marcellus shale gas - enerplus · 21 marcellus horizontal producers lycoming 1 lycoming 2 ......

TRANSCRIPT

The Game PlanMarcellus Shale Gas

Dana W. Johnson, President, U.S. Operations

1

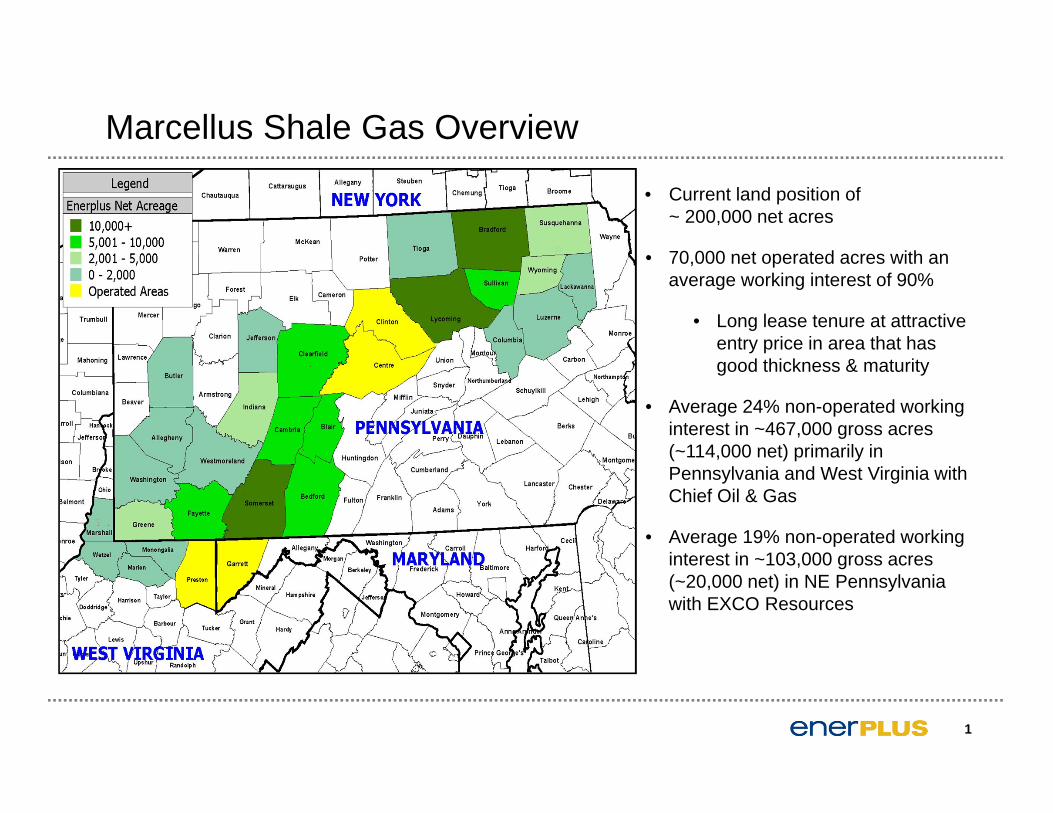

Marcellus Shale Gas Overview

• Current land position of ~ 200,000 net acres

• 70,000 net operated acres with an average working interest of 90%

• Long lease tenure at attractive entry price in area that has good thickness & maturity

• Average 24% non-operated working interest in ~467,000 gross acres (~114,000 net) primarily in Pennsylvania and West Virginia with Chief Oil & Gas

• Average 19% non-operated working interest in ~103,000 gross acres (~20,000 net) in NE Pennsylvania with EXCO Resources

