march 2013 italian ministry of economy and finance, treasury

TRANSCRIPT

What makes Italy attractive?

March 2013

Italian Ministry of Economy and Finance, Treasury Department

2

Export-oriented industry

Sound private sector

balance sheet

Strategic position

Strong manufacturing sector

Entrepreneurship and

high skills

Numerous reforms

undertaken

Key international player

Wide range of opportunities

Solid stock market

Increasingly flexible

labour market

Dynamic small and

medium enterprises

Italy’s strengths OVERVIEW

Italy in the global context

G8 member and the third largest economy in Euro Area.

One of the founders of the European Union.

An active player in the international scene.

A hinge-country between Europe and the Mediterranean

and Middle East regions.

3

KEY INTERNATIONAL PLAYER

4

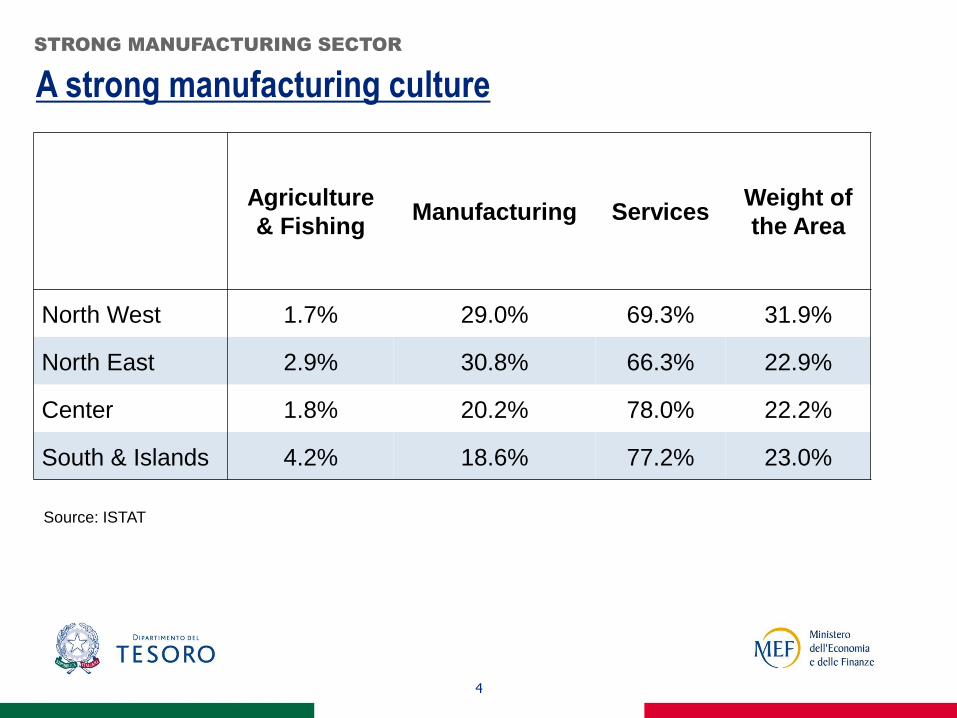

A strong manufacturing culture

STRONG MANUFACTURING SECTOR

Source: ISTAT

Agriculture

& Fishing Manufacturing Services

Weight of

the Area

North West 1.7% 29.0% 69.3% 31.9%

North East 2.9% 30.8% 66.3% 22.9%

Center 1.8% 20.2% 78.0% 22.2%

South & Islands 4.2% 18.6% 77.2% 23.0%

5

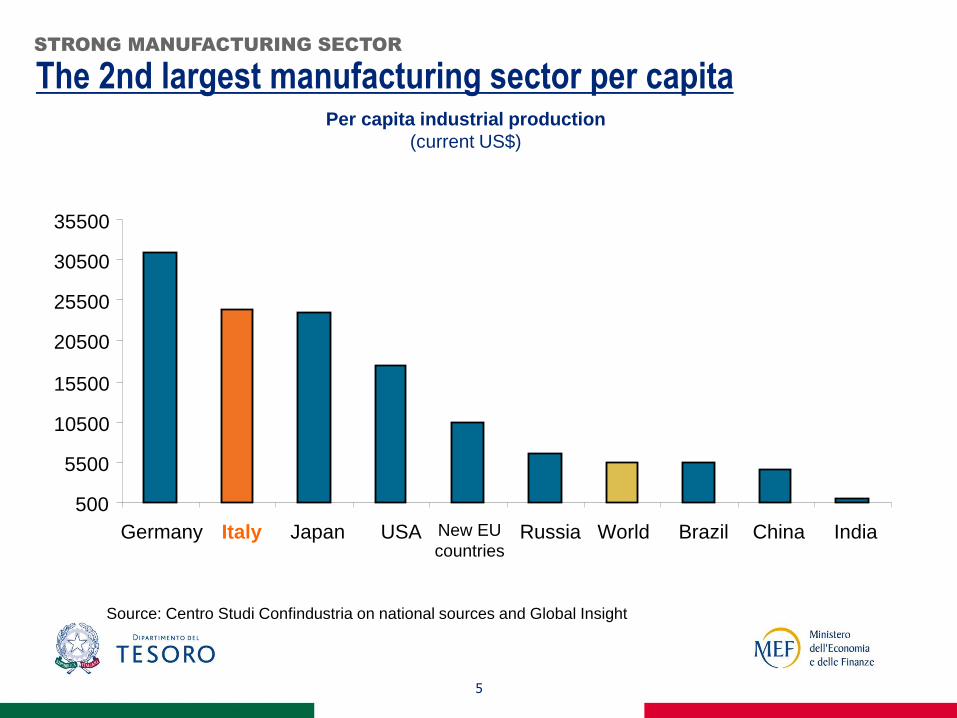

The 2nd largest manufacturing sector per capita

STRONG MANUFACTURING SECTOR

500

5500

10500

15500

20500

25500

30500

35500

Germany Italy Japan USA New EU

countries Russia World Brazil China India

Per capita industrial production

(current US$)

