography,magnetic levitationtransport systems, particle

· Superconducting magnets· Magnetic resonance

imagery (MRI) scanners· Nuclear Magnetic

Resonance (NMR) scanner· Magnetoencephalography

equipment

End of life magnetequipment

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 17

NiobiumProduct

TechnicalAttributes/Benefits Application/Component Final product Estimated Nb

content

End of LifeProduct/wastestream

physics experiments. Rocket thrusters and rocketnozzles

End of life rocketthrusters and nozzles

Niobium-1%zirconiumalloy

Corrosion resistance,fixation of oxygen,resistance toembrittlement.

- Sodium vapour lamps- Chemical processingequipment and pipelines

High-intensity sodium vapourstreet lamps

Waste sodium vapourlamps

Zirconium-2.5% niobiumalloy.

Permits the use of thinwall sections, allowingbetter neutroneconomy

Walls in heavy water nuclearreactors

Heavy water nuclear reactors End of life nuclearreactor

Vacuum-grade ferro-niobium andnickel-niobium(Iconel familyof alloys,superalloys)

Increase in hightemperature resistanceand corrosionresistance, oxidationresistance, improvedcreep resistance,reduced erosion athigh temperatures.

Superalloy additions forturbine blade applications injet engines and land-basedturbines.

· Aircraft gas turbineengines

· Turbines for electricitygeneration

· Other engine parts suchas bolts, fasteners androtor shafts.

· Rockets thruster nozzles

· Iconel 718 (5% wt)· Iconel 706 (3% wt)· Iconel 625 (3.5%

wt)· C103 (89% wt)· Jet engine CFM56

(300 kg)

Waste scrap

End of life turbineengines and otherengine parts

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 18

2.3.END-OF-LIFE VOLUMES OF PRODUCTS AND NB IN PRODUCTS

Niobium is recycled when niobium-bearing steels and superalloys are recycled at industrial scalebut waste recovery specifically for niobium content is generally negligible. Though the amount ofniobium recycled may be as much as 20% of apparent consumption (BGS, 2011), the amount ofniobium recovered from other sources, e.g. end of life products, is minor.

As described in sections Error! Reference source not found. and Error! Reference source notfound., niobium is used in final products such as electrical and electronic equipment (includinglighting equipment) and vehicles; however, few references have been identified regarding thecontent of niobium in such products.

Niobium is recycled when niobium-bearing steels and superalloys are recycled at industrial scalebut waste recovery specifically for niobium content is generally negligible. Though the amount ofniobium recycled may be as much as 20% of apparent consumption (BGS, 2011), the amount ofniobium recovered from other sources, e.g. end of life products, is minor.

As described in sections Error! Reference source not found. and Error! Reference source notfound., niobium is used in final products such as electrical and electronic equipment (includinglighting equipment) and vehicles; however, few references have been identified regarding thecontent of niobium in such products.

The following sections describe the volumes of WEEE and ELV generated in the EU, which maycontain niobium.

2.3.1. WASTE ELECTRICAL AND ELECTRONIC EQUIPMENT, WEEE

Waste electrical and electronic equipment (WEEE) is currently considered to be one of thefastest growing waste streams in the EU, growing at 3-5 % per year. The recycling of WEEE offerssubstantial opportunities in terms of making secondary raw materials such as refractory metalsavailable on the market. The revised WEEE directive promoting the collection and recycling ofsuch equipment (Directive 2012/19/EU) entered into force on 13 August 2012 and becameeffective on 14 February 2014. The legislation provides for the creation of collection schemeswhere consumers return their used waste equipment free of charge, with the aim to increasethe recycling rates and/or re-use of WEEE.

Although niobium, among other critical metals, is not recovered from such waste streams atpresent, the trends in the amount of EEE put on the market and of WEEE collected and treatedfor the EU in the period from 2007–12 contribute to the estimation of the volume of end-of-lifeproducts potentially containing niobium in the EU.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 19

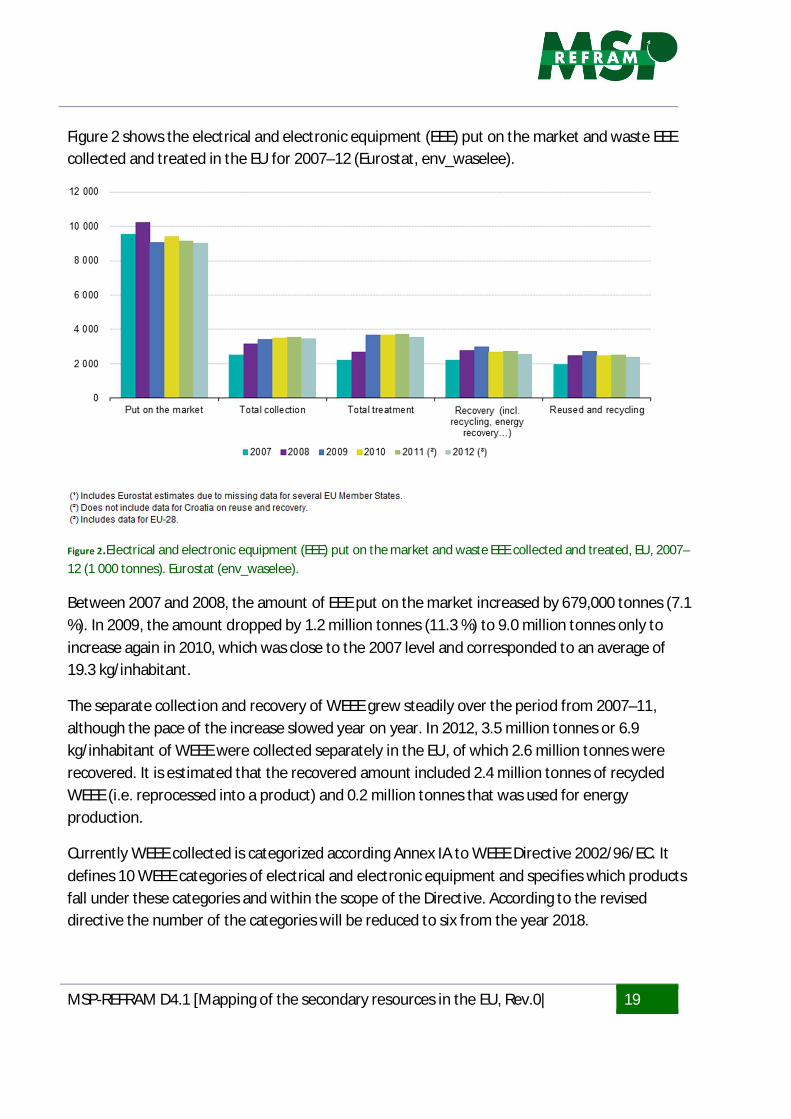

Figure 2 shows the electrical and electronic equipment (EEE) put on the market and waste EEEcollected and treated in the EU for 2007–12 (Eurostat, env_waselee).

Figure 2.Electrical and electronic equipment (EEE) put on the market and waste EEE collected and treated, EU, 2007–12 (1 000 tonnes). Eurostat (env_waselee).

Between 2007 and 2008, the amount of EEE put on the market increased by 679,000 tonnes (7.1%). In 2009, the amount dropped by 1.2 million tonnes (11.3 %) to 9.0 million tonnes only toincrease again in 2010, which was close to the 2007 level and corresponded to an average of19.3 kg/inhabitant.

The separate collection and recovery of WEEE grew steadily over the period from 2007–11,although the pace of the increase slowed year on year. In 2012, 3.5 million tonnes or 6.9kg/inhabitant of WEEE were collected separately in the EU, of which 2.6 million tonnes wererecovered. It is estimated that the recovered amount included 2.4 million tonnes of recycledWEEE (i.e. reprocessed into a product) and 0.2 million tonnes that was used for energyproduction.

