market watch npl the italian scenario july 2017 · 5 market watch npl // july 2017 11% 70% 9% 10%...

TRANSCRIPT

MARKET WATCH NPLThe Italian Scenario

July 2017

2

MARKET WATCH NPL // July 2017

Executive Summary.

NPL transactions on the Italian market>> pag 03

o NPL transactions on the market are about to explode in 2017; in addition to the deals already closed (33,1 Bn€), 70,9 Bn€ are expected to be released on the market during 2017

o The most important category is the one with mixed debtors (retail and corporate), also excluding Unicredit FINO deal; a trend that will continue during the whole 2017

o Portfolios with consumer loans represent the largest part (80%) of the retail category. The utility category is gaining a relevant importance

o Among corporate debtors, the trend is focusing on mixed portfolioso In 2017, domestic buyers are starting to show a strong interest for Italian non performing loanso The price levels show different trends for different categories: secured portfolios are experiencing a drop in price levels; on

the contrary, consumer portfolios are gaining higher prices in 2017o International buyers are equipping themselves through the acquisition of servicers’ platforms (from 2015, already 15

platforms bought) to better face the competition

NPL pipeline deep-dive>> pag 16

o 32,4 Bn€ are next to closing, out of the total pipeline volumes of 70,9 Bn€o The mixed-asset portfolios, which are about to be disposed during 2017, show relevant values: the deal of MPS (26 Bn€) will

have the largest impacto Pipeline confirms the buyers’ interest in secured dealso Regulatory variables are expected to shape future development of the NPL market. Especially the ECB guidelines will

positively impact both disposal and internal management strategies: the objective is to choose the optimal mix relative to each portfolio

Italian asset quality overview>> pag 21

o The GDP growth and the bankruptcies reduction as of the end of 2014 lead to a progressive stabilisation of Bad Loanso In Q1 2017, despite a slight increase of Gross Bad Loans, Net Bad Loans show a sharp reduction due to heavy writedownso The distribution analysis of Bad Loans shows how large customers are the main driver of the Bad Loans growth from 2009o The bad loans coverage index is stable on cyclical high values due to the heavy writedowns observed in January. Moreover,

there is still a relevant amount of Unlikely to Pay loans that could turn into Bad Loans in the next months

NPL TRANSACTIONSON THE ITALIANMARKET

4

MARKET WATCH NPL // July 2017

19,1 17,3

33,1

42

50

35

0

10

20

30

40

50

60

-

5.000,00

10.000,00

15.000,00

20.000,00

25.000,00

30.000,00

35.000,00

2015 2016 2017

Value (Bn €) Number of deals

Transactions are expected to grow exponentially reaching the massive amount of 104,0 Bn€.

*Unicredit retains a minority stake: 49% with the best effort to reduce its share // Sources: Banca IFIS NPL Market Database - Press releases and news

HIGHLIGHTS

o In Q2 2017 strong growth of the market with volumes that increased 192% with respect to Q1 2017; in addition Q3 shows the la rge deal (17,7 Bn€) of Unicredit FINO Project*

o In Q2 2017 the most important deals are:o The acquisition of 2,2 bn€ by Atlante II from the three new banks Etruria, Marche and Carichietio The mixed portfolio sold by Intesa Sanpaolo to CRC with a face value of 2,1 bn€o The portfolio sold by Unicredit to Sistemia, Yard and IT Auction mainly constituted of leasing loans

70,9

58

Expected value in H2 2017 Expected deals in H2 2017

104,0

5

MARKET WATCH NPL // July 2017

11%

70%

9%

10%

The growth of mixed-debtor portfolios is a trend that will continue throughout 2017.

*Unicredit retains a minority stake: 49% with the best effort to reduce its share // Sources: Banca IFIS NPL Market Database - Press releases and news

27%

1%

37%

35% 31%

1%45%

23%

UndisclosedRetail Corporate Mixed

Total 2015: 19,1 Bn€ Total 2016: 17,3 Bn€ YTD 2017: 33,1 Bn€ (o/w 17,7 FINO Project*)

HIGHLIGHTS

o In the first months of 2017, the most important category is the one with mixed debtors (retail and corporate) as opposed to 2016 transactions characterized by sole retail and sole corporate portfolios

o The mixed portfolio incidence in 2017 is relevant (33%) also excluding Unicredit FINO Project

6

MARKET WATCH NPL // July 2017

3%

84%

9%4%

2%

70%

28%

1%

Among retail debtors, consumer loan portfolios confirm the high importance in the market; in the meantime, the utility sector overperforms previous years’ volumes.

Sources: Banca IFIS NPL Market Database - Press releases and news

Consumer Banking - UnsecuredUtility Banking

Total 2015: 7,2 Bn€ Total 2016: 7,8 Bn€ YTD 2017: 3,1 Bn€

HIGHLIGHTS

o Portfolios with consumer loans represent the largest part (80%) of the retail category, after the light decrease observed in 2016o Utility portfolios are increasingly important in the market

11%

80%

9%

7

MARKET WATCH NPL // July 2017

19%

59%

1%5%

16%

54%

14%

9%

0%

23%

TOTAL 2015: 5,2 BN€

25%

60%

0% 8%

7%

TOTAL 2016: 5,4 BN€

Among corporate debtors, mixed-asset portfolios are polarizing the volumes in the 2017 market.