2

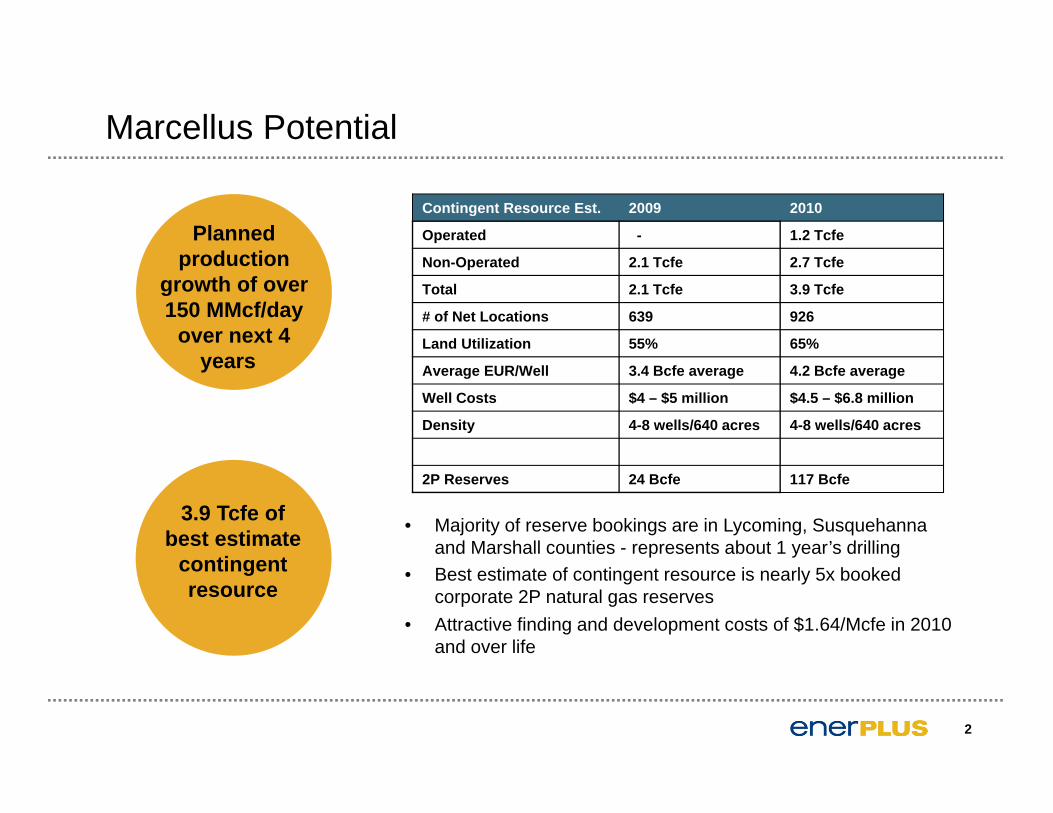

Marcellus Potential

Planned production

growth of over 150 MMcf/day

over next 4 years

3.9 Tcfe of best estimate

contingent resource

Contingent Resource Est. 2009 2010

Operated - 1.2 Tcfe

Non-Operated 2.1 Tcfe 2.7 Tcfe

Total 2.1 Tcfe 3.9 Tcfe

# of Net Locations 639 926

Land Utilization 55% 65%

Average EUR/Well 3.4 Bcfe average 4.2 Bcfe average

Well Costs $4 – $5 million $4.5 – $6.8 million

Density 4-8 wells/640 acres 4-8 wells/640 acres

2P Reserves 24 Bcfe 117 Bcfe

• Majority of reserve bookings are in Lycoming, Susquehanna and Marshall counties - represents about 1 year’s drilling

• Best estimate of contingent resource is nearly 5x booked corporate 2P natural gas reserves

