marine p&i - · pdf filep&i insurance providers. we believe that information is king,...

TRANSCRIPT

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 1

MARINE P&ICOMMERCIAL MARKET REVIEW OCTOBER 2014

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 2 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 3

CONTENTS

Commercial P&I Market Review 2014 4

Welcome From the Executive Director 7The World of P&I According to AJG 8Executive Summary 10P&I Fixed Premium Market Explained 16Review of the last 12 Months 19Non-IG P&I Market Overview 20Introduction to Market Facts & Figures 22

Market Facts and Figures 23

British Marine 24Carina 26Eagle Ocean Agencies Inc 28Hanseatic Underwriters 30Hydor AS 32Ingosstrakh Insurance Co 34Lodestar Marine Limited 36Navigators Insurance Company 38Osprey Underwriting Agency Limited 40RaetsMarine BV 42Rosgosstrakh Ltd 44

Non IG Mutual Market Facts & Figures 46China Shipowners Mutual Assurance Association 46Korea Shipowners Mutual P&I Association 48

Non-IG Charterers Facts & Figures 50Charterama BV 50Charterers P&I Club 52 Norwegian Hull Club 54

Industry Statistics 56

P&I Premium Income Development 58P&I Owned GT Development 60Average P&I Rate per GT Development 62P&I Charterers & Traders Premium Income Development 64Number of Vessels Insured Development 66Average Premium per Vessel Development (Charterers) 68Non-IG Mutual Owned GT Development 70Average Non-IG P&I Mutual Rate per GT Development 71 Rating Agency Analysis 72

Major Limiting Conventions & Statutes Affecting P&I Risks 74

Developments in the last 12 months 76

Marine Division Contacts 87

Marine One Stop Solution 88

FOUNDED BY ARTHUR J. GALLAGHER IN CHICAGO IN 1927, ARTHUR J. GALLAGHER & CO HAS GROWN TO BE ONE OF THE LARGEST, MOST SUCCESSFUL INSURANCE BROKERAGE AND RISK MANAGEMENT COMPANIES IN THE WORLD. WITH EXTRAORDINARY REACH AND DEPTH ACROSS INTERNATIONAL BORDERS, OUR PARENT GROUP EMPLOYS OVER 17,000 PEOPLE AND ITS GLOBAL NETWORK PROVIDES SERVICE IN MORE THAN 140 COUNTRIES.Outside the US, we use the brand name Arthur J. Gallagher.

Wherever and whenever there is an issue of risk we’re there for our clients - from individuals to small businesses to international conglomerates. Our people, our depth of technical expertise and our global reach is critical in delivering unrivalled coverage, risk management and placement expertise.

We work seamlessly across countries and international territories. Where we do encounter difficulties and complexities we meet them head on. We dismantle barriers never letting them get in the way.

We work tirelessly to provide solutions that drive value and competitive advantage for the benefit of all our clients and we liberate our people to do what they do best: promoting and protecting our clients’ interests. We just do not give up; whether it’s sourcing cover for the thatched cottage in England; cyber risks across European borders; complex coverage for the international supermarket chain; marine cargo in Australia; political risk coverage in developing economies; energy cover in extreme environments; or helping our banking partners with their comprehensive homeowner offer.

Family values have been core to our culture since our company was founded and this drives the way in which we, Arthur J. Gallagher, look after our clients. Since 1927 we have built our business for today. For tomorrow, we continue to invest in our business.

A BUSINESS WITHOUT BARRIERS

1

2

3

5

4

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 4 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 5

COMMERCIAL P&I MARKET REVIEW 2014

1

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 6 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 7

Arthur J. Gallagher is one of the leading global marine insurance brokers in the P&I industry sector. One of our core principles is transferring all pertinent market information, statistics as well as our independent reviews on the various P&I insurance providers. We believe that information is king, whereby we aim to enhance information streams to our clients and business partners, which is essential to remain successful this competitive market environment.

The Arthur J. Gallagher “Commercial P&I Market Review” was the first comprehensive review of its kind and compliments our mutual IG Club “Annual Pre-Renewal P&I Review” offering, which will be published later this autumn.

We closely monitor and analyse the P&I market, as it continues to evolve with its ever changing products, service, security, strength and flexibility. Our view at Arthur J. Gallagher is that the Non-IG market continues to play an important role the maritime insurance industry, offering alternative products and services to the small ship sector, where in previous years IG-P&I Clubs have lacked enthusiasm to participate in this risk profile.

As part of the P&I market evolution, we note however that some of the IG-Club managers have developed new fixed P&I facilities and have moved into the commercial market sector to diversify their product ranges, in order to increase revenue streams to enhance free-reserves further.

With the challenging shipping market still trading through this prolonged depressed freight market environment, the commercial P&I market may offer an opportunity for a segment of the world’s small ship operators to reduce their operational expenditure, which this review will offer more detail on.

The “AJG Commercial P&I Market Review” will focus on the leading fixed premium, non-IG mutual and charterers liability facilities, which are generally accessed via London brokers.

Arthur J. Gallagher P&I remains at the forefront as industry leaders, this is something we are extremely proud of and demonstrates our unrivalled value added service and commitment to our clients and partners alike.

Yours sincerely,

Malcolm Godfrey

Executive Director Marine Division | Specialty Risks

WELCOME TO OUR THIRD ANNUAL COMMERCIAL P&I MARKET REVIEW

WELCOME FROM THE EXECUTIVE DIRECTOR

MALCOM GODFREY EXECUTIVE DIRECTOR | MARINE DIVISION | SPECIALTY RISKS

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 8 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 9

THE WORLD OF P&I ACCORDING TO AJG

COMMERCIAL P&I MARKET REVIEW 2014 THE WORLD OF P&I ACCORDING TO AJG

USA, NEW YORK

• Eagle Ocean Marine

INTERNATIONAL GROUP P&I CLUB

COMMERCIAL P&I MARKET

NON-IG MUTUAL P&I CLUB

UK, LONDON

• Britannia P&I Club

• London P&I Club

• Shipowners P&I Club

• Standard Club

• Steamship Mutual P&I

• The UK Club

• West of England

UK, LONDON

• British Marine (QBE Group)

• Carina

• Lodestar Ltd

• Navigators P&I

• Osprey Underwriting Agency

• Charterers P&I Club

USA, NEW YORK

• American Club

UK, NEWCASTLE

• North of England

CHINA, BEIJING

• China P&I Club

KOREA, SEOUL

• Korea P&I Club

JAPAN, TOKYO

• Japan P&I Club

GREECE, ATHENS

• Aigaion Insurance Co. SA

NORWAY, BERGEN

• Norwegian Hull Club

NORWAY, OSLO

• Hydor AS

RUSSIA, MOSCOW

• Ingosstrakh

• Rosgosstrakh Ltd

GERMANY, HAMBURG

• Hanseatic Underwriters

NETHERLANDS, ROTTERDAM

• RaetsMarine BV

• Charterama BV

NORWAY, OSLO

• Skuld P&I

SWEDEN, GOTHENBURG

• Swedish Club

NORWAY, ARENDAL

• Gard AS

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 10 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 11

