mergers & acquisitions … state tax aspects€¦ · variety of multistate, state and local tax...

TRANSCRIPT

Ohi

o T

ax

Workshop Q

Mergers & Acquisitions …

State Tax Aspects

Thursday, January 27, 2011 4:15 p.m. to 5:15 p.m.

Biographical Information

Jeremy A. Hayden, Member, Frost Brown Todd LLC 2200 PNC Center, 201 East Fifth Street, Cincinnati, Ohio 45202

[email protected] 513.651.6912

Jeremy A. Hayden is a member of the law firm of Frost Brown Todd and he chairs the firm’s Entrepreneurial Services Team. A significant portion of Mr. Hayden’s practice is serving as outside general counsel for privately-held businesses. Mr. Hayden regularly leads client engagements on corporate mergers, acquisitions and divestitures. Mr. Hayden also has significant experience representing both private and governmental clients on state and local tax matters including tax controversies before state and local taxing authorities. Mr. Hayden assisted the Ohio Department of Taxation with drafting of guidance for the “agency exemption” as it relates to general contractors under the Ohio Commercial Activity Tax. Mr. Hayden received his Juris Doctorate from the University of Kentucky College of Law and his Masters in Taxation from the University of Cincinnati, magna cum laude. Mr. Hayden received the Young Professional Alumni Award from the University of Kentucky College of Law, and he has been recognized as a member of the 40 Under Forty by the Cincinnati Business Courier and an Ohio Super Lawyers® Rising Star by Thomson Reuters.

Javan A. Kline, Attorney, Frost Brown Todd LLC 2200 PNC Center, 201 East Fifth Street, Cincinnati, Ohio 45202

[email protected] 513.651.6424

Javan A. Kline is a senior associate in the Cincinnati office of Frost Brown Todd focusing his practice on all aspects of state and local taxation planning, compliance and litigation. Mr. Kline advises clients on a variety of multistate, state and local tax matters involving personal income taxes, business income and franchise taxes, sales and use taxes, personal and real property taxes, the Ohio commercial activity tax, excise taxes, and incentive projects. Mr. Kline represents clients in tax controversies before the Ohio Department of Taxation, the Internal Revenue Service and other state and local taxing authorities. Mr. Kline received his B.B.A. from the University of Notre Dame and his J.D. from the University of Cincinnati College of Law.

Teresa L. Worthington. Senior Managing Consultant, BKD LLP 201 N. Illinois Street, Suite 700, Indianapolis, IN 46244

[email protected] 317.383.4000

Terri has worked for more than 15 years in the tax industry. As a member of the State and Local Tax (SALT) Services division, she has experience in multistate taxation, including sales and use taxes and property taxes. She is responsible for performing reviews, researching, training, audit management and developing tax planning strategies. She also renders written opinions, negotiates settlement agreements and provides litigation support.

Cary D. Hines, Partner, BKD LLP 312 Walnut Street, Suite 3000, Cincinnati, Ohio 45202

[email protected] 513.562.5566

Cary has more than fifteen years of public accounting experience in providing tax planning and compliance services to clients mainly in the manufacturing, distribution, and service industries. He has served a number of SEC registered clients, as well as numerous closely held clients, and has a strong background in C corporations, FAS 109, and pass-through entities. Cary has also served numerous clients with international operations. Cary has served as the BKD-Cincinnati office Tax Director since 2005 and is responsible for overseeing all aspects of the office tax practice to ensure quality and compliance with office, firm, industry, and taxing authority standards. Prior to entering public accounting, Cary spent several years in the banking and high-tech industries. Cary is a member of the American Institute of Certified Public Accountants and Ohio Society of Certified Public Accountants. He has been an active member of the community previously serving as the Treasurer for the Kidney Foundation of Greater Cincinnati, the Treasurer for Miami County Children’s International Summer Villages, and periodically serving as a youth soccer coach. Cary is currently a board member of the Cincinnati Center for Respite Care, as well as the Chair of the Cincinnati BKD Foundation Cary received both his Bachelor of Science in Business Economics (1988) and his Master of Accountancy (1995) degrees from Miami University in Oxford, Ohio.

Mergers and Acquisitions… State Tax Aspects

Jeremy A. Hayden, Esq. Frost Brown Todd LLCCary D. Hines, CPA BKD, LLPJavan A. Kline, Esq. Frost Brown Todd LLCTeresa L. Worthington, CPA BKD, LLP

Ohio Tax Conference – January 27, 2010

P t ti O iPresentation Overview

I D DiliI. Due DiligenceII. Stock TransactionsIII. Asset TransactionsIV. Mergers and ReorganizationsV. Successor Liability

2

I Due DiligenceI. Due DiligenceA. Overview

1 Broad Encompasses all state and local taxes1. Broad – Encompasses all state and local taxes

2. Fully Understand Businesses Involveda. Goods or servicesb Wholesaler or retailerb. Wholesaler or retailerc. Exempt or Government

3. Acquisition Structurea Stock or Asseta. Stock or Assetb. Taxable or Non-Taxable

3

I Due DiligenceI. Due DiligenceB. Tax Returns and Specific Taxes

1. Overview

a. States target is currently filing for all tax matters and reasons forfiling in those jurisdictions

b H h tit b t t d d th i t l tib. How has entity been structured and are they appropriately reportingbased on their operations

c. Open tax years for target including extensions and waivers of SOL

4

I Due DiligenceI. Due Diligence2. Income and Franchise Tax Matters

a. Allocation and apportionment figures; whether Target has NOLs,a. Allocation and apportionment figures; whether Target has NOLs,depreciation adjustments, or state specific adjustments

i. Specifically determine sourcing of services (cost of performance,customer’s address) of target

ii. Determine states in which company has payroll expenses and real orl tpersonal property

b. States in which entity files a separate return, a combined return or aconsolidated return

3. Gross Receipts Taxes and Alternative Tax Structures

a. Consider states such as Washington, Ohio, Michigan and Texasb Subject to special industry taxes (e g financial institution)b. Subject to special industry taxes (e.g., financial institution)

5

I Due DiligenceI. Due Diligence4. Sales and Use Tax Matters

a Review maintenance of exemption certificatesa. Review maintenance of exemption certificatesb. Use tax Assessmentc. Whether Exemption will Apply to Transaction:

i. Statutory Merger or Consolidationii Transfer to New Corporationii. Transfer to New Corporationiii. Isolated or Occasional Sale Exemptioniv. Sales for Resale

5 Property Tax Matters5. Property Tax Mattersa. Look at filings, exemptions and whether property has been

understated or overstated in its assessment

6. Payroll, Unemployment and Workers Compensationy , p y pa. Review withholding tax filings, contact Ohio Department of Taxation

or perform lien searchesb. Review unemployment tax filings, contact ODJFS or perform lien

searchesAlth h k ti i t t tt ft dc. Although workers compensation is not a tax matter, often may needto be reviewed by SALT practitioners.

6

I Due DiligenceI. Due DiligenceD. Nexus

1. Analyze activities in states:a. Physical presenceb. Employees or representatives working on behalf of target to

solicit salesc. Employees or representatives working on behalf of target for

activities beyond soliciting salesd. Clients locatede. Any other affiliates, agents, etc. that may establish nexus for

target (e g Amazon law)target (e.g., Amazon law)f. States in which target is registered to do businessg. States in which target is registered for sales tax purposes

