memorandum of private placement the bank of rajasthan ... · pdf filefor retaining rs. 2,000...

TRANSCRIPT

Private & Confidential – For Private Circulation Only (This Information Memorandum is neither a prospectus nor a Statement In Lieu Of Prospectus)

Memorandum of

Private Placement This is not an invitation for the public to subscribe to any of the securities of

The Bank of Rajasthan Limited, and hence not a Prospectus

(Incorporated on May 7, 1943 under the Mewar Companies Act)

Registered Office Clock Tower , Udaipur- 313 001

Tel: 0294 - 2521257 / 2422116 Fax no : 0294 - 2525709

Email: [email protected] Website: www.bankofrajasthan.com

Corporate Office Raghuvanshi Mills Compound,

11/12, Senapati Bapat Marg, Lower Parel (West), Mumbai – 400 013.

Phone : 91-22-30400006 Fax : 91-22-30400019

Email : [email protected]

Private Placement of 700 Unsecured, Non-Convertible, Redeemable, Subordinated Bonds in the nature of Promissory Notes Series IV of face value Rs. 10 Lakhs each for cash at par aggregating Rs. 7,000 Lakhs including green-shoe option

for retaining Rs. 2,000 Lakhs

GENERAL RISK

Investment in debt and debt related securities involve a degree of risk and investors should not invest any funds in the debt instrument privately placed unless they can afford to take the risks attached to such investments. Investors are advised to read the risk factors carefully before taking an investment decision in this private placement. For taking an investment decision, investors must rely on their own examination of The Company and The Placement including the risks involved. The securities have not been recommended or approved by Securities and Exchange Board of India nor does Securities and Exchange Board of India guarantee the accuracy or adequacy of this document. The attention of Investors is drawn to the statement of Risk Factors on Page 6 the Information Memorandum.

ABSOLUTE RESPONSIBILITY OF THE BANK OF RAJASTHAN

The Bank of Rajasthan Limited, having made all reasonable inquiries, accepts responsibility for, and confirms that this contains all information with regard to The Bank and The Placement, which is material in the context of The Placement, that the information contained in this Information Memorandum is true and correct in all material respects and is not misleading in any material respect, that the opinions and intentions expressed herein are honestly held and that there are no other facts, the omission of which makes this document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect.

LISTING

The Bank proposes to get the privately placed Unsecured, Non-Convertible, Redeemable, Subordinated Bonds Series IV listed in the Wholesale Debt Segment (WDM) of The Stock Exchange, Mumbai

LEAD ARRANGER TO THE ISSUE

SPA Merchant Bankers Limited

10-A, Chandermukhi Building Nariman Point, Mumbai – 400 021.

SEBI Registration No.: INM000010825 Tel: +91-22-2280 1240-49

Fax: +91-22-2287 1192, 2284 6318 e-mail: [email protected], [email protected]

PLACEMENT OPENS ON : 26th December 2005 PLACEMENT CLOSES ON : 27th December 2005

2

TABLE OF CONTENTS Chapter Title Page No Definitions / Abbreviations 3 Risk Factors and Management Proposal to address the Risks thereof 5 Highlights 10 PART I I. General Information 11 II. Capital Structure 16 III. Terms of the Present Placement 19 IV. Particulars of The Placement 25 V. Bank, Management, Project and Industry 31 VI. Financial Performance for the past Five Financial Years and for the half year ended

September 30, 2005 52

VII. Management Discussion and Analysis of the Financial Conditions and Results of the Operations as reflected in the Financial Statement

56

VIII. Basis for Placement Price 62 IX. Outstanding Litigation or Defaults 62 X. Risk factors and Management Proposal to address the Risks thereof 64 XI. Disclosure on Investor Protection and Grievances Redressal System 69 PART II A. General Information 70 B. Financial Information 72 C. Statutory and Other Information 111 D. Material Contracts and Documents for Inspection 113 PART III Declaration 113

3

DEFINITIONS / ABBREVIATIONS

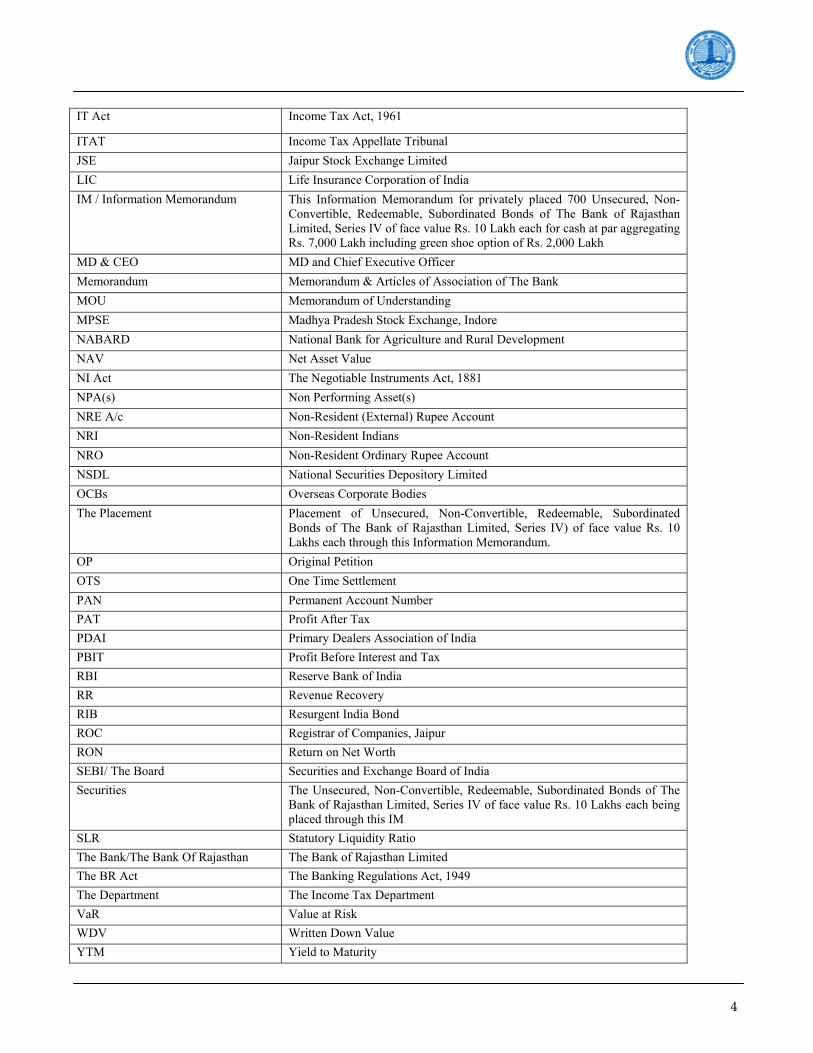

AC Assistant Commissioner ALC Assistant Labour Commissioner AMC Asset Management Company Articles Articles of Association of The Bank of Rajasthan Limited AS Accounting Standard AY Assessment Year Board of Directors Board of Directors of The Bank BSE The Stock Exchange, Mumbai CAF Composite Application Form CAGR Compound Annual Growth Rate CC Criminal Complaint CDSL Central Depository Services Limited CGS Central Government Securities CSE Calcutta Stock Exchange CIT Commissioner of Income Tax CMP Current Market Price CRAR Capital Risk Weighted Adequacy Ratio CRR Cash Reserve Ratio Demat Dematerialised (Electronic/Depository - as the context may be) DICGC Deposit Insurance and Credit Guarantee Corporation DLC District Labour Commissioner DRT Debt Recovery Tribunal DSE Delhi Stock Exchange Association Limited ECGC Export Credit Guarantee Corporation Employees Employees of The Bank of Rajasthan Limited EPS Earning Per Share EXIM Bank Export and Import Bank of India FCNR Foreign Currency (Non-Resident) Account FE Foreign Exchange FEDAI Foreign Exchange Dealers Association of India FEMA Foreign Exchange Management Act, 1999 FII Foreign Institutional Investor FIMMDA Fixed Income & Money Market Derivatives Association FY Financial Year GDP Gross domestic product GIR General Index Register GOI Government of India ICAI Institute of Chartered Accountants of India ID Act Industrial Disputes Act 1947 IDBI Industrial Development Bank of India IM Information Memorandum

4

IT Act Income Tax Act, 1961

ITAT Income Tax Appellate Tribunal JSE Jaipur Stock Exchange Limited LIC Life Insurance Corporation of India IM / Information Memorandum This Information Memorandum for privately placed 700 Unsecured, Non-

Convertible, Redeemable, Subordinated Bonds of The Bank of Rajasthan Limited, Series IV of face value Rs. 10 Lakh each for cash at par aggregating Rs. 7,000 Lakh including green shoe option of Rs. 2,000 Lakh

MD & CEO MD and Chief Executive Officer Memorandum Memorandum & Articles of Association of The Bank MOU Memorandum of Understanding MPSE Madhya Pradesh Stock Exchange, Indore NABARD National Bank for Agriculture and Rural Development NAV Net Asset Value NI Act The Negotiable Instruments Act, 1881 NPA(s) Non Performing Asset(s) NRE A/c Non-Resident (External) Rupee Account NRI Non-Resident Indians NRO Non-Resident Ordinary Rupee Account NSDL National Securities Depository Limited OCBs Overseas Corporate Bodies The Placement Placement of Unsecured, Non-Convertible, Redeemable, Subordinated

Bonds of The Bank of Rajasthan Limited, Series IV) of face value Rs. 10 Lakhs each through this Information Memorandum.

OP Original Petition OTS One Time Settlement PAN Permanent Account Number PAT Profit After Tax PDAI Primary Dealers Association of India PBIT Profit Before Interest and Tax RBI Reserve Bank of India RR Revenue Recovery RIB Resurgent India Bond ROC Registrar of Companies, Jaipur RON Return on Net Worth SEBI/ The Board Securities and Exchange Board of India Securities The Unsecured, Non-Convertible, Redeemable, Subordinated Bonds of The

Bank of Rajasthan Limited, Series IV of face value Rs. 10 Lakhs each being placed through this IM

SLR Statutory Liquidity Ratio The Bank/The Bank Of Rajasthan The Bank of Rajasthan Limited The BR Act The Banking Regulations Act, 1949 The Department The Income Tax Department VaR Value at Risk WDV Written Down Value YTM Yield to Maturity

5

RISK FACTORS ENVISAGED BY THE MANAGEMENT AND PROPOSALS TO ADDRESS SUCH RISKS

INTERNAL RISK FACTORS

1. There are litigations in which The Bank is involved. A brief description of the same is in the table below. For details please refer to page no of this Information Memorandum.

S. No.

Brief Description No. of cases

Amount involved (Rs. In lac)

1 Suits filed by The Bank against defaulting borrowers (including decreed a/cs)

3553 63130.32

2. Appeals filed by The Bank on disputed income tax 18 4977 (approx.) 3 Suits against The Bank which are not treated as

debts 162 7901.80

4 Suits filed by the shareholders 30 - 5 Criminal case against the bank & the directors 1

2. Suit has been filed by HRB Floriculture Limited (as a shareholder of the bank) against The Bank of Rajasthan Limited and some of the Directors u/s 482 of CRPC.