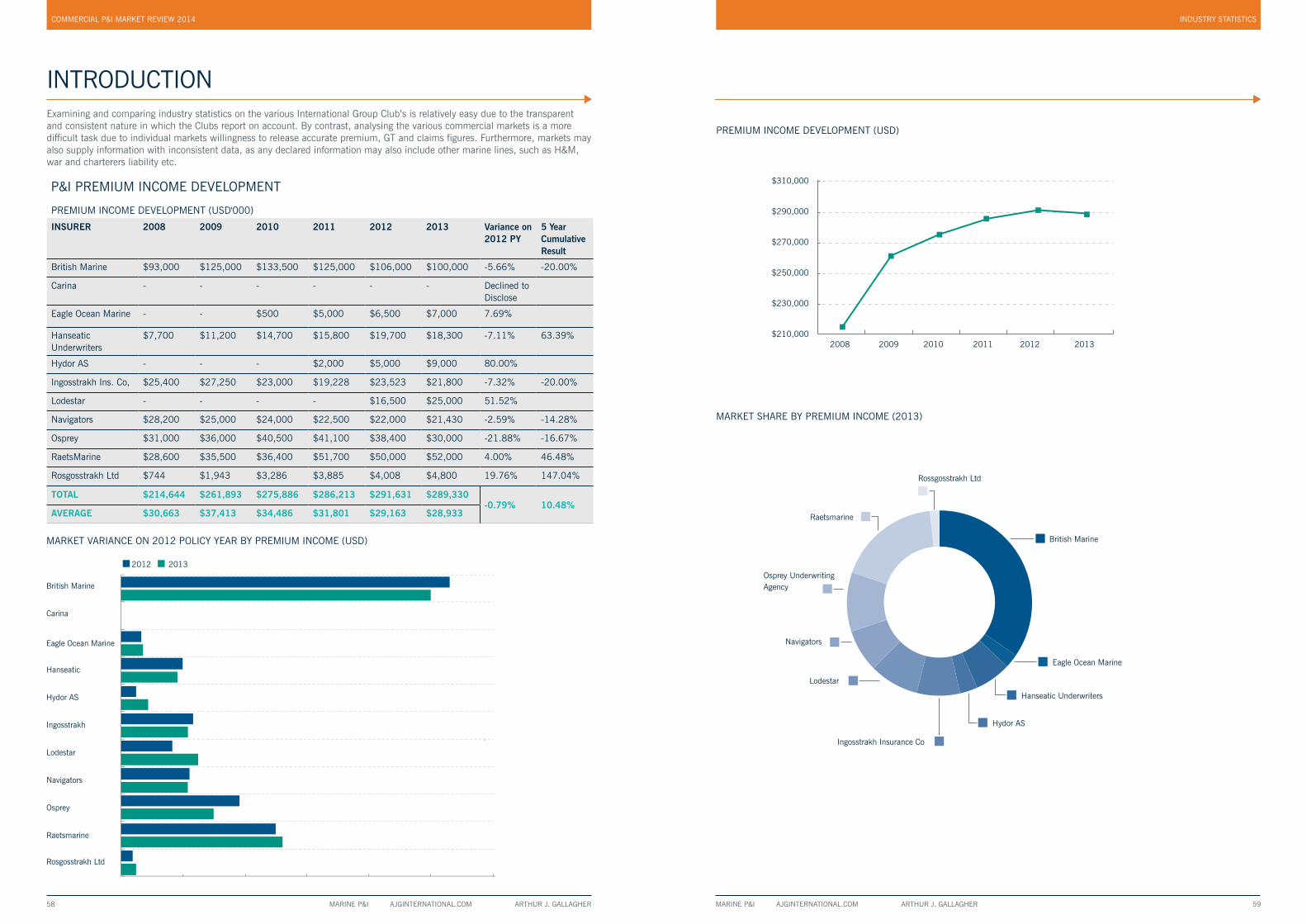

2013 HIGHLIGHTS The allure of fixed premium P&I has intensified in the last five years, which can be discerned by the abundance of capacity and more competition than ever before. With over twenty- five fixed premium insurers and agency facilities operating within the P&I commercial market sector, when will this expansion period end?! The fixed P&I market is viewed as a dynamic marketplace, with aggressive competition, without IGA (International Group Agreement) constraints slowing down business transferring for a better deal. With the expansion and oversupply diluting fixed market premiums annually, could the fixed market move into a loss making business like their hull & machinery and IG-P&I Club counterparts, if rates continue to diminish?

FIXED P&I RATES CONTINUE TO FALL2013 saw the market average rate per GT reduce by another -5.48%, which is a significant difference from the -2.07% average reduction in 2012. In the last five years owned fixed P&I rates have fallen by an average of -9.84%, which suggests that the new entrant expansion cycle, combined with oversupply continued to prolong the commercial soft market

environment. The average P&I owned fixed rate per GT is approximately US$ 6.55 PGT, which is the lowest average in the last five years. The owned P&I market premium decreased from US$ 291.6 million from US$ 289.3 million (-0.79%) in 2012 and the GT development also grew by 2.085 million GT since 2012 (+4.9%).

BUSINESS ENVIRONMENT

2014 has revealed more challenges for some of the new fixed premium market facilities, in particular those new entrants competing for market share. All fixed premium facilities are backed by insurance organisations providing capacity (reinsurance support). One of the major challenges amongst the new entrants is to balance growth expectations to avoid backers losing interest and forcing a potential market exit, by withdrawing reinsurance support. With the average owned P&I rate at a five year low and with more facilities entering an already soft market, only time will tell as to how long some of these facilities will last. However, if a facility is forced out of the market, another new entrant will surely take its place as there may be need for some insurers to diversify their product ranges to meet various solvency and capital adequacy requirements. Therefore in short we do not see the market consolidating in the short to medium term; however we see the market continuing to expand with average rates continuing to decrease.

NEW ENTRANT DEVELOPMENT2013 was an admirable year for some of the commercial markets newest agency facilities, with Hydor A/S making premium gains of +80% (US$ 4 million), GT gains of 8.6%, reporting an average rate per GT US$ 6.92 (a 65.9% increase on the 2012 rate per GT). Lodestar Ltd has also quickly become a top five facility (by premium income) with a twelve month premium gain of +51.5% (US$ 8.5 million), average rate per GT development of (-2.2%) suggests that the facility has managed to somewhat balance competition and underwriting discipline during the 2013 policy year. Lodestar have written US$ 25 million of premium income in the last two years proving that market relationships and broker support is paramount for success in the marine insurance industry.

THE OLD(ISH) GUARDThe established and intermediate fixed P&I providers continue to grapple for market share during this new entrant expansion phase. In 2013 many of the established providers saw premium income decline in the region of (-2.5%) to (-21.8%) on a twelve month basis, and up to (-20%) on a five year basis. RaetsMarine was one of the only established fixed premium providers to see growth in 2013, with an owned premium increase of +4% (US$ 2 million). The established and intermediate fixed markets currently command a total owned P&I premium income of US$ 243.5 million or 84.17%

of the fixed premium owned market, therefore in actual premium terms the new entrant expansion period has seen approximately US$ 45.8 million (15.83%) transfer to new entrant fixed facilities in the last four years (this figure is likely to be more if you consider what IG facilities have taken from the market also). We must not ignore the fact that part of every renewal will include clients leaving the marine industry, selling their assets or laying up vessels (however the owned GT grew by 4.96% in 2013), therefore the reported market development fluctuations are not a result of competition or business transferring alone. We have generally observed that once a facility enters into the “established” category, as a mature business, growing income and market share becomes more of a challenge. Instead the battle of maintaining market share ultimately becomes the test itself. These established markets may need to find a way to diversify and evolve in order to persevere and develop their facilities further.

IG CLUB DIVERSIFICATION Eleven of the thirteen IG P&I Clubs (or Club Managers) offer a fixed premium alternative, with four new facilities being launched only within the last two years. 20th February 2014 saw the soft launch of the new Standard Club fixed premium P&I facility, which was set up to back the newly formed Turkish P&I Agency. The Standard Club fixed facility, is backed by 100% by Lloyds of London and can offer limits up to USD 500 million, targeting vessels up to 5,000 GT. In early March, the completion of the Sunderland Marine and the North of England P&I Association merger was announced, to create the North Group, which adds another re-branded player to fixed premium market. Looking back to autumn 2013, Japanese insurance company Mitsui Sumitomo and Skuld P&I joined forces to facilitate Mitsui offering a blue-water fixed-premium P&I product to the Japanese ship-owning community. This diversification strategy will no doubt put pressure on the existing Japan P&I Club Naiko (Coastal) Class to maintain a local market majority share. If fixed market trends follow the same trajectory then the Japanese small ship operators will be pleased to see fixed P&I rates fall in the region. With the London and UK Club being the only two IG Clubs without a fixed premium P&I facility (excluding charterer’s liability insurance), will we soon see all thirteen IG Clubs compete in this sector within the current IGA framework?

TWELVE MONTH P&I OWNED MARKET DEVELOPMENT PERFORMANCE INDICATOR

PREMIUM INCOME USD

-0.07%

GROSS TONNAGE

+4.9%

AVERAGE RATE PER GT (PGT)

-5.48%2012 PY 2013 PY 2012 PY 2013 PY 2012 PY 2013 PY

USD 291,631,000 USD 289,330,000 42,052,000 44,137,000 USD 6.935 USD 6.555

COMMERCIAL P&I MARKET REVIEW 2014 EXECUTIVE SUMMARY

“SURVIVAL OF THE FITTEST”THE FIXED P&I MARKET MUST EVOLVE TO STAY AHEAD OF THE GAME

ALEX VULLO ASSOCIATE DIRECTOR | MARINE DIVISION | SPECIALTY RISKS

$7.800

$7.600

$7.400

$7.200

$7.000

$6.800

$6.600

$6.400

$6.200

$6.000

AVERAGE RATE PER GROSS TON DEVELOPMENT (US$)

2008 2009 2010 2011 2012 2013 2008 2009 2010 2011 2012 2013

AVERAGE RATE PER GT DEVELOPMENT (US$ PGT)

$7.700

$7.500

$7.300

$7.100

$6.900

$6.700

$6.500

2009 2010 2011 2012 2013

AVERAGE PREMIUM PER VESSEL DEVELOPMENT (US$)

$6,550

$6,450

$6,350

$6,250

$6,150

$6,050

$5,950

$5,850

$5,750

$5,6502008 2009 2010 2011 2012 2013

OWNED P&I PREMIUM DEVELOPMENT (US$’000)

$310,000

$290,000

$280,000

$270,000

$260,000

$250,000

$240,000

$230,000

$220,000

$210,000

$7.800

$7.600

$7.400

$7.200

$7.000

$6.800

$6.600

$6.400

$6.200

$6.000

AVERAGE RATE PER GROSS TON DEVELOPMENT (US$)

2008 2009 2010 2011 2012 2013 2008 2009 2010 2011 2012 2013

AVERAGE RATE PER GT DEVELOPMENT (US$ PGT)

$7.700

$7.500

$7.300

$7.100

$6.900

$6.700

$6.500

2009 2010 2011 2012 2013

AVERAGE PREMIUM PER VESSEL DEVELOPMENT (US$)

$6,550

$6,450

$6,350

$6,250

$6,150

$6,050

$5,950

$5,850

$5,750

$5,6502008 2009 2010 2011 2012 2013

OWNED P&I PREMIUM DEVELOPMENT (US$’000)

$310,000

$290,000

$280,000

$270,000

$260,000

$250,000

$240,000

$230,000

$220,000

$210,000

AVERAGE RATE PER GT DEVELOPMENT (USD PGT) OWNED P&I PREMIUM DEVELOPMENT (USD'000)

OWNED P&I (5 YEAR DEVELOPMENT)

Policy Year Premium Income (USD ‘000)

Market GT (‘000) Av. Rate Per GT Change %

2009 USD 261,893 36,019 USD 7.271 -

2010 USD 275,886 36,022 USD 7.659 +5.33%

2011 USD 286,213 40,417 USD 7.082 -7.54%

2012 USD 291,631 42,052 USD 6.935 -2.07%

2013 USD 289,330 44,137 USD 6.555 -5.48%

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 12 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 13

FIVE YEAR HIGHS & LOWSThe overall fixed owned market premium reduced by -0.79% ($2.3 million) in 2013, where the total premium reported stood at US$ 289.3 million. However, the overall GT development increased by 4.96% (2.085 million GT), suggesting that a fraction of business transferred to IG fixed facilities in 2013. The average owned fixed rate per GT reduce by 5.48% to US$ 6.55 per GT, compared to the 2012 average

rate of US$ 6.93 per GT, representing a new five year low, suggesting that premiums are continuing to dilute. New entrant Eagle Ocean Marine currently has the highest rate per GT at US$ 11.864, with a small GT level of 0.59 million GT, whereas established RaetsMarine has the second lowest rate of US$ 3.38 per GT but has the highest level of GT reported at 15.3 million.

