market opportunities for lignocellulose derived chemicals: the bio base nwe project

TRANSCRIPT

NNFCC

NNFCC: The Bioeconomy Consultants

Market opportunities for

lignocellulose-derived chemicals The Bio Base NWE Project

UK-Norway Symposium: Valorising Woody Biomass

Adrian Higson PhD

25 June 2012

NNFCC

NNFCC: The Bioeconomy Consultants

Company Vision

We view bio-based technologies as key

components of the low carbon economy

delivering economic, social and environmental

benefits.

We believe the bioeconomy will create

sustainable business opportunities for

feedstock suppliers, technology and project

developers, manufacturers and investors.

A specialist ‘not for profit’ Bioeconomy consultancy

Company Mission

To provide clients with a holistic view of feedstock, technology, policy and market

development across the bioeconomy, enabling them to make informed business

decisions and develop sustainable business strategies.

NNFCC

NNFCC: The Bioeconomy Consultants

Services

• Future market analysis

• Feedstock logistics planning

• Sustainability strategy development

• Technology evaluation and due diligence

• Project feasibility assessment

• Policy and regulatory support

• Network & Facilitation

Clients & Partners

• Multinationals & SMEs

• Public Organisations

• Government

• Research Institutes

• Universities

• Transnational Collaborations

• European Framework Projects

Celebrating 10 years of Bioeconomy development

NNFCC

NNFCC: The Bioeconomy Consultants

EU Context

It includes agriculture, forestry, fisheries, food and pulp and paper production,

as well as parts of chemical, biotechnological and energy industries.

• is worth an estimated €2 trillion

• accounts for 22 million jobs

• 9% of total employment in the EU

Each euro invested in EU-funded bioeconomy research and innovation is

estimated to trigger €10 of value added in bioeconomy sectors by 2025.

