mergers and acquisitions involving the eu banking … · ecb mergers and acquisitions involving the...

TRANSCRIPT

MERGERS AND ACQUISITIONSINVOLVING THE EU BANKING

INDUSTRY � FACTS ANDIMPLICATIONS

December 2000

MERGERS AND ACQUISITIONSINVOLVING THE EU BANKING

INDUSTRY � FACTS ANDIMPLICATIONS

December 2000

© European Central Bank, 2000

Address Kaiserstrasse 29

D-60311 Frankfurt am Main

Germany

Postal address Postfach 16 03 19

D-60066 Frankfurt am Main

Germany

Telephone +49 69 1344 0

Internet http://www.ecb.int

Fax +49 69 1344 6000

Telex 411 144 ecb d

All rights reserved.

Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

ISBN 92-9181-133-5

ECB Mergers and acquisitions involving the EU banking industry � December 2000 3

Contents

Executive summary 5

Introduction 8

1 M&As involving European credit institutions � what happens? 91.1 Bank M&As 101.2 Development of financial conglomerates 131.3 Implications for concentration and capacity 16

2 The rationale for M&As � why do they occur? 192.1 Headlines from empirical literature on scale and

scope economies 192.2 Views expressed by the industry in the EU 202.3 The economic literature versus the views expressed

in the industry 22

3 The way M&As are carried out � how do they happen? 233.1 M&As from the credit institution perspective 233.2 M&As from an authority perspective 26

3.2.1 Mergers and acquisitions � what is assessed? 263.2.2 Exchange of information � who is the assessor? 273.2.3 Roles of the �home� and the �host� supervisor16 29

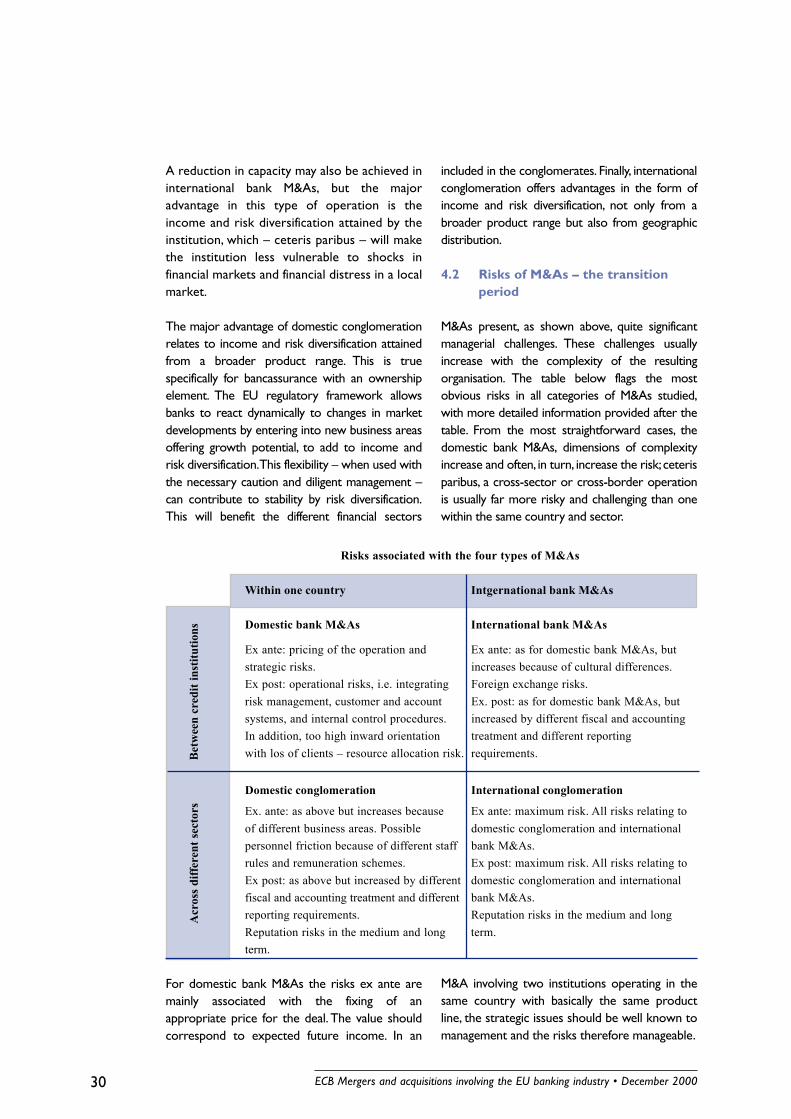

4 Implications of M&As for the institutions involved 294.1 Advantages for the institutions and the sector as a whole 294.2 Risks of M&As � the transition period 30

5 Implications for supervisors 32

Annex 1: Definitions and tables 34

List of tables: 35

ECB Mergers and acquisitions involving the EU banking industry � December 20004

The following country abbreviations are used in the report:

AT AustriaBE BelgiumDE GermanyDK DenmarkES SpainFI FinlandFR FranceGR GreeceIE IrelandIT ItalyLU LuxembourgNL NetherlandsPT PortugalSE SwedenUK United KingdomUS United States

ECB Mergers and acquisitions involving the EU banking industry � December 2000 5

Executive summary

This report � prepared by the BankingSupervision Committee of the EuropeanSystem of Central Banks � investigatesmergers and acquisitions (M&As) in the EUover the past five years.1 It looks into thedevelopment of corporate structures inbanking, including, where relevant,bancassurance. The analysis addresses therationale of M&As, the way in which they havebeen achieved � inter alia, against thebackground of the European legal framework �and their implications in terms of short andlong-term advantages and risks for EU banks.Finally, the implications for supervisors aretouched upon.2

Four different types of M&As have beendistinguished in this report: domestic andinternational bank M&As and M&As leading todomestic and international conglomeration. Thebulk of M&A activity carried out in the EUinvolves domestic bank M&As and, among these,M&As between smaller institutions. It isnoteworthy that most operations (around 80%)were concentrated in four Member States (DE,IT, FR and AT) during the observation period.The evolution in the number of M&As duringthe observation period shows a clear increasein 1998 and 1999 compared with the threeprevious years and there is information tosuggest that the values involved in M&As areincreasing, indicating the involvement of largerinstitutions. This trend is supported by externaldata sources as well.

Another noteworthy feature is that, according tothe number of transactions (little value-basedinformation is available to measure the size ofacquisitions abroad), international bank M&As aremore often carried out outside the EuropeanEconomic Area (EEA) than within it. EEA banksseem to seek profits by expansion into emergingmarkets. The fact may also hint that for somebanking activities the relevant market is the worldmore than the EEA (e.g. asset management).Banking and conglomeration-related M&As withinthe EEA have often been aimed at the creation ofregional groups. Fortis, Dexia andMeritaNordbanken are good examples of this kind

of operation. Over the observation period, there islittle evidence of a trend towards cross-borderM&As within the EEA, EU or euro area. It seemsthat in many countries banking groups have firstsought to consolidate their position withinnational borders before making a strategic moveto respond further to the creation of the singlemarket and the introduction of the single currency.This view needs to be differentiated somewhat,since there are specific developments in individualcountries or regions. For instance, in some of thesmaller Member States the process of industryconcentration and consolidation seems to havetaken place at a faster pace and earlier than insome of the larger Member States.

Conglomeration (i.e. the process leading to thecreation of groups of financial companies operatingin different sectors of the financial industry) hasalso been observed. This partly reflects, however, awide notion of financial conglomerate adopted inthe report that includes also structures with alimited degree of integration (as for instance in thecase of a large bank acquiring a small insurancecompany). Against this background, it is noted thatbanks have most actively been expanding into thebusinesses of investment management and assetmanagement and often through investments toestablish new enterprises. M&As have, however,become more important in recent years in theformation of complex groups. The development offinancial conglomerates combining banking and(life) insurance has also been found to exist inmost Member States. The report shows that theprocess of conglomeration is predominantly bank-driven. In most conglomerates banking assets andrevenue from banking dominate, but there are alsoexamples of insurance-dominated groups.

An increase in concentration, particularly forlarge countries, is observed in the referenceperiod. The increase is linked to the M&As thathave been observed in these countries. A certainrelationship seems to exist between the size ofthe country, concentration and M&A activity. The

1 The observation period for this report is from 1995 to the firsthalf of 2000 (inclusive).

2 The analysis is based on data collected from EU central banksand supervisory authorities. Given that the data have not beengathered on the basis of an agreed statistical framework, butrather as an ad hoc exercise to serve as information for thisreport, they should be interpreted with due caution.

ECB Mergers and acquisitions involving the EU banking industry � December 20006

relationship is that smaller countries tend to havehigh concentration ratios (measured by both theHerfindahl indicator or by way of comparing thetotal assets (or alternatively loans/deposits) ofthe five largest banks with total banking assets)and M&A activity tends to be lower in highlyconcentrated markets. No evident link betweenM&As and capacity indicators was found.

With regard to the rationale for M&As, there isa need to differentiate according to the type ofM&A, the size of the institutions involved and, incase of a cross-border operation, the �targetregion�. Small bank M&As are mostly beingcarried out for cost efficiency reasons(economies of scale) and to achieve a size thatallows survival; for the sector as a whole theycarry the advantage of mopping up excesscapacity. Larger bank M&As often have anelement of strategic re-positioning and, likesmall bank M&As, are driven by considerationsof economies of scale. Conglomeration isintended to diversify the risks and to smoothincome volatility. There are also benefits ofcombining banking and life insurance business inthe linking of enterprises with predominantlyshort-term liabilities and long-term assets(banks) with enterprises that have an inverseterm transformation (insurance). Theoptimisation of the use of different distributionnetworks is identified as a further motivationfor the creation of bancassurance groups. Onoccasion, the operations are also targeted at theacquisition of technological or other skills.

As regards the way M&As are being carried out,the more interesting observations relate to cross-sector and cross-country operations. There, atendency was observed for M&As to result first ina relatively complicated structure that is latersimplified and streamlined. The initial complicatedstructure proposed in connection with M&As isinfluenced by the need to obtain approval frommanagement and owners, or by other specificreasons (e.g. taxation). For more complex groups aholding structure is often chosen. Supervisors areactively involved in the M&A process including theauthorisation stage. There is a well-definedframework of legislation that ensures completeinformation to the supervisory authority on theparties involved, the envisaged structures and

business plans. EU legislation foresees a notificationprocedure in the case of the acquisitionof participations in EU-regulated financialenterprises (credit institutions, investment firms,investment management companies and insuranceundertakings) that exceed thresholds. Accordingto EU legislation, the competent authorities have aright to veto the operation if, in view of the needto ensure sound and prudent management ofthe institution, they are not satisfied as to thesuitability of the acquirer or as to the transparencyof the new group.

For the enterprises involved in M&As, anumber of risks arise during the transitionperiod, i.e. immediately before and after theM&A. Generally, risks related to M&As increasewith the complexity of the operation: a�simple� domestic bank merger is at the lowerend of the transition risk spectrum comparedwith a large-scale cross-border operation.Supervisory authorities have pointed to avariety of operational issues that needattention and monitoring during M&As,including the operational risks that stem fromthe integration of risk management, customerand accounting systems � both the proceduresand the information technology basis � and theadaptation of control procedures.

Turning a merger or acquisition into a successmay be difficult owing to the challenges inherentin virtually all fields of management of a financialservice enterprise. Dealing with culturaldifferences among staff or lines of business or, inthe case of cross-border or cross-sector M&As,differences in regulatory and accountingsystems, requires high-level skills and significantresources. There is also the risk of loss of keystaff and/or clients. It may be on account of theabove risks that �friendly� M&As are morecommon than hostile takeovers in the financialservices sector. Acquisitions with the objectiveof increasing efficiency and achieving cost savingsmay risk being less successful than anticipated,owing to the complexity of the operation(including risks of personal or cultural clashes)or to other reasons such as labour marketrigidities. All above has led many observers toconclude that M&As are far from always�successful�.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 7

M&As have positive implications for theindustry involved. As such they are anindication that the industry is responding andadapting to pressures for change. Thepossibility of a takeover can exert a healthyincentive for managers to optimise theefficiency and service of the enterprise andhence enhance the shareholder value. Internalstructures and corporate governance offinancial institutions in the M&A process alsorequire careful consideration on the part ofsupervisors, who will wish to ensure aneffective internal organisation and allow for theensuing group to be adequately supervised.

With regard to the implications for prudentialregulation and supervision, a continuedmonitoring of rules, regulations and practices isimportant to ensure that an adequateframework is in place for a level playing-fieldbetween financial institutions from differentsectors of the industry and between differentMember States. The current framework for�home� and �host� country supervision workswell. Continued monitoring can eliminate unduesupervisory arbitrage. Work is under way in EUpolicy-making and at the wider internationallevel to develop further prudential regulation offinancial conglomerates.

The existence and anticipated furtherdevelopment of financial conglomerates (alsocross-border) calls for closer supervisory co-

operation. Already the current EU legislationprovides for a close co-operation betweensupervisors. A network of memoranda ofunderstanding of different types � both at thedomestic and the international level � is in placein order to cater for such co-operation.

The risk of contagion � shocks to one part of agroup endangering the group as a whole � is anissue raised in relation to financialconglomerates, for instance bancassurancegroups. Contagion might increase the cost ofrescue operations for deposit guaranteeschemes offered to depositors of banks incountries where financial conglomerates exist.In this context, contagion risk will notnecessarily lead to regulatory conflicts; ifregulators of banking and insurance businesswork together, a co-operative solution can befound. Supervisors already co-operate to limitthe way in which risks may spread, i.e. throughthe setting of limits on large exposures andintra-group exposures and awareness that aholding company structure might be beneficialin this context.

The report also points to a need for continuedmonitoring of capital adequacy, which is typicallyaffected by M&As. The effect on capital adequacyis likely to be highest in acquisitions, wherepayment to shareholders in the acquired entitycan be effected by way of cash or other means,often shares.