COMMERCIAL P&I MARKET REVIEW 2014 EXECUTIVE SUMMARY

TWELVE MONTHS AVERAGE RATE PER GT DEVELOPMENT (MARKET OVERVIEW)

NON-IG CHARTERERS & TRADERS MARKET Since the start of the financial and shipping downturn in 2008/09 the charterers liability market volume has slowly increased by 39.51% in the last five years, albeit reported as a deficit of -0.31% in 2013 (-1,437 vessels). Premiums on the other hand have also increased slightly by +1.61% at US$ 75.9 million reported for 2013, compared to US$ 74.7 million in 2012 (+1.2 million). The average premium per vessel has

also slightly decreased by 1.33%. The charterer’s liability market development figures are based on premium vs. volume averages to demonstrate how the market premium rating for this risk profile has developed in the past five years. It is important to note that a charterer may be on risk from anywhere between 1 day and 365 days within the policy period, which is not taken into account on the average premium vessel per figure.

CHARTERERS & TRADERS

Policy Year Premium

Income (USD’000)

No. Vessels Insured Av. Premium Per vessel

Change %

2009 USD 65,050 32,901 USD 6,493 -

2010 USD 68,400 39,501 USD 5,828 -10.23%

2011 USD 69,150 42,463 USD 5,851 +0.39%

2012 USD 74,700 46,043 USD 5,867 +0.28%

2013 USD 75,900 45,900 USD 5,789 -1.33%

NON-IG MARKET DEVELOPMENTWe have looked back to the policy years ranging from 2008 to 2012 in view of the China P&I Club not yet releasing their 2013 report on accounts. The five year development statistics reveal that the average rate per ton has moved back to the 2008 policy level, albeit the overall GT has increased by more

than doubled during this time. The Korean P&I Club however reportedly grew their 2013 P&I income by 3% (2013 income at US$ 31.1 million) and their GT grew by 53.74% to 18.1 million GT.

$7.800

$7.600

$7.400

$7.200

$7.000

$6.800

$6.600

$6.400

$6.200

$6.000

AVERAGE RATE PER GROSS TON DEVELOPMENT (US$)

2008 2009 2010 2011 2012 2013 2008 2009 2010 2011 2012 2013

AVERAGE RATE PER GT DEVELOPMENT (US$ PGT)

$7.700

$7.500

$7.300

$7.100

$6.900

$6.700

$6.500

2009 2010 2011 2012 2013

AVERAGE PREMIUM PER VESSEL DEVELOPMENT (US$)

$6,550

$6,450

$6,350

$6,250

$6,150

$6,050

$5,950

$5,850

$5,750

$5,6502008 2009 2010 2011 2012 2013

OWNED P&I PREMIUM DEVELOPMENT (US$’000)

$310,000

$290,000

$280,000

$270,000

$260,000

$250,000

$240,000

$230,000

$220,000

$210,0002009 2010 2011 2012 2013

$80,000

$75,000

$70,000

$65,000

$60,000

$55,000

PREMIUM INCOME DEVELOPMENT (US$)

2012 2013

$0.000 $2.000 $4.000 $6.000 $8.000 $10.000 $12.000

Average$6.555

British Marine

Carina

Eagle Ocean Marine

Hanseatic

Hydor AS

Ingosstrakh

Lodestar

Navigators

Osprey

Raetsmarine

Rosgosstrakh Ltd

NON-IG MUTUAL

Policy Year Premium

Income (USD’000)

No. Vessels Insured Av. Premium Per vessel

Change %

2008 USD 46,749 21,506 USD 4.480 -

2009 USD 63,868 25,218 USD 5.104 +13.93%

2010 USD 76,203 30,860 USD 5.788 +13.4%

2011 USD 90,196 37,807 USD 5.175 -10.59%

2012 USD 97,311 43,173 USD 4.695 -9.28%

TWELVE MONTH MARKET DEVELOPMENT BY OWNED P&I PREMIUM INCOME (USD ‘000)

# 2012 P&I Market

P&I owned income USD ‘000

Change # 2013 P&I Market

P&I owned income USD ‘000

Result

1 British Marine USD106,000 1 British Marine USD 100,000

-USD 6,000

2 Raetsmarine USD50,000 2 Raetsmarine USD 52,000 +USD 2,000

3 Osprey USD 38,400 3 Osprey USD 30,000 -USD 8,400

4 Ingosstrakh USD 23,523 4 Lodestar USD 25,000 +USD 8,500

5 Navigators USD 22,000 5 Ingosstrakh USD 21,800 -USD 1,723

6 Hanseatic USD 19,700 6 Navigators USD 21,430 -USD 570

7 Lodestar USD 16,500 7 Hanseatic USD 18,300 -USD 1,400

8 Eagle Ocean USD 6,500 8 Hydor AS USD 9,000 +USD 4,000

9 Hydor AS USD 5,000 9 Eagle Ocean USD 7,000 +USD 500

10 Rosgosstrakh USD 4,008 10 Rosgosstrakh USD 4,800 +USD 792

AVERAGE PREMIUM PER VESSEL DEVELOPMENT (USD) PREMIUM DEVELOPMENT (USD'000)

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 14 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 15

COMMERCIAL P&I MARKET OUTLOOK 2014/2015

CHALLENGES AHEAD“Survival of the fittest” may be an apt term to generalise the fixed premium market during this rapid expansion phase. Challenging times are certainly ahead for all market participants fighting for market share and new opportunities, particularly in a market where the “buyer” has control to pressure existing carriers to reduce premiums or move elsewhere for a better deal. How markets ultimately manage these factors, combined with claims control, loss prevention and reinsurance costs will continue to put pressure on carriers to survive for the future. Whilst painting a bleak picture of what challenges are indeed ahead, over capacity will mean rates will continue to fall in 2014/15.

We anticipate that average market rate per GT will continue to fall in 2014/15 as the effect of increased competition continues to re-shape the market. Each facility will no doubt need to increase their individual market share, to meet growth expectations and budgets, whereas others will need to simply defend their existing portfolio in this buyer’s market. If current trends continue, we expect to see another 5% to 10% reduction in the average rate per ton in 2014/15, bringing the average rate per ton down to between US$ 6.22 and US$ 5.89 per GT.

THE ESTABLISHED MARKETS• Maintaining market share will be the challenge for all

established markets in 2014/15, which is no change from the previous two years, as competition intensifies. We anticipate that the established markets will continue to maintain their existing strategies, whilst developing business in more focused geographical areas, as opposed to general expansion. On the whole we expect to see a further downward trend in premium, GT and rate per GT development whilst the market continues to develop during this expansion cycle.

• Balanced growth will be the challenge for the “intermediate” market facilities in 2014/15, in 2013 we saw most facilities “buy in” tonnage whereby their average rates per GT reduced by up to 17% in one year, resulting in further premium dilution.

• The new entrant and IG Club new fixed facilities will continue to apply pressure on the market; therefore we expect to see this sector drive down premiums further in 2014/15.

CONCLUSIONWe believe that the fixed premium market must look to evolve to stay ahead of market competition for the long term, this is more important for the established markets that are seeing significant downward trends in premiums, tonnage and average rate deterioration. The established and intermediate markets may need to consider offering new marine related products to complement their existing product ranges, as simply reducing rates at renewal and competing more aggressively for growth will only dilute premiums further and will ultimately add to fixed P&I becoming a loss making business in the future.

The three tiers of market facility will continue to battle in 2014/15, where established and intermediate markets will need to react to premium losses sustained in 2013/14. The new entrants will continue to grow at a measured pace whilst enhancing their reputation and developing their market presence.

The fixed premium market continues to play an important role in the marine insurance industry and as this market expands, so does market awareness, credibility and its desirability. All fixed facilities ultimately offer the same product and compete for the same business; however clients will need to be carefully guided on suitable market candidates in the selection process, as there are many factors and disparities offered by each carrier, such as service, reputation, flexibility at renewal, ability to put up security and most importantly pay claims. With rate reductions and even more capacity on the horizon clients will need to choose wisely to take advantage of this prevailing soft market, we at Arthur J. Gallagher are here to help!

COMMERCIAL P&I MARKET REVIEW 2014

BritishMarine

Carina Eagle Ocean Marine

2012 2013

Hanseatic Hydor AS Ingosstrakh Lodestar Navigators Osprey Raetsmarine RosgosstrakhLtd

$12.000

$10.000

$8.000

$6.000

$4.000

$2.000

$0.000

$6.555

2008 2009 2010 2011 2012

$6.000$5.800$5.600$5.400$5.200$5.000$4.800$4.600$4.400$4.200$4.000

AVERAGE PREMIUM PER VESSEL DEVELOPMENT (US$)

Average

$120,000

$100,000

$80,000

$60,000

$40,000

$20,000

$0

PREMIUM INCOME DEVELOPMENT (US$)

2008 2009 2010 2011 2012 2013

Non-IG Mutual Premium Income Development 2008-2012Korean P&I Club Development

AVERAGE PREMIUM PER VESSEL DEVELOPMENT (USD) PREMIUM DEVELOPMENT (USD'000)

EXECUTIVE SUMMARY

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 16 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 17

COMMERCIAL P&I MARKET REVIEW 2014

FIXED PREMIUM P&I INSURANCE EXPLAINED

WHAT IS FIXED PREMIUM INSURANCE?Fixed premium P&I insurance indemnifies ship owners, operators and charterers for third party liabilities arising from a fortuitous event or a marine peril. Third party risks include a carrier’s liability to a cargo owner for damage to cargo, a ship’s liability after a collision, environmental pollution, the ship’s liability to its crew, fines and war risks etc. The term “fixed premium” means exactly that, as the terms and conditions offered by a commercial insurance company, do not expose clients to potential excess supplementary calls, unlike IG Group Clubs.

