mfs 2020 sustainable investing annual report

TRANSCRIPT

MFS® 2020 Sustainable Investing Annual Report

Table of Contents

1 A Message From Barnaby Wiener

4 Sustainable Investing at MFS = Responsible Capital Allocation

5 Strategy and Governance

6 Leadership

11 Fundamental Research

15 Thematic Research

17 Risk Management

18 ESG Data and Tools

19 Stewardship – Engagement

23 Stewardship – Proxy Voting

31 Regulatory Developments

32 Corporate Sustainability at MFS

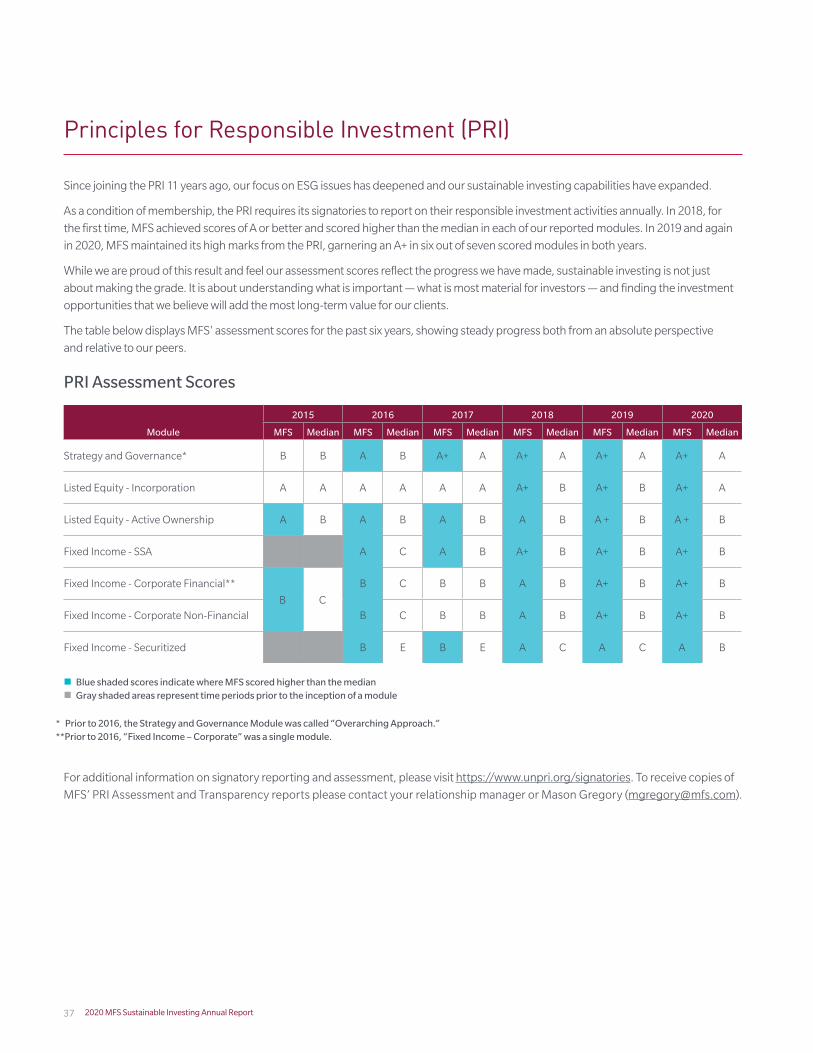

37 Principles for Responsible Investment (PRI)

39 Appendix

12020 MFS Sustainable Investing Annual Report

In its purest form, capitalism is an ingenious mechanism

for directing resources and driving progress. But we

need to remember that its primary purpose is just that:

allocating humanity's aggregate resources on behalf of

humanity. Returns to owners of capital are a byproduct.

They are of course necessary, but only one part of the

process. If companies fail to create value for all their

stakeholders — employees, customers, suppliers,

communities and the environment — they will

ultimately lose their license to operate, and everyone,

investors included, will be the poorer for it.

MFS has been thinking about sustainability for many

years. We have individuals dedicated to sustainability

across various disciplines and departments who play a

critical role in ensuring that we fulfil our stewardship

obligations as a firm. But no investment firm — and

indeed, no company — can hope to 'do sustainability'

simply by hiring a group of experts. Sustainability is

everyone's responsibility. From an investment

perspective, that means that every single one of us,

analyst or portfolio manager, equity or fixed income,

needs to be thinking about the footprint our issuers leave

on society and the environment.

Having done the analysis, what do we do with it?

Clearly, we incorporate it into our valuation, and often

this will be a factor in our deciding not to invest. But

sometimes, when valuation is supportive, we will invest

in companies with elevated environmental, social and

governance (ESG) risks. Does this make us inconsistent?

It does not. We have an obligation to fulfil our clients'

mandates, but more important, we believe engaging

with the companies we invest in has a greater impact

than excluding them from our portfolios. Assuming that

the ultimate objective is improved corporate behaviour,

it would seem to us self-evident that the most effective

way we can contribute to that end is through an active

dialogue with company management and the exercise

of our voting powers. In that context, divestment feels

like a cop-out. It takes the problem off your plate, and

puts it on someone else's.

Barnaby Wiener Portfolio Manager and Head of Sustainability and Stewardship

A Message From Barnaby Wiener

"Sustainability is everyone's responsibility... That means that every single one of us, analyst or portfolio manager, equity or fixed income, needs to be thinking about the footprint our issuers leave on society and the environment."

2 2020 MFS Sustainable Investing Annual Report

No short cuts

Another conviction we hold deeply is that there are no

short cuts in ESG analysis. We utilize a number of firms

who provide us with data and insights into ESG issues,

and they are a useful input in our process, but the idea

that you can outsource the whole problem and distil a

company's ESG profile into a single, simple rating is

anathema to us. Sustainability presents itself in many

shapes and forms; some are brightly lit, others darkly

concealed. Often, the more we dig into these issues

with companies, the more complicated they become.

The only way we can hope to solve the riddle is through

diligent, contextual analysis and judgment. It is arduous

and often far from straightforward, but it is far too

important to offload onto someone else.

To be clear, we are not claiming to have completely

figured this out yet. Our industry has been excessively

preoccupied with short-term financial results and has

not adequately taken into account social and

environmental externalities that are detrimental to the

world and increasingly to the long-term economic

viability of many business models. We cannot claim to

be blameless in this regard. We have made significant

progress in the past few years, but we recognise that we

have to travel further down this road, and we are

determined to do so. As is usually the case when driving

organisational change, there are no magic bullets.

Rather, a combination of education, tools,

encouragement and accountability is driving a shift in

mindset and a reorientation of our investment priorities.

Collaboration is key

The journey towards a more sustainable form of capitalism

is inherently a collaborative one. Many organisations will

no doubt be keen to trumpet their own particular

contribution. But in reality, progress will be the result of

mutual support and joint action. As an asset manager, we

recognise the need to cooperate, not just with asset

owners and companies but also with other asset

managers. We will achieve far more working together

than we would operating alone. With this in mind, we

have joined a select number of high-impact collaborative

initiatives this year, including Climate Action 100+ and

ShareAction's Workforce Disclosure Initiative.

The COVID-19 pandemic, which continues to plague

us, has been a wake-up call in so many ways. In one

sense it has been a huge distraction, but it has also

served to highlight the inherent fragility of our

existence. Most of us have grown up in a period of

peace and prosperity. We have been conditioned to

take so much for granted. In recent years, that

complacency has been challenged repeatedly. We have

had a global financial crisis, growing evidence of a

looming (and existential) climate crisis and now a public

health crisis. At a time when strong leadership has

never been needed more, we are witnessing a collapse

of trust in our democratic institutions. If ever there was

a time for the investment industry to stand up and be

counted, this is it. If not us, who? If not now, when?

Sincerely,

Barnaby Wiener

Portfolio Manager and

Head of Sustainability and Stewardship

A Message From Barnaby Wiener

97 Years of trust"From virtually the beginning, Massachusetts Investors Trust (MIT) has

been distinguished by two significant qualities, apart from its unique redemption feature, that have added greatly to its credibility.

First was the unyielding determination of the Trustees to pursue a conservative investment policy in spite of the prevalent temptations to speculate in the twenties: investments were funneled deliberately into a diversified range of common stocks of established, well-managed companies for the longer term. Second was the Trustee's insistence early in the company's history of making full disclosure of the financial operations of the trust. Accordingly, MIT reports have consistently shown securities owned, changes made in investments in the period, amounts received as income, details of expenses and commissions paid brokers for selling MIT shares — an "open book" policy initiated at a time when business generally revealed little about its operations."

– 50 Years of Trust, H. Lee Silberman, 1974

Founded in March 1924, MIT (the predecessor organization of MFS) was the first

investment trust to offer investors the ability to redeem their shares at will based on

the current net asset value of the fund. As a result of this feature MIT is credited with

being the first open-end mutual fund and creating the modern mutual fund industry.

