market entry (india) strategy - 2012, new country and new market

TRANSCRIPT

Sak

shi ,

Aji

t K

um

ar &

Ham

nee

sh

20

12

Ga

rne

r H

olt

Pro

du

ctio

ns

[Indian Market Scenario]

[K J Somaiya Institute of Management Studies & Research ] [Mumbai ,Group - 8]

[India]

2

Team Details :-

Team No :- 8

SIMSR STUDENT : -

SAKSHI ,AJIT KUMAR ,HAMNEESH

CSU STUDENT :-

Kaushal Tolia ,Viviana Villanueva ,Brian Linton ,James Walker

Contents

3

Contents

Introduction .................................................................................................................................................. 6

[The free trade agreement] .......................................................................................................................... 7

Trade Policy Forum: .................................................................................................................................. 7

High Technology Cooperation Group (HTCG): ......................................................................................... 7

[Foreign firm in India] ................................................................................................................................... 8

Foreign Direct Investment ....................................................................................................................... 8

[Entry Strategies and setting up a Company] ............................................................................................... 8

The principal forms of business organization in India are: ..................................................................... 8

Joint Venture ............................................................................................................................................ 9

Liaison Office / Representative Office ..................................................................................................... 9

Project Office ............................................................................................................................................ 9

Export/Import of goods ........................................................................................................................... 9

Automatic Route .................................................................................................................................... 10

FIPB Territories : ................................................................................................................................... 11

FDI in EOUs / SEZs / Industrial Park / EHTP / STP ................................................................................. 11

Technical Collaboration.......................................................................................................................... 12

Licensing Of Trademarks ...................................................................................................................... 12

The Territorial Scope ............................................................................................................................... 13

About India .................................................................................................................................................. 14

Disposable income of Indian residence ...................................................................................................... 17

COUNTRY FACTFILE ................................................................................................................................ 17

India ............................................................................................................................................................ 17

Areas ....................................................................................................................................................... 17

Population ............................................................................................................................................... 17

4

Demographic and economic indicators 7 ............................................................................................ 17

Top Ten Amusement Parks in India are ...................................................................................................... 18

Other Popular Amusement Parks in India ............................................................................................. 18

FUTURE OF ANIMATION IN INDIA ............................................................................................................... 19

History ..................................................................................................................................................... 19

Awards and festivals ............................................................................................................................... 19

Societies and organizations .................................................................................................................... 20

Market ..................................................................................................................................................... 20

Comparison with the global scenario ......................................................................................................... 22

Ventures .................................................................................................................................................. 22

Animation institutions ............................................................................................................................ 22

CURRENT STATE OF THE INDIAN ANIMATION INDUSTRY ........................................................................... 23

KEY TRENDS ............................................................................................................................................. 23

Why India is the hub? ................................................................................................................................. 24

Qualified Professionals ........................................................................................................................... 24

Cost factor ............................................................................................................................................... 24

Skills ........................................................................................................................................................ 24

Where is Indian animation heading? ...................................................................................................... 25

Partnership model .................................................................................................................................. 26

Challenges ................................................................................................................................................... 26

The Indian animation industry, however, is not without challenges ..................................................... 26

Intellectual Property ................................................................................................................................... 27

Patents .................................................................................................................................................... 27

Trademarks ............................................................................................................................................. 28

Copyrights ............................................................................................................................................... 28

5

Geographical Indications ........................................................................................................................ 28

Designs .................................................................................................................................................... 29

Future Perfect ......................................................................................................................................... 29

Asian Animation Industry: Strategies Trends & Opportunities 2012.......................................................... 30

Animation VFX and Gaming Technology ................................................................................................. 30

Key Highlights during FY2011 ................................................................................................................. 30

[Current News] ............................................................................................................................................ 31

Nickelodeon launches 'Motu Patlu' ........................................................................................................ 31

Being original .......................................................................................................................................... 31

Coming up ............................................................................................................................................... 32

Animation policy: a work in progress? ........................................................................................................ 32

Largely sketchy ........................................................................................................................................ 32

‘Lack of funds' ......................................................................................................................................... 32

Emphasis on training ............................................................................................................................... 33

Taxes and duties on animation industry: .................................................................................................... 33

Licensing in India: ........................................................................................................................................ 34

Pay Scale India - 3d Animation Industry workers Salary ............................................................................. 35

Social factors ............................................................................................................................................... 35

REFERENCE .............................................................................................................................................. 39

6

Introduction Garner Holt Production (GHP) is interested in investigating if India will be a viable market for

its first global entry, versus other major emerging regions: (1) East Asia, particularly China, (2)

Middle East, particularly UAE, (3) Latin America, particularly Brazil, and (4) Eastern Europe,

particularly Russia. Our team8, which comprises of students from SIMSR (Sakshi, Ajit Kumar

and Hamneesh) and from CSU (Kaushal Tolia, Brian Linton,Viviana Villaneueva, James

Walker and LeJean Ware) , has worked on the viability of Indian and Russian market. During

our research we have majorly conducted secondary research but wherever it was necessary

primary research has been conducted.

This report covers all the economic ,legal and social environmental factors of India and other

part of report covers all the above mentioned factors for Russia.

7

[The free trade agreement] Trade Policy Forum:

The India-US Trade Policy Forum was established after the visit of the Prime Minister Dr.

Manmohan Singh to US in July 2005 to discuss bilateral cooperation on trade and commercial

engagements. USTR and the Minister for Commerce and Industry of India are the co-chairs of

this forum. Five Focus Groups under this have been discussing various trade policy issues of

mutual interest relating to (a) tariff and non-tariff barriers; (b) services; (c)agriculture; (d)

investment; and (e) creativity and innovation. The last and seventh meeting of the TPF along

with Focus Groups (except the Focus Group in Services) in specific areas took place in

Washington DC from September 21-22, 2010. In the Third TPF in 2007, Private Sector

Advisory Group (PSAG) was created consisting of prominent Indian and international trade

experts to provide strategic recommendations and insights to the US-India Trade Policy Forum.

The reconstituted PSAG held its first meeting during the visit of Commerce & Industry Minister

Shri Anand Sharma to Washington DC in March 2010.The second

meeting was held in Washington DC on September 21, 2010 on the

sidelines of the TPF.

High Technology Cooperation Group (HTCG):

This mechanism was set up in 2003 that was brought about a review

of US export license regime for export of high technology dual use

goods to India.Private sector has been made an integral part of this

dialogue. The last and 8th meeting was held in New Delhi on 11-12

July 2011.this visit to India in November 2010 President Obama and

PM Singh agreed on steps to reduce trade barriers and protectionist

measures and encourage research and innovation to create jobs These

included removal of Indian entities from the US Department of Commerce’s “Entity List” and

realignment of India in US export control regulations . Accordingly, US Deptt. of Commerce vide its

United States has free trade

agreements in force with 19

countries. These are :

Australia ,Bahrain ,Canada, Chile

Colombia, Costa Rica, Dominican

Republic , El Salvador ,Guatemala

Honduras , Israel , Jordan , Korea

Mexico ,Morocco, Nicaragua

Oman, Panama, Peru ,Singapore 1

POSTPONEMENT OF U.S.-INDIA TRADE POLICY FORUM (TPF) 3

United States Trade Representative Ron Kirk was previously scheduled to lead a delegation to

India this week for the U.S.-India Trade Policy Forum (TPF). However, while considerable

progress on developing the agenda for the TPF has been made, in view of the amount of

preparatory work that remains to be done, the United States and India have decided to postpone

the TPF until later this year. The additional time will allow us to further develop the TPF agenda

and related activities. We look forward to a highly productive Trade Policy Forum in 2012.

