me io imacro economic overview and foreign exchange … · macro economic overview ... 9access to...

TRANSCRIPT

M E i O iMacro Economic Overview and

Foreign Exchange Risk Management

A g‘12A g‘12Aug‘12Aug‘12

Presentation path …Presentation path …

Macro Economic Overview

Global Financial turmoil

Indian economy

Currency update

Hedging Products & Strategies

Hedge factors

Forward

Option

Solution and offeringSolution and offering

Citi: 100 years in India

Offeringg

Global Financial Turmoil and Indian EconomyGlobal Financial Turmoil and Indian Economy

Economies are interlinked- impact of recession spilled all over

Euro Zone extremely turbulent; Sovereign Credit Rating y ; g gdowngrades as well as rising inflation - a major concern

US economy showing mixed signs; another round of QE is a possibility

Japan hit hard by strong currency, slowing growth, political turmoil and the devastating Tsunami

Geo political concerns (Iran Syria etc ) continues to be aGeo political concerns (Iran, Syria etc.) – continues to be a concern

Market displaying heightened uncertainty– similar to 2008/09

India: Falling INR, scam news, slowing growth, high interest rates, rising inflation, no new policy measures & high deficit have reduced sheen

Growth vs. Inflation – Very big challenge

Global Financial Turmoil and Indian EconomyGlobal Financial Turmoil and Indian Economy

India – INR weakness took market by surprise

Headline inflation to remain sticky

Industrial growth stagnating

Currency volatility persists given the global uncertainty

Focus on infrastructure and political/social stability is important

Scams & high inflation keeping global investor communityScams & high inflation keeping global investor community jittery

Rating downgrade is a possibility

Policy inertia

Indian economy and USDINRIndian economy and USDINR

INR at the moment is trading in a narrow range

RBI took steps to curb volatility (eg – Cancel / Rebook facility, EEFC balance, Bank NOP etc.)

RBI FX (D 2007 275 B D 2008 254RBI FX reserves (Dec 2007: 275 Bn, Dec 2008: 254 Bn; Dec 2009: 284 Bn and present : USD 288 Bn)

Poor economic performance indicators (June IIP : -1.8% ; Jul CPI : 9.86 % ; ; Jul WPI: 6.87 % )

Indian equity market is shaky presently

Drought fears are coming true

GAAR has added to the negative sentiment

Rating agencies are increasingly turning bearish

Growth projections getting revised downwards (FY 12 - 5-6% )

High current account & fiscal deficit inflationaryHigh current account & fiscal deficit, inflationary pressure are legitimate concern

RBI seems very concerned on inflation not coming down Source: Reuters

CRR, Repo and Reverse Repo at 4.75%, 8.0% & 7.0%

SLR at 23%

Major currenciesMajor currencies

EUREUR

Greece election provided only a short term relief

Spain & Italy are also showing signs of stress

Threat of ‘currency wars’

‘Quantitative Easing’ may re-shake the global financial market

Credit rating of EU countries – Big Concern

Very large impact on global trade and financial market stability

Containing inflation is a big challenge to Central Bankers

Geopolitical risk

Rising differences amongst EU members on tiding over the issue

Been very volatile and can expect the volatility to continue

GBP

BOE may persist with QE for long time

Fiscal and political risk

Slowing growth

May see choppy price action

Source: Reuters

Major currencies …contd.Major currencies …contd.

JPY

Effects of Tsunami & Earthquake could be spread over a long period Political scenario is fragileVery sharp JPY appreciation (partly owing to flight to safety) hurting exportersInterest rate cut to 0.1% to support economic growth Earning concerns for major Japanese corporate housesCentral Bank intervened in currency market to stem the appreciation (with limited success)

AUD

Movement closely linked with commodity prices Source: ReutersMovement closely linked with commodity pricesGlobal risk aversion and slowing China may lead to falling AUDRising unemployment: 5.2%RBA is cutting the bank rate; latest 3.5 %Price action will be volatile given global uncertaintiesPrice action will be volatile given global uncertaintiesProspect are linked with China economic development

FX Products

Cash MarkingCash Marking

Hedging tools

Forward

Option

Cash Marking and EEFC facilityCash Marking and EEFC facility

Inward/Outward remittances

Dedicated Trade and Fund Transfer Unit to execute and guide through transactions

RM and branch guide you through documentation

R t ld b id d till 4 30 PM FEDAI lRate could be provided till 4:30 PM as per FEDAI rule

EEFC transactions:EEFC transactions:

Customer may park export remittances in EEFC account, subject to RBI guidelines

EEFC balance could be converted to rupee or make outward payment, subject to RBI guidelines

Hedging Strategyedg g St ategy

ForwardForward

Optionp

Hedging: Factors to be consideredHedging: Factors to be considered

Clear understanding & objective

Budgeted Level/Rate sensitivityRisk appetite

Hedge Factors

Forward levelUnderlying/Tenor

Forward level (Spot + Premia)

Forward is a contract with bank to buy/sell a specific currency and amounty p yagainst another currency at a pre-determined exchange rate and on anagreed future date.

