medium term prospects of agricultural commodity markets

TRANSCRIPT

Medium term prospects of agricultural commodity markets – Uncertainties and challenges –

Marcel Adenäuer (OECD)

COCERAL/FEDIOL Symposium, Rome

27 May 2016

2 2 | www.agri-outlook.org | #AgOutlook

2

• UN projections: 8.5 Bn people by 2030 (+ 1.2 Bn from 2015)

• But food demand grows even faster:

Major driver for food demand: Population growth

0

1

2

3

4

19

61

19

64

19

67

19

70

19

73

19

76

19

79

19

82

19

85

19

88

19

91

19

94

19

97

20

00

20

03

20

06

20

09

20

12

20

15

20

18

20

21

20

24

20

27

20

30

Global calorie demand Global population

3 3 | www.agri-outlook.org | #AgOutlook

3

• Experts see:

• Moderate economic growth in the OECD area

• Slight slowdown in major emerging economies

for the coming decade

Also important: Income growth

4 4 | www.agri-outlook.org | #AgOutlook

4

Energy prices, a major source of uncertainty:

Source: IEA WORLD ENERGY OUTLOOK 2015

Crude Oil prices for different future scenarios

5 5 | www.agri-outlook.org | #AgOutlook

5

• Exchange rates • Further US Dollar appreciation against most currencies?

• Inflation • Moderate in most countries ?

• The policy environment • Agricultural/Food-, Trade-, Energy- and Environmental

policies

Other drivers

6 6 | www.agri-outlook.org | #AgOutlook

6

• Real food prices expected to decline slightly, but remain above levels before 2007-08 food price crisis.

• Changing relative prices: › Consumption of staples reaching saturation in many countries › Meat and dairy prices increase relative to crops – higher incomes

and animal-protein demand › Coarse grain and oilseed prices increase relative to food staples – feed demand

• Calmer markets but a risk of resurgent volatility

• Spread of imports across a large number of countries; concentration of exports among a few key suppliers

Highlights of the OECD-FAO Outlook 2015-2024

7 7 | www.agri-outlook.org | #AgOutlook

7

Prices to remain higher than in the years preceding the 2007-08 price spike

40

50

60

70

80

90

100

110

120

Index (2012-14=100)

Cereals Dairy Meat Oilseeds

8 8 | www.agri-outlook.org | #AgOutlook

8

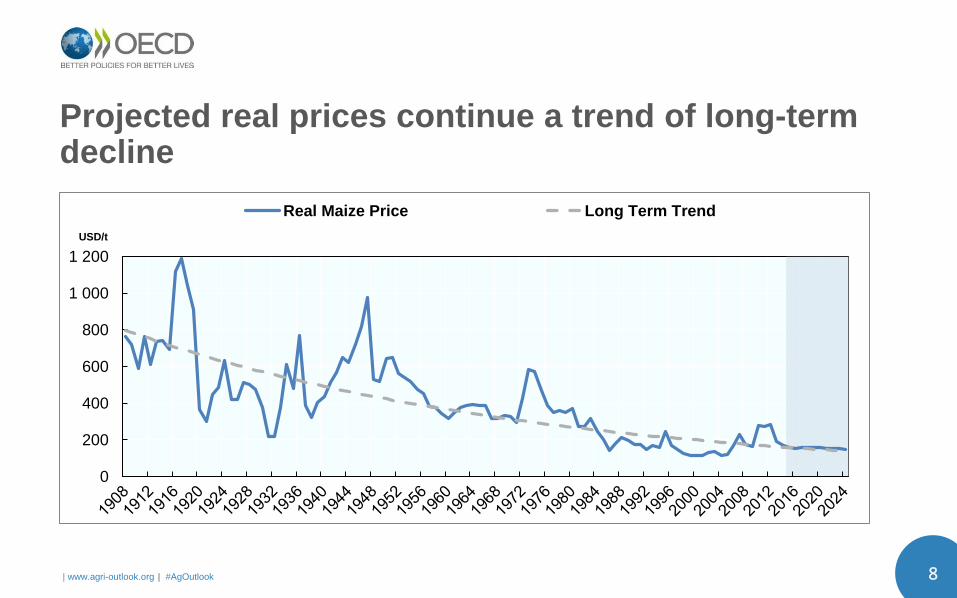

Projected real prices continue a trend of long-term decline

0

200

400

600

800

1 000

1 200

USD/t

Real Maize Price Long Term Trend

9 9 | www.agri-outlook.org | #AgOutlook

9

But there is a substantial risk of a further price shock

10th

90th

0

50

100

150

200

250

300

350

400

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

201

6

201

7

201

8

201

9

202

0

202

1

202

2

202

3

202

4

USD/t Nominal maize price

Probability of price outside the 10-90th percentile = 1 – 0.8**10 or

approximately 90%

10 | www.agri-outlook.org | #AgOutlook

10 10 10 10

• Cereals are still at the core of human nutrition, but growing incomes, urbanisation and a certain globalisation of eating habits contribute to the ongoing transition of diets that are higher in protein, fats and sugar.

• Annual increase in global consumption is projected for cereals at 1.1%, meat 1.3% and dairy 1.6%.

• Demand is growing at slower rates compared to the past decade, due to: population, saturation, recuperation.

Demand trends

11 11 | www.agri-outlook.org | #AgOutlook

11

Global consumption growth by groups

0

500

1 000

1 500

2 000

2 500

3 000

2002-04 2012-14 2024 2002-04 2012-14 2024 2002-04 2012-14 2024

Least Developed Countries Other developing countries Developed countries

kcal/day/person

Fish Dairy Sugar Meat Vegetable oils Cereals Other

+47

+13

+25 +7 +27

+18

+4

+73

+15

+34

+20

+9

+13

+4

+4

+14

+13

12 | www.agri-outlook.org | #AgOutlook

12 12 12 12

• Growth in livestock production is expected to outpace crop production in the next decade.