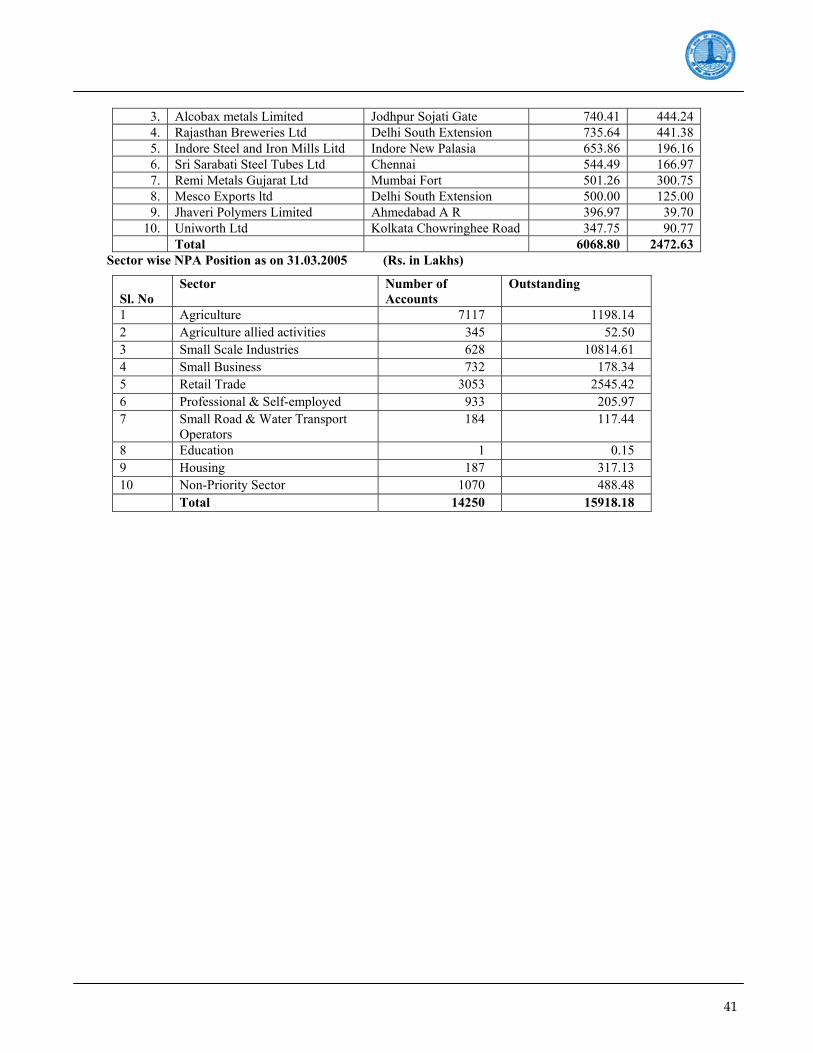

3. As on 31.03.2005, Rs. 15918.18 Lakhs classified as impaired loans out of which Rs. 881.20 Lakhs is sub-standard (A substandard asset is one which has been classified as NPA for a period not exceeding 18 months) and Rs. 13059.22 Lakhs is doubtful (A doubtful asset is one which has remained NPA for a period exceeding 18 months) and Rs. 1977.76 Lakhs is loss assets (A loss asset is one where loss has been identified by The Bank or its internal auditors or external auditors or RBI inspection). The net NPA positions as on 31.03.2002, 31.03.2003, 31.03.2004 and 31.03.2005 are 8.86%, 6.80%, 2.99% and 2.50% respectively of the net advances. A decreasing trend in the NPA has been exhibited over the recent years.

Management Proposal to address the Risk The bank has given thrust for the recovery of Non Performing Assets and arresting the growth of fresh Non Performing Assets. The strategies for reducing the NPA levels are given in detail on page no. of the Information Memorandum.

4. The lending risk involves inability or unwillingness of a customer or counterparty to meet the commitments in relation to lending and other financial transactions.

Management Proposal to address the Risk The Bank has a structured credit appraisal system and lending norms. The Bank takes adequate care to minimise the risk by having a diversified portfolio and fixing lending limits to sensitive sectors.

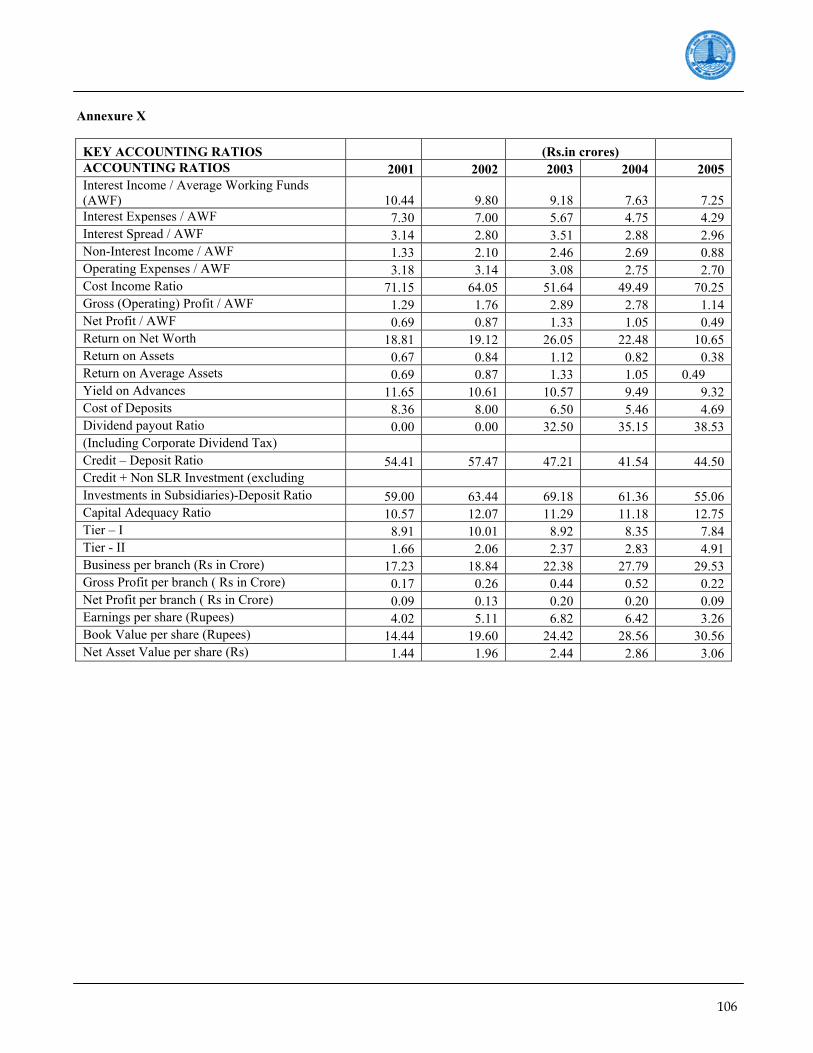

5. In terms of RBI guidelines, the Bank is required to create an Investment Fluctuation Reserve equivalent to 5% of its investment portfolio of its investments in the categories “held for trading “ and “ available for sale” over five years period beginning from financial year 2001-02. The Bank has so far created a reserve of Rs. 56.80 crores (including Rs. 47.90 crores upto the previous year) which is 4% of the investment portfolio (excluding securities under Held to Maturity category) as on March 31, 2005.

6. Market Risks

Increased interest rate volatility exposes BoR to market rate risk arising out of maturity/ rate mismatches.

Management proposal to address the Risk: Risks arising from interest rate volatility are inherent to the business of financial intermediation and lending. However, the Bank has put in place a system of regular review of lending and deposit rates in order to �inimize the interest rate risk. The Asset Liability Management Committees of the Bank reviews the risk on a regular basis. Continuous Risk Management measures are initiated depending upon the movement in the market interest rates. The movement in the interest rates is closely monitored for appropriate action. For more

6

details on the Risk Management procedures, investors are advised to refer to para ‘Risk Management’ mentioned elsewhere in this Information Memorandum.

7 Credit Rating

Bank has obtained credit rating of ‘CARE A-’ (Single A minus) from Credit Analysis & Research Limited AND “LA-“ from ICRA for an amount of Rs. 70 crores for its issue of Tier-II Bonds. Instruments with this rating are considered upper medium grade instruments and have many favourable investment attributes. Safety for principal and interest are considered adequate. Assumptions that do not materialize may have a greater impact as compared to the instruments rated higher.

Management proposal to address the Risk: Investors may please note that, the rating is not a recommendation to buy, sell or hold securities and investors should take their own decision. The rating may be subject to revision; suspension or withdrawal at any time by the assigning rating agency and each rating should be evaluated independently of any other rating. The ratings obtained are subject to revision at any point of time in the future. The Rating agency has the right to suspend, withdraw or revise the rating at any time on the basis of new information etc.

8 Contingent Liabilities

As on March 31, 2005 the contingent liabilities of the Bank were at Rs 90,402.80 Lakhs (comprising claims against the Bank not acknowledged as debts Rs. 8,499.96 Lakhs, liability on account of outstanding forward exchange contracts Rs. 43,040.38 Lakhs, guarantees on behalf of constituents in India Rs. 21,860.62 Lakhs, acceptances, endorsements and other obligations Rs. 15,540.20 Lakhs and others Rs. 1,461.64 Lakhs).

Management proposal to address the Risk: The contingent liabilities have arisen in the normal course of business of the Bank and are according to the prudential norms prescribed by RBI. 9 Non Performing Assets (NPAs)

As on 31.03.2005, the net NPAs of the Bank stood at Rs. 7,225 lakhs or 2.50% of its net advances. In the event of non-recovery of these assets, the Bank may have to provide for these NPAs, which might affect the profitability of the Bank in future.

Management proposal to address the Risk: The Net NPAs of the Bank have reduced from 2.99% in 2004 to 2.50% in 2005. The Bank has provided for its NPAs in conformity with RBI guidelines and is taking steps to reduce the proportion of non-performing assets through aggressive recovery drives combined with improved risk management practices. Further, there have been substantial changes in the legislative and operating environment enabling FIs and Banks to pursue recovery of over-dues. Besides Debt Recovery Tribunal (DRT) set up for faster settlement of recovery litigation, GoI has enacted ‘The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002’ enabling FIs and Banks to securities and reconstruct financial assets and enforce security more effectively. Reserve Bank of India has formulated detailed guidelines for operation of the scheme. The Bank has made provisions for its NPAs over and above the minimum prescribed by the RBI with a view to enhance the financial strength of the Bank.

10 Utilization of Funds The utilization of the funds proposed to be raised through this private placement is entirely at the discretion of the Bank and no monitoring agency has been appointed to monitor the deployment of funds.

