measuring “a significant risk of carbon leakage” according ... · presentation eccp meeting 26...

TRANSCRIPT

1

Measuring “a significant risk of carbon leakage”according to the proposed Art. 10a of Directive

2003/87/EC

The European Commission’s approach

Manfred BergmannDevelopment of Industrial Policy

Presentation ECCP meeting 26 September 2008

2

Why do we care about carbon leakage?

• Negative environmental consequences at the global scale

No emission reductions in the EUHigher emissions in the rest of the world

• Negative economic consequences within the EULower growthJob lossesPotential negative consequences on security of supply

3

When could carbon leakage occur?

• Supply-side driven:Transaction costs of delocalising existing production < CO2 costsTransaction costs of capacity expansion abroad (non-EEA) < CO2 costs

• Demand-side driven:Transaction costs of sourcing supplies from abroad (non-EEA) < CO2 costs

4

… Art. 10a (9), 3

…taking into account the following:(a) the extent to which auctioning would lead to a

substantial increase in production cost;(b) … (benchmarking) …(c) market structure, relevant geographic and product

market, the exposure of the sectors to international competition;

(d) The effects of climate change and energy policies implemented, or expected to be implemented outside the EU in the sectors considered

5

Stage 1: quantitative analysis

• Defining / identifying the (sub)sectors where problems may occur

• Measuring the impact in terms of potential product price increases

• Measuring the exposure to international trade

6

Stage 2: qualitative analysis of other market factors

• Relevant product market• Relevant geographic market• Concentration, competition, profit margins• Tightness of market• Transportation costs• Value-chain characteristics• …

7

Subsectors analysed

• Energy-intensive business, i.e. all business outside the energy sector and where the purchases of energy products and electricity amounts to at least 3.0% of its production value

• Data gathering exercise (tentative list)

Expanded clay

Glass

Copper

Tyres

Technical gases

Zinc

Refineries

Ferro-Alloys

Casting of Iron

SugarSteel tube production

TextilesAviation

LeadPotassium

NickelMagnesite & graphite

BoardsPulp and paperCement and Lime

StarchChemicalsSteel and Iron

Man-made fibersCeramicsAluminium

Sectors that will provide

information

Sectors that have provided

informationSectors currently

being analysed

8

The relevant product market: The degree of disaggregation

• NACE 4-digit causes some problemsManufacture of aluminium (DJ2742), but

• Primary versus secondary aluminiumManufacture of basic iron and steel and of ferro-alloys (DJ2710), but

• BOF process• EAF process

Manufacture of cement (DJ 2651), but• Clinker?