Further details about the rescheduling of the Trade Policy Forum 33oming.

8

notification dated 25 January 2011, removed SRO, DRDO and BDL from its entities list.2

The India-US Trade policy Forum (TPF), established in July 2005, is an arrangement between

the two Governments to discuss trade and investment issues. The TPF is co-chaired by Hon’ble

Minister of Commerce & Industry, Government of India and United States Trade Representative.

The issues and concerns are discussed under five Focus Groups. The dialogue addresses a wide

range of issues that will lead to initiatives in key sectors and create momentum for expanding

bilateral trade. A Private Sector Advisory Group (PSAG) was formed in April 2007 as an adjunct

to TPF to provide the TPF with views and advice from non-government trade and investment

experts. 4

[Foreign firm in India] It is the intent and objective of the Government of India to attract and promote foreign

direct investment in order to supplement domestic capital, technology and skills, for accelerated

economic growth. Foreign Direct Investment, as distinguished from portfolio investment, has

the connotation of establishing a ‗lasting interest‘ in an enterprise that is resident in an economy

other than that of the investor.5

Foreign Direct Investment

Since the beginning of economic liberalization in 1991, the attractiveness of India as an

investment destination has grown at a steady pace. According to a study by Goldman Sachs,

Indian economy is expected to continue growing at the rate of 5% or more & is slated to become

the fourth largest economy by 2050. This favorable scenario has been made possible through an

increased level of flexibility & rationalization of the policies by the government as regards

foreign direct investment.5a

[Entry Strategies and setting up a Company] The principal forms of business organization in India are:

A foreign company can commence operations in India by incorporating a company under the

Companies Act, 1956 through

Joint Ventures

Wholly Owned Subsidiaries

Foreign equity in such Indian companies can be up to 100% depending on the requirements of

the investor, subject to equity caps in respect of the area of activities under the FDI policy.

9

Joint Venture : Foreign Companies can set up their operations in India by forging strategic

alliances with Indian partners. It may entail the advantages like established distribution/

marketing set up of the Indian partner, available financial resource such as accounts receivable

financing & established contacts of the Indian partners which help smoothen the process of

setting up of operations.

Wholly Owned Subsidiary: Foreign companies can also set up wholly owned subsidiary is

sectors where 100% foreign direct investment is permitted under the FDI policy.

For registration an incorporation of a Company an application has to be filed with the Registrar

of Companies (ROC). Once a Company has been duly incorporated & registered as an Indian

company, it is subject to Indian laws & regulations as applicable to other domestic Indian

companies.

As a foreign company

Foreign Companies can set up their operations in

India through

Liaison Office / Representative Office : It acts a channel of communication between

the principal place of business & its entities

in India. Its role is limited to collection of

information about possible market

opportunities & providing information about

the company & its products to the prospective

Indian customers. It can promote

export/import from/to India & also facilitate

technical/financial collaboration between

parent company & companies in India.

Project Office : Foreign companies planning

to execute specific projects in India have now

been granted general permission by Reserve

Bank of India (RBI) to set up temporary

project/site offices in India, subject to

specified conditions. Such offices cannot undertake or carry on any activity except that

incidental & relating to the execution of the project.

Branch Office : Foreign companies engaged in manufacturing and trading activities

abroad are allowed to set up Branch Offices in India for the following purposes

Export/Import of goods

o Rendering professional or consultancy services

o Carrying out research work, in which the parent company is engaged

o Promoting technical or financial collaborations between Indian companies and

parent or overseas group company.

Companies incorporated in

India and branches of

foreign corporations are

regulated by the Companies

Act, 1956, which has been

enacted to oversee the

functioning of companies in

India. The Registrar of

Companies & the Company

Law Board, both working

under the Department of

Company Affairs, ensure

compliance with the Act.

10

o Representing the parent company in India and acting as buying/selling agents in

India.

o Rendering services in Information Technology and development of software in

India.

o Rendering technical support to the products supplied by the parent/ group

companies.

o Foreign airline/shipping Company.

Branch Office on a 'Stand Alone Basis': such branch offices would be isolated &

restricted to the Special Economic Zone (SEZ) alone & no business activity/transaction

will be allowed outside the SEZs in India, which include branches/subsidiaries of its

parent office in India.

Automatic Route

Under the existing policy, FDI up to 100% is allowed under the automatic route in all

activities/sectors except the following, which require the prior approval of the Government

Activities/items that require an Industrial License

Proposals in which the foreign collaborator has an existing financial/technical

collaboration in India in the 'same' field

Proposals for acquisition of shares in an existing Indian Company in

Financial Services Sector

where Securities & Exchange Board of India (Substantial Acquisition of Shares &

Takeovers) Regulations is attracted

All proposals falling outside notified sectoral policy/caps or under sectors in which FDI

is not permitted

FDI in sectors to the extent permitted under the automatic route does not require any

prior approval either by the Government or Reserve Bank of India (RBI).the investors are

only required to notify the Regional office concerned of RBI within 30 days of the receipt

of inward remittances & file the required documents within 30 days of the issue of shares

to the foreign investors.

Government Route

FDI activities not covered under the automatic route require prior Government approval

& are considered by the Foreign Investment Promotion Board (FIPB). An application can

be made online or on a plain paper accompanied by all the relevant documents. The

approvals are generally granted expeditiously.

Forbidden Territories

The extant policy does not permit FDI in the following sectors:

11

Retail Trading

Atomic Energy

Lottery Business

Gambling & Betting

Agricultural or plantation activities or Agriculture (excluding Floriculture, Horticulture,

Development of seeds. Animal husbandry, Pisiculture & cultivation of vegetables, &

service related to agro & allied sectors) and Plantations (other than Tea Plantations)

FIPB Territories

The following comprise an illustrative list of the sectors not under the automatic route (subject to

sectoral regulations & guidelines as notified by the respective Departments/ministries):

Petroleum Sector

Existing Airport Projects

Asset Reconstruction Companies

Atomic Minerals

Broadcasting

Construction Development Projects (Resorts, Townships, commercial Premises etc.)

Defence production

Investing Companies in infrastructure / services sector (except telecom sector)

Print Media

Satellites establishment & operation Equity participation by International Financial

Institutions such as ADB, IFC, CDC, etc. in domestic companies is permitted through

automatic route, subject to SEBI / RBI regulations & sector-specific cap on FDI. Free

repatriation of capital investment & profits is permitted subject to original investment

having being made in convertible foreign exchange. The policy further permits Indian

companies to raise funds in the international capital markets. The Indian capital market is

also open to the Foreign Institutional Investors under the Portfolio Investment Schemes.

FDI in EOUs / SEZs / Industrial Park / EHTP / STP

FDI upto 100% is permitted under the automatic route for setting up of Special Economic Zone

(SEZ). Proposals not covered under the automatic route require approval of FIPB.

FDI upto 100% is permitted under the automatic route for setting up 100% Export

Oriented Units (EOU), subject to sectoral policies. Proposals not covered under the

automatic route would be considered & approved by FIPB.

FDI upto 100% is permitted under automatic route for setting up of Industrial Park

Proposals for FDI / NRI investment in Electronic Hardware Technology Park (EHTP)

Units & Software Technology Park (STP) Units are eligible for approval under the

automatic route, subject to the parameters mentioned under the Automatic route. For

proposals not covered under automatic route, the applicant should seek separate approval

of the Government through the FIPB.

