mercom capital group india solar market update · location mw capacity technical bid opening date...

TRANSCRIPT

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 1

Mercom Capital Group

India Solar Market Update

India Solar Quarterly Market Update – Indian Solar Market Ready for Liftoff

Aug 2015

KEY FINDINGS

� Year-to-date solar installations have reached approximately 1,400 MW

� Cumulative solar installations in India is about 4.5 GW

� Mercom is raising solar installation forecast again to 2.5 GW for 2015

� Proposed 3,000 MW of solar PV projects in Batch 2 are now being implemented by NTPC through open

competitive bidding

� Recent reverse auctions held in the states of Madhya Pradesh and Telangana resulted in record low bids

� Almost 60 percent of collected Cess funds have not been transferred to NCEF and only 43 percent of the

transferred funds have been allocated to MNRE

� In the last two years, approximately 55 percent of the NCEF fund allocation has gone to MNRE while 45

percent has been allocated to river cleaning and miscellaneous projects

� SECI is now a commercial entity and a direct competition to solar developers and manufacturers

List of Charts/Tables

India Solar Installations (MW)……………………………………………………………..……………….. 2

MNRE Year-wise Targets in MW………..…….……………………………………….………………….. 4

JNNSM Phase II Batch 2: NTPC Tenders ……………………………………………………………….. 5

JNNSM Phase II Batch 3: Phasing of Investment Estimation …………………...…………………….. 5

Solar Parks and Ultra Mega Solar Power Projects …………………………………………................... 6

State-wise and Year-wise Proposed Targets for Rooftop Solar Projects ………………..................... 8

Clean Energy Cess Fund Status……………………………………………………………….................. 9

Ministry-wise NCEF Fund Allocation in Different Years …………………………………….................. 10

Average Tariff Decline by Policy and Year (₹/kWh) …………………………………...……................. 12

Monthly Average Chinese Module Spot Prices……………………………………………..................... 12

Utility-Scale Solar Projects in India…………………………………………………………….................. 14

MPPMCL Price Bid: Winners List ……………………………………………..…………………..…..….. 15

India Solar Installations (MW) By Location …………………………………………………………..….. 16

Jharkhand State Solar Power Policy 2015 Target …………………………………………...……..….. 17

Telangana: Revised Timeline ……………………………………………………………………..…..….. 18

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 2

Mercom Capital Group

India Solar Market Update

After a long wait, the solar market in India is finally taking off. Solar installations have been stuck around the gigawatt

level for the last three years. We are now seeing solar installations year-to-date (as of print date Aug 10th) reaching

approximately 1,400 MW which is already the best year for India. Mercom is forecasting installations to reach

approximately 2,500 GW in calendar year 2015.

Since our previous update, the Government of India has officially raised the National Solar Mission’s solar installation

target from 22 GW to 100 GW by 2022. The target was approved by the Cabinet and is split between large-scale

projects (60 GW) and rooftop projects (40 GW). The total investment required for achieving this target is expected to

be about ₹6,00,000 crore (~$95 billion).

Estimating cumulative installations at 5 GW by the end of 2015, 95 GW at a compound annual growth rate of 63

percent is required to reach the 100 GW goal by 2022. While 60 GW may be achievable with the right policies in

place, 40 GW of rooftop in six years is very aggressive considering cumulative rooftop installations in India are just

under 250 MW. China, which has a similar installation goal, has faced a host of issues such as grid constraints,

payment issues and delays, rigid distributed energy deployment goals have hindered growth. Even though there will

be many hiccups along the way, Mercom believes that the Indian solar market has turned the page and will be one of

the Top 5 markets in the world over the next five years.

As government steps up its solar installation goals we are also seeing government-owned entities starting to enter the

solar business, directly competing with private businesses. Solar Energy Corporation of India (SECI) was recently

converted into a commercial entity, which means SECI can now directly engage in owning solar power projects,

generating and selling power and also manufacturing solar products and materials. National Thermal Power

Corporation (NTPC) announced that it is evaluating a plan to setup solar manufacturing. The government entering

6 12

172

986 1,004

883

2,500

0

1,000

2,000

3,000

4,000

5,000

6,000

0

500

1,000

1,500

2,000

2,500

3,000

2009 2010 2011 2012 2013 2014 2015F

Cu

mu

lati

ve

In

sta

llati

on

s (M

W)

An

nu

al I

nst

alla

tio

ns

(MW

)

Source: Mercom Capital Group, llc

India Solar Installations (MW)

Annual Solar Installations

Cumulative Solar Installations

Aug 2015

Data derived from MNRE, Mercom Project Tracker & Public Sources

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 3

Mercom Capital Group

India Solar Market Update

into business directly goes against Mr.Modi’s statement - “It's not the government's business to run a business.” Solar

developers, manufacturers and investors we spoke with view this as a negative development for the industry.

Another bottleneck we are seeing is in the release and allocation of funds from The National Clean Energy Fund

(NCEF) towards the solar industry. With almost $3 billion (~$18,900 crore) sitting in the NCEF fund unused. These

funds can be used to create a ‘reserve backstop fund’ against non-payments that will stimulate much needed lending

for projects.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 4

Mercom Capital Group

India Solar Market Update

MNRE: Year-wise Targets in MW to Achieve 100,000 MW by 2022

Category 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22 Total

Rooftop Solar 200 4,800 5,000 6,000 7,000 8,000 9,000 40,000

Ground Mounted

Solar Power Projects 1,800 7,200 10,000 10,000 10,000 9,500 8,500 57,000

Total 2,000 12,000 15,000 16,000 17,000 17,500 17,500 97,000*

* 3,743 MW commissioned up to 2014-15

Source: MNRE Mercom Capital Group, llc

Policy Developments:

Recent reverse auctions held in the states of Madhya Pradesh and Telangana resulted in record low bids. SkyPower

Southeast Asia’s bid of ₹5.05 (~$0.08)/kWh in Madhya Pradesh was the lowest bid. SkyPower was also the lowest

bid in an auction held in Telangana with ₹5.17 (~$0.082)/kWh. The rationale for low bids in India has been the drop in

system prices due to the time lag between the auction and project commissioning date which can be anywhere

between a year-and-a-half to over two years. Most banks we spoke with said they were not comfortable financing

projects at these tariff levels.

