market recap highlights a1 mr- 12/02/2011 heightened volatility is once again the theme. stocks...

TRANSCRIPT

Market Recap Highlights

A1

MR- 12/02/2011

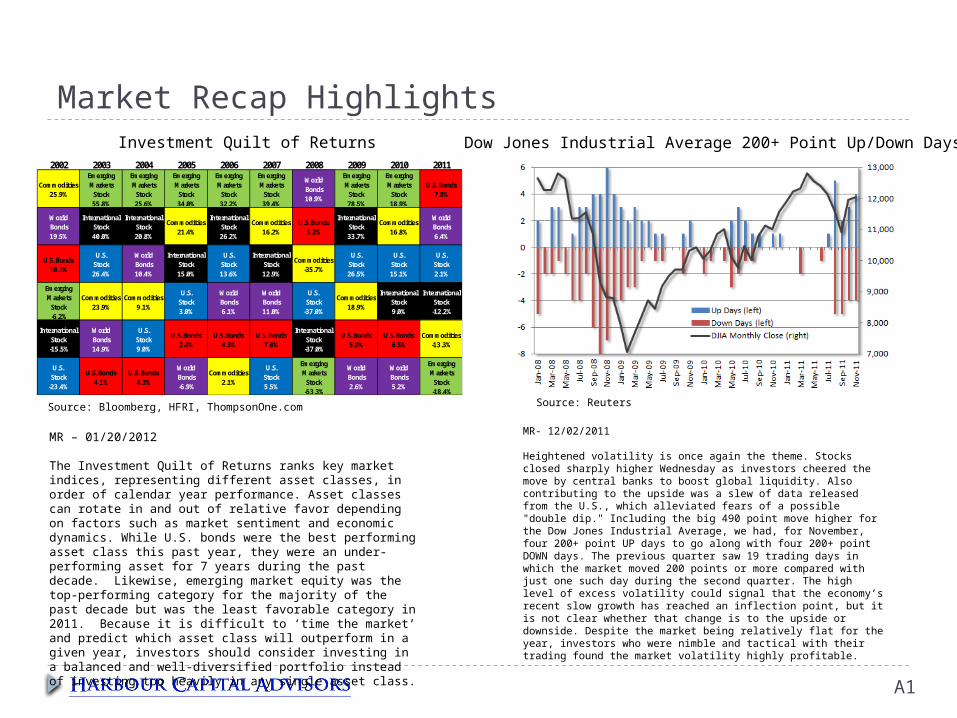

Heightened volatility is once again the theme. Stocks closed sharply higher Wednesday as investors cheered the move by central banks to boost global liquidity. Also contributing to the upside was a slew of data released from the U.S., which alleviated fears of a possible "double dip." Including the big 490 point move higher for the Dow Jones Industrial Average, we had, for November, four 200+ point UP days to go along with four 200+ point DOWN days. The previous quarter saw 19 trading days in which the market moved 200 points or more compared with just one such day during the second quarter. The high level of excess volatility could signal that the economy’s recent slow growth has reached an inflection point, but it is not clear whether that change is to the upside or downside. Despite the market being relatively flat for the year, investors who were nimble and tactical with their trading found the market volatility highly profitable.

Source: Reuters

Dow Jones Industrial Average 200+ Point Up/Down Days2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Commodities25.9%

