mexico - iuj.ac.jp · country profile 2000 mexico this country profile is a reference tool, which...

TRANSCRIPT

COUNTRY PROFILE 2000

MexicoThis Country Profile is a reference tool, which providesanalysis of historical political, infrastructural and economictrends. It is revised and updated annually. The EIU’squarterly Country Reports analyse current trends andprovide a two-year forecast

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newsletters toannual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1000Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryThis publication can now be viewed by subscribing online at http://store.eiu.com/brdes.html

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-linedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

London: Jan Frost Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023New York: Alexander Bateman Tel: (1.212) 554 0600 Fax: (1.212) 586 1181Hong Kong: Amy Ha Tel: (852) 2802 7288/2585 3888 Fax: (852) 2802 7720/7638

Copyright© 2000 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5596

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

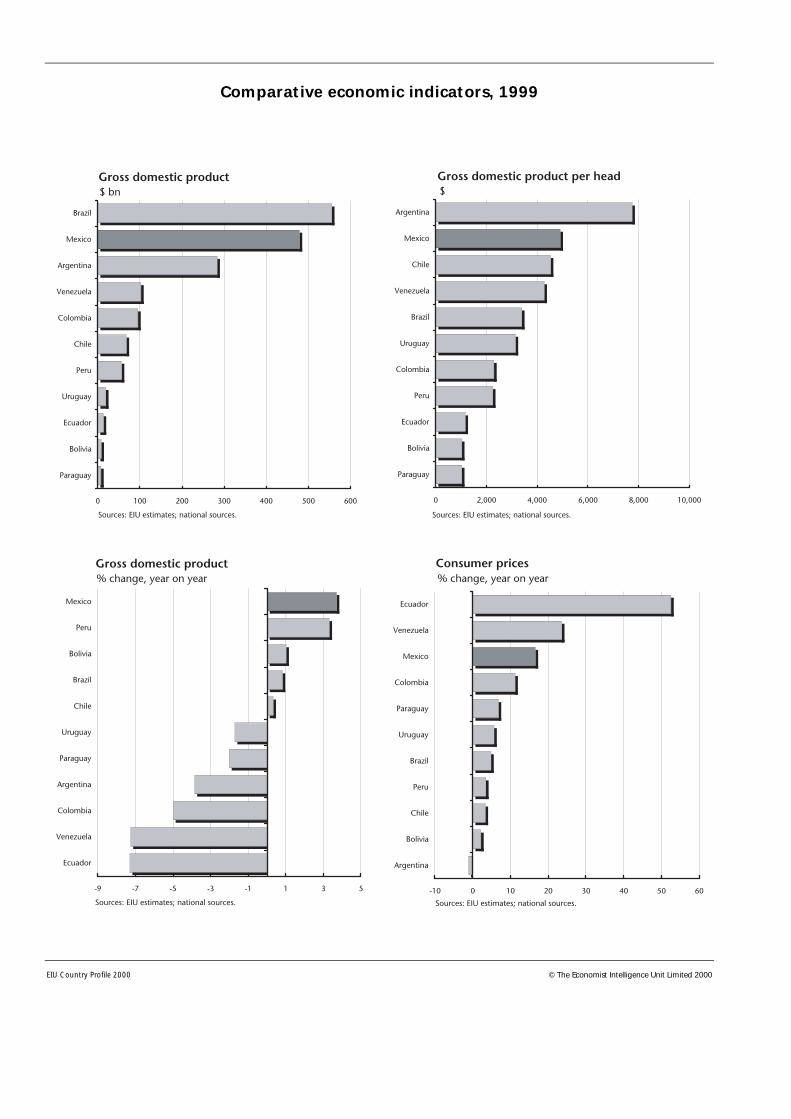

Comparative economic indicators, 1999

1

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Contents

3 Basic data

4 Political background4 Historical background9 Constitution and institutions9 Political forces

11 International relations and defence

12 Resources and infrastructure12 Population13 Education14 Health14 Natural resources and the environment15 Transport and communications17 Energy provision

19 The economy19 Economic structure20 Economic policy24 Economic performance26 Regional trends

26 Economic sectors26 Agriculture, forestry and fishing28 Manufacturing30 Mining and semi-processing31 Construction31 Financial services34 Other services

35 The external sector35 Trade in goods38 Invisibles and the current account39 Capital flows and foreign debt42 Foreign reserves and the exchange rate

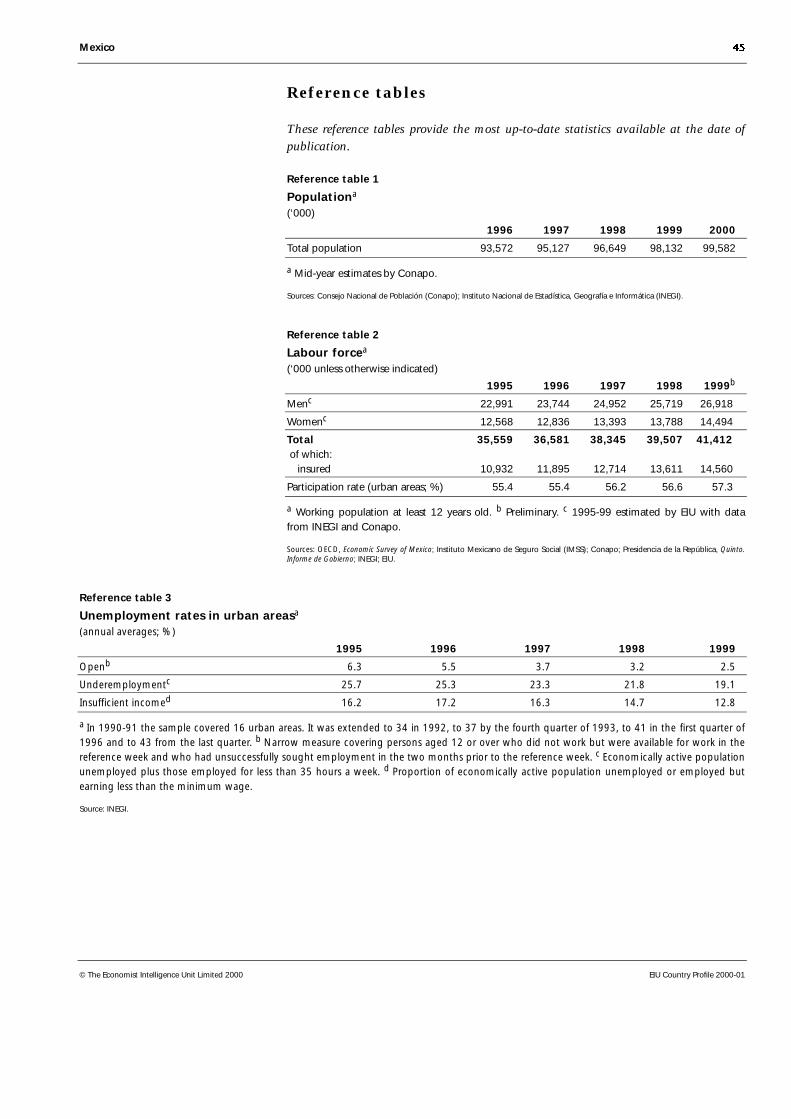

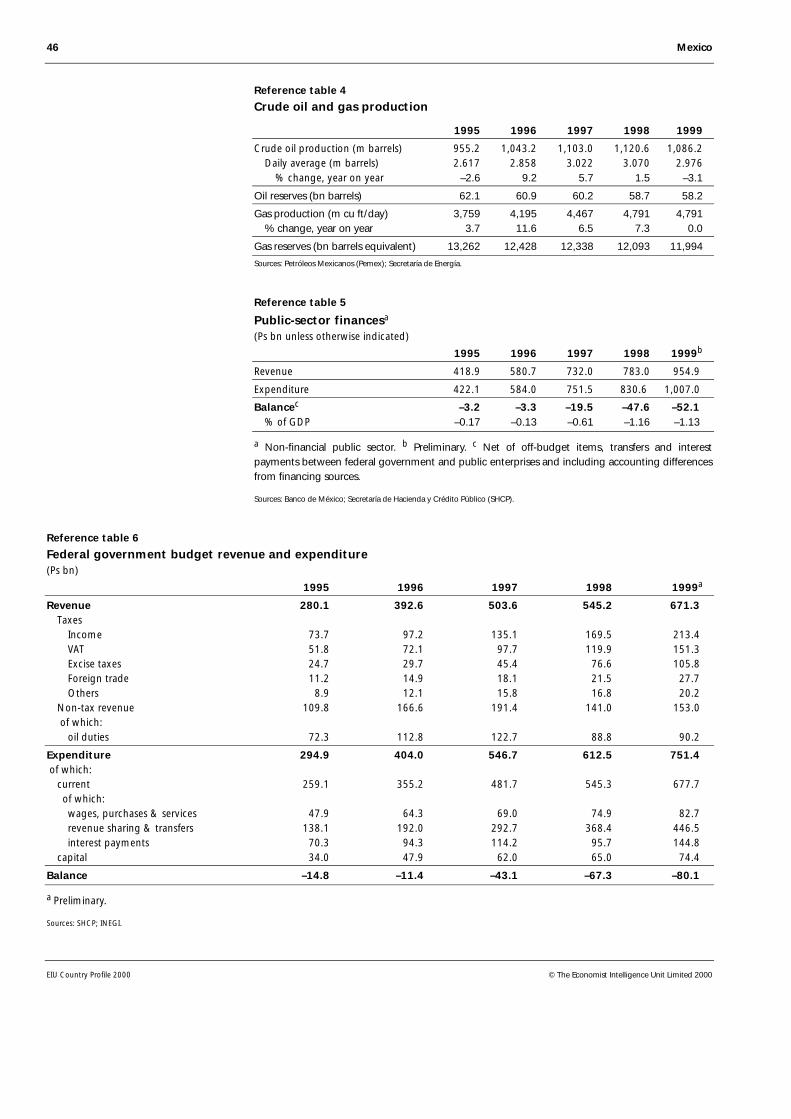

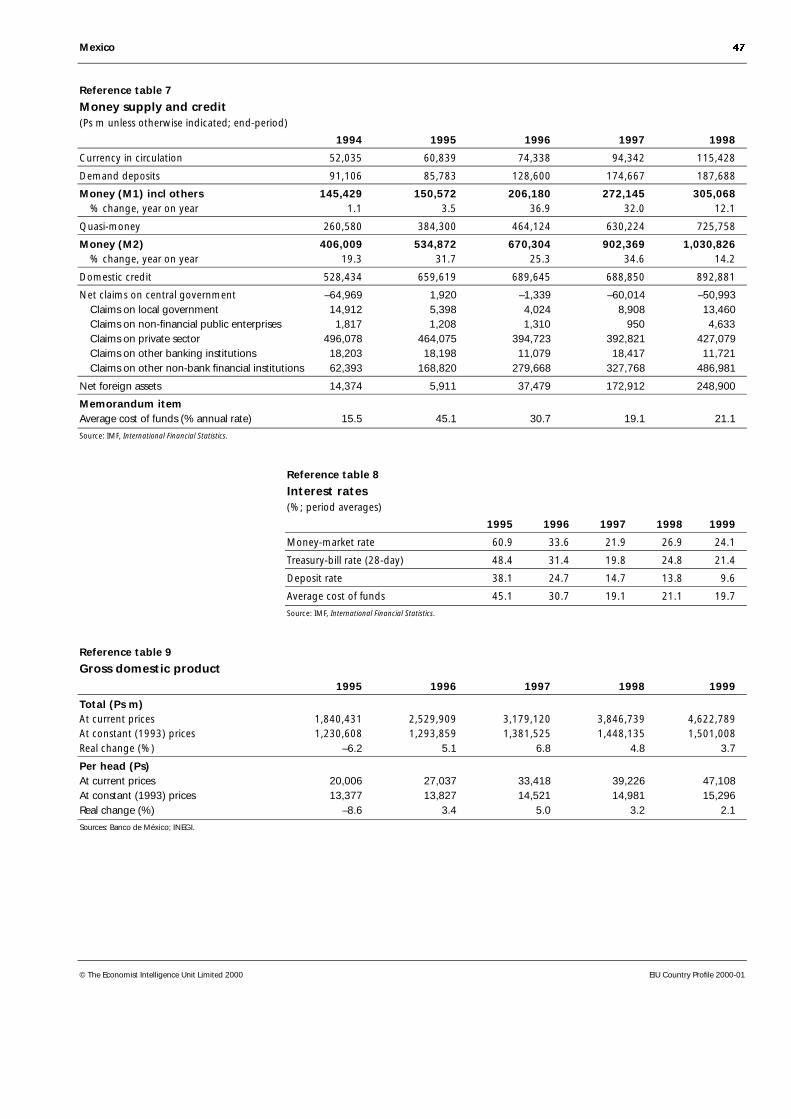

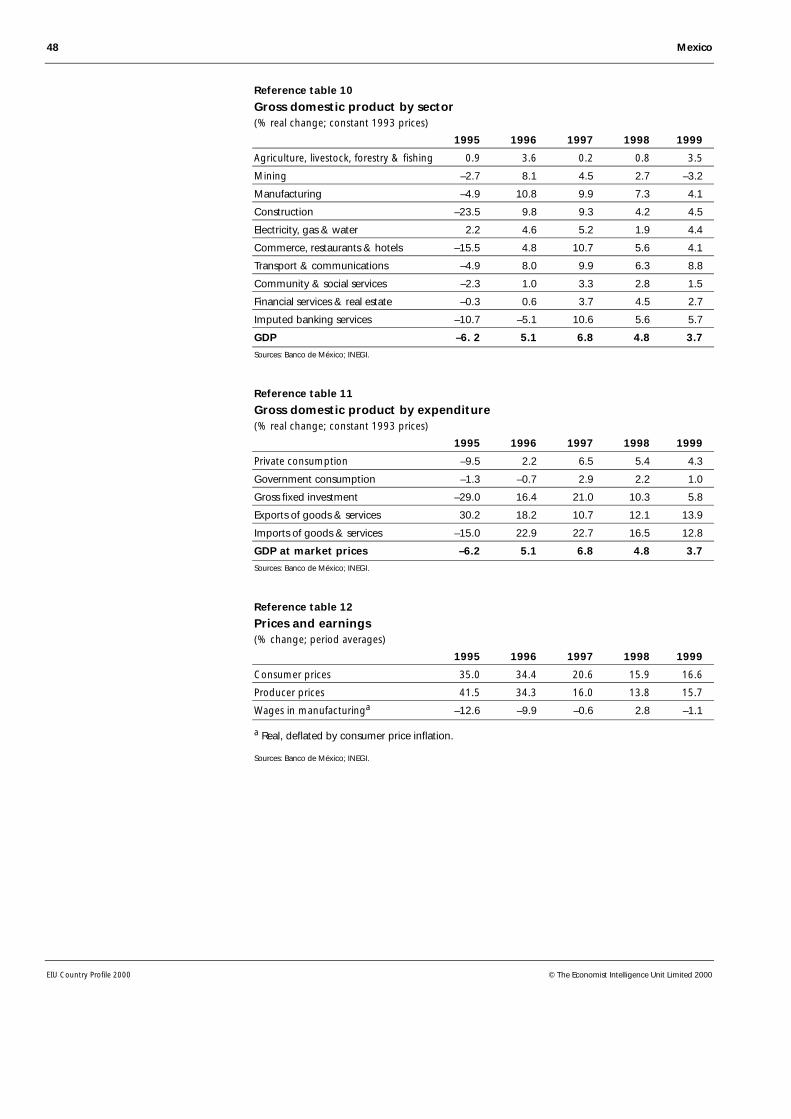

43 Appendices43 Sources of information45 Reference tables45 Population45 Labour force45 Unemployment rates in urban areas46 Crude oil and gas production46 Public-sector finances46 Federal government budget revenue and expenditure47 Money supply and credit47 Interest rates47 Gross domestic product48 Gross domestic product by sector48 Gross domestic product by expenditure48 Prices and earnings

