melting the iceberg - · pdf filemelting the iceberg ... our results also indicate that...

TRANSCRIPT

Melting the Iceberg

A study providing evidence that asset finance is reducing the burden of

‘frozen capital’ in global healthcare markets

SFS Research Study, May 2012 www.siemens.com/finance-publications A white paper issued by: Siemens Financial Services GmbH. © Siemens AG 2012. All rights reserved.

2

Contents

Management Summary ....................................................................................................................... 3

Introduction ............................................................................................................................................ 4

Creating Financially Sustainable Healthcare Systems ................................................................... 5

Frozen Capital Remains High ............................................................................................................ 7

Growth of Asset Finance is Outpacing Market Growth .................................................................. 8

The Benefits of Investment in Up-to-date Medical Technology .................................................. 11

Conclusions ......................................................................................................................................... 13

Country Backgrounders ..................................................................................................................... 14

China ................................................................................................................................................ 14

India .................................................................................................................................................. 15

Germany .......................................................................................................................................... 17

France .............................................................................................................................................. 18

UK ..................................................................................................................................................... 19

Spain ................................................................................................................................................ 20

Poland .............................................................................................................................................. 21

Russia .............................................................................................................................................. 22

Turkey .............................................................................................................................................. 23

3

Management Summary

Medical equipment leasing and renting is developing its role to free up

‘frozen capital’ in world healthcare systems

Annual growth rates for medical equipment leasing and renting is

outpacing growth in the medical device market as a whole

This means that a steadily increasing proportion of healthcare

equipment is being acquired through an efficient financing arrangement,

rather than tying up (or ‘freezing’) precious and scarce public sector

capital

The increasing attractiveness of medical equipment leasing and renting

for health sector finance managers is likely to continue growing

In mature economies, healthcare costs continue to outpace stretched

public capital, and only by accessing private sector investment will

future needs be met

In rapidly developing economies, state authorities are extremely

concerned that medical equipment investments should be sustainable,

kept proportionate and affordable, and be seen to provide efficient

return on investment

Asset finance, in the form of leasing and rental, helps healthcare

organisations spread the cost of equipment over its useful lifetime, and

to calculate a cost-per-treatment by matching monthly payments with

monthly patient throughput rates (although the organisation still bears

the risk of miscalculating its patient projections)

Although capital equipment spending typically only makes up 4-5% of

total healthcare budgets, access to up-to-date technology has a

disproportionately positive effect on increasing patient throughput

rates, reducing cost-per-treatment/diagnosis, and improving patient

outcomes

Therefore, access to asset finance allows healthcare organisations to

make more financially transparent and sustainable investments in

equipment that allows them to improve diagnosis and treatment

efficiency and effectiveness, thereby improving return on investment

4

Introduction

Budget deficit and sovereign debt concerns have prompted many developed countries to

rein in healthcare budgets and reform their healthcare systems in recent years. As a result

of some or all of a range of factors - ageing demographics, accumulated budget deficits,

rising demand for healthcare services, over-prescription, a bewildering array of new

treatments (especially biotech) - healthcare spending has become unsustainable in the long

run in many mature economies. Health policymakers are now confronted with the double

challenges of curbing rising healthcare costs while maintaining the quality of healthcare

services.

In the UK, NHS spending as a whole has been “ring-fenced”, yet capital spending is to fall by

17% between 2012 and 2015 and over £20 billion (€23.9 billion) of efficiency savings are to

be achieved in this period. Germany introduced a major healthcare reform in 2011 with the

aim to raise €11 billion to tackle its severe healthcare spending deficit of €9 billion. A

similarly high deficit is also seen in France, resulting in consistently reduced reimbursement

tariffs for both drugs and equipment. In Spain, the government is grappling with spiralling

health costs while trying to bring down the budget deficit in order to ward off an international

bailout. The controversial US healthcare reform – The Affordable Care Act – which aims to

expand access to insurance to over 30 million Americans and increase insurance coverage

of pre-existing conditions is bound to drive down reimbursement rates for treatments and

therefore demand greater financial efficiency in the US healthcare sector.

In comparison, many developing economies are embarking on a major healthcare

infrastructural build amid surging economic performance in order to satisfy growing demand

for quality healthcare at a reasonable and sustainable cost. In 2009, China unveiled its

RMB850 billion (€100 billion) healthcare reform which aims to provide universal healthcare

coverage by 2020 and overhaul rural and community-level healthcare services. India also

launched its National Rural Health Mission 2005-2012 in April 2005 for the improvement and

capacity enhancement of healthcare facilities throughout the country. The Russian

government also committed US$28 billion (€21 billion) to the “Healthcare National Project” in

2005. The initiative will run through to 2013 and should improve Russian health outcomes

and measure the quality of medical services in the country.

In order to align with the EU norms, healthcare expenditure in Poland is set to rise in the

years to come and private healthcare networks are already expanding rapidly. Similarly,

Turkey’s healthcare system has been making tremendous improvements thanks to the 2003-

2013 Health Transformation Programme. The government is also investing heavily in the

healthcare tourism sector.

All ambitions aside, having witnessed the severe financial pressure experienced by mature

economies, whose outcome-focused systems often mask the reality of rising costs,

healthcare authorities and governments of developing countries are particularly conscious

that any effort to overhaul the current healthcare landscape has to go hand in hand with

financial efficiency and sustainability. However, an iceberg of ‘frozen capital’ has already

been built up, where scarce funds are tied up in outright purchase of medical equipment.

This burden has been evidenced in regular reports from Siemens Financial Services (SFS)

5

on the subject dating back to 2006. However, evidence is also beginning to emerge that

increasing use of financially efficient methods of acquiring medical equipment is starting to

reduce the burden of ‘frozen capital’ in healthcare systems around the world.

Creating Financially Sustainable Healthcare Systems

According to projections from SFS, around €15 trillion will be needed to fund developments

in the global public services infrastructure to 2030. Of that, around €2.5 trillion will be needed

for healthcare provision. These spending projections put into context how much the public

services, and healthcare in particular, are under pressure to identify and use the most

efficient and effective methods to finance these developments. Certainly, it is already evident

that the development of global healthcare systems cannot be funded purely from the public

purse.

The significant financial strain under which the global healthcare system is being put will

inevitably impair its ability to deliver quality healthcare services. Budgetary constraints have

also resulted in the deferment by some healthcare organisations of purchase of the latest

healthcare technology and equipment. With capital spending being suppressed, under-

investment in medical technology can lead to diagnostic and treatment inefficiency, directly

undermining standards of patient care. At the same time, some of the capital that is made

available is often in the form of last-minute annual surpluses, which has to be spent before

the year closes (in public healthcare systems such as the UK). This produces distortions in

planning and is not conducive to careful and sustainable equipment investments.

6

The creation of a financially sustainable healthcare system is therefore imperative.

Financing techniques, where monthly payments can be matched to monthly patient

throughput rates, enable healthcare finance managers to more easily understand, allocate

and calculate cost-per-treatment/diagnosis and therefore manage costs more closely,

accurately and effectively. This explains why forward thinking finance managers are

increasingly using financing techniques such as leasing and renting, rather than tying up or

‘freezing’ scarce and/or unsustainable levels of public sector capital. By refining the delivery

structure and supply chain in healthcare – moving from an input focused management

structure, to one driven by outputs - significant economies and efficiencies can be gained1.

This principle can be underpinned by an innovative reform of financial management and the

financial supply chains within healthcare systems.

Currently, a proportion of capital is “frozen” in healthcare systems across the globe, and is

not effectively or efficiently deployed. Frozen capital is defined as capital funding which is not

appropriate for the purposes to which it is being applied, and is therefore not delivering

adequate return on investment. In short, the notion of frozen capital in the healthcare sector

identifies the amount of money that could be freed up and more efficiently applied to capital

asset acquisition, if asset-financing techniques such as leasing and rental were more widely

employed.

