measuring systemic risk in ... - parmenides foundation · parmenides found. pullach, 2 june 2014...

TRANSCRIPT

Introduction Network Insights Surveillance Open issues

Measuring systemic risk in financial networks:Progress and challenges

Stefano Battiston

University of Zurich

Workshop on Systemic risk and regulatory market risk measuresParmenides Found. Pullach, 2 June 2014

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Acknowledgments

Swiss National Fund, Inst. of Banking and Finance, UZH

SNF Professorship at IBF, UZH - Financial Networks andSystemic risk

EU-FET SIMPOL 2013-2016 www.simpolproject.eu

Financial Systems Simulations and Policy Modeling

Networks of complex fin. instruments and shadow,climate-finance and networks of influence on regulation process

EU-FET FOC 2010-2014 www.focproject.eu

Forecasting Financial Crises

Network tools for financial regulation

INET - Financial Stability Program (dir. by Stiglitz)

WG on Financial Networks - (chair Haldane)Political economy aspects of fin. stability

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Overview

Problem: risk measures (VAR and ES) neglect systemdimension

Insights from network approach for

policies for financial stabilitysurveillance

The future:

Open issues and future research

Battiston and Caldarelli 2013, Systemic Risk in Financial Networks, JMFI

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Progress on Systemic Risk Measures

It is possible to:

quantitatively measure systemic impact conditional to shocks[DebtRank, Battiston ea. 2012]beyond default-only, beyond interbank-only

Policy insights

Connectedness / Risk diversificationOptimal structure of the banking systemIndicators for SIFI and systemic impactHow do we contain systemic risk?International nexus of TBTF institutionsSurveillance

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Issues on Systemic Risk Measures

open questions

estimate the probability of shocks in the futurestructural breaks

VAR and ES are likely to be heavily underestimated

VAR and ES do not account interdependence. No analyticalsolution. Numerical work.VAR of a bank in isolation differs from VAR of a bank in anetworksystemic VAR of a network of interconnected banks from VARof aggregated system

Risk measures are blind1 to asset overvaluation2 network effects3 procyclical effects

risk: the whole exercise might give new but false sense ofsecurity

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

The Financial System as a Network

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

The Financial System as a Network

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

The Financial System as a Network

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

The Financial System as a Network

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

The Financial System as a Network

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Financial Networks: Levels of Analysis

1 Static level, descriptive topology, across countries and legalsettings

2 Simplified agent behaviour: response to shocks and resilience.3 Strategic interaction: endogenous link formation, efficiency vs

stability, welfare issues4 Political economy: endogenous influence over rules of the

game: Meta-game and power

RemarksResilience analysis in absence of amplifications (level 2-3)can be misleading.

Results on connectedness tend to be opposite

Welfare analysis at level 3 maybe misleading. Level 4required.

Are the welfare measures appropriate and encompassing effectsto real economy?Is market power and regulatory capture taken into account?

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Financial Networks: Levels of Analysis

1 Static level, descriptive topology, across countries and legalsettings

2 Simplified agent behaviour: response to shocks and resilience.3 Strategic interaction: endogenous link formation, efficiency vs

stability, welfare issues4 Political economy: endogenous influence over rules of the

game: Meta-game and power

RemarksResilience analysis in absence of amplifications (level 2-3)can be misleading.

Results on connectedness tend to be opposite

Welfare analysis at level 3 maybe misleading. Level 4required.

Are the welfare measures appropriate and encompassing effectsto real economy?Is market power and regulatory capture taken into account?

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Financial Networks: Levels of Analysis

1 Static level, descriptive topology, across countries and legalsettings

2 Simplified agent behaviour: response to shocks and resilience.3 Strategic interaction: endogenous link formation, efficiency vs

stability, welfare issues4 Political economy: endogenous influence over rules of the

game: Meta-game and power

RemarksResilience analysis in absence of amplifications (level 2-3)can be misleading.

Results on connectedness tend to be opposite

Welfare analysis at level 3 maybe misleading. Level 4required.

Are the welfare measures appropriate and encompassing effectsto real economy?Is market power and regulatory capture taken into account?