Source: Centro Studi Confindustria on national sources and Global Insight

6

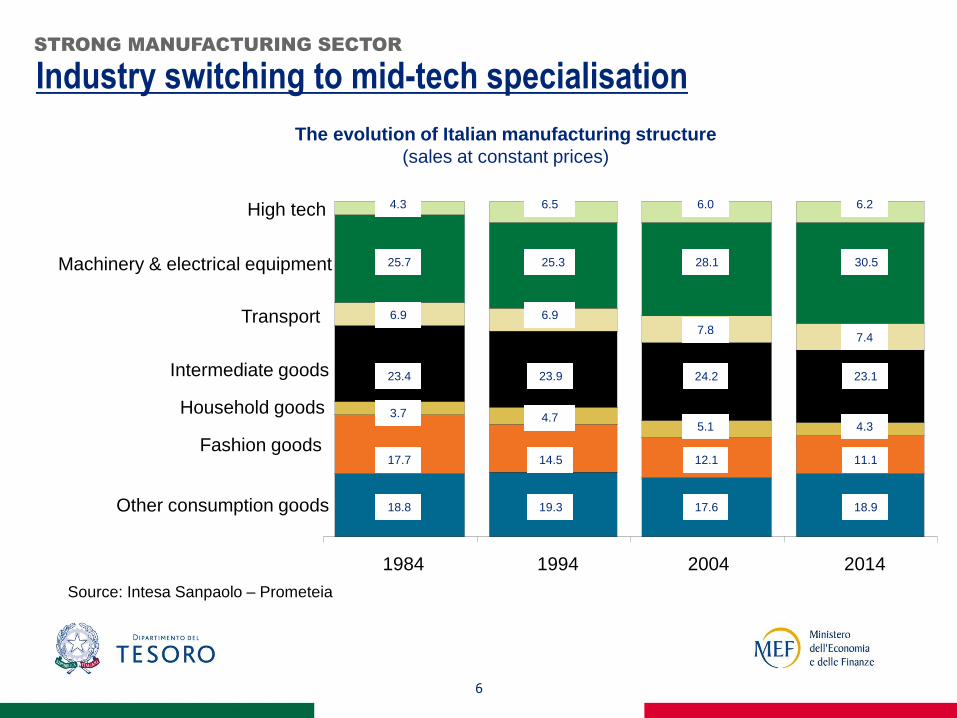

Industry switching to mid-tech specialisation STRONG MANUFACTURING SECTOR

Source: Intesa Sanpaolo – Prometeia

1984 1994 2004 2014

High tech

Machinery & electrical equipment

Transport

Fashion goods

Household goods

Intermediate goods

Other consumption goods

30.5 28.1 25.3 25.7

23.4 23.9 24.2 23.1

14.5 17.7

18.8 19.3 17.6 18.9

11.1 12.1

6.2 6.0 6.5 4.3

7.4 7.8

6.9 6.9

4.3 5.1 4.7 3.7

The evolution of Italian manufacturing structure

(sales at constant prices)

7

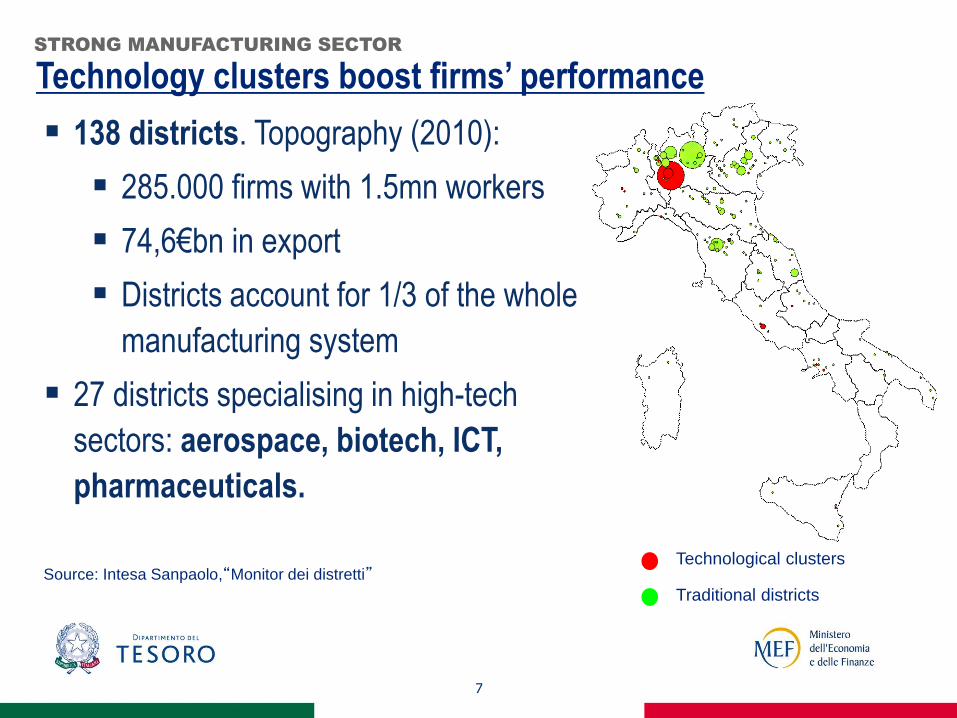

Technology clusters boost firms’ performance STRONG MANUFACTURING SECTOR

138 districts. Topography (2010):

285.000 firms with 1.5mn workers

74,6€bn in export

Districts account for 1/3 of the whole

manufacturing system

27 districts specialising in high-tech

sectors: aerospace, biotech, ICT,

pharmaceuticals.

Traditional districts

Technological clusters Source: Intesa Sanpaolo,“Monitor dei distretti”

8

Export excellence and leadership EXPORT-ORIENTED INDUSTRY

Note: The ranking is within the 5.517 world manufacturing.

