masterclass pe fundraising prof. luc nijs founder & chairman horizon ltd geneva july 2, 2009...

TRANSCRIPT

Masterclass PE Fundraising

Prof. Luc NijsFounder & Chairman Horizon Ltd

Geneva July 2, 2009ICBI Super Return Emerging markets Conference

How today will look like (more or less)

9.30-11.00 Data reviewStructural

considerations and applications 11.15-12.30 Terms & conditions (I)

13.30-14.15 Terms & conditions (II) 14.30-16.00 EM PE as an asset class 16.00-16.30 Wrap-up, Q&A and

discussion

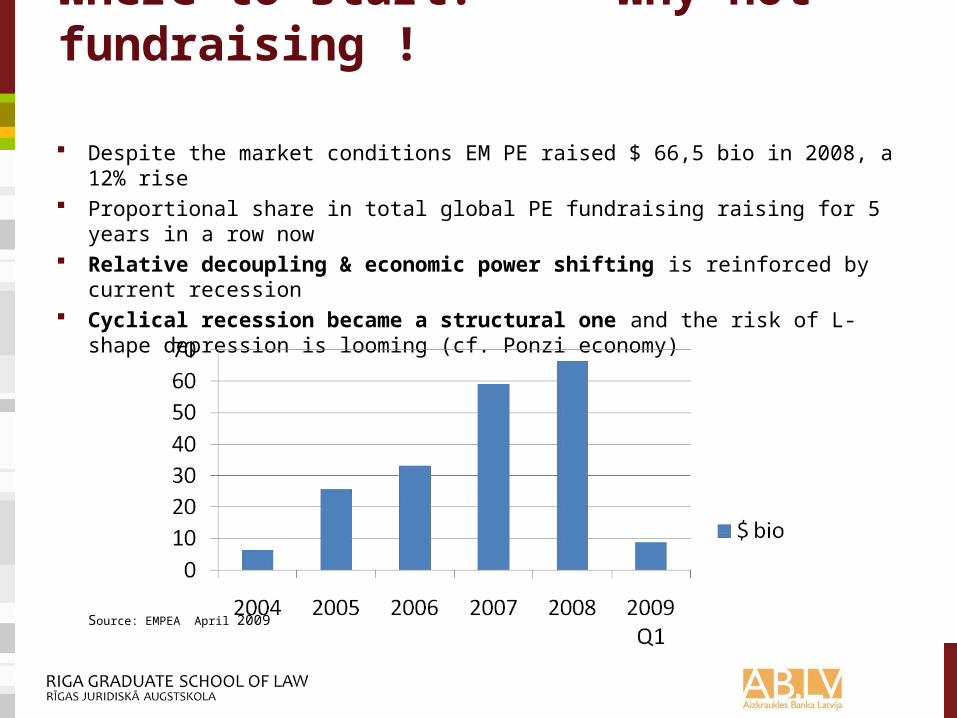

Where to start? Why not fundraising !

Despite the market conditions EM PE raised $ 66,5 bio in 2008, a 12% rise

Proportional share in total global PE fundraising raising for 5 years in a row now

Relative decoupling & economic power shifting is reinforced by current recession

Cyclical recession became a structural one and the risk of L-shape depression is looming (cf. Ponzi economy)

Source: EMPEA April 2009

Fundraising per region

Market outlook for fundraising

Market Outlook

A few conflicting data:

Preqin (April 2009): US leads the way with 23 bio $ Europe 20,2 bio $ EM 2,7 bio$

Lot of funds postpone final closing Development finance will focus more on

direct investing (FOM,…) Force of consolidation coming in 25-50% of GPs are struggling for survival

Market outlook for EM fundraising

The LP ViewSurvey April 2009

94%

6%

Yes

No

Would you consider committing to Emerging Market funds?

50%

50%

Yes

No

Would you invest with a Global Emerging Market Fund?

95%

5%

Yes

No

Would you consider Local Emerging Market Funds?

9%

30%

45%

7%

9%

Africa

Asia Pacific

Latin America

Middle East

Which Region would you invest in?