7

I Due DiligenceI. Due Diligence

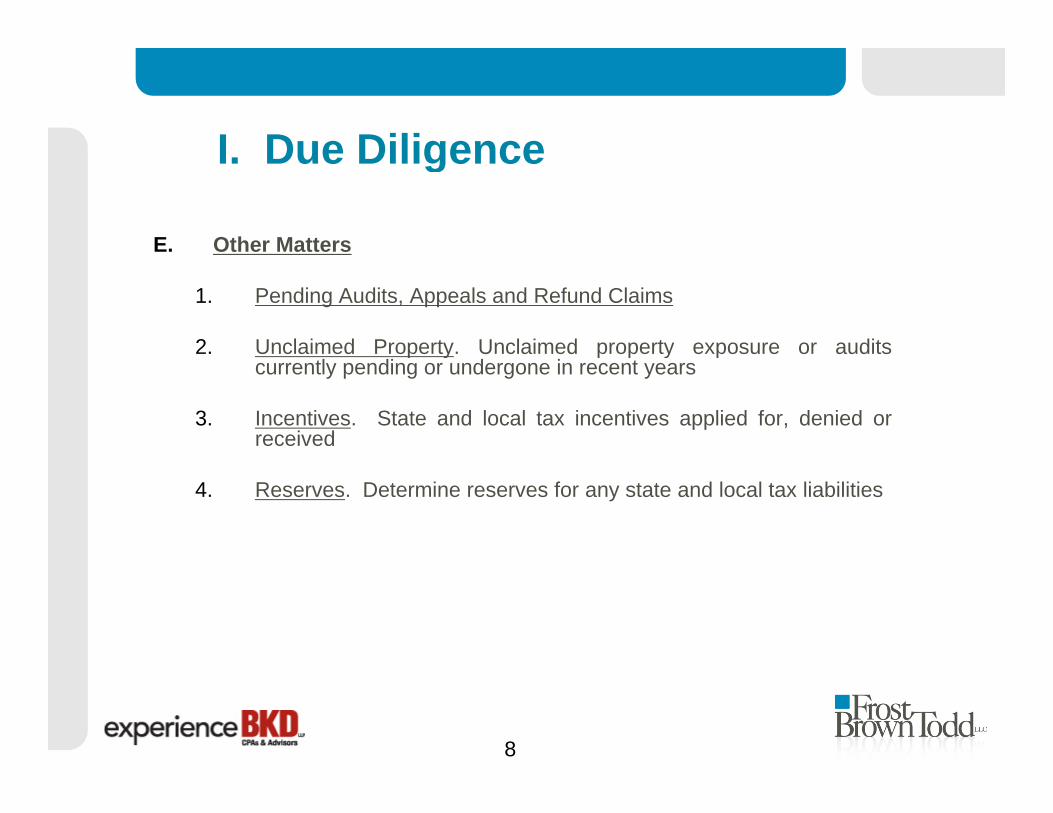

E. Other Matters

1. Pending Audits, Appeals and Refund Claims

2. Unclaimed Property. Unclaimed property exposure or auditsp y p p y pcurrently pending or undergone in recent years

3. Incentives. State and local tax incentives applied for, denied orreceived

4. Reserves. Determine reserves for any state and local tax liabilities

8

II Stock TransactionsII. Stock Transactions

A. Buyer’s PerspectiveA. Buyer s Perspective

1. Representations and Warranties

2 Combined and Consolidated Reporting2. Combined and Consolidated Reportinga. Structural considerations

3. NOLsa. Limitations and treatment methodologies

4. Deductibility of Interesta Debt structurea. Debt structureb. Intercompany charges

5. 338 and 338(h)(10) Elections

9

II Stock TransactionsII. Stock Transactions

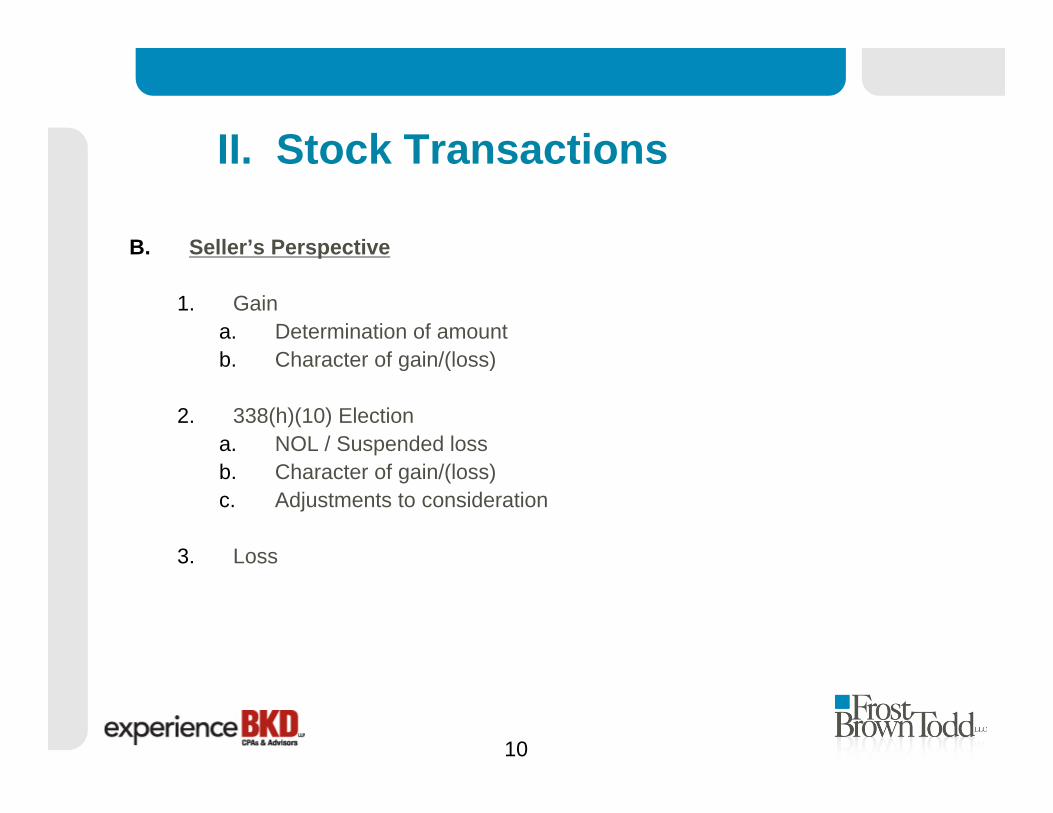

B. Seller’s PerspectiveB. Seller s Perspective

1. Gaina. Determination of amountb Character of gain/(loss)b. Character of gain/(loss)

2. 338(h)(10) Electiona. NOL / Suspended lossb. Character of gain/(loss)c. Adjustments to consideration