ECB Mergers and acquisitions involving the EU banking industry � December 20008

Introduction

This report describes mergers and acquisitions(M&As) involving the European banking sectorover the past five years and has been preparedby the Banking Supervision Committee (BSC)3

in the context of the task of the Eurosystem tocontribute to the smooth conduct of policiespursued by the competent authorities relatingto prudential supervision of credit institutionsand the stability of the financial system (Article105 (5) of the Treaty establishing the EuropeanCommunity). The questions �what� happened,�why� and �how� did it happen, and what arethe implications, are discussed. In this context,the phenomenon of �bancassurance� is givenparticular attention. The analysis was based onquantitative and qualitative information fromcentral banks and banking supervisoryauthorities relating to the years 1995 to 2000(including the second quarter).

M&As within the financial industry arecurrently widely discussed in the media andacademia. This may be because they involvelarge European institutions, are cross-borderor cross-sector, and involve, in particular,insurance or asset management activities. Thecontext, scope and purpose of M&As seem tohave changed in recent years.

M&As are not confined to the banking industry.They take place also in other industries, like,for instance, the media and entertainmentsectors, the automobile industry, and thetelecommunication sector. Furthermore, thepursuit of development in electronicdistribution channels has led to alliances beingannounced between banking organisations, aswell as telecommunication, software andinternet companies; some alliances haveinvolved ownership elements.

Until the 1980s the financial industries in mostEU Member States operated in highly regulatedmarkets and government ownership played amore significant role. The market for corporatecontrol was less developed at that time. A biasexisted towards stability of ownershipstructures and cross-shareholdings in somecountries. At the same time, markets for

banking services were predominantly local bynature. All in all, the environment prevailinguntil the 1980s limited M&As as efficient waysto change the strategies of relevant players andthe structure of the market.

M&As within the financial services sector are,however, not a completely new phenomenon.In a number of EU countries, mergers tookplace years ago and at that time changed themarket structure to a large extent, due to thecreation of large national banks. The M&Asmostly involved institutions within the samesector of the financial industry, whereas therewas widespread discussion about, and anevolution towards, universal banks or financialgroups.

M&As are changing the structure of theEuropean banking sector. However, they arenot a driving force for change themselves.M&As are responses to the driving forces forchange and to changes in market structures.The driving forces have been identified inprevious reports by the Banking SupervisionCommittee. These include, for instance,information technology, disintermediation, andthe integration of international capital markets,where the creation of the single currency isespecially relevant in Europe.

This report is structured in five sections.Section 1 describes what has happened inrecent years by presenting the facts of M&Aactivity in the European banking sector,identifying � for EU Member States �differences and similarities in, for example,M&A activity domestically and abroad; M&As ofsmall or large institutions; and M&As leading tothe creation of financial conglomerates. Thesection also looks at concentration andcapacity indicators. Section 2 focuses on therationale for M&As � why they take place.Section 3 is devoted to the way M&As arecarried out. Section 3.1 deals with the

3 Other reports prepared by the BSC include �Possible effects ofEMU on the EU banking system in the medium to long term�,February 1999; �The effects of technology on the EU bankingsystem�, July 1999; �EU banks� income structure�, April 2000;and �Asset prices and banking stability�, April 2000. All reportsare available on the website of the European Central Bank(www.ecb.int).

ECB Mergers and acquisitions involving the EU banking industry � December 2000 9

management of M&As by the institutionsinvolved. Section 3.2 reviews the involvementof authorities in M&As, including the relevantEuropean legal framework. Section 4 discussesthe implications of M&As for banks in terms ofrisks and advantages for the whole sector.

Section 5 includes a review of implications forsupervisors. The report is accompanied by anannex, which provides a number of tables ondevelopments in the observation period anddefinitions applicable to the data presented inthe report and the annex.

1 M&As involving European credit institutions � what happens?

The M&A activity in Europe shows differentpatterns depending on the market sectors(mutual banks, publicly owned banks, savingsbanks), the size of the market and thus therelative size of the institutions by internationalcomparison. The EU countries have also, in thepast, experienced their own specific pace andhistory of banking system re-structuring.Before studying the recent developments,some of these patterns may be recalled sincethey can, to an extent, explain these recentdevelopments.

During the late 1980s and early 1990s arestructuring and concentration process tookplace in a number of smaller EU countries suchas NL and DK. This process led to the creationof large national institutions, ready to competein the Single Market or a regional part of it. Inthe early 1990s, in the wake of the Scandinavianbanking crisis, M&As to create large institutionstook place in SE and FI. The UK banks were notas small in international comparison, but a cycleof M&As also took place in the late 1980s andearly 1990s. In Spain, a similar process tookplace during the early nineties, involvingespecially savings banks. In the same period inmany countries privatisation efforts were

pursued, in the wake of which many publiclyowned banks were sold to private investors.Moreover, a tendency arose for institutions witha mutual ownership structure to �demutualise�;in some countries (such as the UK and IE and,to some extent, DK and DE) institutions (e.g.building societies and savings banks) that had amutual ownership organisation abandoned thisorganisational form and converted theircorporate ownership to other private legalforms. Both privatisation efforts and�demutualisation� have increased the scope forM&As by increasing the number of institutionsthat can legally participate in M&As.

Another pattern of M&As is characterised bygeographic expansion into emerging marketslike South-East Asia, central and easternEurope and Latin America. EU banks, to someextent, expanded into the emerging countrieswith which they had historical connections �e.g. IT, ES and PT into Latin America, whereasthe expansion into central and eastern Europewas more cautious.

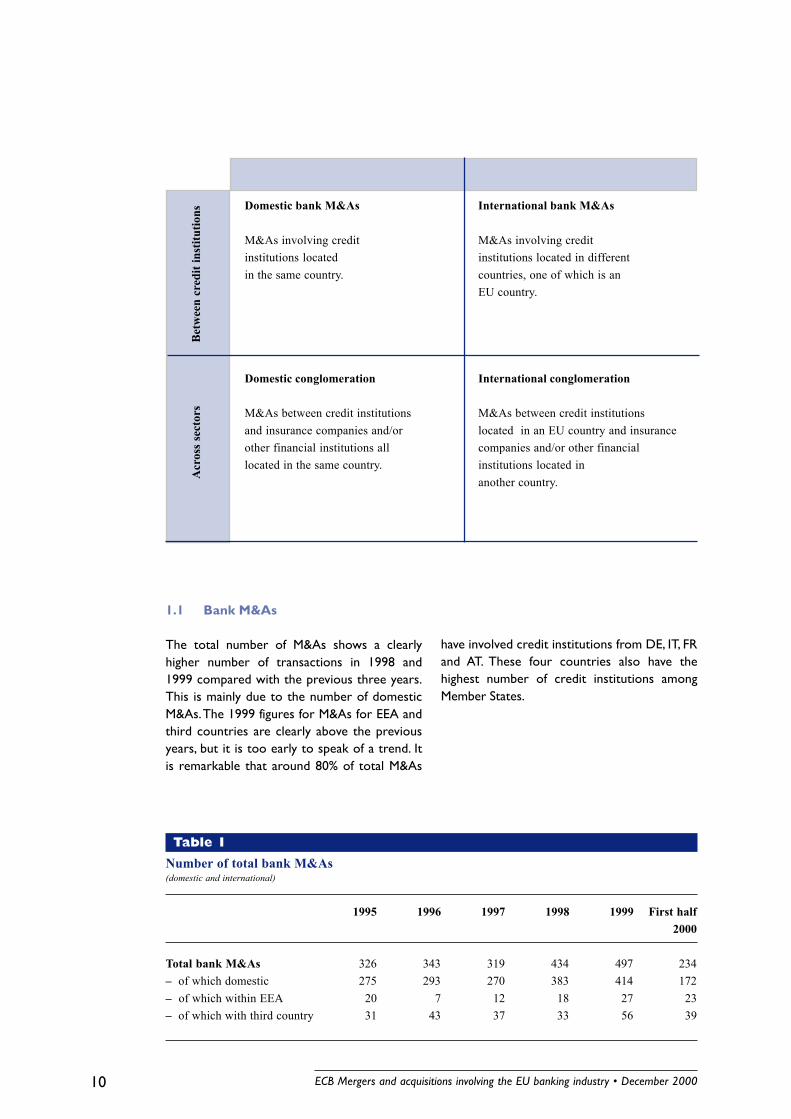

The analysis of M&As has been carried outfollowing, as a rule, a matrix capturing the industrysector and country dimensions as follows:

ECB Mergers and acquisitions involving the EU banking industry � December 200010

Within one country Across countries

Domestic bank M&As International bank M&As

M&As involving credit M&As involving creditinstitutions located institutions located in differentin the same country. countries, one of which is an

EU country.

Domestic conglomeration International conglomeration

M&As between credit institutions M&As between credit institutionsand insurance companies and/or located in an EU country and insuranceother financial institutions all companies and/or other financiallocated in the same country. institutions located in

another country.

Table 1

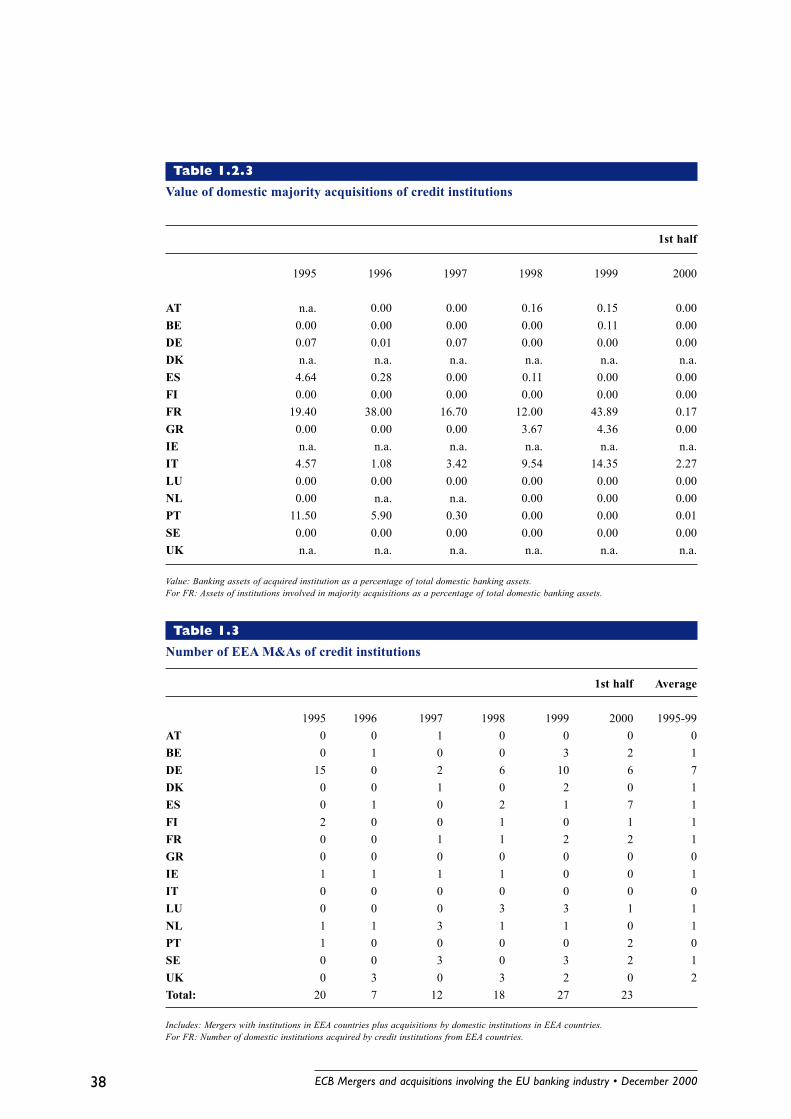

Number of total bank M&As(domestic and international)

1995 1996 1997 1998 1999 First half2000

Total bank M&As 326 343 319 434 497 234� of which domestic 275 293 270 383 414 172� of which within EEA 20 7 12 18 27 23� of which with third country 31 43 37 33 56 39

Acr

oss

sect

ors

Bet

wee

n cr

edit

inst

itutio

ns

1.1 Bank M&As

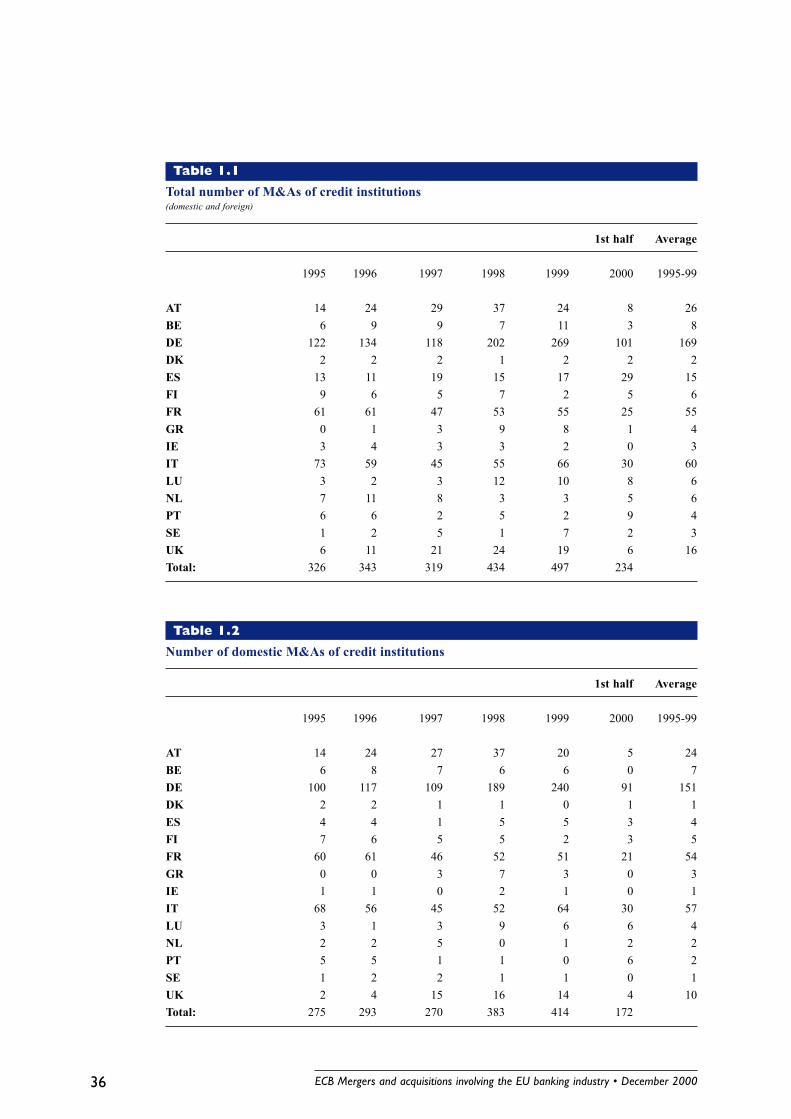

The total number of M&As shows a clearlyhigher number of transactions in 1998 and1999 compared with the previous three years.This is mainly due to the number of domesticM&As. The 1999 figures for M&As for EEA andthird countries are clearly above the previousyears, but it is too early to speak of a trend. Itis remarkable that around 80% of total M&As

have involved credit institutions from DE, IT, FRand AT. These four countries also have thehighest number of credit institutions amongMember States.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 11