Sources: Banca IFIS NPL Market Database - Press releases and news

Total 2015: 5,2 Bn€ Total 2016: 5,4 Bn€ YTD 2017: 3,6 Bn€

HIGHLIGHTS

o In 2017, the trend is shifting again concentrating on mixed portfolios, in contrast to 2015

SecuredMixedUnsecured Secured - CRE Secured - Residential Undisclosed

8

MARKET WATCH NPL // July 2017

5,0

2,5

2,5

2,1

1,5

Fortress; PIMCO

Quaestio Capital ManagementSgr

Banca IFIS

Christofferson Robb; Bayview;Prelios

Sistemia; Yard; IT Auction

In 2017, in contrast to the previous years, domestic buyers are starting to show a strong interest for Italian NPLs.

*Unicredit retains a minority stake: 49% with the best effort to reduce its share // Sources: Banca IFIS NPL Market Database - Press releases and news

3,7

2,4

2,0

1,7

1,3

Banca IFIS

Fortress; Prelios

D.E. Shaw

Deutsche Bank

Banca IFIS; Cerberus

3,0

2,9

2,1

1,2

1,0

Banca IFIS

Anacap

Kruk Group

FBS

Hoist Finance

# 10 deals

# 1 deal

# 1 deal

# 1 deal

# 1 deal

# 13 deals

# 2 deals

# 4 deals

# 1 deal

# 2 deals

# 8 deals

# 2 deals

# 1 deal

# 1 deal

58,1% on the total 59,0% on the total 79,8% on the total

Top 5 buyers 2015 (Bn€) Top 5 buyers 2016 (Bn€) Top 5 buyers 2017 (Bn€)

HIGHLIGHTS

o Despite the huge interest shown by international buyers in 2015 and 2016, in 2017 domestic buyers are showing an increasing commitment to the Italian market: 61% of the deals are in domestic buyers’ portfolios (net of FINO Project)

# 1 deal

17,7*

9

MARKET WATCH NPL // July 2017

4,7

3,0

1,2

0,4

0,4

1,9

0,3

0,8

0,4

0,5

0,4

0,3

0,7

8,2

0,3

1,3

2,2

1,3

2,1

1,5

0,5

Unicredit

Monte dei Paschi di Siena

Gruppo Banco BPM

Nuova Banca Etruria; Nuova Banche Marche; Nuova CariChieti

Gruppo BNP Paribas

Intesa Sanpaolo

Creval

Deutsche Bank

Cassa Centrale Banca

Iccrea Banca

2015 2016 2017

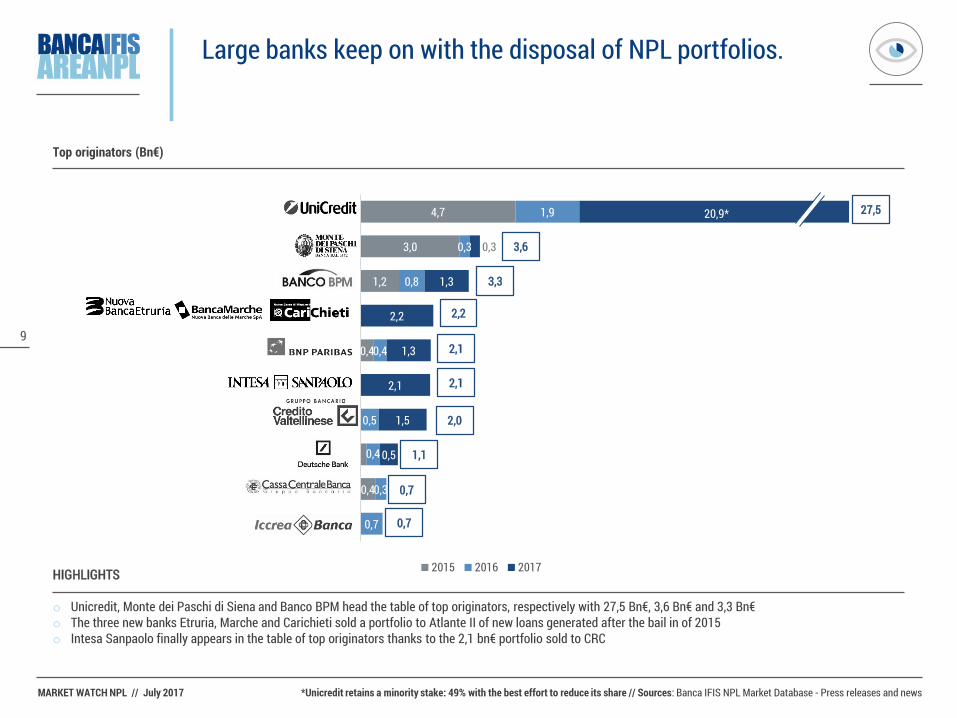

Large banks keep on with the disposal of NPL portfolios.

*Unicredit retains a minority stake: 49% with the best effort to reduce its share // Sources: Banca IFIS NPL Market Database - Press releases and news

27,5

3,6

3,3

2,2

2,1

2,1

2,0

1,1

0,7

Top originators (Bn€)

HIGHLIGHTS

o Unicredit, Monte dei Paschi di Siena and Banco BPM head the table of top originators, respectively with 27,5 Bn€, 3,6 Bn€ and 3,3 Bn€o The three new banks Etruria, Marche and Carichieti sold a portfolio to Atlante II of new loans generated after the bail in of 2015 o Intesa Sanpaolo finally appears in the table of top originators thanks to the 2,1 bn€ portfolio sold to CRC

0,7

20,9*

10

MARKET WATCH NPL // July 2017

Transactions in the NPL market are pushing the securitization trend up.