Emerging Markets

Stock55.8%

Emerging Markets

Stock25.6%

Emerging Markets

Stock34.0%

Emerging Markets

Stock32.2%

Emerging Markets

Stock39.4%

World Bonds10.9%

Emerging Markets

Stock78.5%

Emerging Markets

Stock18.9%

U.S. Bonds7.8%

World Bonds19.5%

InternationalStock40.0%

InternationalStock20.8%

Commodities21.4%

InternationalStock26.2%

Commodities16.2%

U.S. Bonds5.2%

InternationalStock33.7%

Commodities16.8%

World Bonds6.4%

U.S. Bonds10.3%

U.S. Stock26.4%

World Bonds10.4%

InternationalStock15.0%

U.S. Stock13.6%

InternationalStock12.9%

Commodities-35.7%

U.S. Stock26.5%

U.S. Stock15.1%

U.S. Stock2.1%

Emerging Markets

Stock-6.2%

Commodities23.9%

Commodities9.1%

U.S. Stock3.0%

World Bonds6.1%

World Bonds11.0%

U.S. Stock

-37.0%

Commodities18.9%

InternationalStock9.0%

InternationalStock

-12.2%

InternationalStock

-15.5%

World Bonds14.9%

U.S. Stock9.0%

U.S. Bonds2.4%

U.S. Bonds4.3%

U.S. Bonds7.0%

InternationalStock

-37.0%

U.S. Bonds5.9%

U.S. Bonds6.5%

Commodities-13.3%

U.S. Stock

-23.4%

U.S. Bonds4.1%

U.S. Bonds4.3%

World Bonds-6.9%

Commodities2.1%

U.S. Stock5.5%

Emerging Markets

Stock-53.3%

World Bonds2.6%

World Bonds5.2%

Emerging Markets

Stock-18.4%

Investment Quilt of Returns

Source: Bloomberg, HFRI, ThompsonOne.com

MR – 01/20/2012

The Investment Quilt of Returns ranks key market indices, representing different asset classes, in order of calendar year performance. Asset classes can rotate in and out of relative favor depending on factors such as market sentiment and economic dynamics. While U.S. bonds were the best performing asset class this past year, they were an under-performing asset for 7 years during the past decade. Likewise, emerging market equity was the top-performing category for the majority of the past decade but was the least favorable category in 2011. Because it is difficult to ‘time the market’ and predict which asset class will outperform in a given year, investors should consider investing in a balanced and well-diversified portfolio instead of investing too heavily in any single asset class.

Market Recap Highlights

A2

Source: Gallup

MR-11/11/2011

Much of the current focus of the direction of the economy centers on the upcoming election. President Obama faces one of the most challenging political environments, as he prepares to try to win a second term next November. A state-by-state examination of the electoral map suggests that the president faces a far more challenging election than in 2008. President Obama was swept into office with 365 electoral votes (270 needed to win the election), having won several traditionally-Republican states. He is currently falling behind in several of the battleground states that he won in the last election. Based on current polling data, the upcoming election will be decided by 12 swing states, with Florida, Pennsylvania, and Ohio being the most highly-contested.

Electoral Map

MR – 01/06/2012

At the start of each year, market strategists typically attempt to forecast how the market will perform in the coming year. Most Wall Street strategists are optimistic that the stock market will increase in 2012 but are not forecasting a dramatic move higher. The current consensus estimate among strategists is for the S&P 500 index to end 2012 at around 1334, which would be 6.1% higher than the 2011 closing value of 1257. Given the current 2% yield for the S&P 500, the total return for the market would be ~ 8%. Many worry that there seem to be few solutions to the European sovereign-debt crisis and that corporate earnings growth in the U.S. may begin to slow. It is interesting to note that the average forecast for 2011 was 1372, which would have been an 8.3% gain. The market fell well short of that estimate.

S&P 500 Analyst Forecasts

Source: Birinyi Associates/WSJ

Asset Allocation Classes

A3

Tactical Change Key KeyPositioning from 4Q Headwinds Tailwinds

1 Cash & Short-term Bonds N Low Yields Safety; Risk Aversion

2 Government Bonds - High Prices; Low Yields Safety; Liquidity

3 Investment Grade Bonds N Expensive; M&A CycleStrong Balance Sheets; Relative Yields

4 High Yield & Emerging Markets Bonds + Default Risk; Currency ExchangePrices Lower; Highest yields; Corporate Recovery

5 Domestic Equity N Heightened volatility; Global Economic Slowdown

Low Interest Rates; Strong Earnings; Low Multiples

6 International Equities - Eurozone Debt Crisis; Lack of Catalyst

Cheapest Asset Class; Profit Recovery to Continue

7 Emerging Markets Equities + Inflation; Geopolitics Structural Theme of Long-term Growth; Less Expensive

8 Commodities - Valuation; ExpensiveEmerging Market Demand; Diversification; Inflation Protection

9 Real Estate N Liquidation Sales; Negative Perceptions

Yields High; Valuations; Greater Stability

10 Short Investment N Recent Market Recovery; Profit Taking

Portfolio Protection: Heightened Volatility and Macro Concerns

11 Alternative Investments N IlliquidDiversification; Absolute Return; Low Interest Rates

'+' = Overweight; '-' = Underweight; 'N' = Neutral

Economic Forecasts

A4

Other Key Indicators2009 2010 2011E 2012E Current 2009 2010 2011E 2012E

U.S. Unemployment Rate 8.60% 9.30% 9.60% 9.00% 8.60%GDP -3.50% 3.00% 1.80% 2.10% NonFarm Payroll (thousands) 137 (423) 78 137 115 CPI (Inflation) -0.40% 1.60% 3.20% 1.80% Corporate Profits - Operating ($Bill.) 1097 663 952 1063 1111