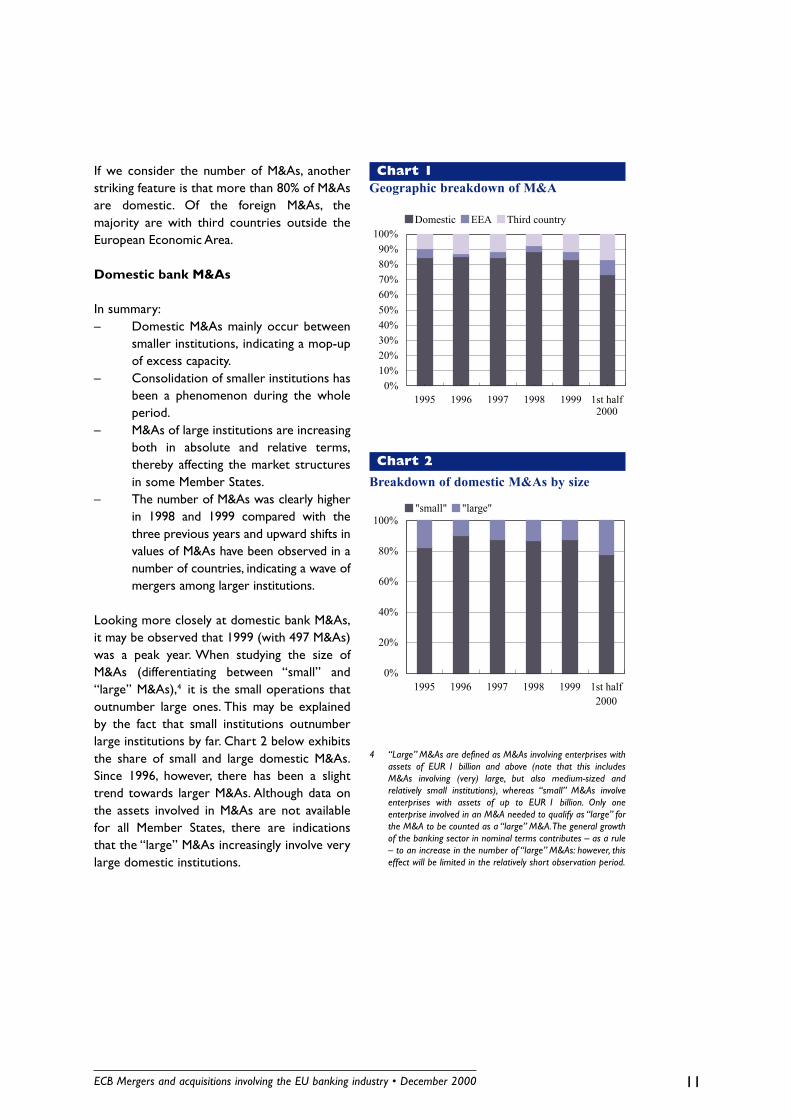

If we consider the number of M&As, anotherstriking feature is that more than 80% of M&Asare domestic. Of the foreign M&As, themajority are with third countries outside theEuropean Economic Area.

Domestic bank M&As

In summary:� Domestic M&As mainly occur between

smaller institutions, indicating a mop-upof excess capacity.

� Consolidation of smaller institutions hasbeen a phenomenon during the wholeperiod.

� M&As of large institutions are increasingboth in absolute and relative terms,thereby affecting the market structuresin some Member States.

� The number of M&As was clearly higherin 1998 and 1999 compared with thethree previous years and upward shifts invalues of M&As have been observed in anumber of countries, indicating a wave ofmergers among larger institutions.

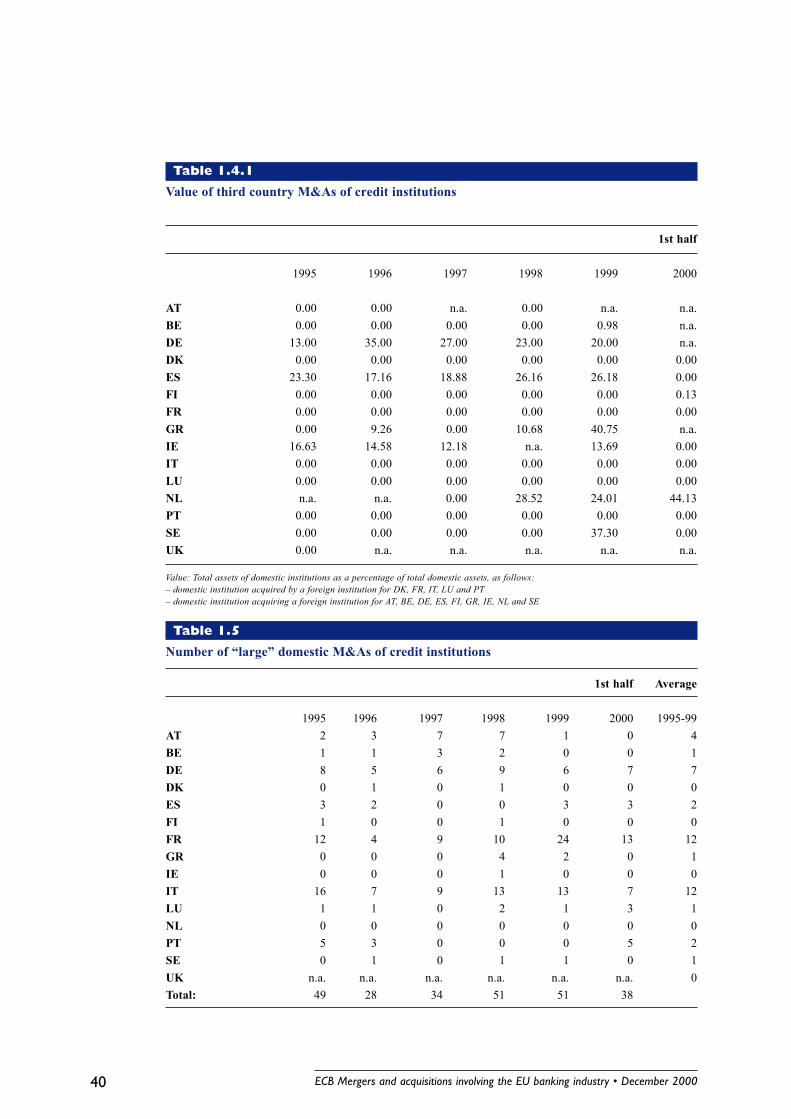

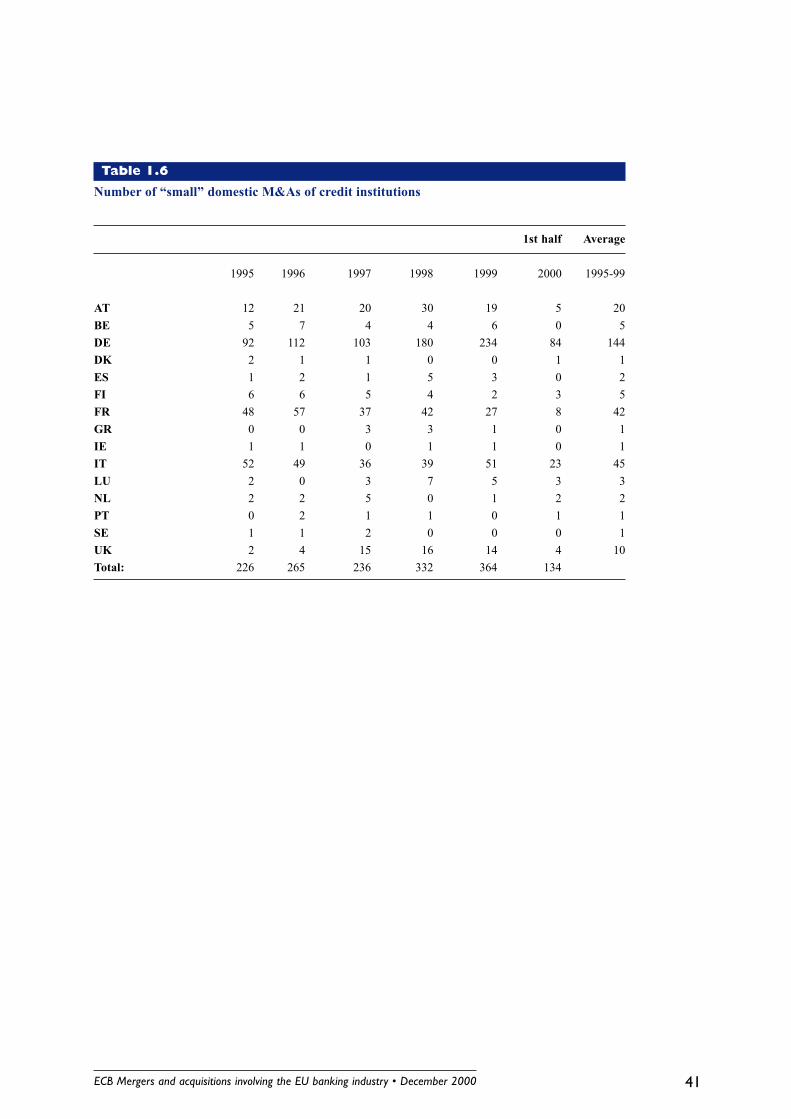

Looking more closely at domestic bank M&As,it may be observed that 1999 (with 497 M&As)was a peak year. When studying the size ofM&As (differentiating between �small� and�large� M&As),4 it is the small operations thatoutnumber large ones. This may be explainedby the fact that small institutions outnumberlarge institutions by far. Chart 2 below exhibitsthe share of small and large domestic M&As.Since 1996, however, there has been a slighttrend towards larger M&As. Although data onthe assets involved in M&As are not availablefor all Member States, there are indicationsthat the �large� M&As increasingly involve verylarge domestic institutions.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 1996 1997 1998 1999 1st half2000

Domestic EEA Third country

Chart 1Geographic breakdown of M&A

Chart 2

Breakdown of domestic M&As by size

0%

20%

40%

60%

80%

100%

1995 1996 1997 1998 1999 1st half

2000

"small" "large"

4 �Large� M&As are defined as M&As involving enterprises withassets of EUR 1 billion and above (note that this includesM&As involving (very) large, but also medium-sized andrelatively small institutions), whereas �small� M&As involveenterprises with assets of up to EUR 1 billion. Only oneenterprise involved in an M&A needed to qualify as �large� forthe M&A to be counted as a �large� M&A. The general growthof the banking sector in nominal terms contributes � as a rule� to an increase in the number of �large� M&As: however, thiseffect will be limited in the relatively short observation period.

ECB Mergers and acquisitions involving the EU banking industry � December 200012

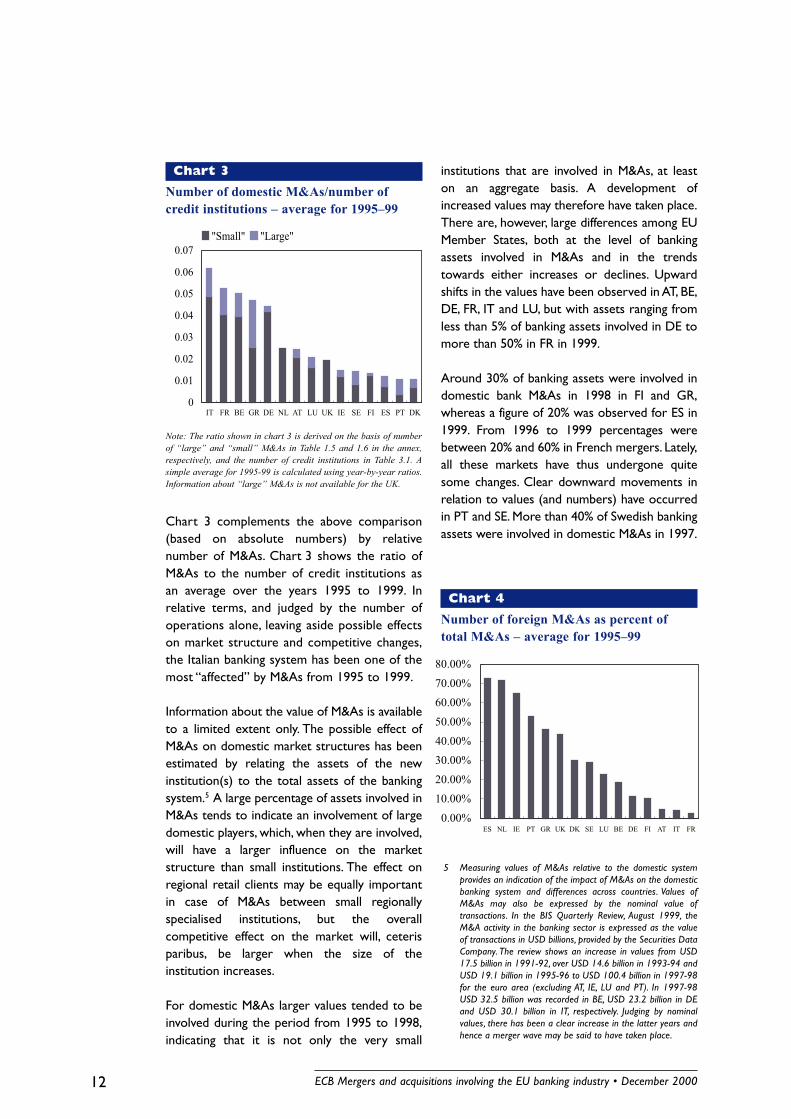

Chart 3 complements the above comparison(based on absolute numbers) by relativenumber of M&As. Chart 3 shows the ratio ofM&As to the number of credit institutions asan average over the years 1995 to 1999. Inrelative terms, and judged by the number ofoperations alone, leaving aside possible effectson market structure and competitive changes,the Italian banking system has been one of themost �affected� by M&As from 1995 to 1999.

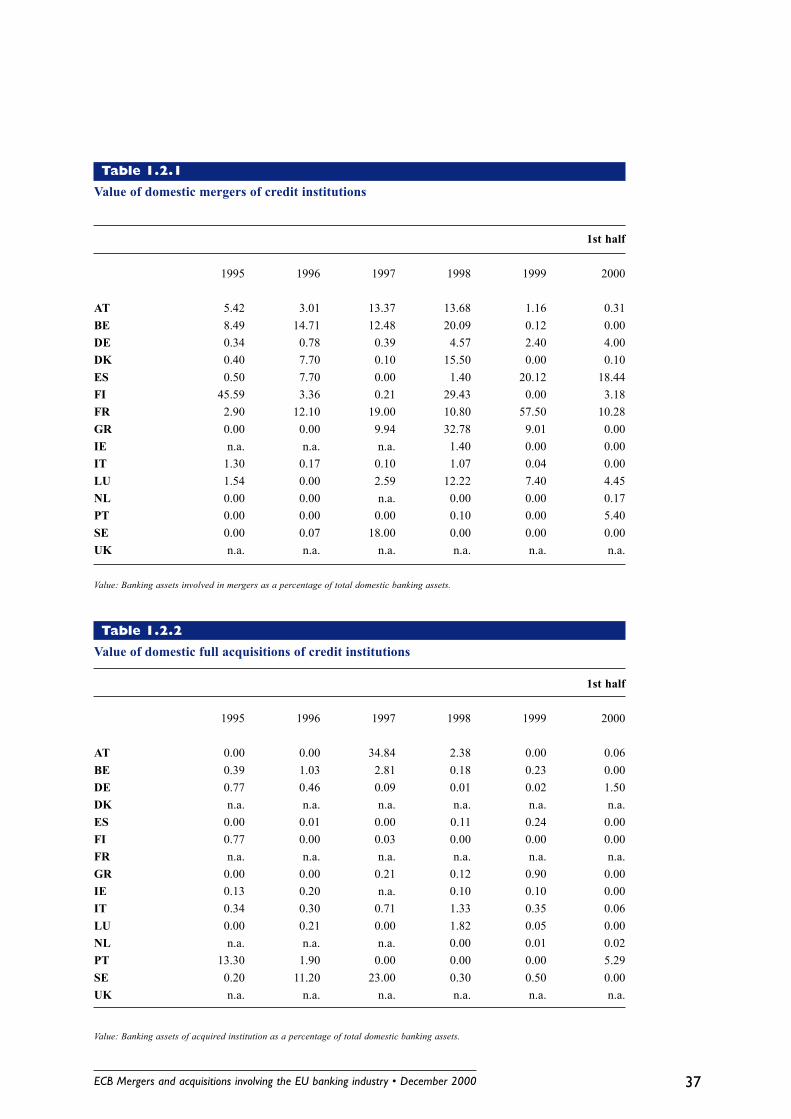

Information about the value of M&As is availableto a limited extent only. The possible effect ofM&As on domestic market structures has beenestimated by relating the assets of the newinstitution(s) to the total assets of the bankingsystem.5 A large percentage of assets involved inM&As tends to indicate an involvement of largedomestic players, which, when they are involved,will have a larger influence on the marketstructure than small institutions. The effect onregional retail clients may be equally importantin case of M&As between small regionallyspecialised institutions, but the overallcompetitive effect on the market will, ceterisparibus, be larger when the size of theinstitution increases.

For domestic M&As larger values tended to beinvolved during the period from 1995 to 1998,indicating that it is not only the very small

institutions that are involved in M&As, at leaston an aggregate basis. A development ofincreased values may therefore have taken place.There are, however, large differences among EUMember States, both at the level of bankingassets involved in M&As and in the trendstowards either increases or declines. Upwardshifts in the values have been observed in AT, BE,DE, FR, IT and LU, but with assets ranging fromless than 5% of banking assets involved in DE tomore than 50% in FR in 1999.

Around 30% of banking assets were involved indomestic bank M&As in 1998 in FI and GR,whereas a figure of 20% was observed for ES in1999. From 1996 to 1999 percentages werebetween 20% and 60% in French mergers. Lately,all these markets have thus undergone quitesome changes. Clear downward movements inrelation to values (and numbers) have occurredin PT and SE. More than 40% of Swedish bankingassets were involved in domestic M&As in 1997.

5 Measuring values of M&As relative to the domestic systemprovides an indication of the impact of M&As on the domesticbanking system and differences across countries. Values ofM&As may also be expressed by the nominal value oftransactions. In the BIS Quarterly Review, August 1999, theM&A activity in the banking sector is expressed as the valueof transactions in USD billions, provided by the Securities DataCompany. The review shows an increase in values from USD17.5 billion in 1991-92, over USD 14.6 billion in 1993-94 andUSD 19.1 billion in 1995-96 to USD 100.4 billion in 1997-98for the euro area (excluding AT, IE, LU and PT). In 1997-98USD 32.5 billion was recorded in BE, USD 23.2 billion in DEand USD 30.1 billion in IT, respectively. Judging by nominalvalues, there has been a clear increase in the latter years andhence a merger wave may be said to have taken place.

Chart 4

Number of foreign M&As as percent oftotal M&As � average for 1995�99

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

ES NL IE PT GR UK DK SE LU BE DE FI AT IT FR

Chart 3

Number of domestic M&As/number ofcredit institutions � average for 1995�99

"Small" "Large"

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

IT FR BE GR DE NL AT LU UK IE SE FI ES PT DK

Note: The ratio shown in chart 3 is derived on the basis of numberof �large� and �small� M&As in Table 1.5 and 1.6 in the annex,respectively, and the number of credit institutions in Table 3.1. Asimple average for 1995-99 is calculated using year-by-year ratios.Information about �large� M&As is not available for the UK.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 13

International bank M&As

In summary:� Far fewer international bank M&As have

taken place than domestic bank M&As.� Measured by number, international bank

M&As were mainly outside the EU area.

In absolute terms international bank M&Aactivity accounted for far fewer operationsthan domestic bank M&A activity in the EUduring the period from 1995 to 1998. M&Aswithin the EEA/EU and euro area seem to haveonly picked up recently. Chart 4 shows therelative importance of international bankM&As compared with total bank M&As. Theoperations were carried out by way ofacquisitions and not mergers. Acquisitions alsorepresent larger deals than mergers.

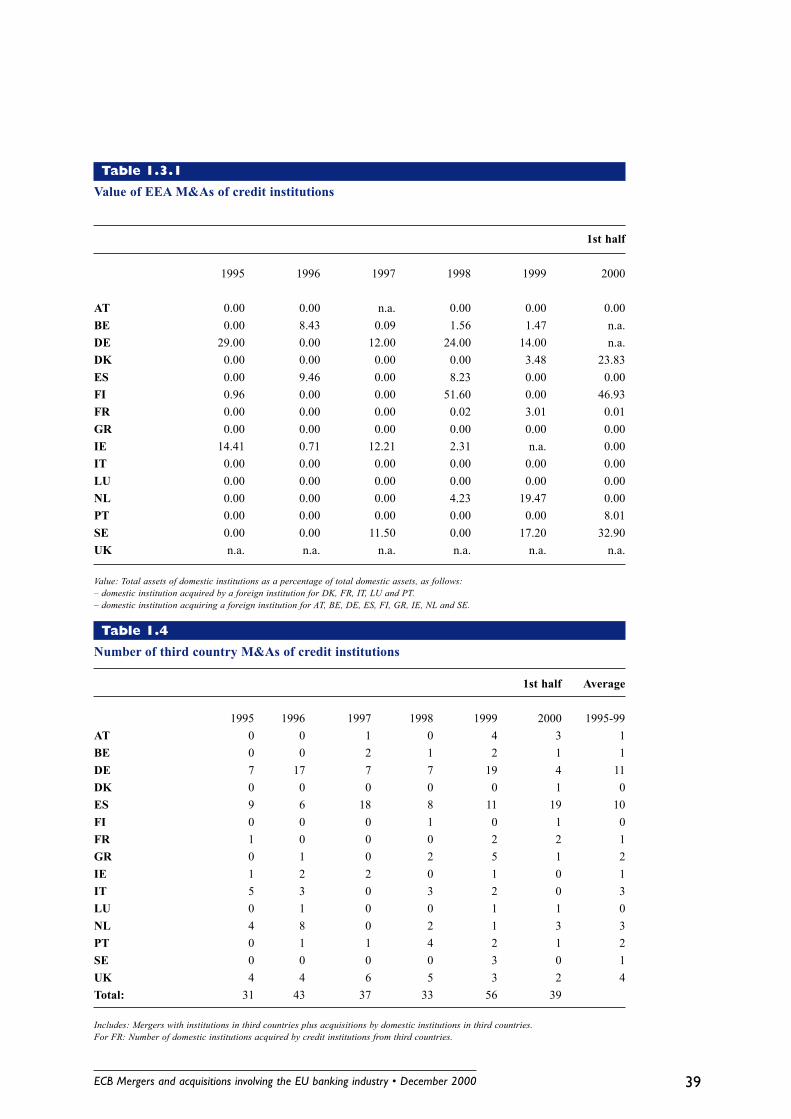

When comparing the direction of foreignacquisitions, third countries have, often in thesearch for markets offering higher margins, beenmore common targets for European banks overrecent years than other EEA countries.European banks have expanded into LatinAmerica (e.g. NL, ES, PT and IT), South-East Asia(e.g. NL) and central and eastern Europe (e.g.NL, IE). In some cases they have also expandedinto developed markets such as the US (i.e. DE).The size of the banks involved is increasing, as isthe importance of intra-EEA M&As.

With regard to the values of internationalM&As, whether within the EEA or with thirdcountries, even less information has beenavailable than on domestic M&As. Again, themeasurement is the outstanding amount ofdomestic assets involved in M&As. Thismeasurement does not provide informationabout the size of the third country institution,which might therefore be a small regional bankor a bank such as Bankers Trust (taken over byDeutsche Bank). As mentioned in connectionwith the analysis of numbers of M&As, there arefar fewer deals to observe internationally thandomestically, thereby limiting possibleinterpretations of trends on an aggregate level. Itshould be noted that singular large deals mayresult in very significant amounts of assets beinginvolved. For example, a deal like the creation of

MeritaNordbanken in 1998 involved almost50% of Finnish domestic banking assets.The holding company of MeritaNordbankenacquired Unidanmark in the first half of 2000.The latter deal was reflected in the Danishfigures (as an acquired institution) as well as inboth the Finnish and the Swedish figures (as aninstitution acquiring an EEA institution). In DE29% of banking assets were involved in EEAacquisitions in 1995 and between 12% and 24%from the beginning of 1997 to 1999. Elsewhere,M&As within the EEA have involved bankingassets of almost 10% in ES in 1996 and morethan 10% in IE in 1995 and 1997.

As for M&As with institutions located in thirdcountries, which have outnumbered M&Aswithin the EEA, ES is an important and stableinvestor, and between 17% and 26% ofdomestic banking assets were involved duringthe whole period under observation. The largebanks in DE have also expanded into thirdcountries and between 13% and 35% of assetswere involved during the observation period.In 1995-97 and the first half of 1999 more than10% of Irish banking assets were also involvedin third country acquisitions, whereas theDutch banks entered into international bankM&As with between 24% and 44% of Dutchbanking assets from 1998.

1.2 Development of financialconglomerates

M&As leading to the establishment of a financialconglomerate are qualitatively different frompure banking M&As, since they lead to thecreation of a group which is active in differentsectors of the financial industry. The largest and/or �leading� company in a conglomerate may be acredit institution, an insurance company, a holdingcompany or another financial institution.6

Financial conglomerates may be created by wayof M&As or by a financial institution setting up acompany in another sector, e.g. a bank setting upan insurance company to expand into theinsurance sector. The creation of a financialconglomerate is not the only way of offeringfinancial services of different character in a jointly

6 See the annex for definitions.

ECB Mergers and acquisitions involving the EU banking industry � December 200014

organised way. Co-operation agreementsbetween, for instance, a bank and an insurancecompany may achieve similar results. Such co-operation agreements are common in manyMember States. They are often found to beprecursors for integration involving ownershipelements.

Akin to but different from conglomeration is theestablishment of jointly owned enterprises offeringspecialised financial services. In some MemberStates savings banks and co-operative banks haveset up such jointly owned enterprises that provideasset management, stock-broking and settlementactivities as well as insurance, all of which are soldto or distributed by the member institutions ofthe sector. An example would be the jointly ownedinvestment management firm of the savings banksector in a country. In economic terms, such jointlyowned enterprises provide equal opportunities ofmarketing and servicing as financial conglomerates.The development of such enterprises as well asco-operation agreements is common, e.g. incountries such as AT and DE, with specific sub-sectors of the banking industry involved, e.g.savings banks and co-operative banks.

Both alternative forms of provision of whole-range financial services should be borne inmind when considering the process ofconglomeration as described below. Thealternative forms have not been captured inthe data on conglomeration considered below.Generally, caution is important whenconsidering and interpreting data onconglomeration. They have been collected froma banking supervisory perspective andtherefore some M&A activities involving othersectors might have been omitted. Furthermore,data have not been available in all MemberStates and a broad definition of financialconglomerates (a group of financial companiesoperating in different sectors of the financialindustry) has been used to capture structuralchanges in the financial landscape. The sizeand market importance of individual companiesin a financial group may vary. In the case of,for instance, a large bank acquiring a smallinsurance company, the degree ofconglomeration remains rather small.

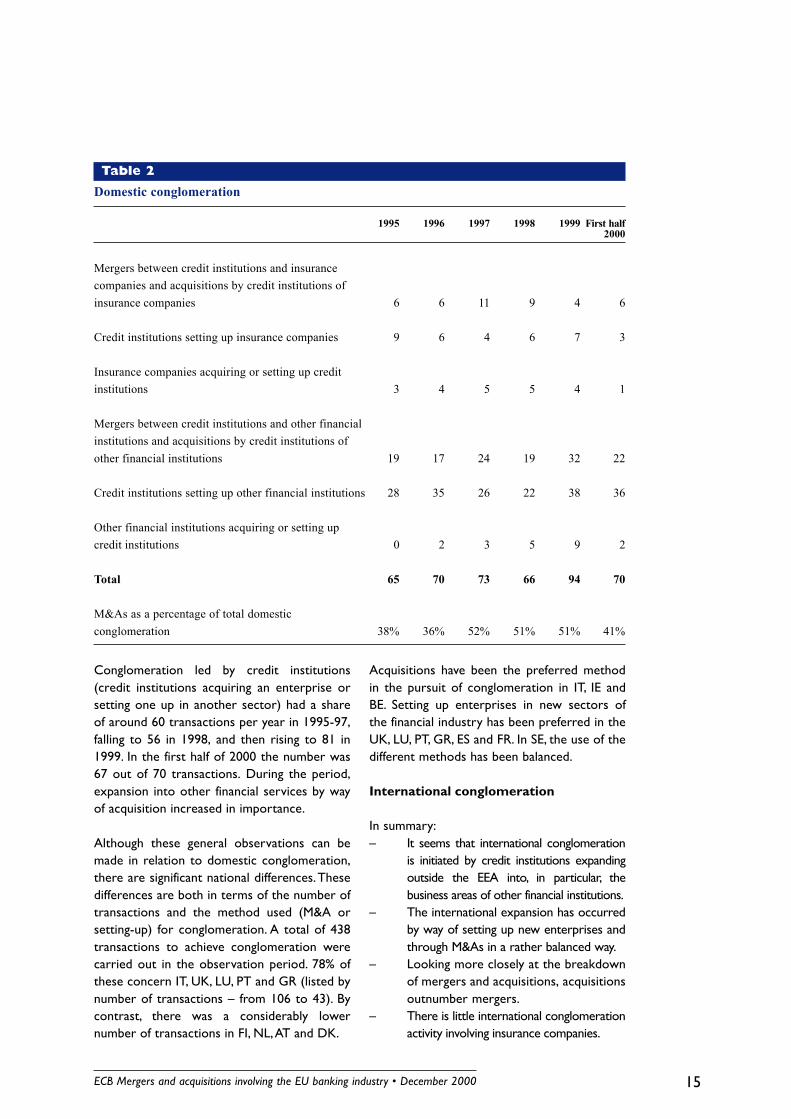

Domestic conglomeration

In summary:� Throughout the observation period

domestic conglomeration was driven bycredit institutions.

� Credit institutions are mainly expandinginto asset management and the businessof investment services in general.Furthermore, such conglomerates seemto be the most widespread form ofconglomerate. In most countries most ofthe asset management and investmentservices activities are provided by creditinstitutions.

In the observation period, credit institutionsexpanded far more actively into other sectors ofthe financial industry than did other financialinstitutions into banking business. This may bedue to the barriers to entry, historically, beinghigher in banking than in insurance. It may also bedue to the fact that in many Member States thebanking industry is far more developed and largerthan the insurance industry. Mergers are virtuallynever used as an �instrument� to achieveconglomeration. This is not surprising since amandatory specialisation principle applies toinsurance undertakings as well as to undertakingsfor collective investment in transferable securities(UCITS).7 The specialisation principle preventsbank/insurance and bank/UCITS mergers fromtaking place in a legal sense. The table below setsout the main data found in relation to domesticconglomeration.

7 Companies set up in accordance with Council Directive85/611/EEC of 20 December 1985.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 15

Table 2

Domestic conglomeration

1995 1996 1997 1998 1999 First half2000

Mergers between credit institutions and insurancecompanies and acquisitions by credit institutions ofinsurance companies 6 6 11 9 4 6

Credit institutions setting up insurance companies 9 6 4 6 7 3

Insurance companies acquiring or setting up creditinstitutions 3 4 5 5 4 1

Mergers between credit institutions and other financialinstitutions and acquisitions by credit institutions ofother financial institutions 19 17 24 19 32 22

Credit institutions setting up other financial institutions 28 35 26 22 38 36

Other financial institutions acquiring or setting upcredit institutions 0 2 3 5 9 2

Total 65 70 73 66 94 70

M&As as a percentage of total domesticconglomeration 38% 36% 52% 51% 51% 41%

Conglomeration led by credit institutions(credit institutions acquiring an enterprise orsetting one up in another sector) had a shareof around 60 transactions per year in 1995-97,falling to 56 in 1998, and then rising to 81 in1999. In the first half of 2000 the number was67 out of 70 transactions. During the period,expansion into other financial services by wayof acquisition increased in importance.

Although these general observations can bemade in relation to domestic conglomeration,there are significant national differences. Thesedifferences are both in terms of the number oftransactions and the method used (M&A orsetting-up) for conglomeration. A total of 438transactions to achieve conglomeration werecarried out in the observation period. 78% ofthese concern IT, UK, LU, PT and GR (listed bynumber of transactions � from 106 to 43). Bycontrast, there was a considerably lowernumber of transactions in FI, NL, AT and DK.

Acquisitions have been the preferred methodin the pursuit of conglomeration in IT, IE andBE. Setting up enterprises in new sectors ofthe financial industry has been preferred in theUK, LU, PT, GR, ES and FR. In SE, the use of thedifferent methods has been balanced.

International conglomeration

In summary:� It seems that international conglomeration

is initiated by credit institutions expandingoutside the EEA into, in particular, thebusiness areas of other financial institutions.

� The international expansion has occurredby way of setting up new enterprises andthrough M&As in a rather balanced way.

� Looking more closely at the breakdownof mergers and acquisitions, acquisitionsoutnumber mergers.

� There is little international conglomerationactivity involving insurance companies.

ECB Mergers and acquisitions involving the EU banking industry � December 200016

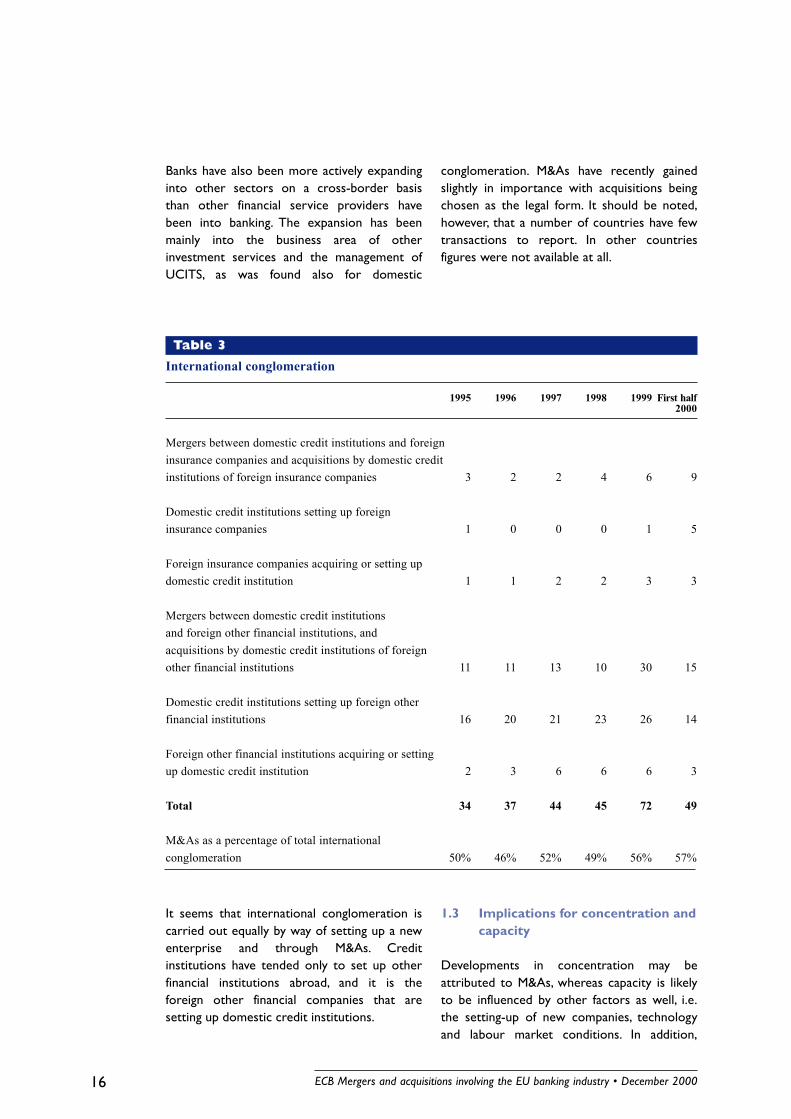

Banks have also been more actively expandinginto other sectors on a cross-border basisthan other financial service providers havebeen into banking. The expansion has beenmainly into the business area of otherinvestment services and the management ofUCITS, as was found also for domestic

conglomeration. M&As have recently gainedslightly in importance with acquisitions beingchosen as the legal form. It should be noted,however, that a number of countries have fewtransactions to report. In other countriesfigures were not available at all.

Table 3

International conglomeration

1995 1996 1997 1998 1999 First half 2000

Mergers between domestic credit institutions and foreigninsurance companies and acquisitions by domestic creditinstitutions of foreign insurance companies 3 2 2 4 6 9

Domestic credit institutions setting up foreigninsurance companies 1 0 0 0 1 5

Foreign insurance companies acquiring or setting updomestic credit institution 1 1 2 2 3 3

Mergers between domestic credit institutionsand foreign other financial institutions, andacquisitions by domestic credit institutions of foreignother financial institutions 11 11 13 10 30 15

Domestic credit institutions setting up foreign otherfinancial institutions 16 20 21 23 26 14

Foreign other financial institutions acquiring or settingup domestic credit institution 2 3 6 6 6 3

Total 34 37 44 45 72 49

M&As as a percentage of total internationalconglomeration 50% 46% 52% 49% 56% 57%

It seems that international conglomeration iscarried out equally by way of setting up a newenterprise and through M&As. Creditinstitutions have tended only to set up otherfinancial institutions abroad, and it is theforeign other financial companies that aresetting up domestic credit institutions.

1.3 Implications for concentration andcapacity

Developments in concentration may beattributed to M&As, whereas capacity is likelyto be influenced by other factors as well, i.e.the setting-up of new companies, technologyand labour market conditions. In addition,

ECB Mergers and acquisitions involving the EU banking industry � December 2000 17

there will be an immediate effect onconcentration, especially if M&As are betweenlarge institutions, whereas there is usually atime lapse of a couple of years beforerationalisation is effected and capacity, asmeasured by the number of branches andemployees, is reduced.

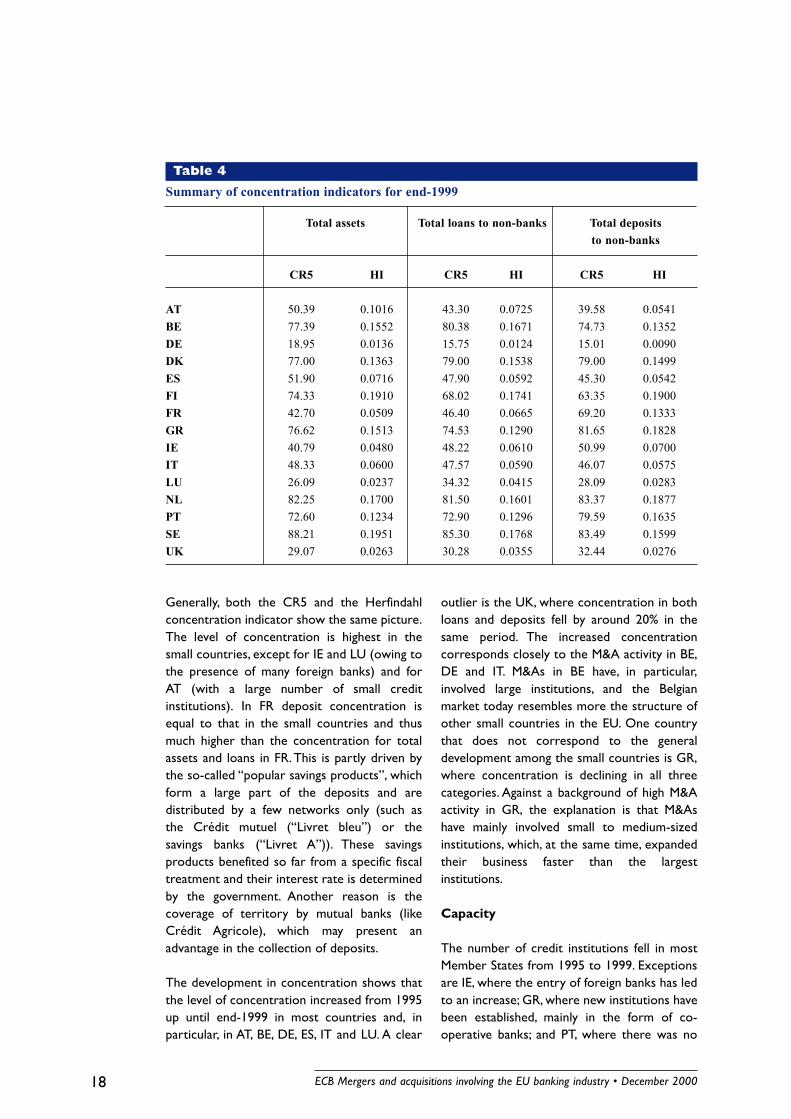

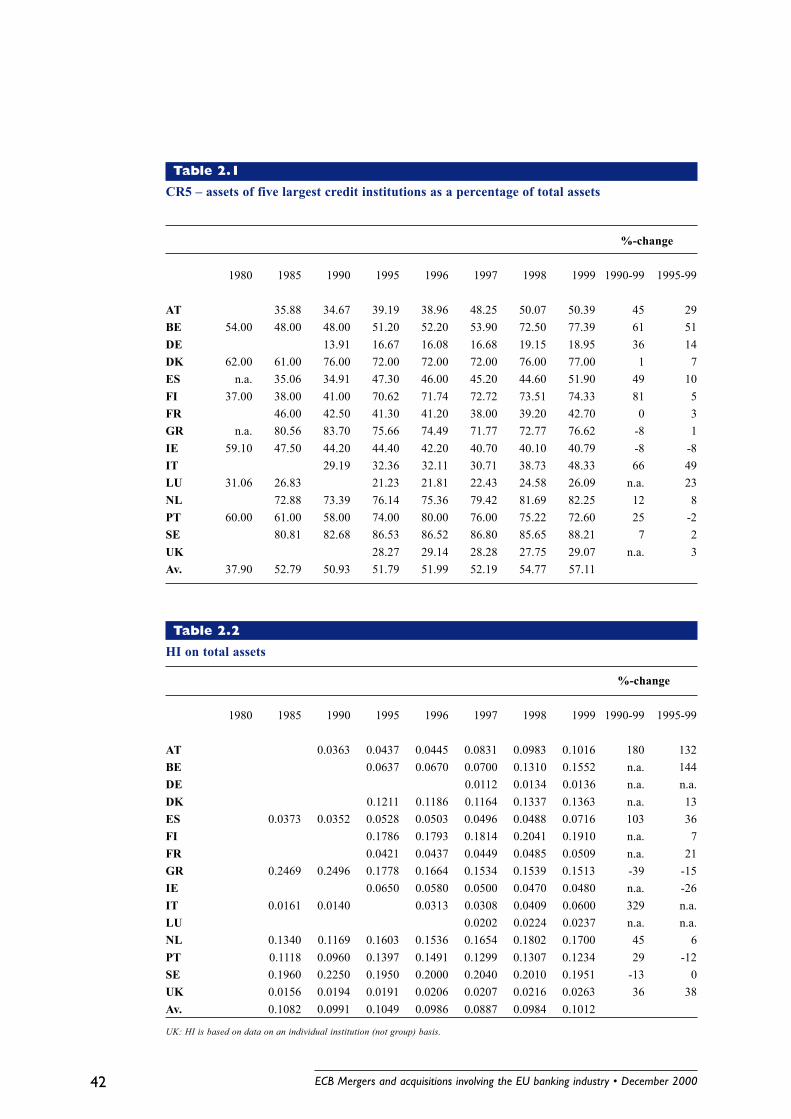

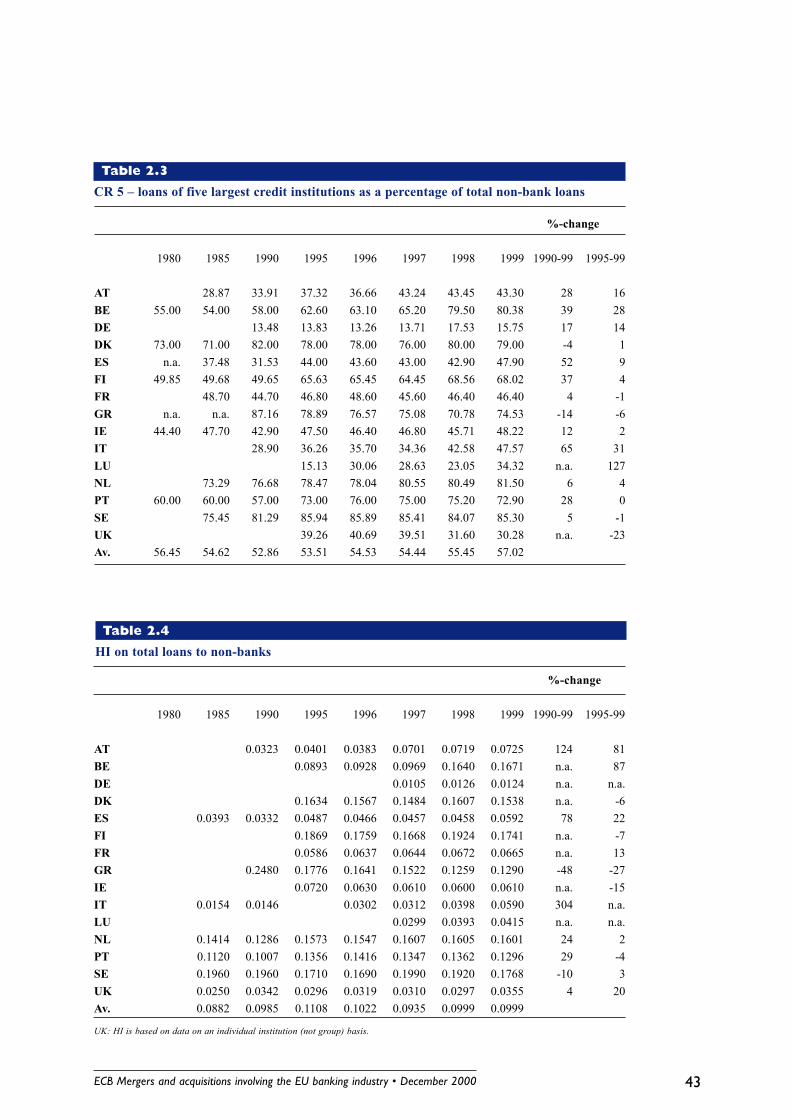

Concentration

Concentration has been measured by twodifferent methodologies. In both cases a groupapproach has been applied; legally independentinstitutions belonging to one group have beencounted as one entity. The simplest methodologyis called CR5 � or concentration ratio 5 � and isa measurement of the combined market share ofthe five largest institutions (for instance,unconsolidated8 domestic assets of the five

largest credit institution groups compared withtotal domestic unconsolidated assets). A moreadvanced methodology is the Herfindahlindicator, which is described in the box below.Concentration has been measured for totalassets, total non-bank loans and total non-bankdeposits.

Table 4 summarises the concentration ratios atend-1999. The annex includes availableconcentration indicators in Tables 2.1 to 2.6(inclusive) and provides information aboutdevelopments over time.

Box 1

The Herfindahl indicator

The Herfindahl indicator (HI) measures concentration in a market. The similarity between HI and CR5 isthat both indicators take the largest institutions mostly into account. The HI achieves this because theimportance of the largest institutions is emphasised through the calculation of this indicator, which is equalto the sum of squared market shares, whereas the CR5 takes into account the effective market share of thefive largest institutions. The difference is that the HI signals the size structure of the entire banking market,whereas the CR5 only shows the market share of the five largest banks, thus ignoring the size structure inthe rest of the market. In other words, the HI takes the so-called tail of institutions into account, byincluding the entire market, whereas the CR5 disregards institutions other than the five largest. Anotherdisadvantage of the simple concentration ratio (CRx) is that the setting of the number for the x-largestinstitutions is arbitrary. Often, CR indicators are for the three, four, five or ten largest institutions. Suchdistinctions may have a huge impact on the level of the indicator. This drawback does not apply to the HI,since it captures everything (the whole market) in one number.

The CR5 lends itself immediately to interpretation whereas the Herfindahl indicator is, at first sight,somewhat more difficult to �read�. Two illustrations may help: First, the US Department of Justice offersan interpretation of the HI which relates to concentration and is used in connection with competition policy,and divides the market into levels of concentration. The basic assumption is that an HI above 0.18 would beequal to high concentration. Second, a more simple interpretation is that a market with an HI of 0.2 has thesame HI as a market equally shared between five banks (the inverse of 0.2).

8 The word �unconsolidated� refers to the fact that only bankingassets are included, whereas �consolidated� statements for afinancial group would also include assets of non-banksubsidiaries of the credit institution.

ECB Mergers and acquisitions involving the EU banking industry � December 200018

Table 4

Summary of concentration indicators for end-1999

Total assets Total loans to non-banks Total depositsto non-banks

CR5 HI CR5 HI CR5 HI

AT 50.39 0.1016 43.30 0.0725 39.58 0.0541BE 77.39 0.1552 80.38 0.1671 74.73 0.1352DE 18.95 0.0136 15.75 0.0124 15.01 0.0090DK 77.00 0.1363 79.00 0.1538 79.00 0.1499ES 51.90 0.0716 47.90 0.0592 45.30 0.0542FI 74.33 0.1910 68.02 0.1741 63.35 0.1900FR 42.70 0.0509 46.40 0.0665 69.20 0.1333GR 76.62 0.1513 74.53 0.1290 81.65 0.1828IE 40.79 0.0480 48.22 0.0610 50.99 0.0700IT 48.33 0.0600 47.57 0.0590 46.07 0.0575LU 26.09 0.0237 34.32 0.0415 28.09 0.0283NL 82.25 0.1700 81.50 0.1601 83.37 0.1877PT 72.60 0.1234 72.90 0.1296 79.59 0.1635SE 88.21 0.1951 85.30 0.1768 83.49 0.1599UK 29.07 0.0263 30.28 0.0355 32.44 0.0276

Generally, both the CR5 and the Herfindahlconcentration indicator show the same picture.The level of concentration is highest in thesmall countries, except for IE and LU (owing tothe presence of many foreign banks) and forAT (with a large number of small creditinstitutions). In FR deposit concentration isequal to that in the small countries and thusmuch higher than the concentration for totalassets and loans in FR. This is partly driven bythe so-called �popular savings products�, whichform a large part of the deposits and aredistributed by a few networks only (such asthe Crédit mutuel (�Livret bleu�) or thesavings banks (�Livret A�)). These savingsproducts benefited so far from a specific fiscaltreatment and their interest rate is determinedby the government. Another reason is thecoverage of territory by mutual banks (likeCrédit Agricole), which may present anadvantage in the collection of deposits.

The development in concentration shows thatthe level of concentration increased from 1995up until end-1999 in most countries and, inparticular, in AT, BE, DE, ES, IT and LU. A clear

outlier is the UK, where concentration in bothloans and deposits fell by around 20% in thesame period. The increased concentrationcorresponds closely to the M&A activity in BE,DE and IT. M&As in BE have, in particular,involved large institutions, and the Belgianmarket today resembles more the structure ofother small countries in the EU. One countrythat does not correspond to the generaldevelopment among the small countries is GR,where concentration is declining in all threecategories. Against a background of high M&Aactivity in GR, the explanation is that M&Ashave mainly involved small to medium-sizedinstitutions, which, at the same time, expandedtheir business faster than the largestinstitutions.

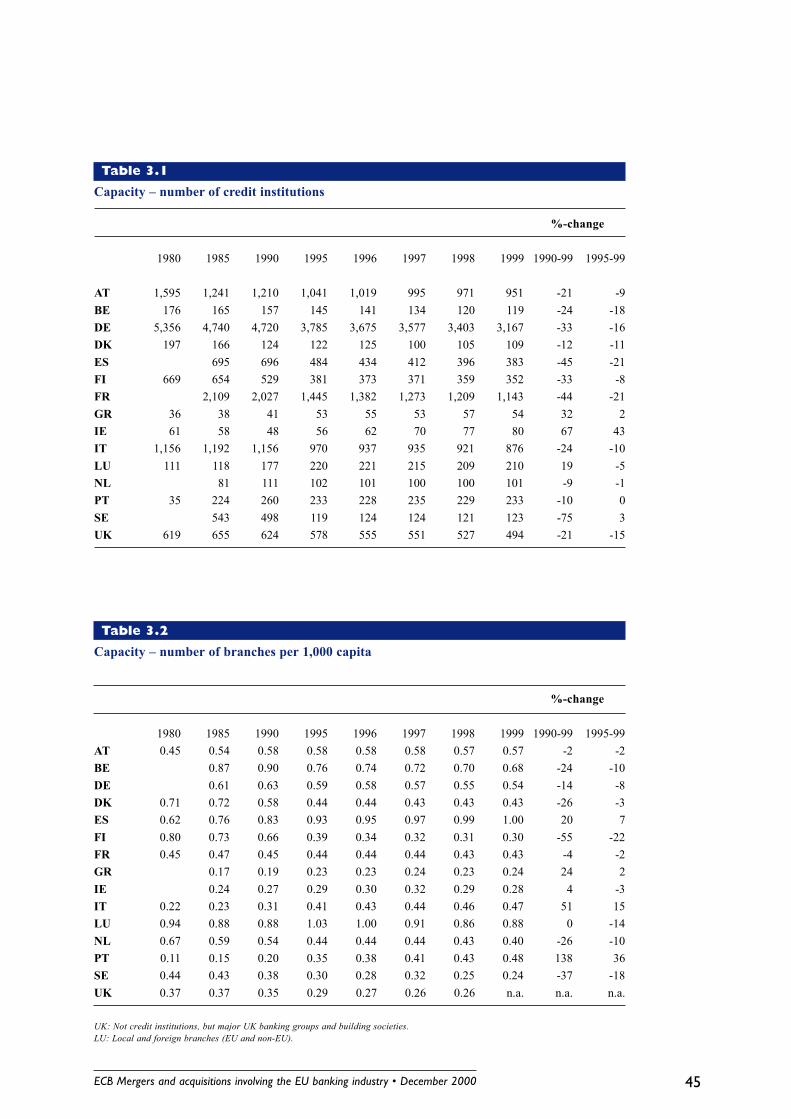

Capacity

The number of credit institutions fell in mostMember States from 1995 to 1999. Exceptionsare IE, where the entry of foreign banks has ledto an increase; GR, where new institutions havebeen established, mainly in the form of co-operative banks; and PT, where there was no

ECB Mergers and acquisitions involving the EU banking industry � December 2000 19

change. The reduction in most countries can beattributed to M&As, but other forms of marketexit (such as liquidation) may also havecontributed to the reduction. The pace atwhich the reduction in the number of creditinstitutions is taking place seems not to havechanged significantly during the observationperiod in spite of an increase in the number ofM&As, as indicated in Table 3.1 in the annex.

Owing to historic differences among MemberStates, there are very different developmentsand levels of the number of branches. Acommon trend cannot be identified. Nor isthere a clear relation to M&As, even if a time-lag is taken into account (to accommodate atransition period between the operation beingcarried out and the subsequent change incapacity). Branch numbers increased from 1995to 1999 in PT, IT, ES and GR, as shown in theannex, Table 3.2. Other Member States showed

a reduction, often a modest one. Over theperiod from 1990 up to and including 1999 thehighest reduction is in smaller countries withrelatively high concentration (BE, DK, FI, NLand SE). In the Nordic countries the mainreduction occurred in the early 1990s and ismore related to cost reductions after the crisisthan to M&As.

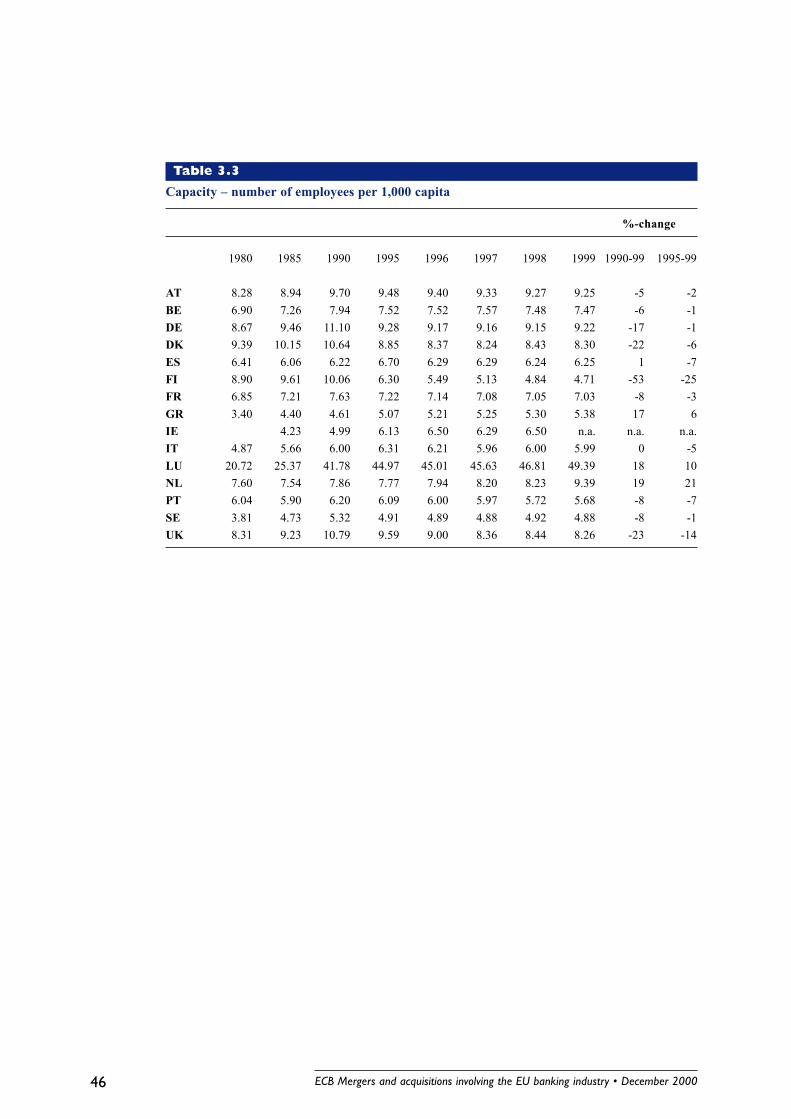

The number of employees (displayed per 1,000capita in Table 3.3 of the annex) declined from1995 to 1999, particularly in FI and the UK,whereas the reduction took place at thebeginning of the 1990s in DE and DK. Thenumber of employees was mostly stable from1997 to 1999. Hence, there seems to be noobvious relation to M&As.

M&As do not, or not yet, show a tangiblestraightforward effect on standard capacityindicators.

2 The rationale for M&As � why do they occur?

Section 2.1 of this chapter summarises theheadlines from the empirical literature analysingthe economic effects of M&As. Section 2.2presents the rationale for the pursuit of M&Asin the views expressed in the EU. Section 2.3compares both views.

2.1 Headlines from empiricalliterature on scale and scopeeconomies

Most empirical literature is based on evidencefrom the US. Fewer studies have beenperformed in Europe, but they have to a largedegree reached the same conclusions, which canbe summarised in the following points:� Banks in more concentrated markets

usually charge higher rates on smallbusiness loans and pay lower rates onretail deposits. Developments in recentyears, such as 1) new delivery channelsmaking local markets more contestable, 2)deregulation increasing competition inlocal markets and 3) products becoming

commodities, thereby making competitionmore perfect than in the past, may,however, have changed the market power.

� Market power studies that take intoaccount institutions that have recentlyengaged in M&As show mixed results. Thesame applies to studies that examineprofitability of institutions before and afterM&As, compared with similar institutionsthat did not engage in such activities.

� Studies of economies of scale are able toidentify a threshold at which these canbe achieved. More recent studies tend toshow that the level of the threshold isincreasing compared with previousstudies. The most obvious reason for thisobserved upward shift in the optimumsize lies in new technologies. Technologyis found to change the cost structuretangibly. Regulatory changes, havingcreated larger markets like the lifting ofrestrictions on inter-state banking in theUS and, within the EU, the creation ofthe euro area, may also play a role.

ECB Mergers and acquisitions involving the EU banking industry � December 200020

� Studies generally fail to find economies ofscope. Finding the appropriate benchmark (aprovider of only one product or service tooffer the required cost or revenue function)is a general problem in relation to thesestudies. The use of one network fordistributing a variety of products seems,however, appealing, if the network alreadyexists.

� Studies have shown that inefficiencies arecommon among banks and that domesticmergers among equally sized partnerssignificantly improved the performance ofthe merged banks to reach X-efficiency.9

Efficiency may therefore be a factor ofgreater relevance than economies ofscale and scope. It should be noted,however, that X-efficiency is not achieved�automatically� but rather through diligentattention to input and output factors. Inthis context, M&As represent excellentoccasions to reorganise the activities ofbanks to achieve a higher efficiency.

2.2 Views expressed by the industry inthe EU

In order to examine the motivation for M&As froman industry perspective, views of bankers werereported (either as a result of interviews orreflecting the knowledge of the supervisors).Overall, the pursuit of increased profitability prevailsas a motive. Cost benefits from economies of scaleare expected in domestic bank M&As, according tobankers. (International) conglomerates are createdfollowing anticipated revenue benefits fromeconomies of scope. The cost benefits are knownbecause they can be assessed on the basis ofknowledge of cost structures in the presentbusiness area combined with insight into historicalannual nominal costs (i.e. through internal costaccounting or in-house management systems),

9 X-efficiency is reached when, regardless of the scale ofoperation, input use is in line with the best practice of theindustry, i.e. there is no waste of inputs given the level ofoutputs.

Acr

oss d

iffer

ent s

ecto

rs

B

etw

een

cred

it in

stitu

tions

Main motives and possible rationalisations for the four types of M&As

Within one country In different countries

Domestic bank M&As International bank M&As

Economies of scale linked to costs are Size, i.e. the need to be big enough in thethe main motive. market, is the main motive.Cutting distribution networks and Matching the size of clients and followingadministrative functions clients.(rationalisation), including information Possible rationalisation withintechnology and risk management areas. administrative functions.

Domestic conglomeration International conglomeration

Economies of scope through cross- Economies of scope through cross-sellingselling are the motive. together with size are the two main motives.Risk and revenue diversification. Risk and revenue diversification.Optimum usage of complementary The M&A offers few rationalisations becausedistribution networks. institutions are in different countries andPossible rationalisations within subject to different regulations andadministrative functions may lead to practices.economies of scale linked to costs.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 21

whereas the expected revenue benefits will bebased on cross-selling possibilities and expectationsof market developments. All in all, costs savingsthereby seem more concrete than revenue benefits,which are much more elusive.

The table below sets out the main elementsidentified in the analysis of the rationale for thefour categories of M&As; these are describedin more detail below:

Domestic bank M&As

Economies of scale are the main rationale for�small� bank M&As. The small institutions aimto achieve critical mass to explore synergiesarising from size and diversification. TheseM&As are clearly related to cost reductionsthat are realised by cutting branch networks,staff and overheads in central head-officefunctions such as information technologydepartments, macroeconomic departmentsand legal departments. M&As are also used toavoid takeovers.

�Large� bank M&As often reflect a repositioningof the institutions involved. The pursuit of sizeincreases reflects the perceived need to becomebig enough for the domestic market. Economiesof scale also play a role. Banks aim at increasedmarket power and a larger capital base, and thusthere is a larger focus on increasing revenuethan for the small institutions. The same costreductions are followed as in small M&As.Together with the possibility of selling offperipheral business areas, the M&A offers theadvantage to owners of optimisation of thecapital structure, and thus increased shareholdervalue. A decisive factor for success is achievingthe possible rationalisations, which, in someMember States, may have been limited due tolabour market rigidities.

International bank M&As

These M&As are mainly motivated by size �the need to be big enough for the regional orglobal market. It is, however, not only the sizeof the institution itself, but also the size ofclients that plays a role, thereby furtheremphasising the repositioning argument and

the aim of achieving access and presence in alarger market. Banking groups follow andaccompany the internationalisation andconsolidation in the industries of their clients.Next to size, both economies of scale andscope have been cited as objectives.

Apart from size, another reason is economiesof scale linked to cost reductions, althoughrationalisations are less obvious than for creditinstitutions in the same country (mainly theoverlap of administrative and back-officeorganisations) owing to different regulatoryrequirements and/or market structures. Thenew institution will have a larger customerbase in a larger market, increasing possibilitiesfor economies of scale linked to increasingrevenue and the possibility of reaching thecritical mass needed to offer specific services,like, for instance, worldwide asset management.Acquisitions in emerging markets allow thetransfer of knowledge and capabilities, leadingto cost and revenue efficiency in the newentity.

In some Member States with high concentration,cross-border M&As may be driven byexpectations among bankers that further nationalconsolidation of large institutions would triggeropposition from anti-trust authorities. On theother hand, cross-border M&As may behampered by political resistance in hostcountries. There is, however, understandably little,if any, empirical evidence for this behaviour.

Domestic conglomeration

Economies of scope are the predominantmotive for domestic conglomeration. The criticalissue is achieving the expected cross-selling ofdifferent financial products to the largercustomer base brought together from theinstitutions involved. The expectation is toachieve �one-stop shopping� from �the cradle tothe grave�. Hence, it is the revenue side that isat the core of the economic rationale, implyingan efficient use of the existing distributionchannels. By bringing together skills fromdifferent sectors, a two-fold achievement isexpected � to respond to the disintermediationprocess within the conglomerate, thereby

ECB Mergers and acquisitions involving the EU banking industry � December 200022

capturing the business otherwise lost in theprocess, and to achieve income and riskdiversification. Usually, existing distributionchannels are maintained in their diversified form.Banks are moving strongly into long-termsavings. This move responds to demographicchanges and changes in fiscal treatment thatencourages investment in personal pensions.Banks are also aiming at an additional use of�brick and mortar� distribution channels tomake more efficient use of the fixed costsassociated with their branches. The decline ininterest margins resulting in a competitivepressure on banks has further fostered banks toseek new business areas. Insurance is a marketin growth and as such has attracted banks.Finally, banks are entering the insurance businessarea because insurance products may be naturalextensions of banking products. Thecombination of the two businesses may achieverisk and income diversification and thus lowerthe sensitivity to economic cycles.

International conglomeration

The two major reasons are economies of scopeand size, in this instance in the form of beingattractive to the large international clients. Theeconomic rationale is almost solely related toincreased revenue through cross-selling ofstrong brands. Overlaps of both administrativefunctions and distribution channels are minimaland institutions are in different countries withdifferent rules and practices, limiting thepossible cost advantages of this type of M&A.In a few instances, where rationalisationshave been achieved, they have been relatedto administrative functions that have beencentralised, i.e. information technology, strategicplanning, risk management and marketing.Such a conglomerate challenges managementcapabilities to achieve the efficiency and theimprovement anticipated.