• Attractive finding and development costs of $1.64/Mcfe in 2010 and over life

3

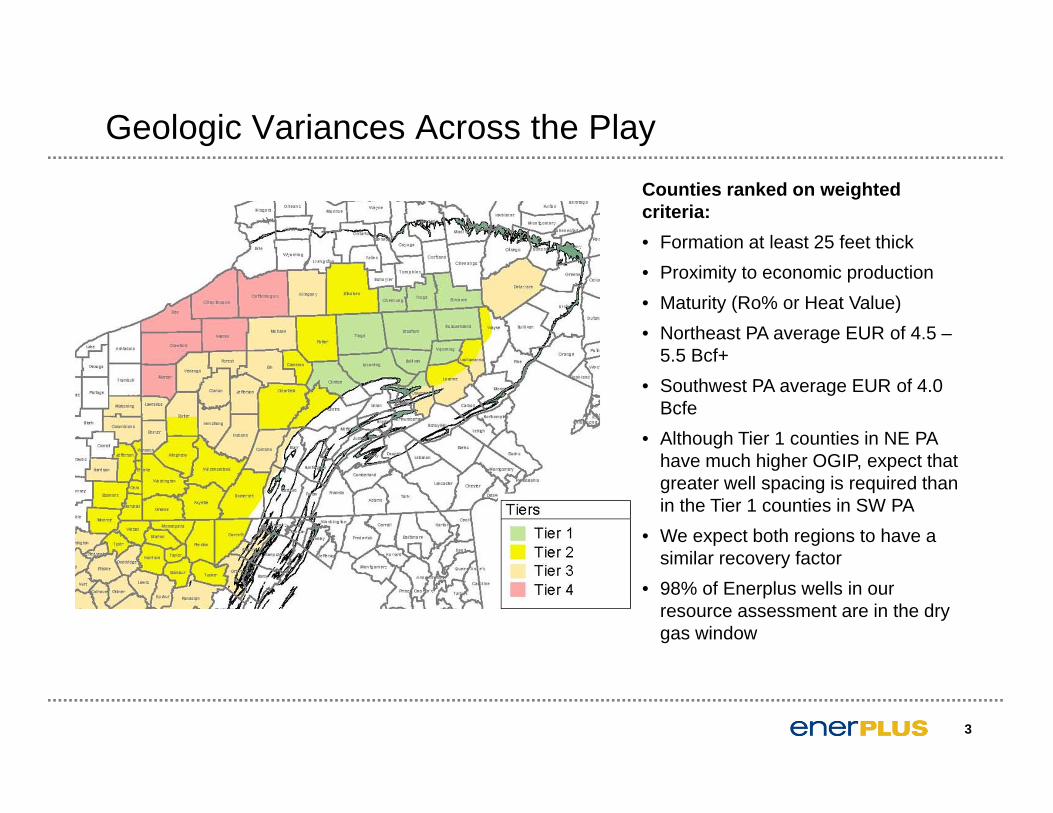

Geologic Variances Across the PlayCounties ranked on weighted criteria:• Formation at least 25 feet thick• Proximity to economic production• Maturity (Ro% or Heat Value)• Northeast PA average EUR of 4.5 –

5.5 Bcf+• Southwest PA average EUR of 4.0

Bcfe• Although Tier 1 counties in NE PA

have much higher OGIP, expect that greater well spacing is required than in the Tier 1 counties in SW PA

• We expect both regions to have a similar recovery factor

• 98% of Enerplus wells in our resource assessment are in the dry gas window

4

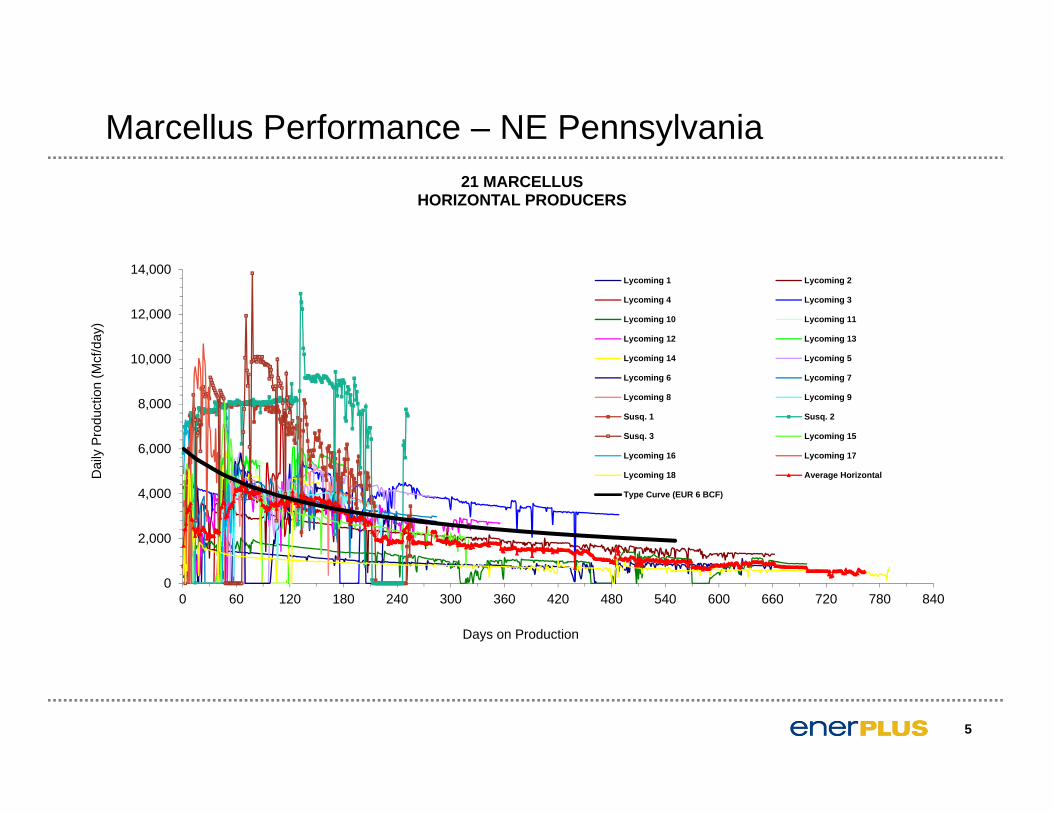

Marcellus Performance – Cumulative ProductionType curve estimates have been increased as well

results have either met or exceeded our expectations 25% of wells are above 6 Bcfe type curve

5

Marcellus Performance – NE Pennsylvania

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0 60 120 180 240 300 360 420 480 540 600 660 720 780 840

Dai

ly P

rodu

ctio

n (M

cf/d

ay)

Days on Production

21 MARCELLUSHORIZONTAL PRODUCERS

Lycoming 1 Lycoming 2

Lycoming 4 Lycoming 3

Lycoming 10 Lycoming 11

Lycoming 12 Lycoming 13

Lycoming 14 Lycoming 5

Lycoming 6 Lycoming 7

Lycoming 8 Lycoming 9

Susq. 1 Susq. 2

Susq. 3 Lycoming 15

Lycoming 16 Lycoming 17

Lycoming 18 Average Horizontal

Type Curve (EUR 6 BCF)