Global %Change Y/Y -8.3% 43.6% 11.7% 4.5%GDP -0.90% 5.00% 3.80% 3.50% S&P 500 Earnings 90 60.8 83.66 98.00 107CPI (Inflation) 1.60% 3.20% 4.30% 3.50% %Change Y/Y -7.0% 50.8% 17.1% 9.2%

Emerging Market S&P 500 1214 903 1258 1257 1330GDP -3.40% 4.30% 4.30% 2.80% %Change Y/Y 26.5% 15.1% -0.1% 5.8%CPI (Inflation) 7.70% 5.70% 6.20% 5.50% Capacity Utilization 78.00% 69.10% 74.50% 77.30% 78.70%

Personal Savings Rate 1.00% 5.10% 5.30% 1.00% 0.90%F/X Rates Housing Starts (thousands) 641 554 585 603 661

Spot Mar'12 Jun'12 Dec '12 Oil ($/bbl) 111.5 62 80 109 121EUR-USD 1.27 1.25 1.25 1.30 Gold ($/oz.) 1571 1092 1404 1682 1920USD-JPY 77 74 73 76

Interest Rates

Current Q112E Q212E Q312E Q412E 2011 2012EFed Funds 0-0.25% 0-0.25% 0-0.25% 0-0.25% 0-0.25% 0-0.25% 0-0.25%3-month T-Bill 0.01% 0.02% 0.05% 0.05% 0.05% 0.05% 0.05%3-month LIBOR 0.58% 0.60% 0.65% 0.50% 0.40% 0.55% 0.40%2-year T-Note 0.24% 0.25% 0.25% 0.30% 0.35% 0.25% 0.35%5-year T-Note 0.83% 0.60% 0.70% 0.80% 1.00% 0.85% 1.00%10-year T-Note 1.88% 1.75% 1.85% 2.10% 2.40% 2.00% 2.40%30-year T-Bond 2.90% 2.50% 2.70% 3.10% 3.60% 2.90% 3.60%

Source: Bloomberg: Barclays Wealth; BofA Merri l l Lynch Global Research; Standard & Poor's Services ; JP Morgan