Russia

5%

43%

8%

18%

8%

13%

5%

Australia

Brazil

China

India

Which emerging country would you invest in?

MENA

Russia

South Africa

Investors stay committed…but…

Some of the underlying fundamentals

What about the converts…

Market Outlook

Argumentation for refusal of EM proposition: (Short-term) EM risk Lack of experience in EMs Only few quality GPs available in EMs

Quantitative easing and systemic risk?

Some of the underlying fundamentals

A (new) inconvenient truth about risk

Political instability

Legal / Regulatory

Curreny (F/X)

Market fundamentals

Counterparty

Market fundamentals

Structural issues

Environmental

Legal / Regulatory

Pre-crisis Thinking

Post-crisis Thinking

Em

ergi

ng M

arke

tsD

eveloped Markets

High RiskHigh Growth

High RiskHigh Growth

High RiskLow Growth

Low RiskLow Growth

Emerging Markets Risks Developed Markets Risks

Av. risk premiums in EMs (%, 2008-2009)

Another inconvenience

Capital inflows to developing world

(Source: IFF, 27 January 2009)

Historic & projected EV/EBITDA

Source: Prop. Research, averages for the clusters

Something else that is inconvenient

Past performance & GP selection

Institutional investor views: EM versus developed (December 2008)

Institutional investor views: EM versus developed (April 2009)

Portfolio allocation

PE penetration as an asset class

Source: Goldman Sachs, EMPEA

Portfolio exposure

Reasons for expansion or continuation

Source: EMPEA 2008

EM Private Equity performance

Source: Cambridge Associates LLC & prop. research,: pooled end-to-end returns, net of fees, expenses and carried interest

Comparative end-to-end results 6/30/2008

(*) Statistical noise likely due to low sample distribution

Source: Cambridge Associates LLC & prop. research,: pooled end-to-end returns, net of fees, expenses and carried interest

Impact on portfolio construction

In 2008 about 1/3 of the total pool of LPs had some kind of exposure to EMs

Portfolio weighting somewhere between 10-30% Do or die for LPs the next couple of years Systemic risk in Western markets are not reflected in risk premiums

Source: Proprietary data

Smoke & mirrors… BVCA and E&Y 2008 performance study

A disaster waiting to happen

So now what…

If PE is an activist shareholders’ position than why have these funds been managed as investment vehicles

Demonstrate inept to manage companies Focus on financial engineering Models have to change

Fund structure Terms & conditions Exit modeling Valuation and transparency

So now what…life after leverage

Value creation/operational side Impact of average /holding periods Massive room for improvement of private capital formation Put capital to work But do they have the right ‘human capital in place’?

Is this time going to be different for EMs?

During previous booms and busts the developed and developing world evolved in a parallel fashion

This time there is a (partly) contra-cyclical pattern

Political & regulatory impact Global versus local teams: the best of both Business model rethinking & paradigm

shift EM debt usage less or more prudent

Is there something we can learn

from the past?

Natural questions

Is this a crises like every other or a profound shift?

How will the industry evolve in the next decade?

What are the implications for the asset class? What is the position of EM propositions within

this space? What is the impact on portfolio management

and allocation Can we learn something that might affect the

fundraising effort?

This talk

Will seek to answer these questions by looking backwards

Traditionally, very hard to understand key drivers of private equity success

In recent years, much more information Drawing on large-sample and case

evidence Thoughts about future of private equity

more generally… And particularly in new private equity markets

Everyone does about the same

Frequent claim among investors: Emphasis on balancing portfolio by:

Type of fund Location of fund Vintage year

Similar to what’s seen in public market investing

Recent work

Has sought to understand how much difference is… Between fund classes Between funds

Seeking to distinguish importance of individual performance

0% 5% 10% 15%

PrivateEquity

EquityFunds

Bond Funds

Difference BetweenTop and BottomQuartile

Evidence from the Yale endowment

Source: Lerner [2003]

More general patterns

0%

5%

10%

15%

20%

All Private Equity Venture Capital Buyouts

Source: Kaplan and Schoar [2005]

The reality

The key difference is between different funds: Unlike public markets

Investing in the right categories is not nearly as critical as getting into the right companies!