Management proposal to address the Risk: The funds raised through this private placement are not meant for any specific project and hence a monitoring agency may not be required. The Bank is managed by professionals under the supervision of its Board of Directors. Further, the Bank is subject to a number of regulatory checks and balances as stipulated in its regulatory environment. Therefore, the management believes that the funds raised via this private placement would be utilised only towards satisfactory fulfillment of the ‘Objects of the Issue’ mentioned elsewhere in this Information Memorandum.

7

External Risk Factors 1. Regulatory restrictions on The Bank and limitations of the powers of bondholders of The Bank

There are a number of restrictions as per The BR Act, which impede flexibility of The Bank’s operations and affect / restrict investors’ right. These are as under:

I. In terms of Section 8 of The BR Act, The Bank is prohibited from doing trading activity, which may act as an

operational constraint.

II. In terms of Section 17(1) of The BR Act, every banking company shall create a Reserve Fund and shall, out of the balance of profit of each year as disclosed in the Profit & Loss a/c prepared under Section and before any dividend is declared, transfer to the Reserve Fund a sum equivalent to not less than twenty percent of such profit.

III. In terms of Section 19 of The BR Act, there are some restrictions on The Banking companies regarding opening

of subsidiaries which may deny The Bank from exploiting emerging business opportunities.

IV. In terms of Section 23 of The BR Act, there are certain restrictions on The Banking companies regarding opening of new place of business and transfer of existing place of business, which may hamper the operational flexibility of The Bank.

V. In terms of Section 25 of The BR Act, each banking company has to maintain assets in India which is not less

than 75% of its demand and time liabilities in India which in turn may prohibit The Bank from creating overseas assets and exploiting overseas business opportunities.

VI. There are restrictions in The BR Act regarding,

a) Management of a bank including appointment of directors. b) Borrowings and creation of floating charge. c) Expansion of business, as the branches need to be licensed. d) Disclosures in the profit & loss account and balance sheet. e) Production of documents and availability of records for inspection by shareholders. f) Reconstruction of banks through amalgamation. g) Maintenance of a percentage of Assets in Unencumbered approved Securities

VII. No banking company shall pay any dividend on its shares until all its capitalised expenses (including

preliminary, organisational expenses, share selling commission, brokerage, amounts of losses and any other item represented by tangible assets) have been completely written off.

2. Sensitivity to the economy and extraneous factors The Bank’s performance is highly correlated to the performance of the economy and the financial markets. The health

of the economy and the financial markets in turn depends on the domestic economic growth, state of the global economy and business and consumer confidence, among other factors. Any event disturbing the dynamic balance of these diverse factors would directly or indirectly affect the performance of The Bank including the quality and growth of its assets.

Management Proposal to Address the Risk The Bank’s performance is highly correlated to the performance of the

economy and the financial markets. The health of the economy and the financial markets in turn depends on the domestic economic growth, state of the global economy and business and consumer confidence, among other factors. Any event disturbing the dynamic balance of these diverse factors would directly or indirectly affect the performance of the Bank including the quality and growth of its assets.

8

3. Competition from existing and new commercial banks Competition in the financial sector has increased with the entry of new players and is likely to increase further as a

result of further deregulation in the financial sector. The Bank may face competition both in raising resources and in deploying them.

Management Proposal to Address the Risk The Bank has an established broad based presence and has been taking

steps to enhance customer satisfaction by upgrading skills, systems and technology to meet such challenges. The Bank is attempting to add quality assets on competitive terms. The Bank is also taking steps to broad base its product bouquet with a special emphasis on enhancement in the non-fund based income. On the resource mobilisation front, The Bank is actively endeavouring to broaden its reach and raise resources through its network of 428 outlets in India.

4. Changes in Regulatory Policies Major changes in Government/RBI policies relating to banking sector may have an impact on the operations of The

Bank. Management Proposal to Address the Risk The policy changes may provide both opportunities and challenges for

The Bank. The Bank has a long presence in The Banking sector, for more than 60 years and does not perceive policy changes to be a major threat.

5. Disintermediation in the Financial Markets: Development of capital markets may result in disintermediation by current and potential borrowers whereby many

companies may access the markets directly, thereby reducing their dependence on the banking system.

Management Proposal to Address the Risk Disintermediation brings with it the opportunity for the Bank to expand its fee-based activities The Bank has been proactive and has increased its thrust on businesses such as Treasury, Investment, Cash Management and Foreign Exchange. Also, The Bank has, in recent years, launched several retail lending schemes and value added products so as to broaden its borrower base Due to its diversified services, The Bank is confident of facing any disintermediation effectively

6. Forex Risk Exchange Rate fluctuations may have an impact on The Bank’s financial performance. Management Proposal to Address the Risk As per RBI guidelines, banks are required to frame guidelines covering

all the risks related to foreign exchange operations, duly approved by their Board of Directors. This includes limits on net open exchange position which is also approved by the Reserve bank of India.

The Bank, has prescribed internal control guidelines for foreign exchange operations and net open positions and kept

well below the prescribed limits. As such the risk from exchange rate fluctuations is minimised and kept under control.

7. Interest Rate Risk Interest rate volatility exposes The Bank to an interest rate risk or market risk. Such interest rate risk has a potential

impact on net interest income or net interest margin as well as on the market value of the fixed income securities held by The Bank in its investment portfolio.

Management Proposal to Address the Risk These risks are inherent in The Banking business. However, The Bank

has put in place a system of regular review of lending and deposit rates in order to minimise the interest rate risk. The Asset Liability Management Committees of The Bank reviews the risk on a regular basis. Continuous Risk Management measures are initiated depending upon the movement in the market interest rates. The movement in the interest rates is closely monitored for appropriate action.

9

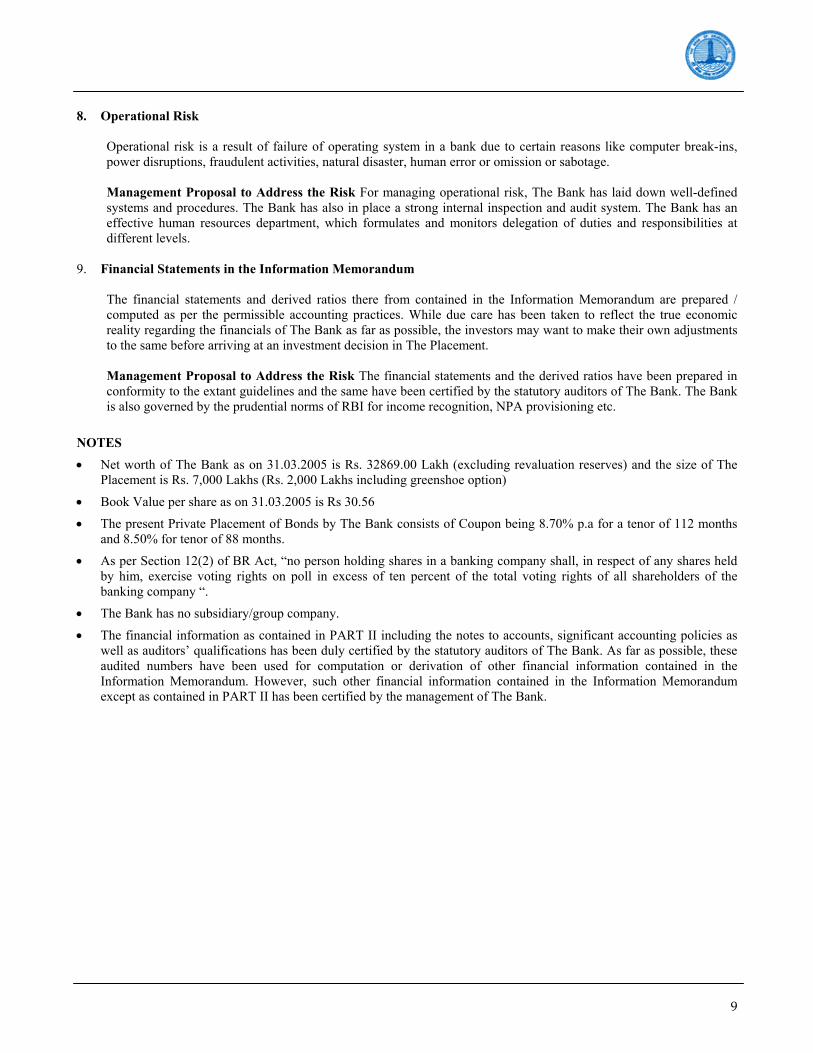

8. Operational Risk Operational risk is a result of failure of operating system in a bank due to certain reasons like computer break-ins,

power disruptions, fraudulent activities, natural disaster, human error or omission or sabotage. Management Proposal to Address the Risk For managing operational risk, The Bank has laid down well-defined

systems and procedures. The Bank has also in place a strong internal inspection and audit system. The Bank has an effective human resources department, which formulates and monitors delegation of duties and responsibilities at different levels.

9. Financial Statements in the Information Memorandum The financial statements and derived ratios there from contained in the Information Memorandum are prepared /

computed as per the permissible accounting practices. While due care has been taken to reflect the true economic reality regarding the financials of The Bank as far as possible, the investors may want to make their own adjustments to the same before arriving at an investment decision in The Placement.

Management Proposal to Address the Risk The financial statements and the derived ratios have been prepared in conformity to the extant guidelines and the same have been certified by the statutory auditors of The Bank. The Bank is also governed by the prudential norms of RBI for income recognition, NPA provisioning etc.