Currently WEEE collected is categorized according Annex IA to WEEE Directive 2002/96/EC. Itdefines 10 WEEE categories of electrical and electronic equipment and specifies which productsfall under these categories and within the scope of the Directive. According to the reviseddirective the number of the categories will be reduced to six from the year 2018.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 20

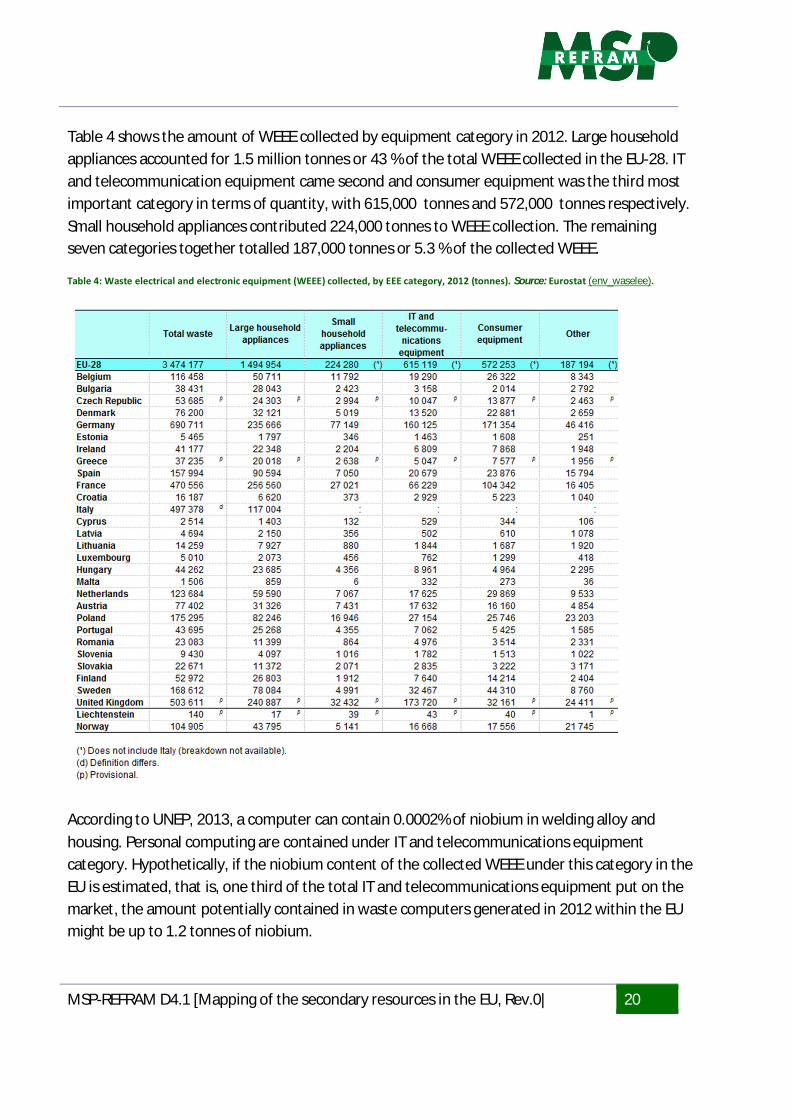

Table 4 shows the amount of WEEE collected by equipment category in 2012. Large householdappliances accounted for 1.5 million tonnes or 43 % of the total WEEE collected in the EU-28. ITand telecommunication equipment came second and consumer equipment was the third mostimportant category in terms of quantity, with 615,000 tonnes and 572,000 tonnes respectively.Small household appliances contributed 224,000 tonnes to WEEE collection. The remainingseven categories together totalled 187,000 tonnes or 5.3 % of the collected WEEE.

Table 4: Waste electrical and electronic equipment (WEEE) collected, by EEE category, 2012 (tonnes). Source: Eurostat (env_waselee).

According to UNEP, 2013, a computer can contain 0.0002% of niobium in welding alloy andhousing. Personal computing are contained under IT and telecommunications equipmentcategory. Hypothetically, if the niobium content of the collected WEEE under this category in theEU is estimated, that is, one third of the total IT and telecommunications equipment put on themarket, the amount potentially contained in waste computers generated in 2012 within the EUmight be up to 1.2 tonnes of niobium.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 21

2.3.2. END OF LIFE VEHICLES (EOL)

No references on content or recyclability rates of niobium in end of life vehicles have beenidentified, however, information gathered annually from EU Member States and other countrieson the total vehicle weight, the total number of end-of-life vehicles and rates for ‘total reuse andrecycling’ since 2006 have been extracted from Eurostat.

Table 5 shows the total number of end-of-life vehicles reported in the EU-27, the major amountof end-of-life vehicles reported is in 2009 - 9.0 million -, however, it is far from the expected totalnumber forecasted by ETC/RWM, up to 14 million end-of-life vehicles (passenger cars) in 2010.

Table 5: Total number of end-of-life vehicles reported in the EU-27 (2006-20112). Source: Eurostat.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 22

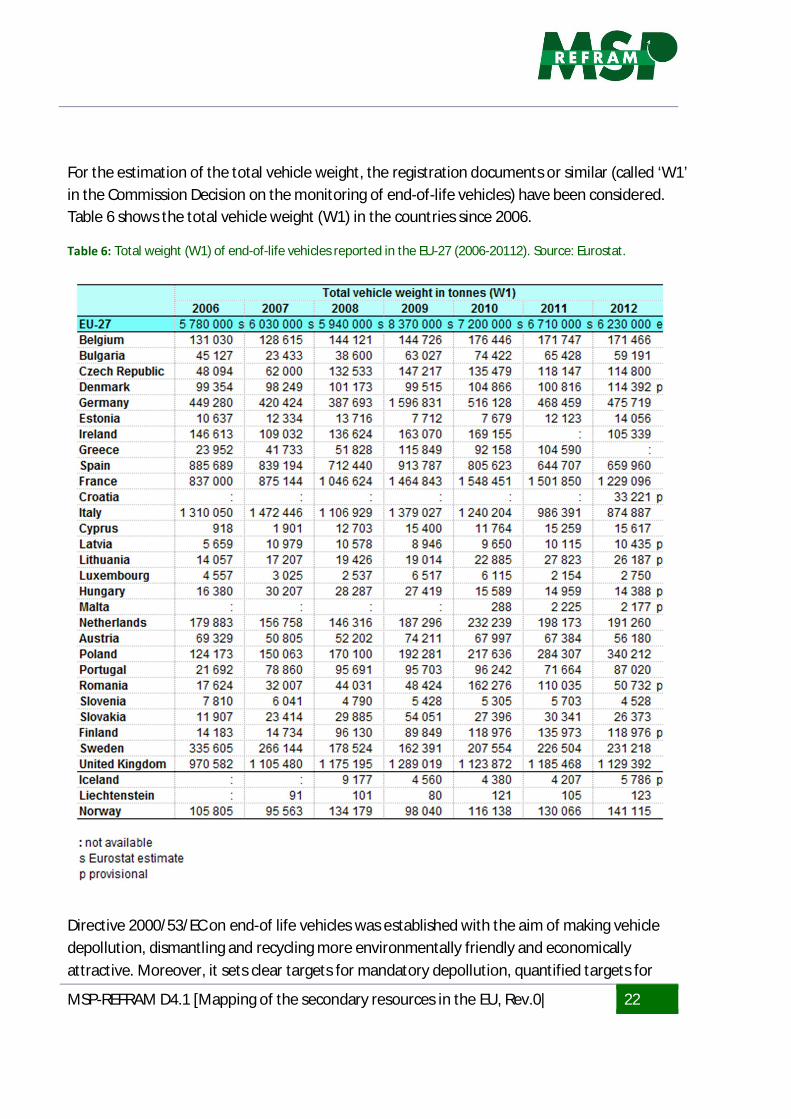

For the estimation of the total vehicle weight, the registration documents or similar (called ‘W1’in the Commission Decision on the monitoring of end-of-life vehicles) have been considered.Table 6 shows the total vehicle weight (W1) in the countries since 2006.