Sources: Banca d’Italia, last update June 2017

25

30

35

40

45

50

55

60

65

70

75

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Q42016

Q12017

72,4

31,0

Amounts (Bn€)

HIGHLIGHTS

o The growth of Bad Loan securitization reaches a new peak in Q1 2017: the amount increased by 134% since 2012.

11

MARKET WATCH NPL // July 2017

0%3%5%8%

10%13%15%18%20%23%25%28%30%33%35%38%40%43%45%48%

Q2 16 Q3 16 Q4 16 Q1 17 Q2 17 Q3 17

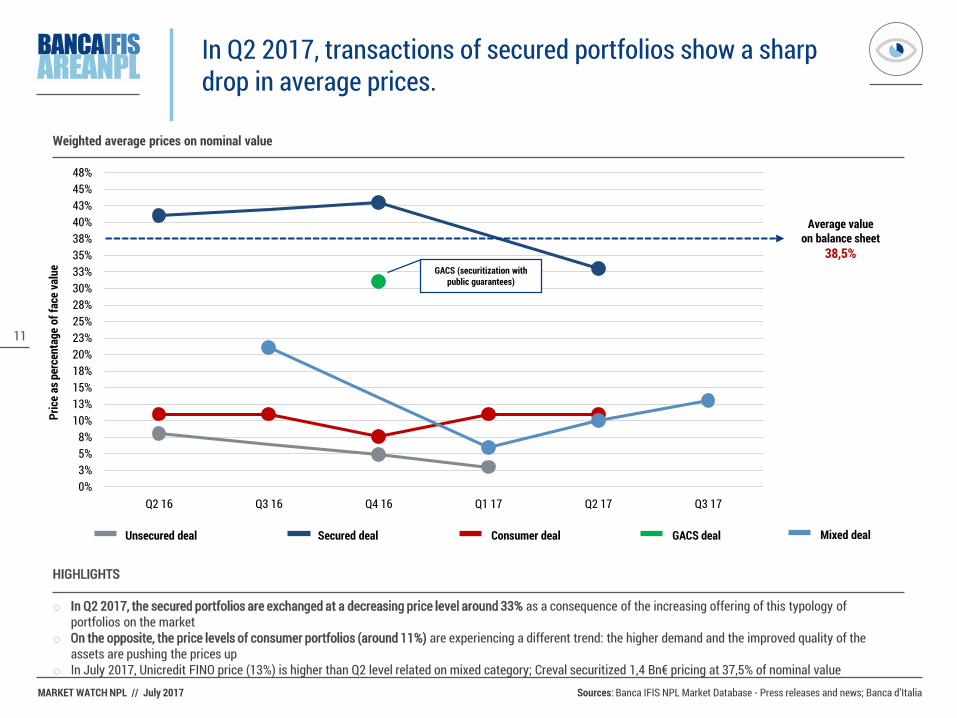

In Q2 2017, transactions of secured portfolios show a sharp drop in average prices.

Sources: Banca IFIS NPL Market Database - Press releases and news; Banca d’Italia

GACS (securitization with public guarantees)

Pric

e as

per

cent

age

of fa

ce v

alue

Average value on balance sheet

38,5%

Consumer dealUnsecured deal Secured deal GACS deal

HIGHLIGHTS

o In Q2 2017, the secured portfolios are exchanged at a decreasing price level around 33% as a consequence of the increasing offering of this typology of portfolios on the market

o On the opposite, the price levels of consumer portfolios (around 11%) are experiencing a different trend: the higher demand and the improved quality of the assets are pushing the prices up

o In July 2017, Unicredit FINO price (13%) is higher than Q2 level related on mixed category; Creval securitized 1,4 Bn€ pricing at 37,5% of nominal value

Mixed deal

Weighted average prices on nominal value

12

MARKET WATCH NPL // July 2017

1,0

0,3

0,3

0,2

0,2

Unicredit

Findomestic Banca

Provis (Intesa Sanpaolo)

Barclays

Santander Consumer…

Originator

1,0

0,8

0,3

0,1

0,1

MBCredit Solution (ex…

Banca IFIS

Credito Fondiario

Kruk Group

LCM Partners

Buyer

Consumer transactions - Stable volumes and increasing price levels; Italian buyers show a strong interest while Unicredit is the top originator in 2017.

Banca IFIS NPL Market Database - Press releases and news

Market trend

Price levels(Primarymarket)

Top buyers and

originatorsin 2017

Size = Number of deals (#)

1217

13

17

,0

2,0

4,0

6,0

8,0

Face

Val

ue (B

n€)

2015 2016 2017 2017 (with pipeline)

4%

10% 11%

2015 2016 2017

Data are in Bn€

13

MARKET WATCH NPL // July 2017

1,0

0,6

BNL BnpParibas

Banco BPM

Originator

1,3

0,6

Banca IFIS

Hoist Finance

Buyer

Banking unsecured transactions – Volumes are expected to increase consistently in 2017 with decreasing price levels.

Banca IFIS NPL Market Database - Press releases and news

Market trend

Price levels(Primarymarket)

Top buyers and

originatorsin 2017

97

3

8

,0

2,0

4,0

6,0

8,0

10,0

Face

Val

ue (B

n€)

2015 2016 2017 2017 (with pipeline)

Size = Number of deals (#)

7%

3%

2015 2016 2017

Data are in Bn€

14

MARKET WATCH NPL // July 2017

2,2

1,5

0,7

0,4

0,2

Nuova Banca Etruria;…

Unicredit

Banco BPM

Banca Mediocredito…

Barclays

Originator 2,2

1,5

0,7

0,4

0,2

Quaestio Capital…

Sistemia; Yard; IT…

Algebris

Bain Capital Credit

Anacap

Buyer

Banking secured transactions – Volumes are expected to soar in 2017 and prices are dropping, as a consequence of the high supply.