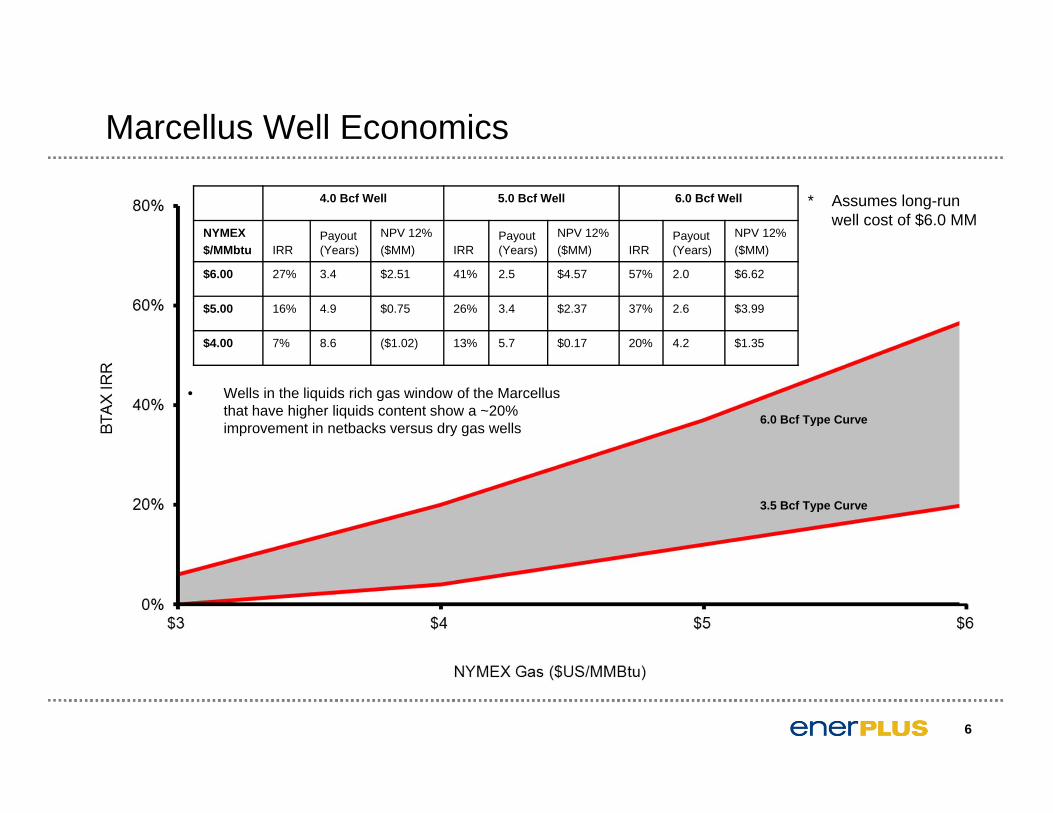

6.0 Bcf Type Curve

3.5 Bcf Type Curve

6

Marcellus Well Economics

4.0 Bcf Well 5.0 Bcf Well 6.0 Bcf Well

NYMEX$/MMbtu IRR

Payout (Years)

NPV 12%($MM) IRR

Payout (Years)

NPV 12%($MM) IRR

Payout (Years)

NPV 12%($MM)

$6.00 27% 3.4 $2.51 41% 2.5 $4.57 57% 2.0 $6.62

$5.00 16% 4.9 $0.75 26% 3.4 $2.37 37% 2.6 $3.99

$4.00 7% 8.6 ($1.02) 13% 5.7 $0.17 20% 4.2 $1.35

* Assumes long-run well cost of $6.0 MM

• Wells in the liquids rich gas window of the Marcellus that have higher liquids content show a ~20% improvement in netbacks versus dry gas wells

7

Well Design• Drilling (Average 30 days)

• Operated• Drilling primarily delineation wells – with vertical pilot, cores and logs• 5 single well pads in Centre County, PA (2 wells ) and Preston County,

WV (3 wells)• Lateral length of 4,000’ to 5,000’• Closed loop system with synthetic mud• Installing water infrastructure

• Non – operated• Drilling primarily lease saving operations, rather than pad drilling• Vast majority single well pads with a few 2 to 4 well pads• Longer laterals 3,000’- 5,000’• Closed loop system with synthetic mud

• Completions (2 to 4 weeks)• Operated

• 10 – 12 frac stages, 300’ to 400’ per stage• 4 perf clusters per stage• Slickwater frac with multiple sweeps

• Non-operated• Fewer frac stages and larger frac intervals 400’ – 450’• 6 – 9 perf clusters per stage• Still testing 1 month “resting” of wells• Reduced chemical loading