While we are proud of this legacy, it is not only the innovation of the redeemable

share that has shaped our culture and investment philosophy for nearly 100 years

but also the other distinguishing features Mr. Silberman so aptly describes.

32020 MFS Sustainable Investing Annual Report

Sustainable Investing at MFS = Responsible Capital Allocation

At MFS, we seek to achieve our clients’ long-term economic

objectives by allocating their capital responsibly.

As an active manager, we have always sought to identify

investments that can add sustainable, long-term value for

our clients. While many asset managers have chased market

demand by launching new ESG strategies or relabeling their

existing portfolios, we have maintained a process-focused

approach that ensures ESG considerations are a part of

every fundamental investment decision.

Comprehensively and holistically integrating ESG factors into

our investment process improves our understanding of what is,

and what is not, priced into equity and fixed income valuations.

This helps us identify businesses that we believe have the

potential to offer more sustainable and durable returns.

Our multifaceted ESG integration strategy combines

analytic, bottom-up research and systematic risk

management, as well as active ownership through

engagement and proxy voting.

A variety of activities, processes, data sets and governance

structures supports our ability to make sound, long-term

investment decisions on behalf of our clients. The

illustration below highlights the principal areas where we

focus our time and attention. This report provides insight

into our activities in each of these areas.

ESG Integration

enables responsible value creation

Fundamental ResearchDetailed, bottom-up research of materiality based on company, industry and geographic factors

Strategy & GovernanceMultiple working groups and committees ensure integration acrossinvestment and stewardship activities

Risk ManagementDeep awareness of ESG

risks at individual companyand portfolio levels

ESG Data & ToolsData from multiple vendors

and specialists accessibleto all investors

StewardshipUsing engagement and proxy

voting to influence governance and business practices and reduce risk

Thematic ResearchProprietary insights on emerging ESG themes that impact multiple sectors and regions

Sustainable Investing Framework

4

52020 MFS Sustainable Investing Annual Report

ESG Strategy and Governance

In 2009, we formed the MFS Responsible Investing

Committee to ensure that our equity and fixed income

investment processes were benefiting from the systematic

integration of financially material ESG considerations. Since

the formation of the committee over a decade ago, the firm

has developed a strong governance structure around our

ESG activities and taken many other actions to accelerate the

implementation of sustainable investing practices.

MFS maintains three distinct governing bodies that provide

broad oversight of our sustainable investing activities: the

MFS Sustainability Group, the MFS Responsible Investing

Committee and the MFS Proxy Voting Committee.

The MFS Sustainability Group was formed in 2017 and

includes the firm's president, chief investment officer, head

of sustainability and stewardship, asset class CIOs, chief

risk officer, ESG analysts and other senior investors and

executives. Its purpose is to guide and accelerate the

implementation of sustainable investing practices across

the firm and to institutionalize ESG integration as a

fundamental component of MFS’ investment process and

corporate culture.

The MFS Responsible Investing Committee was

established in 2009 to ensure the effective integration of ESG

considerations across our investment and proxy voting

activities. In one of its first actions, the committee drafted

and issued the MFS Policy on Responsible Investing and

Engagement. Today, the committee maintains and updates

the policy as necessary and monitors adherence to ESG-

related regulatory issues and external commitments, such as

the Principles for Responsible Investment (PRI). Additionally,

MFS' internal audit team has reviewed our ESG integration

process in light of our responsible investing policy.

The MFS Proxy Voting Committee is co-chaired by our chief

investment officer and comprises senior leaders from our

investment, legal and global investment operations departments.

The committee establishes proxy voting engagement goals and

priorities and oversees the administration of the MFS Proxy Voting

Policies and Procedures.

2009Creation of Responsible Investing Committee

2010MFS becomes a PRI signatory

2013MFS hires first ESG

research analyst (Boston)

2018MFS hires second ESG

research analyst(Singapore)

2020MFS establishes the role of Head of Sustainability

and Stewardship

2011Substantial revision & enhancement of proxy policies

2017MFS Sustainability Group formed

2019MFS hires third ESG research analyst (Fixed Income)

The history behind our formal ESG Integration Process

Leadership

At MFS, sustainable investing describes our fundamental investment process; it is not a separate discipline with different inputs or

outcomes. As such, our process requires that all of our investment professionals are actively engaged in, and responsible for, its success.

In order to facilitate the adoption, implementation and enhancement of sustainable investing practices across the firm, we employ a

number of individuals positioned to provide strategic leadership on sustainable investing and support the effective integration of

sustainability considerations across teams and disciplines.

InvestmentsBarnaby Wiener, one of our most seasoned portfolio managers, serves as head of sustainability and stewardship. A leader and culture

carrier who has long been a champion of sustainability, Barnaby works closely with our ESG research analysts to engage with investment

leadership, portfolio managers and analysts to ensure that all of our investors truly understand and own sustainability in their research and

portfolio management duties. He also plays a strategic role with regard to issuer engagement on sustainability issues.

Our investment team includes two equity analysts and one fixed income analyst dedicated solely to ESG research. They have done

much to advance our investment team's thinking on ESG topics. Our ESG analysts fulfill a critical role in facilitating our sustainable

investing efforts. However, they are not intended to be the source of all ESG research. Their role is to support and enhance the ongoing

research into ESG issues performed by our portfolio managers and analysts.

Barnaby Wiener – Head of Sustainability and Stewardship

Barnaby joined MFS in 1998 as a research analyst. He became a portfolio manager in 2003 and

currently manages the firm's Prudent Wealth, Prudent Capital and Prudent Investor strategies. He

previously held the role of director of European Research and was co-portfolio manager of MFS

International Value and Global Value equity strategies. Prior to joining MFS, he was an equity

research analyst for both Merrill Lynch and Crédit Lyonnais. He also served as a captain in the British

Army. Barnaby is a graduate of Oxford University and the Royal Military Academy, Sandhurst. He is

based in London.

6 2020 MFS Sustainable Investing Annual Report

Leadership

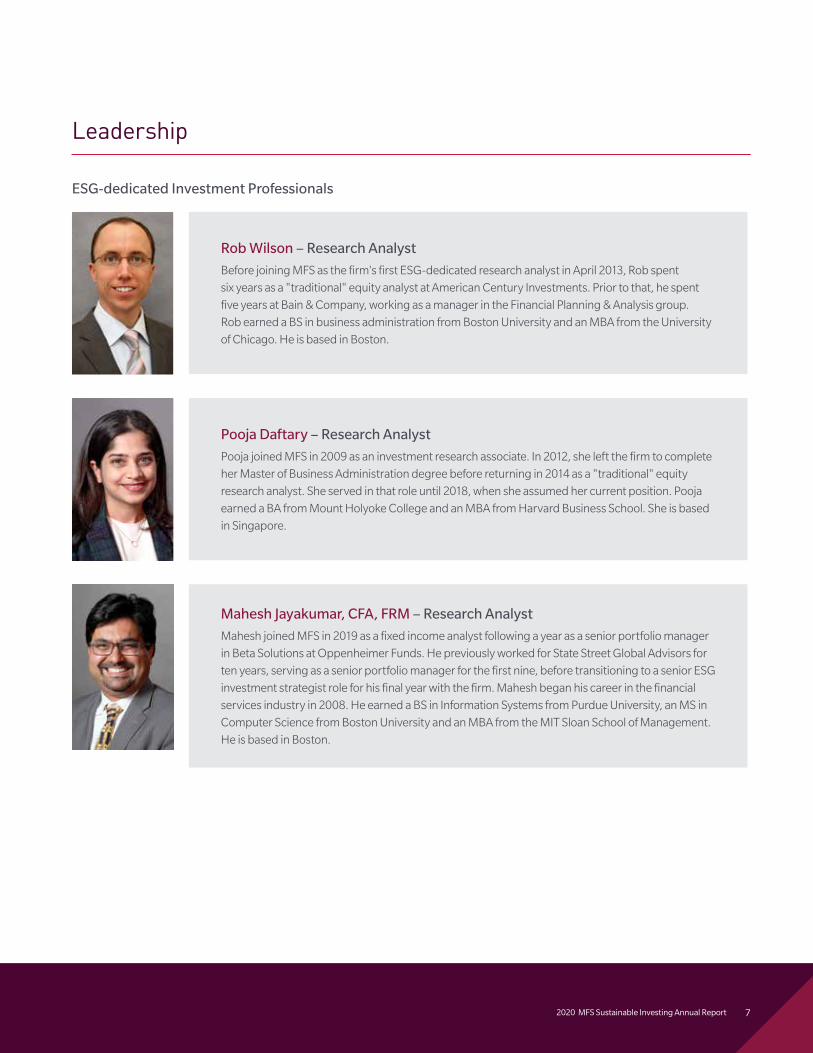

ESG-dedicated Investment Professionals

Rob Wilson – Research Analyst

Before joining MFS as the firm's first ESG-dedicated research analyst in April 2013, Rob spent

six years as a "traditional" equity analyst at American Century Investments. Prior to that, he spent

five years at Bain & Company, working as a manager in the Financial Planning & Analysis group.

