marvin markowitz, et al. v. sensormatic electronics...

TRANSCRIPT

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 1 of 90

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA

Case No: 01-8346-Cl V-RYSKAMP

)

IN RE: SENSORMATIC ELECTRONICS CORP. )

SECURITIES LITIGATION )

)

)

CL

PIL 11) ox

T 1 52001 /

CONSOLIDATED AMENDED CLASS ACTION COMPLAINT

Plaintiffs allege the following, except as to matters specifically pertaining to them and

their counsel, based upon Counsel's investigation, which included analysis of publicly-available

news articles and reports, public filings, press releases and other matters of public record, contact

with factual sources, review of internal documents and consultation with a forensic accountant.

NATURE OF THE ACTION

This is a class action on behalf of all purchasers of the common stock of

Sensormatic Electronics Corp. ("Sensormatic" or the "Company") between August 8, 2000 and

April 9, 2001, inclusive, (the "Class Period"), brought under the Securities Exchange Act of 1934

(the "Exchange Act')

2. Throughout the Class Period, defendants recognized revenue in violation of

Generally Accepted Accounting Principles ("GAAP"). Defendants recognized revenue upon

shipment of a product even when the customer was allowed to return the product within a certain

time, or the customer could test the product for a year and then decide whether or not to make the

purchase. This sales practice was referred to within the Company as the "try-buy" program. As

a result, defendants' financial results for year-end 2000 and the third quarter of fiscal 2001 were

materially overstated.

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 2 of 90

3. This was not the first time Defendants engaged in questionable revenue

recognition tactics. As detailed below, defendants' improper accounting methods caught the eye

of the SEC in 1995, which resulted in an investigation, fine, and settlement. See also Exhs. A

and B hereto.

4. Defendants learned early in the Class Period that Sensormatic's sales were

declining, and would continue to decline. Between February 28 and March 1, 2001, an Annual

Product Sales Forum Meeting was held at the Embassy Suites Hotel in Boca Raton. At the

meeting, a former Marketing Manager presented graphs and information detailing several

adverse sales trends. The presentation detailed a dramatic reduction in sales to Sensormatic's top

customers, a trend which was forecasted to continue well into the third quarter. A hard copy of

the presentation was prepared and sent to several Sensormatic executives, including Loof and

Kendall. TI T 41, 43-44, 48-53.

5. On April 10, 2001, defendants revealed the truth: that retail orders had slowed

during the third fiscal quarter and that Sensormatic's revenues and earnings would fall far short of

expectations. Analyst consensus estimates for Sensormatic were $.021 for the third fiscal

quarter; Sensormatic, however, announced that earnings would only hit $0.06 to $0.07 per share

for the quarter, far below Sensormatic's publicly-expressed expectations. Sensormatic!s stock

declined by 31% to trade at $13.

6. On April 26, 2001. the other shoe dropped when defendants admitted that their

Class Period financial statements included falsely recognized revenue. Subsequently, defendants

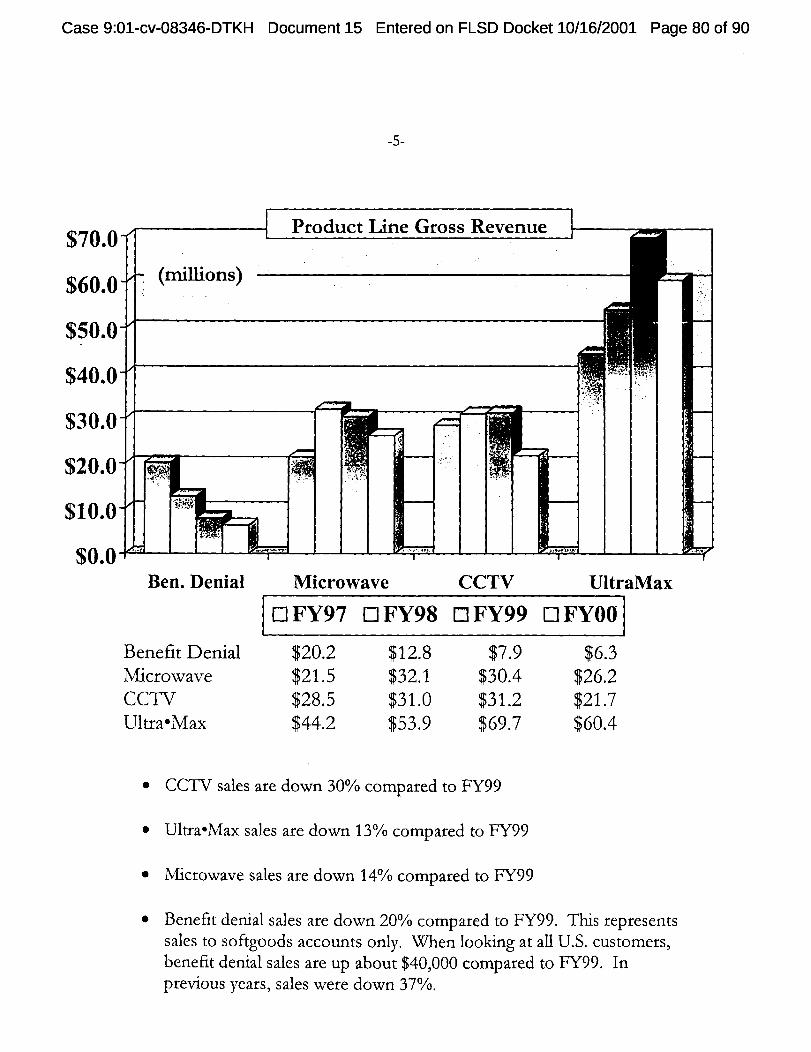

revealed that even the reduced third quarter financial results were materially overstated through

defendants' improper revenue recognition practices.

-2-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 3 of 90

7. Defendants engaged in the fraud for two primary reasons. First, defendants had

for years been seeking a buyer for Sensormatic. Ever since Assaf first initiated negotiations with

Boca-Raton based Tyco Industries in 1997. ¶ 78. A buyer would allow defendants to cash in

their options and receive huge cash bonuses, by virtue of Sensormatic's change of control

provisions. Second, when the possibility of finding a buyer for Sensormatic was not yet

materializing, defendants sold up to 95% of their Sensormatic stock at prices near the Class

Period high, only weeks before the announcement detailed in ¶ 117 below.

While investors and analysts were shocked by the Company's April 10, 2001

announcement in light of the fact that defendants had repeatedly emphasized Sensormatic's

ability to meet third quarter and year-end estimates, defendants were entirely aware of the

Company's declining sales. In addition, defendants were still unsure if a buyer would be found

for Sensormatic. Unwilling to take the risk, defendants rushed to divest themselves of nearly

$8,000,000 worth of Sensormatic stock at prices near the Class Period high. In March, after

selling huge amounts of Sensormatic shares, defendant Assaf renewed negotiations with Tyco in

the hopes that Tyco would bail out Sensormatic. The timing of defendants' stock sales is

illustrated below:

-3-

24

22

20

18

16

14

12

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 4 of 90

SENSORMATIC INSIDER TRADING

Sensormatic SAM

Kendall Resigns

A

Class Period begins- Annual Product Forum in Boca Raton: Sales Are Down

Defendants dump millions of Sensormatic shares

Announcement: Third quarter profit slumps STOCK DROPS 31%

9. These sales were suspicious in both timing and amount.

A. Defendants Sales Were Suspiciously Timed

10. The majority of the shares (approximately $4.3 million) sold by the defendants

were sold between March 2, 2001 and March 13, 2001. This was one day after the February 28 -

March 1. 2001 Annual Product Forum during which a former Sensormatic Marketing Manager

graphically detailed the Company's declining sales. ¶T 40-44. At that point, defendants had

already received Sensormatic's quarterly review report for the second quarter of 2001, which

indicated that sales were down significantly and would continue to be down in the 3rd quarter

ME

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 5 of 90

offiscal 2001. ¶ 55. Defendant Hartman sold 75,000 shares on March 13, 2001, only nineteen

trading days from the April 10, 2001 announcement revealing what defendants already knew -

sales were declining dramatically, and would not meet analysts' estimates.