This inefficiently deployed or ‘frozen’ capital can be replaced with an asset-financing plan

that:

(a) simply charges a fixed equipment lease/rental and maintenance cost against revenue

budgets

(b) introduces the possibility of being able to upgrade technology in broad line with

technology developments

(c) recognises the additional efficiency gains that can be offset against the cost of financing

the equipment

(d) supports the implementation of efficient processes with appropriate equipment

(e) reduces longer-term outlay because the financier retains title and can dispose of the

technology on the secondary markets

The result is a much more transparent and accurate visibility for healthcare managers of the

true cost of the asset over time. By correlating the asset finance costs with patient

throughput volumes, a cost-per-use can be calculated. Ultimately, this allows financial

managers in the healthcare sector to make much more acute judgments about the

affordability and cost-benefits of each equipment acquisition or upgrade.

1 Reform, 1 Jan 2006, The Empire Strikes Back, Professor Nick Bosanquet et al

7

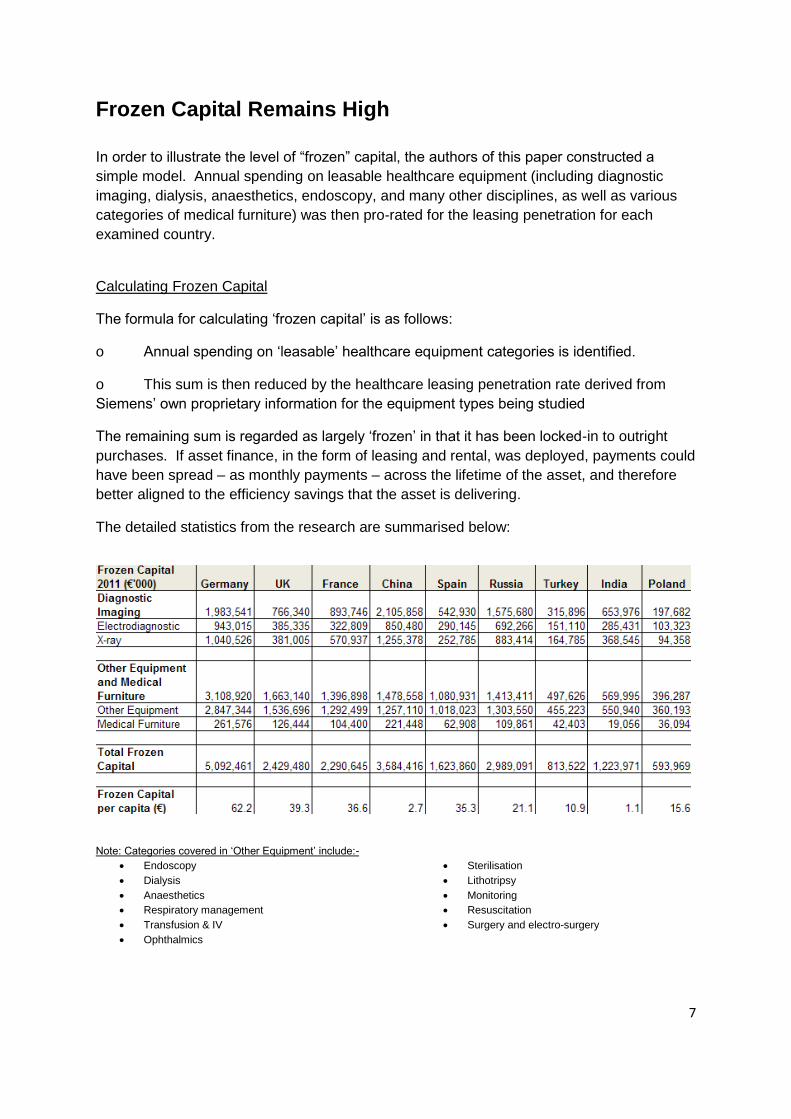

Frozen Capital Remains High

In order to illustrate the level of “frozen” capital, the authors of this paper constructed a

simple model. Annual spending on leasable healthcare equipment (including diagnostic

imaging, dialysis, anaesthetics, endoscopy, and many other disciplines, as well as various

categories of medical furniture) was then pro-rated for the leasing penetration for each

examined country.

Calculating Frozen Capital

The formula for calculating ‘frozen capital’ is as follows:

o Annual spending on ‘leasable’ healthcare equipment categories is identified.

o This sum is then reduced by the healthcare leasing penetration rate derived from

Siemens’ own proprietary information for the equipment types being studied

The remaining sum is regarded as largely ‘frozen’ in that it has been locked-in to outright

purchases. If asset finance, in the form of leasing and rental, was deployed, payments could

have been spread – as monthly payments – across the lifetime of the asset, and therefore

better aligned to the efficiency savings that the asset is delivering.

The detailed statistics from the research are summarised below:

Note: Categories covered in ‘Other Equipment’ include:-

Endoscopy

Dialysis

Anaesthetics

Respiratory management

Transfusion & IV

Ophthalmics

Sterilisation

Lithotripsy

Monitoring

Resuscitation

Surgery and electro-surgery

8

Our research shows that frozen capital remains widespread in global healthcare systems.

Among the European countries examined which all have a public healthcare system,

Germany shows the highest level of frozen capital at just over €5 billion in 2011, followed by

the UK at €2.4 billion and France at €2.3 billion. The fact that frozen capital in Germany is

disproportionately higher than the two other large economies of Western Europe may be

ascribed to the higher density of medical equipment prevalent in the German healthcare

system, exemplified in the number of CT scanners per million population (Germany 16.4, UK

7.4 and France 11) or the number of MRI units per million population (Germany 8.6, France

6.1 and UK 5.6).2

Our results also indicate that significant amount of capital is trapped in the healthcare

systems of developing economies including China, Russia, India and Turkey. As these

developing countries are rapidly expanding their healthcare sector and healthcare

infrastructure to fulfil growing needs and demands, spending on the healthcare is

constantly on the rise. However, in their zeal to modernise their healthcare systems,

inefficient use of capital due to outright purchasing of medical equipment ends up tying up

capital funding, further highlighting the importance of employing financing techniques which

allow for a much more efficient and effective use of funds. Though unlike many developed

countries, these developing economies still have a comparatively low frozen capital per

capita as their governments are only ramping up healthcare expenditure in recent years

in the face of burgeoning economic developments.

Frozen capital is a concept that applies to healthcare systems largely funded out of the state

funds or quasi mandatory health insurance reimbursed at regulated levels. The United

States, however, presents a system which uses fundamentally different funding

mechanisms. Investment grade hospitals (making up perhaps one third of US hospitals) tend

to issue tax-exempt bonds to raise low interest-rate funds for capital projects. Non-

investment grade hospitals will use bank loans, attract philanthropic donations (as do

investment grade hospitals), and access a basket of other financing sources for capital

spending. Asset finance and leasing is widely employed, but cannot be seen as freeing up

“frozen capital” in the same way as healthcare systems in the rest of the world. On the other

hand, there is evidence that asset finance techniques such as leasing are predicted to

increase their penetration of the US medical equipment market as a whole. This is the

subject of the following chapter of this paper.