12

Technical Collaboration

RBI accords approval under the automatic route for foreign technological agreements in all

industries for technical know-how, design & drawings and engineering services within the

prescribed monetary limits for lump sum payments & royalty payments. Indian Companies

entering into technology transfer agreements with the foreign companies are permitted to remit

payments towards know-how & royalty under the terms of the foreign collaborations

agreements, subject to certain limits. Indian Companies can hire services of foreign technicians

& make remittances for technical services fees subject to certain conditions regardless of the

duration of engagement of foreign nationals in any calendar year. Dividends & profits earned in

India by foreign companies are allowed to be repatriated after, however, the payment of taxes if

any due on them. No RBI permission is necessary for such remittances except to the compliance

of certain specified conditions.

Licensing Of Trademarks

The Concept

The provision regarding the licensing of trademarks in favors of the registered users was

introduced for the first time in the United Kingdom by the Trade Marks Act, 1938 on the

recommendations of the Goshen Committee which suggested the relaxation of common law

principle that there could be no separation or splitting up between the proprietorship of the mark

& the trade origin of the goods bearing such marks. Cogently put, Trademark Licensing is an

authorization by the proprietor granting to another person the right to exploit his trademark,

either on an exclusive or non-exclusive basis. In international trade, licensing is in the present

day is much more extensive as compared to the domestic market & has now assumed importance

as an indispensable tool of business organization on an international level.

The Indian Scenario

The law governing the licensing of trademarks (The Trademarks Act, 1999) & registration of the

registered users has been substantially modified to reflect the approach towards the modern trend

of business. A Licensee would fall under the definition of a permitted user under the 1999 Act,

where 'Permitted Use' means not only the use by a third person of a registered trademark as a

registered user but also use by a third person of a registered trademark by consent of the

registered proprietor in a written agreement without that person being a registered user. Though

the Act is mute on the question of licensing of an unregistered trademark, yet the courts have

endorsed the same as common law licensing.

13

The Purpose Registered proprietors of trademarks find it beneficial to enter into licensing agreements for

various reasons :

Grant of license for the use of their trademark to subsidiaries / independent manufacturers

To meet a large demand for the goods or services bearing such marks, which they are not

incapable to meet through their own operations

The profitability quotient which accrues to the proprietor through an exchange for a

license fee or royalty.

The Territorial Scope

The territorial limits of a license agreement for a registered trademark are determined by the

consent of the parties. The owner of an unregistered trademark selling his goods in a particular

territory acquires the right of trademark in that territory only. The same trademark can be used

by any other person outside the territory without violating the trademark rights vested in the

owner.

The Term

There is no fixed term for the grant of license under the Act & the same is dependent on the

terms of license agreement entered into between the licensor & the licensee. Nevertheless, the

law provides for a confirmation at any time by the Registrar of Trademarks from the proprietor,

as to whether the registered user arrangement still subsists.

Rights & Obligations of the Licensor

As the maker of goods seeks to acquire & maintain a reputation for the quality of his goods, the

licensor has the right to exercise control over the quality of the products manufactured &

marketed under the trademark license. The owner also has the means to review the manner in

which the trademark is being used by the licensee. The licensor has a right for the 'permitted use'

of his mark to be considered as use by him & so no application can be filed by anyone for

revocation of the trademark on the grounds of non-use, if there is a permitted use of the

trademark in that period. Further, the registered licensor has the right to maintain the continuing

distinctiveness of the trademark.

Since the function of the trademark is to indicate the trade origin of goods & services, to prevent

any deception of the public, the Act imposes an obligation on the licensor/owner of the

trademark to maintain a connection in the course of trade with those goods & services. The

registered proprietor also has an obligation to confirm to the Registrar as to whether the

Agreement filed before the Registrar continues to be in force.

Rights & Obligations of the Licensee

A registered user has a right to use the registered trademark in relation to the goods or services

for which it is registered, but does not get any assignable or transmissible right to use the mark.

However, the registered user has the right to file suit for infringement in his own name, making

the registered proprietor a defendant. The rights & obligations of such registered user must be

14

concurrent with those of the registered proprietor. A 'permitted user', however will have no rights

to institute any proceedings for any infringement. The obligations of the licensee can be

introduced & the existing ones can be further qualified by the stipulations under the License

Agreement.5b

About India

India is the 7th largest and 2nd most populous country in

the world. It is also the 4th largest economy in the world

in terms of PPP. A series of ambitious economic

reformsaimed at deregulating the economy and

stimulating foreign investment has moved India firmly

into the front runners of the rapidly growing Asia Pacific

Region and unleashed the latent strength of a complex

and rapidly changing nation. Today India is one of the

most exciting emerging markets in the world. Skilled

managerial and technical manpower that matches the best

available in the world, provide India with a distinct

cutting edge in global competition. India’s time tested

institutions offer foreign investors a transparent

environment that guarantees the security of their long

term investments. These include a free and vibrant press,

a well established judiciary, a sophisticated legal and accounting system and a user friendly

intellectual infrastructure. India’s dynamic and highly competitive private sector has long been

the backbone of its economic activity and offers considerable scope for foreign direct

investment, joint ventures and collaborations.

2. Industrial Policy

The Government’s liberalization and economic reforms programmed was initiated in July 1991,

under the new Industrial Policy Resolution. The industrial policy reforms have substantially

reduced the industrial licensing requirements, removed restrictions on expansion and facilitated

easy access to foreign technology and foreign direct investment.

3. Foreign Direct Investment Policy

Foreign Direct Investment in India is allowed on automatic route in almost all sectors except –

Proposals that require an industrial license and cases where foreign investment is more than 24%

in the equity capital of units manufacturing items reserved for the small scale industries.

Proposals in which the foreign collaborator has a previous venture/tie-up in India.

15

Proposals relating to acquisition of shares in an existing Indian company in favour of a

Foreign/Non-Resident Indian (NRI)/Overseas Corporate Body (OCB) investor; and

Proposals falling outside notified sectoral policy/caps or under sectors in which FDI is not

permitted and/or whenever any investor chooses to make an application to the Foreign

Investment Promotion Board and not to avail of the automatic route.

4. Foreign Investment Promotion Board (FIPB)

FIPB is a competent body to consider and recommend foreign direct

investment (FDI), which do not come under the automatic route. With

the shifting of the FIPB to the Department of Economic Affairs,

Ministry of Finance, the FIPB has been reconstituted and renders

more efficient and prompt services.

5. Industrial Approvals/clearances

For starting a new project, a number of industrial

approvals/clearances are required from different authorities such as

Pollution Control Board, Chief Inspector of Factories, Electricity

Board, Municipal Corporations, etc.

6. Foreign Exchange Management Act (FEMA)

The Parliament has enacted the Foreign Exchange Management Act,

1999. This Act came into force on the 1st day of June 2000. The

object of the Act is to consolidate and amend the law relating to

foreign exchange with the objective of facilitating external trade and

payments and for promoting the orderly development and

maintenance of foreign exchange market in India. This Act extends to

the whole of India and will also apply to all branches, offices and

agencies outside India owned or controlled by a person resident in

India. It will also be applicable to any contravention committed

outside India by any person to whom this Act is applicable.

7. Taxation in India

Since the onset of liberalization in the country, tax structure

of the country is also being rationalized keeping in view the

national priorities and practices followed in other countries.

Foreign nationals working in India are generally taxed only

on their Indian income. Income received from sources

outside India is not taxable unless it is received in

India. Company taxation - Foreign companies are subject to

16

a maximum tax of 40% on its net profits. The effective tax rate for domestic companies is

36.75% while the profits of branches in India of foreign companies are taxed at 40%. Companies

incorporated in India even with 100% foreign ownership, are considered domestic companies under the Indian laws.