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

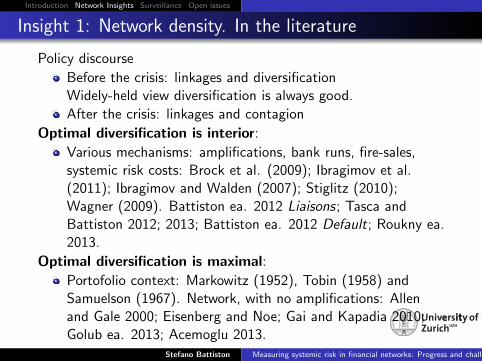

Insight 1: Network density. In the literature

Policy discourse

Before the crisis: linkages and diversificationWidely-held view diversification is always good.

After the crisis: linkages and contagion

Optimal diversification is interior:

Various mechanisms: amplifications, bank runs, fire-sales,systemic risk costs: Brock et al. (2009); Ibragimov et al.(2011); Ibragimov and Walden (2007); Stiglitz (2010);Wagner (2009). Battiston ea. 2012 Liaisons; Tasca andBattiston 2012; 2013; Battiston ea. 2012 Default; Roukny ea.2013.

Optimal diversification is maximal:

Portofolio context: Markowitz (1952), Tobin (1958) andSamuelson (1967). Network, with no amplifications: Allenand Gale 2000; Eisenberg and Noe; Gai and Kapadia 2010;Golub ea. 2013; Acemoglu 2013.

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 1: Network density.In continuous-time dynamics

Optimal diversification is inte-rior:

Continuous stochasticdynamics with trendreinforcement[Battiston, Delli Gatti, Gallegati, Stiglitz,

Greenwald, 2012, JEDC (Liaisons

Dangereuses)]

Continuous stochasticdynamics in bank-assetnetwork[Tasca-Battiston 2012; 2013]

0 25 50 75 1000

0.05

0.1

0.15

Diversification degree k

De

fau

lt p

rob

ab

ility

Pf

α ↑

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 1: Network density - In default cascades models

b market illiquidity, m averagetier-1 capital ratio

Interplay: diversification,amplifications (illiquidity, firesales), allocation of capitalbuffers, topology (scale-free vsrandom)

b = 0: cascade size decreaseswith k[Gai and Kapadia 2010, Golub ea. 2013; Acemoglu

2013)]

b > 0: cascade size nonmonotonic[Battiston ea., 2012 JFS; Roukny ea. SciRep 2013]

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

What Optimal Network Architecture?

1 Topology

2 Tier-1 capital vs degree (no. of contracts)

3 Asset market liquidity and bank liquidity

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

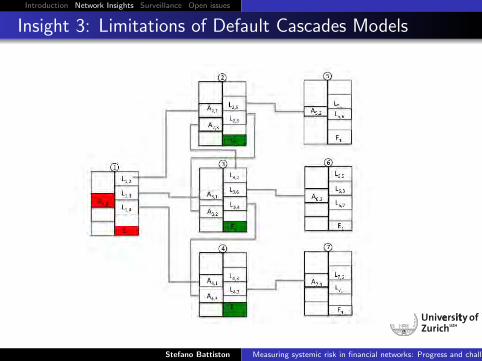

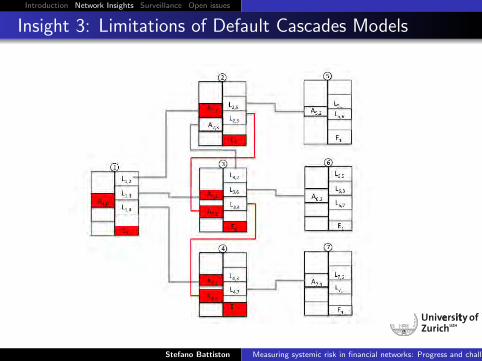

Insight 3: Limitations of Default Cascades Models

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Limitations of Default Cascades Models

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Limitations of Default Cascades Models

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Limitations of Default Cascades Models

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Run of Short Term Lenders

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Run of Short Term Lenders

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Run of Short Term Lenders

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 3: Interconnectedness in stress-tests

Stress tests based on cascades:

With no amplification

cascades almost never occurhigh enough diversification: no cascades at all. Recipe: fulldiversification is best.