In terms of projects in the last quarter, which fall under Jawaharlal Nehru National Solar Mission (JNNSM) - Phase II

Batch 2, 3,000 MW of projects are now being auctioned by National Thermal Power Corporation (NTPC) through

competitive bidding, while SECI last week issued final guidelines for 2,000 MW in viability gap funding (VGF), also

under Phase II Batch 2 projects. Telangana auctioned off 2,000 MW of PV projects with winners to be announced

shortly, and Madhya Pradesh auctioned off 300 MW of projects.

JNNSM - Phase II Batch 1

Under this Batch, a total of 700 MW were scheduled to be completed by May 2015. We have confirmation that 580

MW have been commissioned so far. The remaining 120 MW [60 MW – Domestic Content Requirement (DCR) and

60 MW – Open Category] are expected to be commissioned by the end of August 2015.

JNNSM - Phase II Batch 2 State Specific Bundling Scheme (NTPC)

MNRE released the guidelines for Batch 2 in March 2015.

Now, the proposed 3,000 MW of solar PV projects in Batch 2 are being implemented by NTPC through open

competitive bidding. These projects will be developed in solar parks (large areas designated for solar projects), and

will be developed by central and state agencies on land provided by state governments or land identified and

arranged by developers in their respective states.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 5

Mercom Capital Group

India Solar Market Update

NTPC has been issuing tenders in tranches:

JNNSM Phase II Batch 2: NTPC Tenders

Location MW Capacity Technical Bid Opening Date Reverse Auction

Bhadla Phase II Solar Park, Jodhpur, Rajasthan 420 6 X 70 MW August 20, 2015 TBD

Gani-Sakunala Phase II Solar Park, Kurnool, Andhra Pradesh 500 3 X 50 MW and 1 X 350 MW August 12, 2015 TBD

Ghani Solar Park, Andhra Pradesh 500 10 X 50 MW July 31, 2015 TBD

Rajasthan 100 10 X 10 MW September 7, 2015 TBD

130 13 X 10 MW September 9, 2015 TBD

Uttar Pradesh 100 10 X 10 MW - TBD

Source: NTPC Mercom Capital Group, llc

JNNSM - Phase II Batch 3 (SECI)

SECI will be the implementing agency to set up 2,000 MW of grid-connected solar PV power projects under JNNSM

Phase II Batch 3, “State Specific VGF Scheme.” These projects will be set up in solar parks in various states. The

estimated funds required to provide VGF under this scheme is ₹2,100 crore (~$333 million) (₹1 crore/~$0.16

million/MW for the open category and ₹1.31 crore/~$0.2 million/MW for the DCR category). Out of 2,000 MW, 250

MW will be reserved under the DCR category and the remaining 1,750 MW will be in an open category. The VGF

scheme will be implemented through competitive bidding at a pre-defined tariff of ₹5.43 (~$0.086)/kWh for the first

year escalated by five paisa (~$0.0008)/kWh each year until it reaches ₹6.43 (~$0.1)/kWh, which would take 21

years, after which the tariff will remain at ₹6.43 (~$0.1)/kWh. The commissioning period is expected to be 13 months

from the date of signing Power Purchase Agreements (PPA).

JNNSM Phase II Batch 3

The Phasing of Investment Estimation

Year Amount

₹ in Crores US$ in Million

2016-17 1,000 158.7

2017-18 260 41.3

2018-19 210 33.3

2019-20 210 33.3

2020-21 210 33.3

2021-22 210 33.3

Total 2,100 333.3

Note: Dollar-rupee conversions were calculated at $1 = ₹63

Source: MNRE Mercom Capital Group,llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 6

Mercom Capital Group

India Solar Market Update

Other announced Solar Programs -

Ultra Mega Projects in Solar Parks

The Ministry of New and Renewable Energy’s (MNRE) plan to set up 25 Solar Parks, each with a capacity of 500 MW

and above, targeting 20,000 MW of installed capacity over a span of five years beginning in FY 2014-15, is under

way. Fifteen states have so far agreed to setup 20 solar parks with a combined capacity of 12,999 MW.