11. Defendants' sold their Sensormatic shares at prices ranging from $19.03 to $22.25.

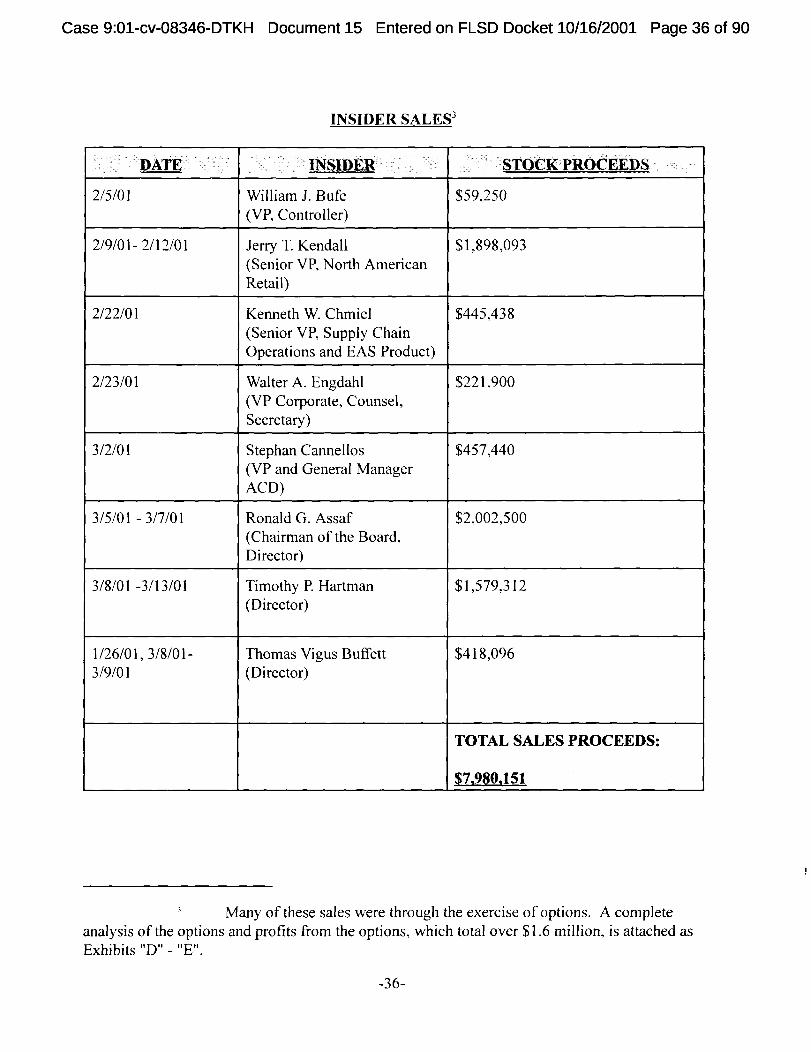

See, Exhibit B. A large portion of these shares were sold during the week Sensormatic stock

reached its Class Period high, on March 6, 2001. The high of $22.25 for which Assaf sold his

shares, was only cents away from Sensormatic's Class Period high of $22.58 reached on March 6,

2001.

12. In addition, the fact that all of these insiders, who received the Company's

quarterly review reports, weekly and monthly sales forecasts, the Softgoods Sales Report, and

attended regular meetings, sold within days of one another prior to the devastating fiscal third

quarter pre-announcement can hardly be coincidental.

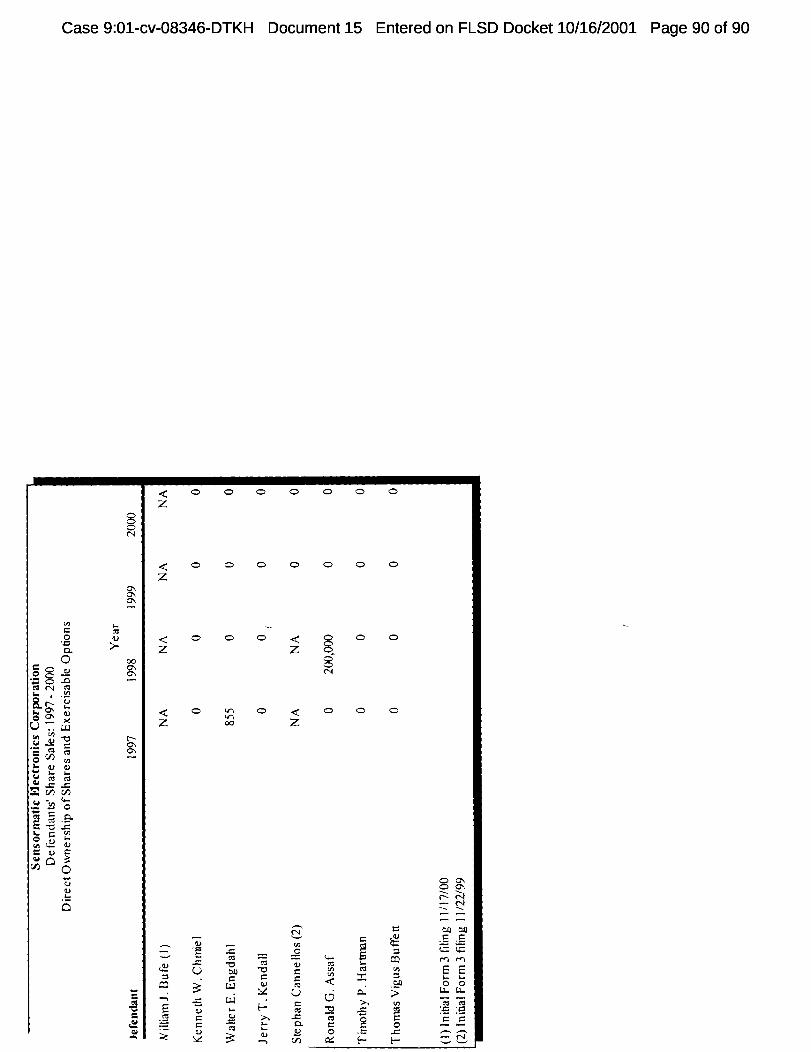

13. Defendants' selling is also suspicious in light of the fact that during 1997-2000,

only defendants Engdahl and Assaf sold shares. Engdahl sold a mere 855 shares in 1997, and

Assaf sold 200.000 in 1998. During 1999 and 2000 none of these defendants sold a single

share. See Exhs. D-E.

B. Defendants Dumped As Much as 95.5% Of Their Sensormatic Holdings

14. In addition to the unusual timing of defendants' sales, the amount of stock they

sold is also indicative of fraudulent intent. As detailed in Exhibit B, these defendants divested

themselves of huge amounts of their Sensormatic holdings. For example, Bufe sold 95.5% of his

holdings; Chmiel sold 65.2%; Engdahl sold 55.7%; Kendall sold 63.5%; Cannellos sold 92.8%;

Assaf sold 14.9%; Hartman sold 58.8% and Buffett sold 25.5%. This unusual selling activity

-5-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 6 of 90

indicates that defendants acted with inside knowledge of adverse facts unknown to the public.

JURISDICTION AND VENUE

15. This Court has jurisdiction over the subject matter of this action pursuant to 28

U.S.C. §1331, 1337 and 1367 and Section 27 of the Exchange Act (15 U.S.C. § 78aa).

16. This action arises under Sections 10(b) and 20(a) of the Exchange Act (15 U.S.C.

§ § 78j(b) and 78t(a)) and Rule lOb-S promulgated thereunder (17 C.F.R. § 240.1Ob-5).

17. Venue is proper in this District pursuant to Section 27 of the Exchange Act (15

U.S.C. § 78aa) and 28 U.S.C. § 1391(b) and (c). Substantial acts in furtherance of the alleged

fraud and/or its effects have occurred within this District and Sensormatic maintains its principal

executive offices in this District.

18. In connection with the acts and omissions alleged in this complaint, defendants,

directly or indirectly, used the means and instrumentalities of interstate commerce, including, but

not limited to, the mails, interstate telephone communications, and the facilities of the national

securities markets.

PARTIES

19. Lead Plaintiffs Leo Bugg, Jr., Frank A. Foilmer and Karl Rugart purchased

Sensormatic common stock during the Class Period, as set forth in the certifications

accompanying plaintiffs' lead plaintiff motion, and were damaged thereby. Those certifications

are incorporated by reference herein.

20. Defendant Sensormatic is a maker of anti-theft equipment for retailers.

Sensormatic's executive offices are located at 951 Yamato Road, Boca Raton, Florida.

21. The individual defendants, at all times relevant to this action, served in the

capacities listed below and received substantial compensation:

I on

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 7 of 90

Name

Per-Olof Loof

Gregory C. Thompson

Ronald G. Assaf

Jerry T. Kendall

Timothy Hartman

Kenneth W. Chmiel

Walter A. Engdahl

Stephan Caimellos

Thomas Buffett

Position

President and Chief Executive Officer

Senior Vice President And Chief Financial Officer

Chairman of the Board, Director

Senior V.P., North Am. Retail

Director

Senior V.P., Supply Chain Operations and EAS Product

V.P. Corporate, Counsel, Secretary

V.P., Geni Manager, ACD

Director

William J. Bufe V.P., Controller

22. Each of the defendants is liable as a participant in a fraudulent scheme that

operated as a fraud or deceit on purchasers of Sensormatic common stock, by disseminating

materially false and misleading statements and/or concealing material adverse facts. In addition,

the Individual Defendants, as senior officers and/or directors of Sensormatic were controlling

persons of the Company. Each exercised their power and influence to cause Sensormatic to

engage in the fraudulent practices complained of herein. Indeed, in Assafs own words, 7aJs

CEO, you should know exactly what you're doing, and not take everyone's word that

everything is okay." Fastirack. pg. 48.