When additional externalities at work: e.g. fire-sales, creditruns, market procyclicality, illiquidity

cascades do occur (including bank-asset network sheds light)diversification has non-monotonic effectthere is no single topology that is just superiorthe most robust architecture depends on: market liquidity,types of shocks, correlations btw capital buffer and degree

[Battiston, Delli Gatti, Gallegati, Greenwald, Stiglitz, 2012 JFS; Roukny, Bersini,

Pirotte, Caldarelli, Battiston, 2013; Tasca, Battiston 2012, ETH RC; Battiston,

Puliga, Kaushik, Tasca, Caldarelli 2012 Sci Rep]

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

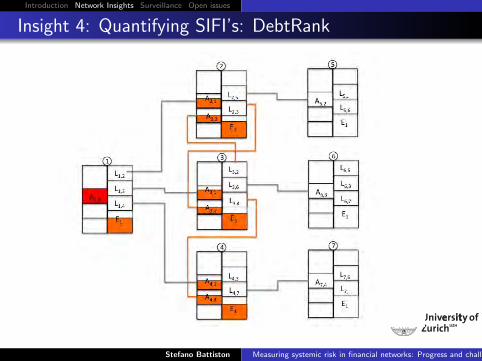

Insight 4: Quantifying SIFI’s: DebtRank

DebtRankmore central = moresystemically important

not just a ranking, butmonetary value of systemicloss

overcome limitations ofstate-of-the art:

1 default-only algo2 (2) non-specific measures

(between. eigenvec.,PageRank ...)

individual and groups;complement to Early WarningSystem

[Battiston ea., DebtRank 2012, Sci Rep. 2:541]Di Iasio ea. 2013 Capital and Contagion, MPR

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 4: Quantifying SIFI’s: DebtRank

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 4: Quantifying SIFI’s: DebtRank

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 4: Quantifying SIFI’s: DebtRank

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Properties of Default vs Distress Propagation Indicators

DebtRank:

hj ∈ [0, 1] = fraction of evaporated equity

hj(0) = 1 except for the shocked banks

hi (t) = min

{1, hi (t − 1) +

∑j

Wjihj(t − 1)χj

}, where

Wji =Aij

Ei

χj = 1 if hj(t − 1) > 0 and 0 else

Dri =∑

j hj(T )Ej(0) = DR-Impact

hi (T ) = DR-Vulnerability

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Properties of Default vs Distress Propagation Indicators

Default Cascades

hj monotonously decreasing with equity of target node

hj non monotonously decreasing with total equity in thesystem

hj non sub-additive: hj(φ1 + φ2) > hj(φ1) + hj(φ2) ifφ1 + φ2 > 1 and φ1 < 1, φ2 < 1

Debt Rank

hj monotonously decreasing with equity of target node andincreasing with shock size

hj is non (?) monotonously decreasing with total equity in thesystem

hj is sub-additive: hj(φ1 + φ2) ≤ hj(φ1) + hj(φ2)

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Application: an exercise on FED data + BvD data

Take banks’ investment in each others equity share as a proxyof all exposures

Focus on the largest borrowers from the FED in 2008-2010

22 inst., peak lending 1.2 USD trillions, total assets 20 USDtrillions)

Incorporate dynamics of core capital (take marketcapitalization as a proxy of core capital)

Recipe

1 market capitalization as proxy of core capital

2 investments in equity as proxy of financial exposures

3 rescaling factor α, conservative scenario: in good the timesevery bank can sustain the default of at least 5 counterparties

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

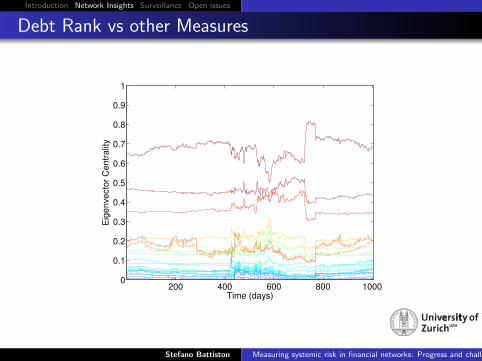

Debt Rank vs other Measures

200 400 600 800 10000

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Time (days)

De

btR

an

k

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Debt Rank vs other Measures

200 400 600 800 10000

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Time (days)

De

fau

lt C

asca

de

Im

pa

ct

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Debt Rank vs other Measures

200 400 600 800 10000

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Time (days)