• ProdCom 8-digit provides some solutions

9

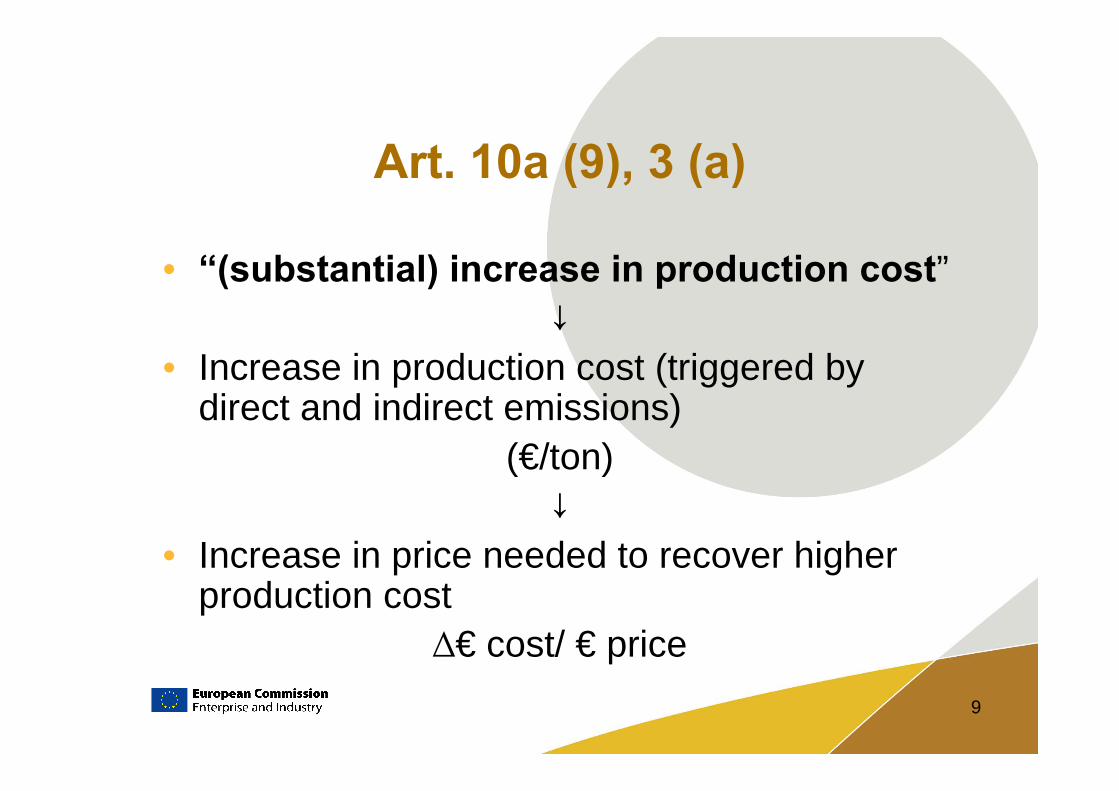

Art. 10a (9), 3 (a)

• “(substantial) increase in production cost”↓

• Increase in production cost (triggered by direct and indirect emissions)