Solar Parks and Ultra Mega Solar Power Projects

No. State Capacity

(MW) Name of the Solar Power Park/Developer Area of Land Identified at

1 Gujarat 700 GPCL 1407 hectares at Vav, Distt. Banaskantha

2 Andhra Pradesh

1,500 AP Solar Power Corporation, JVC of SECI, APGENCO and

NREDCAP

4517 hectares at Anantpuramu, Kadapa

Districts

3 1,000 2,068 hectares at Kurnool District

4 Uttar Pradesh 600 JV between UPNEDA and SECI formed 1,038 hectares at Jalaun, Sonbhadra,

Allahabad & Mirzapur districts

5 Meghalaya 20 Meghalaya Power Generation Corporation (MePGCL) 27 hectares at West Jaintia Hills & East

Jaintia Hills districts

6

Rajasthan

680 Rajasthan Solar Park Development Company Ltd.

(RSDCL), a subsidiary of RRECL

1,797.45 hectares at Bhadla

Phase II

7 1,000 Surya Urja Company of Rajasthan; a JVC between State Govt.

and IL & FS Energy Development Company

2,000 hectares at Bhadla

Phase III

8 1,000 Surya Urja Company of Rajasthan; a JVC between State Govt.

and IL & FS Energy Development Company

2,000 hectares at Jaisalmer

Phase I

9

Madhya Pradesh

750

JV of SECI and MPUVN

1,400 hectares at Rewa

10 750 800 & 600 hectares at Neemuch & Agar

respectively

11 Karnataka 2,000 Karnataka Solar Power Development Corporation (KSPDCL),

JVC of SECI and KREDL

Pavagada taluk Tumkur dist.

(2,429 hectares)

12 Tamil Nadu 500 To be finalized 568 hectare at Ramanathapuram district

13

Punjab

500

PEDA

6,167 acres at Patiala, 1,786 acres at

Fatehgarh Sahib, (5285 hectares)

14 500 2,311 acres at Ludhiana and

2,790 acres at Gurdaspur

15 Telangana 1000 SECI, Telangana GENCO and Telangana New & Renewable

Energy Development Corporation (TNREDC)

2,189 hectare at Gattu, Mehboob Nagar

District

16 Kerala 200 SECI

4,858 hectares at Paivalike, Meenja,

Kinanoor, Kraindalam and Ambalathara

villages of Kasargode district

17 Uttarakhand 39 To be finalized 77.853 hectares at Almora district

18 Arunachal

Pradesh 100 Arunachal Pradesh Energy Development Agency (APEDA)

2,700 acres of waste land Digaru Paya

region in Sonpura circle of Lohit district

19 Nagaland 60 Directorate of New & Renewable Energy, Nagaland Dimapur, Kohima and New Peren

districts

20 A&N Islands 100 To be finalized South Andaman

TOTAL 12,999 20 Solar Parks in 15 States

Source: MNRE Mercom Capital Group, llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 7

Mercom Capital Group

India Solar Market Update

JNNSM - Phase II Batch 5 (CPSUs)

Batch 5 (there is no Batch 4) calls for the establishment of grid-connected solar PV power projects by the Central

Public Sector Undertakings (CPSUs) and Government of India organizations’ self-use or third-party sale or merchant

sale, with VGF over a span of three years from FY 2014-15 to 2016-17. DCR will be mandatory for Batch 5 projects.

NTPC alone has a target of developing 10,000 MW of solar projects. NTPC is already developing 250 MW of solar

projects under this scheme in Andhra Pradesh and has invited tenders for 260 MW of solar projects in Rajasthan with

bid pricing to be announced in August 2015. NTPC also invited tenders for 250 MW of solar projects in Madhya

Pradesh. The National Hydro Electric Power Corporation (NHPC) has invited tenders to develop 50 MW; the last date

for submission of techno-commercial bids was August 10, 2015. Our sources confirm that tenders have been

announced for 683 MW of solar projects by various CPSUs including NTPC, NHPC and shipyards.

Solar Projects by Defence Sector

Under this plan, more than 300 MW of grid-connected and off-grid solar PV power projects are proposed to be set up

by defense establishments under the Ministry of Defence with VGF over the next five years, 2014-2019. It will be

mandatory that all PV cells and modules used in solar projects set up under this program be made in India. According

to our sources, the Ordinance Factory Board under the Ministry of Defence has proposed tenders for 150 MW of

solar projects and the office of the Engineer-in-Chief for another 281 MW. The Defence Research and Development

Organization (DRDO) and Bharat Electronics Limited (BEL) are also expected to develop projects.

Grid Connected Solar PV Power Plants on Canal Banks and Canal Tops

MNRE launched a program for the development of 100 MW of grid-connected solar PV power projects on canal

banks and canal tops at an estimated cost of ₹975 crore (~$155 million) with Central Financial Assistance (CFA) of

₹228 crore (~$36 million). About 69 MW of projects under this program are under development in eight different

states.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 8

Mercom Capital Group

India Solar Market Update

State-wise and Year-wise Proposed Targets for 40 GW Grid Connected Rooftop Solar Projects

States 2015-16 2016-17 2017-18 2018-19 2019-20 2020-21 2021-22 Total (MW)

