mattia corbetta - crowdinvesting in italy: a case study

TRANSCRIPT

Crowdinvesting in Italy:

a case study

OECD Workshop on building business linkages20 February 2018, Mexico City

Mattia CorbettaPolicy Advisor on Innovation and StartupsDG for Industrial Policy, Competitiveness and SMEsItalian Ministry of Economic Development

2

Crowdinvesting

Sub-category of crowdfunding, i.e. the practice of funding a project or venture by raising many small amounts of money from a large number of people, typically via the Internet, in which investors receive returns on invested capital. It does not encompass donation- and reward-based crowdfunding

Online platforms are key: they do not only put in touch enterprises with potential investors, but also do help finalise the deal between the parties

1. Equity Crowdfunding

2. Lending Crowdfunding

3. Invoice Trading

3 main trends

The total amount of capital mobilised through crowdinvesting in Italybetween June 2016 – June 2017 is €189.2 M

Made by: €12,4 EC+€ 88,3 LC +€88,5M IT

3

• €7.7 B: alternative finance market in Europe up to 2016 • ≈€2 B raised capital in 2016 (crowdinvesting≈80%)• +101% between 2015 and 2016 (UK excluded, +41% UK included)• Italy is the 7th European country for online alternative finance market

volume, after UK, France, Germany, the Netherlands, Finland and Spain

European and global alternative finance trends: how does Italy compare?

largest market segment (70+% of crowdinvesting)

more than 45% of crowdinvesting

Lendingcrowdfunding

(2016)

Invoice Trading market is relatively more developed in Italy than the European average (3rd largest European market after Belgium and France)

Regional markets and main playersCompared to Asia and the Americas Europe has a smaller but more scattered market:

Asia €221.6 B China accounts for 99%Americas €31.8 B US account for 98%

Europe €7.7 B UK accounts for 73%Source: The 3rd European Alternative Finance Industry Benchmarking Report, University of Cambridge

4

1. Equity crowdfunding: Italy’s first-of-its-kind regulations

• Italy was the 1st country in the world to introduce dedicated regulations(Consob resolution n. 18592/2013)

• 2014 2014 2015 2015

At first they applied just to innovative startups(as defined by decree law 179/2012, the «Italian Startup Act»)

In 2015 this tool was extended to all innovative SMEs(as defined by decree law 3/2015)

Eventually, Budget Law 2017 enabled all Italian SMEs established asprivate limited companies, just like any other public company, to offer

capital shares to the public, and therefore to carry out equity crowdfunding campaigns

The market is thus likely to grow esponentially in the coming years

5

22 portals authorised by Consob

159 campaigns launched since2013 (135 by startups, 14 by innovative SMEs, 3 by investmentvehicles, 1 by other type of SME)

86 successful campaigns(61.4%)

19 ongoing (8 already reachedtheir minimum target)

54 not successful (38.6%)

79 campaigns completed just in 2017

58.8 investors on average involvedfor each campaign

Updated at 20th January 2018Source: Observatory on Crowdinvesting,

Polytechnic University of Milan

1. Equity crowdfunding: campaigns completed

4 7

19

49

7

19

6

9

9

30

0

10

20

30

40

50

60

70

80

90

2014 2015 2016 2017 2018

Successful campaigns Ongoing campaigns Unsuccessful campaigns

1.3 1.8

4.4

11.4

1.60

2

4

6

8

10

12

2014 2015 2016 2017 2018

Million €

6

€20.5 M collected since 2013

€223,148: average fundraising target 15.5%: average quota of equity

capital offered 160.2%: average ratio between

raised money and target

Total collected capital is 4 timeshigher than 1.5 years ago

Capital collected in 2017 is almost3 times more than the amount of 2016

Total: €20.5 M

Updated at 20th January 2018Source: Observatory on Crowdinvesting,

Polytechnic University of Milan

1. Equity crowdfunding: capital raised

Capital raised up to 2015:

(source: Crowdfunding Hub)

€3.1 M

€50.1 M

€37.3 M

€10.7 M (2014)

7

2. Lending crowdfunding: regulations and data

• Differently from equity crowdfunding, Italy has not enacted dedicatedregulations in this field yet

This hampers the involvement of institutional investors!

• Lending crowdfunding is therefore grounded on general laws for the banking system (i.e. TUB – Testo Unico Bancario)

• Bank of Italy issued dedicated interpretative guidelines in 2016

• 9 lending crowdfunding platforms currently operating in Italy: 6 for loansto individual consumers, 3 to businesses (1 is for non-profits only)

• They adopt either a «diffuse» (i.e. platforms allocate credit on the basis of some general instructions received, a.k.a. «auto-bid functionality») or a «direct» business model (i.e. lenders choose whom to fund)

• Overall 11,773 loans from around 10,000 lenders

Why do companies use it? It is faster than bank loans, conditions and costsare perceived to be very clear and it is a good way to diversify credit sources

Updated at 30th June 2017Source: Observatory on Crowdinvesting, Polytechnic University of Milan

8

2. Lending crowdfunding: data

€88.3M collected, of which €56.5 M (64%) between June 2016 and June 2017 the amount collected tripled in the last year