Drilling costs range from $2.5 – $3.5

million

Completion costs range from $3.0 –$4.0 million

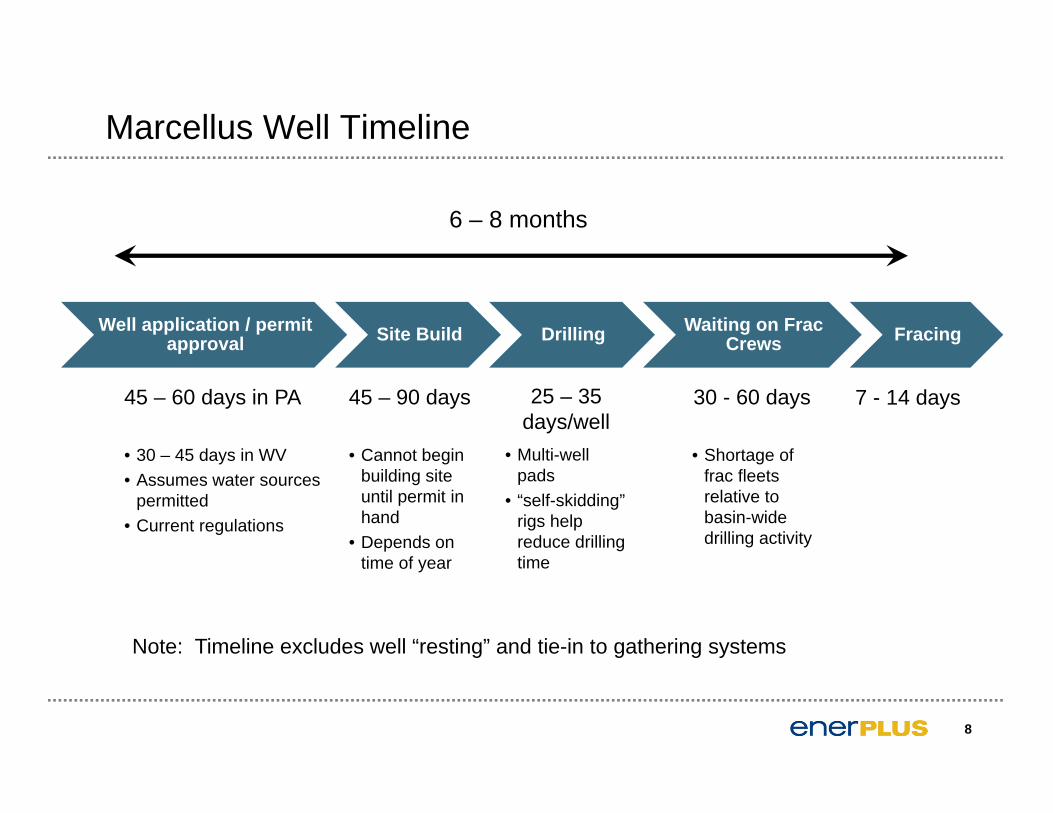

Marcellus Well Timeline

Well application / permit approval Site Build Drilling Waiting on Frac

Crews Fracing

8

45 – 60 days in PA

• 30 – 45 days in WV• Assumes water sources

permitted• Current regulations

45 – 90 days

• Cannot begin building site until permit in hand

• Depends on time of year

25 – 35 days/well

• Multi-well pads

• “self-skidding” rigs help reduce drilling time

30 - 60 days

• Shortage of frac fleets relative to basin-wide drilling activity

7 - 14 days

6 – 8 months

Note: Timeline excludes well “resting” and tie-in to gathering systems

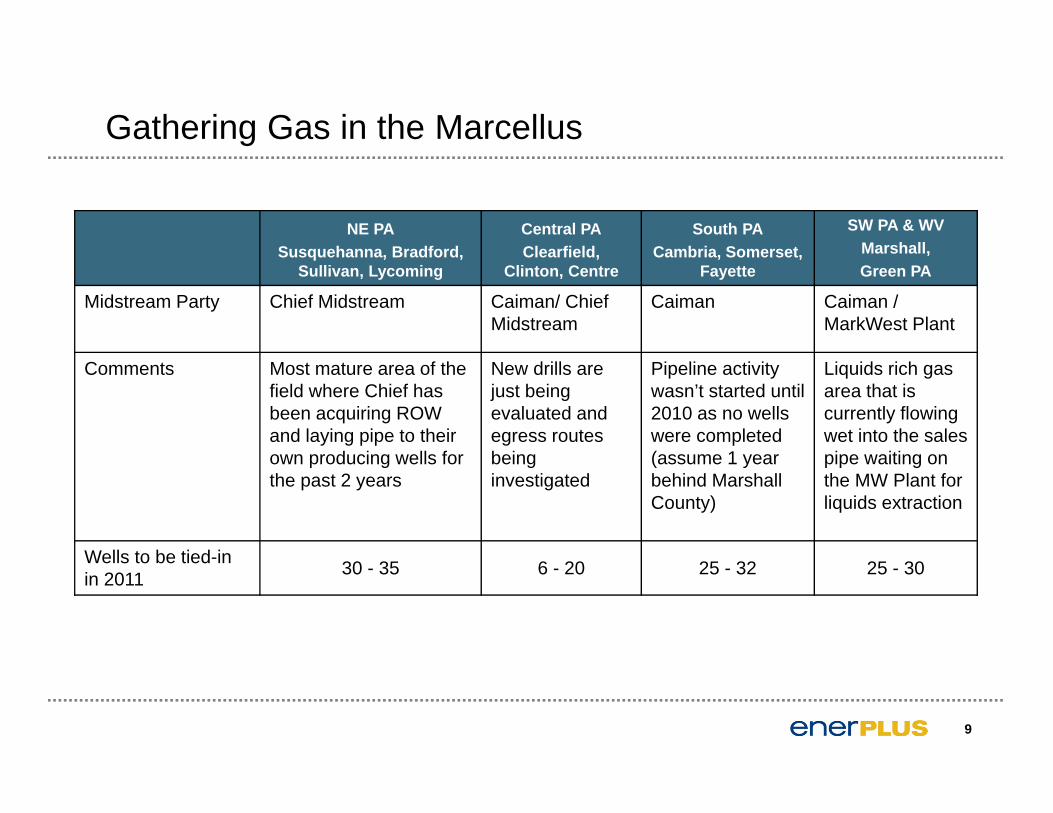

Gathering Gas in the Marcellus

9

NE PASusquehanna, Bradford,

Sullivan, Lycoming

Central PAClearfield,

Clinton, Centre

South PACambria, Somerset,

Fayette

SW PA & WVMarshall, Green PA

Midstream Party Chief Midstream Caiman/ Chief Midstream