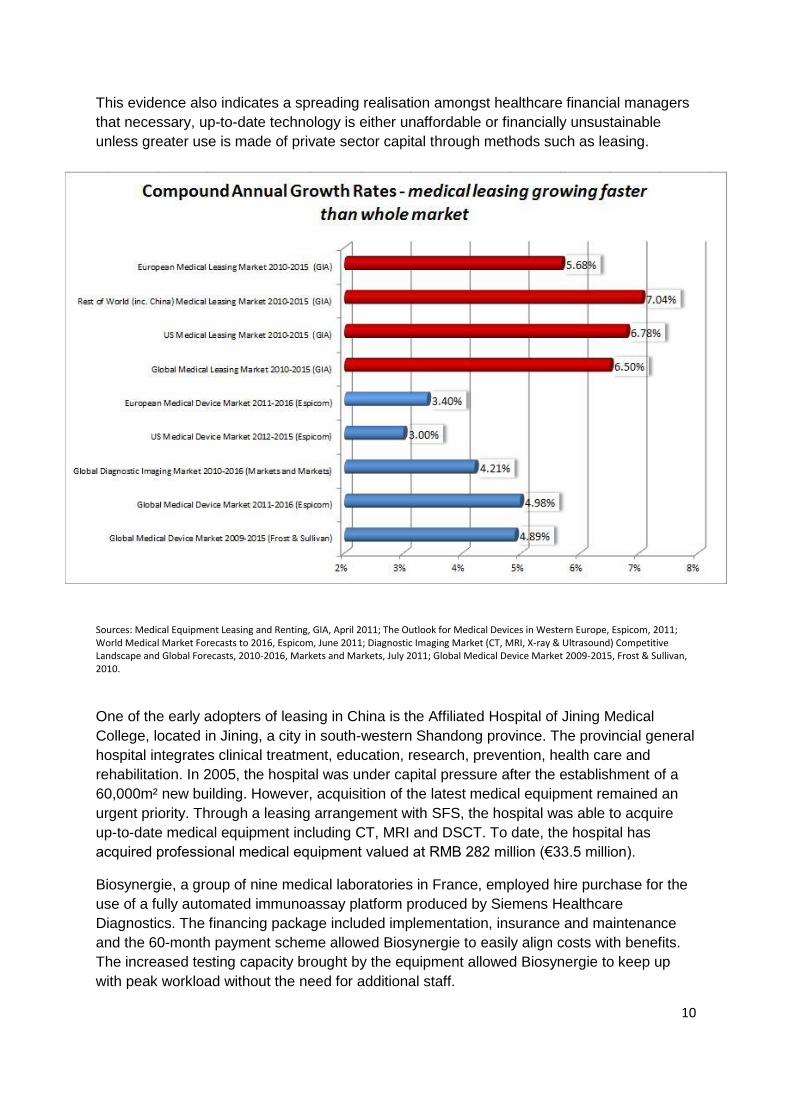

Growth of Asset Finance is Outpacing Market Growth

Evidence is emerging that the use of efficient financing techniques, such as leasing, is on

the rise throughout the world. In countries where healthcare is largely state- or state-

insurance funded, this change in the financing landscape is gradually helping to address the

frozen capital challenge. In 2011, the European market for medical equipment rental and

leasing is estimated at €8.4 billion (US$11.2 billion) in 2011. In 2017, the market is projected

to reach €11.9 billion (US$15.9 billion), registering a compound annual growth rate (CAGR)

2 OECD Health Data 2010; Eurostat Statistics Database.

9

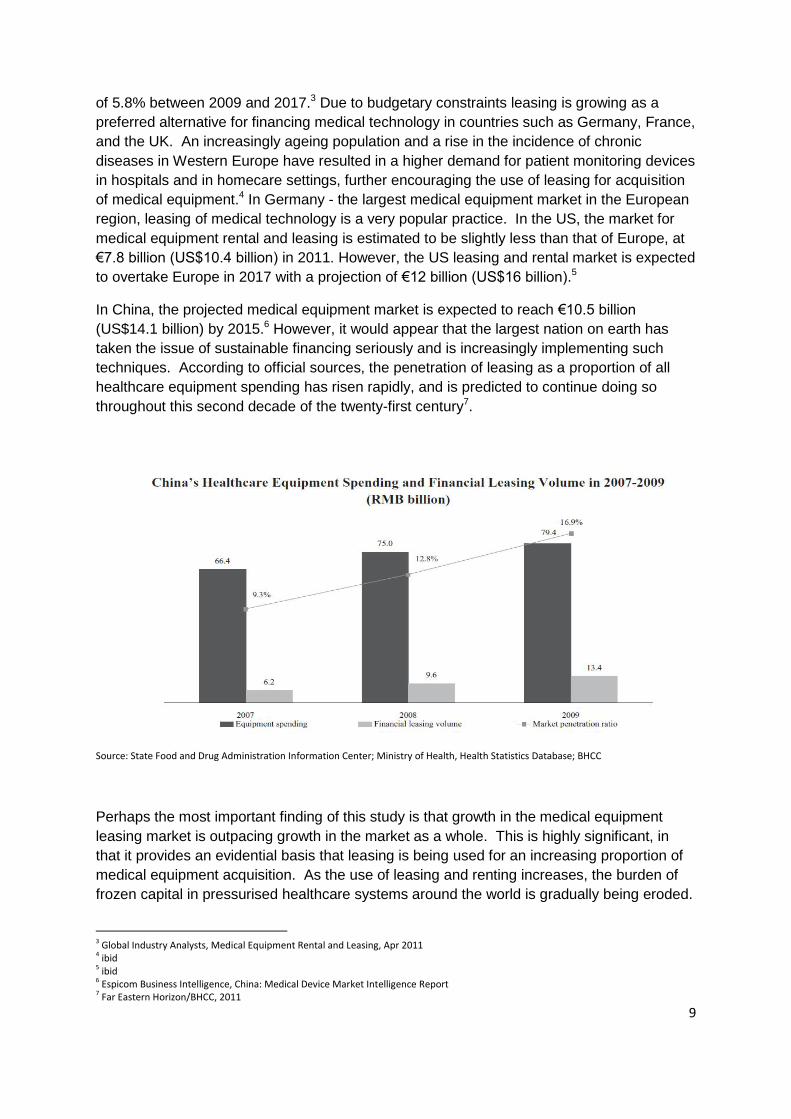

of 5.8% between 2009 and 2017.3 Due to budgetary constraints leasing is growing as a

preferred alternative for financing medical technology in countries such as Germany, France,

and the UK. An increasingly ageing population and a rise in the incidence of chronic

diseases in Western Europe have resulted in a higher demand for patient monitoring devices

in hospitals and in homecare settings, further encouraging the use of leasing for acquisition

of medical equipment.4 In Germany - the largest medical equipment market in the European

region, leasing of medical technology is a very popular practice. In the US, the market for

medical equipment rental and leasing is estimated to be slightly less than that of Europe, at

€7.8 billion (US$10.4 billion) in 2011. However, the US leasing and rental market is expected

to overtake Europe in 2017 with a projection of €12 billion (US$16 billion).5

In China, the projected medical equipment market is expected to reach €10.5 billion

(US$14.1 billion) by 2015.6 However, it would appear that the largest nation on earth has

taken the issue of sustainable financing seriously and is increasingly implementing such

techniques. According to official sources, the penetration of leasing as a proportion of all

healthcare equipment spending has risen rapidly, and is predicted to continue doing so

throughout this second decade of the twenty-first century7.

Source: State Food and Drug Administration Information Center; Ministry of Health, Health Statistics Database; BHCC

Perhaps the most important finding of this study is that growth in the medical equipment

leasing market is outpacing growth in the market as a whole. This is highly significant, in

that it provides an evidential basis that leasing is being used for an increasing proportion of

medical equipment acquisition. As the use of leasing and renting increases, the burden of

frozen capital in pressurised healthcare systems around the world is gradually being eroded.

3 Global Industry Analysts, Medical Equipment Rental and Leasing, Apr 2011 4 ibid 5 ibid 6 Espicom Business Intelligence, China: Medical Device Market Intelligence Report 7 Far Eastern Horizon/BHCC, 2011

10

This evidence also indicates a spreading realisation amongst healthcare financial managers

that necessary, up-to-date technology is either unaffordable or financially unsustainable

unless greater use is made of private sector capital through methods such as leasing.

Sources: Medical Equipment Leasing and Renting, GIA, April 2011; The Outlook for Medical Devices in Western Europe, Espicom, 2011; World Medical Market Forecasts to 2016, Espicom, June 2011; Diagnostic Imaging Market (CT, MRI, X-ray & Ultrasound) Competitive Landscape and Global Forecasts, 2010-2016, Markets and Markets, July 2011; Global Medical Device Market 2009-2015, Frost & Sullivan, 2010.

One of the early adopters of leasing in China is the Affiliated Hospital of Jining Medical

College, located in Jining, a city in south-western Shandong province. The provincial general

hospital integrates clinical treatment, education, research, prevention, health care and

rehabilitation. In 2005, the hospital was under capital pressure after the establishment of a

60,000m² new building. However, acquisition of the latest medical equipment remained an

urgent priority. Through a leasing arrangement with SFS, the hospital was able to acquire

up-to-date medical equipment including CT, MRI and DSCT. To date, the hospital has

acquired professional medical equipment valued at RMB 282 million (€33.5 million).

