market report - michigan€¦ · market report africa - middle east - south asia ... b r omi efu ga...

TRANSCRIPT

Market ReportAfrica - Middle East - South Asia - Oceania

January/February 2017

www.americanhardwood.org

Above: Manufacturing day with the designers for the UAE edition of AHEC's cross-regional Seed to Seat project. See page 4 for more information.

www.americanhardwood.orgPage 1

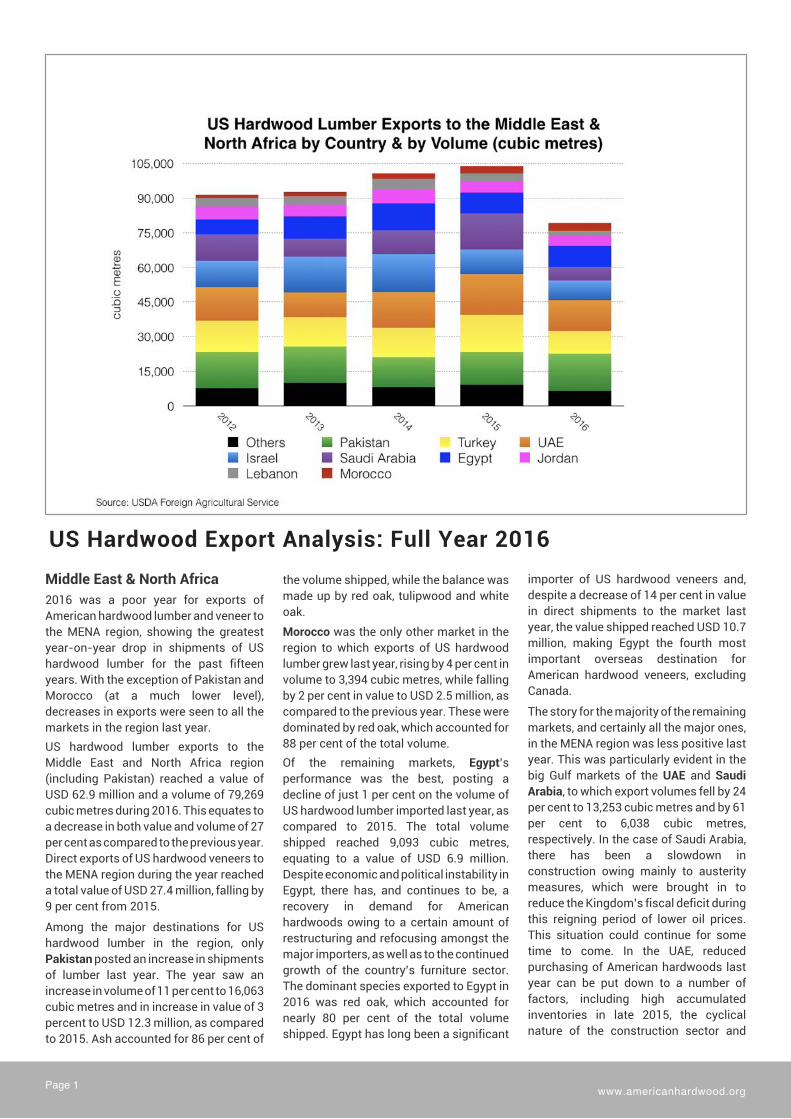

Middle East & North Africa

2016 was a poor year for exports ofAmerican hardwood lumber and veneer tothe MENA region, showing the greatestyear-on-year drop in shipments of UShardwood lumber for the past fifteenyears. With the exception of Pakistan andMorocco (at a much lower level),decreases in exports were seen to all themarkets in the region last year.US hardwood lumber exports to theMiddle East and North Africa region(including Pakistan) reached a value ofUSD 62.9 million and a volume of 79,269cubic metres during 2016. This equates toa decrease in both value and volume of 27per cent as compared to the previous year.Direct exports of US hardwood veneers tothe MENA region during the year reacheda total value of USD 27.4 million, falling by9 per cent from 2015.