(€/ton)↓

• Increase in price needed to recover higher production cost

∆€ cost/ € price

10

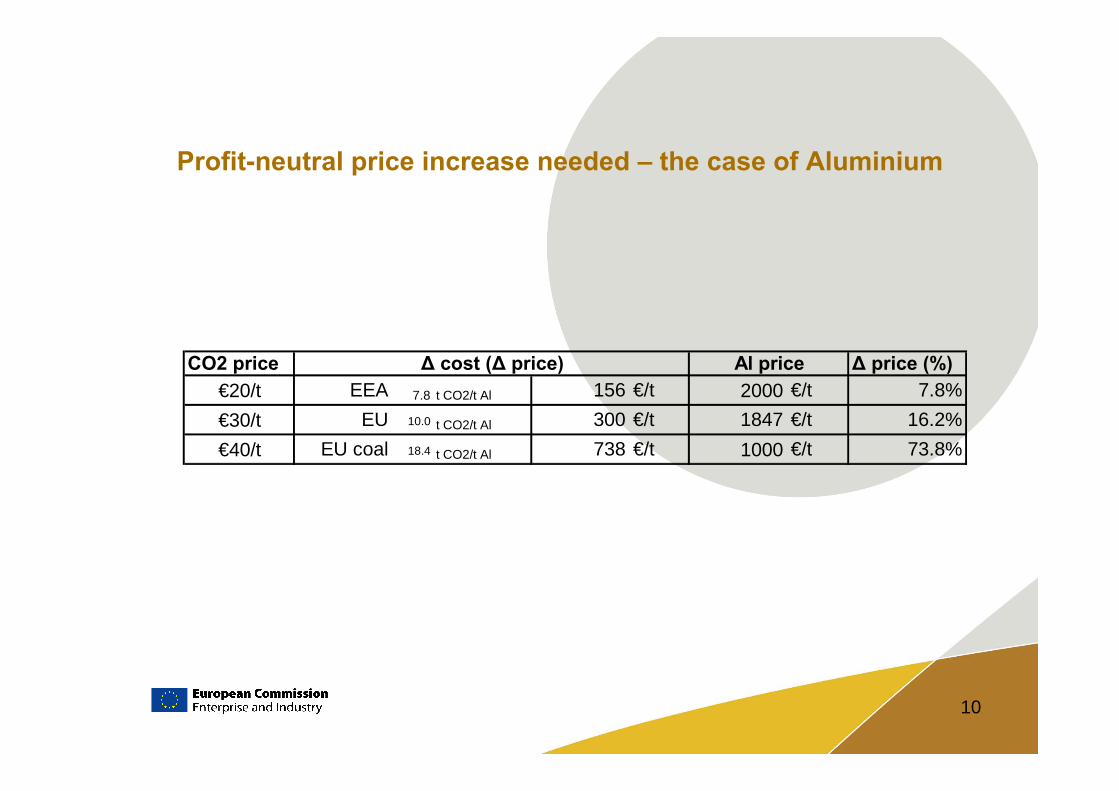

Profit-neutral price increase needed – the case of Aluminium

CO2 price ∆ price (%)€20/t EEA 7.8 t CO2/t Al 156 €/t 2000 €/t 7.8%€30/t EU 10.0 t CO2/t Al 300 €/t 1847 €/t 16.2%€40/t EU coal 18.4 t CO2/t Al 738 €/t 1000 €/t 73.8%

