measuring service quality in developing … is to certify that the research paper on “measuring...

TRANSCRIPT

MEASURING SERVICE QUALITY IN DEVELOPING RETAIL

STRATEGIES FOR SUPER MARKETS IN SRI LANKA.

By

Nishan C. Perera

Dip.M (UK), MCIM , MSLIM , Chartered Marketer (UK)

Certified Professional Marketer (Asia Pacific)

A Research Paper submitted to the

Postgraduate Institute of Management

University of Sri Jayewardenepura

in partial fulfilment of the requirements

of the Master of Business Administration Degree

Colombo 08 – Sri Lanka

2003

This is to certify that the research paper on “Measuring Service Quality in

Developing Retail Strategies for Super Markets in Sri Lanka”

By

Nishan C. Perera

has been accepted by the

Postgraduate Institute of Management

University of Sri Jayewardenepura

in partial fulfilment of the requirement

of the Master of Business Administration Degree

………………………... ………………….

Research Supervisor Director - PIM

Date : Date :

LIST OF ILLUSTRATIONS

Figure 01 Types of service quality gaps 08

Figure 02 Service continuum for a product 10

Figure 03 Service quality and the extended marketing mix for services 11

Figure 04 Nordic model of perceived service quality 12

Figure 05 Gaps model on service quality 14

Figure 06 Customer assessment of service quality 14

Figure 07 Service quality dimensions of the three-component model 16

Figure 08 Service quality levels of the multilevel model 17

Figure 09 Service quality dimensions of the hierarchical approach model. 18

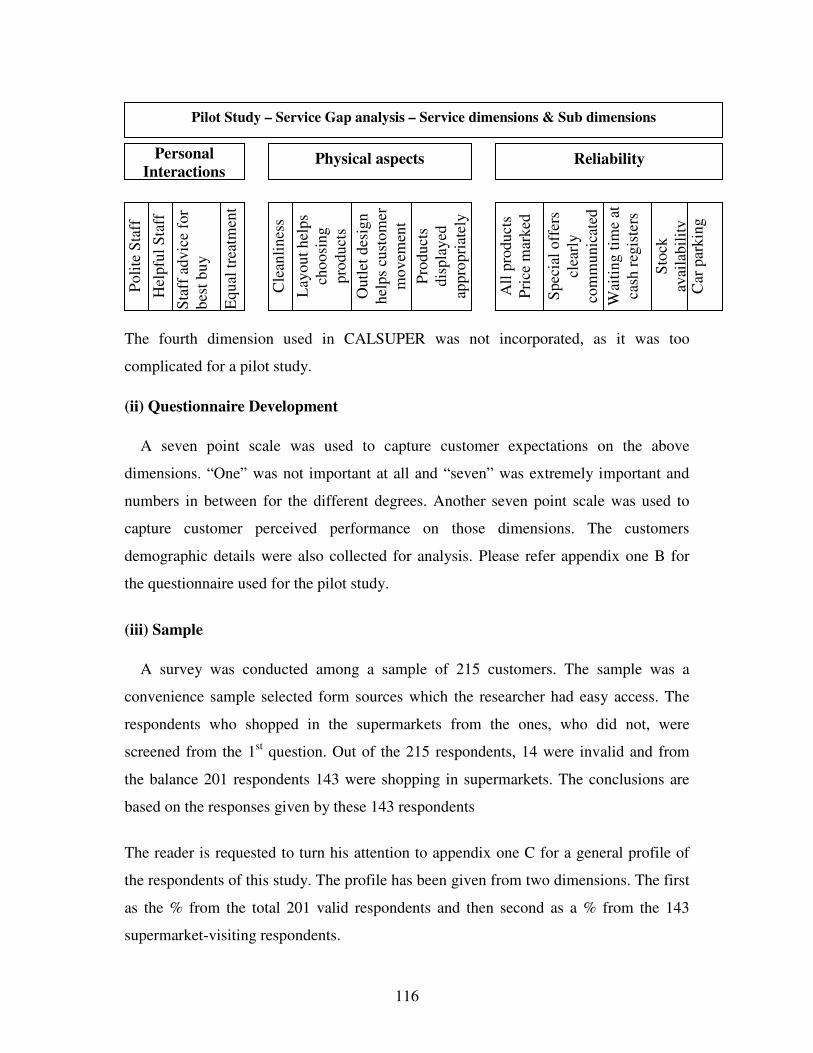

Figure 10 Conceptual framework of the CALSUPER model 19

Figure 11 Tracking service quality 20

Figure 12 Service quality and customer satisfaction 23

Figure 13 Functional & technical service quality and willingness to buy 23

Figure 14 Retail planning process 26

Figure 15 Merchandising mix strategies 28

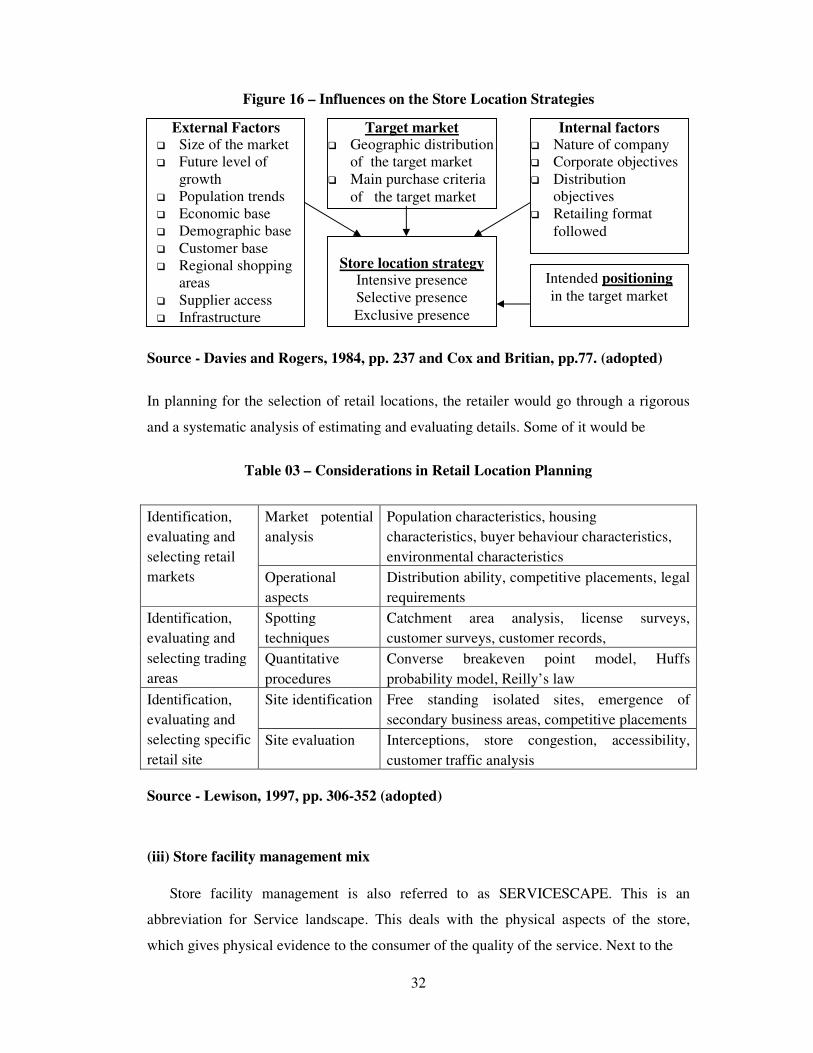

Figure 16 Influences on store location strategy 32

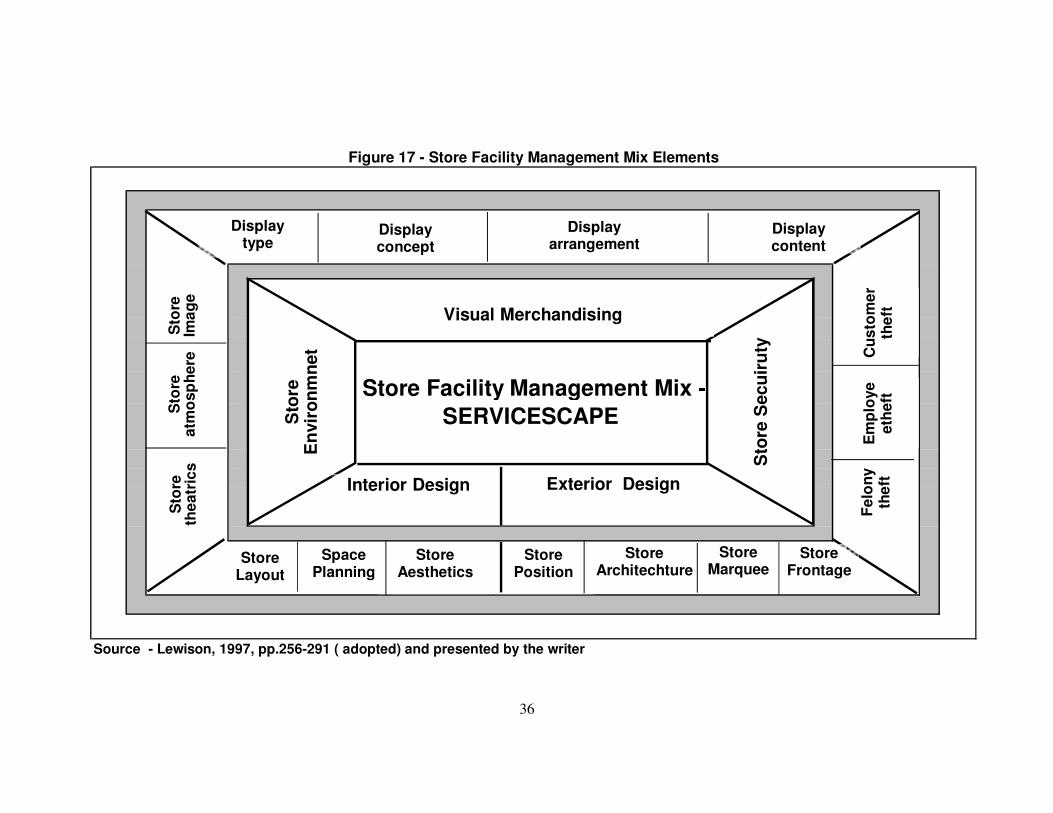

Figure 17 Store facility management mix elements 32-33

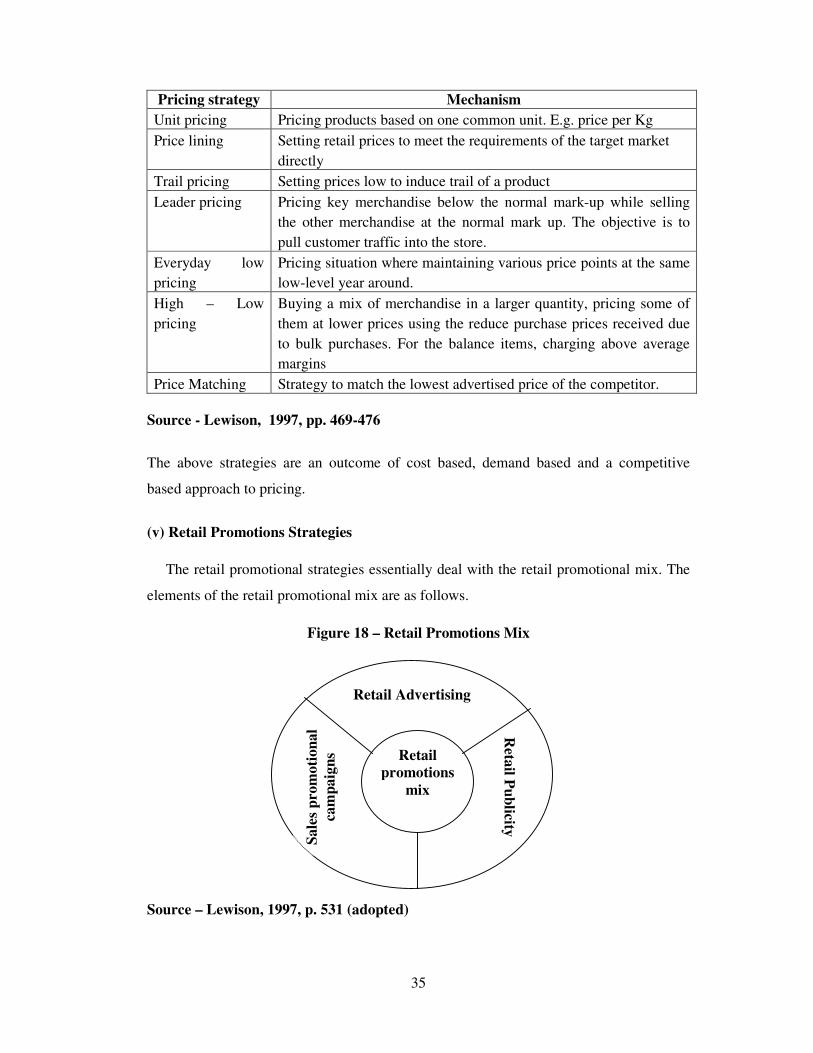

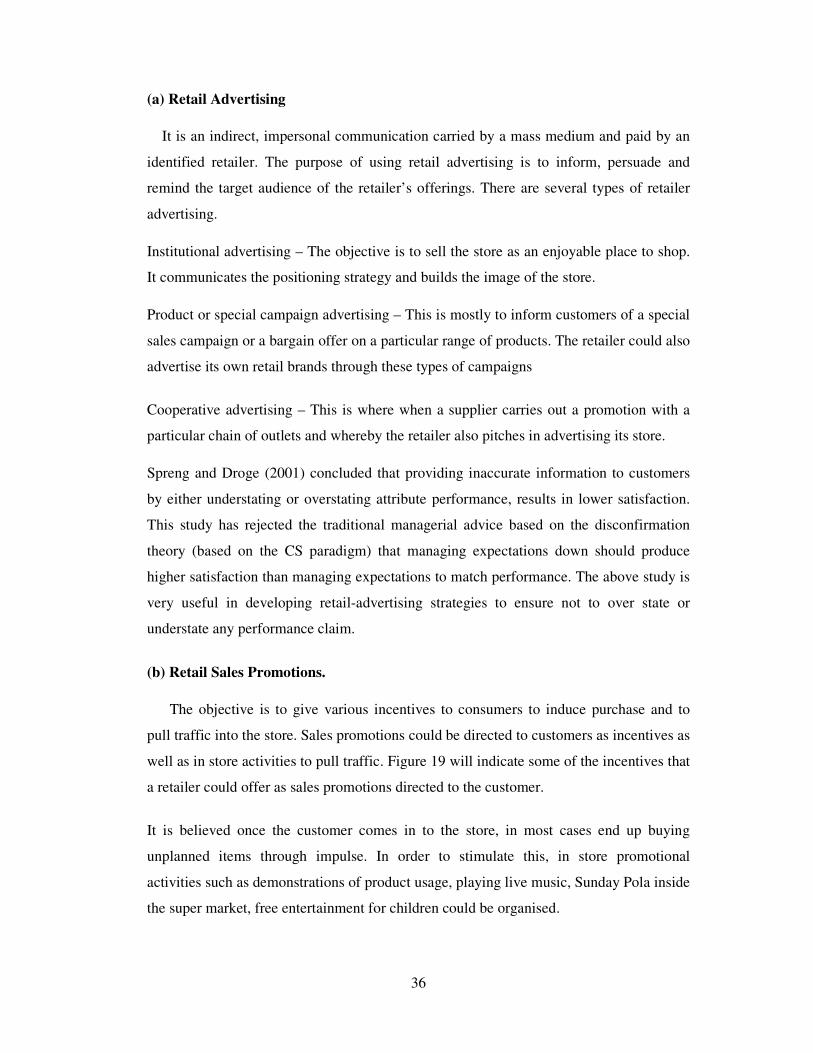

Figure 18 Retail promotions mix 35

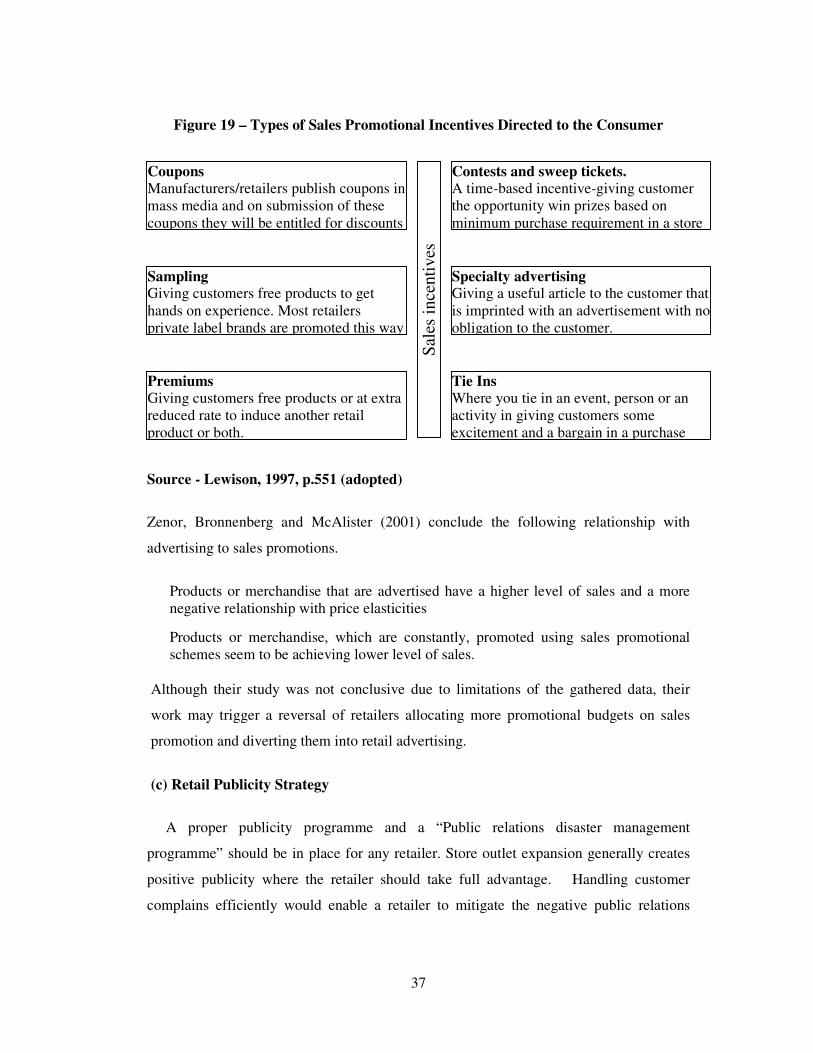

Figure 19 Types of sales promotional incentives directed to the consumer 37

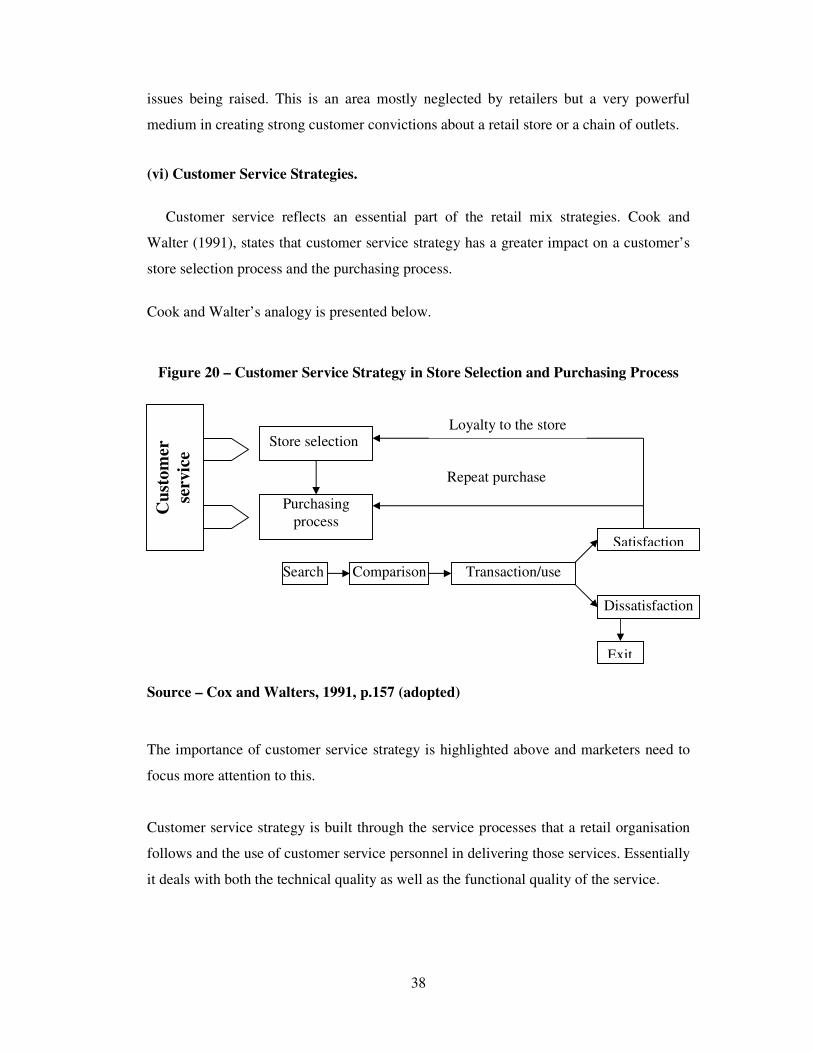

Figure 20 Customer service strategies in store selection and purchasing 38

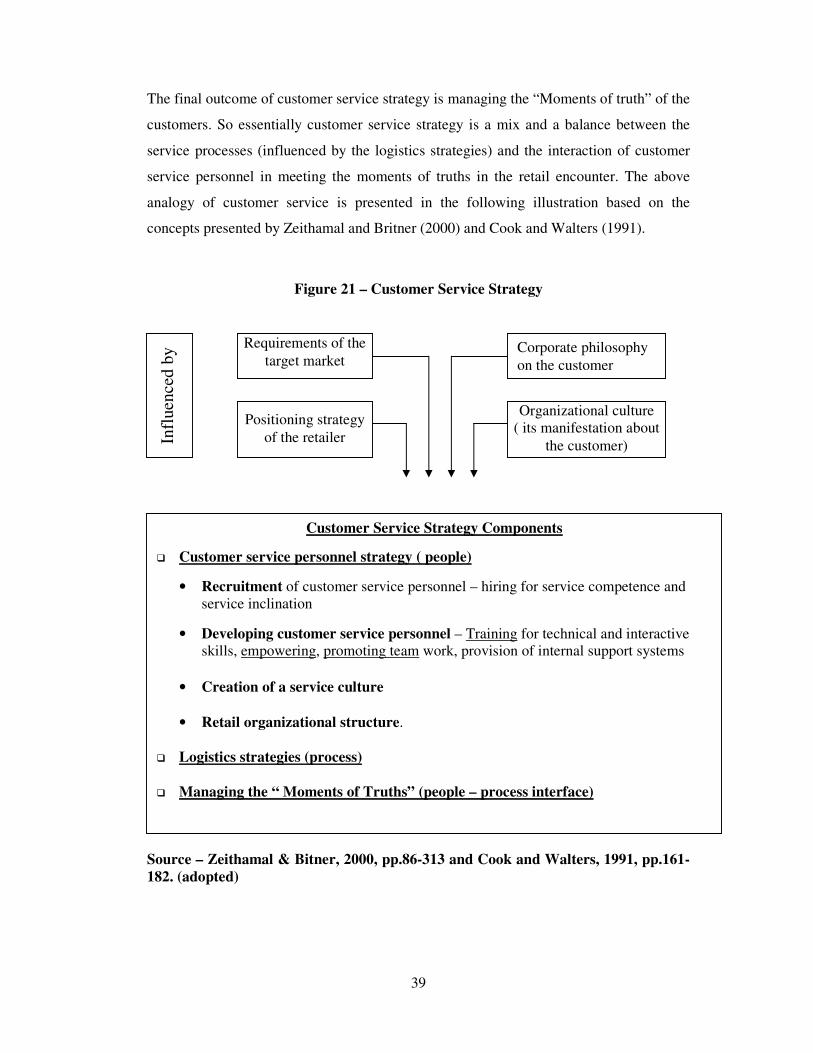

Figure 21 Customer service strategy 39

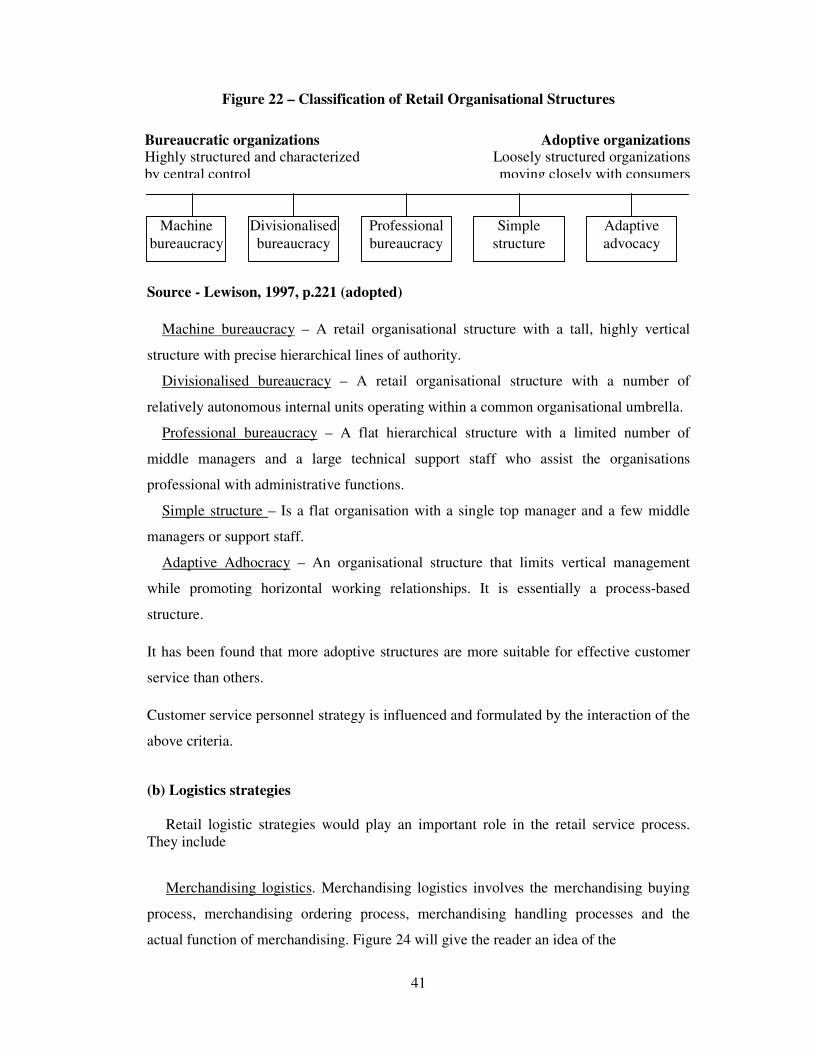

Figure 22 Classifications of in a retail organisational structures 41

Figure 23 Merchandising logistics strategies 42

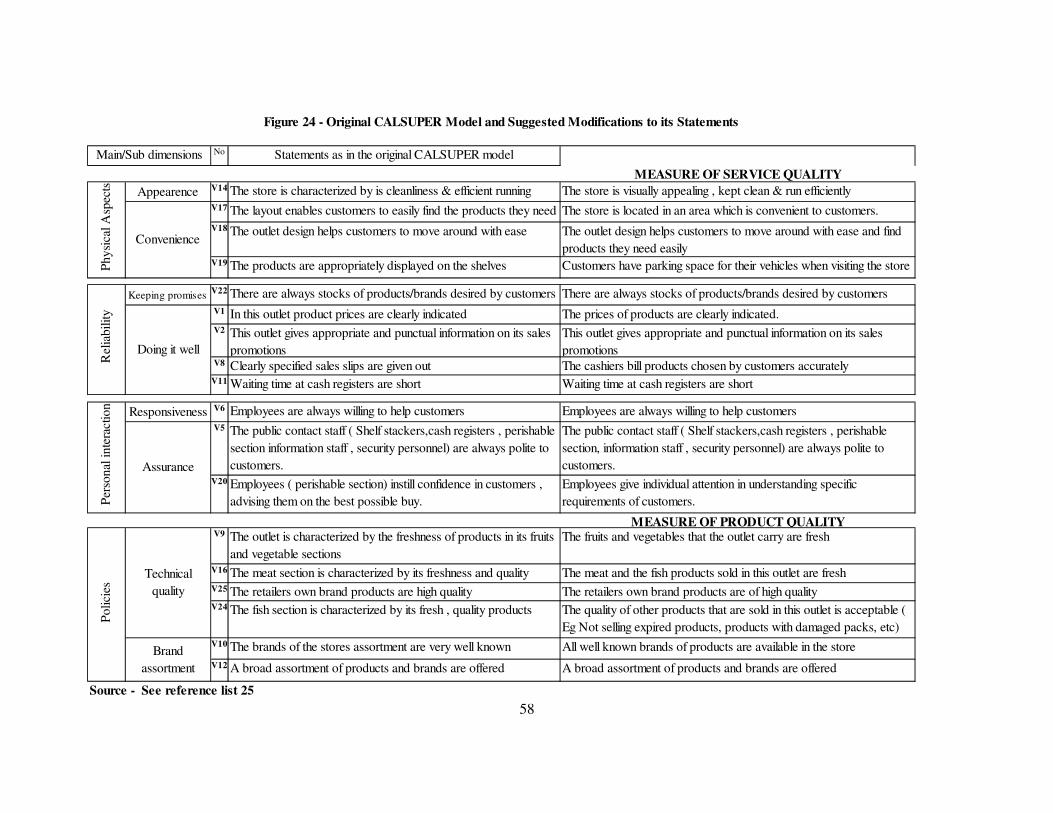

Figure 24 Original CALSUPER model and suggested modifications 57-58

Figure 25 Broad organizational structure of RPD 62

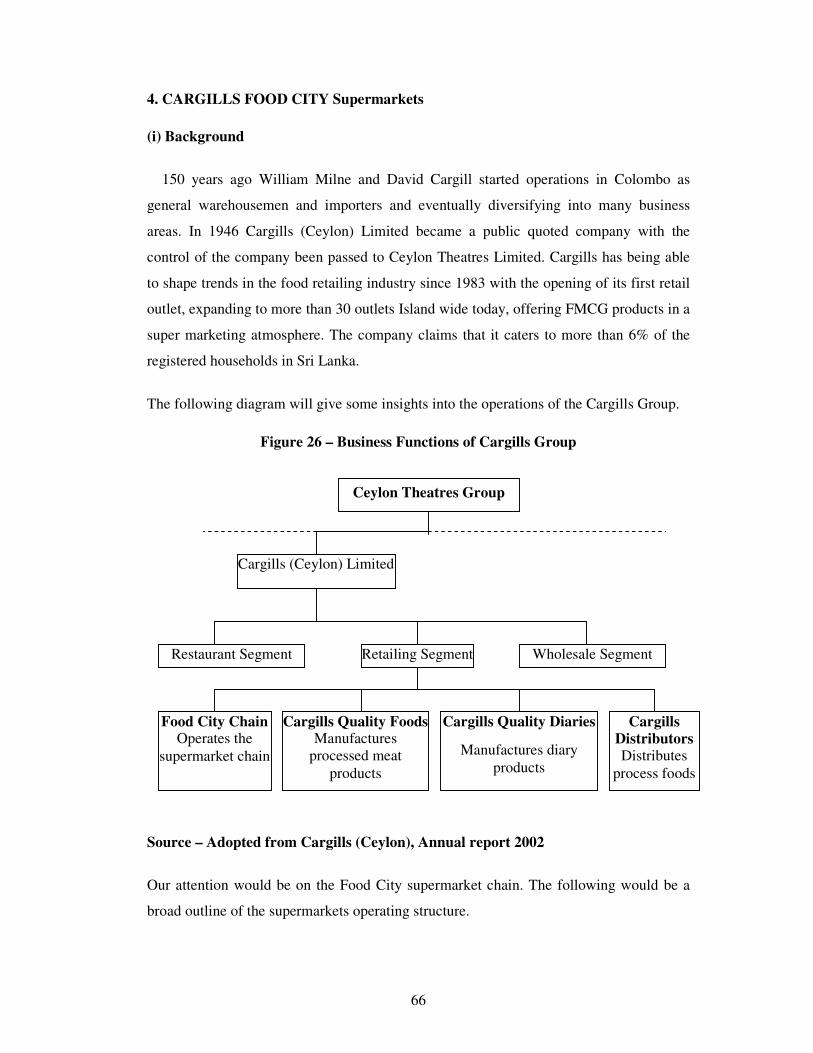

Figure 26 Business functions of Cargills group 66

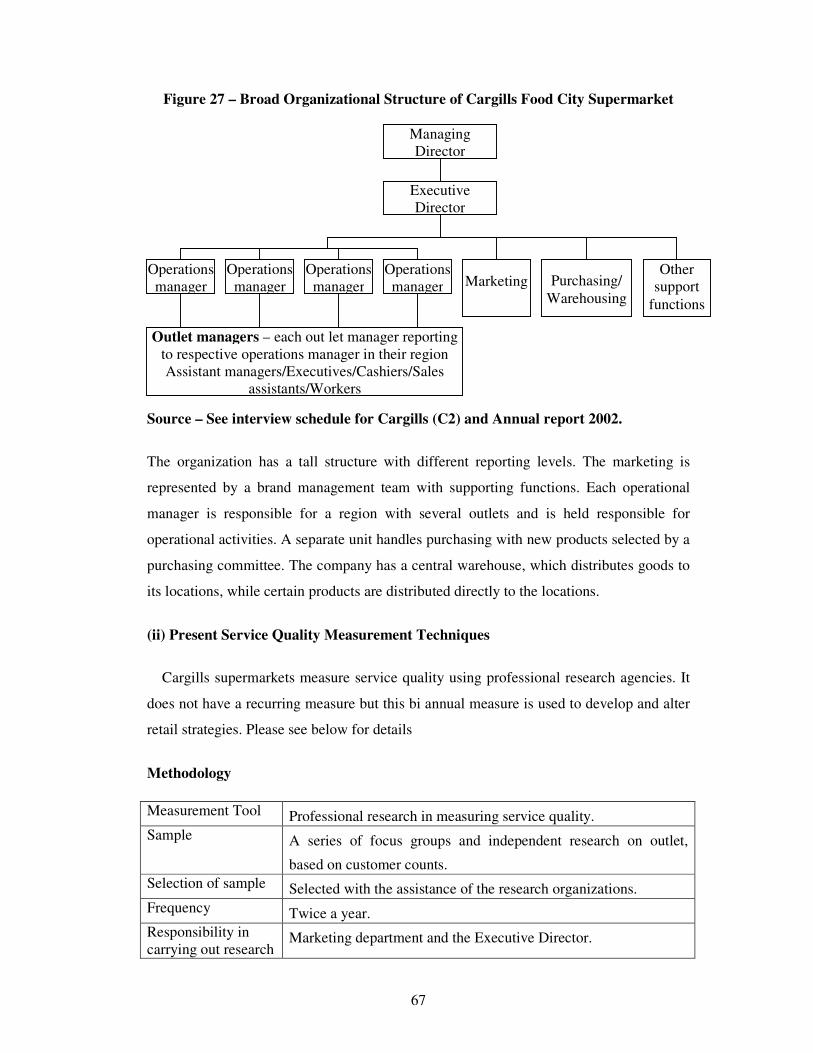

Figure 27 Organizational structure of Cargills Food City supermarket 67

Figure 28 Broad organizational structure of Jaykay Marketing Services 70

Figure 29 Organizational structure of SATHOSA 74

LIST OF ILLUSTRATIONS (continued)