23. On November 29, 2000, the Company announced its promotion of defendant

William J. Bufe from Senior Director of Finance for the Company's American Operations to

Vice President and Controller. The press release stated: "As Vice President and Controller, Bufe

-7-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 8 of 90

is responsible for all financial reporting and analysis, the finance and accounting support for

Sensormatic's sales, research and development and manufacturing business units worldwide, as

well as the management of budgeting, forecasting and financial planning."

24. In addition to his responsibilities as a Director, Hartman was a member of the

Audit Committee, and was charged with specific responsibilities. The Audit Committee was

responsible for fulfilling its oversight responsibilities with respect to (i) the financial information

provided to shareholders and the SEC; (ii) the systems of internal controls that management has

established; and (iii) the internal and external audit processes. The Audit Committee was

required to meet at least four times annually, and to meet in separate executive sessions with the

Chief Financial Officer. The Audit Committee members were also required to review with

management the annual financial statements and related footnotes and financial information

included in the Company's 10-K. See, Sensormatic's Proxy, dated November 17, 2000.

BACKGROUND TO THE CLASS PERIOD

25. Sensormatic was founded in 1966 by Assaf and his cousin, Jack Welsh.

Sensormatic describes itself as the global leader in electronic security" and "develop[s],

manufacture[s]. market[s] and distributes. . . the most advanced lines of integrated security

products for article protection. video surveillance, access control and asset tracking. See Form

10-K dated September 28, 2000.

26. The Company has three product divisions, electronic article surveillance systems

("EAS"), video systems, including closed circuit television ("CCTV") and access control and

management systems. The EAS products include reusable hard tags and disposable labels with

detection and deactivation systems. The access control and asset management systems provide

tagging, tracking, and access systems to monitor movements of people and/or assets. For the

In

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 9 of 90

fiscal year ended June 30, 2000, Sensormatic derived $601.0 million from its EAS division;

$293.9 from Video Systems; and $48.8 from access control and asset management. Id. at 30.

27. Sensormatic's marketing is divided into "softgoods" and 'hardgoods." Softgoods

consist largely of apparel merchandise held by large retailers such as department stores.

Hardgoods consist of non-apparel merchandise sold to customers such as supermarkets, books,

videos, and entertainment stores, as well as the heavy equipment Sensormatic sold, including

pedestals, video cameras and surveillance monitors. Id. at 31.

28. "The early 1990s brought fortune and fame to Sensormatic as more and more

retailers sold security-tagged merchandise." See Fastirack, "The Last Alarm: After Raising

Sensormatic From Birth, Ron Assaf Prepares For A Simpler, If Not Less Hectic, Life." Fall 2001

issue, at pages 47-48. In 1992. Sensormatic was honored as Company of the Year by The Miami

Herald. Id. In 1996, Sensormatic was selected as the exclusive electronic security provider of

the 1996 Olympic Games in Atlanta. id. Along with the high points, Sensormatic experienced

several lows. In November 1995, the Company announced that the SEC was investigating

Sensormatic for accounting violations and "other irregularities." Id. at 46. The federal

investigation alleged that Sensormatic materially misstated profits in 1995 and 1996 by using

out-of-period-revenue to calculate profits. Id. at 47. According to Assaf, Sensormatic was

"recognizing [revenue from] shipments three or four days after the end of the quarter as sales

within the quarter."

29. From 1995 to 1998, Sensormatic experienced slow growth and was forced to

suspend dividend payments to conserve cash. Id. at 48. In August 1999, Per-Olof Loof was

hired as a "rainmaker" to turn the Company's profitability around. Id. Loofs task was "returning

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 10 of 90

Sensormatic to the top of the investment charts'." See Palm Beach Post, "Corporate Rock; Per-

Olof Loof Has Sensormatic Playing a New Tune," January 16, 2000.

30. Prior to the Class Period, defendants seemed to be on-track to achieving record

growth and profitability. On January 25, 2000, defendants reported a 170% climb in operating

income. A January 25, 2000 press release announced that the Company was making "continued

progress toward its longer-term targets of double-digit sustainable revenue growth and double-

digit operating margins." Olof stated in the press release:

"In October. 1 defined four priorities for Sensormatic. The first was the math has got to work. Our financial model revolves around growing revenues, reducing expenses and investing more in research and development. Recently the 'math' at Sensormatic has been working better and better."

31. At the start of the Class Period, it seemed as if the "math" at Sensormatic

was working, and defendants had left Sensormatic's troubled past behind. However, defendants

still struggled to gain market acceptance.

32. Loof felt if the Company could continue to post a few good quarters, the

Company would regain its high stock price, and he would receive significant personal gain. In an

April 17, 2000 interview with The Wall Street Transcript, Loof was asked what misconceptions

there were about Sensormatic. He responded:

Despite the fanfare surrounding Loofs arrival, Sensormatic employees viewed Loof as an excessive leader, who was "out for himself', and frivolously spent corporate money at the expense of corporate needs, such as flying in his rock band from Sweden to perform at a Sensormatic annual meeting and making a video of himself skiing down a mountain side as a promotional tool for the Company. At the same time, legitimate marketing funds were slashed. Indeed, according to a former Senior Information Systems expert, Information Systems employees were regularly sent to Loofs house during work hours to install software on Loof's children's computers, and to install new digital subscriber lines at LooPs residence. Whenever Loof had a problem with his or his family's computers, employees from Sensormatic were sent out on Company time to take care of things.

-10-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 11 of 90

"I think there are a couple of things. I joined the Company in August of 1999, but for a number of years prior to that the company was faced with difficult times that grew out of rapid growth. That caused the company to stumble and earnings suffered from it. I think the investing community wants to ensure that the track we're on now actually continues. We have delivered a couple of really good quarters, and I think they want to make sure that it continues, both in terms of consistent growth as well as managing our expenses. If we can continue to do that, which I really believe we can, I think that the question of our stability will go" away. Id. at 6.

SUBSTANTIVE ALLEGATIONS

Sensormatic's Forward-Looking Statements are Excluded from Safe Harbor Protection As A Result of the SEC's March 25, 1998 Cease-and-Desist Order

33. On March 25, 1998, the Securities and Exchange Commission issued an order in

the administrative proceeding entitled In the Matter of Sensormatic Electronics Corporation, File

No. 3-9563: "Order Instituting Public Administrative Proceedings, Making Findings, and Issuing

Cease-and-Desist Order." (A copy of the SEC Order is annexed hereto as Exhibit A.) In

addition, defendant Assaf entered into a cease-and-desist order with the SEC requiring him to

pay a fine of $50,000 and to refrain from violating the federal securities laws. (A copy of the

cease and desist order entered against Assaf is annexed hereto as Exhibit B.) (The orders are

referred to collectively as the "SEC Cease-and-Desist Orders.")

34. The SEC instituted administrative proceedings against Sensormatic for accounting

violations. Specifically, the SEC Order found that "[f]rom... July 1, 1993 ... through July 10,

1995, Sensormatic manipulated its quarterly revenue and earnings in order to reach its budgeted

earnings goals and thereby meet analysts' quarterly earnings projections. Sensormatic carried out

this fraudulent scheme by improperly recognizing revenue through several different practices.

The conduct. . . primarily involved recognizing and recording revenue in one quarter from

products shipped in the next quarter." The SEC Cease-and-Desist Orders found that Sensormatic

-11-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 12 of 90

and Assaf had violated several provisions of the securities laws, including the anti-fraud

provision of the Securities Exchange Act of 1934, Section 10(b), and ordered them to cease and

desist from committing or causing any violation, and future violation, of Section 10(b) and other

sections of the securities laws.

35. As the Company acknowledged in its proxy statement filed with the SEC in

connection with the Company's November 2000 annual shareholders' meeting:

In April 1998, the Company, certain former Company officers and Ronald G. Assaf, the Company's non-executive Chairman of the Board and former Chief Executive Officer, entered into agreements, without admitting or denying any wrongdoing, with the SEC to resolve an SEC investigation, which was described in previously-filed periodic reports of the Company. ... [T]he SEC alleged, among other things, that during [the period July 1, 1993 to July 10, 1995] the Company improperly recognized and recorded revenue in one quarter from product shipped to customers in the next quarter and misstated its quarterly earnings in certain financial statements contained in periodic reports and registration statements. As part of that settlement, the Company agreed to an Order of the SEC that it will not in the future violate certain periodic reporting, books and records, internal controls and antifraud provisions of the Federal securities laws. There were no penalties imposed on the Company.

In its related civil injunctive complaint, the SEC alleged, among other things, that during the relevant period, * * * * Mr. Assaf knew of certain improper recognition policies and knew or was generally aware that certain Company periodic reports filed with the SEC were false and misleading. Mr. Assaf agreed, without admitting or denying any wrongdoing, to a civil final judgment enjoining him from future violations of certain record keeping and periodic reporting provisions of the Federal securities laws and ordering him to pay a civil penalty of $50,000.

