market outlook 12th august 2011

TRANSCRIPT

8/6/2019 Market Outlook 12th August 2011

http://slidepdf.com/reader/full/market-outlook-12th-august-2011 1/6

1

Market OutlookIndia Research August 12, 2011

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

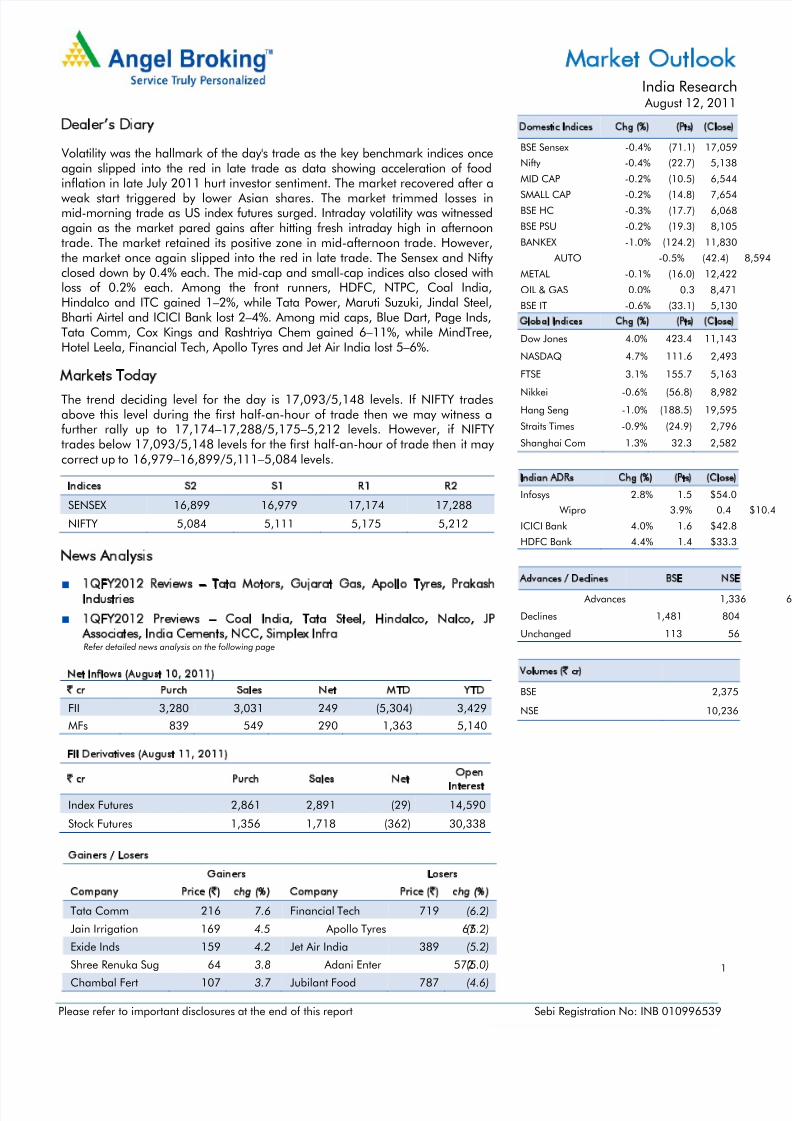

Dealer’s Diary

Volatility was the hallmark of the day's trade as the key benchmark indices onceagain slipped into the red in late trade as data showing acceleration of food

inflation in late July 2011 hurt investor sentiment. The market recovered after aweak start triggered by lower Asian shares. The market trimmed losses inmid-morning trade as US index futures surged. Intraday volatility was witnessedagain as the market pared gains after hitting fresh intraday high in afternoontrade. The market retained its positive zone in mid-afternoon trade. However,the market once again slipped into the red in late trade. The Sensex and Nifty closed down by 0.4% each. The mid-cap and small-cap indices also closed withloss of 0.2% each. Among the front runners, HDFC, NTPC, Coal India,Hindalco and ITC gained 1–2%, while Tata Power, Maruti Suzuki, Jindal Steel,Bharti Airtel and ICICI Bank lost 2–4%. Among mid caps, Blue Dart, Page Inds,Tata Comm, Cox Kings and Rashtriya Chem gained 6–11%, while MindTree,Hotel Leela, Financial Tech, Apollo Tyres and Jet Air India lost 5–6%.

Markets Today

The trend deciding level for the day is 17,093/5,148 levels. If NIFTY tradesabove this level during the first half-an-hour of trade then we may witness afurther rally up to 17,174–17,288/5,175–5,212 levels. However, if NIFTYtrades below 17,093/5,148 levels for the first half-an-hour of trade then it may correct up to 16,979–16,899/5,111–5,084 levels.

Indices S2 S1 R1 R2

SENSEX 16,899 16,979 17,174 17,288

NIFTY 5,084 5,111 5,175 5,212

News Analysis

1QFY2012 Reviews – Tata Motors, Gujarat Gas, Apollo Tyres, PrakashIndustries

1QFY2012 Previews – Coal India, Tata Steel, Hindalco, Nalco, JPAssociates, India Cements, NCC, Simplex InfraRefer detailed news analysis on the following page

Net Inflows (August 10, 2011)

` cr Purch Sales Net MTD YTD

FII 3,280 3,031 249 (5,304) 3,429

MFs 839 549 290 1,363 5,140

FII Derivatives (August 11, 2011)

` cr Purch Sales NetOpen

Interest

Index Futures 2,861 2,891 (29) 14,590

Stock Futures 1,356 1,718 (362) 30,338

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

Tata Comm 216 7.6 Financial Tech 719 (6.2)

Jain Irrigation 169 4.5 Apollo Tyres 67(5.2)

Exide Inds 159 4.2 Jet Air India 389 (5.2)

Shree Renuka Sug 64 3.8 Adani Enter 572(5.0)

Chambal Fert 107 3.7 Jubilant Food 787 (4.6)

Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex -0.4% (71.1) 17,059

Nifty -0.4% (22.7) 5,138

MID CAP -0.2% (10.5) 6,544

SMALL CAP -0.2% (14.8) 7,654

BSE HC -0.3% (17.7) 6,068

BSE PSU -0.2% (19.3) 8,105

BANKEX -1.0% (124.2) 11,830

AUTO -0.5% (42.4) 8,594

METAL -0.1% (16.0) 12,422

OIL & GAS 0.0% 0.3 8,471

BSE IT -0.6% (33.1) 5,130

Global Indices Chg (%) (Pts) (Close)

Dow Jones 4.0% 423.4 11,143

NASDAQ 4.7% 111.6 2,493

FTSE 3.1% 155.7 5,163

Nikkei -0.6% (56.8) 8,982

Hang Seng -1.0% (188.5) 19,595

Straits Times -0.9% (24.9) 2,796

Shanghai Com 1.3% 32.3 2,582

Indian ADRs Chg (%) (Pts) (Close)

Infosys 2.8% 1.5 $54.0

Wipro 3.9% 0.4 $10

ICICI Bank 4.0% 1.6 $42.8

HDFC Bank 4.4% 1.4 $33.3

Advances / Declines BSE NSE

Advances 1,336

Declines 1,481 804

Unchanged 113 56

Volumes (` cr)

BSE 2,375

NSE 10,236

8/6/2019 Market Outlook 12th August 2011

http://slidepdf.com/reader/full/market-outlook-12th-august-2011 2/6

August 12, 2011 2

Market Outlook | India Research

1QFY2012 Result Reviews

Tata Motors

Tata Motors (TML) recorded lower-than-expected bottom-line performance for 1QFY2012,largely on account of cost pressures and higher tax rate at Jaguar and Land Rover (JLR).On the consolidated front, top line registered in-line 24.1% yoy growth (down 5.7% qoq) to ` 33,572cr, aided largely by 19.9% yoy growth in JLR revenue. JLR’s performance was ledby an 8.6% yoy increase in volumes and a 10.4% yoy increase in net average realisation.Operating margin declined by 163bp yoy (flat qoq) to 12.6%, broadly in-line with ourestimates of 12.5%. Margin contraction can be attributed mainly to raw-material costpressures, which increased by 226bp yoy during the quarter. Net profit stood at ` 2,000crvs. our estimate of ` 2,226cr, reporting flat yoy growth; however, it declined significantly by 24.2% on a sequential basis. Higher interest cost on account of bond issuance in May 2011 and high tax rate due to China operations negatively impacted the bottom-lineperformance.

On a standalone basis, TML reported 14.2% yoy (down 18.5% qoq) growth in its top line

to ` 11,898cr, aided by 8.7% yoy (down 16.4% qoq) growth in volumes and 10.1% growthin realisation, led by price increases. Operating margin declined substantially by 297bpyoy (down 41bp qoq) to 8.1% due to higher input cost pressures and increased levels ofhigher other expenditure. As a result, net profit increased marginally by 1.4% yoy (down30% qoq) to ` 401cr.

AT ` 846, TML is trading at 5.3x and 4.8x FY2012E and FY2013E earnings. We shallrevise our estimates and release a detailed result note soon. The stock rating is currentlyunder review.