Caiman Caiman / MarkWest Plant

Comments Most mature area of the field where Chief has been acquiring ROW and laying pipe to their own producing wells for the past 2 years

New drills are just being evaluated and egress routes being investigated

Pipeline activity wasn’t started until 2010 as no wells were completed (assume 1 year behind Marshall County)

Liquids rich gas area that is currently flowing wet into the sales pipe waiting on the MW Plant for liquids extraction

Wells to be tied-in in 2011 30 - 35 6 - 20 25 - 32 25 - 30

10

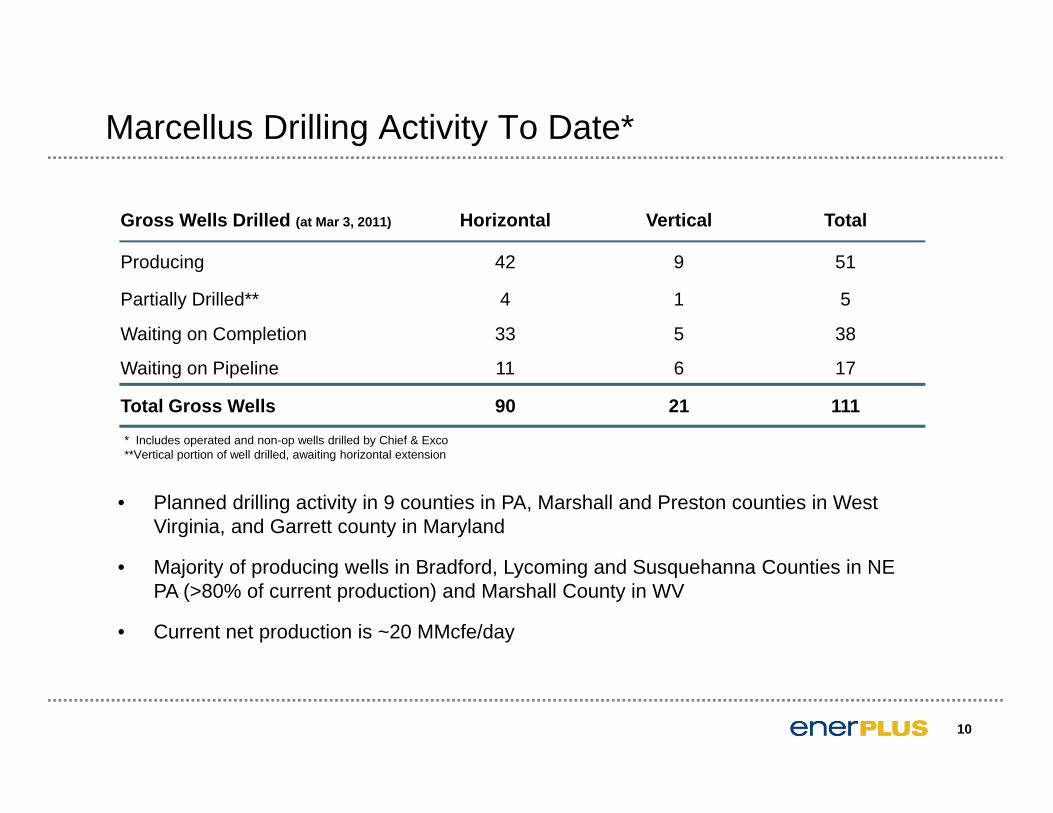

Marcellus Drilling Activity To Date*

Gross Wells Drilled (at Mar 3, 2011) Horizontal Vertical Total

Producing 42 9 51

Partially Drilled** 4 1 5

Waiting on Completion 33 5 38

Waiting on Pipeline 11 6 17

Total Gross Wells 90 21 111

• Planned drilling activity in 9 counties in PA, Marshall and Preston counties in West Virginia, and Garrett county in Maryland