Andhra Pradesh 10 240 250 300 350 400 450 2,000

Bihar 5 120 125 150 175 200 225 1,000

Chhattisgarh 4 84 88 104 120 140 160 700

Delhi 5 132 138 165 190 220 250 1,100

Gujarat 15 385 400 480 560 640 720 3,200

Haryana 5 200 200 235 280 320 360 1,600

Himachal Pradesh 2 38 40 48 56 64 72 320

Jammu & Kashmir 2 54 55 74 80 90 95 450

Jharkhand 4 96 100 120 140 160 180 800

Karnataka 10 275 290 344 403 460 518 2,300

Kerala 4 96 100 120 140 160 180 800

Madhya Pradesh 10 265 275 330 385 440 495 2,200

Maharashtra 20 565 588 704 823 940 1,060 4,700

Orissa 5 120 125 150 175 200 225 1,000

Punjab 10 240 250 300 350 400 450 2,000

Rajasthan 10 275 288 344 403 460 520 2,300

Tamil Nadu 15 420 438 524 613 700 790 3,500

Telangana 10 240 250 300 350 400 450 2,000

Uttarakhand 2 42 44 52 60 70 80 350

Uttar Pradesh 20 510 538 650 752 860 970 4,300

West Bengal 10 252 263 315 370 420 470 2,100

Arunachal Pradesh 2 5 5 8 10 10 10 50

Assam 4 30 30 38 42 50 56 250

Manipur 4 3 6 8 9 10 10 50

Meghalaya 1 6 6 8 9 10 10 50

Mizoram 1 6 6 8 9 10 10 50

Nagaland 1 6 6 8 9 10 10 50

Sikkim 1 6 6 8 9 10 10 50

Tripura 1 6 6 8 9 10 10 50

Chandigarh 1 12 12 14 18 20 23 100

Goa 1 20 20 22 23 30 34 150

Dadra & Nagar Haveli 1 24 25 30 35 40 45 200

Daman & Diu 1 12 12 14 18 20 23 100

Puducherry 1 12 12 14 18 20 23 100

Andaman & Nicobar 1 2 2 2 5 4 4 20

Lakshadweep 1 1 1 1 2 2 2 10

Total (MW) 200 4,800 5,000 6,000 7,000 8,000 9,000 40,000

Source: MNRE Mercom Capital Group, llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 9

Mercom Capital Group

India Solar Market Update

Other Updates:

National Clean Energy Fund (NCEF): Most of the funds are not allocated to clean energy projects

The National Clean Energy Fund was created in 2010, after JNNSM, to fund up to 40 percent of the cost for research

and innovative projects in clean energy technologies by public or private sector entities. The funding is in the form of

a loan or as viability gap funding, as seen fit by the Inter-Ministerial Group (IMG). Clean Energy Cess (a form of

carbon tax) is being levied on coal produced in India, as well as on imported coal. The Cess, which was ₹50 (~$0.8)

per ton when it was introduced in 2010, was raised to ₹100 (~$1.6) per ton in 2014 and to ₹200 (~$3.2) in the 2015-

16 budget. The Cess collected is then required to be transferred to NCEF and to appropriate government agencies.

Starting with the 2014-15 budget, the new administration has expanded the scope of NCEF to fund its clean river

‘Namami Gange’ project. While this type of budget maneuvering is common when governments have to find funds to

finance their pet projects, in this case it is taking away from very important clean energy allocation. In the last two

years, approximately 55 percent of the NCEF fund allocation has gone to MNRE while 45 percent has been allocated

to river cleaning and miscellaneous projects.

Clean Energy Cess Fund Status

Year Clean Energy Cess

Collected

Amount

Transferred to NCEF

% of Cess

Collected

NCEF Fund

Allocation to MNRE

% Diff - Funds

Collected vs. Spent

₹ in Crore US$ in

Million ₹ in Crore

US$ in

Million % ₹ in Crore

US$ in

Million %

2010-11 1,066.46 169.28 0.00 0.00 - 0.00 0.00 -

2011-12 2,579.55 409.45 1,066.46 169.28 41% 160.80 25.52 6%

2012-13 3,053.19 484.63 1,500.00 238.10 49% 125.78 19.97 4%

2013-14 3,471.98 551.11 1,650.00 261.90 48% 1,218.78 193.46 35%

2014-15 8,916.46 1415.31 4,700.00 746.03 53% 1978.00 (RE) 313.97 22%

2015-16 (BE) 13,118.04 2082.23 4,700.00 746.03 36% 2,500.00 396.83 19%

Total 32,205.68 5112.01 13,616.46 2161.34 42% 5,983.36 949.74 19%

Note: Dollar-Rupee conversions were calculated at $1 = ₹63

Source: PIB, MNRE, Ministry of Finance Mercom Capital Group, llc

Looking at the latest available data, it is clear that the majority of the funds collected through the Cess is not reaching

MNRE and consequently clean energy projects. Almost 60 percent of collected Cess funds have not been transferred

to NCEF and only 43 percent of the transferred funds have been allocated to MNRE. Total funds allocated to MNRE

to date is just 19 percent of funds collected. One of the challenges to achieve the government’s new 100 GW solar

installation goal is funding, and if the government is serious about reaching that goal, it has to work to remove

bureaucratic hurdles and bottlenecks to provide confidence to the markets. Offtaker credibility and payments to

developers on time is one of the most common and primary risks quoted by banks. With almost $3 billion (~$18,900

crore)) sitting in the NCEF funds, the government can use these funds to create a ‘reserve backstop fund’ against

non-payments that will stimulate much needed capital for projects. Collecting taxes towards clean energy projects

and not using it is detrimental to the industry.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 10

Mercom Capital Group

India Solar Market Update

Ministry-wise NCEF Fund Allocation in Different Years

Ministry/

Year MNRE

Ministry of Water

Resources, River

Development &

Ganga Rejuvenation

Ministry of Drinking

Water & Sanitation

Ministry of Environment

& Forests Total

₹ in Crore US$ in

Million ₹ in Crore

US$ in

Million ₹ in Crore

US$ in

Million ₹ in Crore

US$ in

Million ₹ in Crore

US$ in

Million

2010-11 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

2011-12 160.80 25.52 0.00 0.00 0.00 0.00 59.95 9.52 220.75 35.04

2012-13 125.78 19.97 0.00 0.00 110.65 17.56 10.00 1.59 246.43 39.12

2013-14 1,218.78 193.46 0.00 0.00 0.00 0.00 0.00 0.00 1,218.78 193.46

2014-15 (RE) 1,978.00 313.97 1,500.00 238.10 110.65 17.56 0.00 0.00 3,588.65 569.63

2015-16 (BE) 2,500.00 396.83 2,100.00 333.33 0.00 0.00 110.00 17.46 4,710.00 747.62

Total 5,983.36 949.74 3,600.00 571.43 221.30 35.13 179.95 28.56 9,984.61 1584.86

Note: Dollar-Rupee conversions were calculated at $1 = ₹63

Source: PIB, MNRE, Ministry of Finance Mercom Capital Group, llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 11