8. Labour Rules/Regulations

Under the Constitution of India, Labour is a subject in the Concurrent List

where both the Central & State Governments are competent to enact

legislation. Some of the important Labour Acts, which are applicable for

carrying out business in India are – Employees’ Provident Fund and

Miscellaneous Provisions Act, 1952; Employees’ State Insurance Act,

1948; Workmen’s Compensation Act, 1923; Maternity Benefit Act, 1961;

Factories Act, 1948; Minimum Wages Act; Payment of Wages Act, 1936.

9. Incentives offered by States

India is a federal country consisting of States and Union Territories. States are also partners in

the economic reforms being undertaken in the country. Most of the States have made serious

efforts for simplifying the rules and procedures for setting up and operating the industrial units.

Single Window System is now in existence in most of the States for granting approval for setting

up industrial units. Moreover, with a view to attract foreign investors in their states, many of

them are offering incentive packages in the form of various tax concessions, capital and interest

subsidies, reduced power tariff, etc.

10. Foreign Investment Implementation Authority (FIIA)

Government of India has set up Foreign Investment Implementation Authority (FIIA) to facilitate

quick translation of Foreign Direct Investment (FDI) approvals into implementation by providing

a pro-active one stop after care service to foreign investors, help them obtain necessary approvals

and by sorting their operational problems. FIIA is assisted by Fast Track Committee (FTC),

which have been established in 30 Ministries/Departments of Government of India for

monitoring and resolution of difficulties for sector specific projects. 6

17

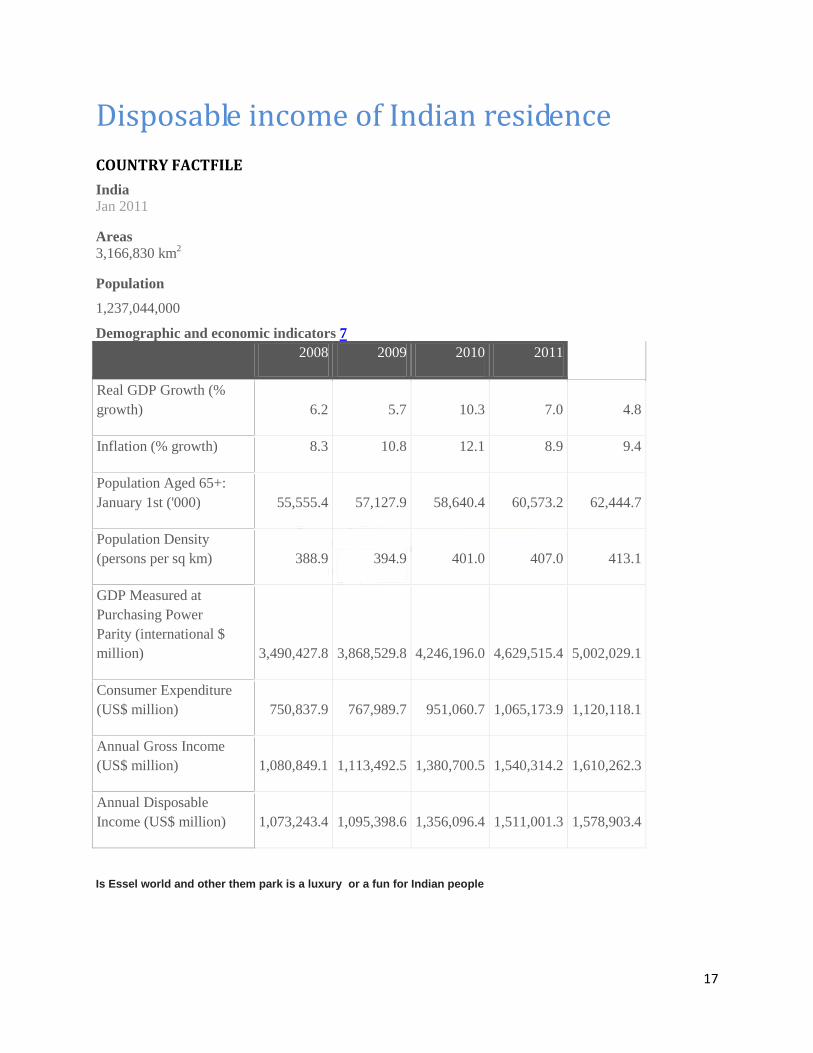

Disposable income of Indian residence

COUNTRY FACTFILE

India Jan 2011

Areas

3,166,830 km2

Population

1,237,044,000

Demographic and economic indicators 7

2008 2009 2010 2011 2012

Real GDP Growth (%

growth) 6.2 5.7 10.3 7.0 4.8

Inflation (% growth) 8.3 10.8 12.1 8.9 9.4

Population Aged 65+:

January 1st ('000) 55,555.4 57,127.9 58,640.4 60,573.2 62,444.7

Population Density

(persons per sq km) 388.9 394.9 401.0 407.0 413.1

GDP Measured at

Purchasing Power

Parity (international $

million) 3,490,427.8 3,868,529.8 4,246,196.0 4,629,515.4 5,002,029.1

Consumer Expenditure

(US$ million) 750,837.9 767,989.7 951,060.7 1,065,173.9 1,120,118.1

Annual Gross Income

(US$ million) 1,080,849.1 1,113,492.5 1,380,700.5 1,540,314.2 1,610,262.3

Annual Disposable

Income (US$ million) 1,073,243.4 1,095,398.6 1,356,096.4 1,511,001.3 1,578,903.4

Is Essel world and other them park is a luxury or a fun for Indian people

18

Top Ten Amusement Parks in India are

1. Ocean Park, Hyderabad

2. Veegaland, Kochi

3. Essel World and Water Kingdom, Mumbai

4. Fun n Food Village, Gurgaon

5. Adventure Island, Delhi

6. Nicco Park, Kolkata

7. Entertainment City, Noida

8. Wonder La, Bangalore

9. MGM Dizzee World, Chennai

10. Ramoji Film City, Hyderabad

Other Popular Amusement Parks in India

11. Gujarat Science City, Ahmedabad

12. Snow World, Hyderabad

13. Worlds of Wonder, Noida

14. Baywatch, Kanyakumari

15. Shanku Water Park, Ahmedabad 8

19

FUTURE OF ANIMATION IN INDIA History

The first animated film from India is considered to be "Ek Anek Aur Ekta", a short

traditionally animated short educational film released in 1974[ from Doordarshan's Film

Division. Doordarshan is a government run public television service in India. The film is

presented as a fable meant to teach children the value of unity. After its success, more

shorts were produced by Doordarshan. This was the first time that original animated films

from India were broadcast on national television in Hindi.

The first Indian animated television series is Ghayab Aaya, aired in 1986 and directed by

Suddhasattwa Basu.

The First Indian 3D + VFX was done for television series "CAPTAIN VYOM" by

MAYA ENTERTAINMENT LTD.

The first Indian 3D animated film is Roadside Romeo, which was a joint venture between

Yash Raj Films and the Indian division of the Walt Disney Company. It was written and

directed by Jugal Hansraj.

Awards and festivals

24FPS Animation Awards is a celebration of animation excellence and recognition of the best

animation talent in India. Organized with the aim of creating a platform that motivates, hones

and showcases Indian animation and student talent. Annually held 24FPS Animation Awards is

amongst the premier animation competitions in the country. It is organized by Maya Academy of

Advanced Cinematic (MAAC).The 24 FPS Animation Award 2005-06 had more than 250

students that participated from across India. 24 FPS acts as a catalyst to bring the students &

studios at one platform wherein the students showcase their skills in front of the top industry

professionals & studios, which in turn acts as a placement platform for the students.

