mathematics of finance - inter · barnett/ziegler/byleen college mathematics 12e 2 learning...

TRANSCRIPT

Chapter 3

Mathematics of

Finance

Section 3

Future Value of an

Annuity; Sinking Funds

2 Barnett/Ziegler/Byleen College Mathematics 12e

Learning Objectives for Section 3.3

The student will be able to compute the future value of an

annuity.

The student will be able to solve problems involving sinking

funds.

The student will be able to approximate interest rates of

annuities.

Future Value of an Annuity;

Sinking Funds

3 Barnett/Ziegler/Byleen College Mathematics 12e

Table of Content

Future Value of an Annuity

Sinking Funds

Approximating Interest Rates

4 Barnett/Ziegler/Byleen College Mathematics 12e

Terms

ordinary annuity

future value

sinking funds

5 Barnett/Ziegler/Byleen College Mathematics 12e

Definition of Annuity

An annuity is any sequence of equal periodic payments.

An ordinary annuity is one in which payments are made at

the end of each time interval. If for example, $100 is deposited

into an account every quarter (3 months) at an interest rate of

8% per year, the following sequence illustrates the growth of

money in the account after one year:

2 3

0.08100 100 1 100 1.02 (1.02) 100(1.02)(1.02)(1.02)

4

100 100(1.02) 100(1.02) 100(1.02)

3rd qtr 2nd quarter 1st quarter

This amount was just put in at the end of the 4th quarter,

so it has earned no interest.

6 Barnett/Ziegler/Byleen College Mathematics 12e

Future Value of an Annuity

Deposit of $100 every 6 months into an account that

pays 6% compounded semiannually, over 3 years.

How much money will be after the last deposit?

7 Barnett/Ziegler/Byleen College Mathematics 12e

Future Value of an Annuity

Let’s look at it in terms of a time line using A = P(1 + i)n.

1 yr 2 yr 3 yr Years

0 1 2 3 4 5 6 Number of periods

$100 $100 $100 $100 $100 $100 Deposit

$100(1.03)

$100(1.03) 2

$100(1.03) 3

$100(1.03) 4

$100(1.03) 5

Future Value

8 Barnett/Ziegler/Byleen College Mathematics 12e

Future Value of an Annuity

Total amount in the account after six deposit:

S = 100 + 100(1.03) + 100(1.03)^2 + 100(1.03)^3 + 00(1.03)^4 + 100(1.03)^5

Multiply each side by 1.03:

1.03S = 100(1.03) + 100(1.03) 2 + 100(1.03)3 + 100(1.03)4 + 100(1.03)5 +

100(1.03)6

Subtract Equation 1 from Equation 2

1.03S - S = 100(1.03)6 - 100

0.03S = 100[(1.03)6 - 1]

1

2

9 Barnett/Ziegler/Byleen College Mathematics 12e

Future Value of an Annuity

10 Barnett/Ziegler/Byleen College Mathematics 12e

General Formula for

Future Value of an Annuity

where

FV = future value (amount)

PMT = periodic payment

i = rate per period

n = number of payments (periods)

Note: Payments are made at the end of each period.

FV PMT

1 i n

1

i

11 Barnett/Ziegler/Byleen College Mathematics 12e

Example

Suppose a $1000 payment is made at the end of each

quarter and the money in the account is compounded

quarterly at 6.5% interest for 15 years. How much is in the

account after the 15 year period?

12 Barnett/Ziegler/Byleen College Mathematics 12e

Example

Suppose a $1000 payment is made at the end of each

quarter and the money in the account is compounded

quarterly at 6.5% interest for 15 years. How much is in the

account after the 15 year period?

Solution: (1 ) 1niFV PMT

i

4(15)

0.0651 1

41000 100,336.68

0.065

4

FV

13 Barnett/Ziegler/Byleen College Mathematics 12e

Graphical Display

14 Barnett/Ziegler/Byleen College Mathematics 12e

Balance in the Account

at the End of Each Period

15 Barnett/Ziegler/Byleen College Mathematics 12e

Amount of Interest Earned

How much interest was earned over the 15 year period?