EUROPEAN COMMISSION – PRESS RELEASE

Brussels, 13 February 2012

Commission proposes strategy for sustainable

bioeconomy in Europe

NNFCC

NNFCC: The Bioeconomy Consultants

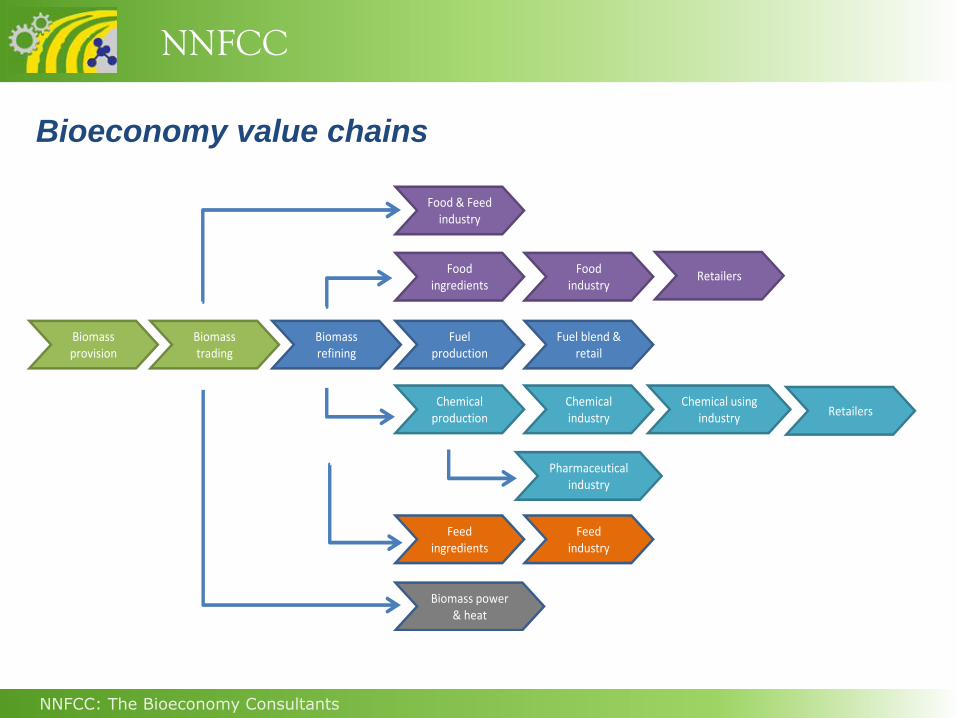

Bioeconomy value chains

Biomassprovision

Biomass trading

Biomassrefining

Fuel production

Fuel blend & retail

Chemical production

Chemicalindustry

Biomass power& heat

Chemical usingindustry

Retailers

Pharmaceutical industry

Food ingredients

Food industry

Retailers

Food & Feed industry

Feed ingredients

Feed industry

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

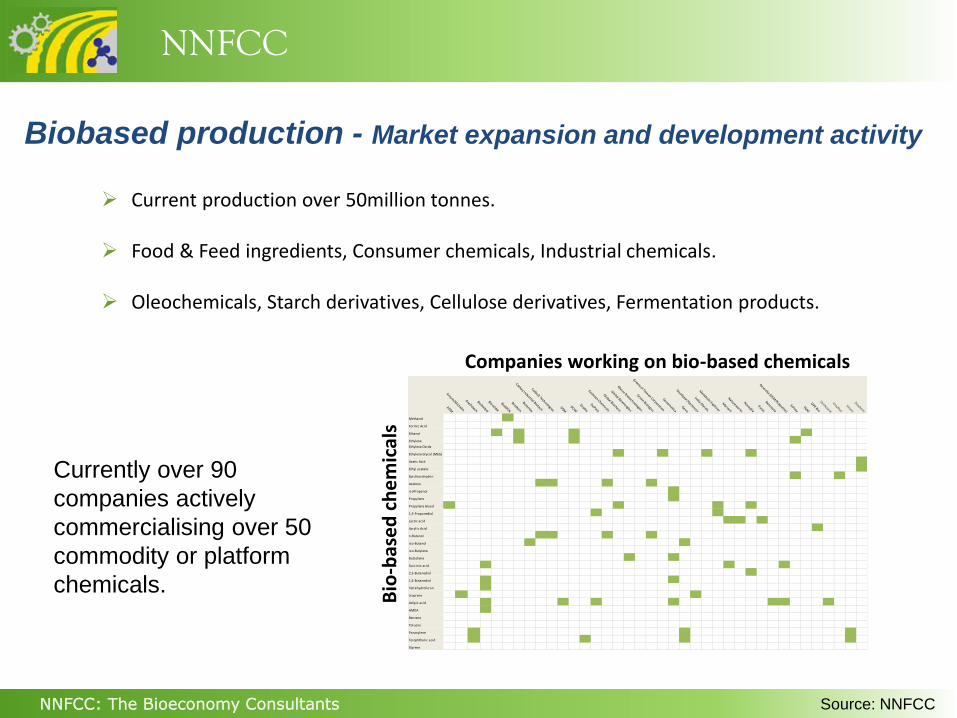

Biobased production - Market expansion and development activity

Currently over 90

companies actively

commercialising over 50

commodity or platform

chemicals.

ADM

Amyris/M

ichelin

Anellotech

BioAmber

Biocaldol

BioMCN

Braskem

Butamax

Cathay Industrial Biotech

Colbolt TechnologiesDSM

DOW

Draths

DuPont

Eastman Chem

icals

Global Biochem

Global Bioenergies

Glycos Biotechnologies

Green Biologics

Greencol Taiwan Corporation

Genomatica

Gevo

Goodyear/Genencor

India Glycols

Metabolic Explorer

Myriant

Natureworks

Novepha

Purac

Rennovia

Reverdia (DSM/Roquette)

SolvayTM

O

OPX Bio

Verdezyne

Vinythai

Virent

Zeachem

Methanol

Formic Acid

Ethanol

Ethylene

Ethylene Oxide

Ethylene Glycol (MEG)

Acetic Acid

Ethyl acetate

Epichlorohydrin

Acetone

isoPropanol

Propylene

Propylene Glycol

1,3-Propanediol

Lactic acid

Acrylic Acid

n-Butanol

iso-Butanol

iso-Butylene

Butadiene

Succinic acid

2,3-Butanediol

1,4-Butanediol

Tetrahydrofuran

Isoprene

Adipic acid

HMDA

Benzene

Toluene

Paraxylene

Terephthalic acid

Styrene

Companies working on bio-based chemicals

Bio

-bas

ed

ch

em

ical

s

Source: NNFCC

Current production over 50million tonnes.

Food & Feed ingredients, Consumer chemicals, Industrial chemicals.

Oleochemicals, Starch derivatives, Cellulose derivatives, Fermentation products.