Table 6: Total weight (W1) of end-of-life vehicles reported in the EU-27 (2006-20112). Source: Eurostat.

Directive 2000/53/EC on end-of life vehicles was established with the aim of making vehicledepollution, dismantling and recycling more environmentally friendly and economicallyattractive. Moreover, it sets clear targets for mandatory depollution, quantified targets for

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 23

reuse, recycling and recovery of vehicles and their components, and pushes producers tomanufacture new vehicles with a view to their recyclability. The Directive also provides theopportunity for producers / importers to bear the expenditure of end-of-life treatment when theprocesses necessary to meet the established targets are not economically viable.

No later than 2006, the countries were required to meet rates for reuse + recycling of ≥ 80 % andfor reuse + recovery of ≥ 85 %. The reported rates in Table 7 show that most countries compliedwith the required rates.

Table 7. Total recycling and reuse rate of ELV in percent in the EU-27 (2006-20112). Source: Eurostat.

2.4.CURRENT FATE OF END-OF_LIFE PRODUTS

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 24

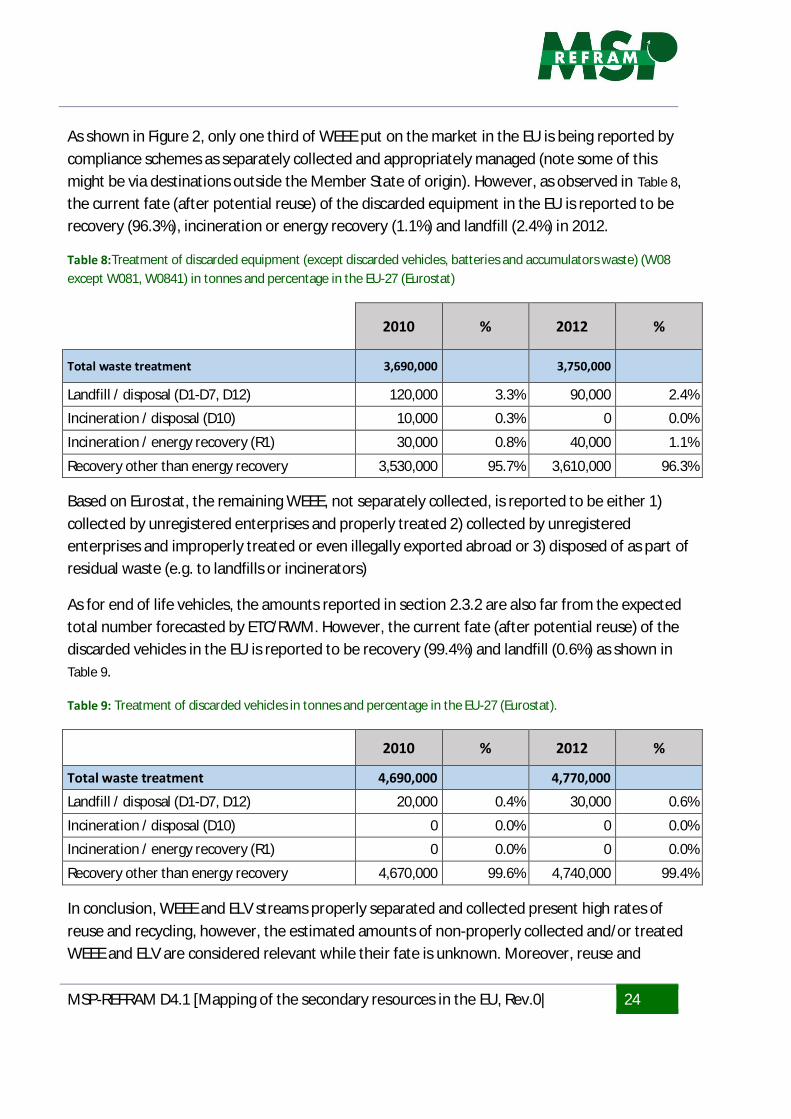

As shown in Figure 2, only one third of WEEE put on the market in the EU is being reported bycompliance schemes as separately collected and appropriately managed (note some of thismight be via destinations outside the Member State of origin). However, as observed in Table 8,the current fate (after potential reuse) of the discarded equipment in the EU is reported to berecovery (96.3%), incineration or energy recovery (1.1%) and landfill (2.4%) in 2012.

Table 8:Treatment of discarded equipment (except discarded vehicles, batteries and accumulators waste) (W08except W081, W0841) in tonnes and percentage in the EU-27 (Eurostat)

2010 % 2012 %

Total waste treatment 3,690,000 3,750,000

Landfill / disposal (D1-D7, D12) 120,000 3.3% 90,000 2.4%

Incineration / disposal (D10) 10,000 0.3% 0 0.0%

Incineration / energy recovery (R1) 30,000 0.8% 40,000 1.1%

Recovery other than energy recovery 3,530,000 95.7% 3,610,000 96.3%

Based on Eurostat, the remaining WEEE, not separately collected, is reported to be either 1)collected by unregistered enterprises and properly treated 2) collected by unregisteredenterprises and improperly treated or even illegally exported abroad or 3) disposed of as part ofresidual waste (e.g. to landfills or incinerators)

As for end of life vehicles, the amounts reported in section 2.3.2 are also far from the expectedtotal number forecasted by ETC/RWM. However, the current fate (after potential reuse) of thediscarded vehicles in the EU is reported to be recovery (99.4%) and landfill (0.6%) as shown inTable 9.

Table 9: Treatment of discarded vehicles in tonnes and percentage in the EU-27 (Eurostat).

2010 % 2012 %

Total waste treatment 4,690,000 4,770,000

Landfill / disposal (D1-D7, D12) 20,000 0.4% 30,000 0.6%

Incineration / disposal (D10) 0 0.0% 0 0.0%

Incineration / energy recovery (R1) 0 0.0% 0 0.0%

Recovery other than energy recovery 4,670,000 99.6% 4,740,000 99.4%

In conclusion, WEEE and ELV streams properly separated and collected present high rates ofreuse and recycling, however, the estimated amounts of non-properly collected and/or treatedWEEE and ELV are considered relevant while their fate is unknown. Moreover, reuse and

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 25

recycling of such waste streams do not involve necessarily the recovery of refractory metals suchas niobium.

2.5.METHODS OF COLLECTION OF THE PRODUCTS

Niobium is recycled when niobium-bearing steels and superalloys are recycled at industrial scalebut waste recovery specifically for niobium content is generally negligible. Though the amount ofniobium recycled may be as much as 20% of apparent consumption (BGS, 2011), the amount ofniobium recovered from other sources, e.g. end of life products, is minor.

As described in section 2.1, niobium-steel alloys, super alloys magnets and capacitors containingniobium are used in electric and electronic equipment; however, the current estimatedrecyclability of niobium in waste electric and electronic equipment (WEEE) is 0%.

Collection schemes for WEEE and end of life vehicles (ELV) are already in place in the EuropeanUnion with the aim to increase the recycling of WEEE and ELV and/or re-use. Several policiesrelate to raw materials and recycling including, among others, the ELV Directive (2000/53/EC)and the WEEE Directive (2012/19/EU). These waste streams are complex mixtures of materialsand components that because of their hazardous content, and if not properly managed, cancause major environmental and health problems. Moreover, the production of modernelectronics requires the use of scarce and expensive resources e.g. niobium and other criticalraw materials. To improve the environmental management of these waste streams and tocontribute to a circular economy and enhance resource efficiency the improvement of collection,treatment and recycling of electronics and vehicles at the end of their life is essential.