NOTES • Net worth of The Bank as on 31.03.2005 is Rs. 32869.00 Lakh (excluding revaluation reserves) and the size of The

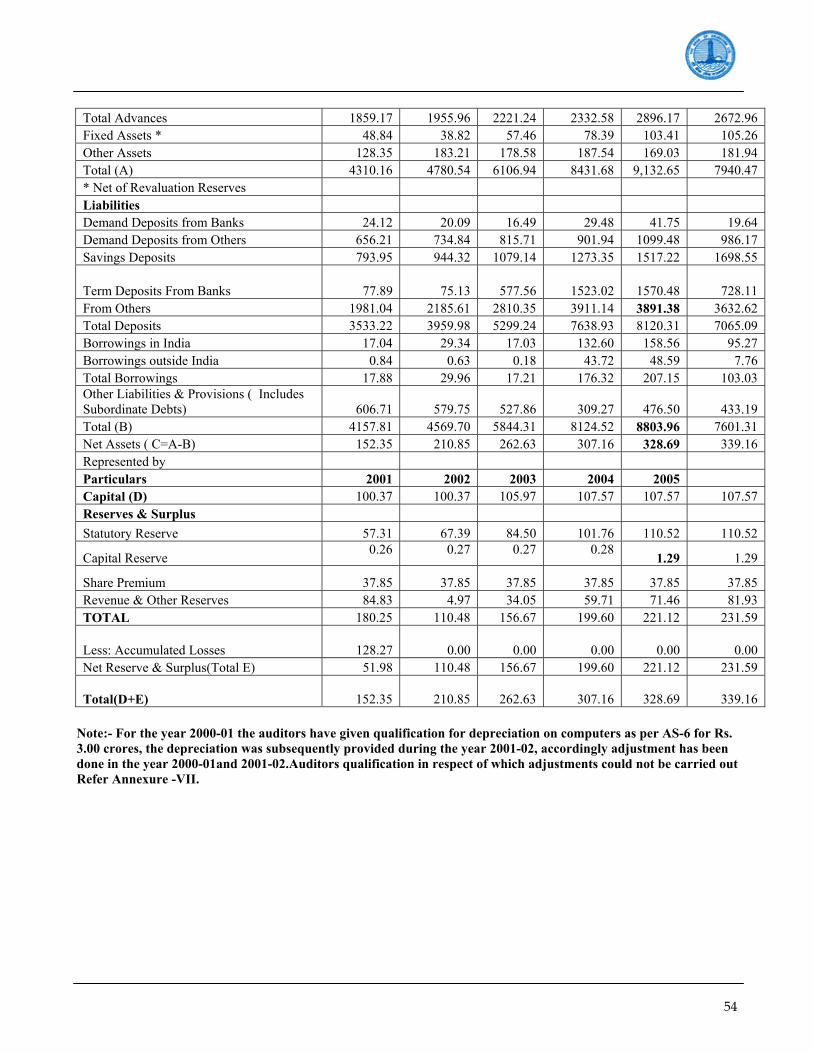

Placement is Rs. 7,000 Lakhs (Rs. 2,000 Lakhs including greenshoe option)

• Book Value per share as on 31.03.2005 is Rs 30.56

• The present Private Placement of Bonds by The Bank consists of Coupon being 8.70% p.a for a tenor of 112 months and 8.50% for tenor of 88 months.

• As per Section 12(2) of BR Act, “no person holding shares in a banking company shall, in respect of any shares held by him, exercise voting rights on poll in excess of ten percent of the total voting rights of all shareholders of the banking company “.

• The Bank has no subsidiary/group company.

• The financial information as contained in PART II including the notes to accounts, significant accounting policies as well as auditors’ qualifications has been duly certified by the statutory auditors of The Bank. As far as possible, these audited numbers have been used for computation or derivation of other financial information contained in the Information Memorandum. However, such other financial information contained in the Information Memorandum except as contained in PART II has been certified by the management of The Bank.

10

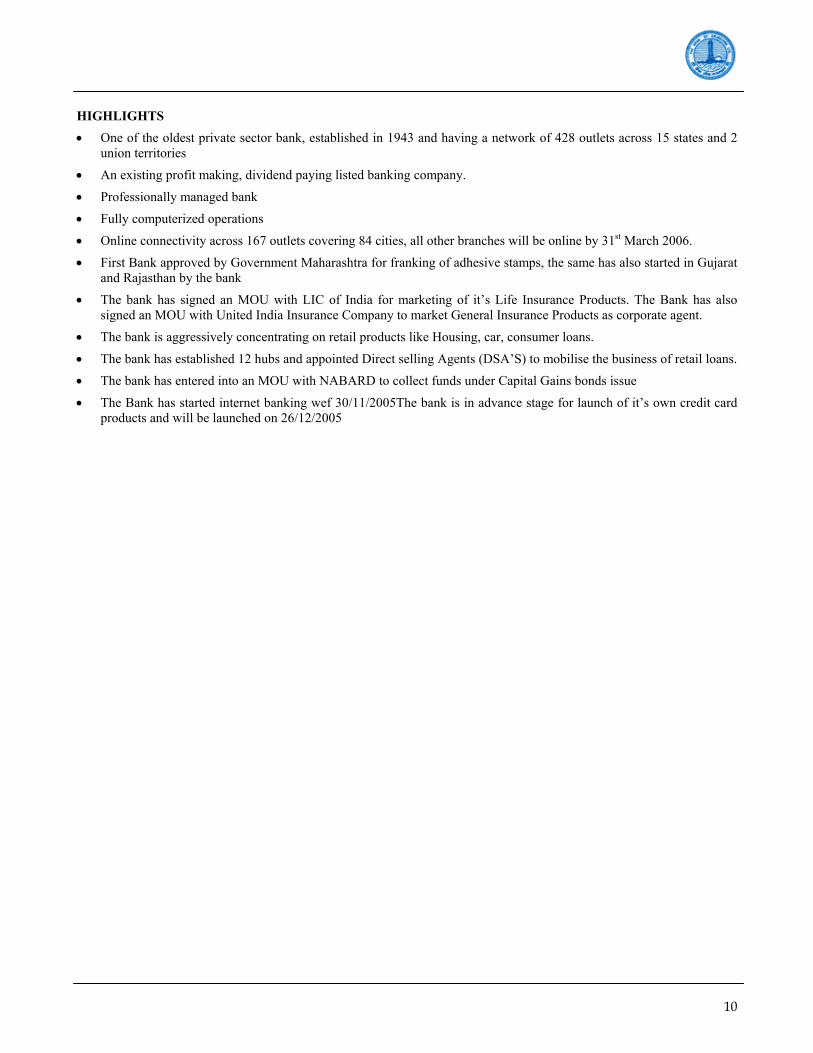

HIGHLIGHTS • One of the oldest private sector bank, established in 1943 and having a network of 428 outlets across 15 states and 2

union territories

• An existing profit making, dividend paying listed banking company.

• Professionally managed bank

• Fully computerized operations

• Online connectivity across 167 outlets covering 84 cities, all other branches will be online by 31st March 2006.

• First Bank approved by Government Maharashtra for franking of adhesive stamps, the same has also started in Gujarat and Rajasthan by the bank

• The bank has signed an MOU with LIC of India for marketing of it’s Life Insurance Products. The Bank has also signed an MOU with United India Insurance Company to market General Insurance Products as corporate agent.

• The bank is aggressively concentrating on retail products like Housing, car, consumer loans.

• The bank has established 12 hubs and appointed Direct selling Agents (DSA’S) to mobilise the business of retail loans.

• The bank has entered into an MOU with NABARD to collect funds under Capital Gains bonds issue

• The Bank has started internet banking wef 30/11/2005The bank is in advance stage for launch of it’s own credit card products and will be launched on 26/12/2005

11

PART I I. GENERAL INFORMATION

THE BANK OF RAJASTHAN LIMITED

(Incorporated on May 7, 1943 under the Mewar Companies Act)

Registered Office: Clock Tower , Udaipur- 313 001

Tel: 0294 - 2521257 / 2422116 Fax no : 0294 - 2525709 Email: [email protected]

Corporate Office : Raghuvanshi Mills Compound, 11/12, Senapati Bapat Marg, Lower Parel (W), Mumbai – 400 013.

Phone : 91-22-30400016 Fax : 91-22- 30400019; Email : [email protected] Website: www.bankofrajasthan.com

Private Placement of 700 Unsecured, Non-Convertible, Redeemable, Subordinated Bonds in the nature of Promissary Notes Series IV of face value Rs. 10 Lakh each for cash at par aggregating Rs. 7,000 Lakhs including

green-shoe option for retaining Rs. 2,000 Lakhs Authority for The Placement

The Placement is being made pursuant to the Resolution of the Board of Directors of The Bank passed at its meeting held on November 7, 2005 Government Approvals No specific Government approval is required for The Bank for raising the Tier II capital. However The Bank is raising the Tier II Capital through this Placement by following the provisions of the Master Circular DBOD No. BP.BC.20/20.01.02/2003-2004 dated September 2, 2003, issued by RBI prescribing the norms for banking companies to raise Tier II Capital. The Bank can undertake the existing activities in view of the present approvals, and no further approvals from any Government authority are required by The Bank to continue the existing business activities save and except those approvals, which may be required to be taken in the normal course of business from time to time. It is to be distinctly understood that the sanction/permission of the Government of India should not in any way, be deemed or construed that the Information Memorandum has been cleared or approved by them nor do they take any responsibility either for the financial soundness of The Bank or the correctness of the statements made or opinions expressed in this Information Memorandum. Disclaimer Clause It is to be distinctly understood that the submission of the Information Memorandum to The Stock Exchange, Mumbai or the National Stock Exchange, Mumbai should not, in any way, be deemed or construed that the same has been cleared or approved by the Stock Exchange(s). Stock Exchange(s) do not take any responsibility either for the financial soundness of any scheme or the project for which The Placement is proposed to be made or for the correctness of the statements made or opinions expressed in the Information Memorandum. The Bank certifies that the disclosures made in the information memorandum are generally adequate and are in conformity with SEBI (Disclosure and Investor Protection) Guidelines, 2000 in force for the time being. This requirement is to facilitate investors to take an informed decision for making investment in the proposed Placement.