Mercom Capital Group

India Solar Market Update

Decline in Solar Tariffs:

There has been a lot of noise recently about the record low tariff bids in the Madhya Pradesh reverse auction

followed by the auction in Telangana. Looking at the tariff chart below (we have excluded VGF projects for

consistency), starting with 2010 JNNSM migration projects which started at ₹17.91 (~$0.28)/kWh all the way to 2015

projects, we see a significant drop in bids over the last five years. The JNNSM Migration Batch was not an auction,

therefore if we calculate the drop in average bids from the first auction (JNNSM Phase I, Batch 1) which had an

average tariff of ₹12.16 (~$0.19)/kWh, to the latest auction results (Telangana Phase II Group 2), we see a 53

percent drop in the average tariff through reverse auctions across various state and central policies. From 2012 to

2015 we see a lot of peaks and valleys with bid prices going up and down in an inconsistent manner due to difference

in insolation levels in various states. The drop in tariffs from the 2012 Odisha Batch 2 auction to the 2015 Telangana

Phase II Group 2 auction is 35 percent.

Though costs of PV project include more than just panels, we have inserted an average Chinese module spot price

chart as a reference point since panels makeup a significant portion of a solar project.

We should also note that most projects in India have anywhere between 12-18 months or more to commission which

gives developers 6-12 months to procure panels at a lower price (assuming prices are always dropping which has its

own risks). Looking at the spot price chart, there is a steep fall in module prices between 2011 and the end of 2012

(46 percent), but module price decline between January 2013 to July 2015 is only about 10 percent.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 12

Mercom Capital Group

India Solar Market Update

17

.91

12

.16

8.7

7

12

.54

15

.61

8.3

6 10

.37

8.3

7

8.0

1

8.7

3

6.4

9

6.8

2

7.0

7

6.7

6 8.2

2

8.4

1

7.1

4

6.4

8

8.6

7

6.1

7

8.4

5

7.3

4

6.9

5

7.0

1

6.7

3 7.7

4 9.1

8

8.4

0

5.4

1

7.5

2

7.1

7

7.1

7

7.6

3

5.7

3

5.6

9

8.0

4

0

500

1,000

1,500

2,000

2,500

0

2

4

6

8

10

12

14

16

18

20

JNN

SM

- M

igra

tio

n

JNN

SM

- P

I B

1

JNN

SM

- P

I B

2

Gu

jara

t

Ma

ha

rash

tra

Od

ish

a B

1

Gu

jara

t

Ka

rna

taka

- P

I

MP

PI

Od

ish

a B

2

AP

PI

Ch

ha

ttis

ga

rh

Ka

rna

taka

- P

II

MP

PII

Pu

nja

b P

I (C

1)

Pu

nja

b P

I (C

2)

Ra

jast

ha

n

Ta

mil

Na

du

UP

B1

AP

PII

Bih

ar

Ka

rna

taka

- P

III

Ka

rna

taka

- P

IV

Ta

mil

Na

du

Te

lan

ga

na

PI

Utt

ark

ha

nd

UP

B2

Ka

rna

taka

(Fa

rme

rs)

MP

PII

I

Pu

nja

b P

II (

C1

)

Pu

nja

b P

II (

C2

)

Pu

nja

b P

II (

C3

)

Pu

nja

b P

II (

Ro

oft

op

)

Te

lan

ga

na

PII

G1

Te

lan

ga

na

PII

G2

UP

B3

2010-

11

2011-12 2012-13 2013-14 2014-15 2015-16

Ph

ase

/Ba

tch

Siz

e (

MW

)

Ave

rag

e T

ari

ff (

₹/k

Wh

)

Average Tariff Decline by Policy and Year (₹/kWh)

PV Projects Capacity (MW) Average Tariff (₹/kWh)

Source: Mercom Capital Group, llc

Notes:

1. Gujarat - FY 2011-12 - levelized tariff is Rs.12.54/kWh for 25 yrs (Rs.15.00 for 12 yrs & Rs 5.00 for next 13 yrs)

2. Gujarat - FY 2012-13 - levelized tariff is Rs.10.37/kWh for 25 yrs (Rs.11.25 for 12 yrs & Rs 7.50 for next 13 yrs)

3. AP Phase II - The range of first-year tariff offered by the successful bidders was Rs.5.25-5.99/kWh with a 3% per annum escalation for the first 10 years, then

flat thereafter. The levelised tariff works out to Rs. 6.17/kWh.

Aug 2015

1.2

1

0.9

1

0.6

4 0.6

8

0.5

9

0.5

4

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

1.30

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

Jan

Fe

b

Ma

r

Ap

r

Ma

y

Jun

Jul

2011 2012 2013 2014 2015

Monthly Avg Chinese Module Spot Prices

Module Prices ($/W)

*Data derived from PVinsights, Energy Trend, Digitimes and other public and private sources Mercom Capital Group, llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 13

Mercom Capital Group

India Solar Market Update

Industry Feedback

These are takeaways from our recent conversation with major developers, manufacturers and investors

Developers

• Among states, Punjab, Karnataka, Andhra Pradesh, Telangana, Madhya Pradesh and Maharashtra look

attractive.