“Regression to the mean”

Frequently heard stories… “Our last two funds were a

disappointment, but we’re getting back on track…”

“I considered investing in the fund, but I decided that their success must be a fluke...”

Recent work

Has sought to understand nature of performance: Is there little continuity from quarter-to-

quarter? Many studies of public markets suggest little

persistence: Mutual funds Hedge funds

Or is the reality different?

Persistence of performance

Bottom Medium Top

Bottom Tercile 61% 22% 17%

Medium Tercile 25% 45% 30%

Top Tercile 27% 24% 48%

• High likelihood that the next funds of a given partnership stays in the same performance bracket Persistence

• 1% boost in past performance → 0.77% boost in next fund’s performance

Source: Kaplan and Schoar [2005]

The reality

Performance seems to be very “sticky”: Good continue to do well Underperformers continue to do so

While exceptions, seems to be the basic rule: Seen in buyouts as well as venture

Growth doesn’t hurt

Numerous venture groups have grown dramatically. Mid 1980s and late 1990s.

Recent dramatic growth by buyout funds Have typically argued that can sustain

performance despite growth But powerful incentives to grow may induce

skepticism Market is now clearly turning away from the at

this stage

Fund sequence number

• Positive relationship between IRR and fund sequence number

• First time funds perform especially poorly

• Regression results control for vintage year effect, fund category and fund size

IRR and Fund Sequence Number

0

5

10

15

20

25

1 2 3 4 5 6 7 8 9 10 11

Sequence Number

IRR

Source: Lerner and Schoar [2005]

Fund size

Concave relationship between IRR and fund size

Fund size is measured as capital committed at closing

Regression results control for vintage year, fund category

Relation IRR and Fund Size

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10 11

Fund size in $100 million

IRR

Source: Lerner and Schoar [2005]

• Negative relationship between change in IRR and change in fund size for a given firm

• Fund size is measured as capital committed at closing

• Regression results control for vintage year effect, fund category, and firm fixed effects

Change in fund size

Source: Lerner and Schoar [2005]

• Positive relationship between IRR and the ratio of partners to committed capital

• Regression results control for vintage year effect, fund category, and fund size

Partner to size ratio

IRR and Partner to Size Ratio

0

5

10

15

20

25

30

0 0.2 0.4 0.6

Number of Partners to $100 million in committed capital

IRR

Source: Lerner and Schoar [2005]

• Positive relationship between IRR and the ratio of partners to total staff

• Total staff includes associates, principals etc, excludes purely admin. positions

• Regression results control for vintage year effect, fund category, and fund size

Partner to total staff ratio

IRR and Partner to total staff ratio

0

2

4

6

8

10

12

14

16

0.1 0.3 0.5 0.7

Number of partners to total staff

IRR

Source: Lerner and Schoar [2005]

Difference in deal success rate

0%

1%

2%

3%

SpecializedFirm with

SpecializedPeople

GeneralistFirm with

SpecializedPeople

GeneralistFirm with

GeneralistPeople

Specialist firms are more likely to have successful deals I.e., 30% vs.

32.1% vs. 33.1%.

Partners’ focus especially matters

Source: Gompers, Kovner, Lerner and Scharfstein [2005]