Rob earned a BS in business administration from Boston University and an MBA from the University

of Chicago. He is based in Boston.

Pooja Daftary – Research Analyst

Pooja joined MFS in 2009 as an investment research associate. In 2012, she left the firm to complete

her Master of Business Administration degree before returning in 2014 as a "traditional" equity

research analyst. She served in that role until 2018, when she assumed her current position. Pooja

earned a BA from Mount Holyoke College and an MBA from Harvard Business School. She is based

in Singapore.

Mahesh Jayakumar, CFA, FRM – Research Analyst

Mahesh joined MFS in 2019 as a fixed income analyst following a year as a senior portfolio manager

in Beta Solutions at Oppenheimer Funds. He previously worked for State Street Global Advisors for

ten years, serving as a senior portfolio manager for the first nine, before transitioning to a senior ESG

investment strategist role for his final year with the firm. Mahesh began his career in the financial

services industry in 2008. He earned a BS in Information Systems from Purdue University, an MS in

Computer Science from Boston University and an MBA from the MIT Sloan School of Management.

He is based in Boston.

72020 MFS Sustainable Investing Annual Report

.

Broad ownershipAt MFS, sustainability is at the core of our corporate identity. We believe that

achieving true ESG integration requires the participation of our entire firm, not

just our investment team. A major priority for 2020 was the development of a

comprehensive training program that offers noninvestment personnel the

opportunity to deepen their understanding of sustainable investing. Launched in

June, the course includes foundational, intermediate and advanced learning

tracks that cover the history, evolution and current state of sustainable investing.

The curriculum also includes detailed information about MFS' approach to sus-

tainable investing through ESG integration and stewardship and discussions

about evolving ESG topics, trends and research. At the end of the third quarter,

over 1,000 MFS employees were actively participating in the course or had

completed all the course modules.

8 2020 MFS Sustainable Investing Annual Report

Proxy Voting, Legal and Regulatory

Our team of two dedicated proxy analysts manages day-to-day proxy voting and engagement activity. The team employs a collaborative

approach in its decision making, incorporating information and perspectives from our global team of investment professionals, corporate

disclosures and engagement discussions, and a variety of third-party research tools. This process fosters well-rounded viewpoints on key

issues, which we believe leads to well-informed voting decisions that are in the best long-term economic interests of our clients.

In early 2020, we tasked a member of our legal team with focusing exclusively on assessing and monitoring the ESG-related

regulatory landscape to ensure that MFS is aware of all the relevant regulations in jurisdictions where we do business, and that we

are responding to them appropriately.

Margaret Therrien – Proxy Voting Analyst III

Margaret is an analyst on MFS' proxy voting team. She is responsible for analyzing case-by-case

voting issues and engaging with MFS' portfolio companies on issues relating to compensation, ESG

and board oversight. Prior to joining MFS in January 2016, Margaret worked as a credit risk analyst at a

biotechnology company. She has also worked in academia, researching corporate governance trends.

Margaret earned a BS in business administration from Boston University. She is based in Boston.

Herald Nikollara – Proxy Voting Analyst II

Herald is an analyst on MFS’ proxy voting team. He is responsible for proxy voting and corporate

governance-related research and analysis and day-to-day voting operations, as well as assisting with

reporting and engagement activities. Prior to joining MFS in May 2018, Herald worked as a paralegal

at a Boston-based law firm. He earned a BS in criminal justice from the University of Massachusetts

Boston. He is based in Boston.

Brad Wilson – Counsel

Brad serves as counsel for MFS. In this role, he supports MFS' sustainability program by tracking and

advising MFS' business groups on regulatory developments, supporting MFS' governance process

and supporting other sustainability initiatives. Brad joined MFS in 2015 as an associate counsel. He

assumed his current role in 2020. He previously spent four years as an associate general counsel for

Franklin Templeton and one year as an analyst for FINRA. Prior to that, he worked as a law clerk for

Franklin Templeton and the US Securities and Exchange Commission. Brad earned a BA in political

science and BBA in finance from the University of Georgia and an MBA and JD from the University of

Maryland. He has been a member of the New York State Bar since 2012.

Leadership

92020 MFS Sustainable Investing Annual Report

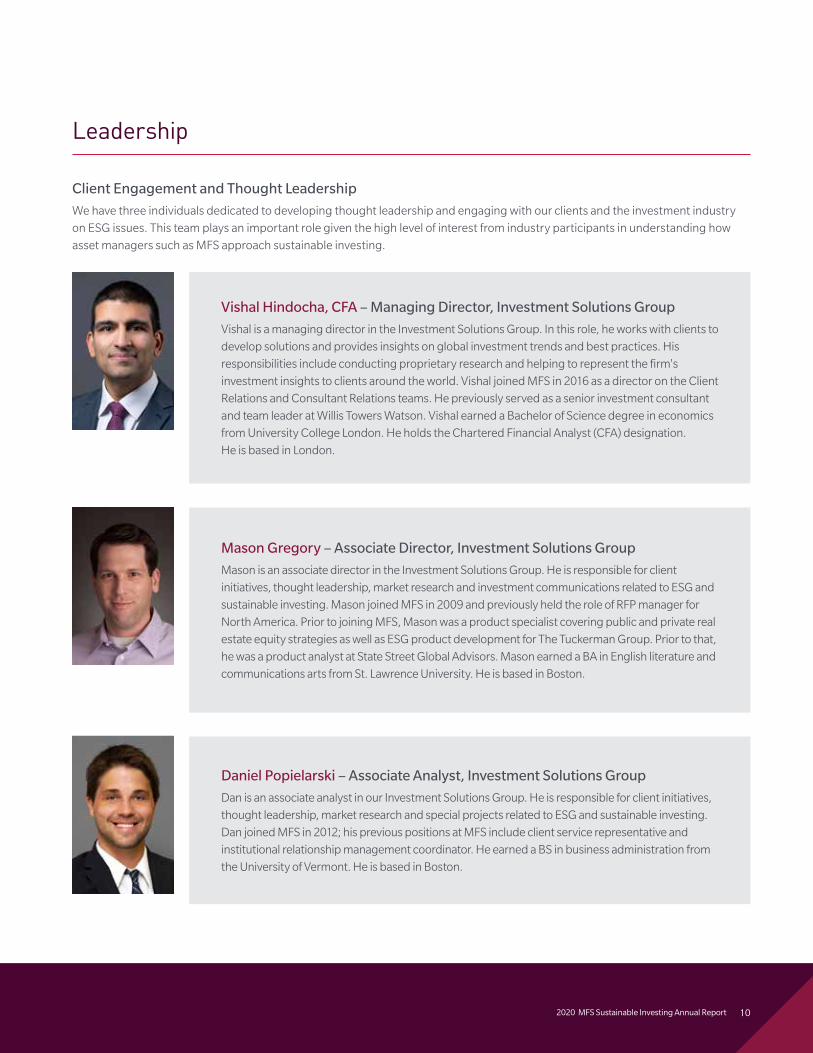

Client Engagement and Thought Leadership

We have three individuals dedicated to developing thought leadership and engaging with our clients and the investment industry

on ESG issues. This team plays an important role given the high level of interest from industry participants in understanding how

asset managers such as MFS approach sustainable investing.

Vishal Hindocha, CFA – Managing Director, Investment Solutions Group

Vishal is a managing director in the Investment Solutions Group. In this role, he works with clients to

develop solutions and provides insights on global investment trends and best practices. His

responsibilities include conducting proprietary research and helping to represent the firm's

investment insights to clients around the world. Vishal joined MFS in 2016 as a director on the Client

Relations and Consultant Relations teams. He previously served as a senior investment consultant

and team leader at Willis Towers Watson. Vishal earned a Bachelor of Science degree in economics

from University College London. He holds the Chartered Financial Analyst (CFA) designation.

He is based in London.

Mason Gregory – Associate Director, Investment Solutions Group

Mason is an associate director in the Investment Solutions Group. He is responsible for client

initiatives, thought leadership, market research and investment communications related to ESG and

sustainable investing. Mason joined MFS in 2009 and previously held the role of RFP manager for

North America. Prior to joining MFS, Mason was a product specialist covering public and private real

estate equity strategies as well as ESG product development for The Tuckerman Group. Prior to that,

he was a product analyst at State Street Global Advisors. Mason earned a BA in English literature and

communications arts from St. Lawrence University. He is based in Boston.

Daniel Popielarski – Associate Analyst, Investment Solutions Group

Dan is an associate analyst in our Investment Solutions Group. He is responsible for client initiatives,

thought leadership, market research and special projects related to ESG and sustainable investing.

Dan joined MFS in 2012; his previous positions at MFS include client service representative and

institutional relationship management coordinator. He earned a BS in business administration from

the University of Vermont. He is based in Boston.

Leadership

102020 MFS Sustainable Investing Annual Report

11 2020 MFS Sustainable Investing Annual Report

Fundamental Research

Our equity and fixed income investment teams rely on deep fundamental research and a long-term perspective to select securities

they believe have the potential to produce sustainable returns throughout an economic cycle. This approach requires the

incorporation of information from a variety of sources and an awareness of multiples viewpoints. We believe that the integration of

ESG factors into our research is essential as these issues often impact the long-term, sustainable value of businesses.

