measuring market inefficiencies in california's...

TRANSCRIPT

Measuring Market Inefreg ciencies in Californiarsquos Restructured

Wholesale Electricity Market

By SEVERIN BORENSTEIN JAMES B BUSHNELL AND FRANK A WOLAK

We present a method for decomposing wholesale electricity payments into produc-tion costs inframarginal competitive rents and payments resulting from the exer-cise of market power Using data from June 1998 to October 2000 in California we nd signi cant departures from competitive pricing during the high-demand sum-mer months and near-competitive pricing during the lower-demand months of the rst two years In summer 2000 wholesale electricity expenditures were $898billion up from $204 billion in summer 1999 We nd that 21 percent of thisincrease was due to production costs 20 percent to competitive rents and 59percent to market power (JEL L1 L9)

In the spring of 2000 the momentum behinda dramatic restructuring of the electricity indus-try appeared to be irresistible There were fourregions of the United States with independentsystem operators running spot markets forwholesale electricitymdashCalifornia PJM (majorparts of Pennsylvania New Jersey MarylandDelaware Virginia and the District of Colum-bia) New England and New York Severalother states were undertaking initiatives to re-structure their electricity sector along similar

lines Beginning in summer 2000 howeversoaring wholesale electricity prices in Califor-nia made international news and threatened the nancial stability of the state The disruptions inCalifornia slowed and threatened to reverse themovement toward restructured electricity mar-kets in the United States and elsewhere

In the aftermath of Californiarsquos electricitycrisis policy makers debated the correct lessonsto take from the statersquos restructuring as well asthe proper regulatory response to the crisisMany of the answers to the questions beingdebated depend upon a proper diagnosis of theproblems that disrupted Californiarsquos power sec-tor during this period Were soaring power coststhe result of market ldquofundamentalsrdquo such asrising fuel prices environmental cost and ascarcity of generating capacity Or were powersuppliers able to exercise signi cant marketpower In this paper we estimate the extent towhich each of these factorsmdashinput costs scar-city and market powermdashin uenced market out-comes in the California power market from1998 through 2000 We analyze input and out-put prices generator variable costs and actualproduction quantities to measure the degree towhich California wholesale electricity pricesexceeded competitive levels We also addressthe question of the ef ciency impacts of marketpower in this market

While market power has been studied andestimated in many industries there has been

Borenstein Haas School of Business University ofCalifornia Berkeley CA 94720 University of CaliforniaEnergy Institute and NBER (e-mail borenstehaasberkeleyedu) Bushnell University of California EnergyInstitute 2539 Channing Way Berkeley CA 94720 (e-mail bushnellhaasberkeleyedu) Wolak Department ofEconomics Stanford University Stanford CA 94305 andNBER (e-mail wolakziastanfordedu) Borenstein is amember of the Governing Board of the California PowerExchange Bushnell was a member of the Power Ex-changersquos Market Monitoring Committee during 1999ndash2000 He is currently a member of the California Indepen-dent System Operatorrsquos Market Surveillance Committeeof which Wolak is the Chair The views expressed in thispaper do not necessarily re ect those of any organizationor committee For helpful discussions and comments wethank Carl Blumstein Roger Bohn Peter Cramton DavidGenesove Rob Gramlich Paul Joskow Ed Kahn AlvinKlevorick Christopher Knittel Patrick McGuire CatherineWolfram an anonymous referee and participants in numer-ous seminars Jun Ishii Matt Lewis Erin Mansur StevePuller Celeste Saravia and Marshall Yan provided excel-lent research assistance

1376

little attention paid to intertemporal variation inthe ability to exercise market power For indus-tries in which the good is storable such inter-temporal variation is necessarily small becauseinventories greatly reduce intertemporal supplyvariation and possibly demand variation Inmarkets for nonstorable goods including elec-tricity and most services this is not possibleThe problem is exacerbated in electricity be-cause demand is very inelastic in the short runand supply becomes very inelastic as productionapproaches the system-generation capacity Rec-ognizing the dynamics of market power is likelyto be important in both determining its causes andcrafting remedies as part of the evolving publicpolicy toward electricity restructuring

Luckily due to the history of regulation inelectricity markets data exist on the hourly out-put of all generating units and transmissionpower ows In addition information collectedon the technical characteristics of each Califor-nia generating unit during the regulated monop-oly regime allows very accurate estimation ofgenerating unit-level variable costs

We nd that due to rising input costs even aperfectly competitive California electricity mar-ket would have seen wholesale electricity ex-penditures triple between the summers of 1998and 20001 Market power however also playeda very signi cant role In summer 1998 25percent of total electricity expenditures could beattributed to market power a gure that in-creased to 50 percent in summer 2000 Theincreased percentage margins due to marketpower combined with substantial productioncost increases for marginal producers to create adrastic rise in absolute margins and thuspushed the market into a crisis later in thesummer of 2000

In Section I we discuss the issues raised inestimating market power in electricity marketsand the consequences of market power Wepresent an overview of Californiarsquos electricitymarket in Section II In Section III we describethe estimation technique in detail in the contextof the California market addressing each com-ponent of the market and outlining the assump-

tions made in implementing the analysis We tryto take a conservative approach interpreting thedata in a way that would be likely to understatethe degree of market power exercised In Sec-tion IV we present estimates of premia of ac-tual prices over the competitive levels InSection V we attempt to parse changes in com-petitive revenues between changes in actualcosts and changes that re ect rents to inframar-ginal competitive sellers We conclude in Sec-tion VI

I Market Power Analysis in theElectricity Industry

During most of the 1990rsquos regulatory evalu-ation of short-run horizontal market power inelectricity focused on concentration measuressuch as the Her ndahl-Hirschman index Unfor-tunately such measures are a poor indicator ofthe potential for or existence of market powerin the electricity industry because the industryis characterized by highly variable price-inelasticdemand signi cant short-run capacity constraintsand extremely costly storage2 It is easy to showthat in such circumstances rms with verysmall market shares could still exercise signi -cant market power

We use data collected on the technologicalcharacteristics of generating units located inCalifornia to construct a competitive marketcounterfactual that we compare to actual mar-ket outcomes This competitive counterfactualmodels each rm as a price-taker that would sellpower from a given plant so long as the price itreceived was greater than its incremental cost ofproduction Of course the cost of selling a unitof electricity can be greater than the simpleproduction costs if the rm has an opportunitycost that is greater than its production cost suchas the revenue the rm would get from sellingpower or reserve capacity in a different locationor market On the other hand a high price in analternative market can re ect market power inthat market resulting in the transmittal of high

1 For the purpose of this analysis we de ne the summerto be June through October of each year

2 See Borenstein et al (1999) for a more detailed dis-cussion of the applicability of concentration measures tomarket power analysis in electricity markets and citationsto regulatory decisions that have relied on concentrationindices

1377VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

prices across markets by the response of com-petitive suppliers We discuss these alternativeopportunities below and how we account forthem in our analysis

Thus far we have discussed only situations inwhich a rm unilaterally exercises marketpower Antitrust law is most often concernedwith collusive attempts to exercise marketpower Unfortunately many of the attributesthat facilitate collusion are present in electricitymarkets In most electricity markets rms playrepeatedly interacting on a daily basis so thereis opportunity to develop subtle communicationand collusive strategies The payoff from cheat-ing on a collusive agreement may be limited dueto capacity constraints on production thoughfor the same reason the ability to punish defec-tors may be limited Finally the industry hasfairly standardized production facilities so ho-mogeneous costs may make it easier for rms toattain tacit or explicit collusive outcomes Allthat said we have not explored the question oftacit or explicit collusion among rms in theCalifornia market as a potential cause of pricesin excess of competitive levels3 Rather in thispaper we focus on the competitiveness of mar-ket outcomes

In focusing on market outcomes there aretwo indicators that clearly distinguish marketpower and each leads to a distinct estimationtechnique First in a competitive market a rmis unable to take any action including outputdecisions or offer prices that signi cantly af-fects the price in a market This suggests amethod of estimation that involves studying thebidding and output supply decisions of each rm in the market to detect successful attemptsto affect prices This is the general approachused by Wolak and Robert H Patrick (1997)Catherine D Wolfram (1998) Roger Bohn etal (1999) Bushnell and Wolak (1999) Wolak(2000) and Puller (2001)

The second empirical approach is at the mar-ket level and this is the one that we adopt hereWe examine whether the market as a whole issetting competitive prices given the productioncapabilities of all players in the market As

such this approach is less vulnerable to thearguments of coincidence bad luck or igno-rance that may be directed at analysis of theactions of a speci c generator It is less infor-mative about the speci c manifestations ofmarket power but it is effective for estimatingits scope and severity as well as identifyinghow departures from competitive outcomesvary over time This is the general approachused in Wolfram (1999) At least two papersErin T Mansur (2001) and Paul L Joskow andEdward Kahn (2002) utilize both of theseapproaches

A potential drawback of the market-level ap-proach is that it captures all inef ciencies in themarket some of which may not be due to mar-ket power If for instance low-cost generatorswere systematically held out of production sim-ply due to a faulty dispatch algorithm thatwould impact the estimate of market powerDuring the period we study the California mar-ket clearly still had a number of design awsthat may have contributed to inef cient dispatchand market pricing For the great majority ofthese however the aw would be benign if rms acted as pure price-takers rather than ex-ploiting these design aws to affect the marketprice Furthermore we nd that over substan-tial periods of time prices did not signi cantlydiffer from our estimates of marginal cost in-dicating that there were no systemic inef cien-cies raising prices in all periods Still ourestimates must be taken with the caveat thatthey include failures to achieve competitivemarket prices for reasons other than marketpower including bad judgment and confusionon the part of some generators or market-making institutions

The Consequences of Market Power

In analyzing the ef ciency consequences ofmarket power in electricity one must beginfrom the recognition that short-run electricitydemand currently exhibits virtually zero priceelasticity Almost none of the customers in Cal-ifornia or anywhere else in the United Statesare charged real-time retail electricity pricesthat vary hour-to-hour as wholesale prices doBecause the extent of market power varies tre-mendously on an hourly basis the absence of

3 See Steven L Puller (2001) for an analysis of thisissue

1378 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

very-short-run elasticity is critical to under-standing its consequences4 In studying Califor-nia speci cally one must also consider thatduring the 1998ndash2001 transition period end-use consumers were insulated from energy price uctuations by the Competition TransitionCharge (CTC) The CTC was implementedalong with the restructuring of the industry inorder to allow the incumbent utilities to recovertheir stranded generation costs Due to the CTCthe vast majority of end-use consumers faced xed retail rate schedules during the transitionperiod5 Thus the CTC greatly lessened eventhe monthly elasticity of nal consumer elec-tricity demand

Due to the extreme short-run inelasticity ofdemand market power in electricity marketshas little effect on consumption quantity orshort-run allocative ef ciency As described be-low however generating companies in Califor-nia vary markedly in their costs and generationcapacity so the exercise of market power byone rm can lead to an inef cient reallocationof production among generating rms a rmexercising market power will restrict its outputso that its marginal cost is below price (andequal to its marginal revenue) while other rmsthat are price-taking will produce units of outputfor which their marginal cost is virtually equalto price Thus there will be inef cient produc-

tion on a marketwide basis as more expensivecompetitive production is substituted for lessexpensive production owned by rms with mar-ket power This is the outcome Wolak andPatrick (1997) described in the UK marketwhere higher-cost combined-cycle gas turbinegenerators owned by new entrants provide base-load power that could be supplied more cheaplyby coal- red plants that were being withheld bythe two largest rms Joskow and Kahn (2002) nd evidence of withholding by large rms inthe California market

In addition several recent analyses havedemonstrated that the exercise of market powerin an electricity network can greatly increase thelevel of congestion on the network6 This in-creased congestion impacts negatively both theef ciency and the reliability of the system Mar-ket power can also lead rms to utilize theirhydroelectric resources in ways that decreaseoverall economic ef ciency7

Lastly electricity prices in uence long-termdecision-making in a way that can seriouslyimpact the economy and generation investmentWhile it has been pointed out that high pricesshould spur new investment and entry in elec-tricity production these investments may not beef cient if motivated by high prices that arecaused by market power which may indicate aneed not for new capacity but for the ef cientuse of existing capacity Arti cially high pricesalso can lead some rms not to invest in pro-ductive enterprises that require signi cant useof electricity or to inef ciently substitute to lesselectric-intensive production technologies

Beyond the ef ciency considerations marketpower has potentially large and important redis-tributional effects The California electricity cri-sis of 2000ndash2001 illustrates both the immensepotential size of these effects and the dif cultyof analyzing them The transitional retail ratefreeze associated with the CTC meant that theutilities bore the brunt of the wholesale priceincreases The utilitiesrsquo eventual response wasto declare bankruptcy in one case and threatento in another so the ratepayers or taxpayers

4 In California and elsewhere time-of-use rates are com-mon for large users These price schedules generally havepreset peak shoulder and off-peak rates which are changedonly twice per year They do not distinguish for instance aweekday afternoon with extremely high wholesale pricesfrom a more moderate weekday afternoon Borenstein(2001 2002) argues that time-of-use rates are an extremelypoor substitute for real-time electricity pricing and thatreal-time pricing would greatly mitigate wholesale pricevolatility Patrick and Wolak (1997) estimate the within-dayprice responsiveness of industrial and commercial custom-ers facing real-time half-hourly energy prices in the Englandand Wales electricity market They argue that an electricitymarket would be much less susceptible to the exercise ofmarket power if even one-quarter of peak demand had theaverage level of price responsiveness that they estimate

5 Even ldquodirect accessrdquo consumers who bought energyfrom some source other than their incumbent utility wereinsulated from wholesale energy price uctuations in theshort run by the CTC This is because the stranded costcomponent paid by all consumers was calculated in a waythat moved inversely to the energy price the higher theenergy price the lower the CTC payment for that hour

6 See Judith B Cardell et al (1997) Bushnell (1999)Borenstein et al (2000) and Joskow and Jean Tirole (2000)

7 See Bushnell (2003)

1379VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

ultimately became the bearers of much of thesecosts At this writing it is still unclear who willbear what share of the expense and how muchof the revenues paid to generators will be re-funded to buyers under orders from federalregulators

II The California Electricity Market

Through December 2000 the two primarymarket institutions in California were the PowerExchange (PX) and the Independent SystemOperator (ISO) The PX ran a day-ahead andday-of market for electrical energy utilizing adouble-auction format Firms submitted bothdemand and supply bids then the PX set themarket-clearing price and quantity at the inter-section of the resulting aggregate supply anddemand curves In the PX day-ahead marketwhich was by far the largest market in Califor-nia rms bid into the PX offers to supply orconsume power the following day for any or allof the 24 hourly markets The PX markets wereeffectively nancial rather than physical rmscould change their day-ahead PX positions bypurchasing or selling electricity in the ISOrsquosreal-time electricity spot market8

The PX was not the only means for buyersand sellers to transact electricity in advance ofthe actual hour of supply A buyer and sellercould make a deal bilaterally All institutionsthat scheduled transactions in advance includ-ing the PX were known as ldquoscheduling coordi-natorsrdquo (SCs)9 Because SCs use the transmissiongrid to complete some transactions they arerequired to submit the generation and loadschedules associated with these transactions tothe ISO

The ISO is responsible for coordinating theusage of the transmission grid and ensuring thatthe cumulative transactions or schedules donot constitute a reliability risk ie are not

likely to overload the transmission system10 Asthe institution responsible for the real-time op-eration of the electric system the ISO must alsoensure that aggregate supply is continuouslymatched with aggregate demand In doing sothe ISO operates an ldquoimbalance energyrdquo marketwhich is also commonly called the real-time orspot energy market In this market additionalgeneration is procured in the event of a supplyshortfall and generators are relieved of theirobligation to provide power in the event thatthere is excess generation being supplied to thegrid Like the PX this market is run through adouble-auctionprocess although of slightly dif-ferent format Firms that deviate from their for-mal schedules are required to purchase (or sell)the amount of their shortfall (or surplus) on theimbalance energy market During our sampleperiod no further penalties were assessed fordeviating from an advance schedule The imbal-ance energy market therefore serves as the defacto spot market for energy in California Dur-ing our sample period the ISO imbalance en-ergy market constituted less than 5 percent oftotal energy sales with the PX accounting forabout 85 percent and the remainder taking placethrough bilateral trades

The ISO also operates markets for the acqui-sition of reserve or stand-by capacity Reservecapacity is used to meet unexpected demandpeaks and to adjust production at differentpoints on the grid in order to relieve congestionon the transmission grid while still meeting alldemand These reserves known as ldquoancillaryservicesrdquo are purchased through a series ofauctions that determine a uniform price for thecapacity of each reserve purchased Most of thereserve capacity is still available to provideimbalance energy in real time and thereforewill impact the spot price A production unitcommitted to provide reserve capacity duringan hour would therefore earn a capacity pay-ment for being available and if called upon inreal time would earn the imbalance energyprice for actually providing energy

ldquoRegulation reserverdquo the most short-term re-8 Though the transaction costs of trading in the PX and

ISO differed these differences were negligible relative tothe costs of the underlying commodity electrical energy

9 In January of 2001 the PX ceased operation and theCalifornia Department of Water Resources assumed respon-sibility for the bulk of wholesale purchases on behalf of allinvestor-owned utilities in California negotiating bilateralpurchases and operating as its own SC

10 Unlike the PX the ISO continued to function in ap-proximately its original role through the 2000ndash2001 elec-tricity crisis

1380 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

serve is treated differently Regulation reserveunits are directly controlled by the ISO andadjusted second-by-second in order to allow theISO to continuously balance supply and de-mand and to avoid overloading of transmissionwires For this reason we treat it differently inour analysis as described later

A Market Structure of California Generation

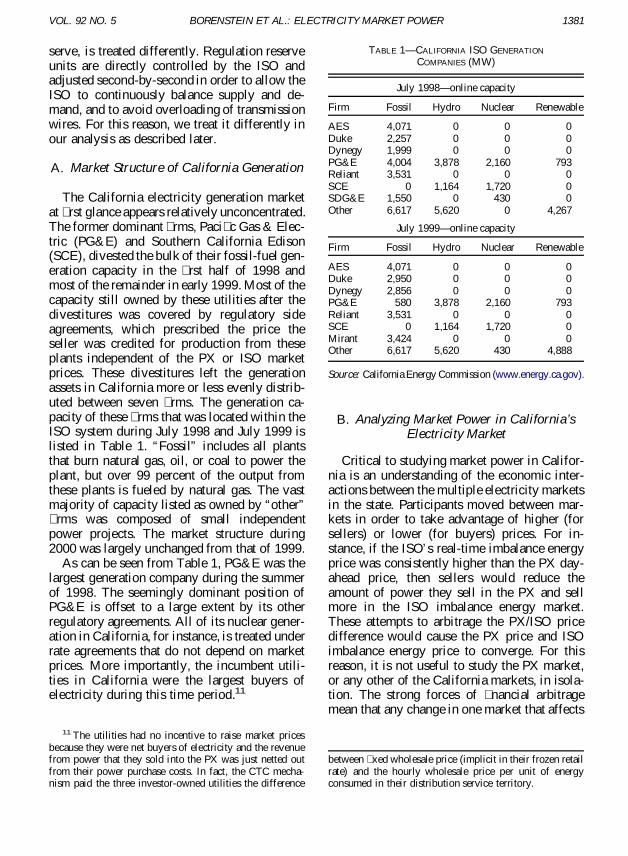

The California electricity generation marketat rst glance appears relatively unconcentratedThe former dominant rms Paci c Gas amp Elec-tric (PGampE) and Southern California Edison(SCE) divested the bulk of their fossil-fuel gen-eration capacity in the rst half of 1998 andmost of the remainder in early 1999 Most of thecapacity still owned by these utilities after thedivestitures was covered by regulatory sideagreements which prescribed the price theseller was credited for production from theseplants independent of the PX or ISO marketprices These divestitures left the generationassets in California more or less evenly distrib-uted between seven rms The generation ca-pacity of these rms that was located within theISO system during July 1998 and July 1999 islisted in Table 1 ldquoFossilrdquo includes all plantsthat burn natural gas oil or coal to power theplant but over 99 percent of the output fromthese plants is fueled by natural gas The vastmajority of capacity listed as owned by ldquootherrdquo rms was composed of small independentpower projects The market structure during2000 was largely unchanged from that of 1999

As can be seen from Table 1 PGampE was thelargest generation company during the summerof 1998 The seemingly dominant position ofPGampE is offset to a large extent by its otherregulatory agreements All of its nuclear gener-ation in California for instance is treated underrate agreements that do not depend on marketprices More importantly the incumbent utili-ties in California were the largest buyers ofelectricity during this time period11

B Analyzing Market Power in CaliforniarsquosElectricity Market

Critical to studying market power in Califor-nia is an understanding of the economic inter-actions between the multiple electricity marketsin the state Participants moved between mar-kets in order to take advantage of higher (forsellers) or lower (for buyers) prices For in-stance if the ISOrsquos real-time imbalance energyprice was consistently higher than the PX day-ahead price then sellers would reduce theamount of power they sell in the PX and sellmore in the ISO imbalance energy marketThese attempts to arbitrage the PXISO pricedifference would cause the PX price and ISOimbalance energy price to converge For thisreason it is not useful to study the PX marketor any other of the California markets in isola-tion The strong forces of nancial arbitragemean that any change in one market that affects

11 The utilities had no incentive to raise market pricesbecause they were net buyers of electricity and the revenuefrom power that they sold into the PX was just netted outfrom their power purchase costs In fact the CTC mecha-nism paid the three investor-owned utilities the difference

between xed wholesale price (implicit in their frozen retailrate) and the hourly wholesale price per unit of energyconsumed in their distribution service territory

TABLE 1mdashCALIFORNIA ISO GENERATION

COMPANIES (MW)

July 1998mdashonline capacity

Firm Fossil Hydro Nuclear Renewable

AES 4071 0 0 0Duke 2257 0 0 0Dynegy 1999 0 0 0PGampE 4004 3878 2160 793Reliant 3531 0 0 0SCE 0 1164 1720 0SDGampE 1550 0 430 0Other 6617 5620 0 4267

July 1999mdashonline capacity

Firm Fossil Hydro Nuclear Renewable

AES 4071 0 0 0Duke 2950 0 0 0Dynegy 2856 0 0 0PGampE 580 3878 2160 793Reliant 3531 0 0 0SCE 0 1164 1720 0Mirant 3424 0 0 0Other 6617 5620 430 4888

Source California Energy Commission (wwwenergycagov)

1381VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

that market price will spill over into the othermarkets12

This interaction of the different Californiaelectricity markets means that we must studythe entire California energy market in order toanalyze market power in the state For thisreason in the analysis below we look at allgeneration in the ISO control area regardless ofwhether the power from a generating plant isbeing sold through the ISO the PX or someother scheduling coordinator

Recognition that the California power marketis effectively an integrated market due to arbi-trage forces yields two other important insightsFirst although the California market has somelarge buyers of electricity directly purchasingfrom the transmission network who may re-spond to hourly wholesale prices the large util-ity distribution companies (UDCs) cannotcontrol the level of end-use demand of theircustomers because these customer face priceschedules that do not vary with the hourlywholesale price The UDCs cannot thereforereduce end-use consumption in a given hour inorder to lower overall power purchase costsThey did have some limited freedom as towhich market they used for purchase of theirrequired power choosing between buying day-ahead in the PX and spot purchases from theISO imbalance energy market Nonetheless be-cause sellers could move between markets aswell ultimately the buyers had no ability toexercise monopsony power because they couldnot reduce their hourly demand for energy

The second insight from a recognition ofmarket integration involves the impact of pricecaps in the various markets Because the ISOimbalance energy market was the last in a se-quence of markets the level of the price cap inthe imbalance energy market fed back to forman implicit cap on prices in the other advancemarkets That is knowing that the maximumone might have to pay for power in real timewas capped at $250 per megawatt-hour (MWh)for example no buyer would be willing to paymore than $250 for purchases in advance Thus

the aggregate demand curve in the day-aheadPX market became near horizontal at pricesapproaching the level of the price cap in the ISOimbalance energy market13

Many of the suppliers that compete in theISO or PX also are eligible to earn capacitypayments for providing ancillary services aswell as energy payments for generating in realtime if they bid successfully into one of theancillary services markets Ancillary servicestherefore represent an alternative use of much ofthe generation capacity in California It is there-fore necessary to consider the interaction be-tween the energy and ancillary servicesmarkets In the case of the California marketthe relevant consideration is that the provisionof ancillary services in most cases does notpreclude the provision of energy in the real-timemarket Thus for the bulk of generation thedecisions to sell into ancillary service capacitymarkets and real-time energy markets are notmutually exclusive

It is important to recognize that the pool ofsuppliers available to ancillary services marketsis very similar to that available to the energymarkets The main difference is that some gen-erators are physically unable to provide certainancillary services Thus there are fewer poten-tial suppliers for some ancillary services thanthere are for energy We therefore would expectthat the energy market would be at least ascompetitive as the ancillary services marketsand probably more so In fact the ancillaryservices markets for a variety of reasons ap-pear to have been signi cantly less competitivethan the energy market during the time period ofour study14

The other prominent opportunity for the us-age of California generation is the supply ofpower to neighboring regions Higher prices forelectricity outside of California could produce aresult in which generators within Californiawere able to earn prices above their marginalcost even if all generators behaved as price-takers For this to be the case however theCalifornia ISO region would have to be a netexporter of power During our sample period

12 Borenstein et al (2001) nds that although signi cantprice differences between the PX and ISO did occur duringindividual months overall there was no consistent patternof the PX price being higher or lower than the ISO price

13 See Bohn et al (1999)14 See Wolak et al (1998)

1382 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

such conditions arose in only 17 hours out of the22681 hours in the sample Even in these hoursthe maximum net quantity of energy exportedout of the ISO control area in any hour was amodest 608 MWh Therefore if we assume thattrading in these markets was ef cient the netexport opportunities for producers within Cali-fornia were very limited relative to the Califor-nia market

Even if this were not the case however ouranalysis would fully account for the opportunitycost of exports because under the Californiamarket structure rms from other states had theoption to purchase power through markets runby the PX and ISO Thus power exported toArizona for example would raise the quantitydemanded in the California market and there-fore would increase the competitive market-clearing price within the California PX and ISOmarkets If transmission became congestedthen further exports would be infeasible and thequantity demanded in the California marketwould include only the exports up to the trans-mission constraint Thus the competitive mar-ket prices we estimate incorporate opportunitiesfor export from California

III Measuring Market Power in CaliforniarsquosElectricity Market

The fundamental measure of market power isthe margin between price and the marginal costof the highest cost unit necessary to meet de-mand As discussed above if no rm wereexercising market power then all units withmarginal cost below the market price would beoperating Even in a market in which some rms exercise considerable market power themarginal unit that is operating could have amarginal cost that is equal to the price When a rm with market power reduces output from itsplants or equivalently raises its offer price forits output its production is usually replaced byother more expensive generation that may beowned by nonstrategic rms

In estimating a price-cost margin in this pa-per we therefore must estimate what the systemmarginal cost of serving a given level of de-mand would be if all rms were behaving asprice-takers In the following subsections wedescribe the assumptions and data used for gen-

erating estimates of the system marginal cost ofsupplying electrical energy in California

A Market-Clearing Prices and Quantities

As described above the California electricitymarket in fact consists of several parallel andoverlapping markets Given that generation anddistribution rms as well as other power trad-ers can arbitrage the expected price of energyacross these commodity markets we rely uponthe unconstrained PX day-ahead energy price asour estimate of energy prices in any givenhour15 We chose to rely upon the PX uncon-strained price because the PX handled over 85percent of the electricity transactions during oursample period and the unconstrained PX pricerepresents the market conditions most closelyreplicated in our estimates of marginal costs Inparticular we do not consider the costs of trans-mission congestion or local reliability con-straints in our estimates of the marginal cost ofserving a given demand The PX unconstrainedprice is also derived by matching aggregatesupply with aggregate demand without consid-ering these constraints The resulting market-clearing price therefore re ects an outcome thatwould occur in the absence of transmission con-straints just as our cost calculations re ect theoutcome in a market in which all producers areprice-takers and there are no transmissionconstraints16

It has been argued that the day-ahead PXprice should be expected to systematically over-state the marginal cost of energy supply becausesellers in the day-ahead market would include a

15 One might be concerned that this arbitrage would nothold in light of the requirement during our sample periodthat the three investor-owned utilities buy all of their energyfrom the PX Given the nancial nature of the PX marketand availability of a number of forward market products tohedge the day-ahead PX price risk the full meaning of thisrequirement was ambiguous More importantly Borensteinet al (2001) nd that the PX and ISO prices track quiteclosely throughout most of our sample period

16 We would like to emphasize again that we use the PXprice as representative of the prices in all California elec-tricity markets This is not a study of the PX market and themarket power we nd is not limited to the PX market It isthe amount we estimate to be present in all Californiaelectricity markets Quantitatively similar results obtain us-ing day-ahead or real-time zonal prices

1383VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

premium in their offer prices to account for theopportunity of earning ancillary services reve-nues which require that the units not be com-mitted to sell power in a forward marketHowever if this were true then the PX pricewould also be systematically higher than theISO real-time price which would not includesuch a premium because suppliers of ancillaryservices are also eligible to sell energy in thereal-time market Empirically this is not thecase Over our sample period the PX averageprice was not signi cantly greater than the ISOaverage price17

The interaction of these energy markets alsorequires us to use the systemwide aggregatedemand as the market-clearing quantity uponwhich we base our marginal cost estimates Thislevel therefore includes consumption throughthe PX other SCs and any ldquoimbalance energyrdquodemand that is provided through the ISO imbal-ance energy market Consumption from all ofthese markets is in fact metered by the ISOwhich in turn allocates imbalance energycharges among SCs during an ex post settlementprocess We are therefore able to obtain theaggregate quantity of energy supplied each hourfrom the ISO settlement data

The acquisition of reserves by the ISO alsorequires discussion here Since the ISO is effec-tively purchasing considerable extra capacityfor the provision of reserves it might seemappropriate to consider these reserve quantitiesas part of the market-clearing demand levelHowever with the exception of regulation re-serve as described below all other reserves arenormally available to meet real-time energyneeds if scheduled generation is not suf cient tosupply market demand18 Thus the real-time

energy price is still set by the interaction ofreal-time energy demandmdashincluding quantitiessupplied by reserve capacitymdashand all of thegenerators that can provide real-time supplyTherefore we consider the real-time energy de-mand in each hour to be the quantity that mustbe supplied and capacity selected for reserveservices to be part of the capacity that can meetthat demand and as such to be part of ouraggregate marginal cost curve

Unlike the other forms of reserve regulationcapacity is in a way held out of the imbalanceenergy market and its capacity could thereforebe considered to be unavailable for additionalsupply For this reason we add the upwardregulation reserve requirement to the market-clearing quantity for the purposes of nding theoverall marginal cost of supply19

B Marginal Cost of Fossil-FuelGenerating Units

To estimate the marginal cost of productionfor an ef cient market we divide productioninto three economic categories reservoir must-take and fossil-fuel generation Reservoir gen-eration includes hydroelectric and geothermalproduction These facilities differ from all oth-ers in that they face a binding intertemporalconstraint on total production which implies anopportunity cost of production that generally

17 See Borenstein et al (2001) There is also a funda-mental theoretical aw in this argument Though optionvalue would cause a rm to offer power in the day-aheadmarket at a price above its marginal cost arbitrage on thedemand side (and by sellers that do not qualify to provideancillary services) would still equalize the market pricesThe equilibrium outcome would just have a reduced shareof power sold through the day-ahead market due to theforgone option value

18 In other words all reserve capacity that is economic atthe market price is assumed to be used to meet energydemands in real time Due to reliability concerns the ISOoccasionally has not utilized some types of reserve (ldquospin-

ningrdquo and ldquononspinningrdquo) for the provision of imbalanceenergy even when the units are economic (see Wolak et al1998) The conditions under which this occurs are some-what irregular and dif cult to predict For the purposes ofthis analysis we have assumed that these forms of reserveare utilized for the provision of imbalance energy

19 Regulation reserve is procured for both an upward(increasing) and downward (decreasing) range of capacityThe amount of upward regulation reserve at times reachedas high as 108 percent of total ISO demand although themean percentage of upward regulation was 22 percent overour sample Because the generation units that are providingdownward regulation are by de nition producing energythe capacity providing downward regulation should not beconsidered to be held out of the energy market Note alsothat by adding regulation needs to the market demand weare implicitly assuming that all regulation requirements aremet by generation units with costs below the market-clearing price To the extent that some units providingregulation would not be economic at the market price thisassumption will tend to bias downward our estimate of theamount of market power exercised

1384 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

exceeds the direct production cost Must-takegeneration operates under a regulatory side agree-ment and is always inframarginal to the marketBecause of the incentives in the regulatoryagreements these units will always operatewhen they physically can All nuclear facilitiesare must-take as well as all wind and solarelectricity production We discuss below ourtreatment of reservoir and must-take generation

For fossil-fuel generation we estimate mar-ginal cost using the fuel costs and generatoref ciency (ldquoheat raterdquo) of each generating unitas well as the variable operating and mainte-nance (OampM) cost of each unit For units underthe jurisdiction of the South Coast Air QualityManagement District (SCAQMD) in southernCalifornia we also include the cost of NOxemissions which are regulated under a trade-able emissions permit system within SCAQMDThe cost of NOx permits was not signi cant in1998 and 1999 but rose sharply during thesummer of 2000 The generator cost estimatesare detailed in Appendix A Figure 1 illustratesthe aggregate marginal cost curve for fossil-fuelgeneration plants located in the ISO control areathat are not considered to be must-take genera-tion and shows how it increased between 1998and 2000 due to higher fuel and environmentalcosts20 Note that because the higher-cost plants

tend to be the least fuel ef cient and the heavi-est polluters increases in fuel costs and pollu-tion permits not only shift the supply curve butalso increase its slope since the costs of high-cost plants increase by more than the costs oflow-cost plants21

The supply curves illustrated in Figure 1 do notinclude any adjustments for ldquoforced outagesrdquoGeneration unit forced (as opposed to sched-uled) outages have traditionally been treated asrandom independent events that at any givenmoment may occur according to a probabilityspeci ed by that unitrsquos forced outage factor Inour analysis each generation unit i is assigneda constant marginal cost mcimdashre ecting thatunitrsquos average heat rate fuel price and its vari-able OampM costmdashas well as a maximum outputcapacity capi Each unit also has a forced out-age factor fofi which represents the probabil-ity of an unplanned outage in any given hour

Because the aggregate marginal cost curve isconvex estimating aggregate marginal cost usingthe expected capacity of each unit capi z (1 2fofi) would understate the actual expected costat any given output level22 We therefore sim-ulate the marginal cost curve that accounts forforced outages using Monte Carlo simulationmethods If the generation units i 5 1 Nare ordered according to increasing marginalcost the aggregate marginal cost curve pro-duced by the jth draw of this simulation Cj(q)is the marginal cost of the kth cheapest gener-ating unit where k is determined by

(1) k 5 arg min5 x Oi 5 1

x

I~i z cap i $ q6

20 Costs of generation shown in Figure 1 are based onmonthly average natural gas and emissions permit pricesHere and throughoutour analysis we assume that gas pricesare competitively determined and accurately reported If gasmarkets were not competitive or reported prices exceeded

the actual prices paid by electricity generators as recentFederal Energy Regulatory Commission ndings have sug-gested then we have underestimated the full impact ofmarket power on the wholesale price of electricity

21 Our estimates assume that the rated capacities of theplants capi are strictly binding constraints It has been pointedout to us that the plants can be run above rated capacity butat the cost of increased wear and more frequent mainte-nance If we incorporated this factormdashabout which thereseems to be very little detailed informationmdashit would shiftrightward the industry supply curve and would increase ourestimates of the extent to which market power was exercised

22 For any convex function C(q) of a random variableq we have by Jensenrsquos inequality E(C(q)) $ C(E(q))

FIGURE 1 CALIFORNIA FOSSIL-FUEL PLANTS MARGINAL

COST CURVES SEPTEMBER

1385VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

where I(i) is an indicator variable that takes thevalue of 1 with probability of 1 2 fofi and 0otherwise For each hour the Monte Carlo sim-ulation of each unitrsquos outage probability is re-peated 100 times In other words for eachiteration the availability of each unit is basedupon a random draw that is performed indepen-dently for each unit according to that unitrsquosforced outage factor The marginal cost at agiven quantity for that iteration is then the mar-ginal cost of the last available unit necessary tomeet that quantity given the unavailability ofthose units that have randomly suffered forcedoutages in that iteration of the simulation Ifduring a given iteration the fossil-fuel demand(total demand minus hydro must-take and thesupply of imports at the price cap) exceededavailable capacity the price was set to the max-imum allowed under the ISO imbalance energyprice cap during that period Note that in nearlyall cases the PX price in that hour did not hitthe price cap so such outcomes were counted asldquonegative market powerrdquo outcomes in the anal-ysis Thus these outcomes are not driving andif anything are reducing our nding of marketpower

We did not adjust the output of generationunits for actual outages because the schedulingand duration of planned outages for mainte-nance and other activities is itself a strategicdecision Wolak and Patrick (1997) present ev-idence that the timing of such outages was ex-tremely pro table for certain rms in the UKelectricity market It would therefore be inap-propriate to treat such decisions as randomevents Because we nd market power in thesummer monthsmdashhigh-demand periods in Cal-ifornia in which the utilities have historicallyavoided scheduled maintenance on most gener-ationmdashit is unlikely that scheduled maintenancecould explain these results in any case23 Wewould expect scheduled maintenance to takeplace in the autumn winter and spring monthswhich is the time period over which we ndlittle if any market power

The operation of generation units entails

other costs in addition to the fuel and short-runoperating expenses It is clear that sunk costssuch as capital costs and periodic xed capitaland maintenance expenses should not be in-cluded in any estimate of short-run marginalcost More dif cult are the impacts of variousunit-commitment costs and constraints such asthe cost of starting up a plant the maximumrates at which a plantrsquos output can be ramped upand down and the minimum time periods forwhich a plant can be on or off These constraintscreate nonconvexities in the production costfunctions of rms For a generating unit that isnot operating these costs are clearly not sunkOn the other hand it is not at all clear how orwhether a price-taking pro t-maximizing rmwould incorporate such costs into its supply bidfor a given hour In fact it is relatively easy toconstruct examples where it would clearly notbe optimal to incorporate start-up costs in asupply bid24 We do not attempt to capturedirectly the impacts of these constraints on ourcost estimates Below we discuss how noncon-vexities could affect the interpretation of ourresults

C Imports and Exports

One of the most challenging aspects of esti-mating the marginal cost of meeting total de-mand in the ISO system is accounting forimports and exports between the ISO and othercontrol areas We can however observe the netquantity of power entering or leaving the ISOsystem at each intertie point as well as thewillingness of rms to import and export to andfrom California

If the power market outside of California

23 Scheduled maintenance on must-take resources andreservoir energy sources was accounted for under the pro-cedures outlined in the following subsections

24 Consider a generator that estimates it will be ldquoinrdquo themarket for six hours on a given day and bids into the marketin each hour at a level equal to its fuel costs plus one-sixthof its start-up cost Consider the results if the market pricein one hour rises to a level suf cient to recover all start-upcosts but in all subsequent hours remains at a level abovethe unitrsquos fuel costs but below the sum of its fuel cost plusthe prorated start-up costs If this unit committed to operatein the one hour that it covers its fuel costs plus one-sixth ofits start-up costs but stayed ldquooutrdquo of the market in subse-quent hours it is not maximizing pro ts because it couldhave earned an operating pro t at market-clearing prices inthe ve remaining hours

1386 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

were perfectly competitive then the marginalgenerator that is importing into Californiawould absent transmission constraints have amarginal cost about equal to the market price inCalifornia When market power is exercisedwithin California this would mean that in aneffort to drive up price some in-state generatorsare withdrawing (or raising the offer price on)their marginal generation and allowing moreexpensive imported power to be substituted forit Thus in the absence of market power wewould see lower imports This means that thecost of serving the demand that remains afterthe competitive level of imports is netted outwould be higher than the cost of serving thedemand that remains after the true level of im-ports is adjusted for25

Figure 2 illustrates a hypothetical marginalcost curve of the in-state generation excludingmust-take (qmt) and reservoir energy resources(qrsv) The market demand is qtot and the ob-served price is Ppx At a price of Ppx we seeimports of qimp (5qtot 2 qr) that shift theremaining demand to the left to a quantity qr If

the price were instead set at the competitiveprice of Pcomp we would see imports at somelevel less than or equal to those seen at PpxThis would shift the residual in-state demand toa quantity qr Thus in order to estimate theprice-taking outcome in the market we need toestimate the net import or net export supplyfunction

Estimating the Net ImportExport SupplyFunctionsmdashOne of the primary responsibilitiesof the California ISO is to ensure the reliableusage of the systemrsquos transmission networkThis requires that the ISO operate a market forrationing transmission capacity when its use isoversubscribed This market is implementedthrough the use of schedule ldquoadjustmentrdquo bidswhich are submitted by scheduling coordinatorsto the ISO along with their preferred day-aheadschedules

Scheduling coordinators submit their pre-ferred import or export quantities and the ISOchecks to see whether these ows exceed trans-mission capacity limits If these proposed power ows are feasible no further adjustments arerequired In the event that the net of proposedimport and export schedules does exceed trans-mission capacity on some intertie the ISO ini-tiates a process of congestion relief by adjustingschedules according to their adjustment bidsAdjustment bids establish for each schedulingcoordinator a willingness-to-pay for transmis-sion usage Schedules are adjusted according tothese values of transmission usage starting atthe lowest value until the congestion along theintertie is relieved A uniform price for trans-mission usage paid by all SCs using the intertieis set at the last or highest value of transmis-sion usage bid by an SC whose usage wascurtailed

Adjustment bids reveal the willingness-to-supply imported energy of out-of-state suppliers(and exported energy of in-state suppliers) ateach intertie over a wide range of quantities notjust at the observed net importexport quantityFor the vast majority of hours the aggregate net ow is into California for the relevant pricerange so we refer to this as the import supplycurve but negative import supply (net export) ispossible Let the import supply curve of sched-uling coordinator sc at import zone z be the net

25 Capacity constraints on both the transmission intertiesinto California and the production capacity of non-Californianproducers complicate this intuition somewhat If such acapacity constraint were binding at the observed Californiamarket-clearing price then the marginal production cost ofimports would most likely be below this market-clearingprice and thus a perfectly competitive price within Cali-fornia would yield only weakly lower imports

FIGURE 2 IMPORT ADJUSTMENTS AND EFFICIENCY LOSSES

1387VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

of its preferred import quantity and all of itsincremental and decremental adjustment bidsinto California from z

(2) qzsc~ p 5 qz

sc init 1 Op p

qzsc inc~p

2 Op p

q zsc dec~ p

In other words the preferred level of importsfrom sc at z at a price of p would be itsscheduled imports which are independent ofprice plus the amount of additional supply it iswilling to provide in exchange for receiving apayment less than or equal to p minus theamount of reduction in supply that it wouldagree to in exchange for making a payment thatis greater than or equal to p The aggregate netimport curve into the California ISO system forany hour can be calculated by summing thevalue of qz

sc( p) over all interties and SCs

(3) q imp ~p 5 Osc

Oz

qzsc~ p

This aggregation constitutes an upper boundon the responsiveness of net imports to changesin the California price The ISO is in practiceprevented from substituting import adjustmentbids across individual scheduling coordinatorsor across transmission interties so that the ac-tual import supply curve will be a signi cantlysteeper function of price than the curve con-structed as described The ISO will only act inthe event that the initial schedules indicate thatcongestion will arise even though the adjust-ment bids may indicate a potential Pareto-improving import adjustment Thus while ouraggregate import supply curve assumes that allimports from all locations are perfect substi-tutes and that these imports are priced at mar-ginal cost reality falls short of this level ofimport ef ciency26

Our analysis assumes that wholesale electric-ity suppliers outside of California are price-takersso that the import supply curve represents theaggregate marginal cost curve of suppliers out-side of California net of their native load obli-gations Some observers have argued that thesuppliers of electricity outside of Californiamay exercise market power (ie offer power atabove their marginal cost) when selling into theCalifornia market If this is the case then animport supply curve that re ected no marketpower from out-of-state suppliers would indi-cate a greater supply of imports at every priceand therefore a leftward shift in the residualdemand curve in Figure 6 which would lowerthe competitive benchmark price Thus ourtreatment of imports will tend to bias downwardour estimates of the extent of market power

D Hydroelectric and Geothermal Generation

Reservoir generation units (ie hydro andgeothermal units) present a different challengebecause the concern is not over a change inaggregate output relative to observed levels butrather a reallocation over time of the limitedenergy that is available to them Thus the bidsof hydro units do not re ect a production costbut rather the opportunity cost of using thehydro energy at some later time

In the case of a hydro rm that is exercisingmarket power this opportunity cost would alsoinclude a component re ecting that rmrsquos abil-ity to impact prices in different hours27 It isimportant to note that even the actual observedbid prices of a small price-taking hydroelectric rm operating in an oligopoly market wouldprovide little information about its opportunitycost of the energy if the entire market wereperfectly competitive because the actual oppor-tunity cost of water for these units will be in- uenced by the expectation of future prices

26 One consequence of this is that the import quantitiesimplied by the aggregate of the adjustment bids do notexactly equal the imports that are actually observed Torealign the import supply curve implied by the adjustmentbids with the observed import-price pair for each hour wecalculate the change in imports in each hour as Dqimp( p) 5

q imp( p) 2 q imp( pactual) where pactual is market priceduring the hour under consideration This adjustment en-sures that at prices equal to the actual observed price for thathour there would be no change from the observed level inimports when performing our counterfactual price calcula-tion A positive Dq imp( p) implies an increase in net importsrelative to the observed price

27 See Bushnell (2003)

1388 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

which in turn will be impacted by the ability ofother rms to raise those prices

For these reasons we make the assumptionthat the actual observed output of these re-sources is the output that would be produced bya price-taking rm participating in a perfectlycompetitive market In practice this assumptionmeans that in constructing our estimate of themarginal cost of meeting load in any given hourwe apply the observed production of hydro andgeothermal resources for each hour and thencalculate the marginal cost of satisfying theremaining demand with the statersquos fossil-fuelresources We give the intuition here for whythis assumption biases downward our estimatesof productive inef ciency and market power Amore detailed explanation is in Appendix C

For the purpose of calculating the impact ofmarket power on total production cost it is easyto see that this is a conservative assumption onethat will produce downward-biased estimateson the ef ciency effects of market power Theoptimal hydro schedule will by de nition leadto weakly lower production cost than any otherhydro schedule To the extent that actual pro-duction differed from the optimal schedule itcould only raise total production cost Thus ourassumption will bias upward our estimate ofperfectly competitive production cost

For the purpose of measuring market powerwe need to consider the impact of our assump-tion on our estimates of marginal productioncost Of concern is the possibility that the ob-served hydro schedule (which may include aresponse by hydro rms to the exercise of mar-ket power by others)mdashwhen combined with acounterfactual perfectly competitive productionof fossil-fuel resourcesmdashcould produce a lowermarginal cost estimate on average than the op-timal hydro schedule However it is straightfor-ward to show that when system marginalproduction costs from nonhydro sources areconvex in quantity any reallocation of hydroenergy away from the least-cost allocation willraise marginal costs more in the hours from whichenergy is removed than it will reduce marginalcost in the hours to which energy is added28 Thus

our assumption of optimal hydro production canonly bias our time-weighted estimates of mar-ginal cost upwards and therefore our estimatesof price-cost margins downward

We present results in which price-cost mar-gins are weighted by the market volumes ineach hour To consider the effect of our hydroassumptions on these results we need to ad-dress the possibility of a reallocation of hydroenergy between off-peak and peak hours rela-tive to the optimal schedule A hydro rm that isattempting to exercise market power wouldlikely allocate less hydro energy during peakhours than would be the case for a price-taking rm (see Bushnell 2003) This strategic hydroallocation when combined with competitivefossil-fuel production would produce a higherweighted average of marginal cost than wouldthe optimal schedule To the extent the rmscontrolling hydro resources attempted to exer-cise market power with those resources ourresults will therefore understate the overall levelof market power

However the vast majority of reservoir re-sources were controlled by the PGampE and SCEeach of which had a fairly strong incentive tolower wholesale power costs Therefore it ispossible that these rms responded to an in-crease in market power with an overconcentra-tion relative to perfect competition of energyduring high-demand periods As argued abovethis reallocation (if allowed by the ow con-straints) would raise off-peak marginal costsmore than it would lower on-peak marginalcosts However since (non-must-take) marketvolumes are likely to be higher on-peak theimpact on the quantity-weighted average ofmarginal cost is uncertain

We examined this issue empirically by askingwhether our estimates of marginal costs produceopportunities for a reallocation of hydro energythat would result in a lower weighted-averagemarginal cost Such an opportunity would existif fossil-fuel marginal costs during some high-demand period were lower (due to ldquooverproduc-tionrdquo from hydro sources) than the marginal costin some lower-demand period If by contrast

28 This is because at the least-cost allocation of hydroenergy marginal fossil-fuel costs will be equalized over all

hours for which hydro ow constraints allow a discretionaryuse of hydro energy

1389VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

our marginal cost estimates (over a period withstable input prices) were monotonic in marketdemand then no systematic opportunity for low-ering the weighted average of marginal cost existsand any bias from our hydro assumption is in thedirection of raising costs and lowering marketpower

To examine this possibility we estimated akernel regression of our estimated marginal cost(ie competitive price) on system demand (pre-sented in Appendix C) in order to detectwhether in aggregate there are systematic devi-ations from a monotonically increasing relation-ship between demand and our estimate ofsystem marginal cost Such regressions for eachof the three summers in our sample period showthat our system marginal cost estimates weremonotonically increasing in demand for each ofthese time periods This leads us to concludethat it is highly unlikely that our assumption thatthe actual schedule of production reservoir re-sources was the cost-minimizing schedule cre-ates a signi cant negative bias on the weighted-average estimates of system marginal costs

E Calculating Cost Increase Relative toCompetitive Outcome

Utilizing the assumptions outlined in the pre-vious sections we estimated the perfectly com-petitive market price in the California energymarkets for each hour of market operation fromJune 1998 through October 2000 The residualmarket demand to be met by in-state fossil-fuelunits within the ISO system in hour t qff

t isestimated to be

(4) q fft ~ p 5 q tot

t 1 qregt 2 qmt

t 2 qrsvt

2 q impact

t 2 Dq impt ~ p

Here q tott is the actual ISO metered generation

(including net imports) including generationscheduled through all energy markets associ-ated with the ISO control area including thePX ISO imbalance energy market and otherSCs qreg

t represents the addition to demand dueto the need for capacity dedicated to regulationreserve The quantities qmt

t and qrsvt represent

the amount of energy produced by must-take

generation and by reservoir generation respec-tively These quantities are all treated as priceinelastic The term qimpact

t 2 Dqimpt (p) is the

level of imported energy adjusted by the re-sponse to changes in the market-clearing priceas described above

For each hour we make 100 fossil-fuel gen-eration marginal cost curve estimates each re- ecting a combination of independent MonteCarlo draws for the outage of each generationunit For each of these draws from the system-wide fossil-fuel marginal cost curves we com-pute the intersection of this marginal cost curvewith the residual market demand curve qff

t ( p)This yields an estimated marginal cost and anin-state market-clearing quantity qrj

t for MonteCarlo draw j We denote the marginal costassociated with this quantity as Cj

t We can thencompute an estimate of the expected value ofthe marginal cost of meeting the in-state de-mand that results from price-taking behavior byin-state generators as

(5) P compt 5

yenj 5 1

100

~C jt

100

Note that there are cases in which Ppxt 2 P comp

t

is negative in our simulations Absent an oper-ational error or an attempt at predatory pricing rms will not actually be willing to sell power atprices below their true economic short-run mar-ginal costs In other words prices will not bebelow the perfectly competitive price Nonethe-less during some hours particularly June 1998and during the winter and spring of 1999 PXprices were below our estimates of the perfectlycompetitive market price At least three factorscontribute to these outcomes

First our cost estimates can exceed the actualmarginal cost because we do not consider thedynamic effects of unit commitment con-straints such as start-up costs ramping ratesand minimum down times These constraintscan create opportunity costs of shutting downunits that in essence lower the true marginalcost of operating that plant Of course thesesame constraints also can create opportunitycosts that at other times raise the true marginal

1390 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

cost This is one reason why we include thenegative markups in our results we did not wantto exclude the off-peak impact of these constraintson our cost estimates since there is an oppositeeffect on our estimates during peak hours

Second cost information for generating unitsare not exact data on which all parties agree Forthe most part we used values submitted to stateand federal regulatory agencies under theformer regulated regime For this reason ourestimate of a unitrsquos marginal cost may beslightly higher than the cost level at which it iscapable of operating in a market environmentTherefore we include negative price-cost differ-ences in order to prevent truncating the effect ofdata uncertainty on our cost estimates

Third and probably most important our cal-culations do not control separately for theoutput levels of reliability must-run (RMR)generation Some fossil-fuel generation unitshave been declared must-run for local grid re-liability under certain system conditions Thesegenerators get separate nonmarket paymentswhen they are called under the RMR contractsthey have signed with the ISO RMR units arenot dispatched through the price-setting pro-cess Because they are held out and paid adifferent price the resulting price in the PX canbe below the marginal cost to the system if thepower provided by RMR units were insteadprovided as part of the full dispatch of thesystem In fact due to the level of RMR calls bythe ISO during some periods during our sampleparticularly the spring of each year it is possi-ble that no other fossil-fuel generation was eco-nomic during these time periods Under thesecircumstances the highest (opportunity) costunits selling in the PX could be hydro or out-of-state coal plants either of which have lowermarginal cost than any of the fossil-fuel plantswe examine However these periods are likelyto occur when the PX price is extremely lownot extremely high In such cases import en-ergy with costs below those of in-state fossil-fuel generation could be the marginalgeneration and the actual PX price could belower than the marginal costs of any of thefossil-fuel units we have examined Because wedonrsquot account for the RMR units our estimatescould still indicate that a fossil-fuel unit is mar-ginal and its cost is the system marginal cost so

our estimated system marginal cost would beabove the actual PX price due to unaccountedfor RMR calls29

If the estimated MC is above the PX price foreither the rst or second reason then it seemsthat the most accurate estimate of market powerwould come from including the ldquonegative mar-ket powerrdquo outcomes in our calculations How-ever total start-up costs for the fossil-fuel unitsin California are about $39 million during oursample period less than 1 percent of total fossil-fuel generation production costs during the pe-riod and less than 1 percent of the market powerrents we nd30 In addition there are otherreasons to think that start-up costs explain onlya minor part of the deviations from marginalcost pricing First the units that turn on to meetpeak demand during the summer have littlestart-up costs (fuel oil or jet fuel units) or noneat all (hydroelectric units) so the impact at thetimes we nd the greatest market power is likelyto be low31 Second our estimates of marketpower are substantially greater in summer 2000than in summer 1999 but the amount of elec-tricity produced per start-up is 57 percent lowerin summer 1999 implying that start-up costswould likely be a greater factor in 1999 than in2000 Similarly the ratio of start-up costs to ourestimated fossil-fuel production costs was

29 This implies that neglecting RMR calls could under-estimate market power In addition it appears that the initialRMR agreements exacerbated some of the local marketpower problems that they were designed to mitigate SeeBushnell and Wolak (1999)

30 For 65 of the 92 units in our fossil-fuel cost curve theunit-speci c formulae for determining the cost per start-up(as a function of both input fuel costs and the price ofelectricity) were submitted to the ISO as part of the RMRcontract renegotiation process For the remaining 27 unitswe estimated the unit-speci c start-up formula by usingparameters from a similar unit that did have an RMRcontract We used the daily price for the input fuel used bythat unit and daily average annual retail price to industrialcustomers for the electricity price in the start-up costformula

31 Additionally if marginal cost functions turn upwardsmoothly around the rated capacity rather than having astrict L-shape the typical argument that a competitive plantwould bid its start-up costs for the ldquosingle hourrdquo it wouldrun are incorrect In that case even the last plant turned onwould run for many hours because it would be replacinghigher-cost output from other plants that would otherwisebe producing along the steepest parts of their MC curves

1391VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

higher in summer 1999 than in summer 2000091 percent versus 037 percent

Likewise it is unlikely that much of the neg-ative market power outcomes could be the resultof cost-data errors Many PX prices in June1998 for instance were well below the coststhat anyone has claimed for operation of fossil-fuel generating units32 Thus it is most likelythat the cost estimates that exceed the PX priceoccur because there were no fossil-fuel gener-ating units that were economic to run at thetime Only fossil-fuel units running under RMRcontracts were active In that case the marginalcost of the system and thus the market price isbeing set by much cheaper out-of-state coalplants by nuclear plants or by hydro or geo-thermal plants If this is the case then the propertreatment would be to truncate the results re-setting any nding of ldquonegative market powerrdquoto set marginal cost equal to price Still in orderto avoid biasing the results in favor of ndingmarket power we do not truncate the negativeoutcomes in the primary results we report

IV Results

We computed the expected perfectly compet-itive price each hour for the months of June1998 through October 2000 using the algorithmdescribed above From the import adjustmentbids the median hourly reduction in importsfrom the observed level at the PX price versusthe level at our estimated competitive price was24 percent For each hour we can calculate anarc elasticity implied by the adjustment bids forthe import response from the change betweenthe competitive and actual price and the result-ing change in imports The median arc elasticityof import supply for these hours is 06333

The added wholesale cost of energy due todepartures from a competitive market DTC iscalculated by taking the difference between thePX price and our estimate of competitive bench-mark price and multiplying it by the total ISO

metered generation less the must-take energyfor that hour34 That is for hour t

(6) DTC t 5 Ppxt 2 P comp

t z q tott 2 qmt

t

where P compt is the expected competitive price

in period t This expectation is taken with re-spect to the distribution of generating unit out-ages as shown in (5)

For any set of hours our measure of mar-ket performance is

(7) MP~ 5

yent [

DTC t

yent [

TC t

MP( ) is the proportional increased wholesalecost of electricity during all hours in De n-ing MP( ) in this manner is consistent with theview re ected in our competitive benchmarkMonte Carlo simulation that the observed mar-ket price is conditional on a realization fromthe joint distribution of generating unit outagesTo re ect this fact let Ppx

t denote the ob-served PX price for hour t and E(Ppx

t ) the ex-pectation of this magnitude with respect to thejoint distribution of generating unit outagesUnlike the counterfactual case of price-takingbehavior we cannot draw from the distributionof generating unit outages and compute a dis-tribution of market prices that re ect the currentlevel of market power This would require amodel for the strategic interaction among play-ers in the California market However by de- ning MP( ) as shown in equation (7) we cantake advantage of the law of large numbers toprove that our measure is a consistent estimateof the proportional cost increase To show thisrewrite the index as

(79) MP~

5

1Card~ yent [

Ppxt 2 P comp

t z qtott 2 qmt

t

1Card~ yent [

Ppxt z qtot

t 2 qmtt

32 If we were to ignore any ldquonegative market powerrdquo

outcomes for prices below say $18MWh virtually all ofthe ldquonegative market powerrdquo effects would be eliminated

33 We calculate the arc elasticity as~P1 1 P2 2

~Q1 1 Q2 2

~Q2 2 Q1

~P2 2 P1

34 By taking the observed quantity as the market de-mand we are for the reasons discussed earlier implicitlyassuming that demand is price inelastic

1392 THE AMERICAN ECONOMIC REVIEW DECEMBER 2002

where Card( ) is the cardinality or number ofelements (hours) in the set For sets with alarge number of elements the index is approx-imately equal to

(70) MP~

5

yent [

E~Ppxt 2 P comp

t z q tott 2 qmt

t

yent [

E~Ppxt z q tot

t 2 qmtt

which is equal to the ratio of the expected costincrease relative to the perfectly competitivebenchmark due to the current level of marketpower and market imperfections divided by theexpected cost of purchasing electricity undercurrent market conditions

Table 2 reports the PX price estimated mar-ginal cost and the added cost of power due toprices that exceeded marginal cost for eachmonth in the sample period As is evident fromTable 2 June 1998 produced very idiosyncraticresults with an average PX price considerablybelow our estimate of marginal cost The mar-ket was only in its third full month of operationat this time and a number of fossil-fuel gener-ation units were going through ownership trans-fer and regulatory approval of these transfersThe CTC mechanism provided the threeinvestor-owned utilities with an incentive toinduce low energy prices and the utilities werestill operating and bidding many of these unitsthrough June 1998 As described above the useof reliability must-run contracts which paidsome fossil-fuel units to run in exchange for

TABLE 2mdashACTUAL PRICE AND ESTIMATED MARGINAL COST

Month Year

Mean of ActualProductionPer Hour(MWh)

Mean ofPX Price($MWh)

Mean ofMarginal

Cost($MWh)

Sum ofDTC

($ million)

AggregateDTCTC(percent)

June 1998 24134 1209 2255 244 251July 1998 28503 3241 2733 103 28August 1998 31256 3953 2771 220 39September 1998 28209 3401 2628 134 33October 1998 25043 2665 2621 13 5November 1998 24107 2574 2753 24 22December 1998 24953 2913 2540 45 17

January 1999 24480 2096 2241 25 22February 1999 24079 1903 2120 212 27March 1999 24734 1883 2080 212 27April 1999 24763 2405 2450 4 2May 1999 24625 2361 2534 0 0June 1999 27081 2352 2589 13 5July 1999 29524 2892 2712 63 17August 1999 29813 3231 3064 56 14September 1999 28573 3391 3025 63 16October 1999 27558 4763 3438 186 31November 1999 26046 3691 2887 105 26December 1999 26647 2966 2773 30 9

January 2000 26377 3118 2766 48 13February 2000 25961 3004 2952 10 3March 2000 25618 2880 3138 217 26April 2000 25728 2660 3243 243 216May 2000 27038 4722 4043 150 25June 2000 30644 12020 5359 1152 63July 2000 30343 10572 5937 801 50August 2000 32310 16624 7619 1475 56September 2000 29981 11487 7686 577 36October 2000 27422 10151 6806 443 34

1393VOL 92 NO 5 BORENSTEIN ET AL ELECTRICITY MARKET POWER

payments that were above the market price wasalso widespread during June For these reasonswe believe the market results from June 1998 donot provide much meaningful information onthe state of competition in the California mar-ket Nevertheless for completeness we haveincluded these results For the set of all hoursover the entire 29-month period from June 1998to October 2000 the MP( ) is equal to 33percent amounting to total payments in excessof competitive levels equal to $555 billion witha standard error of $119 billion35

Having generated estimates of price-costmargins for each hour of the 29-month sampleperiod we can examine subsets of the data togain insight into the underlying dynamics of themarket One test of the credibility of our resultsis whether our estimates of market power varyin the way that economics would predict Wewould expect market power to be quite lowduring the off-peak months December throughApril Electricity demand is low in these monthsand supply is relatively large due to the resur-gence in hydro production from winter rains InDecember 1998ndashApril 1999 we nd an averageMP( ) of 19 percent and in December 1999ndashApril 2000 we nd an average MP( ) of 18percent neither of which is signi cantly differ-ent from zero Thus we nd that there wasessentially no margin between prices and mar-ginal cost during the period in which supply wasmost abundant compared to demand and sellershad the least ability to exercise market powerIn addition these results provide evidence thatsigni cant short-run operating costs are notmissing from our cost estimates because nega-tive or zero margins would not be observed oversuch an extended period of time

The series of events that led to the Californiaelectricity crisis in 2000ndash2001 began with dra-matic price increases during the summer of 2000Many policy makers and regulators have arguedthat the competitive performance of the marketfundamentally changed during summer 2000thereby initiating the crises In order to make suchcomparisons however one must account for dif-

ferences in the relative levels of demand duringthese periods As described above we would ex-pect the estimated market power to increase as thedemand faced by in-state nonutility sellers risesrelative to the capacity of these players Figure3 shows a kernel regression of this relationship forlate summer of 1998 1999 and 200036 The hor-izontal axis of Figure 3 is the demand faced bythese rms after accounting for actual importsmust-take and reservoir production The verticalaxis is the ratio DTC tTC t which is equal to theLerner index for that hour37