36. Defendant Ronald Assaf recently gave an interview to Fasttrack, a magazine

publication. Assaf was questioned about the above-described SEC investigation into

Sensormatic's accounting practices. "We were recognizing shipments three orfour days after

-12-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 13 of 90

the end of the quarter as sales within the quarter, 'Assafsays. 'I thought it was pretty

minimal, but serious. I didn't realize how serious. Nor did anyone in the Company, in my

opinion, understand the extent of it because our systems were so antiquated. We had very little

real-time information. And I think the operations people just let it get out of hand.' As CEO,

Assaf says he bore ultimate responsibility for letting the accounting mess worsen, and calls the

debacle the biggest disappointment of his career. 'As CEO, you should know exactly what

you're doing, and not take everyone's word that everything is okay,' Assaf says." Fasttrack,

"The Last Alarm: After Raising Sensormatic From Birth, Ron Assaf Prepares For A Simpler, If

Not Less Hectic, Life." Fall 2001 issue, at pages 47-48.

37. As a result of the SEC Cease-and-Desist Orders, Sensormatic's forward-looking

statements, if any, made during the Class Period, are expressly excluded from safe harbor

protection pursuant to Section 21E of the Securities Exchange Act of 1934 because, as alleged

below, they were made within three years of the SEC Cease-and-Desist Orders prohibiting

Sensormatic and Assaf from further violations of the antifraud provisions of the Federal

securities laws, namely, Section 10(b):

SEC: 21E. Application of Safe Harbor for Forward-Looking Statements

(b) Exclusions - Except to the extent otherwise specifically provided by rule, regulation, or order of the Commission, this section shall not apply to a forward-looking statement -

(I) that is made with respect to the business or operations of the issuer, if the issuer -

(A) during the 3-year period preceding the date on which the statement was first made -

(ii) has been the subject of judicial or administrative decree or order arising

-13-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 14 of 90

out of a governmental action that -

(I) prohibits future violations of the antifraud provisions of the securities laws;

(II) requires that the issuer cease and desist from violating the antifraud provisions of the securities laws; or

(III) determines that the issuer violated the antifraud provisions of the securities laws.

Section 21E(b) of the Securities Exchange Act of 1934. (Emphasis added.)

DEFENDANTS' WERE AWARE OF SENSORMATIC'S INABILITY TO MEET FINANCIAL ESTIMATES

A. Defendants' Declining Sales Are Discussed At Annual Product Forum Meetings

38. Sensormatic's drastically declining sales were no mystery to defendants. As

detailed below, defendants were regularly confronted with Sensormatic's decreasing sales figures

through attending regular "town meetings", an Annual Product Forum Meeting, by receiving

regular written sales reports and accessing at-will sales information on the computer system. By

receiving inside information about Sensormatic's deteriorating sales trends, defendants were able

to dump millions of dollars worth of Company stock right before the stock plunged.

39. According to a former Marketing Manager employed at Sensormatic from 1996

until April 2001, who marketed sensor and video products, Sensormatic employees "all knew" in

late December 2000 that the next quarter was going to be bad." The fact that sales would be

down in the upcoming third quarter was no surprise to anyone in Sensormatic. Sensormatic's

retail customers were having problems and did not have the money to make purchases of

Sensormatic products. These customers included The Gap; Federated Department Stores

(including Burdine's, Macy's, Bloomingdale's, music chain stores such as Mars Music, and large

-14-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 15 of 90

retail chains such as The Limited, Abercrombie & Fitch. Lord & Taylor, and Dillards. Indeed,

according to this former employee, Sensormatic's sales had been off during the entire 2001 fiscal

year, and as early as July 1999.

40. According to the former Marketing Manager, one of the ways defendants accessed

this inside information was through Sensormatic's Annual Product Forum Meetings. The

Annual Product Forums were held annually in February. Approximately 300 employees from

marketing, engineering, manufacturing, and service from Europe, Asia and the U.S. attended.

Robert Clucas, marketing manager for hard goods," spoke at the forum. Clucas put up a chart

showing that sales would be significantly lower after the Company completed the roll-out of

product sales to Wal-Mart and Auto Zone, which was expected to end later in the year.

According to the former employee, who was present at this meeting. Clucas sought to show that

Sensormatic would have little new business after these large roll-outs were done. According to

this former employee, nothing was done in 2000 to identify new products Sensormatic could sell

in the future.

41. The Product Forum in 2001 was held on February 27, 28, and March Ut at the

Embassy Suites Hotel on Yamato Road, Boca Raton. Several Boca Raton executives attended,

including Dennis Constantine, defendant Dennis Chmiel, and Pedro Del Sol, who was

responsible for the CCTV division (closed-circuit television). After the meeting, a report known

as the Product Forum Presentation Report was published and distributed to all management-level

employees. The report is a hard copy of all the presentations given at the Annual Product Forum.

42. The former Marketing Manager reported that for fiscal years 2000 and 2001,

Sensormatic projected a ten percent year-over-year sales increase, which was unreasonable since

all the major retailers were already Sensormatic customers and were already saturated with

-15-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 16 of 90

Sensormatic products. According to this former employee, the Marketing Department was

"waving the red flag for several years." The first time the decreased sales trends were brought to

the Company's attention was during the Annual Product Forum meeting in February 2000 when

Bob Clucas put up a chart and discussed that fact that hardgoods would experience big sales

decreases after the Walmart contract finished.

43. According to the former Marketing Manager, the "sales problem" was a big

concern and was the main topic of the February 2001 Annual Product Forum Meeting. Bob

Clucas spoke again at the Annual Product Forum Meeting at the Embassy Suites Hotel in

February 2001. Clucas spoke on Hardgoods marketing and emphasized that Hardgoods would be

"hurting for sales" since the "next Walmart" was not there. This was the same thing Clucas was

saying during FY2000 and all of 2001. Clucas presented a series of charts which showed a

decrease in Hardgoods sales compared to the previous years. Clucas showed a projection for

sales at the meeting which showed declining sales in Hardgoods for the 3" fiscal quarter (2001)

compared to the 3rd fiscal quarter of 2000. Sales were mainly in accessories (extra tags or

detachers), but not in hardware. Clucas reported that the Company was not making money

rolling out hardware to new retail chains.

44. The former Marketing Manager also spoke at the Annual Product Forum Meeting.

She discussed the fact that Softgoods sales were down significantly, and were not projected to

increase. She emphasized the need for new products, which was crucial since growth had

essentially stopped at Sensormatic. Sensormatic's customers had no need to buy new sensors,

and the pedestals (devices which raise an alarm when a sensor passes them) worked well. The

sensors were lasting 10 to 15 years. Retailers continued using their old sensors, but were

requesting smaller tags and more coverage from the pedestals within the stores. Sensormatic had

-16-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 17 of 90

not come up with any new products, and customers were not going to update their pedestals for

minor changes. Sensormatic needed to create a whole new system line or needed to acquire a

company to extend their current product lines to increase sales. Only one day after finding out

that sales were down and were not expected to recover in the third quarter, defendants sold

millions of dollars of their stock at near Class-Period highs. ¶Jl0-13.

B. Sensormatic's Anticipated Earnings Miss Is Discussed In-house

45. In late February 2001, the sales department held a meeting at the Company's main

offices on Yamato Road in Boca Raton. The former Sensormatic Marketing Manager again

made a fifteen minute sales presentation at this meeting. At the meeting, she showed charts

which reported that sales were down even more than they were in the 2" fiscal quarter, and again

described the challenges ahead for Softgoods retailers. She reported that the Company was

experiencing several adverse trends, such as the fact that the market was saturated and the

Company needed next generation products to generate sales. She presented bar charts which

depicted sales for the previous quarter and for the year, which showed a downward trend. The

charts included January through February 2001 sales figures, and year to date sales figures, as

well as FY 2001 figures (July 1, 2000 through December 31, 2000). She tried to "shock"

Sensormatic management into taking action, and told the Company that without new products,

the only things selling were accessories, which would lead to Sensormatic missing their

numbers.

46. Indeed, sales figures and the ability to meet Wall Street estimates were regularly

discussed within Sensormatic. According to a former contract employee with Sensormatic from

September 1999 through February 2001 who handled domestic credit sales for Sensormatic

customers, Loof held quarterly meetings at Sensormatic to announce quarterly sales figures.

-17-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 18 of 90

47. According to a former Senior Information Systems Expert who was employed at

the Company between 1995 and April 26, 2001, these all-employee meetings were known as

"town meetings" and were held at the beginning of the Company's fiscal quarter. For example,

the Company held a town meeting in early January, 2001 in the auditorium at Florida Atlantic

University in Boca Raton. The meetings were broadcast live over the Company's network, and

were also videotaped. During these meetings, the status of the Company discussed, sales

statistics for the current quarter were presented and forecasts for future sales in the upcoming

quarters were discussed. There would also be a question and answer session at the end of the

meetings. Loof headed the meetings and all upper management attended, including Jerry

Kendall, Chris Davell, Don Taylor and others. These meetings were not open to investors or

analysts.