Therefore, even though the collection schemes for waste electric and electronic equipment andend of life vehicles are already in place in the European Union, niobium, among other criticalmetals, is not recovered from such waste streams.

2.6.INCENTIVES FOR COLLECTION OF THE PRODUCTS

In general, the low recycling of the critical metals is due to the extremely low overall recyclingefficiencies and to the low collection rates of selected EOL products as well as smallconcentrations in the products. Based on CRI, 2014, main reasons for the low recyclability of thecritical metals are:

· Missing collection of the selected WEEE products groups: only 1/3 is reported ascollected,

· Export of used EEE products or illegal export of WEEE out the EU. At least 12,000 tonnesof old computers are assed to be shipped out of the EU to non-OECD countries,

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 26

· High losses during pre-processing, depending on whether manual or mechanicallydismantling is applied. Manual pre-processing can provide over 90% recycling metal ratefor many of the selected products groups, whereas the mechanical process for mostmetals only give recycling rate between 0 - 60%,

· Although the recycling rate in end-processing (smelting) is very high (90 to 95%) forcertain metals such as silver, cobalt, tellurium, gold, palladium and ruthenium, the rate is0 % (i.e. none of the material is recovered) for 7 of the selected 13 critical metals,

· The recycling rate of WEEE is poor for some of the metals because the whole recyclingprocess (dismantling, pre-processing, end-processing) focuses and is tailored toward theextraction of bulk materials, and satisfactory dismantling,-pre-processing and end-processing technologies are not present,

· There are thermodynamic-limits to the recycling of certain metals if jointly contained incomplex mixes with other elements.

These reasons for the low overall recycling rates indicate that increasing the recycling efficiencywill require more than the further development of technology solutions. Legal initiatives toincrease recycling rates, improve process quality and hinder export out of the EU of WEEE arealso required.

Alternatively, as strategic metals are not generally imported into the EU as minerals: rather, theyenter Europe in the form of components that are then assembled into finished products, reuse isa much more practicable option than recycling. At present, several companies are alreadysuccessfully collecting and reusing their own products and components.

To increase the rate of collection and recovery of WEEE, a review of the Directive is needed inorder to make each manufacturer responsible for the recovery of its own products (individualproducer responsibility); there would be a greater incentive across industry to “design fordisassembly”.

2.7.REFERENCES

British Geological Survey (BGS), 2011. Niobium-Tantalum. www.MineralsUK.com

Copenhagen Resource Institute (CRI), 2014. Present and potential future recycling of criticalmetals in WEEE. November 2014.http://www.cri.dk/sites/cri.dk/files/dokumenter/artikler/weee_recycling_paper_oct14.pdf

The Danish Environmental Protection Agency, 2015. Danish WEEE Market. A study of markets,actors and technologies in treatment of WEEE in Denmark Environmental project No. 1643,2015.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 27

Directive 2000/53/EC on end-of-life vehicles.

Directive 2012/19/EU of the European Parliament and of the Council of 4 July 2012 on wasteelectrical and electronic equipment (WEEE).

Directorate General for Internal Policies, Policy Department A: Economic and scientific policy.Substitutionability of Critical Raw Materials STUDY. October 2012.

H. C. Starck. Environmental, Competent, Unique High Tech Recycling for Refractory Metals.Technology Metals | Advanced Ceramics. http://www.hcstarck.jp/hcs-admin/file/8a8181e225548334012554ccf6e41434.de.0/Tungsten-Tantalum-Niobium-Recycling-HC-Starck.pdf

Labie, R., Willems, G., Nelen, D., Van Acker K., Recuperation of critical metals in Flanders: Scan ofpossible short term opportunities to increase recycling (2015), policy research centre SustainableMaterials Management, research paper 15, Leuven.https://steunpuntsumma.be/nl/publicaties/recuperation-of-critical-metals-in.pdf

Montero, R., Guevara, A., de la Torre, Ernesto, 2012. Recovery of Gold, Silver, Copper andNiobium from Printed Circuit Boards Using Leaching Column Technique. Journal of Earth Scienceand Engineering 2 (2012) 590-595.

Tantalum-Niobium International Study Center. http://tanb.org/niobium

UNEP, 2013. Metal recycling, opportunities, limits, infrastructure, UNEP report 2013.

USGS. National Minerals Information Center. Niobium (Columbium) and Tantalum

Statistics and Information. http://minerals.usgs.gov/minerals/pubs/commodity/niobium/

Web pages:

http://www.commissionoceanindien.org/archives/environment.ioconline.org/solid-waste-management/recycling-of-non-ferrous-metal.html

http://www.cbmm.com/us/p/173/uses-and-end-users-of-niobium.aspx

http://www.grandviewmaterials.com/product/niobium-application

Strategic metals: a priority resource efficiency. https://app.croner.co.uk/feature-articles/strategic-metals-priority-resource-efficiency

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 28

3. MAPPING AND COLLECTION OF TANTALUM CONTAINING END-OF-LIFE WASTEAND SCRAP

3.1.INTRODUCTION

Tantalum (Ta) is a dense, tough and ductile element with very high melting point and highcorrosion resistivity against many organic and inorganic acids below 100ºC. It has good thermaland electrical conducting properties, and it is easy to machine. Biocompatibility makes it usefulfor medical applications (CRM_InnoNet 2013, TIC).

Because of its unique properties Ta is used in many applications. Due to its stability and highvolumetric capacity, the main use of Ta is in the manufacture of capacitors, which are found inapplications requiring high-performance and reliability characteristics, such as portableelectronics, automotive, aerospace and military electronics. End-of-life recycling of tantalum islimited to between 1-9% of total consumption, and focused on applications such as hard metaltools and aero-engines (European Commission, 2010). The recovery of tantalum from EoLelectronic scrap is challenging and therefore does not occur at present.

3.2.APPLICATIONS CONTAINING TANTALUM

3.2.1. CAPACITORS

About 60%, according to some sources about 65% of the yearly Ta consumption is used inelectronics industry (T.I.C, CRM_InnoNet 2013). Most of it (about 40 % of total in 2011) is used inpowder or wire form in manufacture of capacitors (Soto-Viruet et a. 2013; Stratton andHenderson 2012). The estimates about the share of Ta consumed by the capacitor producersvary in different sources. The main reason seems to be that there are different estimates aboutdivision of Ta use between different electronics components.

Capacitors are used for storing electrical charges, for conducting alternating currency orseparating different currency levels of alternating currency (KEMET 2013). They are essentialcomponents of circuit boards.

There are many different types of capacitors manufactured from different materials dependingon the requirements of the application. Competitive solutions, such as ceramic and Nb-oxidecapacitors or solid-polymer Al chips have partly substituted Ta capacitors. However, due to thesuperior performance, robustness and temperature stability Ta capacitors are still used inapplications which require high performance. They can operate over a temperature range from -

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 29

55 to +200 oC (T.I.C 2015). High capacitance coefficient enables smaller components forminiaturized and portable electronics (Bacher, et al. 2013).

It has been estimated that the market share of Ta capacitors is 2-5%, however, in value termstheir market share is over 10% (Stratton & Henderson 2012, EPOW 2013, Salazar & McNutt2013).

Typical end of use-applications include portable electronics, telecom infrastructure, specificcomponents in cars, aerospace and military applications and demanding health applications. Tacapacitors can be found also in instrumentation, some TVs, DVD players, etc. electronics. Usuallythe electronic devices contain different types of capacitors, only a part of them are Ta capacitors(Bacher 2013, Stratton and Henderson 2012). The share of Ta capacitors may also varydepending of the age of the device.