April 25th 2000

2

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

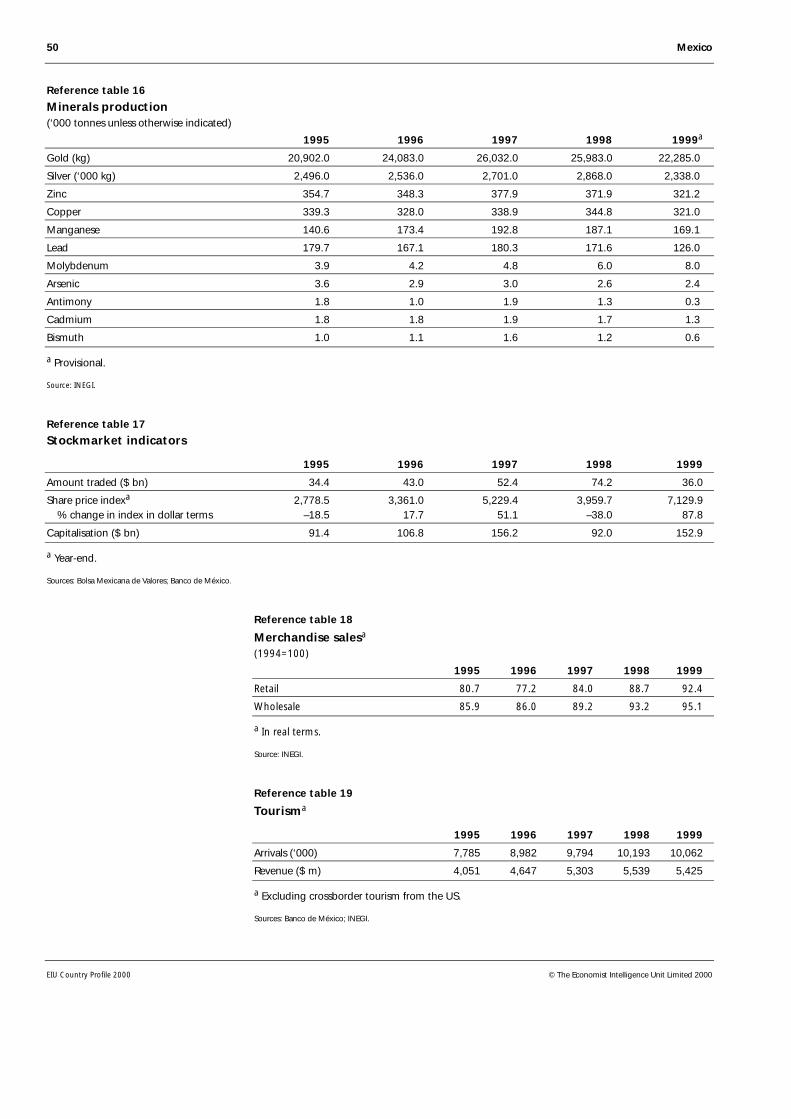

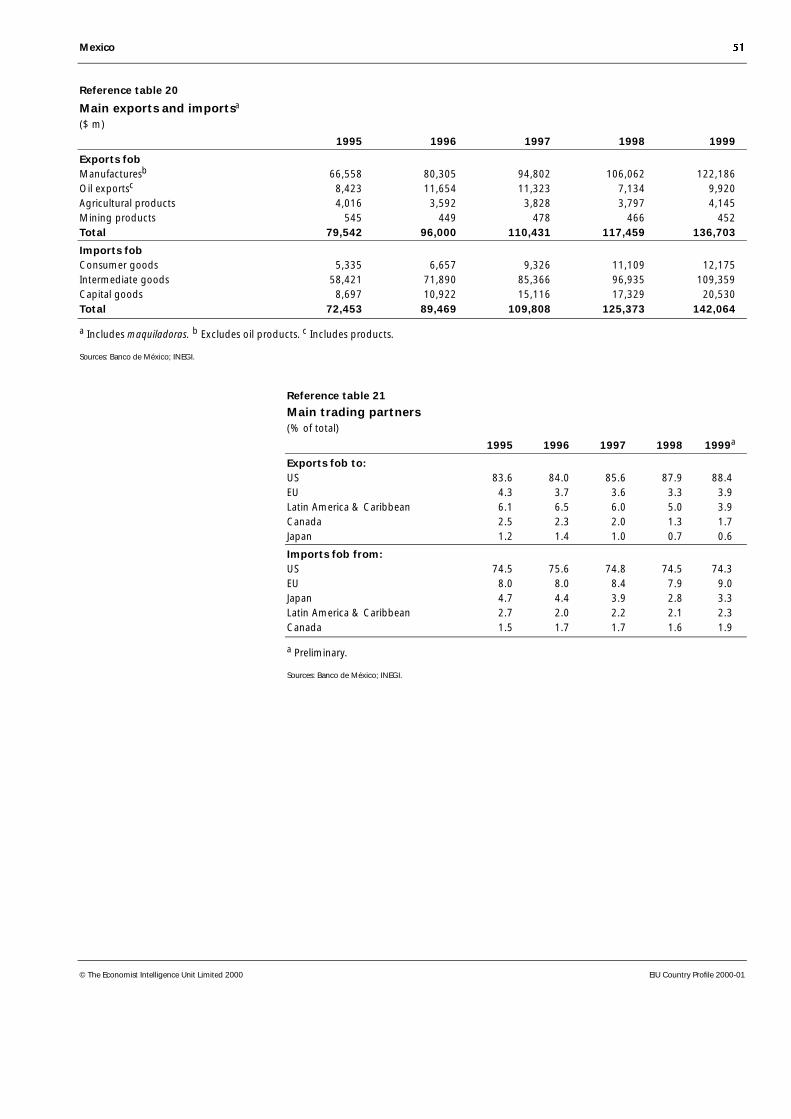

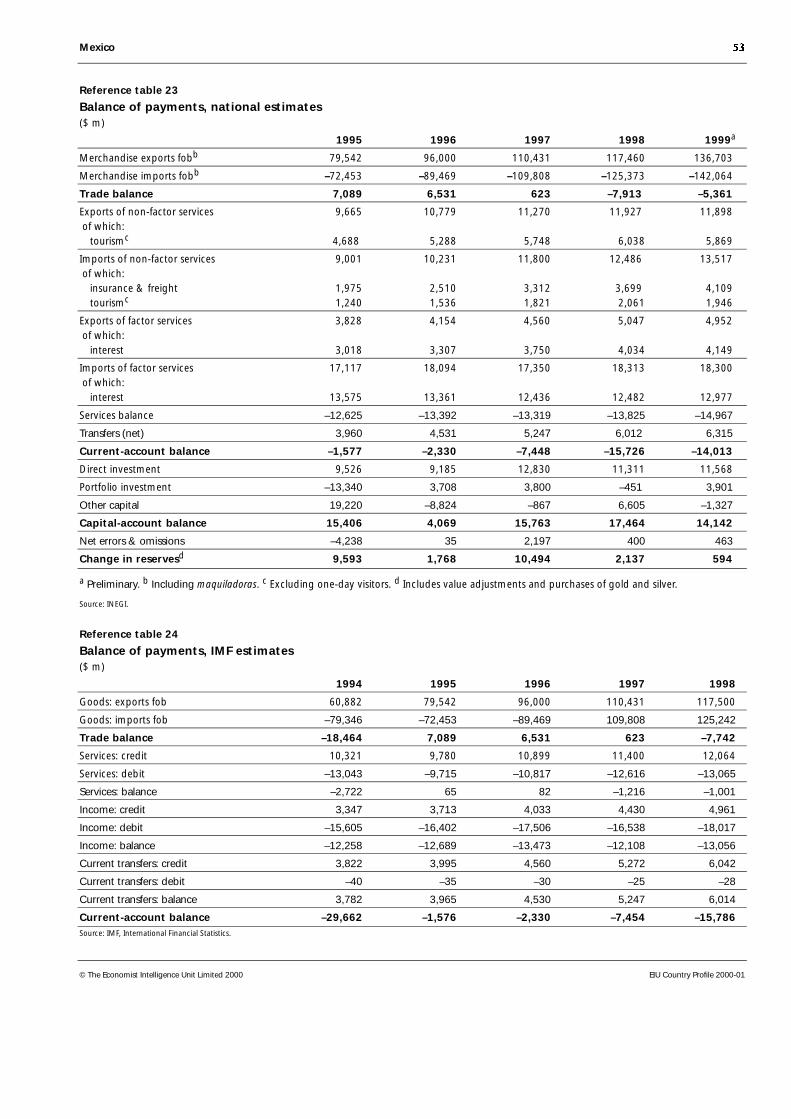

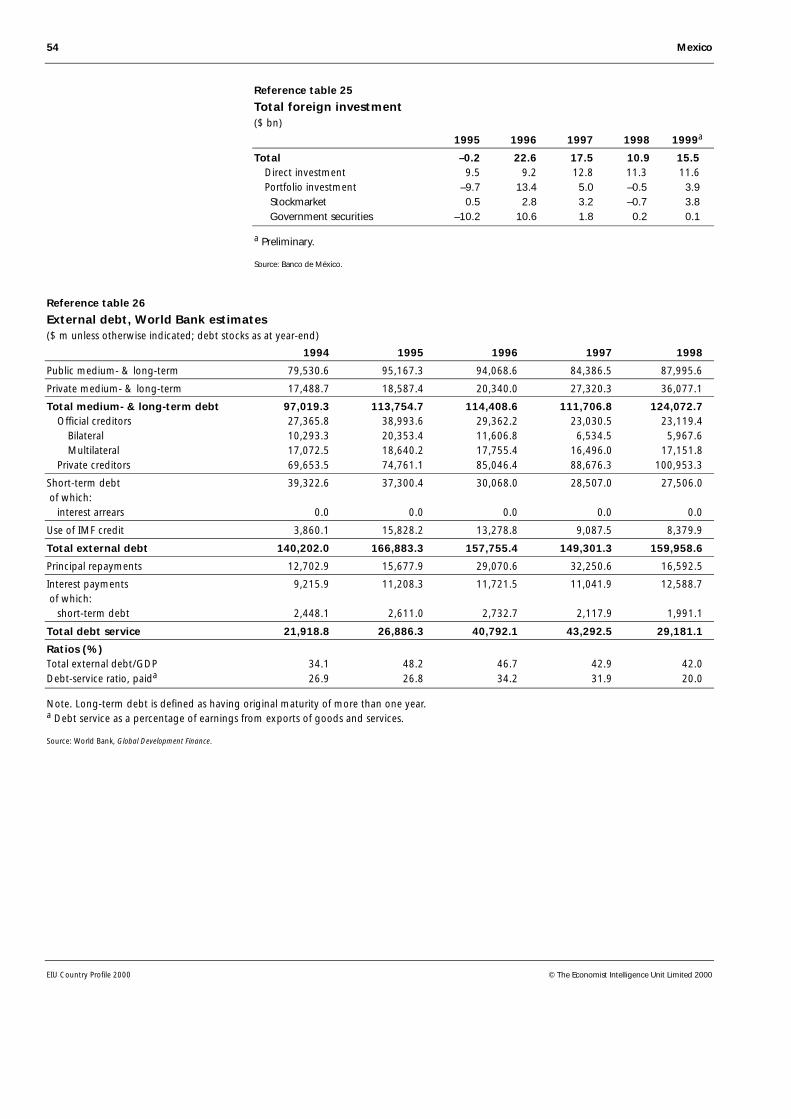

49 Production of principal crops49 Livestock production49 Manufacturing production50 Minerals production50 Stockmarket indicators50 Merchandise sales50 Tourism51 Main exports and imports51 Main trading partners52 Direction and composition of trade, 199853 Balance of payments, national estimates53 Balance of payments, IMF estimates54 Total foreign investment54 External debt, World Bank estimates55 Gross external debt, national estimates55 Amortisation schedule of global external debt55 Foreign reserves56 Exchange rates

Mexico 3

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Mexico

Basic data

1,953,162 sq km

99.58m (mid-2000, Conapo estimate)

Population (m), 1995

Mexico City (capital) 16.4Guadalajara 3.3Monterrey 2.9

Tropical in the south, temperate in the highlands, dry in the north

Hottest month, May, 12-26°C (average daily minimum and maximum); coldestmonth, January, 6-19°C; driest month, February, 5 mm average rainfall; wettestmonth, July, 170 mm average rainfall

Spanish is the official language. Over 60 American Indian languages are alsospoken, mainly Náhuatl, Maya, Zapoteco and Mixteco

Metric system, also old Spanish measures

Peso. Average exchange rate in 1999: Ps9.56:$1; exchange rate in mid-April2000: Ps9.42:$1

6 hours behind GMT in Mexico City

January 1st, February 5th, March 21st, Maundy Thursday, Good Friday, May 1stand 5th, September 16th, October 12th, All Souls’ Day (partial), November20th, December 12th (partial) and 25th

Land area

Population

Main towns

Climate

Weather in Mexico City(altitude 2,309 metres)

Languages

Measures

Currency

Time

Public holidays

4 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Political background

Mexico has been ruled by the Partido Revolucionario Institucional (PRI) and itspredecessors since 1929. At one time strongly nationalistic, the regime hasembraced free-market policies and economic liberalisation since the mid-1980s. The PRI lost its absolute majority in the lower house of Congress for thefirst time in its history in the mid-term election in July 1997. Ernesto ZedilloPonce de León has been the country's president since December 1994.