• Majority of producing wells in Bradford, Lycoming and Susquehanna Counties in NE PA (>80% of current production) and Marshall County in WV

• Current net production is ~20 MMcfe/day

* Includes operated and non-op wells drilled by Chief & Exco**Vertical portion of well drilled, awaiting horizontal extension

2011 Marcellus Plans

• 2011 capital program of $160 million• 150 gross wells planned (22.4 net)

• Operated : 5 gross wells, 1 rig• Non-Operated: 145 gross wells, 8 - 10 rigs

• Expect to complete ~121 gross wells with 94 new gross wells on stream by the end of the year

• Capital:• 25% directed to liquids rich gas in SW PA and NW

WV • 30% directed to delineation activity to preserve

lease positions and identify future potential• 45% of capital directed to development drilling in

areas with EUR’s of 4.5 to 5.5 Bcf

• May see upward pressure on capital due to activity levels

• Current average netback ~$2.50/Mcfe

11

Production growth of

150% in 2011

12

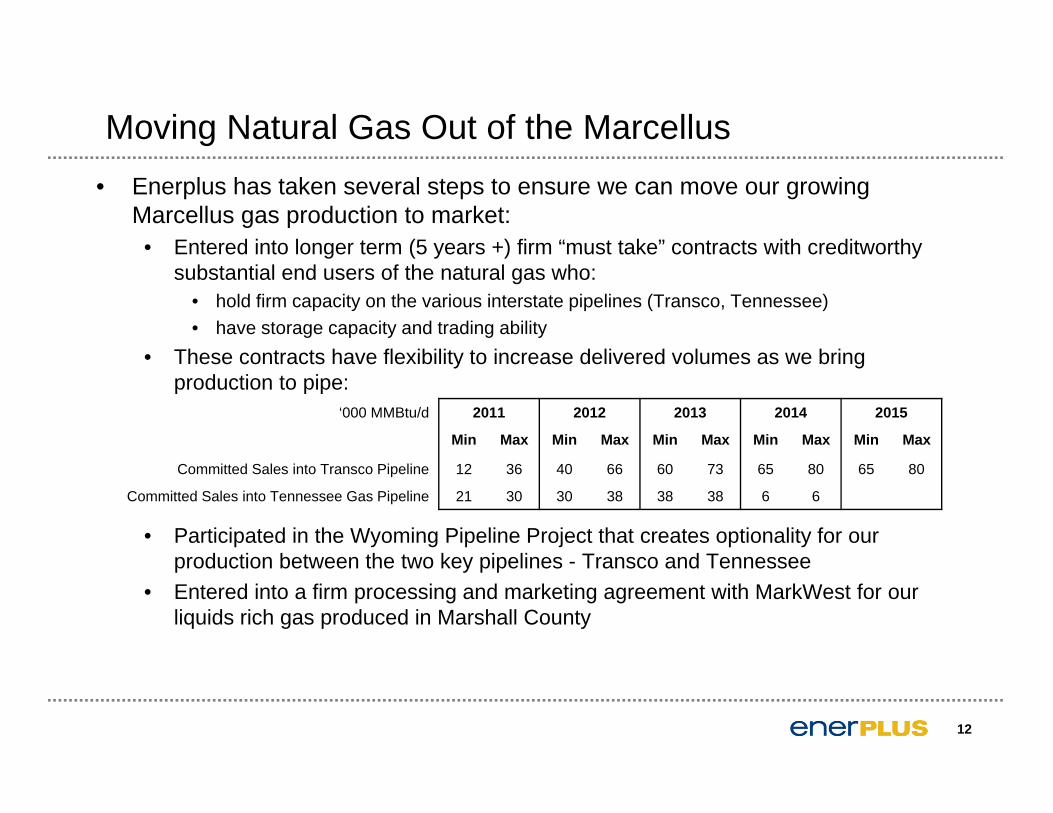

Moving Natural Gas Out of the Marcellus• Enerplus has taken several steps to ensure we can move our growing

Marcellus gas production to market:• Entered into longer term (5 years +) firm “must take” contracts with creditworthy

substantial end users of the natural gas who:• hold firm capacity on the various interstate pipelines (Transco, Tennessee)• have storage capacity and trading ability