The premiums involved in this market sector are often more competitive, compared to an IG Group Club option, as insurance packages are specifically tailored to meet the demands of the risk entailed, on a reduced limit of liability basis.

DO IG P&I CLUBS PROVIDE FIXED PREMIUM INSURANCE?Fixed premium insurance contracts are typically provided by insurance companies or underwriting agents outside of the International Group of P&I Clubs, however some of the IG P&I Clubs do provide “Owners P&I” fixed premium terms for some longstanding fleets, US flagged fleets and Government fleets, which have been approved by the International Group.

A number of P&I Clubs, such as American, Gard, Skuld, SOP and Steamship Mutual also have fixed P&I premium facilities in place for smaller inland craft and U.S. yachts. AJG will focus on these facilities in our “AJG International Group Club P&I Review 2013” which will be published towards the end of this year. All of the IG Clubs provide alternative fixed insurance products, such as Charterers’ Liability Insurance and other marine related products, which do not fall under the conventional IG Group P&I product or IG group reinsurance programme.

DIFFERENCES BETWEEN COMMERCIAL P&I MARKETS AND IG GROUP CLUB P&I INSURANCE

GENERAL INCREASES The fixed premium market does not adopt the annual general increase philosophy, which is a tradition practiced amongst most of the IG P&I Clubs. Renewals are instead underwritten on the assureds’ individual merits and loss record, although there may be increases sought on the basis of exposure, operating costs or the overall performance of the insurers portfolio.

ANNUAL MANDATORY REQUIREMENTS Over the last few years we have seen many P&I Clubs’ insert annual mandatory uplifts/ requirements, which are often non-negotiable, such as deductible increases etc. This is a practice which the commercial market does not follow.

PROSPECTS FOR SUPPLENTARY OR EXCESS CALLS IG Group Clubs have the power to make excess supplementary calls if there is a need to raise funds, which are non-negotiable. The non-mutual commercial insurance companies do not have this capability.

RELEASE CALLS The Commercial Market gives clients freedom to change insurer without having to release themselves from future liabilities to supplementary calls or excess supplementary calls, which is inherent within the IG Club rules.

COMPETITION The commercial insurance companies are able to offer independent terms as well as competing with each other to win business. All of the non-IG facilities are free from the constraints of the International Group Agreement, something which the IG Clubs voluntarily abide by.

SECURITY GUARANTEES IG P&I Clubs have an integral advantage over the commercial insurance market, with the ability to put up an immediate letter of guarantee to secure the release of an arrested vessel, without additional cost. However, fixed premium insurers typically need to contact their reinsurers to obtain security guarantees, which can take time and may come with additional costs, which would ordinarily be passed onto the assured. It is important to note that the ability of each individual insurance company differs, when it comes to issuing letters of security.

THE “OMNIBUS RULE” The fixed premium market does not benefit from the IG Club

“Omnibus Rule”, which allows the individual IG Club board’s to decide whether they can indemnify a Member in difficulty.

UNDERWRITING FOR PROFIT IG Group Clubs are focused on “not for profit service”, whereas a commercial insurance company can be more profit focused, which is an important factor to consider, when handling claims to ensure that the claimant is indemnified at an appropriate level. This is where a strong broker like AJG will add value!

SERVICE PHILOSOPHY In an IG Group Club, the managers are the “servants” of the Club, the overall control of the Clubs are in the hands of its Members and its ship owner boards, who decide on policy changes, scope of cover, claims payments and premiums calls.

LIMITS OF LIABILITY Without access to the International Group Pool, fixed premium coverage will be limited to a specific limit of liability, however clients may still be exposed to catastrophes, which could potentially exceed smaller limits. Choosing the appropriate level of cover is something that AJG can help you with.

BLUE CARDS Some fixed premium insurance companies issue blue cards which are not approved by a number of flag states or port authorities. It is vital to ensure that Bunker Blue Cards and/or CLC Blue Cards are accepted by the shipping authorities prior to trading.

CERTIFICATES OF FINANCIAL RESPONSIBILITY (COFR) A requirement under the US OPA 90 Act (United States Oil Pollution Act), where any vessel over 300 GT requires a valid COFR and COFR guarantee cover in place. Guarantee coverage is provided by several COFR guarantee companies, which require letters of undertaking by an International Group P&I Club, most of the fixed premium facilities are not approved by these guarantee companies. Therefore it is important to check this prior to trading to U.S. waters.

DIVIDENDS Some of the P&I Clubs pass back “dividends”, in the form of premium returns or not calling budgeted supplementary calls in full to the Membership if the Club has experienced a good underwriting year.

P&I FIXED PREMIUM MARKET EXPLAINED

P&I MARKET FACILTY VARIATIONS

FIXED PREMIUM P&I PROVIDERS There are three “facility types” that offer fixed premium P&I insurance, as follows:

THE INTERNATIONAL GROUP OF P&I CLUBSAll of the International Group of P&I Clubs offer alternative fixed premium solutions for their clients. These may include non-pooled insurance products such as charterer’s liabilities, offshore P&I, contractual liabilities, specialist operations etc., however, some of the IG P&I Club managers can provide fixed premium P&I covers aimed at smaller tonnages on a limited liability basis.

INSURANCE COMPANIESInsurance companies are business entities that generally look at multiple lines of insurance, be it marine or non-marine related risks. Insurance companies that provide marine

insurances typically can provide hull and machinery, cargo, ports and terminals, kidnap and ransom covers etc. some of these companies also provide fixed cost P&I insurance. In the past some of the demutualised P&I facilities and managing general agents have been purchased by independent insurance companies.

MANAGING GENERAL AGENTS (MGA)An MGA is an individual or business entity appointed by an insurance company to conduct and arrange insurance contracts on their behalf. An MGA generally acts as a fronting company for the insurer, as well as providing the insured with evidence of cover within the defined underwriting authority. MGA’s also service policies and most importantly handle claims. Traditionally MGA’s were formed where insurance companies wanted to expand their markets, but did not have their own resources or technical knowledge to open and staff offices, therefore utilising the services of an MGA.

The following table identifies the current “facilities” that are able to provide fixed premium P&I insurance:

International Group P&I Club Insurance Company Managing General Agent

Gard OffshoreBritish Marine (a brand of QBE Europe)

Carina (Lloyd's of London)

Japan Club Naiko (Coastal) Class Navigators P&I (Navigators)Charterama BV (Royal Sun Alliance)

North Group Ingosstrakh Insurance Co.Charterers P&I Club (Munich Re)

Shipowners P&I ClubRaetsmarine BV (Amlin Europe)

Eagle Ocean Marine (American Club)

Skuld P&I Club Rosgosstrakh LtdHanseatic P&I (Lloyd's of London)

Standard P&I Club Hydor AS (Brit Syndicate)

Steamship Yacht FacilityLodestar Marine Ltd (Royal Sun Alliance)

Swedish Club OffshoreNorwegian Hull Club (Lloyd's of London)

West of England P&I ClubOsprey Underwriting Agency (Lloyd's of London)

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 18 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 19

COMMERCIAL P&I MARKET REVIEW 2014

COMMERICIAL P&I MARKET TODAY MORE CAPACITY AND MORE COMPETITION THAN EVER BEFORE

The commercial P&I market has more than doubled in size since 2009, with seventeen non-IG P&I fixed premium and charterer’s liability specialist markets competing for business. With the over-supply of choice, we at AJG have observed P&I fixed rates reducing year on year, providing owners, operators and traders with an opportunity to reduce operating expenditure annually. In the last two years the market has seen more of the IG-P&I Clubs “awaken” in their attempts to diversify into this market sector, to increase revenues and free-reserves. In response to this change in appetite, the well-established commercial market facilities claim not to be intimidated by this change in stance, however they generally see it as an opportunity for the shipping community to become more aware of alternative P&I products and markets available.

The commercial market is still aimed at the smaller vessel operators, short-trade vessels, principally operating in coastal or inland waters typically within a tonnage range below 10,000 GT. Market facilities are available for vessels up to 40,000 gross tons (higher GT caps and limits are also available depending on the facility). For charterer’s liabilities, there are no vessel type or size restrictions among the specialist charterer’s liability facilities.

Limits up to USD 1 Billion are available, however typically the larger limit of choice is USD 500 million, where the majority of assureds are usually insured below USD 50 Million. All fixed premium facilities target ship owners, operators, charterers and traders emanating from all geographical areas (subject to EU/US Sanctions), however certain facilities tend to shy away from passenger, cruise and U.S. flagged, trans-Atlantic and trans-Pacific business. Coverage for over-age and non-IACS classed tonnage is also available from the majority of fixed premium facilities.

WHY CHOOSE FIXED PREMIUM?We at Gallagher London believe that some of the key advantages of insuring with a fixed premium insurer are that they can offer certainty of cost and lower, more accessible limits of liability, with no liabilities for unbudgeted supplementary calls or annual general increases. Not all of the alternative non-IG facilities offer fixed premium covers, some are mutual. In addition to this there are also exclusive charterer’s liability specialist insurers, which cater for charterers and traders. The fixed premium P&I market has continued to evolve considerably over the last five years, with more new entrants than exits from this industry sector. This is perhaps to be expected given the IG Group system’s workings and the competitive nature of the commercial market.

