mercer capital's value focus: auto dealer industry | year-end 2015

TRANSCRIPT

VALUE FOCUSAuto Dealer Industry

www.mercercapital.com

Overview Inside

The aptly named Great Recession hit the auto

industry and its dealers harder than almost any

other industry, save for construction and housing:

As unemployment rose, consumer spending

and home values plummeted. With little to no

discretionary income and no means to finance

car purchases, sales tumbled, margins were

squeezed, and GM and Chrysler filed for Chapter

11 bankruptcy. Recovery began in 2009, con-

fidence and disposable incomes rose allowing

consumers to fund purchases of more durable

goods, including cars. These trends are expected

to continue through 2021. However, the auto

dealer industry, though making a strong recovery

from the most recent recession, is facing pressures

from government regulation, shifting demand and

supply, and new market entrants.

More stringent environmental standards are

causing car prices to rise, the shift to internet for

information and purchasing is forcing margins

down (but also increasing volume), and demand is

shifting more toward hybrid, electric, and autono-

mous cars. The leading auto dealers are taking

notice of these shifting trends.

Macroeconomic Indicators

Productivity 1

Housing 3

Personal Consumption

and Confidence 5

Energy 6

Auto Dealer Indicators

Average Dealer Profile 7

Valuation Trends 9

Mergers & Acquisitions 12

Guideline Company Pricing 13

About Mercer Capital 15

Year-End 2015

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 1 www.mercercapital.com

Macroeconomic Indicators // Productivity

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

2008

20

09

2010

20

11

2012

20

13

2014

20

15

GD

P (in Billions)

Ann

ualiz

ed R

eal G

row

th R

ate

Quarterly Annualized Real Growth Rate Annual Real Growth Rate GDP (Current Dollars) GDP (Chained 2009 Dollars)

Source: Bureau of Economic Analysis

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

2008

Q1 Q2 Q3 Q4

2009

Q1 Q2 Q3 Q4

2010

Q1 Q2 Q3 Q4

2011

Q1 Q2 Q3 Q4

2012

Q1 Q2 Q3 Q4

2013

Q1 Q2 Q3 Q4

2014

Q1 Q2 Q3 Q4

2015

Q1 Q2 Q3 Q4

Annualized Quarterly Change Annual Change Source: Bureau of Labor Statistics

Gross Domestic Product

According to advance estimates released

by the Department of Commerce’s Bureau

of Economic Analysis (BEA), Real Gross

Domestic Product (GDP), the output of

goods and services produced by labor

and property located in the United States,

increased at an annualized rate of 0.7%

during the fourth quarter of 2015. The

increase was attributable to gains in per-

sonal consumption expenditures, residential

fixed investment, and federal government

spending. Private inventory investment,

exports, and nonresidential fixed investment

decreased. Imports (which are subtracted

from the national income and product

accounts used in the calculation of GDP)

increased.

Business & Manufacturing Productivity

According to the Bureau of Labor Statistics

(BLS), seasonally adjusted nonfarm busi-

ness productivity decreased at an annual

rate of 3.0% in the fourth quarter of 2015.

The decrease was a function of relatively flat

output growth combined with an increase of

3.3% in hours worked. Hourly compensation,

real hourly compensation, and unit labor costs

also experienced increases. The produc-

tivity decrease in the fourth quarter follows

increases of 3.5% and 2.1% in the second and

third quarters, respectively. Annual average

productivity increased 0.3% in the fourth

quarter of 2015 relative to the fourth quarter

of 2014.

Productivity decreased 2.7% for the business

sector (inclusive of farming activity) in the

fourth quarter of 2015. This was the result

of a 3.4% increase in hours worked and

a 0.6% increase in output. Manufacturing

productivity, generally more volatile in its

Gross Domestic Product

Change in Nonfarm Business Productivity

quarterly measures, decreased 0.4% during the quarter. In the second quarter of 2015, BLS

issued revised productivity measures for all periods since 2010, reflecting revisions in source

data, which resulted in weaker productivity growth than previously thought.

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 2 www.mercercapital.com

Macroeconomic Indicators // Productivity (cont.)

-100.0%

-50.0%

0.0%

50.0%

100.0%

150.0%

Dec

-05

Mar

-06

Jun-

06

Sep-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Dow Jones Industrial Average S&P 500 NASDAQ Composite Source: Bloomberg L.P.

The Financial Markets

December 2015 marked the end of a volatile

year in the financial markets. After losses in

the third quarter, four major indices exhibited

growth during the fourth quarter of 2015. Most

Treasury yields improved during the quarter,

due largely to the actions of the Federal

Reserve. The Dow Jones Industrial Average

ended the fourth quarter of 2015 up 7.0% for

the quarter, though down 2.2% during 2015.

The S&P 500 Index also increased 6.5%

during the fourth quarter and down 0.7% in

2015. The NASDAQ Composite Index rose

8.4% during the fourth, and overall, rose

5.7% during 2015. The following chart shows

the relative price performance of the Dow

Jones Industrial Average, S&P 500, and

NASDAQ Composite Indices.

Equity Index Price Return

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

Dec

-99

Mar

-00

Jun-

00

Sep-

00

Dec

-00

Mar

-01

Jun-

01

Sep-

01

Dec

-01

Mar

-02

Jun-

02

Sep-

02

Dec

-02

Mar

-03

Jun-

03

Sep-

03

Dec

-03

Mar

-04

Jun-

04

Sep-

04

Dec

-04

Mar

-05

Jun-

05

Sep-

05

Dec

-05

Mar

-06

Jun-

06

Sep-

06

Dec

-06

Mar

-07

Jun-

07

Sep-

07

Dec

-07

Mar

-08

Jun-

08

Sep-

08

Dec

-08

Mar

-09

Jun-

09

Sep-

09

Dec

-09

Mar

-10

Jun-

10

Sep-

10

Dec

-10

Mar

-11

Jun-

11

Sep-

11

Dec

-11

Mar

-12

Jun-

12

Sep-

12

Dec

-12

Mar

-13

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Source: Bureau of Labor Statistics

Unemployment and Payroll Jobs

According to the BLS, the unemployment rate

was 5.0% in December 2015, unchanged

from October and November. Unemployment

rates increased steadily throughout 2008

and into 2009, peaking at 10% in October

2009. The October 2009 unemployment rate

represented the highest level since 1983. Pre-

recession unemployment levels were reached

in December 2014. While unemployment has

consistently fallen throughout the past several

years, the labor force participation rate is

also lower relative to pre-recession levels. In

December 2015, the labor force participation

rate stood at 62.6% (relative to mid- to high-

60s prior to the recession). The labor force

participation rate in the third quarter was

generally lower than the rate in the second

quarter of 2015. Excluding the recent trend,

the last time the labor force participation rate

was lower than its current level was 1977.

As job availability increases the labor force

could increase due to individuals re-entering

the workforce, which could lead to periodic

increases in the unemployment rate in the

foreseeable future. Economists surveyed

Civilian Unemployment Rate

by The Wall Street Journal anticipate an unemployment rate of 4.8% by mid-2016 and a further

decline to 4.7% by December 2016. The number of nonfarm payroll jobs increased by 292,000 in

December 2015. December’s gain follows increases of 307,000 and 252,000 jobs in October and

November, respectively. During 2008 and 2009, the economy lost nearly 8.7 million nonfarm payroll

jobs. Experts believe the economy is still short nearly 2.7 million jobs. Economists surveyed by The

Wall Street Journal anticipate payroll gains of approximately 191,000 jobs per month over the next

year. Population growth adds approximately 102,000 individuals to the workforce per month.

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 3 www.mercercapital.com

Home building activity has traditionally been a primary driver of overall economic activity because new home construction stimulates a broad

range of industrial, commercial, and consumer spending and investment. According to the U.S. Census Bureau, new privately owned housing

starts were at a seasonally adjusted annualized rate of 1,149,000 units in December 2015, 2.5% below the revised November rate of 1,179,000

units but 6.4% above the December 2014 level. The seasonally adjusted annual rate of private housing units authorized by building permits

(considered the best indicator of future housing starts) was 1,232,000 units in December 2015, 3.9% below the revised November estimate of

1,282,000 but 14.4% above the December 2014 level.

According to the National Association of Realtors (“NAR”), existing-home sales (at a seasonally adjusted annual rate) totaled 5.5 million in

December 2015, 14.7% above the November level, and 7.7% above the December 2014 level. According to NAR, 2015 marks the best year of

existing home sales since 2006. Housing inventory stood at 1.8 million existing-homes, representing approximately four months of supply at the

current sales pace and down 3.8% since December 2014. The national median existing-home price increased 7.6% relative to December 2014.

Distressed sales, which include foreclosures and short sales, accounted for approximately 8% of sales in December 2015, relative to 11% of

home sales in December 2014.

The December 2015 data indicate that the housing market recovery continues to improve. The housing market has improved considerably from

the depths of the financial crisis, though it remains below peak levels measured in 2005 and 2006. Going forward, slow wage growth and higher

interest rates pose risks to the housing sector.

Macroeconomic Indicators // Housing

0%

1%

2%

3%

4%

5%

6%

7%

8%

Jan-2

006

Jul-2

006

Jan-2

007

Jul-2

007

Jan-2

008

Jul-2

008

Jan-2

009

Jul-2

009

Jan-2

010

Jul-2

010

Jan-2

011

Jul-2

011

Jan-2

012

Jul-2

012

Jan-2

013

Jul-2

013

Jan-2

014

Jul-2

014

Jan-2

015

Jul-2

015

30-Year Mortgage Rate 10-Year Treasury rate Effective Federal Funds Rate

Source: Federal Reserve Economic Data

Key Interest Rates

The Federal Reserve’s Open Market

Committee (“FOMC”) lowered its target for

the federal funds rate to a range of 0% to

0.25% during the fourth quarter of 2008,

representing a total rate cut of 175 to 200

basis points during the quarter. Target

rates were held steady during 2009 and

remained unchanged until December of

2015. This has kept interest rates low,

increasing the ability of households to fund

spending. However, in December 2015,

the FOMC increased the target range for

the federal funds rate to a range of 0.25%

to 0.50%. While still low, this will likely slow

increases in consumer spending. Further,

the yield on the 10-year Treasury note is

expected to increase during 2016, which

could cause consumers to switch to used

cars, as new car loans are less affordable.

Change in Key Interest Rates

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 4 www.mercercapital.com

Macroeconomic Indicators // Housing (cont.)

0

50

100

150

200

250

Jan-20

06

May-20

06

Sep-20

06

Jan-20

07

May-20

07

Sep-20

07

Jan-20

08

May-20

08

Sep-20

08

Jan-20

09

May-20

09

Sep-20

09

Jan-20

10

May-20

10

Sep-20

10

Jan-20

11

May-20

11

Sep-20

11

Jan-20

12

May-20

12

Sep-20

12

Jan-20

13

May-20

13

Sep-20

13

Jan-20

14

May-20

14

Sep-20

14

Jan-20

15

May-20

15

Sep-20

15

Housing Price Index SA Case-Shiller 10 City Index SA Case-Shiller 20 City Index SA

Source: Federal Housing Finance Agency and Federal Reserve Economic Data

Housing Prices

Housing prices have not completely

recovered to pre-recession levels but

have increased year-over-year since

January 2011.

Change in Housing Prices

0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 1.3 1.4 1.5 1.6 1.7 1.8 1.9 2.0 2.1 2.2 2.3 2.4

Dec-00

Jun-01

Dec-01

Jun-02

Dec-02

Jun-03

Dec-03

Jun-04

Dec-04

Jun-05

Dec-05

Jun-06

Dec-06

Jun-07

Dec-07

Jun-08

Dec-08

Jun-09

Dec-09

Jun-10

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Private Housing Starts Single Family Starts

Source: U.S. Census Bureau Note: Permits at a given date are generally a leading indicator of future starts. Beginning with January 2004, building permit data reflects the change to the 20,000 place series.

Private Housing

Single Family Housing

Housing Starts

According to the U.S. Census Bureau,

new privately-owned housing starts were

at a seasonally adjusted annualized rate

of 1,149,000 units in December 2015,

2.5% below the revised November rate

of 1,179,000 units but 6.4% above the

December 2014 level. The seasonally

adjusted annual rate of private housing

units authorized by building permits (con-

sidered the best indicator of future housing

starts) was 1,232,000 units in December

2015, 3.9% below the revised November

estimate of 1,282,000 but 14.4% above

the December 2014 level.

Seasonally Adjusted Annualized Rates of New Housing Starts and Building Permits

(millions of units)

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 5 www.mercercapital.com

Increases in disposable income allow for increases in personal consumption, especially debt-fund purchases like cars. However, these

increases must keep pace with inflation. Further, increases in disposable income tend to increase confidence in consumers and business

owners. Confident consumers have more optimistic expectations of the future: They expect a stronger economy, lower unemployment, higher

future wages, and better ability to pay for debt-funded purchases. Similarly, confident businesses are a gauge of an economy’s ability to employ

labor productively in the future.

Macroeconomic Indicators // Personal Consumption & Confidence

Disposable Income and Personal Consumption

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$33,000

$34,000

$35,000

$36,000

$37,000

$38,000

$39,000

Jan-2

006

Jun-2

006

Nov-20

06

Apr-20

07

Sep-20

07

Feb-20

08

Jul-2

008

Dec-20

08

May-20

09

Oct-20

09

Mar-20

10

Aug-20

10

Jan-2

011

Jun-2

011

Nov-20

11

Apr-20

12

Sep-20

12

Feb-20

13

Jul-2

013

Dec-20

13

May-20

14

Oct-20

14

Mar-20

15

Aug-20

15

Pers

onal

Con

sum

ptio

n (B

Illio

ns)

Pers

onal

Inco

me

Real Disposable Personal Income: Per capita, Chained 2009 Dollars, Monthly, Seasonally Adjusted

Personal Consumption Expendituress, Monthly, Seasonally Adjusted

Source: Federal Reserve Economic Data

0

20

40

60

80

100

120

Jan-

2006

Jul- 2

006

Jan-

2007

Jul- 2

007

Jan-

2008

Jul- 2

008

Jan-

2009

Jul- 2

009

Jan-

2010

Jul- 2

010

Jan-

2011

Jul- 2

011

Jan-

2012

Jul- 2

012

Jan-

2013

Jul- 2

013

Jan-

2014

Jul- 2

014

Jan-

2015

Jul- 2

015

Consumer Confidence Index NFIB Small Business Optimism Index

Source: Bloomberg, L.P.

Disposable Income and

Personal Consumption

Real personal income and personal

consumption have both been steadily

increasing year-over-year since 2010,

partly due to growth and partly due to

Federal Reserve policy keeping inflation

near 0.0%. Further, disposable income is

expected to continue rising through 2016.

Confidence

Both consumer and small business con-

fidence has been trending upward since

the Great Recession. This confidence

will drive demand for cars.

Change in Confidence

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 6 www.mercercapital.com

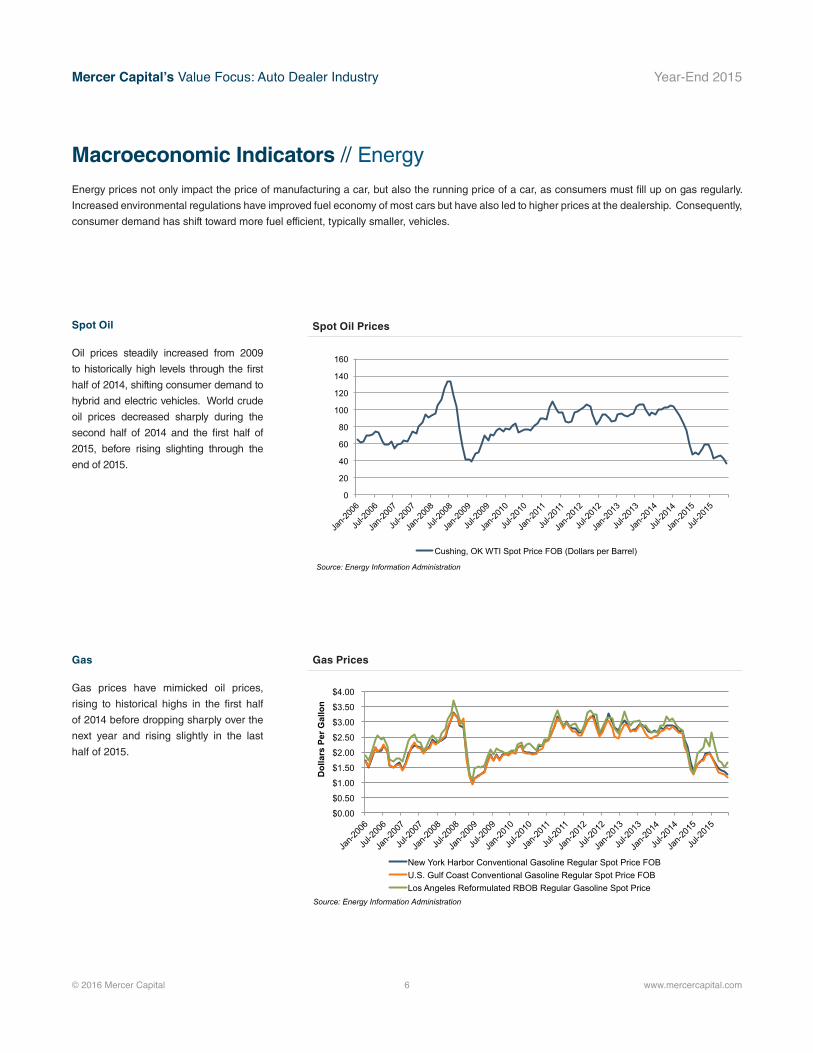

Energy prices not only impact the price of manufacturing a car, but also the running price of a car, as consumers must fill up on gas regularly.

Increased environmental regulations have improved fuel economy of most cars but have also led to higher prices at the dealership. Consequently,

consumer demand has shift toward more fuel efficient, typically smaller, vehicles.

Macroeconomic Indicators // Energy

0

20

40

60

80

100

120

140

160

Jan-2

006

Jul-2

006

Jan-2

007

Jul-2

007

Jan-2

008

Jul-2

008

Jan-2

009

Jul-2

009

Jan-2

010

Jul-2

010

Jan-2

011

Jul-2

011

Jan-2

012

Jul-2

012

Jan-2

013

Jul-2

013

Jan-2

014

Jul-2

014

Jan-2

015

Jul-2

015

Cushing, OK WTI Spot Price FOB (Dollars per Barrel)

Source: Energy Information Administration

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

Jan-2

006

Jul-2

006

Jan-2

007

Jul-2

007

Jan-2

008

Jul-2

008

Jan-2

009

Jul-2

009

Jan-2

010

Jul-2

010

Jan-2

011

Jul-2

011

Jan-2

012

Jul-2

012

Jan-2

013

Jul-2

013

Jan-2

014

Jul-2

014

Jan-2

015

Jul-2

015

Dol

lars

Per

Gal

lon

New York Harbor Conventional Gasoline Regular Spot Price FOB U.S. Gulf Coast Conventional Gasoline Regular Spot Price FOB Los Angeles Reformulated RBOB Regular Gasoline Spot Price

Source: Energy Information Administration

Spot Oil

Oil prices steadily increased from 2009

to historically high levels through the first

half of 2014, shifting consumer demand to

hybrid and electric vehicles. World crude

oil prices decreased sharply during the

second half of 2014 and the first half of

2015, before rising slighting through the

end of 2015.

Gas

Gas prices have mimicked oil prices,

rising to historical highs in the first half

of 2014 before dropping sharply over the

next year and rising slightly in the last

half of 2015.

Spot Oil Prices

Gas Prices

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 7 www.mercercapital.com

Macroeconomic measures including employment, productivity housing prices and starts, interest rates, and disposable income have provided an

environment conducive to car purchases. However, rising prices, downward pressure on margins, and changes in demand have caused shifts

in automobile demand.

Auto Dealer Indicators // Average Dealer Profile

8.0

8.5

9.0

9.5

10.0

10.5

11.0

11.5

12.0

1995

19

96 19

97 19

98 19

99 20

00 20

01 20

02 20

03 20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13 20

14 20

15

F2016

F2017

F2018

Passenger Cars Light Trucks Total

Source: IHS Automotive, formerly Polk

0

5

10

15

20

25

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

Dea

lers

hips

(Tho

usan

ds)

Sale

s (M

illio

ns)

Cost of Sales Total Dealership Expense Pre-Tax Income Dealerships Source: NADA Data

Average Age of Vehicle Fleet

IHS Automotive, a global automotive

market intelligence firm, found that the

average age of all light vehicles hit a record

high of 11.5 years in 2015 due to rising car

quality; they expect this rate to slow as

new vehicle sales continue to recover, not

hitting 11.6 years until 2016 and 11.7 years

until 2018. Further, they expect this trend

to provide more opportunities for the auto-

motive aftermarket.

Dealership Sales

By the end of 2015, there was an increase

of approximately 150 franchised deal-

erships, only the second increase since

1987, reversing a consolidation trend.

Sales rose 6.8% in 2015, the sixth

year in a row, well above pre-recession

highs. However, net profit before taxes

remained flat at 2.2%. Current pres-

sure on margins stems primarily from

the fact that the asymmetric information

that once favored dealers is balanced

by internet sites such as Edmunds,

cars.com, and autotrader.com. While

margins have been decreasing, deal-

erships have benefitted from increases

in volume.

Average Age of Vehicle Fleet

Dealership Sales

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 8 www.mercercapital.com

Auto Dealer Indicators // Average Dealer Profile (cont.)

Products and Services Segmentation

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

20

15

Sale

s

New Vehicle Used Vehicle Service and Parts Source: NADA Data

Products and Services Segmentation

From 2005 to 2010, the percentage of

sales from used vehicles and service and

parts segments of the industry rose, as

financing new vehicle purchases became

more difficult. Since then, new vehicles’

share of sales has gone up, but has not

recovered to pre-recession levels.

Vehicles and Price

0

200

400

600

800

1,000

1,200

$25,000

$26,000

$27,000

$28,000

$29,000

$30,000

$31,000

$32,000

$33,000

$34,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

New

Veh

icle

s So

ld P

er D

eale

rshi

p

Aver

age

Ret

ail S

ellin

g Pr

ice

Average Retail Selling Price New Vehicles Sold Per Dealership

Source: NADA Data

Vehicles and Price

Through the second quarter of 2014,

prices were forced up by rising oil prices

and increased environmental regulations.

While oil prices have decreased dras-

tically, regulations have not resulting in

continuing increases in price. Average

vehicles sold per dealership continued

to rise even as the number of franchised

dealerships increased.

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 9 www.mercercapital.com

Valuation Trends

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

12/31/14 2/28/15 4/30/15 6/30/15 8/31/15 10/31/15 12/31/15

Auto Components Automobile Manufacturers S&P 500 NASDAQ Composite Dow Jones Industrial Average Source: Bloomberg L.P.

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

12/31/14 2/28/15 4/30/15 6/30/15 8/31/15 10/31/15 12/31/15 Ford Motor Co General Motors Co Honda Motor Co Ltd Toyota Motor Corp Tesla Motors Inc Nissan Motor Co Ltd Fiat Chrysler Automobiles NV

Source: Bloomberg, L.P.

Index Performance

OEM Stock Performance

OEMs and Indices

Auto components have continued to outpace auto manufacturers

reflecting continued increases in consumer spending on maintenance

compared to pre-recession levels.

Nissan, Fiat Chrysler, Honda, and Tesla are outperforming General

Motors, Toyota, and Ford. Significant events in the last year influencing

stock prices include volatile oil prices, various high profile recalls, and

increasing EPA emissions standards.

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 10 www.mercercapital.com

Valuation Trends (cont.)

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

100%

1991

19

92 19

93 19

94 19

95 19

96 19

97 19

98 19

99 20

00 20

01 20

02 20

03 20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13 20

15

FCA (Formerly Chrysler) Ford General Motors Toyota Honda Nissan Volkswagen Other Imports

Source: NADA Data *2014 Data Not Available

Brand Market Share By Unit Sales

FCA and other imports such as Subaru

were the only brands to increase market

share. FCA has experienced growth on

fuel efficient European cars entering the

American market. Volkswagen lost a sig-

nificant amount of market share on the

emissions testing scandal.

Brand Market Share By Unit Sales

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 11 www.mercercapital.com

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

12/31/14 1/31/15 2/28/15 3/31/15 4/30/15 5/31/15 6/30/15 7/31/15 8/31/15 9/30/15 10/31/15 11/30/15 12/31/15

AutoNation Inc Penske Automotive Group Inc Sonic Automotive Inc Group 1 Automotive Inc Asbury Automotive Group Inc Lithia Motors Inc

Source: Bloomberg L.P.

Auto Dealership Stock Performance

Publicly Traded Auto Dealerships

“In the fourth quarter, new and used vehicle margins on a combined

basis declined by $217 per vehicle retailed, or 11%, as compared to

the fourth quarter of 2014. As of year-end, our new vehicle invento-

ries increased 13% on a same store basis, as compared to the prior

year, driven by a 49% increase in Premium Luxury inventories. We

have begun, and will continue through the first quarter, to take the

necessary steps to align our costs, inventory, and pricing strategy to

adjust to the current market. In 2016, we expect industry new vehicle

unit sales will again exceed 17 million.” Mike Jackson, President and

CEO of AutoNation. “AutoNation Reports 2015 Fourth Quarter and

Full Year Results.” 28 January 2016.

“The diversification provided by our business model continues to

drive our business forward. Our U.K.-based retail automotive and

U.S.-based commercial truck businesses produced exceptional

results, and the stability of the parts and service business helped

our business produce another solid quarter. We expect 2016 will be

another solid year for both automotive and U.S. commercial truck

sales.” Roger S. Penske, Chairman of Penske Automotive Group.

“Penske Automotive Reports Fourth Quarter Results: Completes

Most Profitable Year in Company History.” 11 February 2016.

“While we delivered a record year in total for revenue, gross profit,

and adjusted diluted earnings per share, our fourth quarter results

were significantly hampered by the negative impact of continued oil

and gas price decreases on the economy in our prime markets of

Houston, Oklahoma and Texas in general. Additionally, we suffered

from increased new and used vehicle margin pressure resulting from

oversupply in a variety of key brands, especially in the U.S. luxury

segment.” Earl J. Hesterberg, President and CEO of Group 1 Auto-

motive. “Group 1 Automotive Reports Fourth Quarter and Full Year

Financial Results: Sets Record Revenue of $10.6 Billion and Earn-

ings of $6.87 Adjusted EPS for FY15.” 11 February 2016.

“I am very pleased with the performance of our team in the fourth

quarter and the year. Subsequent to December 31, 2015, market

news and expectations related to the retail automotive sector created

pressure on public company valuations. As a result, our Board of

Directors increased our authorization to repurchase shares by $100.0

million. During the first quarter of 2016, we repurchased approxi-

mately 4.0 million shares, roughly 7.9% of outstanding shares as

of December 31, 2015, for approximately $72.0 million. We expect

2016 to continue to be favorable to dealers and anticipate new

vehicle industry volume to be between 17.3 million and 17.6 million

units, but expect new vehicle GPU pressure to continue. We project

diluted earnings per share from continuing operations for 2016 to be

between $2.07 and $2.17 per share. This range includes the effect

of projected EchoPark® results and expansion. We are projecting a

loss related to EchoPark® of between $0.21 and $0.23 per diluted

share. We will have additional comments on our 2016 outlook in our

earnings call later today.” B. Scott Smith, President of Sonic Auto-

motive. “Sonic Automotive, Inc. Reports Record Results: Adjusted

Continuing Operations Quarterly EPS of $0.61, Increases Dividend

by 33%.” 23 February 2016.

Valuation Trends (cont.)

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 12 www.mercercapital.com

Mergers and Acquisitions

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

0

5

10

15

20

25

30

35

2009 2010 2011 2012 2013 2014 2015

Tota

l Tra

nsac

tion

Valu

e (m

illio

ns)

Num

ber o

f Tra

nsac

tions

Total Transaction Value Number of Transactions

Source: Capital IQ

M&A ActivityDeal activity slowed in 2014 in terms

of number of transactions, despite total

transaction value increasing. While overall

deal value was down in 2015, number of

transactions increased.

© 2016 Mercer Capital 13 www.mercercapital.com

Dealer Pricing

Auto Manufacturing Pricing

30-Jun Price

$

52 Week Perf.

%

LTM

Ent. Value $ Mil

Debt / Equity

%

EBITDAMargin

%

EV / Sales

Multiple x

EV / EBITDAMultiple

x

EV / Nxt Yr

EBITDA Multiple

x

Price / Earnings

xCompany Name TickerSales$ Mil

EBITDA$ Mil

Ford Motor Co F 13.48 -5.40% 149,558 15,987 186,369 463.84% 10.69% 1.25 11.66 13.46 7.08

General Motors Co GM 33.59 1.52% 152,356 12,914 113,494 158.29% 8.48% 0.74 8.79 6.67 5.61

Honda Motor Co Ltd HMC 31.69 10.65% 119,287 10,881 114,083 94.62% 9.12% 0.96 10.48 nm 13.31

Hyundai Motor Co 005380.KS 126.47 -15.66% 81,304 8,092 81,690 105.25% 9.95% 1.00 10.10 9.52 5.57

Toyota Motor Corp TM 123.04 0.84% 235,936 37,702 545,149 113.28% 15.98% 2.31 14.46 nm 20.04

Tesla Motors Inc TSLA 240.01 7.91% 4,046 (294) 34,259 249.38% -7.27% 8.47 nm 23.55 nm

Nissan Motor Co Ltd NSANY 20.99 23.94% 101,065 13,132 149,933 150.89% 12.99% 1.48 11.42 nm 18.57

Peugeot SA PEUGF 17.42 na 60,690 5,119 22,210 70.84% 8.44% 0.37 4.34 nm 17.78

Average 75.84 3.40% 113,030 12,942 155,898 175.80% 8.55% 2.07 10.18 13.30 12.57

Median 32.64 1.52% 110,176 11,898 113,789 132.08% 9.54% 1.13 10.48 11.49 13.31

Source: Bloomberg L.P.

31-Dec Price

$

52 Week Perf.

%

LTM

Ent. Value $ Mil

Debt / Equity

%

EBITDAMargin

%

EV / Sales

Multiple x

EV / EBITDAMultiple

x

EV / Nxt Yr

EBITDA Multiple

x

Price / Earnings

xCompany Name TickerSales$ Mil

EBITDA$ Mil

Traditional Auto Dealers

AutoNation Inc AN 59.66 -1.24% 20,862 1,001 12,704 259.38% 4.80% 0.61 12.70 11.77 15.34

Penske Automotive Group Inc

PAG 42.34 -12.12% 19,257 645 8,454 260.52% 3.35% 0.44 13.11 11.89 11.66

Sonic Automotive Inc SAH 22.76 -15.42% 9,624 286 3,470 320.06% 2.97% 0.36 12.13 10.90 13.39

Group 1 Automotive Inc GPI 75.70 -14.70% 10,633 326 4,550 302.44% 3.06% 0.43 13.97 11.22 19.41

Asbury Automotive Group Inc

ABG 67.44 -11.17% 6,588 331 3,340 529.89% 5.03% 0.51 10.09 9.92 10.52

Lithia Motors Inc LAD 106.67 23.93% 7,864 344 4,756 236.58% 4.38% 0.60 13.81 10.92 15.44

Average 62.43 -5.12% 12,471 489 6,212 318.15% 3.93% 0.49 12.64 11.10 14.29

Median 63.55 -11.65% 10,128 338 4,653 281.48% 3.86% 0.47 12.90 11.07 14.36

Used Auto Dealers

America's Car-Mart Inc/TX CRMT 26.69 -50.00% 485 (23) 331 45.28% -4.67% 0.68 nm 8.41 12.77

CarMax Inc KMX 53.97 -18.94% 14,958 1,178 21,269 364.26% 7.88% 1.42 18.05 17.16 18.11

Average 40.33 -34.47% 7,721 578 10,800 204.77% 1.60% 1.05 18.05 12.79 15.44

Median 40.33 -34.47% 7,721 578 10,800 204.77% 1.60% 1.05 18.05 12.79 15.44

Source: Bloomberg L.P.

Guideline Company Pricing

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

Mercer Capital’s Value Focus: Auto Dealer Industry Year-End 2015

© 2016 Mercer Capital 14 www.mercercapital.com

Sources

“IBISWorld Industry Report 44111: New Car Dealers in the US”

“IBISWorld Industry Report 44112: Used Car Dealers in the US”

“NADA Data” 2002-2015. http://www.nada.org/Publications/NADADATA/.

Mercer CapitalAuto Dealer Industry Services

Contact Us

Copyright © 2016 Mercer Capital Management, Inc. All rights reserved. It is illegal under Federal law to reproduce this publication or any portion of its contents without the publisher’s permission. Media

quotations with source attribution are encouraged. Reporters requesting additional information or editorial comment should contact Barbara Walters Price at 901.685.2120. Mercer Capital’s Industry

Focus does not constitute legal or financial consulting advice. It is offered as an information service to our clients and friends. Those interested in specific guidance for legal or accounting matters should

seek competent professional advice. Inquiries to discuss specific valuation matters are welcomed. To add your name to our mailing list to receive this complimentary publication, visit our web site at

www.mercercapital.com.

Mercer Capital has expertise providing business valuation and financial advisory services to companies in the auto dealer industry.

Mercer Capital provides business valuation and financial advisory services to auto dealerships

throughout the nation. We provide valuation services for tax purposes, buy-sell agreements,

partner buyouts, and other corporate planning purposes. Mercer Capital also works with owners

who are considering the sale of their dealership or the acquisition of other dealership(s).

Services Provided

• Valuation of auto dealer industry companies

• Transaction advisory for mergers, acquisitions and divestitures

• Valuations for purchase accounting and impairment testing

• Fairness and solvency opinions

• Litigation support for economic damages and valuation and shareholder disputes

Contact a Mercer Capital professional to discuss your needs in confidence.

Timothy R. Lee, [email protected]

Matthew R. Crow, CFA, [email protected]

Nicholas J. Heinz, [email protected]

Chad M. [email protected]

MERCER CAPITAL

Memphis5100 Poplar Avenue, Suite 2600Memphis, Tennessee 38137901.685.2120

Dallas12201 Merit Drive, Suite 480Dallas, Texas 75251214.468.8400

Nashville102 Woodmont Blvd., Suite 231Nashville, Tennessee 37205615.345.0350

www.mercercapital.com

BUSINESS VALUATION & FINANCIAL ADVISORY SERVICES