3.2.2. ESTIMATED CONTENT AND FORM OF TA IN CAPACITORS

Tantalum capacitors are produced by sintering tantalum powder around a tantalum wire toform a pore structure (Figure 3). The surface is anodised to form an oxide (Ta2O5) coating. Alayer of MnO2 is deposited to act as cathode. In more recently produced Ta capacitors thecathode material is a conductive polymer (Knott 2011). The capacitor is contained in fireproof(brominated fire retardants) silica epoxy resin (Error! Reference source not found.). Onecapacitor contains 40-50% Ta.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 30

Figure 3 Structure of a Ta capacitor and the electrode in a Ta capacitor.(Mineta & Okabe)

There are several different sizes of standard Ta capacitors. One example are the capacitorsstudied by MIneta with size 6.0 × 3.2 × 2.5 mm and total weight around 0.3 g /each (Mineta andOkabe 2012, Katanoa et al. 2014). There are both smaller and bigger capacitor sizes available.Miniaturisation is one of the main trends in the production of electronic components, and alsocapacitors are getting smaller. There may be tens of capacitors in one equipment, but usuallyonly some of them are Ta containing.

3.2.3. OTHER ELECTRONIC COMPONENTS

Other electronics applications of Ta include semiconductors (EPOW 2011), resistors andcomputer hard drive discs:

· Mixtures containing tantalum oxide (Ta2O5) are used in gate dielectrics of very small MOS(metal oxide- semiconductor) transistors and as dielectrics of other capacitors inintegrated circuits.

· Prevention of Cu migration in semiconductors: Thin film physical barrier (tantalum nitrideor oxide) is sputtered by Physical Vapour Deposition process onto semiconductorsurfaces beneath copper metal to protect copper interconnects (Bacher et al. 2013).

· 6% Ta alloy has been used in computer hard drive discs because of its shape memoryproperties (T.I.C).

3.2.4. CEMENTED CARBIDES

Tungsten carbide (WC) is mostly used as the hard phase in cemented carbides. The basiccemented carbide structure is formed from WC and cobalt (Co) which forms the binder phase ofthe structure. Other metal carbides, including tantalum, niobium and titanium carbide areusually used with WC. Also the Co binder can be alloyed with e.g. Fe, Ni, Mo or Cr.

Tantalum carbide is used, mostly in association with WC and TiC. because it is an extremely hardrefractory ceramic (harder than WC). Ta increases thermal shock resistance and reduces hightemperature oxidation of the tools (Knott 2011. The applications include high-speed cutting andboring tools, and other tools for environments with high levels of stress and temperatures, suchas teeth for excavator buckets, mining drills, high-performance bearings and cutting blades. Hardmetal carbides are also used in refractory parts and coatings for furnaces and nuclear reactors(CRM_InnoNet 2013).). It has been estimated that about 12-14% of yearly consumption of Ta isused in hard metal tools.

3.2.5. TA SUPERALLOYS

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 31

Due to its high melting point and resistance to corrosion Ta used in superalloys which aretypically nickel based. Typically percentage of Ta in alloy is 3-11% (Knott 2011). Some of thealloys can be Ta based. Ta superalloys are used mostly in aerospace (75% of super-alloy demand,including jet engine and rocket engine nozzles) and defence applications (e.g. missile parts)(CRM_InnoNet 2013).They are also suitable for other turbine-type equipment, such as gasturbines. In addition, Ta-Ru alloy is used in the military due to its oxidation resistance and shapememory properties. About 14% of global Ta market (400 tonnes annually) is consumed insuperalloys (Knott 2011). Stratton & Henderson (2012) estimate that superalloys have probablythe highest demand growth expected, about 8%/year.

3.2.6. PROCESS EQUIPMENT

In process industries, such as chemical, pharmaceutical and metallurgical industries Tantalum isused in applications which require high temperature and corrosion resistance. Such applicationsinclude heat exchangers, boilers, condensers, pressure reactors, distillation columns, crucibles,etc. where Ta is used as liner. The most common alloy employed is tantalum-2.5% tungstenwhich is stronger than pure tantalum (Knott 2011). Ta is also used to produce dimensionallystable anodes that can be used in extreme environments, such as in the production of chlorineand soda in systems with ion exchange membranes (CRM_InnoNet 2013).

In electronics production Ta is used for sintering tray assemblies and shielding components forthe anode sintering furnaces.

3.2.7. MEDICAL APPLICATIONS

Owing to the biocompatibility of tantalum, tantalum alloys are used in medical applications,which include pacemakers (coating and capacitors), surgical implants where Ta is used either asmetal or coating e.g. in skull plates, hip joints, stents for blood vessel and hearing aids. Ta foil orwire can be used to connect torn nerves and as a woven gauze it binds abdominal muscle. It isalso used in surgical tools (CRM_InnoNet 2013).

3.2.8. OTHER APPLICATIONS

Tantalum oxide (Ta2O5) is used in lenses for spectacles, digital cameras and mobile phones.Because its high index of refraction it enables thinner and smaller lenses (T.I.C.). Ta is also usedin glass-coatings and in X-ray film/absorbers where yttrium tantalite reduces X-ray exposure andenhances image quality. Lithium Tantalite containing surface acoustic wave filters are applied forelectronic signal wave dampening in cell phones, TV sets, video recorders, etc. (T.I.C).

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 32

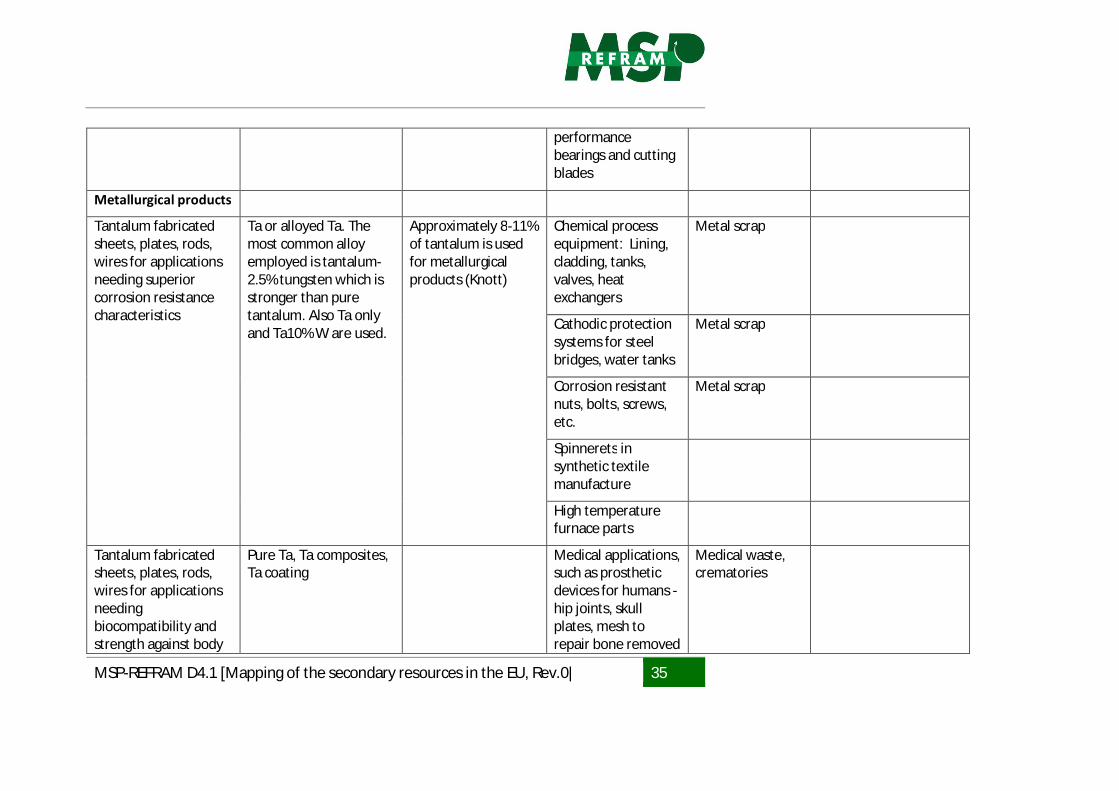

3.3. TA AND TA CONTAINING COMPONENTS IN PRODUCTS AND END-OF-LIFEWASTE

The main basic Ta products used in component or application manufacturing are Ta powder, Taoxide and different Ta alloys in sheet, plate, rod or wire form, Ta ingots and Ta carbide (TaC).Other Ta containing chemicals, such as lithium tantalite, Ta chloride and yttrium tantalatephosphor are also consumed for specific applications. The main applications of Ta in differentforms, the main components where Ta is contained and the corresponding waste streams aresummarized in Overview of tantalum products and their main applicationsTable 10.