The following table provides a snapshot for the last five years' market development:

NON-IG MARKET DEVELOPMENT (YEARS 2009 – 2014)

ESTABLISHED MARKET (10yrs +)

INTERMEDIATE (5-10yrs) NEW ENTRANT (<5yrs) SPECULATIVE MARKET EXIT

British Marine (QBE) (Est. 1876)

Hanseatic P&I (Est. 2005)

Eagle Ocean Marine

(Est. 2010)

New Russian P&I Facility? Terra Nova Insurance Co. (2006)

Ingosstrakh (Est. 1974) Norwegian Hull Club (Est. 2008)

Rosgosstrakh P&I

(Est. 2010)

Axa Corporate Solutions (2008)

China P&I Club (Est. 1984)

Charterama BV (RSA) (Est. 2009)

Lodestar Marine Ltd (RSA) (Est. 2012)

InterCoastal Shipowners BV (2011)

Charterers P&I Club (Munich Re) (Est. 1986)

Hydor(Brit Syndicate) (Est. 2009)

India Ocean P&I Club (Est. 2013)

South of England Mutual (2011)

Osprey Underwriting Agency (Est. 1991)

Carina – Tindal Riley (Est. 2013)

Ceylon P&I Club (2012)

Raetsmarine BV (Amlin) (Est. 1993)

Skuld P&I Club (Fixed) (Est. 2013)

HEMPIRA (2014, due to consolidation with Aigaion)

Korea P&I Club (Est. 2000)

North Group (Sunderland Marine Merger) (Est. 2014)

Navigators P&I (Est. 2004)

Standard Club Fixed Facility (Est. 2014)

Aigaion Ins. Co. (Est. 2004)

P&I FIXED PREMIUM MARKET EXPLAINED

COMMERCIAL P&I MARKET NEWS REVIEW OF THE LAST 12 MONTHS

OCTOBER Mitsui Sumitomo and Skuld P&I Club join forces for Mitsui to offer a blue-water fixed-premium P&I product to the Japanese ship-owning community.

Navigators P&I announce the recruitment of Richard Lovett as underwriter (previously with Osprey Underwriting Agency).

NOVEMBER British Marine announces the recruitment of Julia Maly from competitor RaetsMarine and

Harriet Stillwell from the marine insurance broking community.

DECEMBER Hydor AS announces the recruitment of Andrey Mochalin as underwriter

Royal Sun Alliance downgraded by Standard & Poor’s from A to A- (Charterama BV & Lodestar).

JANUARY Lodestar’s David Mahoney departs to join marine insurance broking community.

Ingosstrakh Ins. Co. announces that the maximum limit of cover available has been increased to USD 1 billion from USD 500 million.

FEBRUARY RaetsMarine Insurance BV is approved as a designated insurer in Japan.

Michael Else & Co Ltd announces opening of Dubai based office Sextant Marine as a strategic hub.

Standard P&I Club soft launch their “Standard Fixed P&I” facility. The Standard Fixed facility is also one of the key backers to the Turkish P&I Club.

MARCH Lodestar Ltd announces an 88% business retention rate, as well as welcoming 82 new assureds, covering 335 vessels globally.

North of England P&I Association and Sunderland Marine Insurance Company Ltd complete all requirements to formally merge to form the “North Group”. The two companies will focus on “integration strategy” to deliver diversification to benefit the Club’s business profile and mutual membership.

Royal Sun Alliance upgraded by Standard & Poor’s from A- back to A (Charterama BV & Lodestar).

APRIL Eagle Ocean Marine announces that the maximum limit of cover available has been increased to from USD 50 million to USD 100 million. Furthermore EOM can also write vessels up to 25,000 GT (previous limit was 12,500 GT).

Hanseatic P&I accounted changes to their P&I and FD&D insurance consortium.

Michael Else & Co announces the opening of Sextant Marine Dubai, as a strategic hub to more efficiently handle overseas clients and provide further claims handling support.

MAY Charterama BV opens Hong Kong office, to be headed by ex-Norwegian Hull Club underwriter Powan Li.

Osprey Underwriting Agency announces that the maximum limit of cover available has been increased to USD 100 million to USD 500 million.

JUNE Hanseatic P&I announce relocation of London Office to 1 Royal Exchange Avenue.

Navigators P&I announce limit of liability increase by a factor 1.51 as of (8th June 2015) to comply with local Japanese law amendments to limits of liability.

OCTOBER Navigators P&I announce the recruitment of Jason Riley from the UK P&I Club

20

14

2013

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 20 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 21

COMMERCIAL P&I MARKET OVERVIEW

FACILITY CARRIER ANNUAL PREMIUM INCOME 2013 (USD)

TOTAL TONNAGE/ VESSELS INSURED

LOCATION MAXIMUM LIMIT MAX SIZE VESSEL EXCLUSIONS ETC

BRITISH MARINE QBE Insurance (Europe) Ltd S&P: A+

USD 100,000,000 11,000,000 GT LONDON, UNITED KINGDOM

USD 1 Billion No Cap. However focus on small & medium GT

Avoids passenger risks, dirty tankers, Tran-Pacific/ Atlantic.

CARINA Lloyd's of London

S&P: A+

UNDISCLOSED 2,000,000 GT LONDON, UNITED KINGDOM

USD 500 Million > 5,000 GT No U.S. flagged or managed business

CHARTERAMA BV Royal Sun Alliance

S&P: A

USD 10,000,000 10,500 Vessels ROTTERDAM, NETHERLANDS

USD 150 Million No limit No exclusions

CHARTERERS P&I Great Lakes/ Munich Re

S&P: AA-

USD 28,200,000 12,500 Vessels LONDON, UNITED KINGDOM

USD 500 Million No limit -

CHINA P&I CLUB Mutual Insurance Company

S&P: Unrated

US$ 69,900,000 31,700,000 GT BEIJING, CHINA No Limit -

EAGLE OCEAN MARINE American Club

S&P: BBB-

USD 7,000,000 590,000 GT NEW YORK, USA USD 100 Million >25,000 GT No U.S. flagged or yachts

HANSEATIC P&I Insurance Consortium – See Page

S&P: Various A Rated

USD 19,500,000 2,700,000 GT HAMBURG, GERMANY USD 500 Million >30,000 GT Bulkers

>20,000 GT Tankers

No U.S. flagged or managed business

HYDOR A/S Lloyd's of London

(Brit Syndicate 2987) S&P: A+

USD 9,000,000 1,300,000 GT BERGEN, NORWAY US$ 500 Million <10,000 GT No U.S. flagged or managed business

INGOSSTRAKH Ingosstrakh

S&P: BBB-

USD 21,800,000 5,001,155 MOSCOW, RUSSIA US$ 1 Billion <10,000 GT -

KOREAN P&I CLUB Mutual Insurance Company

AMB: A-

USD 31,127,000 18,192,000 GT SEOUL, KOREA USD 1 Billion No limit No coastal fishing vessels or dirty tankers over 10,000 GT

LODESTAR LTD Royal Sun Alliance

S&P: A

USD 25,000,000 2,756,154 GT LONDON, UNITED KINGDOM

USD 500 Million >20,000 GT Non-Tanker

>10,000 GT Tanker

No tankers trading to USA, US flagged, large cruise vessels

NAVIGATORS P&I Navigators Insurance Co.

S&P: A

USD 21,430,000 2,000,000 GT LONDON, UNITED KINGDOM

USD 500 Million >10,000 GT Dislike trans-Atlantic/ Pacific trade. No U.S. flagged business

NORWEGIAN HULL CLUB Norwegian Hull Club

S&P: A-

USD 11,000,000 UNDISCLOSED OSLO, NORWAY USD 200 Million No Limit Does not write tanker (persistent) cargoes.

OSPREY Lloyd's of London

S&P: A+

USD 30,000,000 1,800 Vessels LONDON, UNITED KINGDOM

USD 500,000 Million <10,000 GT No U.S. flagged or yachts

RAETSMARINE BV Amlin Europe N.V.

S&P: A-

USD 52,000,000 15,366,000 GT ROTTERDAM, NETHERLANDS

USD 500 Million >40,000 GT U.S. flagged business above USD 50 Million

ROSGOSSTRAKH LTD Rosgosstrakh Ltd

Local Rating: BB-/RU AA

USD 4,800,000 1,424,486 GT MOSCOW, RUSSIA USD 500 Million Tankers <8,500 GT

All others <25,000 GT -

COMMERCIAL P&I MARKET REVIEW 2014 NON-IG P&I MARKET OVERVIEW

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 22 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 23

INTRODUCTION TO FIXED P&I MARKET FACTS & FIGURESThe information contained in the Arthur J. Gallagher P&I facts and figures pages has been compiled by the various insurance providers contained in this report. As part of our assessment in choosing an appropriate fixed premium insurer(s) for our clients, amongst other key factors such as claims service, pricing, flexibility etc. AJG also considers the following parameters as essential indicators in the selection process.

REINSURANCE CARRIER:

The underlying security or insurance company providing the market capacity.

STANDARD AND POOR’S (S&P) RATING:

Arthur J. Gallagher operates a market security policy which sets a minimum standard for insurance markets which can be included on its acceptable market security list. A number of criteria are utilised to evaluate the financial condition of these markets and one of the criteria used is the ratings allocated by either Standard & Poor’s (S&P) or A M Best. The AJG (UK) security policy sets a minimum rating level of A- from these agencies as an indicator of acceptable security. See Page *** for more information on this policy. The specified rating attached to each facility is a credit rating based on S&P’s independent opinion regarding the ability of an issuer, corporation or association to meet its financial obligations. Such ratings are provided by organisations such as S&P and AM Best, also known as credit rating agencies. Each organisation applies its own merits in measuring credit and use a rating scale to publish their individual findings. Ratings are expressed as a letter grade for example AAA being the highest level.

MAXIMUM LIMIT OF LIABILITY AVAILABLE:

It is very common to see a limit of liability in insurance contracts, which stipulate limitations on the maximum amount payable under the contract. Further, the cost of defence, supplementary payments, and punitive damages may or may not be paid in addition to the limits. Separate limits often apply to claims for pollution and/or passenger or seamen claims. An annual aggregate limit may also be offered, which puts a maximum on the amount an insurer must pay in any one policy period.

VESSEL TYPE/ SIZE (GT) CAP:

This is the maximum size (gross ton) of vessel that can be insured by the facility.

FACILITY LOCATION(S):

The primary business location of the facility and various support and claims offices available. Local claims liaison offices are important to ensure that clients in different time zones can access claims or loss prevention assistance in a timely manner.

GEOGRAPHICAL SPREAD OF BUSINESS:

This is an indicator to show where business revenues derive from a geographical overview.

TYPE OF ENTERED VESSEL:

This indicator demonstrates what type of vessel a facility tends to write.

ANNUAL PREMIUM INCOME, GROSS TONNAGE AND PREMIUM PER GT DEVELOPMENT:

AJG analyses premium development to see how a particular facility is performing.

COMMERCIAL P&I MARKET REVIEW 2014

MARKET FACTS & FIGURES

2

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 24 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 25

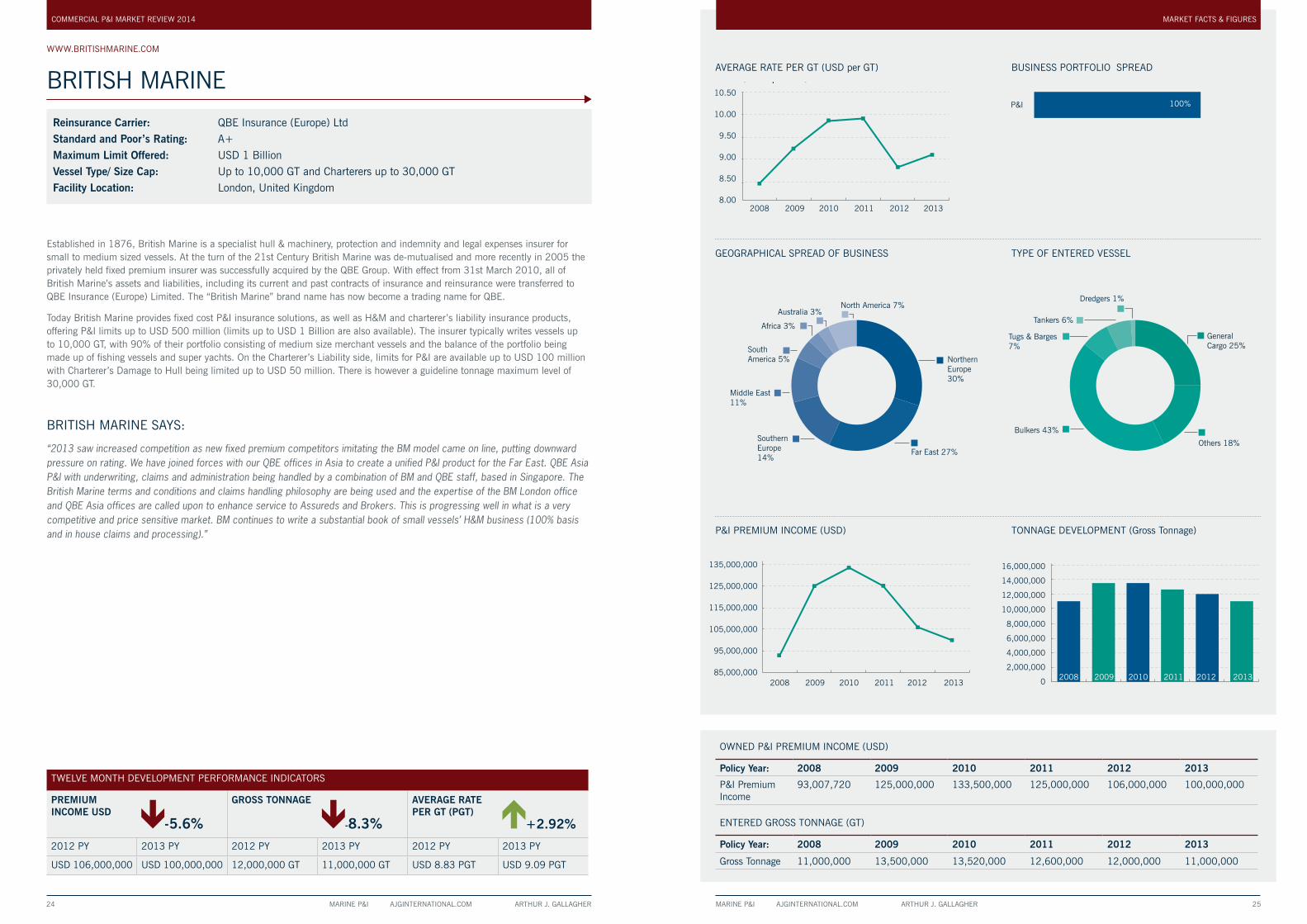

WWW.BRITISHMARINE.COM

BRITISH MARINE

Reinsurance Carrier: QBE Insurance (Europe) LtdStandard and Poor’s Rating: A+Maximum Limit Offered: USD 1 BillionVessel Type/ Size Cap: Up to 10,000 GT and Charterers up to 30,000 GTFacility Location: London, United Kingdom

Established in 1876, British Marine is a specialist hull & machinery, protection and indemnity and legal expenses insurer for small to medium sized vessels. At the turn of the 21st Century British Marine was de-mutualised and more recently in 2005 the privately held fixed premium insurer was successfully acquired by the QBE Group. With effect from 31st March 2010, all of British Marine’s assets and liabilities, including its current and past contracts of insurance and reinsurance were transferred to QBE Insurance (Europe) Limited. The “British Marine” brand name has now become a trading name for QBE.

Today British Marine provides fixed cost P&I insurance solutions, as well as H&M and charterer’s liability insurance products, offering P&I limits up to USD 500 million (limits up to USD 1 Billion are also available). The insurer typically writes vessels up to 10,000 GT, with 90% of their portfolio consisting of medium size merchant vessels and the balance of the portfolio being made up of fishing vessels and super yachts. On the Charterer’s Liability side, limits for P&I are available up to USD 100 million with Charterer’s Damage to Hull being limited up to USD 50 million. There is however a guideline tonnage maximum level of 30,000 GT.

BRITISH MARINE SAYS:

“2013 saw increased competition as new fixed premium competitors imitating the BM model came on line, putting downward pressure on rating. We have joined forces with our QBE offices in Asia to create a unified P&I product for the Far East. QBE Asia P&I with underwriting, claims and administration being handled by a combination of BM and QBE staff, based in Singapore. The British Marine terms and conditions and claims handling philosophy are being used and the expertise of the BM London office and QBE Asia offices are called upon to enhance service to Assureds and Brokers. This is progressing well in what is a very competitive and price sensitive market. BM continues to write a substantial book of small vessels’ H&M business (100% basis and in house claims and processing).”

TWELVE MONTH DEVELOPMENT PERFORMANCE INDICATORS

PREMIUM INCOME USD

-5.6%

GROSS TONNAGE

-8.3%

AVERAGE RATE PER GT (PGT)

+2.92%

2012 PY 2013 PY 2012 PY 2013 PY 2012 PY 2013 PY

USD 106,000,000 USD 100,000,000 12,000,000 GT 11,000,000 GT USD 8.83 PGT USD 9.09 PGT

COMMERCIAL P&I MARKET REVIEW 2014

Middle East11%

SouthernEurope14%

Far East 27%

NorthernEurope30%

SouthAmerica 5%

North America 7%Australia 3%

Africa 3%

P&I

BUSINESS PORTFOLIO SPREAD

100%

Bulkers 43%

Others 18%

GeneralCargo 25%

Tugs & Barges 7%

Dredgers 1%

Tankers 6%

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

135,000,000

125,000,000

115,000,000

105,000,000

95,000,000

85,000,000

10.50

10.00

9.50

9.00

8.50

8.00

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

Middle East11%

SouthernEurope14%

Far East 27%

NorthernEurope30%

SouthAmerica 5%

North America 7%Australia 3%

Africa 3%

P&I

BUSINESS PORTFOLIO SPREAD

100%

Bulkers 43%

Others 18%

GeneralCargo 25%

Tugs & Barges 7%

Dredgers 1%

Tankers 6%

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

135,000,000

125,000,000

115,000,000

105,000,000

95,000,000

85,000,000

10.50

10.00

9.50

9.00

8.50

8.00

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

Middle East11%

SouthernEurope14%

Far East 27%

NorthernEurope30%

SouthAmerica 5%

North America 7%Australia 3%

Africa 3%

P&I

BUSINESS PORTFOLIO SPREAD

100%

Bulkers 43%

Others 18%

GeneralCargo 25%

Tugs & Barges 7%

Dredgers 1%

Tankers 6%

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

135,000,000

125,000,000

115,000,000

105,000,000

95,000,000

85,000,000

10.50

10.00

9.50

9.00

8.50

8.00

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

Middle East11%

SouthernEurope14%

Far East 27%

NorthernEurope30%

SouthAmerica 5%

North America 7%Australia 3%

Africa 3%

P&I

BUSINESS PORTFOLIO SPREAD

100%

Bulkers 43%

Others 18%

GeneralCargo 25%

Tugs & Barges 7%

Dredgers 1%

Tankers 6%

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

135,000,000

125,000,000

115,000,000

105,000,000

95,000,000

85,000,000

10.50

10.00

9.50

9.00

8.50

8.00

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

Middle East11%

SouthernEurope14%

Far East 27%

NorthernEurope30%

SouthAmerica 5%

North America 7%Australia 3%

Africa 3%

P&I

BUSINESS PORTFOLIO SPREAD

100%

Bulkers 43%

Others 18%

GeneralCargo 25%

Tugs & Barges 7%

Dredgers 1%

Tankers 6%

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

135,000,000

125,000,000

115,000,000

105,000,000

95,000,000

85,000,000

10.50

10.00

9.50

9.00

8.50

8.00

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

Middle East11%

SouthernEurope14%

Far East 27%

NorthernEurope30%

SouthAmerica 5%

North America 7%Australia 3%

Africa 3%

P&I

BUSINESS PORTFOLIO SPREAD

100%

Bulkers 43%

Others 18%

GeneralCargo 25%

Tugs & Barges 7%

Dredgers 1%

Tankers 6%

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

135,000,000

125,000,000

115,000,000

105,000,000

95,000,000

85,000,000

10.50

10.00

9.50

9.00

8.50

8.00

16,000,000

14,000,000

12,000,000

10,000,000

8,000,000

6,000,000

4,000,000

2,000,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

OWNED P&I PREMIUM INCOME (USD)