12

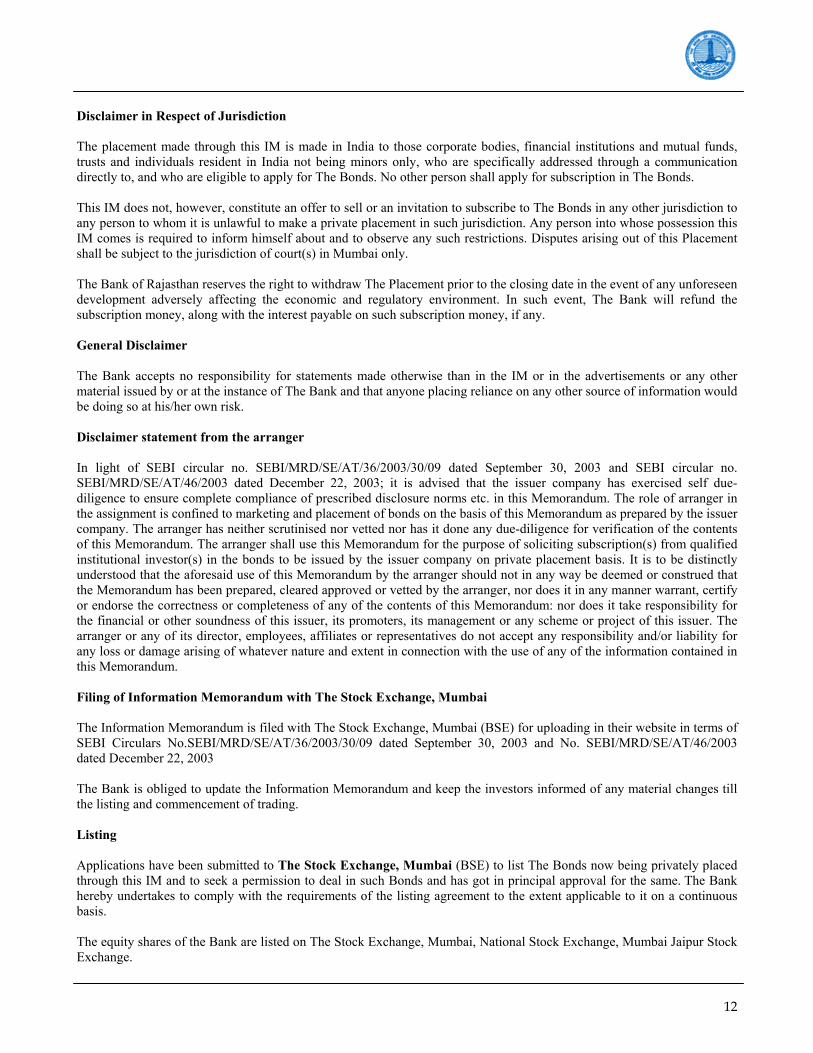

Disclaimer in Respect of Jurisdiction The placement made through this IM is made in India to those corporate bodies, financial institutions and mutual funds, trusts and individuals resident in India not being minors only, who are specifically addressed through a communication directly to, and who are eligible to apply for The Bonds. No other person shall apply for subscription in The Bonds. This IM does not, however, constitute an offer to sell or an invitation to subscribe to The Bonds in any other jurisdiction to any person to whom it is unlawful to make a private placement in such jurisdiction. Any person into whose possession this IM comes is required to inform himself about and to observe any such restrictions. Disputes arising out of this Placement shall be subject to the jurisdiction of court(s) in Mumbai only. The Bank of Rajasthan reserves the right to withdraw The Placement prior to the closing date in the event of any unforeseen development adversely affecting the economic and regulatory environment. In such event, The Bank will refund the subscription money, along with the interest payable on such subscription money, if any. General Disclaimer The Bank accepts no responsibility for statements made otherwise than in the IM or in the advertisements or any other material issued by or at the instance of The Bank and that anyone placing reliance on any other source of information would be doing so at his/her own risk. Disclaimer statement from the arranger In light of SEBI circular no. SEBI/MRD/SE/AT/36/2003/30/09 dated September 30, 2003 and SEBI circular no. SEBI/MRD/SE/AT/46/2003 dated December 22, 2003; it is advised that the issuer company has exercised self due-diligence to ensure complete compliance of prescribed disclosure norms etc. in this Memorandum. The role of arranger in the assignment is confined to marketing and placement of bonds on the basis of this Memorandum as prepared by the issuer company. The arranger has neither scrutinised nor vetted nor has it done any due-diligence for verification of the contents of this Memorandum. The arranger shall use this Memorandum for the purpose of soliciting subscription(s) from qualified institutional investor(s) in the bonds to be issued by the issuer company on private placement basis. It is to be distinctly understood that the aforesaid use of this Memorandum by the arranger should not in any way be deemed or construed that the Memorandum has been prepared, cleared approved or vetted by the arranger, nor does it in any manner warrant, certify or endorse the correctness or completeness of any of the contents of this Memorandum: nor does it take responsibility for the financial or other soundness of this issuer, its promoters, its management or any scheme or project of this issuer. The arranger or any of its director, employees, affiliates or representatives do not accept any responsibility and/or liability for any loss or damage arising of whatever nature and extent in connection with the use of any of the information contained in this Memorandum. Filing of Information Memorandum with The Stock Exchange, Mumbai The Information Memorandum is filed with The Stock Exchange, Mumbai (BSE) for uploading in their website in terms of SEBI Circulars No.SEBI/MRD/SE/AT/36/2003/30/09 dated September 30, 2003 and No. SEBI/MRD/SE/AT/46/2003 dated December 22, 2003 The Bank is obliged to update the Information Memorandum and keep the investors informed of any material changes till the listing and commencement of trading.

Listing Applications have been submitted to The Stock Exchange, Mumbai (BSE) to list The Bonds now being privately placed through this IM and to seek a permission to deal in such Bonds and has got in principal approval for the same. The Bank hereby undertakes to comply with the requirements of the listing agreement to the extent applicable to it on a continuous basis. The equity shares of the Bank are listed on The Stock Exchange, Mumbai, National Stock Exchange, Mumbai Jaipur Stock Exchange.

13

Eligibility of The Bank to Privately Place The Bonds The Bank is raising the Tier II Capital through this Placement by following the provisions of the Master Circular DBOD No. BP No. BP.BC.20/20.01.02/2003-2004 dated September 2, 2003, issued by RBI prescribing the norms for banking companies to raise Tier II Capital.

Prohibition by SEBI The Bank and companies with which the directors of The Bank are associated as directors or promoters are presently not prohibited from accessing the capital market / Money Market under any order or directions passed by SEBI / RBI.

Minimum Subscription Provisions of Section 69 of The Companies Act are not applicable for The Bonds Letters of Allotment / Refund Orders The Bank shall make allotment to investors in due course after verification of the Application Forms, the accompanying documents and on realisation of the subscription money. Dematerialised Form The Depository Account of the investor(s) with NSDL/ CDSL/ Depository Participant will be credited within Thirty (30) days from the Deemed Date of Allotment. The initial credit in the account will be akin to the Letter of Allotment. After completion of the necessary statutory formalities, the initial credit akin to a Letter of Allotment in the Demat Account of the investor would be replaced with the number of Bonds allotted. The Bonds issued in electronic (dematerialised) form, will be governed as per the provisions of The Depository Act, 1996. Securities and Exchange Board of India (Depositories and Participants) Regulations, 1996, rules notified by NSDL/ CDSL/ Depository Participant from time to time and applicable laws and rules notified in respect thereof. Denomination of Bonds The denomination of each Bond will be of the face value of Rs. 10 Lakh. The Bank will issue instructions for a corporate action to give demat credit in the DP beneficiary account of the allottee for the number of bonds allotted. Placement Programme The Placement programme will open at the commencement of banking hours on December 26, 2005 and will close at the close of banking hours on December 27, 2005 unless extended by The Bank Credit Rating Credit Analysis and Research Limited (CARE) & ICRA Ltd. has assigned “A-”(A minus) and “LA_” (Pronounced “ L A minus”) rating respectively to The Bonds being issued under the current private placement. Instruments of this rating are considered to be of investment grade. The rating indicates sufficient safety for payment of interest and principal, at the time of rating. Underwriting The Placement of Bonds is not underwritten. Declaration by The Bank

The Bank accepts full responsibility for the accuracy of the information given in this Information Memorandum and

14

confirms that to the best of their knowledge and belief, there are no other facts, the omission of which makes any statement in this Information Memorandum misleading and further confirms that they have made all reasonable inquiries to ascertain such facts. THE BANK OF RAJASTHAN LIMITED further declares that the Stock Exchange to which an application for listing would be made do not take any responsibility for the financial soundness of this Placement or for the coupon at which The Bonds are placed, or for the correctness of the statements made or opinions expressed in this Information Memorandum.

In the opinion of the The Bank, there are no circumstances that have arisen since the date of the last financial statement disclosed in the Information Memorandum, that materially or adversely affect or are likely to affect the performance or profitability of The Bank or value of its assets or its ability to pay its liabilities within the next twelve months.

All information shall be made available by the Lead Arrangers and The Bank to the Members at large and no selective or additional information would be available for a section of the Members in any manner whatsoever.

The promoters / directors declare and confirm that no information / material likely to have a bearing on the decision of Members in respect of Securities placed in terms of this Information Memorandum has been suppressed / withheld and / or incorporated in the manner that would amount to misstatement / misrepresentation and in the event of it transpiring at any point of time till allotment / refund, as the case may be that any information / material has been suppressed / withheld and / or incorporated in the manner that would amount to misstatement / misrepresentation, The Bank shall refund the entire application monies to all the subscribers within 8 days thereafter without prejudice to the provisions of section 63 of the Companies Act, 1956.

The Bank, its directors and companies with which the directors of The Bank are associated as directors or promoters are presently not prohibitedfrom accessing the capital market under any order or direction passed by SEBI.

The Bank undertakes that it shall take the necessary steps to comply with all the requirements of the guidelines on Corporate Governance as would be applicable to it.

15

Intermediaries

LEAD ARRANGER TO THE ISSUE Trustee to the Bond Holders

SPA Merchant Bankers Limited 10-A, Chandermukhi Building Nariman Point Mumbai – 400 021. SEBI Registration No.: Tel: +91-22-2280 1240 Fax: +91-22-2287 1192 e-mail: [email protected] [email protected]

The Western India Trustee and Executor Company Limited 161/ C, 16th Floor, Mittal Court, Nariman Point, 400021 Tel. no. 022-2281 2883 Fax no.: 022-2281 6477 Email :[email protected]

Rating Agency :- Credit Analysis & Research Limited Kalpataru Point, 2nd Floor, Kamanii Marg, Sion (East), Mumbai – 400 022 Tel no.: 022-56602871-75/24024541-43 Fax no. :022- 5660 2876 Email: [email protected] ICRA Limited Electric Mansion, 3rd Floor Appasaheb Marathe Marg Prabhadevi, Mumbai – 400 025. Tel no.: 022-2433 1046 Fax no. :022- 2433 1390 Email: [email protected]

Company Secretary & Compliance Officer

Mr. D K Jain Company Secretary The Bank of Rajasthan Limited Corporate Office Raghuvanshi Mills Compound, Senapati Bapat Marg, Lower Parel (west), Mumbai – 400 013 Tel. No. -91-22 - 30400006 Fax no. - : 91-22-30400019 Email – [email protected]

Auditors to The Bank ,of Rajasthan Limited

M/s. Chokshi & Chokshi Chartered Accountants 101/102, Kshamalaya, 1st Floor, 37, Sir V. Thackersey Marg, Mumbai – 400020 Tel no.: +91-22-5633 3912 Fax no.: +91-22-2200 3227

16

II CAPITAL STRUCTURE

as on September 30, 2005

Description No. of shares Aggregate NOMINAL Value (Rs.)

Aggregate value (Rs.)

AUTHORISED CAPITAL A) Equity Shares of Rs. 10/- each 25,00,00,000 2,50,00,00,000 — ISSUED, SUBSCRIBED AND PAID-UP CAPITAL Equity Shares of Rs.10/-. each Issued 10,75,98,294 1,07,59,82,940 — Equity Shares of Rs.10/- each Subscribed. 10,75,66,729 1,07,56,67,290 — Equity Shares of Rs.10/- each Called up 0 0

B)

Equity Shares of Rs.10/- each Fully paid up. 10,75,66,729 1,07,56,67,290 — C) SHARE PREMIUM — — 37,84,93,000

Notes to Capital Structure 1. History of the Capital

The details of increase in authorised capital (upto September 30, 2005) are given below

Sr. No

Date No. Shares Face Value (Rs.) Authorised Capital

(Rs. Lakhs)

1. As on 31.12.83 40,000 Rs. 100/- 40.00 2. As on 20.06.84 1,00,000 Rs. 100/- 100.00 3. As on 09.06.86 2,00,000 Rs. 100/- 200.00 4. As on 12.09.89 5,00,000 Rs. 100/- 500.00 5. As on 30.09.93 10,00,000 Rs. 100/- 1000.00 6. As on 05.02.94 25,00,000 Rs. 100/- 2500.00 Subdivision of equity shares from face value of Rs. 100/- each to face value of Rs. 10/- each on

June 16, 1994 7. As on 22.09.94 5,00,00,000 Rs. 10/- 5000.00 8. As on 30.09.96 5,10,00,000 Rs. 10/- 5100.00 9. As on 05.01.99 15,00,00,000 Rs. 10/- 15,000.00 10. As on 17.06.05 25,00,00,000 Rs. 10/- 25,000.00

2. Details of allotments made from 21.07.94

Date of Allotment

No of Shares

Face Value

Per Share (Rs.)