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 33

Table 10 Overview of tantalum products and their main applications

Applications andcomponents1

Form of tantalum in theproduct

Estimated quantitiesof Ta in products

End-of-Life products End-of-Life Wastestream

Current recycling rates

Electronics

Tantalum capacitorsfor electronic circuitsin applicationsrequiring highperformance and highreliabilitycharacteristics.

Other types ofcapacitors are used inlower-voltageapplications.

Tantalum capacitors areproduced by sinteringtantalum powderaround a tantalum wireto form a porestructure. The surface isanodised to form anoxide (Ta2O5) coating.One Ta capacitorcontains 40-50% Ta (Seealso Figures 1 and 2).

About 40-45% oftotal Ta consumptionis used in capacitors.The quantities mayhave somewhatdecreased due to thealternative capacitorsolutions.

Quantity percapacitor depends onthe requirements ofapplication, age ofapplication, etc.

The trend is towardssmaller capacitorswith higherefficiencies

End-of-Life Vehicles(ELV): components,such as ABS, airbagactivation, enginemanagementmodules, GPS

End-of-LifeVehicles

EU ELV recycling target85%, recycling of Tacapacitors from ELValmost zero, Ta ends inmetallurgical slags andshredding waste

Components inaerospace andmilitary products

Metal scrap,specific scrapping

Recycling of Ta almostzero, Ta ends in slagsand waste

Portable electronics,such as laptops,mobile phones,video and digital stillcameras

Waste electricaland electronicequipment

Recycling of Tacapacitors from WEEEalmost zero, Ta ends inslags and waste

Medical appliances,such as hearing aidsand pacemakers

Hospital waste,crematories

Hospital waste notrecycled, somerecycling of implantsfrom crematories

Telecom and Data-com infrastructure,such as mobile

WEEE, metalscrap

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 34

phone signal masts

Instrumentation WEEE, metalscrap, otherindustrial waste

Sputtering targets Thin film physical barrier(Ta, Ta oxice or nitride)sputtered by PVDprocess ontosemiconductor surfacesto protect the Cuinterconnects (preventCu migration)

About 20 % of Ta isused in other EEapplications than Tacapacitors

Semiconductors inEEE, such as DVDplayers, flat screenTVs, game consoles,battery chargers,power rectifiers

WEEE

Integrated capacitorsin integrated circuits

Tantalum Oxide (Ta2O5) WEEE, ELV

Surface Acoustic Wave(SAW) filters

Lithium tantalate Mobile phones, hi-fistereos andtelevisions

WEEE

Ta alloy Alloy containing 6% Tafor shaping of memoryproperties

Computer hard drivediscs

WEEE

Cemented carbides

Tantalum carbide Tantalum carbide is acomponent used inassociation with WC andTIC in hard metal tools

Consumes globallyabout 12% of Taproduced (Knott)

High-speed cuttingand boring tools,such as teeth forexcavator buckets,mining drills, high-

Hard metal toolwaste

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 35

performancebearings and cuttingblades

Metallurgical products

Tantalum fabricatedsheets, plates, rods,wires for applicationsneeding superiorcorrosion resistancecharacteristics

Ta or alloyed Ta. Themost common alloyemployed is tantalum-2.5% tungsten which isstronger than puretantalum. Also Ta onlyand Ta10% W are used.

Approximately 8-11%of tantalum is usedfor metallurgicalproducts (Knott)

Chemical processequipment: Lining,cladding, tanks,valves, heatexchangers

Metal scrap

Cathodic protectionsystems for steelbridges, water tanks

Metal scrap

Corrosion resistantnuts, bolts, screws,etc.

Metal scrap

Spinnerets insynthetic textilemanufacture

High temperaturefurnace parts

Tantalum fabricatedsheets, plates, rods,wires for applicationsneedingbiocompatibility andstrength against body

Pure Ta, Ta composites,Ta coating

Medical applications,such as prostheticdevices for humans -hip joints, skullplates, mesh torepair bone removed

Medical waste,crematories

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 36

fluids after damage bycancer, suture clips,stents for bloodvessels

High temperaturealloys

3-11 % Ta in alloy,typically NI based, alsoother types

Tantalum insuperalloys accountsfor approximately14% of the globalmarket (Knott

Air and land basedturbines (e.g. jetengine discs, bladesand vanes)Rocket nozzles

Metal scrap

Ta-Ru alloy Military applications Metal scrap

Other applications

Lenses Tantalum Oxide (Ta2O5)provides high index ofrefraction

SpectaclesDigital camerasMobile phones

WEEE

Ink jet printers

X-ray film Yttrium tantalatephosphor reduces X-rayexposure and enhancesimage quality

X-ray film

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 37

3.3.1. END-OF-LIFE VOLUMES OF PRODUCTS AND REFRACTORY METALS INPRODUCTS

As described in Chapter 3.2 and Table 10 tantalum is used in quite a long list of final products.From the recycling perspective, they have quite varying characteristics. Also life-time of theproducts, collection systems and responsibilities and the legislative requirements vary betweenproduct groups. The major applications include electrical and electronic waste, especially (butnot only) IT and telecommunication appliances and infrastructure, vehicles and other transportapplications. The other main applications include Ta containing alloys and hard metals. Theinformation regarding the Ta content in the products is quite scarce. The estimation is difficultbecause for example, the amount and size of Ta containing electronic components variesdepending on the requirements of applications and may be different even in the same type ofapplications.

Waste electrical and electronic equipment (WEEE)

Chapter 2.3.1 on niobium contains background information about WEEE development andlegislation as well as statistical information about WEEE collection and treatment in EU-28countries. This information relates also to tantalum and is not repeated here. A summary of thetotal amounts of WEEE collected in EU-28, Liechtenstein and Norway 2012 is presented in Table11 by WEEE categories (Eurostat). It can be estimated that Ta containing applications will mainlybe found in the WEEE categories: IT and telecommunications equipment and Consumerequipment. However, not all the applications in these categories contain Ta, and some Tacontaining equipment can be found also from other categories.

Table 11. The total quantities of WEEE collected in EU-28, Liechtenstein and Norway in 2012 (Eurostat).

Category Equipment collected, tonsLarge household appliances 1 495 000Small household appliances 224 500IT and telecommunications equipment 615 000Consumer equipment 572 500Other 187 000Total WEEE 3 474 000

Buchert et al. (2012) give a rough estimate about Ta content in notebooks 1 700 mg/notebook,from which capacitors on the motherboard account for 90%, and capacitors on other printedcircuit boards PCBs10%. According to Chanceler et al. the Ta content of notebooks was 100 –

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 38

2000 mg/equipment. Tantalum capacitors may have been partially substituted by othercapacitors, and therefore Ta content of notebooks can vary remarkable between themanufacturing year and device generation (Bacher et al. 2013, Buchert et al. 2012)

There are several estimates about Ta consumption in mobile phones. Chanceler et al., 2015estimate that the quantity of Ta in smartphones sold in Germany in 2012 varied from almostzero to 100 mg/per phone. Other sources present values from 20 mg/phone to 40 mg/phone(Nest, 2011; Veronese xxx). In the study of Müller (2013) it was found that the Ta concentrationsin three cell phones manufacturer 2008-2009 were 300-600 mg/kg. The weights of the phonesexcluding battery were 65-85 g which means that the numbers are well comparable with thevalues from other sources. Based on the information available, the estimate of Müller about theyearly consumption of Ta for the production of mobile phones could be on the right level; about61 tonnes Ta/1.6 billion phones.