2.3 The economic literature versusthe views expressed in theindustry

There are divergences between the findings inthe economic literature and the viewsexpressed in the industry. In the industry, there

are higher expectations of economies of scalethan found by various studies. This may beexplained by the banking industry being inprofound evolution, whereby the industryreacts to changes in the market conditionsand not to findings of econometric studies.One of the most important driving forcesfor changes in market conditions is thedevelopment of new technology, which� together with new possibilities foroutsourcing � alters the cost structure ofproduction. Furthermore, disintermediation,internationalisation and EMU have changed themarket conditions for credit institutions. Thediscrepancy between economic literature andthe industry might also result from the difficultyof achieving reliable estimates of scaleeconomies, particularly in a forward-lookingmanner able to predict the causes for thepresent industry restructuring.10 M&As seem tobe seen by many in the industry as a necessarystep to adapt preventively to the likely effects ofthese driving forces for change. The most recentacademic research indicates an increase in thethreshold for economies of scale. As M&As taketime to implement and changing marketconditions also lead to a time lapse, the pastdata to be used for econometric studies showthe effect with some years delay.

As for all M&A cases described11 by thesupervisors contributing to the report, it wasapparent that M&As take time to implement.Usually a period of two to three years elapsesbefore the success of a new institution can bejudged. There are some hints that especiallycost-related economies of scale take time toachieve, whereas revenue-related economies ofscope appear more quickly because cross-selling does not require as much time toimplement. Although revenue increases appear

10 First, econometric studies need long time series of historicaldata, but the cost structures of say a decade ago may nolonger be very relevant owing to the technological evolutions.Second, accounting-based cost input in the studies may notreveal economic scale benefits, since, for example, small banksmight achieve low costs in an accounting sense by outsourcingoperations where there are scale economies (such as paymentprocessing). Third, the overall economies of scale may not bethe full explanation, since benefits from size in certain lines ofbanking business (such as asset management or wholesalebanking) may be a sufficient reason to merge.

11 Each delegation reported in some detail three to fiveexamples of M&As.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 23

quicker, it should be noted that they are moreuncertain and elusive.

The likelihood of �cultural clashes�, which maycause a planned merger to fail, is higher forM&As of institutions operating in differentbusiness areas. They may, however, also appearin cases that do not lead to conglomeration.Differences in opinion between managers ofbanks with differing strategies may suffice toblock an operation. When the operation iscarried out nevertheless, cultural divergencehas often delayed or hampered a smoothimplementation of the operation.

The key importance of managerial behaviour forthe success of M&As may also explain a gooddeal of the divergence between the viewsexpressed and the conclusions one would drawfrom the economic literature. Managers have apositive expectation of their capability to masterthe human and managerial dimension, including

�cultural clashes�. The literature does not seemto confirm, however, the validity of theseexpectations. Furthermore, there might be anelement of following the fashion of a globaltrend towards M&As, and bank managers mayhave been incited to take part in the M&A waveby investment bankers and other consultants.

The best �fit� between economic literature andreality seems to exist for the small bank mergersthat lead to more cost-efficient enterprises andthat, for the sector as a whole, will mop upexcess capacity. Larger scale operations tend tobe less frequent and already more complex sothat it may become difficult to depict all relevantaspects of the operation with econometric toolsand to find large enough samples. This argumentholds even more true for operations leading tolarge complex financial conglomerates. Finally, ifM&As are in fashion, managers may show herdingbehaviour. Following the fashion will be the saferbehaviour than moving against the tide.

3 The way M&As are carried out � how do they happen?

This section examines the way in which M&Ashave been carried out � first from the creditinstitution perspective, second from theauthority perspective.

3.1 M&As from the credit institutionperspective

Data collected on domestic bank M&As showthat these, in the majority of cases, take theform of a merger. There are, however,differences between Member States. Asexamples, mergers outnumber acquisitions inAT and DE, whereas the opposite is observedin FR and IT. For the other three types ofM&As � being cross-border and/or cross-sector � the acquisitions constitute themajority of cases. The legal structures ofinstitutions and conglomerates differ, not onlybetween Member States but also betweeninstitutions and conglomerates within acountry. So does the choice of legal structurein connection with M&As. The choice of

structure is sometimes motivated by taxreasons. Without being a common tendencyacross all Member States, the holding structureseems to be a more recent phenomenon,which has become popular in some MemberStates. Credit institutions might be the maincompany of a conglomerate, in practice owningthe other activities. The co-ordinating andmanagerial function might, however, also beperformed by a holding company.

Supervisory authorities have reported that in anumber of cases an initial acquisition involvingcredit institutions is followed, at a later stage,by a merger. This appears especially to be thecase when the geographic and business areasoverlap. Another way of achieving anintegration of organisations with a similareffect to that of a merger is a substantial re-organisation of the central functions, which hasbeen reported in one case. If either thegeographic distribution differs, the banks arelocated in different regions of the same

ECB Mergers and acquisitions involving the EU banking industry � December 200024

country or different countries (internationalbank M&As), or the business areas are clearlydifferent � for example, a retail/corporate bankin an M&A with an investment bank � a mergeris much less likely to follow the initialacquisition. The aim is often to maintain arecognised brand name, which can be achievedby a merger at the holding company level.When a domestic bank M&A takes place, twosubsidiaries belonging to the same sector ofthe financial industry and located in the sameforeign country will be merged. In relationspecifically to international bank M&As, asuccessful acquisition in another country,whether within the EEA or in a third country,has been followed by another acquisition someyears later. In some cases mergers havefeatures of �acquisitions in disguise�: by thechoice of a merger managers and shareholdersof the �acquired� enterprises may be �pleased�.

As for both domestic and international bankM&As, the cases analysed provide no evidence ofdifferences in how they are carried outdepending on the size of the institutions involved.The geographic and business area differences orsimilarities are the decisive factors.

Specifically for bancassurance, four differentsequences of increasing integration can bedistinguished. First, banks may provide insuranceproducts simply through co-operationagreements with existing insurance companies.The bank will typically distribute insuranceproducts labelled with the name of the insurancecompany. Second, banks and insurance companiesmay decide to establish joint ventures to provideinsurance products through the distributionnetwork of the bank and, most commonly, undera name associated with the bank. Third, banksmay decide to establish subsidiaries to developthe insurance business area and the products to

be distributed through the banks� network(s).Fourth, banks and insurance companies canmerge on a holding level or a bank can acquire aninsurance company to become a subsidiary of thebank. The two latter sequences would constituteconglomerates.

The creation of conglomerates, whetherdomestic or international, has been eitherthrough holding company structures orthrough acquisitions. Restrictions on, forinstance, the conduct of banking and insurancebusiness from one legal entity eliminates thepossibility for an acquisition to become amerger, or a merger to take place initially.International conglomeration has followedgenerally as a second step to an internationalbank M&A, whereby the range of products onthe foreign market has been extended to takeadvantage of cross-selling possibilities.

Cross-border banking groups and conglomerates,of which three cases are mentioned in the boxbelow, have from the outset chosen a complexgroup structure in a holding company form. Theyachieved an �economic merger� on �an equalfooting� with equal ownership and fully sharedmanagement responsibilities. All threeconglomerates (the Fortis group, the Dexiagroup and the MeritaNordbanken group � nowknown as Nordea) have recently adopted, or areabout to adopt, a more simplified structure tostreamline managerial procedures and eliminatethe effect of market inefficiencies picking up ondifferent holding companies and leading to sharesin the same group trading at different prices. Thesimplification has also made the supervisory linesof responsibility more clear. Memoranda ofunderstanding have, since the establishment ofthe three institutions, secured supervisory accessand monitoring of the groups, including thedistribution of consolidated supervision.

ECB Mergers and acquisitions involving the EU banking industry � December 2000 25

Box 2

Three cases of cross-border M&As, their organisation and supervision

In 1990 the Belgian AG and the Dutch Amev, both insurance companies, decided to have an economicmerger of their activities under the name �Fortis�. A bi-national consortium structure was chosen, becauseno adequate legal form was available for two companies of a different nationality to integrate their activitieson an equal footing. The group acquired a number of banks, and the Belgian and Dutch supervisors set upthe necessary arrangements for the supervision of the group as a whole as well as for the banking activities.This was done in two memoranda, the �four parties covenant� (signed by the banking and insurancesupervisors) and the �two parties covenant� (signed by the banking supervisors). In the �four partiescovenant�, the Belgian banking supervisor was designated as the co-ordinating supervisor, responsible forreceiving the reporting of the group, performing a first assessment, and organising the consultation processbetween the four supervisors. In the �two parties covenant�, the Belgian banking supervisor was designatedas the central supervisor, charged with the consolidated supervision of the banking activities of the group.In 1999, owing to new acquisitions, the ownership structure of Fortis changed and the group structure wassimplified. In the light of these changes, the supervisory arrangements have been reviewed.

In 1996, the Belgian Crédit Communal de Belgique and the French Crédit Local de France created thebanking group �Dexia� modelled on the Fortis structure. In order to ensure an adequate consolidatedsupervision of the group, a memorandum providing for a two-tier supervision was concluded between theBelgian and the French banking supervisors. First, the two banks continued to be supervised by theirrespective supervisors. Secondly, prudential supervision of the group as a whole is carried out on the basisof a supervision equivalent to a credit institution heading a group. No central supervisor was designated forthis consolidated supervision, but each supervisor in turn acted for a period of two years as a technical co-ordinator. In 1999, the joint structure of the Dexia group was unwound, and replaced by a single holdingcompany incorporated in Belgium and heading all activities. The supervisory implications were that theBelgian banking supervisor became responsible for the consolidated supervision of the group. Because ofthe importance of the different components of the group, this consolidated supervision will be performed inclose co-operation with the other European banking supervisors involved.

The Finnish-Swedish MeritaNordbanken was formed in 1998 through �an economic merger� � or anownership arrangement like that seen for the Fortis and the Dexia groups. The issuance of common shares andpreference shares made it possible to distribute voting rights equally and a co-operation agreement achieved afull sharing of management responsibilities. The financial holding company � MeritaNordbanken � wasregistered in Finland. The Finnish Financial Supervisory Authority was responsible for consolidatedsupervision. An MoU between the Finnish and Swedish supervisory authorities had an appendix relating toMeritaNordbanken, requesting, among other things, planning and from time to time conduct of inspections inco-operation, and the exchange of supervisory information at regular meetings. In October 1999 a proposal tosimplify the ownership structure was put forward, according to which a new holding company, Nordic BalticHolding, registered in Sweden, became the sole owner of MeritaNordbanken, which remained registered inFinland. In the first half of 2000, Nordic Baltic Holding acquired the holding company of Danish Unibank(Unidanmark), which also included substantial insurance activities in Denmark and Norway. The banking andinsurance supervisors in all four Scandinavian countries now have a special MoU on the supervision of theholding company (now named Nordea) and the banking and insurance activities.

All three cases described above still involve aholding company registered in one country.The legal structure for a supra-nationalEuropean company does not exist.

The internal organisations of institutions/conglomerates are also very different, as is thechoice of internal organisation in connection withM&As. In some cases a company (or legal)structure is preferred, and in other cases abusiness line structure, whereby, for instance,

ECB Mergers and acquisitions involving the EU banking industry � December 200026

business development or risk management is thebasis for the structure to achieve a managerialoverview. Supervisory authorities have no generalobjections to either structure, but there must bea sufficient match between the legal structureand the internal organisation to ensure that thereare no impediments to the adequate exercise ofsupervision and to monitor the decision-makingprocesses with regard to legal correctness.Finding the appropriate legal and organisationalstructure seems to be a major challenge inmerging and acquiring institutions. In cases wherea matrix management or management byproduct line is followed, the legal structure doesnot correspond fully to the managerial structure

and the governing bodies of financial servicesgroups may have difficulties in ensuring thesmooth functioning of the group as a whole and,in particular, compliance with rules.

3.2 M&As from an authorityperspective

National authorities are involved in M&As invarious ways. Mergers and acquisitions aredifferent and require differing approaches andinvolvement by authorities in the authorisationas well as the supervisory assessment.Moreover, the supervisory role as a home or ahost supervisor has an effect.

Box 3

The European legal framework relevant to M&As involving credit institutions is laid down in Article 11 ofthe Second Banking Directive.12 According to the relevant provisions, acquirers of a qualifying holding in acredit institution must inform the competent authority. The Directive sets out certain thresholds, thecrossing of which triggers the notification obligation. Once notified, the competent authorities have a periodof three months to oppose the plan. A veto can be issued if, in view of the need to ensure sound and prudentmanagement, the competent authority is not satisfied with the suitability of the acquirer. Theimplementation of this provision differs slightly across Member States. There are some differencesconcerning the calculation of the thresholds and, in some cases, the right to veto is implemented as anobligation to obtain an authorisation.

Furthermore, Article 2 (2) of the so-called post-BCCI Directive13 is a key provision in relation to theauthorisation of M&As. Banking supervisors can, according to the article, influence the structure of the newgroup resulting from an M&A. The provision obliges banking supervisors to refuse granting the licence if thestructure of the group is an obstacle to their supervision on an individual or a consolidated basis.

3.2.1 Mergers and acquisitions � what isassessed?

Generally, a quasi authorisation (absence of aveto) is required in relation to mergers and toacquisitions.14 In some countries, anauthorisation is required before publication ofthe intended merger or acquisition. Usually,there will be contacts between the authoritiesand the institutions involved at an early stage.However, public notifications of planned M&Asusually include the information that theoperation is subject to authorisation.

Assessment procedures and rules on mergerstypically focus on the new entity, which isassessed in prudential terms. The prudential

assessment aims to ensure continuedcompliance with supervisory rules (e.g.requirements for the suitability ofshareholders, liquidity, capital, large exposures)and sufficient access to supervise the newentity at both company and consolidated level.In acquisitions, the most important issue forthe authority of the acquired institution is thefit and proper characteristics of the newshareholder. The authority supervising anacquiring bank, will concentrate on anadequate supervision on a consolidated basisof the new structure and an appropriate