Historical background

Mexico’s early history was characterised by the rise and fall of severalcivilisations including the Olmecs, Mayas and Aztecs. The Aztec empire wasbrought to an end by the Spanish conquistadores who made New Spain(comprising states of the US South-west, Mexico and Central America) a colonyin 1521. Independence was achieved in 1821.

Important recent events

January 1994: Peasant rebel uprising in Chiapas. Military threat is subsequentlycontained by the army.

March 1994: Assassination of Luis Donaldo Colosio, presidential candidate of the rulingPartido Revolucionario Institucional (PRI).

August 1994: Ernesto Zedillo Ponce de León, the PRI’s replacement candidate, iselected president.

December 1994: Mr Zedillo takes office. Precipitous devaluation of the peso leads tobanking crisis and deep recession in 1995.

July 1996: All political parties in Congress agree on constitutional changes toimplement a radical electoral reform, passed later in the year.

July 1997: National elections. For the first time in nearly 70 years the PRI loses itscontrol of the Chamber of Deputies. The election for the governorship of Mexico City,the first held since 1928, is won by Cuauhtémoc Cárdenas, of the Partido de laRevolución Democrática (PRD). The Partido Acción Nacional (PAN) also makesimportant advances, winning the governorships of Querétaro and the importantindustrial state of Nuevo León.

September 1997: The four opposition parties in Congress unite to outvote the PRI,creating a counter-weight to the executive branch of government.

1998-2000: The opposition continues to advance, but the PRI proves resilient. Of the17 governorships fought during 1998-99, five go to the opposition, including three tothe PRD (its first state governorships). The first-ever PRI presidential primary held at theend of 1999 boosted the party’s chances of winning the 2000 election.

Mexico 5

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Independence did not signal peace and prosperity. For more than a generationMexico was subject to civil wars and predatory incursions. Texas seceded fromMexico in 1835-36. In 1845 a war broke out with the US, which was to costMexico the additional loss of California, Arizona and New Mexico. In 1864France imposed a Habsburg archduke, Maximilian, as emperor. However, afterthe withdrawal of French troops in 1867, the archduke was quickly overthrownand executed. During the Porfirio Díaz dictatorship (1876-1911) order wasimposed and the economy was developed.

When General Díaz engineered, for the seventh time, his own re-election in1910, opposition forces led by Francisco Madero resorted to arms. They werejoined by rebel peasants under the leadership of Emiliano Zapata. General Díazwas forced into exile in 1911 and Mr Madero became president, but was oustedand killed in 1913. New rebellions followed, and although the rebels werecrushed, their ideals (such as land reform) were incorporated into the new(1917) constitution.

President Plutarco Elías Calles (1924-28) did much to shape future politicaldevelopments, particularly through the creation of the Partido NacionalRevolucionario (PNR). Another important presidency was that of LázaroCárdenas (1934-40), who carried out extensive land redistribution andexpropriated foreign oil companies.

In 1945 the official party was renamed the Partido Revolucionario Institucional(PRI). For many years sustained economic growth ensured the PRI a highdegree of popular support. A corporatist system was developed as the regimeco-opted potential opponents, such as the labour and peasant movements,although electoral fraud was sometimes resorted to in order to ensure absolutemonopoly of power. This political stability came under strain in the late 1960swhen intellectuals and students, influenced by left-wing ideals, sought apolitical opening but were repressed by the state. A deterioration in economicpolicy in the 1970s precipitated the external debt crisis of 1982. PresidentMiguel de la Madrid (1982-88) had to embark on a politically costly process ofstructural economic reform.

PRI presidential candidates were traditionally chosen by the outgoingpresident. In a bid to influence the decision, a section of the party, led by aformer PRI president, Porfirio Muñoz Ledo, and a former governor ofMichoacán, Cuauhtémoc Cárdenas (son of Lázaro Cárdenas), formed theCorriente Democrática. When Mr de la Madrid selected Carlos Salinas deGortari as the PRI candidate for 1988, the Corriente Democrática split from theparty. Mr Cárdenas stood in the election and managed to attract the support ofmost of the left for his Frente Democrático Nacional (FDN) alliance. Theofficial results, alleged to be fraudulent, gave Mr Salinas victory with only50.4% of the vote. (PRI governments had rarely announced victories of lessthan 85% prior to 1982.)

The 1988 presidentialelection is marred by

fraud allegations

Post-independenceinstability is followed by

a dictatorship—

—culminating in arevolution—

—which gives rise tothe PRI

6 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

President Salinas (1988-94) restructured the economy and recognised someelectoral gains by the opposition, such as governorships (monopolised untilthen by the PRI). The uprising in Chiapas of the Ejército Zapatista deLiberación Nacional (EZLN, the Zapatista National Liberation Army) in January1994 highlighted the fact that, despite economic progress, social tensions weremounting. Consequently, as well as negotiating with the EZLN, thegovernment enacted a comprehensive electoral reform, which included thegranting of autonomy to the Instituto Federal Electoral (the electoral authority)and other measures to diminish the possibility of electoral fraud.

The elections of August 1994 were the most transparent to date. Ernesto ZedilloPonce de León of the PRI won the presidential contest with 50.2% of all validvotes cast. Diego Fernández de Cevallos of the right-wing Partido AcciónNacional (PAN) polled 26.7%. Mr Cárdenas, who stood for the left-wing Partidode la Revolución Democrática (PRD), took 17.1% of the vote. In Congress thePRI held on to its majority, but it lost seats to both the PAN and the PRD.

Mr Zedillo (1994-2000) continued the process of political change. Progress onelectoral reform was slow, but a breakthrough was finally achieved in July 1996when representatives of all the parties in Congress—the PRI, the PAN, the PRDand the left-wing Partido del Trabajo (PT)—agreed to new election rules andapproved the necessary constitutional changes. However, the specificlegislation was approved by the PRI alone, because of disagreements over thelevel of public funding that political parties are allowed and restrictions placedon forming political coalitions. The government rejected the opposition’sattempts to modify the electoral law in time for the 2000 contest, making itimpossible for a last-minute coalition to be forged to stand against the PRI.

The new rules were tried for the first time in the 1997 mid-term congressionalelection. The governorships of six states and Mexico City were also disputed.For the first time in almost 70 years the PRI lost its majority in the Chamber ofDeputies. The most important gains were made by the PRD, which became thesecond most important force in the new Congress and won the governorshipof Mexico City. The PAN also won congressional seats and the governorships ofNuevo León and Querétaro (thus controlling six of the 31 states).

The four opposition parties that gained seats in the Chamber of Deputies inJuly 1997 united to control the Chamber but the alliance has proved fragile.The PAN and the PRD are too far apart ideologically for a formal coalition,although on some issues they provide a counter-weight to the powerfulpresident. Some opposition deputies defected to the PRI at the end of 1999 andin the first quarter of 2000.

Now that the economic crisis has passed, the PRI remains a popular choice,although the PAN and the PRD have made important gains. Of the 17governorships contested during 1998-99, 12 were won by the PRI, one by thePAN, three by the PRD (each of them in former PRI strongholds and withestranged PRI members as candidates) and one by a rainbow coalition headedby PAN and PRD. Thus, by the beginning of 2000 the opposition held the

Reforms acceleratein response to unrest

in 1994—

—when further importantelections are held

Patchy progress onpolitical reform in 1995

and 1996—

—brought important gainsfor the opposition in 1997

A multiparty democracy isemerging

Mexico 7

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

governorship of 10 states. Confidence in clean elections has increased, andcandidates and regional issues have become more important.

Distribution of seats in Congress

_ Chamber of Deputies_ Senate_________1994-97 1997-2000 1994-97 1997-2000

Partido Revolucionario Institucional (PRI) 300 246 95 76

Partido Acción Nacional (PAN) 119 117 25 33

Partido de la Revolución Democrática (PRD) 71 118 8 13

Partido del Trabajo (PT) 10 7 0 1

Partido Verde Ecologista de México (PVEM) 0 5 0 0

Independents/others 0 7 0 5

Total 500 500 128 128

Sources: Instituto Federal Electoral; EIU.

Since campaigning for the presidency, Mr Zedillo has said he wants a “healthydistance” between the government and the PRI. However, to implement adraconian and unpopular economic adjustment during 1995-96, the presidenthad to rally his party behind him. Important factions of the party are stillsympathetic to government intervention in the economy and, if these hadbeen allowed free rein, the PRI would have clashed with the government. InSeptember 1996 the PRI’s national assembly struck a blow against thetechnocratic wing by voting that presidential candidates must have held anelected post. The last president to fulfil such a condition was elected in 1964.Several attempts to lift that restriction during 1998-99 ended in failure becauseof resolute opposition by the traditionalist wing of the party.

After experimenting successfully since 1998 with a system of open primaries toselect its candidates for gubernatorial elections, the PRI set new rules tonominate its presidential candidate. Traditionally handpicked by the standingpresident, a privilege Mr Zedillo decided to end, the presidential candidate waschosen by PRI members as well as all registered voters at a national primaryelection held on November 8th. Four pre-candidates fought a tough campaign.Francisco Labastida Ochoa, who resigned as Interior secretary to run (and wasconsidered President Zedillo’s preferred candidate), won an overwhelmingvictory, carrying 272 of the 300 electoral districts, with Tabasco governorRoberto Madrazo managing a distant second with 21 districts. The turnout, at9.72 million was unexpectedly high. The PRI came through the unprecedentedexperiment successfully, suffering no divisions.

Main political figures

Ernesto Zedillo Ponce de León (48): President since December 1994 andde facto leader of the Partido Revolucionario Institucional (PRI). An economistby training with a doctorate from Yale University, Mr Zedillo is more atechnocrat than a politician. After a stint at the Banco de México (the centralbank) in 1978-87, he became under-secretary of planning and budget

The PRI and thegovernment remain

entangled—

—even though the PRI optsto choose its candidate in a

primary election

8 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

(1987-88). In the Salinas administration he was secretary of planning andbudget (1988-92) and education (1992-93). Manager of the presidentialcampaign of Luis Donaldo Colosio, Mr Zedillo was nominated in his placewhen he was assassinated. After a mismanaged devaluation in the first weeks ofhis administration, he demonstrated considerable political nerve and couragein dealing with subsequent financial and political crises. He was able to couplea draconian economic adjustment with a radical electoral reform, and hasmanaged to govern effectively while dealing with an opposition-dominatedCongress.

Francisco Labastida Ochoa (57): Became the PRI presidential nomineeafter wining convincingly in the November 1999 open primary. An economist,he has a long experience in the high echelons of government at federal andstate levels. In the cabinet he has held the interior (1998-99), agriculture(1995-98) and energy (1982-86) portfolios. He was governor of Sinaloa (1986-92) and ambassador to Portugal (1993-94). Despite being short of charisma,and his lack of resounding success during his tenure as interior secretary(including an inability effectively to counter the Zapatista movement), he isseen as a safe pair of hands who would govern effectively.

Esteban Moctezuma Barragán (46): Secretary-general of the PRI. Aneconomist who pursued graduate studies in the United Kingdom and Japan, hehas a long career in public service. Mr Moctezuma has forged close workingand personal relationships with both Mr Labastida (in the local government ofSinaloa) and Mr Zedillo (at the planning and budget and the educationministries). During the first months of the Zedillo administration he wasinterior secretary. He resigned after a short spell apparently owing to pressurefrom PRI hardliners. He was elected Senator in 1997, and in 1998 wasappointed social development secretary. He resigned from the cabinet to runthe Labastida campaign in 1999, and would occupy a leading political oreconomic position in the government if the PRI won the presidential election.

Cuauhtémoc Cárdenas Solórzano (66): Alliance for Mexico presidentialcandidate. Elected governor of Mexico City for 1997-2000, Mr Cárdenasresigned from that post to run for the third time for the presidency. He is theundisputed moral leader of the Partido de la Revolución Democrática (PRD). Asa PRI member he was senator (1976), under-secretary of agriculture (1976-80)and governor of Michoacán (1980-86). His main political asset appeared to bethat his father was Lázaro Cárdenas, a revered former president. When he leftthe PRI to run for president in 1988, he successfully united what had been afragmented left-wing opposition. After he lost an election marred by fraud, hisstature diminished during the Salinas administration and he achieved onlythird place in a relatively clean election in 1994. Making an impressivecomeback, he won the Mexico City election by a landslide. However, hislacklustre performance as governor and an inability to appeal to centrist votershave eliminated any chances he had of winning the presidency, despite beingsupported by a five-party coalition headed by the PRD. It is unclear howleft-wing political parties will evolve after his defeat, as for more than a decadeMr Cárdenas has dominated the left-of-centre political scene.

Mexico 9

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Vicente Fox Quesada (57): PAN and PVEM presidential candidate. Electedgovernor of Guanajuato in 1995, he has been campaigning for president foralmost three years (he officially resigned as governor in 1999). His declared aimof wresting the presidency from the PRI has made him a national figure. Abusinessman with a successful career at the Mexican subsidiary of Coca-Cola(he has a degree in business administration), Mr Fox joined the Partido AcciónNacional (PAN) relatively late in life, becoming congressman for Guanajuatoonly in 1988. His charismatic campaigning has been undermined by simplisticremarks and messianic postures, but his solid record as governor shows that hecan be an efficient executive. He is considered the only realistic option by anti-PRI voters. He is not popular among the leaders of his own party, but was ableto circumvent this by building a powerful parallel political movement. He wasalso nominated presidential candidate by the green Partido Verde Ecologista deMéxico (PVEM).

Constitution and institutions

The constitution of 1917, which is still in force, was a far more “social”document than that written in 1857. Apart from subordinating the rights ofprivate property to the public interest and making specific provision for landreform, it stressed the rights of labour. It also “nationalised” the church, greatlycurtailing the power and influence of the clergy.

The constitution established the framework for a federal system ofgovernment, which covers 31 states and the Federal District, and provided forthe separation of executive, legislative and judicial powers. In practice,government has been centralised and the president has had far greater powersthan Congress and considerable influence over the judiciary.

Congress consists of the Senate and the Chamber of Deputies. Senators servefor six years and deputies for three years. In the Chamber of Deputies 300 seatsare allocated on the first-past-the-post system and 200 by proportional repre-sentation. Reforms approved by Congress in 1996 made it easier for a singleparty to gain a working majority in Congress but harder to have the two-thirdmajority necessary to change the Constitution.

The most important political post in the cabinet is that of interior minister.The ministry is charged with preserving the country’s political stability. Thetop economics portfolio is that of the finance and public credit ministry,although the trade and industry ministry is also important.

Political forces

The two main opposition parties are the Partido Acción Nacional (PAN) andthe Partido de la Revolución Democrática (PRD). The PAN was founded in 1939and has built up a support base mainly in northern and central states andamong the urban middle classes, although it has diversified that base since theearly 1990s. It has always been associated with the Roman Catholic church.

A resilient constitution

The compositionof Congress

The ranking of ministries

Opposition partiesand groups

10 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Although inclined to free-market policies, it has also shown some populisttendencies. The leadership of Luis Felipe Bravo Mena, elected in March 1999,has been undermined by the authority of party chiefs in Congress and by thepresidential candidacy of Vicente Fox. The government has managed to reachagreements with PAN, but only after lengthy negotiations.

The PRD was formed in 1989 from the groups that supported Mr Cárdenas’spresidential bid in 1988. After his defeat in the 1994 election, the party lostground. Under the leadership of Andrés Manuel López Obrador (1996-99), theparty’s electoral fortunes improved, thanks partly to the protest vote against thegovernment over the economic crisis. In 1997 Mr Cárdenas easily won thegovernorship of Mexico City, and the PRD became the second most importantforce in Congress. The party has diversified its base by embracing disaffected PRImembers, wresting from the PRI control of states that were consideredimpregnable. Espousing a vague leftist rhetoric, it has made important gains byopposing virtually anything that the government proposes. The March 1999internal election to choose its new president was marred by fraud and had to beannulled. After another controversial election, Senator Amalia García waselected as the party leader in August 1999. Despite the efforts of leading partymembers, the presidential campaign of Mr Cárdenas has not won over voters.

A three-party system evolved during 1997-2000, with the small Partido delTrabajo (PT) and the green Partido Verde Ecologista de México (PVEM) on thefringes, occasionally forming alliances with the PAN or PRD on anti-PRI ticketsat elections. The support of the PT and PVEM deputies is crucial if the PAN andPRD are to secure a majority in the lower house of Congress, enabling bothparties to enjoy a certain amount of influence in government. Six additionalpolitical parties were granted official registry by the electoral authorities at theend of 1999: Partido de la Sociedad Nacionalista (PSN), Covergencia por laDemocracia (CD), Partido Alianza Social (PAS), Partido del Centro Democrático(PCD), Partido Auténtico de la Revolución Mexicana (PARM), and PartidoDemocracia Social (PDS). Both PCD and CD are small PRI splinters. PSN, CDand PAS joined the PRD and the PT to form the Alianza por México andsupport the presidential candidacy of Mr Cárdenas. PCD, PARM and PDS havenominated their own presidential candidates, bringing the total to six. It isunclear how Congress would function if no party attains a working majority,and all the 11 parties gain seats in the 2000-03 legislature.

Civic organisations have developed a degree of strength in recent years. Amongthem is the Barzón (Yoke) movement, which has been at the forefront of adebtors’ revolt. In addition, Mexico has two rebel groups: the Ejército Zapatistade Liberación Nacional (EZLN) based in Chiapas state and the Ejército PopularRevolucionario (EPR) based in Guerrero (which during 1998-99 divided intosplinter groups). No formal peace negotiations have taken place since 1996, asboth the government and the EZLN are unwilling to cede on certain questions.The Zapatistas are militarily cornered and have a small political base but aformidable propaganda machine. In September 1997 a political front—theFrente Zapatista de Liberación Nacional (FZLN)—was formally established, notto fight elections, but to mobilise national support for the principles espousedby the Zapatistas.

Forces outside parliament

Mexico 11

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Neither the church nor the military is a major participant in politics. In 1992the constitution was modified to give official recognition to the church. Sincethen several church leaders have made intermittent attempts to influencepublic policy, particularly on education, but have been rebuffed. Meanwhile,the military has become more prominent in civilian affairs.

International relations and defence

Mexico’s foreign policy is defined by its historical relationship with the US, towhich it lost almost half its original territory in the mid-19th century. Anti-USsentiment has remained strong since then. Nevertheless, the Salinas governmenttook Mexico into the North American Free-Trade Agreement (NAFTA), whichcame into force on January 1st 1994. The Clinton administration was quick tooffer help when Mexico ran into serious financial difficulties at the end of 1994,making $20bn available from the US Treasury. Relations between the twocountries have remained strong, despite the ever-present thorny issues of illegalmigration, drug-trafficking, money-laundering and Cuba.

The Salinas government also strengthened ties with other countries andeconomic blocs. The country was admitted as a full member of the Asia-Pacific Economic Co-operation forum (APEC) in 1993 and to the OECD in1994 (having joined GATT—now the World Trade Organisation (WTO)—in1986). Mexico has also pursued greater regional integration, entering intofree-trade agreements with Costa Rica, Bolivia, Venezuela, Colombia (1995),Nicaragua (1998), Chile (1992, 1998), the European Union and Israel (2000).

Negotiations to reach free-trade agreements (FTAs) are continuing with thegroup formed by Guatemala, Honduras and El Salvador, and in a bilateralmode with Belize, Panama, Ecuador, Trinidad and Tobago and Peru.Negotiations may start during 2000 aiming to reach FTAs with Japan andSingapore.

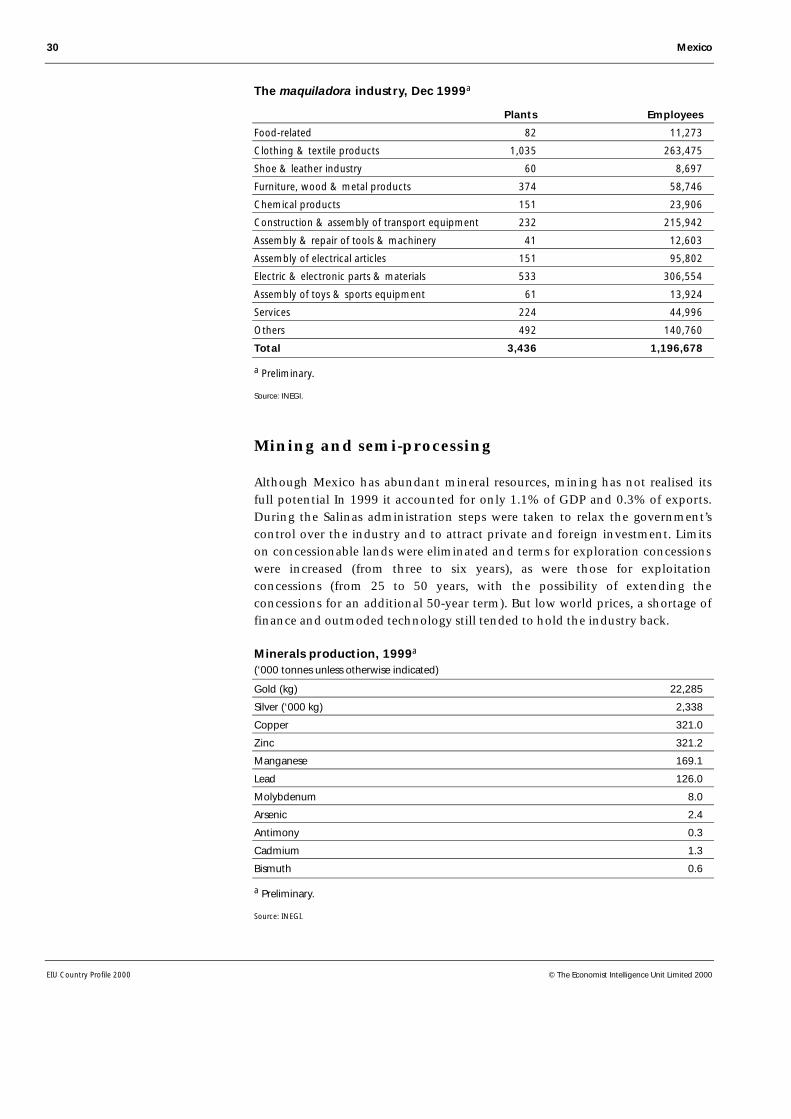

Armed forces, 1999

Active: 178,770

Reserves: 300,000

Army: 130,000 (60,000 conscripts—12 military regions; 41 zonal garrisons, onearmoured brigade; one presidential guard brigade, one motorised infantry brigade, twoinfantry brigades, anti-aircraft, engineering and support units.

Navy: 37,000—including 10,000 marines and 1,100 naval air personnel; 17 navalregions—six in the Gulf of Mexico and 11 in the Pacific; three destroyers and six frigates.

Air force: 11,770—including one squadron with ten fighters and 95 armed helicopters.

Relations with the US arebecoming stronger—

—as are those withother countries

12 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Although the armed forces are ill equipped to defend Mexico from externalaggression, their role in domestic affairs has increased over the last few years.In addition to waging a perennial war against drug-traffickers, they have beencalled on to contain the EZLN and EPR guerrillas and even to take on policingduties. Scandals related to corruption and human rights abuses, however, havetarnished the relatively unblemished image of the army. In 2000 authoriseddefence spending amounted to 0.4% of GDP.

Resources and infrastructure

Population

Mexico’s estimated population for mid-2000 is 99.58m. There has been aslowdown in the rate of population growth from more than 3% per year in theearly 1970s to 1.6% in the late 1990s. (For historical data on the population seeReference table 1.) This deceleration reflects declining fertility rates andimproved healthcare, which have lowered infant mortality rates. Annualpopulation growth is expected to be 1.5% in 2000.

At end-1997 an estimated 34.7% of the population was aged 14 years or under.Inevitably this results in pressure on the education system and labour market. (Forhistorical data on employment see Reference tables 2 and 3.) In 1997, 146,865Mexicans migrated legally to the US (163,572 in 1996), and in 1988-96 anestimated average of 150,000 per year did so illegally. In 1990 the number ofpeople of Mexican extraction living in the US was put at 13.5m, 4m-5m of whomwere born in Mexico. By the end of 1996 an estimated 2.7m illegal Mexicanimmigrants were living in the US. During 1998, 1m Mexicans were expelled by theUS authorities because of their illegal status (that number may be inflated bydouble counting, as many return to the US as soon as they are expelled).

States where at least 30% of the population is migrant(% of migrants in population of state)

Quintana Roo 53.4

Baja California 49.5

Estado de México 38.5

Morelos 35.4

Colima 34.7

Baja California Sur 33.7

Campeche 30.3

Federal District 30.1

Source: Instituto Nacional de Estadística, Geografía e Informática (INEGI), Conteo de Población y Vivienda.

Within Mexico, the search for better living standards has led to migration fromthe country to the cities, especially Mexico City, Monterrey and Guadalajara,but also in more recent times to northern maquiladora (in-bond assembly forre-export) towns such as Tijuana and Ciudad Juárez (that also function as

The armed forces’ priorities

Emigration to the US hasbeen substantial

Internal migration

Mexico 13

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

springboards to migrate illegally to the US), and tourist centres such asCancún. In 1990 some 71% of the population lived in urban areas.

Roughly 10% of the population are pure Indian. There are over 60 recognisedethnic and language groups (around 1% of the total population does not speakany Spanish). The most numerous are the Náhuatls (with 1.3m speakers),Mayas (800,000), Zapotecs and Mixtecs. The Indians’ customs and languagesdiffer greatly from one group to another, but their lot has generally been one ofexploitation, marginalisation and poverty.

Education

In 1998, 9.8% of the population aged 15 or over were illiterate. Althoughprimary education (for children aged between five and 11) is both free andcompulsory, recent records show that only six out of ten children have actuallybeen completing the course. Attendance at secondary school has been limitedand only a very small proportion of students have gone on to highereducation. In the 1999/2000 academic cycle Mexico had only 1,739 studentsper 100,000 population in higher education, compared with 5,404 in the US(1998 data). Education spending is around 5% of GDP, compared with 7% inthe US and Canada.

The Salinas government increased budget allocations for education andinitiated a programme to bring basic education up to date by revising thesyllabus and improving teachers’ training and pay. At the same time, secondaryschooling for children aged between 11 and 14 was made compulsory andtechnical training facilities were expanded. There are more than 4,800 centreswhere students can be trained for jobs in industry. As education minister in1992-94, Mr Zedillo carried out several of these policies. In August 1997, duringhis government, the Progresa programme (Programa de Educación, Salud yAlimentación) was introduced, providing additional subsidies to some of thepoorest families.

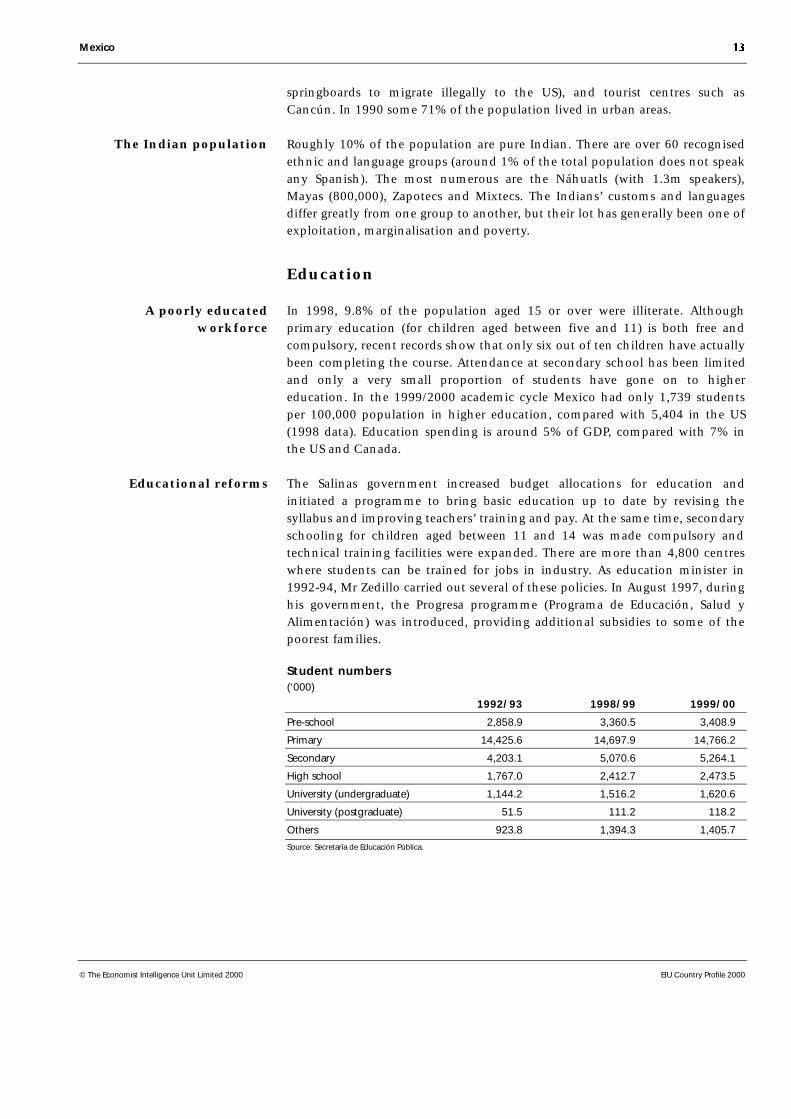

Student numbers(‘000)

1992/93 1998/99 1999/00

Pre-school 2,858.9 3,360.5 3,408.9

Primary 14,425.6 14,697.9 14,766.2

Secondary 4,203.1 5,070.6 5,264.1

High school 1,767.0 2,412.7 2,473.5

University (undergraduate) 1,144.2 1,516.2 1,620.6

University (postgraduate) 51.5 111.2 118.2

Others 923.8 1,394.3 1,405.7

Source: Secretaría de Educación Pública.

The Indian population

A poorly educatedworkforce

Educational reforms

14 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Health

Between 1970 and 2000 life expectancy at birth increased from 61 years to anestimated 75.3 years, while the infant mortality rate fell from 69 per 1,000 livebirths to 25 per 1,000. Universal vaccination programmes have helped toreduce cases of whooping cough and tuberculosis, and poliomyelitis has beenvirtually eliminated. Efforts continue to be made to curb outbreaks of choleraand the spread of AIDS. The government tries to counter malnutrition byproviding subsidised milk to 4.2m children and free school breakfasts for about4.6m children and by giving 1.16m families 1 kg/day of free tortillas (end-1999figures). Nevertheless, malnutrition remains a serious problem, particularly inremote rural areas.

The Instituto Mexicano del Seguro Social (IMSS) and the Instituto de Seguridady Servicios Sociales de los Trabajadores del Estado (ISSSTE) are the two mainproviders of healthcare. In 1999 officially 44.89m people were covered by theIMSS (with 14.56m affiliates paying contributions by the end of 1999). TheISSSTE, with 2.31m state workers affiliated to it, offered services to a further10.09m. The two organisations are funded by employers’ and employees’contributions, returns on investments and, in the case of the ISSSTE, transfersfrom federal government.

In addition to the IMSS and ISSSTE, some healthcare services are provided bythe defence and navy ministries, by the state oil company, Pemex, by stateorganisations such as the Institute for Indigenous People (INI) and the nationalsystem for Integrated Family Development (DIF), and by private institutions.About 4% of the population have private medical cover. Those not in the socialsecurity or private schemes, and without access to other providers, can obtainfree healthcare from the Secretaría de Salud (SSA, Ministry of Health) or theIMSS-Solidaridad anti-poverty programme.

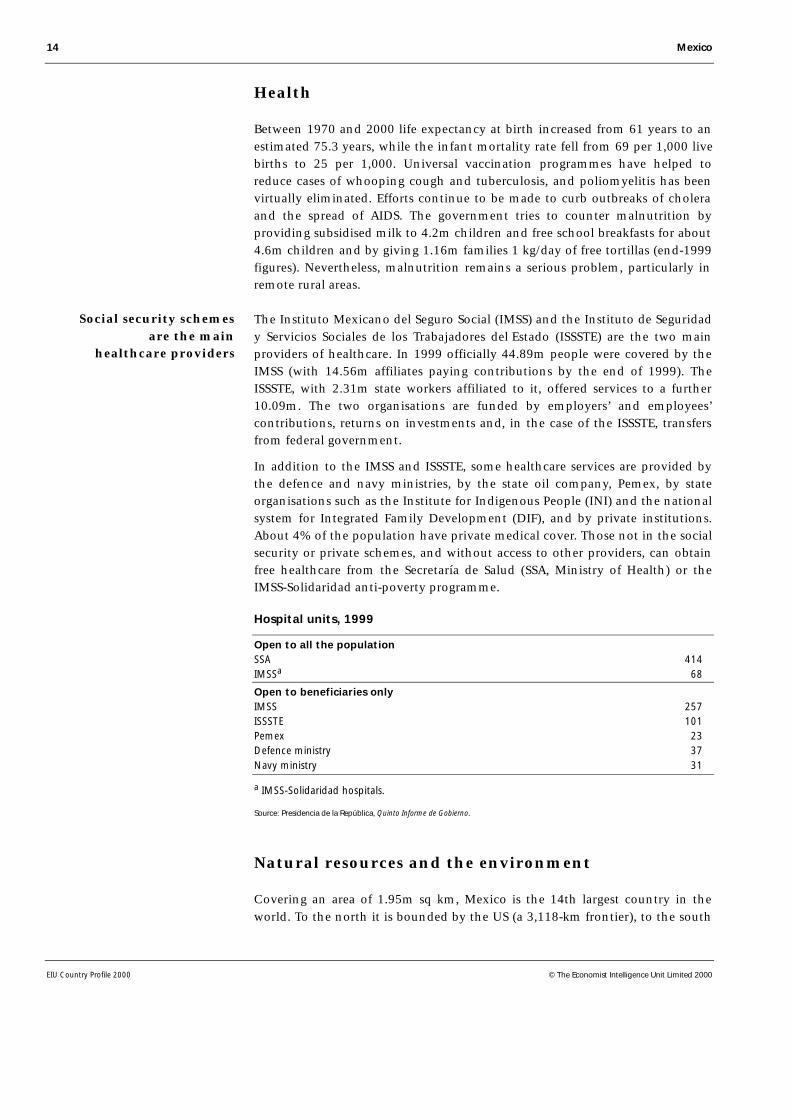

Hospital units, 1999

Open to all the populationSSA 414IMSSa 68

Open to beneficiaries onlyIMSS 257ISSSTE 101Pemex 23Defence ministry 37Navy ministry 31

a IMSS-Solidaridad hospitals.

Source: Presidencia de la República, Quinto Informe de Gobierno.

Natural resources and the environment

Covering an area of 1.95m sq km, Mexico is the 14th largest country in theworld. To the north it is bounded by the US (a 3,118-km frontier), to the south

Social security schemesare the main

healthcare providers

Mexico 15

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

by Guatemala (943 km) and Belize (249 km). The country’s western limit is thePacific coast (7,360 km), and its eastern limit comprises the Gulf of Mexico andCaribbean coasts (2,780 km).

The country’s topography is complex, ranging from coastal plains to volcanoesover 5,000 metres above sea level. More than one-half of the land area is over1,000 metres above sea level.

Because of its topography, climatic conditions in Mexico vary considerably. Butmuch of the country is dry, there are few large rivers and water resources areunevenly distributed.

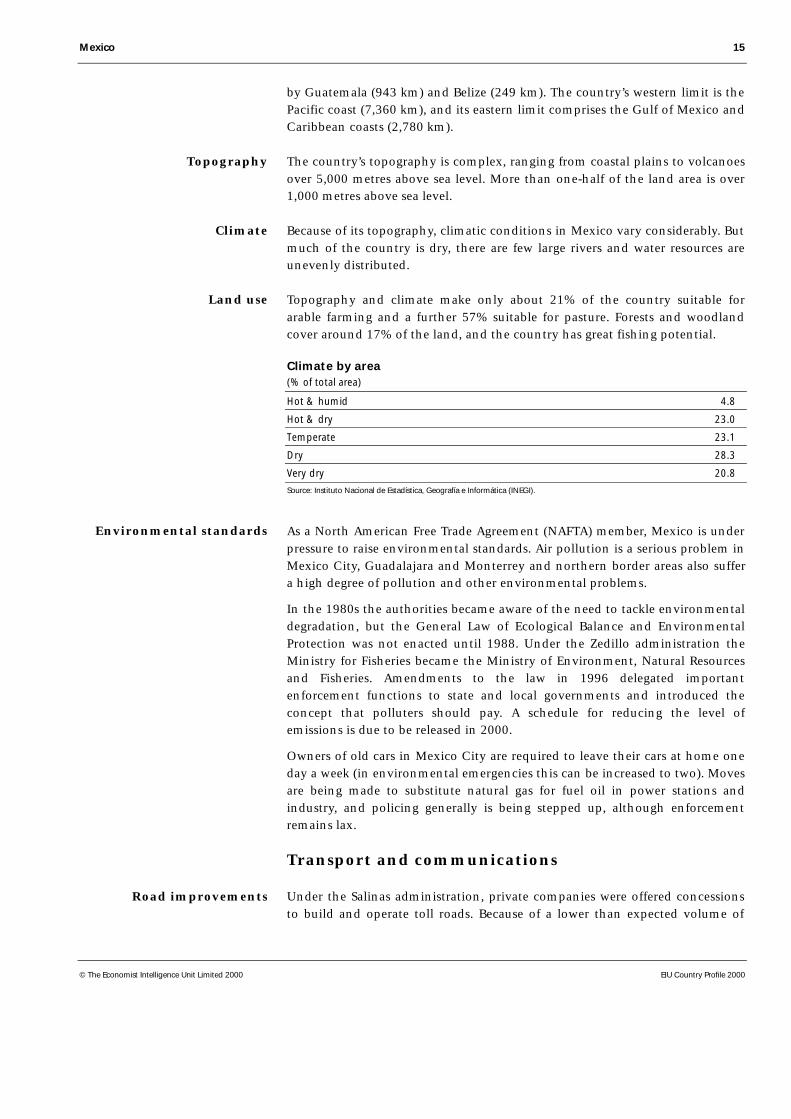

Topography and climate make only about 21% of the country suitable forarable farming and a further 57% suitable for pasture. Forests and woodlandcover around 17% of the land, and the country has great fishing potential.

Climate by area(% of total area)

Hot & humid 4.8

Hot & dry 23.0

Temperate 23.1

Dry 28.3

Very dry 20.8

Source: Instituto Nacional de Estadística, Geografía e Informática (INEGI).

As a North American Free Trade Agreement (NAFTA) member, Mexico is underpressure to raise environmental standards. Air pollution is a serious problem inMexico City, Guadalajara and Monterrey and northern border areas also suffera high degree of pollution and other environmental problems.

In the 1980s the authorities became aware of the need to tackle environmentaldegradation, but the General Law of Ecological Balance and EnvironmentalProtection was not enacted until 1988. Under the Zedillo administration theMinistry for Fisheries became the Ministry of Environment, Natural Resourcesand Fisheries. Amendments to the law in 1996 delegated importantenforcement functions to state and local governments and introduced theconcept that polluters should pay. A schedule for reducing the level ofemissions is due to be released in 2000.

Owners of old cars in Mexico City are required to leave their cars at home oneday a week (in environmental emergencies this can be increased to two). Movesare being made to substitute natural gas for fuel oil in power stations andindustry, and policing generally is being stepped up, although enforcementremains lax.

Transport and communications

Under the Salinas administration, private companies were offered concessionsto build and operate toll roads. Because of a lower than expected volume of

Topography

Climate

Land use

Environmental standards

Road improvements

16 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

traffic and the crisis that began in December 1994, the government had torevoke several of the concessions and at the same time offer financial assistanceto the companies.

Integral port administrations (APIs) were created in 1993. The administrationof each seaport was awarded by concession to an API, which can operate theport terminals and facilities and provide all related port services. The APIsbegan to be privatised in 1995, a process that has continued throughout theZedillo administration. Foreign investors may hold up to 49% equity in APIsand up to 100% equity in the provision of some port services.

The Salinas government managed to cut the losses of the state-owned railwaycompany, Ferrocarriles Nacionales (Ferronales); the Zedillo administration splitit up into regional companies and transferred the management of most ofthem to the private sector during 1997-98, under 50-year concessions.Excluded from the sale were small loss-making segments, and the railwaywhich runs through the Tehuantepec isthmus, because of its politicalsensitivity. The whole of the railway system was either in private hands orunder private management by the end of 1999. Ferronales officially closed itsdoors in August 1999.

The Airports Act became law in December 1995. The process of privatising 35airports, which deal with 97% of total passenger movements, started in 1998.The airports were divided into three groups for auction according to theirgeographical location (plus a special group for Mexico City). A minority (15%)but controlling share will be offered to strategic investors (which must includea foreign investor with experience in airport management), the rest of theshares being offered to the public on the stock exchange. The Airports Actallows for up to 49% foreign investment, although authorisation for highershares may be obtained.

