mergers and acquisitions acquisitions fail acquiring companies: share prices of companies that...

TRANSCRIPT

1

Mergers and Acquisitions Overview

How do companies grow ?

74,000 acquisitions between 1996 and 2001 45,151 acquisitions between 2005 and 2008 In 2003 alone there were 8,385 acquisitions

2

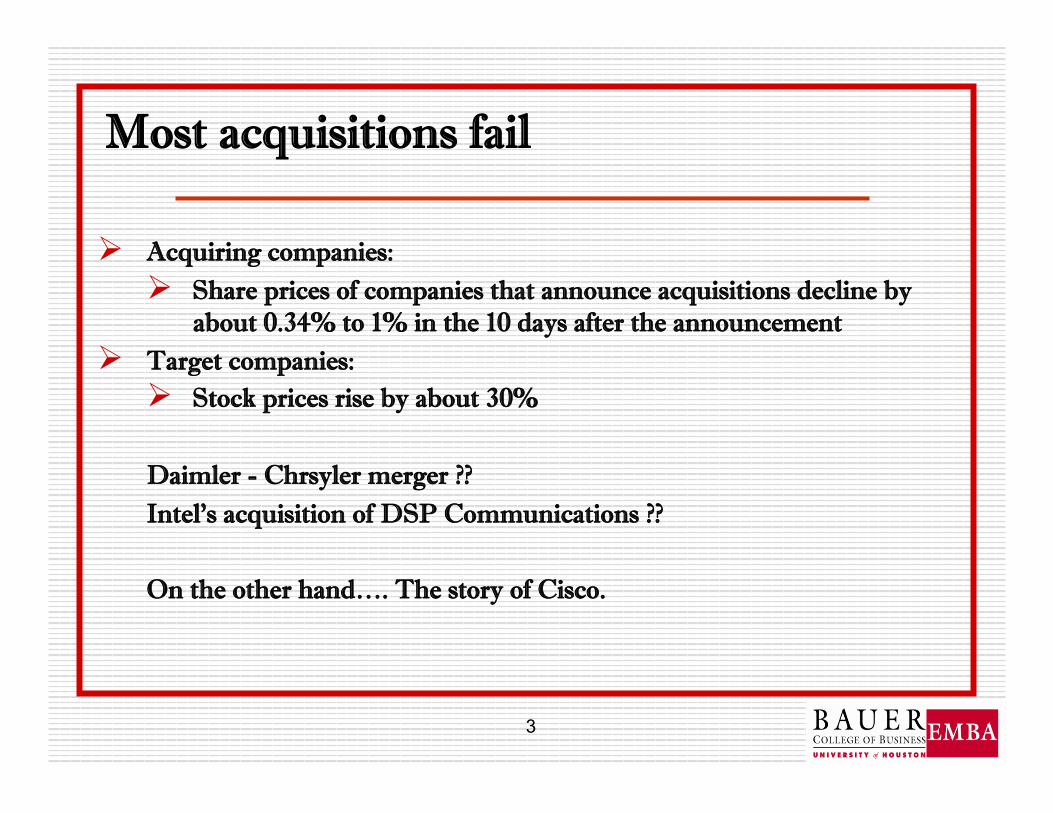

Most acquisitions fail

Acquiring companies: Share prices of companies that announce acquisitions decline by

about 0.34% to 1% in the 10 days after the announcement Target companies:

Stock prices rise by about 30%

Daimler - Chrsyler merger ?? Intel’s acquisition of DSP Communications ??

On the other hand…. The story of Cisco.

3

4

Mergers:

Absorption of one firm by another Acquiring firm buys all the assets, liabilities and franchises of

the acquired firm Acquired firm ceases to exist Stockholders of both firms must approve the merger

Example: In June 2006, Anadarko Petroleum Corp (AP) acquired all the outstanding common stock of Kerr-McGee Corp, an oil and gas exploration and production company, via tender offer, for $70.5 in cash per share or a total value of $16.087 bil. The transaction had been subject to shareholder and regulatory approvals.

Subsidiary Merger: Target company becomes a subsidiary or part of subsidiary of acquirer.

Example: In 2005, Targa Resources Inc (TR), an entity backed by EM Warburg Pincus LLC, acquired the midstream natural gas business of Dynegy Inc, a wholesaler of natural gas products, for $2.445 bil in cash. The transaction was subject to regulatory approval.