• These contracts have flexibility to increase delivered volumes as we bring production to pipe:

• Participated in the Wyoming Pipeline Project that creates optionality for our production between the two key pipelines - Transco and Tennessee

• Entered into a firm processing and marketing agreement with MarkWest for our liquids rich gas produced in Marshall County

‘000 MMBtu/d 2011 2012 2013 2014 2015

Min Max Min Max Min Max Min Max Min Max

Committed Sales into Transco Pipeline 12 36 40 66 60 73 65 80 65 80

Committed Sales into Tennessee Gas Pipeline 21 30 30 38 38 38 6 6

13

Water Access & Handling

• ERF and our JV partners have sufficient water source permits to execute development plans

• ERF and our JV partners are permitting and constructing additional water impoundments

• ERF developing centralized water infrastructure with gas gathering system (Centre County, PA)

• Implemented closed loop system for drilling fluids management in 2010

• Goal to recycle 100% of produced and flow back water by end of 2011

• Chief building a centralized tank farm for storage and recycling

• ERF reusing flow back fluid on location to reduce fresh water use

• JV partners utilizing industrial water treatment plants and disposal wells for water disposal

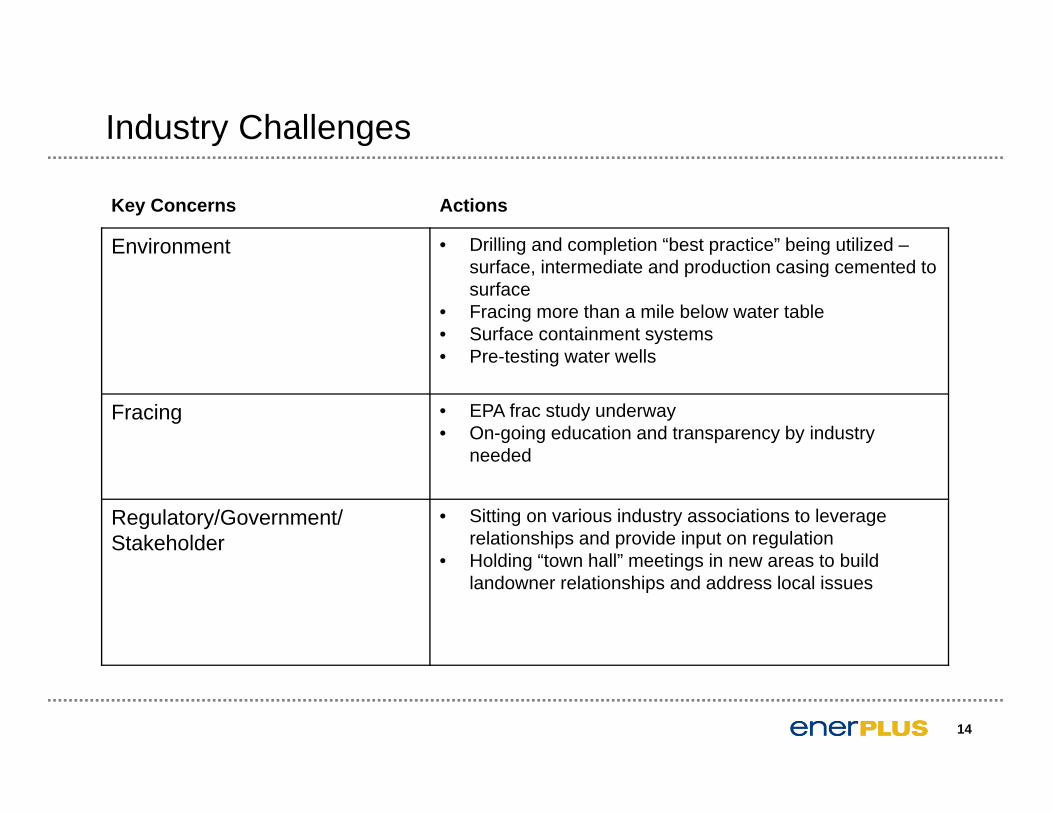

14

Key Concerns Actions

Environment • Drilling and completion “best practice” being utilized –surface, intermediate and production casing cemented to surface

• Fracing more than a mile below water table• Surface containment systems • Pre-testing water wells

Fracing • EPA frac study underway• On-going education and transparency by industry

needed

Regulatory/Government/Stakeholder

• Sitting on various industry associations to leverage relationships and provide input on regulation

• Holding “town hall” meetings in new areas to build landowner relationships and address local issues

Industry Challenges

Marcellus Summary

• Enerplus has a meaningful position in North America’s best shale gas play

• Marcellus offers significant future growth potential

• Results to date exceeding expectations

• 2011 operations focusing on appraisal drilling in our operated leasehold, continued appraisal and development drilling in our non-operated leasehold

• We’re managing the challenges

15