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

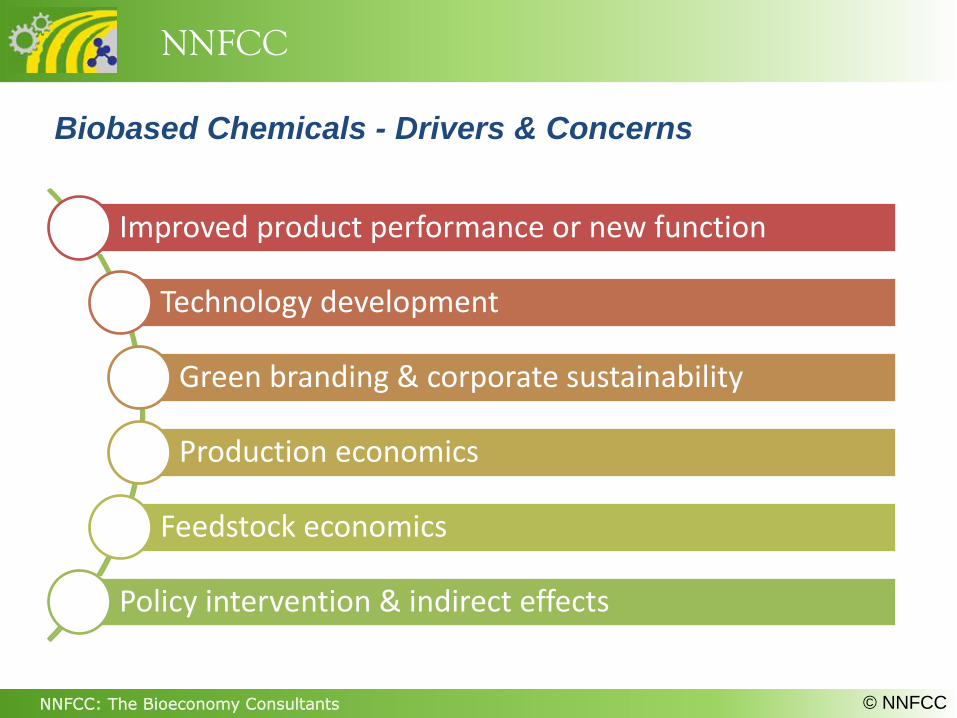

Biobased Chemicals - Drivers & Concerns

Improved product performance or new function

Technology development

Green branding & corporate sustainability

Production economics

Feedstock economics

Policy intervention & indirect effects

© NNFCC

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

0

50

100

150

200

250

300

Feb

-93

De

c-9

3

Oct

-94

Au

g-9

5

Jun

-96

Ap

r-9

7

Feb

-98

De

c-9

8

Oct

-99

Au

g-0

0

Jun

-01

Ap

r-0

2

Feb

-03

De

c-0

3

Oct

-04

Au

g-0

5

Jun

-06

Ap

r-0

7

Feb

-08

De

c-0

8

Oct

-09

Au

g-1

0

Jun

-11

Ap

r-1

2

Feb

-13

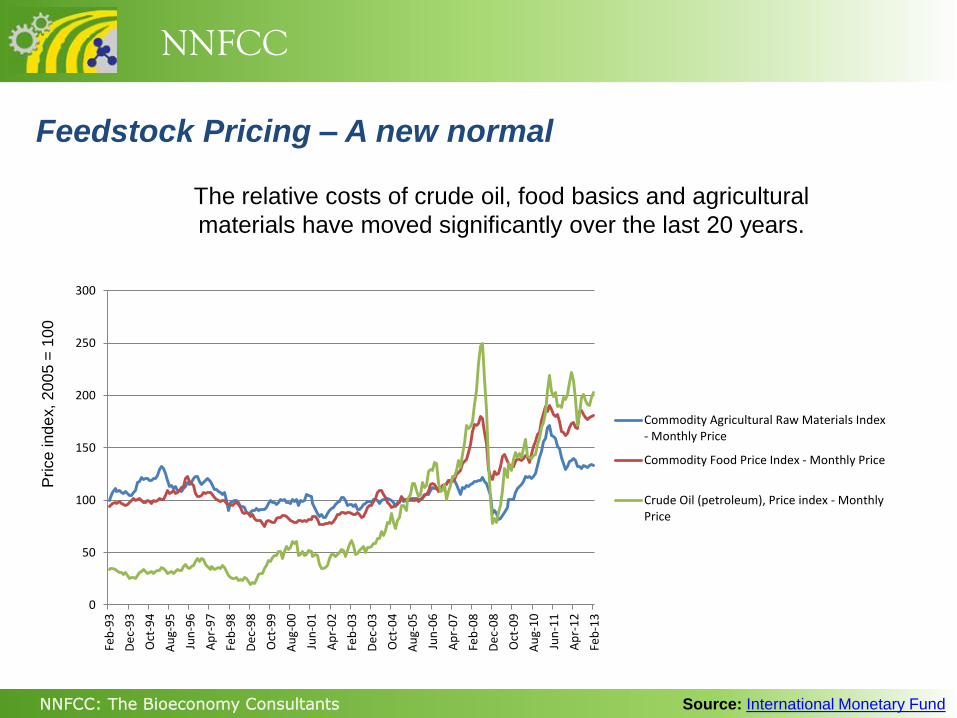

Commodity Agricultural Raw Materials Index- Monthly Price

Commodity Food Price Index - Monthly Price

Crude Oil (petroleum), Price index - MonthlyPrice

Feedstock Pricing – A new normal

Source: International Monetary Fund

Price

ind

ex, 2

00

5 =

10

0

The relative costs of crude oil, food basics and agricultural

materials have moved significantly over the last 20 years.

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

50 shades of green - Every generation now comes with a degree of

environmental consciousness

• Baby boomers (born 1946-1964)

– Silent Spring 1962

– Air quality, water quality

• Generation X (Baby busters) (born 1964-1977)

– Union Carbide and Chernobyl disasters.

– Exxon Valdez oil spill.

• Generation Y (Millennials) (born 1980’s through1990’s)

– Hurricane Katrina and An Inconvenient Truth

– BP Oil Spill in the Gulf of Mexico

– Awareness of the Great Pacific Garbage Patch

• Generation Z (today’s children)