Returns: Disparity between recent past and historical pattern

0%

5%

10%

15%

20%

25%

10/86-9/06 10/03-9/06

Small FundsMedium FundsLarge FundsMega Funds

Source: Venture Economics

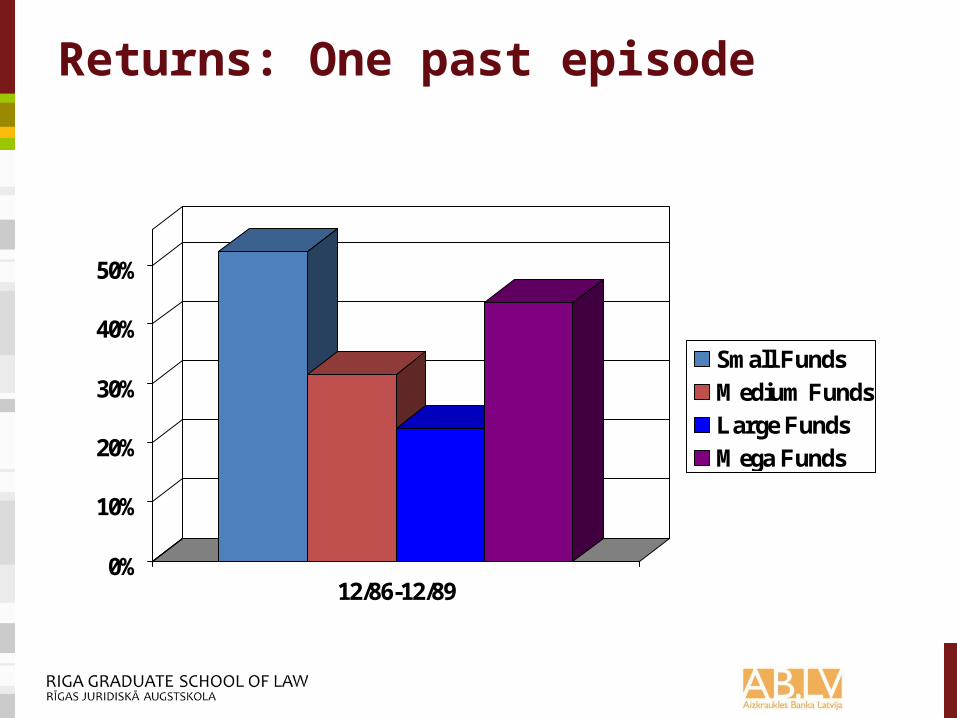

Returns: One past episode

0%

10%

20%

30%

40%

50%

12/86-12/89

Small FundsMedium FundsLarge FundsMega Funds

Source: Venture Economics

One past episode (continued)

0%

10%

20%

30%

40%

50%

12/86-12/89 12/89-12/92

Small FundsMedium FundsLarge FundsMega Funds

Source: Venture Economics

The reality

Funds with higher sequence number, i.e., established funds, perform better

Larger funds have better performance—to a point Rapid growth in capital under management is

associated with performance deterioration May be driven by less impact of partners:

Funds with more partners per dollar managed have higher returns

Funds with higher partner-to-non-partner ratio have higher returns

Decline in specialization leads to poorer performance

Anyone can play

Lately, great deal of interest from new investors: Public pension funds Non-U.S. governmental entities

Attracted by high returns that established investors have enjoyed

Recent research

Has sought to understand the differences between investors Does everyone do the same? Or are there substantial differences?

Key data: LP investment decisions Fund returns GP and LP characteristics

Performance summary

Substantial performance differences: ~13% differential in annual returns

between endowments and next best Entirely driven by early- and late-stage VC

Advisors and banks particularly poor Patterns true when weighted as well

Performance by investor type

-5% 0% 5% 10% 15% 20%

Endowments

Private Pensions

Insurance Companies

Public Pensions

Advisors

Banks

Source: Lerner, Schoar and Wang [2005]

Concerns with univariate tests

Do these reflect other differences: E.g., endowments early investors and

more heavily weight VC Examine through regressions:

Regress IRR on fund and LP characteristics

Only include <1999 funds to insure meaningful performance numbers

Regression analyses

Differences persist: Endowments outperform; corporate

pensions and banks underperform Proximity negatively associated with

performance Younger LPs do worse:

At least among advisors, banks, corporate pensions, and insurers

Regression analyses (cont’d)

Market inflows: Negative in general Especially for advisors, corporate

pensions, and insurers. Hot markets appear to lead to more herding

by these investors Question: Does a bear market have the

same effect?