Issue Price

Per Share(Rs.)

Cumulative Paid-up

Capital (Rs.)

Considera tion

Description

As on 21.07.94

25,00,000 10/- - 2,50,00,000 - As on 21.07.94

8.10.94 to 31.03.95

54,43,640 10/- - 7,94,36,400 Cash Rights Issue and Preferential allotment to employees

12.05.95 to 09.12.95

99,91,712 10/- - 17,93,53,520 Cash Conversion of warrants

8.7.99 420 10/- - 17,93,57,720 Cash 16.12.99 4,48,26,055 10/- 15/- 6,27,61,8270 Cash Rights Issue 29.03.2001 4,48,04,902 10/- 10/- 1,07,56,67,290 Cash Rights Issue TOTAL 1,07,56,67,290

• The Bank had subdivided equity shares of Rs. 100/- each to equity shares of Rs. 10/- each on June 16, 1994

17

3. The Bank came out with a rights issue & warrants issue in 1999 & 2001 and shares pursuant to the said issue were

allotted on 16/12/1999 & 29/03/2001. 4. Directors Shareholding as on 30.09.2005

Sl.No Director No. of shares held

1. Shri. Pravin Kumar Tayal 300

5. No “buy-back” and “stand by” and similar arrangements for purchase of Securities by promoters, directors and lead arrangers have been proposed.

6. The Bonds placed through this Private Placement shall be fully paid-up.

7. Details Regarding Shareholders a) Top 10 shareholders as on date of filing the Information Memorandum with Stock Exchange is as follows (As on December 23, 2005)

S. No. Name of the Shareholder Number of Equity Shares 1 21st Century Entertainment Pvt Ltd 5,085,810 2 Sovotex Textiles Pvt Ltd 5,000,000 3 Cyber Infosystems and Tech. Ltd 4,991,458 4 Global Softech Pvt Ltd 4,981,440 5 EDC Securities Pvt Ltd 4,867,842 6 Cyber Info Zeeboomba.com Ltd 4,330,329 7 Cumballa Hill Property Dev. Pvt Ltd 4,200,000 8 Sumander Property Development Pvt Ltd 4,000,000 9 Ginger Clothing Pvt Ltd 4,000,000 10 Ahmednagar Investments Pvt Ltd 3,190,300

b) Top 10 shareholders ten days prior to the date of filing the Information Memorandum with Stock Exchange is as follows (As on December 13, 2005)

S. No. Name of the Shareholder Number of Equity Shares 1 21st Century Entertainment Pvt Ltd 5,085,810 2 Sovotex Textiles Pvt Ltd 5,000,000 3 Cyber Infosystems and Tech. Ltd 4,991,458 4 Global Softech Pvt Ltd 4,981,440 5 EDC Securities Pvt Ltd 4,867,842 6 Cyber Info Zeeboomba.com Ltd 4,330,329 7 Cumballa Hill Property Dev. Pvt Ltd 4,200,000 8 Sumander Property Development Pvt Ltd 4,000,000 9 Ginger Clothing Pvt Ltd 4,000,000 10 Ahmednagar Investments Pvt Ltd 3,190,300

18

c) Top 10 shareholders two years prior to the date of filing the Information Memorandum with Stock Exchange is as follows (As on 31.12.2003)

S. No. Name of the Shareholder Number of Equity Shares 1 21st Century Entertainment Pvt Ltd 5,085,810 2 Sovotex Textiles Pvt Ltd 5,000,000 3 Cyber Infosystems and Tech. Ltd 4,991,458 4 Global Softech Pvt Ltd 4,981,440 5 EDC Securities Pvt Ltd 4,867,842 6 Sahara India Financial Corporation Limited 4,651,808 7 Solid Vision 4,421,386 8 Cumballa Hill Property Dev. Pvt Ltd 4,200,000 9 Sumander Property Development Pvt Ltd 4,000,000 10 Ginger Clothing Pvt Ltd 4,000,000

d) Shareholding Pattern (as on 30.09.2005)

Sl.No. Shareholder No. of shares held % of holding 1. Promoters Holding 4,75,06,129 44.16

2. Mutual Funds, Banks, Financial Institutions, FIIs, NRIs & OCBs 19,04,477 1.77

3. Domestic Companies 1,41,07,179 13.12 4. Resident Individuals 4,30,77,271 40.05 5. Clearing Member & Clearing House 9,71,673 0.90 Total 10,75,66,729 100.00

8. Bonds issued in Series I, II and III are outstanding and redemption is due in year 30th June 2006, 2nd September 2007

and 15th November 2011and 15th July 2014. No other warrants or instruments other than those issued under Series I and II, III are outstanding as on date.

9. Transactions during the previous six months in the Holdings of Directors and related group from September 30, 2005

NIL

19

III. TERMS OF THE PRESENT PLACEMENT Terms Of The Bonds

Instrument Unsecured, Redeemable, Non-Convertible Subordinated Bonds Series IV in the nature of Promissory notes

Denomination (Face value) Rs. 10,00,000/- (Rs. Ten Lakh only) per one bond

Rating “CARE A-“ & “ICRA “LA-“

Options Option-I Option-II

Tenure 112 months 88 months

Fixed Coupon 8.70% 8.50%

Coupon Frequency Semi Annual Semi Annual

Put & Call Option None None

Redemption/ Maturity At par at the end of 112 months from the deemed date of allotment

At par at the end of 88 months from the deemed date of allotment

Interest on Application Money Interest shall be payable at the coupon rate from the date of realization of cheques/ draft till one day prior to the deemed date of allotment.*

Form of issuance Dematerialised (electronic credit)

Listing Proposed Listing on BSE

Object of the Bond Placement Tier II Capital for capital adequacy requirements and enhancing long-term resources of the Bank.

Deemed Date of Allotment December 28, 2005 (The Bank reserves the right to extend the deemed date of allotment at its sole discretion)

Minimum subscription per investor

5 Bonds. Thereafter in multiples of one bond

Placement size Rs. 70 crores including green shoe option of Rs. 20 crores

Placement opening date December 26, 2005

Placement closing date December 27, 2005 (The Bank reserves the right to extend the closing date at its sole discretion)

* Subject to TDS as applicable. Investors are advised to read the Information Memorandum for more details.

20

Credit Rating Credit Rating & Research Limited (CARE) has assigned “A-” (Pronounced “Single A minus”) & ICRA Ltd, has assigned “LA-“ (pronounced LA minus) rating to its issue of Tier II Bonds being issued under the current private placement of an amount of Rs. 70 crores. Instruments with this rating are considered upper medium grade instruments and have many favourable investment attributes. Safety for principal and interest are considered adequate. Assumptions that do not materialize may have a greater impact as compared to the instruments rated higher. As instruments characteristics or debt management capability could cover a wide range of possible attributes whereas rating is expressed only in limited number of symbols, CARE & ICRA assigns '+' or '-' signs to be shown after the assigned rating (wherever necessary) to indicate the relative position within the band covered by the rating symbol. The Rating Letter and Rating Rationale are reproduced at the end of this IM. Trustees The Bank Of Rajasthan Limited has appointed The Western India Trustee and Executer Company Limited as the trustees to the bondholders (hereinafter referred to as "Trustees"). Under the terms of this appointment the Trustees would monitor timely payment of interest and principal to the Bondholders and take appropriate steps to protect the interest of the Bondholders. The Bank Of Rajasthan Limited And the Trustees will enter into Trustee Agreement, inter alia, specifying the powers, authorities and obligations to the trustees and The Bank of Rajasthan Limited. The bondholder(s) shall, without further act or deed be deemed to have given their consent to the Trustees or any of their agents or authorised officials to do all such acts, deeds, matter and things in respect of or relating to The Bonds as the Trustees may, in their absolute discretion, deemed necessary or required to be done in the interest of the bondholder(s). Underwriting The Placement of Bonds is not underwritten. Deemed Date Of Allotment The deemed date of allotment shall be December28th, 2005. The interest on The Bonds would accrue from the deemed date of allotment. The actual allotment may occur on a date other than the deemed date of allotment. Allotment The Bank of Rajasthan Limited will make allotment to the investors in due course after verification of the application form, the accompanying documents and on realisation of the application money, The Bank of Rajasthan Limited reserves the right to accept or reject any application (in part or full) without assigning any reason thereof. The application forms which are not complete in all respects are liable to be rejected. The full amount of the face value of The Bonds has to be paid along with the application form. After completion of the necessary statutory formalities, the initial credit akin to a Letter of Allotment in the Depository Beneficiary Account of the investor would be replaced with the number of Bonds allotted. Interest on Application Money Interest at the coupon rate applicable to The Bonds placed through this IM (subject to deduction of tax at source at the rate prevailing from time to time under the provisions of Income Tax Act, 1961, or any other statutory modification or re-enactment thereof) will be paid from the date of realisation of the proceeds one day before the deemed date of allotment. The interest warrant would be dispatched by Registered post along with the Letters of Allotment/Refund orders, at the sole risk of the applicant. The interest on application money shall be paid along with Letter of Allotment.

