mergers and business combination by, sanaullah

TRANSCRIPT

Mergers and other business

combinations

BY:SANAULLAHZOHAIBSUNDASSOFIA

Business Combination

“A business combination occurs when two or more companies join under common control, meaning the ability to direct policies and management.”

“A business combination occurs when an enterprise acquires net assets that constitute a business or equity interests of one or more other enterprises and obtains control over that enterprise or enterprises.”

What is the motivation behind business combination

Growth

I. New markets

II. Increase in market share

Reduction in operating costs

Diversification

Tax reasons

Management incentives

TYPES OF BUSINESS COMBINATION

Business Combination

Merger Consolidation

Congeneric conglomeratic

Horizontal

vertical

Upward

Downward

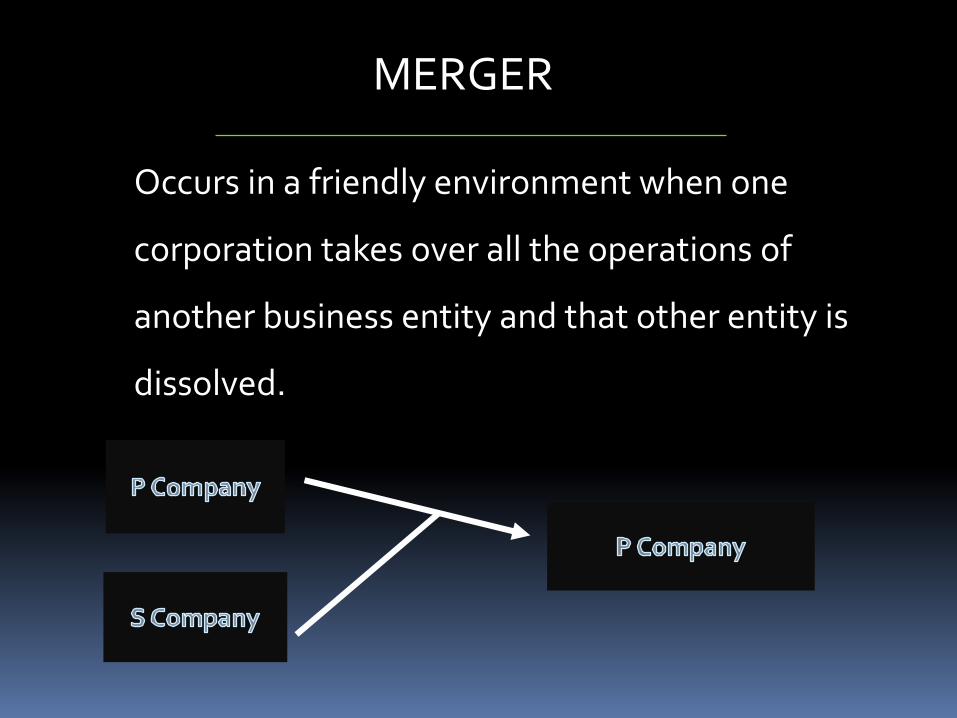

MERGER

Occurs in a friendly environment when one

corporation takes over all the operations of

another business entity and that other entity is

dissolved.

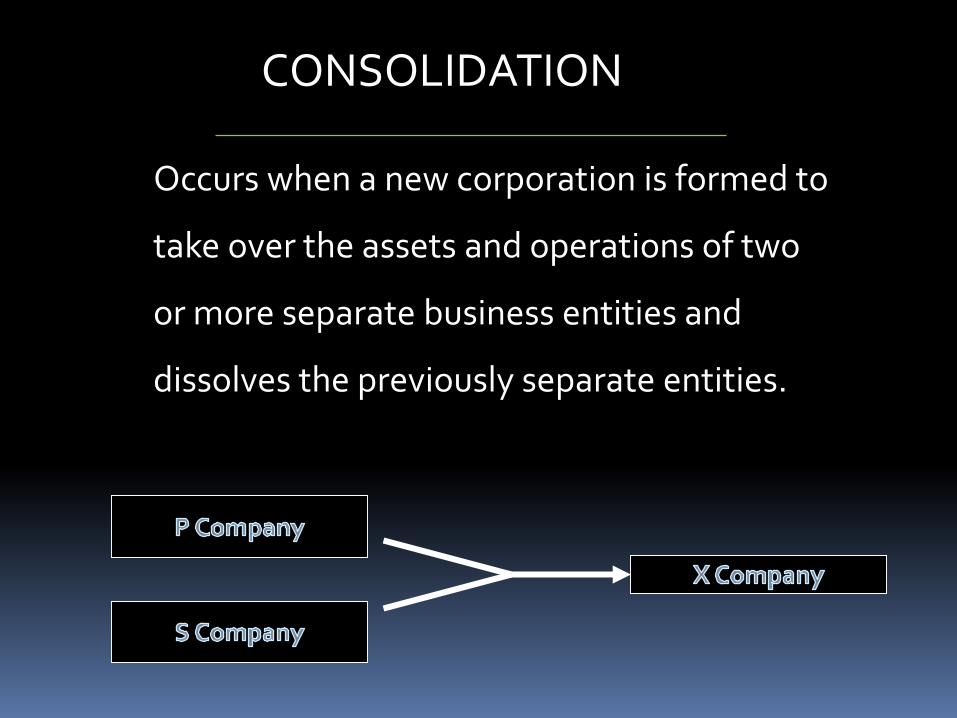

CONSOLIDATION

Occurs when a new corporation is formed to

take over the assets and operations of two

or more separate business entities and

dissolves the previously separate entities.

ACQUISITION

The process of merger where the powerful

companies are eating to the smaller companies.