∆ cost (∆ price) Al price

11

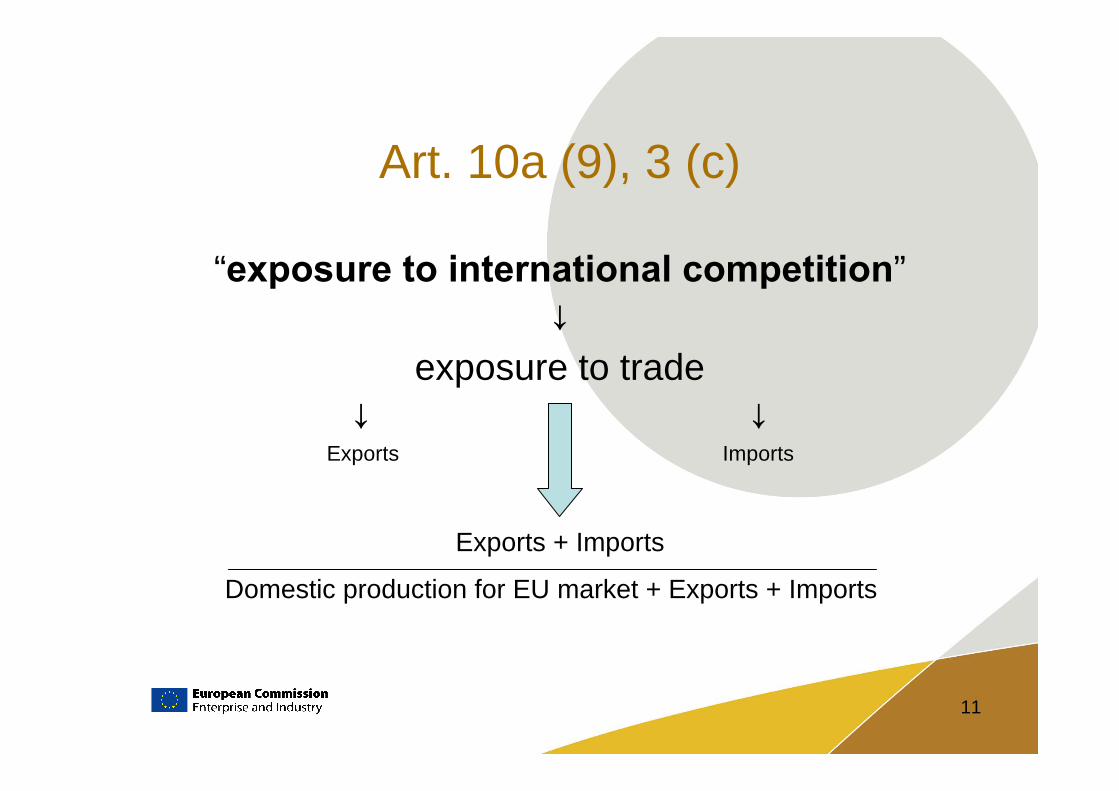

Art. 10a (9), 3 (c)

“exposure to international competition”↓

exposure to trade↓ ↓

Exports Imports

Exports + Imports

Domestic production for EU market + Exports + Imports

12

Trade intensity for selected products

Source: Prodcom total, Prodcom Sold, 2006. Production, Imports and exports are presented in 1000 t.