Biosynergie, a group of nine medical laboratories in France, employed hire purchase for the

use of a fully automated immunoassay platform produced by Siemens Healthcare

Diagnostics. The financing package included implementation, insurance and maintenance

and the 60-month payment scheme allowed Biosynergie to easily align costs with benefits.

The increased testing capacity brought by the equipment allowed Biosynergie to keep up

with peak workload without the need for additional staff.

11

In Germany, Diagnosticum Ingolstadt was able to finance a magnetic resonance imaging

3.0T Magnetom Verio as well as an Axiom Aristos MX with the aid of a leasing solution.

During the move and start-up periods, liquidity could be preserved as a result of a payment-

free phase. The progressive payment schedule was based on the principle of “pay as you

earn”. Moreover, payments could be adjusted to the customer’s earnings situation during the

contract term.

In addition, a Biograph mMR – the world’s first fully integrated whole-body molecular MR

with simultaneous magnetic resonance (MR) and positron emission tomography (PET)

imaging – was supplied to the German private practice MRI, Nuclear Medicine and PET/CT

Center Bremen Central (MRT-, Nuklearmedizin- und PET/CT-Zentrum Bremen Mitte) in

2011, enabled by a SFS financing contract. This represents the first use of the system by a

private practice for the routine examination of patients. With the Biograph mMR, state-of-

the-art 3T MRI and cutting-edge molecular imaging can be fully integrated as one, thus

allowing for highly accurate imaging and new insights into the progress of disease.

The Benefits of Investment in Up-to-date Medical

Technology

Although capital equipment investment represents just 5% of health spending in the health

system of most countries, access to up-to-date healthcare technology often has a

disproportionately large impact on the ability to deliver better health outcomes and operating

efficiencies.

For many conditions, up-to-date healthcare technology enables faster, better diagnoses and

treatments, with throughput rates that help reduce the cost per procedure, either through

early intervention, or by avoiding costly and invasive exploratory surgery, or by improving

recovery times so that the days spent in hospital are radically reduced.

In Germany, for example, Stuttgart Klinikum has invested €14.3 million in the modernisation

and expansion of its imaging systems for diagnostic and therapeutic purposes. Through to

2017 a total of 43 systems, including computer tomography, magnetic resonance imaging,

PET-CT, angiography and radiological equipment will be gradually installed in its four

hospitals.8

With the installation of the latest medical radiology equipment patients can benefit from a

faster, better and more precise treatment experience. With the new PET-CT, which

combines positron-emissions-tomography (PET) with molecular imaging and computer

tomography (CT) in a single device, tumours in the body can be more accurately located,

thus allowing for an earlier and more targeted therapy. A full body examination which used to

take 60-70 minutes can now be finished within 7-8 minutes with the help of a modern PET-

CT – with an improved image quality.

The new CT scanner also enables faster examination and procedures. The duration of a

lung examination can for example be reduced from 10 seconds to just half a second. The

8 Klinikum Stuttgart, Klinikum Stuttgart investiert über 14 Mio. Euro in neue Radiologie, Klinikum, 11 Oct 2010

12

reduction in examination time is a great convenience for patients, especially among children

who tend to need tranquilising medication for CT examinations. A further advantage is the

enormous saving in radiation dose.

In the UK, the Western Trust’s Erne Hospital also invested £125,000 (€152,618) in the

installation of a new echo cardiogram ultrasound machine. Thanks to the advanced

technology quality of images can be enhanced substantially. There is also the option to use

a 3D probe facility where appropriate. Not only does the new equipment improve diagnostic

accuracy, it also contributes to increased efficiency in the assessment process.9

The importance of improved working capital management in the financial supply chain is that

it makes acquisition of the most up-to-date healthcare equipment and technology affordable.

Although capital spending on medical devices only occupies in the region of one twentieth of

total healthcare budgets10, the latest healthcare technology has a disproportionately positive

influence on efficiency and effectiveness. For instance, technological advances have

reduced MRI scan times by up to 75% since the millennium11, not to mention the

improvements in diagnostic imaging.12 The latest technology and equipment often allows

more patients to be diagnosed and treated faster and better, which in return leads to better

clinical outcomes and a more efficient cost-per-treatment.

As patient/physician choice increases and payment for health service provision is considered

at the individual patient level, there is mounting pressure on healthcare institutions to

improve treatment efficiency by means of the latest technology. It is crucial for both public

and private healthcare service providers to find an affordable method of acquiring up-to-date

technology if they are to attract additional patient volumes through high quality services.

This is an urgent issue in particular for developed countries which have substantial budget

deficits in their healthcare systems. To avoid finding themselves trapped in a similar financial

predicament, developing economies with rapidly evolving health systems should also

examine the use of asset finance in their ambitions to transform their healthcare sector.

9 Western Health and Social Care Trust, £190,000 investment in Cardiac Services at Erne Hospital, Western Health and Social Care Trust, 3 Aug 2010 10 Data sources for estimates include: OECD, WHO, National Accounts, Espicom, Forrester, Frost & Sullivan 11 Siemens Medical, MAGNETOM literature 12 A. G. Sorensen, Advancements in MRI Scanner Technology Lead to Improved Functional Imaging, Electromedica 68

13

Conclusions

This paper provides clear evidence, from Siemens-commissioned research and from third

party research sources, that medical equipment leasing and renting is making progress to

free up ‘frozen capital’ in healthcare systems around the world. In the US, where the frozen

capital concept does not apply, leasing is predicted to outpace market growth in coming

years, increasing the proportionate use of this financing tool in the healthcare sector. The

statistics presented in this report indicate that annual growth rates for medical equipment

leasing and renting is outpacing growth in the healthcare equipment market as a whole. The

natural conclusion from this data is that a steadily increasing proportion of healthcare

equipment is being acquired through an efficient financing plan, in the form of leasing or

renting, rather than tying up (or ‘freezing’) precious and scarce public sector capital.

In mature economies, the motivation to use asset finance is mainly focused on capital

budget pressure and equipment affordability. Healthcare costs continue to outpace

stretched public capital, and only by accessing private sector capital will future investment

needs be met. In developing economies, financial sustainability is the key concern, so that

rapidly developing infrastructure does not take on a debt burden that will quietly build up only

to cause financial problems in decades to come. State authorities are extremely concerned

that medical equipment investments should be sustainable, should not be allowed to

escalate, and can be seen to provide efficient return on investment. The transparency and

cash-flow friendliness of asset finance help to support these requirements.

Finally, affordable access to up-to-date technology has a disproportionately positive effect on

increasing patient throughput rates, reducing cost-per-treatment/diagnosis, and improving

patient outcomes. Therefore, access to asset finance allows healthcare organisations to

make more financially transparent and sustainable investments in equipment that allows

them to improve diagnosis and treatment efficiency and effectiveness, thereby improving

return on investment

14

Country Backgrounders

China

In 2009, China kicked off its three-year, RMB850 billion (€100 billion) healthcare reform with an aim to

extend healthcare to every Chinese citizen by 2020. Currently, more than 95 per cent of the nation’s

population are already covered by medical insurance.13

However, access to healthcare and

affordability of services still remain major issues to be overcome. As public hospitals are expected to

generate revenue earned from fees, tests and medicines to cover 70-90% of their operating

expenses, they command a high degree of operating autonomy and hospital managers are generally

free to raise revenue from patients.14

The high degree of operational autonomy has inevitably been occasionally subject to abuse such as

expensive, and unnecessary, fees, prescriptions or clinical tests. The profit-driven operating principle

has also given rise to an uneven service quality of healthcare provision. As larger hospitals have the

equipment and expertise needed to attract patient revenue, they tend to become larger and better-

equipped. In contrast, small hospitals lack the funding to invest in staff and equipment, consequently

failing to attract the same level of patients. They are therefore caught in a self-reinforcing vicious cycle

as fewer patients inevitably mean less revenue and a subsequent deterioration of the service

provided.15

At the moment, Chinese citizens still have a relatively high out-of-pocket share in healthcare

expenses. At the end of 2010, nearly 36 per cent of total health spending in China was borne by out-

of-pocket spending. This is, however, already a considerable reduction from 60 per cent in 200116

.

