market research and competitive intelligence priorities€¦ · growth team membership ™ 2013...

TRANSCRIPT

1

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

growth team m e m b e r s h i p ™

Co-Sponsor

Market Research and Competitive Intelligence Priorities

2013 global survey results

Share this survey on Twitter and Linkedin

2

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

CONTENTSMarket Research and Competitive Intelligence Executive Summary 3

Survey Overview and Distribution of Respondents 4

What is the Growth Team Membership™? 5

Overarching Challenges 6

Key Market Research Challenges 7

Market Research Resource Trends 11

Key Competitive Intelligence Challenges 17

Competitive Intelligence (CI) Resource Trends 21

Special Interest Topic: Supporting Stakeholder Decision‑Making 27

Respondent Demographics 34

INTRO

SECTION

1

SECTION

4

SECTION

2

SECTION

5SECTION

6

SECTION

3

3

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Introduction

Market Research and Competitive Intelligence (CI) Survey Executive Summary

SECTION 1: Key Market Research Challenge

KEY INTERNAL CHALLENGE

Ensuring research insights are actionable and included in stakeholders’ decision‑making

KEY INTERNAL CHALLENGE ROOT CAUSE

Lack of process reinforcement

SECTION 2: Market Research Resource Trends

BUDGETS

R&D typically has an annual budget of less than $500,000*

RESOURCES

For 2013, budgets and staffing levels will remain constant

* All monetary values in this report are in US dollars ($USD).

SECTION 3: Key Competitive Intelligence Challenges

KEY INTERNAL CHALLENGE

Developing, implementing, and monitoring counter‑intelligence tactics

KEY INTERNAL CHALLENGE ROOT CAUSE

Inadequate skills

SECTION 4: Competitive Intelligence (CI)Resource Trends

BUDGETS

R&D typically has an annual budget of less than $250,000*

RESOURCES

For 2013, budgets and staffing levels will remain constant

SECTION 5: Supporting Stakeholder Decision‑Making

PRIMARY INTERNAL CLIENT

Sales/Business Development

TOP ACTIVITY TO SUPPORT SALES

Customer/consumer research

TOP ACTIVITY TO SUPPORT EXECUTIVE MANAGEMENT

SWOT analysis

4

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Introduction

Co-SponsorSurvey PopulationMethodologySurvey Purpose

To understand the most pressing challenges shaping market research and competitive intelligence executives’ 2013 planning

Web‑based survey platform Market research and competitive intelligence executives at manager level and above

Survey Overview and Distribution of Respondents

93survey

respondents *

Americas

50% Africa

1%

Europe

7%

Middle East

19%South Asia

0%

Asia-Pacific

14%

* Percentages do not include respondents who answered “Other” or did not complete the question.

respondents’ roles*Corporate

44%

39%

17%Business Unit/Division

Both Corporate and Business Unit/Division

5

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Introduction

What is the Growth Team Membership™?

GTM provides best practices, events, and services that enable executives to address challenges within their companies

CorporateStrategy

Corporate Development

Marketing

CompetitiveIntelligence

MarketResearch

SalesLeadership

R&D/Innovation

Investors/Finance

CEO

MarketResearch

CompetitiveIntelligence

CEO’s Growth Team™ GTM: Creating Client Value

GTM’s case‑based best practices help executives:

Speed the design and implementation of initiatives by not reinventing the wheel

Save money and reduce risk by avoiding mistakes made by other companies

Accelerate problem‑solving with a cross‑industry perspective

Improve their functions’ and companies’ performance and productivity

[email protected] www.gtm.frost.com slideshare.net/FrostandSullivantwitter.com/Frost_GTM

GTM is a research and consulting program that supports executives within the functions that report to the CEO

6

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Introduction

Contact us at GTMResearch@frost com

Ensuring Research Insights are Actionable

Market Research must deliver actionable customer insights to drive the company’s decision‑making

Learn how BP’s market research function used segment‑based consumer insights to shape companywide marketing initiatives

Capturing Employees’ Competitive Information

Competitive Intelligence needs to harness the competitive insights of its employees

Learn how Cintas developed a companywide intelligence network that incorporated employee insights into the company’s decision‑making

Devising Effective Competitive StrategiesCompetitive Intelligence executives must continually assess the company’s unique strengths, identify high‑growth market opportunities, and analyze potential responses to competitive threats

Learn how our Competitive Strategy toolkit helps you perform internal competency evaluation, market due diligence, and threat mitigation

Market Research’s Overarching Challenges

Competitive Intelligence’s Overarching Challenges

Best Practice Solutions from GTM

What’s Keeping Market Research and Competitive Intelligence Executives Up at Night in 2013?

7

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

SECTION

6

SECTION

5

SECTION

4

SECTION

3

SECTION

2

SECTION

1

INTRO

SECTION

1 Key Market Research Challenges

8

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 1

CHALLENGE

1 Ensuring research insights are actionable and included in stakeholders’ decision‑making

2 Developing an integrated customer and market insights dashboard to support decision‑making

3 Creating an insight generation process that yields high‑quality outputs

4 Integrating global, regional, and local customer/market information to generate insights

5 Demonstrating the ROI of market research

Top Five Key Market Research Challenges

SURVEY QUESTION: What are the top five functional challenges shaping your market research plans?