Reinvestment decisions

Reinvestment decision should be made with better information and without access constraints

Look at follow-on funds in our sample: Only look at same classes of funds

Statistics on reinvestment

Reinvestment rates differ: Public pensions, insurers higher Higher in VC than buyouts

More likely to reinvest when high IRR Next fund has higher IRR when reinvest

Reinvestment (continued)

Pension funds and advisors tend to invest when current returns are high

But much more dramatic difference in future returns from endowments Also smaller funds

Substantial differences in ability to identify or act on inside information

Reinvestment and current returns

0

10

20

30

40

Advisors Banks CorporatePensions

Endowments PublicPensions

Reinvested

Did Not Invest

Source: Lerner, Schoar and Wang [2005]

Reinvestment and future returns

-10

0

10

20

30

40

Advisors Banks CorporatePensions

Endowments PublicPensions

Reinvested

Did Not Invest

Source: Lerner, Schoar and Wang [2005]

Is access an explanation?

Do endowments do well because they were “there first”?

Other way to look at: Funds that were undersubscribed Funds which took a long time to raise

Same patterns appear!

The reality

Huge disparities in performance. Superior performance has been largely

confined to endowments. Raise substantial questions about ability of

new entrants to succeed.

Summary

Funds with higher sequence number, i.e., established funds, have performed better→→Lesson: Being early is critical

Rapid growth in capital under management was associated with performance deterioration May be driven by organizational challenges:

Funds with more partners per dollar managed have higher returns

Funds with higher partner-to-non-partner ratio have higher returns. Decline in specialization leads to poorer performance

→Lesson: Managing growth is major challenge

Investors have had wildly uneven returns.→Lesson: Having right investment partners

matters

The special challenges of new private equity markets Lessons from Celtel, Skype and Shanda:

HBS field cases written on all three

Represent Africa, Europe and China

The checks have cleared!

All markets are global

Skype’s business model depended on consumers calling across borders

Celtel’s pan-African strategy attracted international telecoms equipment companies to become second largest source of financing

Shanda’s revenues were more than 80% dependent on a game written and owned by a Korean company

Expect deals to be massively more work intensive

Skype’s code was written in Estonia, the management team was spread throughout Europe, the customers were all over, and the founders could not travel to the US

Celtel needed to raise over $400mm from 2001 to 2004 during the meltdown of the telecommunication investing markets—all of it to be spent in Africa

Shanda was threatened by a lawsuit from the Korean vendor whose game accounted for most of their revenue

Back to basics

Skype’s founders had control over a sale

Celtel had minority partners in all 15 of its operations (i.e.: 15 different groups in 15 different African countries). It also had an all common stock equity capitalization

Shanda management was furious that SAIF sold some stock after the IPO

The real value added is transparency

Skype owned its technology as a result of the VC investment

Celtel had a prestigious board who insisted on transparency and openly refused licenses that had the taint of corruption

Shanda’s settlement with its key vendor was negotiated by SAIF

Luck still counts

(this space intentionally left blank)

Advice: Top tier firms must be global

LPs will prefer to go global with people they know, but will be skeptical about execution—so they will pursue a mixed model

The top tier firms will need to be global to maintain top tier status—there is simply too much information they would otherwise miss, and the overseas growth and return rates will be higher than US return rates

Global top tier firms will outperform local top tier firms over longer periods of time

Brands will likely cross borders but are no guarantee of success

Advice: Tourist VCs will not be successful, you must be on the ground

Act global but think local.

Local, permanent, day in, day out presence is an absolute must

Advice: The industry will not be replicate that in the U.S.

Less developed PE markets require much more resource on each deal

Investment strategy may vary from location to location:

Less of a premium for early stage investing in less developed markets

Advice: There are no settled models for running a global private equity firm

Lots of models to choose from: Large PE firms provide useful models of

satellite offices There are interesting models of building an

affiliate firm with different GPs and LPs (Accel, Benchmark);

There are many examples of investment in independent firms (Chengwei, Argnor)

But no set answers yet Keys to success: communication among

investing partners, expectation setting between offices, portfolio management globally

Advice: You can’t do this on the cheap

Must be approached with the same intensity and vigor and commitment as your most important initiative

Advice: The key company value builder is transparency

Exits are through one global market, whether they are M&A or public floats (NY/London)

This is the lesson of the 60’s and 70’s all over again: don’t treat portfolio companies as small companies, treat them as large companies who happen to be small right now

PE firms will need to stockpile management talent and keep overseas offices staffed well enough for frequent, persistent oversight of portfolio companies

Five Easy Pieces (of Advice)

1. Top tier firms must be global Global top tier firms will outperform local top tier firms over longer

periods of time

2. Tourist VCs will not be successful, you must be on the ground

3. Overseas industry will not be replicas of U.S. There are no settled models for running a global private equity

firm

4. PE Firms can not go global on the cheap Must be approached with intensity, vigor and commitment.

5. The key company value builder is transparency Teaching the culture of minority equity ownership may be the

lasting legacy of US venture capital.