3 Loss3. Loss

10

III Asset TransactionsIII. Asset Transactions

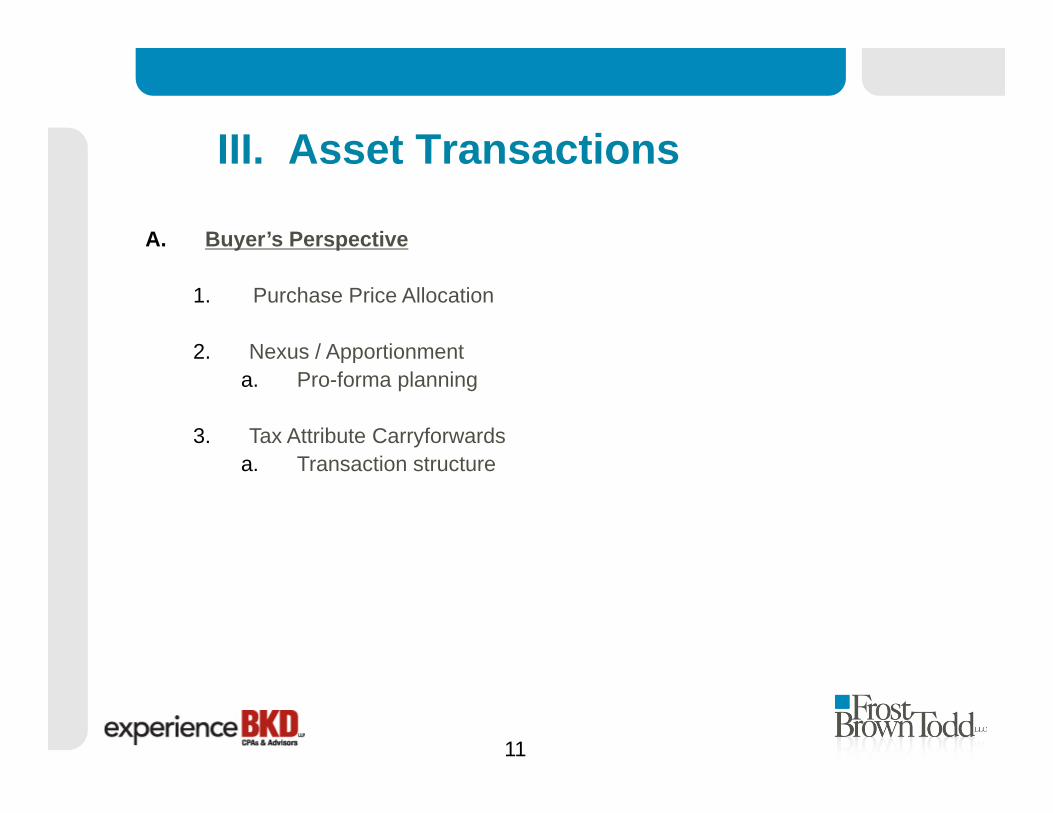

A. Buyer’s Perspective

1. Purchase Price Allocation

2 Nexus / Apportionment2. Nexus / Apportionmenta. Pro-forma planning

3. Tax Attribute CarryforwardsT ti t ta. Transaction structure

11

III Asset TransactionsIII. Asset Transactions

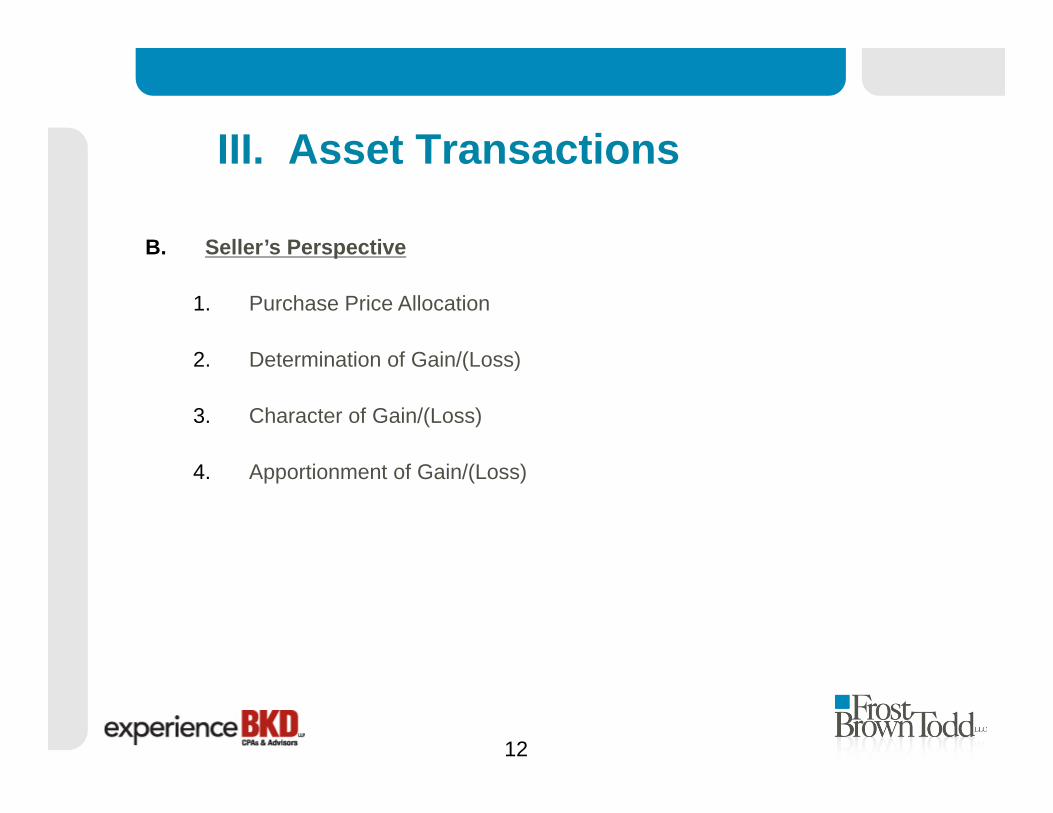

B. Seller’s PerspectiveB. Seller s Perspective

1. Purchase Price Allocation

2 Determination of Gain/(Loss)2. Determination of Gain/(Loss)

3. Character of Gain/(Loss)

4. Apportionment of Gain/(Loss)

12

IV Mergers and ReorganizationsIV. Mergers and Reorganizations

A. Most states follow federal treatment for income taxesA. Most states follow federal treatment for income taxes

B. Same treatment does not necessarily apply to sales taxes

13

V Successor LiabilityV. Successor Liability

A. Determining Exposure: Asset vs. Stock/MergerA. Determining Exposure: Asset vs. Stock/Merger

B. Minimizing Successor Liability

1 Escro1. Escrow2. Lien Searches3. Statement of Condition4. Reps, Warranties & Covenants5. Indemnities

C. Rights to challenge successor liability vs. Merit of taxes owed

14

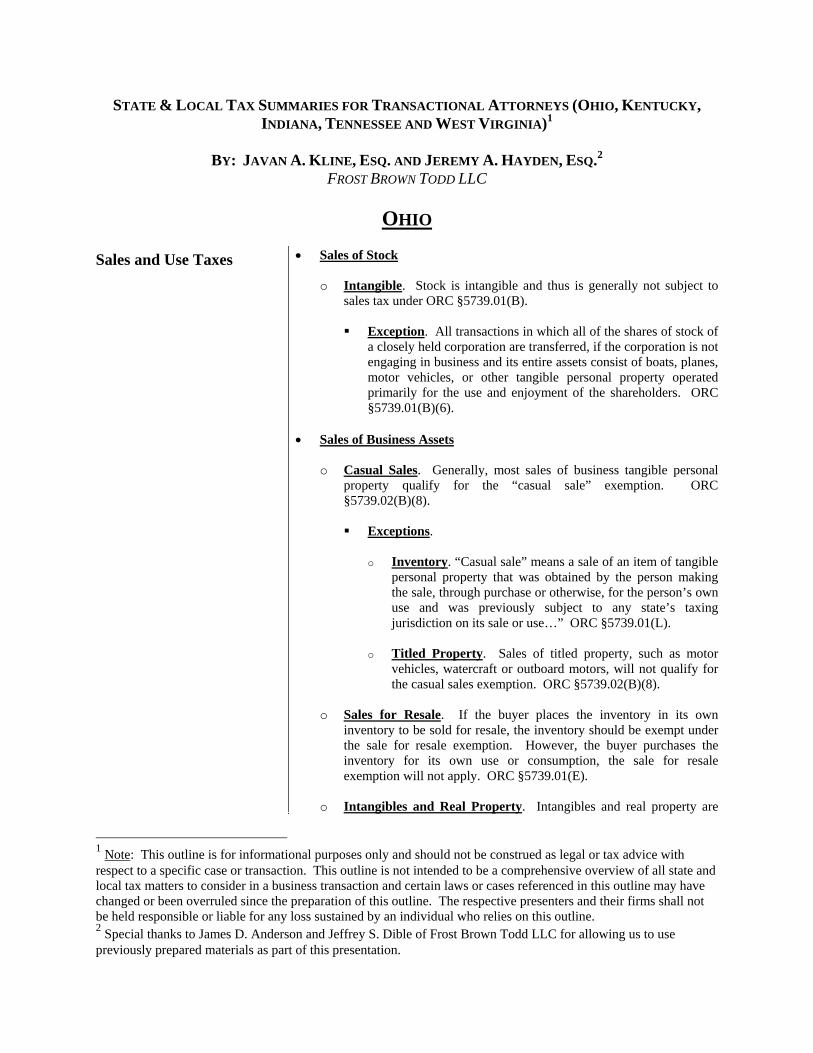

STATE & LOCAL TAX SUMMARIES FOR TRANSACTIONAL ATTORNEYS (OHIO, KENTUCKY, INDIANA, TENNESSEE AND WEST VIRGINIA)1

BY: JAVAN A. KLINE, ESQ. AND JEREMY A. HAYDEN, ESQ.2

FROST BROWN TODD LLC

OHIO

Sales and Use Taxes • Sales of Stock

o Intangible. Stock is intangible and thus is generally not subject to sales tax under ORC §5739.01(B).

Exception. All transactions in which all of the shares of stock of

a closely held corporation are transferred, if the corporation is not engaging in business and its entire assets consist of boats, planes, motor vehicles, or other tangible personal property operated primarily for the use and enjoyment of the shareholders. ORC §5739.01(B)(6).

• Sales of Business Assets

o Casual Sales. Generally, most sales of business tangible personal property qualify for the “casual sale” exemption. ORC §5739.02(B)(8).

Exceptions.

o Inventory. “Casual sale” means a sale of an item of tangible

personal property that was obtained by the person making the sale, through purchase or otherwise, for the person’s own use and was previously subject to any state’s taxing jurisdiction on its sale or use…” ORC §5739.01(L).

o Titled Property. Sales of titled property, such as motor

vehicles, watercraft or outboard motors, will not qualify for the casual sales exemption. ORC §5739.02(B)(8).

o Sales for Resale. If the buyer places the inventory in its own

inventory to be sold for resale, the inventory should be exempt under the sale for resale exemption. However, the buyer purchases the inventory for its own use or consumption, the sale for resale exemption will not apply. ORC §5739.01(E).

o Intangibles and Real Property. Intangibles and real property are

1 Note: This outline is for informational purposes only and should not be construed as legal or tax advice with respect to a specific case or transaction. This outline is not intended to be a comprehensive overview of all state and local tax matters to consider in a business transaction and certain laws or cases referenced in this outline may have changed or been overruled since the preparation of this outline. The respective presenters and their firms shall not be held responsible or liable for any loss sustained by an individual who relies on this outline. 2 Special thanks to James D. Anderson and Jeffrey S. Dible of Frost Brown Todd LLC for allowing us to use previously prepared materials as part of this presentation.

2

generally not subject to the sales, thus when sold as part of an asset transaction should not generate any sales tax. ORC §5739.01(B).

• Successor Liability

o Seller’s Liability. The seller and any responsible persons of the seller (officers or employees responsible for tax returns or company’s fiscal responsibilities) are liable for sales taxes, interest and liabilities that unpaid at the time of the sale. ORC §§ 5739.14 and 5739.33. The seller is required to file a final return within 15 days after the date of selling the business. ORC §§ 5739.14. The seller may also be liable for sales taxes that are incurred after the sale if the buyer continues to use the seller’s vendor’s license. Riley v. Limbach, Ohio Board of Tax Appeals No. 83-G-700 (August 21, 1986). Therefore, it is critical the seller’s vendor’s license is canceled immediately following the sale.

o Purchaser’s Liability. The purchaser must withhold a sufficient

amount of the purchase money to cover the amount of sales taxes, interest, and penalties due and unpaid until the former owner produces a receipt from the tax commissioner showing that the taxes, interest, and penalties have been paid, or a certificate (Form ST 143) indicating that no taxes are due. If the purchaser fails to withhold the purchase money, the purchaser will be personally liable for the taxes, interest and penalties accrued during the operation of the business by the former owner. ORC §5739.14. The purchaser’s liability does not relieve the seller’s liability. Meglen v. Donahue, 8 Ohio App.2d 37, 220 N.E.2d 697 (Franklin Co. 1966).

Commercial Activity Tax • Selling a Business (ORC §5751.10)

o CAT Tax Due Immediately. CAT liability is due immediately if a person liable for the CAT tax does any of the following: Sells the trade or business Disposes in any manner other than in the regular course of

business at least 75% of assets of the trade or business; or Quits the trade or business.

o 45 Days to Pay. The accelerated liability, plus any penalties and

interest, is due and payable within forty-five days after the date of selling or quitting the trade or business.

• Buying a Business – Successor Liability (ORC §5751.10)

o Withhold Purchase Money. The person’s successor shall withhold a sufficient amount of the purchase money to cover the amount due and unpaid until the former owner produces a receipt from the tax commissioner showing that the amounts are paid or a certificate indicating that no taxes are due.

Practice Pointer. One common problem is that the Ohio

Department of Taxation generally will not release the tax certificate until the selling company has sold the company. Therefore, prior to the sale the buyer should request a statement of condition from the Ohio Department of Taxation indicating

3

whether the selling company has any CAT tax liabilities outstanding. This will provide the buyer assurance as to the likely CAT liabilities and also indicate the amount that should be withheld from the purchase amount.

o Failure to Withhold. If a purchaser fails to withhold purchase

money, that person is personally liable up to the purchase money amount, for such amounts that are unpaid during the operation of the business by the former owner.

o Tax Commissioner. The tax commissioner may adopt rules regarding the issuance of certificates under this section, including the waiver of the need for a certificate if certain criteria are met.

Pass-Through Entities • Nonresident Equity Investor in Ohio Pass-Through Entity. If a non-Ohio resident sells an interest in an Ohio pass-through entity, the taxpayer may be subject to Ohio taxes under ORC §5747.212. If the taxpayer owned at least 20% of the equity voting rights of the entity in the current or preceding two tax years, income from the sale would be apportioned to Ohio using the entity’s apportionment factors over the three-year period. ORC §5747.212. If the nonresident investor owned less than 20% of the equity voting rights in the entity, the income would be sourced outside Ohio to the taxpayer’s state of residence under ORC §5747.22(c) and 5747.20(B)(2)(c).

Nexus and Compliance Issues

• Nexus. The application of nexus principles, for determining whether a business entity is subject to various types of Ohio taxes based on doing business in this State, may change (e.g., by expanding the number of locations within which the business has employees or customers) as a result of a business acquisition.

4

KENTUCKY

Corporation Income Tax Corporation Income Tax (Cont.)

Corporation Income Tax • KRS 141.040(1) provides that every corporation doing business in

Kentucky, except those corporations specifically exempted by KRS 141.040(1)(a) through (i), shall pay each taxable year a tax on taxable income.

Corporation Income Tax Rate • The Kentucky corporation income tax is currently imposed at the

following rates: o Four percent (4%) of the first fifty thousand dollars ($50,000) of

taxable net income; o Five percent (5%) of taxable net income over fifty thousand dollars

($50,000) up to one hundred thousand dollars ($100,000); and o Six percent (6%) of taxable net income over one hundred thousand

dollars ($100,000). See KRS 141.040(6). Gross Income/Net Income Defined • In general, Kentucky gross income means gross income as defined in

Internal Revenue Code (“IRC”) Sec. 61, and Kentucky net income is gross income less the deductions allowed under the IRC, subject to certain Kentucky additions and subtractions. See KRS 141.010(12) and (13).

Federal Conformity • Kentucky conforms to the IRC as of a specific date. See KRS 141.010(3).

Thus, for tax years beginning on or after January 1, 2007, there is federal conformity with the IRC in effect on December 31, 2006, exclusive of any amendments made subsequent to that date, other than amendments that extend provisions in effect on December 31, 2006, that would otherwise terminate, except for depreciation and expense deductions allowed under IRC Sections 168 and 179 of the IRC.

Allocation/Apportionment • Where the seller is a multistate business, any gains or losses resulting

from the transaction must be distributed or allocated among the various states that are entitled to tax the seller.