IN 2011, respondents were concerned with providing valuable insights for strategic decision‑makers

BY 2012, respondents were focusing on demonstrating the ROI of market research

9

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 1

Respondents’ challenges are attributed to staff and process limitations

SURVEY QUESTION: Please indicate the root cause—staff, process, technology/systems, or strategic alignment—of your top five market research challenges.

Root Cause of Top Five Market Research ChallengesTop Five Market Research Challenges

CHALLENGE

1Ensuring research insights are actionable and included in stakeholders’ decision‑making

Process: Lack of enforcement

2Developing an integrated customer and market insights dashboard to support decision‑making

Staff: Inadequate headcount

3 Creating an insight generation process that yields high‑quality outputs Process: Lack of process

4Integrating global, regional, and local customer/market information to generate insights

Staff: Inadequate headcount

5 Demonstrating the ROI of market researchProcess: Lack of enforcement

Strategic Alignment: Insufficient support by senior management

10

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 1

B-to-B respondents prioritize dashboards and future trends, while B-to-C respondents focus on portfolio balance and insight quality

Top Five Market Research Challenges (By Business Model)

CHALLENGE B-to-B B-to-C

1 Engaging stakeholders to pinpoint their research needs

Ensuring the research portfolio balance strategic and tactical projects

2 Developing an integrated customer and market insights dashboard to support decision‑making

Ensuring research insights are actionable and included in stakeholders’ decision‑making

3 Ensuring research insights are actionable and included in stakeholders’ decision‑making

Creating an insight generation process that yields high‑quality outputs

4 Demonstrating the ROI of market research Integrating global, regional, and local customer/market information to generate insights

5 Identifying and prioritizing future trends/Mega Trends Demonstrating the ROI of market research

11

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

SECTION

6

SECTION

5

SECTION

4

SECTION

3

SECTION

2

SECTION

1

INTRO

SECTION

2 Market Research Resource Trends

12

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 2

0%

10%

20%

30%

40%

50%

35%

41%

22%

26%

31%

14%16%

9%

29%

15%13%

21%

2% 3%

0%2% 3%

0%2%0%

7%

2%0%

7%

B-to-C market research departments have larger budgets than those in B-to-B companies

2013 Market Research Budgets (By Business Model)

SURVEY QUESTION: Which of the above ranges (in $USD) best describes your 2013 total market research budget (all expenditures on market research activities and general & administrative—including staff)?

$250,000 to $499,999

$500,000 to $999,999

Below $250,000 $1 Million to $2.99 Million

$3 Million to $4.99 Million

$5 Million to $9.99 Million

$10 Million to $19.99 Million

$20 Million or more

All Companies B‑to‑B Companies B‑to‑C Companies

percentage of revenue dedicated to department budget (by business model)

The median percentage of company revenue dedicated to the market research budget is: • All companies = 1% • B-to-B companies = 1% • B-to-C companies = 0.9%

Survey Question: What is your 2013 total market research budget as a percentage of your company’s total 2012 revenue?

Average = $374,999

Median = $374,999

0%

10%

20%

13%

18%

10% 10%

8%

10%

8%

5%

10%9%

8%

10%

1%0%

2%

5%

0%

10%

18% 18%

15%

13

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 2

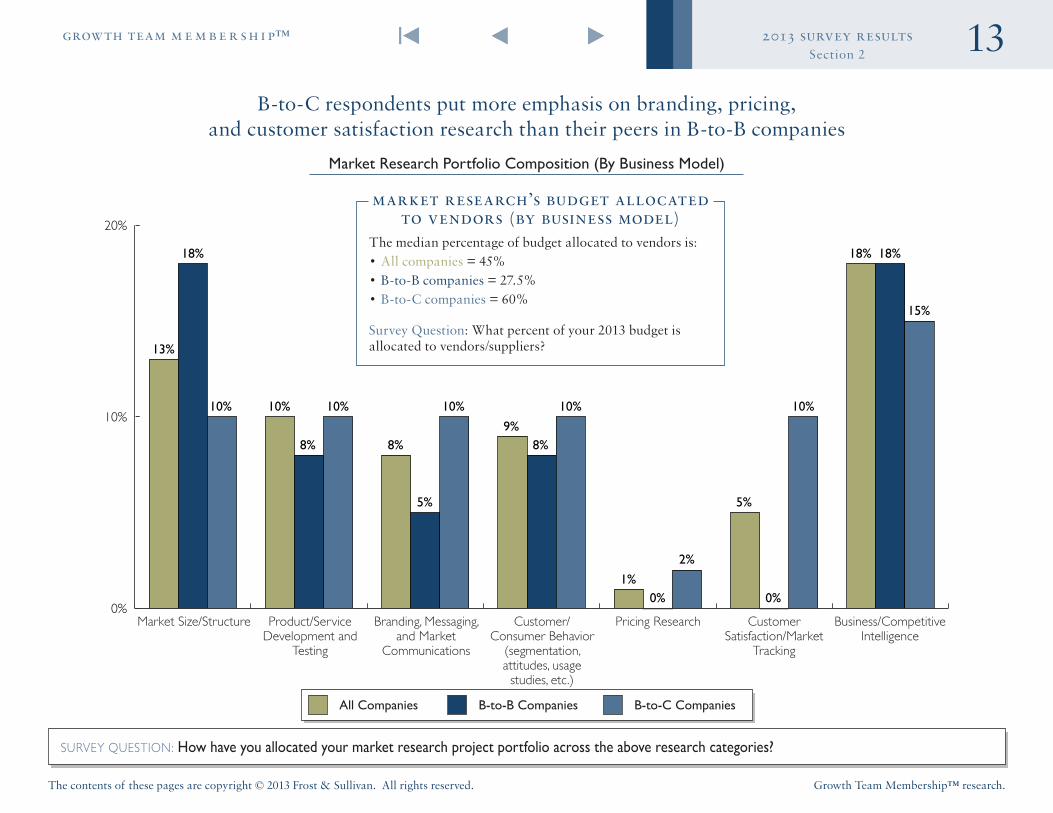

B-to-C respondents put more emphasis on branding, pricing, and customer satisfaction research than their peers in B-to-B companies

Market Research Portfolio Composition (By Business Model)

SURVEY QUESTION: How have you allocated your market research project portfolio across the above research categories?

All Companies B‑to‑B Companies B‑to‑C Companies

Market Size/Structure Product/Service Development and

Testing

Branding, Messaging, and Market

Communications

Customer/Consumer Behavior

(segmentation, attitudes, usage

studies, etc.)

Pricing Research Customer Satisfaction/Market

Tracking

Business/Competitive Intelligence

market research’s budget allocated to vendors (by business model)

The median percentage of budget allocated to vendors is: • All companies = 45% • B-to-B companies = 27.5% • B-to-C companies = 60%

Survey Question: What percent of your 2013 budget is allocated to vendors/suppliers?

0%

10%

20%

30%

40%

50%

60%

70%

2% 3%0%

25%

21%

38%

67%70%

54%

6% 6%8%

0% 0% 0%

14

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 2

The majority of respondents expect staffing levels to remain constant in 2013

Market Research Staffing Changes (By Business Model)

SURVEY QUESTION: In comparison to 2012, your 2013 market research staffing will…

All Companies B‑to‑B Companies B‑to‑C Companies

market research staff (by business model)

The median number of staff is: All companies = 3 employees, B-to-B companies = 3 employees, B-to-C companies = 4.5 employees.

Survey Question: Approximately how many full-time employees are in your market research department?

2013 Average Rating = 3 23

2012 Average Rating = 3 112011 Average Rating = 3 21

4Increase Moderately

1Decrease Substantially

5Increase Substantially

2Decrease Moderately

3Stay the Same

RESPONDENTS’ expectations for additional staff has recovered after a sharp decline in 2012

0%

10%

20%

30%

40%

50%

4%6%

0%

32% 31%

39%

49%47% 46%

13% 13%15%

2% 3%

0%

15

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 2

Most respondents expect budgets to remain static in 2013

Market Research Budget Changes (By Business Model)

SURVEY QUESTION: In comparison to 2012, your 2013 market research budget will…

All Companies B‑to‑B Companies B‑to‑C Companies

2013 Average Rating = 3 232012 Average Rating = 3 06

2011 Average Rating = 3 14

4Increase Moderately

1Decrease Substantially

5Increase Substantially

2Decrease Moderately

3Stay the Same

EXPECTATIONS for additional funding have increased

0%

10%

20%

30%

40%

50%

60%

70%

4% 3%

8%

33%

41%

15%

48%

37%

69%

11%13%

8%

4%6%

0%

16

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 2

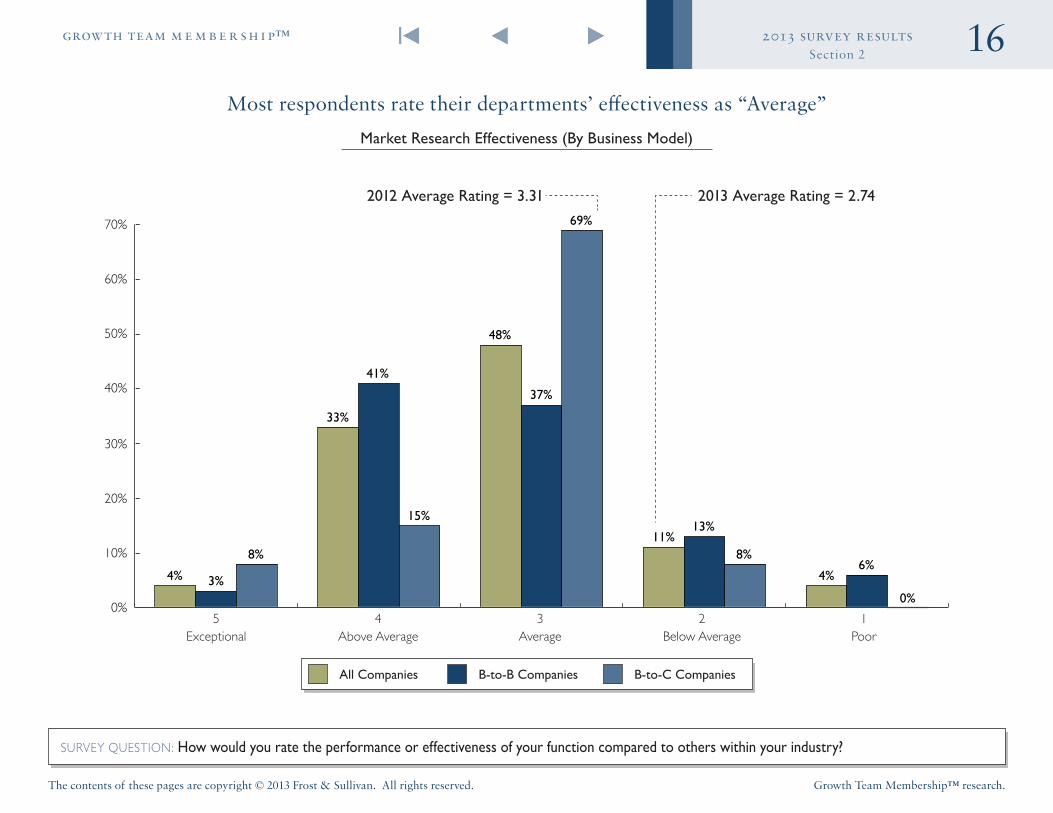

Most respondents rate their departments’ effectiveness as “Average”

Market Research Effectiveness (By Business Model)

SURVEY QUESTION: How would you rate the performance or effectiveness of your function compared to others within your industry?

4Above Average

1Poor

5Exceptional

2Below Average

3Average

All Companies B‑to‑B Companies B‑to‑C Companies

2013 Average Rating = 2 742012 Average Rating = 3 31

17

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

SECTION

6

SECTION

5

SECTION

4

SECTION

3

SECTION

2

SECTION

1

INTRO

SECTION

3 Key Competitive Intelligence Challenges

18

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 3

CHALLENGE

1 Developing, implementing, and monitoring counter‑intelligence tactics

2 Packaging and communicating competitive data and insights to drive stakeholder decision‑making

3 Capturing the competitive information held by your company’s employees

4 Developing an integrated competitive insights dashboard to support decision‑making

5 Conducting actionable win/loss analysis

Top Five Key Competitive Intelligence Challenges

SURVEY QUESTION: What are the top five functional challenges shaping your competitive intelligence strategy?

FOR the previous two years, the top challenge was “Aligning Key Intelligence Topics (KITs) to the company’s strategic priorities ”

19

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 3

Respondents’ challenges are attributed to staff and process limitations

SURVEY QUESTION: Please indicate the root cause—staff, process, technology/systems, or strategic alignment—of your top five competitive intelligence challenges

Root Cause of Top Five Competitive Intelligence ChallengesTop Five Competitive Intelligence Challenges

CHALLENGE

1 Developing, implementing, and monitoring counter‑intelligence tactics Staff: Inadequate skills

2Packaging and communicating competitive data and insights to drive stakeholder decision‑making

Process: Lack of process

3 Capturing the competitive information held by your company’s employees Process: Lack of process

4Developing an integrated competitive insights dashboard to support decision‑making

Technology/Systems: Inadequate/outdated technology

5 Conducting actionable win/loss analysis Staff: Lack of experience

20

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 3

B-to-B respondents focus on dashboards and counter-intelligence tactics, while their B-to-C peers prioritize stakeholder needs and competitive alerts

Top Five Competitive Intelligence Challenges (By Business Model)

CHALLENGE B-to-B B-to-C

1 Developing, implementing, and monitoring counter‑intelligence tactics

Packaging and communicating competitive data and insights to drive stakeholder decision‑making

2 Capturing the competitive information held by your company’s employees Diagnosing stakeholders’ specific intelligence needs

3 Packaging and communicating competitive data and insights to drive stakeholder decision‑making

Capturing the competitive information held by your company’s employees

4 Developing an integrated competitive insights dashboard to support decision‑making Creating effective and timely competitive alerts

5 Conducting actionable win/loss analysis Conducting actionable win/loss analysis

21

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

SECTION

6

SECTION

5

SECTION

4

SECTION

3

SECTION

2

SECTION

1

INTRO

SECTION

4 Competitive Intelligence (CI) Resource Trends

0%

10%

20%

30%

40%

50%

60%

70%

61%63%

60%

15%

22%

0%

11%9%

13%11%

6%

20%

2%0%

7%

22

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 4

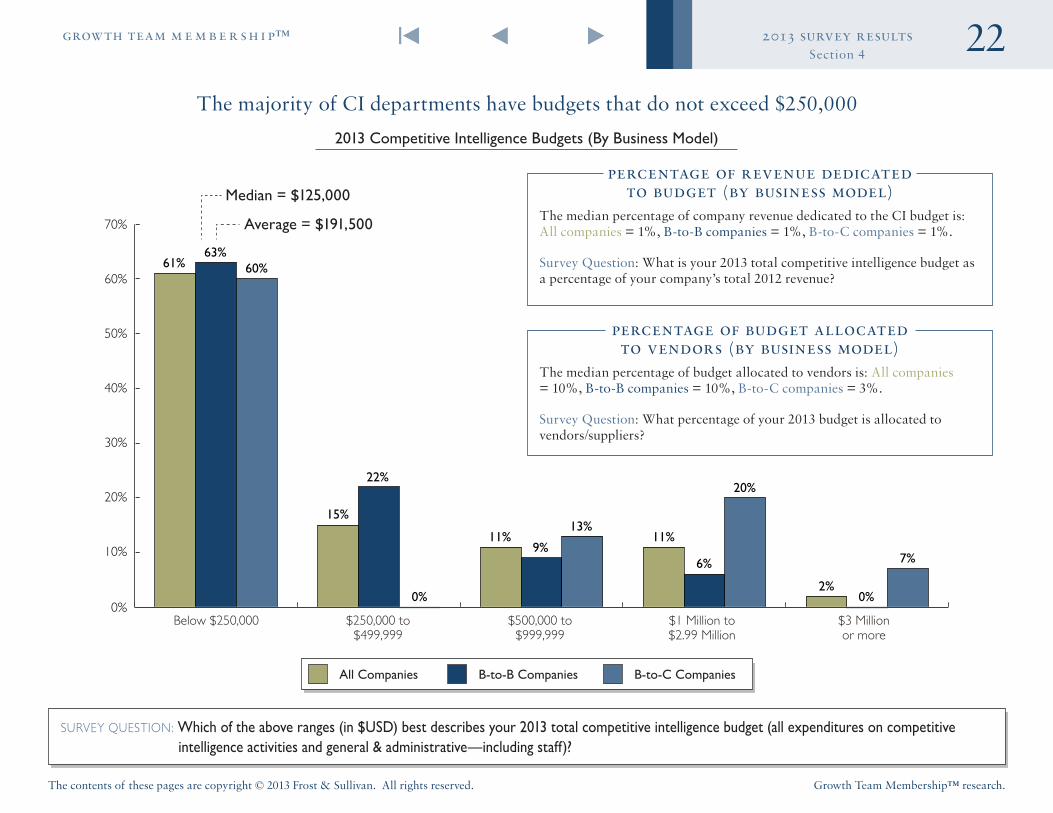

The majority of CI departments have budgets that do not exceed $250,000

2013 Competitive Intelligence Budgets (By Business Model)

SURVEY QUESTION: Which of the above ranges (in $USD) best describes your 2013 total competitive intelligence budget (all expenditures on competitive intelligence activities and general & administrative—including staff)?

$250,000 to $499,999

$500,000 to $999,999

Below $250,000 $1 Million to $2.99 Million

$3 Million or more

All Companies B‑to‑B Companies B‑to‑C Companies

percentage of revenue dedicated to budget (by business model)

The median percentage of company revenue dedicated to the CI budget is: All companies = 1%, B-to-B companies = 1%, B-to-C companies = 1%.

Survey Question: What is your 2013 total competitive intelligence budget as a percentage of your company’s total 2012 revenue?

Average = $191,500

Median = $125,000

percentage of budget allocated to vendors (by business model)

The median percentage of budget allocated to vendors is: All companies = 10%, B-to-B companies = 10%, B-to-C companies = 3%.

Survey Question: What percentage of your 2013 budget is allocated to vendors/suppliers?

All Companies B‑to‑B Companies B‑to‑C Companies

4Increase Moderately

1Decrease Substantially

5Increase Substantially

2Decrease Moderately

3Stay the Same

0%

10%

20%

30%

40%

50%

60%

70%

4%6%

0%

19% 18%

22%

65% 65% 64%

10%8%

14%

2% 3%0%

23

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 4

The majority of respondents expect staffing levels to remain static

Competitive Intelligence Staffing Changes (By Business Model)

SURVEY QUESTION: In comparison to 2012, your 2013 competitive intelligence staffing will…

competitive intelligence staff (by business model)

The median number of employees in 2013 is: • All companies = 2 employees • B-to-B companies = 1.5 employees • B-to-C companies = 2.5 employees

Survey Question: Approximately how many full-time employees are in your competitive intelligence department?

2013 Average Rating = 3 122012 Average Rating = 3 212011 Average Rating = 3 25

EXPECTATIONS for additional staff have declined over the past three years

All Companies B‑to‑B Companies B‑to‑C Companies

4Increase Moderately

1Decrease Substantially

5Increase Substantially

2Decrease Moderately

3Stay the Same

0%

10%

20%

30%

40%

50%

60%

70%

2% 3%0%

22%

27%

12%

58%

52%

69%

18% 18% 19%

0% 0% 0%

24

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 4

The majority of respondents expect little to no budget increase for 2013

Competitive Intelligence Budget Changes

SURVEY QUESTION: In comparison to 2012, your 2013 competitive intelligence budget will…

2013 Average Rating = 3 082012 Average Rating = 3 182011 Average Rating = 3 25

RESPONDENTS’ forecasts for additional funding have declined over the past three years

0%

10%

20%

30%

40%

50%

60%

8% 9%6%

28%30%

25%

33%

21%

56%

29%

37%

13%

2% 3%0%

25

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 4

B-to-C respondents are twice as likely to rate their departments’ effectiveness as “Average” than their B-to-B peers

Competitive Intelligence Effectiveness (By Business Model)

SURVEY QUESTION: How would you rate the performance or effectiveness of your function compared to others within your industry?

4Above Average

1Poor

5Exceptional

2Below Average

3Average

All Companies B‑to‑B Companies B‑to‑C Companies

2013 Average Rating = 3 122012 Average Rating = 3 22

26

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 4

0%

10%

20%

30%

40%

50%

32%

26%

46%

20% 20% 20%

16%

12%

20%

14%

21%

0%

6% 6% 7%

10%12%

7%

2% 3%

0%

Most CI departments report into Marketing

Direct Line Report of Competitive Intelligence (By Business Model)

SURVEY QUESTION: To which department does your competitive intelligence function directly report?

Corporate Strategy/Planning

Executive Management

(CEO/President/General Manager)

OtherMarketing Market Research R&D/Innovation and Product

Development

Sales/Business Development

All Companies B‑to‑B Companies B‑to‑C Companies

SINCE 2012, the percentage of CI departments reporting into Marketing has decreased by 10%, and the percentage reporting into Executive Management has doubled

27

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Special Interest Topic: Supporting Stakeholder Decision‑Making

SECTION

6

SECTION

5

SECTION

4

SECTION

3

SECTION

2

SECTION

1

INTRO

SECTION

5

28

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 5

Corporate Strategy/Planning (65%)

Marketing (74%)Sales/Business Development (78%)

Marketing (66%)

Sales/Business Development (47%)

Sales/Business Development (67%)

Corporate Strategy/Planning (50%)

Corporate Strategy/Planning (50%)

Marketing (63%)

Sales/Business Development accounts for most of the B-to-B respondents’ research portfolio, while Marketing is the primary client for B-to-C respondents

Top Three Clients (By Business Model)

B-to-C CompaniesAll Companies B-to-B Companies

SURVEY QUESTION: Please identify your top three internal clients (in terms of the percentage of your research portfolio they account for)

(100%) (80%) (60%) (40%) (20%) 0% 20% 40% 60% 80% 100%

67%61%

78%

50%(55%)

61%

(59%)(58%)

(61%)

(60%)(68%)

56%

(60%)(61%)

(61%)

(67%)(68%)

(67%)

29

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 5

SURVEY QUESTION: Which of the above activities does your department perform to support Marketing’s decision‑making (please check all that apply)?

Market assessments are a critical activity conducted for Marketing

Activities to Support Marketing (By Business Model)

Currently Conducting

Not Conducting *

* Percentages indicate the number of people not using this activity.

Voice of the Customer

Market Assessments

Pricing Research

Customer Satisfaction and Loyalty Research

Customer/Consumer Research

Branding, Messaging, and Marketing Communications

measuring successThe primary method used to measure impact on Marketing is: • All companies = Customer Satisfaction or Net Promoter Scores (33%)

• B-to-B companies = Customer Satisfaction or Net Promoter Scores (44%)

• B-to-C companies = Key Intelligence Topics (34%)

Survey Question: What metric(s) do you use to measure the impact of your department’s work for Marketing?

All Companies B‑to‑B Companies B‑to‑C Companies

(100%) (80%) (60%) (40%) (20%) 0% 20% 40% 60% 80% 100%

70%

69%

69%

60%

63%

57%

(57%)

(59%)

54%

(62%)

(59%)

(69%)

(79%)

(75%)

(85%)