An appreciation of the current state of play

Despite the record write-offs, liquidity constraints (distribution drought & the denominator effect) and possible defaults LPs are facing there seems to be a continued interest in the asset class.

UK pension fund association (April 2009): continued support for the PE environment through allocations

CalPERS to put less in stocks, raise bet on private equity (June 2009)

Role of private equity in institutional investor portfolios to increase, says fund of funds manager Adveq (June 2009)

An appreciation of the current state of play

Short-term tough with limited visibility LP momentum How to manage a new equilibrium What is the new ‘normal’ How do normal people behave in

‘abnormal times’

Fundraising efforts

First-time fund (infra) Follow-up fund Who are you as a team/organization? Track record

What is considered important

Survey institutional investors by BNY Mellon (May 2009)1. Alignment of interests2. Transparency3. Performance4. ….5. ….

Do you have a fundraising strategy?

Who do you want to approach?

UHNWI Family offices Pension funds Insurance funds Endowments SWFs FoF Other institutional investors In the West or in EMs

Are EM LPs different than their Western peers Better understanding of EMs? More sensitive to (Western) brand

association when selecting GPs Diverting capital flows during crunch times

(reversed globalization) Quite often larger allocations than

Western peers Often faced with regulatory restrictions Lack of transparent decision-making and

communication process

And what do you know about them?

In particular: Their asset allocation program Geographical coverage Recent performance Their understanding and experience in

PE and alternative assets Consistency of in-house team Timeline of their liabilities

F.e. defined benefit vs. defined contribution plans

And who are you as a sponsor?

What have been your previous fund strategies?

Regional/country versus global? Single- versus multi-industry approaches Open ended or closed funds How are you organized? Who is doing fundraising? Fulltime? Do you have Investor relationship managers? What kind of communication protocol do you

have in place?

What comes first?

Putting the whole structure in place Or raising funds and when feasible put

stuff in motion?

The latter occurring more often recently given the uncertainty in the fundraising cycle

The use of FoF Everybody has its own agenda Is there still place for FoFs in an economic

environment where things are ‘back to basic’ Only very few FoFs have decent EM experience

(despite what they tell you) Do you want to invest someone’s money you

don’t know (remember Bank of NY Mellon survey) What kind of mandate do they have? Did they (FoFs) deliver for their investors? Let’s look at the reasons why they exist anyway?

The use of FoF

Avoid them if you can Not instrumental for your business going

forward

Reality is a bit against my position: In hedge fund space 50% of

commitments come through FoF (but are more specialized as well)

‘Hot money’ issue is something you want to avoid

UHNWI

Easier to build a relationship with But reality tells us that given the time lag

between commitment and ‘draw down’ defaults are more common than with institutionals

Often need a feeder fund to facilitate smaller commitments

Your LPs

Do you believe it is your job to educate them? On emerging markets? On the asset class? On expectation re returns?

The value-add of placement agents

Besides raising capital by putting their Rolodex to work

Expansion of LP network beyond your core geographies

Market your fund knowing local cultures re fundraising and investment strategy

Add value towards PPM and content

The value-add of placement agents

How to position the fund towards investors Pinpoint a meaningful amount to be raised Coordinate road shows and be more efficient Make your fundraising more efficient Pimp up your marketing materials What are the internal processes you have to

go through Match LPs with your investment strategy-Who

is buying what? Moving headcount among LPs

First-time funds

Feels often like climbing the Everest without oxygen

Team-up with existing player Work with non- financially focused LPs Include anchor investors

LPs are not there to create a barrier to entry Most LPs have boilerplate DD processes

whatever they proclaim

What are they looking for

Structure

Track record In what? Barrier to entry Why is it so important? Sometimes legal constraints by institutional

investors Impressive team & people versus track

record? Funds perform consistent within quartiles History tells us something about the future In particular important in environment where

new GP have been mushrooming

Strategy

ESG principles in EMs: risk management or value creation?