• Longer timelines to commission, difference in solar insolation levels, and land costs all play a factor in

project development costs and associated bids; however, recent low bids in MP has bureaucrats wrongly

questioning why other state tariffs are higher which is not a good thing for the sector.

• Module pricing has stabilized.

• Borrowing rates are in the range of 12-12.5 percent.

• The best offtakers in terms of timely payments – NVVN, Gujarat, Punjab, MP and Rajasthan.

• Payments delays of 60-90 days are being experienced in UP.

• There are too many government agencies. There is no reason for government to get into the business; SECI

is trying to be a power generator and NTPC is trying to get into manufacturing.

Domestic Manufacturers

• Demand is slowly picking up but there is a lot of price pressure.

• The lowest average selling prices are currently $0.50-0.55 (~₹32-35)/W. For DCR projects it is $0.63-0.71

(~₹40-45)/W.

• Domestic manufacturers are finding it difficult to compete with Chinese manufacturers. A lot of

manufacturers are dependent on DCR projects.

• Most manufacturers are planning to expand capacity in anticipation of increased demand.

Investors

• The new low bids are too aggressive for a lot of banks.

• Most Indian banks are unwilling to lend below ₹6/kWh (~$0.095) tariff.

• Lending rates are in the range of 11-13 percent.

• Most financed projects are performing well in terms of capacity factor.

• NVVN, Gujarat, Rajasthan and MP are paying on time.

• Banks are seeing payments delays of 30 days and above in Tamil Nadu.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 14

Mercom Capital Group

India Solar Market Update

• Banks are perplexed as to why government owned entities are trying to compete with businesses and see a

conflict of interest.

State Policy Updates:

Uttar Pradesh

Uttar Pradesh signed PPAs for 110 MW of solar PV projects in Dec 2013. About 40 MW have been commissioned to

date and another 50 MW is expected to be commissioned by the end of 2015, while the remaining 20 MW is

expected to be complete in the first half of 2016.

A Request for Proposal (RfP) to set up 300 MW of solar PV projects through a reverse auction was announced in

August 2014. PPAs were signed for 105 MW of projects and we are expecting the official list of successful bidders to

be announced soon.

Another RfP to set up 215 MW of solar PV projects was announced in June this year. The letter of intent (LoI) is

expected to be announced by the end of August 2015.

Utility-Scale Solar Projects in India

Operational and Under Development

Aug 2015

Capacity (MW)

In-Operation

Solar PV 4,349

Solar Thermal 209

Total 4,558

Under Development

Solar PV 7,505

Solar Thermal 280

Total 7,785

Source: Mercom Capital Group, llc

Andhra Pradesh

Andhra Pradesh had allowed any company to establish a solar project in the state at a fixed tariff of ₹6.49

(~$0.1)/kWh at the end of 2013. There are 140 MW of projects being developed under this scheme. Of these, about

45 MW have been commissioned and the rest are expected to be commissioned by the end of this year.

Andhra Pradesh DISCOMs have signed PPAs for developing 619 MW of solar projects with first year tariffs of ₹5.25

(~$0.08)/kWh with a three percent annual escalation for 10 years. These projects are expected to be commissioned

by April 2016.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 15

Mercom Capital Group

India Solar Market Update

Punjab

Phase I - Punjab signed PPAs for 251 MW of solar PV projects in December 2013 with average tariffs

ranging between ₹8.20-8.40 (~$0.130-0.133)/kWh. Of these, about 195 MW are commissioned to date and

the remaining projects are expected to be commissioned by the end of 2015.

Phase II - LoIs for 282 MW of solar projects were signed this year in three categories; 1-4 MW sizes (29

MW), 5-24 MW sizes (100 MW) and 25-50 MW sizes (100 MW). Another 53 MW of rooftop projects are

estimated to be under this Phase and are expected to be commissioned by the end of 2016.

Kerala

The Agency for Non-Conventional Energy and Rural Technology (ANERT), the renewable energy agency of Kerala,

has announced a tender for 12 MW of grid-connected rooftop solar projects this year, of which 2 MW will be on

government buildings.

Madhya Pradesh

To date, there are 235 MW of solar projects installed under Madhya Pradesh’s state policy (175 MW – RPO and 60

MW – Phase II). There are another 25 MW under RPO and 60 MW under Phase II, which are expected to be

commissioned by the end of 2015.