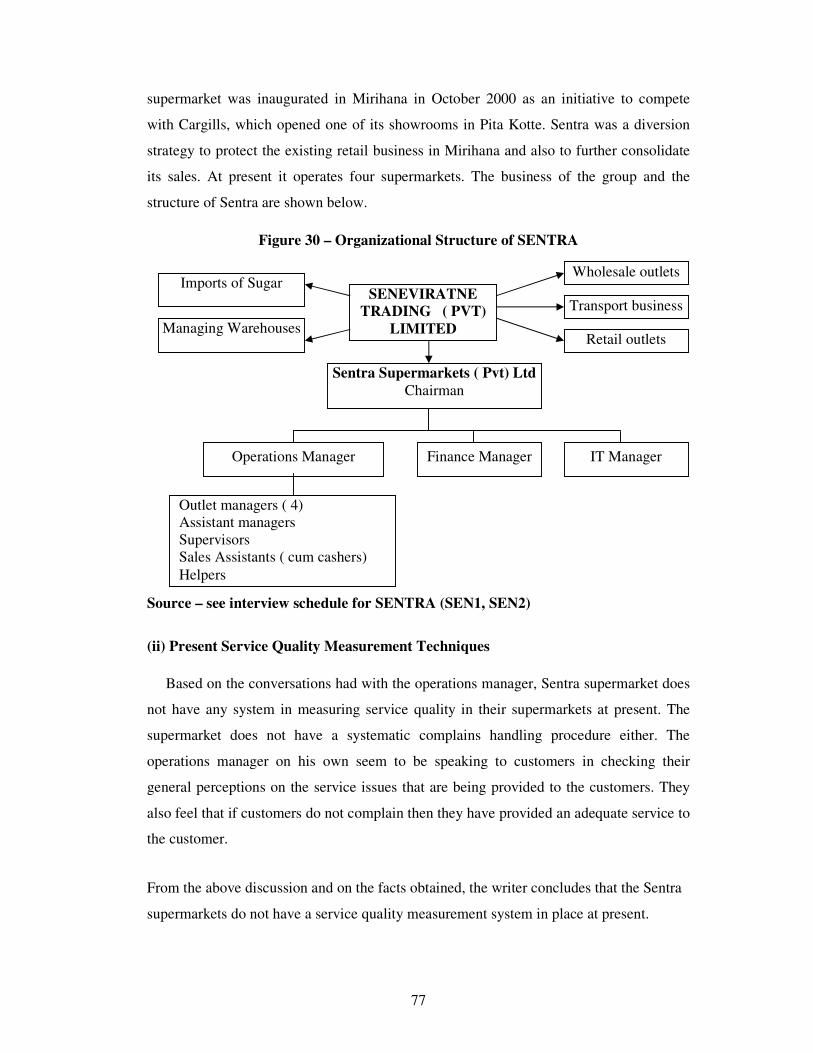

Figure 30 Organizational structure of SENTRA 77

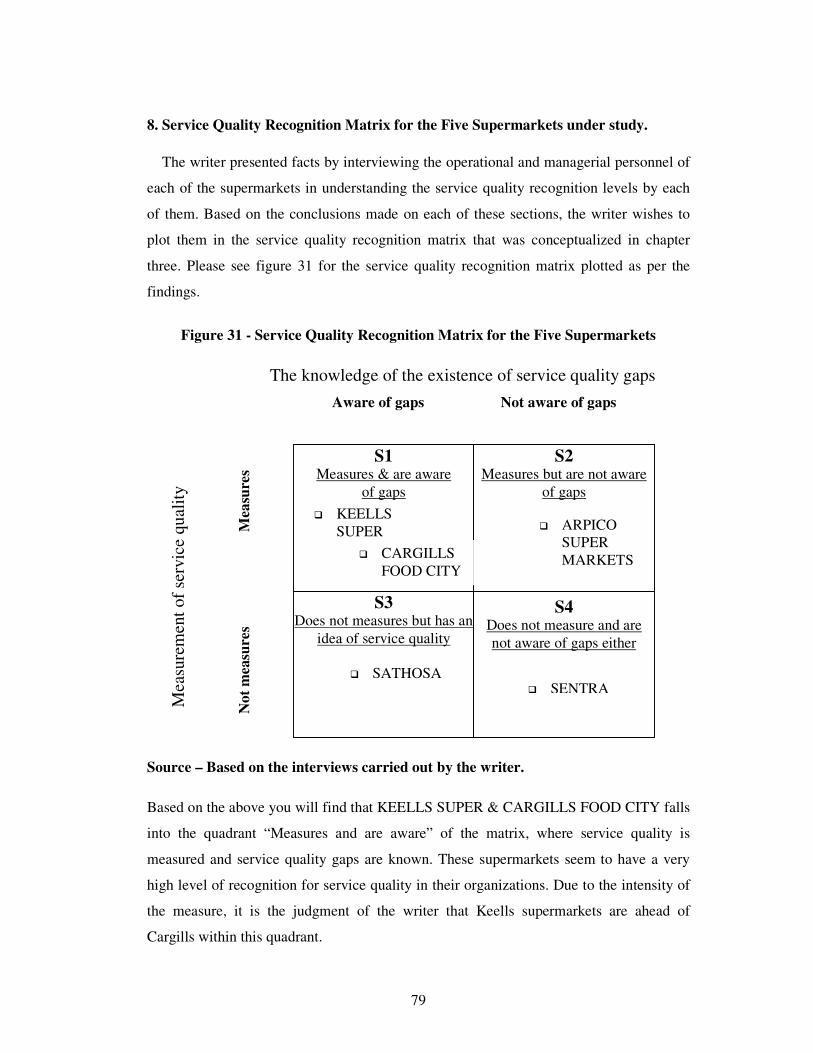

Figure 31 Service quality recognition matrix of the five supermarkets 79

Figure 32 Polarization of supermarket segments 84

Figure 33 Overall conclusion of the research 99

Figure 34 Four step process model 102

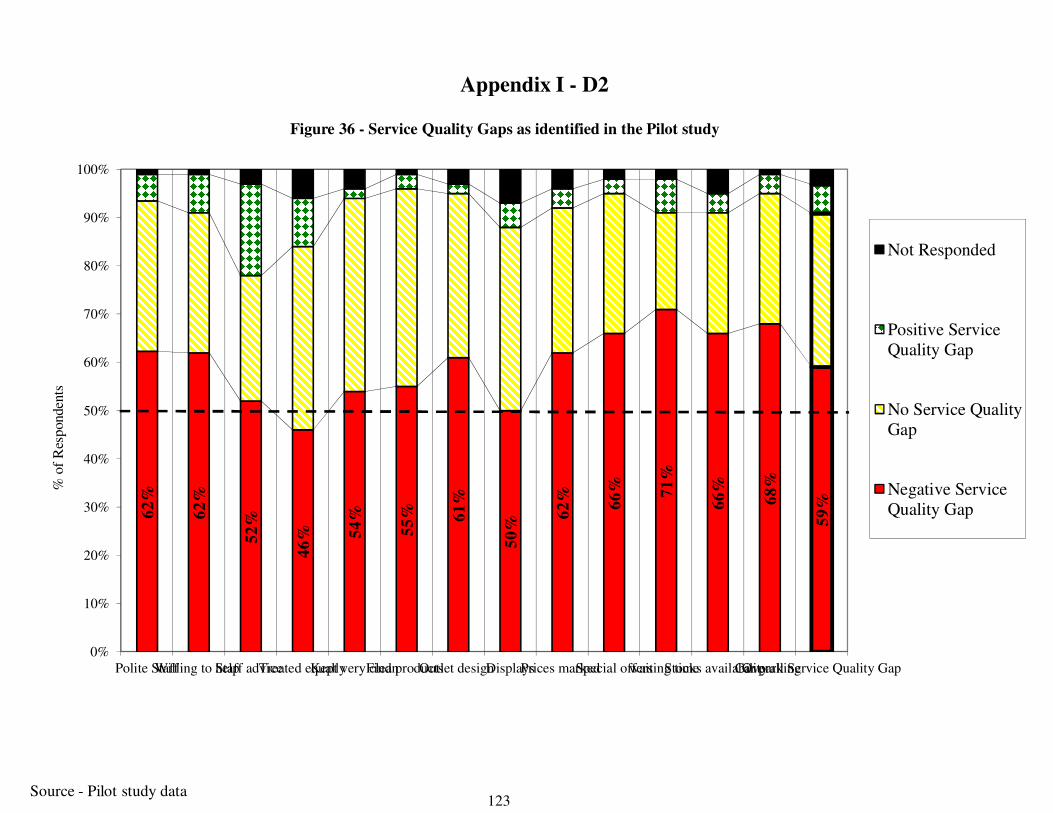

Figure 35 Service quality gaps identified in the pilot study 122

Figure 36 Service quality gaps identified in the pilot study-graph 123

Figure 37 Classification of the retail industry in Sri Lanka 129

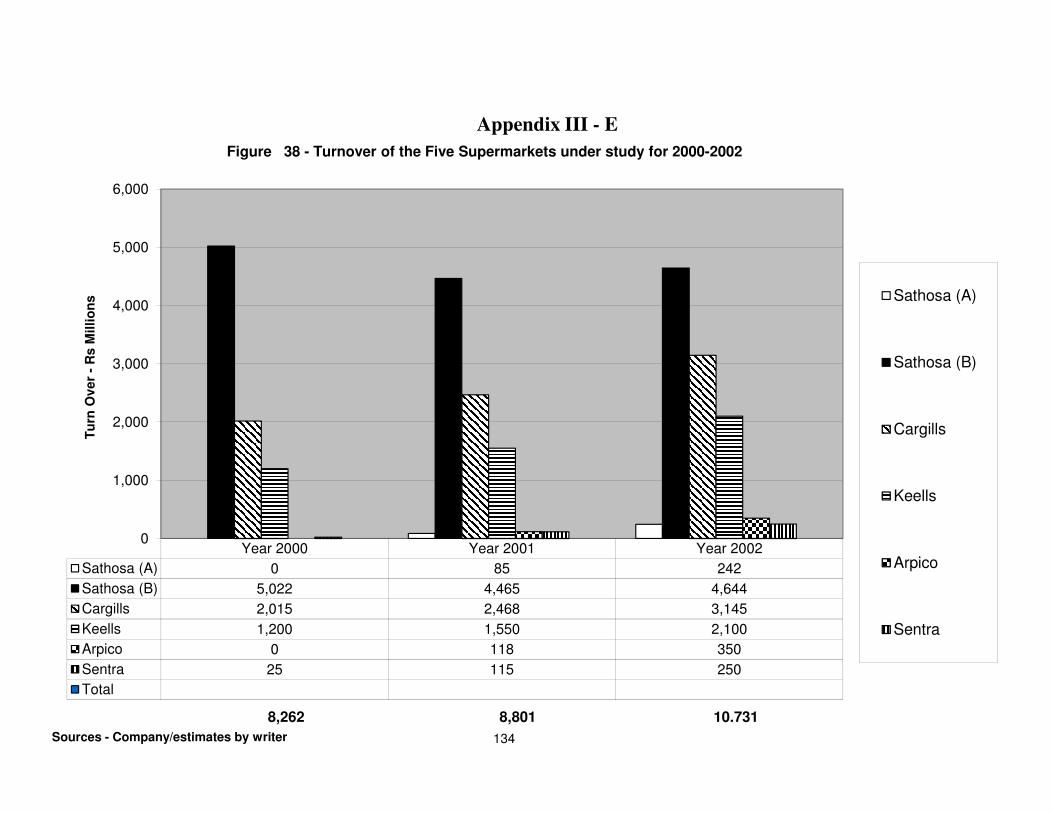

Figure 38 Turnover of the five supermarkets 134

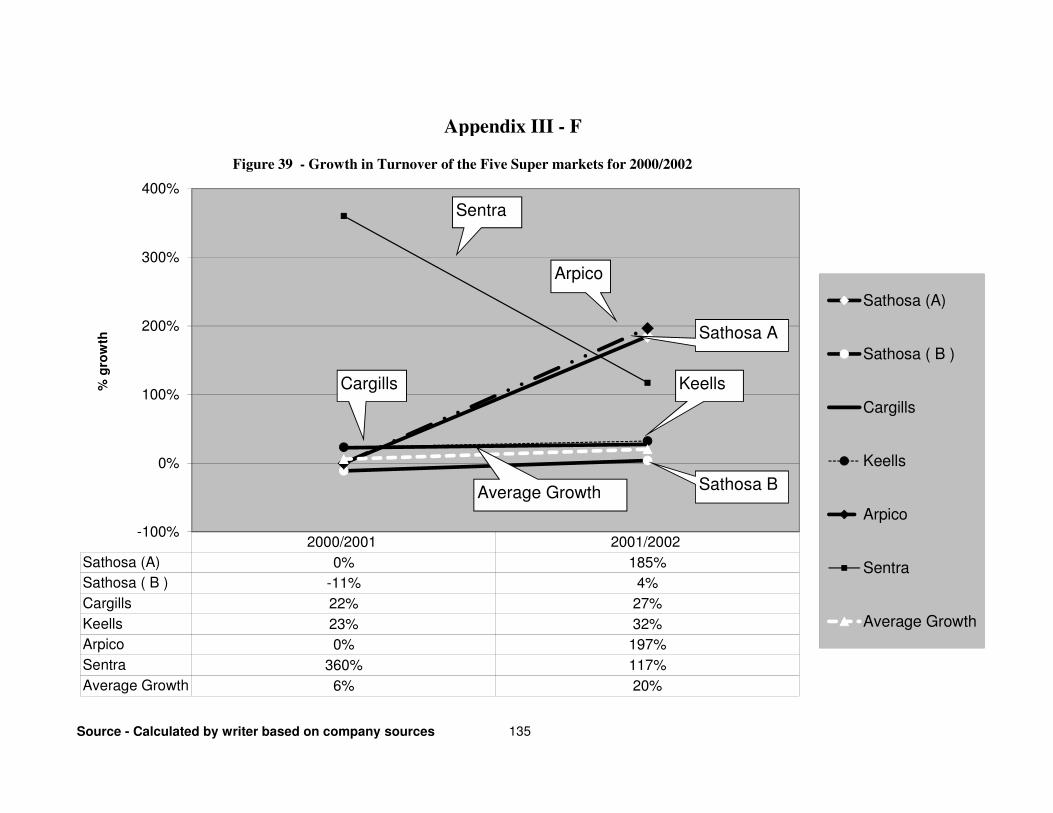

Figure 39 Growth in turnover of five the supermarkets – 2000/2002 135

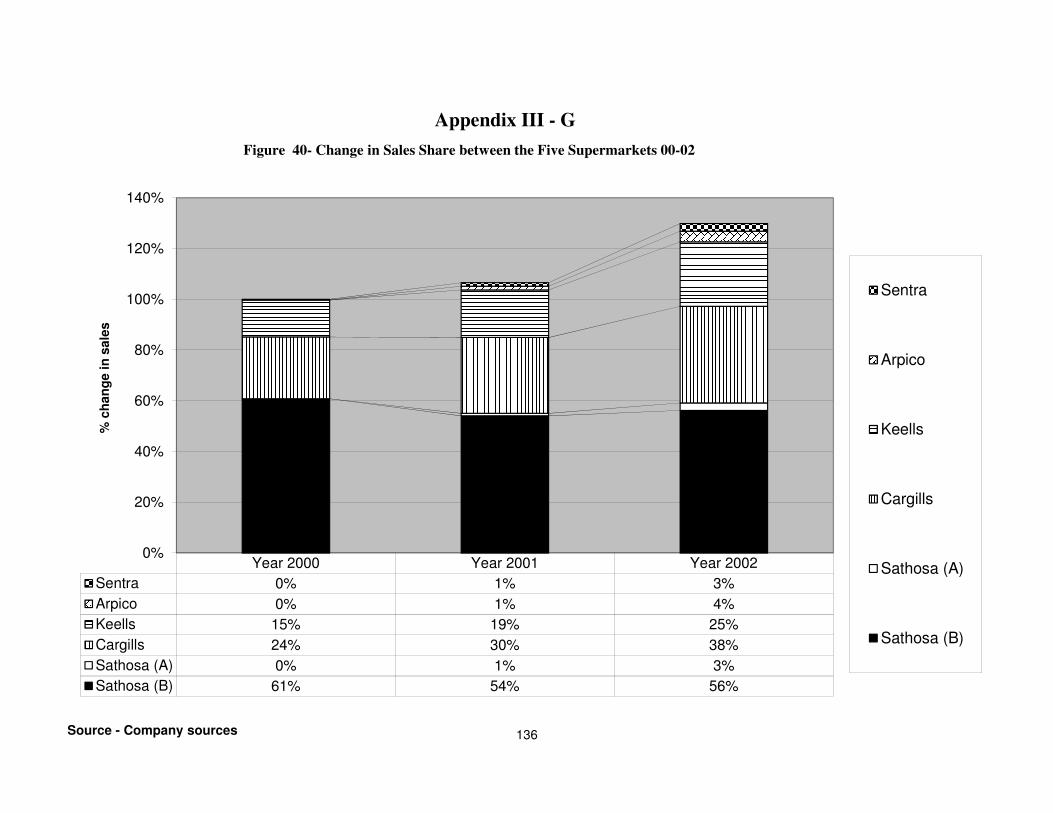

Figure 40 Change in sales share between five supermarkets 136

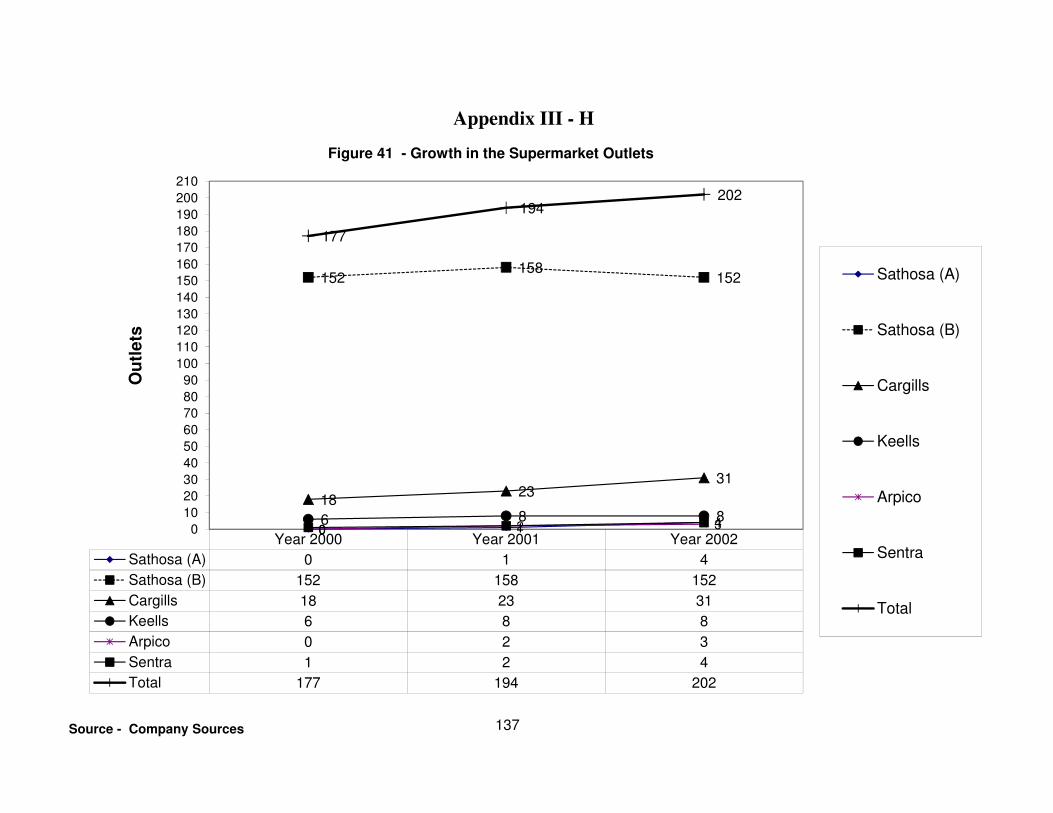

Figure 41 Growth in supermarket outlets 137

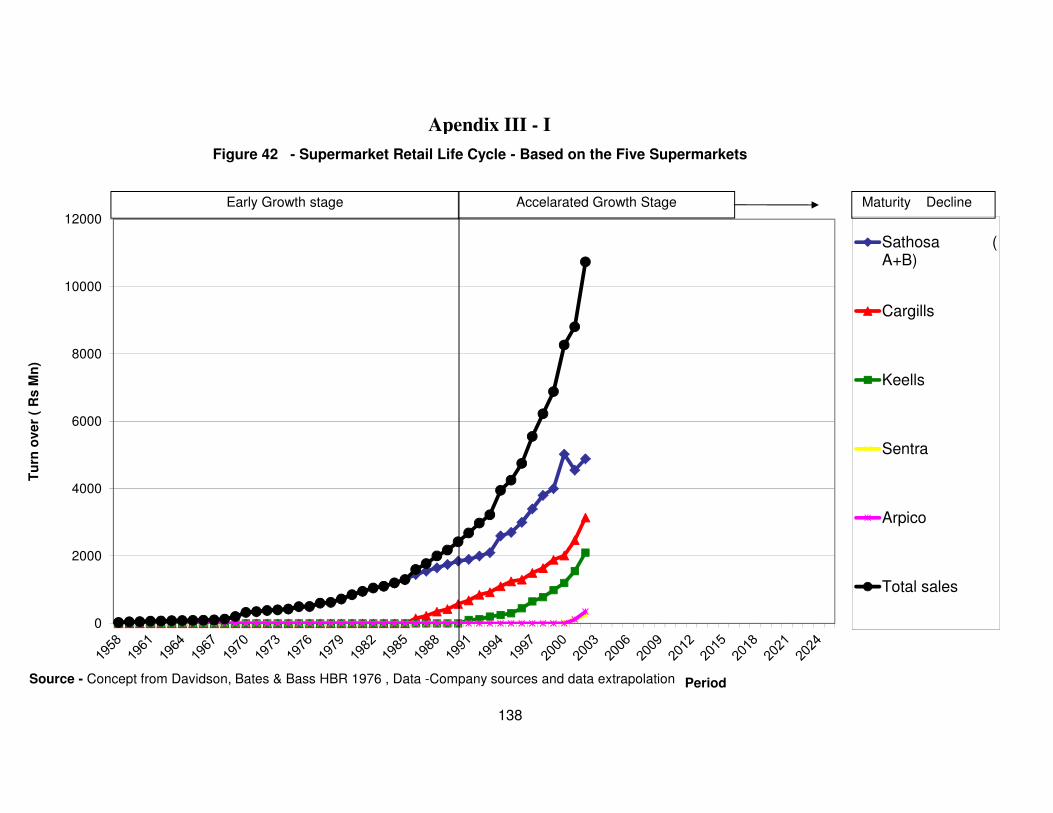

Figure 42 Super market retail life cycle 138

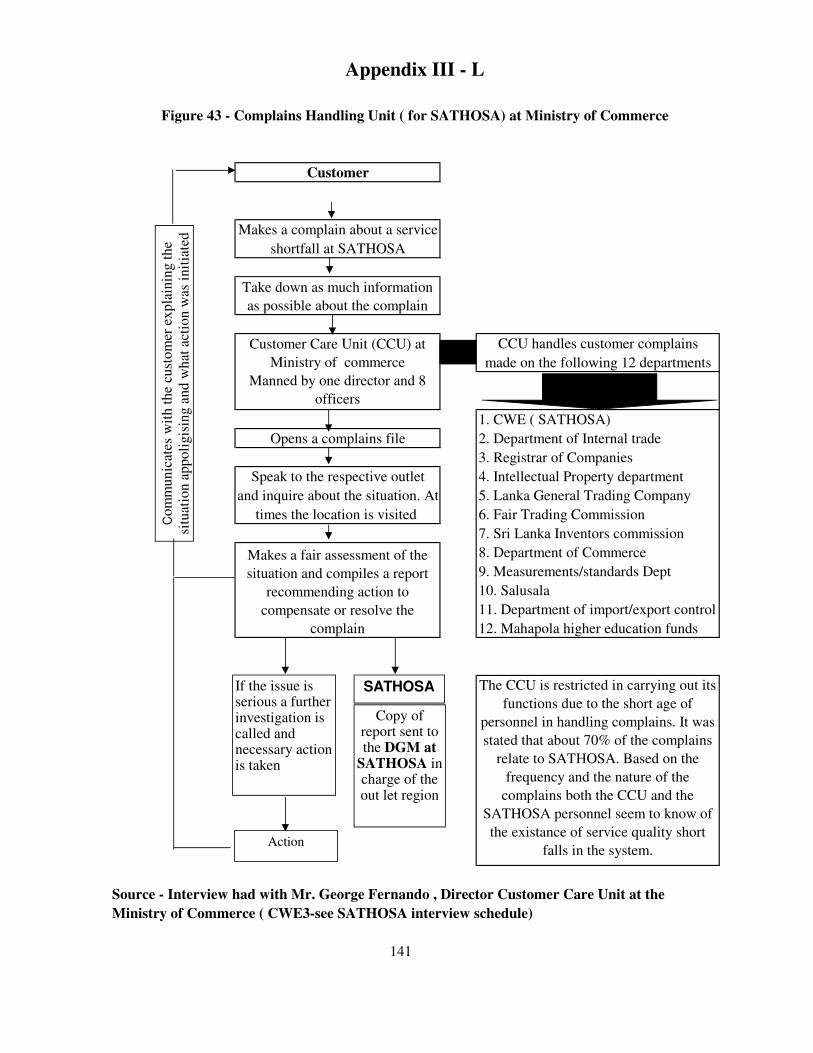

Figure 43 Complains handling procedure - SATHOSA 141

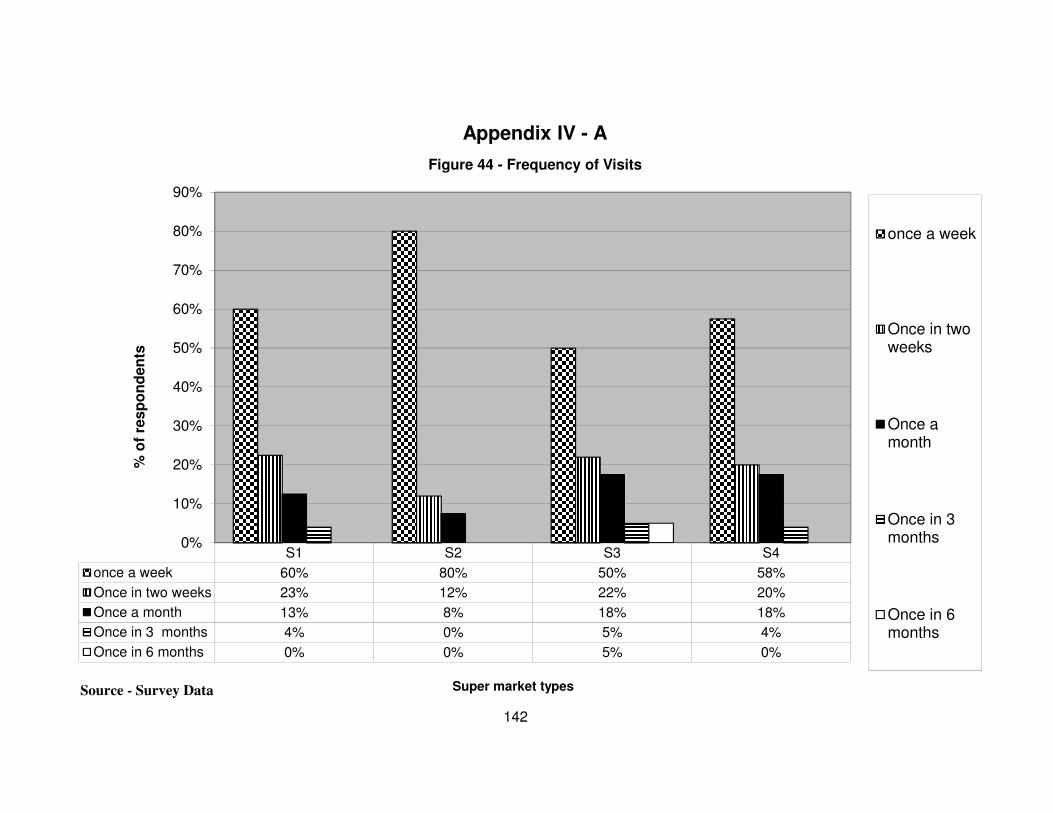

Figure 44 Frequency of visits 142

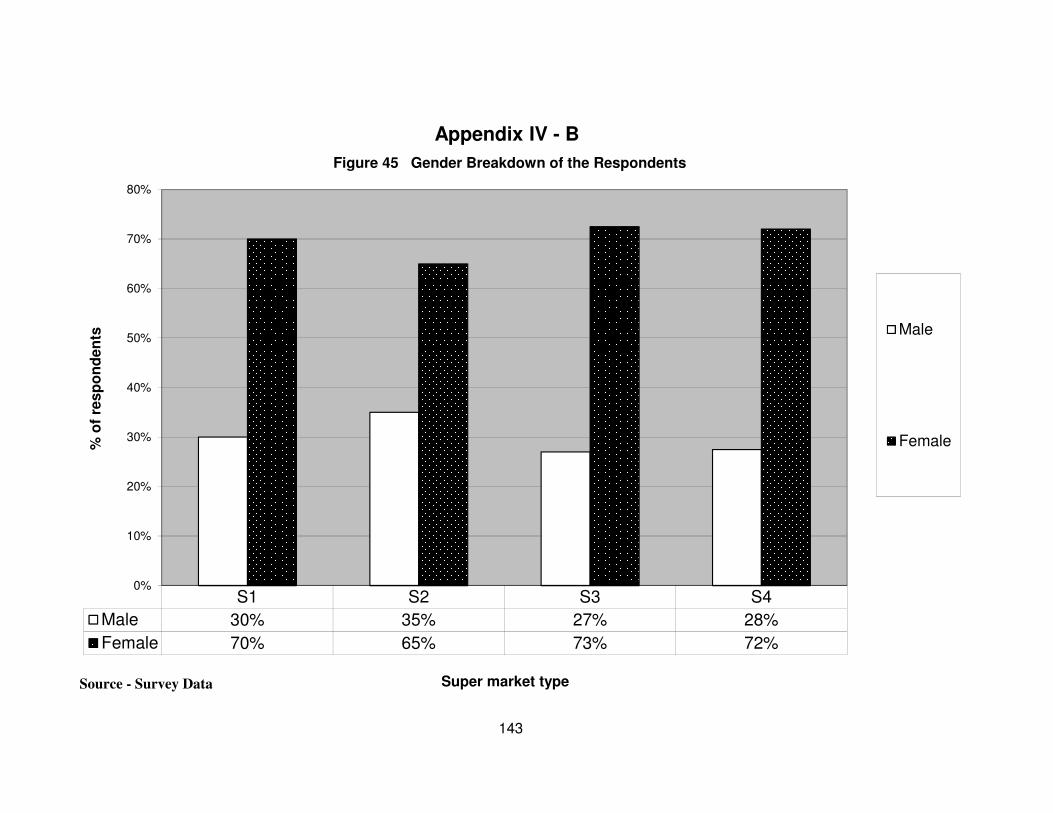

Figure 45 Gender break down of the respondents 143

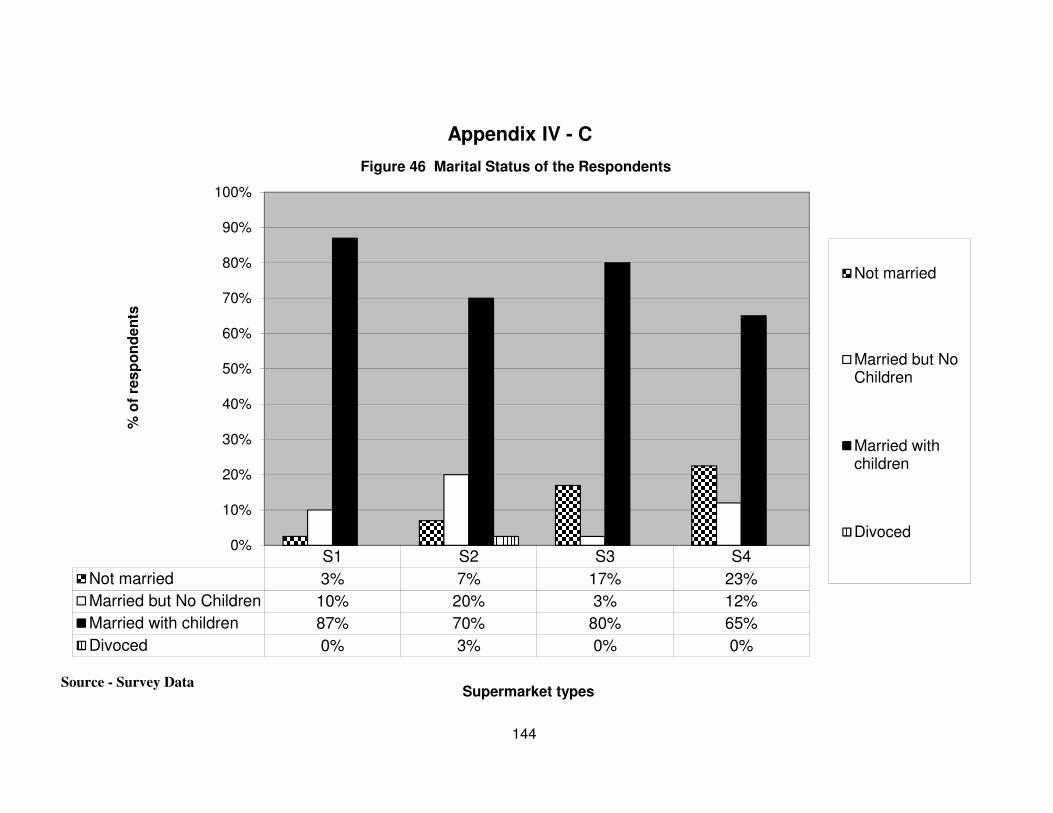

Figure 46 Marital status of respondents 144

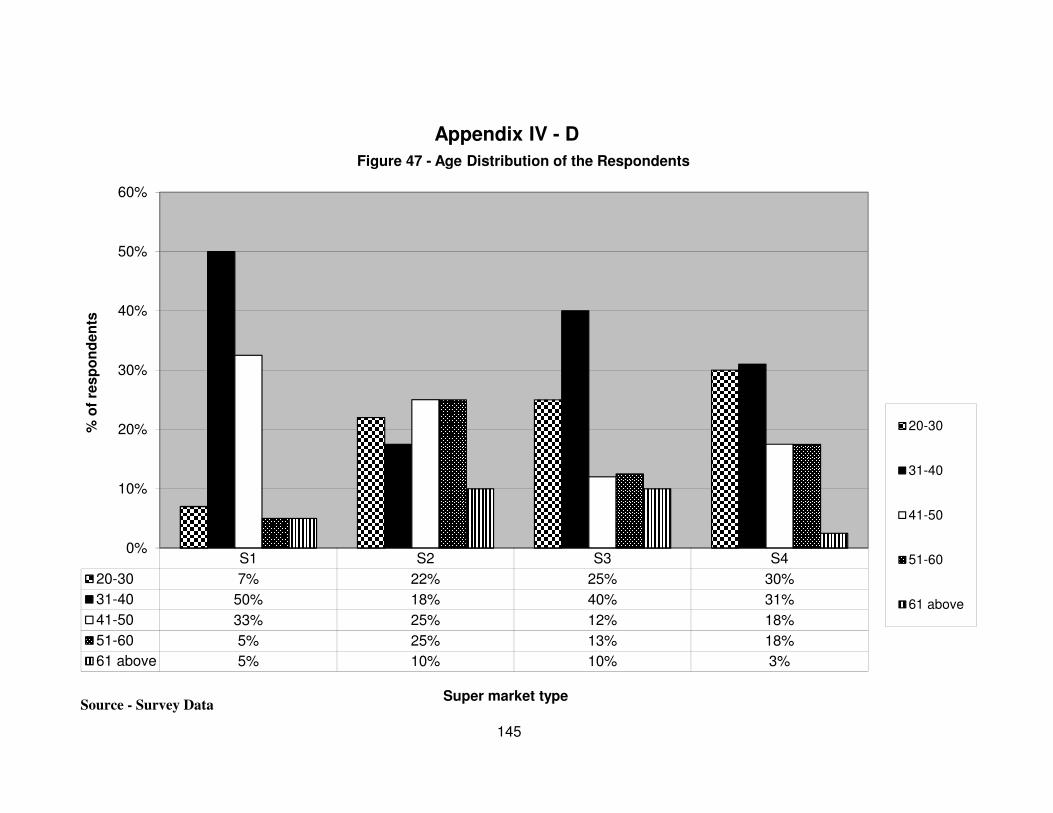

Figure 47 Age distribution of respondents 145

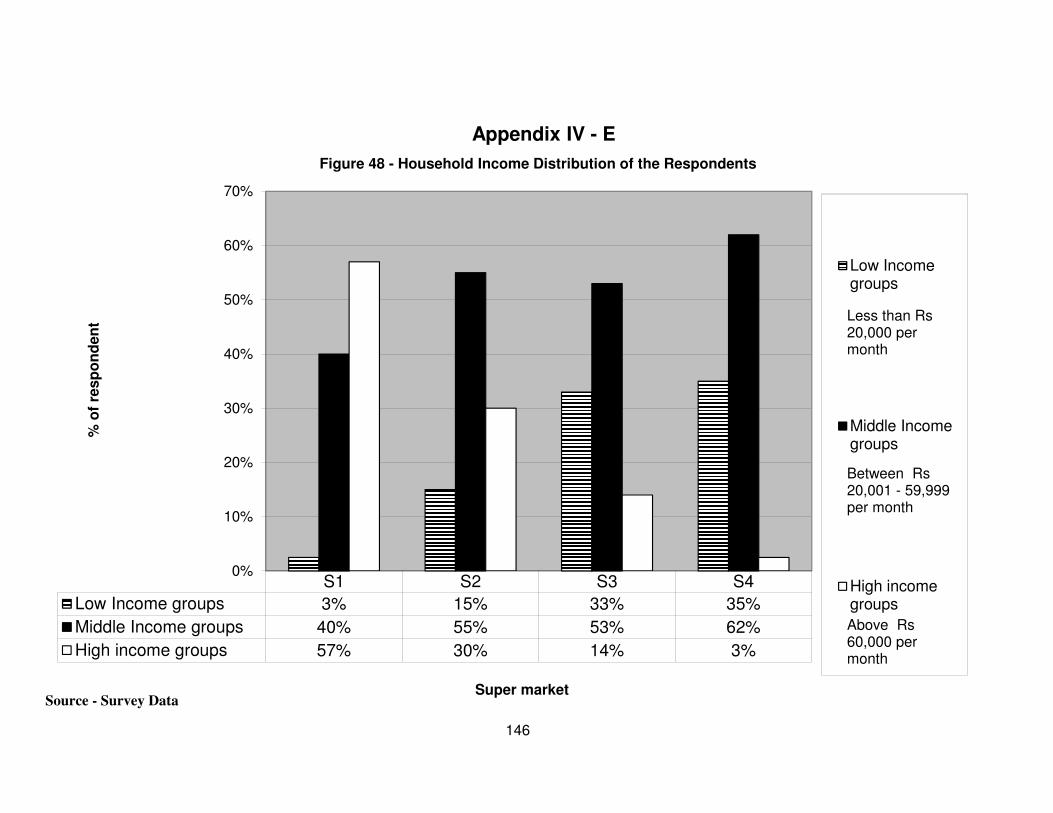

Figure 48 Household income distribution of respondents 146

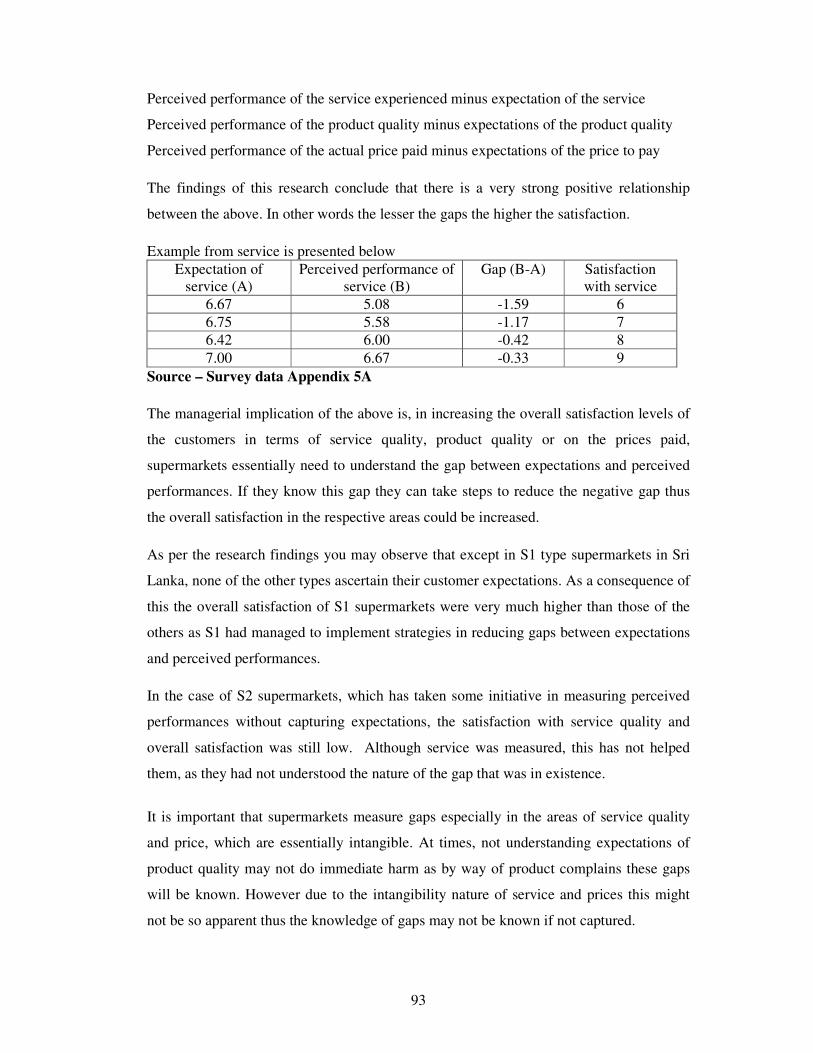

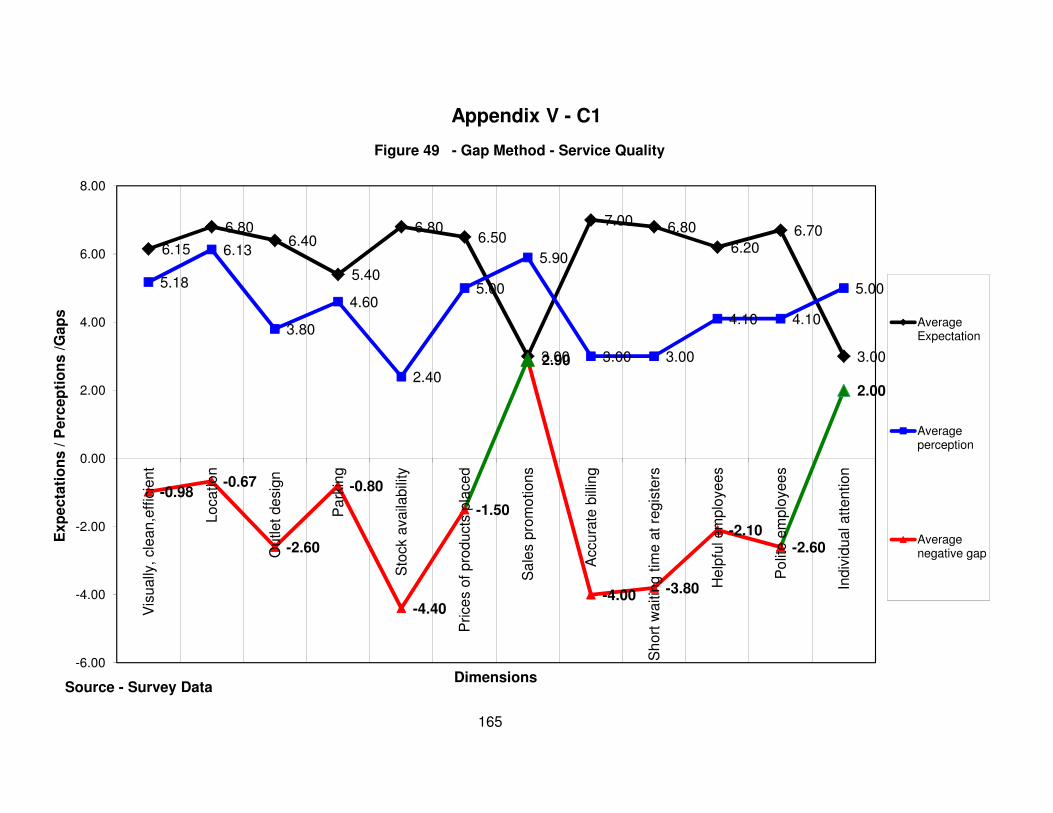

Figure 49 Gap method – service quality 165

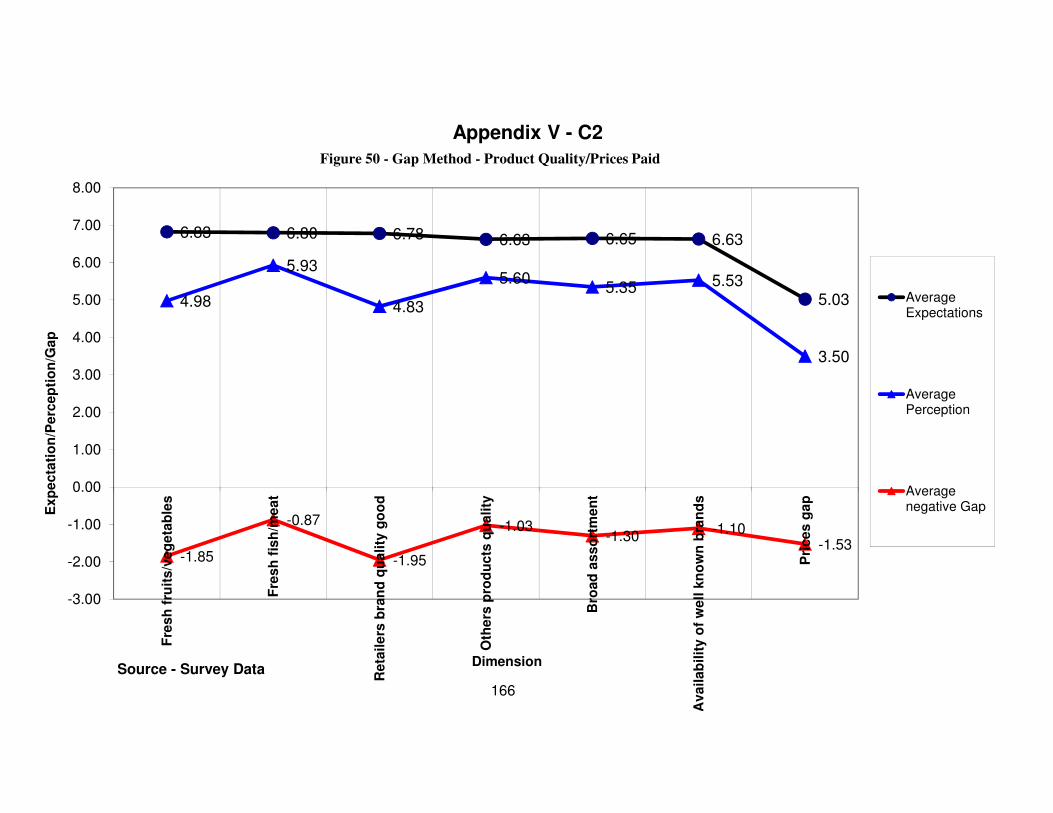

Figure 50 Gap method – product quality/prices paid 166

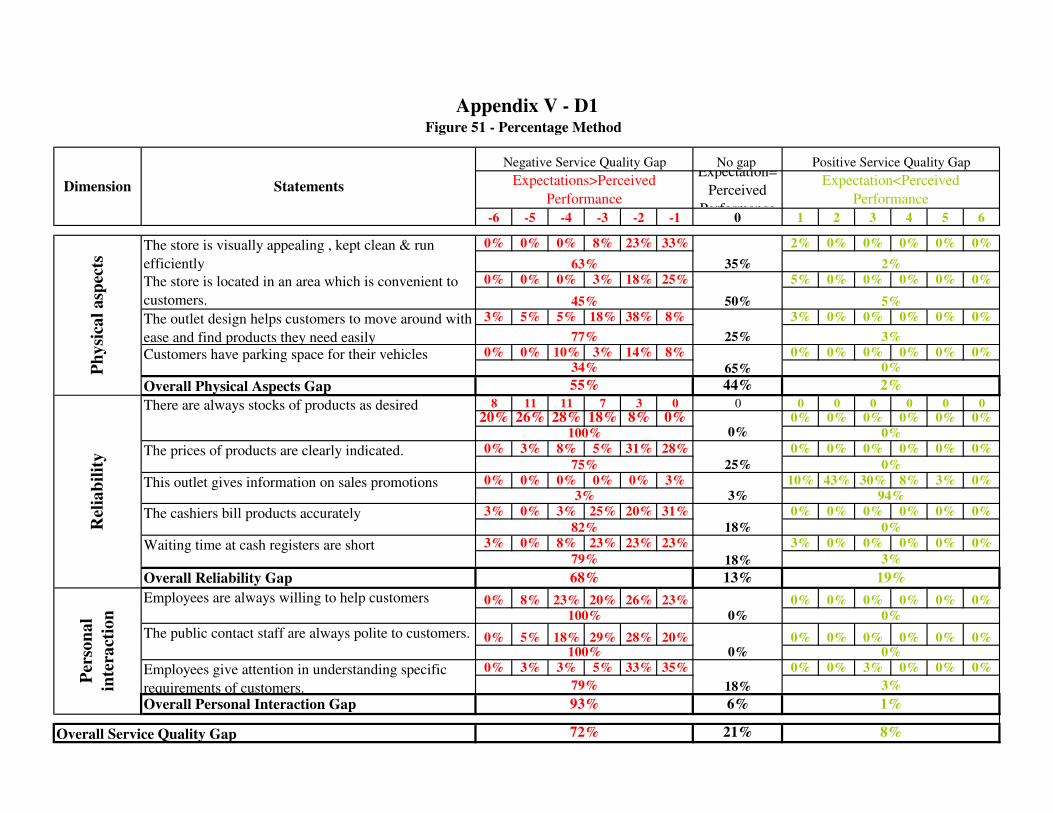

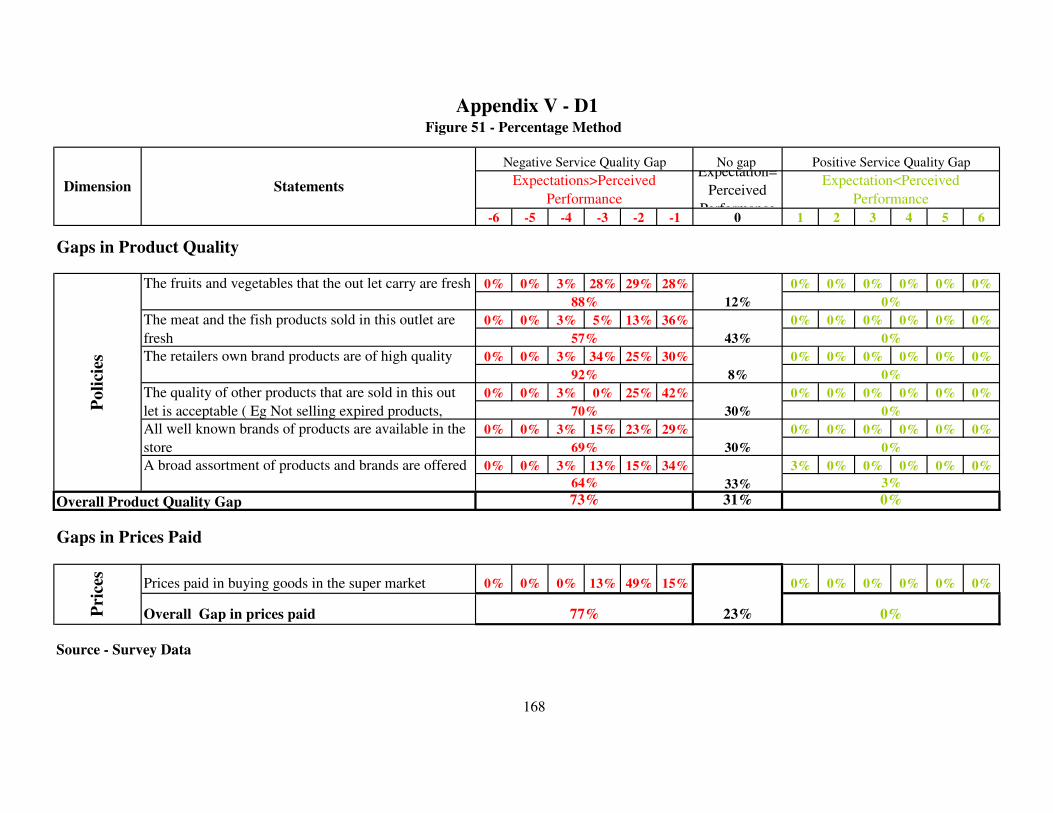