30

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 5

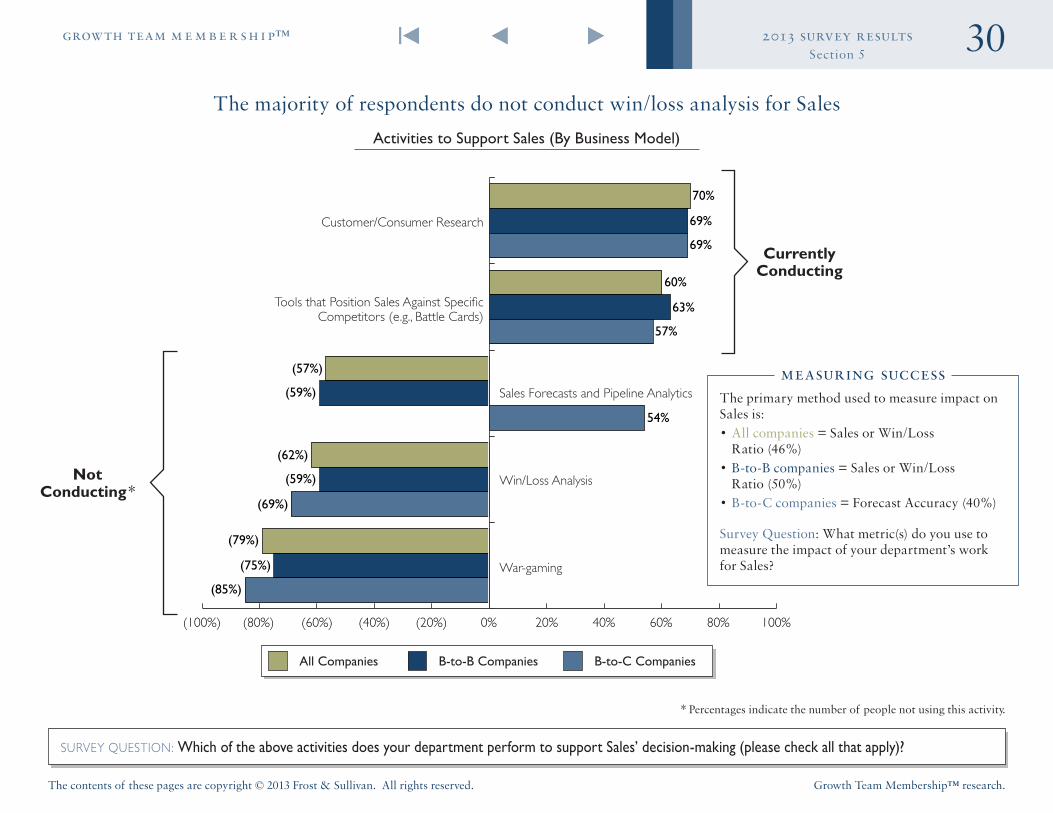

SURVEY QUESTION: Which of the above activities does your department perform to support Sales’ decision‑making (please check all that apply)?

The majority of respondents do not conduct win/loss analysis for Sales

Activities to Support Sales (By Business Model)

* Percentages indicate the number of people not using this activity.

War-gaming

Customer/Consumer Research

Tools that Position Sales Against Specific Competitors (e.g., Battle Cards)

Win/Loss Analysis

Sales Forecasts and Pipeline Analyticsmeasuring success

The primary method used to measure impact on Sales is: • All companies = Sales or Win/Loss Ratio (46%)

• B-to-B companies = Sales or Win/Loss Ratio (50%)

• B-to-C companies = Forecast Accuracy (40%)

Survey Question: What metric(s) do you use to measure the impact of your department’s work for Sales?

Currently Conducting

Not Conducting *

All Companies B‑to‑B Companies B‑to‑C Companies

(100%) (80%) (60%) (40%) (20%) 0% 20% 40% 60% 80% 100%

80%

82%

80%

53%

50%

60%

(62%)

(61%)

(60%)

(80%)

(76%)

(87%)

(84%)

(82%)

(87%)