21

Interest Payment Interest at 8.70% / 8.50% as the case may be (subject to deduction of tax at source at the rate prevailing from time to time under the provisions of Income Tax Act, 1961, or any other statutory modification or re-enactment thereof) will become payable on 28th June and 28th December every year till redemption. The interest instrument will be mailed to the bondholder(s) by Registered Post, at the sole risk of the applicant, to the first / sole applicant. The last interest payment, if any, will be proportionately made on the redemption date. Payment will be made by way of cheque(s) / interest warrant(s) at par / Demand Draft. In order to avoid any fraudulent misuse of interest warrants, the investors are requested to give their Bank Account details / RTGC details in the application form so that Account Payee Interest Instruments can be issued / directly credited via ECS or RTGS. The record date for payment of interest shall be fixed in accordance with the provisions of the listing agreement from time to time. Interest instruments would be sent to the Bondholders whose names appear in the List of Beneficial owners given by the Depository/ies to The Bank of Rajasthan Limited. Interest for each of the interest periods shall be computed on 365 days a year basis, on the face value of each Debenture at the coupon rate applicable to The Bonds. However, where the interest period (start date to end date) includes 29th February, interest shall be computed on 365 days a year basis, on the face value of each Bond at the coupon rate applicable to he instrument. Tax Deduction At Source Tax as applicable under the Income Tax Act, 1961, or any other statutory modification or re-enactment thereof will be deducted at source while making interest payments for bonds. Tax exemption certificate/document, under Section 193 of the Income Tax Act, 1961, if any, must be lodged to Company Secretary (Compliance Officer) at The Bank of Rajasthan Limited, Raghuvanshi Mills Compound, 11/12, Senapati Bapat Marg, Lower Parel (west), Mumbai – 400 013. Letter(s) of Allotment / Allotment Intimation Bonds will be allotted in Electronic (Dematerialised) form only and allotment intimation will be sent to the allottee(s). This Allotment intimation should neither be construed as a Letter(s) of Allotment nor as a credit advice, and hence it is non-transferable / non-transmittable and not tradable. The Bank will despatch the Allotment intimation to allottee(s) and credit the investor’s beneficiary account with the DP within 30 days from the Deemed Date of Allotment. This initial credit in the beneficiary account of the investor would akin to a Letter of Allotment. After completion of the necessary statutory formalities, the initial credit akin to a Letter of Allotment in the Depository Beneficiary Account of the investor would be replaced with the number of Bonds allotted. The Bonds issued in electronic (dematerialised) form, will be governed as per the provisions of The Depository Act, 1996. Securities and Exchange Board of India (Depositories and Participants) Regulations, 1996, rules notified by NSDL/ CDSL/ Depository Participant from time to time and applicable laws and rules notified in respect thereof. Redemption The face value of The Bonds allotted will be redeemed as indicated below:

• The payment will be made in the name of the bondholder whose name appears on the Register of Bondholders / List of Beneficial owners given by depository to The Bank as on the record date. The record date for payment of interest shall be fixed in accordance with the provisions of the listing agreement from time to time.

• The Bank’s liability to Bondholder(s) towards all their rights including payment of interest or otherwise shall

cease and stand extinguished from the due date of redemption in all events. Further, The Bank will not be liable to pay interest, income or compensation of any kind after the date of such redemption of The Bonds.

22

• In case, bonds are lodged (after rematerialisation) for transfer, wherever the signature(s) of transferor(s) in the intimation sent to The Bank is/are not in accordance with the specimen signature(s) of the such transferor(s) available on records of The Bank, all payments on such bonds will be kept in abeyance by The Bank till such time as The Bank is satisfied in this regard.

• On The Bank discharging the payment due upon redemption in the manner specified above in respect of The

Bonds, the liability of The Bank shall stand extinguished.

• The Bonds held in the Dematerialised Form shall be taken as discharged on payment of the redemption amount by The Bank on maturity to the list of Beneficial Owners as provided by NSDL / CDSL. Such payment will be a legal discharge of the liability of The Bank towards the Bondholders. On such payment being made, The Bank will inform NSDL / CDSL and accordingly the account of the Bondholders with NSDL / CDSL will be adjusted.

Put / Call Option There is no put / call option available to the investors / The Bank on The Bonds placed under this IM. Dematerialisation Applications are being made by The Bank to CDSL and NSDL for admitting The Bonds for dematerialisation. The required documentation will be done by The Bank in this regard. The applicants are requested to note the following points while submitting the applications for subscription to The Bonds: 1. An applicant has the only option of seeking allotment of Bonds in electronic mode. 2. The applicants must necessarily fill in the details pertaining to the beneficiary account no. and Depository

Participant’s ID number at the appropriate column in the application form 3. An applicant must have at least one beneficiary account with any of the Depository Participants (DPs) of NSDL or of

CDSL, registered with SEBI, prior to making the application 4. Bonds allotted to an applicant in the electronic account will be credited directly to the respective beneficiary

accounts (with the DP) 5. For allotment in electronic form, names in the Bond application form should be identical to those appearing in the

account details in the depository. In case of joint holders, the names should necessarily be in the same sequence as they appear in the account details in the depository

6. Non-transferable allotment intimations / refund orders will be directly sent to the applicant by the Bank. 7. The applicant is responsible for the correctness of the applicant’s demographic details given in the application form

vis-à-vis those with his / her DP. 8. As per the directives issued by RBI fresh investments by Bonds and Financial institutions are to be held only in

Dematerialised form. 9. Other investors will have the option to hold The Bonds in dematerialised form and deal with the same as per the

provisions of Depositories Act, 1996 and the rules, regulations thereunder and the byelaws (operational instructions) of NSDL / CDSL from time to time (which includes rematerialisation).

23

Succession Since The Bonds are issued in the electronic form, the provisions of the Depositories Act, 1996, and the rules there-under read with the relevant Regulation issued by SEBI and the Byelaws of the respective Depositories shall apply for transmission of The Bonds in the case of death of individual Bondholder(s) Future Fund Raising The Bank of Rajasthan Limited will be entitled to raise funds in future in appropriate form, subject to the permissions required, if any, from RBI or any other competent authority, including issue of debentures / bonds / other securities in any manner having such ranking in priority, pari passu or otherwise. The Bank of Rajasthan Limited will also be entitled to change its capital structure including issue of shares of any class, on such terms and conditions as The Bank of Rajasthan Limited may think appropriate, without the consent of intimation to the bondholder(s) in this connection. Rights of Bondholder(S) The Bondholder(s) will not be entitled to any other rights and privileges of shareholders other than those available to them under relevant statutes. The Bonds shall not confer upon the holders the right to receive notice or to attend or vote at the general meetings of The Bank of Rajasthan Limited. The principal amount and interest, if any, on The Bonds will be paid to the holder only, or in the case of joint holders, to the one whose name stands first. The Bonds shall be subjected to other usual terms and conditions applicable to the terms of the placement and also to the covenants of the Trust Agreement. Modification of Rights The rights, privileges terms and conditions attached to The Bonds may be varied, modified or abrogated with the consent, in writing, of those holders of The Bonds who hold at least three fourth of the outstanding amount of The Bonds or with the sanction accorded pursuant to a resolution passed at a meeting of the Bondholders, provided that nothing in such consent or resolution shall be operative against The Bank where such consent or resolution modifies or varies the terms and conditions of The Bonds, if the same are not acceptable to The Bank. Notices The notices to the Bondholder(s) required to be sent by The Bank shall be deemed to have been given if sent by ordinary post to the original holder or first allottee or registered holders of The Bonds as the case may be. All notices to be given by the Bondholders shall be sent by Registered post or by hand delivery to the Compliance Officer (Company Secretary) at the Corporate Office of The Bank at Mumbai. Who Can Apply Investors in the following categories, who are established / resident in India and who have been addressed through the communication directly, only are eligible to apply: 1. Companies and Bodies Corporate 2. Religious and Charitable Trusts 3. Banks, Financial Institutions and Mutual Funds. 4. Regional Rural Banks and Co-operative Banks. 5. Gratuity Funds and Pension Funds 6. Provident Funds and Superannuation Funds 7. Insurance Companies 8. Port Trusts in India. 9. Co-operative Institutions / Societies 10. Individuals who are not minors

24

Applications not to be made by 1. Partnership Firms or their nominees; 2. Overseas Corporate Bodies (OCBs); 3. Foreign Institutional Investors (FIIs). Applications under Power of Attorney A certified true copy of the power of attorney or the relevant authority as the case may be alongwith the names and specimen signature(s) of all the authorized signatories and the tax exemption certificate/ document, if any, must be lodged alongwith the submission of the completed Application Form. Further modifications/ additions in the power of attorney or authority should be notified to the Bank or to its Registrars or to such other person(s) at such other address(es) as may be specified by the Bank from time to time through a suitable communication. Application By Companies / Corporate Bodies / Financial Institutions / Statutory Companies. The application must be accompanied by certified true copes of (i) Memorandum and Articles of Association / Constitution / Bye laws (ii) resolution authorising investment and containing operating instructions (iii) specimen signatures of authorised signatories (iv) relevant certificate(s) in the prescribed form(s) under Income Tax Rules, 1961, if exemption is .sought from deduction of tax at source on interest income. Application by Mutual Funds In case of applications by Mutual Funds, a separate application must be made in respect of each scheme of an Indian Mutual Fund registered with SEBI and such applications will not be treated as multiple applications, provided that the applications made by the Asset Management Company/ Trustees/ Custodian clearly indicate their intention as to the scheme for which the application has been made The applications must be accompanied by certified true copies of (i) Power of Attorney (ii) specimen signatures of authorised signatories. Under the SEBI (Mutual Funds) regulations, 1996, Mutual Funds may invest in debt instruments. In case of application by Mutual Funds, certified true copies of (i) SEBI registration certificate, (ii) resolution authorising investments and containing all operating instructions must accompany the applications, and (iii) specimen signatures of authorised signatories. Application by Provident Funds, Superannuation Funds, Pension and Gratuity Funds The Government of India has permitted Provident, Superannuation, Pension and Gratuity Funds, subject to their assessment of the risk-return prospects, to invest up to 10 per cent in the Bonds and securities issued by private sector organisation including banks provided that the bonds or securities have an investment grade rating from atleast two credit rating agencies. Accordingly, provident, superannuation, pension and gratuity funds can invest up to 10 per cent of their corpus in these bonds. The applications must be accompanied by certified true copies of (I) Trust Deed/Bye laws (ii) resolution authorising investment and containing operating instructions (iii) specimen signatures of authorised signatories (iv) Recognition Certificate from Income Tax Department. Documents to be provided by Investors Investors need to submit the following documentation, along with the application form, as applicable.

1. Memorandum and Articles of Association / Documents Governing Constitution 2. Resolution authorizing investment 3. Certified True Copy of the Power of Attorney 4. Specimen signatures of the authorised signatories duly certified by an appropriate authority.

25

IV PARTICULARS OF THE PLACEMENT Object of The Placement

The proceeds of this offer will be utilised for the regular business activities of the bank after meeting all expenses of the issue.

Size of The Placement The Bank is privately placing 700 Unsecured, Redeemable, Non-convertible, non-cumulative, Taxable bonds in the nature of promissory notes of face value Rs.10 Lakh each for cash at par aggregating Rs. 7000 Lakh including green-shoe option of Rs. 2000 Lakh, through this IM.