Among the major destinations for UShardwood lumber in the region, onlyPakistan posted an increase in shipmentsof lumber last year. The year saw anincrease in volume of 11 per cent to 16,063cubic metres and in increase in value of 3percent to USD 12.3 million, as comparedto 2015. Ash accounted for 86 per cent of

the volume shipped, while the balance wasmade up by red oak, tulipwood and whiteoak.

Morocco was the only other market in theregion to which exports of US hardwoodlumber grew last year, rising by 4 per cent involume to 3,394 cubic metres, while fallingby 2 per cent in value to USD 2.5 million, ascompared to the previous year. These weredominated by red oak, which accounted for88 per cent of the total volume.Of the remaining markets, Egypt’sperformance was the best, posting adecline of just 1 per cent on the volume ofUS hardwood lumber imported last year, ascompared to 2015. The total volumeshipped reached 9,093 cubic metres,equating to a value of USD 6.9 million.Despite economic and political instability inEgypt, there has, and continues to be, arecovery in demand for Americanhardwoods owing to a certain amount ofrestructuring and refocusing amongst themajor importers, as well as to the continuedgrowth of the country’s furniture sector.The dominant species exported to Egypt in2016 was red oak, which accounted fornearly 80 per cent of the total volumeshipped. Egypt has long been a significant

importer of US hardwood veneers and,despite a decrease of 14 per cent in valuein direct shipments to the market lastyear, the value shipped reached USD 10.7million, making Egypt the fourth mostimportant overseas destination forAmerican hardwood veneers, excludingCanada.

The story for the majority of the remainingmarkets, and certainly all the major ones,in the MENA region was less positive lastyear. This was particularly evident in thebig Gulf markets of the UAE and Saudi

Arabia, to which export volumes fell by 24per cent to 13,253 cubic metres and by 61per cent to 6,038 cubic metres,respectively. In the case of Saudi Arabia,there has been a slowdown inconstruction owing mainly to austeritymeasures, which were brought in toreduce the Kingdom’s fiscal deficit duringthis reigning period of lower oil prices.This situation could continue for sometime to come. In the UAE, reducedpurchasing of American hardwoods lastyear can be put down to a number offactors, including high accumulatedinventories in late 2015, the cyclicalnature of the construction sector and

US Hardwood Export Analysis: Full Year 2016

www.americanhardwood.org Page 2

fiscal tightening in the lower oil-priceenvironment. However, the constructionsector in the UAE remains very active andthe major joinery manufacturers are beingkept busy by on-going and up-and-coming projects. This is partly confirmedby the fact that demand for US hardwoodveneers in the UAE grew significantly lastyear, rising by 100 per cent to USD 4.3million.

A significant amount of AHEC’s activitiesin the Middle East take place in the UAEand Dubai, in particular. This can beexplained by the fact that the UAE acts asa hub, both for the trade in wood products,but also for joinery and furnituremanufacturing. At the same time, the vastmajority of architectural and interiordesign firms operating in the regionchoose Dubai as their base. More recently,with the opening of Dubai Design District(d3) in 2015, Dubai has become the Gulfregion’s hub for design and innovation aswell.

In terms of trade, the UAE, notably Dubai,has long been an East-West entrepôt fornumerous food and luxury goods as wellas construction products and materialsincluding hardwood lumber and veneers.There are an estimated twenty large-scale timber importers in the country anda great many more smaller, tradingcompanies who deal in timber as part oftheir overall building products inventory.Much (an estimated 30 per cent) of thehardwood lumber and veneer that is

imported in to the UAE is re-exported toneighbouring Gulf markets, as well as toIran and East Africa. What remains isprocessed in to joinery and furniture(mainly case goods) for the significantnumber of on-going commercial andresidential construction projects in themarket, as well as in neighbouring Gulfcountries, but also further afield in Europe,Africa, India and even the United States.