In what strategies would that show up? Real issue in relation to EMs Are they all executed the same way Relevant for your portfolio companies but

also for yourself as a GP

Team

What is the DNA of your team? What is the set-up of the team? Locations? How is decision-making shared? How is the carry shared? Stability- How are you going to execute your

strategy Is your team ready for the ‘new normal’ ..i.e.

generating returns by improving operations and creating synergies rather than leverage

Can your HC live up to that test?

Team

The HC rainmaker paradox Human Capital center of excellence

Retention Change management Compliance Organizational Development Recruiting Sourcing Resource Development

The due diligence process They will tell you that they have a very

sophisticated system which is thorough and even groundbreaking

Reality is that most of the process is boilerplate and based on gut feeling

Some of them will not go beyond your track record

That way great time ‘first-time funds’ are missed out on

Be aware of those that tell you the are interested in emerging markets but have never made an allocation before

The due diligence process Manage the timeline It can also help you emerging your true

potential Often external advisors are hired to execute the

DD Re-run of older fund number to measure

accurateness What are they looking for?

Besides everything discussed Deal flow origination capabilities Exit strategies

The due diligence process

Important given the high dispersion of results in the asset class

Excess returns depend largely on manager selection

Identifying risk and relating then to the return capacity of any given manager against the background of competing investment opportunities

The due diligence process Size, geography and strategy screen Formal part starts with a meeting Following that the LP will (in)validate the

investment thesis through Site visits at GP and some portfolio

companies Reference checks with existing LPs, portfolio

company management team, etc Track record analysis Market positioning analysis Review of legal conditions

Terms & conditions

Compensation 2 & 20 Alternatives? After the investment

period? Imputing transaction fees by GP?

Source: SJ Berwin AS 2009

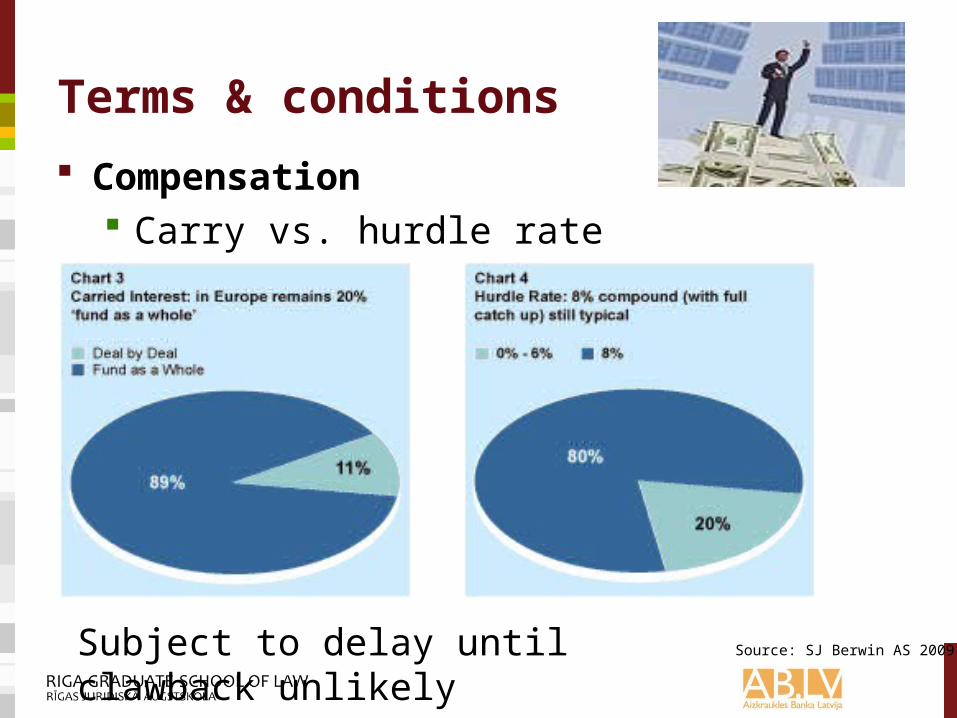

Terms & conditions

Compensation Carry vs. hurdle rate

Source: SJ Berwin AS 2009Subject to delay until clawback unlikely

Terms & conditions

Fund structure Open or closed fund structure Key terminology Basic considerations Master/feeder structure What types of vehicles to use European vs. US vs. EM investors ? You can’t be everything to everybody Offshore structures(?)