• Kentucky has adopted language substantially similar to the Uniform Division of Income for Tax Purposes Act (UDITPA) provision that divides corporate income into business income, which is subject to formula apportionment, and nonbusiness income, which is subject to allocation to a particular jurisdiction. See KRS 141.120.

Allocation of Nonbusiness Income • Kentucky applies both the transactional test and the functional test when

determining whether corporate income may be apportioned to the state as business income. See 103 KAR 16:060.

o Transactional Test – Income shall be considered “business income” arises from transactions and activities in the regular course of the corporation’s trade or business, part of which business is conducted within Kentucky. Under the transactional test, income may be business income even though the actual transaction or activity that gives rise to the income does not occur in Kentucky. See 103 KAR 16:060, Section 3.

The transactional test shall include: (a) Income from the

5

Corporation Income Tax (continued)

sales of inventory, property held for sale to customers, and services which are commonly sold by the trade or business; and (b) Income from the sale of property used in the production of business income of a kind that is sold and replaced with some regularity, even if replaced less frequently than once a year. See103 KAR 16:060, Section 3(2)(d).

o Functional Test – Business income shall include income from tangible and intangible property if the acquisition, management, and disposition of the property constitute integral parts of the taxpayer’s regular trade or business operations. Under the functional test, business income shall not be required to be derived from transactions or activities that are in the regular course of the taxpayer’s own particular trade or business. See 103 KAR 16:060, Section 4.

1. Property that was an integral part of the trade or business shall not be considered converted to investment purposes merely because it is placed for sale. See 103 KAR 16:060, Section 4(1)(c).

2. Income that is derived from isolated sales, leases, assignments, licenses, and other infrequently-occurring dispositions, transfers, or transactions involving property, including transactions made in liquidation or the winding-up of business, shall be business income, if the property is or was used in the taxpayer’s trade or business operations, unless the property has been converted to nonbusiness use. See 103 KAR 16:060, Section 4(2)(a).

3. If the property is or was held for furtherance of the taxpayer’s trade or business, income from that property may be business income, even though the actual transaction or activity involving that property that gives rise to the income does not occur in Kentucky. See 103 KAR 16:060, Section 4(4).

• Generally, nonbusiness income is allocated to Kentucky if (a) the corporation’s commercial domicile (the principal place from which the trade or business is managed) is located in Kentucky, or (b) property creating the nonbusiness income is utilized in Kentucky. See Instructions, Form 41A720A, Apportionment and Allocation.

• Capital gain or loss from a sale or other disposition of property that is subject to allocation as nonbusiness income is allocated to Kentucky in the following situations:

o The property sold is real property located in Kentucky. o The property sold is tangible personal property with a situs in

Kentucky at the time of the sale. o Tangible personal property is sold when the corporation’s

commercial domicile is in Kentucky and the corporation is not taxable in which the property had a situs.

o Intangible personal property is sold when the corporation's commercial domicile is in Kentucky. See KRS 141.120(5).

Apportionment of Business Income • Kentucky uses a formula to apportion corporate income to Kentucky that

is substantially similar to the three factor apportionment formula (property, payroll, and sales) adopted by UDITPA. However, in

6

Corporation Income Tax (continued)

Kentucky, the sales factor is double-weighted. See KRS 141.120(8). Allocation/Apportionment Issues and Concerns • A seller operating in several states must determine which state it should

source any gain from the sale. Generally, the seller’s gain should either be allocated to a particular state as nonbusiness income or it should be included in the seller’s business income subject to the three factor apportionment formula discussed above.

• It is important to consider the impact of an acquisition on an entity’s apportionment factor calculation. For example, following a merger or an asset acquisition, the acquired corporation’s property, payroll, sales and other applicable factors will be taken into account in determining the acquiring corporation’s apportionment factors in the states where it does business. Even where the reorganization is structured as a stock acquisition, with the acquiring corporation maintaining a separate existence, a similar merging of the apportionment factors could result if the related parties are required to use combined reporting in determining their appropriate state income tax liability. KRS 141.200(11)(a) requires the members of an affiliated group (as defined by KRS 141.200(9)(b)(1)) to file a consolidated state tax return which includes all includible corporations, even though the affiliated group may not have filed a federal consolidated return.

• Additionally, other states have adopted apportionment formulas that are very different from the Kentucky formula. Differences between these state apportionment formulas could potentially create a situation where income is not apportioned to any particular jurisdiction or where the same income is subject to taxation by multiple jurisdictions.

Unitary Groups/Combined Reporting • Kentucky does not permit affiliated groups to file combined reports

utilizing the unitary business concept as a filing method. See KRS 141.200(10) and (15).

• KRS 141.200(11)(a) requires the members of an affiliated group (as defined by KRS 141.200(9)(b)(1)) to file a consolidated state tax return which includes all includible corporations, even though the affiliated group may not have filed a federal consolidated return.

• An affiliated group required to file a consolidated return under KRS 141.200(11)(a) shall be treated for all purposes as a single corporation and all transactions between corporations included in the consolidated return shall be eliminated in computing net income and in determining the property, payroll, and sales factors for apportionment purposes. See KRS 141.200(11)(b).

• Generally, each member of an affiliated group filing a consolidated return is jointly and severally liable for the income tax liability computed on the consolidated return. See KRS 141.200(12).

Reorganizations • Generally, the gain or loss recognized on a reorganization for Kentucky

tax purposes will be the same as the gain or loss recognized for federal tax purposes. This is due to the fact that the computation of a corporation’s Kentucky taxable net income begins with the amount of “federal taxable income” reported on the corporation’s federal tax return (IRS Form 1120, Line 28), before net operating loss and special deductions. See KRS 141.010(12); See Also Instructions, Form 720, Kentucky Corporation Income Tax Return. Further, there is no provision of Kentucky law that

7

Corporation Income Tax (continued)

modifies the federal recognition or nonrecognition rules applicable to reorganizations.

• Where a reorganization involves entities that conduct business in more than one state, the parties must be aware of the potential impact that the transaction could have on nexus considerations (e.g., as a result of reorganization, the corporation is now obligated to pay income taxes in states where the acquired company conducted business), apportionment factor calculations, and consolidated filing requirements.

• Kentucky does not specifically disallow the succession of NOL carryovers of a predecessor entity.

Net Operating Loss Considerations • Kentucky does not specifically disallow the succession of NOL carryovers

of a predecessor entity. Thus, it is presumed that the federal rules (IRC Sections 381 and 382) would apply.

• No NOL carryback deduction is permitted in Kentucky. See KRS 141.011(2).

Capital Gain/Loss Considerations • As discussed above, Kentucky has adopted federal taxable income as the

starting point for determining net taxable income for state tax purposes. Further, Kentucky has no statutory provision that specifically modifies or adjusts federal treatment of capital loss and contribution carryovers. Thus, it is presumed that the federal rules with respect to succession to capital loss and contribution carryovers of a predecessor would apply for Kentucky tax purposes.

• Kentucky does not provide an alternative tax rate on capital gains. IRC Section 338(h)(10) Election • Kentucky has no statutory provision that specifically addresses whether an

IRC Section 338(h)(10) election should be disregarded for Kentucky tax purposes. Further, there is no statutory provision that imposes any special rules with respect to IRC Section 338(h)(10) transactions. Thus, it is presumed that Kentucky would follow the federal tax treatment of the parties to a taxable stock sale making an election under IRC Section 338(h)(10).

Local Taxing Jurisdictions – Occupational License Tax • Pursuant to Section 181 of the Kentucky Constitution, the General

Assembly has granted cities and counties in Kentucky the power to impose and collect license fees on franchises, trades, occupations and professions.

• These license fees will vary by jurisdiction, but often are measured by some percentage of the “net profit” of a business, corporation, partnership, other association, or resident sole proprietor conducting business in the jurisdiction. Gain realized from the sale of a business may be subject to occupational license tax in the appropriate jurisdiction.

Sales and Use Taxes Overview • Kentucky sales and use taxes are imposed at the rate of six percent (6%). • Kentucky sales tax is imposed on a retailer’s gross receipts from retail

sales, or rental or lease, of tangible personal property and digital property. Use tax is imposed on tangible personal property and digital property purchased for storage, use, or consumption in Kentucky if sales tax has

8

not been paid. Whether use tax applies to transactions involving out-of-state parties turns on constitutional nexus issues and concerns.

Exemptions • Kentucky law provides several sales and use tax exemptions that are

applicable to specific goods, services, transactions, taxpayers or businesses. Examples include exemptions for farm machinery, fuels used in manufacturing that exceed three percent of production costs, industrial machinery, industrial processing tools and supplies (including raw materials), machinery for new and expanded industry, property held for resale and occasional sales.

• The “occasional sale” exemption is typically the exemption that the parties to a transaction will rely upon with respect to any potential sales/use tax liability related to tangible personal property that is a part of the transaction. As stated above, “occasional sales” are generally not subject to sales and use taxes. The term occasional sale includes the following:

o A sale of property not held or used by the seller in the course an activity for which a seller’s permit is required, provided the sale is not one of a series of sales sufficient in number, scope, and character to constitute an activity requiring the holding of a seller’s permit. In the case of the sale of the entire, or a substantial portion of the nonretail assets of the seller, the number of previous sales of similar assets is disregarded in determining whether or not the current sale qualifies as an occasional sale.

o A transfer of all or substantially all the property held or used in the course of an activity for which a seller’s permit is required, provided that after the transfer the real or ultimate ownership of the property is substantially unchanged (i.e., inter-company sales).

A seller qualifies as a retailer requiring a permit when the seller makes more than two retail sales during any 12-month period.

• Thus, if a retail business sells all of its assets as part of a bulk sale, the inventory that the business held for sale would not satisfy the occasional sale exemption. However, the retail inventory may be exempt from sales and use tax as property held for resale. Accordingly, the seller should obtain a resale certificate from the buyer.

Successor Liability • Where a retailer liable for sales or use tax sells a business or business

assets, or otherwise quits the business, the purchaser or successor is obligated to withhold from the purchase price an amount that is sufficient to cover the liability until the retailer produces a receipt from the Kentucky Department of Revenue evidencing that the liability is paid or a certificate stating that no amount is due. If the purchaser fails to withhold the purchase price, the purchaser becomes personally liable for payment of the amount required to be withheld to the extent of the purchase price.

• As a result, the parties to a transaction should analyze whether the transaction is subject to tax, identify any appropriate exemptions (as well as obtain necessary certification of the exemption), and ensure that any tax liability is satisfied as part of the transaction.