Banca IFIS NPL Market Database - Press releases and news

Size = Number of deals (#)

Market trend

Price levels(Primarymarket)

Top buyers and

originatorsin 2017

6

45

11

-2,0

,0

2,0

4,0

6,0

8,0

10,0

Face

Val

ue (B

n€)

2015 2016 2017 2017 (with pipeline)

41% 42%

33%

2015 2016 2017

Data are in Bn€

15

MARKET WATCH NPL // July 2017

International buyers are equipping themselves through the acquisition of servicers’ platforms to better face the competition.

Banca IFIS NPL Market Database - Press releases and news

2016

Acquisition of CrossFactor(AuM 2 Bn€)

Acquisition of NonPerforming Loans SpA

(AuM 1 Bn€)

Acquisition of Centaurus Credit Recovery (AuM 0,7 Bn€)

Acquisition of CS Union (AuM 0,2 Bn€)

Acquisition of Italfondiario(AuM 41,5 Bn€) from

Fortress

Acquisition of SPC Credit Management

Acquisition of Credit Base International

Acquisition of Zenith Service (AuM 14,1 Bn€)

2017

Acquisition of Heta Asset Resolutions (AuM 0,6 Bn€)

Acquisition of 33% of Guber (AuM 12,6 Bn€)

Acquisition of Sistemia(AuM 4,6 Bn€)

Acquisition of Gextra(AuM 0,6 Bn€)

2015

Acquisition of UCCMB (AuM 2,4 Bn€) from

Unicredit

Acquisition of CAF (AuM 7,8 Bn€)

Acquisition of FinanziariaSan Giacomo from CreVal

NPL PIPELINE DEEP-DIVE

17

MARKET WATCH NPL // July 2017

70,9 Bn€ are expected to be released on the market in 2017; 32,4 Bn€ are next to closing.

Sources: Banca IFIS NPL Market Database - Press releases and news

HIGHLIGHTS

o Unicredit has just released on the market 17,7 Bn€: Fortress and PIMCO have acquired 51% of the shares, while Unicredit will keep ownership of the remaining (disclosed the goal to reduce the share)

o Monte dei Paschi di Siena’s sole investor in the securitization of 26 Bn€ will be Atlante II after Fortress withdrew its offer because of the high priceo Rev Gestione Crediti is expected to release the first portfolio of 1 Bn€ with the project Rossini

Status Seller Nominal value (Bn€)Ongoing 32,4

Monte dei Paschi di Siena 26,0 Confidential 3,6

Caricesena; Carim; Carismi 2,8 Announced 20,5

Banca Popolare di Vicenza 5,2 Veneto Banca 5,0

Monte dei Paschi di Siena 2,5 Gruppo Delta 2,0

Intesa Sanpaolo 1,5 Carige 1,2

REV Gestione Crediti 1,0 Hypo Alpe Adria Bank 0,8 Cassa Centrale Banca 0,6

Iccrea Banca 0,5 Banca Popolare di Bari 0,3

On plan 18,0 REV Gestione Crediti 9,3

Unipol 3,7 Unicredit 3,0

Banco BPM 2,0

Grand total 70,9

18

MARKET WATCH NPL // July 2017

The mixed-asset portfolios, which are about to be disposed during 2017, show relevant values.

Sources: Banca IFIS NPL Market Database - Press releases and news

N.a.

28,5 Bn€

20,5%

Securitization of 26 Bn€ with Atlante II acting as sole buyer of mezzanine and junior tranches. An unsecured portfolio of 1,5/2 Bn€ will be disposed by Dec 2017

Seller

Project Name

Nominal Value

Price

Portfolio details

N.a.

10,2 Bn€

N.a.

The total value of NPE (around16 Bn€) will be managed by SGA with the support of the Italian Government

Seller

Project Name

Nominal Value

Price

Portfolio details

19

MARKET WATCH NPL // July 2017

Pipeline confirms the buyers’ interest in secured deals.

Sources: Banca IFIS NPL Market Database - Press releases and news

REP

1,5 Bn€

70

50% Corporate/Residential

REV Gestione Crediti

Rossini

1,0 Bn€

78

35% Residential, 10% Industrial, 8,5% CRE, 8%

Hotels, 38,5% mixed Real estate

Seller

Project Name

Nominal Value

Number of loans

Portfolio details

Seller

Project Name

Nominal Value

Number of loans

Portfolio details

Terzo

750 M€

-

84% Real Estate

Seller

Project Name

Nominal Value

Number of loans

Portfolio details

Buonconsiglio

560 M€

10

85% real estate (mixed CRE and Residential)

Seller

Project Name

Nominal Value

Number of loans

Portfolio details

20

MARKET WATCH NPL // July 2017

Regulatory variables expected to shape the future development of the NPL market

Disposal Internal Management Comments

February 2016: GACS are established (first time used in August 2016)

+ -The possibility of selling NPL portfolio backed by public guarantees is likely to ease the transaction with buyers (e.g. the cases of Banca Monte dei Paschi di Siena and Banca Carige)

April 2016: Atlante I Fund is established + +

Due to the hybrid nature of the Fund (70% in banks recapitalizations, 30% in NPL purchase), sales of NPLs are expected to increase but at the same time banks are empowered to internally manage these exposures because of higher capital endowment. In turn, higher capital availability could allow banks to undertake heavier write-downs to ease NPL disposal