5

Consolidation: Merger results in a new corporation.

Exxon and Mobil

6

Takeovers

Acquisitions

Proxy Control

Going Private

Merger or Consolidation

Acquisition of Stock

Acquisition of Assets

Proxy

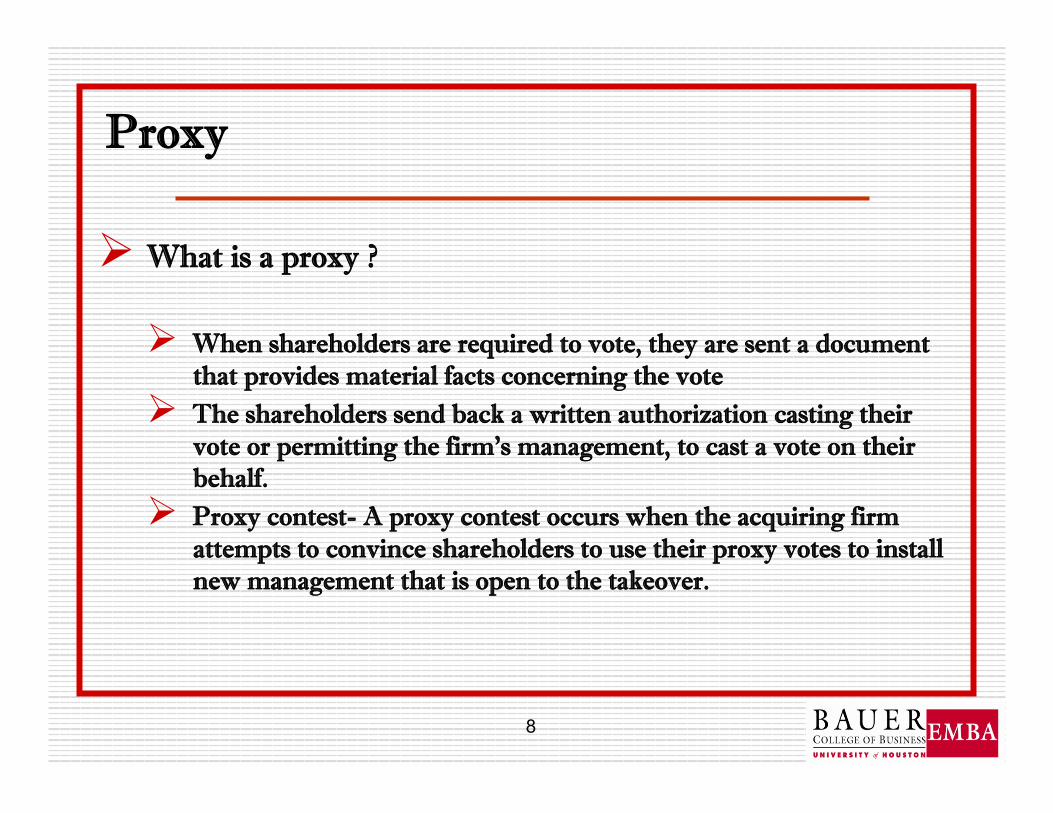

What is a proxy ?

When shareholders are required to vote, they are sent a document that provides material facts concerning the vote

The shareholders send back a written authorization casting their vote or permitting the firm's management, to cast a vote on their behalf.

Proxy contest- A proxy contest occurs when the acquiring firm attempts to convince shareholders to use their proxy votes to install new management that is open to the takeover.

8

9

Types of Mergers

Horizontal Mergers: Combination of erstwhile competitors (e.g., Exxon + Mobil = Exxon Mobil)--- greatest scrutiny from FTC.

Vertical Mergers: Combination of upstream and downstream companies (e.g., Merck + Medco).

Conglomerate Mergers: Mergers across industries (or industry segments) (e.g., Phillip Morris + Kraft)

Acquisition

Acquisition of stock: Example: US – In 2005 Norsk Hydro ASA acquired all the

outstanding common stock of Spinnaker Exploration Co, a provider of oil and gas exploration and production services, for $65.5 in cash per share, or a total value of $2.448 bil. The largest seller in the transaction was Warburg Pincus Ventures. The transaction was subject to customary conditions and regulatory approvals.

Purchase the firm’s voting stock in exchange for cash, shares or other securities Tender offers

Public offer to buy shares of a target firm Public announcements General mailings

10

Acquisition of assets:

Example: Eni SpA, through its Eni Petroleum Co unit, acquired the production, development and exploration assets, located in the Gulf of Mexico, of Dominion Resources Inc, an electric and gas utility and holding company, for $4.757 bil. The transaction had been subject to regulatory approvals.

Example: US - Norway state-owned StatoilHydro ASA acquired a 32.5% stake in Marcellus shale property (MS) of Chesapeake Energy Corp (CE), an oil and gas exploration and production company, for $3.375 bil. On completion, MS was operated as a joint venture. Originally, in September 2008, CE announced that it was seeking a buyer for its undisclosed minority stake in its MS unit.

11

Leveraged Buy-Out (LBO)

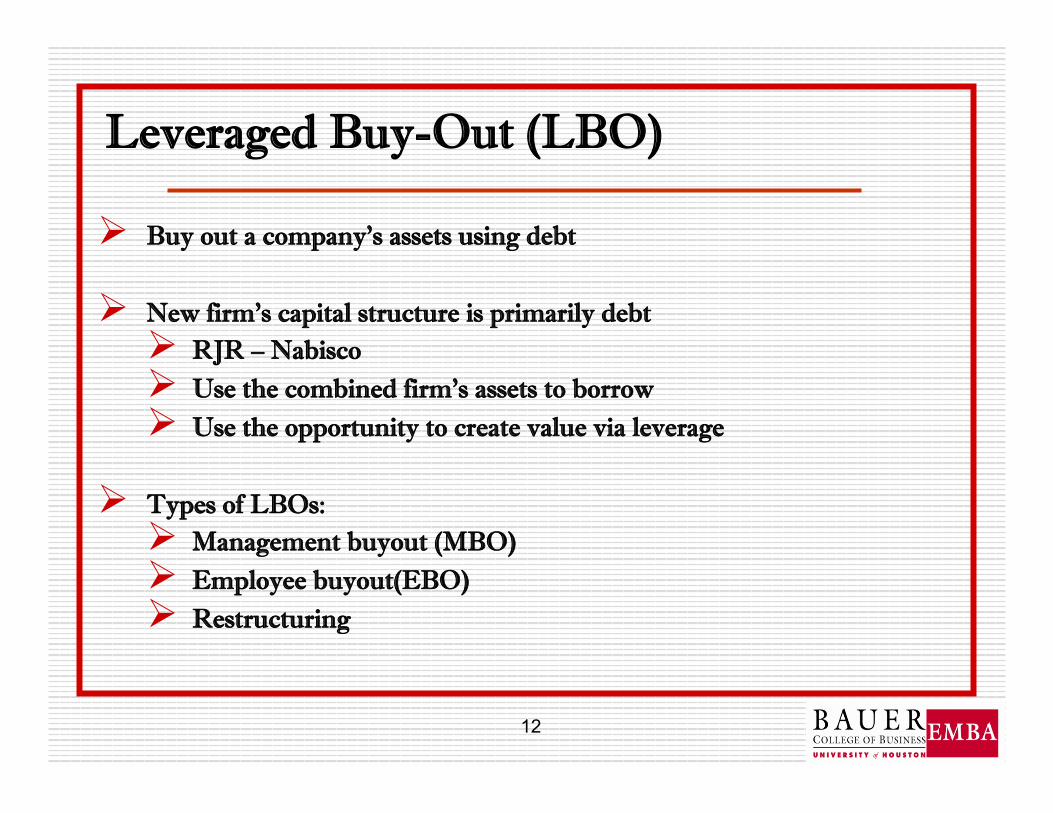

Buy out a company’s assets using debt

New firm’s capital structure is primarily debt RJR – Nabisco Use the combined firm’s assets to borrow Use the opportunity to create value via leverage

Types of LBOs: Management buyout (MBO) Employee buyout(EBO) Restructuring

12

13

Reasons for M&A

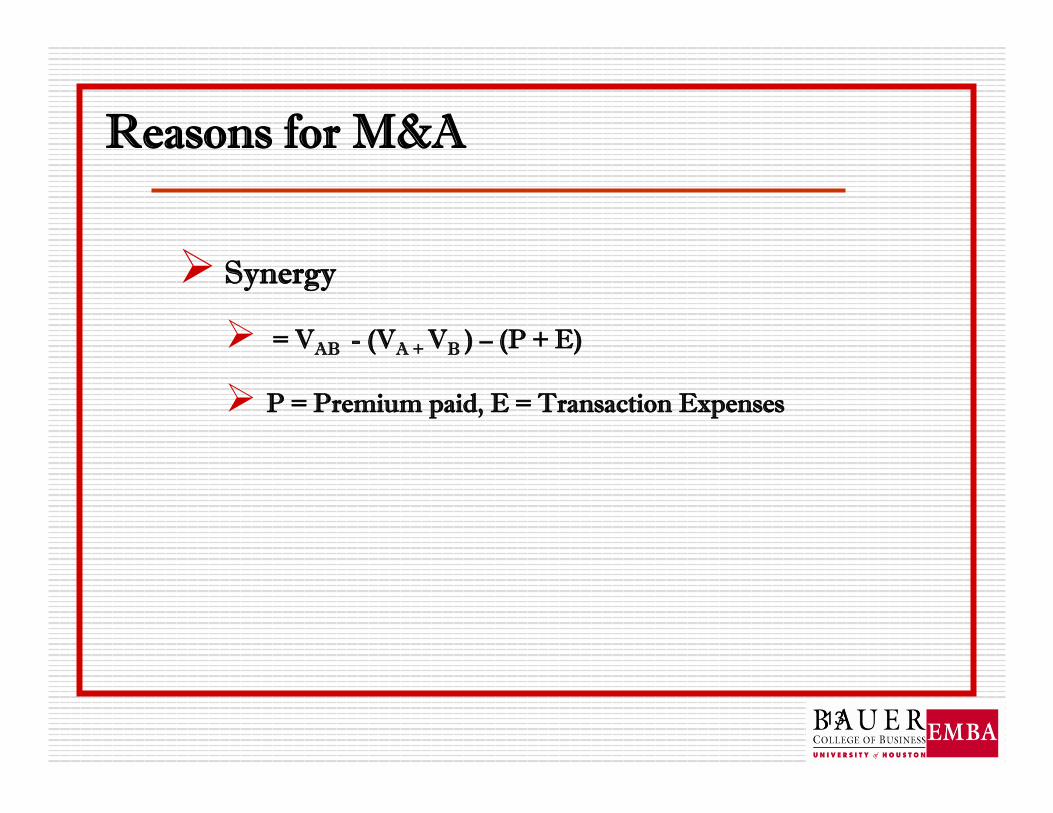

Synergy

= VAB - (VA + VB ) – (P + E)

P = Premium paid, E = Transaction Expenses

Sources of Synergy

Strategic Benefits

Integration: Vertical or horizontal

Expansion

DuPont – Conoco merger – supply of oil for DuPont P&G’s acquisition of Charmin Paper – integrate paper products GE – Hughes aircraft merger – technology transfer Phillips and Getty Oil – led to more efficient management being put

in place HP- Compaq merger was driven by the goal of reducing

redundancies in resources

14

Tax Gains

In the U.S. tax law permits tax loss carryforwards A firms with NOL this year can get refunds of income taxes paid in

the last 3 years This benefit can be carried forward for 15 years M&A can result in tax gains over and above this T1_tax_gains.xls

Diversification U.S. Steel’s acquisition of Marathon Oil

15

Strategic Planning for M&A Begins with a discussion between the board of directors and

management Elements to consider:

Internal: Mission and vision statements – XOM:

We are the world's largest publicly traded international oil and gas company, providing energy that helps underpin growing economies and improve living standards around the world…

We are committed to meeting the world's growing demand for energy in an economically, environmentally and socially responsible manner.

Core competencies and assets Culture

16

External elements: Business environment – scenarios Customers – product, price, service and quality Competitors Suppliers – contracts and bargaining power Alliances – affiliations with customers and suppliers

Checklist of items: Physical asset Financial assets Intellectual assets / Organizational assets Risks

17

18

Define Acquisition Objectives

Primary objectives:

Horizontal/vertical integration

Geographic expansion (regional/national/international)

Other

Other objectives/issues:

Accretive to earnings

Synergies

Form of consideration

Accounting, tax, legal and regulatory

Cultural (e.g., management and employees)

19

Candidate Investigation

Preparation Phase

Marketing Phase

Final Agreement

Phase

Valuation

Descriptive Memorandum

Candidate Analysis

Analysis of Proposal(s)

Candidate(s) Due Diligence

Selecting a Marketing Strategy

Approaching Potential Candidates

Solicitation of Proposals

Negotiations

Closing

Steps in the Sale Process

20

M&A Intermediaries

Business brokers

Accountants

Lawyers

Consultants

Business valuation firms

Commercial banks

Investment banks

21

Financial Advisory Services Sale Engagement

Value company

Assist in selecting sale strategy

Assist in identifying potential purchasers

Contact potential purchasers

Assist in evaluating offers

Assist in responding to offers

Assist in negotiations with potential purchasers

Assist in negotiating ancillary agreements

Fairness Opinion

22

Financing the Acquisition

Financing sources:

Internal Capital

Private placements of debt or equity

Public offerings of debt or equity

Seller notes

23

Due Diligence

Due diligence is the process of identifying and confirming or disconfirming the business reasons for the proposed M&A transaction.

Several functions are involved in due diligence: Strategy, finance, legal, marketing, operations, human resources, and internal audit services.

24

The Due Diligence Process

Interview management

Collect company/industry information

Understand drivers of business

Build financial models

Valuation

Assessment of post-Acquisition Operation Plans

Why Due Diligence ?

Guard against the Winner’s Curse:

Groucho Marx:

“I would never join a club that would have me for a member.”

Woody Allen (paraphrase):

“I would never marry a woman who would accept me as a husband..”

M&A Analogy:

“I will not do an acquisition that other potential buyers have passed on.”

25

26

Most major sales and acquisitions (especially in energy) either implicitly or explicitly involve auctions.

The winners curse says that in an auction, since the most optimistic bidder usually wins, the winning bidder tends to be overly optimistic and may thus overvalue the auctioned property.

27

A rigorous due diligence in valuation (and financing) is needed to allow management to account for the winners curse.

In other words, management must ask,

“How big must be the shareholder value-add from the acquisition, before it makes sense to take the investment?”

Target firms resistance

Provisions in the corporate charter: Boards – classified vs not Voting – supermajority vs not

Golden Parachutes

Poison pills Peoplesoft (PS)’s poison pill (2005)–

Once a bidder acquired 20% of their shares, all shareholders except the acquirer could buy more shares from the corporation at half price.

PS had 400 million shares outstanding so if a bidder acquired 80 million shares, each existing shareholder (except the bider) could buy 16 more shares for every share held

28

If all shareholders exercised the right PS would have to issue 0.8 x 400 x 16 = 5.12 billion shares

The total number of shares outstanding = 5.12 +0.4 = 5.52 illion Stock price would drop to half because the existing shareholders can

buy at half price Hence the bidder’s proportion of the firm’s onwership will drop to 80

million / 5.52 billion = 1.45% Greenmail

In 1986 Ashland Oil Ince, a large independent oil refiner had 28 million shares outstanding. The firm’s share price closed at 49.75 on April 1, 1986. On April 2, the board decided to buy 2.6 million shares from the Belzberg family of Canada so as to prevent the family from taking over the firm. The same day, the board also authorized the firm to repurchase 7.5 million shares and to set up an ESOP funded with 5.3 million shares.

29

Regulatory considerations Antitrust: Some businesses need clearance from the Federal Trade

Commission or the Dept of Justice (DOJ) Hart-Scott-Rodino (HSR) Act of 1976

Parties to a transaction are required to furnish certain information about themselves to the FTC and the DOJ

Information on the nature of the business and the revenues based on the industry classification of the firms

This information is used to determine if the deal could unleash anticompetitive forces

Some mergers are exempt from the HSR Act (small asset size, little voting control)

Horizontal mergers – use the Herfindahl-Hirschman Index (HHI) to determine postmerger share of the new entity

30

Planning is important… While planning may take up only 20% of the M&A process it requires

80% of the energy involved Strategic planning:

Hiring the right advisors Doing the research Studying the regulatory factors

31

Global Environment of Business

Case discussion:

HBR article – The Dubious Logic of Global Megamergers (Ghemawat and Ghadar)

32