Eig

en

ve

cto

r C

en

tra

lity

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Latent Correlations: Shock to a Common External Asset

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Latent Correlations: Shock to a Common External Asset

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Latent Correlations: Shock to a Common External Asset

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Network Effects

For regulators: measuring the systemic impact of the distressof one or more institutions

beyond default-only chains

For investors: evaluating counterparty risk beyondcorrelationNo network effects:

correlation ρ = 0: probability of joint defaults is pN

correlation ρ = 1: probability of joint defaults is p

With network effects

probability of joint defaults can be p (and not pN) even withlow correlationpotential massive underestimation of Value-at-Risk

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Network Effects

For regulators: measuring the systemic impact of the distressof one or more institutions

beyond default-only chains

For investors: evaluating counterparty risk beyondcorrelationNo network effects:

correlation ρ = 0: probability of joint defaults is pN

correlation ρ = 1: probability of joint defaults is p

With network effects

probability of joint defaults can be p (and not pN) even withlow correlationpotential massive underestimation of Value-at-Risk

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Network Effects

For regulators: measuring the systemic impact of the distressof one or more institutions

beyond default-only chains

For investors: evaluating counterparty risk beyondcorrelationNo network effects:

correlation ρ = 0: probability of joint defaults is pN

correlation ρ = 1: probability of joint defaults is p

With network effects

probability of joint defaults can be p (and not pN) even withlow correlationpotential massive underestimation of Value-at-Risk

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Network Effects

Theorem (conjecture!): No-Systemic Risk is a Self-negatingProfecy

Systemic events may emerge precisely because financial actorsassume away systemic events.

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Network Effects

Theorem (conjecture!): No-Systemic Risk is a Self-negatingProfecy

Systemic events may emerge precisely because financial actorsassume away systemic events.

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 5: How do we contain systemic risk?

Systemic risk: there exist a bad equilibrium with a combination

high interconnectedness/ interdependence

high correlation on bank behaviour

high illiquidity

high complexity of instruments and structure

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 6: International Nexus of TBTF Institutions

TBTF - too-big-too-fail

TCTF -too-connected-to-fail

TCTF - too-central-to-fail

Should we regard financialinstitutions as aninternational nexus?

Sustainability: need to copewith global moral hazard.

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 6: International Nexus of TBTF Institutions

TBTF - too-big-too-fail

TCTF -too-connected-to-fail

TCTF - too-central-to-fail

Should we regard financialinstitutions as aninternational nexus?

Sustainability: need to copewith global moral hazard.

200 400 600 800 10000

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Time (days)D

ebtR

ank

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 6: International Nexus of TBTF Institutions

TBTF - too-big-too-fail

TCTF -too-connected-to-fail

TCTF - too-central-to-fail

Should we regard financialinstitutions as aninternational nexus?

Sustainability: need to copewith global moral hazard.

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Insight 7: Tools for Surveillance

A coordinate effort on data gathering: it would be possible tomake tentative estimations of systemic impact of shocks

direct effect on balance sheets

amplifications via procyclical leverage-price dynamics

amplifications via balance-sheet distress propagation

Workflow

Monitor over time interconnectedness in exposures

bank-bank, bank-asset, bank-firms, country-country

Estimate networks whereas data are missing

Compute systemic risk, conditional to given distribution ofshocks

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Monitoring: proof of concept

Live daily monitoring of DebtRank on the GSIFI correlationnetwork http://ethz.focproject.eu/lwidgetnets

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Monitoring: proof of concept

Live daily monitoring of DebtRank on the GSIFI correlationnetwork http://ethz.focproject.eu/gsifi

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Monitoring: proof of concept

Co-occurrence of terms in financial blogs. Ex: “IMF” and“Ukraine” http://www.focproject.eu/focjsiwidget

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Issues on Systemic Risk Measures

VAR and ES are likely to be heavily underestimated

VAR and ES do not account interdependence. No analyticalsolution. Numerical work.VAR of a bank in isolation differs from VAR of a bank in anetworksystemic VAR of a network of interconnected banks from VARof aggregated system

Risk measures are blind1 to asset overvaluation2 network effects3 procyclical effects

risk: the whole exercise might give new but false sense ofsecurity

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Related International Activities