31

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 5

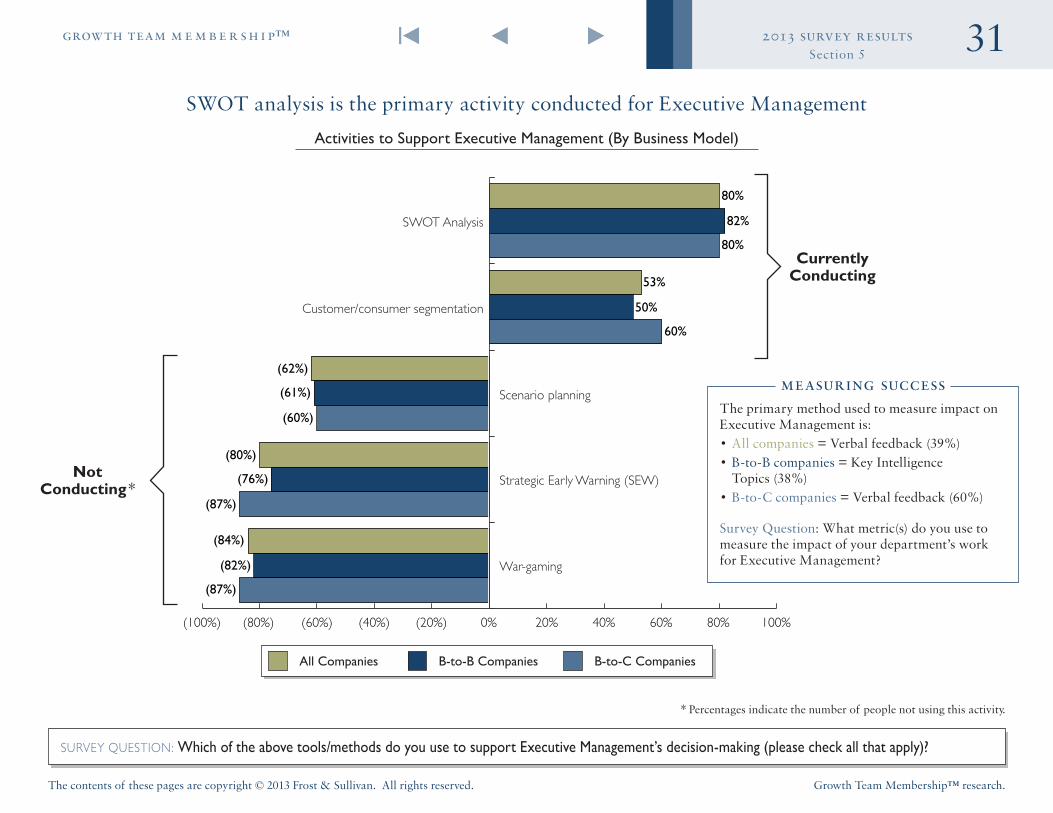

SURVEY QUESTION: Which of the above tools/methods do you use to support Executive Management’s decision‑making (please check all that apply)?

SWOT analysis is the primary activity conducted for Executive Management

Activities to Support Executive Management (By Business Model)

* Percentages indicate the number of people not using this activity.

War-gaming

SWOT Analysis

Customer/consumer segmentation

Strategic Early Warning (SEW)

Scenario planning

Currently Conducting

Not Conducting *

measuring successThe primary method used to measure impact on Executive Management is: • All companies = Verbal feedback (39%) • B-to-B companies = Key Intelligence Topics (38%)

• B-to-C companies = Verbal feedback (60%)

Survey Question: What metric(s) do you use to measure the impact of your department’s work for Executive Management?

All Companies B‑to‑B Companies B‑to‑C Companies

(100%) (80%) (60%) (40%) (20%) 0% 20% 40% 60% 80% 100%

74%

78%

64%

52%

(56%)

64%

(63%)

(58%)

(71%)

(84%)

(78%)

(100%)

(87%)

(86%)

(86%)

32

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 5

SURVEY QUESTION: Which of the above tools/methods do you use to support Corporate Strategy’s decision‑making (please check all that apply)?

SWOT analysis is the primary activity conducted for Corporate Strategy

Activities to Support Corporate Strategy (By Business Model)

* Percentages indicate the number of people not using this activity.

measuring successThe primary method used to measure impact on Corporate Strategy is: • All companies = Sales (40%) • B-to-B companies = Sales (50%) • B-to-C companies = Key Intelligence Topics (50%)

Survey Question: What metric(s) do you use to measure the impact of your department’s work for Corporate Strategy?

Currently Conducting

Not Conducting *

All Companies B‑to‑B Companies B‑to‑C Companies

War-gaming

SWOT Analysis

Customer/Consumer Segmentation

Strategic Early Warning (SEW)

Scenario Planning

(100%) (80%) (60%) (40%) (20%) 0% 20% 40% 60% 80% 100%

86%

86%

83%

57%

50%

67%

(51%)

(55%)

50%

(54%)

(68%)

67%

(66%)

(73%)

(58%)

33

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 5

SURVEY QUESTION: Which of the above activities do you conduct to contribute to Product Development’s decision‑making (please check all that apply)?

Most respondents provide front-end inputs (needs analysis and brand positioning) for Product Development

Activities to Support Product Development (By Business Model)

* Percentages indicate the number of people not using this activity.Note: The number of respondents who measure their support for product development, was not statistically significant enough for analysis.

Product Testing

Customer Needs Analysis

Brand Positioning

Post-launch Evaluations

Product Concept and Packaging Testing

Currently Conducting

Not Conducting *

All Companies B‑to‑B Companies B‑to‑C Companies

34

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

SECTION

6

SECTION

5

SECTION

4

SECTION

3

SECTION

2

SECTION

1

INTRO

SECTION

6 Respondent Demographics

35

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 6

Respondent Demographics

SURVEY QUESTION: Please indicate the type of enterprise, business model, and revenue that best represents your company

N = 88

N = 87N = 91

Enterprise Type Business Model

Company Revenue

41%

4%2%

6%1%

46%

25%

8% 67%

Public

Private

Hybrid

B-to-B Company

Venture CapitalGovernment/Public Sector

Not for Profit

0%

20%

40%

19%

6%

17%

9%

24% 25%

$50 Million to $99.99 Million

Below $50 Million

$100 Million to $499.99 Million

$500 Million to $999.99 Million

$1 Billion to $11 Billion

More than $11 Billion

B-to-C Company (Indirect)

B-to-C Company (Direct)

The majority of the respondents come from B‑to‑B companies

Most respondents are from Public companies

36

The contents of these pages are copyright © 2013 Frost & Sullivan. All rights reserved.

2013 survey resultsgrowth team m e m b e r s h i p ™

Growth Team Membership™ research.

Section 6

0%

10%

20%

30%

40%37%

31%

20%19%

18%

Chemicals, Materials, and Food

SURVEY QUESTION: Please indicate which industry categories best describe your company (check all that apply)

Respondent Demographics: Top Five Participating Industries

N = 85

Automotive and Transportation

Information and Communication

Technologies

Energy and Power Systems

Healthcare and Life Sciences