June 2016: the II Reform of the Bankrupcy Law is enacted - + Guarantees expropriation processes are simplified and sped up, thus becoming less risky for banks to internally

manage non performing exposures

August 2016: Atlante II Fund is established + - The Fund was created to invest in financial instruments issued by NPL securitization vehicles

March 2017: ECB Guidelines + +The ECB guidelines implication is dual:• Higher NPL disposal to meet the reduction objectives• Selection of the best recovery strategies tailored to each NPL portfolio categories (both through internal

departments and outsourcing)

June 2017: Reform of the Securitization Law (Article 7.1) + -

The introduction of the new article 7.1 has the objective to ease the disposal of NPLs improving the action of SPV 130, in case of recovery situations or resulting from leasing contracts. The reform operates on several directions: possibility to concede loans; possibility to sign for equity or other instruments in case of recovery or restructuring situations; possibility to set SPV corporations (ReoCo) to purchase and manage assets securing securitized receivables (including assets object of leasing contracts); improved information to be given in case of disposal to an SPV that are not identifiable as a pool (“in blocco”)

July 2017: Ecofin approves a plan to handle bad loans + - Agreement on the creation of national “bad banks” or “asset management companies” in order to push up the prices

End of 2017: Accelerated loan security project + - European Commission launches a public survey in order to ease the development of a secondary market to avoid

negative effects of increasing levels of NPL

January 2018: IFRS 9 +/- +/-

• On the one hand, the adoption of a “forward-looking” approach in the exposures valuation could lead a share of loans previously judged as performing to be considered as non performing in order to anticipate losses at the first signals of deterioration

• On the other hand, the increase of new Bad Loans could be restrained upstream by the impact of the IFRS 9 adoption of banks’ internal processes such as stricter selection of borrowers through the “forward-looking approach”, establishment of Early Warning signals and adoption of pre-collection and collection processes aimed at setting up corrective actions

Sources: PWC, UNIREC, AIFIRM; DLA Piper

ITALIAN ASSET QUALITY OVERVIEW

22

MARKET WATCH NPL // July 2017

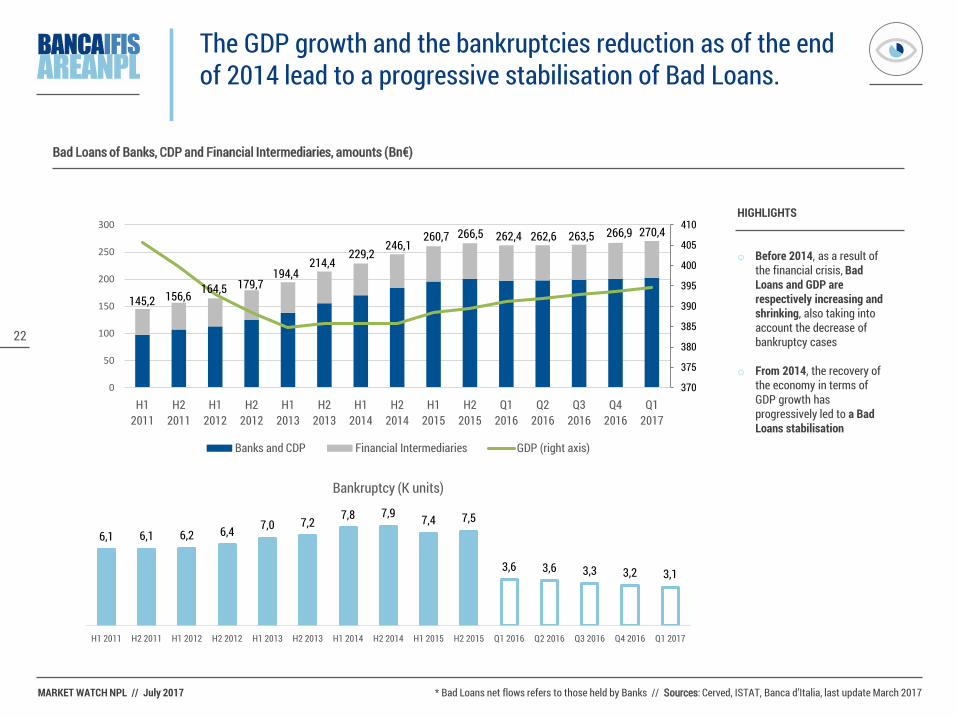

The GDP growth and the bankruptcies reduction as of the end of 2014 lead to a progressive stabilisation of Bad Loans.

* Bad Loans net flows refers to those held by Banks // Sources: Cerved, ISTAT, Banca d’Italia, last update March 2017

370

375

380

385

390

395

400

405

410

0

50

100

150

200

250

300

H12011

H22011

H12012

H22012

H12013

H22013

H12014

H22014

H12015

H22015

Q12016

Q22016

Q32016

Q42016

Q12017

Banks and CDP Financial Intermediaries GDP (right axis)

HIGHLIGHTS

o Before 2014, as a result of the financial crisis, Bad Loans and GDP are respectively increasing and shrinking, also taking into account the decrease of bankruptcy cases

o From 2014, the recovery of the economy in terms of GDP growth has progressively led to a Bad Loans stabilisation

Bad Loans of Banks, CDP and Financial Intermediaries, amounts (Bn€)

6,1 6,1 6,2 6,4 7,0 7,2 7,8 7,9 7,4 7,5

3,6 3,6 3,3 3,2 3,1

H1 2011 H2 2011 H1 2012 H2 2012 H1 2013 H2 2013 H1 2014 H2 2014 H1 2015 H2 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017

Bankruptcy (K units)

270,4

145,2 156,6 164,5 179,7194,4

214,4229,2

246,1260,7 266,5 262,4 262,6 263,5 266,9

23

MARKET WATCH NPL // July 2017

In Q1 2017, despite a slight increase of Gross Bad Loans, Net Bad Loans show a sharp reduction due to heavy writedowns.