Gujarat Gas

Gujarat Gas reported its 2QCY2011 results. The company’s top line increased by 39.9%yoy to ` 584cr mainly on account of higher realisation, led by the recent price hikes.Natural gas volume sold grew by 1.8% yoy to 302mmscm. Average sales realisation stoodat ` 19.1/scm, (+35.6% yoy and +11.2% qoq), led by hike in selling prices of industrialretail and CNG segments. EBITDA grew by 51.0% yoy to ` 140cr, while EBITDA marginexpanded by 176bp yoy on the back of the recent price hike across segments.Consequently, the company’s net profit grew by 67.1% yoy to ` 97cr. We maintain ourNeutral view on the stock.

Apollo Tyres

Apollo Tyres (Apollo) registered a lower-than-expected performance on the net profit fronton account of continued raw-material cost pressures and higher interest cost, led by commissioning of the Chennai facility. Consolidated revenue posted better-than-expected55% yoy (3.4% qoq) growth to ` 2,822cr, aided by a 34.4% yoy (flat qoq) jump in volumesand a 15.3% yoy (3.4% qoq) increase in average realisation. Domestic and Europerevenue grew by strong 74.9% and 37.9% yoy, respectively, while South Africa witnessed amodest 5.1% yoy increase in revenue. Operating margin declined by 239bp yoy (289bpqoq) to 8.5%, mainly due to the 48.5% (6.5% qoq) and 25% yoy (14% qoq) increase innatural rubber and carbon black prices. As a result, net profit grew marginally by 4% yoy ` 77cr. However, on a sequential basis, net profit declined significantly by 57.8%.Further, a substantial increase in interest cost, which jumped 83.2% yoy, impacted net

profit growth.

At ` 67, the stock is trading at 5x and 4.2x FY2012E and FY2013E earnings, respectively.We retain our Buy rating on the stock; however, the target price is under review. We shallrelease a detailed result note soon.

8/6/2019 Market Outlook 12th August 2011

http://slidepdf.com/reader/full/market-outlook-12th-august-2011 3/6

August 12, 2011 3

Market Outlook | India Research

Prakash Industries

Prakash Industries’ net sales increased by 7.3% yoy to ` 499cr, mainly on account of aincrease in average realisation across product categories. However, EBITDA decreased by 2.3% yoy to ` 91cr. Despite increased realisation, EBITDA margin dipped by 180bp yoy to

18.2% on account of a sharp rise in iron ore and coal costs. On account of lower interestcosts, net profit increased by 2.0% yoy to ` 71cr. The company’s 125MW power expansionhas been delayed again by a quarter to December 2011. We maintain our Buy rating,while we keep our target price under review.

1QFY2012 Result Previews

Coal India

Coal India is slated to report its 1QFY2012 results. We expect net sales to increase by

26.3% yoy to ` 15,078cr mainly on account of higher coal prices. EBITDA margin isexpected to expand by 887bp yoy to 34.3% in 1QFY2012. Net profit is expected toincrease by 56.1% yoy to ` 3,943cr. We maintain our Neutral view on the stock.

Tata Steel

Tata Steel is slated to report its consolidated 1QFY2012 results. We expect net sales toincrease by 27.5% yoy to ` 34,668cr mainly on account of higher steel prices. However,EBITDA margin is expected to contract by 367bp yoy to 12.6% on account of higherraw-material costs (mainly in its European operations). Net profit is expected todecrease by 0.4% yoy to ` 1,858cr. We maintain our Buy rating on the stock with a target

price of `799.

Hindalco

Hindalco is slated to report its standalone 1QFY2012 results. The company had already reported Novelis’ results on August 10, 2011. We expect consolidated net sales to increaseby 17.7% yoy to ` 19,476cr mainly on account of higher aluminium prices. However,EBITDA margin is expected to contract by 136bp yoy to 9.9% on account of rising cost ofkey inputs (primarily coal). Net profit is expected to increase by 7.8% yoy to ` 819cr.We maintain our Buy rating on the stock with a target price of `242.

Nalco

Nalco is slated to report its 1QFY2012 results. We expect net sales to increase by 31.5%yoy to ` 1,698cr mainly on account of higher aluminium prices. However, EBITDA marginis expected to contract by 488bp yoy to 25.6% due to rise in prices of key inputs (primarily coal). Net profit is expected to decrease by 5.6% yoy to ` 268cr. We maintain our Neutralview on the stock.

8/6/2019 Market Outlook 12th August 2011

http://slidepdf.com/reader/full/market-outlook-12th-august-2011 4/6

August 12, 2011 4

Market Outlook | India Research

JP Associates

JP Associates (JAL) is expected to announce its fourth quarter results. We expect JAL to postmodest top-line growth of 11.6% yoy to ` 3,588cr ( ` 3,215cr) for the quarter. We expectmarginal growth of 2.0% in C&EPC revenue to ` 1,466cr. For the cement segment,we expect JAL to post revenue of ` 1,487cr – volume of 4.2mt with realisation of

` 3,622/tonne for the quarter. The real estate sector is expected to continue its robustperformance and post healthy top-line growth of 60% yoy to ` 585.8cr.