Amount of loansgranted throughItalian activeplatforms, overall and between June 2016 -2017 (Million €)

Updated at 30th June 2017. Source: Observatory on Crowdinvesting, Polytechnic University of Milan

26.8

6.2

40.0

0.022

13.0

3.3 2.9 0.6

37.3

10.5

2.00

5

10

15

20

25

30

35

40

45

Smartika Prestiamoci Soisy YounitedCredit

Motus Quo Borsa delCredito

Lendix

Overall

June '16 - June '17

Business

Consumer

9

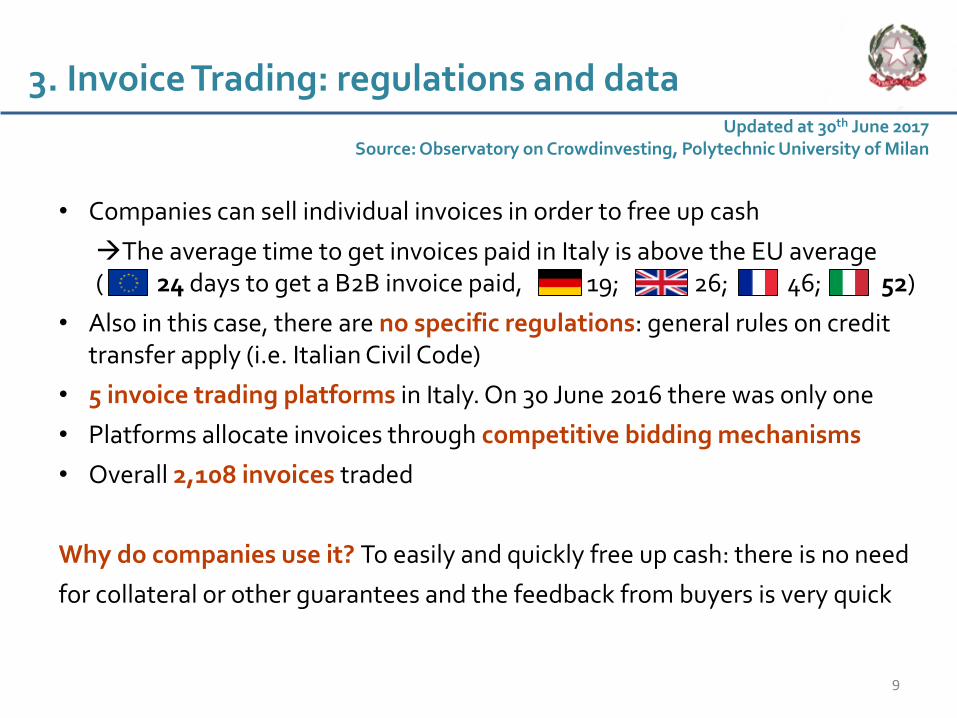

3. Invoice Trading: regulations and data

• Companies can sell individual invoices in order to free up cash

The average time to get invoices paid in Italy is above the EU average( 24 days to get a B2B invoice paid, 19; 26; 46; 52)

• Also in this case, there are no specific regulations: general rules on credit transfer apply (i.e. Italian Civil Code)

• 5 invoice trading platforms in Italy. On 30 June 2016 there was only one

• Platforms allocate invoices through competitive bidding mechanisms

• Overall 2,108 invoices traded

Why do companies use it? To easily and quickly free up cash: there is no need

for collateral or other guarantees and the feedback from buyers is very quick

Updated at 30th June 2017Source: Observatory on Crowdinvesting, Polytechnic University of Milan

10

3. Invoice Trading

€88.5 M collected (≈85% between June 2016 – June 2017)i.e. 8 times the amount registered at 30 June 2016

It is the crowdinvesting sector that reported the highest growth trend

Amount of invoicestraded on Italianplatforms, overall and between June 2016 and June 2017 (Million €)

Updated at 30th June 2017Source: Observatory on Crowdinvesting, Polytechnic University of Milan

66.5

17.02.9 2.1

53.1

17.02.9 2.1

0

10

20

30

40

50

60

70

WorkInvoice Credimi CashMe CrowdCity

Overall

June '16 - June '17

11

3 take-home messages from Italy’s experience

1. Startups are an ideal sandbox for new policy toolsSuccessful experimentation with a niche of companies paved the way for a broadening of the target group (step-by-step approach)

2. Consultation with stakeholders is keyRegulations on equity crowdfunding have been amended and improvedseveral times (2016 and 2018) thanks to public consultation with platforms and other financial players with solid hands-on experience (e.g. definition of institutional anchor investors, dematerialisation of shares to foster secondary market)

3. Crowdinvesting can be a catalyst for further investmentA survey carried out by the Polytechnic University of Milan shows thatequity crowdfunding campaigns can have a signalling effect towardinvestors, i.e. in many cases they have been followed by largerinvestment by corporations or financial institutions

Thank you for your attention

Mattia CorbettaPolicy Advisor on Innovation and StartupsDG for Industrial Policy, Competitiveness and SMEsItalian Ministry of Economic Development

Contact:

[email protected] @CorbettaMattia [email protected]

Visit:

mise.gov.it osservatoriocrowdinvesting.it startup.registroimprese.it