marketing x finance = product with high return and low risk profile joost m.e. pennings professor of...

TRANSCRIPT

Marketing X Finance = Product

with High Return and Low Risk Profile

Joost M.E. Pennings

Professor of Marketing

ALEX Beleggersbank Professor in Finance

Faculty of Economics and Business Administration

Marketing-Finance Interface: New Frontiers

1. Financial Product Development

2. Channel Relationships & Financial Derivatives

3. Shareholder Activism & Marketing

4. Market Sentiment

5. Interdepartmental MF Integration

Faculty of Economics and Business Administration

• Financial Product Development:

– $630 trillion derivatives traded

– Fierce competition

– Low new product success rate

Marketing-Finance Interface: New Frontiers

Faculty of Economics and Business Administration

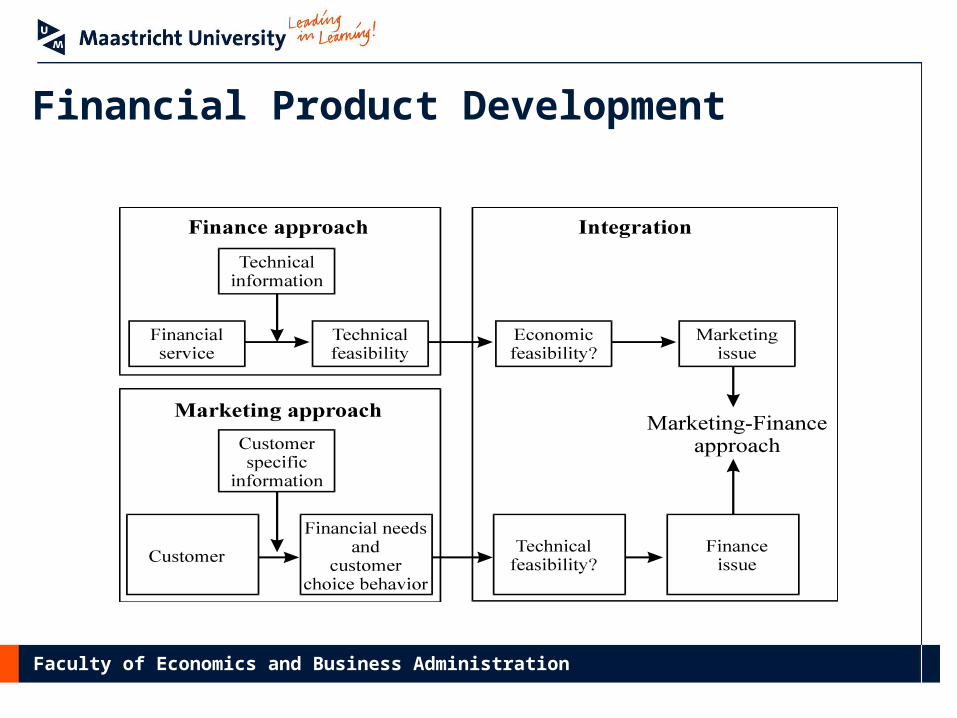

Financial Product Development

Faculty of Economics and Business Administration

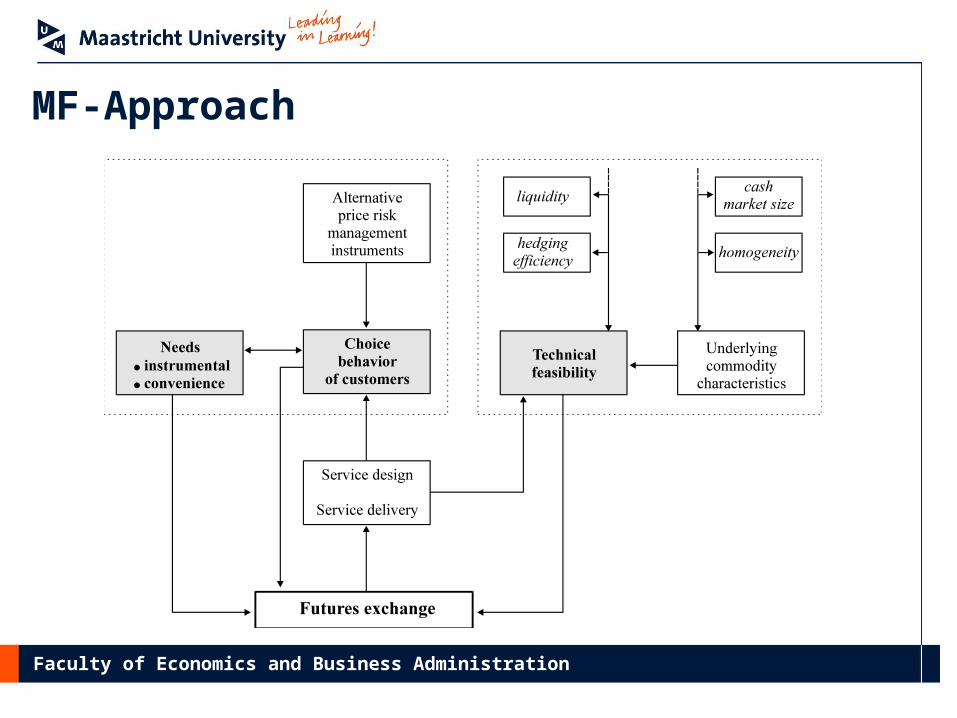

MF-Approach

Faculty of Economics and Business Administration

Financial Product Development: Challenges-Future Research