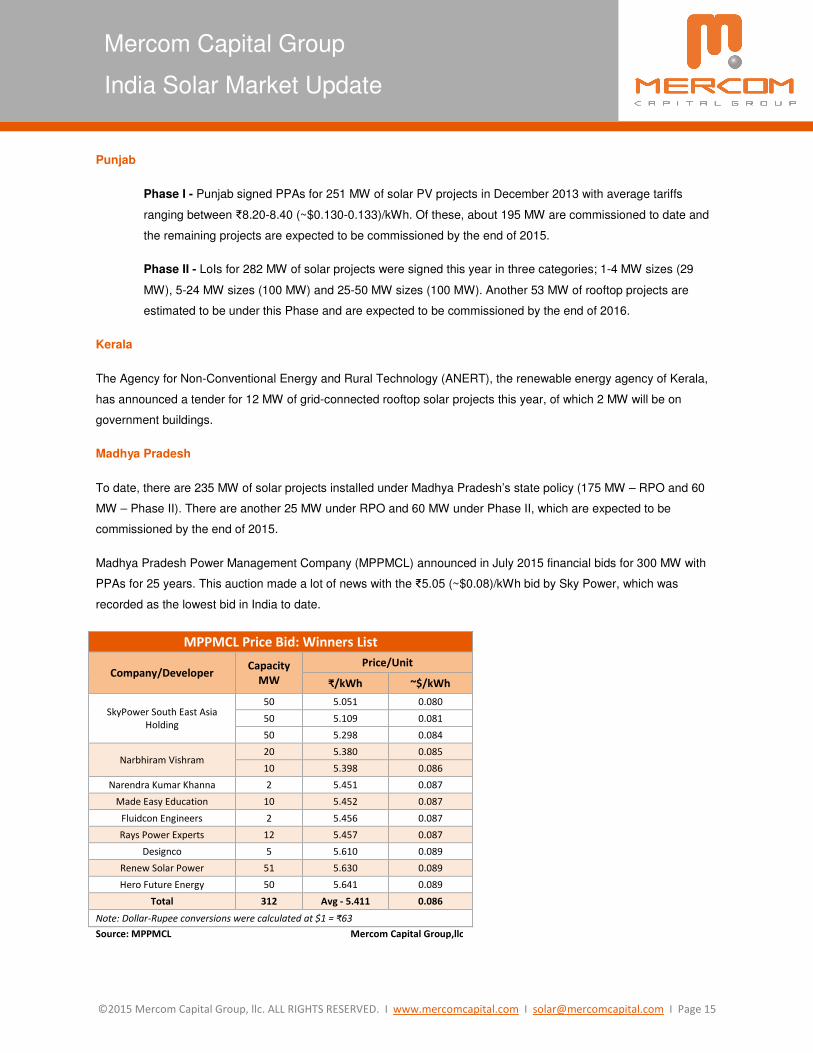

Madhya Pradesh Power Management Company (MPPMCL) announced in July 2015 financial bids for 300 MW with

PPAs for 25 years. This auction made a lot of news with the ₹5.05 (~$0.08)/kWh bid by Sky Power, which was

recorded as the lowest bid in India to date.

MPPMCL Price Bid: Winners List

Company/Developer Capacity

MW

Price/Unit

₹/kWh ~$/kWh

SkyPower South East Asia

Holding

50 5.051 0.080

50 5.109 0.081

50 5.298 0.084

Narbhiram Vishram 20 5.380 0.085

10 5.398 0.086

Narendra Kumar Khanna 2 5.451 0.087

Made Easy Education 10 5.452 0.087

Fluidcon Engineers 2 5.456 0.087

Rays Power Experts 12 5.457 0.087

Designco 5 5.610 0.089

Renew Solar Power 51 5.630 0.089

Hero Future Energy 50 5.641 0.089

Total 312 Avg - 5.411 0.086

Note: Dollar-Rupee conversions were calculated at $1 = ₹63

Source: MPPMCL Mercom Capital Group,llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 16

Mercom Capital Group

India Solar Market Update

Haryana

A tender inviting bids for 50 MW of solar PV projects was issued by the utility Uttar Haryana Bijli Vitran Nigam

(UHBVN) in May of 2014 but only 25 MW are expected to be developed.

Haryana Power Purchase Centre, on behalf of UHBVN and Dakshin Haryana Bijli Vitran Nigam (DHBVN), invited

tenders for 150 MW of solar projects in June 2015, and the list of selected bidders is expected to be announced by

the end of August 2015.

Maharashtra

The State recently announced a renewable energy policy to develop 7,500 MW of solar power by 2020.

Chhattisgarh

Chhattisgarh State Power Distribution Company Limited (CSPDCL) announced bid results for 100 MW of solar

projects. Mercom has confirmation that only 76 MW of the 100 MW of projects will be developed. A 10 MW project

has already been commissioned and the remaining projects are expected to be commissioned by the end of 2015.

0 100 200 300 400 500 600 700 800 900 1,000 1,100 1,200 1,300

Kerala

Arunachal Pradesh

Tripura

Chandigarh

Uttarakhand

Goa & UT

West Bengal

New Delhi

Jharkhand

Chhattisgarh

Haryana

Odisha

Telangana

Uttar Pradesh

Karnataka

Tamil Nadu

Punjab

Andhra Pradesh

Maharashtra

Madhya Pradesh

Gujarat

Rajasthan

India Solar Installations (MW) By Location (Aug 2015)

Source: Mercom Capital Group, llc

Total Solar Installations

4,558 MW

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 17

Mercom Capital Group

India Solar Market Update

Karnataka

The State has 93 MW of solar projects installed to date, including 40 MW commissioned under Batch 1 (Batch 1

called for 60 MW). A 10 MW CSP project under Batch I is expected to be commissioned by the end of 2016.

Of the 130 MW of solar projects announced in February 2014 under Batch 2, 33 MW have already been

commissioned and 10 MW have been cancelled. The remaining projects are expected to be commissioned by the

end of 2015.

The State also announced solar projects totaling 50 MW under Batch 3 in September 2014, of which 10 MW are

commissioned and the remainder are expected to be complete in 2016.

Karnataka Renewable Energy Development Limited (KREDL) also signed PPAs in February 2015 for 500 MW under

Batch 4, which are expected to be commissioned by the end of 2016.

The MNRE allotted 600 MW of solar energy projects to Karnataka for farmers and unemployed youth. Under this

scheme, farmers and unemployed youth would get a central subsidy of ₹50,00,000 (~$79,365)/MW. The State

recently allotted solar energy projects of 258 MW to farmers under this scheme. PPAs for the 258 MW were signed in

June-July 2015 for a tariff of ₹8.40 (~$0.13)/kWh. Another 300 MW are expected to be announced soon for allotment

to unemployed youth.