* Bad Loans net flows refers to those held by Banks // Sources: Banca d’Italia, last update March 2017

0

50

100

150

200

250

H12011

H22011

H12012

H22012

H12013

H22013

H12014

H22014

H12015

H22015

Q12016

Q22016

Q32016

Q42016

Q12017

Gross Bad Loans Net Bad Loans

HIGHLIGHTS

o In the period, Gross Bad Loans have increased by 108%

o The analysis of the ratio between Net Bad Loans and Total Assets shows a drop with a value around 4,3%

o After a constant growth from H1 2011, the weight of Gross Bad Loans on the total assets has settled around 11% from H1 2014

Banks and CDP, amounts (Bn€)

5,0% 5,5% 5,9%6,5%

7,4%8,5%

9,3%10,1% 10,7% 11,0% 10,8% 10,9% 11,0% 11,14% 11,22%

2,3% 2,… 2,8%3,4% 3,8% 4,3% 4,2%

4,6% 4,6% 4,9% 4,6% 4,6% 4,7% 4,8% 4,3%

H1 2011 H2 2011 H1 2012 H2 2012 H1 2013 H2 2013 H1 2014 H2 2013 H1 2014 H2 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017

Gross Bad Loans/Total Assets Net Bad Loans/Total Assets

200,8198,9197,9197,0200,7195,8183,7

170,4155,9138,2

125,0113,1107,297,7

202,8

86,885,283,783,188,584,284,577,080,070,664,854,351,744,8

77,8

24

MARKET WATCH NPL // July 2017

The volume of transactions exceeded the new bad loan growth in Q1 2017.

Banca IFIS NPL Market Database - Press releases and news , Banca d’Italia, last update March 2017

Bad Loans held by Banks & Financial Intermediaries, Amount and flows (Bn€)

32,6

8,512,2

3,4

11,5

232,8

2014 Q1 2017

1,3255,5

257,6

2015

253,9

2016

Retail: 3,6 Bn€ (31,3%)Corporate: 4,3 Bn€ (37,7%)

Retail: 4,0 Bn€ (46,7%)Corporate: 2,9 Bn€ (34,0%)

Retail: 0,7 Bn€ (20,6%)Corporate: 0,2 Bn€ (5,9%)

Retail: 40,4 Bn€ (17,3%)

Corporate: 185,3 Bn€ (79,6%)

Retail: 44,6 Bn€ (17,5%)

Corporate: 204,1 Bn€ (79,9%)

Bad loans Transactions New bad loans

25

MARKET WATCH NPL // July 2017

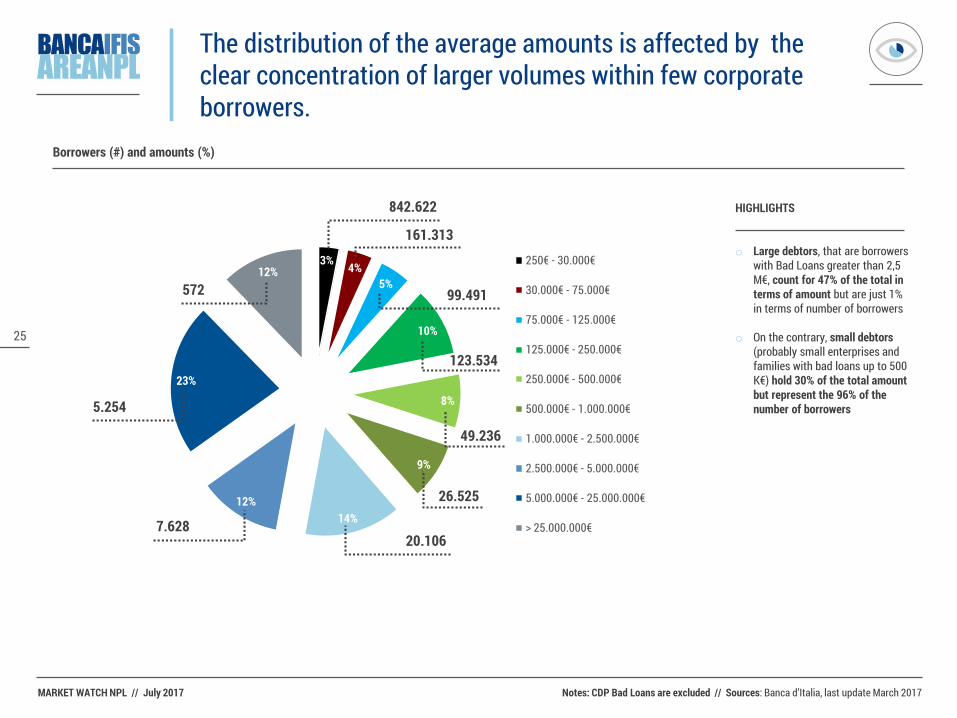

The distribution of the average amounts is affected by the clear concentration of larger volumes within few corporate borrowers.