• How can we translate customer needs into concrete attributes that are technical feasible?

• Research methodology– Marketing-finance approach

• Attributes of financial product– Marketing approach conjoint approach

– Finance approach objective measure e.g., hedging effectiveness

Faculty of Economics and Business Administration

Financial Product Development: Challenges-Future Research

• New tools are needed that:

– Can transform customers’ preferences in concrete attributes AND………….

– are able to take the technical constraints into account simultaneously

Hence operationalize the MF approach toward product development

Faculty of Economics and Business Administration

Financial Product Development: Challenges-Future Research

• Research methodology– Marketing-finance approach

• (Mis)-match subjective vs. objective performance

• Current case study:– Dairy futures

Faculty of Economics and Business Administration

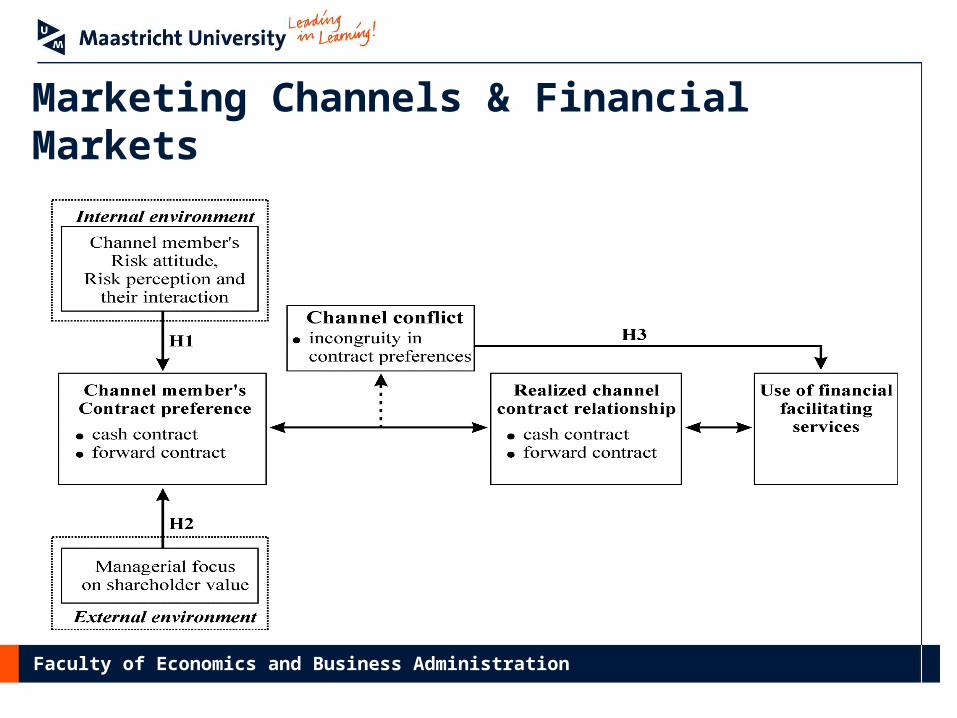

Channel Relationships & Financial Derivatives

• Channel contract preferences differ– Driven by risk attitudes, capital structure etc.