C. Internal Reports Detail Sensormatic's Quarterly Sales Decline

1. The September 5, 2000 SoftGoods Sales Report

48. A former Marketing Manager reported that the entire Sensormatic executive team,

including Loof, Kendall, Chmiel, Dennis Constantine (a Senior Vice President) were directly

aware of the decreased sales Sensormatic was experiencing throughout the Class Period.

According to this former employee, two types of internal reports were prepared: a Softgoods

Sales Report and a Quarterly Sales Report. On September 5. 2000, this former employee

prepared and circulated a Sofigoods Sales Report to a large number of Sensormatic executives

and sales people, including defendant Jerry T. Kendall. (A copy of the report is annexed hereto,

and is incorporated as if fully set forth herein, as Exhibit C.) For the first time, the Report

indicated that SofiGoods sales were down significantly. The Sofigoods Sales Report for the 2

quarter was prepared in February of 2001 and discussed results of October through December

on

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 19 of 90

2000 as well as sales predictions for the 3 rd quarter of fiscal year 2001.

49. The Softgoods Sales Report was distributed by Ann Hasen. assistant to Don

Taylor. Director of Marketing. Taylor reported to Chris Davell and Jerry Kendall (who reported

to Loof). The Sofigoods report included on U.S. sales. The September 5, 2000 Report stated:

You will see in the attached that Sensormatic 's sales to the sofigoods market are declining. While this segment has been our company's bread and butter for many years, the environment in which our customers operate is undergoing tremendous changes. We need creative approaches and new products if we hope to increase sales to the sofigoods market. (Emphasis added).

50. For fiscal year 1999, Softgoods revenue was $139.8 million, and for fiscal year

2000, only $116.9 million. The fiscal year 2000 Sofigoods Sales Report also contained sales

results for the year, an analysis of sales trends, and an action plan for the future. The report

covered all U.S. softgoods accounts.

51. The Softgoods Sales Report set forth data showing that the Company's Softgoods

Gross Revenue was down by 16% in FY 2000 (p. 2): that Department Store Gross Revenue was

down 41% in FY 2000; and that CCTV, Ultra-Max and Microwave sales were all substantially

down compared with FY 2000 (See chart on p.S of Report). ("Ultra-Max" refers to one of

Sensormatic's electronic article surveillance products).

52. The Softgoods Sales Report also showed very clearly that Sensormatic's top 10

softgoods customers continued to decline materially from 1998 to 2000 (See chart on p.6 of

report). The report specifically identified several adverse sales trends:

-19-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 20 of 90

FY98

$11.2 Sears $ 8.9MarMaxx $ 6.5 JC Penney $ 6.2 Macy's East $ 5.3 Vict. Secret $ 3.8 Gap $ 3.4 Saks 5 " Ave. $ 3.3 May D&C $ 1.7 Banana Rep. $ 1.4 Macy's West

Top 10 Softgoods Customers

FY99

$9.5 Macy's East $8.5 MarMaxx $7.6 Macy's West $7.0 Sears $5.8 Gap $4.6 Charming Sh. $4.3 JC Penney $3.4 Lord & Taylor $3.2 Famous Barr $2.8 Gap Kids

FY00

$4.9 Aber. & Fitch $4.3 Gap $4.2 MarMaxx $3.8 Sears $3.3 Macy's East $3.3 Macy's West $3.0 Charming Shop $2.9 Old Navy $2.9 Victoria's Secret $2.9 Belk

(Millions)

53. The Report identified several negative sales trends which would

materially and adversely affect the Company's business going forward:

Trends regarding the top 10 softgoods customers:

Sales volume: In FY98, our #1 softgoods customer spent $11.2 million. In FY00, our #1 softgoods customer spent only $4.9 million.

Mix of customers: In FY98 and FY99, 6 of the top 10 customers were department stores. In FY00, only 4 of the top 10 were department stores.

Sears: Sales have declined significantly. The company has severely cut its LP budget.

JC Penney: While ranked 43 in FY98, the company did not make the top 10 list in FY00. Like Sears, JC Penney has severely cut its LP budget.

Macy's: Both divisions had a spike in FY99, but sales have declined due to decreased funding from Federated.

2. Defendants Were Aware Of Sensorinatic 's Third Quarter Drop Through Quarterly Review Reports

54. A former Communications Specialist based in Boca Raton reported that

employees knew Sensormatic sales and revenue numbers were down from January through

March 2001. One of the ways management was privy to this inside information was through

-20-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 21 of 90

regular receipt of quarterly sales reports. In addition to "Softgoods Sales Reports", there were

also 'North American Retail Quarterly Marketing Reports" prepared after the product forum

meetings, which included additional information about quarterly sales and trends for the United

States region.

55. According to the former Marketing Manager, there was also a quarterly review

report which was presented orally to the entire executive team, and then widely distributed

throughout the entire management level of Sensormatic. All the executives, including Loof, as

well as managers from marketing, were advised of the sales numbers and the reasons for the

numbers. The 2' quarter report was prepared in February or early March 2001, and reported the

results of October through December 2000 sales. The report also discussed sales predictions for

the 3 rd quarter of fiscal year 2001. The former Marketing Manager saw the report in late

February or early March of 2001, which indicated that sales were down significantly, and

predicted that sales would continue to be down in the 3 quarter offiscal year 2001. The

report indicated that retailers' sales to consumers were down in the 2 quarter of FY2001, which

impacted retailers' purchases from Serisormatic. The report said sales were down for the 2'

quarter of FY200I, and that looking into the 3 r quarter, sales would be down as well.

56. The former Manager reported that sales were down because a large anti-theft

device installation for Walmart was ending, and the retail sales climate was down. Also, retailers

reused Sensormatic products such as the electronic tags, which adversely impacted Sensormatic

sales. Some of the tags lasted ten to fifteen years.

57. According to the former Marketing Manager, two individuals in the Boca Raton

headquarters were responsible sales forecasting, Katrina Holcomb and Monique Young. They

had access to the computer systems and communicated with the salesmen in the field. Young

-21-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 22 of 90

and Holcomb reported directly to Chris Davell and Jerry Kendall. Dave!! and Kendall also

regularly had conference calls with field salesmen. Sales representatives would send facsimile

copies of their sales deals to the forecasting department, who in turn prepared sales forecast

reports.

58. The former Marketing Manager reported that both Kendall and Davell had the

sales numbers and reported them "up the ladder" to senior management, including Loof. From

these sales figures, Young and Holcomb prepared weekly and monthly sales forecasts. They

generated a report which projected Sensormatic numbers, which was distributed to the top

executive team and to the Marketing Group. The report contained projected sales revenue in

dollars and units in order to allow the manufacturing department to order raw materials for

production purposes.

59. Defendants knew that Sensormatic's 3 d quarter 2001 sales forecasts - and Wall

Street estimates - were not going to be met, because the sales numbers just were not there.

Young and Holcomb also knew because they received the numbers first from the field

representatives, and created weekly and monthly reports from the numbers received from the

field. From January through March 2001, the following individuals knew what actual sales

volume was by March 1, 2001: Ed Foley (Vice President of the Eastern Region); Steve Watson

(Vice President of Western Region); Chris Davel!; Jerry Kendall and Loof.

60. Defendants could also access Sensonnatic's actual and budgeted sales figures at

will through the Company's computer system. According to a former Senior Principal Engineer

in the Sensormatic Video Systems Division in San Diego, Wendell Keevins, Director of Finance

in San Diego, disseminated sales, revenue and forecasting information. Keevins was in direct

contact with senior management in Boca Raton. All Sensormatic senior employees had direct

-22-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 23 of 90

access to financial information at any given time through the Company's MIS (management

information systems) computer systems. Each employee had his own separate drive on the

computer network. The access to specific drives was limited to an employee's position and their

"need to know." Any official with proper access information could "access the financial drive

and pull up the numbers." The higher an employee's position, the more access they were given.

D. Sensormatic Employs a "Try-buy" Practice

61. According to a former Product Development Manager in Boca Raton from

October 2000 through May 2001, Sensormatic management had a "quarter-to-quarter"

philosophy, and were focused on hitting the numbers rather than long-term growth. Due to the

saturated market and the need for new products to stem the trend of declining sales, retail

customers had no need for additional Sensormatic products, and defendants could not meet

quarterly estimates. As a result of this reduced subsequent demand, defendants sought to spur

purchases by offering significant end of quarter discounts.

62. According to a former employee who worked as a Marketing Manager for

Sensormatic during and prior to the Class Period, Sensormatic had a "Try-Buy" practice in place

to aid sales. Under this practice, Sensormatic would install products, such as pedestals, and

allow the customer "try" it out before being obliged to "buy" it later. According to the former

employee, the customer had up to one year to try the merchandise out before they had to buy it.

Sensormatic, however, booked these "tries" as sales, even though customers had not agreed to

purchase the equipment, according to the former employee.