Figure 51 Percentage method 167

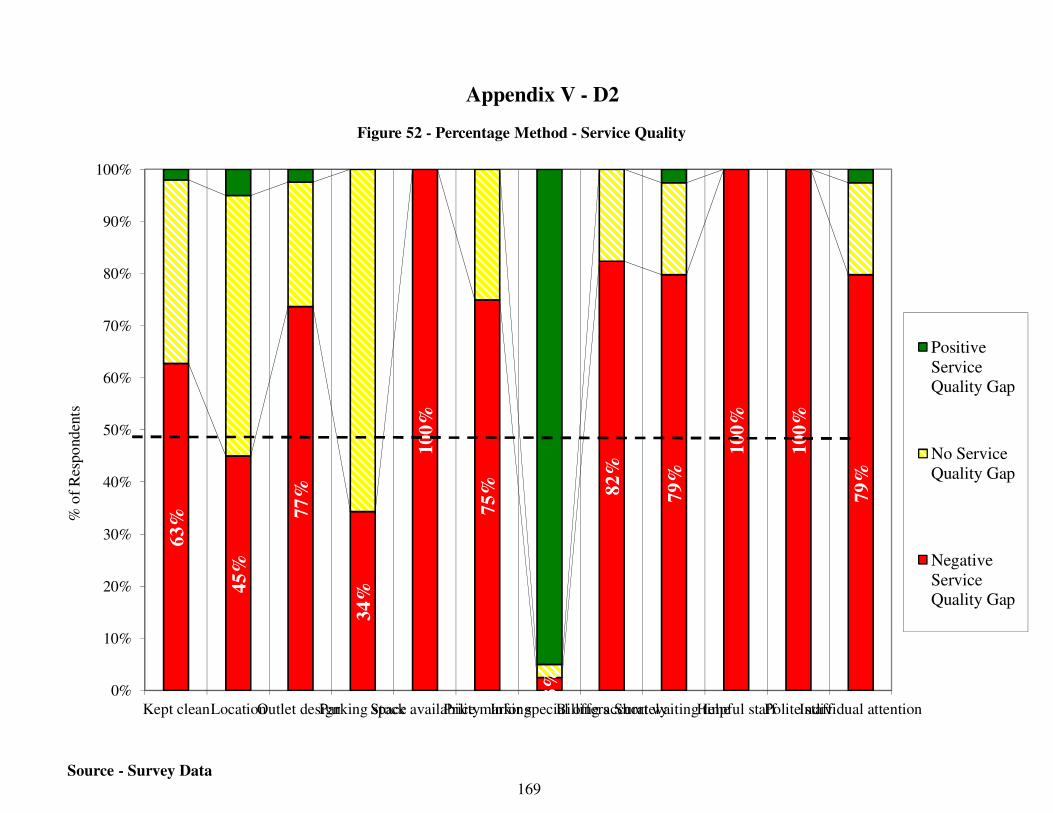

Figure 52 Percentage method – Service quality – graphical 169

Figure 53 Percentage method – Product quality/prices - graphical 170

Figure 54 Importance perception matrix – service statements 171

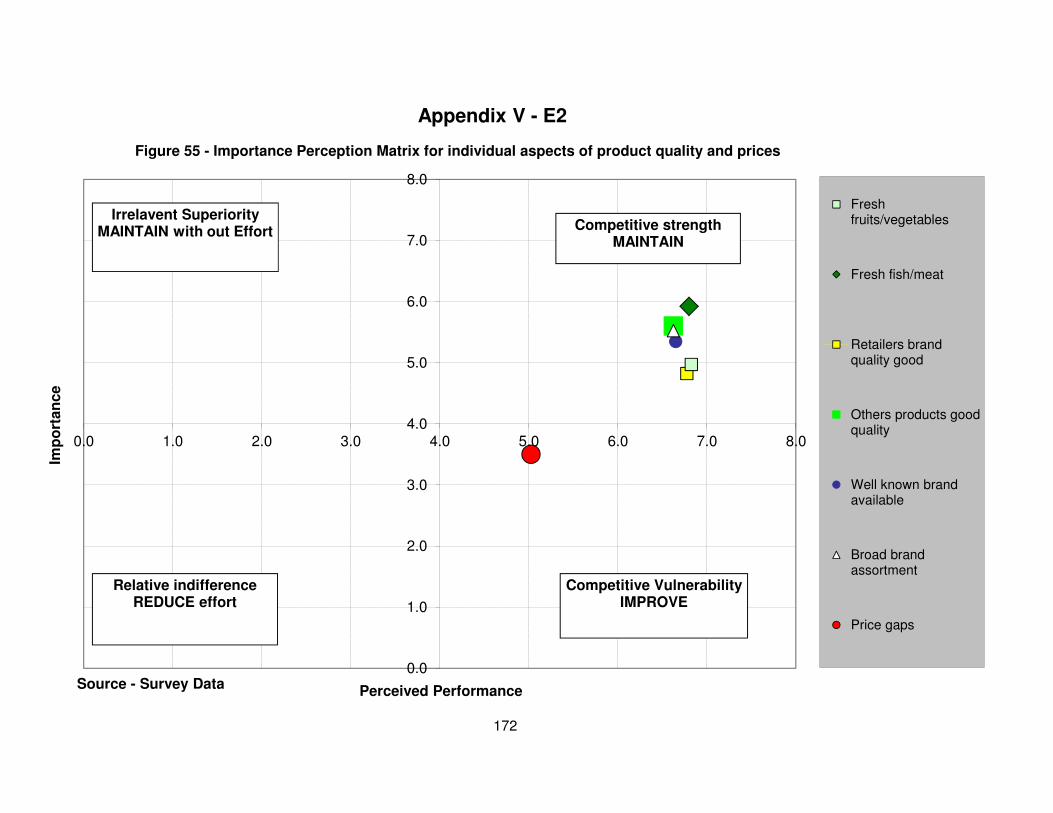

Figure 55 Importance perception matrix – product statements 172

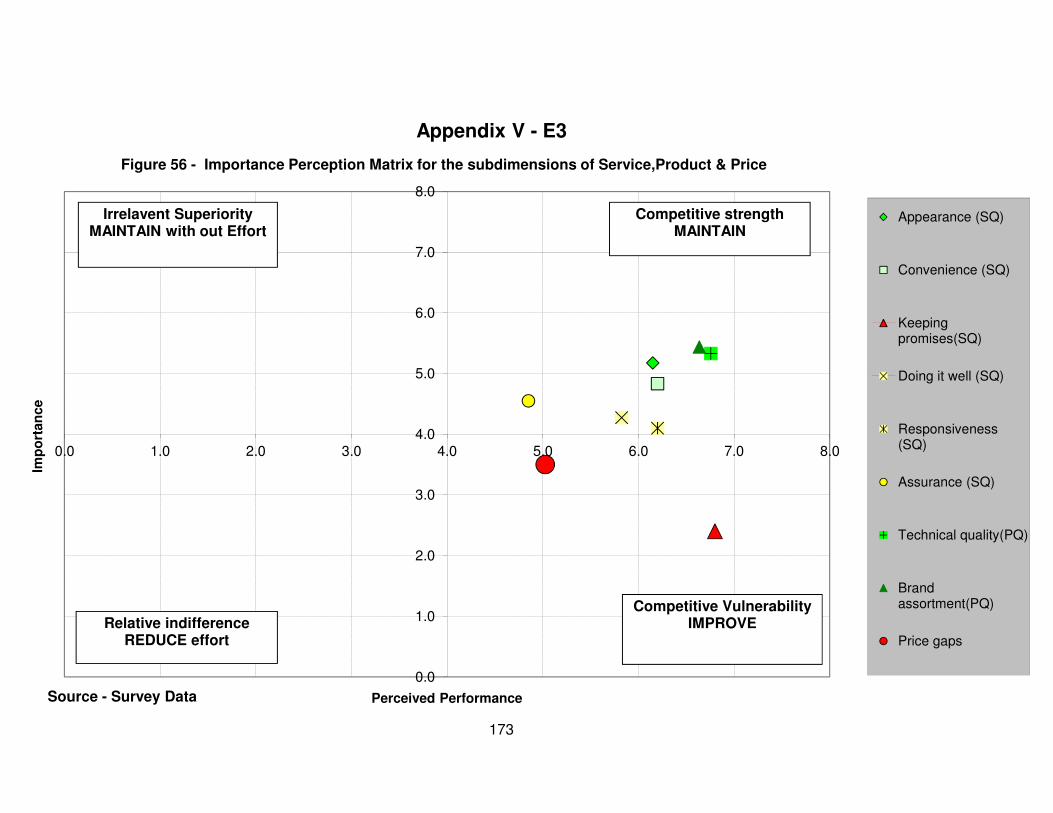

Figure 56 Importance perception matrix – sub dimensions 173

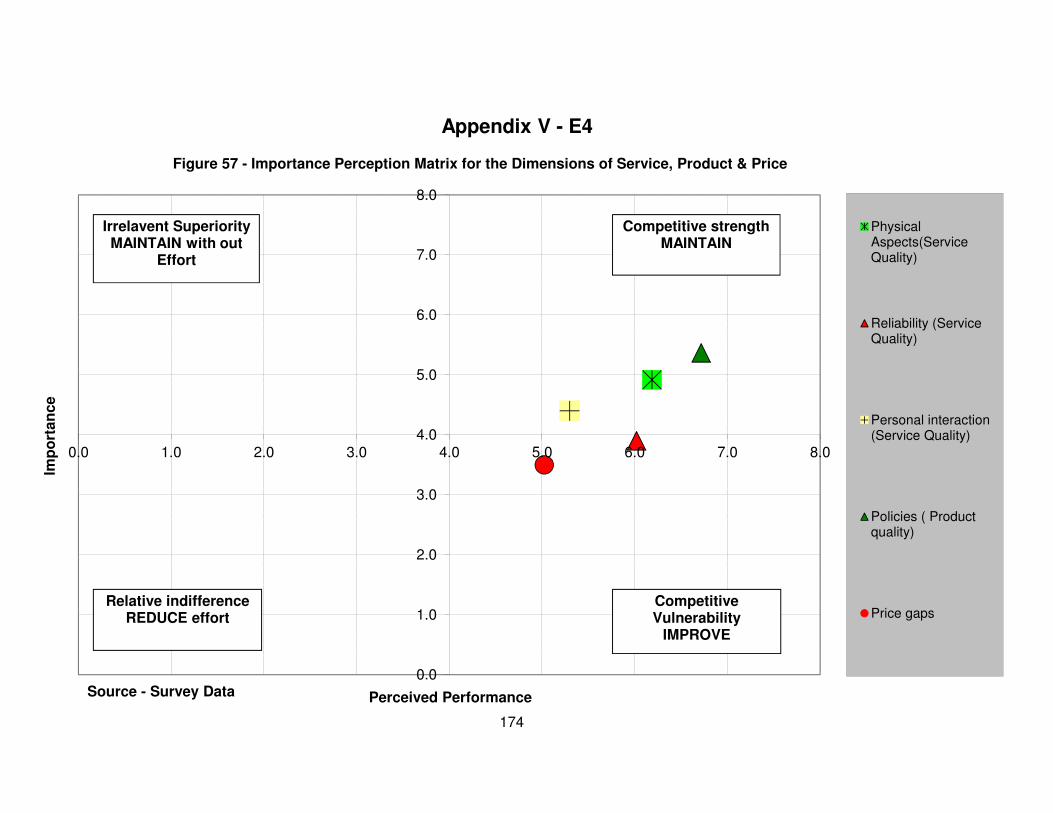

Figure 57 Importance perception matrix – dimensions 174

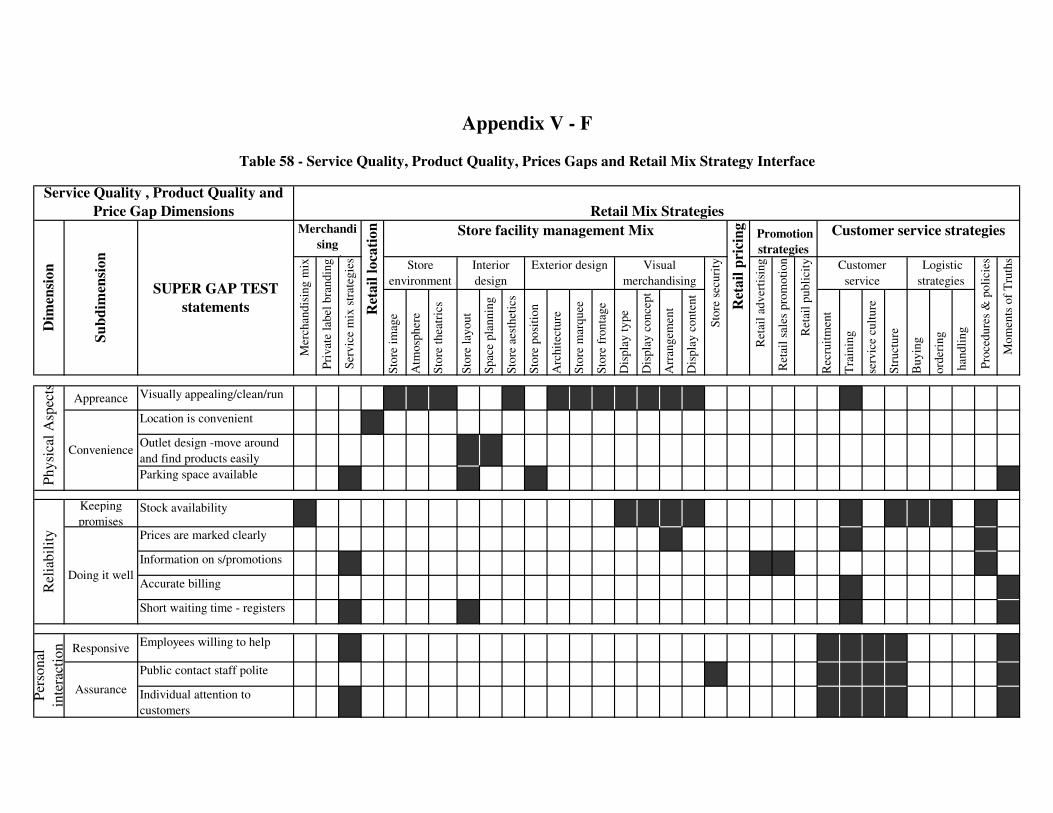

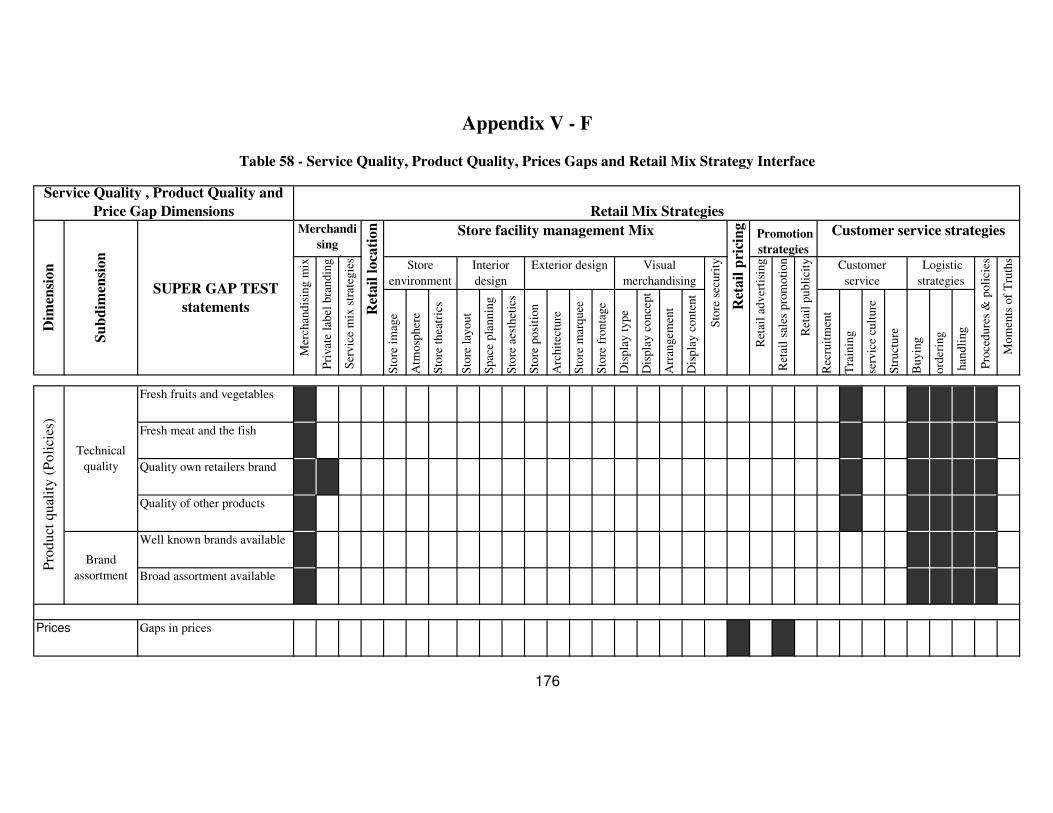

Figure 58 Gaps & strategy interface 175

LIST OF TABLES

Table 01 Results of the pilot study 02

Table 02 Elements of the extended marketing mix for services 10

Table 03 Considerations in retail location planning 32

Table 04 Considerations for Store facility management elements 33

Table 05 Retail pricing strategies 34

Table 06 Income distribution of respondents and price expectations 83

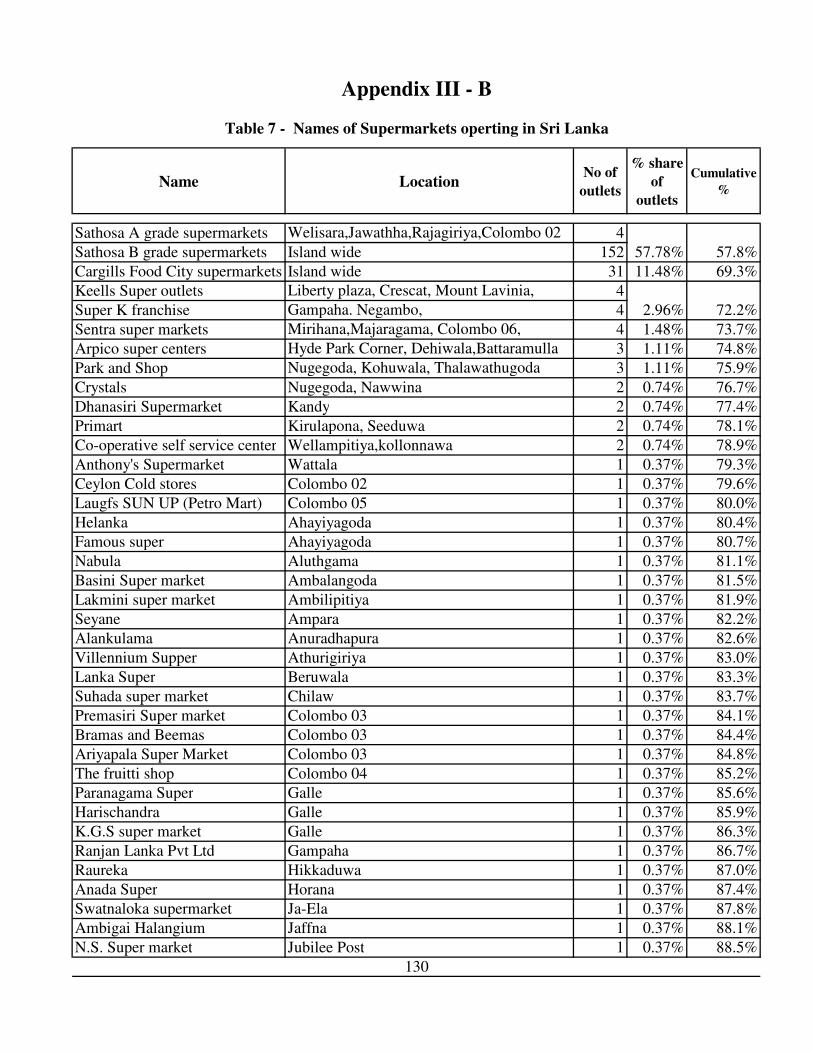

Table 07 Names of supermarkets operating in Sri Lanka 130

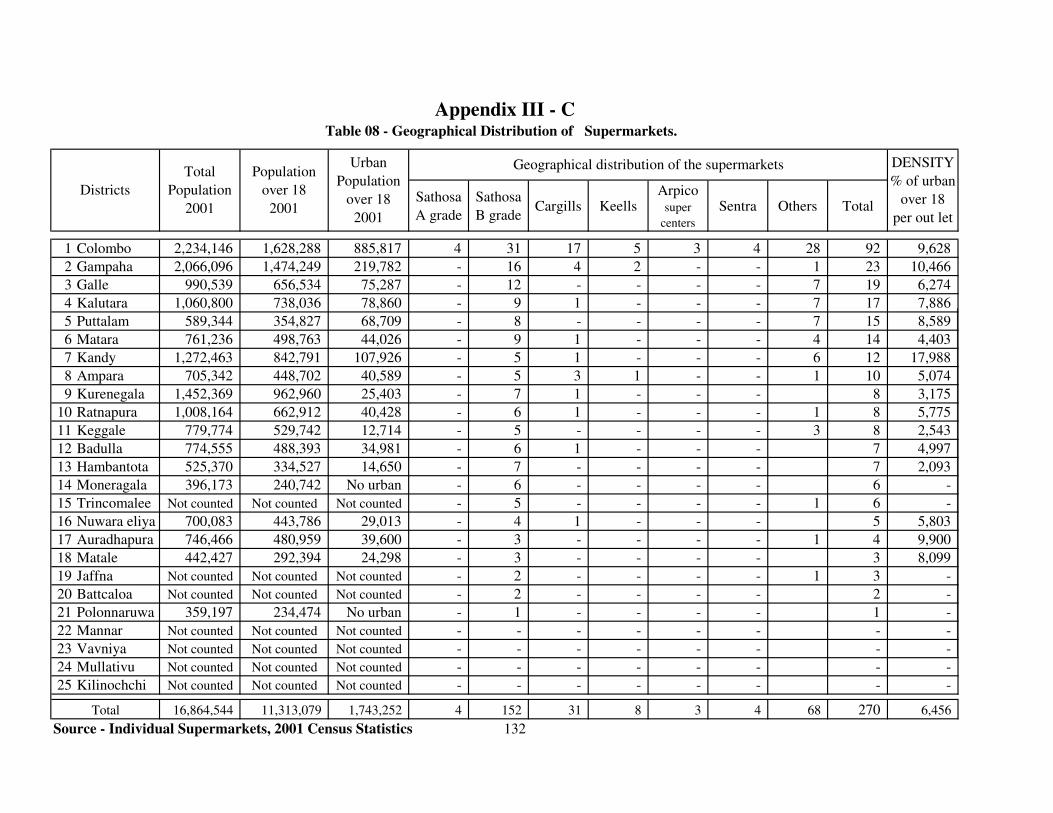

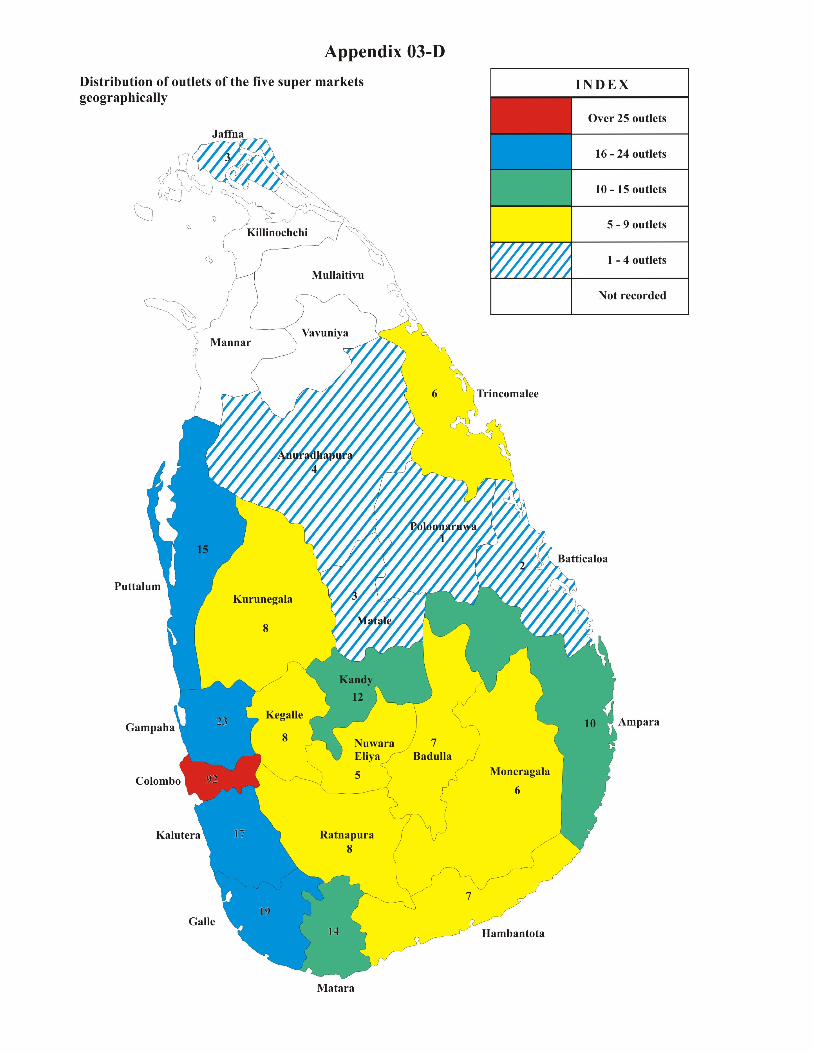

Table 08 Geographical distribution of super markets 132

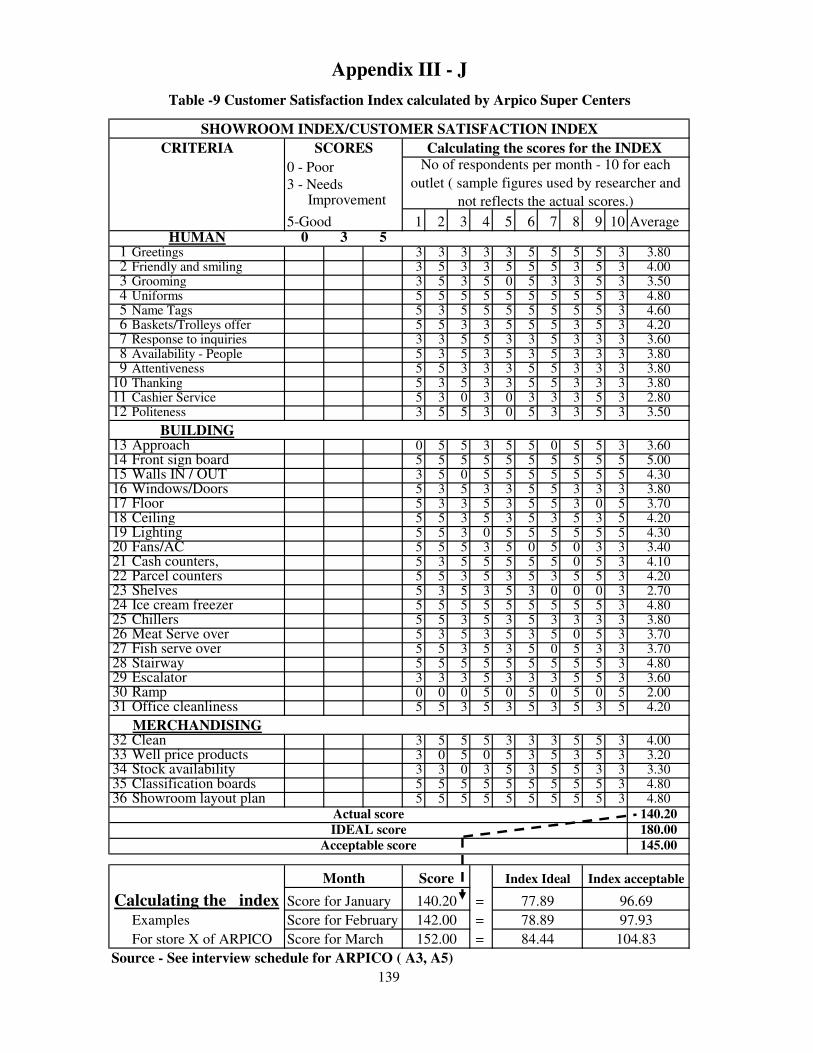

Table 09 Customer satisfaction index – Arpico 139

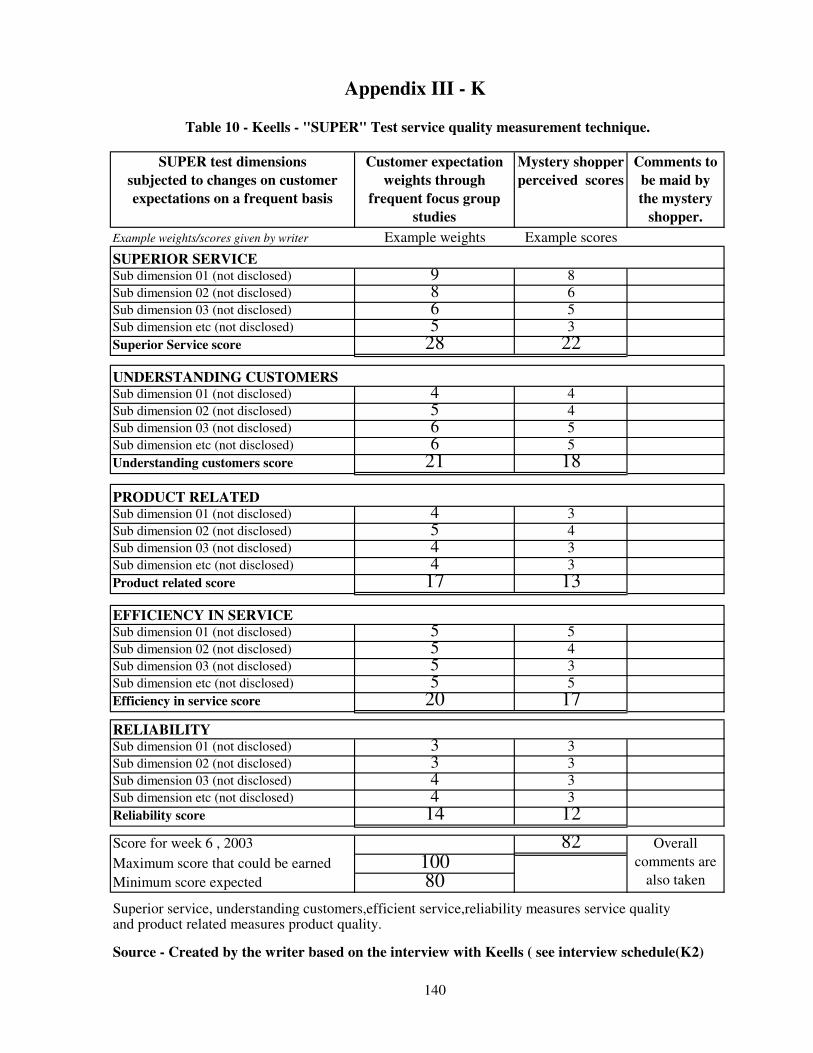

Table 10 SUPER TEST - KEELLS 140

Table 11 Correlation between income level and price expectations 147

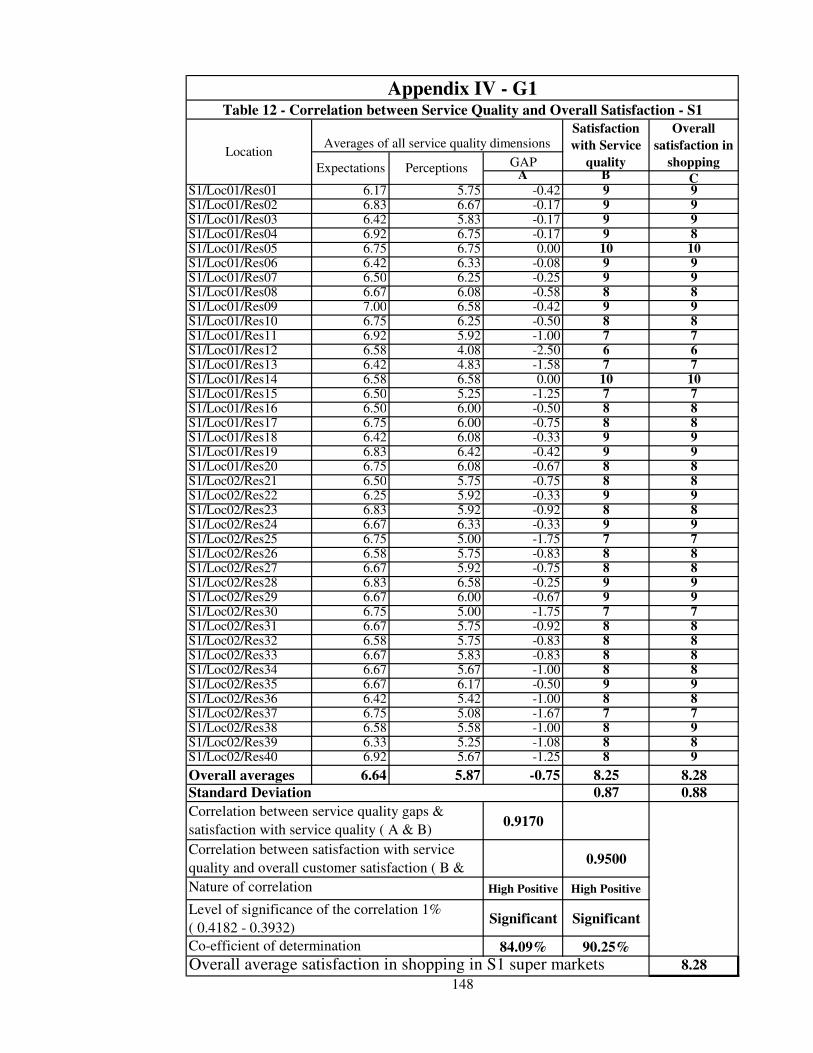

Table 12 Correlation between service quality and overall satisfaction S1 148

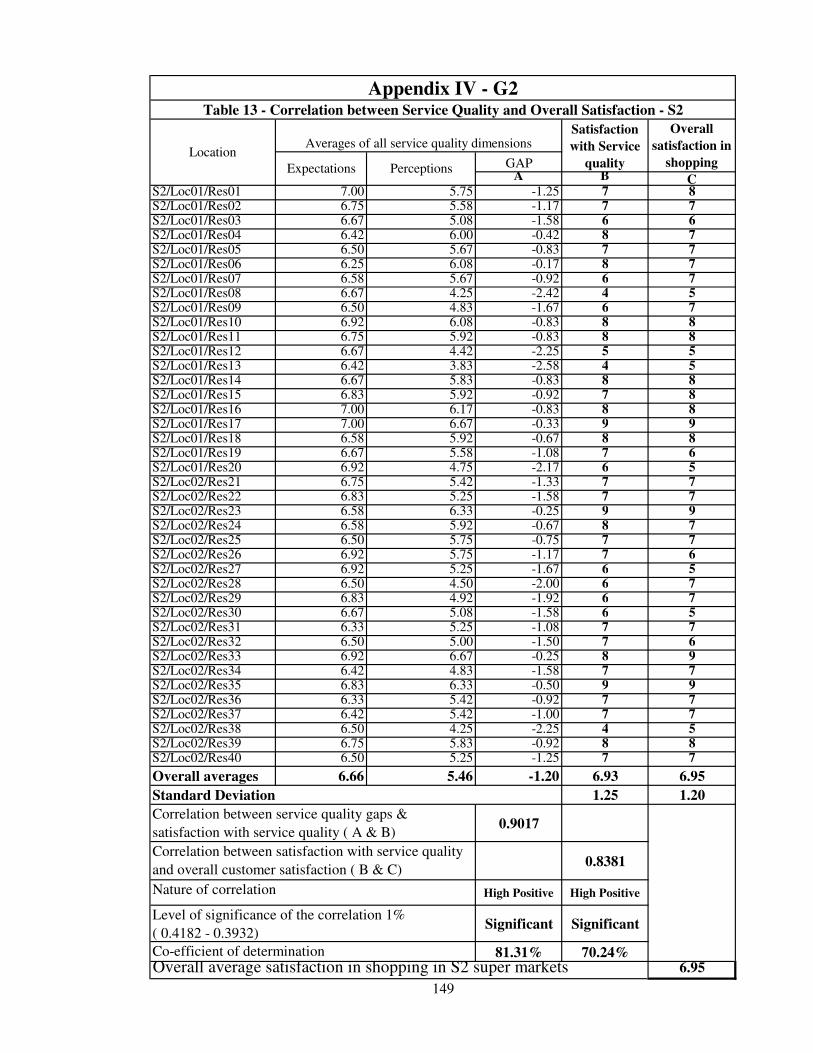

Table 13 Correlation between service quality and overall satisfaction S2 149

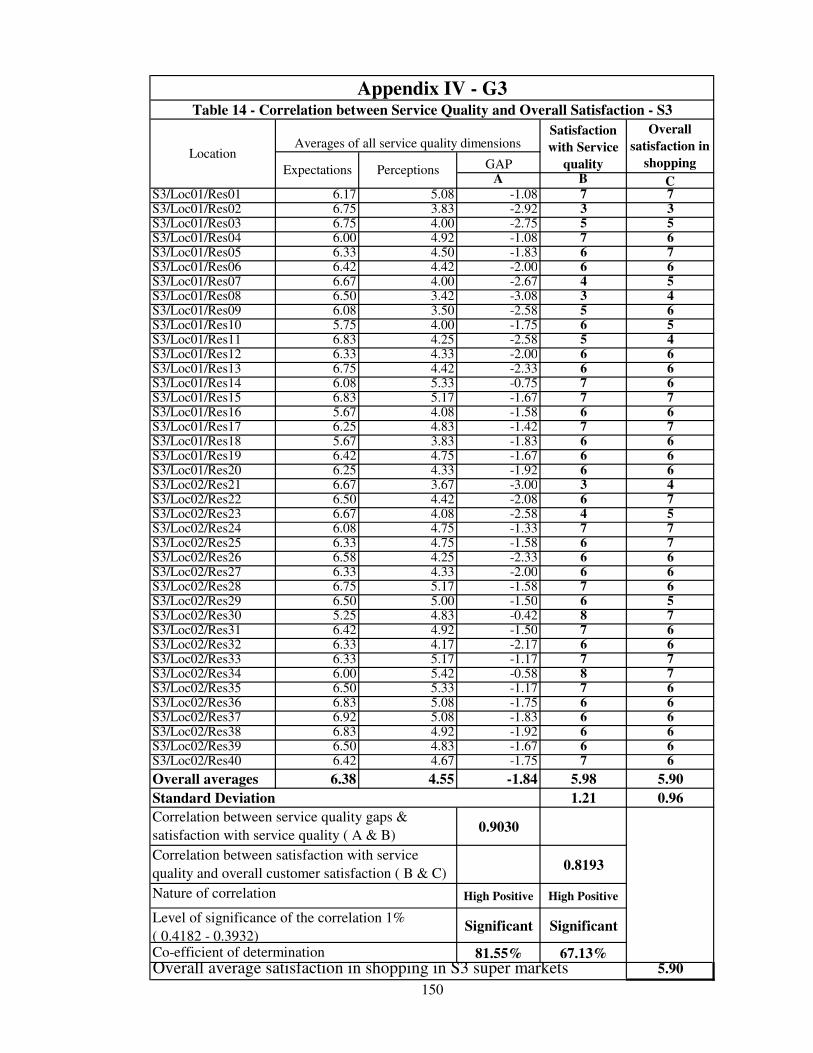

Table 14 Correlation between service quality and overall satisfaction S3 150

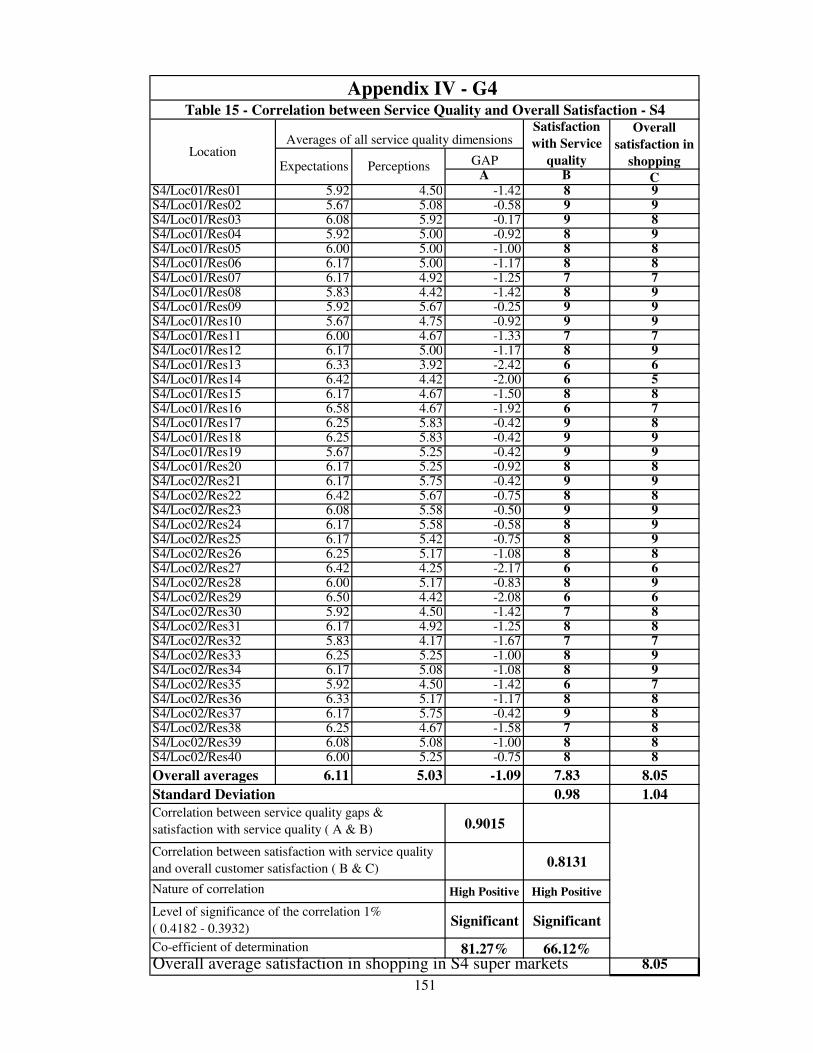

Table 15 Correlation between service quality and overall satisfaction S4 151

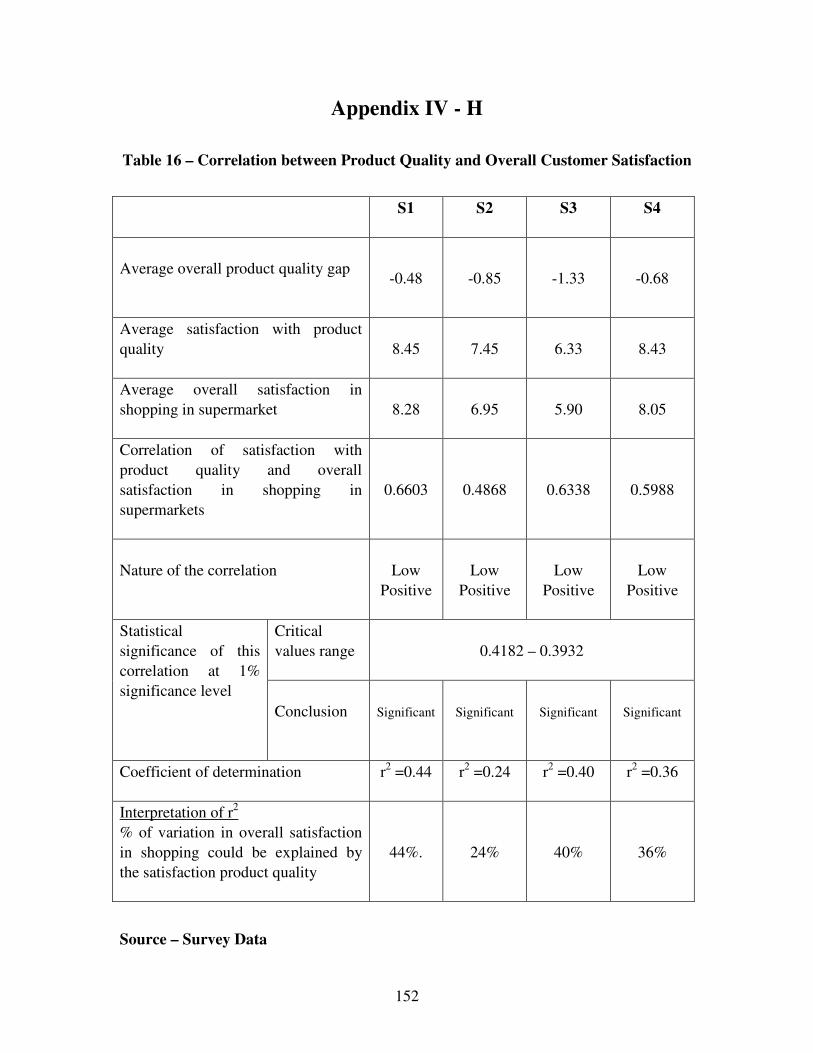

Table 16 Correlation between product quality and overall satisfaction 152

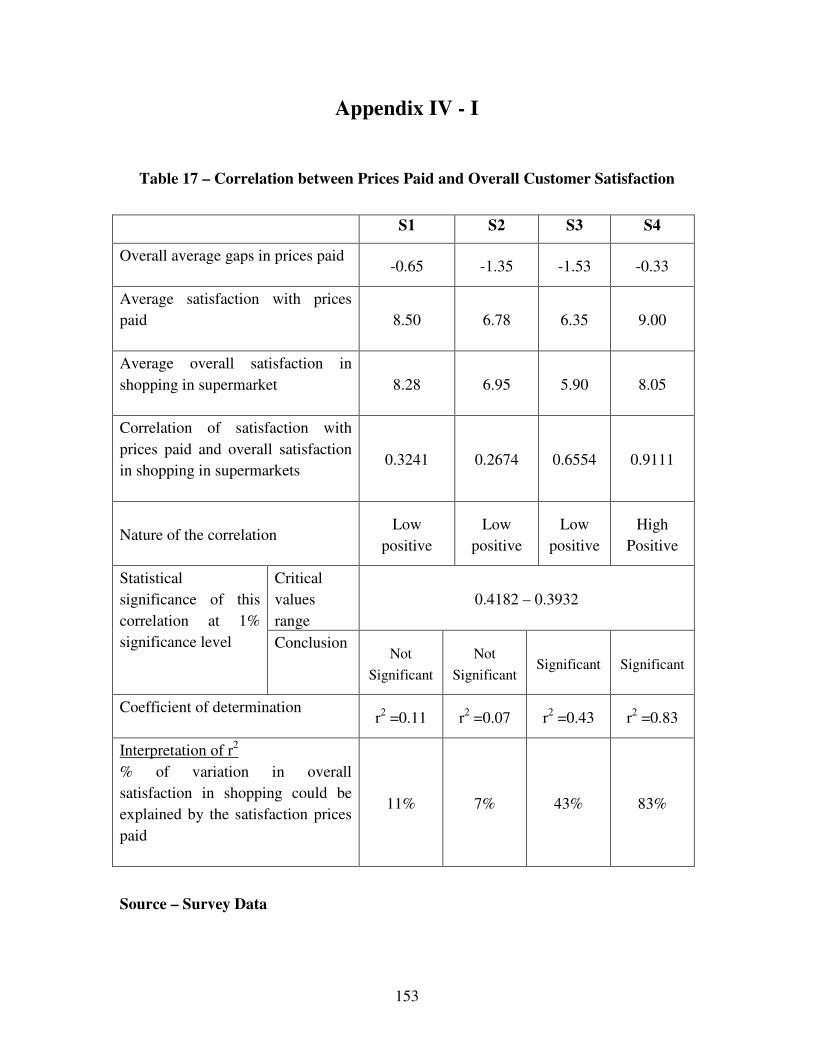

Table 17 Correlation between prices paid and overall satisfaction 153

Table 18 Hypothesis testing of H1 using a null hypothesis 157

Table 19 Hypothesis testing of H2 using a null hypothesis 158

Table 20 Hypothesis testing of H3 using a null hypothesis 159

Table 21 Summary of regression model for all supermarkets 160

LIST OF APPENDICES

Appendix I

I - A Report of the pilot study to establish the research problem. 115

I - B Questionnaire used for the pilot study 119

I - C Respondent profile of the pilot study 121

I - D1 Service quality gaps identified in the pilot study 122

I - D2 Service quality gaps identified in the pilot study-graph 123

Appendix II

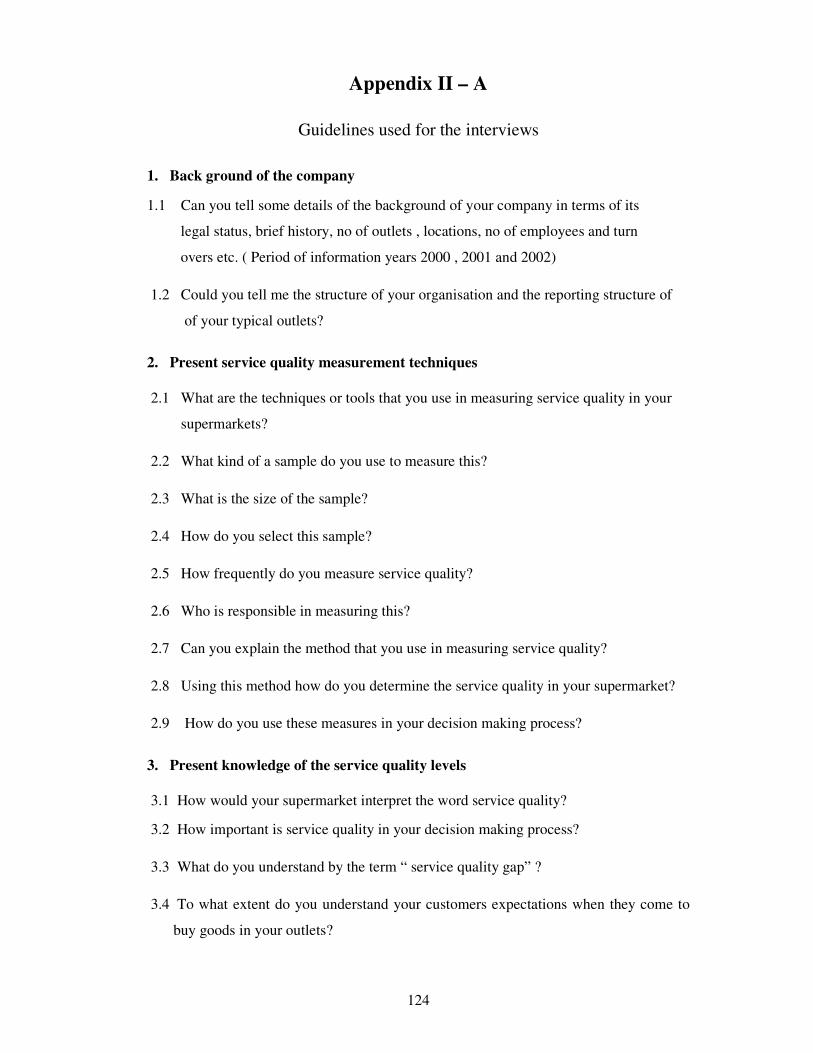

II - A Guidelines used for the interviews 124

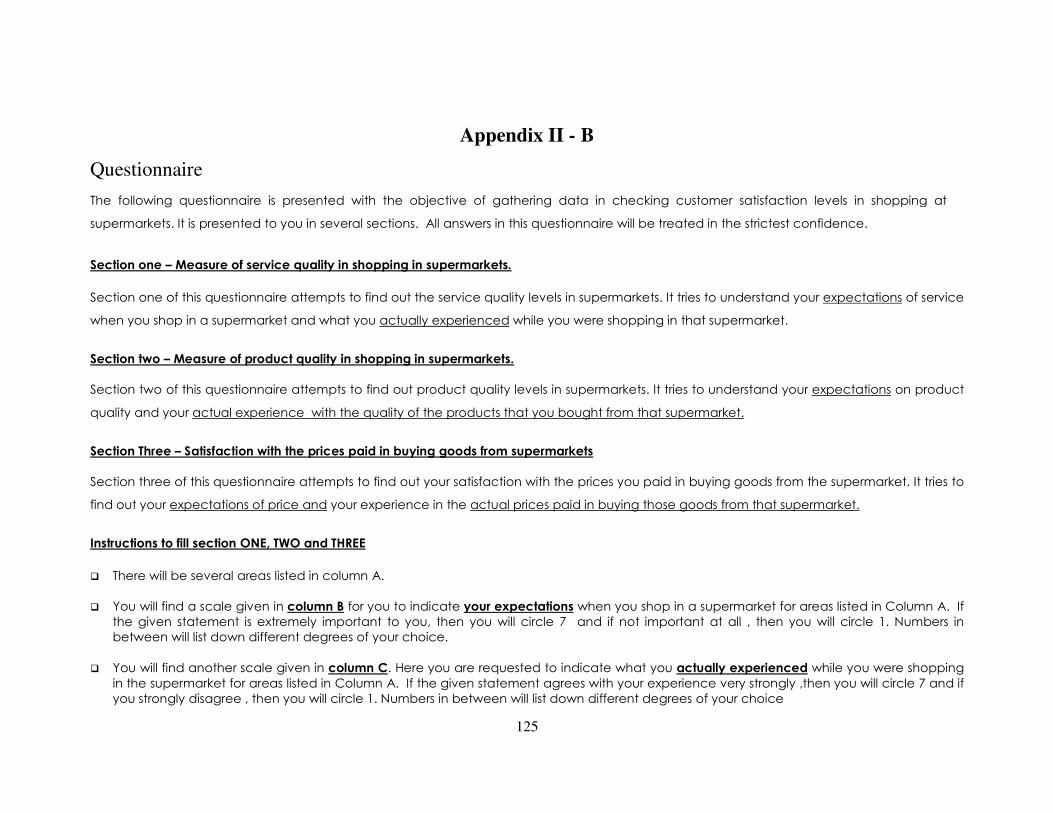

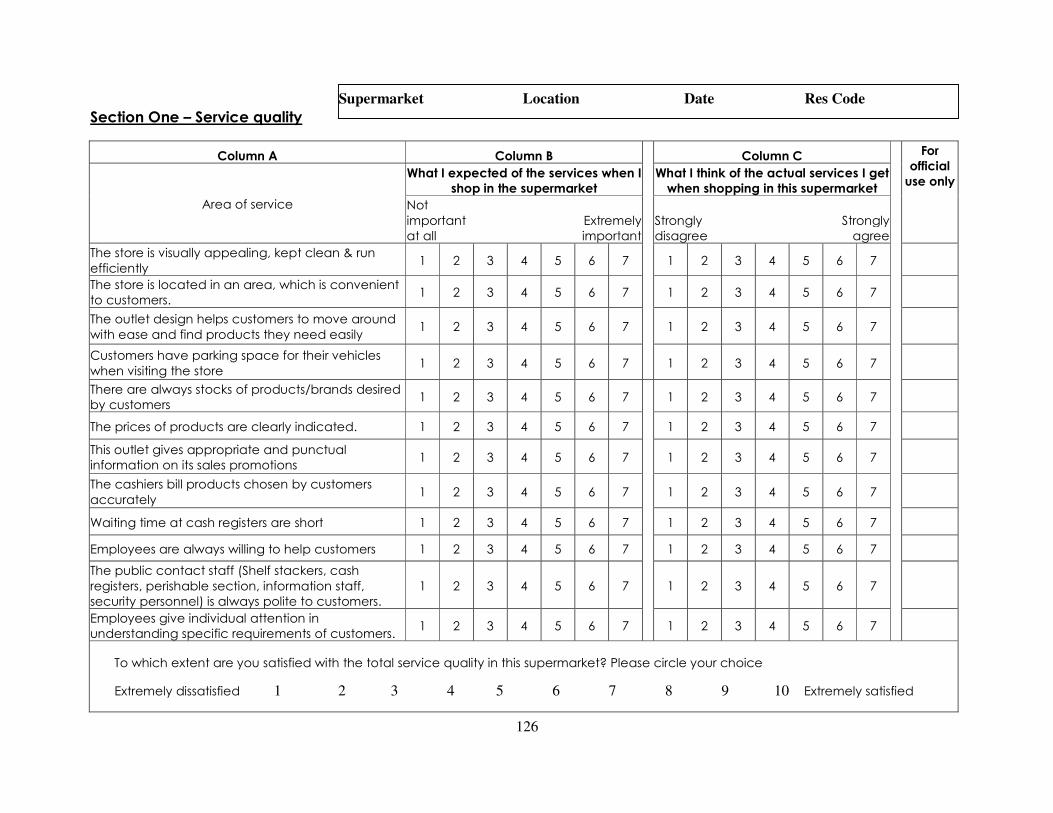

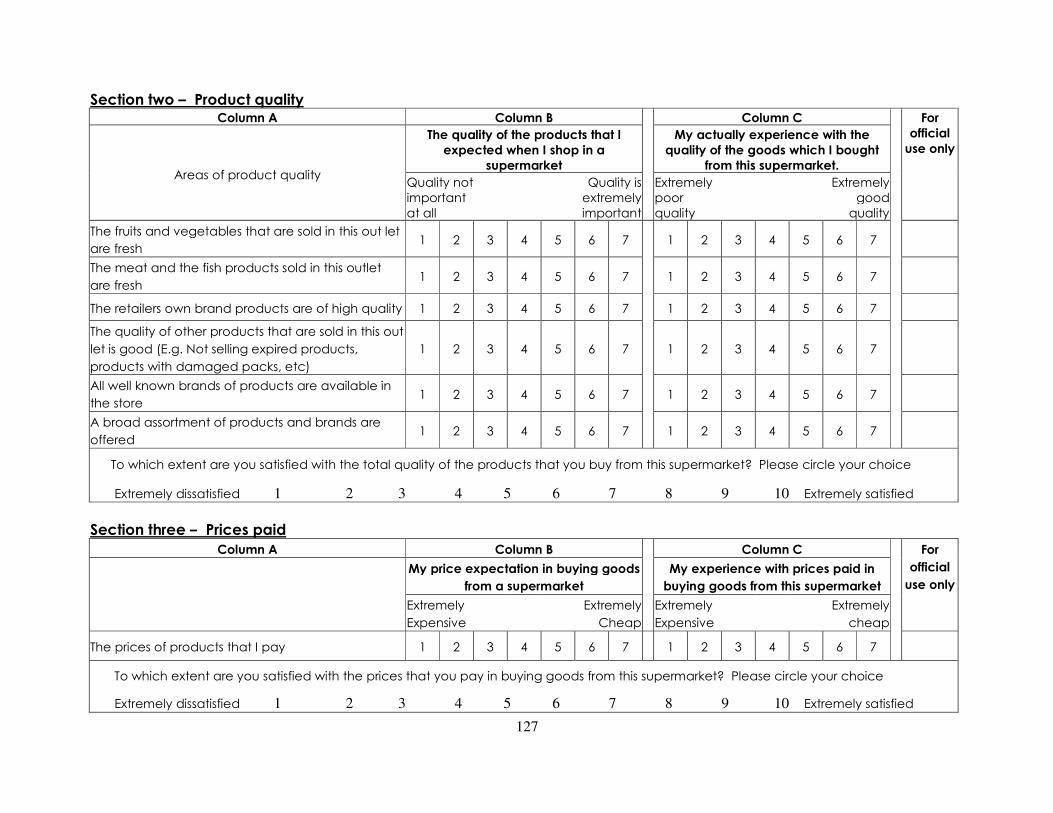

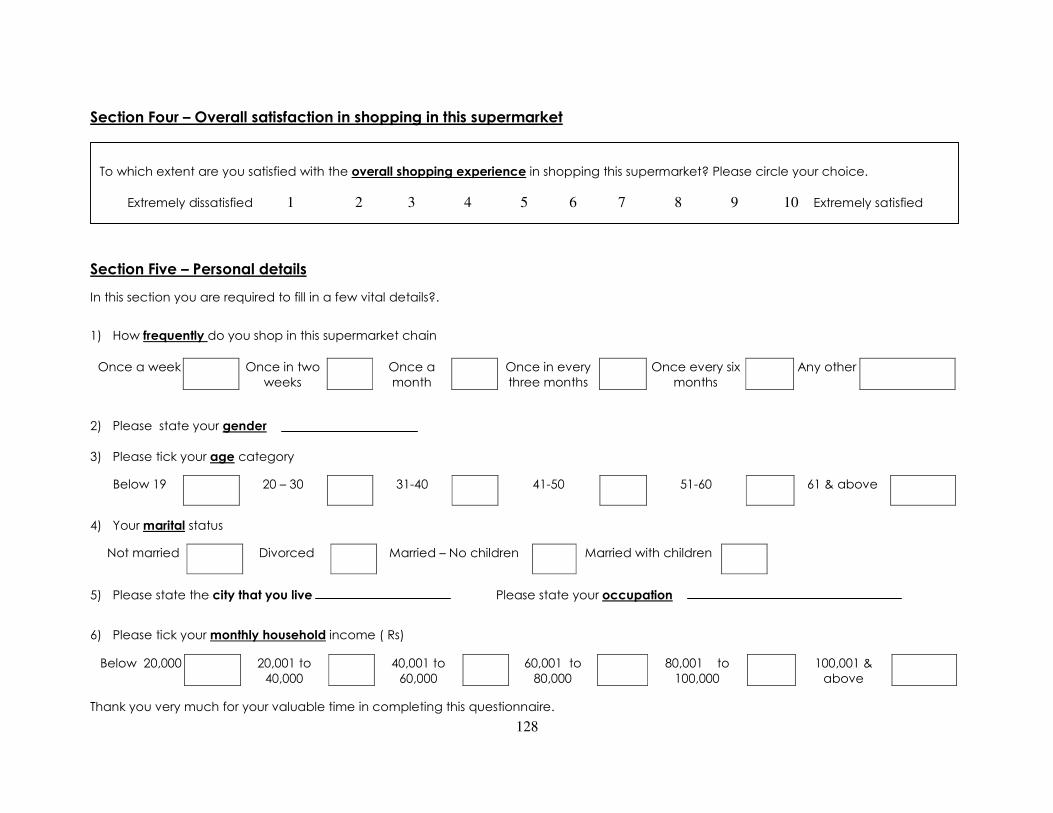

II - B Questionnaire used for the main study 125

Appendix III

III - A Classification of the retail formats in Sri Lanka 129

III - B Names of supermarkets operating in Sri Lanka 130

III - C Geographical distribution of supermarkets 132

III - D Geographical distribution of supermarkets - map 133

III - E Turnover of the five supermarkets 134

III - F Growth in turnover of five supermarkets – 2000/2002 135

III - G Change in sales share between five supermarkets 136

III - H Growth in supermarket outlets 137

III - I Supermarket retail life cycle 138

III - J Customer satisfaction index – Arpico 139

III - K Keels Super Test , service quality measurement technique. 140

III - L Complains handling unit at the ministry of commerce 141

LIST OF APPENDICES (Continued)

Appendix IV

IV - A Frequency of visits 142

IV - B Gender break down of the respondents 143

IV - C Marital status of respondents 144

IV - D Age distribution of respondents 145

IV - E Household income distribution of respondents 146

IV - F Correlation between income and price expectations 147

IV - G 1- 4 Tabulation of results for service quality – S1 to S4 148

IV - H Correlation between product quality and overall satisfaction 152

IV - I Correlation between prices paid and overall satisfaction 153

IV - J Results of the multiple regression analysis 154

IV - K 1-3 Hypotheses Testing 157

IV - L Summary of the regression analysis 160

Appendix V

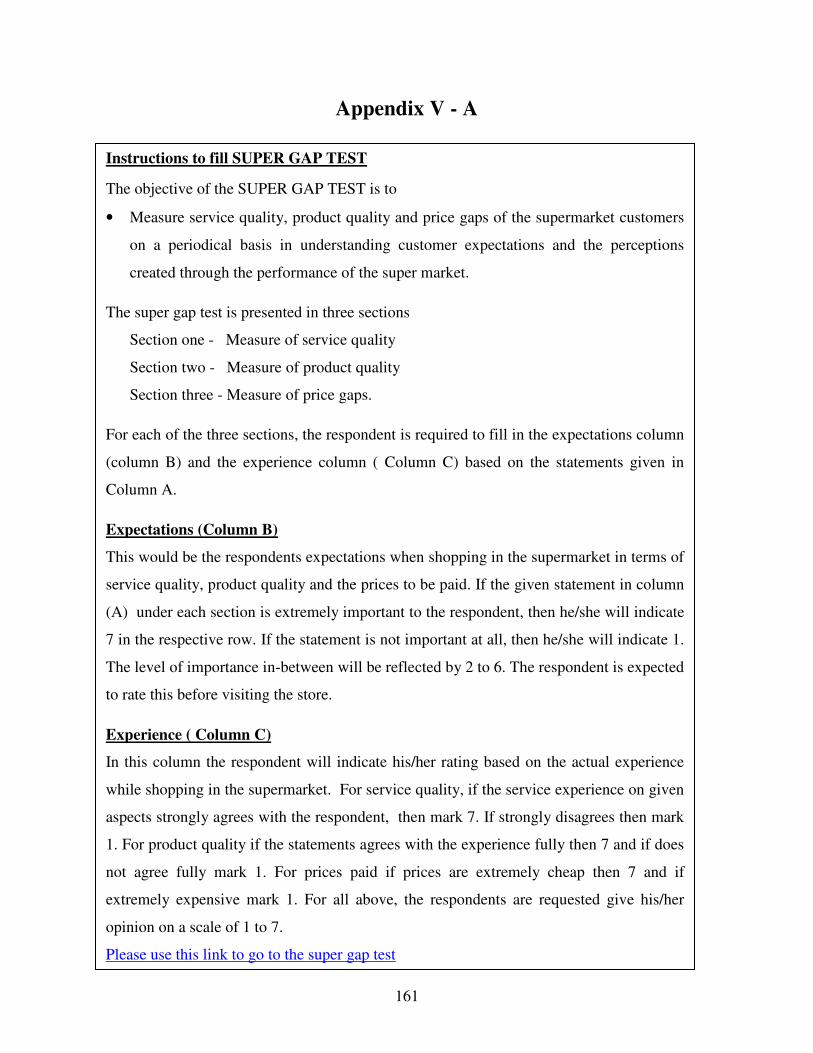

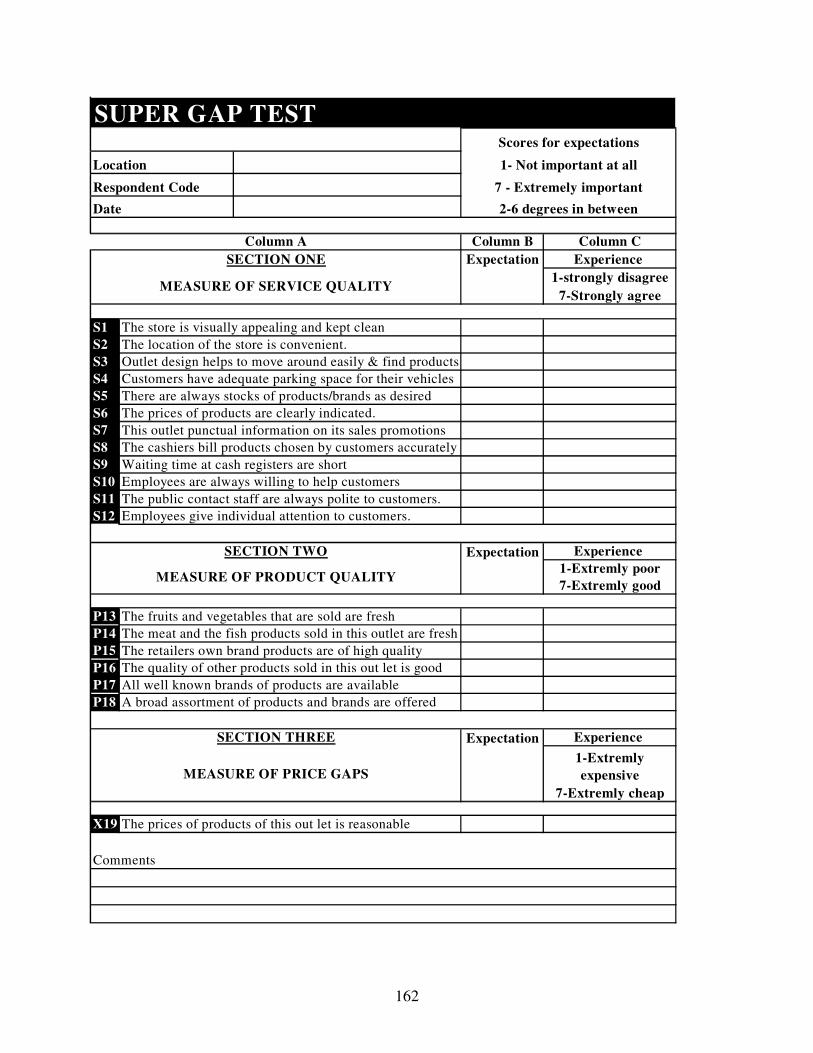

V - A SUPER GAP TEST questionnaire 161

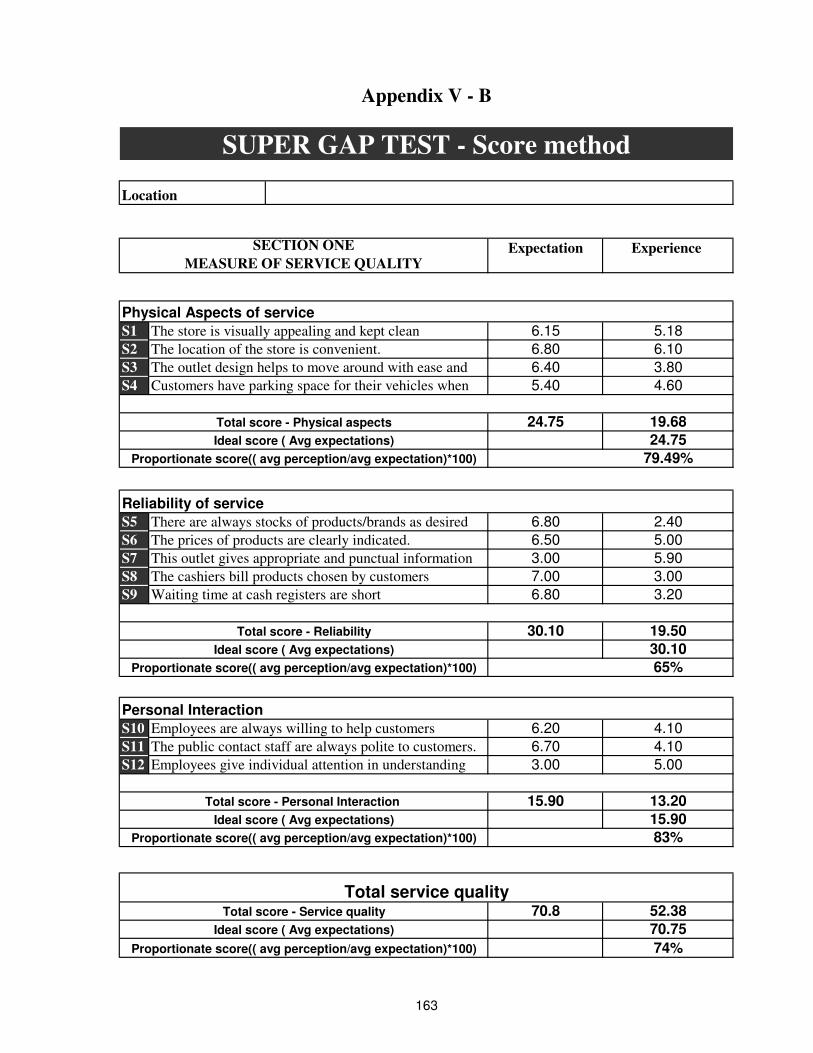

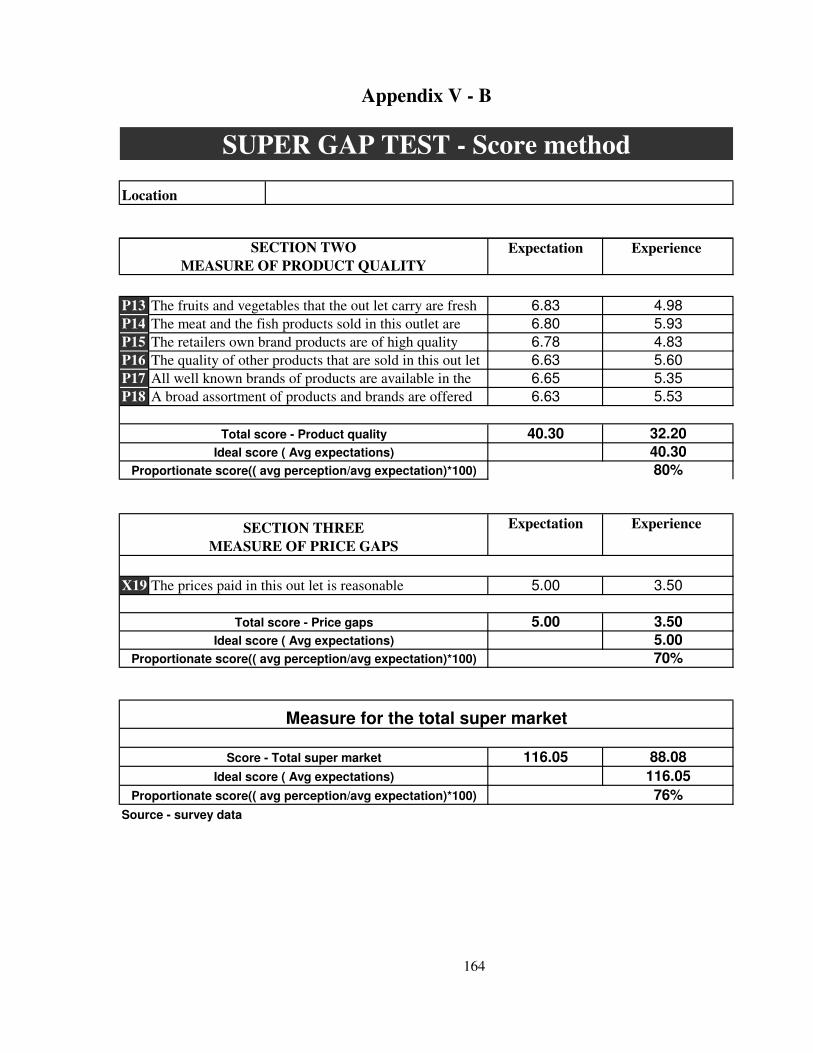

V - B Score method 162

V - C1 Gap method – service quality 165

V - C2 Gap method – product quality/prices paid 166

V - D1 Percentage method – table for all 167

V - D2 Percentage method – service quality – graphical 169

V - D3 Percentage method – product quality/prices - graphical 170

V - E1 Importance perception matrix – service statements 171

V - E2 Importance perception matrix – product statements 172

V - E3 Importance perception matrix – sub dimensions 173

V - E4 Importance perception matrix – dimensions 174

V - F Gaps & strategy interface 175

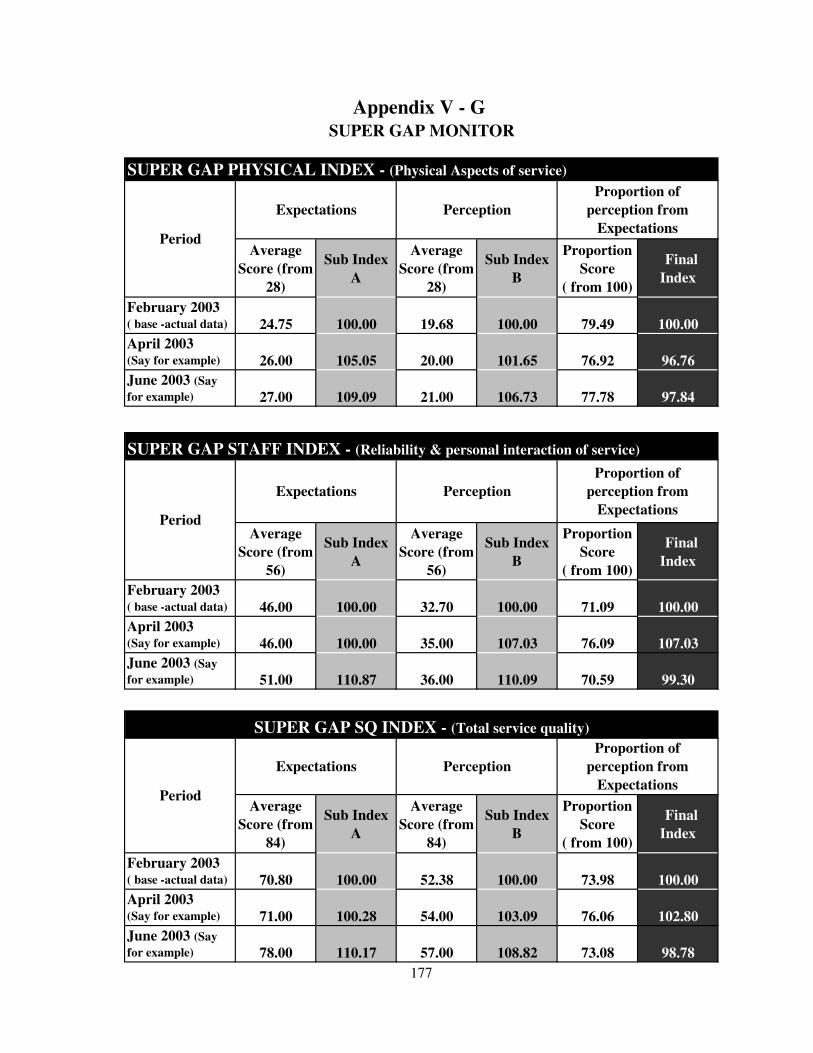

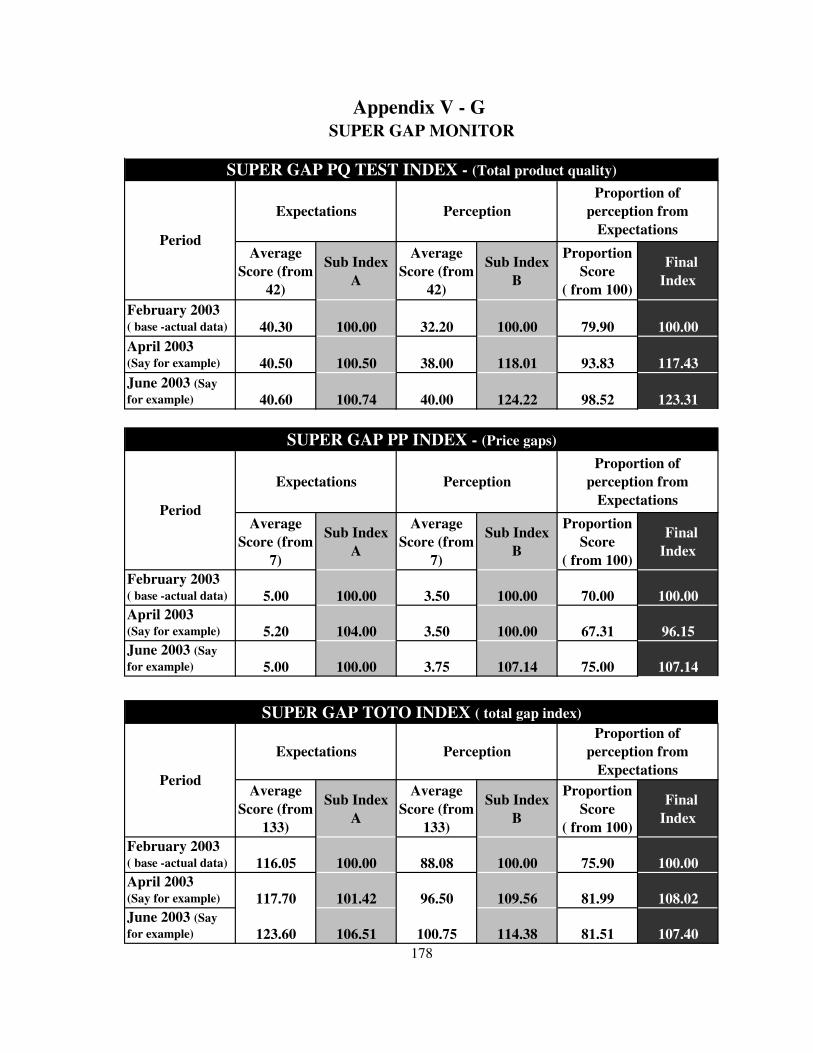

V - G SUPER GAP MONITER – Index to monitor performance 177

ACKNOWLEDEGEMENT

The writer would like to acknowledge the contribution made by several individuals in making

this research study a success.

A special note of appreciation is extended towards, Dr. Uditha Liyanage, for his insights in

guiding and supervising this research study.

The PIM librarian staff together with the librarians of the University of Colombo, University of

Sri Jayewardenepura, and the American Center is commended for an excellent job done in

extracting important articles required for the research.

The managers and the executives of Jaykay Marketing, Cargills Food City, Sentra, Sathosa and

Arpico supermarkets needs a special word of thanks for the support extended in carrying out this

study. The contribution by Mr. Shantha Kularatne at Arpico, Mr. Kumar De Silva at Jaykay

Marketing, Mr. Daraniyagala at Sentra and Mr. Wasantha Wanigasooriya at Sathosa is

appreciated for spending time explaining their operations and coordinating arrangements for the

writer in carrying out the study in their supermarkets.

Mrs. Niranjala Sendanayake at Lanka Market Research Bureau, Mr. Lohitha Karunaratne at

Arpico, Mr Dusty Alahakoon at Ceylon Tobacco Company is thanked for the extended support

given in helping the writer to compute and analyse data in interpreting the outcome of the study.

The director, the members of the faculty and all the staff at PIM, are acknowledged for their

immense contribution extended to me during my stay at PIM.

Finally I would like to thank my wife Tania for her unstinted support given in making this a

reality and my son Arith, as young as he is, in understanding his father spending long hours

away from him in completing this study.

ABSTRACT

The focus of this research study is measuring service quality as a basis for developing retail

strategies for the supermarkets in Sri Lanka. The study limits its scope to supermarkets, which

sells fast moving consumer goods (FMCG).

As identified in literature, service quality assessment is the discrepancy between the

expectations of a service and the perceived performance of that service. If perceived

performance meets or exceeds the expectation, then service quality could be regarded as good

(positive or no gap) and if it falls short of the expectation, then service quality could be stated as

poor (negative gap). The core problem that this research addresses is the non-recognition of

service quality gaps by Sri Lankan supermarkets in serving their customers. The writer argues

that this may result in a decrease in the overall satisfaction among customers in shopping in

supermarkets. The writer defines non-recognition of service quality as a combination of

measurement and awareness of service quality gaps by the supermarkets.

In studying the above problem, this research study unfolds four clear objectives.

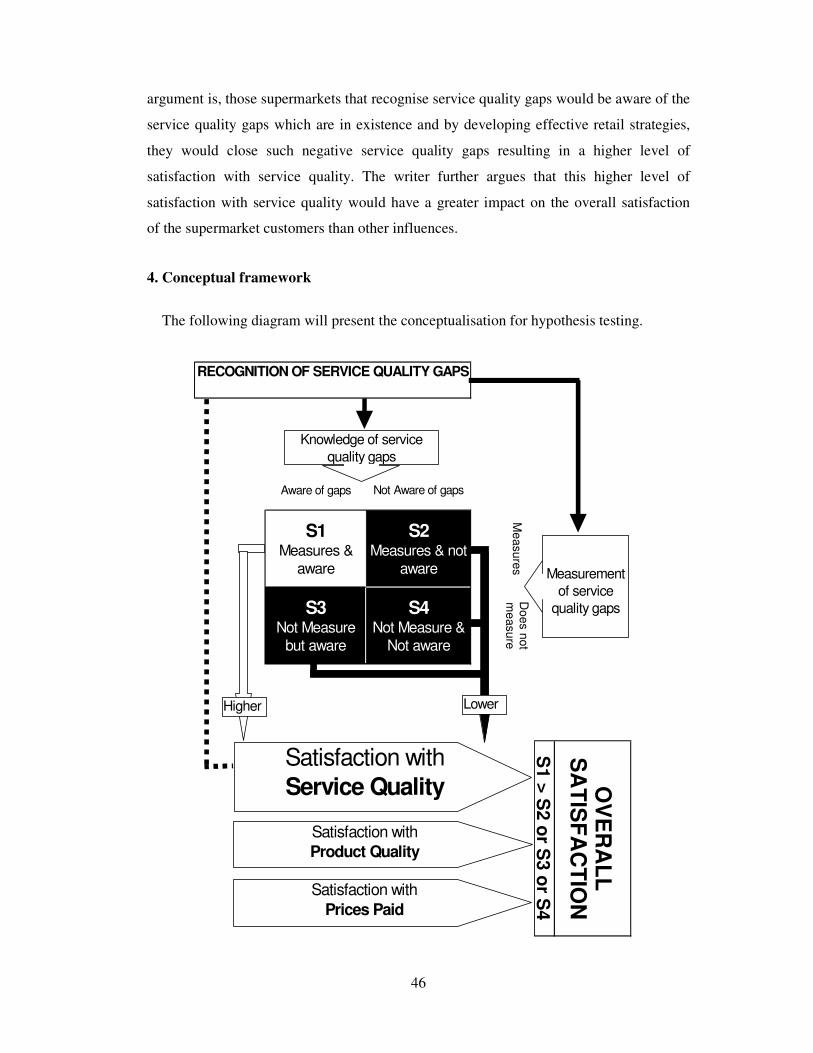

The first objective is to assess the state of service quality recognition levels in the supermarkets

in Sri Lanka. In achieving this objective the writer develops the service quality recognition

matrix, which is a combination of two dimensions, as per the definition given for service quality

recognition. Through the intersection of these two dimensions, four types of supermarkets are

argued to be in force. These are

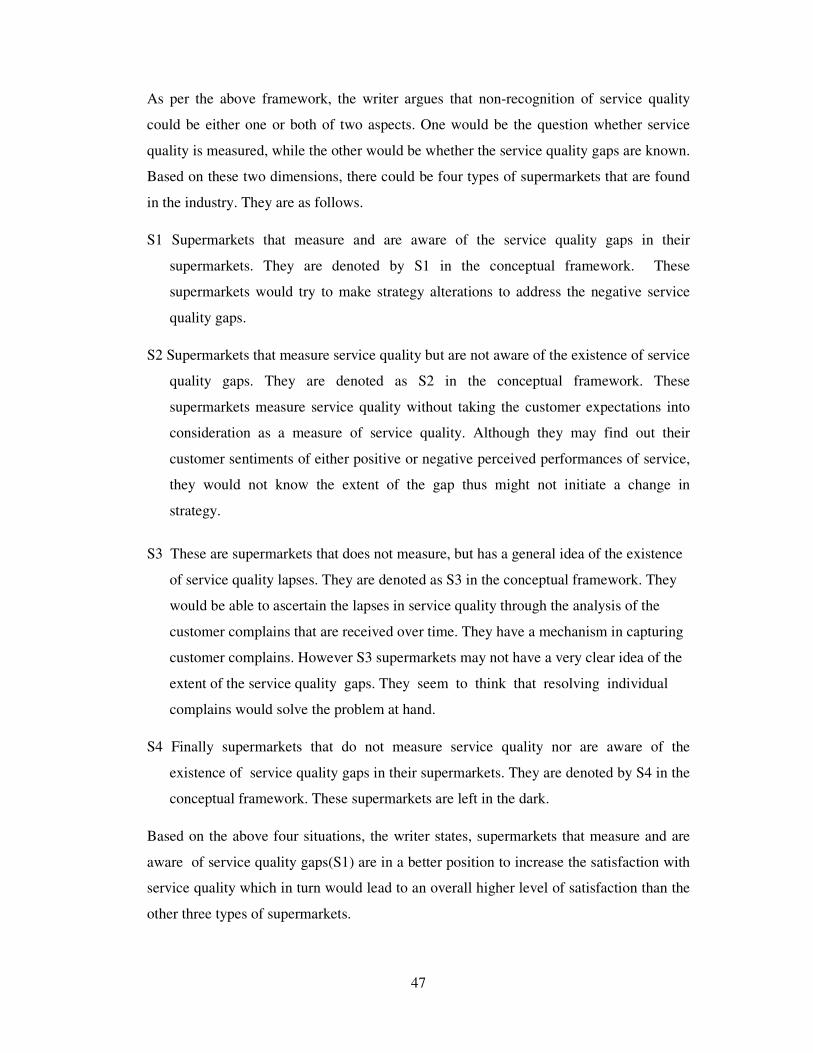

S1 type – Supermarkets that measure and are aware of service quality gaps.

S2 type – Supermarkets that measure but are not aware of service quality gaps.

S3 type – Supermarkets that does not measure but has an idea of the service quality

S4 type – Supermarkets that does not measure neither are aware of service quality gaps.

Five of the largest supermarkets, which sell FMCG products in Sri Lanka, were studied and

were plotted into this matrix based on their level of awareness and how they measure service

quality gaps in their supermarkets

The second objective set for the research was to study the relationship between the recognition

of service quality and the overall satisfaction in shopping in supermarkets. The writer questioned

the relationship between service quality gaps and the overall satisfaction in shopping in

supermarkets in depth and presented his argument that S1 type supermarkets would increase

their customer satisfaction with service quality leading to a higher impact on the overall

customer satisfaction than the rest. A conceptual model was developed where three hypotheses

were presented for testing which essentially stated that the overall satisfaction of customers who

shop in S1 type supermarkets are greater than customers who shop in either S2, S3 or S4 types.

The rationale for this argument was that supermarkets, which had a high level of service quality

recognition level, understood the gaps better than the others. Through the development of retail

strategies they were able to close some of those negative gaps efficiently than the rest.

The third objective set for the research was to identify the influence of satisfaction with product

quality and satisfaction with prices paid on the overall satisfaction of the super market customer.

In order to test the second and the third objectives, a questionnaire survey was carried out among

4 supermarkets representing each of the quadrants of the service quality recognition matrix. The

overall satisfaction of those supermarkets was arrived at by measuring gaps in service quality,

product quality and satisfaction with prices paid. The questionnaire was adapted by a similar

study done in supermarkets in Spain with minimum changes. The findings suggested that the

overall satisfaction of S1 supermarkets were higher than S2, S3 or S4 in terms of an average.

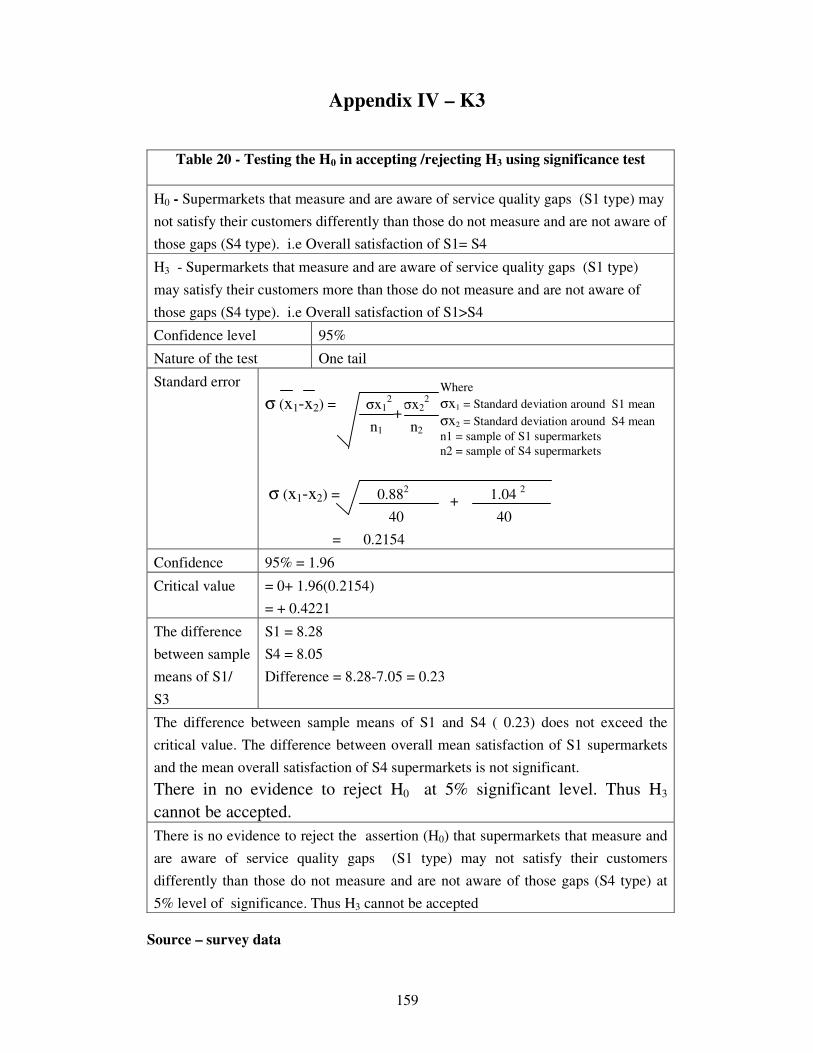

However during the hypotheses test, although S1 satisfaction was significantly higher than S2

and S3, it was not significantly different from S4. This lead to the rejection of hypotheses three.

(S1 satisfaction > S4 satisfaction).

In understanding the possible reasons for the above relationships through correlation analysis,

multiple regression analysis, and analysis of supermarket customer segments and through other

cross analysis, the following conclusions were arrived at.

The customers of the four supermarkets could be clearly segmented into two distinct groups

based on their level of income and price expectations. They are price inelastic customer

segments (S1 and S2) and price elastic customer segments (S3 & S4)

Service quality appears to have a significant impact on the overall satisfaction of all

supermarkets.

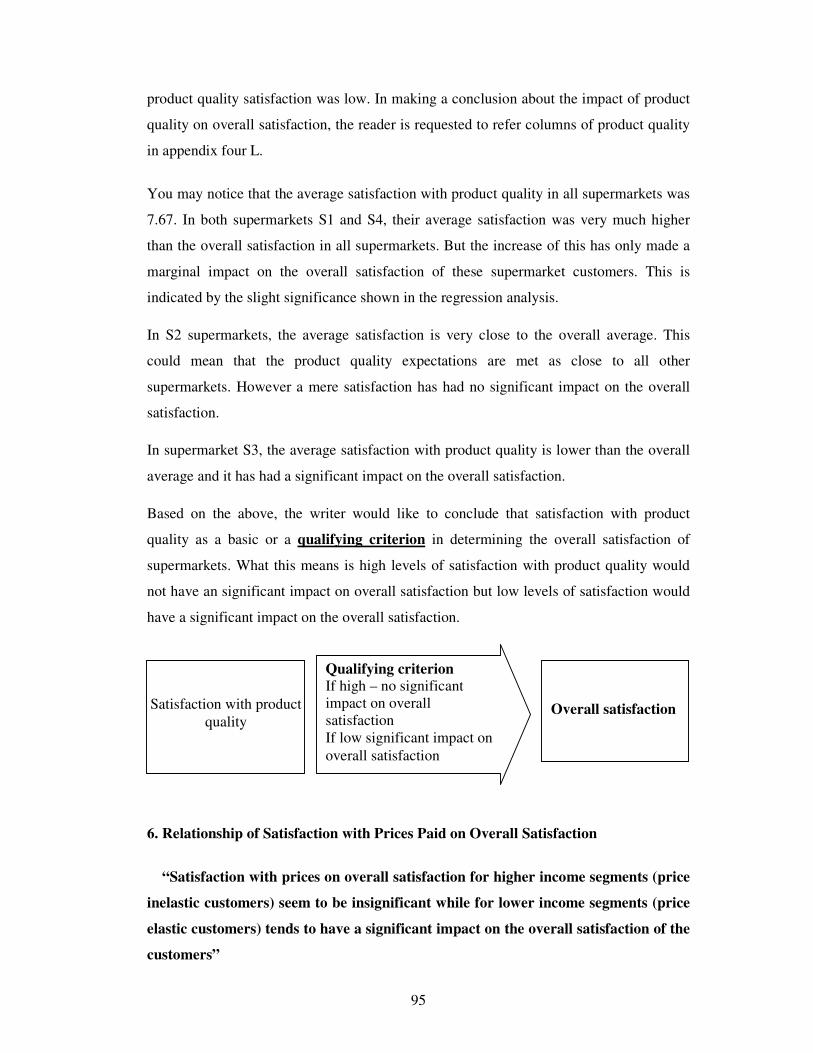

Satisfaction with product quality acted as a qualifying criterion in influencing the overall

satisfaction of supermarket customers irrespective of segments.

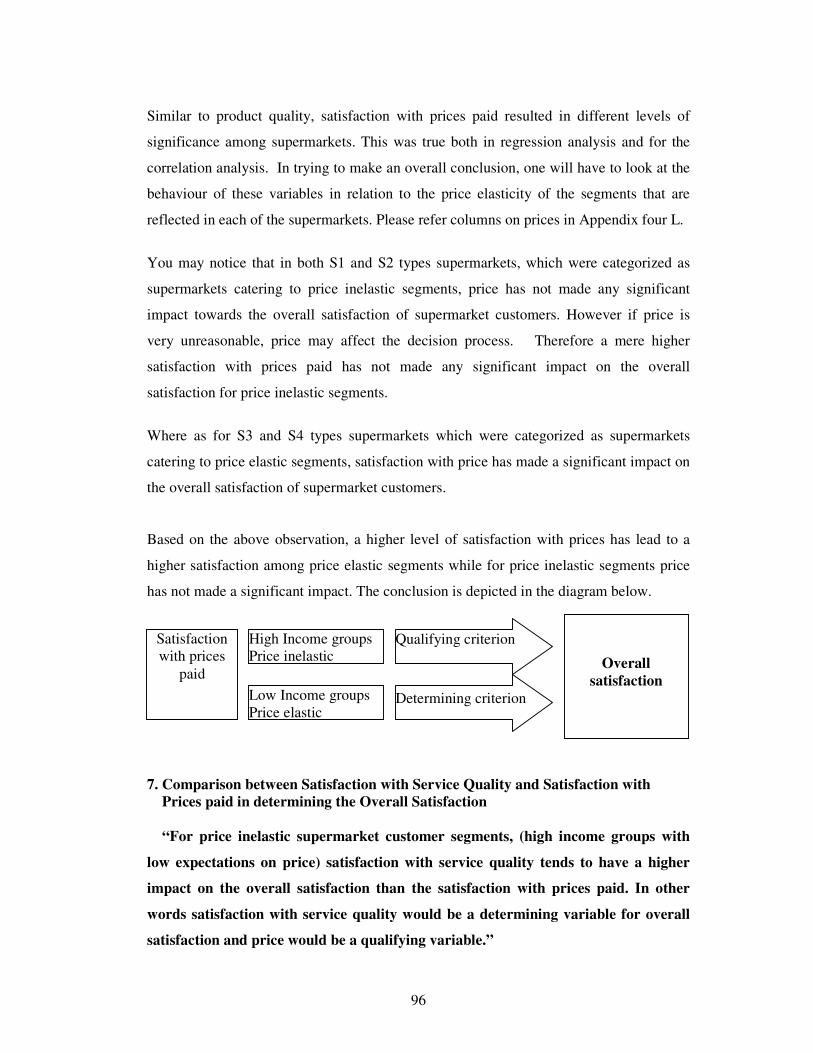

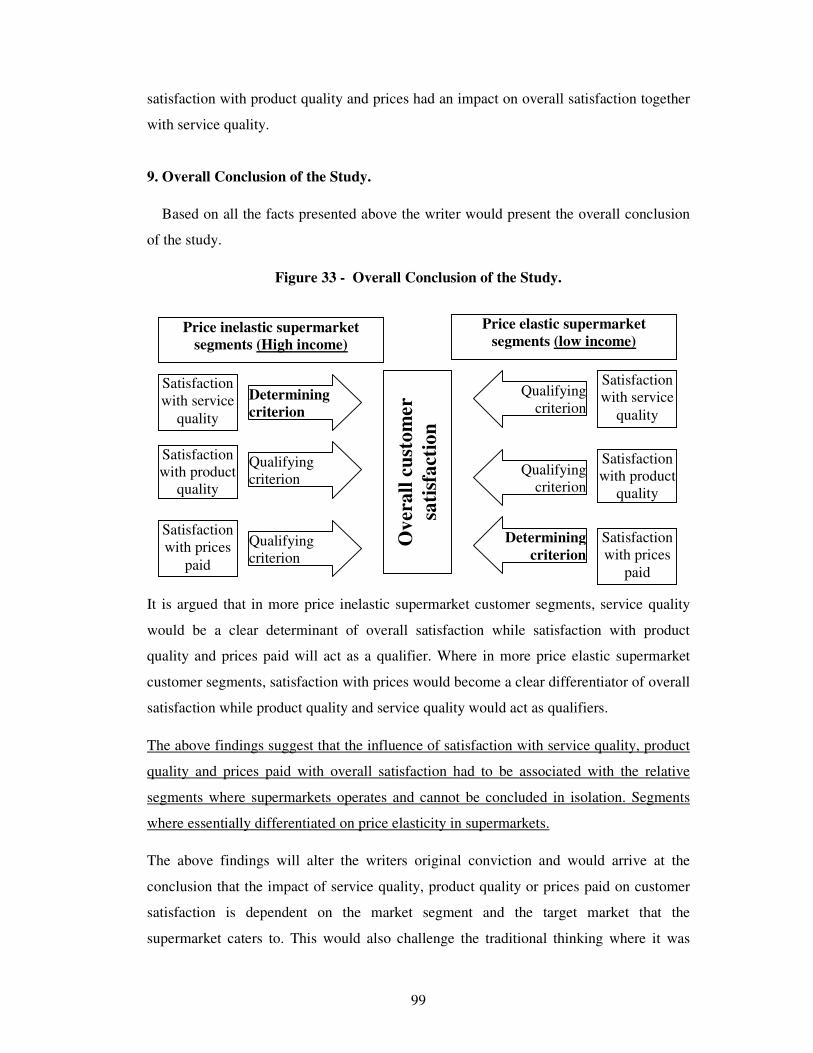

In more price inelastic markets, service quality acts as a clear determinant of overall

satisfaction while satisfaction with product quality and prices paid acts as qualifiers. In more

price elastic markets, satisfaction with prices would become a clear differentiator of overall

satisfaction while product quality and service quality would act as qualifiers.

The above findings explain why the third hypothesis which compared overall satisfaction with

price inelastic (S1) and price elastic (S4) market segments had different levels of influence from

service quality and prices. The original conviction of the writer, which stated service quality as a

determining criterion of satisfaction did not hold true for every situation. The overall conclusion

was that the impact of service quality, product quality and prices paid in influencing the overall

satisfaction needs to be understood and commented based on the respective market segments the

supermarkets were targeting to.

The fourth and the final objective of this study was to make strategy recommendations in closing

service quality gaps. As recommendations the writer will present a four-step model, which gives

new insights as to how, service quality, product quality and gaps in prices paid should be

measured using the SUPER GAP TEST as suggested by the writer. Insights into how gaps could

be quantified using three techniques namely the score method, gap method and the percentage

method will be discussed in length. Recommendations were also made giving the supermarkets

two strategy tools, which could be used as diagnostic tools in bridging the gaps in service

quality. A proposal is made in developing an index in measuring and monitoring the

implementation of the strategies in closing gaps. Finally the writer also recommends two generic

strategies for supermarkets to consider influencing the overall customer satisfaction for both

types of segments that were identified in the research.

TABLE OF CONTENTS

List of Illustrations …………………………. ii

List of Tables …………………………. iv

List of Appendices …………………………. v

Acknowledgement …………………………. vii

Abstract …………………………. viii

PART I

CHAPTER I - INTRODUCTION

1. Background …………………………. 01

2. Research problem …………………………. 01

3. Justification of the problem …………………………. 02

4. Objectives of the study …………………………. 03

5. Significance of the study …………………………. 04

6. Scope of the study …………………………. 05

7. Chapter framework …………………………. 06

CHAPTER II - LITERATURE REVIEW

1. Introduction …………………………. 07

2. Definition of service quality …………………………. 07

3. Service quality and the service marketing mix …………………. 09

4. Techniques in measuring service quality ……………….………… 12

5. Service quality, product quality, prices and customer satisfaction 21

6. Developing retail mix strategies ………………………….. 25

7. Summary …………………………. 44

CHAPTER III - CONCEPTUAL FRAMEWORK & METHODOLOGY

1. Introduction …………………………. 45

2. Research question …………………………. 45

3. Argument …………………………. 45

4. Conceptual framework ………………………… 46

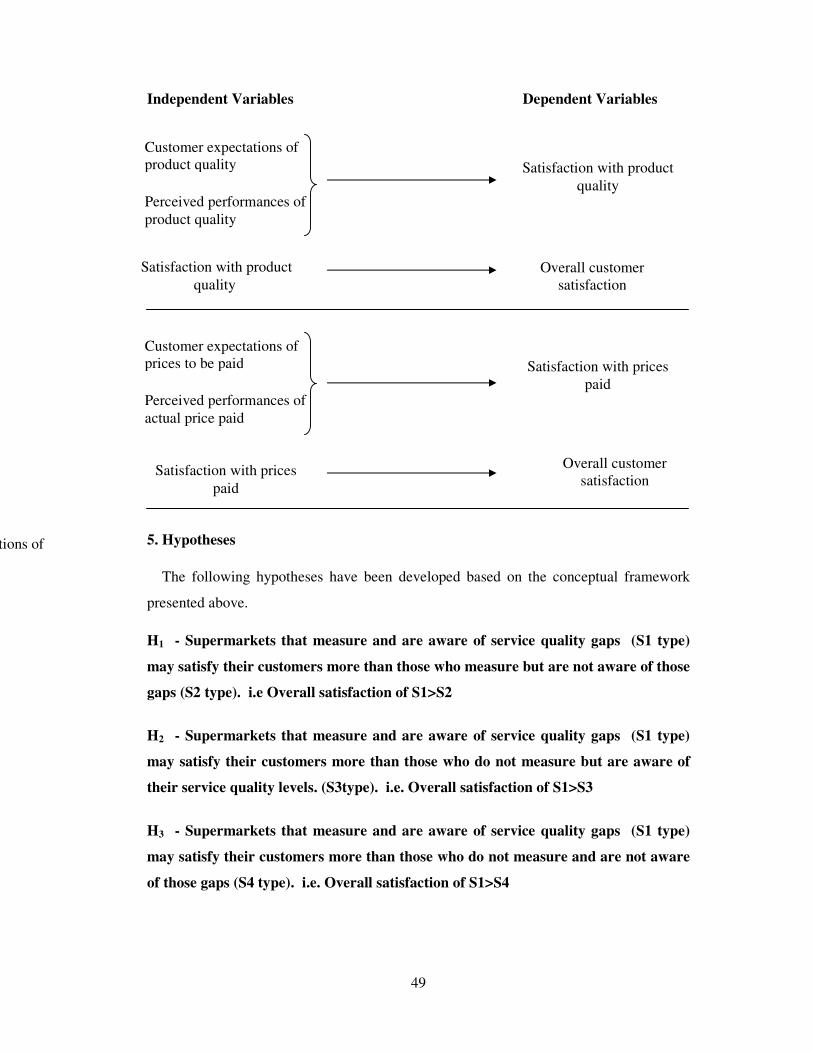

5. Hypothesis ………………………… 49

6. Definition of key concepts ………………………… 50

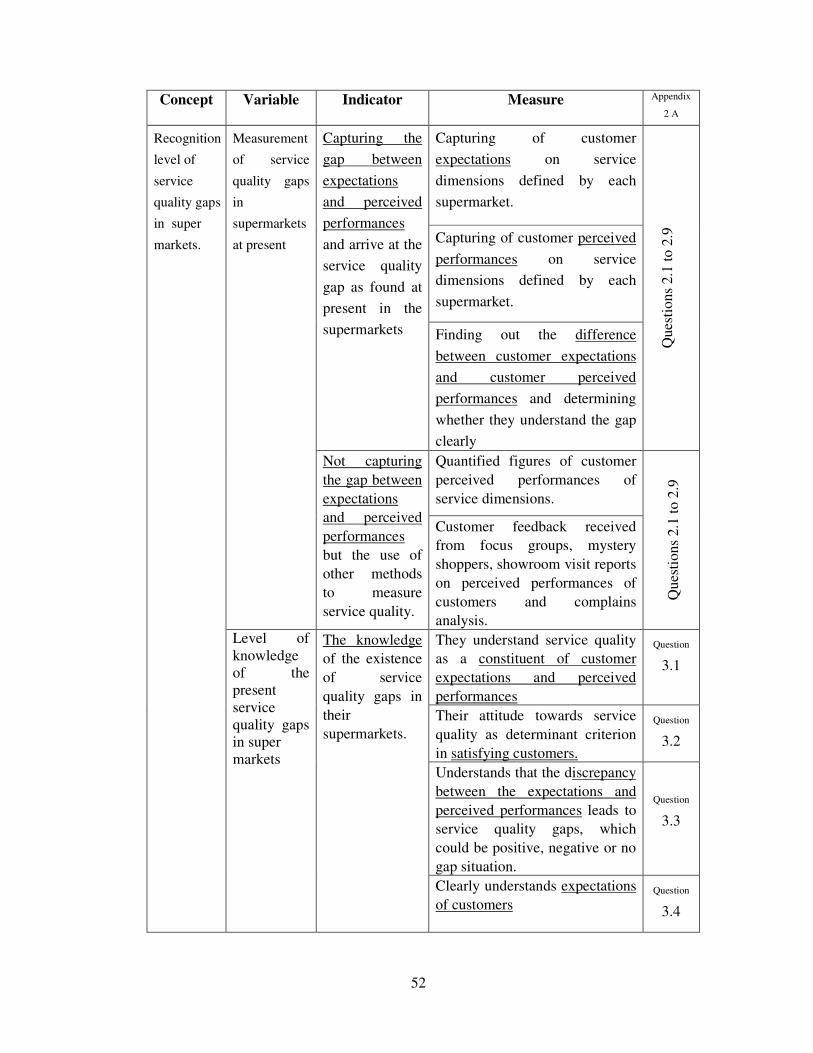

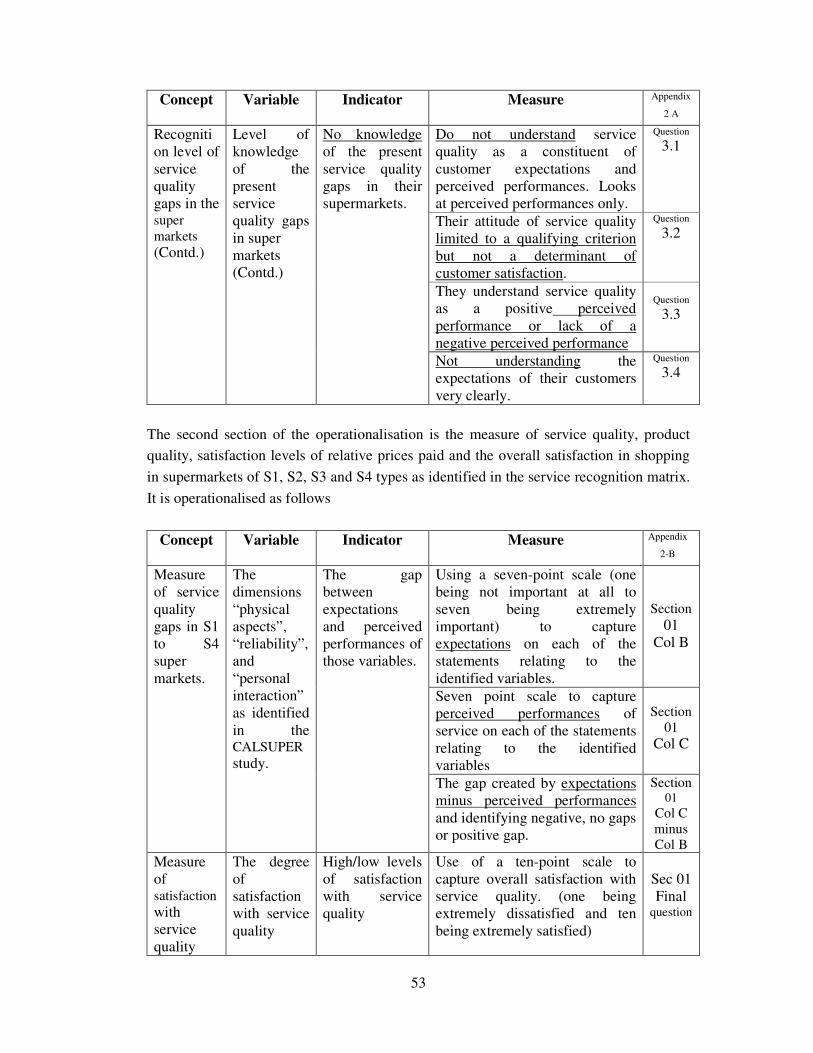

7. Operationalisation ………………………… 51

8. Methodology ………………………… 55

8.1 Methodology of collecting information ……………………. 55

8.2 Selection of the sample ………………………… 55

8.3 Questionnaire design ………………………… 55

8.4 Method of data analysis ………………………… 57

9. Limitations of the study …………………………. 58

10. Summary …………………………. 59

PART II

CHAPTER IV – PRESENT SERVICE QUALITY RECOGNITION LEVELS

1. Introduction …………………………. 60

2. Super markets at a glance ………………………… 61

3. Arpico Super centers ………………………… 62

4. Cargills Super markets ………………………… 66

5. Keells Super markets ………………………… 70

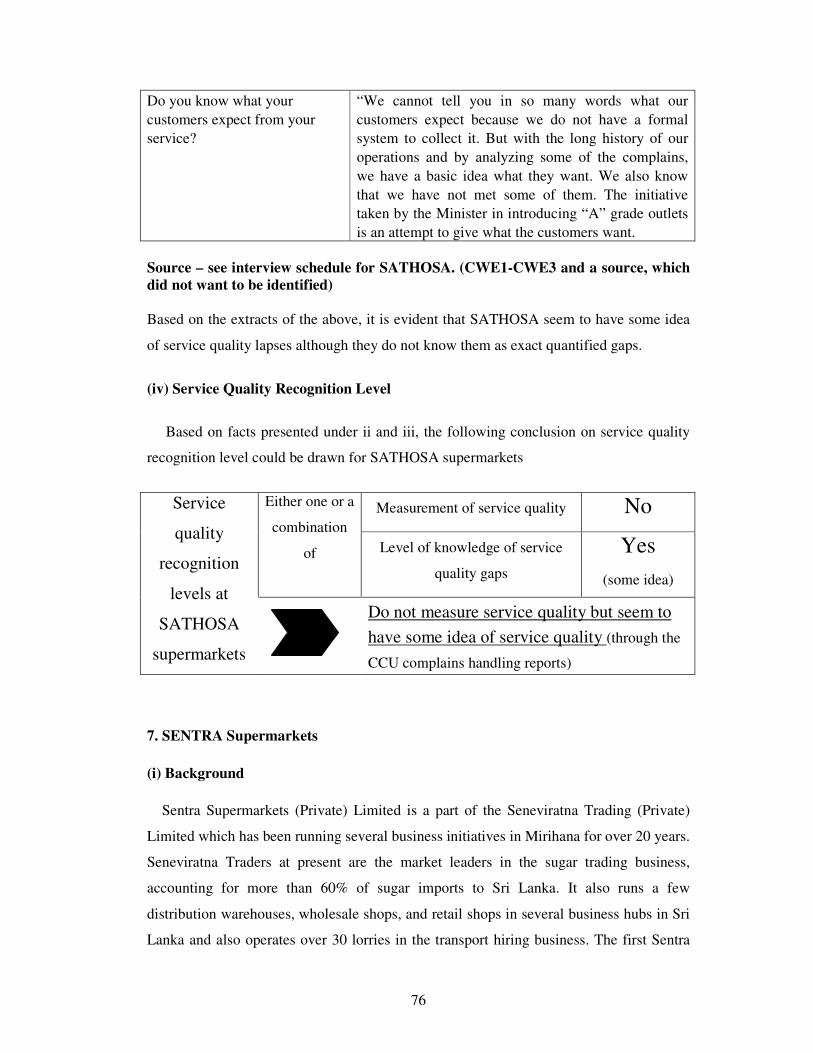

6. Sathosa Super markets ………………………… 74

7. Sentra Super markets ………………………… 76

8. Service quality recognition matrix for the five supermarkets …….. 79

9. Summary …………………………. 80

CHAPTER V – DATA ANALYSIS AND DISCUSSION OF FINDINGS

1. Introduction ………………………….. 81

2. Target market profile of the sample ………….……………….. 81

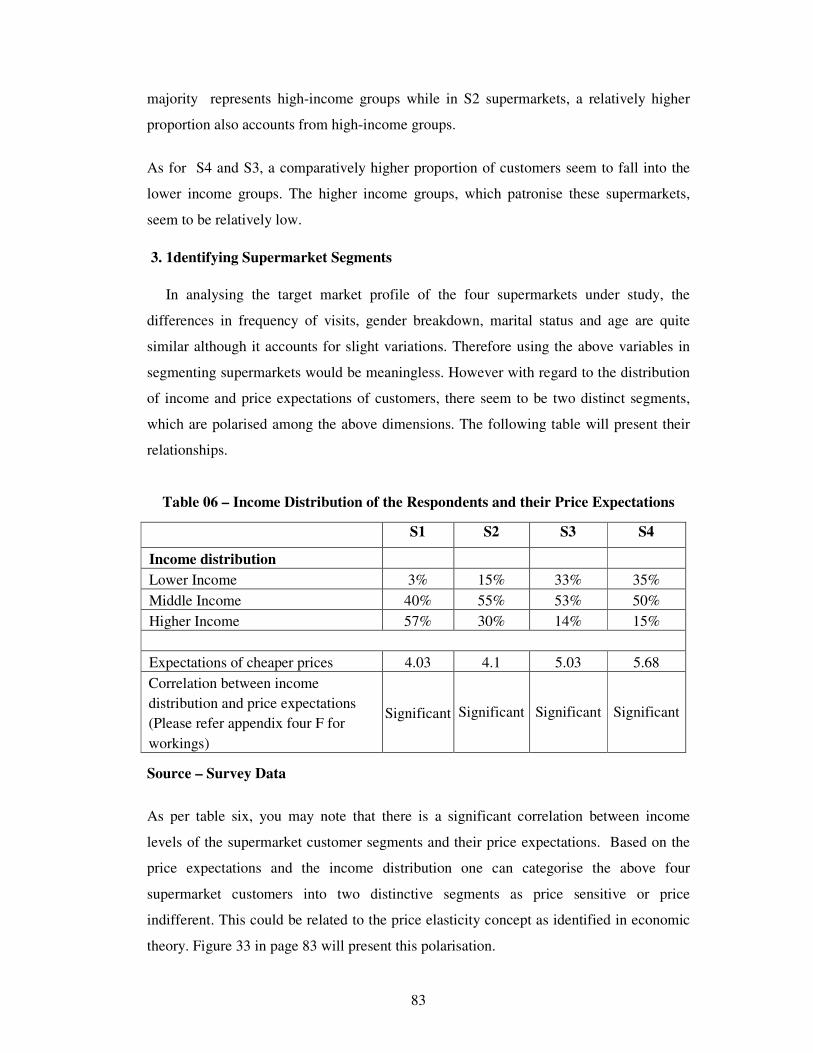

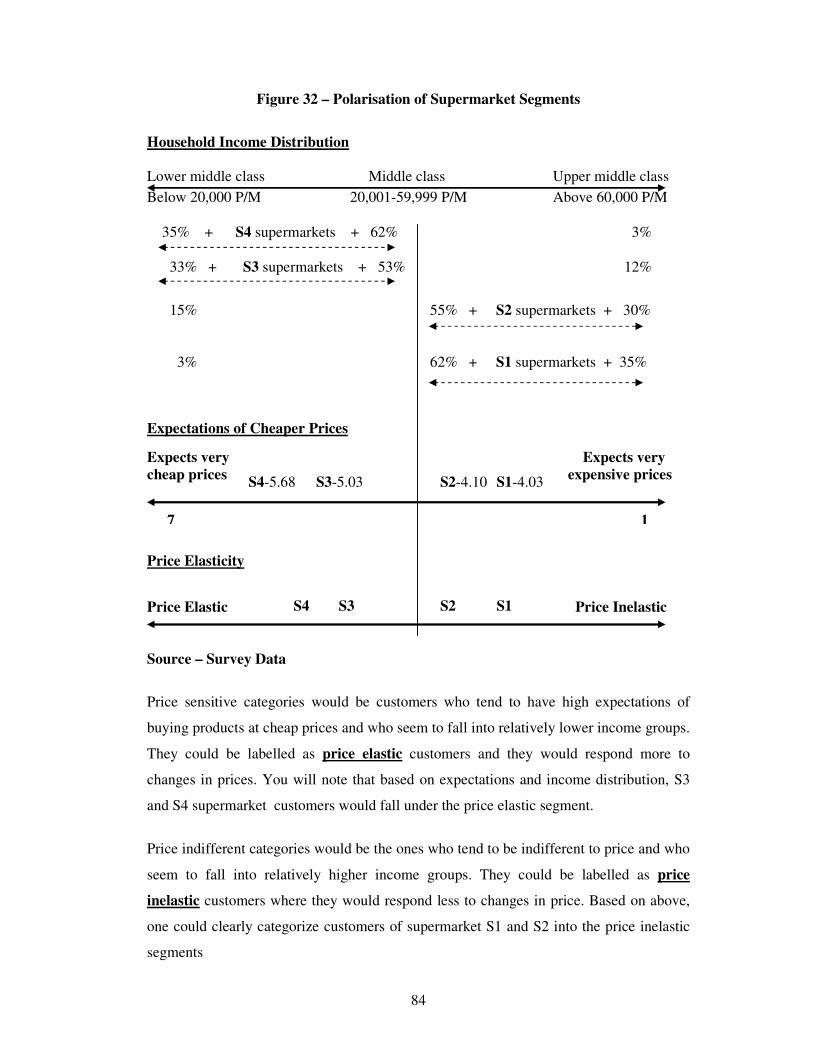

3. Identifying super market segments …….……………………. 83

4. Findings on service quality recognition and overall satisfaction…… 85

5. Findings on product quality and overall satisfaction ……………… 86

6. Findings on prices paid and overall satisfaction ……………..……. 86

7. Discussion of finding of the multiple regression analysis …………. 87

8. Testing of hypothesis ………………………….. 89

9. Summary ………………………….. 91

CHAPTER VI – CONCLUSIONS

1. Introduction ………………………….. 92

2. Service quality recognition in Sri Lankan supermarkets .…………. 92

3. Relationships between gaps and satisfaction of those attributes…… 92

4. Relationships between service quality and overall satisfaction ..….. 94

5. Relationships between product quality and overall satisfaction ..….. 94

6. Relationships between prices paid and overall satisfaction ……….. 95

7. Service and prices vs overall satisfaction ………………………….. 96

8. Conclusions from hypothesis testing …………………………. 97

9. Overall conclusion of the study …………………………. 99

10. Summary …………………………. 100

CHAPTER VII – RECOMMENDATIONS

1. Introduction …………………….… 101

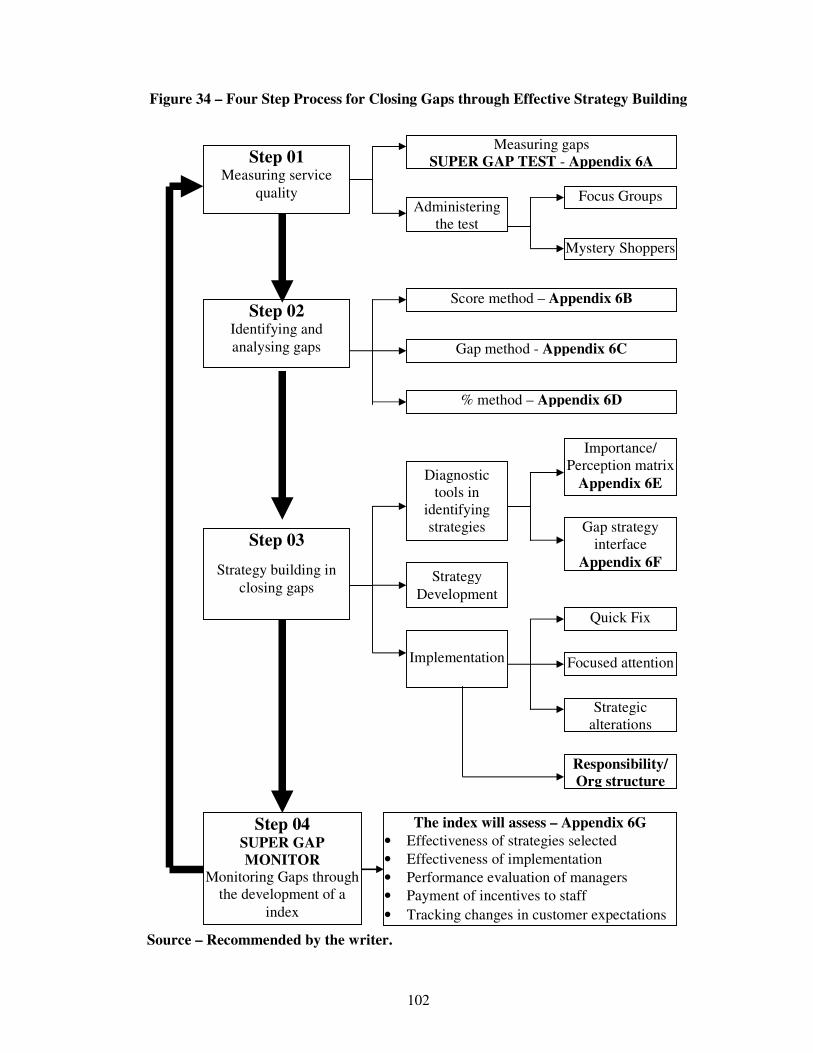

2. Four step process approach in closing gaps ………. .…………….. 102

3. Step one – Measuring gaps …………………….… 103

4. Step two – Analysing the gaps .……………………… 104

5. Step three – Building strategies to close gaps …..…………………. 106

6. Step four – Monitoring gaps .………………………. 110

7. Overall strategies based on research findings ……………………… 112

8. Summary ………………………. 114

Appendix I - Pilot study results …………………………. 115

Appendix II - Questionnaires used for the research …………... 124

Appendix III - Glance at the supermarket industry in Sri Lanka 129

Appendix IV - Survey data …………………………. 142

Appendix V - Recommendations …………………………. 161

List of references …………………………. 179

Bibliography …………………………. 182

Interview schedule …………………………. 183

1

Chapter I

INTRODUCTION

1. Background

Service quality is an essential element in the customer satisfaction process. However

the supermarkets under study, does not heed to recognise the importance of measuring

service quality and identifying gaps that may have caused by the existing retail strategies

in practise. This research paper is an attempt to find out the relationship between the

service quality recognition levels and customer satisfaction in the Sri Lankan

supermarkets selling FMCG products and recommending the measurement of same as a

basis for developing retail strategies to close such gaps.

2. Research Problem

“The non-recognition of service quality gaps by the supermarkets in Sri Lanka in

serving supermarket customers.”

Service quality assessment relates to the discrepancy between customer expectations and

perceived performance of the service delivery. This will be explored in depth under the

literature review. As per this short definition of service quality, three types of service

quality gaps could be identified. They are the no gap situation, positive gap situation and

the negative gap situation. Out of the three, the most adverse situation would be negative

service quality gaps where by the perceived service delivery falls short of customer

expectations.

As per the problem statement, the writer is of the view that supermarkets in Sri Lanka

does not recognise service quality gaps in serving supermarket customers who shop in

their supermarkets. The result of this would be poor levels of satisfaction with service

quality, which may lead to a decrease in the overall satisfaction in shopping in

supermarkets. In focusing on the problem, the writer argues that non-recognition of

service quality gaps may occur due to one or many of the following;

Not measuring service quality in the supermarkets

Not knowing the existence of service quality gaps in the supermarkets.

2

3. Justification of the Research Problem

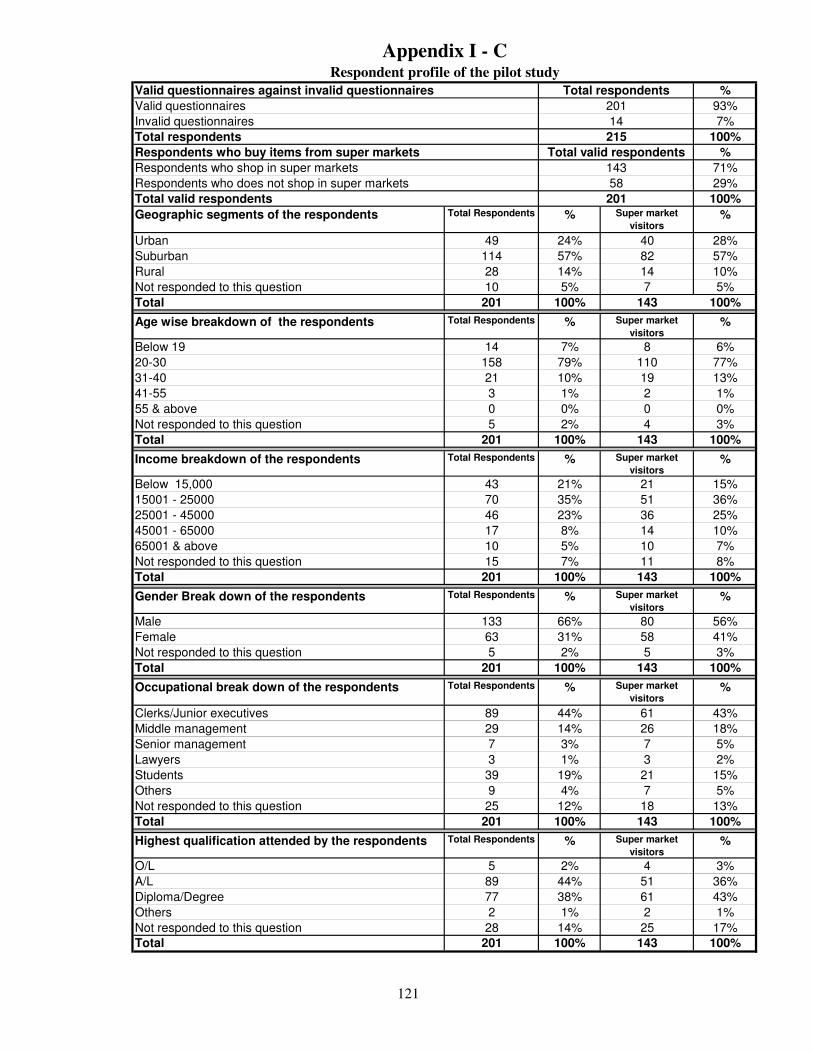

Lack of published empirical studies on the supermarket industry in Sri Lanka deprives

the writer in quoting previous work in providing evidence that the problem stated is in

existence. A pilot study was commissioned for this purpose.

In order to prove that there is a state of non-recognition of service quality in supermarkets

in Sri Lanka, highlighting the existence of service quality gaps would provide sufficient

evidence for the existence of the problem at hand. Out of the three service quality gaps

that the writer mentioned above, the existence of negative service quality gaps (where the

expected service falls short of the perceived service level) might seem to be harmful to

the supermarkets. No supermarket would like to operate with these negative gaps if they

are aware of its existence. On the other hand a “No gap” situation or a “Positive gap”

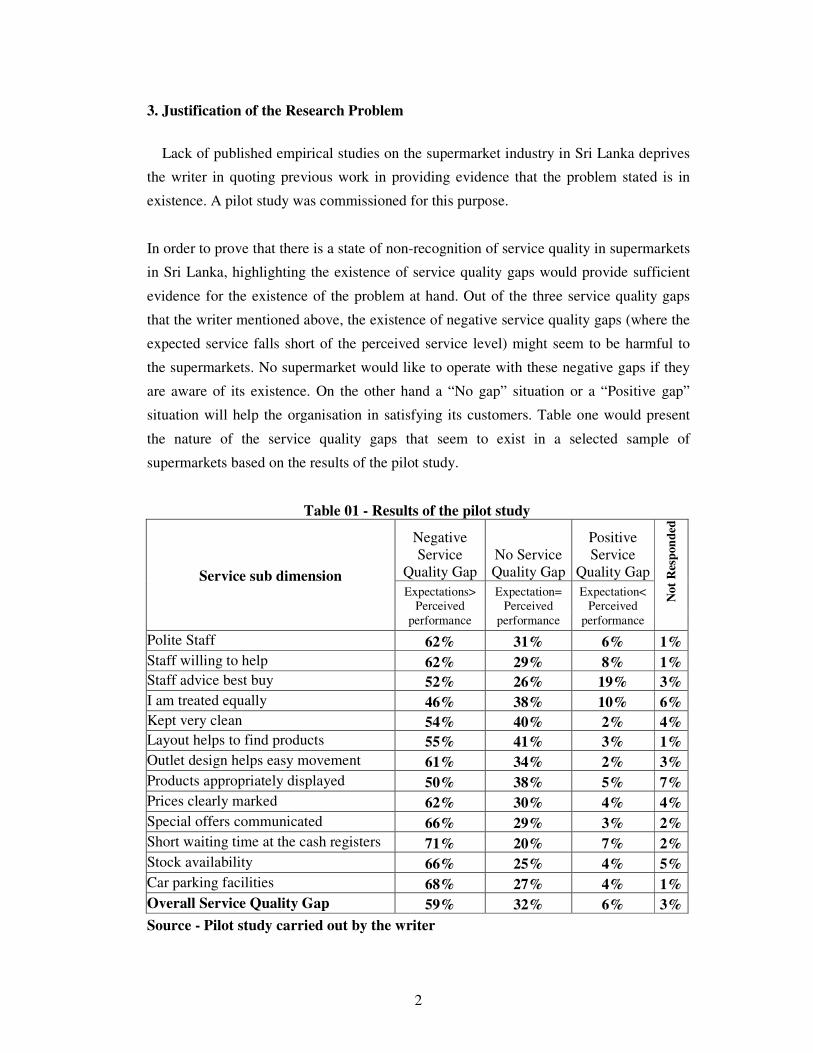

situation will help the organisation in satisfying its customers. Table one would present

the nature of the service quality gaps that seem to exist in a selected sample of

supermarkets based on the results of the pilot study.

Table 01 - Results of the pilot study

Service sub dimension

Negative

Service

Quality Gap

No Service

Quality Gap

Positive

Service

Quality Gap

No

t R

esp

on

ded

Expectations>

Perceived

performance

Expectation=

Perceived

performance

Expectation<

Perceived

performance

Polite Staff 62% 31% 6% 1%

Staff willing to help 62% 29% 8% 1%

Staff advice best buy 52% 26% 19% 3%

I am treated equally 46% 38% 10% 6%

Kept very clean 54% 40% 2% 4%

Layout helps to find products 55% 41% 3% 1%

Outlet design helps easy movement 61% 34% 2% 3%

Products appropriately displayed 50% 38% 5% 7%

Prices clearly marked 62% 30% 4% 4%

Special offers communicated 66% 29% 3% 2%

Short waiting time at the cash registers 71% 20% 7% 2%

Stock availability 66% 25% 4% 5%

Car parking facilities 68% 27% 4% 1%

Overall Service Quality Gap 59% 32% 6% 3%

Source - Pilot study carried out by the writer

3

The above table clearly indicates that almost in all the dimensions tested, more than 50%

of the respondents felt that the perceived performance of the service had fallen short of

their expectations of that service. The overall negative percentage was 59%. Only 6%

felt that the perceived performance encountered was more than their expecatations. 32%

experienced a no gap situation meaning that they were satisfied with the experience when

comparing with their expectations.

When you analyse the above service quality gaps, one could say that if supermarkets

recognise service quality gaps then no supermarket would allow the existence of negative

service quality gaps as it may lead to customer dissatisfaction. This it self proves that the

level of service quality recognition by supermarkets at present is very low.

The reader is requested to refer appendix one A – D of this study for the methodology

used, the sample chosen, the questionnaire used and the detailed quantification of the

service quality gaps of the pilot study.

4. Objectives of the Study

There are four objectives set to achieve in this study. They are as follows;

1) To assess the present service quality recognition levels of the supermarkets, which

sell FMCG products in Sri Lanka, based on the existing techniques used in

measuring service quality and their level of awareness of such gaps.

2) To study the relationship between the recognition of service quality and the

overall satisfaction in asserting their level of influence on the overall satisfaction

of supermarket customers.

3) To ascertain the influence of satisfaction with product quality and prices paid on

the overall satisfaction of supermarket customers.

4) To recommend a process in closing gaps to increase overall satisfaction of

supermarket customers by developing retail strategies.

4

5. Significance of the Study.

The significance of this study is presented from the three points of view as identified

by the writer.

The significance of service quality in the overall satisfaction of supermarket customers.

The significance of the study to the super market operators in Sri Lanka.

The significance of the supermarket industry to the Sri Lankan consumers

In assessing the significance of service quality for the overall satisfaction, literature

clearly points out the significance of service quality in influencing the overall satisfaction

of the customers in terms of the pre purchase evaluation as well as the post purchase

satisfaction of customers. This will be explored in the literature review in detail.

In discussing the significance of the study to the super market operators in Sri Lanka the

following are sited as valid inputs.

The assessment of present service quality recognition levels in the industry would give

the major operators an opportunity to asses their stand in the process. This study will

present techniques in measuring service quality in quantifying the existing gaps. This in

turn would help supermarkets to understand gaps more preciously in finding solutions.

The investigation of the relationship between service quality, product quality and the

prices paid in influencing the overall satisfaction process would help supermarkets to

prioritise those three elements in their strategies as per their influence.

The suggested tools and strategies in closing service quality gaps would allow the

operators in enhancing overall customer satisfaction levels in the industry inducing the

non users to patronise supermarkets for their shopping needs.

In terms of the importance of the supermarket industry to the Sri Lankan consumer, the

following trends would allow the reader to understand its significance.

Lifestyle of the Sri Lankan consumer is fast changing. It is moving away from a

traditional timeless orientation to a more time bound orientation. The large number of

women entering the work force, the increased number of women opting to higher

education has made time, a factor that most Sri Lankans tend to compete today. This has

made convenience, a number one priority among many customers. In this regard the

5

concept of one stop shopping which the supermarkets promote would allow a continuous

growth opportunity for the industry.

The number of supermarkets operating in Sri Lanka in recent times has expanded rapidly.

As per the data available there are approximately 270 supermarket outlets offering FMCG

products in major areas in the country where the super five chains control 75% of the

outlets. The change in government policy in expanding the service facilities in this sector

through restructuring of the market leader SATHOSA, has created precedence a new set

of norms are being imposed on the industry enhancing customer service.

The high-end supermarkets, which traditionally served the higher segments in society, is

moving down to the middle and lower segments having identified there potential. The

entry of the Sentra supermarket chain together with the restructuring of the SATHOSA

chain has brought the concept of discounted super marketing into the country taking super

marketing into the masses.

The above reasons will justify the significance of this study.

6. Scope of the Study

The scope of the study is limited to the retailing supermarket industry, which sells fast

moving consumer goods (FMCG). The qualifying criteria in identifying them would be

outlets, which offer;

Goods to the retail customers for final consumption

Goods which are on self service display

Outlets which sell FMCG goods

Examples of organizations that are involved in this industry would be, Cargills Food City,

Keells Super, Arpico Supercentres, Sentra, Crystals, Sathosa supermarkets & other

regional supermarkets. Other retail outlets, which sell different goods or similar goods

without self-service, will not be included into this study for reasons of manageability. As

an outcome of this study, specific organisations would be able to recognise service quality

gaps and build retail strategies in reducing negative gaps influencing an increase the

overall satisfaction of supermarket customers.

6

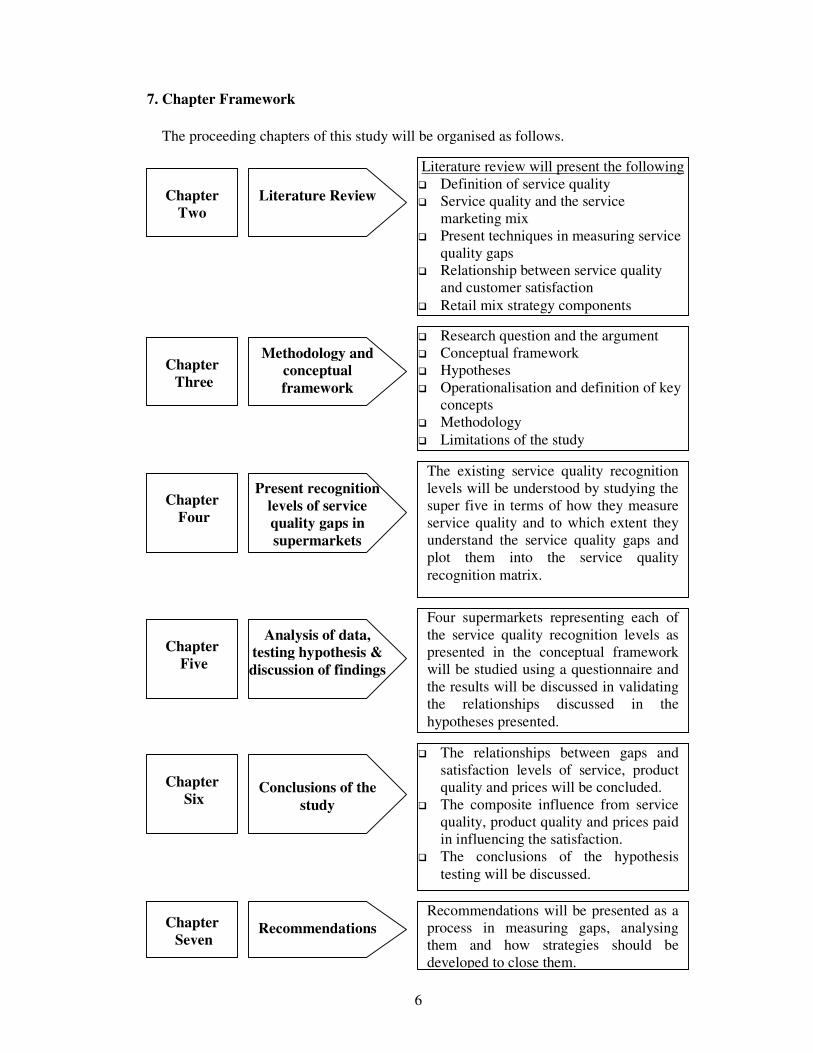

7. Chapter Framework

The proceeding chapters of this study will be organised as follows.

Chapter

Two

Literature review will present the following

� Definition of service quality

� Service quality and the service

marketing mix

� Present techniques in measuring service

quality gaps

� Relationship between service quality

and customer satisfaction

� Retail mix strategy components

Literature Review

Chapter

Three

Methodology and

conceptual

framework

� Research question and the argument

� Conceptual framework

� Hypotheses

� Operationalisation and definition of key

concepts

� Methodology

� Limitations of the study

Chapter

Four

Present recognition

levels of service

quality gaps in

supermarkets

The existing service quality recognition

levels will be understood by studying the

super five in terms of how they measure

service quality and to which extent they

understand the service quality gaps and

plot them into the service quality

recognition matrix.

Chapter

Five

Analysis of data,

testing hypothesis &

discussion of findings

Four supermarkets representing each of

the service quality recognition levels as

presented in the conceptual framework

will be studied using a questionnaire and

the results will be discussed in validating

the relationships discussed in the

hypotheses presented.

Chapter

Six

Conclusions of the

study

� The relationships between gaps and

satisfaction levels of service, product

quality and prices will be concluded.

� The composite influence from service

quality, product quality and prices paid

in influencing the satisfaction.

� The conclusions of the hypothesis

testing will be discussed.

Chapter

Seven

Recommendations

Recommendations will be presented as a

process in measuring gaps, analysing

them and how strategies should be

developed to close them.

7

Chapter II

LITERATURE REVIEW

1. Introduction

The literature review is presented in several sections in this chapter. Section two will

examine the definition of service quality. Section three will identify the elements of the

service marketing mix that would fall under service quality. Section four will present

knowledge of the existing dimensions & techniques used in measuring service quality in

general for the service industry and in particularly for the selected retailing supermarket

industry. This section will also discuss how service quality could be monitored over time

very briefly. Section five will review existing knowledge on the relationships between

service quality and customer satisfaction and other influences of customer satisfaction.

Finally section six will look at the components of the retail mix strategies in getting more

insights in building retail strategies.

2. Definition of Service Quality

The following are some definitions given by some researchers who have pioneered the

service quality theory.

The perceive service quality will be the result of an evaluation process in which

customers compare their perceptions of service delivery and its out come against what

they expect ” (Christian Gronroos : 1984)

The discrepancy between customer expectations and perceptions of service

(Parasuraman, Zeithamal and Berry: 1988)

A measure of how well the service level (perception) matches customer expectation.

Delivering quality service means conforming to customer expectations on a

continuous basis. (Lewis and Booms: 1989).

The above definitions clearly identify two components of service quality. They are

1) Expectations of the service

2) Perceived performance of that service encounter.

8

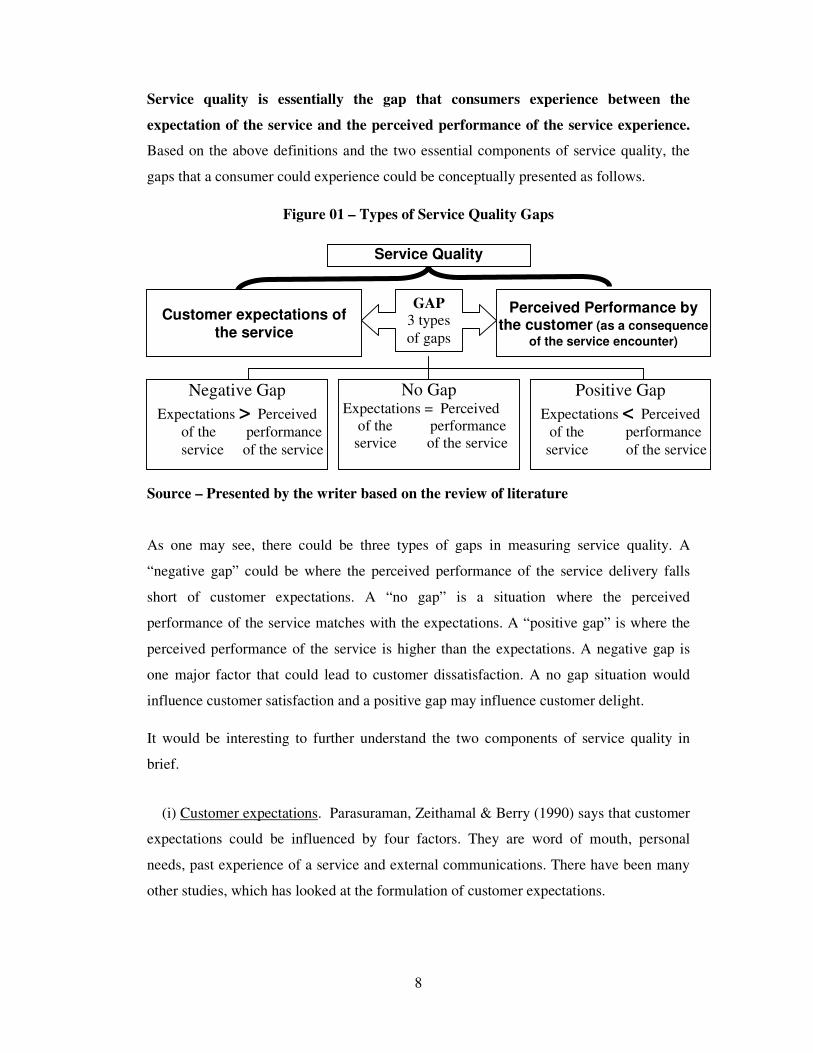

Service quality is essentially the gap that consumers experience between the

expectation of the service and the perceived performance of the service experience.

Based on the above definitions and the two essential components of service quality, the

gaps that a consumer could experience could be conceptually presented as follows.

Figure 01 – Types of Service Quality Gaps

Source – Presented by the writer based on the review of literature

As one may see, there could be three types of gaps in measuring service quality. A

“negative gap” could be where the perceived performance of the service delivery falls

short of customer expectations. A “no gap” is a situation where the perceived

performance of the service matches with the expectations. A “positive gap” is where the

perceived performance of the service is higher than the expectations. A negative gap is

one major factor that could lead to customer dissatisfaction. A no gap situation would

influence customer satisfaction and a positive gap may influence customer delight.

It would be interesting to further understand the two components of service quality in

brief.

(i) Customer expectations. Parasuraman, Zeithamal & Berry (1990) says that customer

expectations could be influenced by four factors. They are word of mouth, personal

needs, past experience of a service and external communications. There have been many

other studies, which has looked at the formulation of customer expectations.

Customer expectations of the service

Perceived Performance by the customer (as a consequence

of the service encounter)

Service Quality

GAP

3 types

of gaps

Negative Gap

Expectations > Perceived

of the performance

service of the service

No Gap Expectations = Perceived

of the performance

service of the service

Positive Gap

Expectations < Perceived

of the performance

service of the service

9

(ii) Perceived performance. Bitner (1994) says that customer’s perceived performance is

created through the “moments of truths” that occur whenever the customer encounters the

service organization. Through such moments of truth encounters, perceptions of service

accumulate over time leading to the determination of service quality gaps by a

comparison of the perceived performance against the expectations.

Service quality is an important issue due to many reasons.

The first aspect would be that over half of our gross domestic production is contributed

from the service industry. This is also a trend world over.

Secondly almost all organizations compete to some degree on the basis of service.

Thirdly superior service quality is proving to be a winning strategy in gaining competitive

advantage. The importance of the concept is self-evident.

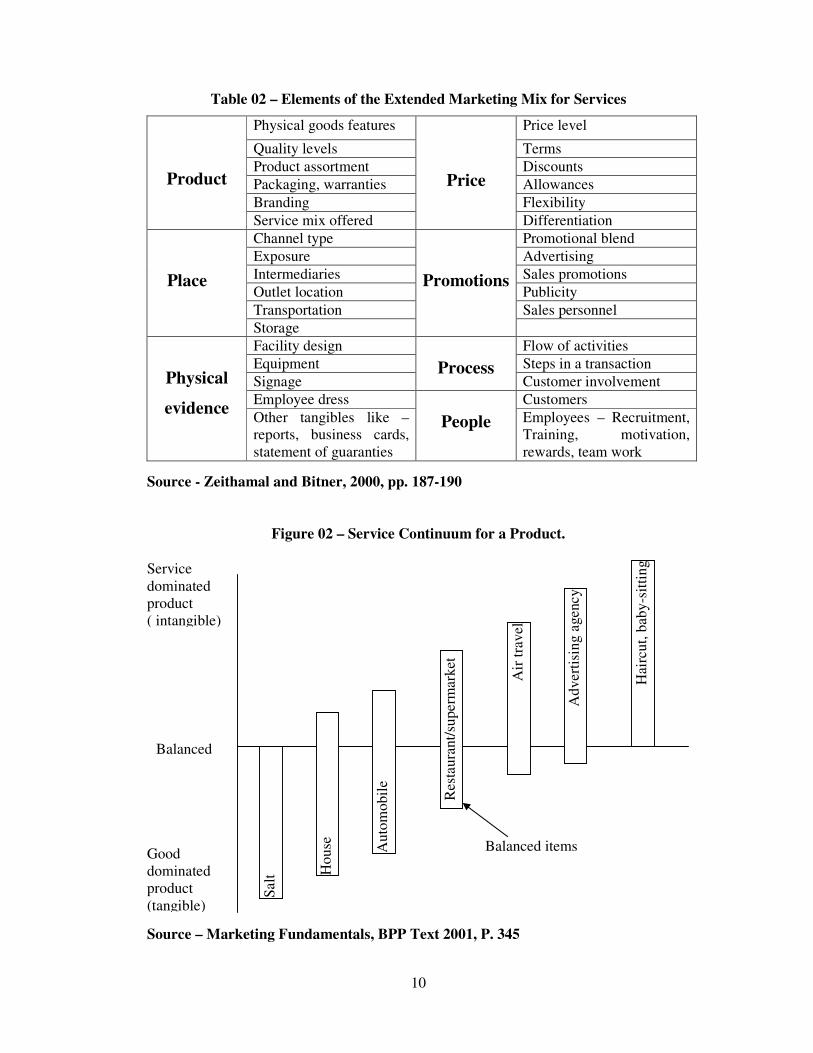

3. Service Quality and the Service Marketing Mix.

In many literature on service, it has been argued that the four “P”s of the traditional

marketing mix does not reflect the entirety of the service situation, as a service is

differentiated from a physical product with features such as intangibility, perishability,

variation of the service delivery and inseparability. The traditional marketing mix has

been extended to seven “P”s for service situations. Zeithaml and Bitner (2000) present the

elements of the extended marketing mix for services as follows. Please refer table two in

page ten.

In determining which elements of the service marketing mix is represented by service

quality, one may have to understand the nature of the service on offer it self. Levitt says

That there is no such thing such as service industries. There are only industries whose

service components are greater or less than those of other industries. Every body is in

service. (Levitt : 1972)

Based on Levitt’s argument the service continuum was developed which indicates

different degrees of tangibility/intangibility of a product. Please refer figure two in page

ten for the service continuum of a product.

10

Table 02 – Elements of the Extended Marketing Mix for Services

Product

Physical goods features

Price

Price level

Quality levels Terms

Product assortment Discounts

Packaging, warranties Allowances

Branding Flexibility

Service mix offered Differentiation

Place

Channel type

Promotions

Promotional blend

Exposure Advertising

Intermediaries Sales promotions

Outlet location Publicity

Transportation Sales personnel

Storage

Physical

evidence

Facility design

Process

Flow of activities

Equipment Steps in a transaction

Signage Customer involvement

Employee dress

People

Customers

Other tangibles like –

reports, business cards,

statement of guaranties

Employees – Recruitment,

Training, motivation,

rewards, team work

Source - Zeithamal and Bitner, 2000, pp. 187-190

Figure 02 – Service Continuum for a Product.

Source – Marketing Fundamentals, BPP Text 2001, P. 345

Service

dominated

product

( intangible)

Good

dominated

product

(tangible)

Balanced

Salt

Ho

use

Au

tom

ob

ile

Res

tau

ran

t/su

perm

ark

et

Air

tra

vel

Ad

vert

isin

g a

gen

cy

Hai

rcu

t, b

aby

-sit

tin

g

Balanced items

11

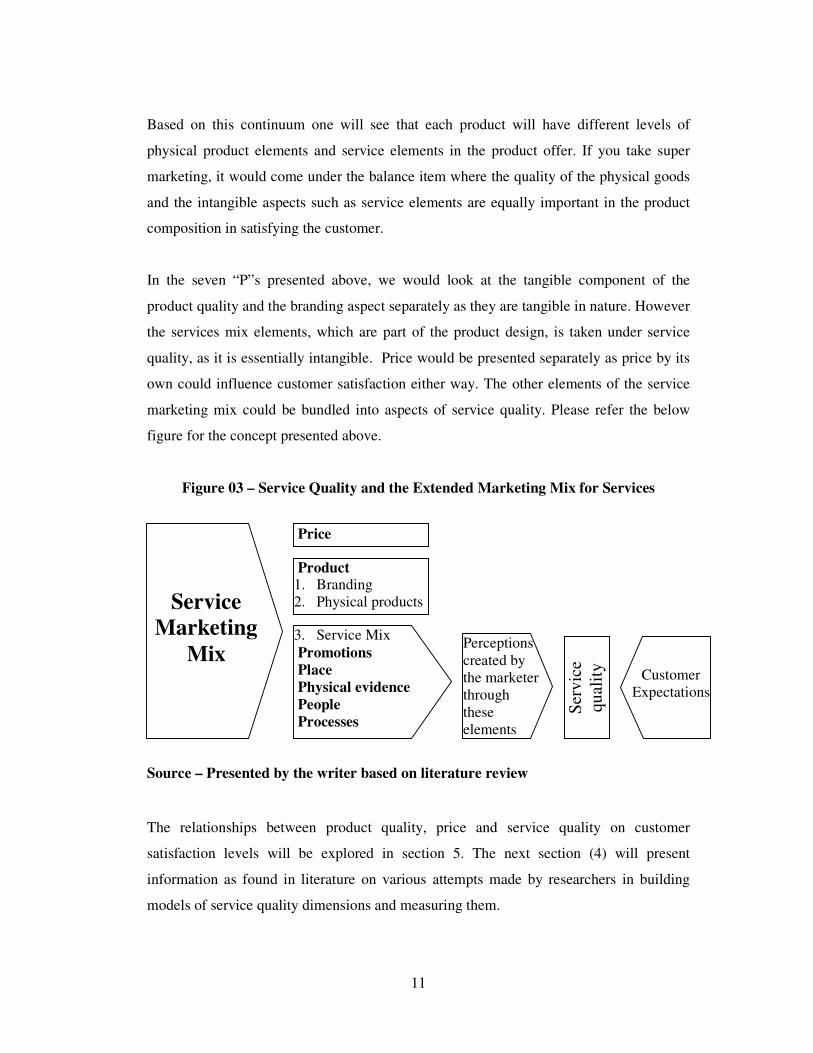

Based on this continuum one will see that each product will have different levels of

physical product elements and service elements in the product offer. If you take super

marketing, it would come under the balance item where the quality of the physical goods

and the intangible aspects such as service elements are equally important in the product

composition in satisfying the customer.

In the seven “P”s presented above, we would look at the tangible component of the

product quality and the branding aspect separately as they are tangible in nature. However

the services mix elements, which are part of the product design, is taken under service

quality, as it is essentially intangible. Price would be presented separately as price by its

own could influence customer satisfaction either way. The other elements of the service

marketing mix could be bundled into aspects of service quality. Please refer the below

figure for the concept presented above.

Figure 03 – Service Quality and the Extended Marketing Mix for Services

Source – Presented by the writer based on literature review

The relationships between product quality, price and service quality on customer

satisfaction levels will be explored in section 5. The next section (4) will present

information as found in literature on various attempts made by researchers in building

models of service quality dimensions and measuring them.

Product 1. Branding

2. Physical products

Price

Service

Marketing

Mix 3. Service Mix

Promotions

Place

Physical evidence

People

Processes

Ser

vic

e

qu

alit

y

Customer

Expectations

Perceptions

created by

the marketer

through

these

elements

12

4. Techniques in Measuring Service Quality

In this section the writer will examine the dimensions and techniques used to

measuring service quality. Also literature, which discusses how service quality measures

are monitored over time, are also explored.

There are many methodologies suggested in literature in measuring service quality and

service quality dimensions. The origins of the service quality theory lie in the literature

presented on product quality and customer satisfaction. However in recent times there had

been much research on service quality. It is said that service quality is the most

researched topic to date. The following are some of the important elements of the service

quality theories presented by different researchers. They are as follows

(i) The Nordic Model by Gronroos in 1984.

This is one of the earliest models of service quality presented in 1984 by Christain

Gronroos. It essentially highlights two service dimensions in measuring service quality.

The following diagram will elaborate this further.

Figure 04 – Nordic Model of Perceived Service Quality

Source – Gronroos, 1982, p. 79 (adopted)

As presented above, the Nordic model presents service quality as the interaction between

expected service and the perceived performance of the service. The gaps are similar to

that presented in the definition.

Expected Service Perceived performance

of the service Perceived Service Quality

Technical Quality

� Technical solutions

� Know how

� Computerized systems

� Machines

Functional Quality � Attitudes, behaviour

� Customer contacts

� Accessibility

� Appearances

� Service mindness

� Internal relations

13

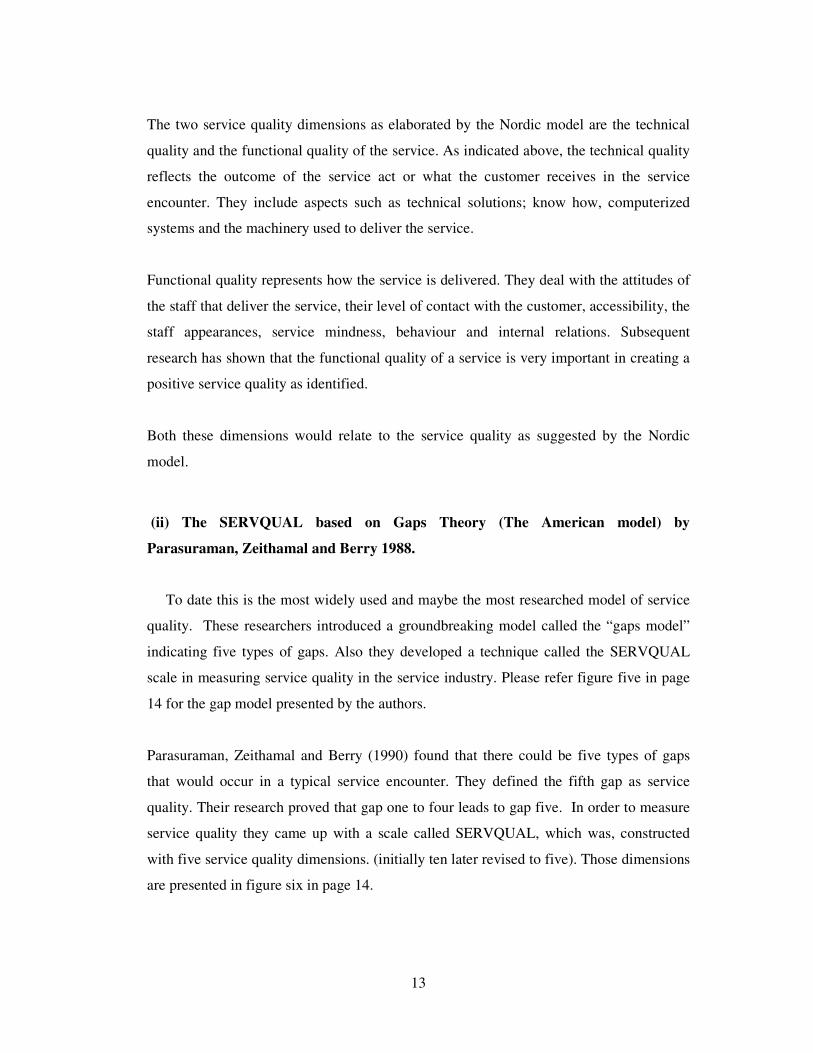

The two service quality dimensions as elaborated by the Nordic model are the technical

quality and the functional quality of the service. As indicated above, the technical quality

reflects the outcome of the service act or what the customer receives in the service

encounter. They include aspects such as technical solutions; know how, computerized

systems and the machinery used to deliver the service.

Functional quality represents how the service is delivered. They deal with the attitudes of

the staff that deliver the service, their level of contact with the customer, accessibility, the

staff appearances, service mindness, behaviour and internal relations. Subsequent

research has shown that the functional quality of a service is very important in creating a

positive service quality as identified.

Both these dimensions would relate to the service quality as suggested by the Nordic

model.

(ii) The SERVQUAL based on Gaps Theory (The American model) by

Parasuraman, Zeithamal and Berry 1988.

To date this is the most widely used and maybe the most researched model of service

quality. These researchers introduced a groundbreaking model called the “gaps model”

indicating five types of gaps. Also they developed a technique called the SERVQUAL

scale in measuring service quality in the service industry. Please refer figure five in page

14 for the gap model presented by the authors.

Parasuraman, Zeithamal and Berry (1990) found that there could be five types of gaps

that would occur in a typical service encounter. They defined the fifth gap as service

quality. Their research proved that gap one to four leads to gap five. In order to measure

service quality they came up with a scale called SERVQUAL, which was, constructed

with five service quality dimensions. (initially ten later revised to five). Those dimensions

are presented in figure six in page 14.

14

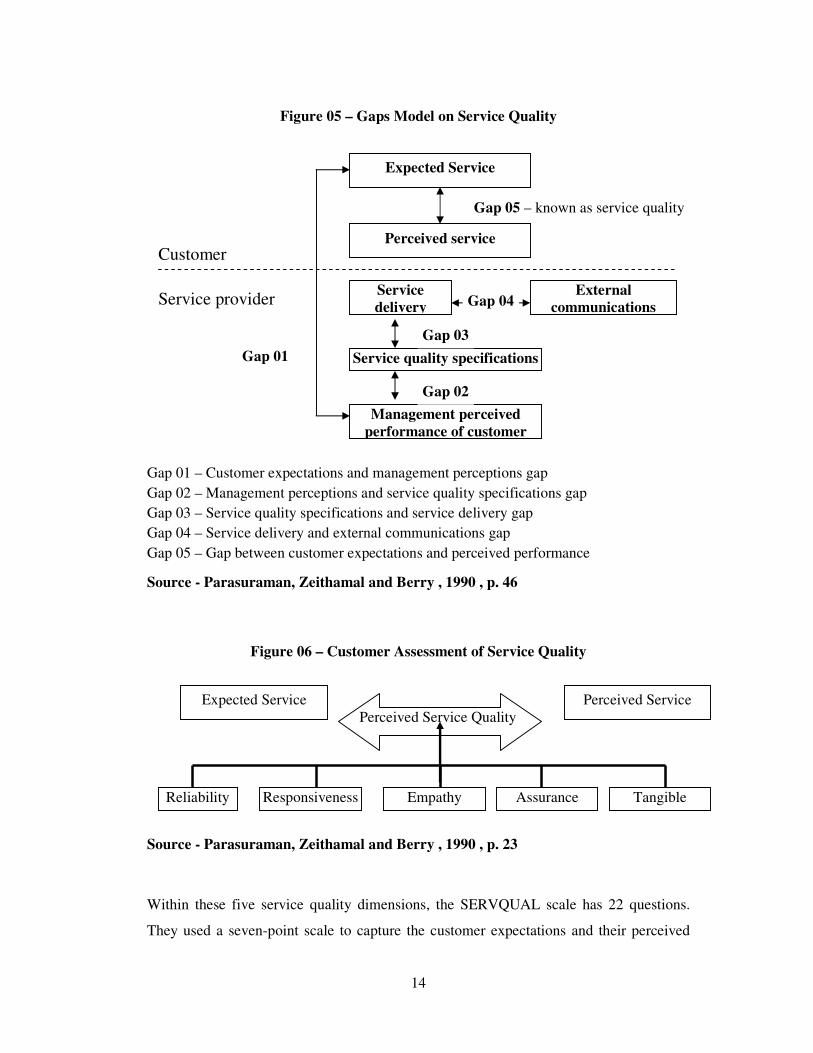

Figure 05 – Gaps Model on Service Quality

Gap 01 – Customer expectations and management perceptions gap

Gap 02 – Management perceptions and service quality specifications gap

Gap 03 – Service quality specifications and service delivery gap

Gap 04 – Service delivery and external communications gap

Gap 05 – Gap between customer expectations and perceived performance

Source - Parasuraman, Zeithamal and Berry , 1990 , p. 46

Figure 06 – Customer Assessment of Service Quality

Source - Parasuraman, Zeithamal and Berry , 1990 , p. 23

Within these five service quality dimensions, the SERVQUAL scale has 22 questions.

They used a seven-point scale to capture the customer expectations and their perceived

Expected Service Perceived Service

Perceived Service Quality

Reliability Responsiveness Empathy Assurance Tangible

Expected Service

Perceived service

Gap 05 – known as service quality

Customer

Service provider Service

delivery

Service quality specifications

Management perceived

performance of customer

External

communications Gap 04

Gap 02

Gap 03

Gap 01

15

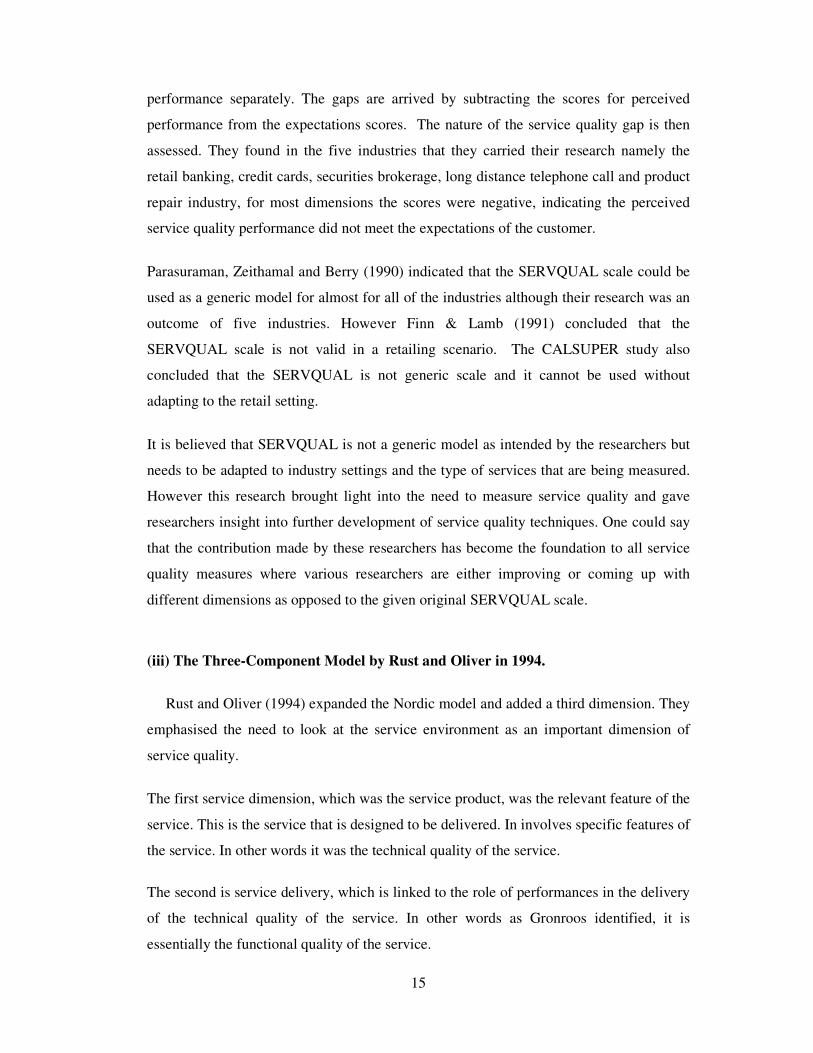

performance separately. The gaps are arrived by subtracting the scores for perceived

performance from the expectations scores. The nature of the service quality gap is then

assessed. They found in the five industries that they carried their research namely the

retail banking, credit cards, securities brokerage, long distance telephone call and product

repair industry, for most dimensions the scores were negative, indicating the perceived

service quality performance did not meet the expectations of the customer.

Parasuraman, Zeithamal and Berry (1990) indicated that the SERVQUAL scale could be

used as a generic model for almost for all of the industries although their research was an

outcome of five industries. However Finn & Lamb (1991) concluded that the

SERVQUAL scale is not valid in a retailing scenario. The CALSUPER study also

concluded that the SERVQUAL is not generic scale and it cannot be used without

adapting to the retail setting.

It is believed that SERVQUAL is not a generic model as intended by the researchers but

needs to be adapted to industry settings and the type of services that are being measured.

However this research brought light into the need to measure service quality and gave

researchers insight into further development of service quality techniques. One could say

that the contribution made by these researchers has become the foundation to all service

quality measures where various researchers are either improving or coming up with

different dimensions as opposed to the given original SERVQUAL scale.

(iii) The Three-Component Model by Rust and Oliver in 1994.

Rust and Oliver (1994) expanded the Nordic model and added a third dimension. They

emphasised the need to look at the service environment as an important dimension of

service quality.

The first service dimension, which was the service product, was the relevant feature of the

service. This is the service that is designed to be delivered. In involves specific features of

the service. In other words it was the technical quality of the service.

The second is service delivery, which is linked to the role of performances in the delivery

of the technical quality of the service. In other words as Gronroos identified, it is

essentially the functional quality of the service.

16

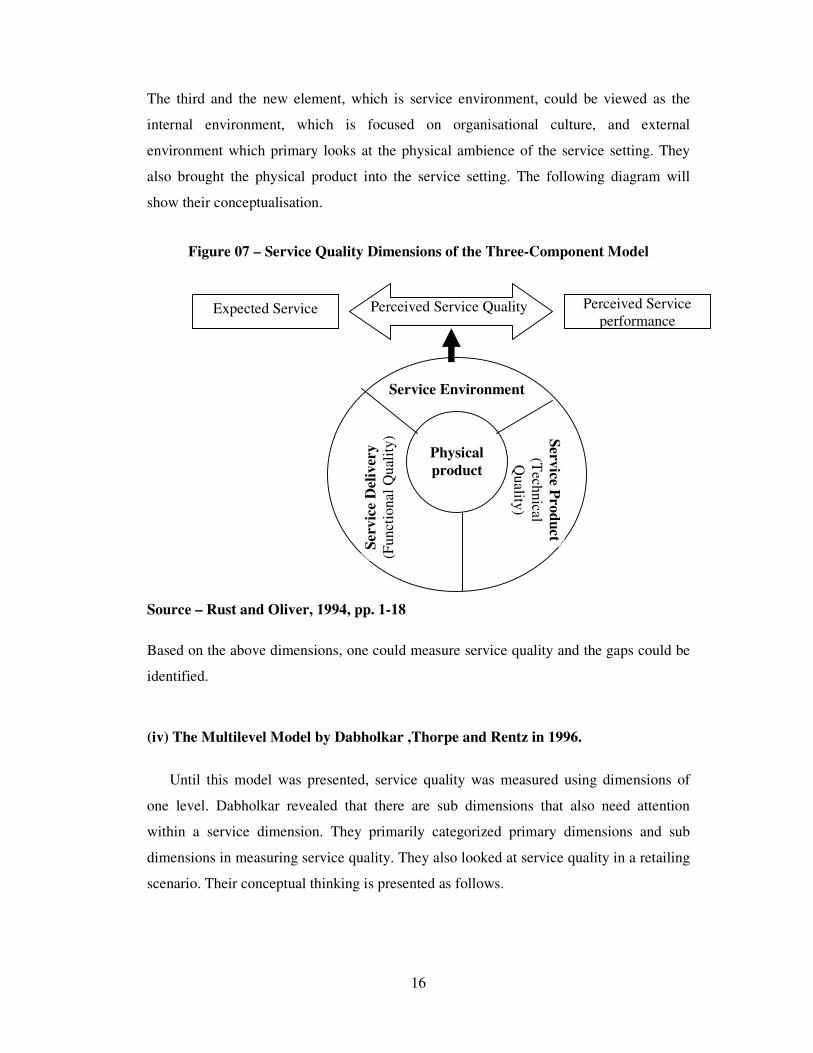

The third and the new element, which is service environment, could be viewed as the

internal environment, which is focused on organisational culture, and external

environment which primary looks at the physical ambience of the service setting. They

also brought the physical product into the service setting. The following diagram will

show their conceptualisation.

Figure 07 – Service Quality Dimensions of the Three-Component Model

Source – Rust and Oliver, 1994, pp. 1-18

Based on the above dimensions, one could measure service quality and the gaps could be

identified.

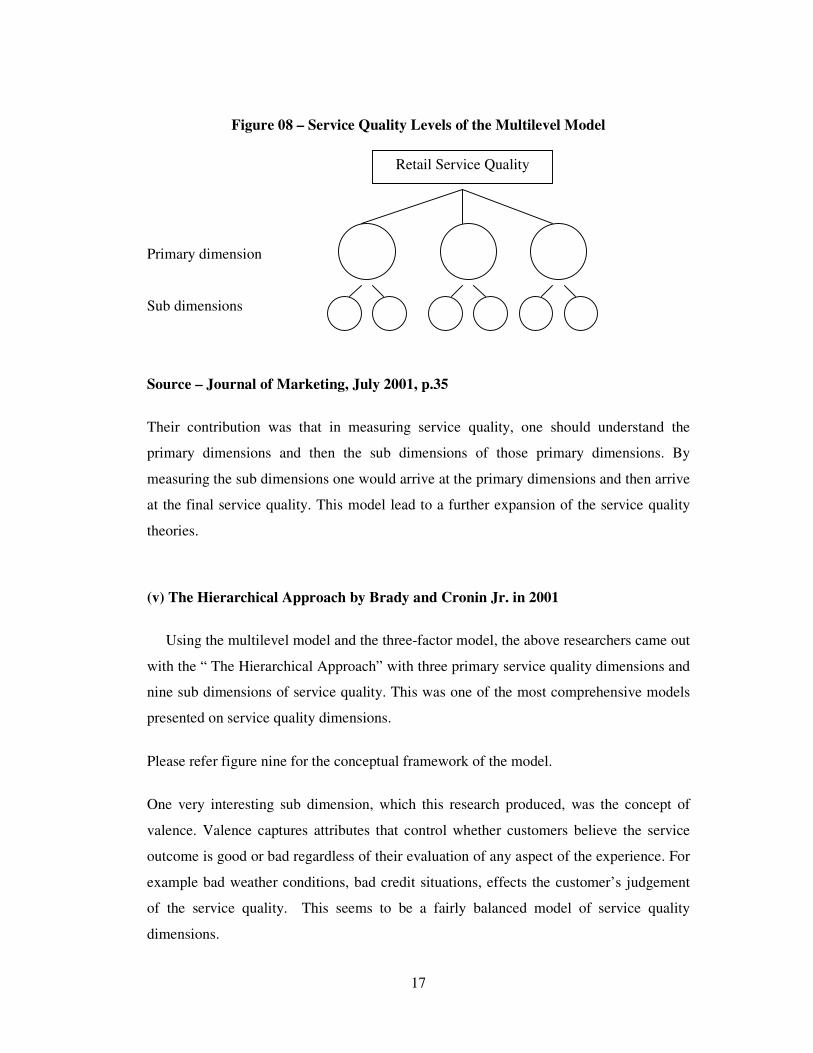

(iv) The Multilevel Model by Dabholkar ,Thorpe and Rentz in 1996.