FOC Forecasting Financial Crises www.focproject.eu

MULTIPLEX Multi-level Complex Networks www.multiplexproject.eu

GSDP Global Systems and Policies

GSS Global Systems Science http://global-systems-science.eu/

SIMPOL (Financial Systems Simulation and Policy Modelingwww.simpol.eu

INET - Financial stability Programhttp://ineteconomics.org/research-programs/financial-stability

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Related International Activities

European Conference on Complex Systems, Lucca September22-26

Satellite workshop 24 September, Global systems science andpolicy modeling: financial networks, inequality, sustainability

http://www.eccs14.eu/

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

References - 1

Anand, K., Gai, P., Kapadia, S., Brennan, S. and Willison, M. A network modelof financial system resilience. J. Econ. Behav. Organ. 85, 219–235 (2013).

Battiston, S., Puliga, M., Kaushik, R., Tasca, P. and Caldarelli, G. DebtRank:Too Central to Fail? Financial Networks, the FED and Systemic Risk. Sci. Rep.2, (2012).

Battiston, S., Gatti, D. D., Gallegati, M., Greenwald, B. C. N. and Stiglitz, J. E.Liaisons Dangereuses: Increasing Connectivity, Risk Sharing, and Systemic Risk.J. Econ. Dyn. Control 36, 1121–1141 (2012).

Cifuentes, R., Ferrucci, G. and Shin, H. S. Liquidity risk and contagion. J. Eur.Econ. Assoc. 3, 556–566 (2005).

Eisenberg, L. and Noe, T. H. Systemic Risk in Financial Systems. Manage. Sci.47, 236–249 (2001).

Elsinger, H., Lehar, A. and Summer, M. Risk Assessment for Banking Systems.Manage. Sci. 52, 1301–1314 (2006).

Gai, P. and Kapadia, S. Contagion in financial networks. Proc. R. Soc. A Math.Phys. Eng. Sci. 466, 2401–2423 (2010).

Gai, P., Haldane, A., Kapadia, S. Complexity, concentration and contagion. J.Monet. Econ. 58, 453–470 (2011).

Haldane, A. G. Rethinking Financial Networks. Speech Financial Student Assoc.Amsterdam (2009).

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

References - 2

Haldane, A. G. Rethinking Financial Networks. Speech Financial Student Assoc.Amsterdam (2009).

Hommes C., van der Leij M., in’t Veld D., Formation of a core-peripherynetwork in OTC markets

Kubler, F. , Schmedders, K. Stationary Equilibria in Asset-Pricing Models withIncomplete Markets and Collateral. Econometrica 71, 1767–1793 (2003).

Roukny, T., Bersini, H., Pirotte, H., Caldarelli, G., Battiston, S. DefaultCascades in Complex Networks: Topology and Systemic Risk. Sci. Rep. 3,(2013).

Tasca, P., Battiston, S. Market Procyclicality and Systemic Risk. Submitt.earlier version ETH Risk Cent. Work. Pap. Ser. ETH-RC-12-012 (2012).

Tasca, P., Battiston, S. Diversification and Financial Stability. Submitt. earlierversion ETH Risk Cent. Work. Pap. Ser. ETH-RC-12-013 (2012).

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges

Introduction Network Insights Surveillance Open issues

Recent Papers

Debtrank: [Battiston, Puliga, Kaushik, Tasca, Caldarelli, DebtRank:Too-central-to-fail? (2012) Sci. Rep. 2:541]

Complex derivatives [ Battiston, Caldarelli, Georg, May, Stiglitz, Nat. Phys.,2013]

CDS and network reconstruction [Kaushik R., Battiston S., 2013 PLoS-ONE,forth], [Puliga M., Kaushik R., Battiston S., Caldarelli G., 2013 in progress]

Estimation of systemic risk in networks from partial information: [Musmeci,Puliga, Gabrielli, Battiston, Caldarelli, JOSS 2013, forth.]

Controllability in e-mid [Delpini, Battiston, Riccaboni, Pammolli, Gabbi,Caldarelli, Sci. Rep., 2013, forth.]

Controllability in TARGET2 [Galbiati, Delpini, Battiston, (2013) Nat Phys]

All works supported by FOC are available atwww.focproject.eu/publications

Stefano Battiston Measuring systemic risk in financial networks: Progress and challenges