The pace of construction in the Middle Easthas picked up considerably in the past threeyears or so and various in-market contactsare now talking of ‘pre-Global FinancialCrisis’ levels of activity in certain markets,whilst tempering this with warnings of atight credit situation. In particular, thehospitality sector in the Middle East isshowing massive growth, with a reported159,127 rooms in 555 projects underconstruction or in the final planning stagesas of last September, representing a 14.8per cent increase over September 2015.More importantly, some 257 hotels,housing more than half the rooms undercontract – 83,416 – are currently in theconstruction phase, according to the STRSeptember Pipeline Report. Thisrepresents an 8.5 per cent increase year-on-year. This growth comes with goodreason. There are world-class events suchas the World Expo 2020 in Dubai and theFIFA World Cup 2022 in Qatar on thehorizon, both of which are expected to drawmillions of visitors from around the world.

Political unrest has deepened in Turkey in

the wake of the unsuccessful 15/16 July2016 military coup and mounting politicalturmoil, exacerbated by terrorist attacks,is expected to drag on businessconfidence going forward. This situation,coupled with rising geopolitical risks, on-going clashes with Kurdish militants andincreased volatility in the financialmarkets following the Brexit vote,promises to have a negative impact on thecountry’s growth in the short-term.American hardwood lumber exports toTurkey dropped by 37 per cent in bothvolume and value last year, to 10,066cubic metres and to USD 8.0 million,respectively. While this would seem to bein line with the country’s lower economicperformance, the majority of thisdecrease was accounted for by a majordrop in the volumes of ash shipped to themarket - mostly destined for thermal-modification. European ash, particularlyfrom Ukraine, is, increasingly, being usedfor this process and this is due both to thereduced access to American ash, as aresult of EAB-related Customsrestrictions, as well as the weakness ofthe US dollar-euro exchange rate. Directshipments of American hardwoodveneers to Turkey also decreased lastyear, falling by 33 per cent to USD 5.4million, as compared to 2015.

Australia & New Zealand

US hardwood lumber exports to Australia

reached a value of USD 11.9 million and avolume of 15,473 cubic metres during2016, dropping by 2 per cent in value, butrising by 5 per cent in volume over theprevious year. Direct exports of UShardwood veneers to Australia reached avalue of USD 1.6 million during the year,rising by 15 per cent from 2015.The continued strength of the US dollaragainst the Australian dollar has certainlymade American hardwoods lessaffordable in the past two to three years,but demand has remained high, as theyhave become increasingly appreciated bythe country’s designers and consumersalike. This is especially true of white oak,which continued to dominate exportsduring 2016, accounting for 87 per cent ofthe total volume shipped during the year.However, the dominance of white oak hasdecreased marginally, since importers

www.americanhardwood.orgPage 3

and end users alike are starting to becomemore familiar with a wider range of UShardwood species. Shipments of both redoak and tulipwood to Australia increasedsignificantly last year, albeit from a fairlylow starting point. The volume of red oaklumber shipped reached 568 cubic metreslast year, rising from a total of just 75cubic metres in 2015. At the same time,shipments of tulipwood rose to 121 cubicmetres from just 12 cubic metres in theprevious year.

US hardwood lumber exports to New

Zealand reached a value of USD 5.9 millionand a volume of 7,594 cubic metres during2016, rising by 8 per cent and 11 per cent,respectively, as compared to the previousyear. This is in stark contrast to the firstsix months of 2016, which saw fairlysignificant decreases in shipments to themarket. This also makes 2016 the bestyear yet for US hardwood lumber exportsto New Zealand and marks a 106 per centincrease in shipments compared to fiveyears previously.

In line with the prevailing trend, the mainUS hardwood species exported to NewZealand was white oak, which accountedfor 75 per cent of the total volume shippedlast year. However, as in Australia, anuptake was seen demand for other UShardwood species; namely ash andwalnut.