63. In addition to the improper recognition of revenue through these "try-buys" which

artificially inflated defendants' Class Period financial statements, there were other problems with

the program. According to the former Marketing Manager, the Company would install products

-23-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 24 of 90

and the customer would try the product and possibly buy it later. Sensormatic counted on the

idea that once the pedestals were installed and embedded into the customer's floor, they would

buy it to avoid the hassle of removing it. However, a great deal of equipment did not 'flip" from

try to buy. The customer had a year to buy the product. Once a year went by, Sensormatic lost

track of who was responsible for converting the 'try" to a "buy". For that reason, try-buys would

fall through the cracks.

64. The use of "try-buys" and improper recognition of revenue during the "try" stage,

resulted in a material overstatement of defendants' financial statements for year-end 2000 and for

the third quarter of 2001. These results were later restated to conform with GAAP. ¶J122-133.

E. Defendants Deeply Discount Product At Quarter-End To Meet Estimates

65. A former Marketing Manager reported that Sensormatic discounted their products

heavily each quarter in order to 'make their numbers" [Sensormatic sales and revenue numbers].

The decision to discount products was made by various sales managers, including Eastern

Regional Vice President Ed Foley, Western Regional Vice President Steve Watson, or Jerry

Kendall for larger accounts. Customers were aware of the deep discounting Sensormatic

engaged in to make their numbers, and would often wait until the last day of the quarter or the

very end of the quarter to make purchases. As discussed below, this practice was material fact

which should have been disclosed to investors. ¶134.

-24-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 25 of 90

THE CLASS PERIOD BEGINS

The August 8, 2000 Press Release

66. On August 8. 2000, the Company issued a press release announcing net income of

$72.2 million for its fiscal year ended June 30, 2000.2 Sensormatic achieved this net income

level in substantial part by failing to disclose its practice of recognizing revenue on contingent

sales (i.e. booking revenue when product was shipped that the customer had neither accepted nor

agreed to pay for).

67. The press release announced Fiscal 2000 earnings had surged 123%, the highest

annual revenue Sensormatic's history, and the fifth consecutive quarter in which the Company

has reported significantly improved financial results. Commenting on the Company's seemingly

stellar results, defendant Loof stated: "Our exceptional performance over the past year is clear

proof that this Company has turned around and is again in growth mode."

68. The August 8. 2000 press release attributed the strong earnings improvement" in

fiscal 2000 to "improving margins across all sales regions and product divisions."

69. The market accepted the Company's false statements, as defendants intended. An

August 9. 2000 article in the Palm Beach Post commented on the 123% increase for fiscal 2000,

and quoted Loof as stating, "[i]t's going to be hard to keep that up - 100 percent growth a year,

but I would think that these are numbers that would excite investors." The numbers did "excite

investors." After the press release was issued, the stock jumped 21%, on volume of 1.59 million

shares, the Company's second largest in a year.

2 Sensormatic's fiscal year begins on July 1. Accordingly, fourth quarter and year-end 2000 results are reported on June 30, 2000; first quarter 2001 results are reported on September 30, 2000; second quarter 2001 results are reported on December 31, 2000, and third quarter 2001 results are reported on March 30, 2001.

-25-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 26 of 90

70. Wall Street analysts also accepted Sensormatic's reversal of fortune. On August

8, 2000, Bear Stearns (in a research report written by Peter Barry and Cohn McArdle)

Sensormatic raised its rating on the Company from "attractive" to "buy." Analyst Jeff Kessler of

Lehman Brothers, referring to the previous SEC investigation for accounting fraud, noted in the

August 9, 2000 Palm Beach Post article, "[tihis company is so different from the disaster of '95.

It's fair to say that its recovery period is over."

The August 8, 2000 Press Release Was Materially False And Misleading

71. Contrary to LooPs representation that Sensormatic "has turned around," the

Company was in fact once again resorting to improper revenue recognition tactics in order to

artificially inflate Sensormatic's financial results. The August 8, 2000 press release was false.

The press release reported net income of $72.2 million, when actual net income was only slightly

more than $62 million. ¶128. The Company's reported net income was only achieved through

fraudulently recognizing revenue on shipment of products that the customer had not yet accepted

or agreed to pay for (contingent sales). As later revealed on April 26, 2000, defendants issued a

press release announcing the Company would adopt the provisions of SAB 101, and would start

recognizing revenue after product installation is complete and customer acceptance provisions

had been met.

72. This disclosure meant that prior to the fourth quarter of fiscal 2001, defendants

had been fraudulently recognizing revenue to meet quarterly estimates, by recognizing revenue

upon shipment, despite the fact that under GAAP, there were conditions which needed to be

fulfilled prior to revenue recognition. This revenue recognition practice was improper because:

(a) when Sensormatic installed an anti-theft system, even if the installation process took several

months, Sensormatic was recognizing the revenue right away; and (b) when Sensormatic sold

-26-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 27 of 90

products on a "contingent" basis, such as through the "try-buy" program, the Company booked

revenue upon shipment of the product. This was improper because the customer would often

decide not to purchase the product (such as in try-buy situations) and the revenue would later

have to be reversed.

73. This fraudulent revenue recognition practice violated GAAP (J122-133), and

materially overstated the Company's net income reported for year-end 2000, and the third quarter

of fiscal 2001. For example, as the Company later admitted, when net income was reported in

compliance with GAAP, the Company actually earned net income of only $63.3 million, not

$72.2 million. See Item 6, Selected Financial Data and Quarterly Summary, 10-K for the fiscal

year ended June 30, 2001.

74. Through the continued use of non-GAAP accounting, defendants were able to

artificially inflate the price of the Company's stock. In the April 26, 2001 press release,

defendants attempted to hide the fact that Sensormatic's revenue recognition practices were

fraudulent. Defendants announced that the Company would be adopting the "recently issued

provisions of SAB 101" in the fourth quarter of fiscal 2001. Defendants falsely stated that prior

to SAB 101, GAAP allowed the recognition of revenue for equipment sales upon shipment.

75. In fact, recognition or revenue prior to the time that customer acceptance

provisions had been met was never allowed under GAAP. See, ¶J122-133.

76. The statements detailed above were also materially false and misleading because

defendants knew, and failed to disclose that Sensormatic employees were deeply discounting

products at the end of each quarter in order to meet quarterly sales numbers. This practice is

considered material information which should have been disclosed to investors. See, ¶134

below.

-27-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 28 of 90

77. In addition, decreased sales trends were brought to the Company's attention for the

first time at the Company's Annual Product Forum Meeting in February 2000. At the 2000

Meeting, Bob Clucas put up a chart indicating that sales would be significantly lower after two

new sales roll-outs for Walmart and AutoZone were completed, and because no progress was

made during 2000 in identifying new products that Sensormatic could sell to boost sales to

retailers who were already saturated with Sensormatic products. ¶J38, 40, 43.

78. One of the reasons defendants' were issuing false financial statements was to post

a few good quarters and sell Sensormatic. Assaf was looking to sell Sensormatic for at least

three years. Executive employees at Sensormatic could receive huge cash bonuses if

Sensormatic were sold for a premium. See Proxy, November 17, 2000. According to an article

in the fall 2001 edition of Fastirack magazine, Sensormatic executives had "spoken with Tyco

three or four years ago. . . but the timing wasn't right." This year was different. According to

Assaf, "two friends, one a member of the Tyco board, the other a member of the Sensormatic

board met for dinner in early 2001" to discuss a "transaction of mutual interest." Id. Assaf was

personally involved in talks with Tyco from March through August.

79. On August 4, 2001, defendants announced that Tyco agreed to buy Sensormatic

for $2.3 billion in stock. The Sensormatic bail-out resulted in big gains for the defendants.

Assaf himself will receive a $1.56 million cash bonus and $7 million in Tyco stock. Loof will

receive a $3.3 million cash bonus - - equal to 344% of his annual pay, and $16.1 million in Tyco

stock. Other top executives will receive bonuses equal to 86 to 172 percent of their pay. Id at

48. In addition, Loof received a $1,000,000 loan from Sensormatic to purchase a home in Boca

Raton which will be paid off prior to the Tyco merger. See, Proxy, November 17, 2000.

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 29 of 90

The Company's Annual Report On Form 10-K

80. On September 28, 2000, defendants filed Sensormatic's Annual Report on Form

10-K for the fiscal year ended June 30, 2000. The 10-K reported an increase in revenues for

fiscal 2000 of 8.1% to $1,100.0 million from $1,017.5 million in fiscal 1999. The Report stated

that fiscal 2000 results reflect strong growth in the Company's Americas business unit, which

improved 10.6% with $678.0 million in revenues. For fiscal 2000, defendants reported $907.3 in

sales and net income of $72.2 million.