Source: Fortis-Corradini Index, Un Comtrade, ISTAT, Fondazione Edison Analysis

Italy – 2010 World

Export Ranking Number of Products Value in USD billion

First 249 59

Second 334 60

Third 350 54

9

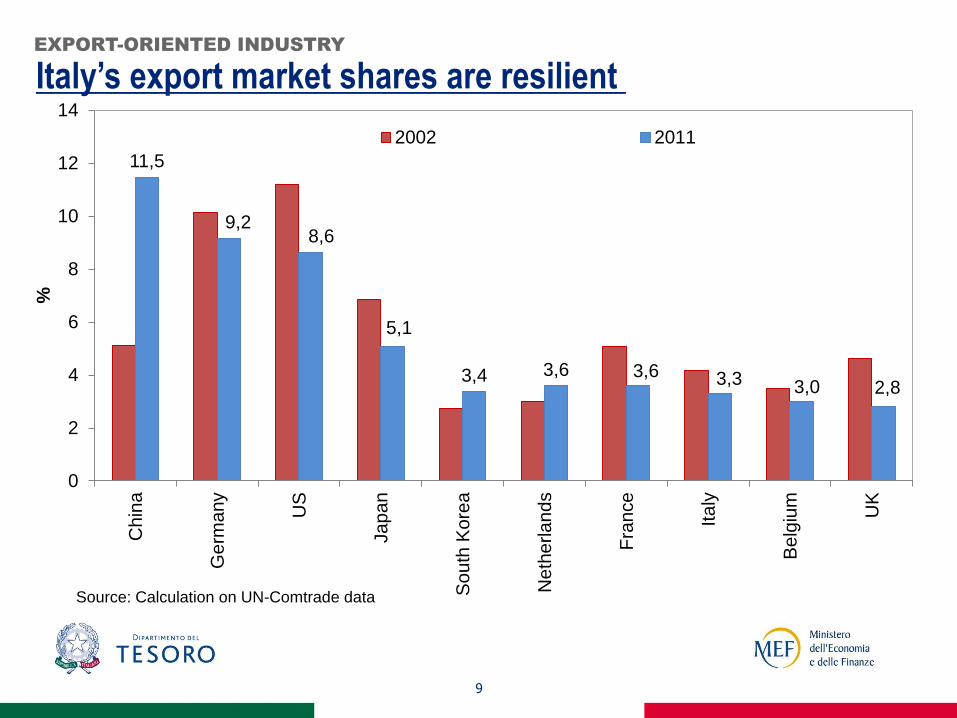

Italy’s export market shares are resilient

EXPORT-ORIENTED INDUSTRY

11,5

9,2 8,6

5,1

3,4 3,6 3,6 3,3 3,0 2,8

0

2

4

6

8

10

12

14

Ch

ina

Ge

rma

ny

US

Ja

pa

n

So

uth

Ko

rea

Ne

the

rla

nd

s

Fra

nce

Ita

ly

Be

lgiu

m

UK

%

Source: Calculation on UN-Comtrade data

2002 2011

10

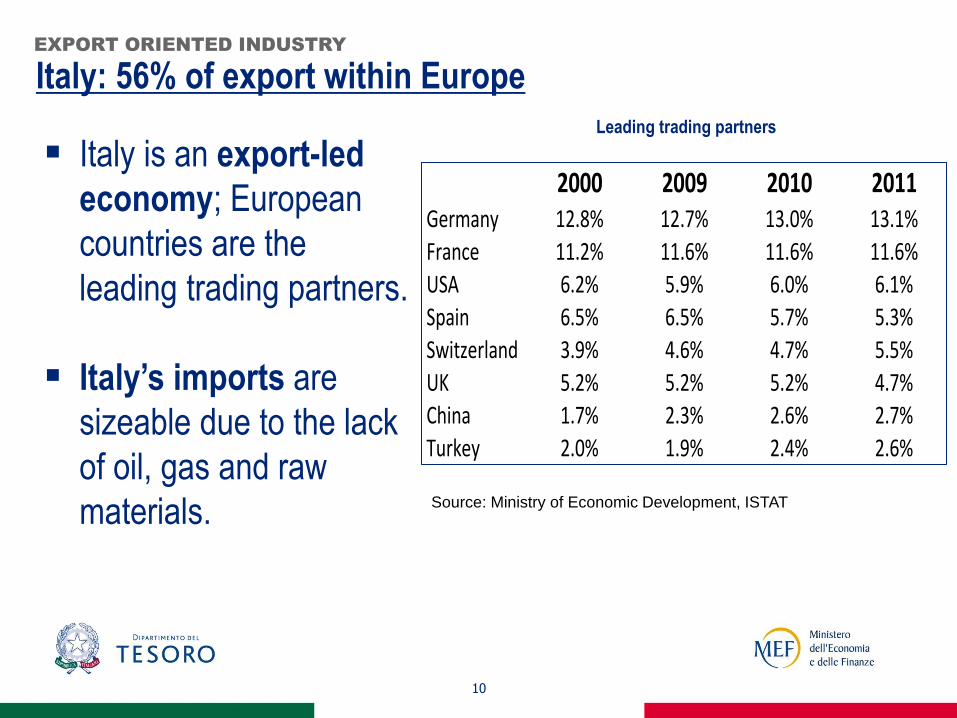

Italy: 56% of export within Europe EXPORT ORIENTED INDUSTRY

Source: Ministry of Economic Development, ISTAT

2000 2009 2010 2011Germany 12.8% 12.7% 13.0% 13.1%France 11.2% 11.6% 11.6% 11.6%

USA 6.2% 5.9% 6.0% 6.1%

Spain 6.5% 6.5% 5.7% 5.3%Switzerland 3.9% 4.6% 4.7% 5.5%

UK 5.2% 5.2% 5.2% 4.7%China 1.7% 2.3% 2.6% 2.7%

Turkey 2.0% 1.9% 2.4% 2.6%

Italy is an export-led

economy; European

countries are the

leading trading partners.

Italy’s imports are

sizeable due to the lack

of oil, gas and raw

materials.

Leading trading partners

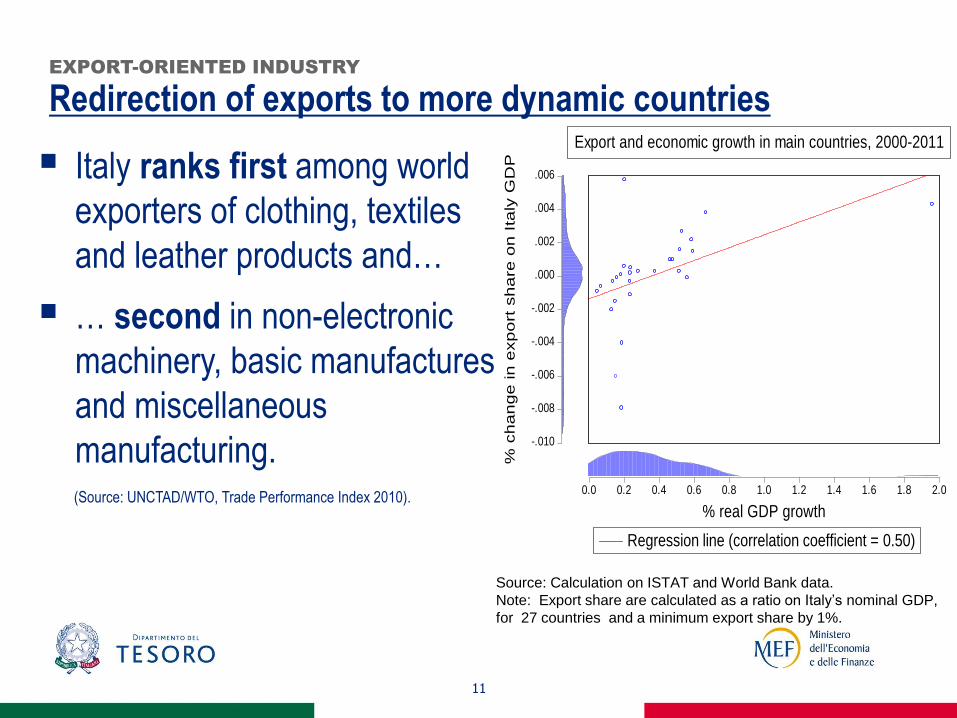

Redirection of exports to more dynamic countries

11

EXPORT-ORIENTED INDUSTRY

Italy ranks first among world

exporters of clothing, textiles

and leather products and…

… second in non-electronic

machinery, basic manufactures

and miscellaneous

manufacturing. (Source: UNCTAD/WTO, Trade Performance Index 2010).

Source: Calculation on ISTAT and World Bank data.

Note: Export share are calculated as a ratio on Italy’s nominal GDP,

for 27 countries and a minimum export share by 1%.