Conflicts and unable to meet financial performance targets in terms of risk (volatility)

– expected cash flow (return) trade offs.

Faculty of Economics and Business Administration

Marketing Channels & Financial Markets

Faculty of Economics and Business Administration

Channel Relationships & Financial Derivatives

• Role of Financial Markets:

– May complement cash flow stream from internal channel relation with external third part financial service, if………….

– How should we organize or marketing activities and financial product design to accomplish this?

Faculty of Economics and Business Administration

Channel relationships & financial derivatives

• Marketing: Behavioral & cash flow characteristics of “relationships”

– How does “Trust”, “Power” influence cash flow structures?

• Finance: what are the attributes of financial products that can complement cash flow structure of relations?

– Hedging effectiveness– Market micro structure (liquidity)– Complete markets (arbitrage; marketing relationships and

financial products)

Faculty of Economics and Business Administration

Shareholder Activism

• “Upheaval at VNU is yet another example of increasing shareholder activism in Europe.” (The Economist April 6th 2006)

• “Activist shareholders are getting tough with boards and managers.” (The Economist May 31st 2007)

• “Investors are making life uncomfortable for boards in America.” (The Economist May 31st 2007)

• “Keeping shareholders in their place: Bosses around the world celebrate a series of victories over activist shareholders.” (The Economist October 11th 2007)

Faculty of Economics and Business Administration

Shareholder Activism

• Questions from the Industry:

– Why do shareholders become active?

– What is the impact of shareholder activism?

– How can we improve Investor Relations (IR)?

– Who is leading in IR: Finance or Marketing?

Faculty of Economics and Business Administration

Shareholder Activism

• Research questions:

– What are the underlying dimensions of shareholder activism?

– What is the impact of shareholder activism on firms’ marketing activities:

• 4 P’s (price, product, place, promotion)

• Time horizon (short versus long term view)

– What is the role of Marketing in IR?

Faculty of Economics and Business Administration

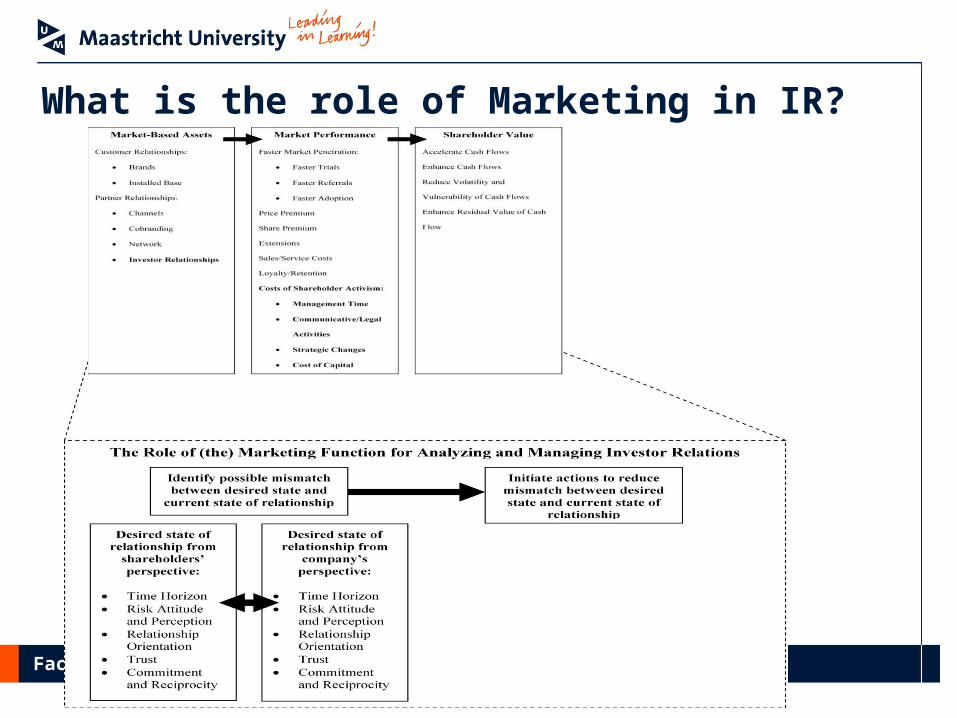

What is the role of Marketing in IR?