Anifest India is an annually held animation festival with an education track. The focus is on

technical and hands-on presentations with case studies from top professionals across holistic

disciplines of art, animation and filmmaking. On the education side, premier schools and

educators from all over India and overseas present their approach and viewpoints. The best

student, faculty and professional films get showcased at the TASI Viewers Choice Awards

(TVCA), an audience award which for many attendees is their first taste of attending a film

festival and voting. Over three thousand people attend the festival which in recent years has

spanned three entire days.

20

Societies and organizations

The Animation Society of India (TASI) is a non-profit organization with its head-office in

Mumbai. It aims to educate about the emerging animation technologies and at the same time

provide a platform for exchange of creative and technical information within the existing art and

animation fraternity in India. It also hosts Anifest India, the biggest annual animation festival in

the Indian subcontinent, which features the TASI Viewer's Choice Awards. It also hold technical

and in-depth workshops and sessions nearly every month

Market

The Indian animation industry was estimated at $354 million in 2006 and was forecast to reach

$869 million by 2010.[5] Animation in India is currently riding on two key factors - a large base

of highly skilled labour, and low cost of production. While the industry is gaining prominence

steadily, several important factors such as the government's role in supporting the animation

industry, and producing original content locally.

In 2009, the state of the animation industry in India, was growing at a CAGR of 30%, is

estimated to reach US$ 1.5 billion by 2015.[citation needed]

Some of the other estimates of the NASSCOM report on animation indicate the following:

The global entertainment market will generate a demand for animation production

services of the order of US$ 37 billion by 2003

In the non-entertainment segment the demand for animation production services will

touch US$ 14.7 billion by 2015

The global film/TV program production market will create a US $ 17.5 billion revenue

opportunity for animation production houses

The usual procedure is for pre-production (preparing the script, storyboard, and exposure sheets)

to be done in the United States or other headquarter countries, after which, the package is sent to

Asia for production (drawing cels, colouring by hand, inking, painting, and camera work). The

work is sent back to the U.S. or other headquarter country for post-production (film editing,

colour timing, and sound). Offshore animation has led to the creating and nurturing of a local

industry, as an infrastructure is built up, equipment is put into place, and skills are transferred.

An emerging trend in the Asian animation industry is the increasing focus towards production of

local animation content for television as well as production of animated movies. An increasing

number of Asian animation studios are giving importance to owning and protecting animation

content by investing in intellectual property protection mechanisms.10

21

The Indian gaming industry was estimated at nearly $48 million in 2006 and is expected

to cross $424 million by 2010.

Pune, is competing with Hyderabad and Mumbai to be the country's animation hub. With the

sector facing severe human resources shortage, more and more studios are increasingly venturing

into animation training. Chetan Deshmukh, an animator and special effects expert, recently

shifted his base to Pune from US. He has worked on Hollywood movies like Chicago and

Shanghai Knights. The Mahratta Chamber of Commerce, Industries and Agriculture (MCCIA), a

premier body of industries in and around Pune region has launched a programme to catapult

Pune as a global hub for animation and gaming. It has recently formed a group of professionals,

training institutes and celebrities to implement the initiative, with filmmaker Amol Palekar has as

their brand ambassador.9

The Indian animation industry was estimated at $354 million in 2006 and was forecast to reach

$869 million by 2010.[5] Animation in India is currently riding on two key factors - a large base

of highly skilled labour, and low cost of production. While the industry is gaining prominence

steadily, several important factors such as the government's role in supporting the animation

industry, and producing original content locally.

In 2009, the state of the animation industry in India, was growing at a CAGR of 30%, is

estimated to reach US$ 1.5 billion by 2015.[citation needed]

Some of the other estimates of the NASSCOM report on animation indicate the following:

The global entertainment market will generate a demand for animation production services of the

order of US$ 37 billion by 2003

In the non-entertainment segment the demand for animation production services will touch US$

14.7 billion by 2015

The global film/TV program production market will create a US $ 17.5 billion revenue

opportunity for animation production houses

The Indian gaming industry was estimated at nearly $48 million in 2006 and is expected to cross

$424 million by 2010.[6]

Pune, is competing with Hyderabad and Mumbai to be the country's animation hub. With the

sector facing severe human resources shortage, more and more studios are increasingly venturing

into animation training. Chetan Deshmukh, an animator and special effects expert, recently

shifted his base to Pune from US. He has worked on Hollywood movies like Chicago and

Shanghai Knights. The Mahratta Chamber of Commerce, Industries and Agriculture (MCCIA), a

premier body of industries in and around Pune region has launched a programme to catapult

Pune as a global hub for animation and gaming. It has recently formed a group of professionals,

training institutes and celebrities to implement the initiative, with filmmaker Amol Palekar has as

their brand ambassador.[7]

22

Comparison with the global scenario The total global animation production figures, according to the NASSCOM Animation report,

range between US$ 16-31.5 billion for the year 2000. Statistics for 2001 stand anywhere between

US$ 25 billion and US$ 38 billion. Analysts estimate that the global animation production rose

to about US$ 45 billion in 2002.[8]

Ventures

Continuing its impressive financial run, Chennai-based Media Technology Company Sanraa

media,has signed a £ 2 million deal with the global production company Endemol, UK for the

production of the animated series The 99, which is based on the illustrated comic The 99. The

99, a 3D animation series, will comprise 26 episodes will be done by Sanraa Media and day-to-

day production will be overseen by Endemol.

The co-production deal also entitles Sanraa Media to the rights of distributing the series in India,

Indonesia, Malaysia, Pakistan, Sri Lanka and Thailand.

Animation institutions

Asian Academy Of Film & Television

DSK Supinfocom

Frameboxx Animation & Visual Effects

Image College of Arts, Animation & Technology

MAAC (Maya Academy of Advanced Cinematics)-An Aptech Company

National Institute of Design,Ahmedabad

Whistling woods school of Animation, Mumbai

college of art,delhi

priyass film & animation academy kunnamkulam,kerala

23

CURRENT STATE OF THE INDIAN ANIMATION INDUSTRY

There is a considerable increase in the 2D and 3D animation outsourcing to India. Due to the

extremely competitive climate as well as the global slow-down, some of the large studios in the

US have implemented large amounts of layoffs of animators and artists. India is slowly emerging

as an alternative to Korea, Philippine and Taipei for animation outsourcing. India is also

emerging as a post-production hub for animation. Post production involves a lot of ink, paint and

compositing and scanning work, which is the labor intensive part of the entire process of

animation and requires less skill. Thus we can see that the animation industry in India is

following a similar evolutionary part as the software industry. In the early part of the evolution

of the India software industry, it was the low value jobs which were shifted to India. Over time it

is projected that more and more high value jobs would be outsourced to India. For low value

post-production works, it is easier for a studio in the US to outsource its post production work as

probably nothing is going to go wrong. India has one of the lowest labor rates, which makes it an

attractive destination for animation outsourcing.

KEY TRENDS

Indian animation companies are moving up the value chain to own and co-produce intellectual

property rights. This is a shift from the model of outsourcing animation production from

international studios. The Indian animation companies are also focusing on strategic alliances

with overseas studios with the eye to establish a presence in the global animation market.

Content creation in the country has peaked and big Indian studios are increasingly making their

presence felt in foreign markets. Indian studios are developing rapidly and a trend being

witnessed is one of modularization of animation wherein expert from multiple animation

companies, come together to execute specific functions in the production value chain. Some

work on the design, storyboarding, layouts etc while others focus more on other elements of the

process i.e. animation, texturing, lighting etc. These were models which had been perfected

previously in mature animation countries such as Korea. This model is being increasingly

adopted by Indian animation studios based on the ability of the studios to be process driven

enough to distribute the work in modular units without loss of time or quality.