16 Barnett/Ziegler/Byleen College Mathematics 12e

Amount of Interest Earned

Solution

How much interest was earned over the 15 year period?

Solution:

Each periodic payment was $1000. Over 15 years,

15(4)=60 payments were made for a total of $60,000.

Total amount in account after 15 years is $100,336.68.

Therefore, amount of accrued interest is $100,336.68 -

$60,000 = $40,336.68.

17 Barnett/Ziegler/Byleen College Mathematics 12e

Example of Future Value of an

Ordinary Annuity

Example 1

Interest: Deposits = 20(2,000) = $40,000

Interest = value – deposits = 96,754.03 – 40,000

= $56,754.03

18 Barnett/Ziegler/Byleen College Mathematics 12e

Example of Future Value of an

Ordinary Annuity

Balance Sheet

The Table in next display is called a balance sheet. Taking a

closer look we can see that the first line is a special case

because the payment is made at the of the period and no interest

is earned.

Eacg subsequent line is computed as follows:

Payment + Interest + Old Balance = New Balance

The amounts at the bottom of each column agree with the

results obtained with the formula of the Future Value of an

Ordinary Annuity.

19 Barnett/Ziegler/Byleen College Mathematics 12e

Example of Future Value of an Ordinary Annuity

Balance Sheet A B C D

Period Payment Interest Balance

1 2,000 0 2,000.00

2 2,000 170.00 4,170.00

3 2,000 354.45 6,524.45

4 2,000 554.58 9,079.03

5 2,000 771.72 11,850.75

6 2,000 1,007.31 14,858.06

7 2,000 1,262.94 18,120.99

8 2,000 1,540.28 21,661.28

9 2,000 1,841.21 25,502.49

10 2,000 2,167.71 29,670.20

11 2,000 2,521.97 34,192.17

12 2,000 2,906.33 39,098.50

13 2,000 3,323.37 44,421.87

14 2,000 3,775.86 50,197.73

15 2,000 4,266.81 56,464.54

16 2,000 4,799.49 63,264.02

17 2,000 5,377.44 70,641.47

18 2,000 6,004.52 78,645.99

19 2,000 6,684.91 87,330.90

20 2,000 7,423.13 $ 96,754.03

TOTALS 40,000 $ 56,754.03

20 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Definition: Any account that is established for

accumulating funds to meet future obligations or debts is

called a sinking fund.

The sinking fund payment is defined to be the amount

that must be deposited into an account periodically to have

a given future amount.

21 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund Payment Formula

To derive the sinking fund payment formula, we use

algebraic techniques to rewrite the formula for the future

value of an annuity and solve for the variable PMT:

(1 ) 1

(1 ) 1

n

n

iFV PMT

i

iFV PMT

i

22 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Sample Problem 1

How much must Harry save each month in order to buy a new

car for $12,000 in three years if the interest rate is 6%

compounded monthly?

23 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Sample Problem 1 Solution

How much must Harry save each month in order to buy a new

car for $12,000 in three years if the interest rate is 6%

compounded monthly?

Solution:

36

(1 ) 1

0.06

1212000 305.060.06

1 112

n

iFV PMT

i

pmt

24 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Sample Problem 2

The parents of a newborn child decide that on each of the child’s

birthday up to the 17th year, they will deposit $PMT in an account

that pays 6% compound annually. The money is to be used for

college expenses. What should the annual deposit ($PMT) be in

order for the amount in the account to be $80,000 after the 17th

deposit?

25 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Sample Problem 2 Solution

26 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

A company estimates that it will have to replace a piece of

equipment at a cost of $800,000 in 5 years. To have the

money available in 5 years, a sinking fund is established by

making equally monthly payments into an account paying

6.6% compounded monthly.