It can be eating up the stocks and increasing

the holding rights

Or the customers of other smaller companies

then transferring the assets into their own

accounts

ACQUISITION (Customers of other smaller

companies)

ACQUISITION (Stocks of other smaller

companies)

TYPES OF MERGERS

Congeneric

Conglomerate

1. Horizontal:when similar nature of

companies merge1. vertical

Upward: Suppliers or raw material

providers of the similar nature of companies merge with the parent company

Downward: distributors or resellers of the

similar nature of companies merge with the parent company

TYPES OF MERGERS(continued)

Congeneric

Conglomerate

TYPES OF MERGERS

Congeneric

Conglomerate

Occurs when the unrelated

businesses are combined/

merged

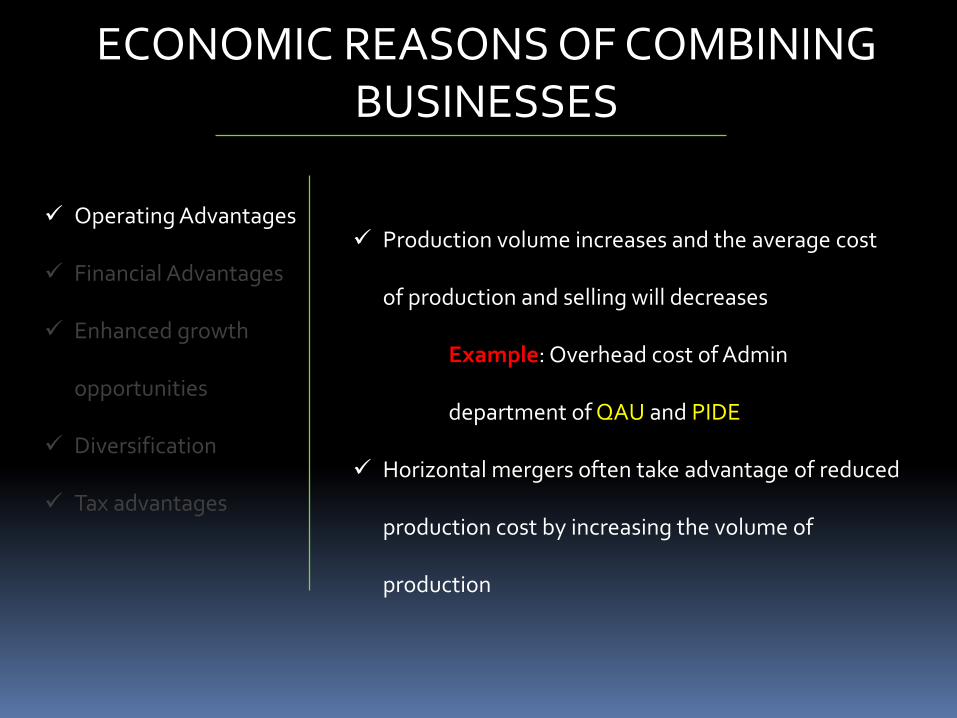

ECONOMIC REASONS OF COMBINING BUSINESSES

Operating Advantages

Financial Advantages

Enhanced growth

opportunities

Diversification

Tax advantages

Production volume increases and the average cost

of production and selling will decreases

Example: Overhead cost of Admin

department of QAU and PIDE

Horizontal mergers often take advantage of reduced

production cost by increasing the volume of

production

ECONOMIC REASONS OF COMBINING BUSINESSES

Operating Advantages

Financial Advantages

Enhanced growth

opportunities

Diversification

Tax advantages

The firms can take opportunities in the financial

markets because of its increased size or

efficiencies

Example: two companies one has obtained high

debt capacity and the other firm low. When they

merge the lower debt capacity holding firm will

take the financial advantage

ECONOMIC REASONS OF COMBINING BUSINESSES

Operating Advantages

Financial Advantages

Enhanced growth

opportunities

Diversification

Tax advantages

Merged companies grow at a faster rate as

compared to individual companies

Quicker

Provides product in a more timely fashion

ECONOMIC REASONS OF COMBINING BUSINESSES

Operating Advantages

Financial Advantages

Enhanced growth

opportunities

Diversification

Tax advantages

Smooth earning instead of fluctuations in seasonal

economic cycle

Example: Auto mobile manufacturer might

acquire a replacement parts company

Reduces the risk factor i.e. illiquidity or bankruptcy

ECONOMIC REASONS OF COMBINING BUSINESSES

Operating Advantages

Financial Advantages

Enhanced growth

opportunities

Diversification

Tax advantages

Mergers between two companies reduces

the acquiring firm’s tax liability

HOW A MERGER IS EFFECTED

Friendly takeover

•Purchase of Assets

•Purchase the Stock

Hostile takeover

•Tender offers

•Proxy fight

LETS SEE WHAT HAPPEN IN REAL LIFE

Unilever has acquired the shares of Ambrosia International Ltd.,

Mehran International Ltd., and Pakistan Industrial Promoters Ltd.,

which form what is often called the Polka group of ice-cream

companies

Two broadband companies of Pakistan, i.e. Wateen

and Qubee have decided to merge to conduct joint

operations in Pakistan to enhance energy in wireless

broadband market

YOU WILL READ AN ADDITIONAL ARTICLE ON THE MERGERS AND ACQUISITION IN PAKISTAN AT FOOT NOTE OF THIS SLIDE

International - Mergers and AcquisitionsMergers & Acquisitions in Omanby Taimur MalikLegal Advisor, Middle East & North Africa Region, Vale Minerals and Metals

PUBLISHED:

You will find the Article in foot notes