Obligation on both the parties to the contractAvailable in all major currency pairsProtection from foreign exchange market volatilityPotential loss due to unfavorable movement in currency market

Forward Rate = Spot Rate + Premia

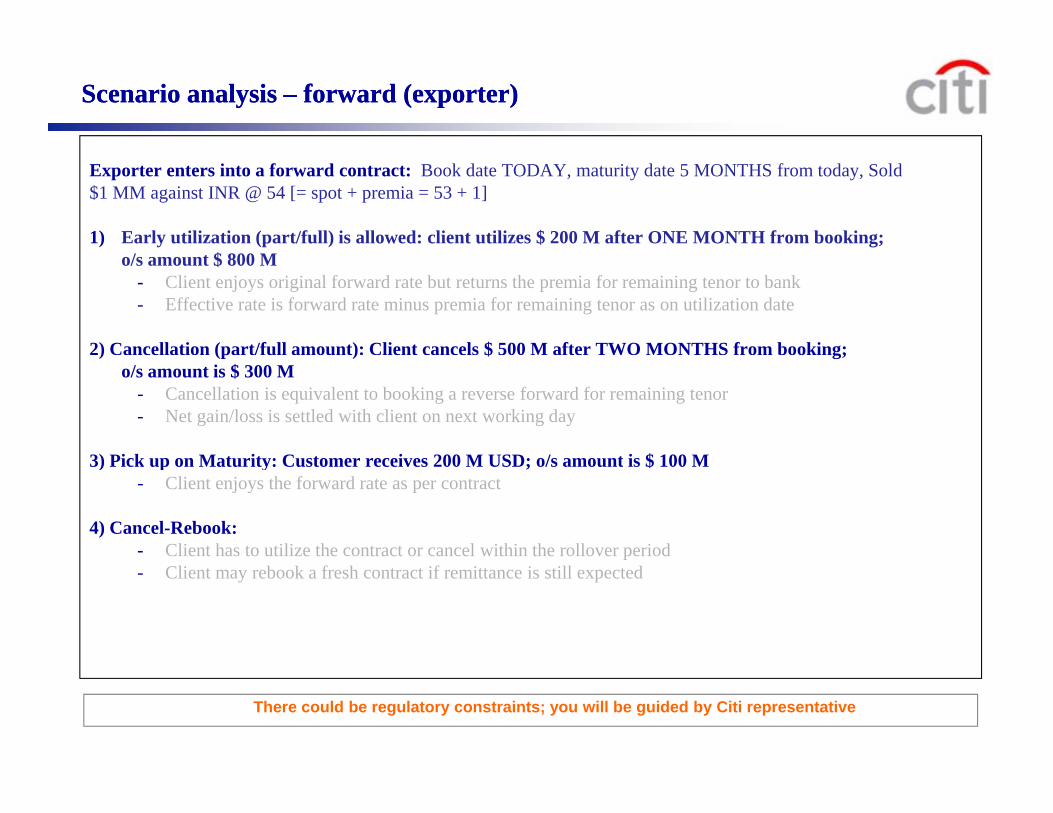

Scenario analysis Scenario analysis –– forward (exporter)forward (exporter)

Exporter enters into a forward contract: Book date TODAY, maturity date 5 MONTHS from today, Sold$1 MM against INR @ 54 [= spot + premia = 53 + 1]

1) Early utilization (part/full) is allowed: client utilizes $ 200 M after ONE MONTH from booking;o/s amount $ 800 M

- Client enjoys original forward rate but returns the premia for remaining tenor to bank- Effective rate is forward rate minus premia for remaining tenor as on utilization date

2) Cancellation (part/full amount): Client cancels $ 500 M after TWO MONTHS from booking;) (p ) $ g;o/s amount is $ 300 M

- Cancellation is equivalent to booking a reverse forward for remaining tenor- Net gain/loss is settled with client on next working day

3) Pick p on Mat rit : C stomer recei es 200 M USD; o/s amo nt is $ 100 M3) Pick up on Maturity: Customer receives 200 M USD; o/s amount is $ 100 M- Client enjoys the forward rate as per contract

4) Cancel-Rebook:- Client has to utilize the contract or cancel within the rollover period- Client may rebook a fresh contract if remittance is still expected

There could be regulatory constraints; you will be guided by Citi representative

“I Don’t like forward because it restricts me to enjoy favorable market “I Don’t like forward because it restricts me to enjoy favorable market movement” movement”

“Please give me an alternative”“Please give me an alternative”

Give me an “Option” please..Give me an “Option” please..Give me an Option please..Give me an Option please..