• The structure of global agricultural production is expected to respond to the increased need for coarse grains and oilseeds compared to wheat or rice.

• The limited availability of additional arable land will impact the expansion and concentration of additional crop production.

Supply Trends

13 13 | www.agri-outlook.org | #AgOutlook

13

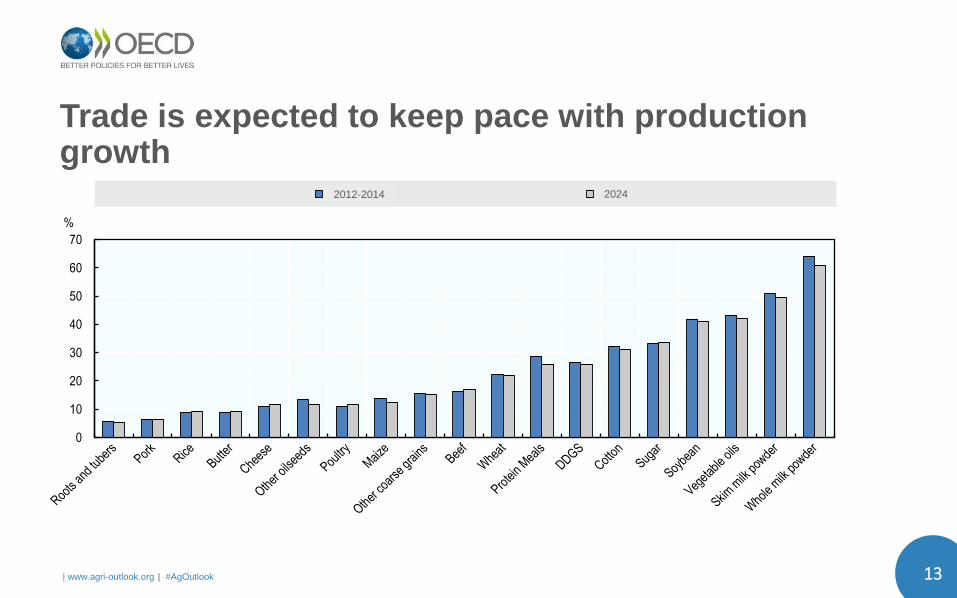

Trade is expected to keep pace with production growth

0

10

20

30

40

50

60

70

%

2013-15 20252012-2014 2024

14 14 | www.agri-outlook.org | #AgOutlook

14

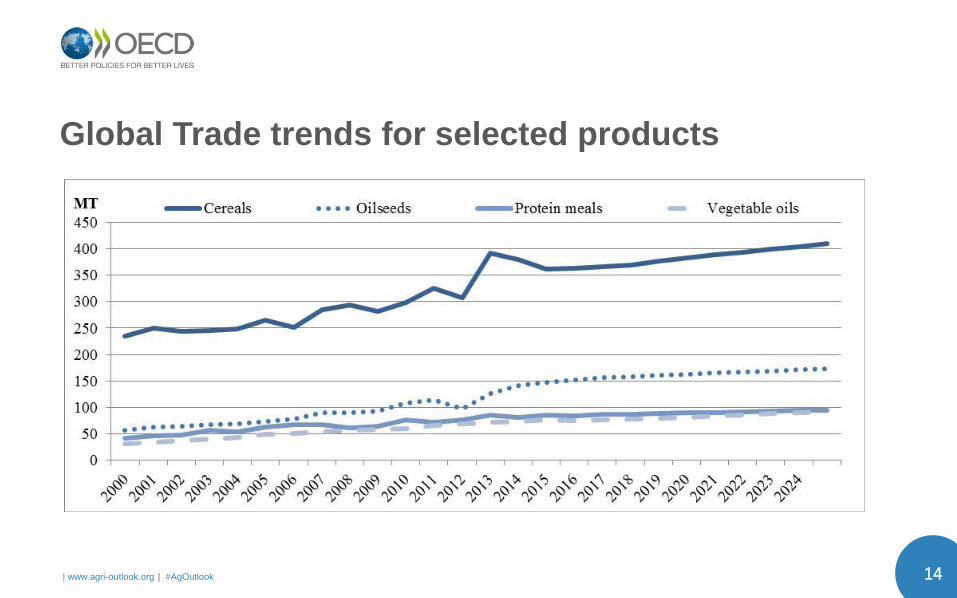

Global Trade trends for selected products

15 15 | www.agri-outlook.org | #AgOutlook

15

World exports to remain highly concentrated Shares of top five countries in global exports in 2024

0

10

20

30

40

50

60

70

80

90

100

%

5th exporter 4th exporter 3rd exporter 2nd exporter 1st exporter 2013-15 top 5

16 16 | www.agri-outlook.org | #AgOutlook

16

Imports in 2024 more dispersed…but China matters!

Shares of top five importers in world imports

0

10

20

30

40

50

60

70

80

90

100

%

China 5th importer 4th importer 3rd importer 2nd importer 1st importer

17 17 | www.agri-outlook.org | #AgOutlook

17

World price impacts of China growth at 5% (versus 6% under the baseline)

-7

-6

-5

-4

-3

-2

-1

0

%

18 | www.agri-outlook.org | #AgOutlook

18 18 18 18

• Sustainable productivity growth

• The role of Foreign Direct Investments

• Pressure on Resources used by agriculture and the food sector

• Climate change constraints and opportunities

• The role of the ongoing urbanization process on the service content of food

• Impacts of consumer- and nutrition policies as well as consumer preferences on food demand

Challenges for the Agricultural sector