Aeropuertos del Sureste (nine airports in six states, of which Cancún is thejewel in the crown) were the first to be auctioned. Managerial control was wonby a consortium with Mexican, Danish, French and Spanish capital inDecember 1998. A consortium of Mexican and Spanish capital won thebidding to manage Aeropuertos del Pacífico (12 airports including Guadalajaraand Tijuana) in August 1999. Aeropuertos del Centro-Norte (13 airports,including those serving Acapulco and Monterrey) will be handed over toprivate management in mid-2000. The privatisation of Mexico City airport hasbeen delayed because the government has still to decide on the location of anew airport to serve: in Texcoco (near the existing one) or in the Valley ofTizayuca, in Hidalgo. The sale will probably have to wait until the incominggovernment takes office. The placement of 85% of the shares in the privatisedairports’ groups on the stock exchange has been delayed several times, but issupposed to occur during 2000.

Port facilities

Airports

Railways

Mexico 17

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Transport and communications indicators, 1999

Roads (km) 365,119

Paved roads (km) 108,803

Vehicles (m registered) 14.49a

Railway track (km) 26,595

Rail passengers (m) 0.7

Rail freight (‘000 tonnes) 80,420

International airports (no.) 55

Domestic airports (no.) 29

Air passengers (m) 32.95

Air freight (‘000 tonnes) 431.0

Ports (no.) 108

Port facilities (docks in km) 176.5

Maritime passengers (m) 7.80

Shipping (‘000 tonnes handled) 240,419

Telephones (‘000 lines in service) 10,927

Cellular telephones (‘000 subscribers) 6,944a

Internet users (‘000 subscribers) 2,453b

a November 1999. b August 1999.

Sources: Banco de México; Instituto Nacional de Estadística, Geografía e Informática (INEGI); Secretaría de Comunicaciones yTransportes; Aeropuertos y Servicios Auxiliares; Caminos y Puentes Federales de Ingreso; Comisión Federal de Telecomunicaciones;Presidencia de la República, Quinto Informe de Gobierno.

In 1990 the government privatised Teléfonos de México (Telmex), which hassince greatly expanded the telephone network; the number of telephone linesincreased by 104% between 1990 and 1999. With privatisation cameconcessions for cellular telephone operations and in August 1996 the long-distance market was opened up to competition. Fifteen companies have wonconcessions to compete against Telmex in the local telephone service market.In October 1997 the government privatised Satélites Mexicanos (Satmex).

Energy provision

Mexico was the world’s fifth largest oil producer in 1999: output averaged3.34m barrels/day of crude oil and their liquid gas equivalent. Three types ofoil are sold: heavy Maya (22.3° API), Isthmus (34.6° API) and Olmeca (39.1°API). Official hydrocarbons reserves at the start of 2000 were 58.2bn barrels, ofwhich 46.2bn were crude oil and condensates and 12bn were the gasequivalent. Reserves have declined steadily over the past 15 years, reflecting acontraction in exploratory activity. About 56% of reserves are in the Gulf ofMexico, 24% in the Chicontepec region and 15% in Chiapas and Tabasco.

Oil exports did well in 1996 and 1997, as a result of higher volumes and prices,exceeding the $10bn mark for the first time since 1985. However, oil pricesstarted to plunge in December 1997 and remained extremely low (the lowest inreal terms since Mexico became an important oil exporter) until February 1999.This caused a negative shock, as crude oil is the second most important exportand the state oil company, Petróleos Mexicanos (Pemex), accounts for almost

Oil production

Communications

18 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

one-third (32.5% in 1999) of the federal government’s revenue. Prices started torecover in February 1999. The government had estimated an average price of$9.25/barrel for 1999 (for the so-called Mexican blend of crude) and the actualfigure was $15.62/b. The value of crude exports during the year was $8.86bn.During the first two months of 2000 the price averaged $24.34/b.

Outside companies have been brought in to undertake drilling operations forPemex, although to date they have been doing so under limited types ofservice and performance contracts as the constitution prohibits payment inkind and, by extension, payment tied to output. (For historical data on oil andgas production and reserves see Reference table 4.)

There has been a steady reduction of the company’s monopoly over theproduction of petrochemicals. Modifications to the constitution in November1996 restricted the state’s exclusive production rights to only eight basicpetrochemicals. The private sector may now participate in the production ofpetrochemicals (other than the eight reserved for the state) with 100% of theequity, but may hold only 49% of the equity in the plants owned by Pemex.However, this restriction has deterred investors and an attempt to sell the mostmodern complex in public hands (the Morelos complex) failed to attract anybidders in February 1999. Six other petrochemical complexes were supposed tofollow, but most probably the privatisation attempts will be abandoned, atleast until the next administration comes to power.

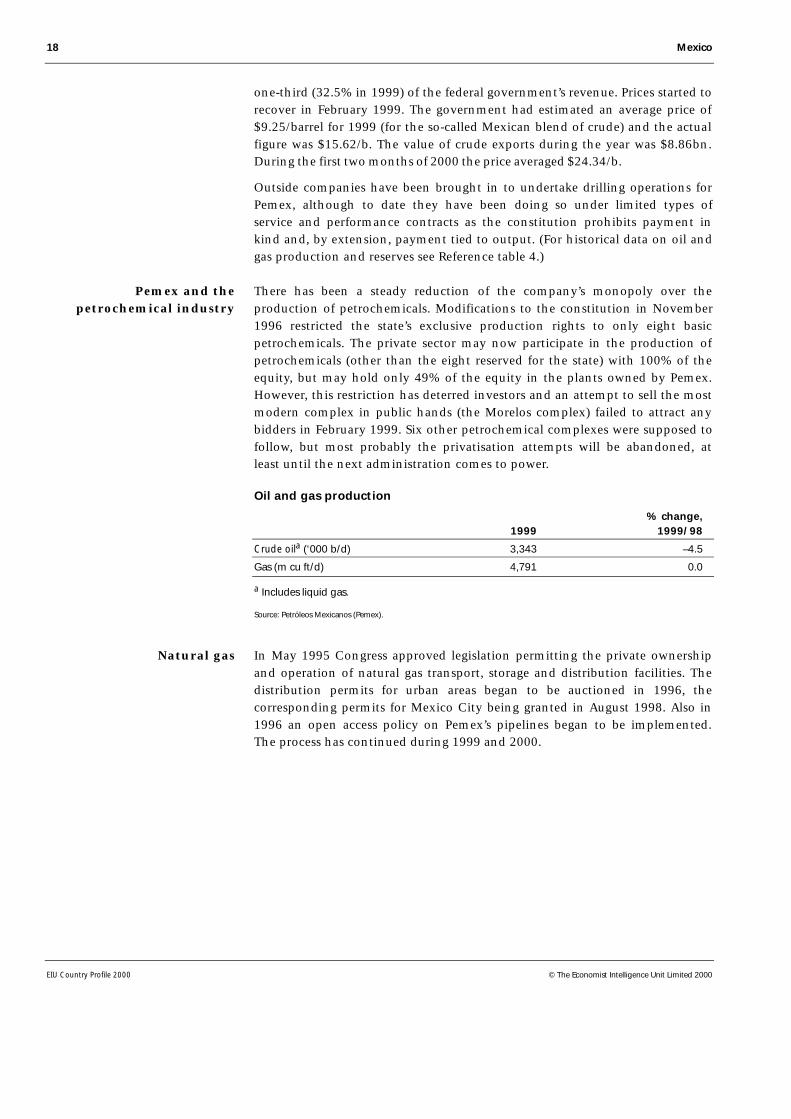

Oil and gas production

% change,1999 1999/98

Crude oila (‘000 b/d) 3,343 –4.5

Gas (m cu ft/d) 4,791 0.0

a Includes liquid gas.

Source: Petróleos Mexicanos (Pemex).

In May 1995 Congress approved legislation permitting the private ownershipand operation of natural gas transport, storage and distribution facilities. Thedistribution permits for urban areas began to be auctioned in 1996, thecorresponding permits for Mexico City being granted in August 1998. Also in1996 an open access policy on Pemex’s pipelines began to be implemented.The process has continued during 1999 and 2000.

Pemex and thepetrochemical industry

Natural gas

Mexico 19

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

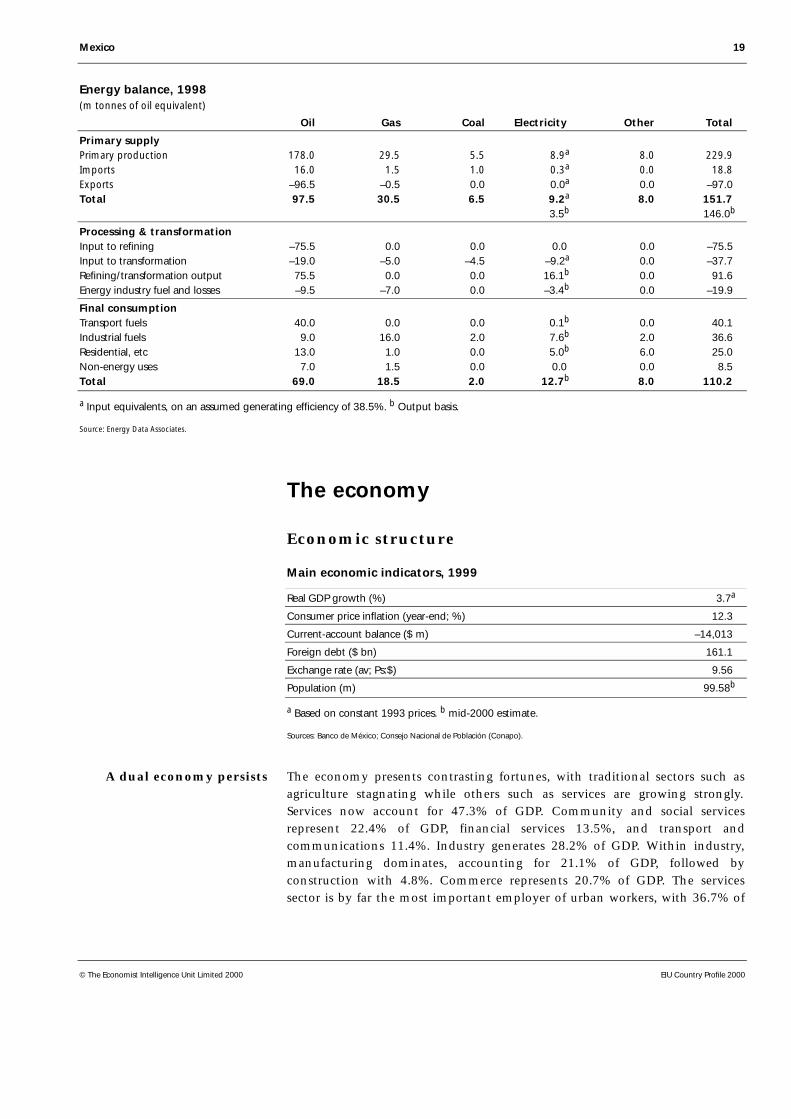

Energy balance, 1998(m tonnes of oil equivalent)

Oil Gas Coal Electricity Other Total

Primary supplyPrimary production 178.0 29.5 5.5 8.9a 8.0 229.9 Imports 16.0 1.5 1.0 0.3a 0.0 18.8 Exports –96.5 –0.5 0.0 0.0a 0.0 –97.0 Total 97.5 30.5 6.5 9.2a 8.0 151.7

3.5b 146.0b

Processing & transformationInput to refining –75.5 0.0 0.0 0.0 0.0 –75.5 Input to transformation –19.0 –5.0 –4.5 –9.2a 0.0 –37.7 Refining/transformation output 75.5 0.0 0.0 16.1b 0.0 91.6 Energy industry fuel and losses –9.5 –7.0 0.0 –3.4b 0.0 –19.9

Final consumptionTransport fuels 40.0 0.0 0.0 0.1b 0.0 40.1 Industrial fuels 9.0 16.0 2.0 7.6b 2.0 36.6 Residential, etc 13.0 1.0 0.0 5.0b 6.0 25.0 Non-energy uses 7.0 1.5 0.0 0.0 0.0 8.5 Total 69.0 18.5 2.0 12.7b 8.0 110.2

a Input equivalents, on an assumed generating efficiency of 38.5%. b Output basis.

Source: Energy Data Associates.

The economy

Economic structure

Main economic indicators, 1999

Real GDP growth (%) 3.7a

Consumer price inflation (year-end; %) 12.3

Current-account balance ($ m) –14,013

Foreign debt ($ bn) 161.1

Exchange rate (av; Ps:$) 9.56

Population (m) 99.58b

a Based on constant 1993 prices. b mid-2000 estimate.

Sources: Banco de México; Consejo Nacional de Población (Conapo).

The economy presents contrasting fortunes, with traditional sectors such asagriculture stagnating while others such as services are growing strongly.Services now account for 47.3% of GDP. Community and social servicesrepresent 22.4% of GDP, financial services 13.5%, and transport andcommunications 11.4%. Industry generates 28.2% of GDP. Within industry,manufacturing dominates, accounting for 21.1% of GDP, followed byconstruction with 4.8%. Commerce represents 20.7% of GDP. The servicessector is by far the most important employer of urban workers, with 36.7% of

A dual economy persists

20 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

the 1999 total, followed by manufacturing (22.7%) and commerce (20.6%).Construction employs 5.4% of the urban workforce, and the government 5.9%.

Agriculture accounted for 5% of GDP in 1999, but employed about 23% of thetotal workforce. Mining was equivalent to just 1.2% of GDP during 1999.However, that figure heavily understates the importance of oil production,particularly in terms of government revenue. Its price having recoveredstrongly during 1999, oil represented 7.3% of the total exports that year (6.1%in 1998; 10.3% in 1997) and 32.5% of total fiscal revenue (32.6% in 1998;36.4% in 1997).

Manufacturing is not only the most important productive sector, but also themain source of exports: 89.4% of the total during 1999 (although over half ofthe total, 52.2%, is produced in maquiladoras—in-bond assembly plants).