4.33%

GDP & Inflation

Quarter

0.59%2.01%3.29%

Annual

0.30%0.12%0.125%

2010

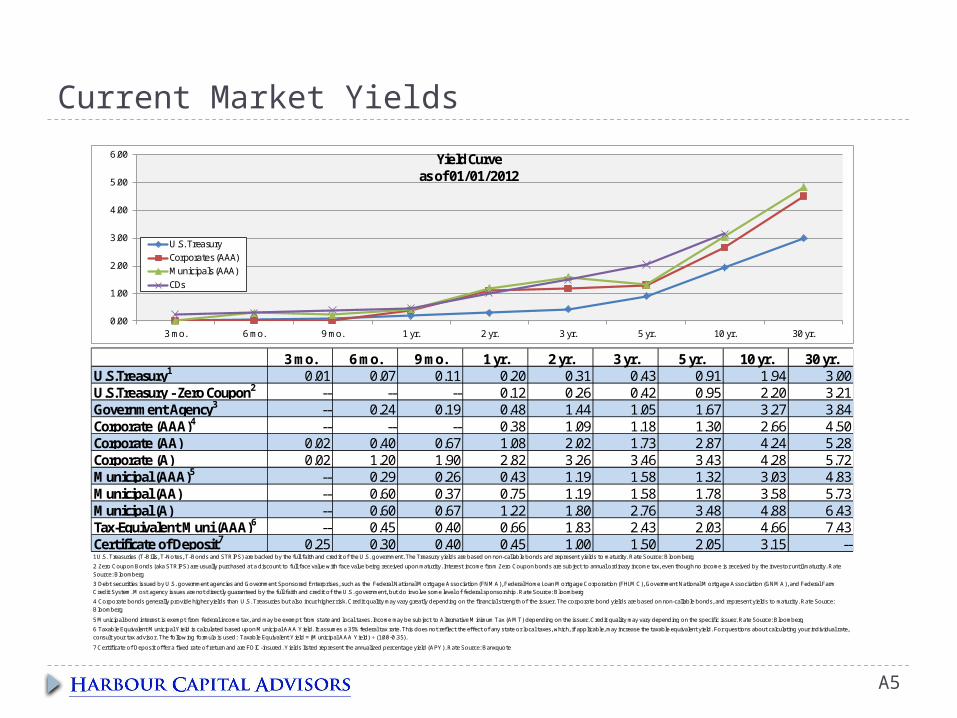

Current Market Yields

Implementation

A5

3 mo. 6 mo. 9 mo. 1 yr. 2 yr. 3 yr. 5 yr. 10 yr. 30 yr.U.S.Treasury1 0.01 0.07 0.11 0.20 0.31 0.43 0.91 1.94 3.00U.S.Treasury - Zero Coupon2 -- -- -- 0.12 0.26 0.42 0.95 2.20 3.21Government Agency3 -- 0.24 0.19 0.48 1.44 1.05 1.67 3.27 3.84Corporate (AAA)4 -- -- -- 0.38 1.09 1.18 1.30 2.66 4.50Corporate (AA) 0.02 0.40 0.67 1.08 2.02 1.73 2.87 4.24 5.28Corporate (A) 0.02 1.20 1.90 2.82 3.26 3.46 3.43 4.28 5.72Municipal (AAA)5 -- 0.29 0.26 0.43 1.19 1.58 1.32 3.03 4.83Municipal (AA) -- 0.60 0.37 0.75 1.19 1.58 1.78 3.58 5.73Municipal (A) -- 0.60 0.67 1.22 1.80 2.76 3.48 4.88 6.43Tax-Equivalent Muni (AAA)6 -- 0.45 0.40 0.66 1.83 2.43 2.03 4.66 7.43Certificate of Deposit7 0.25 0.30 0.40 0.45 1.00 1.50 2.05 3.15 --

7 Certificate of Deposit offer a fixed rate of return and are FDIC-insured. Y ields listed represent the annualized percentage yield (APY). Rate Source: Banxquote

1 U.S. Treasuries (T-Bills, T-Notes, T-Bonds and STRIPS) are backed by the full faith and credit of the U.S. government. The Treasury yields are based on non-callable bonds and represent yields to maturity. Rate Source: Bloomberg

2 Zero Coupon Bonds (aka STRIPS) are usually purchased at a discount to full face value with face value being received upon maturity. Interest income from Zero Coupon bonds are subject to annual ordinary income tax, even though no income is received by the investor until maturity. Rate Source: Bloomberg

3 Debt securities issued by U.S. government agencies and Government Sponsored Enterprises, such as the Federal National Mortgage Association (FNMA), Federal Home Loan Mortgage Corporation (FHLMC), Government National Mortgage Association (GNMA), and Federal Farm Credit System. Most agency issues are not directly guaranteed by the full faith and credit of the U.S. government, but do involve some level of federal sponsorship. Rate Source: Bloomberg

4 Corporate bonds generally provide higher yields than U.S. Treasuries but also incur higher risk. Credit quality may vary greatly depending on the financial strength of the issuer. The corporate bond yields are based on non-callable bonds, and represent yields to maturity. Rate Source: Bloomberg

5 Municipal bond interest is exempt from federal income tax, and may be exempt from state and local taxes. Income may be subject to Alternative Minimum Tax (AMT) depending on the issuer. Credit quality may vary depending on the specific issuer. Rate Source: Bloomberg

6 Taxable Equivalent Municipal Y ield is calculated based upon Municipal AAA Y ield. It assumes a 35% federal tax rate. This does not reflect the effect of any state or local taxes, which, if applicable, may increase the taxable equivalent yield. For questions about calculating your individual rate, consult your tax advisor. The following formula is used: Taxable Equivalent Y ield = (Municipal AAA Y ield) ÷ (1.00-0.35).

0.00

1.00

2.00

3.00

4.00

5.00

6.00

3 mo. 6 mo. 9 mo. 1 yr. 2 yr. 3 yr. 5 yr. 10 yr. 30 yr.