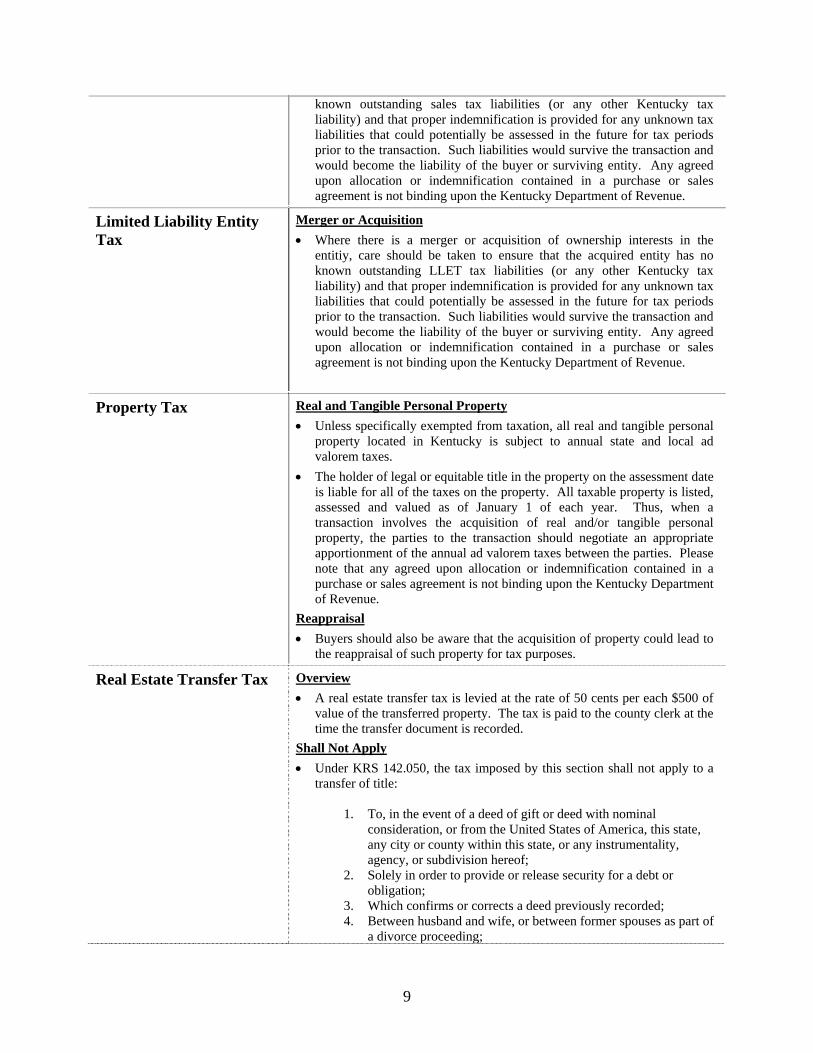

• Where there is a merger or acquisition of ownership interests in the entitiy, care should be taken to ensure that the acquired entity has no

9

known outstanding sales tax liabilities (or any other Kentucky tax liability) and that proper indemnification is provided for any unknown tax liabilities that could potentially be assessed in the future for tax periods prior to the transaction. Such liabilities would survive the transaction and would become the liability of the buyer or surviving entity. Any agreed upon allocation or indemnification contained in a purchase or sales agreement is not binding upon the Kentucky Department of Revenue.

Limited Liability Entity Tax

Merger or Acquisition • Where there is a merger or acquisition of ownership interests in the

entitiy, care should be taken to ensure that the acquired entity has no known outstanding LLET tax liabilities (or any other Kentucky tax liability) and that proper indemnification is provided for any unknown tax liabilities that could potentially be assessed in the future for tax periods prior to the transaction. Such liabilities would survive the transaction and would become the liability of the buyer or surviving entity. Any agreed upon allocation or indemnification contained in a purchase or sales agreement is not binding upon the Kentucky Department of Revenue.

Property Tax Real and Tangible Personal Property • Unless specifically exempted from taxation, all real and tangible personal

property located in Kentucky is subject to annual state and local ad valorem taxes.

• The holder of legal or equitable title in the property on the assessment date is liable for all of the taxes on the property. All taxable property is listed, assessed and valued as of January 1 of each year. Thus, when a transaction involves the acquisition of real and/or tangible personal property, the parties to the transaction should negotiate an appropriate apportionment of the annual ad valorem taxes between the parties. Please note that any agreed upon allocation or indemnification contained in a purchase or sales agreement is not binding upon the Kentucky Department of Revenue.

Reappraisal • Buyers should also be aware that the acquisition of property could lead to

the reappraisal of such property for tax purposes.

Real Estate Transfer Tax Overview • A real estate transfer tax is levied at the rate of 50 cents per each $500 of

value of the transferred property. The tax is paid to the county clerk at the time the transfer document is recorded.

Shall Not Apply • Under KRS 142.050, the tax imposed by this section shall not apply to a

transfer of title:

1. To, in the event of a deed of gift or deed with nominal consideration, or from the United States of America, this state, any city or county within this state, or any instrumentality, agency, or subdivision hereof;

2. Solely in order to provide or release security for a debt or obligation;

3. Which confirms or corrects a deed previously recorded; 4. Between husband and wife, or between former spouses as part of

a divorce proceeding;

10

5. On a sale for delinquent taxes or assessments; 6. On partition; 7. Pursuant to: (a) Merger or consolidation between and among

corporations, partnerships, limited partnerships, or limited liability companies; or (b) any conversion of a partnership, limited partnership, corporation, or limited liability company into a partnership, limited partnership, corporation, or limited liability company;

8. Between a subsidiary corporation and its parent corporation for no consideration, nominal consideration, or in sole consideration of the cancellation or surrender of either corporation's stock;

9. Under a foreclosure proceeding; 10. Between a person and a corporation, partnership, limited

partnership or limited liability company in an amount equal to the portion of the value of the real property transferred that represents the proportionate interest of the transferor of the property in the entity to which the property was transferred, if the transfer was for nominal consideration;

11. Between parent and child or grandparent and grandchild, with only nominal consideration therefor;

12. By a corporation, partnership, limited partnership, or limited liability company to a person as owner or shareholder of the entity, upon dissolution of the entity, in an amount equal to the portion of the value of the real property transferred that represents the proportionate interest of the person to whom the property was transferred, if the transfer was for nominal consideration;

13. Between a trustee and a successor trustee; and 14. Between a limited liability company and any of its members.

Kentucky Unemployment Insurance Tax – Successor Liability

Successorship • In general, a company conducting business in Kentucky is required to pay

unemployment insurance tax with respect to its Kentucky employees. KRS 341.540(2) authorizes the Department to promulgate administrative regulations establishing the conditions under which an employing unit shall be found to be successor to another. Such conditions are set forth in 787 KAR 1:300(2). Under 782 KAR 1:300(2), successorship is deemed to have occurred between two employing units if:

1. Negotiation occurs to bring about the transfer, either directly between the parties to the transfer, or indirectly through a third party intermediary; and

2. At least two of the conditions established in the subsection are met, except this requirement shall not be satisfied if only paragraphs (c) and (d) of this subsection are met:

(a) The employing unit was a going concern at the time negotiations for the transfer began;

(b) The subsequent owner or operator continued or resumed basically the same type of employing unit in the same location;

(c) The subsequent owner employed fifty (50) percent or more of the previous owner’s

11

workers in covered employment;

(d) The previous owner employed fifty (50) percent or more of the subsequent owner’s workers in covered employment; or

(e) The subsequent owner acquired work contracts or commitments from the previous owner.

Due Diligence • Thus, transactional due diligence should include a review of the target

company’s unemployment insurance tax compliance history. Appropriate steps should be taken to address any outstanding liability at the time of the transaction either through payment or through structuring the transaction in such a way to avoid a determination of successorship.

Motor Vehicles included in Acquisition

Motor Vehicles • In Kentucky, trucks, tractors and other commercial motor vehicles owned

and used in Kentucky would be exempt from sales and use tax where the applicable motor vehicle usage tax has been paid or where the occasional sale exemption is satisfied. Trailers and Semi-trailers are exempt from both sales and use tax and motor vehicle usage tax. Trucks and tractors constitute "motor vehicles" subject to the motor vehicle usage tax. A limited exemption is provided for commercial motor vehicles that are owned by nonresidents, used primarily in interstate commerce, and based in another state, yet are required to be registered in Kentucky due to certain operational requirements or fleet proration agreements, and which are registered pursuant to these forced registration provisions. Other vehicles exempt from the motor vehicle usage tax include the following:

1. Motor vehicles transferred when a name is changed by a business

or an individual and no other transaction has taken place: and 2. Motor vehicles transferred to a corporation from a proprietorship

or limited liability company to a limited liability company from a corporation or proprietorship, or from a corporation of limited liability company to a proprietorship, within six months from the time that the business is incorporated, organized, or dissolved.

Local Occupational Taxes Local Taxing Jurisdictions – Occupational License Tax • Pursuant to Section 181 of the Kentucky Constitution, the General

Assembly has granted cities and counties in Kentucky the power to impose and collect license fees on franchises, trades, occupations and professions.

• These license fees will vary by jurisdiction, but often are measured by some percentage of the “net profit” of a business, corporation, partnership, other association, or resident sole proprietor conducting business in the jurisdiction. Gain realized from the sale of a business may be subject to occupational license tax in the appropriate jurisdiction.