The informal sector is huge. Although estimates of its size and importance varywidely, it is telling that an estimated 15-25% (the precise number depends onthe month) of the urban workforce during 1999 worked, if at all, fewer than 35hours per week.

Although much is explained by the dynamism of the maquiladora industry, thegrowth in external trade has been impressive. The collapse in domestic de-mand in 1995 forced producers to redirect their production to overseasmarkets. This was facilitated by the North American Free Trade Agreement(NAFTA), which provided privileged access to the US and Canadian markets,and the competitive edge given by the peso devaluation. Combined exportsand imports soared, from 29.1% of GDP in 1993 to 57.6% in 1999.

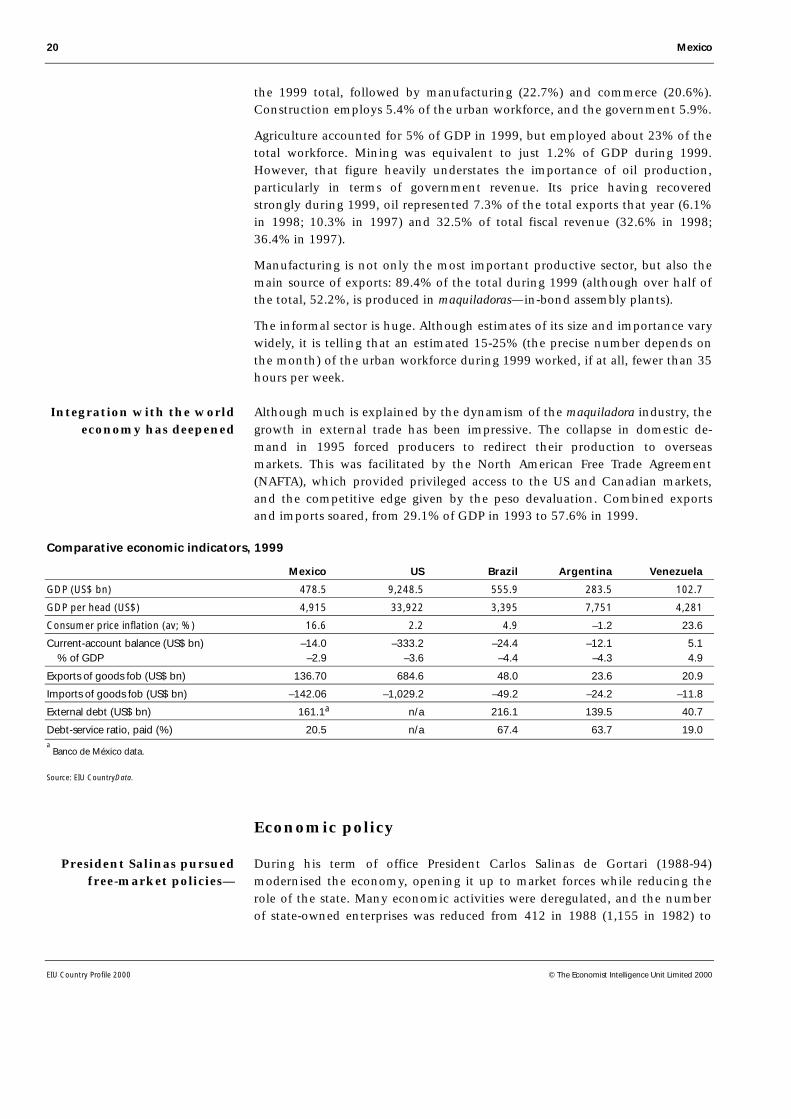

Comparative economic indicators, 1999

Mexico US Brazil Argentina Venezuela

GDP (US$ bn) 478.5 9,248.5 555.9 283.5 102.7

GDP per head (US$) 4,915 33,922 3,395 7,751 4,281

Consumer price inflation (av; %) 16.6 2.2 4.9 –1.2 23.6

Current-account balance (US$ bn) –14.0 –333.2 –24.4 –12.1 5.1 % of GDP –2.9 –3.6 –4.4 –4.3 4.9

Exports of goods fob (US$ bn) 136.70 684.6 48.0 23.6 20.9

Imports of goods fob (US$ bn) –142.06 –1,029.2 –49.2 –24.2 –11.8

External debt (US$ bn) 161.1a n/a 216.1 139.5 40.7

Debt-service ratio, paid (%) 20.5 n/a 67.4 63.7 19.0a Banco de México data.

Source: EIU CountryData.

Economic policy

During his term of office President Carlos Salinas de Gortari (1988-94)modernised the economy, opening it up to market forces while reducing therole of the state. Many economic activities were deregulated, and the numberof state-owned enterprises was reduced from 412 in 1988 (1,155 in 1982) to

Integration with the worldeconomy has deepened

President Salinas pursuedfree-market policies—

Mexico 21

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

215 in 1994. The trade liberalisation begun by Mr Salinas’s predecessor, Miguelde la Madrid, was consolidated and enhanced by free-trade pacts, notablyNAFTA, and foreign investment rules were made more attractive.

Mr Salinas’s government was successful in reducing the rate of inflation from52% in 1988 to 7% in 1994, by exploiting the corporatist structure of thePartido Revolucionario Institucional (PRI) to extract concessions from the mainlabour and peasant unions and business organisations on fiscal cuts and wagerestraint. This took the form of an incomes policy known as the pacto. Apublic-sector borrowing requirement (PSBR) of 12.5% of GDP in 1988 had beenturned into a surplus of 0.5% of GDP by 1992 (3.2% including privatisationrevenue), although there was some fiscal relaxation in the next two years.Lower inflation led to lower interest rates, which in turn helped the fiscalaccounts by lowering the cost of domestic debt service. (For details of public-sector finances see Reference tables 5 and 6.)

A reduction in interest rates was also assisted by the liberalisation of thefinancial markets, specifically, the lifting of interest-rate controls and thegradual phasing out of cash reserve requirements. In 1991-92 the governmentprivatised its 18 commercial banks, and in 1993 it allowed the establishment ofnew domestic banks. In 1994 access was granted to foreign banks (albeit onlythose operating in the US and Canada), the object being to improve theavailability of credit and drive intermediation margins down throughcompetition. In April 1994 the Banco de México (the central bank) becameindependent. However, the finance ministry retained control over exchange-rate policy, creating a possible source of conflict. A proposal put to Congress(which may be approved during 2000) would give the central bank full controlover exchange-rate policy. (For historical data on money, credit and interestrates see Reference tables 7 and 8.)

The exchange rate was unified in November 1991 and exchange controls wereabolished. The existing policy of a daily depreciation was retained, although itapplied to the ceiling of a band in which the peso was allowed to float. (Forhistorical data on the exchange rate see Reference table 30.)

The Salinas government stuck resolutely to its exchange-rate policy eventhough trade liberalisation and economic growth produced ever-larger tradeand current-account deficits. It was argued that the size of the current-accountdeficit was not important, as public finances were in balance; therefore a deficitreflected the dynamism of the private sector, and if capital ceased to flow intothe economy, the current account would adjust accordingly. In 1994 thegovernment rolled over domestic debt by issuing $29.2bn of dollar-linkedbonds, known as tesobonos, to try to halt a loss of reserves. Investors becameincreasingly skittish as the euphoria that had built up over Mexico’s economicprospects dissipated when political shocks struck in an election year.Eventually the exchange-rate policy ceased to be tenable.

Only three weeks into its term in office, on December 20th 1994, the Zedillogovernment devalued in effect by lifting the exchange-band ceiling by 15%.

—and greater fiscaldiscipline

Financial markets wereliberalised—

—but exchange-rate policyeventually proved to

be flawed—

—forcing the Zedillogovernment to devalue

22 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Billions of dollars left the country in a few hours. With reserves depleted, thepeso was floated, and a financial meltdown seemed imminent. The peso ended1994 at Ps5.325:$1.

The peso continued to plunge in the first few weeks of 1995, as economicagents feared (correctly) that the government lacked enough resources to paythe $29bn of tesobonos falling due in 1995. The solvency of the banking systembecame another cause for concern. Banks now faced a huge increase in externaldebt-servicing costs (as a result of the devaluation) and an escalation in baddebts as the government forced interest rates up to try to keep foreign anddomestic capital in the country.

In January 1995, after several days of further uncertainty, the governmentagreed with labour and business on an emergency economic plan, whichconsisted of a tighter fiscal and monetary stance and wage restraint. On thestrength of this plan the US contributed $20bn, the Bank for InternationalSettlements (BIS) $10bn and the IMF offered in total $17.8bn. However, inMarch the government was forced to redouble its adjustment efforts. Value-added tax (VAT) was raised from 10% to 15% and public (government-set)prices were increased, public spending was cut and a tight lid was kept on wagerises. Despite a contraction in GDP of 6.2%, a non-financial public-sectorsurplus of 0.7% of GDP was achieved, an improvement on the previous year’sPSBR of 3.4% of GDP. However, this included only a fraction of the cost of thebank bail-out. At the end of 1999, that cost, which will be eventually absorbedas internal public debt or written down over a 30-year period, was equivalentto 18.3% of GDP.

The government stuck to a policy of fiscal and monetary prudence in 1996.Inflation was nearly halved, from 52% at the end of 1995 to 27.7% a year later.Public finances were almost in balance, the non-financial public sector posting adeficit of 0.1% of GDP. This required reining in spending to compensate for therising cost of supporting the banking system and for defaults on tax payments.The central bank kept within its restrictive target for monetary growth.

Although the government seemed to consider the free-floating peso as atransitional phase, over time confidence and reserves were restored, andexchange-rate volatility gave way to extended periods in which the pesoremained relatively stable. The inflation target for 1997 of 15% was almostachieved. During the year public finances registered a deficit (including costsrelating to reform of the social security system incurred during the second halfof the year) slightly above the 0.5% of GDP goal.

Although initially costly, that reform is at the heart of the growth strategypresented in the Programa Nacional de Financiamiento del Desarrollo(Pronafide), which in essence involves increasing savings and investment. Themain feature of the new capitalisation pension system is that a worker’spension benefits will depend on the contributions made by workers to theirindividual pension accounts. The accounts will be managed by retirement fundadministrators (afores) of the contributor’s choosing. Seventeen afores, most ofthem allied with foreign companies, started operation during 1997.

There was little scope forrelaxation in 1996

The adjustment continuedin 1997—

Mexico 23

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Public-sector balance, 1999(Ps m unless otherwise indicated)

Federal government –80,041

Public entities under direct budget control 27,997 Pemex 5,031 Others 22,966

Budget balance –52,044

Balance of entities under indirect budget control –465

Overall balance –52,509 % of GDP 1.1

Source: Secretaría de Hacienda y Crédito Público.

During 1998 the peso was much more volatile. Oil prices collapsed and Mexicowas affected by the economic crisis in South-east Asia. The Russian financialmeltdown of August 1998 was the heaviest blow. The peso depreciated sharply,throwing the economy off course. Several times during the year the Banco deMéxico tightened monetary policy, leaving the money market “short” byincreasing amounts and requiring compulsory deposits from commercial banksin order to establish greater influence over interest rates. The governmenttightened fiscal policy. Three budget cuts were implemented in January, Marchand July, totalling Ps36.2bn ($4bn or 1% of GDP). Despite tight money andspending cuts, the economy managed to grow by 4.8% during 1998 (althoughgrowth had clearly lost momentum by the end of the year). At 1.25% of GDP,the deficit of the non-financial public sector closed precisely on target.However, the downward trend of inflation was broken and it ended 1998 at18.6%, well above the originally expected 12%.

Although the peso was affected by the devaluation of the Brazilian real inJanuary, it quickly recovered, even regaining some of the ground lost after theRussian devaluation. Economic agents began to believe the government’srepeated claims that Mexico was fundamentally stronger than other emergingmarkets. As the government kept its fiscal accounts under control, the pesoremained stable throughout the rest of 1999, aided by increasing oil prices anda diminishing trade-account deficit (assuaging fears of over-valuation).Inflation ended the year at 12.3%—below the official target of 13%—whileeconomic growth of 3.7% was higher than the 3% target. Both goals had beenconsidered optimistic by private analysts at the beginning of 1999.

The 1999 macroeconomic performance strengthened the government’s credi-bility. There is no doubt that during its last months in office, the Zedillo ad-ministration will not deviate from the consistent course it has followed. It isunable to implement radical changes during 2000, as the electoral contest hasreduced the incentive for the Partido Acción Nacional (PAN) to co-operate injoint initiatives—arguably the full opening of the electricity sector to privateinvestment was the most important victim of that lack of co-operation.Nevertheless, the government will be able to maintain its economic course.Barring an abrupt downturn of the US economy, the 4.5% growth target for2000 looks attainable (industrial production grew by 8.1% during January). Theinflation target for December 2000, 10%, should be reached by April, althoughthe trend in the rest of the year will depend on the stability of the peso.

—which bore fruitduring 1999

—and with redoubledefforts in 1998—

24 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Whatever the macroeconomic outturn for 2000, Mexico should have ended thecycle of economic crises coinciding with changes of government.

Orthodox economic policies were discredited by the 1994-95 crisis but haveregained public support during the recovery and no major party is proposing acredible alternative. The incoming president will not change the general thrustof economic policy. A potentially unruly and opposition-dominated Congress,however, will pose problems for the new government.

Economic performance

In 1992 the delayed effects of the US recession, together with theovervaluation of the peso, held real growth of exports of goods and services at5%, while imports of goods and services increased by 19.6% in real terms.The deterioration in the net foreign balance was mainly responsible for aslowdown in GDP growth to 3.6%. In 1993 the arrival of the Clintonadministration in the US brought uncertainty with respect to approval of theNorth American Free Trade Agreement (NAFTA). This had a directimpact on investment decisions. It also exerted upward pressure on domesticinterest rates and exacerbated the problem of growing bad debts. Banksresponded by restricting lending. Following a recovery in the US and slackdemand at home, exports grew by 8.1% in real terms and imports by 1.9%.GDP growth was 1.9%. (For historical data on GDP see Reference tables 9-11.)

