market feasibility study: mbabane value centre, swaziland april 2007 feasibility study: demographics...

TRANSCRIPT

Market Feasibility Study:Mbabane Value Centre,

Swaziland

April 2007

Feasibility Study:Demographics & Retail Potential

Note: This project should be regarded as confidential as it contains Data, Information and Intellectual Property of Fernridge Consulting- Copyright (Limited Distribution)Copyright 2007: Fernridge Consulting.

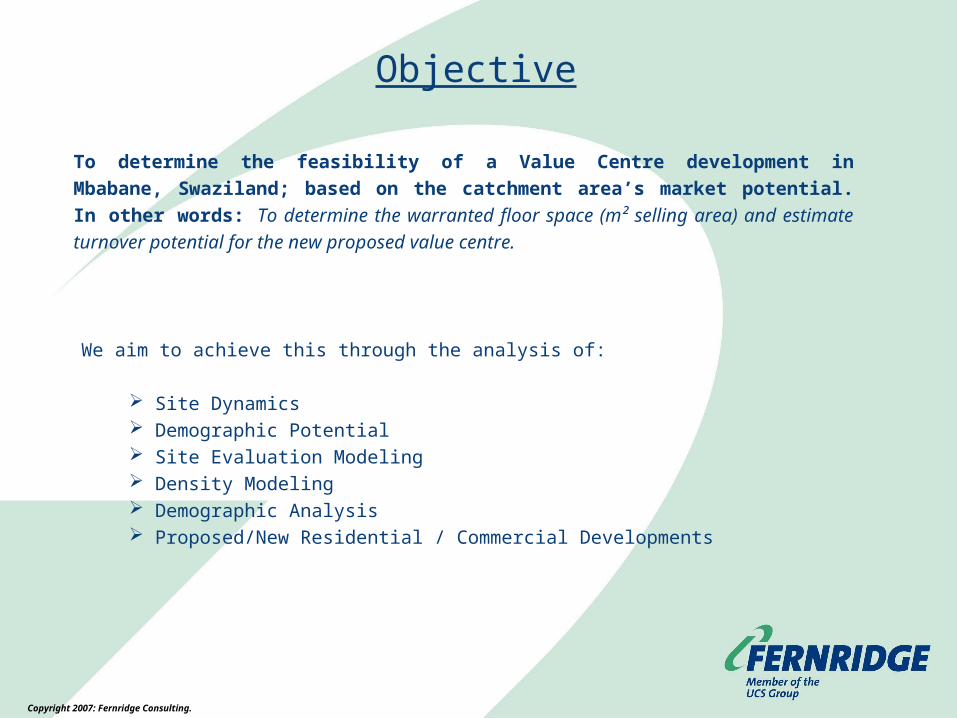

Objective

To determine the feasibility of a Value Centre development in Mbabane, Swaziland; based on the catchment area’s market potential. In other words: To determine the warranted floor space (m² selling area) and estimate turnover potential for the new proposed value centre.

We aim to achieve this through the analysis of:

Site Dynamics Demographic Potential Site Evaluation Modeling Density Modeling Demographic Analysis Proposed/New Residential / Commercial Developments

Copyright 2007: Fernridge Consulting.

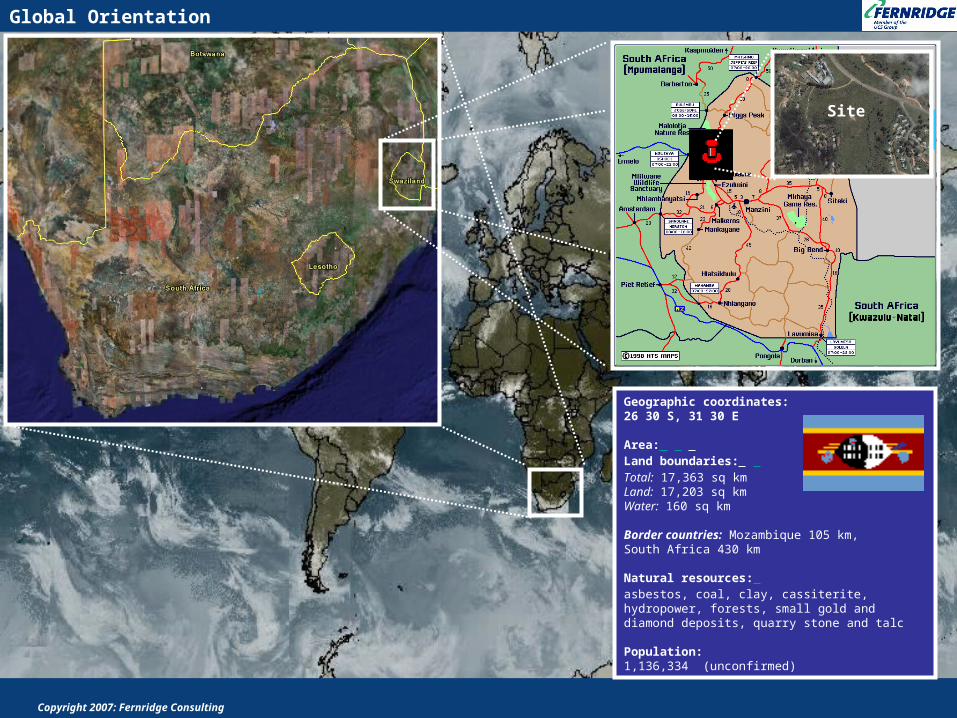

Global Orientation

Copyright 2007: Fernridge Consulting

Geographic coordinates:26 30 S, 31 30 E

Area: Land boundaries: Total: 17,363 sq km Land: 17,203 sq km Water: 160 sq km

Border countries: Mozambique 105 km, South Africa 430 km

Natural resources: asbestos, coal, clay, cassiterite,hydropower, forests, small gold and diamond deposits, quarry stone and talc

Population: 1,136,334 (unconfirmed)

Site

Copyright 2007: Fernridge Consulting

Fast Facts

Copyright 2007: Fernridge Consulting

Copyright 2005: Fernridge Consulting.Swaziland Overview

Copyright 2007: Fernridge Consulting

Mbabane

ManziniSiteki

Big Bend

Pigs Peak

Nhlangano

Swaziland main places…

The Site

Mbabane Overview

Copyright 2007: Fernridge Consulting

Mahwalala

Mangwaneni

Msunduza

CorporationHighlands View

P.T.S.

MalungeKentRock

MbabaneTownship

SelectionPark

Sandla

Manzana

SidwashiniSouth

WaterfordPark

SidwashiniNorth

NewThembelihle

Mbangweni Thembelihle

Woodlands

Eveni

Dalriach East

GolfCourse

WestridgePark

Nkwalini

MbabaneClinic

NewCheckers

Pine Valley

Fonteyn

CBD

GovernmentOffices Hub

IndustrialArea

IndustrialArea

To

Man

zin

i

To

Mh

lam

ban

yats

i

To Oshoek

Mhla

mban

yats

i Rd.

MR3

Mbabane •Mbabane is the capital of the Hhohho Region and seen as the capital of Swaziland.• Mbabane is home to the Central Governmental Offices of Swaziland. These offices are located at the Government Office Hub.• The CBD is the central node of activity in Mbabane where most of the retail and services are found.• The industrial areas have a range of retailers such as motoring and building materials. Other activities include warehousing, light industrial and manufacturing.• The proposed site is located just outside the CBD area of Mbabane.

Rand / m² selling per year

Main Category Total Exp / month Total Exp / year Ave Trading Density Area Potential GLA

R 36,390,179 R 436,682,146 R 30,000 18,195

R 17,181,920 R 206,183,039 R 18,000 14,318

R 7,137,787 R 85,653,443 R 24,000 4,461

R 8,024,240 R 96,290,883 R 20,000 6,018

R 9,943,655 R 119,323,860 R 11,000 13,560

R 5,280,622 R 63,367,467 R 7,500 10,561

R 4,802,261 R 57,627,130 R 13,000 5,541

R 5,522,121 R 66,265,454 R 23,000 3,601

R 7,417,332 R 89,007,982 R 12,000 9,272

R 2,556,772 R 30,681,261 R 5,500 6,973

Total Potential R 104,256,889 R 1,251,082,664 R 16,400 92,501

Area warranted GLA

Main Category Centre Capture Rate Warranted Centre GLA Monthly Centre Turnover

20% 3,639 R 7,278,036

35% 5,011 R 6,013,672

30% 1,338 R 2,141,336

35% 2,106 R 2,808,484

35% 4,746 R 3,480,279

25% 2,640 R 1,320,156

30% 1,662 R 1,440,678

35% 1,260 R 1,932,742

35% 3,245 R 2,596,066

30% 2,092 R 767,032

@ Capture rate 27,741 R 29,778,481

Food & Groceries

*CFTA

Speciality

Home

Furniture & Appliances

Services

Outdoor

Wine & Dine

Hardware / DIY

Entertainment

Food & Groceries

*CFTA

Speciality

Home

Furniture & Appliances

Entertainment

Services

Outdoor

Wine & Dine

Hardware / DIY

Copyright 2006: Fernridge Consulting.

Full Retail Potential Estimate (RPE)

The RPE Model estimate that currently a Centre of 28,000 m² GLA to 30,000 m² GLA including 15% inflow will be feasible at the site. The model does not take into account motoring such as Kwik-Fit, Supa Quick, etc. which could be free standers on the Centre premises. The Centre potential will increase if the current growth rate persists. The total feasible Centre size projected for 2010 is an estimated ± 32,000 m² GLA (excluding motoring).

Add 25% to selling area to calculate GLA.

A++ 8A+ 16A 236B 1,382C 3,594D 4,785DL 25,338Total 35,358

2007 Demographics CATCHMENT AREA

15% inflow included

Copyright 2007: Fernridge Consulting

Copyright 2006: Fernridge Consulting.

Site:• The proposed site for the Value Centre is well located in relation to the new Freeway bypass that is under construction.• The site will have good visibility from both main roads north and south of the site and provision for off - ramps from the new bypass will allow access to the site.• Mbabane CBD is an uncomplicated ± 2km drive from the site. High traffic volumes are expected to pass the site on both the passing main roads.• The development will however have to make provision for public transport facilities as there are no other formal transport ranks in close proximity to the site.• The site location in macro context of Mbabane is good, as the development could capture the passing trade and has the potential to get good support from the residents of Mbabane and surrounding rural areas.• Mbabane CBD has a strong retail offer, with Superspar at the The Mall Centre performing exceptionally well. The proposed development will also feed from the same market and thus some element of competition will exist. The development location is however more convenient by being out of the busy CBD which is a psychological barrier.• The City Council has set out land for commercial use along the new bypass road. Once these areas start to develop, synergy will be established with the proposed Centre.• The site rates 74% in the Fernridge Site Evaluation Model, thus good.

Developments:• The new MR3 bypass will bypass the Mbabane CBD and according to City Planning the CBD are made more attractive and inviting to passing travelers in order to retain the current high inflow into the CBD area where the retail and services infrastructure are well developed.• Developer confidence in Mbabane is high and it is evident by observing the number of office developments that are currently under construction within the CBD, including additional retail and office space at the Swazi Plaza.• Residential developments are taking place in mostly all residential suburbs of Mbabane as there are still many open stands available for development. The developments are mainly single residential stands developed by private buyers with limited cluster type developments. The developments are evenly spread over the income group ranges.• Industrial and manufacturing plant developments are limited in Mbabane due to the uneven topography of the area.

Executive Summary

Copyright 2007: Fernridge Consulting

Copyright 2006: Fernridge Consulting.

Demographics:• The Mbabane urban area has a good mix of upper and lower income residents with a 30:70 split. Mbabane has a large presence of white collar workers due to the presence of the Central Governmental Offices and a number of businesses in the area as opposed to Manzini and Matsapha with a much larger blue collar workforce due to the prominent manufacturing and industrial sector present in that area. The surrounding rural areas are mainly lower income (D Low income) households with a high level of subsistence farming.• Mbabane urban area has a projected growth rate of ± 3.5% per annum. The rural areas surrounding Mbabane has a slightly lower growth rate of 3.4% per annum (Swaziland Central Statistics and City Planning Department 2007). The national growth rate has slowed down due to the impact of HIV Aids, especially within the more rural areas where medical care is limited.• The topography of the area creates many physical and psychological barriers and thus complicates the development of Convenience Centres or Community Centres. The residential suburbs are highly fragmented.• The Mbabane residential suburbs also does not necessarily have a set income profile, most of the suburbs have mixed income groups residing in the area. • A retail centre with a strong offer will be needed to overcome the topographical factor and mixed income profiles of the residential suburbs. Also a centre servicing a dual market will be essential to optimise Centre performance or even justify the development of a larger format retail facility such as a Value Centre.

Mbabane Retail:• Mbabane has two prominent retail centres located within the CBD, Swazi Plaza (Shoprite Anchor and secondary anchor Woolworths Food) and The Mall (Superspar anchor).• The CBD has currently the only substantial retail offer within Mbabane. The other nearest offer is The Gables (Pick ‘n Pay Family anchor) and the proposed Regional Centre both located within the Ezulwini area. Development details on the proposed Regional Mall is still vague, but it seems like the development will eventually get off the ground. We have considered these two retail Centres when the catchment area was delineated. Residents from the southern suburbs of Mbabane would possibly flow out to an extend to these Centres, but with a unique Value Centre offer the outflow is not expected to be as substantial.• The Mbabane retail infrastructure is currently still very much similar to South African towns where the CBD is the only shopping destination for the town. The Value Centre concept outside the CBD will be a pioneer retail development of its type, but is expected to be well received by the Mbabane market as it will be an alternative retail experience to the currently highly congested and busy Mbabane CBD.

Executive Summary

Copyright 2007: Fernridge Consulting

Copyright 2006: Fernridge Consulting.

Conclusion:

• The RPE model estimates a current feasible Value Centre at the site with a total GLA of between 28,000m² and 30,000m² (excluding motoring which could be freestanding outlets on the Centre premises).• 15% inflow has been added to the model as the site has good potential to intercept passing traffic coming from outside the catchment area.• Assuming the development rate continues on a steady rate the total potential for the development will increase to ± 32,000m² GLA by 2010.• The development will have to service a dual market, thus provide sufficient public transport facilities at the Centre.• A strong and relevant tenant mix at the Value Centre will be necessary to attract upper and lower income residents from the total catchment area and to make the trip to the Centre worthwhile. Furthermore, the Centre should have a unique offer to intercept passing traffic.• The tenant mix at Value Centres have a strong presence of stores which are destination stores such as Furniture, Hi-Fi Corporation, Mr. Price Home (other home stores), etc.• The Centre will have an added advantage if brands that are currently not represented in Swaziland, but only South Africa are introduced at the Centre.• The development could be feasible if the abovementioned guidelines are followed.

Executive Summary

Copyright 2007: Fernridge Consulting

Sybrand Strauss (Director)Fernridge Consulting PTY LTDSouth Africa

Tel: 011 712 1720Fax: 011 339 1833Cell: 082 330 5168e-mail: [email protected]

Andre Annandale (Business Analyst)Fernridge Consulting PTY LTDSouth Africa

Tel: 011 712 1714Fax: 011 339 1833Cell: 082 776 6353e-mail: [email protected]

Contact Details

Copyright 2007: Fernridge Consulting