Jharkhand

Jharkhand Renewable Energy Development Agency has announced the final ‘Jharkhand State Solar Power Policy

2015’ on August 12, 2015. The objective of the policy is to encourage participation of private sector to set up solar

power based projects in the state and increase solar power generation to 2,650 MW by the year 2020 in a phased

manner. The state shall strive to achieve the objective of the policy and aim to implement the following target within a

5 year period.

Jharkhand State Solar Power Policy 2015 Target

Description Unit FY 2015-16 FY 2016-17 FY 2017-18 FY 2018-19 FY 2019-20 Total

Solar PV Projects* MW 100 250 500 500 750 2,100

Rooftop Solar Projects** MW 25 50 100 125 200 500

Solar Thermal Projects MW 5 10 10 10 15 50

Total MW 130 310 610 635 965 2,650

*The minimum size of the solar PV power project at a single location shall be 1 MW

**The minimum size of the rooftop solar PV power project at a single location shall be 1kW

Source: JREDA Mercom Capital Group, llc

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 18

Mercom Capital Group

India Solar Market Update

Telangana

Telangana signed PPAs for 515 MW in February 2015 through reverse bidding. Of this, a 20 MW project has been

commissioned and the remaining projects are expected to be commissioned in the first half of 2016.

The Southern Power Distribution Company of Telangana (TSSPDCL) invited bids for 2,000 MW of solar projects on a

'Build, Own, Operate' basis in April 2015. The financial bids were opened on August 3, 2015. The bids are divided

into two groups: Group 1 (for projects injecting solar at 33/11 kv substation level) with a commissioning deadline of 12

months from PPA signing with a ceiling tariff of ₹6.45 (~$0.1)/kWh, and Group 2 (for projects injecting solar at 133/33

kv substation level) with a commissioning deadline of 15 months from PPA signing with a tariff upper limit of ₹6.32

(~$0.1)/kWh. A LoI is expected to be issued by August 13, 2015 and PPAs are expected to be signed by September

13, 2015.

Telangana: Revised Timeline

Event Schedule

Date of issue of RFS and PPA 01 April 2015

Bid Document Download Start Date 01 April 2015

Pre-bid Meeting 10 April 2015

Revision of RFS and PPA if any 09 June 2015

Bid Document download end date 10 July 2015, 15:00 Hours

Bid Deadline 10 July 2015, 17:00 Hours

Submission of hard copies of EMD and Bid Processing Fee 11 July 2015, 17:00 Hours

Opening of Prequalification Bid 14 July 2015

Opening of Technical Bids 20 July 2015

Opening of Financial Bids 03 Aug 2015

Issue of LoI to Successful Bidders 13 Aug 2015

Signing of PPA On or before 13 Sep 2015

Financial Closure (180 days from signing of PPA) 14 Mar 2016

Commissioning Schedule:

12 months from signing of PPA for Group 1 Bidders 14 Sep 2016

15 months from signing of PPA for Group 2 Bidders 14 Dec 2016

Source: TSSPDCL

Bihar

Bihar State Electricity Board (BSEB) signed PPAs in February 2015 to establish 100 MW of solar projects. The

projects have a deadline for commissioning by the second half of 2016. There is a 40 MW project that is expected to

be commissioned by the end of 2015.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 19

Mercom Capital Group

India Solar Market Update

Tamil Nadu

According to our sources, Tamil Nadu Generation and Distribution Corporation (Tangedco), the state utility, has

signed PPAs for over 2,000 MW of solar power at a tariff of ₹7.01 (~$0.11)/kWh and these projects are expected to

be commissioned by March 2016. We expect 150 MW to be commissioned by the end of 2015 and the remaining by

March 2016.

Note: Dollar-Rupee conversions were calculated at $1 = ₹63

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 20

Mercom Capital Group

India Solar Market Update

About Mercom Capital Group

Mercom Capital Group, llc, is a global communications and consulting firm focused on Cleantech, Healthcare IT and

financial communications. Mercom’s consulting division advises companies on new market entry, overall strategic

decision-making, and provides custom market research. Mercom delivers highly respected industry market

intelligence reports covering Solar Energy, Wind Energy, Smart Grid and Healthcare IT. Our reports provide timely

industry happenings and ahead-of-the-curve analysis specifically for C-level decision making. Mercom’s

communications division helps companies and financial institutions build powerful relationships with media, analysts,

local communities and strategic partners. To receive Mercom’s popular market intelligence reports,

visit: http://www.mercomcapital.com.

©2015 Mercom Capital Group, llc. ALL RIGHTS RESERVED. I www.mercomcapital.com I [email protected] I Page 21

Mercom Capital Group

India Solar Market Update

Mercom Capital Group, llc

4611 Bee Caves Road, Suite 303

Austin, Texas 78746

t | +1.512.215.4452

w | www.mercomcapital.com

Mercom Communications India, Pvt. Ltd.

A subsidiary of Mercom Capital Group, llc

S-3, Harshita Arcade

No.138, First Main Road

Sheshadripuram

Bangalore-560020

t | +91.80.2356.0436

DISCLAIMER © 2015 by Mercom Capital Group, llc. All rights reserved. Strictly no redistribution allowed without prior written

permission of Mercom Capital Group. When quoting, please cite “Mercom Capital Group, llc”. Although information in

this report has been obtained from sources that we believe to be reliable, Mercom Capital Group does not guarantee

its accuracy. Published by Mercom Capital Group, llc, 4611 Bee Cave Rd, Suite 303, Austin, TX 78746 USA.

A copy of the full Terms and Conditions that you agreed to can be found at:

http://mercomcapital.com/termsandconditions.php. For information about this document, please contact us at: