mf0002 set 1&set2

TRANSCRIPT

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 1/20

MBA – FINANCE

Semester 3

MF0011 – Mergers And Acquisitions

Assignment Set- 1

Submitted By :

Student Name : Yogesh Kumar

Roll No : 521056970

LC Name & Code : NIPSTec Ltd. 1640

Date of Submission : 20/12/2011

Q.1.What are the basic steps in strategic planning for a merger?.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 2/20

Ans.

BASIC STEPS IN STRATEGIC PLANNING IN MERGER

Any merger and acquisition involve the following critical activities in strategic planning

processes. Some of the essential elements in strategic planning processes of mergers andacquisitions are as listed here below :

1. Assessment of changes in the organization environment

2. Evaluation of company capacities and limitations

3. Assessment of expectations of stakeholders

4. Analysis of company, competitors, industry, domestic economy and international economies

5. Formulation of the missions, goals and polices

6. Development of sensitivity to critical external environmental changes7. Formulation of internal organizational performance measurements

8. Formulation of long range strategy programs

9. Formulation of mid-range programmes and short-run plans

10. Organization, funding and other methods to implement all of the proceeding elements

11. Information flow and feedback system for continued repetition of all essential elements and

for adjustment and changes at each stage

12. Review and evaluation of all the processes

In each of these activities, staff and line personnel have important Responsibilities in thestrategic decision making processes. The scope of mergers and acquisition set the tone for thenature of mergers and acquisition activities and in turn affects the factors which have significantinfluence over these activities. This can be seen by observing the factors considered during thedifferent stages of mergers and acquisition activities. Proper identification of different phasesand related activities smoothen the process of involved in merger

Q.2.What are the sources of operating synergy?

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 3/20

Ans.

SOURCES OF OPERATING SYNERGY

Operating synergies are those synergies that allow firms to increase their operating

income, increase growth or both. We would categorize operating synergies into four types:1. Economies of scale that may arise from the merger, allowing the combined firm to becomemore cost-efficient and profitable. Economics of scales can be seen in mergers of firms in thesame business

For example : two banks combining together to create a larger bank. Merger of HDFC bank withCenturion bank of Punjab can be taken as an example of cost reducing operating synergy. Boththe banks after combination can expect to cut costs considerably on account of sharing of their resources and thus avoiding duplication of facilities available.

2. Greater pricing power from reduced competition and higher market share, which should resultin higher margins and operating income. This synergy is also more likely to show up in mergers

of firms which are in the same line of business and should be more likely to yield benefits whenthere are relatively few firms in the business. When there are more firms in the industry ability of firms to exercise relatively higher price reduces and in such a situation the synergy does notseem to work as desired.

3. Combination of different functional strengths, combination of different functional strengthsmay enhance the revenues of each merger partner thereby enabling each company to expand itsrevenues. The phenomenon can be understood in cases where one company with an established brand name lends its reputation to a company with upcoming product line or a company. Acompany with strong distribution network merges with a firm that has products of great potential but is unable to reach the market before its competitors can do so. In other words the twocompanies should get the advantage of the combination of their complimentary functional

strengths.

4. Higher growth in new or existing markets, arising from the combination of the two firms. Thiswould be case when a US consumer products firm acquires an emerging market firm, with anestablished distribution network and brand name recognition, and uses these strengths to increasesales of its products.

Operating synergies can affect margins and growth, and through these the value of the firmsinvolved in the merger or acquisition. Synergy results from complementary activities. This can be understood with the following example

Example : Consider a situation where there are two firms A and B. Firm A is having substantialamount of financial resources (having enough surplus cash that can be invested somewhere)while firm B is having profitable investment opportunities ( but is lacking surplus cash). If A andB combine with each other both can utilize each other strengths, for example here A can investits resource in the opportunities available to B. note that this can happen only when the two firmsare combined with each other or in other words they must act in a way as if they are one.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 4/20

Q.3.Explain the process of a leveraged buyout.

Ans.

In the realm of increased globalized economy, mergers and acquisitions have assumedsignificant importance both with the country as well as across the borders. Such acquisitions

need huge amount of finance to be provided. In search of an ideal mechanism to finance andacquisition, the concept of Leverage Buyout (LBO) has emerged. LBO is a financing techniqueof purchasing a private company with the help of borrowed or debt capital. The leveraged buyoutare cash transactions in nature where cash is borrowed by the acquiring firm and the debtfinancing represents 50% or more of the purchase price. Generally the tangible assets of thetarget company are used as the collateral security for the loans borrowed by acquiring firm inorder to finance the acquisition. Sometimes, a proportionate amount of the long term financing issecured with the fixed assets of the firm and in order to raise the balance amount of the total purchase price, unrated or low rated debt known as junk bond financing is utilized.

Modes of purchase

There are a number of types of financing which can be used in an LBO. These include :

Senior debt : this is the debt which ranks ahead of all other debt and equity capital in the business. Bank loans are typically structured in up to three trenches : A, B and C. The debt isusually secured on specific assets of the company, which means the lender can automaticallyacquire these assets if the company breaches its obligations under the relevant loan agreement;therefore it has the lowest cost of debt. These obligations are usually quite stringent. The bank loans are usually held by a syndicate of banks and specialized funds.

Subordinated debt : This debt ranks behind senior debt in order of priority on anyliquidation. The terms of the subordinated debt are usually less stringent than senior debt.Repayment is usually required in one ‘bullet’ payment at the end of the term. Since subordinateddebt gives the lender less security than senior debt, lending costs are typically higher. An

increasingly important form of subordinated debt is the high yield bond, often listed on Indianmarkets. High yield bonds can either be senior or subordinated securities that are publicly placedwith institutional investors. They are fixed rate, publicly traded, long term securities with alooser covenant package than senior debt though they are subject to stringent reportingrequirements.

Mezzanine finance : This is usually high risk subordinated debt and is regarded as a type of intermediate financing between debt and equity and an alternative of high yield bonds. Anenhanced return is made available to lenders by the grant of an ‘equity kicker’ which crystallizesupon an exit. A form of this is called a PIK, which reflects interest ‘paid in kind’, or rolled upinto the principal, and generally includes an attached equity warrant.

Loan stock : This can be a form of equity financing if it is convertible into equity capital. Thequestion of whether loan stock is tax deductible should be investigated thoroughly with thecompany’s advisers.

Preference share : This forms part of a company’s share capital and usually gives preferenceshareholders a fixed dividend and fixed share of the company’s equity.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 5/20

Ordinary shares : This is the riskiest part of a LBOs capital structure. However, ordinaryshareholders will enjoy majority of the upside if the company is successful.

Q.4.What are the cultural aspects involved in a merger. Give sufficient examples.

Ans.

The value chains of the acquirer and the acquired, need to be integrated in order toachieve the value creation objectives of the acquirer. This integration process has threedimensions: the technical, political and cultural. The technical integration is similar to thecapability transfer discussed above. The integration of social interaction and politicalrelationships represents the informal processes and systems which influence people’s ability andmotivation to perform. At the time of integration, the acquirer should have regard to these political relationships, if acquired employees are not to feel unfairly treated. An important aspectof integration is the cultural integration of the acquiring and acquired firms. The culture of anorganization is embodied in its collective value systems, beliefs, norms, ideologies myths and

rituals. They can motivate people and can become valuable sources of efficiency andeffectiveness. The following are the illustrative organizational diverse cultures which may haveto be integrated during post-merger period:. Strong top leadership versus Team approach· Management by formal paper work versus management by wandering around· Individual decision versus group consensus decision· Rapid evaluation based on performance versus Long term relationship based on loyalty· Rapid feedback for changes versus formal bureaucratic rules and procedures· Narrow career path versus movement through many areas· Risk taking encouraged versus ‘one mistake you are out’· Risky activities versus low risk activities

· Narrow responsibility arrangement versus ‘Everyone in this company is salesman (or costcontroller, or product quality improver etc.)’· Learn from customer versus ‘We know what is best for the customer’

There are four different types of organizational culture as mentioned below:

Power : The main characteristics are: essentially autocratic and suppressive of challenge;emphasis on individual rather than group decision making

Role: The important features are: bureaucratic and hierarchical; emphasis on formal rules and procedures; values fast, efficient and standardized culture service

Task/achievement: The main characteristics are: emphasis on team commitment; task determinesorganization of work; flexibility and worker autonomy; needs creative environment

Person/support: The important features are: emphasis on equality; seeks to nurture personaldevelopment of individual members

Poor cultural fit or incompatibility is likely to result in considerable fragmentation,uncertainty and cultural ambiguity, which may be experienced as stressful by organizationalmembers. Such stressful experience may lead to their loss of morale, loss of commitment,confusion and hopelessness and may have a dysfunctional impact on organizational performance.Mergers between certain types can be disastrous. Differences in culture may lead to polarization,

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 6/20

negative evaluation of counterparts, anxiety and ethnocentrism between top management teamsof the acquired and acquiring firms. In assessing the advisability of an acquisition, the acquirer must consider cultural risk in addition to strategic issues. The differences between the nationaland the organizational culture influence the cross-border acquisition integration. Thus, mergingfirms must consciously and proactively seek to transform the cultures of their organizations.

Q.5. Study a recent merger that you have read about and discuss the synergies that

resulted from the merger.

Ans.

Synergy is the additional value that is generated by the combination of two or more thantwo firms creating opportunities that would not be available to the firms independently.

There are two main types of synergy:1. Operating synergy2. Financial synergy

Operating Synergy

Operating synergies are those synergies that allow firms to increase their operating income,increase growth or both. We would categorize operating synergies into four types:

1. Economies of scale that may arise from the merger, allowing the combined firm to becomemore cost-efficient and profitable. Economics of scales can be seen in mergers of firms in thesame business

For example : two banks combining together to create a larger bank. Merger of HDFC bank with Centurion bank of Punjab can be taken as an example of cost reducing operating synergy.Both the banks after combination can expect to cut costs considerably on account of sharing of their resources and thus avoiding duplication of facilities available.

2. Greater pricing power from reduced competition and higher market share, which shouldresult in higher margins and operating income. This synergy is also more likely to show up inmergers of firms which are in the same line of business and should be more likely to yield benefits when there are relatively few firms in the business. When there are more firms in theindustry ability of firms to exercise relatively higher price reduces and in such a situation thesynergy does not seem to work as desired.

An example of limiting competition to increase pricing power is the acquisition of universalluggage by Blow Plast. The two companies were in the same line of business and were in directcompetition with each other leading to a severe price war and increased marketing costs. After the acquisition blow past acquired a strong hold on the market and operated under near monopoly situation. Another example is the acquisition of Tomco by Hindustan Lever.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 7/20

3. Combination of different functional strengths, combination of different functional strengthsmay enhance the revenues of each merger partner thereby enabling each company to expand itsrevenues. The phenomenon can be understood in cases where one company with an established brand name lends its reputation to a company with upcoming product line or a company. Acompany with strong distribution network merges with a firm that has products of great potential

but is unable to reach the market before its competitors can do so. In other words the twocompanies should get the advantage of the combination of their complimentary functionalstrengths.

4. Higher growth in new or existing markets, arising from the combination of the two firms.This would be case when a US consumer products firm acquires an emerging market firm, withan established distribution network and brand name recognition, and uses these strengths toincrease sales of its products. Operating synergies can affect margins and growth, and throughthese the value of the firms involved in the merger or acquisition. Synergy results fromcomplementary activities. This can be understood with the following example

Example : Consider a situation where there are two firms A and B. Firm A is having substantialamount of financial resources (having enough surplus cash that can be invested somewhere)while firm B is having profitable investment opportunities ( but is lacking surplus cash). If A andB combine with each other both can utilize each other strengths, for example here A can investits resource in the opportunities available to B. note that this can happen only when the two firmsare combined with each other or in other words they must act in a way as if they are one.

Financial Synergy

With financial synergies, the payoff can take the form of either higher cash flows or a lower costof capital (discount rate). Included are the following:

• A combination of a firm with excess cash, or cash slack, (and limited projectopportunities) and a firm with high-return projects (and limited cash) can yield a payoff in terms of higher value for the combined firm. The increase in value comes from the projects that were taken with the excess cash that otherwise would not have been taken.This synergy is likely to show up most often when large firms acquire smaller firms, or when publicly traded firms acquire private businesses.

• Debt capacity can increase, because when two firms combine, their earnings and cashflows may become more stable and predictable. This, in turn, allows them to borrowmore than they could have as individual entities, which creates a tax benefit for thecombined firm. This tax benefit can either be shown as higher cash flows, or take the

form of a lower cost of capital for the combined firm.• Tax benefits can arise either from the acquisition taking advantage of tax laws or from

the use of net operating losses to shelter income. Thus, a profitable firm that acquires amoney-losing firm may be able to use the net operating losses of the latter to reduce itstax burden. Alternatively, a firm that is able to increase its depreciation charges after anacquisition will save in taxes, and increase its value.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 8/20

Clearly, there is potential for synergy in many mergers. The more important issues arewhether that synergy can be valued and, if so, how to value it. This result has to be interpretedwith caution, however, since the increase in the value of the combined firm after a merger is alsoconsistent with a number of other hypotheses explaining acquisitions, including under valuationand a change in corporate control. It is thus a weak test of the synergy hypothesis. The existence

of synergy generally implies that the combined firm will become more profitable or grow at afaster rate after the merger than will the firms operating separately. A stronger test of synergy isto evaluate whether merged firms improve their performance (profitability and growth) relativeto their competitors, after takeovers. On this test, as we show later in this chapter, many mergersfail.

Q.6.What are the motives for a joint venture, explain with an example of a joint venture.

Ans.

As there are good business and accounting reasons to create a joint venture with acompany that has complementary capabilities and resources, such as distribution channels,technology, or finance, joint ventures are becoming an increasingly common way for companiesto form strategic alliances. In a joint venture, two or more “parent” companies agree to sharecapital, technology, human resources, risks and rewards in a formation of a new entity under shared control. Broadly, the important reasons for forming a joint venture can be presented below:

Internal Reasons to Form a JV

• Spreading Costs: You and a JV partner can share costs associated with marketing, product development, and other expenses, reducing your financial burden.

•

Opening Access to Financial Resources: Together you and a JV partner might have better credit or more assets to access bigger resources for loans and grants than you couldobtain on your own.

Connection to Technological Resources: You might want access to technological resources youcouldn't afford on your own, or vice versa. Sharing innovative and proprietary technologycan improve products, as well as your own understanding of technological processes.

Improving Access to New Markets: You and a JV partner can combine customer contacts andtogether even form a joint product that accesses new markets.

Help Economies of Scale: Together you and a JV partner can develop products or services thatreduce total overall production expenses. Bring your product to market cheaper where thecustomer can enjoy the cost savings.

External Reasons to Form a JV

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 9/20

Develop Stronger Innovative Product: Together you and a JV partner may be able to share ideasto develop a product that is more competitive in your industry.

Improve Speed to Market: With shared access to financial, technological, and distributionresources, you and a JV partner can get your joint product to market faster and moreefficiently.

Strategic Move Against Competition: A JV may be able to better compete against another industry leader through the combination of markets, technology, and innovation.

Strategic Reasons

Synergistic Reasons: You may find a JV partner with whom you can create synergy, which produces a greater result together than doing it on your own. Share and Improve Technology and Skills: Two innovative companies can share technology toimprove upon each other's ideas and skills.

Diversification - There could be many diversification reasons: access to diverse markets,development of diverse products, diversify the innovative working force, etc. Don't let a JVopportunity pass you by because you don't think it will fit in with your own small business.

Small and big companies alike can benefit from the reasons listed above. Analyze how your company can benefit internally, externally, and strategically, and then find a joint venture partner that will fit with your needs.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 10/20

MBA – FINANCE

Semester 3

MF0011 – Mergers and Acquisitions

Assignment Set- 2

Submitted By :

Student Name : Yogesh Kumar

Roll No : 521056970

LC Name & Code : NIPSTec Ltd. 1640

Date of Submission : 20/12/2011

Q.1. What is the basis for valuation of a target company?

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 11/20

Ans.

OVERVIEW OF ACQUISITION VALUATION METHODS

There are a number of acquisition valuation methods. While the most common is

discounted cash flow, it is best to evaluate a number of alternative methods, and compare their results to see if several approaches arrive at approximately the same general valuation. Thisgives the buyer solid grounds for making its offer. Using a variety of methods is especiallyimportant for valuing newer target companies with minimal historical results, and especially for those growing quickly – all of their cash is being used for growth, so cash flow is an inadequate basis for valuation.Valuation Based on Stock Market Price

If the target company is publicly held, then the buyer can simply base its valuation on thecurrent market price per share, multiplied by the number of shares outstanding. The actual price paid is usually higher, since the buyer must also account for the control premium. The currenttrading price of a company’s stock is not a good valuation tool if the stock is thinly traded. In this

case, a small number of trades can alter the market price to a substantial extent, so that the buyer’s estimate is far off from the value it would normally assign to the target. Most targetcompanies do not issue publicly traded stock, so other methods must be used to derive their valuation. When a private company wants to be valued using a market price, it can adopt theunusual ploy of filing for an initial public offering while also being courted by the buyer. Bydoing so, the buyer is forced to make an offer that is near the marketvaluation at which the targetexpects its stock to be traded. If the buyer declines to bid that high, then the target still has theoption of going public and realizing value by selling shares to the general public. However,given the expensive control measures mandated by the Sarbanes-Oxley Act and the stock lockup periods required for many new public companies, a target’s shareholders are usually more thanwilling to accepta buyout offer if the price is reasonably close to the target’s expected market

value.Valuation Based on a Multiple

Another option is to use a revenue multiple or EBITDA multiple. It is quite easy to look up the market capitalizations and financial information for thousands of publicly held companies.The buyer then converts this information into a multiples table, which itemizes a selection of valuations within the consulting industry. The table should be restricted to comparablecompanies in the same industry as that of the seller, and of roughly the same marketcapitalization. If some of the information for other companies is unusually high or low, theneliminate these outlying values in order to obtain a median value for the company’s size range.Also, it is better to use a multiday average of market prices, since these figures are subject tosignificant daily fluctuation. The buyer can then use this table to derive an approximation of the

price to be paid for a target company. For example, if a target has sales of $100 million, and themarket capitalization for several public companies in the same revenue range is 1.4 timesrevenue, then the buyer could value the target at $140 million. This method is most useful for aturn-around situation or a fast growth company, where there are fewprofits (if any).Valuation Based on Enterprise Value

Another possibility is to replace the market capitalization figure in the table withenterprise value. The enterprise value is a company’s market capitalization, plus its total debt

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 12/20

outstanding, minus any cash on hand. In essence, it is a company’s theoretical takeover price, because the buyer would have to buy all of the stock and pay off existing debt, while pocketingany remaining cash.Valuation Based on Comparable Transactions

Another way to value an acquisition is to use a database of comparable transactions to

determine what was paid for other recent acquisitions. Investment bankers have access to thisinformation through a variety of private databases, while a great deal of information can becollected on-line through public filings or press releases.Valuation Based on Real Estate Values

The buyer can also derive a valuation based on a target’s underlying real estate values.This method only works in those isolated cases where the target has a substantial real estate portfolio. For example, in the retailing industry, where some chains own the property on whichtheir stores are situated, the value of the real estate is greater than the cash flow generated by thestores themselves. In cases where the business is financially troubled, it is entirely possible thatthe purchase price is based entirely on the underlying real estate, with the operations of the business itself being valued at essentially zero. The buyer then uses the value of the real estate as

the primary reason for completing the deal. In some situations, the prospective buyer has no realestate experience, and so is more likely to heavily discount the potential value of any real estatewhen making an offer. If the seller wishes to increase its price, it could consider selling the realestate prior to the sale transactionValuation Based on Product Development Costs

If a target has products that the buyer could develop in-house, then an alternativevaluation method is to compare the cost of in-house development to the cost of acquiring thecompleted product through the target. This type of valuation is especially important if the marketis expanding rapidly right now, and the buyer will otherwise forego sales if it takes the time to pursue an in-house development path. In this case, the proper valuation technique is to combinethe cost of an in-house development effort with the present value of profits foregone by waitingto complete the in-house project. Interestingly, this is the only valuation technique where most of the source material comes from the buyer’s financial statements, rather than those of the seller.Valuation Based on Liquidation Value

The most conservative valuation method of all is the liquidation value method. This is ananalysis of what the selling entity would be worth if all of its assets were to be sold off. Thismethod assumes that the ongoing value of the company as a business entity is eliminated, leavingthe individual auction prices at which its fixed assets, properties, and other assets can be sold off,less any outstanding liabilities. It is useful for the buyer to at least estimate this number, so that itcan determine its downside risk in case it completes the acquisition, but the acquired businessthen fails utterly.Valuation Based on Replacement Cost

The replacement value method yields a somewhat higher valuation than the liquidationvalue method. Under this approach, the buyer calculates what it would cost to duplicate thetarget company. The analysis addresses the replacement of the seller’s key infrastructure. Thiscan yield surprising results if the seller owns infrastructure that originally required lengthyregulatory approval. For example, if the seller owns a chain of mountain huts that are located ongovernment property, it is essentially impossible to replace them at all, or only at vast expense.An additional factor in this analysis is the time required to replace the target. If the time period

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 13/20

for replacement is considerable, the buyer may be forced to pay a premium in order to gain quick access to a key market.

Q.2. Discuss the factors in post-merger integration process.

Ans.

Some important factors that can contribute to success or failure in mergers and

acquisitions are :

Due Diligence : Lack of due diligence has caused many merger failures. It involves

comprehensive analysis of firm characteristics such as financial condition, management

capabilities, physical assets and intangible assets.

Financing : Manageable debt levels should be ensured. Complementary Resources : Occurswhen the ‘primary resources of the acquiring and target firms are somewhat different, yet

simultaneously supportive of one another.’ This tends to create economic value to a greater value

that exists when the merging firms have identical or unrelated resources.

Friendly/Hostile Acquisitions : Friendly acquisitions tend to create greater economic value. A

hostile acquisition can reduce the transfer of information during due diligence and merger

integration, and increase turnover of key executives in the firm being acquired.

Synergy Creation : Four foundations to creation of synergy are strategic fit, organizational fit,

managerial actions and value creation.

Organizational Learning : Many people should participate in the acquisition process to ensure

knowledge about acquisitions is being spread throughout the firm, and isn’t lost if one of the key

people typically involved leaves. The learning process should be managed, with steps taken to

study and learn from acquisitions, with the information gained recorded.

Focus on Core Business : Cultural and management differences are more greatly magnified the

less firms have in common, therefore constraining the sharing of resources and capabilities. ‘

Result is that positive benefits from financial synergy are not enough to offset the negative

effects of diversification.

Emphasis on Innovation : Innovation is critical to organizational competitiveness. ‘Companies

that innovate enjoy the first-mover advantages of acquiring a deep knowledge of new markets

and developing strong relationships with key stakeholders in those markets’.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 14/20

Ethical Concerns/Opportunism : Risk in mergers and acquisitions are that the information

received may be incorrect, misleading or deceptive. Steps should be taken to ensure that the

information is accurate and hasn’t been manipulated by management with the aim to making

performance appear higher than it is.

Q.3. List out the defense strategies in the face of a hostile takeover bid.

Ans.

RAID TECHNIQUES

Techniques used in raids are such as Techniques of raid takeover bid and tender offer.The procedure for organizing takeovers includes collection of relevant information and itsanalysis, examine shareholders' profile, investigation of title and searches into indebtedness,examining of articles of association etc,. Defence against takeover bid may be in the form of

advance preventive measures for defence such as - joint holdings or joint voting agreement,interlocking shareholdings or cross shareholdings, issue of block of shares to friends andassociates, defensive merger apart from other things. Tactical defence' strategies include friendly purchase of shares, emotional attachment, loyalty and patriotism, recourse to legal action,operation ‘White Knights', "Golden Parachutes" etc,.

Four basic tactics or schemes can be carved out when we study the practice of corporateraiding which are bankruptcy, corporate, litigation, and land schemes to be the most widespreadapart from the other supplementary tactics such as the creation and presentation of false evidencein civil litigation. At least three causes can be identified, first is the general uncertainty of property rights resulting from the privatization of state assets, second cause is poor corporategovernance and final cause of raiding is the fact that the legal system is simply not yet equippedto deal with this novel form of crime. The court structure, the inadequacy of criminal law, theflaws in criminal investigation, the problems of good faith purchaser and the verification of corporate documents are also among the loopholes that can be identified. In order to address this problem, a new bankruptcy law must be imposed with more stringent screening and ethicalrequirements for trustees, expanding the time for judges to consider and take decisions, and alsoexpand debtors' rights to contest creditors' petitions.

The corrupt acquisition of control over the target company usually by falsifying internalcorporate documents and/or corruptly obtaining control over a significant portion of the votingstock or the board of directors of the target company is common in nature. The raider may createa false power of attorney or other document authorizing him or a co-conspirator to enter intotransactions on behalf of the target company and then transfer the target's assets to himself or affiliated companies or the raider bribes officials at state registration agencies to alter the targetcompany's registration documents to give him and/or his confederates faux control over thetarget company. He then uses this control to drain off the target's assets.

Another important tactic that may be used by raider is the creation and presentation of false evidence in civil litigation. For example, in answering claims by victims, raiders typicallyoffer false evidence, such as fabricated contracts and corporate resolutions, to "prove" the allegedlegitimacy of their acquisitions. There are certain measures that businesses can take to protectthemselves. These measures include retaining qualified legal counsel to draft and review allincorporation documents and contracts, retaining corporate investigation firms to investigate

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 15/20

partners and major customers, and, above always complying with all relevant laws andregulations. The term ‘takeover' is nowhere defined in the Companies Act 1956 (Act) or inSecurities and Exchange Board of India Act, 1992 (SEBI Act), or in SEBI (SubstantialAcquisition of Shares and Takeovers) Regulations, 1997 (Takeover Code). In the absence of alegal definition, the term takeover has to be understood from its commercial usage. In

commercial parlance, the term takeover denotes the act of a person or group of persons (acquirer)acquiring shares or acquiring voting rights or both of a company (target company), from itsshareholders, either through private negotiations with majority shareholders, or by a public offer in the open market with an intention to gain control over its management. A takeover isconsidered ‘hostile' when the management of the target company resists the attempted takeover.The basic principle is that when acquisition becomes a takeover, the Takeover Code becomesapplicable besides other provisions of the Act. In other words, in case of a takeover, complianceof both the Takeover Code as well as that of the Act is necessary, while in case of acquisition,compliance of only the Act is required. Further, if an acquisition results in a ‘combination', thenthe provisions of the Competition Act 2002 also become applicable, and the approval of theCompetition Commission of India is required. If the acquisition results in either inflow or

outflow of funds, to or from India, then the provisions of the Foreign Exchange Management Act1999 would become applicable and in such a case, the permission from either the Reserve Bank of India or the Central Government may be required.

The objective behind the Takeover Code is to bring transparency in takeover andacquisition transactions in public listed companies and to ensure that if minority shareholders arenot given a raw deal through price fixation. The Takeover Code lays down the mandatory andcompulsory disclosure of an acquisition if the acquirer intends to do. The procedure in case aninvestor wants to takeover has been clearly laid down in the Companies Act, 1956, the Takeover Code etc,. These regulatory mechanisms also lays down the offences, penalties in case of anyviolation, obligations and restrictions upon the merchant bankers, acquirers, the company itself etc,.

DEFENCE TECHNIQUES

Preventive measures:

Preventive measures against hostile takeovers are much more effective than reactivemeasures implemented once takeover attempts have already been launched. The first step in acompany’s defence, therefore, is for management and controlling shareholders to begin their preparations for a possible fight long before the battle is joined. There are several principalweapons in the hands of target management to prevent takeovers, some of which are described below.

Control over the register:

The raider needs to know who the shareholders of the target are in order to approachthem with the offer to sell their shares. With joint stock companies this information is containedin the share register. In particular, the share register provides for the possibility to identify theowners of the shares, quantity, nominal value and type of shares held by shareholders. So it isvery important to ensure that non-authorized persons do not have access to the share register of the company by taking the following steps:• Careful consideration is needed when choosing the registrar; the preference should be given toa reputable registrar;

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 16/20

• Check the track record of the share registrar in regards to its involvement in hostile takeovers inthe past;• Check who controls the registrar company. In case of transfer of shares to a nominee holder (custodian or depository) information on the beneficiary owners of shares is not stated in theshare register. Instead, the share register contains information on the nominee holders. This

makes it much more difficult for the raider to identify who is the real owner of the shares.Control over debts:

Creditor indebtedness of the company may be used by a raider as the principal or auxiliary tool in the process of hostile takeover. In particular, the raider may employ so-called“contract bankruptcy” in order to acquire the assets of the target. In connection with this thefollowing cautionary measures should be taken:

• Monitor the creditors of company carefully;• Prevent overdue debts;• If there is indirect evidence that a bankruptcy procedure is about to be launched, the companyshould do its best to pay all outstanding debts;• Accumulate all the debts and risks relating to commercial activity of the company on a special purpose vehicle that does not hold any substantial assets.

Cross shareholding:

Several subsidiaries of a company (at least three) have to be established, where the parentcompany owns 100% of share capital in each subsidiary. The parent transfers to subsidiaries themost valuable assets as a contribution to the share capital. Then the subsidiaries issue moreshares. The amount of these should be more than four times the initial share capital. Subsidiariesthen distribute the shares among themselves. The result of such an operation is that the parentowns less that 25% of the share capital of each subsidiary. In other words the parent companydoes not even have a blocking shareholding. When implementing this Golden parachute Thismeasure discourages an unwanted takeover by offering lucrative benefits to the current top

executives, who may lose their job if their company is taken over by another fi rm. The“triggering” events that enable the golden parachute clause are change of control over thecompany and subsequent dismissal of the executive by a raider provided that this dismissal isoutside the executive’s control (for instance, reduction in workforce2 or dismissal of the head of the board of directors due to the decision of the general meeting of shareholders provided suchadditional ground for dismissal is stated in the labour contract with the head of the board3).Benefits written into the executives’ contracts may include items such as stock options, bonuses,hefty severance pay and so on. Golden parachutes can be prohibitively expensive for theacquiring firm and, therefore, may make undesirable suitors think twice before acquiring acompany if they do not want to retain the target’s management nor dismiss them at a high price.The golden parachute defence is widely used by American companies. The presence of “golden

parachute” plans at Fortune 1000 companies increased from 35% in 1987 to 81% in 2001,according to a survey by Executive Compensation Advisory Services. Notable examples includeex- Mattel CEO Jill Barad’s USD 50 million departure payment, and Citigroup Inc. John Reed’sUSD 30 million in severance and USD 5 million per year for life.

Change of control clauses (“Shark Repellents”):

The company may include in loan agreements or some other agreements conditionalcovenants that in the event of the company passing under the control of a third party, the other

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 17/20

party to the agreement has the right to accelerate the debt or terminate the contract. The result of such agreements is that a potential raider may not be sure whether it will be able to benefit fromimportant advantages enjoyed by the target. Although one of the effects of change of controlclauses is to discourage raiders, their purpose is legitimate: to protect creditors from being placedin a worse position than they visualised.

Q.4. What are the legal compliance issues a company has to adhere to in case of a merger.

Explain through an example.

Ans.

There are only seven sections from section 390 to 396 in the Companies act 1956 whichare related to the matters pertaining to Mergers and Acquisitions and have been given in Chapter V under the heading Arbitration, Compromises, Arrangements and Reconstruction. The Act laysdown the legal procedures for mergers or acquisitions :

Permission for merger : Two or more companies can amalgamate only when theamalgamation is permitted under their memorandum of association. Also, the acquiring companyshould have the permission in its object clause to carry on the business of the acquired company.In the absence of these provisions in the memorandum of association, it is necessary to seek the permission of the shareholders, board of directors and the Company Law Board before affectingthe merger.

Information to the stock exchange : The acquiring and the acquired companies shouldinform the stock exchanges about the merger.

Approval of board of directors : The board of directors of the individual companies shouldapprove the draft proposal for amalgamation and authorize the managements of the companies tofurther pursue the proposal.

Application in the high court : An application for approving the draft amalgamation proposal duly approved by the board of directors of the individual companies should be made tothe High Court.

Shareholders’ and creators’ meetings : The individual companies should hold separatemeetings of their shareholders and creditors for approving the amalgamation scheme. At least, 75 percent of shareholders and creditors in separate meetings, voting in person or by proxy, mustaccord their approval to the scheme.

Sanction by the high court : After the approval of the shareholders and creditors, on the

petitions of the companies, the High Court will pass an order, sanctioning the amalgamationscheme after it is satisfied that the scheme is fair and reasonable. The date of the court’s hearingwill be published in two newspapers, and also, the regional director of the Company Law Boardwill be intimated.

Filing of the court order : After the Court order, its certified true copies will be filed withthe Registrar of Companies.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 18/20

Transfer of assets and liabilities : The assets and liabilities of the acquired company will betransferred to the acquiring company in accordance with the approved scheme, with effect fromthe specified date.

Payment by cash or securities : As per the proposal, the acquiring company will exchangeshares and debentures and/or cash for the shares and debentures of the acquired company. These

securities will be listed on the stock exchange.

Q.5. Take a cross border acquisition by an Indian company and critically evaluate.

Ans.

In a study conducted in 2000 by Lehman Brothers, it was found that, on average, largeM&A deals cause the domestic currency of the target corporation to appreciate by 1% relative tothe acquirer's. For every $1-billion deal, the currency of the target corporation increased in value

by 0.5%. More specifically, the report found that in the period immediately after the deal isannounced, there is generally a strong upward movement in the target corporation's domesticcurrency (relative to the acquirer's currency). Fifty days after the announcement, the targetcurrency is then, on average, 1% stronger.

The rise of globalization has exponentially increased the market for cross border M&A.In 1996 alone there were over 2000 cross border transactions worth a total of approximately$256 billion. This rapid increase has taken many M&A firms by surprise because the majority of them never had to consider acquiring the capabilities or skills required to effectively handle thiskind of transaction. In the past, the market's lack of significance and a more strictly nationalmindset prevented the vast majority of small and mid-sized companies from considering cross border intermediation as an option which left M&A firms inexperienced in this field. This same

reason also prevented the development of any extensive academic works on the subject.Due to the complicated nature of cross border M&A, the vast majority of cross border

actions have unsuccessful results. Cross border intermediation has many more levels of complexity to it then regular intermediation seeing as corporate governance, the power of theaverage employee, company regulations, political factors customer expectations, and countries'culture are all crucial factors that could spoil the transaction.[3][4] Because of suchcomplications, many business brokers are finding the International Corporate Finance Group andorganizations like it to be a necessity in M&A today.

CROSS-BORDER MERGER AND ACQUISITION: INDIA

Until upto a couple of years back, the news that Indian companies having acquired

American-European entities was very rare. However, this scenario has taken a sudden U turn. Nowadays, news of Indian Companies acquiring a foreign businesses are more common thanother way round. Buoyant Indian Economy, extra cash with Indian corporates, Government policies and newly found dynamism in Indian businessmenhave all contributed to this newacquisition trend. Indian companies are now aggressively looking at North American andEuropean markets to spread their wings and become the global players. The Indian IT and ITEScompanies already have a strong presence in foreign markets, however, other sectors are alsonow growing rapidly. The increasing engagement of the Indian companies in the world markets,

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 19/20

and particularly in the US, is not only an indication of the maturity reached by Indian Industry but also the extent of their participation in the overall globalization process.

If you calculate top 10 deals itself account for nearly US $ 21,500 million. This is morethan double the amount involved in US companies' acquisition of Indian counterparts.Graphicalrepresentation of Indian outbound deals since 2000. Indian outbound deals, which were valued at

US$ 0.7 billion in 2000-01, increased to US$ 4.3 billion in 2005 , and further crossed US$ 15 billion-mark in 2006. In fact, 2006 will be remembered in India's corporate history as a year when Indian companies covered a lot of new ground. They went shopping across the globe andacquired a number of strategically significant companies. This comprised 60 per cent of the totalmergers and acquisitions (M&A) activity in India in 2006. And almost 99 per cent of acquisitions were made with cash payments.

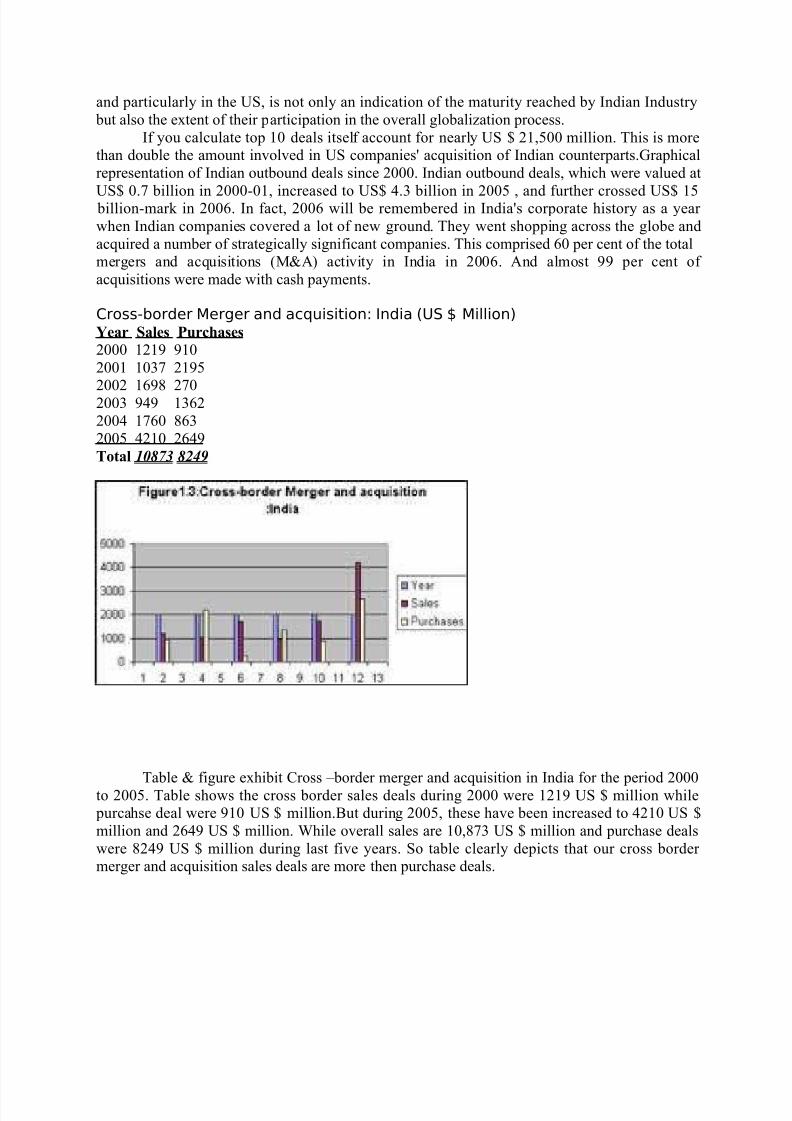

Cross-border Merger and acquisition: India (US $ Million)Year Sales Purchases

2000 1219 9102001 1037 2195

2002 1698 2702003 949 13622004 1760 8632005 4210 2649Total 10873 8249

Table & figure exhibit Cross –border merger and acquisition in India for the period 2000to 2005. Table shows the cross border sales deals during 2000 were 1219 US $ million while purcahse deal were 910 US $ million.But during 2005, these have been increased to 4210 US $million and 2649 US $ million. While overall sales are 10,873 US $ million and purchase dealswere 8249 US $ million during last five years. So table clearly depicts that our cross border merger and acquisition sales deals are more then purchase deals.

8/3/2019 MF0002 Set 1&Set2

http://slidepdf.com/reader/full/mf0002-set-1set2 20/20

Q.6. Choose any firm of your choice and identify suitable acquisition opportunity and give

reasons for the same.

Ans.

Identifying takeover opportunities

The basic purpose of valuation of Target company is to locate the possibilities of takeover. Valuation technique discussed above serves the purpose of identification of targetcompanies for takeover as well as serves the basic purpose of fixing exchange ratio in case thetarget company is finally selected for acquisition. Some financial experts suggest selectioncriteria based on following two approaches.

Present value analysis : The present value analysis is more or less the same as valuation on netmaintaining earning basis for listed companies and the technique is the same as used for dividendanalysis. In other words, the earnings or the target firm are projected and discounted at theacquirers cost of capital to obtain a theoretical market price on the shares of the target company.This is then compared with the actual market price to determine the net present value oninvestments. For calculating theoretical price the following example will serve the purpose :Given the following dataI=k=Acquirer Co’s cost of capital 10%D0 = p0 For target co’s payout ratio at Rs. 1 per share.MPS for Target Co’s market price per share Rs. 50-For Target Co’s merger @ 100% basisg for Target Co’s earning and dividend expected to grow at 8% p.a.using above data and the formula for the constant annual growth rate of dividend d0 (1+g) / (i-g)as discussed earlier in dividend approach, then target company’s theoretical price is as under :P = P0 (1+g) / (k-g) = 1(1.08) / .10 – .08 = 1.08 / .02 = 54The theoretical price exceeds the Market Price i.e. 54 – 50 = 4. here, NPV is 4 per share. Theresult requires reconsideration. The above approach does not consider the risk posture of acquisition i.e. the portfolio effect. The capital assets pricing model considers these aspects asdiscussed below.Capital assets pricing : The above approach provides a superior theoretical framework and ishelpful in identifying a merger partner, the target company. The basic logic behind the model isthat if expected rate of return exceeds the required rate of return, then the acquirer company hasgreen signal for acquiring the target company.The required rate of return is calculated by solving the following equation :E(Rj ) = Rf+ [E(Rm) – Rf] (Bj)Where,E(Rj ) = Required return

E(Rj ) = Expected returnE(Rm) = Expected return for market indexRf = Risk free returnBj = Beta (normally determines past performance) j = Potential merger partner (target company)