Indian animation companies are garnering larger chunks of the animation outsourcing pie and are

also moving up the value chain by co-owning IPR, co-producing animation products for

television or home videos or theatrical releases. Given the large domestic demand, India is also

likely to evolve into a significant animation consumption country and the demand for local

animation content is rising which is exemplified by the tremendous success of the first fully

locally produced movies such as Hanuman, and TV shows such as Chhota Bheem etc. Plus there

is the tremendous untapped market for merchandising. Popularity of channels such as Cartoon

Network, Pogo, Nick etc. has resulted in more opportunities for studios in India. Indian cities

such as Mumbai, Hyderabad and Bangalore are offering a state-of-the-art mix of software skills,

production and animation expertise and studio infrastructure.

24

The demand for Indian animation production for export comes mainly from feature film

producers and distributors, broadcasting channels, game software producers and advertisement

film producers. As of now, Indian animation companies are working with a number of leading

foreign studios. 11

The global animation industry is all set to explode to double digit growth with India fast

emerging as a leading animation and visual effects outsourcing hub for Hollywood filmmakers.

Production houses in the U.S. are making a beeline to outsource large chunks of work to India,

catapulting Indian professionals to a different league of big-budget blockbusters.

Although the Indian outsourcing industry is at a nascent stage, the industry's growth has been

phenomenal, largely due to the reputation that the Indian outsourcing has earned across the

world in a short time. The National Association of Software and Service Companies (NASSCOM)

has estimated that the global animation market will grow from USD 59 billion in 2006 to USD

80 billion by 2010. The global market for animated content and related services is estimated at

USD 26 billion and is forecast to cross USD 34 billion by 2010. The Indian animation industry is

expected to reach USD 869 million (Rs. 4084.3 crore) by the end of year 2010 at an estimated

CAGR of 52.2 percent

Why India is the hub?

Qualified Professionals

One definite answer is that large numbers of qualified and employable professionals in India,

combined with increasing interest amongst the younger, college-going strata, make the country

lucrative as an outsourcing destination. Moreover, India's workforce is known to have the

dexterity to partner with the clients for better customer service. Also most of the workforce in the

Indian animation outsourcing industry has better understanding of English language and this

places them ahead of other countries.

Cost factor Consider this. It costs anywhere between USD 200,000 - USD 400,000 to produce a 30-minute

animated show in the US. The same work is executed in India at a cost of USD 70,000 (Rs.

0.32crore). Companies like Walt Disney Pictures, Time Warner's Cartoon Network, and Sony

Pictures have already outsourced work to India. Though initially it all started with low-end bulk

work, Indian companies have worked their way up the ladder and are now working on high-end

animation. The Indian animation outsourcing industry started work on the cost arbitrage platform

but soon moved to the quality parameters for deal making. Now the deals are quality, delivery

timelines, and adherence to norms which have ensured that we have an enhanced reputation in

the global market.

Skills The animation industry is still young. Indian cinema is yet to make its mark on the global stage.

The booming animation outsourcing industry is constantly demanding new skills and fresh

infusion of new talent into the industry. As such, it is imperative that we have a healthy pipeline

to supply talent to the industry.

25

Skills required in the animation field can be clubbed under two broad categories, mainly

technical skills and soft skills. Programming expertise, analytical ability, and proficiency on the

software are basic requirements for technical skills. The number of professionals joining the

animation industry has been growing at a compound annual growth rate (CAGR) of 18.2 percent

and is expected to grow at the same rate. Though India possesses the manpower with the

requisite skill set, what remains an area of concern is the education imparted to this manpower

from the quality perspective.

This has resulted in mushrooming of multimedia institutes. What is interesting is that quite a few

reputed organizations have come forward and started a chain of multimedia institutions for two

reasons. One, they can use the trained professionals for in-house animation development and

secondly, use this education channel for market diversification and penetration. However,

companies need to invest considerable time and money in bringing these students up to the levels

where they start earning revenue for the organization.

Look at what some Indian animation companies, especially those operating in the outsourcing

sphere, are doing to meet the quality manpower. The solution involves hiring beginners from the

market and then imparting training to them so as to bring them up to client expectations. They

are also bringing in experienced professionals (especially from Hollywood) to train the

workforce. Some organizations have even gone to the extent of hiring international talent.

Where is Indian animation heading?

The Indian animation industry is currently at the bottom of the animation pyramid. Presently,

global outsourcing happens at the production stage. This involves creation of animation, air-

brushing of characters, lip synchronization, scanning, and compositing. As with all the work that

we do in the outsourcing space, we are steadily moving up the value chain. The industry is

pitching for business in both pre-and-post production stages. In the pre-production stage, Indian

firms are targeting activities like

Storyboarding

Dialog writing

Layout preparation

Post-production work primarily revolves around audio and music editing and film compositing.

The major work in this field is happening around content development for TV and broadcast

mediums. The present quality of work being delivered by Indian companies is encouraging

outsourcers to look at sending out even high-end post-production work to India. This will enable

Indian firms to focus on end-to-end delivery, with the client focusing on the creative and pre-

production work.

Indian firms are also pitching for work in the visual effects (VFX) arena as the demand for the

same is increasing. It is VFX which constitutes majority of the work in the post-production stage

of films. Indian companies today are focusing on low-end work like wire removal, removing

tracking markers, crowd multiplication, green matte removal and compositing, and set extension.

A clutch of companies is putting their energies behind similar work for films. This involves not

26

only convincing customers about the assured quality but also training the resources for delivering

international quality of work. Companies like Satyam BPO and Prime Focus have built

capabilities in the VFX arena. Other creative studios like Cinesite have also done the same.

Partnership model

With the Indian television and movie industry creating content worth hundreds of hours each day, it is but

obvious that Indian outsourcing firms would also look at this form of outsourcing. In an age when

'Content is King', many firms like DQ Entertainment are looking at not just outsourced work but also at

co-producing/sole producing movies. This helps them gain content rights and build their portfolio. These

initiatives place India firmly on the outsourcing world map. Many boutique animation outsourcing firms

are now solely focusing on generating content and selling it to various organizations. This is not only in

the field of movies and episode-based programs but also in the arena of marketing and educative

programs. Organizations are targeting the huge market for interactive marketing and e-learning and using

the expertise gained in animation outsourcing to service leading customers in these areas.

Challenges

The Indian animation industry, however, is not without challenges.

Quality manpower shortage. Indian firms are looking at innovative ideas for shoring up their

workforce. Apart from calling in industry experts, the industry is also tying up with institutions

to develop and impart industry specific course content.

Government support. The Indian animation outsourcing industry has grown at a scorching pace.

This gets dwarfed when compared to the opportunity available in the market. Countries like

Singapore and Canada are giving stiff competition to the Indian outsourcing industry. They have

been able to do so due to the support of their governments. In Singapore, the animation industry

has made great strides due to the immense support provided by the Economic Development

Board of Singapore. It has even formed a Media Development Agency to facilitate the same.

India, though being the pioneer of outsourcing industry, has not found much initiative being

taken by the government to promote animation industry. The IT industry is a great example of

how industry beneficial policies can help industry growth. What the animation outsourcing

industry requires now is a whole set of policies for its benefit.

Outsourcers have always been concerned with the protection of their intellectual property in

India. India is one of the few countries which have failed to take stern action against its

infringement. India needs to strengthen its IP policy and ensure that companies operating in the

outsourcing sphere take stringent steps to take care of clients' IP rights.

Ability to scale operations. Indian firms are facing a talent shortage which affects their ability to

scale up their operations based on client demands. This also affects the client's confidence in

offshoring large chunks of work. Though Indian companies have put in place huge expansion

plans, these are often marred by various reasons. Tie-ups with educational institutes are helping

overcome this difficulty.