Fx OptionsFx Options

DefinitionDefinition-- Currency OptionsCurrency Options

A Currency Option is a Financial Contract which gives the Buyer (Holder) theRight, but not the Obligation, to exchange a specified amount of currency versusg g g p yanother at a specified rate on, or up to, a specified date.

The Seller (or Writer) of the Currency Option contract has the Obligation todeliver the specified amount of currency at the specified rate on the specified date.

Options offer Flexibility to not lock in rates

Benefits over Forwards

Options offer Flexibility to not lock in rates.Can tailor risk / reward to specific client requirements

C St diC St diCase StudiesCase Studies

C 1 E tCase 1 - Exporter

Customer is an exporter*:Customer is an exporter :

Need – To protect against potential USD depreciation against the INR from current levels over the month.cu e t eve s ove t e o t .

Spot Rate : 56.00Notional : $ 1 million receivable 5 month from nowNotional : $ 1 million receivable 5 month from now

Premia : 100 paise (5 months).

Hence, the forward rate will be 57 ( Spot :56.00 + Premia 1.00)

*This is a hypothetical example for illustration purpose only

Strategy 1: Customers books a forward at 57.00 (Exporter)Strategy 1: Customers books a forward at 57.00 (Exporter)

Scenario 1: US$ has Depreciated, say to 54

The Exporter receives INR 57 million instead of the market offer of INR 54 millionThe Exporter receives INR 57 million instead of the market offer of INR 54 million.

Customer gains Rs 3 milliongains Rs 3 million by entering into the forward contract

Scenario 2: US$ has Appreciated, say to 59

The Exporter receives INR 57 million instead of the market rate of 59 million.p

Customer loses Rs 2 millionloses Rs 2 million by entering into the forward contract

Alternate product could be option to enjoy the upside.

Note: Customer has an option to cancel the contract before the maturity date.Profit / loss will be credited/debited to the account

Strategy 2: Hedging using OptionsStrategy 2: Hedging using Options

Customer buys 5 month Put @ 57 for $ 1.0 mioCustomer pays 2.0% or USD 20,000 for this option

On expiry:p y

Scenario 1:US$ has Depreciated, say to 54

Customer would exercise the option at 57p

Customer gains Rs 3 milliongains Rs 3 million by entering into the option contractTotal Gain = Rs 3 mm – option premia paid on day zero

Scenario 2:US$ has appreciated, say to 59

Customer would not exercise the option and enjoy market rate 59

Customer enjoys the upside and maximum pay off is the premia USD 20,000 by entering into the option contract

Opportunity benefit at a cost of USD 20,000Opportunity benefit at a cost of USD 20,000

Strategy 3 Strategy 3 –– Can we reduce the premia? Zero cost (Exporter)Can we reduce the premia? Zero cost (Exporter)

Customer (Fwd level is 57 00: Spot @ 56 00 and premia 100 paise)

Customer: “I don’t want to pay any premia on day zero but like to protect the downside and ready to compromise the upside beyond a level”

Customer (Fwd level is 57.00: Spot @ 56.00 and premia 100 paise)(a) buys put [sells USD buys INR ] @ 55.00; (b) sells a call [bank buys USD sells INR ≡ customer sells USD and buys INR] @ 58

On Expiry:On Expiry:Scenario 1: US$ has depreciated to 50.00

– Customer exercises the Put and receives 55.00– Banks does not exercise Call and it expires

Scenario 2: US$ has appreciated to 56– Customer does not exercises the Put – Banks does not exercise Call and it expires– Customer receives 56 (market rate)Customer receives 56 (market rate)

Scenario 3: US$ has appreciated to 59– Customer does not exercises the Put and it expires– Banks exercises Call and customer realizes only 58Banks exercises Call and customer realizes only 58

FX offeringFX offering

Product: Remittances, EEFC account, Forward and Option

Daily/weekly/monthly market & research updates from tradersDaily/weekly/monthly market & research updates from traders

Experienced RMs and Treasury officers who closely monitor global markets and update on market developmentp p

Access to Treasury Dealers for online information

Remittances, FX Forward and Options coverage from 09.00 AM to 4.30 PM IST

Award winning, Electronic platform (FX Pulse) where rate can be tracked andAward winning, Electronic platform (FX Pulse) where rate can be tracked and fixed online

Why Citi? Key benefits and CredentialsWhy Citi? Key benefits and Credentials

Largest foreign bank in India: Our FX market share almost double vis-à-vis the next largest bankLargest market presence

Ability to quote competitively on both spot & forwards owing to offsetting flows and large book sizeC titi i i