U.S. TreasuryCorporates (AAA)Municipals (AAA)CDs

Yield Curve as of 01/01/2012

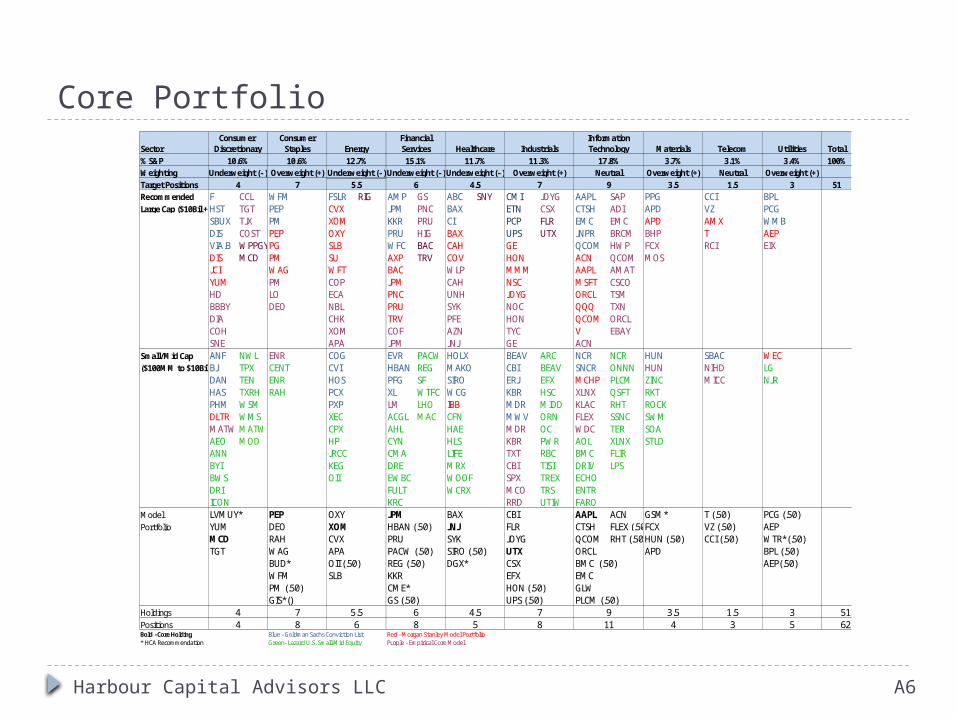

Core Portfolio

Harbour Capital Advisors LLC A6

ConsumerSector Staples Materials Telecom Utilities Total% S&P 10.6% 3.7% 3.1% 3.4% 100%Weighting Overweight (+) Overweight (+) Neutral Overweight (+)Target Positions 7 3.5 1.5 3 51Recommended F CCL WFM FSLR RIG AMP GS ABC SNY CMI JOYG AAPL SAP PPG CCI BPLLarge Cap ($10Bil +)HST TGT PEP CVX JPM PNC BAX ETN CSX CTSH ADI APD VZ PCG

SBUX TJX PM XOM KKR PRU CI PCP FLR EMC EMC APD AMX WMBDIS COST PEP OXY PRU HIG BAX UPS UTX JNPR BRCM BHP T AEPVIA.B WPPGYPG SLB WFC BAC CAH GE QCOM HWP FCX RCI EIXDIS MCD PM SU AXP TRV COV HON ACN QCOM MOSJCI WAG WFT BAC WLP MMM AAPL AMATYUM PM COP JPM CAH NSC MSFT CSCOHD LO ECA PNC UNH JOYG ORCL TSMBBBY DEO NBL PRU SYK NOC QQQ TXNDIA CHK TRV PFE HON QCOM ORCLCOH XOM COF AZN TYC V EBAYSNE APA JPM JNJ GE ACN

Small/Mid Cap ANF NWL ENR COG EVR PACW HOLX BEAV ARC NCR NCR HUN SBAC WEC($100MM to $10Bil)BJ TPX CENT CVI HBAN REG MAKO CBI BEAV SNCR ONNN HUN NIHD LG

DAN TEN ENR HOS PFG SF SIRO ERJ EFX MCHP PLCM ZINC MICC NJRHAS TXRH RAH PCX XL WTFC WCG KBR HSC XLNX QSFT RKTPHM WSM PXP LM LHO IBB MDR MIDD KLAC RHT ROCKDLTR WMS XEC ACGL MAC CFN MWV ORN FLEX SSNC SWMMATW MATW CPX AHL HAE MDR OC WDC TER SOAAEO MOD HP CYN HLS KBR PWR AOL XLNX STLDANN JRCC CMA LIFE TXT RBC BMC FLIRBYI KEG DRE MRX CBI TISI DRIV LPSBWS OII EWBC WOOF SPX TREX ECHODRI FULT WCRX MCO TRS ENTRICON KRC RRD UTIW FARO