Sustainable Investment Steering Group and thematic working groups

To further our ESG integration

efforts, we created the

Sustainable Investment

Steering Group within our

investment team. Comprising

our head of sustainability and

stewardship, CIO, ESG analysts

and various other members of

our investment team, the

group's purpose is to provide

guidance and feedback on our

ESG integration strategy and

execution.

We also formed four working

groups to lead efforts related to

key sustainability pillars:

Climate Change, Societal

Impact, Governance and

Sovereign Risk. Each group

includes our ESG analysts and a

cross-section of investment

team members, including

specialists and generalists from

fixed income and equity. The

purpose of these groups is to

stimulate discussion across the

investment team and develop

practical frameworks to inform

our investment decision-

making process and corporate

engagement strategy.

Enhanced access to ESG research and data

We want to ensure that our

investment team has easy

access to all internal research,

along with the best available

third-party resources. Invest,

our proprietary online global

research collaboration

platform, organizes both

internal and external ESG

research and data for each

issuer. This includes ESG

commentary written by

covering equity and fixed

income analysts, links to

relevant internal research

notes and our proprietary

Sector Map materiality

framework that highlights key

ESG issues for the issuer's

industry/sub-industry.

Adjacent tabs include

information from various

external research providers

that is specific to the issuer.

Additionally, in 2020, our ESG

analysts developed an ESG

dashboard that allows

members of our investment

team to view a broad

spectrum of ESG metrics for

up to 100 securities

simultaneously.

Education program

We have developed a program

of monthly seminars for the

entire investment team. The

program was launched in early

2021 and will feature a wide

range of mostly external

presenters, including asset

owners and managers,

academics and other industry

stakeholders who have an

interesting perspective that

promises to enhance our

team's understanding of

sustainability-related issues.

Sector and asset class research

Our eight sector research

teams are continually

incorporating ESG-focused

research into their meeting

schedules and have set a new

goal of dedicating at least one

meeting a quarter to a

discussion of relevant

sustainability topics. Likewise,

our fixed income sub-asset-

class teams are dedicating

meetings solely to ESG issues

affecting sovereigns,

municipals, high yield, etc.

4321WORKING GROUPS DATA EDUCATION ASSET CLASS

Fundamental Research

In our view, ESG information is fundamental data that must be considered along with all other material

information. Our ESG research framework for equities and corporate bonds comprises both analytic

and systematic elements designed to ensure our global investment team can efficiently and effectively

identify and analyze the material ESG issues impacting their investment decisions.

Investment Roundtable

On the agenda of our virtual

Investment Roundtable event

in September 2020 were

several sustainability related

keynotes and thematic

presentations. Kasper Rorsted,

CEO of Adidas, provided

insights into his company's

sustainability journey during

his presentation and Q&A with

the investment team.

Additionally, our ESG analysts

delivered a presentation on

how rising inequality is

affecting society, companies

and stakeholders. This was

followed by breakout sessions

in which various members of

the investment research and

portfolio management teams

discussed the implications of

this important social theme on

their portfolios and sector

coverage.

Portfolio sustainability reviews

As part of our systematic

approach to ESG risk

management, all MFS

strategies are now subject to

annual sustainability reviews

focused exclusively on ESG

risks. These reviews cover a

wide variety of sustainability

metrics and complement the

ESG dimension of our

semiannual portfolio risk

review process, which is

described below. Select

strategies were reviewed

during the fourth quarter of

2020, and we will continue

to roll out this process

throughout 2021.

Performance evaluation and compensation

The analysis of ESG risks and

opportunities is part of our

investment process, and the

long-term performance of

each individual reflects this

integration. In addition to

assessment on a quantitative

basis, a portion of our

investment team members'

compensation is based on

qualitative factors, and ESG is

now an explicit element of the

qualitative assessment of

performance, alongside other

factors such as teamwork,

communication and

collaboration throughout the

investment process.

765ROUNDTABLE REVIEWS PERFORMANCE

12

13 2020 MFS Sustainable Investing Annual Report

MFS Transformative CapitalESG integration has often been viewed as primarily an exercise in risk management.

This is largely because ESG factors represent a diverse array of issues that are

increasingly shaping our future as a society and many investors fear that compa-

nies will fail to adequately anticipate and adapt to new ways of doing business.

However, ESG factors are also a source of opportunity as technology and industry

evolve to meet the changing needs of society. We believe companies that are

positioned to take advantage of these ESG tailwinds and create value for society

and the environment have the potential to outperform.

The MFS® Transformative Capital strategy is a high-conviction, global equity

portfolio that seeks to invest in companies proactively meeting environmental or

social needs. Portfolio Manager Nicole Zatlyn and our global team of research

analysts qualitatively identify companies that among other things 1) derive a

significant percentage of their revenue from products or services that address

environmental or social needs, 2) have boards that act in the best long-term

interests of their stakeholders, 3) exhibit a strong and unique culture and 4) are

trading at a discount to their long-term growth prospects.

The goal of Transformative Capital is to maximize returns while simultaneously

investing in companies that serve an environmental or social need. We believe

these goals are aligned and that companies that serve an environmental or social

purpose and create value for all of their stakeholders can sustainably compound

earnings, free cash flow and returns over a full market cycle.

This portfolio was launched October 1, 2019, and is currently funded exclusively by MFS seed capital.

142020 MFS Sustainable Investing Annual Report

Fundamental Research

Fixed incomeDuring 2020 we continued to focus on improving our ESG integration frameworks for all fixed income sub-asset classes, including investment-

grade corporates, sovereigns, US municipals, high yield and securitized fixed income. Some examples of this work are described below.

Sovereign debt

Members of the newly formed

Sovereign Risk Working Group

were tasked with developing an

ESG sovereign risk framework to

support and enhance our

investment decision-making

process across all asset classes.

Once codified, it will enable the

broader investment team to look

at country risk through an ESG

lens and better understand how it

might be impacting their

investments. This working group

includes emerging and developed

market sovereign fixed income

analysts, our fixed income ESG

analyst and one of our emerging

market equity portfolio managers.

Municipal bonds

The head of our municipal fixed

income research team and our

fixed income ESG analyst

participated in the PRI's Sub-

Sovereign Debt Advisory

Committee, which is working to

develop ESG integration guidance

for US municipal bonds. This is

expected to mirror similar

guidance available for other fixed

income sub-asset classes. We also

undertook due diligence on

research providers that offer

sustainability data for US

municipal bond issuers. Relative to

corporates, issuer-specific ESG

data is still scarce for municipals

and analysts rely largely on other

sources such as regulatory and

government-mandated

disclosures for relevant

information. We selected a vendor

that can provide demographic,

socioeconomic and climate risk

data, which will improve our ability

to assess the physical risks faced

by municipal issuers.

High yield

During the year, our fixed income

ESG analyst engaged in robust

conversations with his sector

counterparts to analyze material

ESG issues in their issuer

coverage. One of the most

productive ways to increase

awareness of both the materiality

and the implications of these

issues is for the ESG analyst to

deliver a thematic presentation to

the broader team and then

facilitate a discussion. Members

of the High Yield research team

covered a wide variety of issues in

this way in the second half of the

year. For example, our covering

analyst for one of the largest

subscription streaming services

discussed the importance of

governance factors that could

have a financial impact, including

founder control and impending

digital tax legislation. Our analyst

covering gaming companies

discussed the potential for

increased regulation to protect

communities from the perceived

harmful effects of gambling. The

analyst covering autos and auto

parts companies discussed the

implications of the shift to electric

vehicles and its effect on financials

and credit metrics in the medium

and long term. Our UK-based

analyst touched on various

governance red flags that he has

encountered over the course of his

career and discussed how and

when they may be an early

indicator of credit downgrades and

potential defaults in the European

high-yield issuer universe.

Sustainability bonds

We continue to own themed

bonds, including green bonds,

social bonds and sustainability-

linked bonds across various

portfolios. Our exposure to these

bonds more than doubled in 2020,

reflecting greater issuance and our

increasing asset base. Social bond

issuance soared as a result of the

COVID-19 crisis as both

corporates and governments

issued bonds to fight the

pandemic on a variety of fronts.

Issuance approached $150 billion

for the full year compared with $18

billion in 2019.1 Examples of the

use of proceeds include improved

access to health care, loans to

small businesses and an increased

supply of protective equipment.

Cumulative green bond issuance

in 2020 surpassed the $1 trillion

level in late September as that

market continued to draw in new

issuers and investors.

1 Source: Bloomberg.

Social Bond Issuance

$160

$120

$80

$40

$0

BIL

LIO

NS

2013 2014 2015 2016 2017 2018 2019 2020

$0.1 $0.6 $2.3 $2,2 $9.1 $11.9 $18.8

$147.7

15 2020 MFS Sustainable Investing Annual Report

Thematic Research

During the past year, our investment team produced in-depth research on a variety of ESG themes we believe to be financially

material to companies we own.

Culture and diversity

Culture and diversity have remained important topics for our investment and proxy voting teams for several years, but we stepped

up our research and engagement in these areas during 2020. This work led to many changes in our investment decision-making

process. For example, we reduced our exposure to a health care company due to ongoing corporate culture and governance risks.

In another example, corporate culture influenced the ratings of two companies covered by our US life science tools analyst. He

assigned a 1 rating (buy) to one company and a 2 rating (hold) to the other due in large part to his view on culture and its associated

impact on innovation within each firm.

Labor and income inequality

Labor and income inequality remained a key theme in 2020 due to the COVID-19 pandemic, which brought to light the challenges faced

by low-wage and hourly workers. During the year, MFS analysts and portfolio managers took these actions:

■ Engaged with a large number of companies regarding their employee practices

■ Spoke to members of multiple trade unions to obtain labor's viewpoints

■ Held sector team meetings to review data on employee wages, satisfaction and other factors

■ Offered a thematic presentation on the topic to the entire investment team during our Global Investment Roundtable in September

As an example of investment outcomes from this research, one of our portfolio management teams chose to sell an apparel retailer

due in part to poor labor practices (particularly very low wages) while adding to an existing holding that we believe exhibits much

better practices.

Modern slavery

Modern slavery took on additional importance as a thematic research topic for our team in 2020. Building on research initially conducted

by our ESG research analysts, our team spent time evaluating the supply chain practices of companies in multiple industries, most

notably apparel and footwear. We engaged both with companies and their key suppliers, and our team hosted and participated in calls

with various external experts on the topic.

This research increased our confidence in a footwear company. We evaluated the quality and frequency of company audits for tier 1, 2

and 3 suppliers, measures undertaken to hold erring suppliers accountable, and C-suite involvement in supply chain auditing and safety.

We found the company's commitment to improving the transparency of its supply chain to be industry leading, which boosted our

confidence in its brand's competitive moat as well as in its ability to manage the risk of supply chain disruption. MFS increased its

ownership of this company throughout the year.

We have made some of our research on modern slavery available to our clients and other stakeholders through our research publication

series ESG in Depth – Modern Slavery and Forced Labor.

Climate change

Climate change has been a central focus for our global sector teams. In 2020, we expanded available climate data and improved the

investment team's access to it. Every MFS investment professional now has several data sets to draw from when analyzing year-over-year

changes in scope 1, 2 and 3 emissions, water usage, waste recycling and other important environmental measures. Over the course of

the year, our capital goods, consumer cyclicals, consumer staples, financials and utilities sector teams all performed significant sector-

and stock level analysis of potential climate risks and opportunities. Our sector teams have also identified which companies have

162020 MFS Sustainable Investing Annual Report

Thematic Research

set science-based targets aligned with the goals of the Paris

Accord. In 2020, we engaged on climate-related issues with

sustainability leaders, management teams and board members at

many companies, and these in-depth discussions around

decarbonizing to achieve net-zero emissions are ongoing.

Plastic waste

Plastic waste was an important theme for our team in 2020. Our

ESG analysts developed a framework for assessing the

environmental impacts of single-use plastic packaging and the

potential implications for the entire plastics value chain. This

framework initially focused on the chemicals, plastic packaging,

consumer staples and waste management industries. It provided a

basis for identifying the risks and opportunities associated with

plastic packaging, especially with regard to changing consumer

preferences, regulation and costs, that may affect the competitive

positioning and profitability of many companies over the long

term. Our analysts' evaluation included engagements with various

companies and the development of data sets to compare company

progress versus stated targets. These data sets will be used for

further engagement.

Many investment decisions have been impacted by this research.

Most notably, our US-based packaging analyst upgraded an

aluminum can manufacturer from a 2 to a 1 rating based primarily

on her view that lower plastic bottle consumption due to consumer

concern and the regulatory costs associated with emissions and

plastic pollution would likely cause a resurgence in the demand for

aluminum cans. Aluminum cans have an emissions footprint similar

to that of recycled plastic and are infinitely recyclable, whereas the

recyclability of plastic is severely limited by current recycling

technology. In addition, one of our Singapore-based equity

analysts reduced the growth rate in his long-term terminal value

calculation for a plastics supplier to account for regulatory risks

and consumer shifts away from plastic. More on this topic can be

found in our research publication series ESG in Depth: Sustainable

Packaging – Risks to the Plastic Value Chain.

Although our team researched and debated a number of other

ESG themes during 2020, such as Chinese VIE structures,2

corporate tax practices and technology ethics, the examples above

illustrate the breadth of our thematic ESG research and its

importance to our investment process.

2 A Variable Interest Entity (VIE) is a legal business structure in which an investor has a controlling interest despite not having a majority of voting rights.

Risk Management

Our cultural emphasis on risk management is incorporated into all facets of our

investment process. At MFS, the goal is not to minimize risk but rather to understand

its sources and effectively manage it. The risk management process strives to ensure

that each strategy takes an appropriate level of risk that is disciplined and consistent

with the investment philosophies of its mandate while also meeting long-term

investment objectives.

At MFS, the goal is not to minimize risk but rather to understand its sources

and effectively manage it.

We consider both risks and opportunities when evaluating ESG factors and trends, and

we have implemented systematic processes to help our investment team manage

ESG-related risks at the security and portfolio levels. The annual portfolio sustainability

reviews described above are designed by our ESG analysts to provide portfolio

managers with a comprehensive view of the ESG risks and opportunities in their

portfolios, based on MFS' own internal research and viewpoints. Separately, the

semiannual portfolio risk review process, which is conducted by the firm's chief risk

officer and respective asset class CIOs, covers a wide variety of factors, including third-

party ESG ratings and perspectives. Each portfolio's ESG score is evaluated against

that of its benchmark, and ESG rating changes since the last review are discussed.

Both the annual portfolio sustainability reviews and the semiannual risk reviews are

intended to prompt additional research and collaboration among the investment team.

In addition to these reviews, automated reports highlighting third-party ESG ratings

changes are disseminated to covering analysts on an ongoing basis.

17

182020 MFS Sustainable Investing Annual Report

ESG Data and Tools

The ESG data landscape is changing rapidly, as are the tools available for analyzing the data.

During 2020, MFS' ESG data integration strategy advanced substantially. We enhanced our investment team's access to both internal

and external ESG data and insights. We broadened the scope of data we receive from existing third-party ESG research providers and

added a new provider that offers insights on municipal bond issuers. This will help our investment team better understand the physical

risks faced by municipal issuers and enhance integration of other ESG factors in this important fixed income sub-asset class.

To house our proprietary ESG research and relevant third-party data, MFS maintains easily accessible, issuer-specific ESG pages within

our investment research system. Notes written by our analysts and portfolio managers that are tagged as containing ESG content are

automatically linked to these pages, enabling the broader team to quickly identify and evaluate internal viewpoints on material ESG

factors impacting the companies they cover or hold in a portfolio.

During 2020, we added our proprietary ESG "sector maps" to each company ESG page. MFS' sector maps outline the key

environmental and social issues we believe are material to the industry in which a company operates. Each topic shown on a

company's map includes an assessment of the magnitude of the risk or opportunity, an overview of the topic (including key data

points to analyze) and potential engagement questions.

Over the past year, we have increased the amount of external ESG research available on these company-specific ESG pages.

Our team can now access multiple providers' data and reports from a centralized location, making it a powerful ESG research tool.

Over the past year, we have increased the amount of external ESG research available on these company-specific ESG pages. Our team

can now access multiple providers' data and reports from a centralized location, making it a powerful ESG research tool.

In addition to increasing the availability of data within our research database, we have enhanced the team's access to ESG data through

other means. For example, in 2020, our ESG analysts developed an ESG dashboard that instantly and simultaneously displays a wide

variety of third-party data and insights for up to 100 issuers. This includes data associated with emissions, water usage, diversity, injury

rates, employee attrition, data security and bribery and corruption practices, executive compensation and governance information,

audit quality, and controversies.

ESG issues are complex, interconnected and evolving too quickly for a single rating or data point to reflect the full extent of

sustainability-related risks and opportunities facing a company or investment. There are still many inadequacies when it comes to the

availability and comparability of ESG data, which is one reason that we believe there is no substitute for in-depth issuer analysis.

Materiality assessment cannot be automated.

19 2020 MFS Sustainable Investing Annual Report

Stewardship – Engagement

Engagement is at the heart of our sustainability agenda. As an active manager, we believe open communication with issuers is vital

to ensuring that ESG risks and opportunities receive the necessary attention from management teams and other stakeholders, and

we strive to maintain a regular dialogue with companies over time. Increasingly, we are using our privileged access to executive

teams to engage with them on social and environmental issues that are, or could be, material to their business. Recognizing the

critical importance of the board in influencing corporate culture and strategy, as well as appointing the executive team, we are

making a point of setting up periodic meetings with nonexecutive directors to complement our discussions with management. We

prefer conversation to confrontation and expect to make more progress that way, but we are willing to use our vote or other means,

if necessary, to expedite change.

To enable our investment and proxy voting teams to more accurately track, monitor and report on the many engagements occurring

across our global investment platform, we have embedded a new engagement tracking tool in our global research system. The first

phase of this tool went live during the fourth quarter of 2020.

We engage with issuers in several ways, as shown below.

MFS Engagement Activities

FormalInvestment-Led

CollectiveInformalInvestment-Led

FormalProxy-Led

Informal investment-led engagementOur investment team engages with companies on a continual basis, sharing ideas and asking ESG-related questions of

management teams during in-house meetings, onsite visits and investment conferences.

Formal investment-led engagementOur investment team also pursues what we regard as "formal" ESG engagements. More limited in number than informal

engagements, formal engagements occur when other avenues have failed to produce a desired outcome.

Collective engagementMFS believes that collective (or collaborative) engagement can generate positive impacts for industries, individual companies and a

wide range of stakeholders, including shareholders. We actively participate in industry initiatives, organizations and working groups

that seek to improve and provide guidance on corporate and investor best practices, ESG integration and proxy voting issues.

Stewardship – Engagement

Below we outline some of the collaborative engagements

we participated in during 2020.

CDP Science-Based Targets Campaign MFS signed on to

the CDP Science-Based Targets Campaign in early

September. The campaign provides a platform from which

CDP signatories can support the Science-Based Targets

Initiative (SBTi) by encouraging companies to adopt

science-based emissions reductions targets. Science-based

targets enable companies to align with Paris Agreement

goals, increase the effectiveness of their scenario analyses

and provide their stakeholders with greater transparency

around climate-related risks and opportunities.

ShareAction Workforce Disclosure Initiative (WDI) MFS

joined the WDI in September 2020. The WDI focuses on how

companies treat their employees with the goal of improving

both the quantity and quality of company disclosure on

employee management practices. The WDI survey provides

companies a standardized format for reporting on such issues

as human rights diligence, workforce composition, diversity

and inclusion, wage levels and pay gaps. Our ESG and

covering analysts have been engaging with our portfolio

companies to improve participation in the WDI survey. We

have also been using WDI data to enhance our due diligence

on employee management practices at a number of different

companies. In an effort to offer disclosure where we seek it,

MFS has also completed the WDI survey.

Investors Against Slavery and Trafficking Asia-Pacific

(IAST APAC) MFS signed on to IAST APAC in October 2020,

with the objective of encouraging companies to improve

transparency and operational processes that address modern

slavery, trafficking and labor exploitation in the supply chain.

In supporting the initiative, our aim is to join other investors in

clarifying what steps companies should take to combat

modern slavery and to help them take action.

Climate Action 100+ (CA100+) In November 2020, MFS

joined CA100+, an investor initiative focused on engaging with

the world’s highest emitters of greenhouse gas (GHG) to

ensure that they implement a strong governance framework,

that they take steps to reduce emissions across their value

chain and that they provide enhanced disclosure in accordance

with Task Force on Climate-Related Financial Disclosures

(TCFD). We support CA100+’s mission of delivering emissions

reductions in the real economy as opposed to ducking the

issue by simply divesting from high emitters.

Over the past several years, our

investment team has spent a

great deal of time discussing

the importance and potential

impact of corporate culture on

sustainability. This work, and

our ongoing discussions on

culture and diversity with a

wide variety of companies, led

us in 2020 to issue a letter to

our 100 largest holdings

requesting the explicit disclo-

sure of each company's work-

force composition, diversity

and employee turnover data.

As investors, we believe this

information is important and

can have a material impact on

our investment decisions. We

also feel strongly that we

should be willing to disclose

the same data we expect our

portfolio companies to dis-

close. Accordingly, the letter

included our company data on

these metrics as a show of

good faith.

202020 MFS Sustainable Investing Annual Report

21 2020 MFS Sustainable Investing Annual Report

Stewardship – Engagement

Collective Investor Statements

MFS signed on to a number of investor statements over the course of 2020 that are focused on issues we believe to be material, or potentially material, to companies held in our portfolios. These included statements calling for the following:

n Living incomes and wages for workers in agricultural supply chains

n Improved transparency in supply chains and ESG due diligence in the luxury fashion sector

n The mitigation of modern slavery, human trafficking and labor exploitation

n The prevention of PFAS pollution by removing "forever" chemicals from food packaging

n Urgent action on the "stranded seafarer" crisis

Formal proxy-led engagementMFS believes that open communication with issuers on proxy voting and corporate governance matters is an important aspect of our

ownership responsibilities. Our proxy voting team engages in dialogues with management teams, board members and other senior

representatives of MFS' portfolio companies through in-person meetings, conference calls and formal letter-writing campaigns.

MFS' long-term approach to investing inspires a long-term approach to engagement. Our multiyear engagement horizon typically allows

us to develop strong relationships with our portfolio companies. As a result, we are able to have more candid and insightful discussions as

we foster these long-term dialogues. During the 2020 calendar year, the proxy team led 111 engagements with 94 distinct portfolio

companies across 11 different markets (see Appendix).

When engaging with companies from a proxy perspective, MFS aims to do the following:

Communicate our voting policies and the rationale behind our voting decisions

We aim to be proactive and transparent regarding our policies, approach to proxy voting and expectations of portfolio companies following

low support on a shareholder vote. MFS maintains a letter-writing initiative that focuses on encouraging our portfolio companies to

respond to particular areas of concern for shareholders. In 2020, the firm sent letters to the boards of 28 companies encouraging them to

respond in an appropriate and meaningful way to the concerns demonstrated by shareholders at their annual general meeting.

Exchange views on relevant ESG issues and advocate for meaningful progress

Given our long-term view, our engagements are often focused on encouraging sustainable progress over multiple years. However, in

many instances, our portfolio companies have responded promptly to actionable feedback from shareholders.

For example, over the course of 2020, members of our proxy team conducted multiple meetings with representatives of an agricultural

machinery company to discuss our concerns regarding the company's governance practices, board composition and compensation

policies. The board recently appointed a new lead independent director with enhanced duties (along with three new committee chairs),

adopted term limits for board leadership positions and updated hedging and pledging policies.

We also engaged with members of the board from an American gas and electric company regarding the diversity of both its board and wider

workforce. The company is working to improve its diversity, as evidenced by a number of concrete changes made, such as the nomination

of a female director to the board, updating corporate governance guidelines to promote the active recruitment of women and minority

candidates in the board candidate pool, enhancing disclosure around board refreshment and agreeing to provide EEO-1 disclosure.3

3 An EEO-1 Report is a government form that requests information about employees' job categories, ethnicity, race, and gender. Employers with at least 100 employees must submit one to the US Equal Employment Opportunity Commission (EEOC) and the US Department of Labor (DOL) every year.

222020 MFS Sustainable Investing Annual Report

Stewardship – Engagement

Address thematic and long-term engagement priorities

In advance of the 2020 proxy season, we published the MFS 2020 Proxy Season Preview, which summarized recent amendments to

our proxy voting policies, shared MFS' outlook and expectations for the upcoming proxy season and discussed long-term

engagement priorities and thematic issues of interest to our proxy voting committee.

Our 2020 engagement priorities were focused on corporate culture, board gender diversity and board composition issues. When

engaging on diversity, we seek to understand a board's refreshment and recruitment processes, as well as the demonstrated impact

of diversity and inclusion initiatives. It is important for us to see an active and transparent board evaluation and refreshment process

wherein new board members are considered annually. With respect to the broader workforce, we look for initiatives aimed at

strengthening diversity and investments in a culture of belonging and inclusion. Accountability for employee diversity in the

workforce can be demonstrated by disclosing employee diversity metrics and goals, making progress toward achieving diversity

related goals, hiring diverse talent and fostering inclusive leadership. Reviewing diversity-related goals and metrics such as

percentage of underrepresented minorities in the workforce, promotion rate and pay equity analysis are a few examples of tools

helpful to shareholders when they are assessing the impact of company-wide diversity initiatives.

Measure our impact

Over time, we have found that robust engagement combined with thoughtful proxy voting can have a strong positive effect on ESG

practices. Two examples of that positive impact are outlined below.

■ Our proxy team has engaged over 20 times with a US based aerospace/technology conglomerate over the past eight years to

communicate our expectations as shareholders. Most recently, we engaged with the company on political and lobbying

disclosures to monitor the alignment of such contributions with the company's stewardship commitments. In response to our

feedback and voting activity, the company has improved related disclosures by publishing a list of contributions in excess of

$50,000 made to trade associations.

■ Members of our proxy voting and investment teams engaged with a US-based financial services company both before and after the

company's 2020 annual shareholder meeting. These discussions were primarily focused on executive compensation. Prior to the

shareholder meeting, we discussed the board's approach to measuring and rewarding performance. In light of the amount of pay

driven by qualitative assessment as opposed to quantitative metrics, MFS did not support the advisory vote on executive

compensation. Discussions following the meeting to explain the rationale behind our voting decision prompted modifications to the

company's compensation program such that quantitative measures now figure much more prominently in executive remuneration.