-.010

-.008

-.006

-.004

-.002

.000

.002

.004

.006

% c

ha

ng

e in

exp

ort

sh

are

on

Ita

ly G

DP

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6 1.8 2.0

% real GDP growth

Regression line (correlation coefficient = 0.50)

Export and economic growth in main countries, 2000-2011

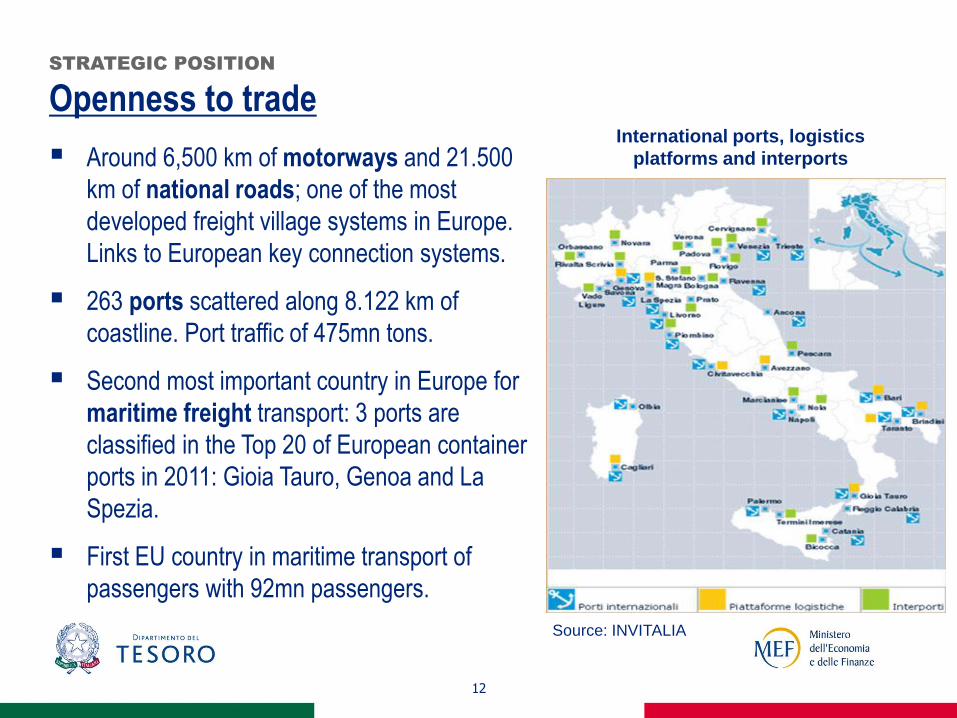

Openness to trade

12

STRATEGIC POSITION

Around 6,500 km of motorways and 21.500

km of national roads; one of the most

developed freight village systems in Europe.

Links to European key connection systems.

263 ports scattered along 8.122 km of

coastline. Port traffic of 475mn tons.

Second most important country in Europe for

maritime freight transport: 3 ports are

classified in the Top 20 of European container

ports in 2011: Gioia Tauro, Genoa and La

Spezia.

First EU country in maritime transport of

passengers with 92mn passengers.

International ports, logistics

platforms and interports

Source: INVITALIA

13

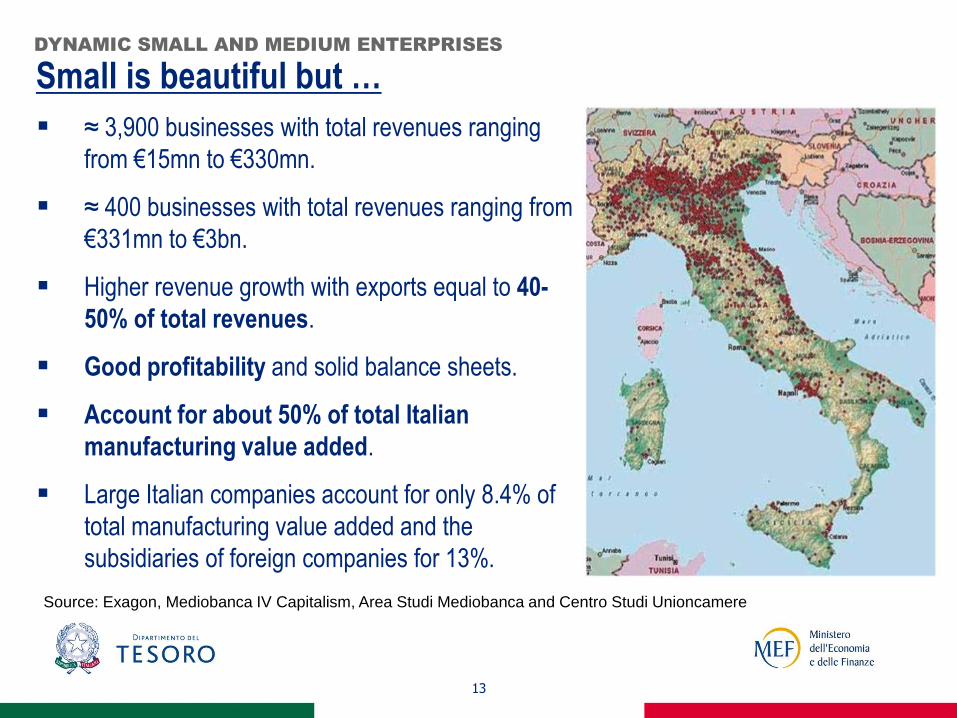

Small is beautiful but … DYNAMIC SMALL AND MEDIUM ENTERPRISES

≈ 3,900 businesses with total revenues ranging

from €15mn to €330mn.

≈ 400 businesses with total revenues ranging from

€331mn to €3bn.

Higher revenue growth with exports equal to 40-

50% of total revenues.

Good profitability and solid balance sheets.

Account for about 50% of total Italian

manufacturing value added.

Large Italian companies account for only 8.4% of

total manufacturing value added and the

subsidiaries of foreign companies for 13%.

Source: Exagon, Mediobanca IV Capitalism, Area Studi Mediobanca and Centro Studi Unioncamere