Faculty of Economics and Business Administration

Market Sentiment

• Explanation for all movements in markets?!– Industry, Academia in disagreement

No consensus: remains a black box

• Market sentiment index industry:– Proprietary methods– Technical Indicators– Surveys– Put/call ratio

Do they add value?these are not measures but the result of market sentiment!

Faculty of Economics and Business Administration

Market Sentiment

• What is it? What drives it?– Affective constructs

• Mood A mood is a lasting affective state triggered by a particular stimulus or event. Moods generally have either a positive or negative valence.

• Optimism Expectation of positive outcomes in (e.g., online investing).

• Confidence-> A state of being certain, either that a hypothesis or prediction is correct, or that a chosen course of action is the best or most effective given the circumstances.

Faculty of Economics and Business Administration

Market Sentiment

• MF approach:

– Bottom-Up approach: Start with individual decision-maker

– Determining drivers of sentiment

– Most approaches are top-down• aggregate studies do not address causality.

Faculty of Economics and Business Administration

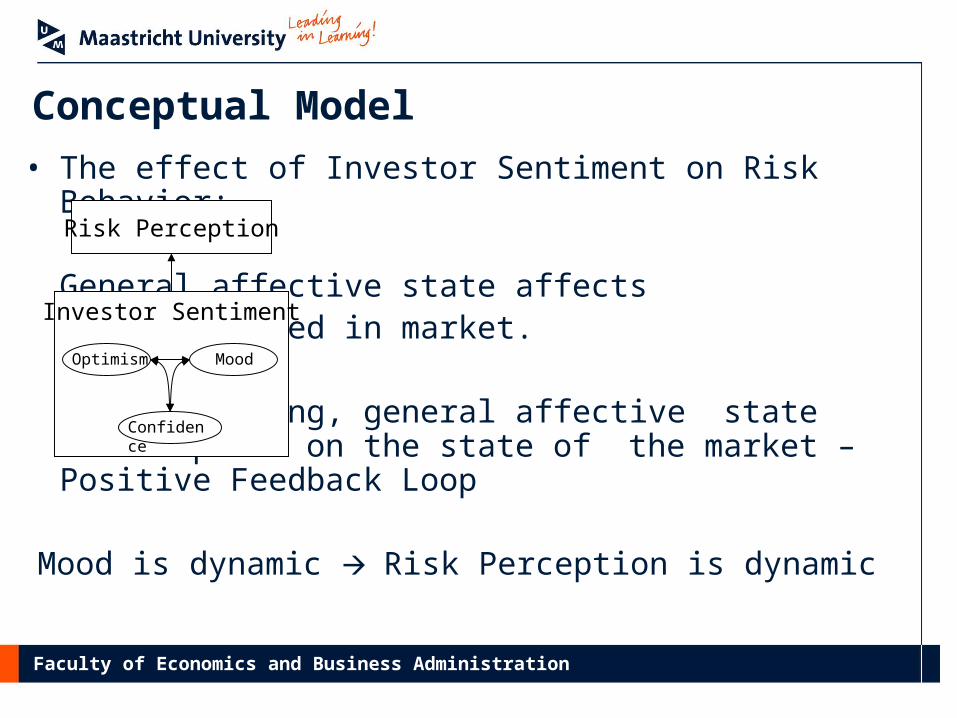

Conceptual Model

• The effect of Investor Sentiment on Risk Behavior:

General affective state affectsrisk perceived in market.