Proxy Engagement by Year■ 2018 ■ 2019 ■ 2020

0

30

60

90

120

150

180

Compensation IssuesGovernance IssuesEnvironmental & Social Issues

123

92

55

145

127

9099

67

83

23 2020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

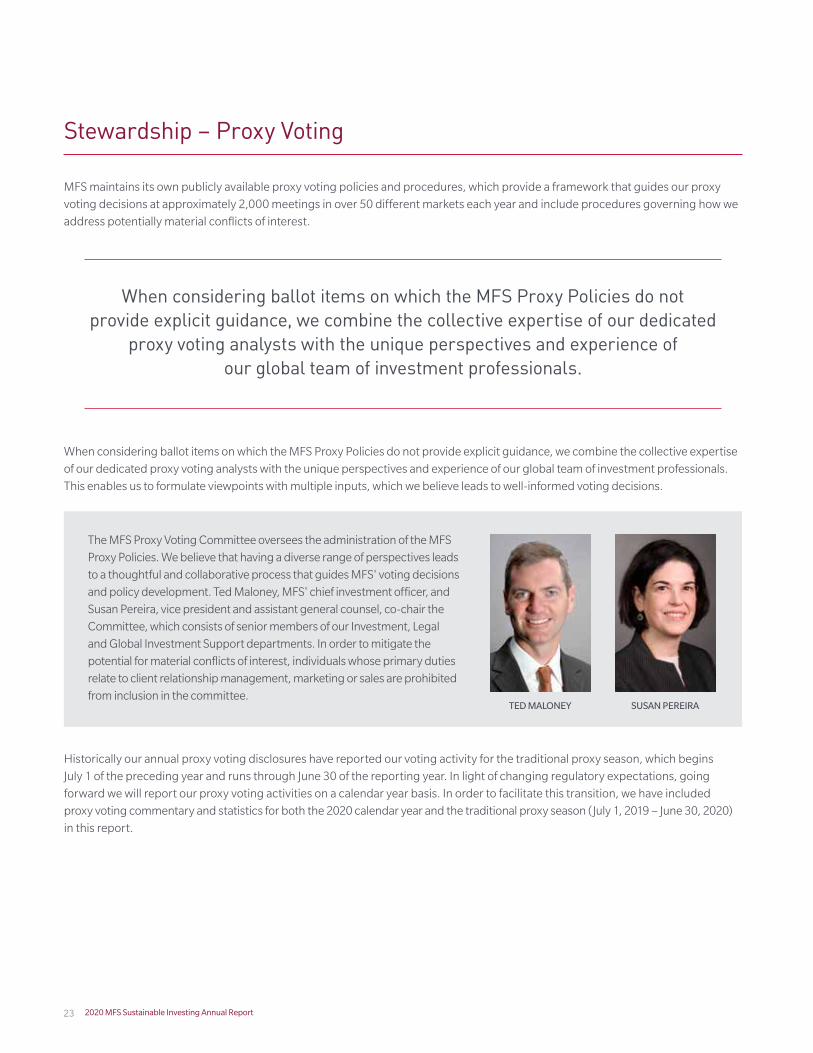

MFS maintains its own publicly available proxy voting policies and procedures, which provide a framework that guides our proxy

voting decisions at approximately 2,000 meetings in over 50 different markets each year and include procedures governing how we

address potentially material conflicts of interest.

When considering ballot items on which the MFS Proxy Policies do not provide explicit guidance, we combine the collective expertise of our dedicated

proxy voting analysts with the unique perspectives and experience of our global team of investment professionals.

When considering ballot items on which the MFS Proxy Policies do not provide explicit guidance, we combine the collective expertise

of our dedicated proxy voting analysts with the unique perspectives and experience of our global team of investment professionals.

This enables us to formulate viewpoints with multiple inputs, which we believe leads to well-informed voting decisions.

The MFS Proxy Voting Committee oversees the administration of the MFS

Proxy Policies. We believe that having a diverse range of perspectives leads

to a thoughtful and collaborative process that guides MFS' voting decisions

and policy development. Ted Maloney, MFS' chief investment officer, and

Susan Pereira, vice president and assistant general counsel, co-chair the

Committee, which consists of senior members of our Investment, Legal

and Global Investment Support departments. In order to mitigate the

potential for material conflicts of interest, individuals whose primary duties

relate to client relationship management, marketing or sales are prohibited

from inclusion in the committee.TED MALONEY SUSAN PEREIRA

Historically our annual proxy voting disclosures have reported our voting activity for the traditional proxy season, which begins

July 1 of the preceding year and runs through June 30 of the reporting year. In light of changing regulatory expectations, going

forward we will report our proxy voting activities on a calendar year basis. In order to facilitate this transition, we have included

proxy voting commentary and statistics for both the 2020 calendar year and the traditional proxy season (July 1, 2019 – June 30, 2020)

in this report.

242020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

Reviewing the 2020 calendar year

During the 2020 calendar year, MFS was eligible to vote on 22,976 ballot items at 1,992 shareholder meetings across 60 markets. MFS

voted shares at approximately 99% of these meetings, with the remaining meetings not voted due to share-blocking concerns (nine

meetings), late receipt of ballot (one meeting) or market-specific voting impediments (13 meetings). The map below shows the number of

meetings voted around the world along with the overall percentage of meetings voted within each region.

During the 2020 calendar year, MFS voted against:

n management recommendations on approximately 7% of all ballot items globally.

n management recommendations on at least one ballot item at approximately 39% of all shareholder meetings.

n approximately 10% of executive remuneration proposals.

n board members at six companies for failing to adequately respond to shareholder concerns.

n 104 directors over diversity concerns.

Canada87 meetingsvoted (100%)

UK & Ireland248 meetingsvoted (94.4%)

US & US Territories726 meetingsvoted (100%)

Latin & South America129 meetingsvoted (94.2%)

Europe295 meetingsvoted (96.4%)

Middle East & Africa36 meetingsvoted (100%)

Australia & New Zealand51 meetingsvoted (100%)

Asia397 meetingsvoted (100%)

25 2020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

Pushing for progress through our voting activities

Shareholder proposals can often be used as a catalyst to bring about positive change on ESG issues. In 2020, the most prevalent

shareholder proposals were those relating to climate change, lobbying and political activities, human capital management and

independent board chairs.

During 2020, shareholder proposals relating to environmental issues typically centered on increased disclosure around climate change,

community-environmental impact and specific reductions in GHG emissions. In general, shareholder support for climate change

proposals increased from 2019, and four climate change proposals received majority support. MFS was entitled to vote on two such

proposals, both at multinational energy companies, and supported both. The firm also supported a shareholder proposal requesting that

a multinational package-delivery and supply-chain-management company publish a report on climate change disclosing how it plans to

manage GHG emissions. We supported this proposal because we believe such disclosure is valuable for shareholders seeking to

ascertain how the company is managing climate related risks.

As they have in past years, shareholder proposals requesting greater disclosure of corporate political contributions represented a

significant share of social issues covered in 2020, accounting for 47 of the 128 social shareholder proposals MFS voted on. Of the 43

proposals we supported, two received the majority support of shareholders. We look forward to engaging with these companies around

the enhanced disclosure of political contributions and lobbying activities.

For: 25%Against: 75%

For: 59.4%Against: 40.6%

For: 52%Against: 48%

70%

21%

9%

How MFS Voted on Shareholder Proposals

■ Environmental proposals

■ Social proposals

■ Governance proposals

262020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

Shareholder proposals requesting the disclosure of diversity policies and goals at both the board and workplace level were also a focus

during 2020. MFS voted to support a proposal requesting an employment diversity report at a multinational hospitality company. In our

view, these disclosures help shareholders better assess the company's diversity initiatives and its management of related risks. We also

voted in favor of a majority-supported proposal aimed at the adoption of a policy on board diversity at a global logistics company. We

look forward to reviewing the company's response on this matter.

Among the governance-related shareholder proposals we reviewed during 2020, the most prevalent topic was the separation of the chair

and CEO roles. MFS supported 15 out of 38 of these proposals. We analyze these proposals on a case-by-case basis, evaluating the board

structure to ensure robust independent oversight along with any unique facts and circumstances of the existing leadership structure, to

determine what we believe would be the optimal structure for the company. For example, we supported a proposal aimed at separating

the roles of CEO and chair as part of the next CEO transition at a global media and technology company because we believe this large,

complex organization would be best served by the most independent form of oversight.

During the 2020 calendar year, MFS voted for:

n 100% of proposals to declassify the board.

n 100% of proposals seeking majority voting in director elections.

n 100% of proposals to provide the right to act by written consent.

n 100% of proposals to eliminate supermajority voting rights.

n 100% of proposals to provide certain shareholders the ability to nominate a certain number of board nominees (adopt a proxy access right).