India

Through last year, exports of Americanhardwood lumber to India continued toremain somewhat haphazard, with littlesign of settling in to a steady pattern.While there is a lot of anecdotal evidenceto suggest that US hardwood species arebecoming better known and that there is aneed for greater volumes and a greatervariety of imported kiln-dried hardwoodsfor the furniture and interiors sector, thevolumes actually imported remain at avery low level.US hardwood lumber exports to Indiareached a value of USD 1.1 million and avolume of just 1,751 cubic metres during2016. This equates to a significantdecrease in value of 45 per cent over theprevious year and an even moresignificant increase in volume of 56 percent. However, the export statisticssuggest that there could be an anomaly,since the volume of “other temperate”hardwood lumber shipped to India duringthe year was just 37 cubic metres, havingbeen, somewhat inexplicably, in excess of1,500 cubic metres in the previous year. If

these numbers are discounted aserroneous, then the volume shipped lastyear would be somewhat less of asignificant decrease as compared to 2015.At the same time, direct exports of UShardwood veneers to India reached a totalvalue of USD 1.4 million, rising by 3 per centon 2015.

Of the 1,751 cubic metres of US hardwoodlumber shipped to the market last year,nearly 40 per cent was accounted for by redoak. This is a new development, sincehickory has been the dominant UShardwood species in the past few years. Infact, imports of hickory lumber declinedconsiderably last year, falling by 78 per centto 288 cubic metres.

There are two developments which mayhave a positive impact on exports of UShardwood lumber to India in the comingyears. The first is that India remainssteadfast in its insistence upon methylbromide fumigation for imported logs,despite the almost total global ban on thischemical treatment. This means that bothhardwood log shippers and buyers arefinding it increasingly difficult to get theirproducts through Indian Customs.

The second is the CITES listing of theentire Dalbergia genus, which includessheesham (Dalbergia sisoo). This locally-grown species is one of the mainstays ofthe Indian wood furniture sector,especially when it comes to the large-

www.americanhardwood.org Page 4

scale production of solid hardwoodfurniture for export, such as can be foundin Jodhpur and Jaipur in Rajasthan. Thishas already had an impact on the furnituresector there and factories are currently

investigating alternative hardwoodspecies. Of course, cost will be the keydeciding factor, as overseas buyers ofIndian hardwood furniture, such as the

major furniture US furniture retailers, maybe forced to source from other countries ifproduction costs are driven too high bythe cost of raw materials.

South Africa

In contrast to the previous year, UShardwood lumber exports to South Africagrew during 2016. In total, lumber exportsreached a value of USD 7.4 million and avolume of 10,744 cubic metres, rising by 4per cent and by 6 per cent, respectively, onthe previous year. Direct exports of UShardwood veneers to South Africareached a total value of USD 4.8 millionlast year, rising by 3 per cent on 2015.

While the South African economy on thewhole, is anything but buoyant, thereremains considerable purchasing powerwithin a small segment of society and this,in the main, is what drives demand for UShardwoods in furniture, flooring andinterior joinery. The construction sector isalso picking up and there is a significantamount of activity on the skylines of bothJohannesburg and Cape Town, inparticular. The design sector is alsogrowing and South African designers arebecoming increasingly well-knownacross Africa, as well as around the globe.While a fairly wide range of US hardwoodspecies were shipped to South Africaduring the period, 61 per cent of the totalvolume shipped was accounted for bywhite oak at 6,584 cubic metres. This was

more or less the same as in 2015 and itshows how the trend for white oak infurniture, joinery and flooring is completelyglobal. At the same time, lower shipmentsof red oak and walnut lumber were more

than made up for by increased volumes ofash and tulipwood going to the market.

AHEC Seed to Seat Project: Update

Starting in early 2016, AHEC launched across-regional project, which aimed todemonstrate the true environmentalimpact of designing furniture withAmerican hardwoods through life cycleassessment (LCA). The Seed to Seatproject was also conceived as a way forAHEC to collaborate with high profiledesigners and to introduce them to UShardwood species that were less well-known in their markets.