The Ministry of Health has planned to further reduce the share of out-of-pocket payments to 30 per

cent by 2015. Given that the out-of-pocket share in most countries with universal health coverage is

less than 30 per cent, the attainment of the goal would signify a milestone on China’s journey in

providing effective health coverage for its citizens.17

In comparison to many developed countries, China’s healthcare expenditure is still relatively low. In

2009, China spent 4.3 per cent of GDP on healthcare - less than half the OECD average18

. Even

though the government has pledged more health funding in the coming years, it starts from the

premise that local governments, who shoulder most public health financing, will continue to register

robust revenue increase at the local level. This, however, is likely turn out to be a volatile premise.

Revenues from land sales usually constitute a vital source of funding for local governments. Land

sales during the first eleven months of 2011 was disappointing, with local government revenue

decreased by 30 per cent compared with the same period in 2010.19

Consequently, there are some

question marks over government’s ability to finance healthcare in coming years.

The healthcare sector is put under further financial strain by a rapidly aging demographic as well as

the prevalence of chronic diseases. Today, China has 160 million people over 60 years of age and

that number is expected to rise to 240 million people by 2020. Incidences of cancer are increasingly

comparable to the OECD average. The number of cardiac patients in China is already growing at a

20-30 per cent annual rate. It is also estimated that between 2000 and 2025, the number of patients

13 China Daily, Universal healthcare is within reach, 13 January 2012 14 Espicom Business Intelligence, China: Medical Device Market Intelligence Report 15 Espicom Business Intelligence, China: Medical Device Market Intelligence Report 16 Xinhua, Personal spending on health expenditures decreasing in China: Minister, 6 January 2012 17 China Daily, Universal healthcare is within reach, 13 January 2012 18 Insight, Chinese Healthcare Reform and the Medical Device Sector, May 2011 19 China Daily, Universal healthcare is within reach, 13 January 2012

15

will increase by nearly 70 per cent, admissions to hospital more than 43 per cent, and overall medical

spending more than 50 per cent.20

Apart from the challenge of containing substantial healthcare costs, the government must also

address the issue of access by enhancing service capacity of underdeveloped hospitals in rural areas

and urban communities.21

A key component of the government’s healthcare reform is to build 2000

county-level hospitals (best equipped hospitals in the country with at least 250 beds). The government

also aims to establish village clinics in remote areas so that every village will have at least one unit by

the end of 2012. At the same time, 3700 community health centres and 1,000 community health

stations are to be established or upgraded in cities. Township-level or higher level health centres will

also provide X-ray apparatus, type-B ultrasonic devices and life support machines as standard.22

With the government’s commitment in expanding the healthcare infrastructure, the prospects for

medical device spending is huge. In 2010, the Chinese medical device market was valued at US$7.4

billion (€5.5 billion), making it the 6th largest market in the world.

23 To aid development of public

healthcare infrastructure, medical equipment leasing will emerge as a viable financial means in the

delivery of higher standard and more cost-efficient healthcare services. Indeed, it will also maximise

the benefits of health services’ end users by channelling government funding to the demand side

(patients) to reduce individual healthcare cost, in particular for those who cannot afford quality

healthcare.

India

India’s healthcare is state and territory-organised. It is estimated there are nearly 8000 hospitals in

India, around half of them are owned and operated by the state or local government. The charitable

sector owns and operates a further 25% with the rest, usually smaller units, operating privately24

.

However, for the majority of Indians, in particular the poor, accessible and affordable healthcare is still

an ambition, rather than a reality. Every year more than a million Indians die due to lack of healthcare

access. Some 700 million Indians in the villages and rural areas do not have access to healthcare

facilities because around 80% of the specialists and medical facilities are located in urban areas.

Around 250 million Indians live below the poverty line (BPL) and survive on less than Rs100 (€1.5)

per day, making it almost impossible for them to afford medicines.25

The World Health Organisation

(WHO) suggested that about 70% Indians are spending their out-of-pocket income on medicines and

healthcare services in comparison to 30-40% in other Asian countries such as Sri Lanka, yet they are

still suffering from infectious diseases due to lack of best quality drugs and healthcare facilities26

.

At the moment, less than 15% of the Indian population is covered under some form of health

insurance, including government-supported schemes. Only around 2.2% of the population is covered

under private health insurance. With a number of private players and foreign players entering the

market to meet increased demand, healthcare insurance market is expected to grow at a CAGR of

15% till 2015. At the current rate of growth only 50% of India’s population would have health

insurance coverage by 2033.27

20 Insight, Chinese Healthcare Reform and the Medical Device Sector, May 2011 21 Xinhua, China’s community clinics to boost capacity, 7 January 2012 22 Espicom Business Intelligence, China: Medical Device Market Intelligence Report 23 ibid 24 The Guardian, BRICs build healthy economic growth but uncertain healthcare, 13 July 2012 25 PWC, Healthcare unwired – Health insurance and healthcare access, March 2011 26 The Times of India, Indians' growing healthcare expenses concern WHO, 2 November 2011 27 PWC, Healthcare unwired – Health insurance and healthcare access, March 2011

16

Indian healthcare expenditure is still amongst the lowest globally. Over 80% of health financing is

private financing, illustrating the scale of the funding problem.28

In its 12th Five Year Plan commencing

April 1, 2012, India has pledged to increase spending on healthcare from the present level of around

1 per cent of the GDP to 2.5 per cent. One of the focus areas of the Plan is the development of

healthcare facilities. It targets to invest over US$1 trillion (€750 billion) in infrastructure development.

It aims to provide “complete basic infrastructure” in rural areas by the end of the next five year plan

period by upgrading existing primary health centres and community health centres to Indian public

health standards’ norms. The plan also aims to strengthen diagnostic services at block and district

levels and provide ancillary services at district levels such as drug storage, warehousing, medical

waste management etc..29

The Indian market for medical equipment and supplies is valued at around US$2,352 million (€1,760

million) in 2010. The market remains disproportionately small despite strong growth rates. Diagnostic

imaging apparatus is the largest segment of the Indian market, accounting for 36.3% of the total at a

total value of US$854 million (€639 million) in 2010. This category is expected to reach US$1,665

million (€1,246 million) by 2015 at a CAGR of 14.3% between 2009 and 201530

. In view of growing

private sector investment in healthcare since the mid-1980s, it is expected that private sector

hospitals and medical centres will continue to accelerate future increased demand for medical

equipment and supplies.

Booming population, ageing demographic, emergence of lifestyle-related diseases due to a

burgeoning middle class and limited government funding mean that the Indian healthcare system is

severely overloaded und underfunded. To create new capacity and tap financing, the government is

increasingly embracing Public-Private Partnership models. It is also encouraging foreign direct

investment (FDI) in opening of hospitals by placing such investments on the fast track for official

approvals.31

At present, the market for medical equipment leasing is still in its nascent stage.

However, in its zeal to develop healthcare infrastructure across the vast nation, coupled with

increased demand for expensive and high-technology equipment from the private healthcare sector,

the Indian market provides ample opportunities for leasing. Asset financing techniques will serve as a

critical tool for the affordable acquisition of medical technology on a large scale, it will also be

instrumental in improving financial efficiency in the current healthcare landscape.

28 The Guardian, BRICs build healthy economic growth but uncertain healthcare, 13 July 2012 29 Zeenews, Healthcare spending to be raised to 2.5% of GDP: Azad, 7 January 2012 30 Espicom Business Intelligence, India: Medical Device Market Intelligence Report 31 KPMG, Current State of Healthcare in India, 17 February 2012

17

Germany

The German healthcare system has seen newly introduced major reforms in 2011 that are expected

to reduce a deficit for 2011 that would otherwise have amounted to some €9 billion.32

In order for this

reform to be successful, aggregated savings of €11billion are being funded by tax payers, public

insurers, health insurance providers as well as the pharmaceutical and medical industries and

healthcare sector personnel.