In 1994, an election year, public consumption grew by 2.9% and publicinvestment by a similar amount. NAFTA helped to revive private investment,despite political upheavals, and to boost exports, which grew by 9.8% and17.8% respectively in real terms. The recovery in domestic demand sentimports up again, limiting GDP growth to 4.5%.

The financial crisis at the end of 1994 had a profound effect on the economyin 1995. High real interest rates, tight monetary policy and the loss of businessconfidence choked private investment. Swingeing fiscal cuts meant sharp fallsin public investment and spending. In August the official (very narrow)measure of open urban unemployment reached 7.6% before falling to 5.2% inDecember, well above the 3.2% recorded at the end of 1994. Inflation—fuelledby the weakness of the peso—eroded wages, and private consumptioncollapsed. GDP contracted by 6.2%, the worst recession experienced by thecountry since the Great Depression. The only positive developments werein the external sector, where a surge in exports was accompanied by a fallin imports.

Uneven growth in1992-94—

—followed by recessionin 1995

Mexico 25

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Gross domestic product(% real change; constant 1993 prices)

Annual average1990-95 1996 1997 1998 1999a

Private consumption 2.1 2.2 6.5 5.4 4.3

Government consumption 2.5 –0.7 2.9 2.2 1.0

Gross fixed investment 2.0 16.4 21.0 10.3 5.8

Exports of goods & services 8.2 18.2 10.7 12.1 13.9

Imports of goods & services 11.9 22.8 22.7 16.5 12.8

GDP at market prices 2.2 5.2 6.8 4.8 3.7

a Preliminary.

Sources: Instituto Nacional de Estadística, Geografía e Informática (INEGI); Banco de México.

The increase in exports helped to lift the economy out of recession in 1996.Private consumption was held back by declining real wages andunemployment, which remained stubbornly high. At the same time a hugedebt overhang depressed both private consumption and investment. There wasa credit crunch as domestic banks struggled to deal with non-performing loansand to build up capital and reserves. But inflation fell from 52% in December1995 to 27.7% at the end of 1996.

The economic recovery broadened and strengthened in 1997, with GDPgrowth of 6.8%, the highest rate since 1981, and inflation falling at year-end to15.7%. Mexico attracted record levels of foreign direct investment. Privateconsumption finally recovered, thanks to job creation and a rebound in realearnings. New investment and strong demand in the US ensured that exportscontinued to contribute to output growth.

Inflation(% change, year on year)

1995-991999 Annual average

Consumer prices 16.6 24.5

Source: Banco de México.

Although GDP growth lost momentum at the end of the year, it continued tobe strong during 1998. Fuelled by the private sector (consumption, investmentand exports), GDP grew by 4.8%. In response to the plunge in oil prices thegovernment restricted spending; public consumption rose by only 2.2% andgross fixed investment by 10.3%. The year-end inflation rate edged up to18.6%. The government’s tight fiscal stance continued during 1999, withpublic consumption increasing by just 1%. Again the private sector was theengine of growth: private consumption rose by 4.3% and exports by 13.9%,with GDP growing 3.7%, as inflation fell to 12.3% by the end of the year (Forhistorical data on inflation see Reference table 12.)

The partial recoveryin 1996—

—strengthened in 1997and 1998

26 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Regional trends

Regional development has been uneven, industrialisation and the decline ofagriculture sharpening the divisions that exist between different areas as aresult of their varied natural resource endowments and location.

The Federal District, which includes the capital, Mexico City, accounted for noless than 23% of GDP and 21% of manufacturing value added in 1997 (morerecent data are not available). The central region, which includes the FederalDistrict and the state of Mexico bordering it, accounts for nearly one-third ofGDP despite the fact that it covers only 1.2% of the land area. The next mostimportant economic zones are the north-east and the centre-north and west.Monterrey (Nuevo León) and Guadalajara (Jalisco) are the leading industrialcities after the capital. On the Gulf coast, Veracruz has developed on the backof agricultural and, more importantly, oil resources.

The thriving maquiladora industry (in-bond assembly for re-export) has boostedemployment in the northern border area, but some states such as Chiapas,Hidalgo, Guerrero and Oaxaca are still suffering extreme poverty. Tijuana, inBaja California, and Ciudad Juárez, in Chihuahua, have evolved into importantmaquiladora cities.

The inadequate transport and communications infrastructure has impededmore balanced regional growth. However, the present government is continu-ing the infrastructure improvements begun by its predecessor. The 1998 budgetincluded the creation of a new item, Ramo 33, through which the resources forexpenditure in basic education, health services and municipal infrastructureare transferred to states and local governments. That has brought an enormousincrease in the number of transfers from the central to state and localgovernments. Moreover, those transfers are evenly spread throughout the year(previously a large proportion was allocated during the last quarter of the year).State and local governments account for only about 1% of national tax andsocial security collections, compared with 32% in the US and 25% in Japan.However, a proposal in the 1999 and 2000 budgets to allow states to top up theVAT rate by up to 2% was rejected by the opposition and scrapped. From April2000 the restrictions that state governments faced on issuing debt will beeased. That debt will be graded by rating agencies, aiming to make the processmarket-oriented.

Economic sectors

Agriculture, forestry and fishing

Although northern parts of Mexico are very dry, suffering drought for five orsix years out of ten, they have become the most productive areas for agri-culture, not only because these areas benefited most from the public irrigationschemes of the 1950s and 1960s, but because the larger farms established here

The importance of theFederal District

Regional inequalitiesremain severe—

—despite infrastructureimprovements and

federal transfers

Reforms are introduced inland ownership—

Mexico 27

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

have increasingly geared production for the US market. Farms in the centreand south have lagged behind, partly as a result of the legacy of agrarianreform there: large landholdings were divided up into ejidos and allocated asunits to individuals or communes by the government, could not be sold,rented or mortgaged, only inherited, and were liable to expropriation if notworked upon. The system caused increasing fragmentation of farming units,insecurity and inefficiency. The Salinas government amended the constitutionin 1992, paving the way for ejidatarios (owners of ejidos) to be given fullproperty rights to over 9m plots on the 30,000 ejidos that account for half thecountry’s area. Under the Programa de Certificación de Derechos Ejidales yTitulación de Solares (Procede) the agrarian reform ministry and the agrariantribunals had, by the beginning of 2000, provided ownership titles to 6mejidatarios (2.6m families), covering 49m ha.

The Salinas government also privatised sugar mills, the tobacco company andparts of the national basic foods supply company, Conasupo (which disap-peared in 1999). In 1993 a new scheme, Procampo, was introduced to replacethe former system of price support for basic grains, providing yearly cashpayments for 15 years to producers of cotton, rice, safflower, barley, beans,maize, sorghum, soybeans and wheat.

Inadequate investment and low productivity continue to affect agriculture,exacerbating the extreme poverty in rural areas. Its growth has consistentlyunderperformed that of the rest of the economy (growing by 0.2% in 1997, 0.8%in 1998 and 3.5% in 1999), and as a proportion of total GDP it fell from 5.8% to4.5% between 1993 and 1999. At the same time, Mexico has tended to rundeficits in its foreign trade in agricultural products. Between 1992 and 1998 asurplus was registered (in 1995 only because of recession and the effect of thedevaluation). During 1999 the deficit was $364m ($845m during 1998). In 1995President Zedillo initiated the Alianza para el Campo (Alliance for theCountryside) programme, reinforcing the Procampo system of direct cashsubsidies by providing that these should be maintained in real terms for 15 years.

To support its agricultural programme, the government has raised the level offinancing per hectare and is improving the flow of credit from state agencies.In 1996 it also had to step in with a rescheduling plan for debtors in thefarming and fishing industries as well as providing emergency funding to helpthe sector confront the third consecutive year of drought. The Punto Finalprogramme instituted at the end of 1998 and ended a year later reinforced thisobjective (see Economic sectors: Financial services).

Despite the problems in agriculture, Mexican crop production is among thehighest in the world. Overall it accounts for more than 50% of agriculturaloutput. Maize, beans, wheat and sorghum are important for the domesticmarket and coffee, sugar, fruit and vegetables are the leading agriculturalexports. Production of some traditional crops has declined. In 1999 the maizeharvest yielded 15.7m tonnes, (16.9m in 1998 and 18.1m in 1997). Wheatproduction was 3m tonnes (down from 3.2m in 1998, 3.6m in 1997). Sugarcane production reached 46.8m tonnes in 1999, below the 49.3m of 1998 (buthigher than the 44.8m of 1997). At 1m tonnes in 1999, beans were at the same

—and in the role ofthe state

Crop production is themost important activity

28 Mexico

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

level as 1997, but below the 1.2m tonnes of 1998. Livestock contributes about30% of agricultural output. In 1999 meat production, the most important,increased by 4.1% to a record 4.2m tonnes; milk production increased by 6.1%to 9bn litres, also a record. (Historical data on agricultural and livestockproduction are in Reference tables 13 and 14.)

Forestry accounts for about 21% of sectoral output. Over-exploitation and lackof investment and planning have hindered the industry’s growth in recenttimes (widespread fires during 1998 were an added problem), but the reform ofthe land tenure system should improve its fortunes.

The potential of fishing is a long way from being realised. Output has declined:during 1999 the catch was 1.27m tonnes, just above the 1.23m of 1998, butwell below the 1.57m of 1997. Among the main types of fish caught are tuna,prawn, sardine and squid. Domestic consumption is not high (10.2 kg per headin 1999, down from 10.7 kg in 1998 and 13 kg in 1997). The trade balance hasshown consistently a surplus for several years ($516m during 1999). Exports(prawns are by far the most important) brought in $672m in 1999 ($676m in1998 and $784m in 1997). The fishing fleet, which totalled 102,807 vessels in1998, and the country’s 62 fishing ports are in need of modernisation.

Manufacturing

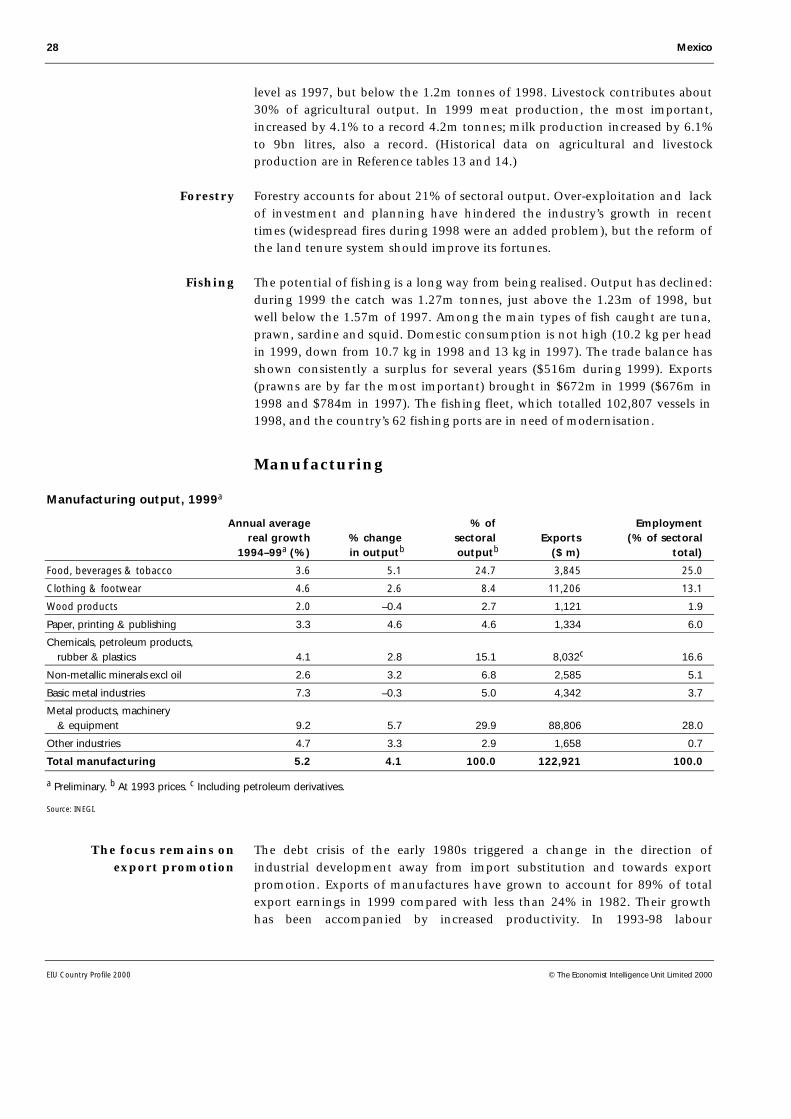

Manufacturing output, 1999a

Annual average % of Employmentreal growth % change sectoral Exports (% of sectoral

1994–99a (%) in outputb outputb ($ m) total)

Food, beverages & tobacco 3.6 5.1 24.7 3,845 25.0

Clothing & footwear 4.6 2.6 8.4 11,206 13.1

Wood products 2.0 –0.4 2.7 1,121 1.9

Paper, printing & publishing 3.3 4.6 4.6 1,334 6.0

Chemicals, petroleum products, rubber & plastics 4.1 2.8 15.1 8,032c 16.6

Non-metallic minerals excl oil 2.6 3.2 6.8 2,585 5.1

Basic metal industries 7.3 –0.3 5.0 4,342 3.7

Metal products, machinery & equipment 9.2 5.7 29.9 88,806 28.0

Other industries 4.7 3.3 2.9 1,658 0.7

Total manufacturing 5.2 4.1 100.0 122,921 100.0

a Preliminary. b At 1993 prices. c Including petroleum derivatives.

Source: INEGI.

The debt crisis of the early 1980s triggered a change in the direction ofindustrial development away from import substitution and towards exportpromotion. Exports of manufactures have grown to account for 89% of totalexport earnings in 1999 compared with less than 24% in 1982. Their growthhas been accompanied by increased productivity. In 1993-98 labour

Forestry

Fishing

The focus remains onexport promotion

Mexico 29

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

productivity in manufacturing rose by an annual average of 6.3% (comparedwith 4.4% in the United States and 8.7% in Germany). However, the exportbase has remained rather narrow. At the same time, Mexico’s dependence onimported intermediate goods has meant that export growth has inflated theimport bill.