4.4%36315903214840Cement

53.1%12198119813042Clinker

1.0%6214420648Hot dipped metallic coated

28.4%5006843671Stainless Cold Rolled

0.3%163920281Rebar EAF

0.6%635218674Wire Rod EAF

54.1%543916367629slabs

29.8%7967419032760Hot rolled coil (total)

23.3%6137315146Rolling Aluminium

13.1%3413184699Extrusion Aluminium

8.0%2311013939Recycled Aluminium

47.3%4635855344Primary Aluminium

Exposure to tradeImportsExportsProduction

13

Results of stage 1: A tentative illustration

Preliminary results of Stage 1

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

Profit neutral price increase

Non

-EU

trad

e in

tens

ity

Recycled Aluminium

Rebar EAF-hot rolling

Wire Rod EAF-hot rolling

Hot dipped metallic coated BOF

Hot rolled coil BOF

slabs BOF

Primary Aluminium (EU average electricitymix)

Grey portland cement Dry process with multistage cyclone preheater and precalciner kilns(EU average clinker industry energy mix)Primary Aluminium (Coal-lignite basedelectricity mix)

Clinker Dry process with multi stage cyclonepreheater and precalciner kilns (EU average

14

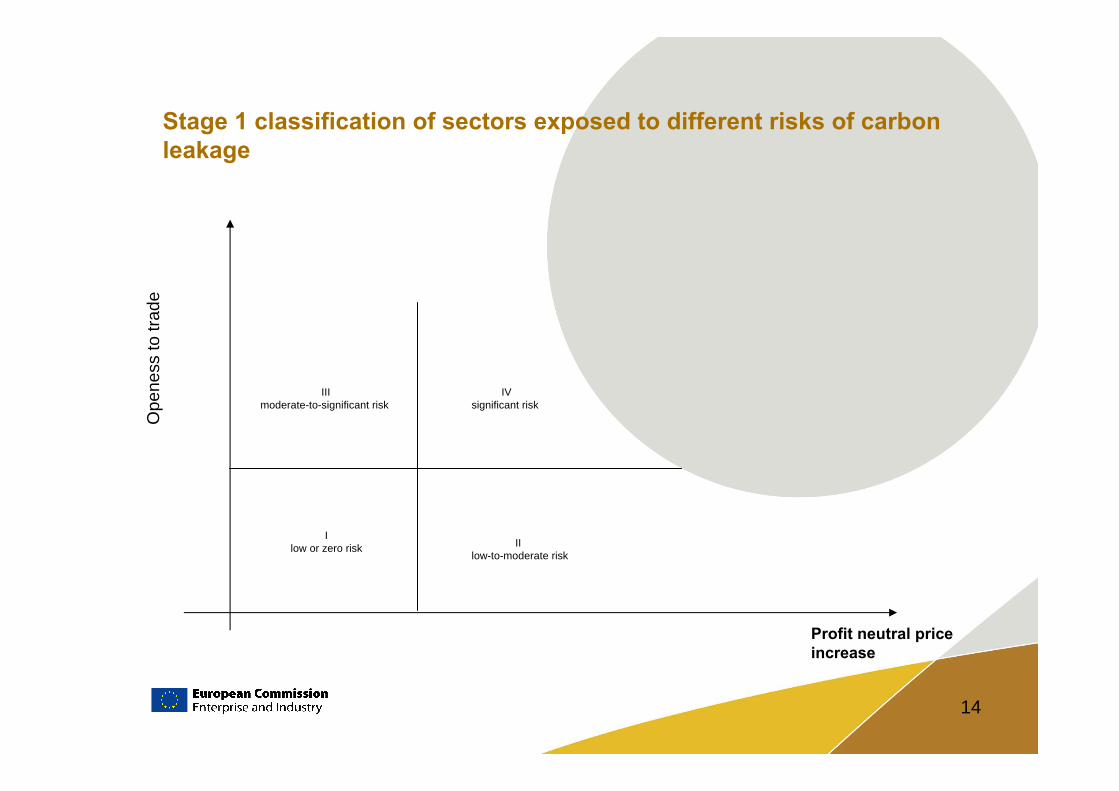

Stage 1 classification of sectors exposed to different risks of carbon leakage

Profit neutral priceincrease

Ope

ness

totra

de

I low or zero risk II

low-to-moderate risk

IIImoderate-to-significant risk

IVsignificant risk

15

Stage 2: qualitative analysis of other market factors

• Relevant product market• Relevant geographic market• Concentration, competition, profit margins• Tightness of market• Transportation costs• Value-chain characteristics• …

16

Art. 10a (9), 4

“For the purposes of evaluating whether the cost increase resulting from the Community scheme can be passed on, estimates of lost sales resulting from the increased carbon price or the impact on the profitability of the installations concerned may inter alia be used”

17

Prices and (global) demand – what price elasticity?Net volumes on the market and price 1992 - 2008 - primary aluminium - quarterly

0

1.000

2.000

3.000

4.000

5.000

6.000

Fourth 1992 Fourth 1993 Fourth 1994 Fourth 1995 Fourth 1996 Fourth 1997 Fourth 1998 Fourth 1999 Fourth2000

Fourth 2001 Fourth2002

Fourth2003

Fourth2004

Fourth 2005 Fourth2006

Fourth 2007

1000

tn

0

500

1.000

1.500

2.000

2.500

€/tn

Quarterly net volume on the market quarterly price (€)

18

Art. 10a (9), 3 (c)