Model LVMUY* PEP OXY JPM BAX CBI AAPL ACN GSM* T (.50) PCG (.50)Portfolio YUM DEO XOM HBAN (.50) JNJ FLR CTSH FLEX (.50)FCX VZ (.50) AEP

MCD RAH CVX PRU SYK JOYG QCOM RHT (.50)HUN (.50) CCI (.50) WTR*(.50)TGT WAG APA PACW (.50) SIRO (.50) UTX ORCL APD BPL (.50)

BUD* OII (.50) REG (.50) DGX* CSX BMC (.50) AEP(.50)WFM SLB KKR EFX EMCPM (.50) CME* HON (.50) GLW GIS*() GS (.50) UPS (.50) PLCM (.50)

Holdings 7 3.5 1.5 3 51Positions 8 4 3 5 62Bold - Core Holding Blue - Goldman Sachs Conviction List Red - Morgan Stanley Model Portfolio* HCA Recommendation Green- Lazard U.S. Small-Mid Equity Purple - Empirical Core Model

78

911

9

InformationTechnology

17.8%Neutral

Industrials11.3%

Overweight (+)7

44

FinancialServices15.1%

Underweight (- )6

Consumer Discretionary

10.6%Underweight (- )

4

68

Energy12.7%

Underweight (- )5.5

5.56 5

4.5

Healthcare11.7%

Underweight (- )4.5

Thematic Investments

Harbour Capital Advisors LLC A7

Sector Overweights: Industrials, Technology and Materials are the more economically sensitive areas of the market and benefit from overseas demand. We expect to maintain this view for the first half of the year but will consider a more defensive view later in the year which is more reflective of the business cycle.

Income-producing Securities provide attractive yields and hedge against near-term equity market volatility. Initiate positions in Master Limited Partnerships (MLPs), Floating Rate Bank Notes, High Yield Bonds, and Preferred Stocks.

Rise of Cloud Computing: Life in the clouds means applications are based in remote internet data centers – not on your PC or local server. Technology spending will be devoted to network applications, IT security, and systems management.

With strong balance sheets and hoards of cash, US Capital Expenditure Acceleration will be in stark contrast to both the consumer and government sectors. Corporate balance sheets are in better shape than they’ve been in over half a century. Focus on the stock of companies increasing dividends and buying back their stock.

Several factors suggest a Domestic Manufacturing Renaissance, as overseas manufacturing jobs may be returning to the U.S. as wages in many emerging economies have been increasing and companies are more willing to reconsider the U.S. in order to gain greater reliability and reduce the risks associated with the loss of intellectual property.

Dividend-paying Stocks are attractive to those seeking income but also as a means to offset market volatility. Companies able to consistently increase dividend payouts signal stability and an ability to weather an economic soft patch.

Be Nimble, with a Safety Net. The need to be active is greater than ever in a volatile market. Consider resorting to regular, dynamic portfolio rebalancing to adjust to economic and market developments.

Contrarian Investments

Harbour Capital Advisors LLC A8

Execution of Short-interest Strategies focused on timely investment when perception is that the market is “over-bought.” The market increases 2/3 of the time. This means that there are times when the market is under pressure. Short-interest prospers in such times and allows for greater conviction with the “long” portion of the portfolio.

Real over nominal assets: The potential for higher inflation favors real assets and those that are inflation-protected. Commodities are a winner. Precious metals such as Gold and Silver also serve as safe havens in times of market turbulence. Second-derivative investments (miners) should also benefit from elevated metal prices.

Distressed and Deep-value investments have led us to look at opportunities in areas such as Precious Metals and Financial Services companies. These would represent relatively short-term, tactical investments focused on the tendency of the market to over-discount headline news.

While Japan’s economy continues its recovery process and expects limited growth of domestic demand, it has an enormous potential of benefiting from the increasing Asian consumption market, given that Asia now accounts for more than 50% of Japan’s total exports

Hedge against equity Market Volatility by investing in the VIX. In times of market distress and sell-off, markets tend to converge, increasing trading volume.

Short the Euro versus the U.S. Dollar: With the unsettled nature of European Sovereign credit, we believe investment in European exporters is appealing, but we would also look to hedge Euro Dollar exposure.

The prices of Natural Gas Companies have plummeted as the commodity has fallen to historical lows. Many believe that natural gas is now significantly undervalued and presents room for sizable upsize.