Are you the danger zone after the G20

Terms & conditions Fund structure

Tax transparency Limited liability for LP and GP Authorization and/or regulation of fund and

manager Does it support an alignment of interest

between GP and LPs Tax-efficient structuring of man. Fees and carry Nature of co-investment arrangements Permanent establishment & operational issues

Terms & conditions

Fund structure Combining structures is an option Increases complexity and costs but will

appeal to a wider range of LPs

Terms & conditions

Governance EM GPs have reduced track record relative

to their Western peers Different regulatory environment and legal

protection of shareholders/partners Common law vs. Rule of law systems Role of the Investment committee’s

liabilities and responsibilities Pinning down investment policy to prevent

style drift

Terms & conditions

Managing expectations Re future returns Re existing funds

Re the latter: Re-invest proceeds of realizations,

including an ability to re-draw proceeds already distributed

Extended investment periods or reopened a closed fund to new capital, while some have raised annex or top-up funds

Terms & conditions

Managing expectations: distressed situations Allow (some) investors to scale down

commitments in exchange for some dilution of their interest?

Do you know where you fit in your LPs portfolio?

Terms & conditions

Communication strategies: LPs are your primary clients…ALWAYS!!! How, how much and on what? Portfolio valuation? Deal affairs Quarterly scorecards? Watch how you communicate as it is

determined by your overall objective re the relation with your LP/LP community

Key components of a good IR program?

Terms & conditions

No-fault divorce? Once again downward protection

mechanism Big deal or not?

Terms & conditions Who are your advisors?

Do they shine off on you? Madoff Stanford and the likes

Bring them in for hot issues: Valuation of the entire portfolio once a year Structuring the deal

Don’t be stingy: bring in the big guns-it will pay off

What do you want your lawyers to do Selecting a law firm

Terms & conditions

Co-investment rights?

Benefits Detriments Limits Consequences going forward

Terms & conditions

Co-decision rights?

Independence versus commitments Value of independence Board of advisors vs. Investment

committee Who is the captain on your ship? Under what conditions Financial conditions for anchor investors?

Terms & conditions

The Private Offering Memorandum

Purposes of the offering memorandum Stages in the life of the offering

memorandum Sponsor considerations Contents of the offering memorandum Key terms Marketing and regulatory considerations

Terms & conditions

The Private Offering Memorandum

Material omissions Compliance with securities laws for

private placement of securities What does it serve: (1) market the fund

and (2) describe risks to avoid liabilities, (3) facilitate due diligence

Terms & conditions

Risk management in EM Creating alpha? What is the system you’re going to use? How to deal with non-economic risk Does Value-At-Risk work the same way

here Designing your own system is probably

more authoritative

Risk management

(*) Corruption, Legal systems, Enforcement policies, Accounting transparency & Regulatory transparency and quality

(**) Deutsche Bank Eurasia Group Stability Index

(*) Corruption, Legal systems, Enforcement policies, Accounting transparency & Regulatory transparency and quality(**) Deutsche Bank Eurasia Group Stability Index

Terms & conditions

Put your money where your mouth is How much do you support the fund with your

own money? Difficult one for first-time-funds

Co-investing in deals by partners privately? Cross-fund investing not appreciated by LPs

Terms & conditions

Distributions and balancing carry

Avoid clawbacks Fund or deal level Re-investment periods … Redemptions under what conditions

Contact

Riga Graduate School of LawLaw & Finance ChairStrelnieku iela 4k-2

Riga LV-1010LATVIA

[email protected]. +37167039230