Until this model was presented, service quality was measured using dimensions of

one level. Dabholkar revealed that there are sub dimensions that also need attention

within a service dimension. They primarily categorized primary dimensions and sub

dimensions in measuring service quality. They also looked at service quality in a retailing

scenario. Their conceptual thinking is presented as follows.

Expected Service Perceived Service

performance

Service Environment

Perceived Service Quality

Serv

ice

Del

iver

y

(Fu

nct

ion

al

Qu

alit

y)

Serv

ice Pro

du

ct

(Tech

nica

l

Qu

ality

)

Physical

product

17

Figure 08 – Service Quality Levels of the Multilevel Model

Primary dimension

Sub dimensions

Source – Journal of Marketing, July 2001, p.35

Their contribution was that in measuring service quality, one should understand the

primary dimensions and then the sub dimensions of those primary dimensions. By

measuring the sub dimensions one would arrive at the primary dimensions and then arrive

at the final service quality. This model lead to a further expansion of the service quality

theories.

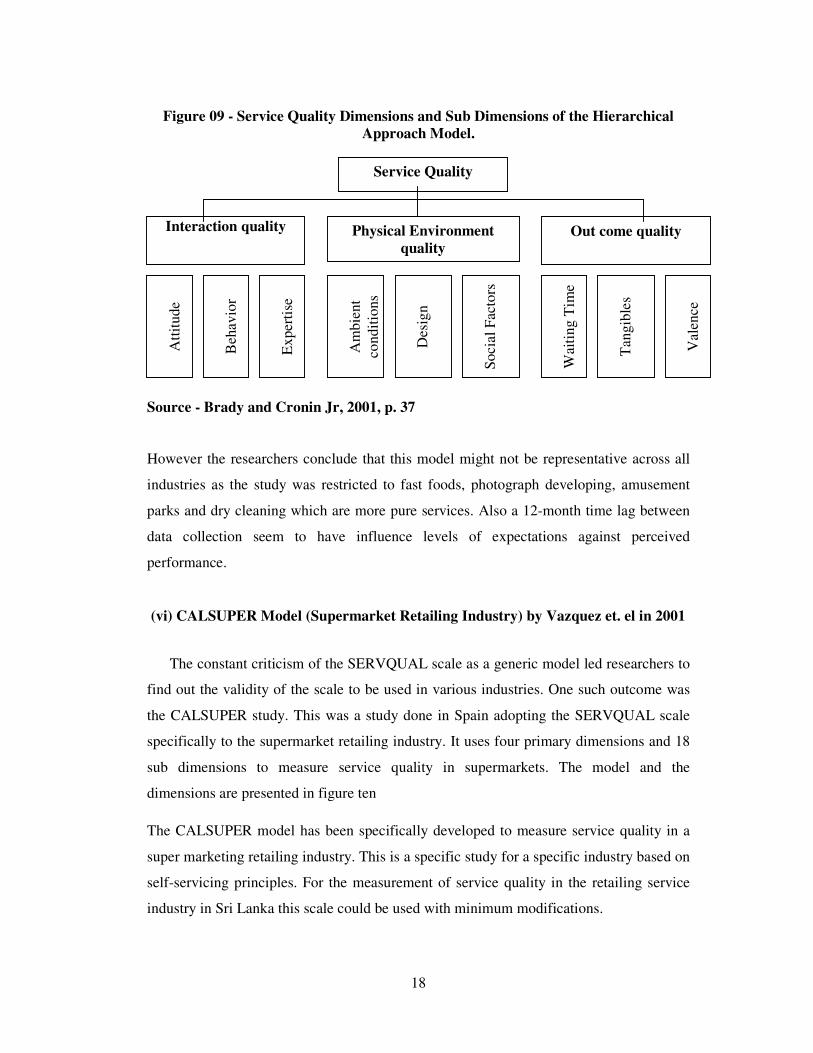

(v) The Hierarchical Approach by Brady and Cronin Jr. in 2001

Using the multilevel model and the three-factor model, the above researchers came out

with the “ The Hierarchical Approach” with three primary service quality dimensions and

nine sub dimensions of service quality. This was one of the most comprehensive models

presented on service quality dimensions.

Please refer figure nine for the conceptual framework of the model.

One very interesting sub dimension, which this research produced, was the concept of

valence. Valence captures attributes that control whether customers believe the service

outcome is good or bad regardless of their evaluation of any aspect of the experience. For

example bad weather conditions, bad credit situations, effects the customer’s judgement

of the service quality. This seems to be a fairly balanced model of service quality

dimensions.

Retail Service Quality

18

Figure 09 - Service Quality Dimensions and Sub Dimensions of the Hierarchical

Approach Model.

.

Source - Brady and Cronin Jr, 2001, p. 37

However the researchers conclude that this model might not be representative across all

industries as the study was restricted to fast foods, photograph developing, amusement

parks and dry cleaning which are more pure services. Also a 12-month time lag between

data collection seem to have influence levels of expectations against perceived

performance.

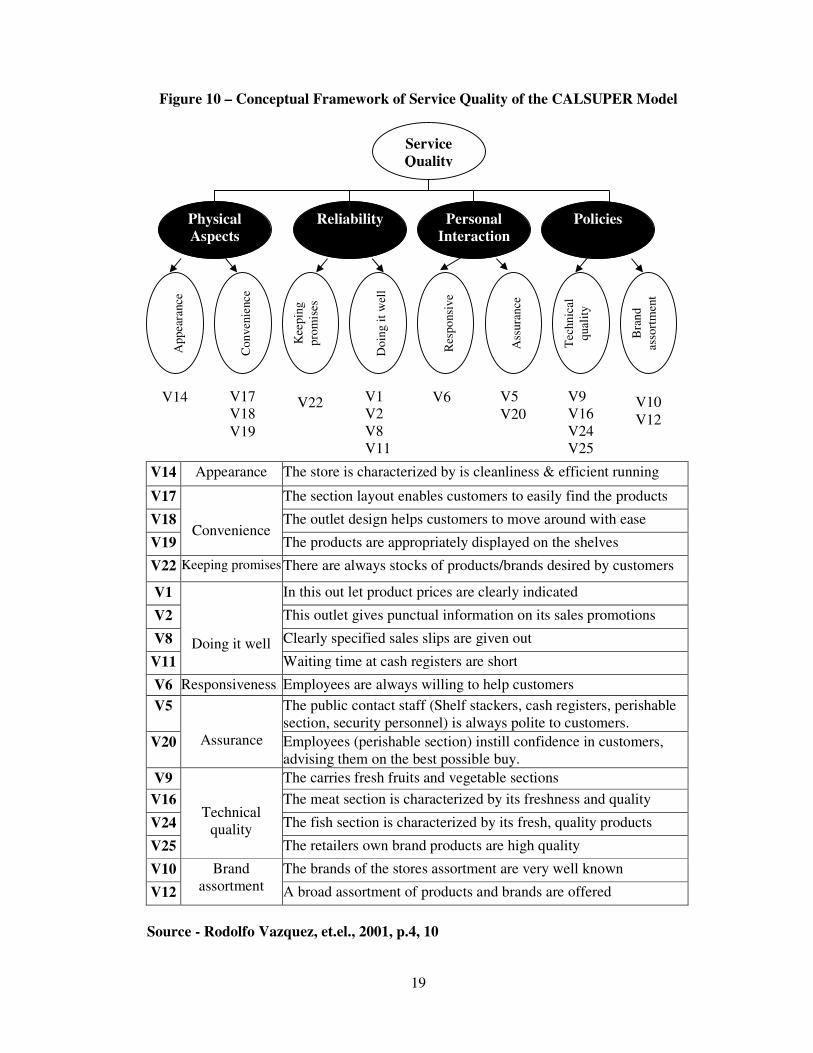

(vi) CALSUPER Model (Supermarket Retailing Industry) by Vazquez et. el in 2001

The constant criticism of the SERVQUAL scale as a generic model led researchers to

find out the validity of the scale to be used in various industries. One such outcome was

the CALSUPER study. This was a study done in Spain adopting the SERVQUAL scale

specifically to the supermarket retailing industry. It uses four primary dimensions and 18

sub dimensions to measure service quality in supermarkets. The model and the

dimensions are presented in figure ten

The CALSUPER model has been specifically developed to measure service quality in a

super marketing retailing industry. This is a specific study for a specific industry based on

self-servicing principles. For the measurement of service quality in the retailing service

industry in Sri Lanka this scale could be used with minimum modifications.

Interaction quality Physical Environment

quality

Out come quality

Att

itu

de

Beh

av

ior

Ex

per

tise

Am

bie

nt

con

dit

ion

s

Des

ign

So

cia

l F

acto

rs

Wai

tin

g T

ime

Tan

gib

les

Vale

nce

Service Quality

19

Figure 10 – Conceptual Framework of Service Quality of the CALSUPER Model

V14 Appearance The store is characterized by is cleanliness & efficient running

V17

Convenience

The section layout enables customers to easily find the products

V18 The outlet design helps customers to move around with ease

V19 The products are appropriately displayed on the shelves

V22 Keeping promises There are always stocks of products/brands desired by customers

V1

Doing it well

In this out let product prices are clearly indicated

V2 This outlet gives punctual information on its sales promotions

V8 Clearly specified sales slips are given out

V11 Waiting time at cash registers are short

V6 Responsiveness Employees are always willing to help customers

V5

Assurance

The public contact staff (Shelf stackers, cash registers, perishable

section, security personnel) is always polite to customers.

V20 Employees (perishable section) instill confidence in customers,

advising them on the best possible buy.

V9

Technical

quality

The carries fresh fruits and vegetable sections

V16 The meat section is characterized by its freshness and quality

V24 The fish section is characterized by its fresh, quality products

V25 The retailers own brand products are high quality

V10 Brand

assortment

The brands of the stores assortment are very well known

V12 A broad assortment of products and brands are offered

Source - Rodolfo Vazquez, et.el., 2001, p.4, 10

Physical

Aspects

Reliability

Personal

Interaction

Policies

Service

Quality A

pp

eara

nce

Co

nv

enie

nce

Kee

pin

g

pro

mis

es

Do

ing i

t w

ell

Res

po

nsi

ve

Ass

ura

nce

Tec

hn

ical

qual

ity

Bra

nd

asso

rtm

ent

V14 V17

V18

V19

V22 V1

V2

V8

V11

V6 V5

V20

V9

V16

V24

V25

V10

V12

20

(vi) Others

There were also other methods introduced such as the SERPERF by Cronin and Taylor

(1992) using direct measures to what extent customers consider their perceptions of

performances of the service to be superior, similar or inferior to the expected service.

The above are some methods available for service organisations in measuring service

quality.

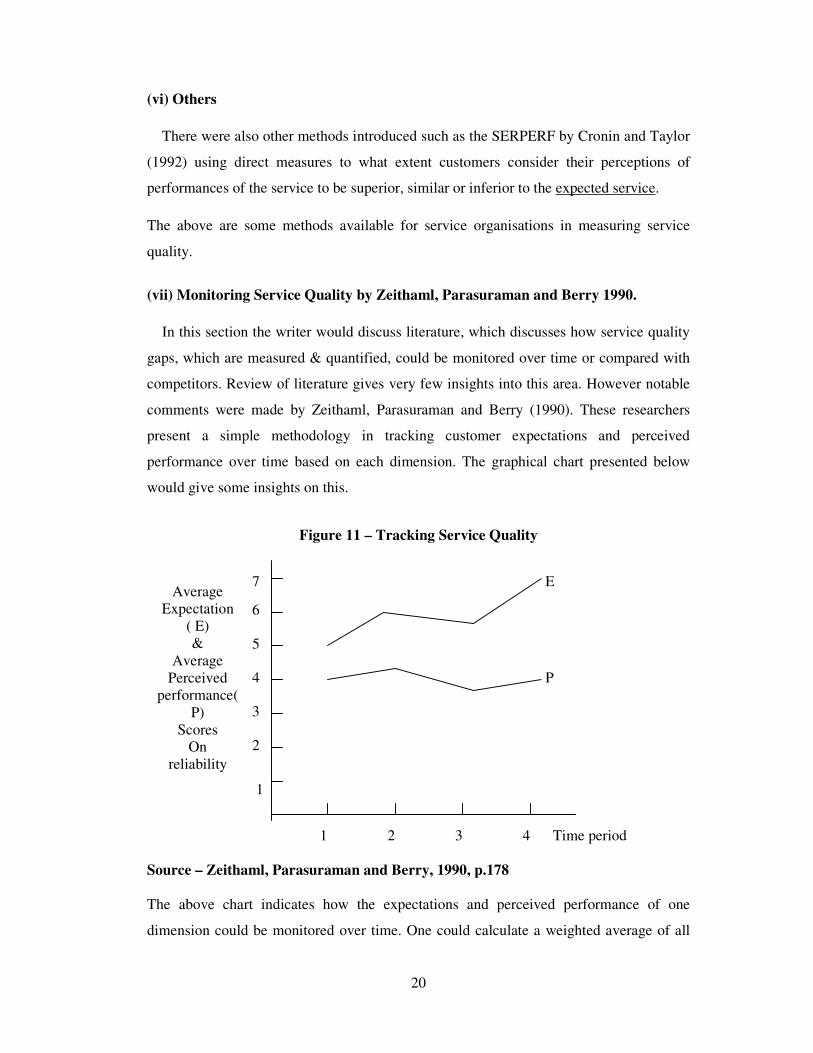

(vii) Monitoring Service Quality by Zeithaml, Parasuraman and Berry 1990.

In this section the writer would discuss literature, which discusses how service quality

gaps, which are measured & quantified, could be monitored over time or compared with

competitors. Review of literature gives very few insights into this area. However notable

comments were made by Zeithaml, Parasuraman and Berry (1990). These researchers

present a simple methodology in tracking customer expectations and perceived

performance over time based on each dimension. The graphical chart presented below

would give some insights on this.

Figure 11 – Tracking Service Quality

1

Source – Zeithaml, Parasuraman and Berry, 1990, p.178

The above chart indicates how the expectations and perceived performance of one

dimension could be monitored over time. One could calculate a weighted average of all

2

3

4

5

6

7 Average

Expectation

( E)

&

Average

Perceived

performance(

P)

Scores

On

reliability

Time period 1 2 3 4

P

E

21

the dimensions and monitor the change every time a measure is made on service quality.

By doing this, organisations would be able to monitor how expectations change over time

as well as perceived performance of the service experience. Also this would be very

useful in monitoring the effectiveness of any retail strategies implemented and correcting

any negative service quality gaps, which was identified, by a previous measure of service

quality. It would also be an effective tool for performance measurement over time.

Similarly one could take the overall scores and plot it against their immediate

competitors. This would give insights in how one is standing against other competitive

retailing supermarkets.

5. Service Quality , Product quality, Prices and Customer Satisfaction

In this section, our attention would be to review literature, which discusses the

relationship between service quality and customer satisfaction. In other words what is the

significance of service quality in the customer satisfaction process. In determining this the

influence from product quality and prices paid for customer satisfaction process will also

be explored for completeness sake. As a prelude some definitions of customer

satisfaction are explored below.

As noted by Oliver (1993), satisfaction is derived from the Latin word “satis” (which

means enough) and “facere” (which means to do or make). The related word is

“satiation” which loosely means “enough” or “enough to excess”. This term implies that

satisfaction refers to a fulfillment response. Based on above, Oliver (1997) defines

satisfaction as follows

Satisfaction is the customer’s fulfillment response. It is a judgment that a product or

service feature, or the product or service itself, provides a pleasurable level of

consumption – related fulfillment. (Oliver:1997:85)

As per Oliver, satisfaction is the customer’s evaluation of a product or service in terms of

whether that product or service has met their needs and expectations.

Fournier & Glen (1999) concluded that the above process of satisfaction was based on the

paradigm of “Comparison Standards”. They called this the CS Paradigm. According to

them the CS paradigm basically states that consumers hold pre consumption product

standards, observe product performance, compare performance with their standards, form

22

confirmation or disconfirmation perceptions, combine these perceived performance with

standard levels and then form summary satisfaction judgements.

Fournier & Glen (1999) brings out a new paradigm on consumer satisfaction called the

balancing paradigm, which looks at a more holistic, context dependent and dynamic

process of satisfaction. They say that it is a multi model, multi modal blend of

motivations, cognitions, emotions and meanings embedded in socio cultural settings,

which transforms during progressive and regressive consumer-product interactions. This

brings light that customer satisfaction is more than a mere comparison between pre

consumption standards (expectations) and perceived performance.

Oliver (1989) expanded the customer satisfaction theory as a consumer experience. He

conceptualised this experience as a combination of “satisfaction as contentment”,

“satisfaction as surprise”, “satisfaction as pleasure”, and “satisfaction as relief”.

Pine and Gilmore (1998) in their ground breaking article also concluded that today

customers are mostly looking for experiences and elaborated the characteristics of such

experiences in terms of four realms. Today most customer satisfaction theories present

customer satisfaction as a process rather than a mere activity of fulfilment.

In turning our attention to the relationships between service quality and customer

satisfaction, the work of Zeithaml and Bitner ( 2000) needs to be highlighted. They

presented a model in depicting the relationship between satisfaction with service quality

and customer satisfaction and points out that product (Physical) quality and prices paid

are also important variables in the customer satisfaction process. Please refer figure 12 for

their model. They acknowledge the CS paradigm where customers form expectations of

preconceived notions of product quality, expectations of value and expectations of service

standards and compare their perceived performance with those in forming conclusions.

Their attention was mainly on the service quality whereby the comparison of service

expectations and perceived performance of the service, was instrumental in formulating

the perceived service quality. While highlighting product quality and price, Zeithaml and

Bitner (1990) also concluded that situational factors and personal factors could also affect

the customer satisfaction process.

23

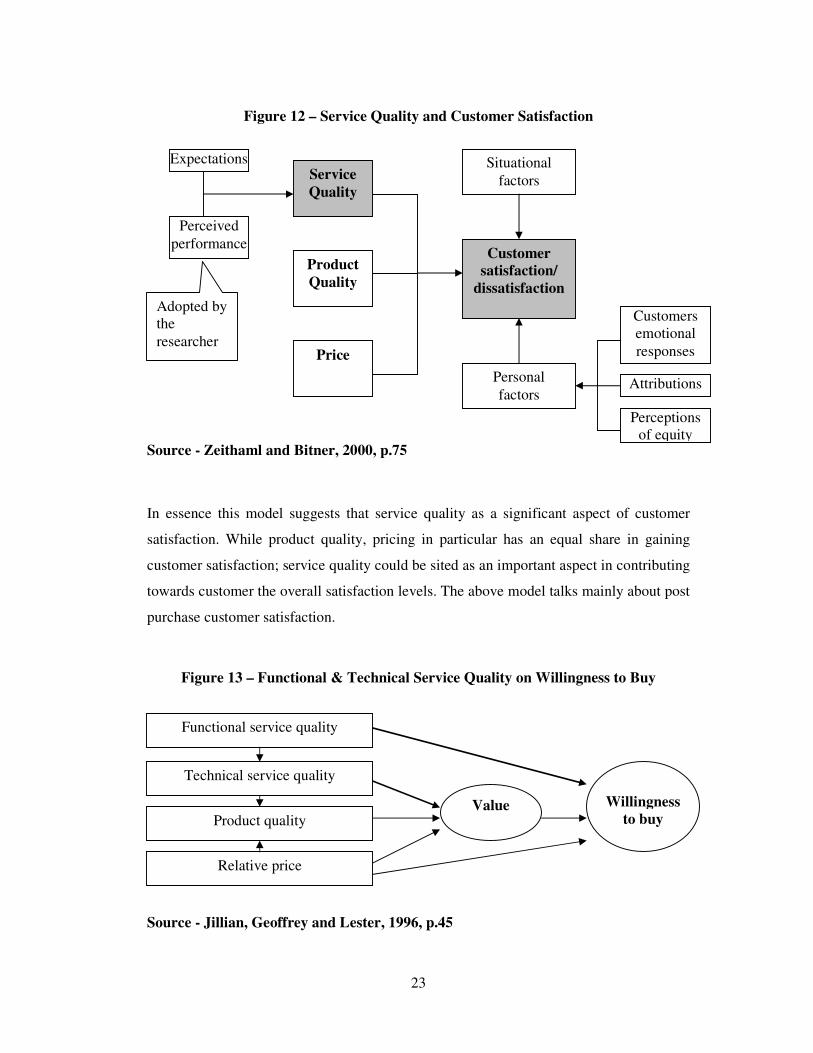

Figure 12 – Service Quality and Customer Satisfaction

Source - Zeithaml and Bitner, 2000, p.75

In essence this model suggests that service quality as a significant aspect of customer

satisfaction. While product quality, pricing in particular has an equal share in gaining

customer satisfaction; service quality could be sited as an important aspect in contributing

towards customer the overall satisfaction levels. The above model talks mainly about post

purchase customer satisfaction.

Figure 13 – Functional & Technical Service Quality on Willingness to Buy

Source - Jillian, Geoffrey and Lester, 1996, p.45

Service

Quality

Product

Quality

Price

Customer

satisfaction/

dissatisfaction

Situational

factors

Expectations

Perceived

performance

Adopted by

the

researcher

Personal

factors

Customers

emotional

responses

Attributions

Perceptions

of equity

Functional service quality

Technical service quality

Product quality

Relative price

Value

Willingness

to buy

24

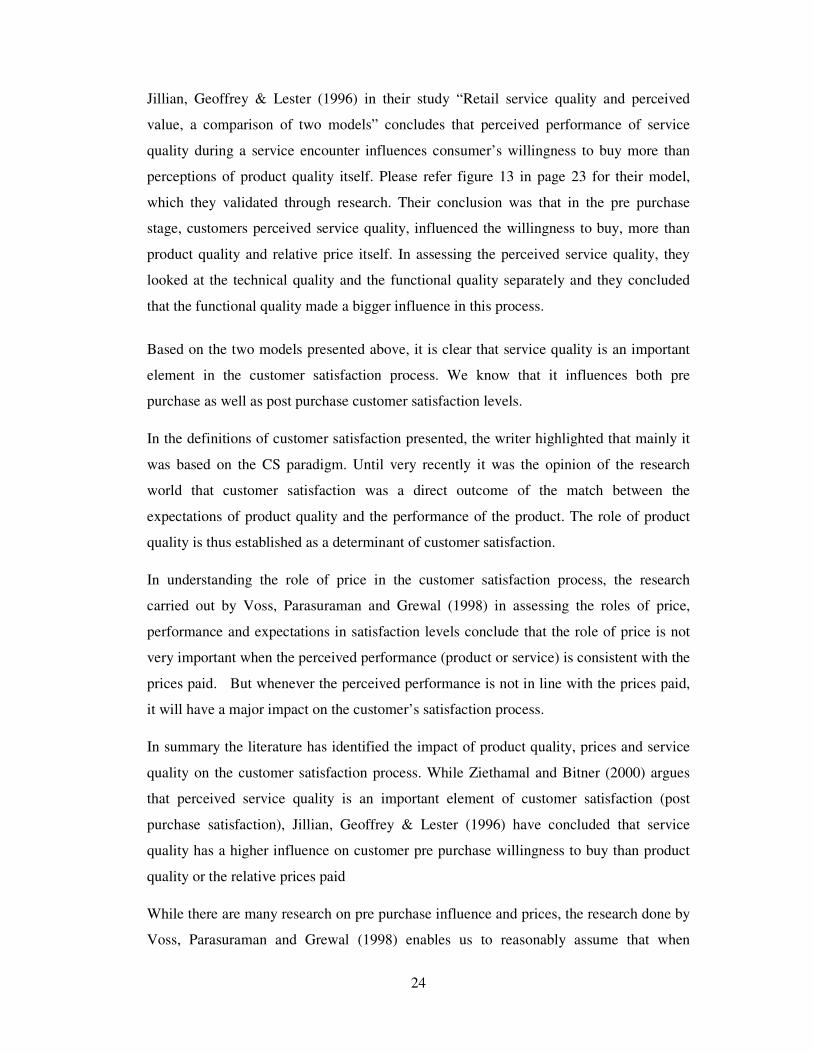

Jillian, Geoffrey & Lester (1996) in their study “Retail service quality and perceived

value, a comparison of two models” concludes that perceived performance of service

quality during a service encounter influences consumer’s willingness to buy more than

perceptions of product quality itself. Please refer figure 13 in page 23 for their model,

which they validated through research. Their conclusion was that in the pre purchase

stage, customers perceived service quality, influenced the willingness to buy, more than

product quality and relative price itself. In assessing the perceived service quality, they

looked at the technical quality and the functional quality separately and they concluded

that the functional quality made a bigger influence in this process.

Based on the two models presented above, it is clear that service quality is an important

element in the customer satisfaction process. We know that it influences both pre

purchase as well as post purchase customer satisfaction levels.

In the definitions of customer satisfaction presented, the writer highlighted that mainly it

was based on the CS paradigm. Until very recently it was the opinion of the research

world that customer satisfaction was a direct outcome of the match between the

expectations of product quality and the performance of the product. The role of product

quality is thus established as a determinant of customer satisfaction.

In understanding the role of price in the customer satisfaction process, the research

carried out by Voss, Parasuraman and Grewal (1998) in assessing the roles of price,

performance and expectations in satisfaction levels conclude that the role of price is not

very important when the perceived performance (product or service) is consistent with the

prices paid. But whenever the perceived performance is not in line with the prices paid,

it will have a major impact on the customer’s satisfaction process.

In summary the literature has identified the impact of product quality, prices and service

quality on the customer satisfaction process. While Ziethamal and Bitner (2000) argues

that perceived service quality is an important element of customer satisfaction (post

purchase satisfaction), Jillian, Geoffrey & Lester (1996) have concluded that service

quality has a higher influence on customer pre purchase willingness to buy than product

quality or the relative prices paid

While there are many research on pre purchase influence and prices, the research done by

Voss, Parasuraman and Grewal (1998) enables us to reasonably assume that when

25

performance (could be product quality as well) is consistent (may even be among

competitors), the role of price in the customer satisfaction process would be insignificant

and in time of inconsistencies, the role of price would be a determining factor in

increasing or decreasing customer satisfaction levels. They highlighted the importance of

this to see the relationship with other determinants of customer satisfaction as well.

6. Developing Retail Mix Strategies

This section of the literature review will attempt to understand the components of the

retail strategy. In order to supplement the readers understanding in building retail

strategies, the retail planning process is discussed in brief as a pre amble.

Retailing is essentially “ All activities involved in selling goods or services directly to

final customers for their personal, non business use” – Kotler (1996). The retailer

essentially solves the discrepancy of assortment between the customer and the

manufacturer (wholesalers) in meeting both their expectations of assortment and

quantity. Retailing deals with all strategies in providing the products to the final customer

and is considered today as a marketing organization, a link between the producer and the

customer, a member in the distribution channel and finally as an image creator.

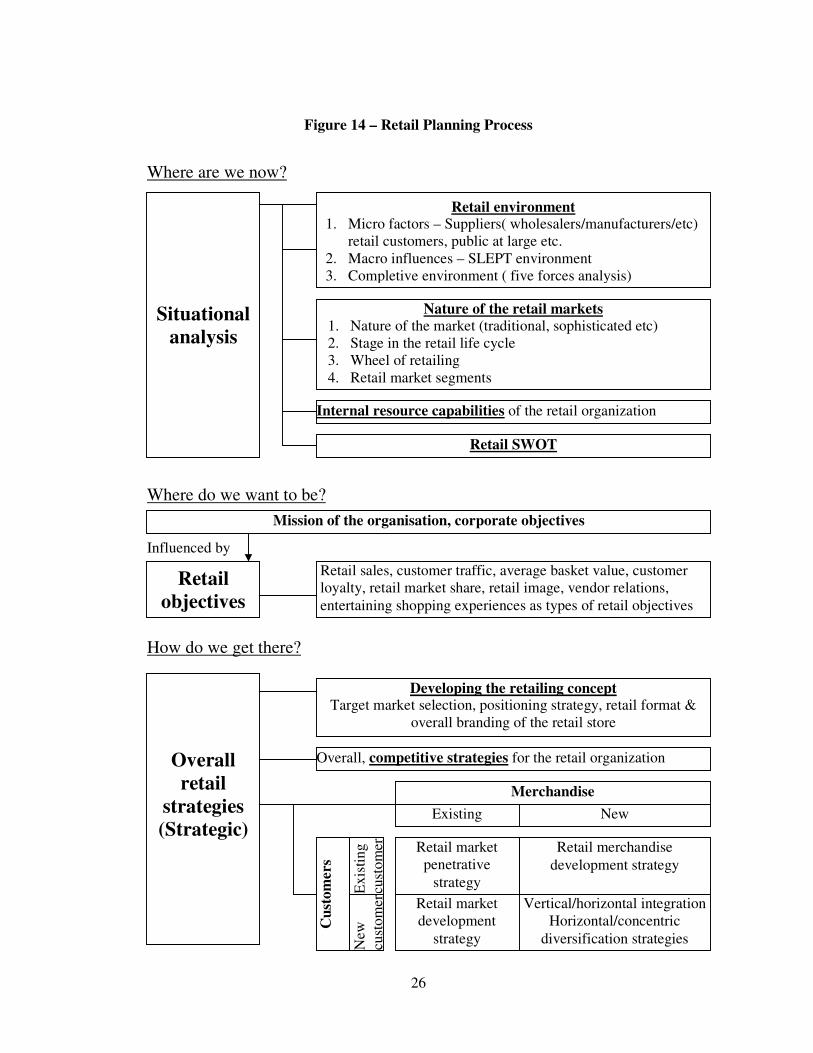

The retail planning process is no different to normal planning activities, but the

terminology and some of the elements could be quite different in certain situations. In

understanding retail strategy building, one needs to look at this from a total perspective.

The diagram 14 will elaborate the entire retail planning process. The writer has taken the

concepts from literature and arranged for the easy comprehension of the reader. Please

refer this figure for the retail planning process.

With retailing planning process in mind the writer will elaborate the components of the

retail mix strategies in the proceeding section. Supermarket retailing essentially lies in the

middle of the service continuum where the tangible product quality as well as the

intangible service quality would be important to the customer in his satisfaction process.

This is especially true for a self-service super marketing experience. Therefore retail mix

strategies needs to be viewed in parallel to the service marketing strategies, which are

organised within the seven P’s concept.

26

Figure 14 – Retail Planning Process

Where are we now?

Where do we want to be?

Influenced by

How do we get there?

Situational

analysis

Retail environment 1. Micro factors – Suppliers( wholesalers/manufacturers/etc)

retail customers, public at large etc.

2. Macro influences – SLEPT environment

3. Completive environment ( five forces analysis)

Nature of the retail markets

1. Nature of the market (traditional, sophisticated etc)

2. Stage in the retail life cycle

3. Wheel of retailing

4. Retail market segments

Internal resource capabilities of the retail organization

Retail SWOT

Retail

objectives

Retail sales, customer traffic, average basket value, customer

loyalty, retail market share, retail image, vendor relations,

entertaining shopping experiences as types of retail objectives

Mission of the organisation, corporate objectives

Overall

retail

strategies

(Strategic)

Overall, competitive strategies for the retail organization

Developing the retailing concept Target market selection, positioning strategy, retail format &

overall branding of the retail store

Retail merchandise

development strategy

Retail market

development

strategy

Vertical/horizontal integration

Horizontal/concentric

diversification strategies

Cu

sto

mers

New

cust

om

er

Retail market

penetrative

strategy Ex

isti

ng

cust

om

er

Merchandise

Existing New

27

Source – Created by the writer based on references made from books -See reference

list

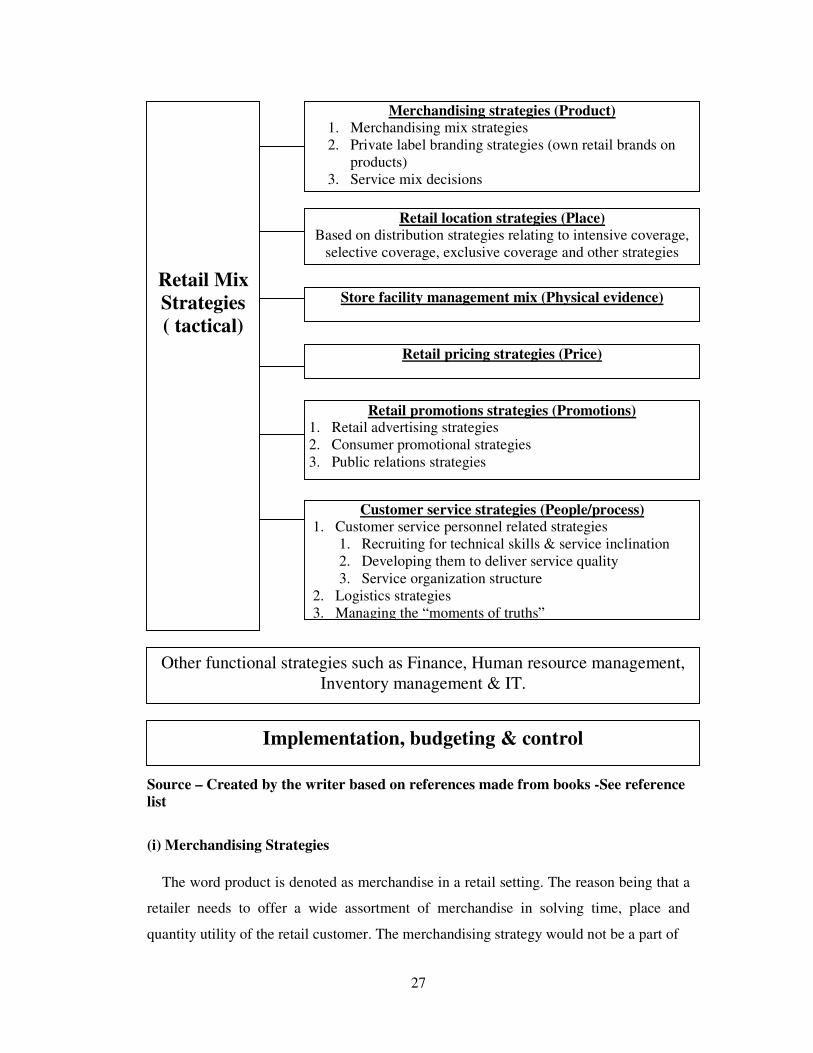

(i) Merchandising Strategies

The word product is denoted as merchandise in a retail setting. The reason being that a

retailer needs to offer a wide assortment of merchandise in solving time, place and

quantity utility of the retail customer. The merchandising strategy would not be a part of

Retail Mix

Strategies

( tactical)

Merchandising strategies (Product)

1. Merchandising mix strategies

2. Private label branding strategies (own retail brands on

products)

3. Service mix decisions

Retail location strategies (Place)

Based on distribution strategies relating to intensive coverage,

selective coverage, exclusive coverage and other strategies

Store facility management mix (Physical evidence)

Retail pricing strategies (Price)

Retail promotions strategies (Promotions) 1. Retail advertising strategies

2. Consumer promotional strategies

3. Public relations strategies

Customer service strategies (People/process)

1. Customer service personnel related strategies

1. Recruiting for technical skills & service inclination

2. Developing them to deliver service quality

3. Service organization structure

2. Logistics strategies

3. Managing the “moments of truths”

Implementation, budgeting & control

Other functional strategies such as Finance, Human resource management,

Inventory management & IT.

28

service quality but will influence the product quality of the consumers. The

merchandising strategy is made out of merchandising mix strategies; private labelling

branding strategies and the service mix strategies in a retailing scenario.

(a) Merchandising mix strategies.

Merchandising mix refers to the full range or mixture of products that the retailer offers

to the customer. The merchandising mix should represent an appropriate combination of

products to meet specific requirements of the target market. Due to the unlimited

combinations of merchandise the consumer may require, it is generally a difficult task to

operationalize this. Effective merchandising mix planning is essential for a supermarket

to operate effectively. In doing this a retailer will have to give thought to the degree of

perishability of many products.

Also developing the merchandise mix, a retailer would need to pay close attention to the

classifications of products. A retailer will carefully plan different product lines based on

typical target market requirements and purchasing sequence and group them as product

item groups and present individual product units within them.

The matrix presented in figure 15 would give insights on the various merchandising mix

strategies available to a retailer based on merchandise variety and assortment

combinations.

Figure 15 – Merchandising Strategies based on Merchandise Variety/Assortment

Source - Lewison, 1997, p. 391

Narrow Variety

Shallow assortment

Wide Variety

Shallow assortment

Narrow Variety

Deep assortment

Wide Variety

Deep assortment

Variety

No of product lines

Few Many

Ass

ort

men

t

nu

mb

er

of

pro

du

ct i

tem

s w

ith

in

each

pro

du

ct l

ine Few

M

an

y

29

Based on the above matrix the following four merchandising mix strategies could be

formulated.

Narrow variety/shallow assortment strategy. Offers the most limited product selection

to any of the combination strategies. Good example would be vending machines offering

limited types of newspapers, drinks, candy etc. Generally this strategy suffers from poor

image and less customer loyalty other than that generated by convenience.

Wide variety/shallow assortment strategy. The basic principle of this is “ stock a little

of everything”. The retailer offers a wide selection of different product lines but limits the

assortment of brands, styles, and sizes, and so on within each line. This strategy appeals

to a broad market, satisfying customers in terms of product availability, promoting one

stop shopping and permitting reasonable control over inventories. The disadvantage of

this would be loss of sales and customer disappointment with lack of selection within

product lines.