14

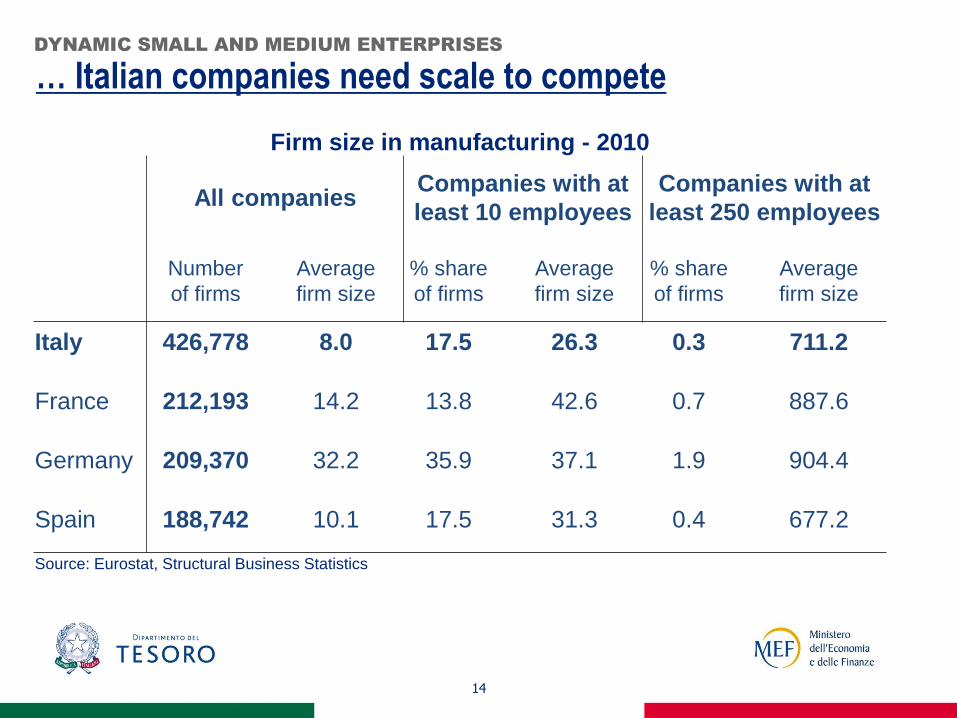

… Italian companies need scale to compete DYNAMIC SMALL AND MEDIUM ENTERPRISES

Firm size in manufacturing - 2010

All companies Companies with at

least 10 employees

Companies with at

least 250 employees

Number

of firms

Average

firm size

% share

of firms

Average

firm size

% share

of firms

Average

firm size

Italy 426,778 8.0 17.5 26.3 0.3 711.2

France 212,193 14.2 13.8 42.6 0.7 887.6

Germany 209,370 32.2 35.9 37.1 1.9 904.4

Spain 188,742 10.1 17.5 31.3 0.4 677.2

Source: Eurostat, Structural Business Statistics

15

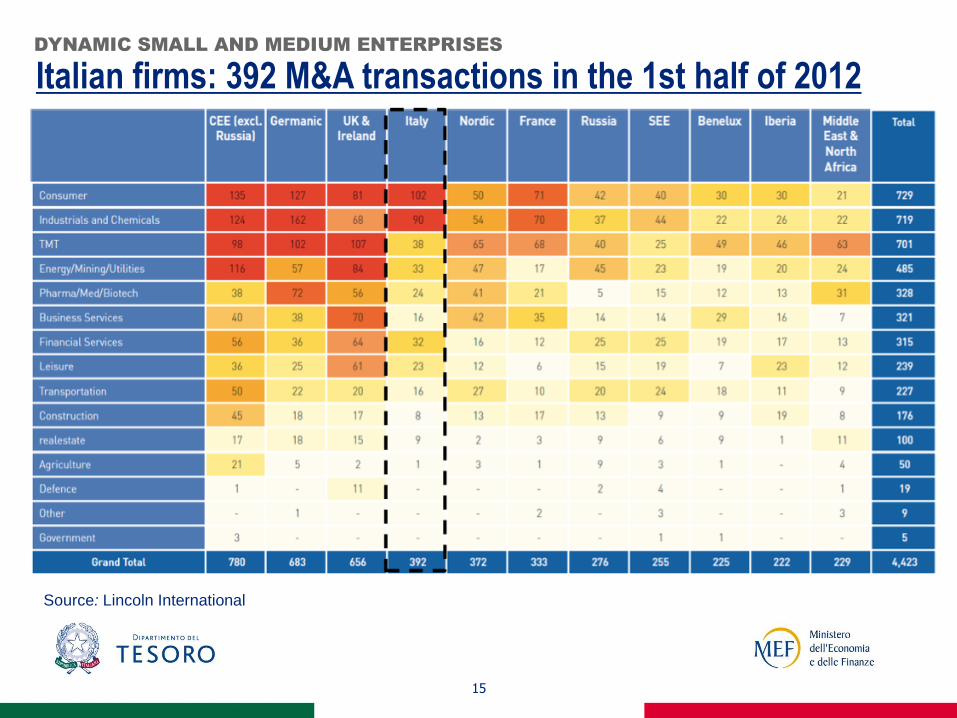

Italian firms: 392 M&A transactions in the 1st half of 2012 DYNAMIC SMALL AND MEDIUM ENTERPRISES

Source: Lincoln International

16

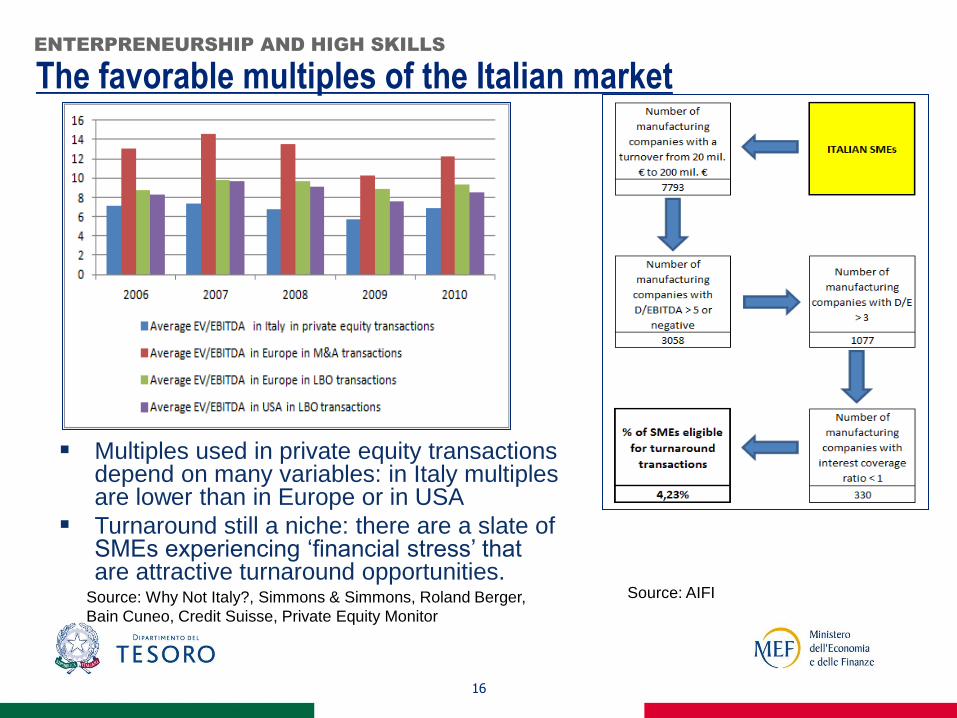

The favorable multiples of the Italian market ENTERPRENEURSHIP AND HIGH SKILLS

Multiples used in private equity transactions depend on many variables: in Italy multiples are lower than in Europe or in USA

Turnaround still a niche: there are a slate of SMEs experiencing ‘financial stress’ that are attractive turnaround opportunities.

Source: Why Not Italy?, Simmons & Simmons, Roland Berger,

Bain Cuneo, Credit Suisse, Private Equity Monitor

Source: AIFI

Entrepreneurial culture and high labour skill

17

ENTREPRENEURSHIP AND HIGH SKILLS

The Italian production network is based on strong

entrepreneurial culture, high quality products in several

economic sectors and export-oriented attitude.

Italy ranks 2nd in Europe in terms of manufacturing

companies with a skilled workforce, which in turn contributes

to the high quality of Made-in-Italy products.

High skills gained with on-the-job training and closely related

to traditional craftsmanship, not well captured by

international statistics.

18

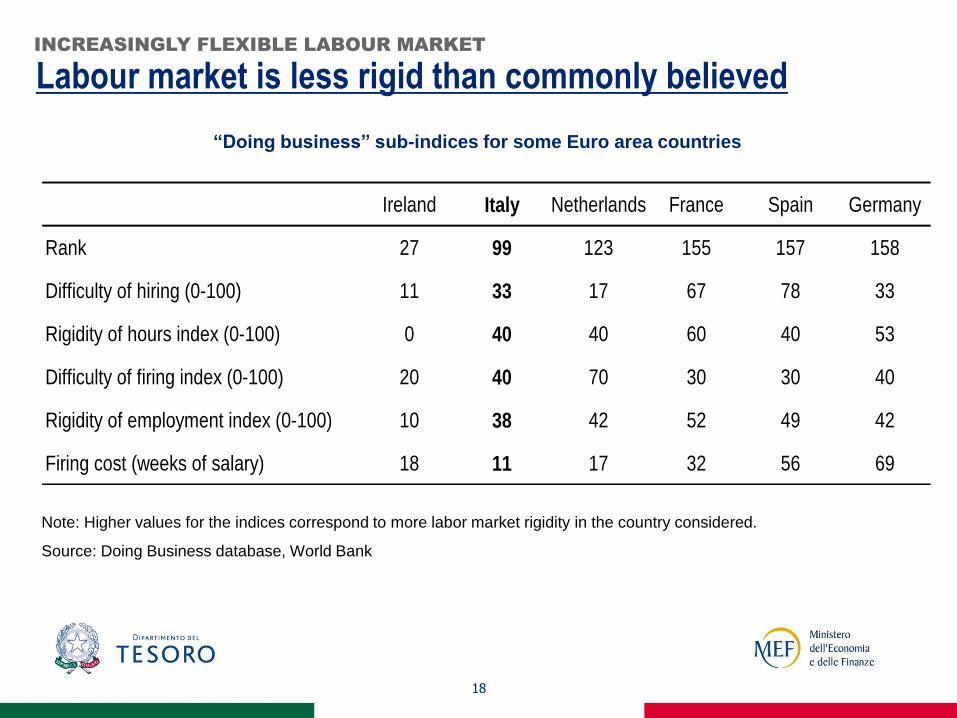

Labour market is less rigid than commonly believed INCREASINGLY FLEXIBLE LABOUR MARKET

Note: Higher values for the indices correspond to more labor market rigidity in the country considered.

Source: Doing Business database, World Bank

“Doing business” sub-indices for some Euro area countries

Ireland Italy Netherlands France Spain Germany

Rank 27 99 123 155 157 158

Difficulty of hiring (0-100) 11 33 17 67 78 33

Rigidity of hours index (0-100) 0 40 40 60 40 53

Difficulty of firing index (0-100) 20 40 70 30 30 40

Rigidity of employment index (0-100) 10 38 42 52 49 42

Firing cost (weeks of salary) 18 11 17 32 56 69

19

The recent reform has increased labour market flexibility

INCREASINGLY FLEXIBLE LABOUR MARKET

The recent labour market reform enhanced entry and exit

flexibility for apprenticeship and fixed-term contracts.

Apprenticeship is the preferential channel for young people

(up to 29 years old) to enter the labour market.

Hiring apprentices: employers benefit from fiscal incentives

for a 3-year period.

National agreement to help boosting labour productivity

Agreement between trade unions and employers’

associations to help boosting labour productivity by providing

for labour contracts that better reflect the needs of individual

companies.

A special fund is designed to cover the reduction of taxes on

productivity-linked wage increases set at local level.

A pact between generations is introduced, allowing for senior

workers to stay at work longer by smoothing retirement

transition and increasing employment of young workers.

20

INCREASINGLY FLEXIBLE LABOUR MARKET

21

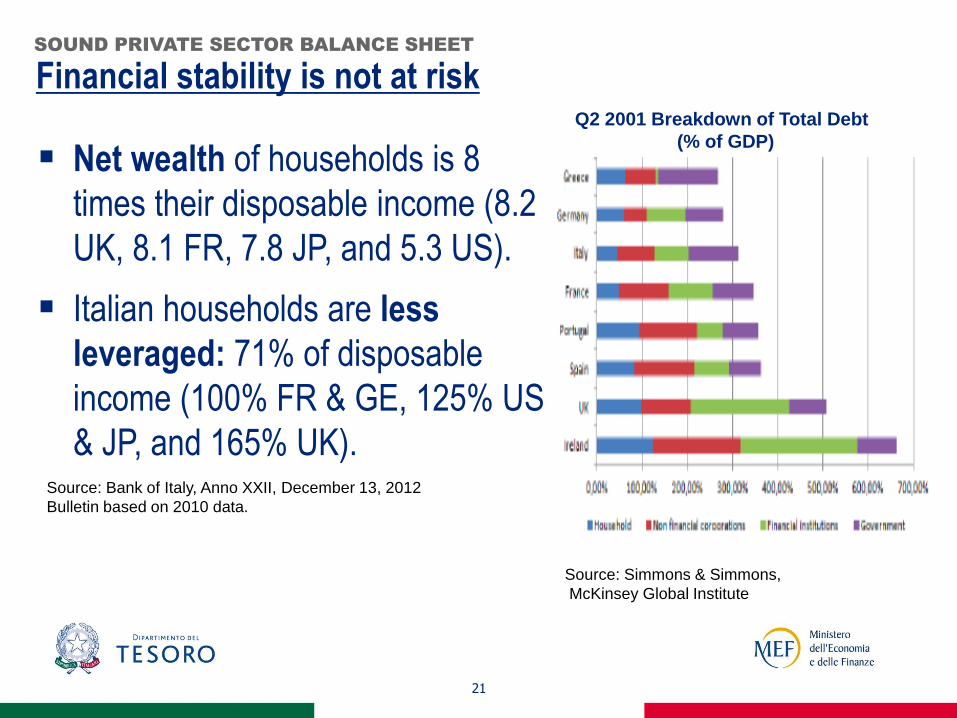

Financial stability is not at risk SOUND PRIVATE SECTOR BALANCE SHEET

Q2 2001 Breakdown of Total Debt

(% of GDP)

Source: Simmons & Simmons,

McKinsey Global Institute

Net wealth of households is 8

times their disposable income (8.2

UK, 8.1 FR, 7.8 JP, and 5.3 US).

Italian households are less

leveraged: 71% of disposable

income (100% FR & GE, 125% US

& JP, and 165% UK). Source: Bank of Italy, Anno XXII, December 13, 2012

Bulletin based on 2010 data.