Policy Year: 2008 2009 2010 2011 2012 2013

P&I Premium Income

93,007,720 125,000,000 133,500,000 125,000,000 106,000,000 100,000,000

ENTERED GROSS TONNAGE (GT)

Policy Year: 2008 2009 2010 2011 2012 2013

Gross Tonnage 11,000,000 13,500,000 13,520,000 12,600,000 12,000,000 11,000,000

AVERAGE RATE PER GT (USD per GT) BUSINESS PORTFOLIO SPREAD

GEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

P&I PREMIUM INCOME (USD) TONNAGE DEVELOPMENT (Gross Tonnage)

MARKET FACTS & FIGURES

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 26 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 27

WWW.CARINAPANDI.COM

CARINA

Reinsurance Carrier: Lloyd's of LondonStandard and Poor’s Rating: A+Maximum Limit Offered: Up to USD 500 MillionVessel Type/ Size Cap: Up to 5,000 GTFacility Location: London, United Kingdom

Carina is one of the most recent fixed premium new entrants starting in the early part of 2013. The facility is managed by Tindall Riley Marine (UK) Limited (who are the managers of the Britannia P&I Club), trading as Carina Managers. This facility offers fixed premium P&I coverage for Owners and Charterers of smaller vessels ranging up to 5,000 gross tons, operating in domestic or inland waters, worldwide. Policy limits of up to USD 500 million are available for Owners, whereas Charterers and Traders will be able to purchase limits up to USD 50 million.

The focus of the facility targets small ship sector operators only. Legal Defence Cover is also available together with additional ancillary covers that may be required. Carina will benefit from Tindall Riley Marine Limited vast experience in underwriting, claims and support services. Carina’s reinsurance programme is backed by Lloyd's of London syndicates, which hold an S&P A+ rating.

CARINA SAYS:

“Carina launched its business on 1 March 2013, so there are no figures relating to 2012. Carina does not have a ‘policy year,’ as such. In 2013, our Binder ran until 31 December, so the premium figures for 2013 would not be representative, covering just over 9 months of the year. Carina is now insuring over 4,200 ships, only 18 months after entering the market and that, we believe, is the most accurate indication of how well the facility has been supported. The combined net loss ratio for the year to 31 December 2013 is currently 72%. Carina believes that competition is a good thing and we always try to be as competitive as possible. Providing quotations by return and giving a first class service to the broker have helped us to build our reputation in a short period. Most of the new entrants are targeting ships of over 10,000 GT. Carina has focussed exclusively on ships with a maximum GT of 5,000. The new entrants have had little effect on the sector in which we specialise. To date, we have been very successful in retaining business, notwithstanding the competition. From Carina’s perspective, the last 12 months have been very successful. We have produced solid results and built a firm base in the small ships market. We intend to grow the business over the coming years and are very encouraged by the continuing interest in the facility.”

COMMERCIAL P&I MARKET REVIEW 2014

TWELVE MONTH DEVELOPMENT PERFORMANCE INDICATORS

PREMIUM INCOME USD

GROSS TONNAGE AVERAGE RATE PER GT (PGT)

2012 PY 2013 PY 2012 PY 2013 PY 2012 PY 2013 PY

No data provided

AVERAGE RATE PER GT (USD per GT) BUSINESS PORTFOLIO SPREAD

GEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

P&I PREMIUM INCOME (USD) TONNAGE DEVELOPMENT (Gross Tonnage)

GEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

Far East30%

Europe42%

Russia 21%

South America 7%

Passenger 14%

GeneralCargo 24%

Tankers 8% Tugs & Barges 37%

Others 12%

Fishing 5%

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

TONNAGE DEVELOPMENT(Gross Tonnage)

2008 2009 2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

Far East30%

Europe42%

Russia 21%

South America 7%

Passenger 14%

GeneralCargo 24%

Tankers 8% Tugs & Barges 37%

Others 12%

Fishing 5%

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

TONNAGE DEVELOPMENT(Gross Tonnage)

2008 2009 2010 2011 2012 2013

OWNED P&I PREMIUM INCOME (USD)

Policy Year: 2008 2009 2010 2011 2012 2013

P&I Premium Income

GROSS TONNAGE DEVELOPMENT (GT)

Policy Year: 2008 2009 2010 2011 2012 2013

Gross Tonnage - - - - - 2,000,000

No data providedNo data provided

No data provided

No data provided

MARKET FACTS & FIGURESGEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

Far East30%

Europe42%

Russia 21%

South America 7%

Passenger 14%

GeneralCargo 24%

Tankers 8% Tugs & Barges 37%

Others 12%

Fishing 5%

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

TONNAGE DEVELOPMENT(Gross Tonnage)

2008 2009 2010 2011 2012 2013

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 28 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 29

WWW.EAGLEOCEANMARINE.COM

EAGLE OCEAN MARINE

Reinsurance Carrier: American P&I ClubStandard and Poor’s Rating: BBB-Maximum Limit Offered: Up to USD 100 MillionVessel Type/ Size Cap: Up to 25,000 GTFacility Location: New York, United States of America

Eagle Ocean Agencies, Inc. is an affiliated company of The Shipowners Claims Bureau, Inc., who are the managers of the American P&I Club, and Atlantic Marine Associates, Inc., which is a general marine adjusting and claims handling company. In 2010, the Directors of the American P&I Club formed a separate fixed premium facility, namely Eagle Ocean Marine, offering Protection and Indemnity and Freight, Demurrage and Defence insurance solutions. The facility is primarily focused on operators of smaller ships, below 25,000 gross tons, operating in regional waters, with policy limits being available up to $50 million for P&I and $2 million for FD&D. P&I coverage is available to operators on a worldwide basis; however coverage is not available to operators based in the U.S.A. or trading exclusively in U.S. waters. At present the facility is more Far East focused, with 60% of their portfolio emanating from this region.

The agency has recently re-structured its insurance and reinsurance arrangements, with American Steamship Owners Mutual Protection and Indemnity Association, Inc. providing the primary security. This in turn will allow Eagle Ocean to put up American Club security guarantees up to its primary limits, as well as providing American Club blue cards.

EAGLE OCEAN MARINE SAYS:

“With a softening ratings environment, EOM has focussed on maintaining a conservative approach to risk and therefore not allowing themselves to “follow the market down”. New entrants with high cost base are rating at prices which are unsustainable in the long term. EOM have confident that they will maintain its market share. The challenge is to grow the facility without compromising on rating. The fixed P&I market has continued to grow considerably over the past few years, doubling since 2008. The initial driver for this growth was smaller owners recognising the need to de-risk their operations, by moving capacity into the fixed P&I market, which gives them more transparency over what they will be paying for cover at a fixed annual cost. While rates may not continue to drop from current levels, EOM do not see any significant upwards movement in rates over the next 6 to 12 months. This in-balance will, ultimately, be reconciled. It will be interesting to see which players will remain.”

TWELVE MONTH DEVELOPMENT PERFORMANCE INDICATORS

PREMIUM INCOME USD

+7.6%

GROSS TONNAGE

-9.2%

AVERAGE RATE PER GT (PGT)

+18.6%2012 PY 2013 PY 2012 PY 2013 PY 2012 PY 2013 PY

USD 6,500,000 USD 7,000,000 650,000 GT 590,000 GT USD 10.00 PGT USD 11.86 PGT

COMMERCIAL P&I MARKET REVIEW 2014

AVERAGE RATE PER GT (USD per GT) BUSINESS PORTFOLIO SPREAD

GEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

P&I PREMIUM INCOME (USD) TONNAGE DEVELOPMENT (Gross Tonnage)

OWNED P&I PREMIUM INCOME (USD)

Policy Year: 2008 2009 2010 2011 2012 2013

P&I Premium Income

- - 500,000 5,000,000 6,500,000 7,000,000

P&I Claims Incurred

50,000 3,000,000 5,000,000 1,200,000

ENTERED GROSS TONNAGE (GT)

Policy Year: 2008 2009 2010 2011 2012 2013

Gross Tonnage - - 50,000 470,000 650,000 590,000

2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS

P&I

BUSINESS PORTFOLIO SPREAD

98%

FD&D 2%

TYPE OF ENTERED VESSEL

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

General Cargo 14%

Tugs & Barges 42%

Containers 3%

Tankers 22%

Bulkers 3%Fishing 1%

Others 15%

Africa 27%

Far East 59%

North America 1%

Fishing 1%

Middle East 6%

Southern Europe 3%

South America 1%

2010 2011 2012 2013

2010 2011 2012 2013

10.50

10.00

9.50

9.00

8.50

8.00

AVERAGE RATE PER GT(USD per GT)

2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS

P&I

BUSINESS PORTFOLIO SPREAD

98%

FD&D 2%

TYPE OF ENTERED VESSEL

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

General Cargo 14%

Tugs & Barges 42%

Containers 3%

Tankers 22%

Bulkers 3%Fishing 1%

Others 15%

Africa 27%

Far East 59%

North America 1%

Fishing 1%

Middle East 6%

Southern Europe 3%

South America 1%

2010 2011 2012 2013

2010 2011 2012 2013

10.50

10.00

9.50

9.00

8.50

8.00

AVERAGE RATE PER GT(USD per GT)

2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS

P&I

BUSINESS PORTFOLIO SPREAD

98%

FD&D 2%

TYPE OF ENTERED VESSEL

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

General Cargo 14%

Tugs & Barges 42%

Containers 3%

Tankers 22%

Bulkers 3%Fishing 1%

Others 15%

Africa 27%

Far East 59%

North America 1%

Fishing 1%

Middle East 6%

Southern Europe 3%

South America 1%

2010 2011 2012 2013

2010 2011 2012 2013

10.50

10.00

9.50

9.00

8.50

8.00

AVERAGE RATE PER GT(USD per GT)

2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS

P&I

BUSINESS PORTFOLIO SPREAD

98%

FD&D 2%

TYPE OF ENTERED VESSEL

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

General Cargo 14%

Tugs & Barges 42%

Containers 3%

Tankers 22%

Bulkers 3%Fishing 1%

Others 15%

Africa 27%

Far East 59%

North America 1%

Fishing 1%

Middle East 6%

Southern Europe 3%

South America 1%

2010 2011 2012 2013

2010 2011 2012 2013

10.50

10.00

9.50

9.00

8.50

8.00

AVERAGE RATE PER GT(USD per GT)

2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS

P&I

BUSINESS PORTFOLIO SPREAD

98%

FD&D 2%

TYPE OF ENTERED VESSEL

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

General Cargo 14%

Tugs & Barges 42%

Containers 3%

Tankers 22%

Bulkers 3%Fishing 1%

Others 15%

Africa 27%

Far East 59%

North America 1%

Fishing 1%

Middle East 6%

Southern Europe 3%

South America 1%

2010 2011 2012 2013

2010 2011 2012 2013

10.50

10.00

9.50

9.00

8.50

8.00

AVERAGE RATE PER GT(USD per GT)

2010 2011 2012 2013

GEOGRAPHICAL SPREAD OF BUSINESS

P&I

BUSINESS PORTFOLIO SPREAD

98%

FD&D 2%

TYPE OF ENTERED VESSEL

8,000,000

7,000,000

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

700,000

600,000

500,000

400,000

300,000

200,000

100,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

General Cargo 14%

Tugs & Barges 42%

Containers 3%

Tankers 22%

Bulkers 3%Fishing 1%

Others 15%

Africa 27%

Far East 59%

North America 1%

Fishing 1%

Middle East 6%

Southern Europe 3%

South America 1%

2010 2011 2012 2013

2010 2011 2012 2013

10.50

10.00

9.50

9.00

8.50

8.00

AVERAGE RATE PER GT(USD per GT)

MARKET FACTS & FIGURES

MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 30 MARINE P&I AJGINTERNATIONAL.COM ARTHUR J. GALLAGHER 31

WWW.HANSEATIC_PANDI.COM

HANSEATIC UNDERWRITERS

Reinsurance Carrier: Allianz Global Corporate & Speciality AG – Swiss Re – Lloyd's of LondonStandard and Poor’s Rating: AA or AMaximum Limit Offered: Up to USD 500 MillionVessel Type/ Size Cap: 30,000 GT for Bulk Carriers and 20,000 GT for TankersFacility Location: Hamburg, Germany

Hanseatic P&I is an insurance consortium, which was founded in 2005, by five German Insurance Companies. All of the market participants in the consortium have an A or AA ratings. The consortium is managed by Zeller Associates Management Services GmbH, Hamburg. Hanseatic P&I provide ship owner’s liability, charterer’s liability and inland craft P&I cover. In addition FD&D is provided as either an additional or separate legal expenses cover under the brand name “Hanseatic Defence”, based on the same consortium of insurance companies as its P&I product. The facility offers P&I cover for all types of vessels with a limit up to USD 500 Million.

The core risk appetite of Hanseatic P&I is small and medium size general cargo and container vessels, as well as liquid cargo and dry bulk. Additionally Hanseatic has expertise in traditional, offshore and specialist vessels of any type. The underwriting philosophy at Hanseatic was originally focused on German and Northern European interests and later diversified its underwriting criteria to include other geographical areas. At present, Hanseatic P&I core business emanates from all parts of Europe, Russia and Turkey and it is presently looking to expand to select Middle East/North Africa and Asian regions.

HANSEATIC SAYS:

“Growth in both traditional and new markets has been our stand-out feature this year but to have managed that on the back of sustained and sensible pricing is very pleasing. The underwriting result is developing exceptionally well and is a reward for the faith shown in our team by the Hanseatic consortium which underwent a second renewal recently. The overall future for the sector should be seen as very good – at least there need be no stumbling blocks for those organisations with disciplined rating, experienced servicing capabilities and good relations with its security providers. We have managed a growth in written business of over 10% in the first 6 months of 2014 and anticipate a year-end increase approaching 20% overall on the previous year whilst sticking to our underwriting disciplines throughout. The modest reduction in premium and rate per GT in the reported figures represent, respectively, a re-writing of the book’s less profitable element during 2012/13 and an increase in ship size, with the facility being able to write up to 30,000GT dry and 20,000GT tanker tonnage.”

TWELVE MONTH DEVELOPMENT PERFORMANCE INDICATORS

PREMIUM INCOME USD

-7.1%

GROSS TONNAGE

+12.5%

AVERAGE RATE PER GT (PGT)

-12%2012 PY 2013 PY 2012 PY 2013 PY 2012 PY 2013 PY

USD 19,700,00 USD 18,300,000 2,400,000 GT 2,700,000 GT USD 8.21 PGT USD 7.22 PGT

COMMERCIAL P&I MARKET REVIEW 2014

AVERAGE RATE PER GT (USD per GT) BUSINESS PORTFOLIO SPREAD

GEOGRAPHICAL SPREAD OF BUSINESS TYPE OF ENTERED VESSEL

P&I PREMIUM INCOME (USD) TONNAGE DEVELOPMENT (Gross Tonnage)

OWNED P&I PREMIUM INCOME (USD)

Policy Year: 2008 2009 2010 2011 2012 2013

P&I Premium Income 7,700,000 11,200,000 14,700,000 15,800,000 19,700,000 18,300,000

P&I Claims Incurred 7,900,000 7,200,000 12,900,000 14,700,000 13,700,000 8,700,000

Surplus/ Deficit -200,000 4,000,000 1,800,000 1,100,000 6,000,000 9,600,000

CHARTERERS LIABILTIY INCOME

Policy Year: 2008 2009 2010 2011 2012 2013

Charterers Premium Income

1,200,000 850,000 900,000 950,000 1,000,000 1,200,000

Charterers Claims Incurred

1,800,000 700,000 200,000 150,000 170,000 154,000

Surplus/ Deficit -600,000 150,000 700,000 800,000 830,000 1,046,000

ENTERED GROSS TONNAGE (GT)

Policy Year: 2008 2009 2010 2011 2012 2013

Gross Tonnage 1,400,000 1,600,000 1,900,000 2,100,000 2,400,000 2,700,000

P&I

BUSINESS PORTFOLIO SPREAD

84%

Charterers/DTH 8%

5%

2%

1%

FD&D

War

Sol to Cargo

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

8.50

8.00

7.50

7.00

6.50

6.00

5.50

5.00

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

21,000,000

19,000,000

17,000,000

15,000,000

13,000,000

11,000,000

9,000,000

7,000,000

0

Middle East9%

SouthernEurope23%

NorthernEurope49%

Africa 4%South America 4%

Far East 11%

Containers 18%

Bulkers 26%

GeneralCargo 37%

Tugs & Barges 8%

Fishing 3%

Tankers 2%

Dredgers 1%Offshore 3%

Others 2%

P&I

BUSINESS PORTFOLIO SPREAD

84%

Charterers/DTH 8%

5%

2%

1%

FD&D

War

Sol to Cargo

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

8.50

8.00

7.50

7.00

6.50

6.00

5.50

5.00

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

21,000,000

19,000,000

17,000,000

15,000,000

13,000,000

11,000,000

9,000,000

7,000,000

0

Middle East9%

SouthernEurope23%

NorthernEurope49%

Africa 4%South America 4%

Far East 11%

Containers 18%

Bulkers 26%

GeneralCargo 37%

Tugs & Barges 8%

Fishing 3%

Tankers 2%

Dredgers 1%Offshore 3%

Others 2%

P&I

BUSINESS PORTFOLIO SPREAD

84%

Charterers/DTH 8%

5%

2%

1%

FD&D

War

Sol to Cargo

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

8.50

8.00

7.50

7.00

6.50

6.00

5.50

5.00

3,000,000

2,500,000

2,000,000

1,500,000

1,000,000

500,000

0

P&I PREMIUM INCOME (USD)

TONNAGE DEVELOPMENT(Gross Tonnage)

AVERAGE RATE PER GT(USD per GT)

2008 2009 2010 2011 2012 2013

21,000,000

19,000,000

17,000,000

15,000,000

13,000,000

11,000,000

9,000,000

7,000,000

0

Middle East9%

SouthernEurope23%

NorthernEurope49%

Africa 4%South America 4%

Far East 11%

Containers 18%

Bulkers 26%

GeneralCargo 37%

Tugs & Barges 8%

Fishing 3%

Tankers 2%

Dredgers 1%Offshore 3%

Others 2%

P&I

BUSINESS PORTFOLIO SPREAD

84%

Charterers/DTH 8%

5%

2%

1%

FD&D

War

Sol to Cargo

2008 2009 2010 2011 2012 2013

2008 2009 2010 2011 2012 2013

8.50

8.00

7.50

7.00

6.50

6.00

5.50