27

Intellectual Property

Intellectual property, of whatever species, vests in the valuable production of human mind,

labour, skill & efforts. It is in the nature of intangible incorporate property & vests in the owner

an exclusive right that is vital to success in obtaining & maintaining a competitive advantage in

any commercial & industrial activity. It primarily comprises of: Patents, Trademarks,

Copyrights, Designs & Geographical Indications. As a reflection of the maxim ubi jus ibi

remedium, in India there are four statutes (along with rules) which protect the infringement or

violation of the intellectual property of a person :

The Patents Act, 1970

The Trademarks Act, 1999

The Copyright Act, 1957

The Designs Act, 2000

Patents

Patent is an exclusive & territorial right granted to the owner of an invention (product /

process) to make, use, manufacture & market the invention. To be patentable, a product /

process must embrace the characteristics of novelty, industrial applicability & non-

obviousness. The protection granted to the invention is for a limited period (normally 20

yrs.)

An application for obtaining may be made by the first & true inventor or his assignee /

legal representative .The patent application would be accompanied with complete

/ provisional specification (description, usage methods & scope of the invention) which is

then allotted a priority date. The applicant should then file for the examination of his

patent application within 12 months of his filing for the patent.

Accordingly, examination report is received upon which objections are to be invited

within 3-4 months. If the examiner raises no objections, the same would be published in

the gazette. If no objections are received from the public the applicant is awarded the

patent within a further period of three months. On the other hand, if objections are

received the same goes for hearing & disposal to the Examiner (patents). There are

provisions for appeal to the Appellate Board & further to the High courts & Supreme

Court. The final disposal may take around 6-8 years.

The month of January 2005 was marked by the lapse of the 'transition period' given to the

developing nations to adjust themselves to the global patent regime; thus rendering the

provision of EMRs & mailbox applications redundant.

India joining the Patent Cooperation Treaty, Dec'98 (hereinafter PCT) simplified the

procedure of filing of patents. The PCT application allows the applicant to know about

the potential Patentability of his invention (through international search report & optional

international preliminary examination). Unlike the traditional patent system, the PCT

system consolidates & streamlines patenting procedures, reduces costs & helps in

decision making.

28

Trademarks

Trademark may be defined as a mark (in the form of label, word, device etc.) capable of

distinguishing goods or services of one person from another & which can be graphically

represented. Distinctiveness (acquired / inherent) is the most important feature of a

trademark.

The registration of a trademark is not mandatory, but its non- registration keeps it devoid

of protection against infringement; though, of course, the common law remedy of passing

- off is always available.

The Act provides for absolute (devoid of distinctive character etc.) as well as relative

(identity or similarity with other goods or services etc.) Grounds of refusal of registration.

The act further gives an exclusive right to the proprietor of a registered trademark to use

the same in relation to his goods or services & even to file a suit for infringement &

obtain injunction, damages etc.

The registration of the trademark involves application to the registrar, advertisement of

the application, inviting of opposition, correction & amendment followed by registration.

The registration subsists for a period of ten years after which it has to be renewed.

The trademark is also capable of being assigned & transmitted by the proprietor

Copyrights

Copyright subsists in the original literary, dramatic, musical, artistic works,

cinematograph films & sound recordings. It is an intangible, incorporeal right granted to

the author or originator of the above works whereby he is invested, for a specific period,

with the sole & exclusive privilege of multiplying, publishing & selling copies of his

works. The specified period is sixty years, following the year in which the work was first

published.

The copyright exists in the tangible expression or the form of an idea & not in the idea

itself. That is why even translations & arrangements form a part of copyrightable subject

matter.

The author is generally the owner of copyright & enjoys a bundle of rights in relation to

his creation - reproduction in any form, communication, translation, adaptation etc. this

further augments the scope of assignment & transmission of copyright.

Barring cases of fair dealing or reproduction for educational or judicial purposes, any act

done by a person, in relation to the matter that enjoys copyright & without a license from

its exclusive owner, constitutes infringement. Civil, criminal & administrative remedies

are available to the owner & his assignees.

Geographical Indications

Geographical indications may be defined as an indication, which identifies such goods as

agricultural, natural, or manufactured goods as manufactured in particular territory,

region locality etc. the indication specifies the quality & reputation, which is essentially

attributable to the geographical origin of goods.

29

The Geographical Indication of Goods Act, 1999 provides detailed & streamlined

procedure for the registration of such indications. The registration, though not

compulsory, of course, provides prima-facie evidence of validity. The procedure is

similar to that of trademarks - application, advertisement, inviting

opposition, amendment/correction & the grant. Registration subsists for 10 years after

which it should be renewed

Nevertheless, unlike trademarks, there is an express prohibition on assignment/

transmission of geographical indication.

Designs

Design means the feature of shape, configuration, and pattern applied to any article by

any industrial process; which in the finished article appear to & are judged solely by the

eye. The primary object of the statute in India is to protect the shape & not the function. it

does not include a method or principle of construction.

The designs which are not new / original or has been disclosed or is not sufficiently

distinguishable cannot qualify for registration. After the registration of the designs, the

registered proprietor enjoys a copyright in the design for 10 years; this right can be

further extended for a period of 5 years.

After obtaining registration of the design the owner of the design is entitled to restrain

others from infringing his designs or importing articles bearing the designs.

Future Perfect

India is well on its way to becoming the hub for animation outsourcing. A step further,

Hollywood filmmakers are looking at shooting their movies in India. The Indian

entertainment industry is booming like never before. In fact, there could be a time when

Hollywood flicks will be shot in India, the post production work done here, and the

movies sold out of India.11a

30

Asian Animation Industry: Strategies Trends & Opportunities 2012

Much of Asia's animation production since the 1960s has been tied to foreign interests attracted

by stable and inexpensive labour supplies. For nearly forty years, western studios have

established and maintained production facilities, first in Japan, then in South Korea and Taiwan,

and now also in the Philippines, Malaysia, Singapore, Vietnam, Thailand, India, Indonesia, and

China. The economics of the industry made it feasible for Asia to feed the cartoon world, to the

extent that today, about 90% of all American television animation is produced in Asia.

The usual procedure is for pre-production (preparing the script, storyboard, and exposure sheets)

to be done in the United States or other headquarter countries, after which, the package is sent to

Asia for production (drawing cels, colouring by hand, inking, painting, and camera work). The

work is sent back to the U.S. or other headquarter country for post-production (film editing,

colour timing, and sound). Offshore animation has led to the creating and nurturing of a local

industry, as an infrastructure is built up, equipment is put into place, and skills are transferred.

An emerging trend in the Asian animation industry is the increasing focus towards production of

local animation content for television as well as production of animated movies. An increasing

number of Asian animation studios are giving importance to owning and protecting animation

content by investing in intellectual property protection mechanisms. 12

Animation VFX and Gaming Technology

Over the years, the Animation & Gaming industry has seen the entry of many global majors who

have tapped into India’s talent pool for offshore delivery of services. While initial work

offshored to India was low end and support oriented, India is now seen as a leading destination

for high end, skill based activities. As a result, there has been an uptake of activities around co-

production of animation movies that involve participation of Indian studios across the value

chain. Increased availability of latest games at lower price points and newer pricing models has

made gaming an attractive industry in India. However, the industry being in a nascent stage of

development, it is critical to nurture this industry for it to be able to compete at a global scale.