12

INDIANA

“Successor Liability” case law in Indiana

• General rule that the purchaser in an asset sale does not impliedly assume any liability of the seller: Winkler v. V. G. Reed & Sons, Inc., 638 N.E.2d 1228 (Ind. 1994)

• Four exceptions to the general rule are described in Winkler and in Markham v. Prutsman Mirror Co., 565 N.E.2d 385 (Ind. Ct. App. 1991) o Express or implied agreement to assume the obligation o Fraudulent asset sale with intent to escape liability o Purchase that is a de facto merger or consolidation o Purchaser is a mere continuation of the seller Per Markham, all 4 exceptions depend on (1) purchaser acquiring substantially all of the seller’s assets and (2) seller or predecessor ceasing to exist

• Per Sorenson v. Allied Products Corp.,, 706 N.E.2d 1097 (Ind. Ct. App. 1999), a de facto merger is established by showing all of the following: o Continuity of ownership; o Continuity of management, personnel and physical operation; o Predecessor or seller’s cessation of business operations and dissolution

as soon as practically and legally possible after closing o Successor’s assumption of those liabilities ordinarily necessary for

uninterrupted continuation of the predecessor’s business

“Successor Liability” case law in Indiana — continued

• Indiana might apply a fifth exception when a distinct product line is acquired and continued by the purchaser; see Guerrero v. Allison Engine Co., 725 N.E.2d 479 (Ind. Ct. App. 2000)

• J. Dible does not know of any reported Indiana appellate decisions applying common law successor liability specifically in the context of state or local taxes (i.e., not relying on statutory tax lien or statutory liability)

No General Indiana Franchise Tax for Corps, P’ships, or LLCs

• Indiana has a “gross premium privilege tax” (I.C. §27-1-18-2, imposed on foreign insurance companies doing business in Indiana and domestic insurance companies who elect to be taxed)

• Indiana has a bank franchise tax (I.C. §6-5.5-1-1 et seq.) imposed on banks and other defined entities engaged in “transacting the business of a financial institution”; computed on modified federal taxable income and imposed in lieu of the adjusted gross income tax (see I.C. §6-3-2-2.8)

• Indiana imposes an entity-level “utility receipts tax” at 1.4% on the gross receipts of any entity derived from the retail sale in Indiana of utility services (water, steam, gas, electricity, telecommunications) for consumption; see I.C. §6-2.3-1-1 et seq.-

Indiana Adjusted Gross Income Tax (net income tax) See I.C. §6-3-1-1 et seq.

• Principal income tax imposed by Indiana, based on federal taxable income plus / minus all stated adjustments

• Broad rule requiring add-back of all federal deductions taken for income taxes “based on or measured by income and levied at the state level by any state” (see I.C. §6-3-1-3.5(a)(2) and (b)(3)

• 8.5% rate for C corporations, 3.4% for individuals • Pass-through treatment recognized for S corp. shareholders, partners, and

LLC members

13

• The sales factor (under the 3-factor formula) has been given progressively more weight since 2006; sales factor is weighted 7x for 2008, 8x for 2009, and 9x for 2010; for tax years beginning after Dec. 31, 2010, 1-factor apportionment based on sales only (I.C. §6-3-2-2(b))

• County taxes (COIT and CAGIT) increase the effective rate and are computed and reported on the state return

• Indiana allows (and occasionally requires) unitary method of reporting by parent and subsidiaries

Indiana Adjusted Gross Income Tax (net income tax) — continued

• Computation of Indiana NOLs and carrybacks can differ from federal; see Form IT-20NOL

• Employers required to withhold Indiana AGI tax from wages or compensation are subject to personal “trust fund liability” for withheld tax: “In the case of a corporate or partnership employer, every officer, employee, or member of such employer, who, as such officer, employee, or member is under a duty to deduct and remit such taxes shall be personally liable for such taxes, penalties, and interest.” – I.C. §6-3-4-8(f) and (g)

• Taxpayer must provide Indiana Dept. of Revenue (IDOR) with a copy of any federal tax return upon demand (I.C. §6-3-4-6(a)

• Taxpayer must notify the IDOR in writing within 120 days after changes are made to the taxpayer’s federal income tax return or federal income tax liability, including an amended Indiana return if Indiana AGI changes (I.C. §6-4-3-6(b) and (c))

• IDOR has 6 months after the filing of that notice within which to assess additional Indiana tax (I.C. §6-8.1-5-2(i))

A.G.I. Tax Withholding on Distributions to Non-Indiana Shareholders, Partners, and LLC Members

Required by I.C. §§6-3-4-12 and 6-3-4-13

Indiana Sales & Use Taxes (gross retail taxes)

• See I.C. §6-2.5-1-1 et seq.; 7-percent rate • Imposed on “retail sales,” and “wholesale sales” of tangible personal

property and (use tax) on the possession, use or storage of tangible personal property within Indiana

• Utility services, many telecommunications services, and installation charges are taxable, but most other services are excluded from the sales tax base

• Broad exemption in regulations (not in statute) for “casual sales,” i.e., “an isolated or occasional an isolated or occasional sale by the owner of tangible personal property purchased or otherwise acquired for his use or consumption, where he is not regularly engaged in the business of making such sales” (45 IAC 2.2-1-1(d))

14

Indiana Sales & Use Taxes (gross retail taxes) — continued

• Exemptions for various manufacturing and agricultural inputs, food ingredients, consumed raw materials, etc. are defined piecemeal and in detail in the statute and regulations

• “Trust fund tax” personal liability can be imposed on a retail merchant or its employee, director, officer or manager who fails to remit collected sales tax; Class D felony treatment for “knowing” violations (I.C. §6-2.5-9-3)

• I.C. §6-2.5-6-9 permits a retail merchant to claim a deduction on a subsequent sales tax return (or a claim for refund) with respect to sales tax remitted on retail sales but not collected from the retail customer, where the receivable was written off as uncollectible bad debt under Code §166

Administration of Indiana “listed taxes”

• I.C. §6-8.1-1-1 defines “listed taxes,” which includes the adjusted gross income tax and the sales and use (gross retail) tax

• Article 8.1 of title 6 establishes uniform procedures for assessment, administrative protest, collection, penalties and interest, refunds, etc. for all “listed taxes”

Assessment for under-statements of listed taxes

• Procedure and timetables for proposed assessment, protest and administrative appeal, and Indiana Tax Court review are stated in I.C. §6-8.1-5-1 et seq.

• General 3-year limitations period on assessment starts running from the filing of a valid and substantially complete return (I.C. §6-8.1-5-2(a)

• For sales tax deficiencies, the 3 years starts running immediately after the end of the calendar year in which the taxable sales were reported or reportable

• 6-year limitations period for assessments in the case of understatements of 25% or more of certain state income tax liabilities (I.C. §6-8.1-5-2(b)

• Limitations period does not start running if no return at all is filed or if a substantially blank, fraudulent, or unsigned return is filed (I.C. §6-8.1-5-2(f)

• IDOR can propose an assessment based on an erroneously issued refund within 2 years (or 5 years in the case of a fraudulent refund); see I.C. §6-8.1-5-2(g)

Statutory lien for unpaid state “listed taxes”

• I.C. §6-8.1-8-1 requires IDOR to issue a notice and demand (Form AR-40) for payment of unpaid tax that has been finally assessed

• Lien arises by operation of law if payment in full does not occur within 10 days after demand and upon issuance of tax warrant to County Sheriff and filing of warrant with County Clerk at least 20 days after the payment demand is mailed (I.C. §6-8.1-8-2)

• County Clerk records the tax warrant in the judgment docket; IDOR can file the warrant in more than 1 county

• The tax lien is effective for 10-year periods and can be repeatedly renewed by a new filing (I.C. §6-8.1-8-2(f))

• IDOR sometimes issues “alias tax warrants” to and in the name of a responsible officer, director or manager with respect to an unpaid listed tax liability owed by an entity

• I.C. §6-8.1-3-16 requires the IDOR to maintain a list of outstanding and unpaid tax warrants (not more than 10 years old) for listed taxes; with respect to delinquent sales taxes, the list is searchable (http://www.in.gov/apps/dor/rrmc/Default.aspx)

Claims for refund of state- • General procedure and timetables are in I.C. §6-8.1-9-1

15

level “listed taxes” • General time limit for filing a refund claim is 3 years after the later of the date of the tax payment or the due date of the return

Effect of state tax delinquency on state business license

Relying on I.C. §6-8.1-7-1(f), the IDOR claims the general right to provide general information about a taxpayer’s delinquent status to any Indiana state agency that has issued a license or operating permit to that taxpayer

Procedures for “tax clearances” for business taxpayers that dissolve, liquidate, or cease operations

• Each new business that will be withholding and remitting taxes on wages or collecting sales taxes is required to register on-line with the IDOR (Form BT-1)

• Form BT-1 lists the names and social security numbers of officers, directors, general partners or LLC managers

• The IDOR presumes that each individual listed on the BT-1 remains potentially and personally liable for the business’s failure to remit withheld payroll taxes or collected sales taxes

• A seller business that is ceasing operations or dissolving should file a Form BC-100 (State Form 52038) along with documentary evidence of dissolution or ceased operations

• Information (including names and SSNs) regarding new and former responsible officers can be filed with the IDOR on Form ROC-1 (State Form 52039)

• There is no specific statutory procedure for seeking a state tax clearance for a dissolving or disappearing partnership or LLC

• I.C. §6-8.1-10-9 requires a dissolving domestic corporation or a withdrawing foreign corporation to notify the IDOR within 30 days (A corporation that files a federal Form 966 as a result of dissolution or a reorganization must also file a copy of the Form 966 or an IT-966 (State Form 50150) with the IDOR)

• I.C. §6-8.1-10-9(g) permits a dissolving corporation to apply to the IDOR for a clearance letter or certificate (showing that all required returns have been filed and all taxes paid)

• If a dissolving corporation does not apply for and obtain a clearance, §6-8.1-10-9(c) and (d) impose personal liability on all officers or directors, for 1 year, for all acts or omissions that result in distributions of corporate assets “in violation of the interests of the state or political subdivision,” including statutory interest, penalties, and an additional penalty of up to 30%

• 1-year personal liability of officers and directors is subject to contribution among officers and directors and contribution from shareholders to the extent of assets received (I.C. §6-8.1-10-9(c))

• The IDOR or county treasurer must commence an action against the officer or director within the 1-year period after a substantially complete notification of dissolution or withdrawal is received by the IDOR

Indiana unemployment insurance contribution issues

• The administrative agency in Indiana is the Department of Workforce Development (DWD)

• Substantive law is found in Ind. Code 22-4 and in 646 Ind. Admin. Code [IAC] title 3

• Unpaid or underpaid employer contributions (i.e., state unemployment tax contributions) are assessed and collected under parallel procedures (I.C. §§22-4-29-1 through 22-4-31-7) that are similar to the IDOR’s procedures for income taxes on wages and other listed taxes

16

• “Employing unit” and “employer” are defined in I.C. §§22-4-6-1, 22-4-7-1, and 22-4-7-2

Indiana unemployment insurance contribution issues — continued

• Complex rules governing employers’ “experience accounts” are in I.C. 22-4-10 and 22-4-11.5

• Per I.C. §§22-4-7-2(a) and (b) and 22-4-10-6, an employing unit can be treated by DWD as a “successor employer” and therefore as an “employer” if it: o “acquires the organization, trade, or business within this state of

another which at the time of such acquisition is an employer subject to this article” or

o acquires substantially all the Indiana assets of a covered employer, where the acquisition results in the continuation or operation of a trade or business, or

o “acquires a distinct and segregable portion of the organization, trade, or business within this state of another employing unit” [subject to some other conditions]

• Per I.C. §22-4-32-21, an entity or individual(s) that acquires part or all of a covered “employer” or its assets must notify the DWD commissioner at least 5 days before the closing o If the notice is not given, DWD may proceed with collection remedies

against either the predecessor or successor and the unpaid contributions will be a lien against the assets acquired by the successor

o The lien will not exceed the value of the assets acquired by the successor and will not be valid against a good-faith purchaser who acquires assets from the successor without notice of the lien

o After the closing, the acquirer/successor may demand and receive from DWD a statement of unpaid contributions owed by predecessor

• “Concurrent employment” and “related entities” are defined in I.C. §22-4-6-3

• The issue of when a purchaser may assume part or all of the “experience account” of the seller or predecessor employer is subject to vague and complicated rules in I.C. §22-4-9-3 and I.C. 22-4-11.5; these rules are applied inconsistently and sometimes irrationally by DWD hearing officers and other personnel

• Under I.C. §22-4-32-19(a), an application for an adjustment or for refund of an overpaid employer contribution must be submitted to DWD within 4 years after the contribution was paid

Indiana ad valorem property taxes (assessed and collected at the county level)

• Effective January 1, 2008, there is effectively no ad valorem property tax imposed on inventory; see I.C. §§6-1.1-1-8.4 and 6-1.1-1-11

• Taxable business personal property includes equipment, bases for equipment, motor vehicles, and advertising billboards on land not owned by the advertiser, and other non-inventory tangible property held for investment or used in a business

• Business personal property is reported by May 15 of each year on various versions of Forms 103 or 104

• I.C. §22-4-32-23 provides a procedure analogous to the IDOR’s dissolution clearance procedures for corporate taxpayers

• A covered employer that is dissolving, withdrawing as an admitted foreign entity, etc. can file with DWD a request for a clearance letter confirming that all reports have been filed and that all contributions have been paid

17

• An employer that completely ceases operations (without selling to another business) should file a “Report of Inactivation” (State Form 46800) with DWD within 30 days after ceasing operations

• An employer that undergoes a reorganization (change of federal EIN) or that sells substantially all of its assets to a purchaser that will continue operations should file a “Report of Transfer – Complete Sale” (State Form 46799)

• An employer that sells only part of its assets to a purchaser and that will continue to pay employees under the seller’s federal EIN should file a “Report of Transfer – Partial Sale” (State Form 23299)

• Property taxes on both real property and business personal property become a lien on March 1 but become due and payable on May 10 and November 10 of the following year, assuming that the County Treasurer sends out the tax bills on time (in recent years, a big IF)

• Although property taxes become a lien on March 1 (in the “assessment year”), the actual amount of the taxes will not be known until the following year (the “payment year”) when the approved tax rate is set and the tax bills are issued

• Taxable tangible property’s assessed value (true tax value) is not supposed to exceed its “market value in use” (a USPAP appraisal is always the best evidence that the assessing official’s conclusion is wrong)

Indiana ad valorem property taxes — continued

• I.C. §6-1.1-15-1 et seq. describes and governs the multi-stage procedure for administrative appeal and Tax Court appeal of a disputed assessment

• Generally, in order for an appeal of a disputed assessment to be effective for that assessment year, the taxpayer / property owner must commence the appeal process within 45 days after receiving a Form 11 or a Form 113 from the county or township assessor or (if no Form 11 or Form 113 is issued) by the later of May 10th of the year or the mailing of the tax statement

• When an overpayment of property tax is determined as a result of a successful assessment appeal or settlement, I.C. §6-1.1-15-11 requires that the resulting overpayment amount be credited first against the next property tax installment owed by that taxpayer, with the excess to be issued by the county auditor as a refund

Other Indiana state excise taxes or annual ad valorem taxes that may apply to a seller business

• Alcoholic beverage excise taxes imposed and collected under Indiana Code title 7.1

• Cigarette tax under I.C. §6-7-1-1 et seq. • Tobacco products excise tax on non-cigarette products under I.C. §6-7-2-1

et seq. • Gasoline excise tax under I.C. §6-6-1.1-101 et seq. • Special fuel tax under I.C. §6-6-2.5-1 et seq. on LPG, propane, biodiesel,

blended biodiesel, and other fuels besides gasoline, kerosene and jet fuel • Motor carrier fuel tax imposed by I.C. §6-4.1-1-1 et seq. on fuel consumed

by commercial carriers operating large trucks and certain passenger vehicles (imposed on the basis of fuel consumed and miles traveled in Indiana; parallel procedures for audit, administrative appeal, and refund under IFTA)

• Annual motor vehicle excise tax under I.C. §6-6-5-1 et seq. • Auto rental excise tax (4%) on gross income from rental of passenger

motor vehicles and small trucks (see I.C. §6-6-9-1 et seq.; Marion County

18

[Indianapolis] and Vanderburgh County [Evansville] have supplemental auto rental excise taxes

• Annual commercial vehicle excise tax under I.C. §6-6-5.5-1 for vehicles base-registered in Indiana under the International Registration Plan

Other Indiana excise taxes or annual ad valorem taxes that may apply to a seller business — continued

• Aircraft excise tax under I.C. §6-6-6.5-1 • Commercial vessel tonnage tax on commercial watercraft (I.C. §6-6-6-1 et

seq.) • Boat excise tax on non-commercial watercraft (I.C. §6-6-11-1 et

seq.)Hazardous waste disposal tax of $11.50 per ton under I.C. §6-6-6.6-1 et seq.

• Innkeepers (hotel & motel) taxes, food and beverage taxes, stadium taxes, and entertainment facility taxes have been established or adopted by many Indiana counties under article 9 of title 6 (I.C. 6-9)

19

TENNESSEE

No General Individual Income Tax

• Tennessee has no generally applicable income tax on individuals, because such a tax is prohibited by the Constitution of Tennessee. Tenn. Con. Art. II, Sec. 28. Evans v. McCabe, 52 S.W.2d 159 (Tenn. 1932); Jack Cole Co. v. MacFarland, 337 S.W.2d 453 (Tenn. 1964).

• Taxation of individuals’ incomes is limited to a tax imposed on certain categories of dividends and interest. Tenn. Con. Art. II, Sec. 28; Tennessee Code Annotated (“T.C.A.”) §§ 67-2-101, et seq.

• Because Tennessee has no general individual income tax, there are no Tennessee counterparts to the Internal Revenue Code provisions dealing with the federal income tax consequences to shareholders (I.R.C. §§ 354 to 358) and partners (I.R.C. §§ 741 to 743) upon transfers of corporate stock or partnership interests.

Sales Taxes • Tennessee imposes a tax (generally 7% of total consideration at the state level, T.C.A. § 67-6-202, and 2¼ -2¾ % of consideration, up to $1,600 per single article, at the local level, T.C.A. § 67-6-702) on sales of tangible personal property. o There is a corresponding use tax on the use, consumption, storage, etc.,

of tangible personal property. T.C.A. § 67-6-203. o Transfers of corporate stock, partnership interests, and interests in

limited liability companies and similar entities are not subject to Tennessee sales taxes, because such assets are not tangible personal property. T.C.A. § 67-6-102(92)(A).

• A “sale” of tangible personal property occurs at the time and place of a transfer (in exchange for consideration) of possession or title, or both. T.C.A. § 67-6-102(81)(A). The timing and placement of a transfer of title is determined under applicable provisions of the Uniform Commercial Code. Eusco, Inc. v. Huddleston, 835 S.W.2d 576 (Tenn. 1992).

• An exception from sales taxes exists for occasional and isolated sales by persons not in the business of regularly selling the type of property being sold. T.C.A. § 67-6-102(9)(B). This exception does not apply to most transfers of motor vehicles, aircraft and vessels that are subject to registration with state government agencies. T.C.A. § 67-6-102(9)(C).

• An exception also exists for sales of “industrial machinery,” T.C.A. §§ 67-6-206(a); 67-6-102(47); Eastman Chemical Co. v. Johnson, 151 S.W.3d 994 (Tenn. 2004),and “industrial materials,” T.C.A. §§ 67-6-329(a)(12); 67-6-106(b)(31), that are used in manufacturing, fabricating and processing other tangible personal property for resale.

• A sale of tangible personal property that is subject to a taxable lease can cause unanticipated or accelerated sales tax liability. T.C.A. §§ 67-6-102(79) and (81)(A).

• A successor in interest of a business that owes sales taxes can become liable for such taxes in an amount up to the “purchase money” paid in acquiring the business. T.C.A. § 67-6-513. A successor is required to withhold an amount of the purchase money that is sufficient to pay the sales tax liability. T.C.A. § 67-6-513(b).

Excise Taxes • Tennessee imposes a 6½% excise tax on the “net earnings” of corporations (including real estate investment trusts, T.C.A. §§ 67-4-2007; 67-4-2004(34)) and designated other business entities that do business in

20

the state. “Net earnings” is defined as federal taxable income, with specified modifications. T.C.A. § 67-4-2006.

• The excise tax applies to limited liability entities that, for federal income tax purposes, are treated as “flow-through” entities and are not subject to taxation. T.C.A. § 67-4-2004(34). o This tax also applies to “Subchapter S corporations,” including to

gains thereof that are not subject to federal income taxation and that are attributable to an election under Internal Revenue Code § 338(h)(10). T.C.A. § 67-4-2006(b)(1)(M).

o In many cases, the excise tax liability of a Subchapter S corporation is greater than that of entities that are treated as partnerships for federal income tax purposes, because the latter group is allowed a deduction for amounts of income that are subject to federal self-employment taxes. T.C.A. §§ 67-4-2006(a)(2); 67-4-2006(a)(4)(B).

• For corporations and other taxable entities doing business in more than one state, T.C.A. § 67-4-2010, it is necessary to determine whether the net earnings generated by a business acquisition constitute business earnings (and therefore are apportioned among states according to factors based on receipts, property and payroll), T.C.A. § 67-6-2012, or non-business earnings (and thus are allocated among states based on commercial domicile and other factors), T.C.A. § 67-6-2011. Under respective definitions, earnings are deemed to be business earnings, unless “clear and cogent evidence” indicates otherwise. T.C.A. §§ 67-4-2004(3); 67-4-2004(24).

• Generally, in computing Tennessee excise tax liability businesses are not required or allowed to file consolidated returns. T.C.A. § 67-4-2007(e)(1). o An exception applies to financial institutions that are members of a

unitary group, which are required to file combined returns. T.C.A. § 67-4-2007(e)(2).

o One corollary to the generally applicable separate return rule is that a surviving party to a reorganization is not permitted to use a net operating loss carryover generated by a predecessor. T.C.A. § 67-4-2006(c)(2).

• Accelerated depreciation methods that are allowed in computing federal taxable income are not permitted in determining Tennessee excise tax liability. T.C.A. § 67-4-2006(b)(1)(G). This creates a discrepancy between the respective bases of assets under the two tax systems.

Tax on Property, Property Transfers and Property Liens; Tax Liens

• When the ownership of real and tangible personal property used in business changes hands, the annual ad valorem taxes on such property should be apportioned by agreement between the acquiring party and the exchanging party. Whether or not there is an apportionment agreement, a lien for ad valorem taxes attaches to the subject property. T.C.A. §§ 67-5-2101 and 2102.

• A tax is imposed (at a rate of 0.37%) on the transfer of real property by a recorded deed, in exchange for consideration. T.C.A. § 67-4-409(a). Instruments made pursuant to mergers, consolidations, and plans of reorganization are not subject to this transfer tax.

• A tax is imposed (at a rate of 0.115%) on the recordation of instruments that evidence secured indebtedness. T.C.A. § 67-4-409(h).

• In addition to liens that are imposed for unpaid property taxes, liens are

21

imposed on the assets in Tennessee owned by parties against whom the Tennessee Department of Revenue makes an assessment of any of the types of taxes that it collects and administers (which includes sales taxes and excise tax). T.C.A. § 67-1-1403. These liens remain in place following a transfer of ownership of such assets.

Nexus Considerations • The application of nexus principles, for determining whether a business entity is subject to various types of Tennessee taxes based on doing business in this State, may change (e.g., by expanding the number of locations within which the business has employees or customers) as a result of a business acquisition. T.C.A. §§ 67-6-203-313 and - 608; Arco Bldg Systems, Inc. v. Chumley, 209 S.W.3d 63 (Tenn. App. 2006).

22

WEST VIRGINIA

Business Registration Tax • Registration. Businesses are required to obtain a business registration certificate from the West Virginia State Tax Department (“Tax Department”) prior to engaging in business in West Virginia. W. Va. Code § 11-12-3. In order to obtain the certificate, Form BUS-APP must be completed and filed with the Tax Department. A “separate business registration certificate is required for each fixed business location from which property or services are offered for sale or lease to the public.” W. Va. Code § 11-12-3(b)(1). o Registration Permanent. As of July 1, 2010, a business registration

certificate is generally permanent and does not need to be renewed. W. Va. Code § 11-12-5(a).

West Virginia State Taxes -Sales and Use Taxes -Business Franchise Tax -Corporation Net Income Tax -Health Care Provider Taxes -Withholding Taxes -Excise Taxes -Business and Occupation Tax -Severance Taxes -Telecommunications Tax

• Seller’s Liability. If any person subject to any state taxes administered under the West Virginia Tax Procedure and Administration Act sells out his or its business or stock of goods, or ceases doing business, any tax, additions to tax, penalties and interest imposed shall become due and payable immediately and such person shall, within thirty days after selling out his or its business or stock of goods or ceasing to do business, make a final return or returns and pay any tax or taxes which may be due. The unpaid amount of any such tax shall be a lien upon the property of such person. W. Va. Code § 11-10-11(f)(1).

• Successor’s Liability. The successor in business of any person who sells

out his or its business or stock of goods, or ceases doing business, shall be personally liable for the payment of tax, additions to tax, penalties and interest unpaid after expiration of the thirty-day period allowed for payment. The amount of tax, additions to tax, penalties and interest for which the successor is liable shall be a lien on the property of the successor, which shall be enforced by the tax commissioner. Va. Code § 11-10-11(f)(2) and WV Code of State Rules 110-15-4.9.

o Applicable West Virginia State Taxes. The successor liability

provisions apply to inheritance and transfer taxes, estate tax and interstate compromise and arbitration of inheritance and death taxes, business registration tax, minimum severance tax on coal, corporate license tax, business and occupation tax, severance tax, additional severance taxes, telecommunications tax, interstate fuel tax, consumers sales and service tax, use tax, tobacco products excise taxes, soft drinks tax, personal income tax, business franchise tax, corporation net income tax, gasoline and special fuels excise tax, motor fuels excise tax, motor carrier road tax, health care provider taxes and tax relief for elderly homeowners and renters administered by the state tax commissioner. W. Va. Code § 11-10-3(a). Legislative Rule Applies to Most West Virginia Taxes. While

the legislative rule discussed in detail below (WV Code of State Rules 110-15-4.9, et seq.) pertains to sales and use taxes, it construes a section of the West Virginia Code contained in the Tax Procedures Act, W. Va. Code § 11-10-1, et seq., and thus should pertain to all taxes administered by the tax commissioner as listed above. West Virginia Administrative Division No. 08-286 W, 01/08/2010.

23

o Successor Withholds Proceeds or Obtains Certificate. If the

business is purchased in an arms-length transaction, and if the purchaser withholds so much of the consideration for the purchase as will satisfy any tax, additions to tax, penalties and interest which may be due until the seller produces a receipt/certificate from the tax commissioner evidencing the payment thereof, the purchaser shall not be personally liable for any taxes attributable to the former owner of the business unless the contract of sale provides for the purchaser to be liable for some or all of such taxes. W. Va. Code § 11-10-11(f)(2) and WV Code of State Rules 110-15-4.9. Purchase price is not limited to cash transferred to the seller, but includes any consideration flowing directly or indirectly to the seller. WV Code of State Rules 110-15-4.9.7.

o Successor Defined. The term successor means any person who directly or indirectly purchases, acquires, or succeeds to the business or the stock of goods of any person quitting, selling, or otherwise disposing of a business or stock of goods. The purchase or acquisition of a business may give rise to successor liability whether the consideration is money, property, assumption of liabilities or cancellation of indebtedness. WV Code of State Rules 110-15-4.9.1.

o Includes Taxes Not Determined or Assessed at Date of Purchase.

The liability of a successor includes taxes that are required by law to be paid prior to the sale or transfer of the business or stock of goods, even if the liability of the former owner is not determined at the time of the sale or transfer. If an audit conducted after the sale or transfer shows a deficiency for periods prior to the sale or transfer, the deficiency is a liability of the former owner and a liability of the successor. WV Code of State Rules 110-15-4.9.8.1. The liability may include any liability of the former owner for tax, interest, additions to tax, and penalties that is due and payable, and any such liability that is not due and payable because the former owner has not filed tax returns at the time required by law. The liability includes all taxes, penalties, interest, and additions to tax, whether assessed or unassessed against the former owner, without regard to whether a tax lien has been issued or perfected against the former owner. If any former owner is given a certificate from the Tax Department stating that no taxes are due from his former owner, then the successor shall only be liable for the tax liability of successors' former owner not covered by the said certificate.

o Liability Cannot Be Avoided by Contract. The liability of a successor is determined by law and cannot be avoided or altered by contracts or agreements between the former owner and successor. Thus, a contract or other agreement, providing that the purchaser, transferee, seller, or transferor is or is not responsible for the tax liability of the former owner, or that the former owner has no tax liability, does not alter the liability of the successor. WV Code of State Rules 110-15-4.9.10.

o Substantial Portion of Business. A person who purchases or

acquires a portion of a business or stock of goods may become liable as a successor where he purchases or acquires substantially all of the business assets or stock of goods of such business. If two or more

24

persons purchase or acquire a business or stock of goods, their liability as successor is in proportion to the value of the business assets or stock of goods acquired by each person. WV Code of State Rules 110-15-4.9.2.

o Business Assets. The business assets include all assets of a business

pertaining directly to the conduct of the business. Business assets include real property or any interest therein; tangible personal property, including fixtures, equipment, machinery, furniture and vehicles; and intangible property, including accounts receivable, contracts, business name, business goodwill, customer lists, delivery routes, patents, trademarks or copyrights. Any asset owned by a corporation is a business asset. “Stock of goods” means the inventory or merchandise that the taxpayer is in the business of selling, but does not include fixtures, equipment, machinery or vehicles used in connection with such business. WV Code of State Rules 110-15-4.9.3.

o Change in Business Form. The change in the form of a business

will generally give rise to successor liability. A change in the form of a business would include changes such as the incorporation of a sole proprietorship or partnership, the voluntary or involuntary dissolution of a corporation, the merger or consolidation of two or more corporations, the formation of a partnership from one or more sole proprietorships or corporations. WV Code of State Rules 110-15-4.9.5.

Change to LLC. A limited liability company’s sole managing

member merely changed the form of the business from corporation to an LLC, but otherwise operated the business in the same manner in virtually every respect. As a result, the LLC was liable for the corporation's unpaid assessments as the corporation's “successor” or “successor in business.” West Virginia Administrative Decision S 08-286 W, 01/06/2010 ; West Virginia Administrative Decision 08-287 C, 01/06/2010 .

o Creditors. If a business or stock of goods is voluntarily sold or

transferred to a creditor, and the creditor operates the business, the creditor is a successor. If the creditor does not operate the business or operates the business in liquidation with the sole purpose to recover its debt, the creditor is not a successor. WV Code of State Rules 110-15-4.9.6.1.

o Liability Not Limited By Purchase Price. The liability of a successor in business is not limited to the amount of purchase money, or consideration received by the former owner, unless the successor avoids liability or limits liability by one or more of the following methods. if the purchase of the business or stock of goods is an arms-length transaction, the purchaser may avoid any successor liability by requiring the seller to produce a receipt from the Tax Commissioner showing all taxes of the seller have been paid. If the purchase of a business is an arms-length transaction, the purchaser may limit successor liability by withholding enough of the purchase money to satisfy the tax liability of the seller. If the purchase or transfer of a business or stock of goods is not an arms-length transaction, the purchaser or transferee may avoid any successor liability by requiring

25

the seller or transferor to produce a receipt from the Tax Commissioner showing all taxes of the seller or transferor have been paid. WV Code of State Rules 110-15-4.9.9.

o Successor Liability Does Not Apply. Successor liability does not