– Recycling, solar panels, hybrid cars, energy saving light bulbs

Source: Jacquelyn Ottman: The new rules of Green Marketing

NNFCC

NNFCC: The Bioeconomy Consultants

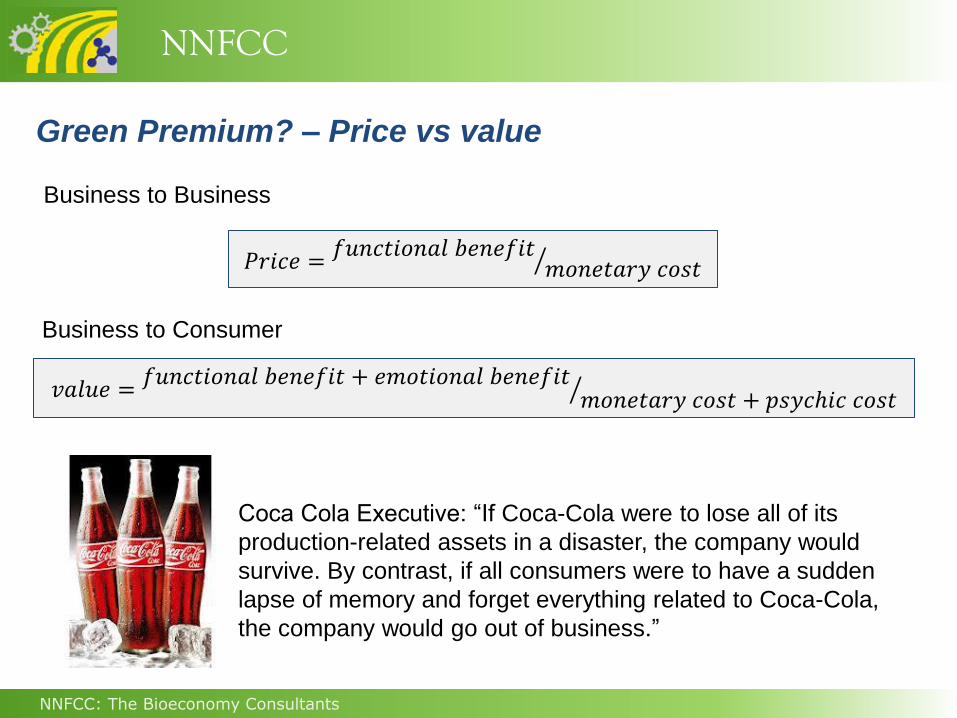

𝑃𝑟𝑖𝑐𝑒 =𝑓𝑢𝑛𝑐𝑡𝑖𝑜𝑛𝑎𝑙 𝑏𝑒𝑛𝑒𝑓𝑖𝑡

𝑚𝑜𝑛𝑒𝑡𝑎𝑟𝑦 𝑐𝑜𝑠𝑡

𝑣𝑎𝑙𝑢𝑒 =𝑓𝑢𝑛𝑐𝑡𝑖𝑜𝑛𝑎𝑙 𝑏𝑒𝑛𝑒𝑓𝑖𝑡 + 𝑒𝑚𝑜𝑡𝑖𝑜𝑛𝑎𝑙 𝑏𝑒𝑛𝑒𝑓𝑖𝑡

𝑚𝑜𝑛𝑒𝑡𝑎𝑟𝑦 𝑐𝑜𝑠𝑡 + 𝑝𝑠𝑦𝑐ℎ𝑖𝑐 𝑐𝑜𝑠𝑡

Business to Business

Business to Consumer

Green Premium? – Price vs value

Coca Cola Executive: “If Coca-Cola were to lose all of its

production-related assets in a disaster, the company would

survive. By contrast, if all consumers were to have a sudden

lapse of memory and forget everything related to Coca-Cola,

the company would go out of business.”

NNFCC

NNFCC: The Bioeconomy Consultants

0

400

800

1200

1600

2000

2010 2020 2030 2040 2050

Mill

ion

to

nn

es

Plastics production: projected growth

Medium

Low

High

Plastic production: medium growth

2020 339 million tonnes

2030 434 million tonnes

2050 712 million tonnes

A high value market for lignocellulose? 1967 – There’s a great future in plastics 2012 - There’s a great future in bio-based plastics

The Graduate (1967),

© NNFCC

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

Ethylene Polyethylenes

Styrene Monomer

Ethylene Oxide/Glycol

EDC

Other

Polymers/Rubbers

Polyester

PVC

Alpha Olefins

PVA

Ethanol

60%

7%

14%

12%

7%

Ethylene value chain

PET Collaborative

NNFCC

NNFCC: The Bioeconomy Consultants

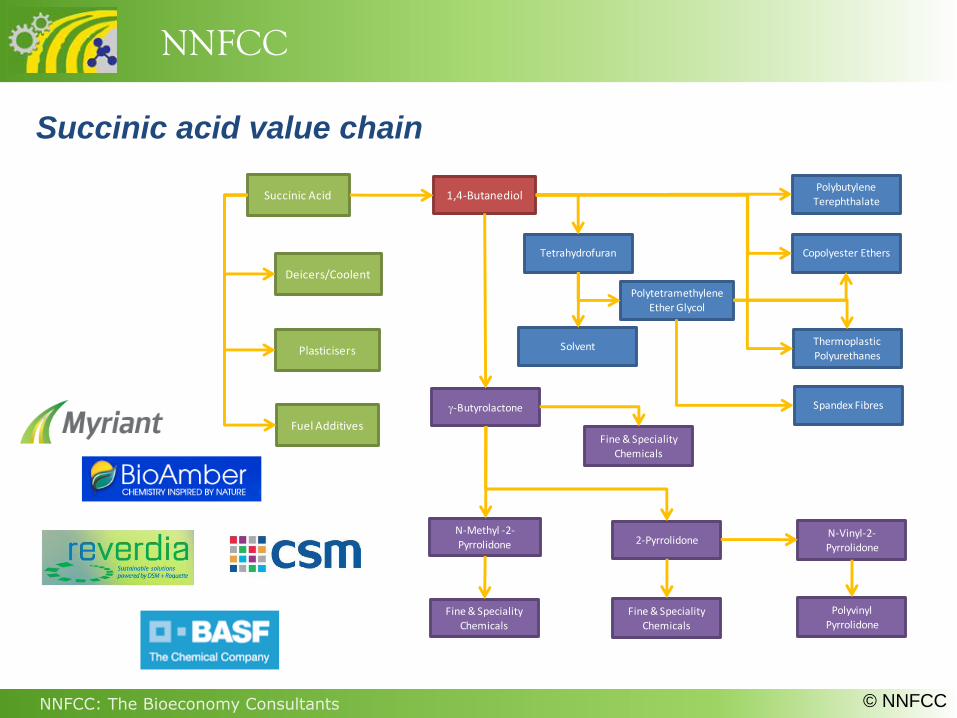

Succinic Acid 1,4-ButanediolPolybutylene

Terephthalate

Copolyester Ethers

Thermoplastic Polyurethanes

Spandex Fibres

Tetrahydrofuran

Solvent

Polytetramethylene Ether Glycol

g-Butyrolactone

Fine & Speciality Chemicals

N-Methyl -2-Pyrrolidone

Fine & Speciality Chemicals

2-Pyrrolidone

Fine & Speciality Chemicals

N-Vinyl-2-Pyrrolidone

Polyvinyl Pyrrolidone

Deicers/Coolent

Plasticisers

Fuel Additives

Succinic acid value chain

© NNFCC

NNFCC

NNFCC: The Bioeconomy Consultants

Cellulosic ethanol – No longer 10 years away

ST. LOUIS, MO. (June 11, 2013) – Construction of POET-

DSM Advanced Biofuels’ first commercial cellulosic bio-

ethanol plant is on schedule to start up in early 2014 ….

Beta Renewables Crescentino plant commercial-scale

cellulosic ethanol plant, in Crescentino Italy, started

operations in Q4, 2012.

With construction completed in 2012, KiOR commenced

operations at Columbus and validated its proprietary

technology. Shipments of cellulosic fuels from Columbus

began in early 2013

NNFCC

NNFCC: The Bioeconomy Consultants

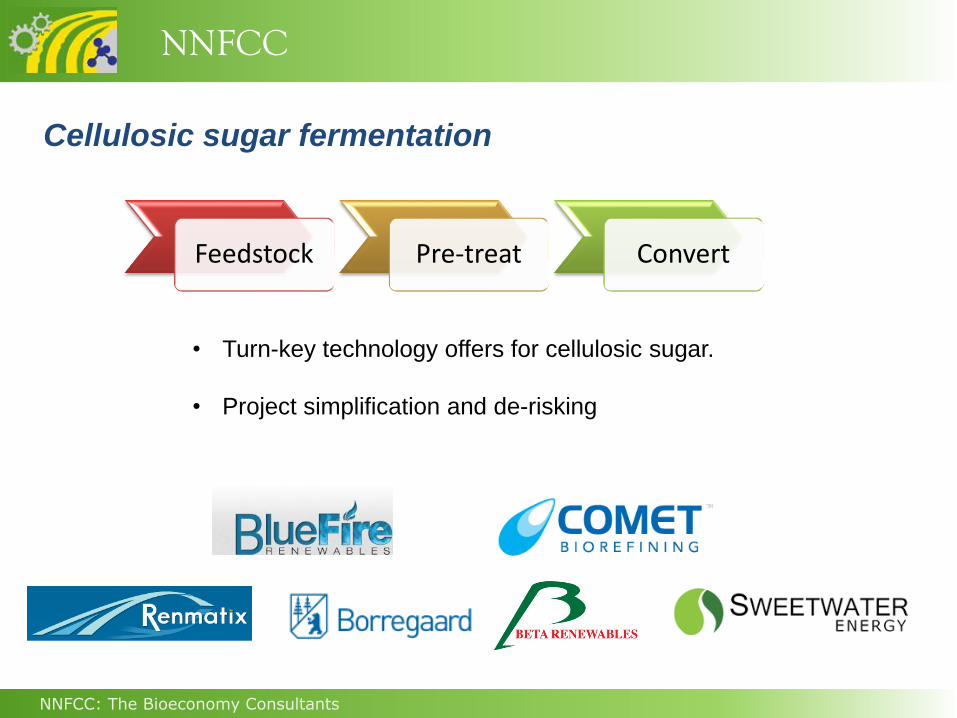

Cellulosic sugar fermentation

• Turn-key technology offers for cellulosic sugar.

• Project simplification and de-risking

Feedstock Pre-treat Convert

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

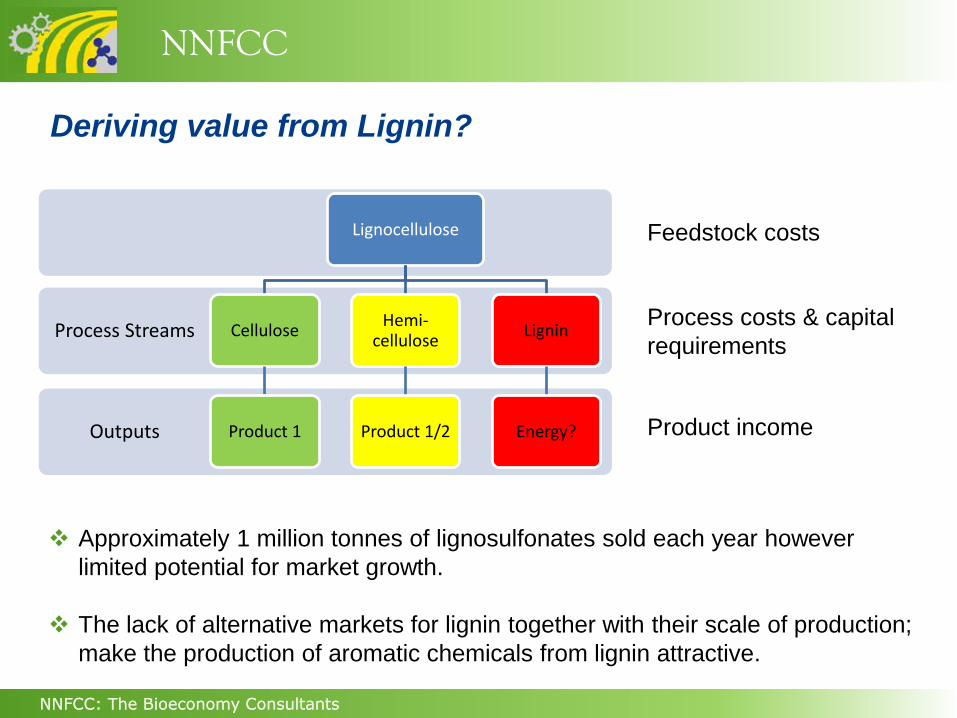

Outputs

Process Streams

Lignocellulose

Cellulose

Product 1

Hemi-cellulose

Product 1/2

Lignin

Energy?

Deriving value from Lignin?

Approximately 1 million tonnes of lignosulfonates sold each year however

limited potential for market growth.

The lack of alternative markets for lignin together with their scale of production;

make the production of aromatic chemicals from lignin attractive.

Process costs & capital

requirements

Feedstock costs

Product income

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

Bulk aromatics (BTX value chain)

Benzene

(~40 million tonnes/year)

Ethylbenzene (52%)

Cumene

(22%)

Phenol

(~9 million tonnes/year)

Bisphenol A (44%)

Polycarbonate resins

Epoxy resins

Phenolic resins (27%)

Caprolactam

Nylon 6

Cyclohexane (15%)

Other

(11%)

Toluene Xylene

Added value

targets

NNFCC

NNFCC: The Bioeconomy Consultants

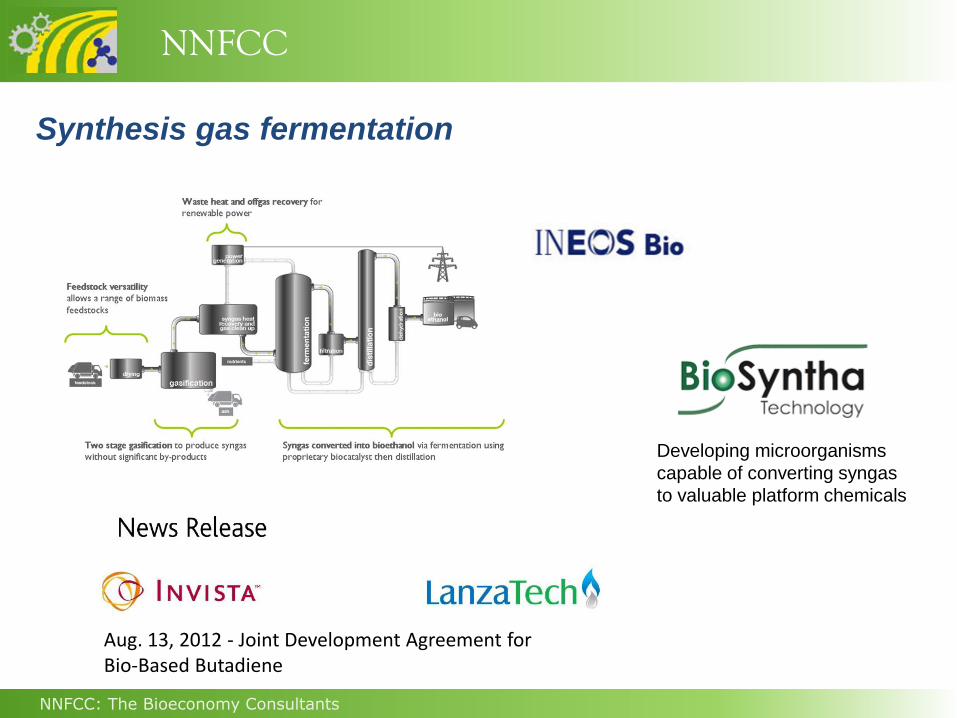

Aug. 13, 2012 - Joint Development Agreement for Bio-Based Butadiene

Synthesis gas fermentation

Developing microorganisms

capable of converting syngas

to valuable platform chemicals

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

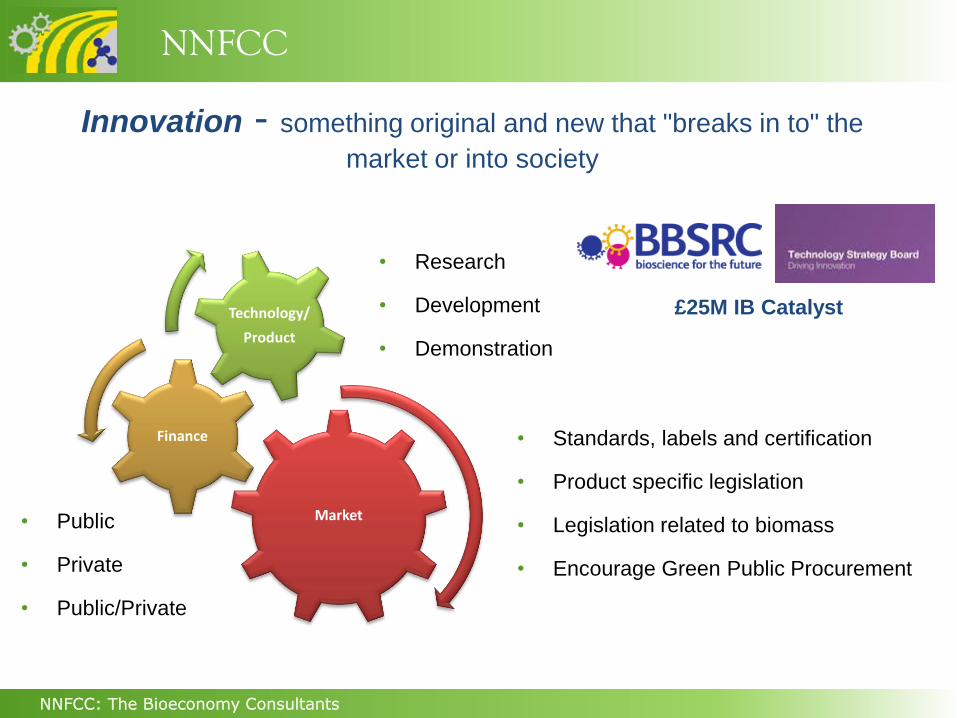

Innovation - something original and new that "breaks in to" the

market or into society

Market

Finance

Technology/

Product

• Standards, labels and certification

• Product specific legislation

• Legislation related to biomass

• Encourage Green Public Procurement

• Research

• Development

• Demonstration

• Public

• Private

• Public/Private

£25M IB Catalyst

NNFCC

NNFCC: The Bioeconomy Consultants

BRIDGE PPP: The challenge, Overcoming the innovation Valley of

Death by bridging the gap from research to the marketplace.

The EU contributes €1 billion to the research and innovation program,

European industries have committed to another €2.8 billion

Building supply chains

Developing technology

Upgrading and building

demonstration and flagship

biorefineries

http://bridge2020.eu/

NNFCC

NNFCC: The Bioeconomy Consultants

Process scale up and pilot demonstration

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

Bio Base NWE Supporting the development of the bio-based economy

in North West Europe

• To aid companies, research centers and education centers of NWE to

network internationally

• Political support for the bio-based economy by giving SMEs a voice, and by

developing a common strategy

• To acquaint companies, research centers and education centers of NWE with

Bio Base Europe

NNFCC

NNFCC: The Bioeconomy Consultants NNFCC: The Bioeconomy Consultants

Bio Base NWE Supporting the development of the bio-based economy

in North West Europe

NNFCC

NNFCC: The Bioeconomy Consultants

Bio economy

Feedstock pricing & volatility

Technology

Development

(performance & cost)

Environmental considerations

Summary Biobased Economy Drivers

Process development

drivers are multiple and

varied.

Commercialisation led by

brand owner pressure on

supply chains.

Identifying ‘added value’

markets important for first

movers.

Increasing public funding

and market development

support.

NNFCC

NNFCC: The Bioeconomy Consultants

The NNFCC provides high quality, industry leading consultancy

for more information contact us

Email - [email protected]

+44 (0) 1904 435182

Follow us on Twitter @NNFCC

• Future Market Analysis

• Feedstock Logistics Planning

• Sustainability Strategy

Development

• Technology evaluation & associated

due diligence

• Project feasibility assessment

• Policy and regulatory support