An additional tax has been put in place to raise €2 billion from all German tax payers, while those in

public insurance have also seen their fees rise in order to save €3 billion. The medical sector was

targeted to reduce costs by €3 billion through limits on spending. This should primarily have affected

the pharmaceutical industry with a share of two thirds of this amount. Finally, employers were to

contribute €3 billion in fees for their employees.33

Public health care costs in Germany are split almost

even between employees and employer, with a slightly bigger burden on the employee’s side.

German citizens enjoy a wide range of healthcare services covering preventive services,

comprehensive inpatient and outpatient hospital care, office-based physician services, mental health

care, dental care, prescription drugs, medical aids, rehabilitation, and sick leave (short-term disability)

compensation. In order to improve treatment quality while being cost effective, the government aims

to create a more diverse insurance landscape with more competition. As insurance fees are rising,

patients are now allowed to change their provider at a shorter notice for one that better suits their

needs. At the same time, unprecedented measures have been put in place that keeps healthcare

affordable for the economically less fortunate. The aforementioned tax of €2 billion for all Germans,

regardless of their type of insurance, is meant to support this social group.

In order to improve diagnoses, Germany - together with many other countries – has seen a dramatic

increase in the use of CT and MRI scanners. Between 1996 and 2008 the number of CT scans has

more than doubled34

, the number of MRI scans has quadrupled 35

, often replacing X-Ray. In this

context, the German Federal Office for Radiation Protection has reported that the contribution of CT

scans to the total frequency and collective effective dose of radiation accounted for 60% in 2008. In

this regard, the usage of up-to-date technology offers clear advantages: modern equipment can

reduce the radiation dose as well as the scanning time (for a whole body scan, reducing the time

taken from sixty minutes to as low as seven)36

, making the procedure more bearable and accurate for

patients, and especially children.

To finance these increased equipment investments, and to be able to afford regular upgrades of

technology, healthcare procurement is becoming less wedded to the idea of ownership. The

traditional notion of ‘sweating the asset’ is looking increasingly antiquated in the light of the quickly

evolving technology of today’s medical landscape, where a piece of equipment is out-dated long

before standard 7-10 year write-off periods are completed. Asset finance allows healthcare

organisations to upgrade their technology in broad line with technology developments without having

to write down the full capital cost of purchase. Additionally, the variety of available leasing contracts

include regular upgrades, maintenance and service according to individual needs. To meet the

principles of Germany’s latest healthcare reform initiative - high quality diagnosis and treatment in a

responsible and financially sustainable way - asset finance is becoming a recognised as a key

enabling factor.

32 Bundesministerium für Gesundheit; REGIERUNGonline, Die Gesundheitsreform 2011, Berlin, December 2010 33 ibid 34 Bundesministerium für Strahlenschutz, Strahlenexposition durch medizinische Maßnahmen, S.245 35 Bundesministerium für Strahlenschutz, Strahlenexposition durch medizinische Maßnahmen, S.250 36 Klinikum Stuttgart, Press Release, 11 October 2010

18

France

France, like most of its European neighbours, relies heavily on statutory health insurance to fund and

maintain its high quality of care in both its private and public health care services.

The country’s level of healthcare expenditure, however, has now reached over 12% of GDP, and in

2010, the healthcare deficit of €11.6 billion was the biggest source of France’s substantial Social

Security deficit, estimated at €18.1 billion. This prompted various reform programmes, such as the

2009 HPST law (Hôpital, Patients, Santé et Territoires) and its subsequent activity/performance pools

in every hospital, aimed at curtailing costs and improving efficiency in the healthcare system.

Unsurprisingly, the current economic downturn is increasing financial pressures on the health service,

with austerity measures succeeding in reducing the health care deficit to €9.5 billion in 2011, aiming

to reach €5.9 billion in 2012.37

However, numerous sources expect France’s health expenditure to

remain around 12% of GDP from 2011 to 2015.38

In its healthcare reform plan, the French Government’s DGOS (Direction Générale de l’Offre de

Soins) has consistently reduced reimbursement tariffs, both for drugs and for equipment, and as of

October 2011, has strengthened its application of the HPST law by launching a new programme,

dedicated solely to hospital purchasing. By pooling regions’ hospital resources and setting strict

standards for increased performance and efficiency for purchasing, among other measures, the

national PHARE programme is expected to bring savings of €910 million within the next three years.39

This focus on healthcare purchasing efficiencies will no doubt have to incorporate the urgent need for

modernisation and acquisition of new equipment: although the French medical device market is the

fourth largest in the world, per capita spending on medical products is low. Some sectors remain

underdeveloped, particularly for the more innovative forms of technology such as diagnostic imaging,

which made up 19.1% of the market in 2010, with the slowest growth (7.7%) in all types of healthcare

spending per capita, following a complete standstill in 2009.40

Various investment programmes, such as the (extended) Hospital 2012 plan, the 2009-2013 Cancer

Plan, and the five-year Alzheimer programme launched in 2008, all target the increased demand for

screening and diagnostic imaging equipment, aiming to provide 10 MRI scanners per million

population. Nevertheless, this will still leave France lagging behind the European average of 13.5

units per million population.41

Up to now, as witnessed by technology manufacturers’ private data on replacement rates, French

healthcare equipment has remained relatively up-to-date, as a result of the French reimbursement

system. However, the country’s healthcare system is facing the challenge of a major deficit, funds will

not remain available for the same level of capital purchasing, and equipment will be at risk of

becoming outdated. France will still have to face the same challenges and increased demands

witnessed all over Europe: an ageing population, unhealthy lifestyles, and the rise of chronic diseases

all call for patient-driven demands, such as preventive measures heavily reliant on screening and

imaging procedures, which combine to put additional pressure on hospital and care spending.42

37 Ministère du Tavail, de l’Emploi et de la Santé, Loi de Financement de la Sécurité Sociale 2012 en chiffres, 2012, 38 Espicom Business Intelligence, France: Medical Device Market Intelligence Report 39 Ministère de la Santé, 2 February 2012 40 Espicom Business Intelligence, France: Medical Device Market Intelligence Report 41 Espicom Business Intelligence, France: Medical Device Market Intelligence Report 42 Albouy Valérie, Bretin Emmanuel, Carnot Nicolas, Deprez Muriel, Les Dépenses de santé en France : Déterminants et impact du vieillissement à l’horizon 2050, Les Cahiers de la GTPE, July 2009,

19

In the current economic climate, the drive for efficiency gains and cost cutting measures is set

alongside the crucial need for state of the art medical equipment which positively impacts the

economic performance of healthcare organisations. As all eyes are turned to cost-efficient

management and purchases, French public and private health care organisations are likely to rely

increasingly on leasing and financing solutions, specifically for the radiotherapy and imaging

equipment, as these options provide an affordable and easily manageable way to achieve high

performance in the context of constrained budgets.43

UK

According to the Commonwealth Fund survey, Britain’s healthcare system is consistently rated as one

of the best in the world.44

Despite the fact that per capita health spending in the UK is the third lowest

among the 11 high income countries surveyed, at £2,170 (€2,596) per head, compared with £3,200

(€3,828) in Switzerland and £4,950 (€5,921) in the US, the survey finds that people in Britain have

among the fastest access to GPs, the best coordinated care, and suffer from among the fewest

medical errors45

.

The scale of the NHS is vast: every month 21 million people visit their GP surgery, while every day

community pharmacists dispense 2.3 million prescription items and 13,000 people call NHS Direct.46

The challenges of an ageing population and increasing chronic illness will further raise the costs of

healthcare services. Estimates suggest that demographic change will cost the NHS an extra £1 billion

(€1.2 billion) every year alone.47

Clearly, there is an urgent need to cut back on the mounting costs

while introducing measures to improve productivity and efficiency of the NHS. Under the coalition

government’s spending review the NHS has to achieve efficiency savings of £20 billion (€23.9 billion)

by 2015.48

The government has also introduced a Health and Social Care Bill, which at the heart of it,

aims to drive more competition in health services and pass control over commissioning to general

practitioners. It is hoped that the Bill will allow patients to be more involved in decisions about their

treatment and care, and that the NHS will be more focused on results that are meaningful to patients

by measuring outcomes such as how successful their treatment was and their quality of life.49

At a time that the NHS is confronted with the unprecedented challenge of delivering 4% annual

efficiency savings in the four years to 2015, the National Audit Office found in a 2011 report that £500

million (€598 million) is potentially being wasted because of poor procurement.50

The report found that

the NHS is spending too much on scanners and radiotherapy equipment and is not using it intensively

enough. This is mainly because the NHS trusts are not co-operating in their purchasing decisions.

Between 2004 and 2007 the Labour government invested some £400 million (€478 million) in capital

equipment to reduce waiting times. Nevertheless, hospitals in Britain still have fewer high-tech

medical machines than those in poorer countries such as Estonia and Turkey. The NHS in England

had 6 MRI machines per million population in 2010, with figures across Britain putting the country

below the Slovak Republic, Turkey, Estonia and Ireland in a league table of provision. For CT

scanners, there were 8.4 per million population in Britain in 2010 in comparison to about 30 in Greece

43 Global Industry Analysts, Inc. Medical Equipment Rental and Leasing, A Global Strategic Business Report, April 2011 44 The Commonwealth Fund, Why not the best? Results from the national scorecard on US health system performance, 2011, October 2011 45 Daily Telegraph, NHS ‘among best health care system in the world’, 11 November 2011 46 Department of Health, innovation Health and Wealth: accelerating Adoption and Diffusion in the NHS, 5 December 2011 47 The Guardian, NHS budget increase of 0.1% is nowhere near enough, 13 April 2011 48 Health Equipment Supplies, Report claims 'unprecedented' cuts to health budgets mean quality of services cannot be assured and suppliers could lose out, 16 December 2010 49 Department of Health, Health and Social Care Bill 2011 50 National Audit Office, Managing high value capital equipment in the NHS in England, 30 March 2011

20

and about 15 in Czech Republic. While there were 13 Linac machines per million population in the

Slovak Republic, there were just 4.8 in the NHS.51

With most of the CT scanners, MRI scanners and Linac machines installed in the past decade, about

half the machines are due for replacement within three years and 80 per cent within six years. This

will require an investment of about £460 million (€550 million) by 2014, and a further £330 million

(€395 million) in the succeeding three years.52

As NHS spending is squeezed, hospitals are facing a

daunting challenge of finding money from revenue budgets and loans to replace old machines and

purchase new ones.

The NAO report said that the number of diagnostic scans carried out using these machines has

increased almost three fold over the past decade. Demand for scans is expected to rise to support

early diagnosis. In order to afford necessary equipment investments, asset finance techniques are

now becoming part of the recommended financial armoury of healthcare managers, with NHS Supply

Chain guidance specifically citing the issue of ‘frozen capital’ and highlighting the benefits of leasing53

.

As highlighted by the Department of Health in its Innovation Health and Wealth report, procurement is

an important lever for economic growth, a potential driver for better public service and a means of

stimulating innovation. The department has subscribed itself to the goal of improving arrangements

for procurement in the NHS to drive up quality and value.54

Indeed, NHS trusts are already

increasingly turning to leasing as an affordable way of purchasing the most up-to-date technology,

with NHS Supply Chain witnessing a 2011 increase in the value of the businesses awarded through

its framework by 35% and the volume of tenders by 11%.55

Spain

Spain’s universal public healthcare system is also ranked among one of the best in the world. Its free

services and subsidised drugs funded by the autonomous regions are embraced by the country’s

citizens to such an extent that they have shown a rising expenditure of nearly 10% annually since

2002.56

This accounts for the second-biggest government expense after pensions.57

Despite low

expenditure by global comparison, budgets are said to have overrun by 15%58

. Plummeting tax

revenue as a result of the economic crisis has added its part in the deficit.

Spanish healthcare costs need to decrease, and in fact, have done so over the last years from €1,344

per capita (2010) to € 1,210 (2012)59

, but further savings are essential. Cutting health costs at a time

when the country is struggling to ward off an international bailout in line with the reduction of the

overall public-sector deficit from 9.3% of gross domestic product in 2010 to 3% by 201360

is of major

importance.

Much of the debt is borne by drug companies and health-care technology suppliers. They are owed

€12 billion61

by the regions who are subsidising the services. However, the public purse is stretching

51 Daily Telegraph, Britain has fewer high-tech medical machines than Estonia and Turkey, 30 March 2011 52 Financial Times, Watchdog attacks NHS kit costs, 30 March 2011 53 NHS, NHS Supply Chain launches new leasing contract, 4 June 2010 54 Department of Health, innovation Health and Wealth: accelerating adoption and diffusion in the NHS, 5 December 2011 55 Building Better Healthcare, NHS capital funding crisis leads to increase in leasing, 7 February 2012 56 Wall Street Journal, Spain's Shortfall in Health Care Causes Alarm, 5 July 2011 57 ibid 58 The Economist, Health spending in Spain- Fat-trimming needed, 17 September 2011 59

El Pais, Fall in Spanish Healthcare costs predicted for 2012, 5 January 2012 60 Wall Street Journal, Spain's Shortfall in Health Care Causes Alarm, 5 July 2011 61 ibid

21

the payment period to an average of more than one year.62

Some suppliers have already warned

hospitals that they may stop deliveries63

. This could force authorities into a reform that demanded

more personal co-payments.

Spain’s wealthy but highly-indebted province Catalonia has already begun measures to tackle the

situation. Catalonia has announced a one-euro charge for patients who get prescriptions from the

public health service to be introduced in May 2012.64

Additionally, in order to reduce expenditure on

health care by 6% this year, thousands of workers are being laid off, and initiatives are being

introduced to reduce hospital hours or rent out facilities to private clinics.65

While these activities do

cut costs, it is also feared they may impair the quality of public healthcare.

Spain is yet another country facing the challenge of maintaining healthcare quality, while at the same

time reducing expenditure. As a leader in the use of Public Private Partnerships, the country has

already embraced the need for private and public sector collaboration. Asset financing techniques that

help align costs with reimbursements are critical to effective financial management. They also avoid

the rising maintenance and servicing costs (whole life costs) associated with ageing equipment.

Poland

With healthcare expenditure representing only 7% of its GDP, Poland has the lowest level of

expenditure in Europe66

. This does not fully cover the costs of required upgrades and new equipment

in healthcare organisations67

.

Poland has also been affected by the economic downturn and its subsequent credit squeeze.

Nevertheless, the country remains on a steady GDP growth path, and can count on the European

Investment Bank’s recent decision to extend €75 million in credit for public sector and SME projects.68

Compulsory state health insurance, administered through the national health fund, is responsible for

the main part of healthcare financing. However, the Polish 1997 constitution, which automatically

triggers corrective measures and budget balancing if public debt rises above 5.5%69

, sets an

imperative of efficiency to all public sector services, and Poland is set to remain under high cost

pressure in the run up to 2050, in order to finance its health care system, which could rise to 10% of

GDP, according to an OECD report.70

In parallel, private healthcare networks are expanding rapidly at an annual rate of 20%. The value of

the Polish private healthcare market is estimated to exceed PLN20 billion (€4.8 billion) by 2014. This

will be in conjunction with an average annual growth of 25% for the medical device market in the

same period, rising even further until 2016.71

Indeed, the development of private healthcare infrastructures can be seen as a response to the lack

of public funds to invest in up-to-date medical equipment. Diagnostic imaging, including CT, MRI, X-

62 The Economist, Health spending in Spain- Fat-trimming needed, 17 September 2011 63 El Pais, Drug suppliers warn health-sector debts could lead to treatment shortages, 12 February 2012 64 ibid 65Wall Street Journal, Spain's Shortfall in Health Care Causes Alarm, 5 July 2011 66 OECD, Total Expenditure on Health % GDP, OECD Health Data, November 2011 67 Espicom, The Outlook for Medical Devices in Central & Eastern Europe 68 EIB, Poland, Finance Contracts Signed, February 2012 69 The Constitution of the Republic of Poland 70 OECD, Projected Increase in Public Health and Long-Term Care Spending By Country Over the Period 2005-2050, 71 PMR, Private healthcare market in Poland 2011. Development forecasts for 2011-2013, 2011.

22

ray Angiography, and PET technologies, is still in great need of modernisation. In order to comply with

European ISO norms and sanitary standards, a vast array of the equipment in use until now must be

replaced. As of 2011, 11,000 X-ray machines, for example, must be upgraded to digital X-ray

machines so that healthcare worker and patient safety can be ensured against radiations.72

Whilst high basic costs and rapid consumption of EU funding (for example, approximately 90% of the

ROP - Regional Operational Programmes - resources have already been exhausted73

) have impacted

healthcare spending at the beginning of 2012, private and public healthcare organisations will

nevertheless need to meet growing demand and quality standards. This explains why medical

equipment leasing has been on a fast track in Poland, where 2010 saw leasing deals reaching €130

million in 2010, and was projected to double in 2011.74

Research reports on the subject have

emphasised the appeal of leasing solutions to Polish hospitals by citing the variety of bespoke

financing arrangements to address specific needs of individual practices, clinics and hospitals.

The deadline of 2016, when all Polish healthcare centres have to be strictly aligned to EU norms and

certifications, will contribute to the pressure on Polish healthcare organisations to find alternative,

flexible and affordable financing methods to upgrade and acquire new medical equipment.

Russia

Although Russia constitutes one of the world’s fastest growing economies, and reportedly has more

doctors, healthcare workers and hospitals per capita than most other countries, it also faces

considerable challenges in developing its healthcare system to provide quality medical care to its

citizens, and is said by researchers to be unlikely to meet EU standards even by 202075

.

With a 140 million population (of which 13% are over 65)76

, poor lifestyle habits, and a fairly recent

mandatory health insurance system implemented in 1991, healthcare in Russia remains problematic.

Varying widely by region in this vast territory, public hospitals and polyclinics often receive insufficient

funding, bureaucracy and the relative apathy of insurance companies frequently forces patients to pay

for care out of their own pocket, and much equipment used in hospitals is ageing or obsolete77

.

Furthermore, private healthcare is still in the first stages of development, and is not expected to grow

dramatically in the next few years78

.

Health expenditure per capita currently represents only 5.5% of GDP, and is not set to rise above

5.6% before 201579

.

This, added to a growing concern at the numerous reports cataloguing the rising proportion of deaths

linked to alcohol, tobacco and poor infrastructure, has triggered the government to announce new

healthcare investment programmes in late 2011, in continuation of the US$28 billion (€21 billion)

‘Health Project’ in 2005, which has allowed for numerous medical facilities to be upgraded and for

72 PMR, Private healthcare market in Poland 2011. Development forecasts for 2011-2013, 2011. 73 PMR, Private healthcare market in Poland 2011. Development forecasts for 2011-2013, 2011. 74 Global Industry Analysts, Inc. Medical Equipment Rental and Leasing, A Global Strategic Business Report, April 2011 75 RAI Novosti, Russian healthcare 'decades behind EU standards' , 17 March 2011 76 Espicom, The Outlook for Medical Devices in Russia 77 Espicom, The Outlook for Medical Devices in Russia 78 PMR, Private Healthcare Market in Russia and Ukraine 2011 — Development Forecasts for 2011-2013 79 Espicom, The Outlook for Medical Devices in Russia

23

healthcare workers’ salaries to be increased. In 2012 and 2013, a total of US$16 billion (€12 billion)

will be allocated to the healthcare sector.80

Although this extensive spending plan, to be funded by the rise in insurance premiums, aims to

provide more than 100,000 units of modern medical equipment to healthcare establishments81

, it is

still largely dedicated to improving the quality of primary care through free vaccination programmes,

improving general working conditions, and more generally, to reform the country’s healthcare

infrastructure in order to give more responsibility at regional levels.

Experts have been quick to point out that, in order to modernize the 30% of medical institutions

described by the government as ‘hazardous or in need of major repairs’82

, new lines of funding still

need to be found83

. As the country is looking for sustainable ways to both develop its quality of care to

reach EU levels and improve the involvement and participation of its healthcare organisations in the

creation of an efficient, transparent and competitive healthcare system, it faces an approximate

annual increase in healthcare spending of 15%.84

Since this level of spending is unlikely to be realised through taxes and insurance premiums alone,

the main actors in the Russian healthcare sector, in particular private healthcare providers, will need

to look for alternative sources of financing such as asset finance, in order to have a chance of raising

standards to the level of the rest of the world’s healthcare systems, within an acceptable period.

Turkey

Turkey’s healthcare market is experiencing a growth boost, supported by the government’s 2003-

2013 Health Transformation Programme that aims to deliver improved and accessible public

healthcare services across the country. Health status in Turkey is low compared to other OECD and

middle-income countries, and to become part of the EU, needs to meet their guidelines. Most recent

reports reveal that the healthcare expenditure accounted for 6.7% 85

of the GDP in 2009. The

healthcare reform aims to reduce the great regional inequalities in access to healthcare and reduce

fragmentation in financing and delivery of health services – something which has been identified as

contributing to inefficiency and undermining financial sustainability.86

To ensure universal coverage,

public health insurance needs to extend to one third of the population87

, and The General Health

Insurance Scheme (GHIS) enacted by the Turkish Parliament in 2007 standardised the method by

which social security institutions were paid.88

Public health spending as a proportion of total health spending has increased gradually from 67.8% in

2007 to 75.2% in 2009.89

The prospects for the medical device market in Turkey also remain good.

80 International Insurance News: Putin Talks Russia Healthcare Reform, 19 April 2011 81 Modern Russia, Russian health care: A healthy future? , 14 February 2011 82 Modern Russia, Russian health care: A healthy future?,14 February 2011 83 RAI Novosti, Russian healthcare 'decades behind EU standards', 17 March 2011 84 RAI Novosti, Russian healthcare 'decades behind EU standards', 17 March 2011 85 World Health Organisation, Global Health Observatory 86 OECD and IBRD/The World Bank 2008 OECD Reviews of Health Systems 87 Aksan, Ergin, Ocek: The change in capacity and service delivery at public and private hospitals in Turkey: A closer look at regional differences, BMC Health Services Research 2010 10:300 88 88 OECD and IBRD/The World Bank 2008, OECD Reviews of Health Systems 89 World Health Organization National Health Account database

24

Strong import growth trends as well as the expansion of healthcare facilities, coupled with rising

health expenditure, should see the market grow at a rate of 7.4% during the 2011-2016 period.90

Turkeys health care system shows stark regional differences that need to be smoothed: While a major

part of the services provided are public, the private sector is steadily growing, condensed in the most

prosperous areas and shows much higher patient satisfaction rates than public facilities.91

Research

has shown that big surgical operations are carried out in private facilities to a much higher degree,

despite a decrease since the reform has been put into place.92

Further expansion of the healthcare system requires significant financial resources, and due to the

scale of the project, cost-effectiveness should be on the top of the agenda. Besides initial acquisition

and construction costs, reoccurring expenditure for maintenance and upgrade of equipment are

required. Here, private financiers can play a significant role in realising projects, both on a large and

small scale: In order to realise their ambitious plans, Turkey has already administered tenders for 15

PPP hospital projects with costs of over US$5 billion (€3.7 billion)93

that will care for construction and

maintenance for a limited period of time. Institutions can also benefit from private financing in

equipment. Leasing allows to invest in cutting-edge technology with monthly rates that are set against

revenue budgets. Public hospitals that need to gain patients’ trust, may find free working capital to

invest in excellent medical staff in addition to modern equipment.

90 Espicom Business Intelligence, Turkey: Medical Device Market Intelligence Report, Q4 2011 91 Aksan, Ergin, Ocek: The change in capacity and service delivery at public and private hospitals in Turkey: A closer look at regional differences, BMC Health Services Research 2010 10:300 92 ibid 93 White & Case LLP, Aslı Başgöz, Mehtap Yıldırım Öztürk and Meltem Akol, Reform of Turkey’s public healthcare system