When investing, general affective state also depends on the

state of the market – Positive Feedback Loop

Mood is dynamic Risk Perception is dynamic

Investor Sentiment

Risk Perception

Optimism

Confidence

Mood

Faculty of Economics and Business Administration

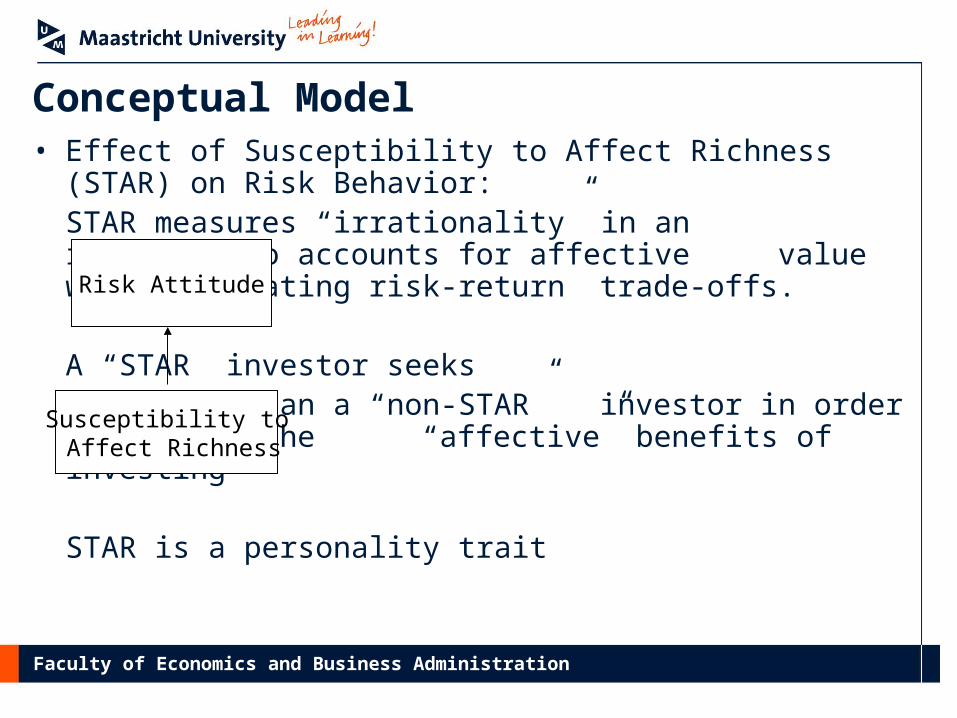

Conceptual Model• Effect of Susceptibility to Affect Richness (STAR) on Risk

Behavior:STAR measures “irrationality” in an investor who accounts for affective value when calculating risk-return trade-offs.

A “STAR” investor seeks more risk than a “non-STAR” investor in order to acquire the “affective” benefits of investing

STAR is a personality trait

Susceptibility to Affect Richness

Risk Attitude

Faculty of Economics and Business Administration

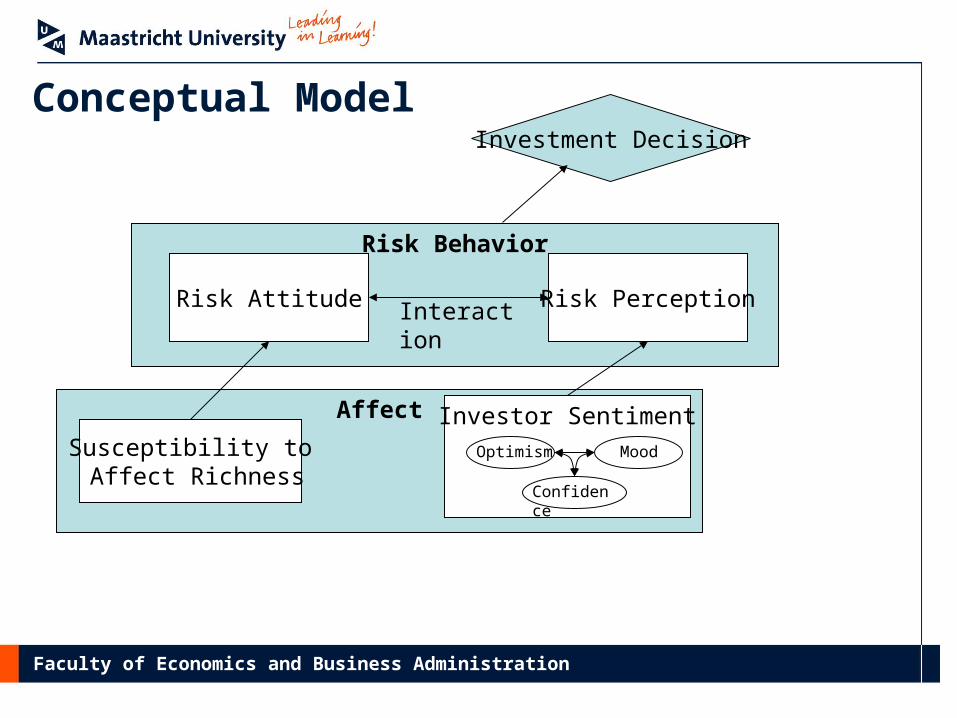

Conceptual ModelInvestment Decision

Risk Behavior

Affect Investor SentimentSusceptibility to Affect Richness

Risk Attitude Risk Perception

Optimism

Confidence

Mood

Interaction

Faculty of Economics and Business Administration

Market Sentiment

• Financial Product Development:– Investment products

– Trading support systems

– Market sentiment derivatives

– Insurance products

– Regulation– Confidence during crises

» (in the US credit system for example)