A. How much should each payment be?

B. How much interest is earned during the last year?

Example 2 – Computing the Payment

27 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Example 2 – Computing the Payment

28 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Example 2 – Computing the Payment (continued)

29 Barnett/Ziegler/Byleen College Mathematics 12e

Example of Sinking Fund

Problem (1)

Solution:

B. (Cont.)

Interest:

800,000 – 618,277.04 = 181,722.96 Growth in the 5yr

12 x 11,290.42 = 135,485.04 Payments during the 5yr

181,722.96 - 135,485.04 = $46,237.92 Interest during the 5yr

Example 2 – Computing the Payment (continued)

30 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Jane deposits $2,000 annually into an IRA that earns 6.85%

compounded annually. Due to a change in employment, these

deposits stops after 10 years, but the account continues to

earn until Jane retires 25 years after the last deposit was

made. How much is in the account when Jane retires?

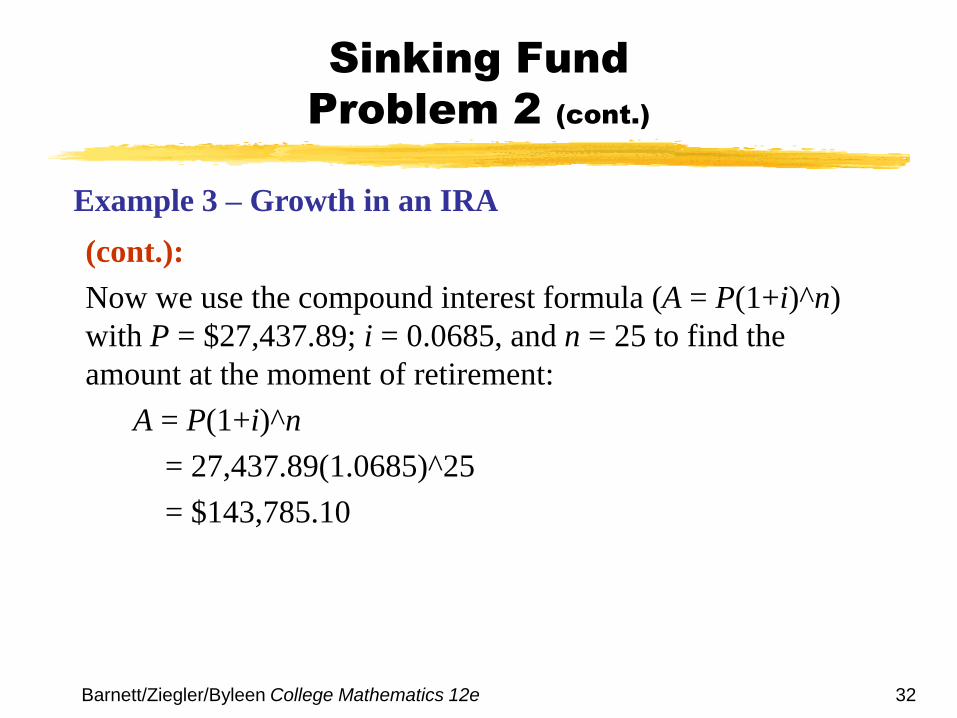

Example 3 – Growth in an IRA

31 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Example 3 – Growth in an IRA

32 Barnett/Ziegler/Byleen College Mathematics 12e

Sinking Fund

Problem 2 (cont.)

(cont.):

Now we use the compound interest formula (A = P(1+i)^n)

with P = $27,437.89; i = 0.0685, and n = 25 to find the

amount at the moment of retirement:

A = P(1+i)^n

= 27,437.89(1.0685)^25

= $143,785.10

Example 3 – Growth in an IRA

Chapter 3

Mathematics of

Finance

Section 3

Future Value of an

Annuity; Sinking Funds

END Last Update: April 1/2013