Subscription Money The entire amount of Rs.10,00,000/- (Rupees Ten Lakh only) per bond is payable on application. Where an applicant is allotted a lesser number of bonds than applied for, the excess amount paid on application will be refunded to the applicant. Deemed Date of Allotment The deemed date of allotment shall be December 28, 2005. The interest on The Bonds would accrue from the deemed date of allotment. The actual allotment may occur on a date other than the deemed date of allotment. Listing The Bank proposes to get The Bonds listed on the Wholesale Debt Market (WDM) Segment of The Stock Exchange, Mumbai (BSE) Payment of Interest Interest payable in respect of The Bonds shall be payable semi annually every year from the deemed date of allotment. If any interest payment date falls on a day, which is not a business day in Mumbai (hereinafter called “business day”, being a day on which Commercial Banks are open for business), then payment of interest will be made on the next business day but without liability for making payment of interest for the delayed period. Payment of interest will be made to the sole holder or in the case of joint holders to the one whose name stands first in the Register of Bondholders, on the Semi Annual Interest Payment Date. Interest cheques will be payable at par at all the designated branches of The Bank. For this purpose, record date will be announced as per the applicable rules. All interests on The Bonds will cease from the date of redemption in all events. Interest on Subscription Money Interest at the coupon rate (subject to deduction of tax at source at the rate prevailing from time to time under the provisions of the Income Tax Act, 1961, or any other statutory modification or re-enactment thereof), would be payable on the entire application money to all allottees. Such interest shall be paid for the period commencing from the date of realisation of cheque(s)/ demand draft(s) upto one day prior to the Deemed Date of Allotment. In the case of allottees to whom partial allotment is made, such interest shall not be payable on the subscription money to the extent refunded. The interest warrants will be credited via ECS/RTGS or dispatched by registered post at the sole risk of the applicant, to the sole/ first applicant. No interest on subscription money will be payable in cases of invalid applications. Interest on The Bonds The Bonds shall carry interest of 8.70% / 8.50% per annum payable semi annually on 28th June and 28th December every year till the redemption of The Bonds.

26

Tax Deduction at Source Tax as applicable under the Income Tax Act, 1961 or any other statutory modification or re-enactment thereof will be deducted at source. Those desirous of claiming exemption from deduction of income tax at source on the interest on subscription money, are required to submit the necessary certificate (s), in duplicate, along with the application form in terms of Income Tax Rules. Interest payable subsequent to the Deemed Date of Allotment of Bonds will be treated as “Interest on Securities” as per Income Tax Rules and Bondholders desirous of claiming exemption from deduction of income tax at source on the interest payable on Bonds will have to submit a certificate on Form 15-F (in case of individuals) or Certificate issued by the Assessing Officer / Income Tax Officer on Form 15 AA (in the case of others) under Income Tax Rules, 1962, in duplicate, periodically so as to reach the Registers at least 15 days before the Interest Payment Date. Basis of Allotment The allotment will be finalised based on the applications received from the investors. In the event of over-subscription, The Bank reserves the right to decide the basis of allotment in consultation with the Lead Arrangers to The Placement. The Bank reserves the right to reject in full or part any or all of the offers received by it to invest in The Bonds without assigning any reason for such rejection acceptance of the offer shall be subject to completion of subscription formalities as detailed in the application form. Issue of Letter of Allotment Allotment to investors shall be made after due verification of the application forms, the accompanying documents and or realisation of the application money. Appropriate letters intimating the allotment will be mailed to the investors. The demat credit for The Bonds will be made into the respective depository participant beneficiary account of the investor by way of corporate action after completing the legal formalities relating to stamp duty, documentation etc. Refunds For applicants whose applications have been rejected or allotted in part, refund orders will be dispatched within 15 days from the Deemed Date of Allotment. Refund of applicants will be dispatched through post/courier. Denomination of The Bonds The Bonds are issued in denominations of Rs. 10 Lakh. Appropriate credit in electronic form will be given in the respective beneficiary accounts following a corporate action after completing all statutory formalities.

Splitting and Consolidation This concept is not applicable in the demat form since the saleable lot is one bond. Redemption The face value of The Bonds issued will be redeemed at par, at the end of 112 / 88 months from the Deemed Date of Allotment. Payment on Redemption Payment of redemption proceeds of The Bonds will be made to the Bondholder(s) whose name(s) appear(s) as registered Bondholder(s) on the records of The Bank on the Date of Redemption. All interests on The Bonds (s) will cease from the Date of Redemption in all events. In the case of joint holders, payment will be made to the person whose name stands first in the register of bonds.

27

Transfer and Transmission of The Bonds Transfer and Transmission of The Bonds shall be subject to the Depositories Act, 1996, the rules made thereunder, the byelaws, rules and regulations of the depositories as amended from time to time. Notices Notices to the Bondholder (s) required to be given by The Bank shall be deemed to have been given if sent by ordinary post to the original sole / first allottee (s) / beneficiary holder of The Bonds. All notice to be given by the Bondholder (s) shall be sent by registered post or by hand delivery to the Head Office of The Bank or to the Registrars or to such persons at such address as may be notified by The Bank from time to time. Effect of Holidays Should any of the date(s) defined above or elsewhere in this Information Memorandum, excepting the Date of Allotment, fall on a Sunday or a Public Holiday or a holiday under the NI Act, the next working day shall be considered as the effective date. Ranking of Bonds The Bonds are Unsecured Redeemable Non-Convertible Non-Cumulative Subordinated debt and are in the nature of promissory notes. The Bonds will constitute direct, unsecured and subordinated obligations of The Bank, ranking pari passu with the existing subordinated debt of The Bank and subordinated to the claims of all other creditors and depositors of The Bank as regards repayment of principal and interest by The Bank. The Bonds shall be free of any restrictive clauses and shall not be redeemable at the initiative of the holder or without the consent of the Reserve Bank of India. Bondholder Not a Shareholder The Bondholder(s) shall not be entitled to any rights and privileges of shareholders other than those available to them under statute. The Bond(s) shall not confer upon the holders the right to receive notice(s), or to attend and vote at General Meetings of shareholders of The Bank. Future Borrowings The Bank shall be entitled to borrow / raise loans or avail of financial assistance in whatever form as also issue any securities debt, equity or hybrid by whatever name called in any manner ranking pari passu or otherwise with the existing classes of such securities and to change its capital structure, including issue of share of any class or redemption or reduction of any class of paid up capital, on such terms and conditions as The Bank may think appropriate, without the consent of, or intimation to, the holders of The Bonds, in this connection. Miscellaneous A Register of Bondholders shall be maintained at the Corporate Office of the Bank. Such Register shall be closed as per applicable rules prior to the date of redemption. In case of dissolution/bankruptcy/insolvency/winding up of Bondholders, the Bond certificates shall be transmittable to the Legal Representative(s) / Successor(s) or the Liquidator as the case may be in accordance with the applicable provisions of law on such terms as may be deemed appropriate by The Bank. Governing Law The Bonds are governed by and shall be construed to be in accordance with the existing laws of India. Any dispute arising thereof will be subject to the jurisdiction of courts at Mumbai only.

28

How To Apply

• Application forms duly completed in all respects must be submitted with the Main Branches of The Bank of Rajasthan Limited at Mumbai, Kolkata, New Delhi, Chennai, Bangalore, Jaipur, Chandigarh, Bhilwara, Jodhpur, Kota, Indore and Udaipur

• Cheque(s)/Demand Draft(s) should be drawn in favour of “BOR– Tier II Bond Issue (Series IV)” and crossed "Account Payee Only". Cheque(s)/Demand draft(s) may be drawn on a Scheduled Commercial Bank, which is a member or a sub-member of the Banker’s Clearing House located at Mumbai, Kolkata, New Delhi, Chennai, Bangalore, Jaipur, Chandigarh, Bhilwara, Jodhpur, Kota, Indore and Udaipur.

• Code for Electronic transfer of funds

IFSC Code: BRAJ 0003350

Current Account No. 3390 302 112413

Narration: Subscription towards Tier II Series IV Bonds

• Outstation cheques, cash, money orders and postal orders shall not be accepted.

• As a matter of precaution against possible fraudulent encashment of interest warrants due to loss/misplacement, applicants are requested to mention the full particulars to their bank account/RTGS details, as specified in the Application Form. Interest warrants will then be made out in favour of the bank for credit to the applicant’s account. In case the full particulars are not given, cheques will be issued in the name of the applicant at his/ her risk.

• Receipt of applications will be acknowledged by the respective Collecting Banker in the “Acknowledgment Slip”, appearing below the Application Form. No separate receipt will be issued.

• All applicants should mention their Permanent Account Number or the GIR number allotted under Income Tax Act, 1961 and the Income Tax Circle/Ward/District. In case where neither the PAN nor GIR number has been allotted, the fact of non-allotment should be mentioned in the application form in the space provided.

• The application would be accepted as per the terms of the Scheme outlined in the Memorandum of Private Placement.

These details are available in the application form also. Applications under Power of Attorney In case of application under powers of Attorney by limited companies or other bodies corporate, a certified true copy of Power of Attorney or a copy of the approval of the relevant authority / resolution as the case may be must be deposited along with the Application Form. Right to Accept or Reject Application The Bank is entitled at its sole and absolute discretion, to accept or reject any application, in part or in full, without assigning any reason. Application Forms which are not complete in all respects are liable to be rejected. Interest on subscription money will be paid from the date of realisation of cheque (s) / demand draft (s) till the date of refund. Joint Applications Applications may be made in single or joint names (not more than three). In case of Joint Applications, refund, pay orders, interest warrants etc. if any, will be drawn in favour of the first applicant and all communications will be addressed to the first applicant at her/his address as stated in the application form.

29

Multiple Applications An applicant should submit only one application form (and not more than one) for the total number of Bonds applied for. Two or more applications in single or joint names will be deemed to be multiple applications if the sole and/or first applicant is one and the same. The Bank reserves the right to accept or reject, in its absolute discretion, any or all multiple applications. Application by Mutual Funds In case of applications by Mutual Funds, a separate application must be made in respect of each scheme of an Indian Mutual Fund registered with SEBI and such applications will not be treated as multiple applications, provided that the application made by the Asset Management Company / Trustees / Custodian clearly indicate their intention as to the scheme for which the application has been made. Applications under Power of Attorney or by Limited Companies In case of applications under Power of Attorney or by Companies, Bodies Corporate, Societies registered under the applicable laws, trustees of Trusts, Provident Funds, Superannuation Funds, Gratuity Funds and Scientific and/or Industrial Research Organisations, a certified copy of the Power of Attorney or the relevant authority, as the case may be, must be lodged separately at the office of the Registrars to The Placement simultaneously with the submission of the application form, indicating the serial number of the application form and the name of The Bank and the branch office where the application has been submitted and The Bank and the branch on which the cheque/draft has been drawn. The Bank in its absolute discretion reserves the right to relax the above condition of simultaneous lodging of the power of attorney along with application form subject to such terms and conditions as it may deem fit. PAN/GIR Number Applicant, or, in case of applications in joint names, each of the applicants should mention his/her/their Permanent Account number (PAN) allotted under Income Tax Act, 1961 or where the same has not been allotted, the GIR Number and the IT Circle/Ward/District. In case where neither the PAN nor the GIR number has been allotted, or the applicant is not assessed to Income tax, the appropriate box provided for the purpose in the Application Form must be ticked. Applications without this will be considered incomplete and are liable to be rejected. Signatures, thumb impressions and signatures other than in English/Hindi or any other language specified in the 8th Schedule to the Constitution of India, must be attested by a Magistrate or a Notary Public or a Special Executive Magistrate under his/her official seal. Nomination Facility The Bonds being issued in electronic form shall be governed by the provisions of the Depositories Act, 1996 and the Rules made there under. Rejection of Applications