Faculty of Economics and Business Administration

Interdepartmental MF integration

• Interdepartmental integration:– interaction and – collaboration

• in a way that benefits are produced to them that exceed individually produced benefits of the departments.

In order to effectively work together, marketing and finance must align their goals

Faculty of Economics and Business Administration

Interdepartmental MF integration

• Research questions– Does M-F integration within a firm contribute to

business performance? – Do relational characteristics and organizational

structure variables have an influence on the level of M-F integration?

– Is there a gap between perceived versus actual integration, and does this have an influence on business performance?

Faculty of Economics and Business Administration

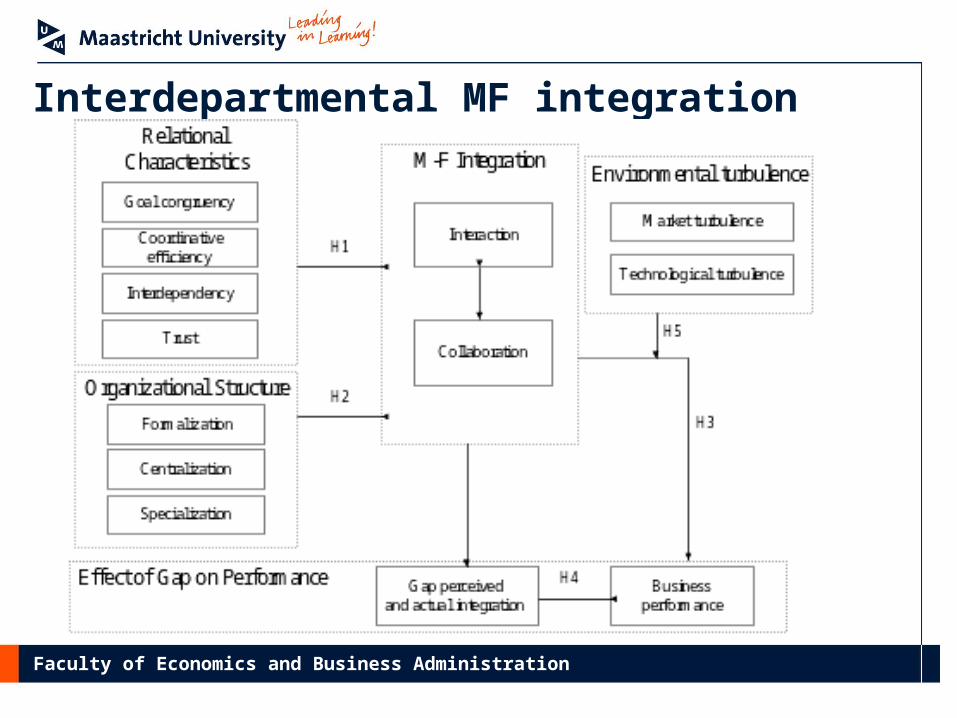

Interdepartmental MF integration

Faculty of Economics and Business Administration

Interdepartmental MF integration

• Managerial implications– Provide insights into how interdepartmental

integration should be managed– Provide guidelines for top management on how to

design their organization– Marketing managers can learn how to interact

and collaborate with finance managers– Develop a measure that measures actual

interdepartmental integration in terms of contribution to financial performance

Faculty of Economics and Business Administration

Marketing X Finance = Product with High Return and Low Risk Profile

• Can we disentangle what discipline contributes what to financial performance?

– Marketing X finance

• Is that a relevant question?

– Not for shareholders

– For rewards for both disciplines

Faculty of Economics and Business Administration

Marketing X Finance = Product with High Return and Low Risk Profile

• Because:

– High return:

• They complement each other: The Whole is greater than the sum of its parts.

– Low Risk

• Natural hedge between the disciplines– Risk, in terms of contribution, is cancelled out by both disciplines

MF approach is investment with high Sharpe ratio!