27 2020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

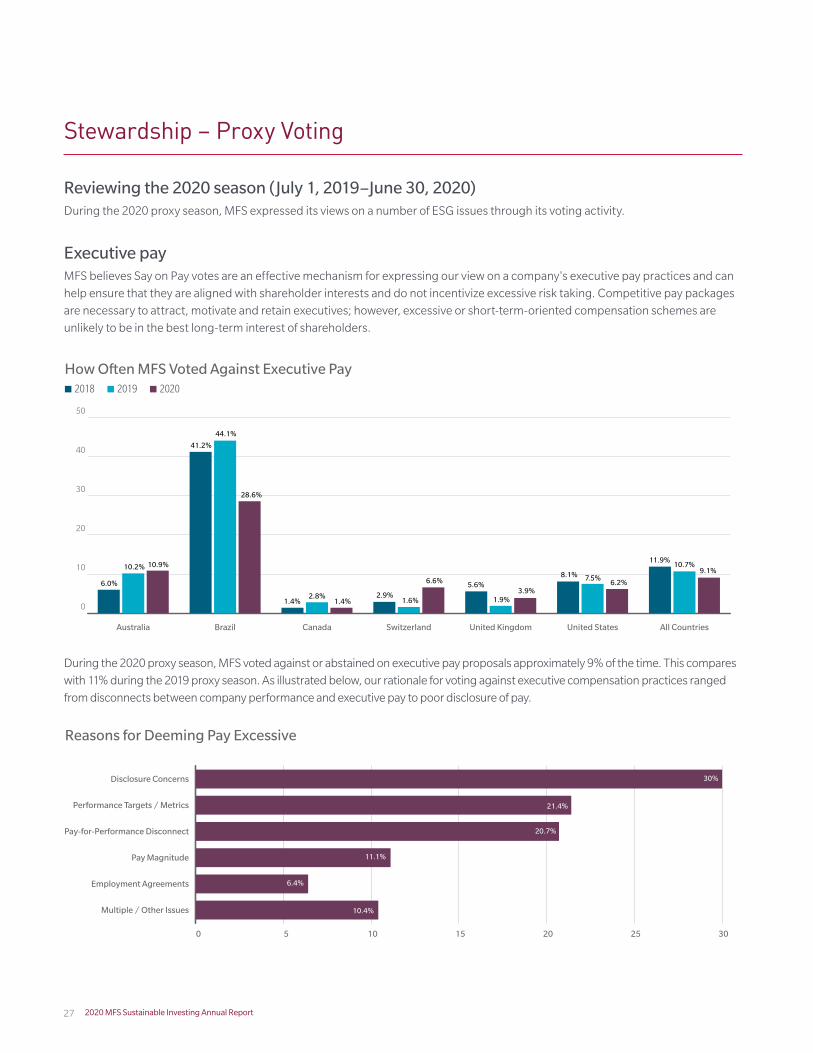

Reviewing the 2020 season (July 1, 2019–June 30, 2020)During the 2020 proxy season, MFS expressed its views on a number of ESG issues through its voting activity.

Executive payMFS believes Say on Pay votes are an effective mechanism for expressing our view on a company's executive pay practices and can

help ensure that they are aligned with shareholder interests and do not incentivize excessive risk taking. Competitive pay packages

are necessary to attract, motivate and retain executives; however, excessive or short-term-oriented compensation schemes are

unlikely to be in the best long-term interest of shareholders.

How Often MFS Voted Against Executive Pay ■ 2018 ■ 2019 ■ 2020

0

10

20

30

40

50

All CountriesUnited StatesUnited KingdomSwitzerlandCanadaBrazilAustralia

6.0%

10.2% 10.9%

41.2%

44.1%

28.6%

1.4%2.8%

1.4%2.9%

1.6%

6.6% 5.6%

1.9%3.9%

11.9%10.7%

9.1%

6.2%7.5%8.1%

During the 2020 proxy season, MFS voted against or abstained on executive pay proposals approximately 9% of the time. This compares

with 11% during the 2019 proxy season. As illustrated below, our rationale for voting against executive compensation practices ranged

from disconnects between company performance and executive pay to poor disclosure of pay.

Reasons for Deeming Pay Excessive

0 5 10 15 20 25 30

Multiple / Other Issues

Employment Agreements

Pay Magnitude

Pay-for-Performance Disconnect

Performance Targets / Metrics

Disclosure Concerns 30%

21.4%

20.7%

11.1%

6.4%

10.4%

282020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

On a global scale, the number of remuneration report "strikes" in Australia continues to increase. MFS voted against approximately

11% of remuneration-related proposals at Australian portfolio companies during the 2020 proxy season as compared with 10% and

4% in the 2019 and 2018 proxy seasons, respectively. This increase is primarily due to a growing number of issuers amending

executive remuneration structures to include problematic performance metrics or targets compounded by concerns over

corresponding disclosure.

We note an increase in remuneration-related proposals in European markets given the amendments to the Shareholder Rights

Directive (SRD II). Remuneration reports are now subject to an annual vote, and the content of remuneration disclosures going

forward will contain more specific performance criteria disclosure. While the impact of voting remains to be seen, as compliance

becomes mandatory in 2021, the uptick in remuneration consultation engagements with European issuers has been notable.

We believe that a well-balanced board with diverse perspectives is the foundation of sound corporate governance and that

gender diversity is one of the many ways corporate boards can enhance the diversity of their views, skill sets and collective expertise.

Finally, the revised UK Corporate Governance Code stipulates that pension contribution rates for executive directors should be

aligned with those available to the workforce. MFS will vote against remuneration-related proposals where companies do not take

action in line with this provision of the code, and we engage with companies lagging in this regard.

Director electionsWe believe that a well-balanced board with diverse perspectives is the foundation of sound corporate governance and that gender

diversity is one of the many ways corporate boards can enhance the diversity of their views, skill sets and collective expertise. In

2019, we amended the MFS Proxy Policies to require votes against the nominating and governance committee chairs of the boards

of US companies where less than 15% of directors are female. In 2020, we expanded this amendment to include Canadian and

European issuers. As a result, we voted against nominees at more than 100 companies across Canada, Europe and the US during

the 2020 proxy season.

We also believe that the amount of time required of US public company directors has grown significantly in recent years, and we are

mindful of the impact of excessive service on outside boards. During the 2020 proxy season, we voted against director nominees at

90 US companies due to excessive outside service.

MFS may also vote against director nominees if the board has not taken responsive action on an issue of concern to shareholders.

For example, if a shareholder proposal receives majority approval at a prior shareholder meeting and the board has not acted on the

resolution, MFS will typically vote against the entire board's reelection at subsequent AGMs. Similarly, if a significant number of

shareholders has expressed dissatisfaction with a company's executive pay program and the board has not addressed the issue,

MFS may vote against members of the compensation committee or the full board. In 2020, MFS voted against board members at

five companies for failing to adequately respond to shareholder concerns (compared with four in 2019). The firm also maintains a list

of directors who we believe do not warrant support at any company based on their poor corporate governance track records.

During 2020, MFS voted against approximately 6.0% of director nominees globally (compared with 7.2% in 2019).

29 2020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

How Often MFS Voted Against Directors■ 2018 ■ 2019 ■ 2020

0

5

10

15

20

All CountriesUnited StatesUnited KingdomSwitzerlandJapanFranceCanadaBrazilAustralia

7.2%

1.9%

8.6% 8.2%

3.2% 2.9%

1.4%

20.0%20.0%

12.3%

1.5%

6.1%

4.8%

12.7%

7.4%

11.7%

18.7%

0.9% 1.2% 1.3%

5.5% 6.0%

7.2%7.5%7.0%

9.4%

4.1%

Shareholder proposalsDuring the 2020 proxy season, more than 550 proposals were submitted to companies by shareholders seeking a vote on a wide

variety of ESG issues. The most prevalent topics included climate change, lobbying and political activities, human capital

management and independent board chairs.

For: 25%Against: 75%

For: 59.4%Against: 40.6%

For: 52%Against: 48%

70%

21%

9%

How MFS Voted on Shareholder Proposals

■ Environmental proposals

■ Social proposals

■ Governance proposals

Environmental IssuesDuring the 2020 proxy season, shareholder proposals relating to environmental issues most often called for the increased disclosure of

climate change impacts or environmental impacts on communities, with some calling for specific reductions in GHG emissions. We note

that the number of environmental proposals put to a vote has decreased over the past five years; however, average support continues to

increase, with more proposals receiving majority support in 2020 than in 2019.

302020 MFS Sustainable Investing Annual Report

Stewardship – Proxy Voting

MFS generally supports proposals that request additional disclosure on the impact of environmental issues such as climate change on a

company’s operations unless we believe that the company already provides enough information on the topic to allow shareholders to assess

the relevant risks. The firm supported 33% of the climate change-related proposals we were eligible to vote on globally. Overall, MFS supported

25% of 52 proposals relating to environmental issues during the 2020 proxy season (compared with 38% in 2019). The change is largely

attributable to the higher percentage of environmentally focused shareholder proposals submitted outside the United States that we deemed

overly prescriptive or poorly drafted. For example, we do not support proposals calling for companies to amend their articles to mandate