22

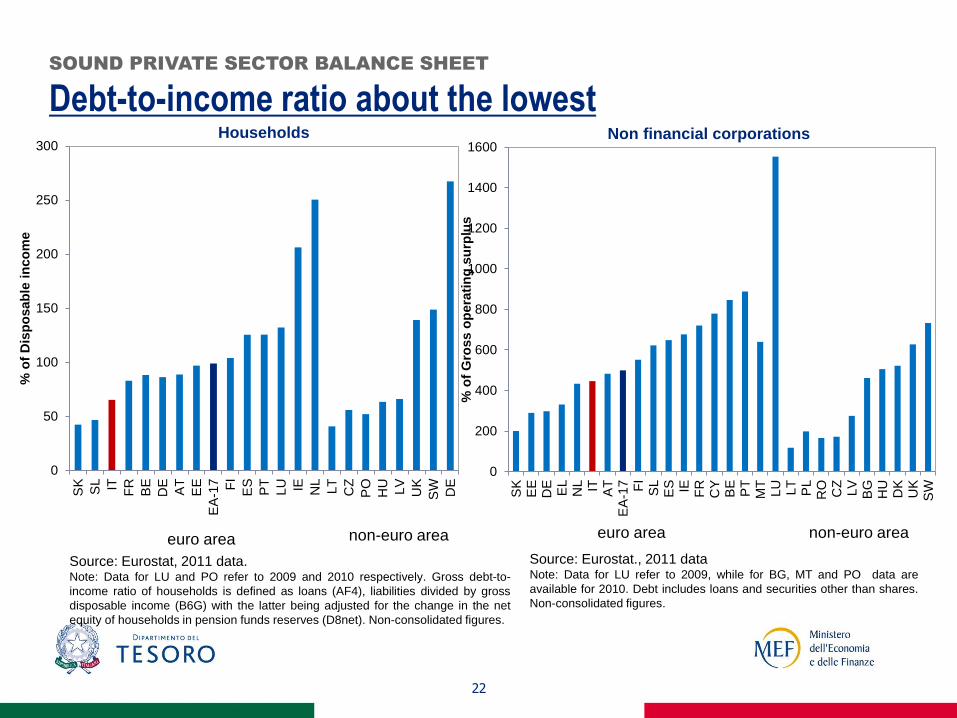

SOUND PRIVATE SECTOR BALANCE SHEET

Debt-to-income ratio about the lowest

Source: Eurostat, 2011 data. Note: Data for LU and PO refer to 2009 and 2010 respectively. Gross debt-to-

income ratio of households is defined as loans (AF4), liabilities divided by gross

disposable income (B6G) with the latter being adjusted for the change in the net

equity of households in pension funds reserves (D8net). Non-consolidated figures.

0

50

100

150

200

250

300

SK

SL IT FR

BE

DE

AT

EE

EA

-17 FI

ES

PT

LU IE NL

LT

CZ

PO

HU

LV

UK

SW DE

% o

f D

isp

osab

le i

nco

me

euro area non-euro area

Households

0

200

400

600

800

1000

1200

1400

1600

SK

EE

DE

EL

NL IT AT

EA

-17 FI

SL

ES IE FR

CY

BE

PT

MT

LU LT

PL

RO

CZ

LV

BG

HU

DK

UK

SW

% o

f G

ross o

pera

tin

g s

urp

lus

euro area non-euro area

Non financial corporations

Source: Eurostat., 2011 data Note: Data for LU refer to 2009, while for BG, MT and PO data are

available for 2010. Debt includes loans and securities other than shares.

Non-consolidated figures.

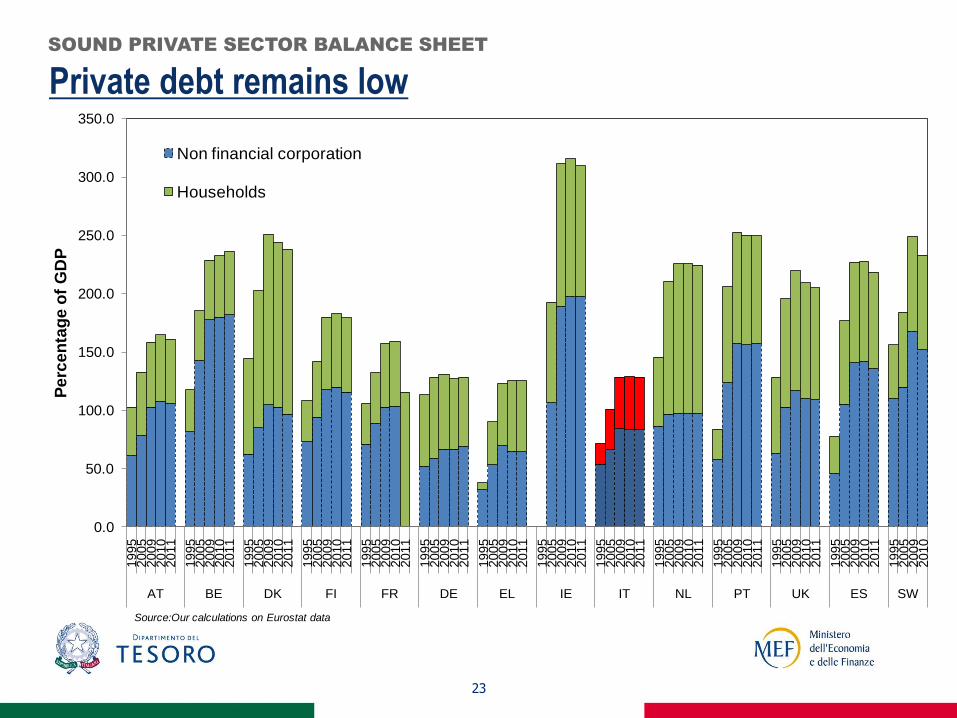

Private debt remains low

23

SOUND PRIVATE SECTOR BALANCE SHEET

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.01

99

52

00

52

00

92

01

02

01

1

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

20

11

19

95

20

05

20

09

20

10

AT BE DK FI FR DE EL IE IT NL PT UK ES SW

Pe

rce

nta

ge

of

GD

P

Non financial corporation

Households

Source:Our calculations on Eurostat data

24

Italian households’ wealth and its components

SOUND PRIVATE SECTOR BALANCE SHEET

Real

Estate

(62.8 % in 2011)

Financial

Assets

(37.2% in 2011)

Financial

Liabilities

(9.5% in 2011)

Net Wealth Euro

million

Houses

Source: Bank of Italy, Anno XXII, December 13, 2012 Bullettin

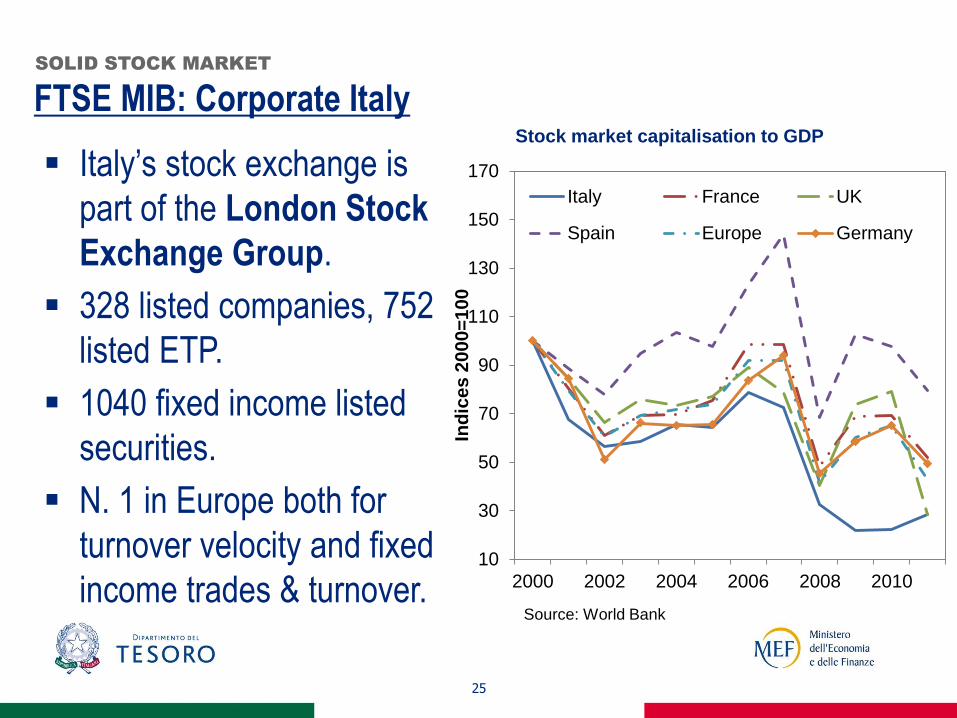

FTSE MIB: Corporate Italy

25

SOLID STOCK MARKET

10

30

50

70

90

110

130

150

170

2000 2002 2004 2006 2008 2010

Ind

ice

s 2

00

0=

10

0

Italy France UK

Spain Europe Germany

Source: World Bank

Stock market capitalisation to GDP

Italy’s stock exchange is

part of the London Stock

Exchange Group.