The first edition was completed inAustralia and New Zealand with theexhibition of six seats by six designers atDenfair in Melbourne last June. In thiscase, the species used were red oak,cherry, tulipwood and thermally-modifiedash.

The second edition of the project is nownearing completion in Dubai, UAE. Withthe exception of thermally-modified ash,

the same species are being used and sevenUAE-based designers have created sevenseats. Crafted by AMBB FurnitureManufacturing in Dubai, the finished pieceswill be exhibited for the first time at DesignDays Dubai, which opens on 13 March 2017for 5 days at Dubai's Design District (d3).

At the same time, the South African editionof the same project is now well-underway.Seven designers, five in Cape Town and twoin Johannesburg, are currently finalisingtheir designs. In this edition, the designersare able to choose between cherry, red oak,soft maple and tulipwood.

In mid-February, AHEC's SustainabilityConsultant, Rupert Oliver, flew to SouthAfrica to brief the designers on LCA anddata collection during manufacturing.Unlike in the Australia/NZ and UAE editionsof Seed to Seat, all seven of the designers in

South Africa are also manufacturers andeach of the seven seats will be made bytheir individual designers. This meansthat it is crucial to ensure that all are fullyconversant with the data collectionprocess, so that full environmentalprofiles for the finished pieces can beproduced.

The seven seats will be exhibited for thefirst time at 100% Design South Africa,which will take place in Johannesurg from9-13 August 2017.

To follow the project, please see:www.seedtoseat.info.

www.americanhardwood.orgPage 5

PR Highlights

USD 1.00 =

Euro (EUR)Bahraini Dinar (BHD)*Egyptian Pound (EGP)Israeli New Shekel (ILS)Jordanian Dinar (JOD)*Kuwaiti Dinar (KWD)Lebanese Pound (LBP)*Moroccan Dirham (MAD)Omani Rial (OMR)*Pakistani Rupee (PKR)Qatari Rial (QAR)*Saudi Riyal (SAR)*Turkish Lira (TRY)UAE Dirham (AED)*South African Rand (ZAR)Bangladeshi Taka (BDT)Indian Rupee (INR)Sri Lanka Rupee (LKR)Australian Dollar (AUD)New Zealand Dollar (NZD)

31 Jan 2017

0.930.3718.773.770.710.301,482.079.890.38103.673.643.753.833.6713.5278.1467.93148.821.321.38

28 Feb 2017

0.950.3715.843.670.710.301,506.8510.030.38104.063.643.753.603.6712.9478.8866.66151.921.301.39

Exchange Rates

Source: OANDA FX Converter*denotes currency pegged to USD

Regional Events *Bold denotes AHEC event or AHECparticipation

www.americanhardwood.org

AHEC Africa - Middle East - South Asia - [email protected]

MENA - Mimarlik (TurkishArchitectural magazine) - Jan2017

2 page feature on Tel Avivtulipwood staircase

Oceania - AustralasianTimber - Feb 2017

Cover & feature on TelAviv tulipwood staircase

India - Commercial Design- Feb 2017

4 page feature on Dubaiinterior in white oak &winner of CID Awards 2016

MENA - TradeArabia - 17Jan 2017

Story on UAE edition ofAHEC's Seed to Seatproject

1-4 Mar Delhiwood Greater Noida, India

7-9 Mar Dubai Wood Show Dubai, United Arab Emirates

13-17 Mar Design Days Dubai Dubai, United Arab Emirates

9-13 Aug 100% Design SA Johannesburg, South Africa

8-10 Jun Denfair Melbourne, Australia

22-25 May INDEX Dubai Dubai, United Arab Emirates

23-27 May Turkeybuild Istanbul, Turkey

2-5 Nov Interwood Mumbai, India

11-13 Nov Woodtech Forum Damietta, Egypt

13-18 Nov Dubai Design Week Dubai, United Arab Emirates