Chanceler et al., 2015 also present an estimate about total amount of 4-46 tonnes of Ta in ICTequipment sold in Germany in 2012; the most significant applications being laptops, stationarycomputers and mobile phones. The Ta concentrations of tablets are very low, which may lead toreduced amounts of Ta available in ICT product waste. Based on that the quantities of Taimported to EU countries in WEEE could be 20 -230 tonnes. If extreme values are removed, avery rough estimate could be 100 – 150 tonnes Ta in WEEE annually.

END-OF-LIFE VEHICLES (ELV)

The total number and recycling rates of end-of-life vehicles in EU member states are presentedChapter 2.3.2 on Niobium. However as for WEEE, the officially reported numbers underestimatethe amount of end-of-life vehicles.

The information about the amounts of Ta in cars is quite scarce. The following estimates arebased on the study of Cullbrand and Magnusson (2012) on quantities of CRMs in four differentVolvo car types, three conventional and one hybrid car, which were in production in thebeginning of 2010s.The data was gathered from the International Material Data System (IMDS),which is automobile industry’s material data system (Cullbrand and Magnusson 2012).

It was found that tantalum was mostly used in printed circuit boards in electronic applications,such as engine subsystem, infotainment, security systems and body Electronics. 5.8 – 11 g Ta/carwas consumed. As can be expected the total amount of Ta increased considerably with increasedequipment level. According to the writers the impact of increased electrification on the use of Tawas observed, but it was quite small. Although these values are based on very limited amount ofsamples and only one brand, these are used here as indicative values. In the cars that are

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 39

currently deregistered , less electronics is used than currently but the capacitors may containmore tantalum. If Ta content in registered cars would be 4-6 g/car, it would mean about 80 t Tain EU end-of-life cars annually.

OTHER APPLICATIONS

The recycling rates of cemented carbide tools and Ta alloys are quite significant. Usually Ta isrecovered with main components of the hard metal tools and it remains in the producedtungsten carbide – cobalt powder. However, some recyclers separate tungsten from other rawmaterials. Tantalum containing alloys are also recovered in alloy form. There are a fewcompanies in Europe which recycle refractory metals, see chapter 5.

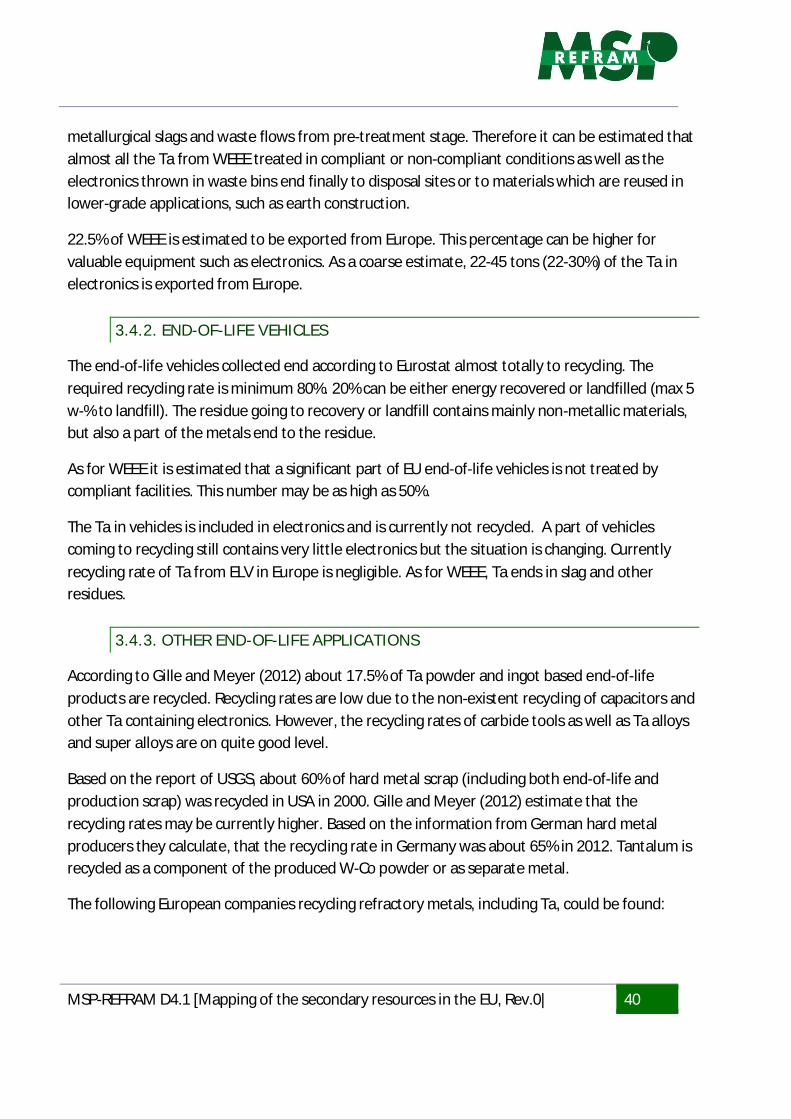

3.4.CURRENT FATE OF END-OF-LIFE PRODUCTS AND MANUFACTURING SCRAP

In Europe and even globally there are quite few companies recycling tantalum. Most of therecycled Ta originates from manufacturing waste. In addition, a part of end-of-life cementedcarbides and alloys is also recycled. Recycling of Ta from capacitors and other electroniccomponents is difficult and almost negligible in Europe due the small Ta concentrations incomplex waste streams (JRC). However, some literature sources estimate, that a part of Tacapacitors in the ICT equipment that are exported to China and developing countries will berecycled. For example Israel based company IsraSpecMet Oy (http://www.israspecmet.com/)claims to have capability of extracting Ta capacitors from EoL printed circuit boards. Therecovery requires manual separation of the capacitors and is therefore currently feasible onlywhen the salary costs are low.

3.4.1. WEEE

It is estimated that only 35% of the waste produced ends to the officially reported collectionsystems (CWIT 2015). The report further estimates that about 1.5 million tons WEEE is exported,3.15 million tons treated under non-compliant conditions, 0.75 million tons scavenged forvaluable parts and 0.75 million tons mainly small appliances landfilled or incinerated (CWIT2015). Based on this numbers there is a large potential, from which only a part is recoveredunder compliant or non-compliant conditions.

Ta can mainly be found in the categories IT and telecommunications equipment (collectedamount 615 00 tons in 2012) and consumer equipment (572 500 tons collected in 2012). Fromthe officially collected WEEE only 2.4% goes to landfill and 1.1% to energy recovery. However,currently there is almost no recovery of Ta from WEEE and Ta in collected electronics ends to

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 40

metallurgical slags and waste flows from pre-treatment stage. Therefore it can be estimated thatalmost all the Ta from WEEE treated in compliant or non-compliant conditions as well as theelectronics thrown in waste bins end finally to disposal sites or to materials which are reused inlower-grade applications, such as earth construction.

22.5% of WEEE is estimated to be exported from Europe. This percentage can be higher forvaluable equipment such as electronics. As a coarse estimate, 22-45 tons (22-30%) of the Ta inelectronics is exported from Europe.