Key Highlights during FY2011

In 2010, the Animation, VFX and post production industry witnessed a growth of 17.5

per cent over 2009 to reach Rs 23.6 billion. The growth was largely led by the VFX

segment which grew by 42 per cent and post production which grew by 17 per cent*

In 2010, the Animation industry grew by 10 per cent to touch Rs 10 billion*

Domestic companies have started to focus on improving quality and the creation of

original IP, which can be leveraged in terms of merchandizing and broadcast revenues.

New business models have evolved in the marketplace, to successfully tackle current

challenges such as piracy, lack of effective distribution etc, which has led to increased

market penetration, and heightened awareness about the animation and gaming industry.

Consolidation in the industry will continue in the coming 3 to 5 years, with smaller

facilities likely to get absorbed by larger players and the studio model expected to gain

dominance in India.

31

While the growing demand for television content continues to be a key driver for growth

of the animation industry, the demand supply issue for trained talent still exists, though

vocational programs are being introduced along with regular curriculum to offset this

demand.

Recognizing this industry as a significant user of technology, and to play a seminal role

in developing India’s domestic media and entertainment industry, NASSCOM formed

NAGFO (NASSCOM Animation & Gaming Forum) to catalyze the growth of the

industry and also establish an interface with the government.

(*Source: FICCI-KPMG Indian Media and Entertainment Industry Report 2011)13

[Current News]

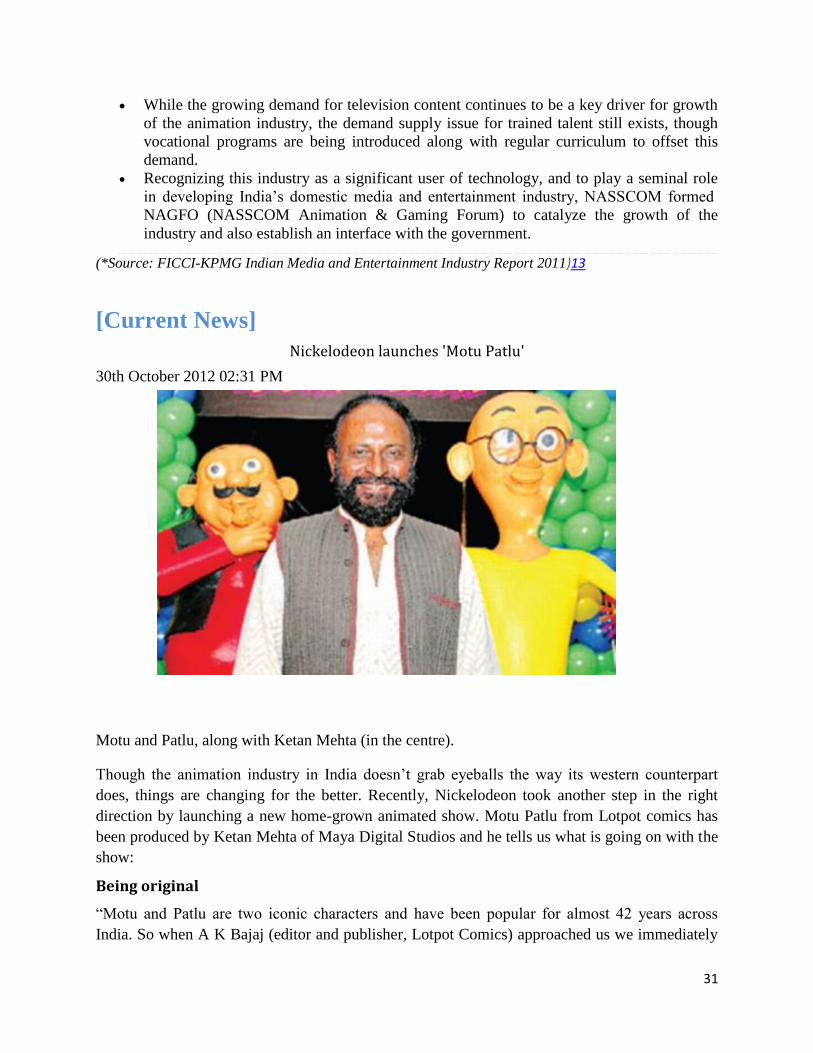

Nickelodeon launches 'Motu Patlu'

30th October 2012 02:31 PM

Photos

Motu and Patlu, along with Ketan Mehta (in the centre).

Though the animation industry in India doesn’t grab eyeballs the way its western counterpart

does, things are changing for the better. Recently, Nickelodeon took another step in the right

direction by launching a new home-grown animated show. Motu Patlu from Lotpot comics has

been produced by Ketan Mehta of Maya Digital Studios and he tells us what is going on with the

show:

Being original

“Motu and Patlu are two iconic characters and have been popular for almost 42 years across

India. So when A K Bajaj (editor and publisher, Lotpot Comics) approached us we immediately

32

agreed,” shares Mehta who feels that while the animation industry is still at the nascent stage, it

is “growing at a rapid pace.”

Coming up

Mehta’s production house has completed converting Sons of Ramayana to 3D. “We are also

working on Captain Vyom, India’s first sci-fi animated series,” offers the director whose movie,

Rang Rasiya, will also release next year. “Talking about movies, there is Mountain Man with

Nawazuddin Siddiqui in the the lead, about a poor man in Bihar who dug up a mountain for 22

years in memory of his wife,” concludes Mehta.14

Animation policy: a work in progress?

This week, the State Government unveiled its much-talked-about policy on the animation and

gaming sector. Akin to its previous policies for the IT, BT and hardware sector, this policy too

primarily aims to attract fresh investments in this emerging field, with an eye on the services and

outsourcing sector, and on building and training a skilled workforce to meet the projected

demand.

With this policy, titled ‘Karnataka Animation, Visual Effects, Gaming and Comics Policy', the

State projects an industry worth of Rs. 10,000 crore by the end of 2012, which it hopes will grow

by at least 40 per cent by 2015.

Largely sketchy

However, industry members, many of whom have collaborated with the Government in evolving

this policy, see the current version of the policy as a “work in progress”. A lot of the policy,

particularly the parts dealing with venture funds and sops the Government has promised, is

largely sketchy.

At the panel discussion and interactions that followed the celebrated unveiling event,

entrepreneurs and stakeholders voiced their concerns and reservations about the policy. While

some pointed out that in the absence of guidelines, a lot of this may remain on paper, others said

that the allocations made therein were “all too paltry”.

For instance, the fund of Rs. 1 crore that has been allotted under the head of “promoting IP

creation”, industry members pointed out, is “all too nominal”. Industry sources point out that on

an average, a typical 90-minute film takes four to five years to create, and an investment of

around Rs. 10 crore.

‘Lack of funds'

Ankur Bhasin, secretary of ABAI, agrees that the biggest issue facing the industry is paucity of

funds. The current situation in the industry, he describes as a “chicken-and-egg” condition,

where the predominant issue is the poor quality of IP being generated. “Now, the reason for this

is the lack of funds for creating IP. So the quality does not meet international standards, and so

naturally, the work does not distribute well,” he explains. This, he emphasises, can only be

solved if some sort of Government support, in terms of tax breaks or even seed funds, is

provided.

33

Mr. Bhasin explains that unlike other industries, creating content takes longer, sometimes up to

five years. “During this period, it is important that a production house or company be able to

sustain. Only if this initial part is taken care of can companies or entrepreneurs even think of

working on original content,” he says.

More critical interventions by the Government, he adds, would be in sectors such as power,

where animation companies (that operate large data centres and high-end computing units) have

been demanding a shift in tariff patterns from industrial to commercial. Entrepreneurs feel that

the policy should be more focussed on issues that are specific to this industry.

A key commitment by the Government is to promote public and private parks on the SEZ model