Notes: CDP Bad Loans are excluded // Sources: Banca d’Italia, last update March 2017

3% 4%5%

10%

8%

9%

14%12%

23%

12%250€ - 30.000€

30.000€ - 75.000€

75.000€ - 125.000€

125.000€ - 250.000€

250.000€ - 500.000€

500.000€ - 1.000.000€

1.000.000€ - 2.500.000€

2.500.000€ - 5.000.000€

5.000.000€ - 25.000.000€

> 25.000.000€

572

5.254

7.62820.106

26.525

49.236

123.534

99.491

161.313

842.622

Borrowers (#) and amounts (%)

HIGHLIGHTS

o Large debtors, that are borrowers with Bad Loans greater than 2,5 M€, count for 47% of the total in terms of amount but are just 1% in terms of number of borrowers

o On the contrary, small debtors (probably small enterprises and families with bad loans up to 500 K€) hold 30% of the total amount but represent the 96% of the number of borrowers

26

MARKET WATCH NPL // July 2017

Large customers are the main driver behind Bad Loans growth from 2009.

Notes: CDP Bad Loans are excluded // Sources: Banca d’Italia, last update March 2017

Size-class (€), amounts (Bn€)

HIGHLIGHTS

o The financial crisis resulted in pronounced differences between higher and lower size-classes

o The «large customers» pushed Bad Loans growth in Italy both in terms of % growth (536%) and in terms of weight on total (+16 percentage points)

Q1 2009 Q4 2013 Q1 2017

More than 2.500.000

From 250.000 to 2.500.000

From 250 to 250.000

Amount: +536%% on total: +16,0pp

Growth % Q1 2009 – Q1 2017

Amount: +263%% on total: -4,6pp

Amount: +175%% on total: -11,4pp

186,4

148,9

44,6

47,0%

31,0%

22,0%

44,5%

30,0%

25,5%

31,0%

35,6%

33,4%

27

MARKET WATCH NPL // July 2017

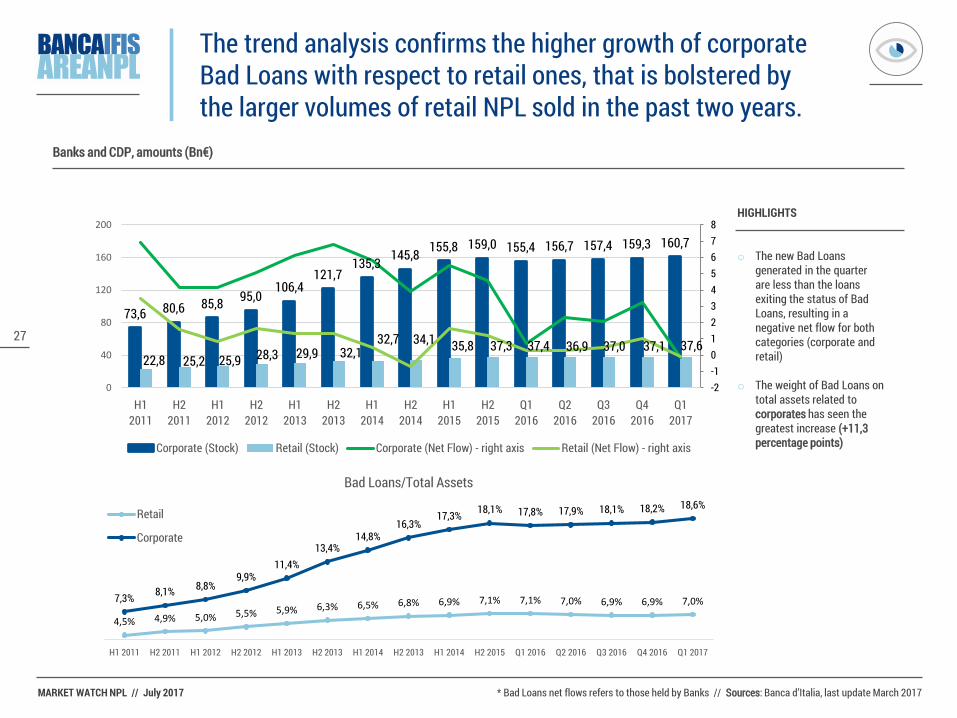

The trend analysis confirms the higher growth of corporate Bad Loans with respect to retail ones, that is bolstered by the larger volumes of retail NPL sold in the past two years.

* Bad Loans net flows refers to those held by Banks // Sources: Banca d’Italia, last update March 2017

HIGHLIGHTS

o The new Bad Loans generated in the quarter are less than the loans exiting the status of Bad Loans, resulting in a negative net flow for both categories (corporate and retail)

o The weight of Bad Loans on total assets related to corporates has seen the greatest increase (+11,3 percentage points)

4,5% 4,9% 5,0% 5,5% 5,9% 6,3% 6,5% 6,8% 6,9% 7,1% 7,1% 7,0% 6,9% 6,9% 7,0%7,3% 8,1% 8,8%9,9%

11,4%13,4%

14,8%16,3%

17,3% 18,1% 17,8% 17,9% 18,1% 18,2% 18,6%

H1 2011 H2 2011 H1 2012 H2 2012 H1 2013 H2 2013 H1 2014 H2 2013 H1 2014 H2 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017

Bad Loans/Total Assets

Retail

Corporate

Banks and CDP, amounts (Bn€)

73,6 80,6 85,8 95,0106,4

121,7135,3 145,8 155,8 159,0 155,4 156,7 157,4 159,3 160,7

22,8 25,2 25,9 28,3 29,9 32,132,7 34,1 35,8 37,3 37,4 36,9 37,0 37,1 37,6

-2-1012345678

0

40

80

120

160

200

H12011

H22011

H12012

H22012

H12013

H22013

H12014

H22014

H12015

H22015

Q12016

Q22016

Q32016

Q42016

Q12017

Corporate (Stock) Retail (Stock) Corporate (Net Flow) - right axis Retail (Net Flow) - right axis

28

MARKET WATCH NPL // July 2017

The deep-dive on the industry split highlights the role of the “Construction” sector as the main driver behind Bad Loans growth in the last seven years.