3.4.2. END-OF-LIFE VEHICLES

The end-of-life vehicles collected end according to Eurostat almost totally to recycling. Therequired recycling rate is minimum 80%. 20% can be either energy recovered or landfilled (max 5w-% to landfill). The residue going to recovery or landfill contains mainly non-metallic materials,but also a part of the metals end to the residue.

As for WEEE it is estimated that a significant part of EU end-of-life vehicles is not treated bycompliant facilities. This number may be as high as 50%.

The Ta in vehicles is included in electronics and is currently not recycled. A part of vehiclescoming to recycling still contains very little electronics but the situation is changing. Currentlyrecycling rate of Ta from ELV in Europe is negligible. As for WEEE, Ta ends in slag and otherresidues.

3.4.3. OTHER END-OF-LIFE APPLICATIONS

According to Gille and Meyer (2012) about 17.5% of Ta powder and ingot based end-of-lifeproducts are recycled. Recycling rates are low due to the non-existent recycling of capacitors andother Ta containing electronics. However, the recycling rates of carbide tools as well as Ta alloysand super alloys are on quite good level.

Based on the report of USGS, about 60% of hard metal scrap (including both end-of-life andproduction scrap) was recycled in USA in 2000. Gille and Meyer (2012) estimate that therecycling rates may be currently higher. Based on the information from German hard metalproducers they calculate, that the recycling rate in Germany was about 65% in 2012. Tantalum isrecycled as a component of the produced W-Co powder or as separate metal.

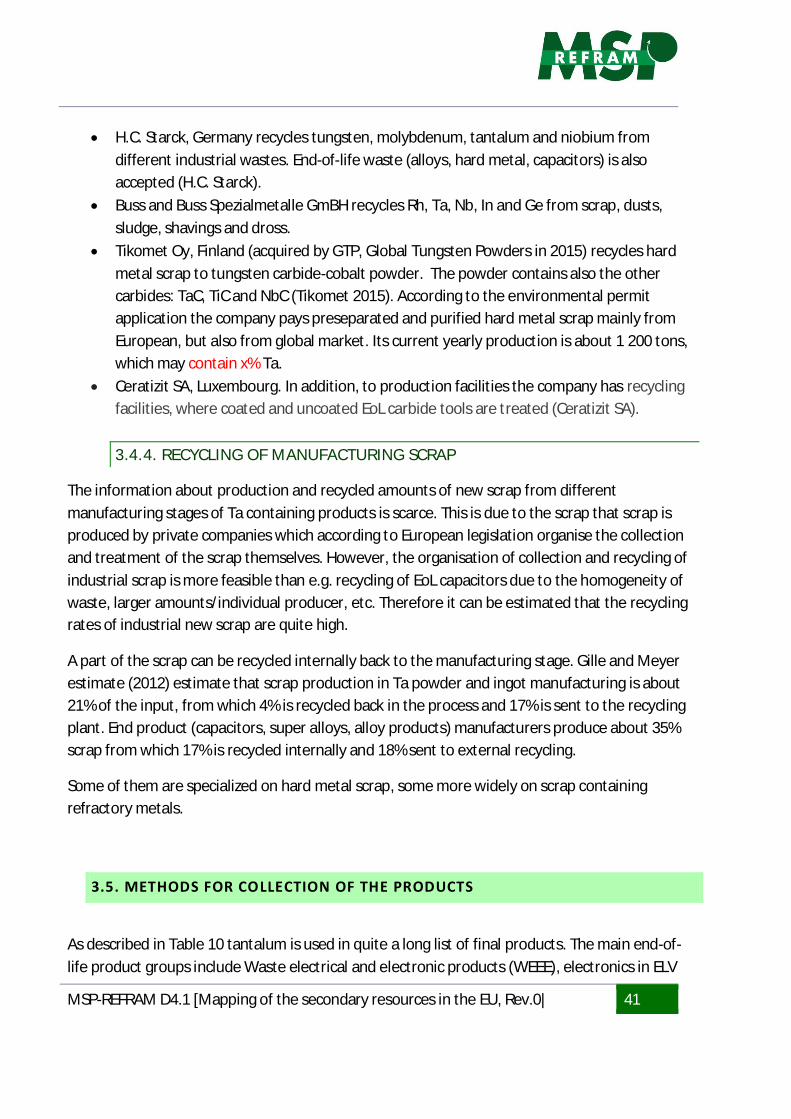

The following European companies recycling refractory metals, including Ta, could be found:

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 41

· H.C. Starck, Germany recycles tungsten, molybdenum, tantalum and niobium fromdifferent industrial wastes. End-of-life waste (alloys, hard metal, capacitors) is alsoaccepted (H.C. Starck).

· Buss and Buss Spezialmetalle GmBH recycles Rh, Ta, Nb, In and Ge from scrap, dusts,sludge, shavings and dross.

· Tikomet Oy, Finland (acquired by GTP, Global Tungsten Powders in 2015) recycles hardmetal scrap to tungsten carbide-cobalt powder. The powder contains also the othercarbides: TaC, TiC and NbC (Tikomet 2015). According to the environmental permitapplication the company pays preseparated and purified hard metal scrap mainly fromEuropean, but also from global market. Its current yearly production is about 1 200 tons,which may contain x% Ta.

· Ceratizit SA, Luxembourg. In addition, to production facilities the company has recyclingfacilities, where coated and uncoated EoL carbide tools are treated (Ceratizit SA).

3.4.4. RECYCLING OF MANUFACTURING SCRAP

The information about production and recycled amounts of new scrap from differentmanufacturing stages of Ta containing products is scarce. This is due to the scrap that scrap isproduced by private companies which according to European legislation organise the collectionand treatment of the scrap themselves. However, the organisation of collection and recycling ofindustrial scrap is more feasible than e.g. recycling of EoL capacitors due to the homogeneity ofwaste, larger amounts/individual producer, etc. Therefore it can be estimated that the recyclingrates of industrial new scrap are quite high.

A part of the scrap can be recycled internally back to the manufacturing stage. Gille and Meyerestimate (2012) estimate that scrap production in Ta powder and ingot manufacturing is about21% of the input, from which 4% is recycled back in the process and 17% is sent to the recyclingplant. End product (capacitors, super alloys, alloy products) manufacturers produce about 35%scrap from which 17% is recycled internally and 18% sent to external recycling.

Some of them are specialized on hard metal scrap, some more widely on scrap containingrefractory metals.

3.5. METHODS FOR COLLECTION OF THE PRODUCTS

As described in Table 10 tantalum is used in quite a long list of final products. The main end-of-life product groups include Waste electrical and electronic products (WEEE), electronics in ELV

MSP-REFRAM D4.1 [Mapping of the secondary resources in the EU, Rev.0| 42

and other transport applications, hard metal tools, super alloys and Ta containing metallurgicalproducts used by different industrial sectors and medical applications. The knowledge about theamounts of Ta in different end-of-life products is quite limited. Some coarse estimates can bemade on the basis of estimated Ta consumption. About 50-60% Ta is used in electronics, 14 % insuper alloys, 12 % in hard metal tools and about 10% in sheets, rods, etc. However, the lifetimesof the products vary from short lifetimes of WEEE to much longer lifetimes of some industrialapplications, and this may also reflect to waste amounts.

3.5.1. ELV AND WEEE

The legislative framework for the collection and recycling of waste in EU countries is provided byWaste framework directive (2008/98/EC). The ELV Directive 2000/53/EC and the new WEEEDirective 2012/19/EU are based on Extended Produced Responsibility (EPR) principle requiringoriginal equipment manufacturers (OEMs) to take responsibility for their end-of-life goods anddescribing legal criteria. Mostly Producer Responsibility Organisations (PRO) are set up to takecare of practical implementation of the system on behalf of the member companies.