Largest foreign bank in India: Our FX market share almost double vis-à-vis the next largest bank

Our market share greater than State bank of India: SBI 8000+ branches vs Citi 39 Branches

FX market share [including XCCY]: 30.67% … largest amongst all players in India*

Largest market presence

Dedicated FX desk with extended coverage time [8:00 AM to 9:30 PM IST]

Capability to quote cash [same day value deals] even post local cut off time by using Citi’s prop

Innovative pricing solutions: various execution methodologies can be adoptedCompetitive pricing

Favorable FX coverage time p y q [ y ] p y g p p

book

g

Enhanced services

Dedicated foreign investor desk: Local market expertise on related regulations professionals who

are conversant with securities market

Select dealers having prior securities experience

Citi India awards Best FX Bank for Corporates’11Best Bank in Asia ‘11Best Foreign Investment Bank ’10

Select dealers having prior securities experience

Best for G3 & local ccy denom. deriv 10, 09 & ’08Best for comm. deriv ’10, ‘09 & ’08Best FX prime broking services ’10 ,’09 & ’08Best bank - overall FX services – Corp. ’10 & 08Best for innovative FX prod & structures ideas ’10

Best Foreign Investment Bank ’10Best Private Bank in India ‘ 10Best Structured Products House ‘08

Best Investment Bank ‘ 10Best Private Bank in India ‘ 10Best Commercial Bank ‘10Best FX House ‘09

Best for innovative FX prod & structures ideas - 10Best bank - competitive & prompt spot pricing

Best Structured Products House 08Best Derivatives House ‘08

Most Trusted Foreign Bank’ 10* As per Euromoney Polls 2011

DisclaimerDisclaimerWe are pleased to make this presentation and/or examples for discussion purpose. Although the information contained herein is believed to be reliable, wep p p p p g ,make no representation as to the accuracy or completeness of any information contained herein or otherwise provided by us. The ultimate decision toproceed with any transaction rests solely with you. We are not acting as your advisor or agent. Therefore, prior to entering into any transaction you shoulddetermine, without reliance upon us or our affiliates, the economic risks and merits, as well as the legal, tax and accounting characterizations andconsequences of the transaction, and independently determine that you are able to assume these risks. In this regard, by acceptance of these materials,you acknowledge that you have been advised that (a) we are not in the business of providing legal, tax or accounting advice and we expressly disclaim anyresponsibility for the contents hereof, (b) you understand that there may be legal, tax or accounting risks associated with the transaction, (c) you should

i l l t d ti d i f d i ith i t ti t l t i k d (d) h ld i i t ireceive legal, tax and accounting advice from advisors with appropriate expertise to assess relevant risks and (d) you should apprise senior management inyour organization as to the legal, tax and accounting advice (and, if applicable, risks) associated with this transaction and our disclaimers as to thesematters.

The terms and/or examples set forth herein are intended for discussion purposes only and subject to the final expression of the terms of a transaction as setforth in a definitive agreement and/or confirmation. This proposal is neither an offer to sell nor the solicitation of an offer to enter into a transaction. Our firmand o r affiliates ma act as principal or agent in similar transactions or in transactions ith respect to instr ments nderl ing a proposed transaction Thisand our affiliates may act as principal or agent in similar transactions or in transactions with respect to instruments underlying a proposed transaction. Thisdocument and its contents are proprietary information and products of our firm and may not be reproduced or otherwise disseminated in whole or in partwithout our written consent unless required to by judicial or administrative proceeding.

We are willing to negotiate a transaction with you because of our understanding that (1) you have sufficient knowledge, experience, and professional adviceto make your own evaluation of the merits and risks of a transaction of this type and (2) you are not relying on us nor on any of our affiliates for information,advice or recommendations of any sort except for the accuracy of specific factual information about the terms of the transactionadvice or recommendations of any sort except for the accuracy of specific factual information about the terms of the transaction.

The transactions may be subject to the risk of loss of the entire principal/notional amount of the transaction, the risk that your counterparty will fail to performobligations when due an d/or given that the transaction may be linked to the credit of one or more entities the deterioration of the credit of any of theseentities may result in the loss of your principal or notional amount. Further this transaction may leverage exposures to interest rates, indices or the prices ofcertain securities and, as a result, any changes in the value of the underlying securities, prices, indices or interest rates may cause proportionally greater(positive and negative) movements in the value of the trans action pose convexity or gamma risk volatility risk time decay (theta) risk basis risk correlation(positive and negative) movements in the value of the trans action, pose convexity or gamma risk, volatility risk, time decay (theta) risk, basis risk, correlationrisk, amortization risk and/or prepayment risk, any or all of which may affect the payments received or made by you and could result in loss to you.If you have any questions or would like additional information, please contact your sales representative.

Thank YouThank You