Overall, we expect JAL to post EBITDA margin of 24.0%, a jump of 274bp yoy, owing toincreased contribution from the high-margin real estate segment. The bottom line isexpected to come in at ` 199.3cr, registering a yoy jump of 88.4% (adjusting forextraordinary post tax gain of ` 410cr in 1QFY2011) for the quarter.

We have valued JAL’s cement business at 6.5x EV/EBITDA ( ` 67.4/share) and constructiondivision at FY2013E target EV/EBITDA multiple of 6.5x ( ` 32.1/share). We have valued itspower and real estate businesses on market cap basis (giving 15% holding company discount), contributing ` 61.8/share to our target price. The treasury shares ( ` 7.2/share)

have been valued at the current market price, whereas net debt is accounted for on a pershare basis in our valuation at ` 61.8. We maintain our Buy view on the stock with an SOTPtarget price of `108.

India Cements

India Cements is expected to announce its 1QFY2012 results. We expect the top line togrow by 16.5% yoy to ` 1,026cr on account of higher cement realisation. Cement prices,which reached all-time high levels in March 2011, were sustained in the southern regionresulting in strong realisation for the company. OPM is expected to expand by 579bp yoy to 16.1% despite the increase in power and fuel and freight costs on account of the

substantial improvement in realisation. Net profit is expected to grow by 68.6% yoy to ` 42cr. We maintain our Neutral view on the stock.

Nagarjuna Construction Company

We expect Nagarjuna Construction Company (NCC) to post poor numbers for 1QFY2012.On the top-line front, NCC is expected to post modest growth of 7.6% yoy to ` 1,169.5cr.EBITDA margin is expected to be flat at ~9.7%. However, a shocker should come on theearnings front, as we expect the company to post a decline of 38.9% yoy/29.0% qoq to ` 25.3cr for the quarter. This would be primarily on account of burgeoning interest cost(jump of ~96.3% yoy), led by elongated working capital cycle. The financial closure status

for the 1,320MW power plant, which was guided by the company to be achieved inMarch, would be another important development for the quarter. We maintain our Buyrating on the stock with a target price of `109.

Simplex Infra

For Simplex Infra, we project flat top-line growth of 6.3% yoy to ` 1,251cr for 1QFY2012.This subdued performance would be mainly on account of slowdown faced by thecompany on the international front. It should be noted that during the last quarter orderawarding activity had picked up on the international front, but we believe it would taketime for the same to get converted into revenue. We expect EBITDA margin to remain

stable at 10.2%, in-line with management's guidance. However, the bottom line isexpected to be under pressure due to increased interest cost (yoy expected jump of ~41%),resulting in a yoy decline of around 10.1% to ` 32.5cr for the quarter. We maintain our Buyview on the stock with a target price of `404.

8/6/2019 Market Outlook 12th August 2011

http://slidepdf.com/reader/full/market-outlook-12th-august-2011 5/6

August 12, 2011 5

Market Outlook | India Research

Economic and Political News

July exports surge 82%, may slow from now

Food inflation rises to 9.9%

DTC set to miss deadline again

RBI surplus profit dips 20% in FY2011, liquidity overhang blamed

Corporate News

SBI, ICICI Bank hike lending rates 50bp

HCL Tech to create US$1bn business analytics segment

Manappuram Finance to raise ` 750cr through NCDs

Mahindra auto component arm pushes for integration

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Bajaj Hind Results

BF Utilities Results

BPCL Results

Century Tex Results

Coal India Results D B Realty Results HDIL Results Hindalco Inds Results HPCL Results

India Cements Results

Jaiprakash Asso Results

KSK Energy Results NCC Results Patel Engr Results Pipavav Ship Results Punj Lloyd Results Simplex Infra Results Spicejet Results Tata Steel Results Tech Mahindra Results Unitech Results

Videocon Inds Results

8/6/2019 Market Outlook 12th August 2011

http://slidepdf.com/reader/full/market-outlook-12th-august-2011 6/6

August 12, 2011 6

Market Outlook | India Research

Research Team Tel: 022-3935 7800 E-mail: [email protected] Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companiesreferred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is forgeneral guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to thelatest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may haveinvestment positions in the stocks recommended in this report.

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

Address: 6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai - 400 093.

Tel: (022) 3935 7800

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)Reduce (-5% to 15%) Sell (< -15%)