The Company's Annual Report On Form 10-K Was False And Misleading

81. The statements detailed above in ¶80 were materially false and misleading

because the financial results reported in the 10-K were overstated, as admitted in the Company's

April 26, 2001 press release and Form 10-K for the fiscal year ended June 30. 2001, by material

amounts:

NetJncomç (Loss)

As originally reported

As restated

Difference

2000 1999 1998

($ In Millions)

72.0 38.1

63.3 36.2

(30.9)

8.9 1.9

1.8

1991

(21.4)

(22.6)

1.2

82. The overstatements resulted from defendants' improper revenue recognition

practices, including recognizing revenue as a result of "try-buys". ¶61-63, 122-133.

83. The statements in the 10-K were also materially false and misleading for the

following reasons:

-29-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 30 of 90

(a) Defendants knew, and failed to disclose that Sensormatic employees were deeply discounting products at the end of each quarter in order to meet quarterly sales numbers; See, ¶134 below.

(b) The 10-K omitted any information of a declining sales trend. Indeed, by September 5, 2000, a former Marketing Manager had prepared the "Softgoods Sales Report which revealed that: (1) softgoods revenue was down by 16% in Fiscal Year 2000 (pg. 2); (2) that Department Store Gross Revenue was down 41% in Fiscal Year 2000; and (3) that CCTV, Ultra-Max and Microwave sales were all down substantially (See, chart on pg. 5 of report); ¶J48-53.

(c) The Report showed clearly that sales to Sensormatic's top ten customers were declining materially from 1998 to 2000 (See chart on pg. 6 of report); Id.

(d) The Report identified several adverse trends resulting from declining sales to major customers such as Sears, JCPenney, and Macy's; Id.

(e) The Report indicated that in Fiscal Year 1998, Sensormatic's top customer spent $11.2 million, and that in Fiscal Year 2000, the top customer spent only $4.9 million; Id.

(f) The Report failed to disclose that the Company's revenue recognition policies did not comply with GAAP and that the Company had been recognizing contingent revenue before it had been earned. Id.

84. On September 5, 2000, when the Softgoods Sales Report was finalized by the

former Marketing Manager, it was circulated to a large number of Sensormatic executives and

salespeople, including defendant Jerry Kendall - - who reported directly to Loof. Accordingly, at

the time the 10-K was disseminated to the market and filed with the SEC, defendants had adverse

knowledge of the Company's financial condition and prospects, and failed to include any

discussion of those trends in the 10-K.

Defendants' Fraud Continues In Fiscal Year 2001

85. On October 19, 2000, defendants issued a press release announcing first quarter

fiscal 2001 earnings per share. Defendants reported an earnings per share climb of 100%. The

press release reported that 'increased revenue and higher margins [drove] 6t consecutive quarter

-30-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 31 of 90

of improved results." The Company reported net income for the first quarter ended September

30. 2000 of $12.0 million, or $0.12 earnings per diluted share, compared with net income of $7.4

million, or $0.06 per share in the quarter ended September 30, 1999. Commenting on the

enormous rise in profitability, defendant Loof stated: "It is clear that our earnings improvement

continues as we remain focused on consistently delivering improved bottom line results."

86. On or about November 14, 2000, the Company filed its Form l0-Q for the quarter

ended September 30, 2000 with the SEC. This document (which was signed by Defendant

Gregory Thompson and which represented that, 'bin the opinion of management, all adjustments

considered necessary for a fair presentation have been included") was silent with regard to SAB

101 and omitted all disclosures required by SAB 75. J122-133. In addition, the MD&A section

of this Form 10-Q omitted any mention of the declining sales trend analyzed in the September 5,

2000 Softgoods Sales memo described above.

Defendants' First Ouarter 2001 Statements Were False And Misleading

87. Defendants' statements in the October 19, 2000 press release and November 14,

2000 10-Q were materially false and misleading for the following reasons:

(a) As later disclosed, defendants were improperly recognizing revenue through i.e., use of "try-buys." Correction of defendants' false statements ultimately resulted in a cumulative effect adjustment of $27.2 million, a pre-tax restatement of $43.3 million; ¶J 122- 133.

(b) Defendants were aware of, but failed to disclose the adverse trends detailed in the September 5, 2000 Softgoods Sales Report, which included a discussion of significant and continued sales declines ¶J48-53;

(c) Defendants were constantly apprised of actual sales figures, and Sensormatic's inability to meet its own, and Wall Street's financial estimates. Sensormatic employees Katrina Holcomb and Monica Young compiled a monthly and weekly sales forecast report based on information received from sales representatives in the field; ¶J54-60.

-31-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 32 of 90

(d) Defendants knew that sales were declining throughout the Class Period, including during the first quarter of fiscal year 2001. Holcomb and Young tracked sales on both a daily and weekly basis. Both had access to Sensormatic's computer systems and communicated with the salesmen in the field. Young and Holcomb reported to Chris Davell and Jerry Kendall. Dave!! and Kendall, in turn, held conference calls with Sensormatic's field people. Kendall and Davell reported "up the ladder" to Per-Olof Loof. ¶J 48-60.

88. Defendants also omitted any mention of Sensormatic's regular deep discounting

policy employed at quarter-end in order to meet estimates. According to a former Marketing

Manager for Sensormatic, the discounting decision was directed by sales managers, especially the

Eastern Regional Vice President, Ed Foley; the Western Regional Vice President, Steve Watson;

and the Divisional Vice President of Sales, Chris Dave!!. Some of the discount deals went to

Jerry Kendall, if the sale was big enough. According to the former employee, Sensormatic's

customers knew of this discounting policy and waited until the end of the quarter to make their

purchases.

89. Defendants failed to disclose these facts in order to post another quarter of

growth, and "deliver improved bottom line results" even if those results were false. Defendants

hoped to draw the eye of a purchaser for Sensormatic, including Tyco, with whom defendants

had begun negotiations years prior. Defendants knew that by posting a few good quarters, they

could regain market credibility and sell the Company, reaping enormous personal benefits.

The Second Quarter Of Fiscal 2001: The Fraud Escalates

90. On January 12, 2001. Sensormatic issued the following press release:

The Company.. .expects revenue growth for the second half of fiscal 2001 to be significantly greater than in the first half.

We are confident about the rest of the year and in our plans to address the issues we are facing," remarked Per-Olaf Loof,

-32-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 33 of 90

Sensormatic's president and chief executive officer. "The recent strengthening of the Euro and more favorable currency forecasts should result in accelerating revenue growth in the second half of the year.

Sales Growth in the total UltraMax product line of 16% and pending new contracts support our optimistic view.

91. The press release announced Sensormatic expected to report second quarter

revenue growth of 4% or approximately $281 million, which was less than previously expected.

The shortfall was attributed in part to "weakness in the Euro and other currencies." The press

release announced that EPS was expected to grow by approximately 20% or $0.20 to $0.21 per

share. Loof stated:

"Although it appears that our revenue and earnings will be somewhat lower than previously expected, our overall business is healthy and we expect to report our seventh consecutive quarter of results improvement."

92. On January 12. 2001, defendants held a conference call for the investing public

and analysts. On the conference call, Loof stated that "retail sales were sluggish" but reassured

investors that Sensormatic 's "EPS earnings projections remain the same. On a plan

perspective [Sensormatic] is on target." Loof added "we are holding to the year forecast that we

gave you [analysts] in August, of 35% earnings per share growth."

93. On the January 12 conference call, Loof was asked a question by analyst David

Katz and once again falsely emphasized that Sensormatic would have no trouble meeting

analysts' estimates:

[Katz]: If the street was looking for a buck 25 to a buck 27 a year out, you're not suggesting any changes to those numbers?

[Loofi: Right. We're not suggesting any change to that, and we're not suggesting any change, you know, to the 35% earnings per share growth for this fiscal year. I think this is a little bump.

-33-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 34 of 90

94. On January 16, 2001, Jeff Kessler of Lehman Brothers issued a report on

Sensormatic, stating: "This miss [$.04 lower in the second fiscal quarter than expected] will

more than likely be made up in the second half of the fiscal year as a stream of new contract

signings, some large and more take-aways from the competition, should be announced over the

next few weeks, which could provide naother boost to the stock." Kessler rated the stock a

"BUY."

95. On January 25, 2001, the Company also issued a press release announcing its

results of operations for its second fiscal quarter ended December 3 1, 2000. Sensormatic

announced that net income for its second quarter reached $19.2 million, or $0.21 per diluted

common share. EPS for the first half of the year period, the Company announced "This marks

the seventh consecutive quarter of improved results for the Company."

96. The January 25, 2001 earnings announcement also quoted defendant Loof,

Sensormatic's president and chief executive officer: "1 am optimistic that aggressive pricing in

our video division, new customer contracts and innovative product introductions will keep us on

track to meet our 35% earnings growth goal for the fully year, or earnings per share of about

$0.95.

97. On February 12, 2001. Sensormatic filed Form 10-Q with the SEC for the

quarterly period ended December 31, 2000 (the Company's second fiscal quarter). The l0-Q was

signed by defendant Gregory S. Thompson, CFO.