328 listed companies, 752

listed ETP.

1040 fixed income listed

securities.

N. 1 in Europe both for

turnover velocity and fixed

income trades & turnover.

26

FTSE MIB: Corporate Italy SOLID STOCK MARKET

1 ENI 67.38 126.06 7.45 Oil&Gas

2 Enel 30.03 83.92 3.46 ElectricUtilities3 Unicredit 21.68 14.89 1.95 RegionalBanks4 Generali 21.50 80.87 1.19 Insurance(Life)5 IntesaSanPaolo 21.32 9.79 2.18 RegionalBanks

6 Tenaris 18.66 8.18 1.32 Constr.Supplies&Fixtures7 Luxottica 14.61 6.96 0.529 Medicalequipment&Supplies8 Saipem 12.98 13.40 0.98 OilWellServices&Equipment9 TelecomItalia 12.85 30.26 -1.59 Communicationsservices

10 Snam 11.90 3.69 0.753 Naturalgasutilities

Top 10 by Capitalization (12-20-2012)

Capital. 2011Rev. NetIncomeEuro billion

Source: Borsa Italiana

Structural reforms for a sound business environment

27

STRONG REFORM MOMENTUM

Public administration: (1) access to all services on line; (2)

certified electronic mailing for communications; (3) reduced

administrative burden especially for networks of companies.

Support to businesses: (1) Aid for Economic Growth (ACE) to

reduce the tax burden on capital investment; (2) Central

Guarantee Fund to refinance financial transactions for SMEs.

Cohesion Action Plan: (1) education and professional training;

(2) digital agenda; (3) employment; and (4) railways.

Making bankruptcy procedure easier and reducing trial length.

28

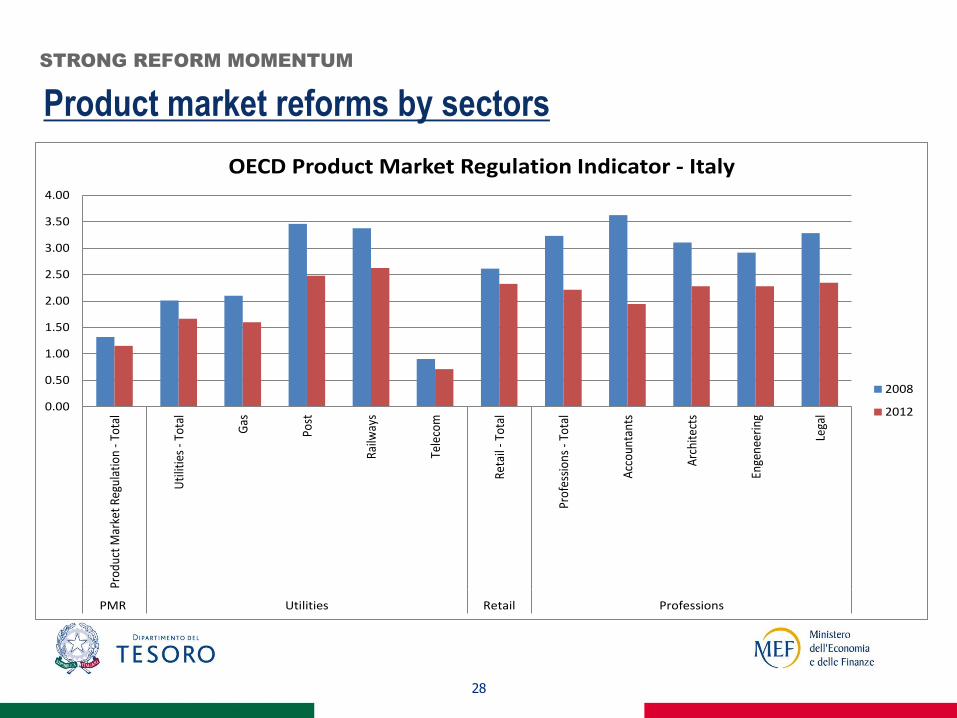

Product market reforms by sectors

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

Prod

uct

Mar

ket

Regu

lati

on -

Tota

l

Uti

litie

s - T

otal

Gas

Post

Railw

ays

Tele

com

Reta

il - T

otal

Prof

essi

ons

- Tot

al

Acc

ount

ants

Arc

hite

cts

Enge

neer

ing

Lega

l

PMR Utilities Retail Professions

OECD Product Market Regulation Indicator - Italy

2008

2012

STRONG REFORM MOMENTUM

A boost to competitiveness

29

STRONG REFORM MOMENTUM

Single point of contact (Desk Italia) to speed up the

internationalisation of Italian businesses and attract FDI.

Agency for Digital Italy to promote the establishment and the

development of major strategic projects.

More investment in innovation and research: (1) a special

fund for SMEs’ investment in R&D; (2) innovative start-ups to

improve innovation and youth employment

New opportunities for companies growing fast

30

Potential market of almost 60mn consumers for innovative

services (more than 30mn internet users) and products.

Countless opportunities to expand businesses in strategic

sectors such as logistics, tourism, renewable energy and

energy efficiency, green-tech and bio-tech projects.

Plan to boost infrastructure projects (€40bn funded): highways,

high speed trains, intermodal.

Financing of new projects.

WIDE RANGE OF OPPORTUNITIES

31

Sizeable reduction in pension spending due to reforms

Source: Update of 2012 Economic and Financial Document, September 20, 2012. Demographic

projections from Istat, central demographic scenario 2012

WIDE RANGE OF OPPORTUNITIES

12%

13%

14%

15%

16%

17%

18%

19%

2007 2010 2013 2016 2019 2022 2025 2028 2031 2034 2037 2040 2043 2046 2049 2052 2055 2058

Current Legislation Legislation before DL. 201/2011

Legislation before DL. 98/2011 Legislation before DL. 78/2010

Legislation before L. 243/2004

% o

f G

DP

Investment in undersized sectors due to population ageing

32

Investment opportunities both in health services and

childcare and long-term care as a result of the ageing process

and the recent pension reforms.

Recent pension reforms have made the social protection system

fully sustainable: large potential for developments in

alternative and private pension schemes.

WIDE RANGE OF OPPORTUNITIES

33

A new season for privatisation and dismissal of public assets

Conservative estimates of potential revenues from

privatisation of municipally-owned companies (some

listed) is about €200bn.

Real estate assets will be transferred from central and local

government to a real estate fund, which has a mandate to

create value and/or dismiss assets.

A political commitment to reduce the stock of debt by 1pp of

GDP per year with privatisation and dismissals.

WIDE RANGE OF OPPORTUNITIES