*The Q1 2009 detail of the total assets related to each ATECO code is not available // Sources: Banca d’Italia, last update March 2017

Industry (ATECO Code)

Construction

Manufacturing

Wholesale/retail trade

Real estate

Agriculture

Accomodation and Ho.Re.Ca.

Transportation and storage

Professional and scientific act.

Administrative and support serv.

Information and communication

Q1 2009

Bn€ % on tot. NPL

% on Assets*

6,7 15,0% n.a.

10,7 23,9% n.a.

6,3 14,1% n.a.

2,7 6,1% n.a.

1,8 4,1% n.a.

1,3 3,0% n.a.

1,0 2,2% n.a.

0,7 1,6% n.a.

0,8 1,8% n.a.

0,6 1,3% n.a.

30,7 19,7% 19,2%

30,0 19,2% 14,5%

20,7 13,3% 15,0%

12,4 8,0% 10,4%

4,7 3,0% 10,7%

4,4 2,8% 11,70%

3,4 2,2% 8,5%

2,4 1,5% 5,9%

2,7 1,7% 13,3%

1,7 1,1% 10,5%

42,1 26,2% 31,7%

29,9 18,6% 14,4%

24,9 15,5% 17,3%

24,8 15,4% 21,7%

6,0 3,7% 13,9%

5,7 3,5% 15,7%

3,5 2,2% 10,1%

3,7 2,3% 8,8%

3,5 2,2% 17,2%

1,6 1,0% 9,2%

Q4 2013

Bn€ % on tot. NPL

% on Assets

Q1 2017

Bn€ % on tot. NPL

% on Assets

HIGHLIGHTS

o The top 4 industries (Construction, Manufacturing, Wholesale/Retail Trade, Real Estate) contribute to the 75,7% of the total NPL

29

MARKET WATCH NPL // July 2017

The Bad Loans concentrated in Southern Italy, although low in terms of stock, highlight a heavier credit deterioration when compared with the Region’s total assets.

* Bad Loans net flows refers to those held by Banks // Sources: Banca d’Italia, last update March 2017

HIGHLIGHTS

o The Bad Loans concentrated in Northern Italy grew by 125,3%in the period being reviewed

o Even though the Bad Loans stick to high stock in Northern Italy, in the early 2017 the net flows show negative values

o The ratios between Bad Loans and Assets keep on increasing for all regions

4,3% 4,7% 5,1% 5,6% 6,4%7,3% 8,1% 8,8% 9,4% 9,8% 9,9% 9,9% 10,0% 10,3% 10,9%

4,4% 4,9% 5,1% 5,6% 6,3%7,3% 7,9% 7,9% 8,3% 8,6% 8,0% 8,2% 8,5% 8,6% 8,9%

8,2% 8,9% 9,3%10,4% 11,1%

12,4%13,4% 13,7% 14,3% 15,1% 15,1% 15,2% 15,3% 15,5% 16,3%

H1 2011 H2 2011 H1 2012 H2 2012 H1 2013 H2 2013 H1 2014 H2 2013 H1 2014 H2 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017

Bad Loans/Total AssetsNorthern Italy

Central Italy

Southern Italy

Banks, amounts (Bn€)

-2-10123456

0

20

40

60

80

100

120

Northern Italy (Stock) Central Italy (Stock)

Southern Italy and Islands (Stock) Northern Italy (Net Flow) - right axis

Central Italy (Net Flow) - right axis Southern Italy and Islands (Net Flow) - right axis

30

MARKET WATCH NPL // July 2017

Large writedowns on balance sheet and the relevant amount of Unlikely to Pay loans could support the growth of NPL transactions.

Sources: Banca d’Italia, last update March 2017

Bad Loans Coverage (%)

53%

55%

56%

58%

59%

61%

62%

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Jan2016

Feb2016

Mar2016

Apr2016

May2016

Jun2016

Jul2016

Aug2016

Sept2016

Oct2016

Nov2016

Dec2016

Jan2017

Feb2017

Mar2017

61,75%

54,0%

HIGHLIGHTS

o The coverage index, despite a light decrease in March, is stable on cyclical high values after the huge leap observed in January

o The larger writedowns in early 2017 will potentially foster the future development of NPL transactions because of the narrower demand-supply gap

o Although the trend is decreasing, there is still a relevant amount of non performing exposures that could turn into Bad Loans in the next months

o There is wide room for growth suggested by writedownsincrease and size of the amount of Unlikely to Pay loans

0

20

40

60

80

100

120

140

160

H12010

H22010

H12011

H22011

H12012

H22012

H12013

H22013

H12014

H22014

H12015

H22015

Q12016

Q22016

Q32016

Q42016

Q12017

Past Due Unlikely to Pay Watchlist Restructured

Classification of Impaired Loans updated in 2015

31

MARKET WATCH NPL // July 2017 Sources: Banca IFIS NPL Market Database - Press releases and news

General statement

This publication is edited by Banca IFIS.The information contained herein, obtained from sources believed to be reliable by Banca IFIS,

are not necessarily complete, and their accuracy cannot be guaranteed.This publication is provided merely for purposes of illustration and information and

does not in any way represent financial and investment advice.