“relevant geographic and product market”↓ ↓

Global market What degree of (yes/no) disaggregation?↓ ↓ ↓ ↓

Global Stock Transport cost NACE ProdComExchange? tbd 4-digit 8-digit

19

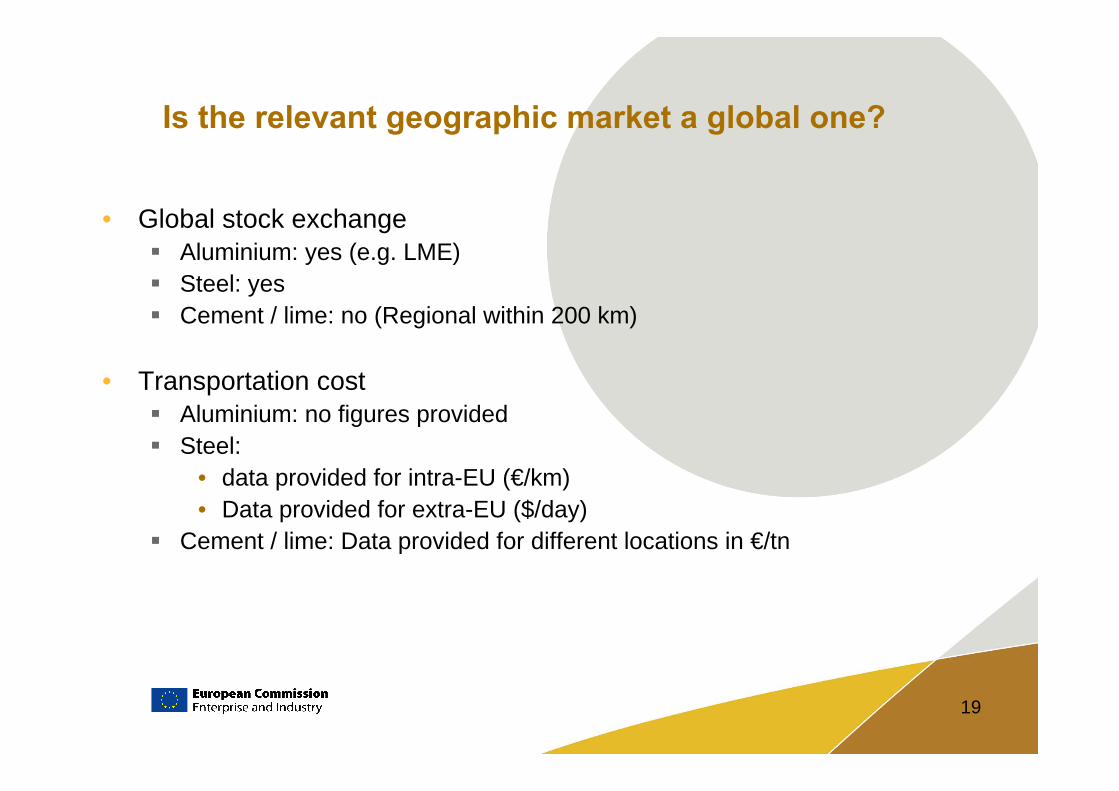

Is the relevant geographic market a global one?

• Global stock exchangeAluminium: yes (e.g. LME)Steel: yesCement / lime: no (Regional within 200 km)

• Transportation costAluminium: no figures providedSteel:

• data provided for intra-EU (€/km)• Data provided for extra-EU ($/day)

Cement / lime: Data provided for different locations in €/tn

20

Art. 10a (9), 3 (c)

Market structure↓ ↓

concentration tightness↓ ↓ ↓ ↓

market vertical level of capacityshares integration (global) utilization

stocks

21

Global market shares

Global market shares of major aluminium producers (2006)

Rusal11%

Alcoa11%

Alcan10%Hydro

5%Chalco

4%

Rio Tinto3%

Venezuela Gov'2%

Century2%

Bahrain Gov'2%

Dubal2%

Other48%

22

AL price and stock evolution 1997 - 2007A L p ric e a n d s to c k e v o lu tio n - 1 9 9 7 -2 0 0 6

0

5 0 0

1 0 0 0

1 5 0 0

2 0 0 0

2 5 0 0

Ja n 9 7 Ja n 9 8 Ja n 9 9 Ja n 0 0 Ja n 0 1 Ja n 0 2 Ja n 0 3 Ja n 0 4 Ja n 0 5 Ja n 0 6 Ja n 0 7

m o n th

Eur

o/tn

0

1 0

2 0

3 0

4 0

5 0

6 0

Sto

cks

in n

b of

day

s of

pro

duct

ion

E u ro sIn ve n to rie s e x p re s s e d in d a y s o f p ro d u c t io n (m o n th ly a ve ra g e )1 2 p e r. M o v. A vg . (E u ro s )1 2 p e r. M o v. A vg . (In ve n to rie s e x p re s s e d in d a y s o f p ro d u c t io n (m o n th ly a ve ra g e ))

23

Stage 2: Tentative illustration of results for aluminium

• Positive impact on ability to pass through cost increases:• market is tight,• little spare capacity at the global level,• a high degree of concentration,• geographically clustered value chain• …• …

• Negative impact on ability to pass through cost increases:• market is global,• homogeneous product easy to substitute (in case of primary aluminium),• eventually installations will compete with each other• …• …

• bottom line:

24

Stage 2: Tentative illustration of results for cement

• Positive impact on ability to pass through cost increases:high transportation cost, especially with respect to inland transport,market is rather regional (except for clinker, where producers close to

overseas ports are in competition with non-EU producers)……

• Negative impact on ability to pass through cost increases:potential cyclical downturn of construction sector in most OECD countries,potential slowdown of boom in China,potentially excess capacities at the regional, global level……

• bottom line:

25

Operational conclusions1. At the end of “Stage 1”, and after the thresholds will have been

decided upon (in a policy process), each (sub)sector will belong to either category I, II, III or IV!

2. The (qualitative) analysis undertaken in “Stage 2” could lead to a reclassification (up or down by at most one category)!

3. The assessment of the results of international negotiations to be undertaken in “Stage 3” could lead to a further reclassification!

4. [Finally, the directive could specify how many free allowances the (sub)sectors should receive, depending on whether they are at the end of “Stage 3” belonging to either category I, II, III or IV]