98. The l0-Q stated, with respect to Gross Margin and Operating Expenses:

The Company achieved a substantial cost reduction on hard tags used in the European markets by moving the production from Ireland to China. Also, by expanding capacity and continuing cost reduction efforts in its Boca Raton, Florida manufacturing facility, the Company increased production of source tagging labels while

-34-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 35 of 90

significantly reducing the unit cost. As the Company continues its focus on reducing manufacturing costs and improving overall processes, it expects to maintain the gross margin level at its 45% target for the remainder of the current fiscal year.

99. On January 26, 2001, Lehman Brothers (Jeff Kessler), ranked the stock a

"STRONG BUY."

100. On February 9, 2001, Ryan Beck (Peter R. McMullin) issued a "STRONG BUY"

rating for Sensormatic shares. The report predicted $0.21 per share earnings in third fiscal

quarter, as a result of "managements' guidance."

101. Notwithstanding these positive statements, the following Sensormatic insiders

sold their stock between February 5, 2001 and March 13, 2001: William J. Bufe (Vice President

and Controller); Jerry T. Kendall (Senior Vice President, North American Retail); Kenneth W.

Chniiel (Senior Vice President, Supply Chain Operations and EAS Product); Walter A. Engdahl

(Vice President Corporate, Counsel, Secretary); Stephan Cannellos (Vice President and General

Manager, ACD); Ronald G. Assaf (Chairman of the Board of Directors); Timothy P. Hartman

(Director); Thomas Vigus Buffett (Director). The total amount of selling during this period by

these insiders was $7,980,151, as detailed below:

-35-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 36 of 90

INSIDER SALES 3

DATE INSIDER STOCK PROCEEDS

215101 William J. Bufe $59,250 (VP, Controller)

2/9/01- 2/12/01 Jerry T. Kendall $1,898,093 (Senior VP, North American Retail)

2/22/01 Kenneth W. Chmiel $445,438 (Senior VP, Supply Chain Operations and EAS Product)

2/23/01 Walter A. Engdahl $221,900 (VP Corporate, Counsel, Secretary)

3/2/01 Stephan Cannellos $457,440 (VP and General Manager ACD)

3/5/01 - 3/7/01 Ronald G. Assaf $2.002.500 (Chairman of the Board, Director)

3/8/01 -3/13/01 Timothy P. Hartman $1,579,312 (Director)

1/26/01, 3/8/01- Thomas Vigus Buffett $418,096 3/9/01 (Director)

TOTAL SALES PROCEEDS:

$7.980J51

Many of these sales were through the exercise of options. A complete analysis of the options and profits from the options, which total over $1.6 million, is attached as Exhibits "D" -

-36-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 37 of 90

Defendants' Second Quarter 2001 Statements Were False

102. Defendants' statements detailed above touting strong financial results were

materially false and misleading. Despite Loofs emphasis on Sensormatic's ability to meet the

35% earnings growth goal for the entire year (or EPS of $0.95), defendants knew these

statements were baseless.

103. According to the former Marketing Manager, Sensormatic's second fiscal quarter

(ending December 31, 2000), was prepared some time in February or March 2001. The sales

report set forth the sales results of October through December 2001 and discussed predictions for

the fiscal third quarter of 2001 (ending March 30, 2001).

104. The quarterly sales reports stated that sales were down for the second fiscal

quarter of 2001 and looking into the third fiscal quarter of 2001, sales were down as well.

According to the former Marketing Manager, sales were down for at least two reasons: (i) the

Wal-Mart installation was coming to an end or was over by this time, and (ii) the general retail

climate was down. Retailers typically re-used Sensormatic's products which reduced the number

of new sales of tags Sensormatic could make to retailers. These retailers included The Gap, all

Federated Department Stores, such as Burdine's, Macy's, Bloomingdale's, music chain stores

such as Mars, and the larger retail chains, namely The Limited, Abercrombie & Fitch, all the

May Department Stores, such as Foley's, May Stores, Lord & Taylor and Dillards. The former

employee stated that some tags can last from ten to fifteen years.

105. According to this former employee, the fact that sales would be down in the

Companys third fiscal quarter (January to March 30, 2001) was not a surprise to anyone at

Sensormatic. By late December 2000, defendants Loof, Kendall and Chmiel, as well as Dennis

Constantine, senior vice president, were directly aware of the probability of decreased fiscal third

-37-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 38 of 90

quarter sales because they received a copy of the employee's quarterly report, described above,

which identified the adverse sales trends. In addition, Sensormatic had a Quarterly Review

Report which was prepared in hard copy form. The report was presented orally to the entire

executive team, including Loof, Kendall, Chmiel and Constantine.

106. At the time of defendants' statements above touting the "seventh consecutive

quarter of improved results", defendants were also aware of the following adverse facts which

made their statements false:

(a) Sensormatic's sales had "been off" during the entire 2001 fiscal year, according to a former Marketing Manager. Sensormatic employees "all knew in late December 2000 that the next quarter "was going to be bad." Defendants knew that retail customers such as The Gap and Federated Department Stores were having problems selling to retailers, and did not have the budget to purchase Sensormatic products; ¶T48-5 3.

(b) During a February 2000 Annual Product Forum Meeting, Bob Clucas brought up decreased sales trends which indicated that sales were decreasing unless the Company could come up with new products; Id.

(c) Defendants received regular quarterly sales reports which indicated that sales and revenue numbers were down from January through March 2001; ¶J54-59.

(d) Defendants were aware of Sensormatic's actual declining sales figures by virtue of weekly and monthly reports and forecasts, which they were also able to access through the computer systems; ¶J54-60.

(e) Defendants received the September 5, 2000 Softgoods Sales Report which Kendall and Chmiel described specific adverse sales trends - - trends which remained undisclosed; 48-53.

(f) An article in the Sun-Sentinel, dated April 11, 2001, disclosed, as alleged below, that the Company was then discounting product sold by its Video Division to make up for the reduction in sales Sensormatic was then experiencing. ¶119.

107. Similarly, the Form 10-Q was false and misleading because it made no disclosure

in the Management's Discussion and Analysis Section or elsewhere regarding the lower retail

No

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 39 of 90

sales Sensormatic was then experiencing.

108. On February 19, 2001, Sensormatic issued a press release announcing that

Vitamin Shoppe, a specialty retailer of vitamins, would install Sensormatic's UltraMax anti-theft

system in all 90 of its stores as a first step toward implementing a chain-wide source tagging

program. Jerry Kendall was quoted in the press release as saying: "source tagging has made

impressive inroads among retailers because its advantages are hard to ignore. Retail tests have

shown that source tagging with UltraMax decreases theft while increasing sales." "Those are two

main reasons why UltraMax has become the fastest growing anti-theft technology around the

world."

109. On February 21, 2001, Lehman Brothers (Jeff Kessler) issued a "STRONG BUY"

rating on Sensormatic shares and a June 2001 price target of $25 per share.

110. On February 26, 2001, Sensormatic announced in a press release that it had

acquired Controlled Electronic Management Systems, Ltd. of Belfast, Northern Ireland along

with its parent Company Intellectual Systems, Ltd. "In addition to the range of technology this

acquisition brings to Sensormatic. "the press release stated, "CEM Systems professional staff of

hardware and software engineers along with its network personnel will further strengthen

Sensormatic's future development efforts."

Ill. Two days later, Sensormatic held its annual product forum on February 27, 28 and

March 1, 2001 at the Embassy Suites Hotel on Yamato Road in Boca Raton, Florida, described

above.

112. As set forth above, within afeiv days of the end of this sales forum, defendants

Cannellos, Assaf, Hartman and Buffett had together sold millions of dollars of their Sensormatic

stock, from March 3 to March 9, 2001.

-39-

Case 9:01-cv-08346-DTKH Document 15 Entered on FLSD Docket 10/16/2001 Page 40 of 90

113. On March 27, 2001, Lehman Brothers (Jeff Kessler) again issued a "STRONG

BUY" rating on the stock. The report made the case for Sensormatic's continued growth and

vitality during economic slowdowns and recessions, explaining that the UltraMax product saves

retailers money by reducing inventory "shrinkage" or employee theft of product. The Lehman

report continued to estimate EPS for Sensormatic's third fiscal quarter (the period ending March

31, 200 1) at $0.20 per share, up 49% for the same period one year prior.

114. On March 29, 2001. Sensormatic issued a press release announcing its acquisition

of Richmond Security Limited, based in Leeds. U.K. The press release stated:

"Richmond has been a valued business partner of Sensormatic for several years and has helped increase our customer base through the sales of our UltraMax® technology and video surveillance systems to some of the U.K.'s leading retailers," said John Smith, executive vice president of Sensormatic's Europe, Middle East and Asia/Pacific Operations. "Through this acquisition, we now have the reach to sell our products to an even broader market."

115. On April 4, 2001, Sensormatic issued a press release announcing its acquisition of

the assets of BEC Technologies, Inc. of Orlando, Florida. The acquired company designs,

manufactures and markets a combination of hardware and software to provide fiber optic